Abstract

Many developing and transitional countries have grown faster than advanced countries in the past decade, resulting in a shift in the distribution of world income in their favor. China is now the second largest economy in the world, behind the United States and ahead of Japan. As the relative economic weight of China and several others has come to match or exceed that of the middle-ranking G7 economies, the world economy has shifted from “unipolar” toward “multipolar,” less dominated by the G7. How is this change being translated into changes in authority and influence within multilateral organizations like the G20, the World Bank, and the International Monetary Fund (IMF)? Alarm bells are ringing in G7 capitals about G7 loss of influence. According to a WikiLeaks cable from the senior U.S. official for the G20 process, from January 2010, “It is remarkable how closely coordinated the BASIC group of countries [Brazil, South Africa, India, China] have become in international fora, taking turns to impede US/EU initiatives and playing the US and EU off against each other.”

This essay suggests that the shift in power is much smaller than the headlines or private alarm bells suggest. The United States remains the dominant state, and the G7 states together continue to exercise primacy, but now more fearfully and defensively. China is split between asserting itself as “the wave of the future” and defending itself as too poor to take on global responsibilities (it is roughly 100th in the per capita income hierarchy). The combination of G7 defensiveness and emerging states’ jealous guarding of sovereignty produces a spirit of Westphalian assertion in international fora, or “every state for itself.” On the assumption that the world economy is in a transitional period, the article suggests reforms in the G20 and the World Bank that would boost their role and legitimacy as multilateral organizations in a more multipolar world.

Until the lions have their own historians, the history of hunting will glorify the

hunters. Growth has gone south; debt has gone north.

In April 2010, Robert Zoellick, president of the World Bank, gave a speech hailed by some as the most important speech of a World Bank president since Robert McNamara’s in 1973, when McNamara set poverty reduction as the Bank’s new mission. Zoellick’s main point was the end of the Third World—the end of the distinction between developed and developing countries.

If 1989 saw the end of the “Second World” with Communism’s demise, then 2009 saw the end

of what was known as the “Third World.” We are now in a new, fast-evolving multipolar

world economy—in which some developing countries are emerging as economic powers; others

are moving towards becoming additional poles of growth; and some are struggling to attain

their potential within this new system.

1

Zoellick was in effect saying that the distribution of material power in the interstate system has become more fluid in the past decade than at any time since the beginning of the Cold War, and that we are finally at the end of the Truman era, which began in the early postwar years when President Truman called on the West to take up the challenge of using “our” knowledge and resources to deliver development to the rest of the noncommunist world. From a largely unipolar (noncommunist) world, with the United States as hegemon, we have moved to “a new, fast-evolving multipolar world economy” as economic weight and political power has flowed east and south. Zoellick went on to indicate how this multipolar world economy requires changes in the governance and operations of the World Bank to make it more multilateral, and less dominated by the Western states.

Zoellick implied a hopeful answer to a basic question: Will the international system be able to induce rule-bound cooperation between states, given the falling concentration of economic activity and political power in the West and the growing number and importance of “global problems” (including global warming, regulation of cross-border trade and finance, migration, criminal networks, nuclear proliferation, cyberwar, and many more)? Will the aging post–World War II legacy organizations, like the World Bank and the International Monetary Fund (IMF), be able to reform themselves so as to reflect the new multipolarity, while also strengthening their ability to provide public goods to their borrowers and the world economy at large? Will Southern states—on the other side of the Truman divide—become sources of initiative in interstate organizations, not just participants and takers?

While Zoellick implied a yes, it is equally plausible that the growing number and diversity of states with enough weight in the world economy to exercise voice about international governance has a centrifugal effect, intensifying assertions of Westphalian sovereignty, and that Southern states show no more inclination to take on leadership roles than in the past, even as they claim a larger presence.

In other words, economic weight and influence in governance are different things. The “rise of (some of) the rest,” combined with surging global problems, may not induce the established states to compromise with the newcomers and may not induce the newcomers to compromise with the established states or among themselves. All the more so for those countries in economic slump, with populations facing interrupted rising expectations, whose governments like to respond to accumulating social anger by blaming outsiders. And all the more so for fast-growing China, with hundreds of millions of people experiencing relative deprivation as millions of fellow citizens become superrich, while an authoritarian government tries to suppress news of domestic abuses of power and bristles at criticism from other states, interpreting it as infringement of sovereignty. 2

The outcome may be “multipolarity without multilateralism,” as newly empowered states go their own way. Respect for the dissenting views of the now more numerous players may shrink the scope of cooperative solutions to global issues and tend toward stalemate.

The G20 and the Bretton Woods organizations have their very identities rooted in inclusion of both Northern and Southern states. Governance reforms in all three since 2008 have been heralded as major advances in multilateralism. When the G20 was upgraded from finance ministers level to heads-of-government level in November 2008 (in the wake of the fall of Lehman Brothers and the onset of the global financial crisis), President Nicolas Sarkozy of France enthused, “The G20 foreshadows the planetary governance of the twenty-first century.” Stewart Patrick of the U.S. Council on Foreign Relations describes the G20 as “the most significant advance in multilateral policy coordination since the end of the Cold War.” 3 Similar enthusiasm greeted the governance reforms at the World Bank and IMF announced in 2010. How should we interpret these claims? 4

First, I will introduce a more general discussion of polarity and governance, then return to the organizations themselves.

The Starting Point: The U.S.-Dominated Unipolar System

For most of the second half of the twentieth century, the United States was by far the largest national economy in terms of gross domestic product (GDP) and one of the most prosperous in terms of average income. It exercised political primacy in the noncommunist world, using its position to promote a liberal, market-based economic order.

The Bretton Woods system of the postwar decades up to the early 1970s did impose some constraints on U.S. policy through the dollar–gold link, but since its breakdown, the United States has been largely unconstrained in its monetary and fiscal policies by the need to take account of other states’ interests. For example, leading up to Paul Volcker’s decision to hike the Federal Reserve rate in 1979 (to curb U.S. inflation), the Fed did no analysis of the impact on the rest of the world, and specifically not on the impact on Latin America—which, having loaded up on debt from U.S. banks, was plunged into a decade-long debt-and-development crisis. 5

Indeed, for the whole period from the 1940s to the 2000s, U.S. monetary policy was set almost entirely for U.S. objectives, although it strongly affected global economic conditions. Thanks to its currency also being the main international reserve currency, the United States was able to run current account deficits every year from 1992 to 2010, eighteen years—its deficit in 2008 being about the size of India’s GDP. These deficits strongly affected financial stability and economic growth in the rest of the world, but the rest of the world had no say in U.S. policies. As a senior U.S. official remarked, “The dollar is our currency but your problem”; or in the more colorful language of President Richard Nixon, “I don’t give a [expletive] about the lire!”

The United States has exercised predominant power in the IMF and the World Bank, crystallized in its monopoly of the presidency of the Bank and the number two position at the IMF, and its veto over decisions requiring a supermajority, the only state with such power. The veto enables the United States to block changes on its own, without the support of even one other state. Conversely, the IMF has always been very weak in its ability to discipline the United States. Joe Stiglitz tells how when he was chair of the Council of Economic Advisors he saw the Treasury ostentatiously toss the Fund’s Article IV consultation reports on the U.S. economy in the rubbish bin. 6

U.S. choices were at the center of everything, not just in American eyes but also in European eyes. When it was the turn of a European country to chair the G7 or G20 meetings, the sherpa from that country routinely consulted his U.S. counterpart before consulting other Europeans. Only around 2000 did the German sherpa make a determined effort to consult with other Europeans before consulting with the United States. 7

This is the substance behind Financial Times columnist Philip Stevens’ summary remark, “Membership of the west once meant doing whatever Washington said.” 8

Rise of Multipolarity

The rise of multipolarity (in the economic rather than bombs-and-rockets sense) means a fall in the concentration of economic activity in the international system and, within this, the rise of concentrations outside the previous core. The trend can be made more concrete by means of several indicators.

