Abstract

The power of finance vis-à-vis the nonfinancial sector is changing. Macroeconomic developments and financial innovations have reduced financial actors’ exit options, thus diminishing exit-based structural power. At the same time, shareholdings have become more concentrated in the hands of large asset managers, thus increasing control-based power. This article documents these trends, before examining whether asset managers wield their power and why, despite being universal shareholders, they have not steered corporate behavior toward decarbonization. Rather than assuming orderly, good-faith interactions between shareholders and managers, this article argues that in the United States today, political considerations govern the use of control-based power. Asset managers’ corporate governance policies are subservient to the—increasingly inconsistent—goals of maximizing assets under management while avoiding regulatory backlash. Unlike exit-based power, control-based power is constrained by being highly visible and, therefore, easily politicized.

The structural power of capital is conventionally thought of as a function of its ability to threaten to exit firms, sectors, or entire countries. This holds for business in general, and for finance in particular. 1 Much of the literature has focused on the structural power of capital vis-à-vis the state, but relationships of structural power exist among private economic actors, too. 2 In particular, financialized economies offer a variety of channels through which the financial sector exercises power vis-à-vis the nonfinancial corporate sector. The chief example is the structural power of shareholders in corporate governance, the paradigmatic actor being the “impatient,” exit-happy institutional investors that rose to dominance in the 1990s. 3

This article argues that the mechanism underpinning the power of finance vis-à-vis the nonfinancial sector has changed. The argument comes in three parts. First, both macroeconomic developments and financial innovations have diminished financiers’ exit-based structural power vis-à-vis the nonfinancial corporate sector. Second, in the publicly listed corporate sector, this has been compensated for by a steady increase in control-based power, exercised through large, illiquid equity stakes held by asset managers. Control-based power arises from capitalism's tendency toward what Hilferding called finance capital and it could, in principle, be construed as a different form of structural power. For reasons of conceptual clarity, however, this article will distinguish simply between control-based power and exit-based power, the latter being the conventional definition of structural power.

Does the shift from exit to control impact financial actors’ ability to exercise their power, or the goals they pursue? Here, prevailing understandings of corporate governance—inspired by Berle and Means, Hirschman, and agency theory—fall short because they theorize the interaction between shareholders and managers in isolation. Instead—and this is the third argument—the largest asset managers are engaged in a multilevel game that, besides corporate governance, also comprises regulatory politics and the market for asset management services. In this multilevel game, the largest shareholders face constraints on their power that are new, and specific to asset manager capitalism: Whereas the strength of exit-based structural power was enhanced by its depoliticized nature, control-based power is inherently more visible, and thus more easily contested and politicized. 4

The nature of the power of finance is a key question for the political economy of capitalism and—because of the financialization of household wealth—inequality. 5 The need to rethink this power arises from the ongoing transformation of the financial sector. As the financing function of the financial system has been superseded by the wealth-preservation—or asset management—function, power has shifted from banks to institutional capital pools. The latter category has steadily expanded and today includes asset owners, such as insurers, pension funds, and sovereign wealth funds, as well as asset management companies. Supported by a broader “wealth defence industry” of lawyers and accountants, these asset managers constantly reorganize economic activity with the goal of increasing financial returns. 6 This reorganization takes different forms in different segments of the economy. Outside the realm of publicly listed corporations, alternative asset managers have pushed financialization by making ever new areas of economic activity accessible for financial investment. Venture capital firms groom startup companies, while private equity firms turn companies, housing, infrastructure, and even farmland into asset classes accessible to institutional capital pools. 7 In this world of private capital, asset managers forfeit the exit option in exchange for full ownership rights. Their power is clearly based on control.

The case of publicly listed companies is theoretically more interesting. Here, the power of the Big Three asset managers—BlackRock, Vanguard, and State Street—is no longer “hidden.” 8 However, economists, legal scholars, and political economists have debated the sources of this power and the degree to which it is wielded. 9 While the promise of the shareholder primacy regime was efficiency, achieved via the combination of exit and voice, the promise of asset manager capitalism is sustainability, made necessary by (involuntary) loyalty: Since their globally diversified shareholdings expose them to the a very significant chunk of the global economy, “universal owners” should, in principle, internalize negative externalities arising from the conduct of individual portfolio companies; and they should, therefore, use their power to enforce socially and environmentally sustainable corporate behaviors. 10 Although the Big Three have all embraced the rhetoric of universal ownership, they have clearly failed to deliver on the promise of sustainability. 11 Instead of a green transition driven by large-scale corporate investment in renewable energy and other green technologies, the United States in particular has seen increasingly monopolistic market structures and record payouts to shareholders. 12 Does this mean that asset managers are powerless?

Taking the analysis of asset manager capitalism as a distinct corporate governance regime one step further, this article argues that under conditions of actually existing asset manager capitalism, corporate governance is only one of three battlegrounds for asset managers—the others being the market for asset management services and, crucially, politics. Asset managers wield their control-based power according to a political calculus that is not captured by the notion, still dominant in the legal and management literatures, of corporate governance as a field neatly organized around agency conflicts between managers and shareholders. While such a field may have existed at one time, corporate governance has become a more complex and messier—in a word, political—affair. 13 When asset managers exercise “voice,” they address not only a portfolio company's management but also (prospective) clients, regulators, and politicians and their voters. This political understanding of voice is, of course, consistent with Hirschman's original conception, which contrasted exit, an economistic form of action, with the “messy” concept of voice, which referred to “political action par excellence.” 14 Today, the messy politics of actually existing asset manager capitalism is characterized by a growing tension between the overriding goals of maximizing assets under management and minimizing political and regulatory risk. This tension finds its expression in the escalating controversy over environmental, social, and governance (ESG) investing, greenwashing, and “woke capital.” In the United States, the largest asset managers have increasingly found themselves between a rock—attempts by the left to enforce green stewardship—and a hard place—attempts by the right to outlaw green stewardship.

In the following, the empirical focus is on the United States, which is home to the lion's share of institutional capital and of the global asset management industry, and where asset manager capitalism has reached its most advanced stage. 15 However, as the stock-market footprint of the largest asset managers continues to expand across most advanced economies, the argument increasingly applies elsewhere. 16 The article proceeds as follows. I first present data to document the decline of exit options for finance. I then introduce the notion of control-based power, relating it to early twentieth-century finance capital. Next, I discuss asset manager capitalism as a corporate governance regime. I then examine if, and how, asset managers wield their potential control-based power in their quest to maximize assets under management and to minimize political and regulatory risk.

