Abstract

How does the receipt of remittances shape recipients’ attitudes towards taxation? We argue that remittances are likely to reduce support for the fiscal contract of taxes in exchange for public services because recipients rely less on the national economy and the state for their well-being. Remittance recipients can use the money sent by friends or family overseas to obtain public services in the private market instead of, or in addition to, tax-funded welfare services. In doing so, remittance recipients become detached from the national political community and develop a transactional relationship with the state whereby they pay licence fees, taxes and bribes to protect investment goods procured with remittances, making them less willing to support general taxation and more likely to approve of tax evasion and avoidance. We find strong support for our theory in analysis of survey data from Africa and Latin America. Our article contributes to knowledge of the micro-foundations of the fiscal contract and the political-economic effects of emigration and remittances on migrants’ homelands.

Introduction

Limited ability to collect taxation is a serious problem for governments in many developing countries. It undermines fiscal capacity and therefore the ability of governments to provide high-quality public goods and services, such as infrastructure, healthcare and education (Brautigam et al., 2008). Poor or non-existent public services can lead citizens to emigrate and send remittances back to their families and communities (Stark, 1991, 2009; Stark and Bloom, 1985), thereby providing a cross-national social safety net to compensate for government failure (Germano, 2018). We can therefore view emigration and remittances as responses to the failure to build states underpinned by a robust fiscal contact of taxes in exchange for good-quality public services. In this article, we argue that remittances can further hinder the development of such a fiscal contract by making those who receive remittances less likely to support general taxation and to view tax evasion and avoidance more favourably.

Remittances can provide a short-term boost to tax revenue, but this comes at the price of the long-term development of a robust fiscal contract. While emigration reduces the supply of labour and thus the potential pool of workers who might pay income taxes, this effect is outweighed by the boost to the tax base for indirect taxes driven by increased consumption by remittance recipients (Astrayan et al., 2017; Ebeke, 2014). Tax collection is influenced not only by the capacity of the state to collect revenue from citizens, but also by the citizen’s attitudes towards the state and taxation (Ortega et al., 2016; Torgler, 2005). Building stronger states in which governments provide high-quality public services funded by a robust system of taxation requires the development of a fiscal contract in which citizens generally accept the need to pay taxes because they see the benefits to themselves and their communities (Levi, 1988). Building such fiscal contracts is a long-term process. Our contention in this article is that, while remittances might cause short-term increases in tax revenue, they undermine the development of fiscal contracts and can thus have a negative long-term effect on tax revenues in developing countries.

The key contribution of this article is to examine the micro-level relationship between remittances and tax attitudes and behaviours. We argue that receiving remittances makes individuals less supportive of paying taxes to fund the state. Individuals agree to pay taxes according to the quantity and quality of goods and public services they receive. Those who receive remittances, however, rely less on the national economy and the state for their well-being and can use the money sent by friends or family overseas to obtain public services in the private market instead of or in addition to tax-funded public services. Remittance recipients have less need for public services and therefore see less benefit from buying into the fiscal contract. Furthermore, when recipients do pay for services from the government, it is often for the specific purpose of registering or protecting investment goods purchased with remittances. The payment of licence fees, property taxes and bribes promotes a transactional relationship between remittance recipients and the state which further undermines recipients’ support for a general fiscal contract to benefit a national political community from which they feel disconnected.

To test our argument, we examine survey data from Africa (Afrobarometer) and Latin America (Latinobarometro). Our analysis shows that recipients are less supportive of taxation and more likely to approve of tax evasion and avoidance than non-recipients. These results are robust to controlling for a range of variables – including emigration plans, economic assessments, and trust in authorities – as well as to matching individuals on observable characteristics. Consistent with our theory, remittance recipients feel lower levels of identification with the national (political) community and are more likely to engage to pay licence fees, property taxes and bribes to the government to secure assets purchased with remittances. Our findings suggest that migrant remittances reduce individual support for the fiscal contract, which has important implications for the ability of labour-exporting states to raise revenue through taxation.

Our article makes a series of contributions to the existing literature. By showing how support for taxation is shaped by connections with migrants already living abroad, and particularly those who send remittances to their country of origin, our findings add a new perspective to work on the migration–development nexus (De Haas, 2010; Nyberg-Sørensen et al., 2002). Our research also builds on recent literature examining the micro-foundations of the fiscal contract in developing countries by considering the influence of emigration and remittances (Ali et al., 2014; Castañeda et al., 2020; Flores-Macías and Sánchez-Talanquer, 2020; Ortega et al., 2016). Finally, we contribute to work on the relationship between emigration, remittances and attitudes towards fiscal policy. Existing literature, focused on Latin America, has examined how migration and remittances affect support for redistribution (Acevedo, 2020), social spending (Doyle, 2015) and the role of the state in the economy (Meseguer et al., 2016). We build on this work by examining how remittances affect the development of the broader fiscal contract and examining data from Africa in addition to Latin America.