Share of G7 (12 percent of world population) in global GDP: In 2000, the G7’s share was 72 percent; by 2011 it will have fallen to 53 percent, according to the IMF (measured at market exchange rates).

China’s rise: Chinese output per head to that of the United States rose from about 6 percent to 22 percent between 1980 and 2008 (the proportion in 2008 was roughly similar to Japan’s in the late 1940s).

Whose monetary policy matters to the rest of the world? Ten years ago, the world paid attention to U.S. and EU monetary policy, and nobody outside China paid attention to China’s monetary policy. Today China’s monetary policy is closely watched, especially in New York; Washington, D.C.; and London.

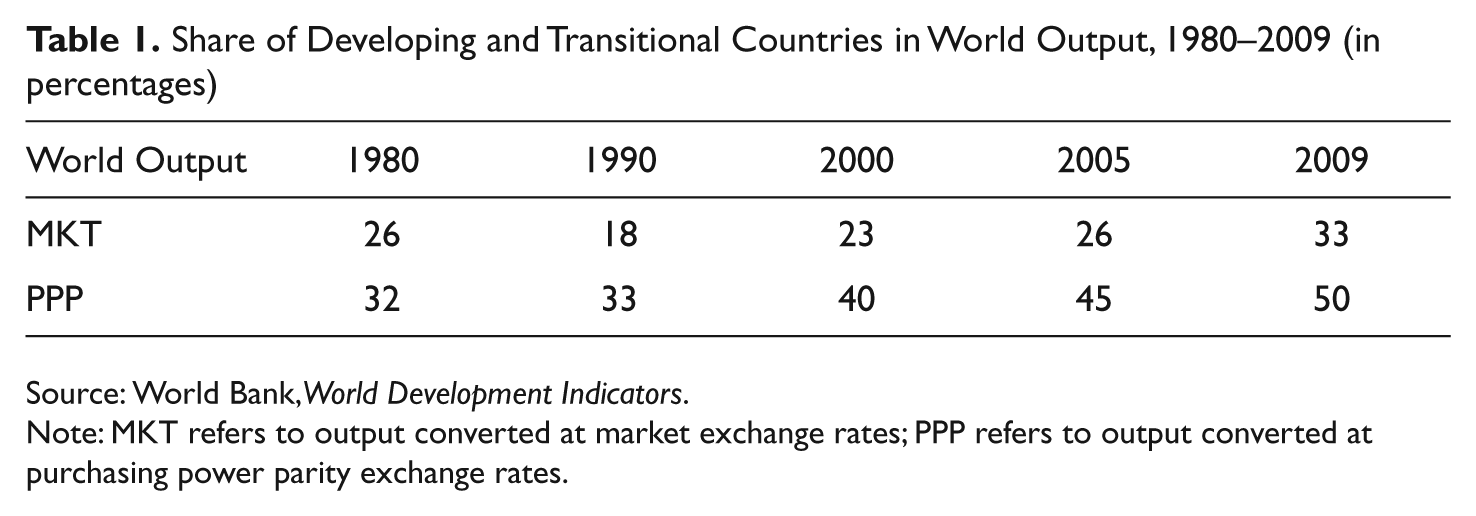

Share of developing and transitional countries (DTCs) in world output: Between 2000 and 2009, the share of DTCs in world output rose by 10 percentage points, from 23 percent to 33 percent (measured at market exchange rates) and from 40 percent to 50 percent measured in purchasing power parity dollars. See Table 1.

South-South trade: In 1997, the ten biggest Asian exporters (excluding Japan) sent 46 percent of their exports to the United States, the EU, and Japan; in 2009, only 36 percent, the difference going to developing countries and oil exporters. China is now Brazil’s biggest trading partner, displacing the United States from its long-held top spot.

EU and euro: The EU, for all its recent travails, is slowly becoming more cohesive than it was; and the euro is slowly becoming the world’s second main international reserve currency. (The share of the euro in world foreign exchange reserves rose from 18 percent in 1999 to 27 percent in 2009.) So the increasing economic cohesion in Europe—together with its sheer economic weight in the world economy—makes it a separate source of pressure on the international economic governance system.

Share of Developing and Transitional Countries in World Output, 1980–2009 (in percentages)

Source: World Bank,World Development Indicators.

Note: MKT refers to output converted at market exchange rates; PPP refers to output converted at purchasing power parity exchange rates.

For convenience, we can think of the new multipolarity in economic and financial affairs as involving three poles—the United States, the EU, and BRICs (Brazil, Russia, India, and China). This sets the context of the new Great Game, with four qualifications. First, the BRICs have little collective identity. The leaders of the four states met for the first time as a fraternity of rising powers as recently as June 16, 2009, in Russia. (However, for the past couple of years, the BRICs executive directors at the World Bank have met together once or twice a month, as have those at the IMF.) Second, when used as the third pole, BRICs have permeable boundaries and may include a larger number of states, including middleweights like Korea, Mexico, and Turkey. Third, the BASIC group (BRICs minus Russia and including South Africa) has also been meeting to concert actions in multilateral fora. Fourth, for some purposes, the operative G is the G2 (United States and China).

Stronger Multilateralism?

Has the big increase in the relative economic size of the world’s southern poles translated into stronger multilateralism in global economic governance?

Several indicators might be used. One is entry of new states to apex governing forums (such as the expansion of the G7 to the G20). Another is increased voting power of Southern states in international organizations. A third might be new agreements on global issues subscribed to by many states of North and South.

We also have to distinguish modes of participation. One is “hegemonic incorporation,” in which the organization becomes more inclusive, the larger body reaches agreements, but the agreements are scripted by the hegemon or hegemonic core. 9 New members go along with the wishes of the dominant states and use their participation to secure national advantage within this constraint. A second mode is “multilateral cooperation,” where member states are willing to compromise in order to reach agreements and initiatives that come from across the membership, not just from the old hegemonic core. A third is Westphalian assertion, where states assert national sovereignties in the form of “nos,” yielding cooperation mainly for the purpose of blocking initiatives of others—which may be masked by agreement on fine words.

Participation in a given forum (such as the World Bank) will probably oscillate on a continuum between these modes, the center of gravity moving over time. And as multipolarity increases (as countries outside the old core become economically more powerful, and clusters of countries gravitate to form new poles), country clusters may act in one mode internally (for example, cooperation or incorporation) and in another mode with other clusters in the same forum (for example, assertion).

The Multipolar Governance Dilemma

Multipolarity generates a higher premium on policy cooperation between sovereign states than a unipolar system does; but larger numbers of states with larger differences in their preferences, interests, and beliefs make cooperation more difficult to achieve and sustain. In the words of a report on the new U.S. national security strategy, “Strengthening ties is proving far harder than the Obama administration had bargained for, but it is difficult to see that it has any other choice.” 10

This is the “multipolar governance dilemma.” On the face of it, the dilemma has so far proved not too difficult. The formation of the G20 at finance ministers level in 1999 and its upgrading to heads-of-government level in 2008; the governance reforms at the World Bank and IMF announced in 2010; the new global rules on banking supervision, known as Basel 3, approved by the G20 leaders at the Seoul summit in November 2010—these and other developments suggest a real expansion of multilateral cooperation.