The End of Exit

Presenting data from the US financial accounts, this section shows that the nonfinancial corporate sector has, in the aggregate, become financially self-sufficient. In such a world, the exit-based theory of the structural power of finance loses much of its appeal. 17

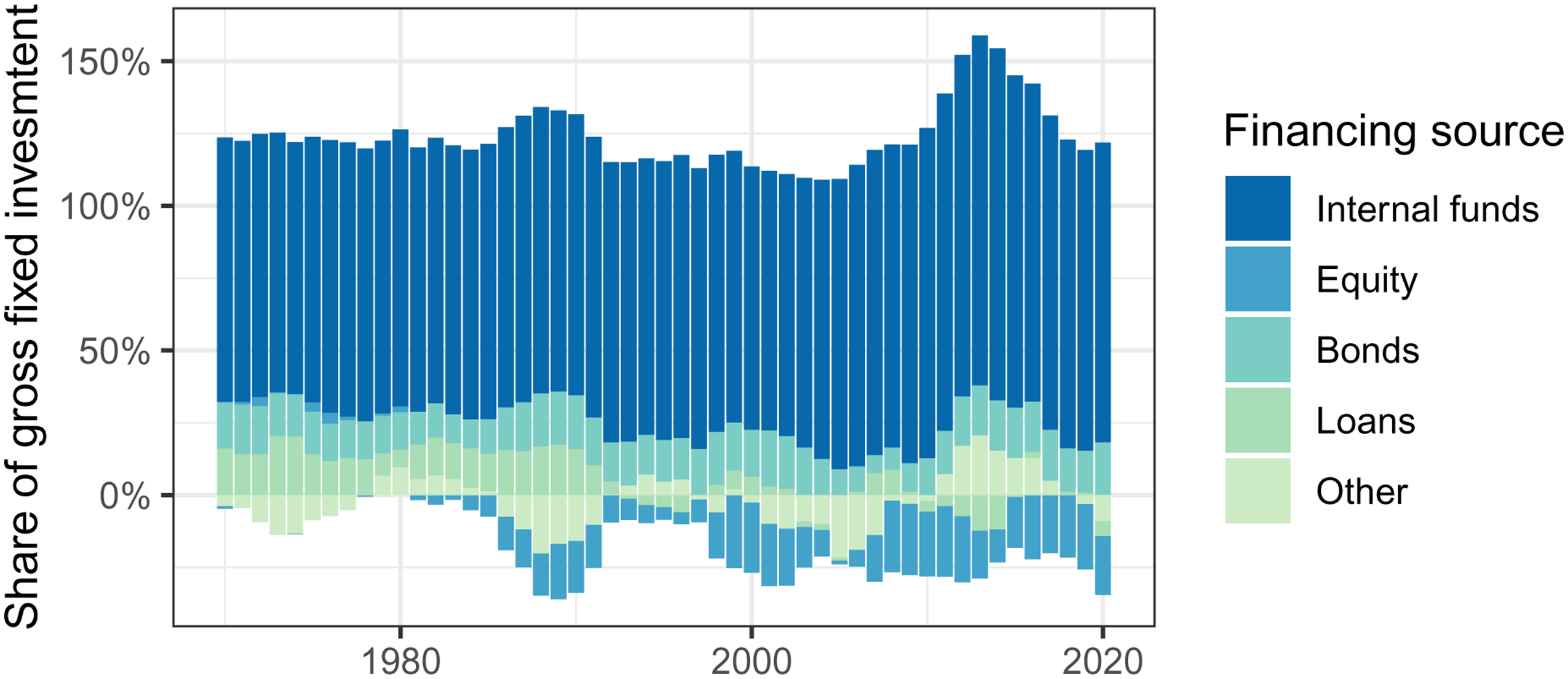

The most direct way of measuring the nonfinancial corporate sector's dependence on finance is to look at the extent to which capital formation is financed by external funds. Figure 1 shows results obtained by using the methodology proposed by Corbett and Jenkinson and van Treeck. 18 It shows, first, that the vast majority of corporate investment is financed from internal funds, that is, retained profits. Second, the stock market's contribution to the net financing of corporations turned negative in the 1980s, meaning it has helped ferret capital out of the corporate sector, at the expense of workers and of investment. 19 Third, and most remarkably, even traditional loans have made a negative contribution since 1990. 20

Financing of gross fixed investment, US nonfinancial corporations, 1970–2020. (Federal Reserve, US Financial Accounts.) Author's calculations based on Jenny Corbett and Tim Jenkinson, “How Is Investment Financed? A Study of Germany, Japan, the United Kingdom and the United States,” Manchester School 65, no. S (1997): 69–93; Till van Treeck, “The Political Economy Debate on ‘Financialization’—a Macroeconomic Perspective,” Review of International Political Economy 16, no. 5 (2009): 907–44. Sums do not add up to 100 percent due to the approximate nature of both the method and the underlying data.