Fiscal Contracts and Remittances in Developing Countries

A fiscal contract is an agreement in which citizens pay taxes to the state in exchange for public services and goods based on contractarian views of the state in which citizens offer taxation and restricted liberty in exchange for protection and public goods (Rousseau, 1920). In more recent fiscal sociology, the fiscal contract promotes ‘quasi-voluntary compliance’ with taxation; it is much easier for states to offer public services in reciprocal exchange for taxation than to rely on coercion alone (Levi, 1988). The concept of the fiscal contract has been used to explain both the macro-level development of fiscal systems (Emmenegger et al., 2021; Timmons, 2005) and micro-level tax attitudes (Castañeda et al., 2020; McCulloch et al., 2021).

How might the receipt of migrant remittances influence individual views on the fiscal contract? We begin to address this question by looking at migrants’ motivation to emigrate and send money back home. According to the New Economics of Labour Migration (NELM), families in developing countries strategically send one or more members to live in a labour market abroad that is not correlated with the one at home (Stark, 1991, 2009; Stark and Bloom, 1985). Migrant households use remittances to overcome restricted access to labour, credit and insurance markets and to purchase welfare goods, such as healthcare and education on the private market rather than relying on poor or non-existent government provision (Acosta et al., 2008; Adida and Girod, 2011; Duquette-Rury, 2014). From this perspective, dissatisfaction with the provision and delivery of public services and goods drives people to migrate abroad and send remittances. Remittance-receiving households might also forego access to state-provided goods and services because they do not view the state as efficient in providing welfare as the private sector (because of poor quality or perceived wasteful spending), or out of political considerations (e.g. abuse of power or clientelism; Escribà-Folch et al., 2015; Pfutze, 2014). Irrespective of the circumstances, remittance recipients are less likely to rely on the state for welfare (Germano, 2018), and more likely to buy welfare goods (such as education or health) in the private market with the money they receive from overseas; Drabo and Ebeke, 2010).

The fiscal contract approach posits that citizens’ attitudes and willingness to pay taxes depend on government performance in the provision of public goods and services. Accordingly, individuals who do not feel that they benefit from government services are less willing to support taxation in general and less likely to consider tax non-compliance as a negative social issue. This idea has been corroborated by recent studies of tax attitudes in Africa and Latin America; individuals are more supportive of taxation if they perceive their government to be providing good-quality services (Ali et al., 2014; Ortega et al., 2016). Support for taxation is also increased by greater trust in state institutions (Berens and von Schiller, 2017) and decreased by experiences of corruption (Jahnke and Weisser, 2019). Castañeda et al. (2020) argue that the fiscal contract is conceived as something that can be opted into or out of in Latin America. They find that those who purchase private health insurance are less willing to pay taxes than those who utilise government-provided public goods.

If citizens’ engagement with the fiscal contract depends on the benefits that they believe they obtain from the state, and remittances are used to substitute the goods and services that the government provides, it follows that remittance recipients are more likely to justify cheating on taxes and to be hesitant to paying them because they do not (want to) use state-provided goods and services. Put another way, remittances diminish citizens’ support for the fiscal contract by allowing recipients to buy substitutes for public goods and services.

Since their income and welfare originates primarily from abroad, remittance-receiving households are also less vulnerable to fluctuations in the national economy and allocations of public spending – mainly because remittances tend to be stable and counter-cyclical (Ratha, 2006; Yang, 2008). This can lead to a disconnection of remittance recipients from national political affairs, which has been evidenced by studies showing that remittances reduce formal political participation, such as electoral turnout (Dionne et al., 2014; Germano, 2018; Goodman and Hiskey, 2008; López García, 2018; López García and Maydom, 2021). This reduced interest in national affairs can lead to a decline in a sense of shared national political identity which also reduces tax compliance (Konrad and Qari, 2012; MacGregor and Wilkinson, 2012). As a result of their conversations with relatives living in wealthier countries, remittance recipients may also develop higher expectations about the quality of public services. This could lead recipients of remittances from migrants in wealthier countries to feel even more dissatisfied with the quality of welfare delivered at home, and hence be less willing to contribute to the tax effort.