But look a little deeper and it is not hard to find evidence across many domains that interstate cooperation has either stalled (exchange rates, the Doha trade round, global warming) or has labored mightily to produce a mouse (Basel 3, the Cancun climate change road map of December 2010). 11

As for leadership, a study of transnational institutional innovations in the past one-and-a-half decades comes to negative conclusions about the role of Southern states and nonstate actors. Looking at more than 50 cases of institutional innovation—including transgovernmental networks (e.g., in finance, and accounting), arbitration bodies (e.g., the World Bank’s Inspection Panel), multistakeholder bodies (e.g., Global Polio Foundation), and voluntary regulation (e.g., Marine Stewardship Council)—it finds a pronounced North-South governance gap:

Many of the programs rely on Southern participation and serve the interests of Southern

stakeholders, [but] none of the innovations in transnational governance

gathered here can be described as a Southern-led initiative. Instead, Northern actors

have driven institutional innovation: states, NGOs [nongovernmental organizations],

corporations, and international organizations. While some of the innovative institutions

(e.g., the World Commission on Dams . . .) have been careful to try to ensure Southern

participation, and many of the programs target policies in the global South, Southern

leadership remains limited.

12

Against this background, let us consider trends in the G20 and the Bretton Woods organizations.

G20

The G20, as noted, is a direct answer to the rise of multipolarity. It remains an informal grouping, a club. It is organized with an annually rotating chair and secretariat provided by the chair’s government. What the G20 says and does depends heavily on the chair, or on the ability of others to manipulate and incentivize the chair. 13

Origins

The East Asia/Russia/Brazil crisis of 1997–99, with the Long-Term Capital Management crisis in the middle, provoked panic in the High Command of world finance. Federal Reserve chairman Alan Greenspan declared in October 1998, “I have been looking at the American economy on a day-by-day basis for almost a half century, but I have never seen anything like this.” 14 Panic prompted an upsurge of proposals for a “new international financial architecture” (NIFA). The G7 finance ministers and central bankers quickly realized that a larger deliberation group had to be convened. Otherwise they would be like the captain of the ship who stands at the wheel turning it this way and that, knowing that the wheel is not connected to the rudder. 15

The Europeans wanted the expansion to take the form of the G7 plus five “outreach” countries (the five invitees to be chosen ad hoc by the G7). The Americans and Canadians wanted a bigger and more representative grouping. This was an unusual response from the United States, whose general principle of multilateralism is “smaller and informal is better.” Behind the normative flag of “more representation,” the United States wanted to bring in more U.S. allies to counter the overrepresented Europeans, as part of a broader effort to de-Europeanize the governing boards of the IMF, the World Bank, and many other multilateral organizations in favor of DTCs.

The specific initiative came from Canadian Prime Minister Paul Martin and U.S. Treasury Secretary Lawrence Summers. The selection of the new members was made by Summers’ deputy, Timothy Geithner (then in charge of international economic affairs) and his counterpart in the German Finance Ministry, Ciao Koch-Weser, former managing director at the World Bank. 16 In 1999, they had several transatlantic telephone calls, each equipped with a list of the world’s countries and their GDP, population, trade, and the like. They proceeded down the list, ticking some countries and crossing others: Canada in, Spain out, South Africa in, Nigeria and Egypt out, Argentina in, Colombia out, and so on. They sent their list to the other G7 members. Once approved, invitations were dispatched to the first meeting of G20 finance ministers and central bankers.

The G20 includes nineteen states plus the EU. The twelve newcomers meet the criterion of being large by GDP or population (though the resulting nineteen are not the nineteen biggest by either measure). The emphasis on sheer size means that the G20 could be called “multilateralism of the big,” or MOB for short. But the United States also shoehorned in some of its relatively small allies, such as Australia, Argentina, Saudi Arabia, and South Korea. 17

As long as the G20 remained a gathering of finance ministers and central bankers, it had a useful but minor role in the play of events. Once it became clear that the East Asian/Russian/Brazilian crisis would not ricochet out of the periphery and into the West, the G7 finance ministers lost interest in talking about NIFA and began to lose interest in the G20 meetings. They sent ministers and officials of decreasing seniority.

The global crash of September 2008 revived the finance ministers’ meetings and prompted the government of George W. Bush to call the G20 leaders (G20L) together for the first time, to constitute an ongoing leaders’ forum. The leaders boldly announced their intention to make themselves the global economic steering committee. The communiqué of the second summit (London, April 2009) read,

We are determined to reform and modernize the international financial institutions to

ensure they can assist members and shareholders effectively in the new challenges they

face. We will reform their mandates, scope and governance [emphasis

added] to reflect changes in the world economy and the new challenges of

globalization, and that emerging and development economies, including the poorest,

must have greater voice and representation. This must be accompanied by action to

increase the credibility and accountability of the institutions through better

strategic oversight and decision making.

The communiqué from the third summit, September 2009, read,

We designated the G20 to be the premier forum for our international economic

co-operation. After this crisis, critical players need to be at the table and fully

vested in our institutions to allow us to co-operate to lay the foundation for strong,

sustainable and balanced growth.

Legitimacy

The G20 has unquestioned legitimacy in the eyes of its members, who collectively boost it as the top table of global governance (excluding matters of security and war, where the UN Security Council remains the apex). In its own words, its “economic weight and broad membership gives it a high degree of legitimacy and influence over the management of the global economy and financial system.” 18 Indeed, developing countries account for half the seats (with Russia and South Korea included); and its members account for nearly 90 percent of world GDP and two-thirds of world population (though these figures questionably include the whole of the EU via the EU seat). 19 The countries that especially love it are the “last ones in the door,” the smaller countries whose claims to sit at the top table are most contestable, like Australia and Canada.

The giants also like it. For example, both the United States and China recognize that embedding their often-tense bilateral relationship in a larger grouping can dampen the tensions. China also boosts the G20 as the first top-level global body to reflect its global role but not authoritative enough to press it to take on leadership responsibilities it does not wish to assume.

The G20 champions do not make a distinction between efficiency and legitimacy—indeed, the word legitimacy rarely passes their lips, and if pressed, they use it to mean no more than “representative” or “efficient.” They pirouette around questions about (1) the legitimacy of the process by which the twenty were selected, (2) the lack of explicit criteria for membership, (3) the principle of exclusive membership (with no rotation), and (4) the thinness of regional representation.

However, many states outside the G20 do question the G20’s legitimacy. 20 The Norwegian foreign minister even described it as “one of the greatest setbacks since World War II.” 21 The UN, as the embodiment of the principle of inclusive multilateralism, was a center of resistance to the upgrading of the G20 from finance ministers level to heads-of-government level, on grounds that the G20’s self-selecting, exclusive, nonrotating membership breaks a fundamental principle of liberalism—universality. Neither the secretary-general nor the president of the General Assembly were invited to join the G20 leaders in an ex officio capacity (as were the managing director of the IMF and the president of the World Bank). The UN General Assembly convened the UN Conference on the Global Economic Crisis in June 2009 as a rival forum, with lukewarm response from G7 members and outright hostility from the UN Secretary-General’s office, deferring to G7 wishes.

The G20’s critics emphasize that its composition meets no criteria that would justify the inclusion of Argentina (population 40 million) rather than, say, Colombia (46 million), or South Africa (50 million) rather than, say, Nigeria (158 million). They become incensed when they hear the G20 leaders announce from on high, as at the second summit, “We will reform [the international financial institutions’] mandates, scope, and governance.” By what authority do the G20 leaders supersede the legitimate governing bodies of these organizations (the Development Committee for the World Bank and the International Monetary and Financial Committee for the IMF)? they ask. By what right do the G20 leaders call for a change of voting shares in the World Bank in favor of developing countries by at least 3 percentage points and in the IMF by at least 5 percentage points? When they hear the managing director of the IMF claiming at IMF board meetings that he is the legitimate representative of the non-G20 DTCs at the G20—implying that despite appearances to the contrary, the non-G20 DTCs are well represented at the top table—they are incredulous. Indian representatives sometimes counter in private that since India is the poorest of the G20 states, it has the right to, and does, represent the poorest countries. 22

Since the first two summits, in November 2008 and April 2009, regional bodies have pressed for inclusion. The African Union has said that Africa is woefully underrepresented (only by South Africa), and that a seat for the union would help. The Association of Southeast Asian Nations (ASEAN) has said the same. The G20 has responded by inviting ASEAN to nominate a country to represent it and the African Union to send representatives from two of its member states. So at the Seoul summit, November 2011, twenty countries represented themselves alone (the nineteen plus Spain, which has managed to wangle the status of “permanent guest”); four countries represented collectivities (two from the African Union; one from ASEAN; Singapore represented the Global Governance Group, which covers 28 small states); and the EU occupied one seat. 23 In effect, the G20 has become the G20 + 5.