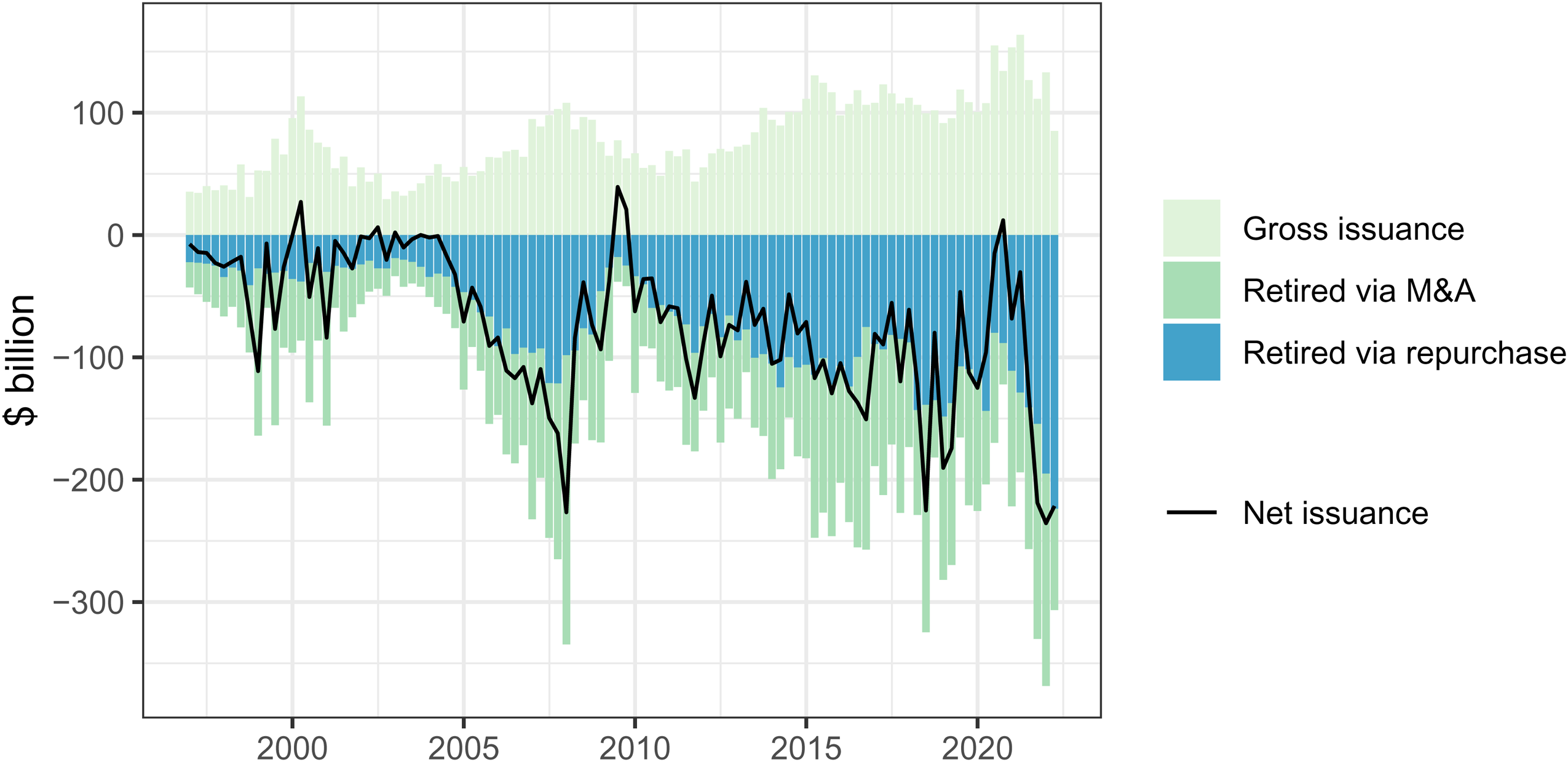

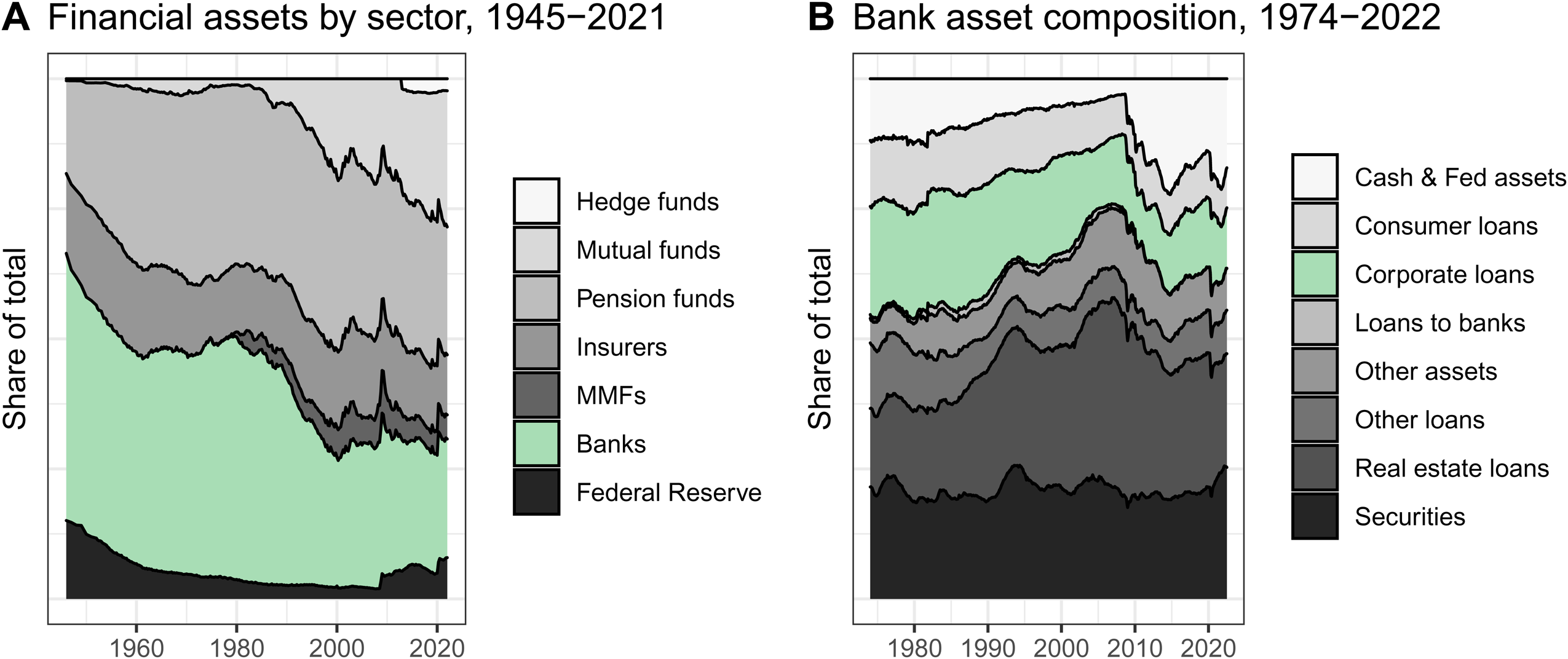

We can drill down further into the equity and loan categories. Figure 2 shows why net issuance of corporate equity in the United States has been negative since 1996. Although gross issuance has followed an upward trend, that growth has—until the beginning of the COVID-19 pandemic—been eclipsed by the retiring of shares via stock buybacks and mergers and acquisitions. Lending to nonfinancial corporations has also turned negative. Since the category “loans” also includes government loans and loans from nonbank financial institutions, shedding light on bank lending to nonfinancial corporations requires data on commercial bank assets, displayed in Figure 3. The first panel shows the declining importance of banks, whose share of total financial asset holdings has declined from 50 percent in 1945 to 25 percent today. The second panel shows that commercial and industrial loans have seen the largest decline in total bank assets, whereas real estate loans have seen the largest increase. At the same time, loans to nondepository financial institutions, such as private equity and hedge funds (not shown in Figure 3), have more than doubled in absolute terms since 2015, fueling leverage in the global shadow banking system. 21 This “debt shift” from business lending to mortgage lending and intrafinance lending has been documented for a large number of countries. 22 In sum, while banks remain the pivotal actors within the financial system, their traditional creditor power vis-à-vis the nonfinancial corporate sector has, at least in relative terms, diminished. 23

Net corporate equity issuance, United States, 1996–2021. (Federal Reserve, US Financial Accounts.)

The declining relative size of US banks and of their corporate lending. (Federal Reserve, US Financial Accounts.) MMFs are money market funds. Bank data include US branches and agencies of foreign banks.