Although remittance recipients are less likely to use state-provided welfare services, this does not mean that they are isolated from and do not come into contact with state officials and institutions. In fact, they are likely to come into greater contact because of the way in which they spend their remittance income. There is good evidence that compared with other sources of income, remittances are more likely to be spent on asset accumulation and investment, for example, purchasing durable goods, such as vehicles, buying housing or property or opening small businesses (Adams, 1991; Adams and Cuecuecha, 2010; Airola, 2007; Amuedo-Dorantes and Pozo, 2011; Yang, 2008). From the perspective of the NELM, these investments follow an insurance motive – they diversify households’ sources of income and reduce the risk of income losses in case of an unexpected event.

Durable and investment goods are likely to be taxed by the state, in the form of property taxes, vehicle taxes or licence fees. As migrant households invest more, they become exposed to taxation in a transactional manner; they pay specific fees to own or licence an asset or investment. Taxes are thus paid to protect access to or ownership of a specific good or investment rather than generally to provide public services. As recipients increase their interactions with state officers, they are more likely to be solicited for bribes. These experiences of corruption can further reduce recipients’ tax morale (YJahnke and Weisser 2019).

To summarise, we argue that remittances reduce support for the fiscal contract. We attribute this effect to the sources and uses of remittance income. Recipients are less reliant on the domestic economy and government services. Consequently, they are less likely to develop feelings of belonging to the national community or reciprocity or obligation towards the state. Recipients’ weak tax morale is furthermore heightened because of their increased exposure to and interactions with and state bureaucracies. Recipients develop a more transactional relationship with the state in which taxation becomes a fee for protecting or licencing specific assets and investments rather than a reciprocal fiscal contract in exchange for public services. On the basis of these considerations, we advance the following key hypothesis:

H1. The receipt of remittances decreases support for paying taxes.

Our proposed causal mechanisms – the development of a transactional relationship with the state and a reduction in feeling part of the national political community embodied by the state – have a number of testable implications. We therefore posit:

H2. The receipt of remittances reduces national political identification.

H3. The receipt of remittances increases the likelihood of payment of licence fees and taxes on investment goods.

H4. The receipt of remittances increases citizens’ exposure to corruption.

Data

Our theory applies to poor- and middle-income states that have yet to develop a robust fiscal contract. We test our hypotheses using survey data from two regions in which these states predominate: Africa and Latin America. In both regions, direct tax-collection levels are low, tax schemes are highly regressive and informality is very high. Nevertheless, there is significant variation in income, levels of emigration, democracy and political stability between and within the two regions. If our findings are robust across Africa and Latin America, we would therefore expect them to be applicable more widely to other developing regions.

Data for Africa comes from rounds 4, 6 and 7 of the Afrobarometer survey, conducted in 2008–2009, 2014–2015 and 2017–2018. Data for Latin America was gathered from the 2009 wave of the Latinobarometro survey. 1 Afrobarometer and Latinobarometro ask nationally representative samples of respondents a wide range of questions about their social and political attitudes and behaviour in their respective regions. In this article, we focus on questions relating to tax, remittance receipt and strength of national identity. The surveys ask different sets of questions, so we analyse data from Afrobarometer and Latinobarometro separately. Where possible, we combine the different rounds of Afrobarometer.