However, the complaints have not gone away. The Nordics, for one, argue that since the Nordic-Baltic economies are the ninth biggest economic bloc in the world, they should be at the top table. But they and other critics can equally turn rejectionist and say that as long as the G20 permanently excludes 168 countries of the World Bank and IMF and 172 countries of the UN, it cannot be deemed a legitimate global body, period.

Effectiveness

The G20 was created to promote multilateral cooperation, but in the context of a system still largely dominated by the United States—the system Philip Stephens referred to when he said, “Membership of the west once meant doing whatever Washington said.” As multipolarity has increased since 1999, how have Southern states participated in the G20? In the mode of hegemonic incorporation (where the DTCs accept the G7 consensus), multilateral cooperation (where the DTCs do not simply rubber-stamp the G7 consensus; they undertake initiatives, and all members are prepared to find compromises on matters they did not initially agree about), or Westphalian assertion?

For most of its history, the finance ministers’ G20 has functioned toward the hegemonic incorporation end of the spectrum. All the way through, it has been standard practice for the chair country to send proposals for the meeting and the communiqué (drafted before the meeting starts) to the U.S. government first to get its views. 24 A report from the G20 finance ministers’ meeting in South Korea in October 2010, chaired by the Koreans, said that the ministers had had “intense talks—built largely around an agenda the United States brought to the meeting.” 25

Not that the United States has dominated in an overt way; its representatives have often played the strong, silent types, content to let U.S. muscle do the talking. The key animators and organizers have been the Canadians and the Australians (“last in the door” of the Anglo states). They repeatedly got the G20 working groups and ministers’ meetings to endorse the formula that “globalization works,” where globalization policies amount to privatization, liberalization, and stabilization, plus social safety nets. The World Bank provided support for this agenda, sending reliable staff to address G20 technical meetings. 26

At these meetings, the representatives from the DTCs tended to sit passively, contributing little to the agenda, the debate, or the communiqué. They felt at a disadvantage because the language of the G20 is English, and because they did not have a good feel for the informal ways of G7 diplomacy that the G7 representatives used to run the G20. They had won an important symbolic gain just by being present, “equal” alongside the United States, Europe, and Japan.

There is not much sign that the finance ministers’ G20 has been able to coordinate governments into mutually desired outcomes—and it certainly cannot induce them to undertake unwanted but necessary policies. 27 One reason is that the G7 has by no means been eclipsed, and indeed, from the beginning, the G7 saw the G20 as a way to leverage its influence via the larger body. The Canadians are especially keen on keeping the G7 going, because in it, they have more influence than in the G20. So instead of the G20 replacing the G7 (or G8 at leaders level), it has become an additional forum, diluting its claim to be the top table. 28

For all its ringing declarations about global leadership (“We designated the G20 to be the premier forum for our international economic co-operation”), the leaders’ G20 has no means of enforcing its agreements. It decided at the first summit in 2008, in Washington, to eschew trade protection, but some of its members broke the promise as soon as they walked out the door. It decided at the same meeting to boost government spending, but almost all the programs announced after the summit—as evidence of G20 cooperation—had already been decided on before the summit. Similarly, it promised to treble the resources of the IMF up to $1 trillion, making an arresting headline; but as Ngaire Woods reports, “the new financing for the IMF is mostly credit lines,” which allow it to borrow more when it thinks its present resources are insufficient to meet members’ demands, and borrow mostly from the G7 states, which ties the organization back into the G7 orbit. 29

However, in recent years, the United States and its allies (including the United Kingdom, Canada, and Australia) have by no means gotten their own way in terms of the internal discussions and agreed-upon conclusions. Developing country members have not had much role in setting the agenda but have become more active in reacting, sometimes fighting back. They can and do apply an informal veto. Examples include China on the subjects of “global imbalances” and “exchange rates”; and many developing country members were active in shaping what the G20 said and did not say in the run-up to the Copenhagen climate summit. We could interpret this DTC participation as moving from hegemonic incorporation toward Westphalian assertion.

This is what the top U.S. official for the G20 process was referring to in January 2010 remarks to EU officials (made available on WikiLeaks):

It is remarkable how closely coordinated the BASIC group of countries . . . have

become in international fora, taking turns to impede US/EU initiatives and playing the

US and EU off against each other. BASIC countries have widely different interests . .

. but have subordinated these to their common short term goals to block some western

initiatives.

30

At the Seoul leaders’ summit in November 2010, the wheels fell off. The “fellowship of the lifeboat” that prevailed in the acute phase of the global crisis vanished. The Financial Times headlined its comment, “The G20 show how not to run the world.” It described the “action plan” as “déjà vu,” “similar to past failures.” The G20, it said, “is doing little to assuage fears of an impending conflict over currencies and trade, and its vague communiqués can do little to disguise the bitter divisions.” 31

The World Bank

The World Bank remains the world’s premier development agency, especially as generator and sustainer of beliefs about the best policies and institutions for development. It has been a prime beneficiary of the global economic crisis, to the point where its lending commitments in fiscal year 2009 were three times higher than two years before. The middle-income countries—the ones best placed to walk away from the Bank and borrow from private markets under their own names or from regional development banks—have come out in strong support. The days of the early 1990s, when a powerful NGO movement with much influence in the U.S. Congress was campaigning to close down the World Bank and IMF under the slogan “50 years is enough,” and when a powerful right-wing American constituency that disliked multilateralism and foreign aid was pushing for much the same, are long gone. 32

The Package of Reforms

The spring meetings of the Bretton Woods organizations in late April 2010 may be looked back on as a seminal event in the organizations’ history. The governors of both— ministers from the member countries 33 —agreed on the outlines and some specifics of reforms hailed as equipping them for the new multipolar era (recall Zoellick’s speech in the run-up to the spring meetings).

The World Bank reform package includes five main components:

Voice: Increase in shares and votes of Part II (borrower) countries.

Capital increase: To support future lending.

Strategy: Laid out in a paper called “New World, New World Bank Group: I Post-Crisis Directions.”

Internal organization: For example, further decentralization out of Washington, D.C.

Internal governance: For example, organization of the board, relations between board and president.

Causes of the Reforms

The impetus for voice reform was building for several years before the global economic crisis, focused on the fact that the Part I (high-income, nonborrowing) countries had well over half of the voting shares. Moreover, the United States on its own, and the western Europeans acting as one, both wielded a veto on important (“supermajority”) decisions. The Monterrey Consensus in 2002 stated that the Part IIs should have more voice in international organizations, in line with their rising weight in the world economy. But the Part I countries dragged their feet. Voice reform was not their priority.

The formation of the leaders’ G20 in 2008, at the initiative of President Bush, gave new impetus. Now the top political leaders were dealing face-to-face, and the developing country leaders put the voice demand firmly on the table. They readily agreed to put forth a demand for a bigger share of votes, while disagreeing on much else. Moreover, the U.S. government came to see support for the change as a way to hit two birds with one stone—to cut Europe’s (alleged) overrepresentation and to strengthen its alliances with the BRICs.