Given these developments, how have wealth owners fared? Other things equal, the corporate sector's declining demand for financing should put downward pressure on corporate bond and equity yields. However, things have not remained equal, and the “plunder” has, if anything, escalated. 24 The best measure of rentier power—Piketty's r − g, the gap between the rate of return on capital (r) and the rate of economic growth (g)—has proven remarkably resilient. 25 Indeed, the data collected by Jordà et al. on real returns on wealth indicate a larger r − g gap for the four decades since 1980 than during any comparable period since the late nineteenth century. 26 These data point to the enduring power of finance in the economy. Are we, therefore, in a Wile E. Coyote moment, in which the structural power of finance holds up while its institutional underpinnings have already crumbled? Or has there been a change in the mechanism through which this power operates?

Structural Power and the Return of Finance Capital

The ability of capitalists to hold back investment or to permanently move capital elsewhere is the subject of a large literature on the structural power of business. 27 The literature on the structural power of finance is more explicitly focused on exit, the threat of which became much more potent with global financial liberalization. 28 Political economists have studied financiers’ ability to (threaten to) withdraw credit or portfolio investment from firms, sectors, or entire countries, both in the Global South and in the Global North. 29 Subject to certain scope conditions—such as issue salience, regulatory capacity, intrafinance disunity, and the characteristics of the state-finance nexus 30 —exit-based structural power allows financial actors to “influence the policy choices of corporate and sovereign borrowers.” 31 Crucially, exit-based power not only requires little organization on the part of capital, it also remains largely invisible and, therefore, depoliticized—there simply seems to be no alternative for firms or policymakers. 32

In recent decades, however, the growth of institutional capital pools has strengthened the control-based power of finance vis-à-vis the nonfinancial corporate sector. Control-based power, too, is “structural” in that it arises from structural tendencies within capitalism. To see why, it is important to recall Rudolf Hilferding's analysis of early twentieth-century “finance capital,” the relevance of which for early twenty-first-century financialization has long been emphasized by Marxist scholars. 33 Taking his cue from Marx and anticipating the arguments of Braudel and Arrighi, Hilferding viewed finance capital as the outcome of an extended period of capitalist accumulation, during which a “steadily increasing proportion of capital in industry does not belong to the industrialists who employ it” but instead belongs to the banking sector, which in turn “is forced to keep an increasing share of its funds engaged in industry.” This “capital in money form which is . . . transformed into industrial capital” is what Hilferding called finance capital. 34 The hallmarks of finance capitalism were the dominance of the financial sector—as opposed to states, families, or individuals—among the creditors and shareholders of corporations and the high degree of control the financial sector exercised in the corporate economy.

Hilferding saw in finance not just a source of financing but also a means of (re-)organizing industry. Capitalists whose profits exceeded what they could, or wished to, reinvest looked to the banks for returns, thereby pushing banks to increase their lending, as well as their purchases of debt and equity securities. As a result, banks acquired “a permanent interest” in corporations and faced the problem of control—corporations now had to be “closely watched . . . and so far as possible controlled by the bank in order to make the latter's profitable financial transaction secure.” 35 Although historians of corporate governance regimes around 1900 tend to reach more nuanced conclusions about the power of “Morgan's men,” Hilferding's point stands: both in the United States and in Germany, banks’ role in corporate governance was geared toward minimizing competition, maximizing profits, and thus bolstering the ability of corporations to service their debts and pay out dividends. 36

This control-based understanding of the power of finance capital was largely forgotten in the political economy literature, but it lived on in the sociology of the corporate elite and in the French regulation school. The former focused on the power of corporate managers and the network of interlocking directorates, especially in the United States. While scholars debated the relative influence of the corporate versus the financial communities, a consensus emerged that an “inner circle” existed whose power was rooted not primarily in ownership but in a dense and stable interlocked network. 37 Hilferding's ideas also informed the French regulation school. Taking his cue from Baran and Sweezy, Michel Aglietta diagnosed a strong tendency toward “capital concentration” for US capitalism. Finance capital constitutes “the ultimate mode of capital centralization” that took “concrete form in financial groups” whose economic importance consisted in their ability to foster “the cohesion of finance capital”—that is, to act as aggregators and coordinators of the interests of wealth owners. 38 More recently, however, Hilferding has seen a revival. Some of the best attempts to theorize the post-2008 configuration have revolved around the concept of the “new finance capital.” 39

Hilferding's analysis is key to understanding how the current financial configuration is linked to the structural dynamics of capitalism. At the level of agency, however, there is an important discontinuity. Who are the agents of finance capital? When Aglietta asked this question based on data for 1968, he found that banks still dominated the financial landscape. Since then, however, banks have been joined, and then increasingly overshadowed, by what Aglietta called institutions of “contractual saving,” and what this article refers to as “institutional capital pools.” This diverse group comprises asset owners—pension funds, insurers, endowments, sovereign wealth funds, and the family offices of the superrich—and their asset managers. 40 Funded pension systems have been the most important driver of the rise of institutional capital pools, and the chief source of growth for asset management companies. 41 Asset managers are intermediaries who invest other people's money for a fee. Just like pension funds pool the savings of many households, asset managers pool the capital of many institutional investors (as well as households). The asset management sector comprises mutual funds and exchange-traded funds, as well as less regulated and more leveraged institutions, namely, hedge funds, private equity funds, and venture capital funds. The sector has seen exceptional growth over the past half century. Since the global financial crisis, most large banks have moved into asset management, as have many insurers. On the list of the world's top ten asset managers, BlackRock and Vanguard are closely followed by the asset management arms of Goldman Sachs, Allianz, and the like.

A comprehensive comparison between exit-based and control-based financial-sector power would need to consider all major asset classes, including listed and unlisted corporate equity, corporate, household, and government debt, and real estate. The remainder of this article focuses on listed equity, and thus on corporate governance.

The Rise of Control

The theoretical, legal, and practical edifice of corporate governance was erected on a foundation defined by the “Berle-Means-Jensen-Meckling ontology.” 42 According to this ontology, shareholdings in the United States were dispersed among atomistic, weak shareholders (the Berle-Means component) who were, nevertheless, the only stakeholders with a long-term interest in the economic performance of the corporation, whose governance they therefore ought to dominate (the Jensen-Meckling component). The main power resource of these individually weak shareholders was their ability to exit by selling their shares, thereby pushing down the share price and exposing corporate managers to the dangers of the market for corporate control. 43 This ontology has also underpinned the comparative political economy literature, which equated institutional investors in liberal market economies with “impatient” capital, in contrast to the “patient” capital provided by banks and other strategic blockholders in coordinated market economies. 44

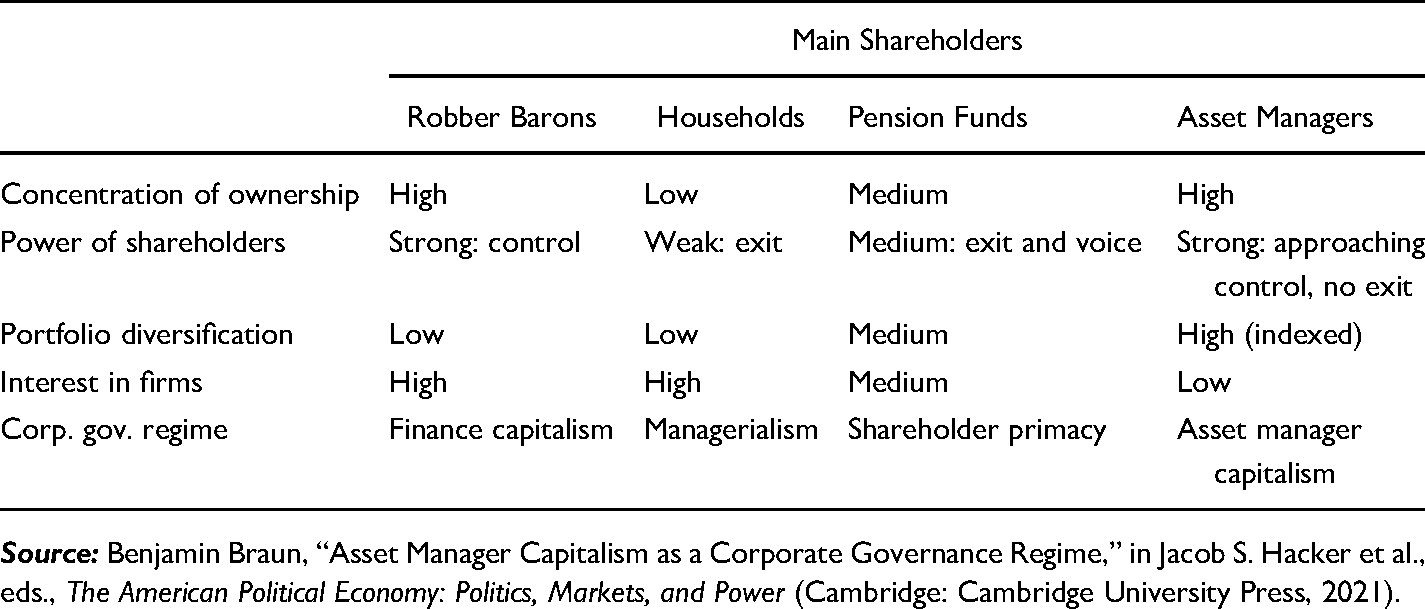

The Berle-Means-Jensen-Meckling ontology does not, however, map onto the new landscape of asset manager capitalism. Table 1 presents a stylized overview of the evolution of US corporate equity ownership and corporate governance since 1900. Each of the four columns represents a distinct corporate governance regime, classified according to four criteria. The hallmarks of finance capitalism were a high concentration of share ownership, substantial control exercised by shareholders, poorly diversified portfolios, and therefore a strong shareholder interest in the performance of individual firms. This regime gave way under the early twentieth-century diffusion of share ownership, which brought about the separation of ownership and control and ushered in managerialism. Driven by the growth of institutional capital pools, the post–World War II decades then brought a “Great Re-concentration” of shareholdings, weakening shareholders’ exit options while strengthening their control. Today, the United States is no longer the dispersed ownership society that scholars across disciplines and across generations—from Berle and Means, to Jensen and Meckling, to Hall and Soskice—took for granted. This section traces the regime shifts from managerialism to shareholder primacy, and from shareholder primacy to asset manager capitalism.

Hallmarks of Shareholder Power under Four Corporate Governance Regimes.

Shareholder Primacy: Exit Plus Voice

Among the drivers of the transition from managerialism to the shareholder primacy regime, the rise of the law and economics movement and the growth of institutional investors stand out. 45 Law and economics took the corporate governance field by storm via the idea of a “market for corporate control,” which redefined the economic function of capital markets. 46 Manne's idea underpinned Jensen and Meckling's agency theory of the corporation, which revolved around the idea of a conflict of interest between weak outsiders (shareholders) and strong insiders (managers) and therefore the need, justified on efficiency grounds, to strengthen the rights of shareholders vis-à-vis managers. By the end of the 1970s, agency theory had reduced the complex political question of how to organize the corporate system to the need to protect outside shareholders against “expropriation” by insiders. 47 Although the law and economics movement paved the ideological ground for the shareholder primacy regime, it could hardly have succeeded had it not been for the rise of institutional capital pools. 48

Two developments related to institutional capital pools tipped the balance in favor of shareholders—the takeover wave led by private equity firms, and the rise of pension funds pushing for governance reforms. The 1980s saw the emergence and rapid growth of private equity firms. 49 Specializing in leveraged buyouts of listed firms, these “corporate raiders” systematically dismantled the conglomerates managerialism had built. 50 From a structural power perspective, the significance of the creation of a market for corporate control was that it weaponized the exit option. While shareholders had always had the option to sell their holdings in a corporation, managers did not need to worry too much about the resulting downward pressure on the share price. The emergence of institutional capital pools with a business model centered on hostile takeovers and asset stripping fundamentally changed the managerial calculus regarding the price of their company's stock.

The rise of buyout firms coincided with an explosion in the growth of pension funds, whose direct holdings of total corporate equity (listed and unlisted) reached an all-time high of 27 percent in 1985. 51 What made US institutional investors such a revolutionary force was their unique “capacity to unite liquidity and control.” 52 Public pension funds’ equity stakes—approaching but rarely exceeding 1 percent—were small enough to make exit a credible threat and, at the same time, large enough for their voice to carry weight within the newly shareholder-friendly corporate governance system. 53 Indeed, public pension funds emerged as the driving force of the corporate governance reforms of the 1990s and early 2000s, successfully campaigning against poison pills, and for independent directors, destaggered boards, and proxy voting. 54 At the same time, these funds, despite holding diversified portfolios, were generally still active stock pickers and traders. An asset-weighted turnover rate of between 60 and 80 percent in the early 1980s certainly justified their reputation, in the comparative political economy literature, as “impatient” investors. 55

By the mid-2000s, the “revolt of the owners” was over. 56 Not only in the United States and the United Kingdom but across many advanced economies, CEO remuneration was now tied to stock market performance, 57 minority shareholder rights were highly protected, and private equity and hedge funds enforced the rules of the game via the (newly) liberalized market for corporate control. 58 Such was the success of the owners’ revolt that two legal scholars declared the “end of history for corporate law.” 59 Their declaration could hardly have been timed more poorly.