At this time of crisis, the World Bank and IMF both faced soaring demand for loans. As the Bank’s lending commitments rose, it became clear—at least to some senior World Bank officials and some member states—that it needed a big general capital increase (GCI) just to avoid having to cut back its lending sharply in future years in order to stay within its prudential limit, let alone to expand its future lending.

But all the G7 states opposed a GCI, especially the United States, the United Kingdom, and France. Right up to the summer of 2009, President Zoellick insisted that the Bank could boost its lending by making “efficiency savings.” Only at the annual meetings in Istanbul in September did he finally lend support to a GCI. Why the G7 reluctance to support a GCI?

The G7 governors, executive directors, and many other Part I states said they would have a hard time persuading their parliaments—especially the U.S. Congress—to increase funding for the World Bank at a time of fiscal stringency at home (even though the amounts of paid-in capital are tiny, only about 5 percent of pledged or “callable” capital). 34 The western Europeans were doubly doubtful, because they knew that they were going to lose voting shares in the voice reform, so they would be paying in more capital at the same time as they lost votes. 35

During 2009, the World Bank management (with grudging permission of the president) worked intensively to demonstrate to doubtful Part I executive directors that if the World Bank did not get a big general capital increase, it would have to cut back its lending by 2014 to far below the rate before the global economic crisis. This evidence eventually persuaded many Part I executive directors that the World Bank had to have a GCI.

So the Part I governments began to say, We’ll consider a GCI, but first you must make big reforms in internal organization. As U.S. Treasury Secretary Geithner said, “Donor countries are facing severe financial constraints at home; [so] we will be seeking critical institutional reforms in any consideration of additional resources.” 36

As the board and the management worked on the reform package, the Part I governments reluctantly accepted that the GCI had to come now. 37

So the main driver of the reform package at the World Bank was demands by external shareholders, led by the United States, for reforms that looked bold and could be sold to legislators as quid pro quo for more capital at a time of fiscal stringency. This is the short answer to why the governors approved the reform package at the spring meetings in Washington, D.C., in April 2010 and why the package was boosted as a “New World Bank for a New Multipolar World.”

What Do the Reforms Amount To?

When the reality becomes visible through the mist of euphoria, the reforms look modest. Most of the Part II executive directors feel disappointed but not surprised, with the important exception of the Chinese executive director, who takes the view that they are a positive first step—in the spirit of crossing the river by feeling for the stones one at a time.

1. General capital increase

The agreed increase in the capital base is actually very small, probably only big enough to allow the Bank to sustain beyond 2014 the same level of lending in real terms as in the early 1980s.

2. Voice reform

The G20 leaders’ meeting in September 2009 declared that the World Bank should raise the share of Part II votes by “at least 3 percentage points,” and this statement, interpreted as “3.13 percentage points,” constituted the Development Committee’s and executive directors’ marching orders. The shift would raise the Part IIs’ share from about 44 percent of the votes to about 47 percent.

This fell well short of what Part IIs were demanding: parity, or 50 percent. How were the 3 percentage points arrived at? By the ancient haggling principle of “split the difference.” Three percentage points on the existing 44 percent brought the Part II share up to half of the Part IIs’ demand. 38

Once the G20 had laid down the target, the board spent months of nearly 24/7 negotiations to allocate the change in shares among member countries. As one observer said, the process became a search for “compromises at the third decimal point.” 39

The negotiations were guided by the general principle that voting power should be proportional to economic weight in the world economy, translated into a formula. But the formula was highly contested—and called a “framework” rather than a “formula,” on grounds that “formula” sounded like something permanent, which would set the starting point for the next round of negotiations. The United States said it should be based largely on “weight in world economy as measured by GDP at market exchange rates”; and not coincidentally, the United States is underrepresented in the World Bank by this criterion. Europeans said that the formula should also include “contributions to the poverty-reduction mandate of the World Bank, as measured by IDA (International Development Association) contributions”; and not coincidentally, Europe’s are much bigger than those of the United States. Many Part II countries argued that the only criterion should be a country’s share of world GDP in purchasing power parity terms—which would substantially raise the share of the Part IIs. Eventually a compromise was reached: the GDP metric should be weighted 60 percent at market exchange rates and 40 percent at purchasing power parity exchange rates, reflecting the continuing tilt toward the Part I countries. 40

But beyond the general principle that votes should be related to GDP, what really happened was, in the words of a close participant, “a messy and opaque process of reverse engineering of political deals, which caused a lot of bad blood.” 41 One of the Bank’s main officials on the voice reform resigned from the Bank because she could not stand to go on spoiling her life in such bizarre and bitter wrangling.

In the end (including the entire change in voting shares since 2008), 42

The headline jump in the Part II share from 44 percent to 47 percent was misleading. More than a dozen countries which by the Bank’s criteria should have been counted as Part I (“high income”) were counted as Part II. They include South Korea, Singapore, Saudi Arabia, Kuwait, Poland, and Hungary. If added to the “high-income” countries, the latter end up with a bit more than 60 percent of the vote (60.95 percent). 43

Within the Part I countries, the western Europeans combined lost the most, Japan lost the most of any single country, and the United States effectively stayed the same.

Being described as a “Part II gain” concealed that most of the shift went to a small number of middle-income countries, notably, China, Brazil, and Turkey. Of the BRICs, Russia did not gain and India gained only a little.

The middle-income countries now have about a third of the votes.

None of the low-income countries lost, but few gained, and then insignificantly. 44

The low-income countries have 4.46 percent of the votes.

China won respect by giving up about half of its entitled increase in shares (by share of world GDP) so as to allow this half to go to other Part IIs. (If China had not done so, it would have received the whole of the 3 percentage-point shift.)

China plus India increased their combined share from 5.56 percent to 7.33 percent, compared to Belgium plus the Netherlands’ fall from 4.01 percent to 3.49 percent. This gives China plus India 110 percent more share than Belgium plus the Netherlands. But if shares were proportional to GDP shares (the Bank claims this to be the guiding principle), China plus India should have more than 600 percent of the share of Belgium plus the Netherlands. Other middle-income countries are similarly underrepresented and high-income countries overrepresented.

Under the formula relating the capital increase to the change in shares, Russia and Saudi Arabia were destined to lose shares. Russian Prime Minister Vladimir Putin and his Saudi counterpart informed the president in imperative tones that they would block the whole voice reform if they lost shares. (The Articles of Agreement say that a change in voting shares must be agreed upon unanimously to be valid.) So the architects of the voice reform changed the formula in such a way as to enable these states to gain back what they would have lost—by pledging an additional amount for the next International Development Association (IDA) subscription (IDA16), and weighing these future contributions much more heavily than countries’ past contributions (to the anger of the IDA-generous Nordics). Several other idiosyncratic arrangements were bolted on to accommodate the determined defense of existing voting shares by the top leaders of certain states, using the threat of veto. 45

The voting shares are due to be revised in 2015, not before. 46

3. Strategy

The focus on voice reforms at the third decimal point meant that other issues, especially the Bank’s strategy for the new multipolar age, were eclipsed. This suited the Part I countries well.

The strategy document is short, vague, and platitudinous, containing little to disagree with. It presents no new vision for a larger World Bank. Strip away the fluff and it reduces to something close to “business as usual”—to be done in a more decentralized way than before. However, the fact of its existence satisfied the demand of the Part I governments that the Bank show them what it was going to do with the additional resources made possible by a GCI.

The many drafts of the strategy paper, up to the last two (a couple of weeks before the April 2010 meetings), began with the following sentence:

The vision of the World Bank Group is to support an inclusive and

sustainable globalization—to overcome poverty, enhance growth with care

for the environment, and create individual opportunity and hope. (emphasis

added).

This reflected Zoellick’s wish to pavilion “globalization” with praise. Many middle-income countries, whose representatives question the Bank’s long established focus on poverty reduction, have supported him. They say that a World Bank devoted to poverty reduction will go out of business, because the middle-income countries want to borrow from it not mainly for poverty-targeted projects but for general development projects, especially infrastructure.

The Nordics protested again and again at the draft strategy’s prioritizing of globalization over poverty reduction (after all, they were arguing against a cut in their voting share on grounds of their generous support to the Bank’s poverty-reduction mission). Finally, at the last minute, their efforts paid off. The strategy team revised the headline statement to read,

The vision of the World Bank Group is to overcome poverty—by

supporting an inclusive and sustainable globalization, enhancing growth with care

for the environment, and creating individual opportunity and hope. (emphasis

added).

The headline reaffirms the vision statement that has been displayed in the foyer of the main building of the World Bank since the days of James Wolfensohn’s presidency in the mid-1990s. But in the intervening years, several of the letters have lost their moorings and now droop at decrepit angles.

The IMF

Following G20 instruction, the IMF’s governing body agreed at the annual meetings of October 2009 on “a shift in quota share to dynamic emerging market and developing countries of at least 5 per cent from over-represented to under-represented countries.” This ungrammatical sentence was a fudge, to conceal disagreement on whether the shift should be to dynamic emerging market or to DTCs as a bloc or to underrepresented countries (in the latter case, Spain, Ireland, and Luxembourg would also gain).

By November 2010, the board agreed on a 6 percent shift—boasting that it had exceeded the G20 target. Hidden in the small print was the fact that the shift was to dynamic emerging economies only. The changes will make China the third largest shareholder after the United States and Japan and vault India, Russia, and Brazil into the top ten. As at the World Bank, the loss to “advanced countries” is very small: from 57.9 percent to 55.3 percent, or 2.6 percent. But as also at the World Bank, South Korea and Singapore were counted as dynamic emerging markets, though the IMF itself normally classifies them as “advanced.” With them in the advanced category, the advanced states lose only 2 percent. Meanwhile, Africa as a group loses voting share from 5.9 percent to 5.6 percent. 47

These shifts form part of a larger package, which include changes in the composition of the seats on the board. Here the Americans made another attempt to curb Europe’s alleged overrepresentation by forcing the “advanced European” countries to give up two of their eight seats on the Fund’s twenty-four-seat board. 48 They forced the issue by announcing with little notice before the October 2010 annual meetings that they would not approve the continuation of twenty-four seats on the executive board. The Fund’s Articles of Agreement stipulate a twenty-seat board, and the enlargement to twenty-four has to be approved by the board every two years. Thanks to their veto, the Americans can block it. (Key Fund decisions require approval by 85 percent of the voting shares, and the United States has 17 percent.) Having previously automatically approved, their sudden refusal threw the board and the Europeans into panic. Who would lose their seats?

To cut a long story short, Managing Director Strauss-Kahn, perhaps with an eye to a top position in European politics, launched a diplomatic drive to limit the damage to Europe. He and the Europeans largely succeeded. By the time of the Seoul G20 meeting in November 2010, the Americans again agreed to approve the twenty-four-seat board, while the advanced Europeans agreed to give up some positional authority by going from eight to six seats. This is not exactly a revolution.

The advanced Europeans are just starting (early 2011) to negotiate among themselves about how the loss of seats will be distributed among themselves. Seats can be sliced up, such that if Belgium, which has represented a constituency of countries including Turkey, were to share the executive director position with Turkey in rotation, this would count as advanced Europe’s giving up half a seat. If Spain were to exit from the constituency where it now shares a seat with Mexico and Venezuela, this would count as advanced Europe giving up one-third of a seat. Once it is clearer how the loss will be distributed, negotiations will begin over how the two-seat gain will be distributed. It is quite possible that western Europe loss will go mostly to eastern Europe, so that the transfer becomes one within Europe (plus Turkey). The outcome is unlikely to be clear before 2013.

Strauss-Kahn called the agreements “historic.” Certainly they are bigger than previous changes, but hardly major relative to the rise in multipolarity. Nevertheless, tensions have been diffused, limited agreements reached, important issues kicked into the future. Europe has lost much less than looked likely in the summer of 2010; DTCs as a group have gained much less. Within the DTCs, China gained the most by far (it is now the IMF’s third biggest shareholder); Brazil and some “honorary BRICs,” like Turkey and Mexico, also gained substantially; and now DTCs have four of the top ten shareholding positions, having earlier had two. The United States, having forced the issue of seats and demonstrated its commitment to a general power shift from Europe to the South, can expect the winners to show gratitude. 49

Conclusions

We have entered a time of more turbulence in global governance than for many decades. The turbulence reflects (1) the increasing share of global economic activity outside the established Atlantic states plus Japan, (2) the associated growth of excess production capacity relative to effective demand, (3) the efforts of states to blame outsiders for their troubles and shift unemployment elsewhere by boosting exports as they contract domestic demand, and (4) the West’s preternatural fear of China. 50

This essay has discussed some of the institutional innovations made or proposed in response to the new international distribution of economic activity. It has illustrated how the tension between the newcomers and the old G7 is playing out—right down to the capillaries (third decimal point) of world politics. On the one hand, the advanced countries attempt to incorporate newcomers into their own beliefs and preferences for the global meta-agenda of economic policy (“globalization” in the sense of further market expansion plus social safety nets for the poorest, together with, post-2008, some tighter financial regulation). On the other hand, the newcomers demand more voice but without as yet much coordination of beliefs and preferences among themselves. (But recall that the BRIC executive directors at the World Bank and at the IMF have started to meet once or twice a month.)

The transition from the waning to the emerging global order is clearly proving tricky. In terms of the multipolar governance dilemma, economic multipolarity, particularly at a time of economic slump, is generating more demands for interstate cooperation; but the supply response in the form of political multilateralism lags far behind. The G20 and the Bretton Woods organizations continue to show more “hegemonic incorporation” and “Westphalian assertion” than “multilateral cooperation.”

The Americans and the Europeans are ambivalent about ceding some leadership to the DTCs, sometimes cooperating among themselves and sometimes falling out on what changes should and should not be made. At the World Bank, the Part I countries as a group dragged their feet on significantly increasing the Part II voting share, and on increasing the general capital base, and on opening the selection process for the heads of the World Bank and the IMF to global recruitment without nationality restrictions. And they cooperated to ensure that the real shift of votes to DTCs was much less than the headline.

The U.S. executive branch is fixated on a power play, first, to retain its veto in both organizations and, second, to retain the presidency of the World Bank. If it keeps these two things and does not have to pay in more capital, it is not too worried. The U.S. Congress is even more adamant about protecting U.S. dominance in both organizations, which it treats as arms of U.S. foreign policy. For example, the U.S. Senate demanded (March 2010) that the Obama administration maintain “United States voting shares and veto rights at the international financial institutions,” and preserve “U.S. leadership of the World Bank and senior level positions at the other international financial institutions.” 51 U.S. Westphalian pressure may well intensify in the wake of the November 2010 U.S. congressional elections, which returned a Republican majority in the House of Representatives. U.S. foreign policy may become more unilaterally assertive, self-righteous, and self-pitying than in the first two years of the Obama administration, because American conservatives unify around the belief in America’s unique virtue and its corollary that the rules for others do not necessarily apply to the United States. Hence, many conservatives are reluctant to adapt to the rise of new centers of power, and want to rely instead on “coalitions of the willing” or a “concert of democracies.”