Asset Manager Capitalism: De Facto Control Plus Diversification

Whereas pension funds pool the retirement assets of households, asset managers pool assets of both households and institutional investors. This makes them very large. The resulting shift in the US stock ownership structure from dispersed to concentrated was not anticipated and caught most corporate governance scholars by surprise. In 2009, the very first sentence of an article published by leading finance scholars in a leading finance journal still described dispersed ownership in the United States as “one of the best established stylized facts about corporate ownership.” 60 At that point, however, BlackRock's average equity stake in S&P 500 companies had already surpassed 5 percent.

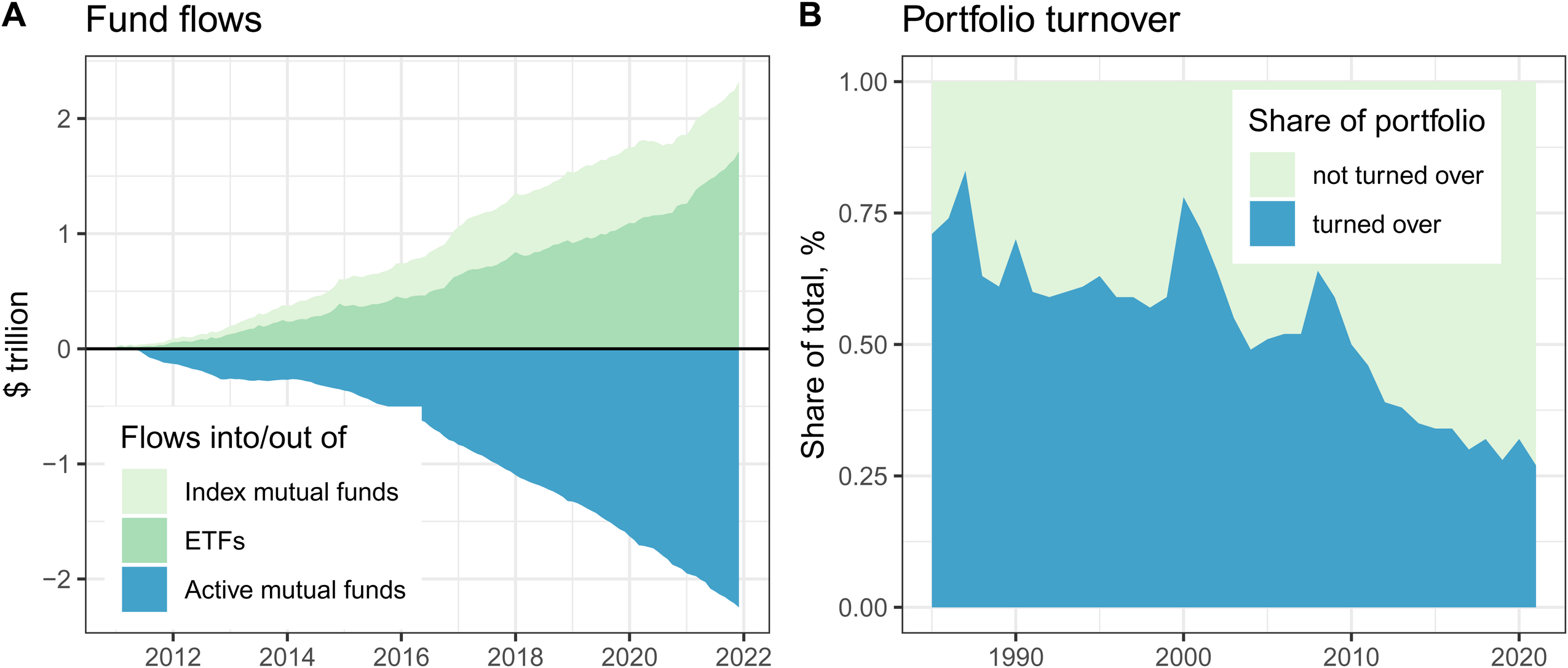

The implications of this Great Re-concentration for the power of finance are not straightforward. Consider, first, the question of exit. In their quest for scale, large asset managers have essentially relinquished the option to exit individual investments. 61 This is a consequence, first, of the size of their stakes in individual companies, which even in a liquid market cannot be sold without causing a major drop in the share price. Indeed, as shown in Figure 4, Panel B, the turnover rate in mutual fund equity portfolios has continuously declined over the past four decades, from around 70 percent in the late 1980s to around 30 percent in recent years. Second, the loss of exit is a feature of the index-tracking investment strategies pursued by the majority of funds offered by the Big Three asset managers. Figure 4, Panel A, shows that investors have reallocated almost $2 trillion from actively managed domestic mutual funds to index-tracking equity funds over the past decade. These data points should be seen in the context of the evidence, cited above, of the declining dependence of the corporate sector on outside financing. In addition to corporations borrowing less from banks and capital markets, they also have less to fear from the trading of their outstanding equity liabilities on the stock market. Exit-based theories would predict the power of large asset managers to be weakened by this decline of exit options. 62

Indicators of declining exit options for US domestic equity funds. (Investment Company Institute Factbooks 2021 and 2022.) Panel A, domestic equity funds. Mutual fund data include net new cash flow and reinvested dividends; ETF data for net share issuance include reinvested dividends. Panel B, asset-weighted averages for mutual equity funds.

However, exit was, and is, a relatively weak mechanism to enforce shareholder power. Where there's a seller, there's also always a buyer. Unless the volume of shares sold is large, the impact on the share price is small. Even the combination of exit and voice—the hallmark of the shareholder primacy regime—was often insufficient for even large institutional shareholders to prevail in conflicts with corporate management. 63 Today, however, managers of S&P 500 companies face a highly concentrated ownership landscape in which the joint holdings of BlackRock and Vanguard often approach 20 percent—a common threshold to identify controlling shareholders. 64 Thus, although the largest shareholders have lost the option to exit individual portfolio companies, they have gained a considerable degree of control.

At the same time, today's dominant shareholders are fully diversified. Pension funds, in order to achieve reasonably high diversification, could only hold relatively small stakes in individual companies, which limited the effectiveness of their voice in corporate governance. The growth of asset managers eliminated this temporary bottleneck. Large institutional capital pools (pension funds) could now pool their investments in even larger institutional capital pools (asset managers). Contrary to the previous dynamic, pension funds’ quest for diversification now contributed actively to the strengthening of shareholder control, exercised by asset managers. As a result, for the first time, shareholder control and full shareholder diversification have ceased to be mutually exclusive.

The combination of control and full diversification is what marks asset manager capitalism as a distinct corporate governance regime (see Table 1). At the same time, however, it is largely accidental. Rather than the outcome of BlackRock and Vanguard seeking control over portfolio firms, the size of their shareholdings is a by-product of their success in the market for equity investment funds, both active and index-tracking. They would, arguably, prefer to manage $10 trillion each without holding 10 percent stakes in most S&P 500 companies. Alas, there is nowhere else for this money to go. Inevitably, this puts these firms in the spotlight, exposing them to unwanted public and political scrutiny that could result in costly regulatory policies. The politics of actually existing asset manager capitalism boils down to this dilemma—maximizing assets under management, while minimizing the risk of political and regulatory backlash. More than a corporate governance asset, control-based power represents a political liability.