At the IMF, the Europeans have seemingly snatched victory from the jaws of defeat as they pushed back against U.S.-led attempts to curb their overrepresentation. They have particularly focused on the U.S. veto, knowing that the Americans place high importance on retaining it and knowing that it is widely recognized as illegitimate. The Europeans therefore say that if Europe is to give up some authority to the DTCs, so, too, must the United States; above all, the United States must give up its veto. As the German executive director to the Fund said in late 2010,

It [the veto] is anachronistic at this point. For one country, no matter how big it is,

to have the right to dominate decisions in that unique way is not legitimate anymore.

If you talk about legitimacy, that’s the major flaw in the

organization.

52

Faced with the prospect of European-led challenges to their sacred veto, the Americans have softened their drive against the Europeans.

As for the DTCs, they wish to be at the top table, in global governance, but are wary of more global governance (which would curb their sovereignty) and wary of proposing initiatives that would put more responsibilities on their shoulders. This helps to explain the otherwise puzzling fact that at the World Bank, countries that should have been graduated to the Part I category according to the income-per-head criterion (like South Korea, Saudi Arabia, and Kuwait) resist. One reason, noted earlier, is that the Part I countries wish them to continue to be classified as Part II, so that the shift in votes to “true” DTCs is less than it seems. But they themselves also wish to continue in Part II because once graduated, they would be expected to (1) contribute more capital, (2) give up voting share, and (3) share the burden of global responsibilities.

Meanwhile, China, the world’s biggest creditor state, is becoming increasingly assertive, even swaggering, as the ruling Communist Party tries to show that it has made China a respected world power, not to be pushed around by anybody. It is drawing sharper distinctions between its own and others’ national interests, as seen in its responses to rising tensions on the Korean peninsula and in the South China Sea.

To my knowledge, there is no body of theory that might shape our expectations about the gap—large or small, increasing or diminishing—between economic globalization and multipolarity, on the one hand, and political globalization and multilateralism, on the other. It remains an open question whether the gap will reduce or widen over time. The optimistic answer is that surging global problems plus repeated interaction within the expanded body of leading states, in many international organizations, will generate convergence in both solutions and enmeshed beliefs about causes (as repeated interaction among the Permanent 5 of the Security Council has helped to maintain the peace between them—with occasional exceptions—for more than 60 years, an epochal achievement).

The more pessimistic answer is that while bits and pieces of agreements (loosely coupled regulatory systems, or “regime complexes”) may be forged by overcoming coordination problems of the prisoner’s dilemma kind (where the parties agree on the nature of the problem), bigger advances in the form of strong, integrated regulatory systems (“comprehensive regimes”) are blocked by differences in enmeshed beliefs about the nature of the problem, now combined with deep tensions resulting from the economic slump in the Atlantic economies. Making enmeshed beliefs converge, especially when economic tensions run high, is more intractable than solving coordination problems. 53

Think, for example, of the profound differences between the Chinese and U.S. governments in their diagnosis of the causes of China–U.S. payment imbalances, which go far beyond differences of the prisoner’s dilemma type. 54 China says the root of the problem is loose U.S. monetary policy and excessive borrowing since the early 2000s; the United States fingers China’s pegging of the yuan to the dollar, which results in yuan undervaluation and unfair advantage for China’s exports. On the basis of these different diagnoses, the two governments are now adopting recovery policies that undermine each other, at cost to the rest of the world as well as themselves. The United States continues to rely on cheap money policies, whereas China continues to keep the yuan loosely pegged to the U.S. dollar and continues to emphasize export growth. Cheap U.S. money goes in search of strong returns, which contributes to increases in commodity prices (agriculture, metals, oil) and in inflows of capital to China and other developing country markets. These flows stoke the imbalances even further.

Clearly the repeated interaction between China and the United States in multilateral forums like the G20 and the Bretton Woods organizations has not been sufficient to generate convergence in their understanding of the root causes of global imbalances or complementarity in their policy responses. Yet, think how much worse things would be in the absence of such forums, as in a pre–World War II type of order. In such a world, the imbalances would be reduced through bilateral assertion, elephant against elephant, as the United States creates dollars without limit and China responds by creating yuan without limit with which to buy the dollars and prevent yuan appreciation. Innocent bystander states suffer, and the world moves from currency wars to even worse trade protection wars.

Whether this outcome now can be avoided will be a test of the diffuse value of global forums. Hopefully, they will soften bilateral tensions between the giants by embedding them in cross-cutting ties, which expose them to pressure from those sitting alongside whose economies suffer because of their actions. And hopefully they help the rising states to learn about open debate and superpower diplomacy. In this optimistic spirit let us consider how their role and governance might be improved.

Reform of the G20

The G20, as we saw, is beginning to intervene directly into the Bretton Woods organizations, by setting reform directions and deciding on shifts in voting shares. This may be temporary: once the Atlantic recession lifts, the non-G20 may resist its interventions sufficiently for it to find something else to worry about. On the other hand, an increasing proportion of top appointments in both organizations are going to G20 states. Insiders refer to “the G20ization of the World Bank.” This may be an indirect channel for making these organizations more responsive to G20 beliefs, preferences, and strategies.

However, the G20 is not a viable long-term solution to global coordination of economic and financial policies, particularly because of its legitimacy problem in the eyes of many of the 160-plus non-G20 states. Whether at the level of finance ministers or of heads of government, the G20 has yet to demonstrate that it can graduate from crisis committee to steering committee.

We can think of two new models. The first uses explicit criteria to guide the selection of members of a new Global Economic Council (GEC), of which at least four are relevant. One is weight in the world economy, measured by GDP, an indicator of effectiveness in turning decisions into action. A second is representation, which means that the group must cover a high proportion of the world’s population. A third is regional representation, to ensure that no region is left out. A fourth is intimacy: the grouping should be kept small enough to allow personal trust to develop among the members. 55

With reference to the first two criteria, sixteen countries meet the condition of 2 percent or more of either world GDP or world population (using 2008 figures and GDP measured at purchasing power parities). Applying the 2 percent rule would exclude Argentina, Australia, Mexico, Saudi Arabia, South Africa, and Turkey of the current G20, and include Bangladesh, Nigeria, Pakistan, and Spain. However, the result is a bloc of rich countries and a bloc of poor, aid-dependent countries, and its business may be taken over by the latter’s attempts to wrestle more aid from the former. For this reason, the 2 percent of population criterion may have to be qualified by criteria relating to economic dynamism or international trade, or raised to 3 percent.

The third criterion could be met by each region selecting one or more states to represent it in the GEC, perhaps in a regional election, or else by each regional body, like the African Union, sending a representative. Dividing the world into five regions would make another five seats. The UN secretary-general and the president of the General Assembly would further enhance its legitimacy. They would bring the total to twenty-three seats (using the 2 percent criterion), consistent with the fourth criterion of lowish transaction costs.

The second—and by criteria of representational legitimacy, much better—model is a modified version of the existing Bretton Woods governance arrangement. A small number (roughly six) of the biggest states by GDP and population would represent themselves alone. All the rest (roughly 180) would be assembled in about twenty constituencies of at least six states each. Each constituency would regularly elect a state to represent it, with votes based on each country’s share of the constituency’s GDP and population. In this model, each constituency state on the GEC would represent roughly eight other states, in contrast with the first model, where each regional representative would represent roughly thirty-six other states.

Either of these models would allow a better balance between established and rising powers and a more robust way of changing the governing balance as the economic balance changes. The G7 states themselves are no more likely to push in this direction than turkeys are to vote for Christmas, but this should not stop others.

Reform of the World Bank

The World Bank’s future is assured because the BRICs and other middle-income countries have come out strongly in support, though best placed to borrow from other sources. Many are now more credit worthy than some Part I countries, such as the southern European Mediterranean states. However, some Part I governments—notably, the U.S. government—are holding back its growth, as seen in their reluctance to support a GCI. These governments have no strong interest in allowing the bank to grow much bigger and compete with their private financiers and consulting firms. 56

A big fight is likely within the next few years over the president of the World Bank and the managing director of IMF, especially over whether the Americans can keep their monopoly on the bank presidency and the Europeans their monopoly of the Fund. The reform packages for both organizations call for open selection of the heads, unrestricted by nationality. But many commentators immediately shrink back: what if Lula da Silva, former president of Brazil, decides that he wishes to be president of the World Bank? How does the organization hard-wire in a merit test? Worse, what happens if the Chinese government wishes to appoint a senior official or politician as managing director of the IMF? What would happen to the organization’s transparency and accountability? 57 In the case of the bank, should the positions of CEO and chair of the board, which have always been held by the president, be separated, so that a Lula da Silva could be chair with an effective manager as CEO?

The Europeans say that they and the Americans agree to give up the gentleman’s agreement—but that it is up to the United States to make the first move by giving up the bank. They worry about a U.S. strategy whereby it agrees to open up both jobs, then mobilizes an emerging market candidate as managing director of the IMF and deploys its veto to ensure his or her election, in return for which grateful emerging market states support an American as the next president of the World Bank—through “open” selection, of course. 58

The allocation of votes—due to be revisited in 2015—is another looming fight. The idea of aiming for “parity” between Part I and Part II countries clearly does not make sense, not least because as more countries graduate from Part II, ever fewer countries would gain ever more voting rights—or else ways would be found to halt the graduation. As also for G20 membership, the Bank needs a shareholding formula based on transparent and legitimate principles, consistent with preserving the willingness of governments to fund and guarantee the organization and hence protect its AAA rating.

Another sensitive issue concerns the World Bank’s role in servicing the emerging development agenda of the G20. Some non-G20 states strenuously object to the World Bank making itself into the “secretariat” for a self-appointed, nonrepresentative body that includes no low-income countries (India now officially being classed as a middle-income country) and no premier aid donors except the United Kingdom. Any World Bank help to the G20 only ratifies the G20’s claims to be the global steering committee, they say. (In this spirit, they take a microscope to the bank’s budget in order to discover where the costs of servicing the G20 are being concealed.) Other voices take a more pragmatic view that since the G20 exists and wants to talk about development, the World Bank had better lead the way in telling it what to say.

But in the larger scheme of things, these are minor issues. What would be a bold vision for a new World Bank (bearing in mind Helmut Schmidt’s warning that people who have visions should see a doctor)? It might start from the point that there is an obvious unmet global need for a financing mechanism to provide below-commercial-rate long-term loans on a much bigger scale than at present: first, for projects that provide “global public goods,” where the investments are made in specific countries but the benefits spill over to many other countries (global warming investments are the obvious case in point); second, for other kinds of investments where the benefits are mostly captured within the country but where costs are high and benefits accrue over a much longer period, such as some kinds of infrastructural and industrial loans.

The sum of both demands means that developing countries laying down production and distribution capacity have a very high demand for many kinds of commodities, and a very high demand for food as incomes rise. They need below-market loans which—to be safe—mature in fifteen to twenty years. Until developing countries build a diversified production base and its associated infrastructure, they should be net importers of capital—provided that the capital imports are used to increase productive capacity rather than increase consumption and provided that the loans are long term. 59 At present, with only a small supply of long-term loans, developing countries have been borrowing abroad on much shorter terms and at commercial rates—setting themselves up for whiplash reversal of capital flows and ensuing financial crises (as in the East Asian/Russian/Brazil crisis of 1997–98) and forcing them excessively into export production in order to repay the short-term loans. 60 In this way, they help to produce global imbalances and associated financial fragility. This is the core argument for enabling one or more World Bank–like organizations to expand long-term lending to middle-income countries by ten times or more its present level.

A big increase in such loans from the World Bank means that the International Bank for Reconstruction and Development (IBRD) and IDA would probably have to be governed separately. The IBRD is the World Bank’s lending arm for middle-income countries, financed by sale of bonds plus repayments of previous IBRD loans. IDA is the lending arm for very-low-income countries, financed by grants plus repayments of previous IDA loans. The two arms are now governed by the same set of executive directors and share the same staff.

The IBRD might be thought of as a credit union or cooperative bank, as distinct from a shareholder bank. In a cooperative bank, shares and votes are allocated according to some combination of (1) one member, one vote; (2) financial contributions; and (3) borrowings. Since the Part Is now contribute very little paid-in capital and the bulk of the IBRD revenue comes from sale of IBRD bonds and borrowers’ repayments, the switch to the cooperative bank model would imply a big shift of votes away from the Part Is to the middle-income countries, which would raise their shareholding to much more than parity.

The Part I countries say they provide the guarantees on IBRD bonds, and hence enable the IBRD to raise revenue at a cheap rate. But now that many Part II governments have a high credit rating, Part II governments could equally guarantee IBRD bonds. And some of those with large foreign exchange reserves would be very happy to increase their capital subscriptions to the IBRD instead of using their reserves to finance the United States’ external deficits and overseas adventures.

The IBRD would then be run more by the middle-income countries, and could lend ten and more times its present rate to meet the surging demand for infrastructure loans, heavy and chemical industry loans, global warming loans, and the like (based on a dynamic-stages model of economic development distinct from the static comparative advantage and poverty-focused model that has dominated World Bank thinking for the past three decades). 61 IDA might then be governed separately by a board that continued to be dominated by Part Is as long as they gave most of the grants. Needless to say, all Part Is, and also (at least publicly) most Part IIs, completely reject this vision. 62

In the next decade or so, we are likely to see repeated stalemates in global multilateral forums. Quests for global, top-down, everyone-in treaties may not be abandoned, but more progress is likely on more fragmentary regimes, composed of narrow agreements on specific issues, and on diffusion of policy norms for shifting market incentives in globally sustainable directions (such as a tax on carbon emissions coupled with tax credits for energy-efficient investments by households and firms, or prizes for carbon-saving energy innovations.)

Also, we can expect states to devote more effort to constructing regional economic governance regimes. Already several initiatives are underway in regions of the global South. The early Chiang Mai Initiative has more recently been joined by the South Summit (at heads-of-government level, held every five years since the first meeting in Havana in 2000), the Bank of the South (due to start lending in 2011), IBSA (annual meetings of the heads of government of India, Brazil, and South Africa), and UNASUR (ministerial meetings among Latin American countries to coordinate on matters of finance, social policy, defense, and more). Brazil is taking a leading role in promoting South-South coordination; China is bringing African countries into common dialogues; but India is more ambivalent, being less willing than Brazil and China to court U.S. disapproval.

The growth of fragmentary global and regional regimes will—hopefully—induce efforts in global forums to make the rules more consistent with each other (on analogy with “middleware,” a type of software that enables different systems within an organization to communicate without the need for a single unified system). Much depends on what happens to China’s foreign policy as the economy grows and closes the never-before-seen gap between its high ranking in terms of aggregate size (second largest GDP in the world) and low ranking in terms of average income (about one hundredth when measured at gross national income per head using the World Bank’s Atlas method of adjusting market exchange rates) and as the polity slowly becomes more democratic. As these trends mature, China is likely—hopefully—to cease playing the double game of a superpower in some contexts and an impoverished developing country in others, and to assume more international responsibilities. And the West is likely to cease viewing China’s international behavior through the prism of skepticism and distrust. Eventually we can expect global institutional innovations to come from the South, too.

Footnotes

Acknowledgements

Thanks to Jakob Vestergaard of the Danish Institute of International Studies, who shared in the interviews at the World Bank and the International Monetary Fund in 2010 and contributed to the development of the argument made here.

The author declared no conflict of interest with respect to the authorship and/or publication of this article.

The author received no financial support for the research and/or authorship of this article.