The Politics of Actually Existing Asset Manager Capitalism

The behavior of diversified “universal owners” should differ from that of nondiversified shareholders. 65 Specifically, instead of pushing individual corporations to do whatever it takes to maximize profits, universal shareholders should act as “forceful stewards” to internalize negative external effects from the conduct of individual portfolio companies. 66 The theoretical and legal case for diversified asset managers to wield their power so as to minimize negative externalities at the portfolio level is compelling. 67 Following the invention of environmental, social, and governance (ESG) investing in 2004, the discourse and practice of ESG increasingly defined the rules of the universal-ownership game. 68 Asset managers embraced the ESG rhetoric, presenting themselves as quintessential long-term shareholders. 69 They supported establishing so-called stewardship codes in dozens of countries, which spell out the implications of ESG for shareholder engagement. 70 For a decade, Larry Fink, the CEO of BlackRock, has made a point of sending an annual letter to all CEOs of BlackRock's portfolio companies in which he extols the virtues of “long-term thinking,” “sustainability,” and “corporate purpose.” At the time of writing, however, it is clear that asset managers have systematically engaged in “greenwashing”—the misrepresentation of investment products as more environmentally sustainable than they are, while refraining from enforcing ESG principles at their portfolio companies. 71 Why have asset managers not used their control-based power for an aggressive corporate governance push for decarbonization?

The Broken Promise of Universal Ownership

The first step toward an answer is a critique of the “Berle-Means-Jensen-Meckling ontology,” especially of its concept of ownership. 72 Berle and Means defined ownership as “having interests in an enterprise.” 73 The entire edifice of agency theory hinges on the assumption that shareholders have more skin in the game than either managers or workers. 74 Yet precisely this assumption has become difficult to defend. That the corporation itself “is not an object of property rights” in US corporate law and is therefore not “owned” by its shareholders has been known for some time. 75 However, as agency relationships have proliferated, even share ownership has fragmented along the investment chain. 76 Asset managers, who hold shares and control the associated voting rights, have a fiduciary duty to asset owners (e.g., pension funds), who have a fiduciary duty to the individual savers who are the ultimate beneficiaries of this investment chain. In other words, the separation of ownership and control has been joined by the “separation of ownership from ownership.” 77 At the same time, asset managers are profit- and shareholder-oriented corporations themselves. For their business model, corporate governance is a second-order variable that matters only to the extent that it impacts assets under management, fee income, and costs. Here, too, for-profit asset managers are fundamentally different from not-for-profit asset owners, such as pension funds. Asset managers have much more to lose from actions—such as casting their proxy votes against management—that could cause the latter to retaliate by shifting corporate retirement plan assets to competing asset managers. 78

It is therefore not surprising that the empirical evidence provides scarce support for the forceful stewardship hypothesis. Baines and Hager, who focus on the proxy voting record of the Big Three asset managers at the shareholder meetings of a group of fifty-five fossil fuel, mining, and cement companies, have found that the Big Three “seldom defy management in supporting shareholder resolutions aimed at improving environmental governance” and that “the voting behavior of their ESG funds . . . is almost identical to that of their non-ESG funds.” 79 Similarly, a study of 146 shareholder resolutions related to environmental and social issues, from the 2021 proxy season, has shown that the world's six largest asset managers are more likely than almost all their peers to vote against those resolutions. 80 All six supported fewer resolutions than recommended by the two leading proxy advisory firms, ISS and Glass Lewis. For a significant number of resolutions, the lack of support from the largest asset managers proved decisive. While 30 out 146 resolutions passed, 18 more resolutions would have passed had one or more of the Big Three voted yes. In other words, the voting power that comes with large shareholdings effectively makes BlackRock, Vanguard, and State Street the decisive swing vote on controversial shareholder resolutions. To date, they have used that power to shield corporations from the environmental and social demands tabled by activist shareholders. The counterargument that large asset managers do not depend on voting because their size allows them to engage with portfolio companies behind closed doors is also invalidated by the data, which show that index funds are less likely than other funds to engage with portfolio firms. 81

For corporate governance to reflect the logic of universal ownership, asset managers would have to enforce it, which the available evidence suggests they are unable, or unwilling, to do. The same is not true for the logic of “common ownership,” which is largely self-enforcing. Here, the question is whether the same small group of asset managers holding significant stakes in all competing firms in a given sector is associated with anticompetitive behavior by portfolio firms. 82 Common ownership can be understood as the evil twin of universal ownership. 83 Whereas the latter postulates the internalization of negative environmental or social externalities at the level of the entire portfolio, the former postulates, for the sectoral level, the internalization of the negative externality competition exerts on profits. The agenda-setting studies in this field have found evidence that when competing firms in the same sector—notably, airlines and banks—have the same dominant shareholders, anticompetitive collusion becomes more likely. 84 The hypothesized causal mechanisms range from shareholder passivity, to large shareholder payouts reducing investment and thus product market competition, to shareholders actively discouraging price competition.

The question of a causal relationship between common ownership and oligopolistic pricing notwithstanding, the common ownership argument provides a better explanation of recent trends in corporate governance than the universal ownership argument. The rise of asset manager capitalism has coincided with a steep increase in payouts to shareholders. Figure 2 above, which is based on data for all listed US corporations, shows that average quarterly stock buybacks doubled from $51 billion during 2000–2010 to $106 billion during 2011–21. Similarly, between 2010 and 2020, both the average quarterly spending of S&P 500 companies on buybacks and the ratio of buyback spending to net income roughly doubled. 85 A similar pattern can be observed for executive remuneration, which almost doubled between 2000 and 2014 in the United States, while more than tripling in the United Kingdom, where pay increases with the size of shareholdings by US asset managers. 86

In light of the institutional realities of asset manager capitalism, how should these observed outcomes be assessed? Unlike pension funds under the shareholder primacy regime, BlackRock and Vanguard do have the power to enforce far-reaching changes at their portfolio companies. However, they have made no attempt whatsoever to orchestrate a rapid decarbonization of the economy. Following the revival of fossil fuel production in the wake of Russia's invasion of Ukraine, the largest asset managers stated explicitly that decarbonization, be it through divestment or engagement, was not their primary goal. Thus, Vanguard announced its intention to continue investing in fossil fuel industries because climate change was “only one factor in an investment decision.” 87 BlackRock announced that it considered many climate-related shareholder proposals made for the 2022 proxy season overly “prescriptive” and “[not] consistent with our clients’ long-term financial interests,” signaling that it was going to vote against them. 88 The firm followed through, reducing its support for US shareholder proposals on environmental and social issues by half, to a mere 24 percent. 89 What motivated this realignment of rhetoric and action?

Maximizing Assets under Management, Minimizing Political Risk

As in all politics, the politics of asset manager capitalism is driven by interests. On the revenue side, asset managers’ overriding interest is in maximizing their fee revenue, and thus their assets under management. For this, returns matter, but only indirectly, and to the extent that they cause asset owners to move their money to or from competitors. Instead, aggregate asset prices are the variable of greatest interest to (conventional) asset managers. This is because the fees they charge are calculated as a percentage of the current value of a client's assets. Across a large asset manager's portfolio of funds, the impact of individual fund performance on the growth of assets under management is far less than the impact of aggregate asset price developments.

Although forceful stewardship across the entire portfolio would, in theory, be a means to ensure high aggregate asset prices, a cheaper and simpler strategy exists: macroeconomic policies that sustain high asset prices. BlackRock's preference for such policies is illustrated by its strategic and persistent lobbying for expansionary monetary policy. 90 The actor with the greatest power over the asset management sector's profitability is the Federal Reserve, whose monetary policy decisions are the single most important driver of global asset prices. 91 For instance, in 2020, when the Fed's unexpected resumption of financial asset purchases sparked a stock market rally, net inflows of new money into the asset management sector contributed only $5 billion toward the sector's gross revenue increase, whereas the aggregate rise in asset prices contributed $29 billion. 92

On the cost side, the single most important risk for the Big Three asset managers is regulatory risk. This holds for financial firms generally, but the Big Three are treading a particularly tricky tightrope. Nowhere has this been more obvious than in the United States, where regulatory actions against asset managers are, at this point, as likely to originate from the left as from the right. Progressive Democrats criticize the Big Three for their complicity in perpetuating the distributional outcomes of the shareholder value regime and for not wielding their potential power in the service of a rapid decarbonization. Republicans, meanwhile, have rekindled their own brand of antifinance politics under the banner “woke capital.” 93 Senator Ted Cruz's recent comment that “every time you fill up your tank, you can thank Larry [Fink] for the massive and inappropriate ESG pressure” is representative of what has become a concerted Republican campaign against large asset managers. 94

Thus caught between a rock and a hard place, it appears that asset managers seek to perform as much environmental and social stewardship as necessary to appease progressives, while saying and doing as little as possible that could be weaponized by the ascendant antifinance wing within the Republican Party. 95 Larry Fink's most recent annual letter to CEOs, in which he explained that the “stakeholder capitalism” BlackRock had been advocating was neither “a social or ideological agenda” nor “woke,” illustrates the contortions required by this tightrope walk. 96 Fink has since doubled down, saying that he did not “want to be the environmental police.” 97 Beyond rhetoric, smoking gun evidence that BlackRock's proxy voting is driven by political rather than by universal-owner considerations can be found in the regional variation in its voting behavior: Since 2017, BlackRock has voted in favor of environmental and social shareholder proposals 87 percent of the time in ESG-friendly Europe, while voting against such proposals 84 percent of the time in North America. 98 In an evident attempt to further reduce its footprint in proxy voting, BlackRock, in late 2021, announced a pilot project to allow institutional investors in the United States and the United Kingdom the option to decide themselves how their proxy votes should be cast by BlackRock. 99 It has since expanded the program, dubbed “Voting Choice.” 100

BlackRock's pro-management stance in US proxy voting and its move toward redelegating proxy voting to institutional clients could not, however, prevent political backlash from the right. In May 2022, Dan Sullivan, a Republican senator from Alaska, together with ten cosponsors, introduced the Investor Democracy Is Expected, or INDEX Act. Under the bill, index-tracking asset managers holding more than 1 percent of a listed company's shares would be required to vote shares according to each individual investor's instructions. 101 Practical problems with implementation notwithstanding, such a rule would radically curtail the proxy voting power of the Big Three.

Conclusion

The declining dependence of nonfinancial corporations on outside financing and the growth of institutional capital pools have reduced the capacity of financial actors to sell their shareholdings in individual firms. As a result, exit is no longer the main mechanism underpinning the power of finance in general, and of shareholders in particular. Instead, control has largely replaced exit as the primary mechanism underpinning the power of finance vis-à-vis nonfinancial firms. The question is if, and how, the new finance capitalists wield this potential power.

Recent developments indicate that the largest asset managers have not been using their control-based power to push corporations to decarbonize. To explain this absence of forceful green stewardship, this article proposes a theory of actually existing asset manager capitalism. This theory acknowledges that for the largest asset managers, corporate governance outcomes are secondary concerns, less important than the twin goals of maximizing assets under management and minimizing political or regulatory backlash. In the United States, where both Democrats and Republicans have voiced ambitions to crack down on the Big Three asset managers, these goals have become increasingly difficult to reconcile. It is tempting to conclude that when financial institutions cross the size threshold at which they should, in theory, internalize negative environmental externalities, they have become too big to escape politics. Rather than externalities, BlackRock and Vanguard appear to have internalized the social forces that are holding back “forceful green stewardship” in Congress. In contrast to exit-based structural power, whose strength is enhanced by its depoliticized nature, control-based power is more visible, and therefore more easily politicized and contested.

Besides regulatory backlash, this politicization has manifested in a renewed debate about alternative, more democratic ways of organizing share ownership and corporate governance. 102 In particular, public options for asset management and public purpose–oriented alternatives to the corporate form have garnered increasing attention. 103 Here, a firm grasp of the historical uniqueness of asset manager capitalism can help make the case that the ideological defense of the shareholder primacy is bankrupt even on its own terms. The fragmentation of what the law-and-economics tradition called “ownership” and the breakdown of the Berle-Means-Jensen-Meckling ontology undermine the efficiency-based rationale for shareholder primacy. At the same time, the sustainability-based rationale is undermined by the reluctance of universal shareholders to deploy their control-based power in the service of a green transition.

Footnotes

Acknowledgments

This article owes much to the organizers of this special issue on the structural power of finance, Florence Dafe, Sandy Brian Hager, Natalya Naqvi, and Leon Wansleben. Earlier drafts have benefited from comments by Lucio Baccaro, Jens Beckert, Dirk Bezemer, Mark Blyth, Brett Christophers, Jeffrey Chwieroth, Daniela Gabor, Rainer Haselmann, Sebastian Kohl, J. W. Mason, Elsa Massoc, Enrico Perotti, Martin Schmalz, and Matthias Thiemann, as well as from feedback received at two events hosted by the LawFin Research Seminar of the Center for Advanced Studies on the Foundations of Law and Finance at Goethe University Frankfurt. The editors of Politics & Society have provided exceptionally constructive comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.