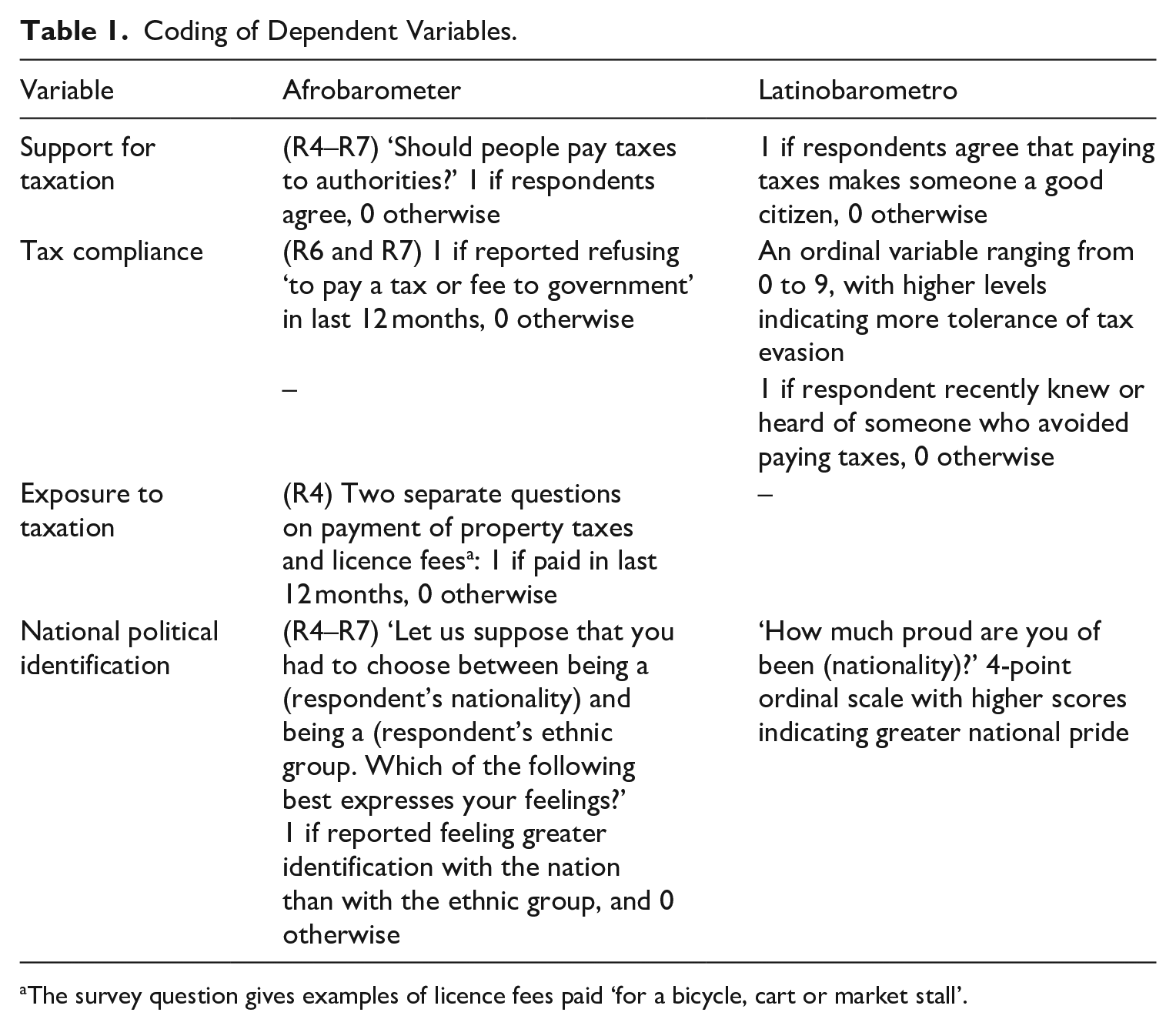

The main independent variable in this study is individuals’ status as remittance recipients. Remittance receipt is measured as a binary variable, coded as 1 if respondents reported having received remittances from abroad in the 12 months prior to the survey and 0 otherwise. The key dependent variables and their coding are described in Table 1.

Coding of Dependent Variables.

The survey question gives examples of licence fees paid ‘for a bicycle, cart or market stall’.

Survey questions on tax attitudes may be inaccurate if respondents fear reporting illegal activity or feel uncomfortable admitting that they do not support or have evaded paying taxes. This would be a particular concern for our analysis if any such propensity to misreport varied according to remittance recipient status. We examine the extent to which this might be a problem by considering the distribution of non-responses to the key questions on the survey. In the Afrobarometer sample, the share of respondents who were evasive about reporting their support for taxation and their tax behaviour is very small at 4.4% and 3.7%, respectively. In the Latinobarometro, the share of individuals who did not report their support of tax evasion is 6.1%. These low rates of question evasion suggest that in both regions, respondents are generally forthcoming about expressing their tax-related behaviours and attitudes. Furthermore, we find in both samples that non-response is marginally more frequent among non-recipients than recipients. In Afrobarometer, the share of respondents who refused to report their tax behaviour is 3.1% among remittance recipients and 3.9% among non-recipients. Similarly, the share of respondents in Africa who did not report their support for taxation is 3.6% among remittance recipients, and 4.6% among non-recipients. In Latin America, the non-response is 5.5% among remittance recipients and 6.3% among non-recipients. These small quantitative differences suggest that differential propensity to misreport across recipients and non-recipients is not a threat to our identification strategy.

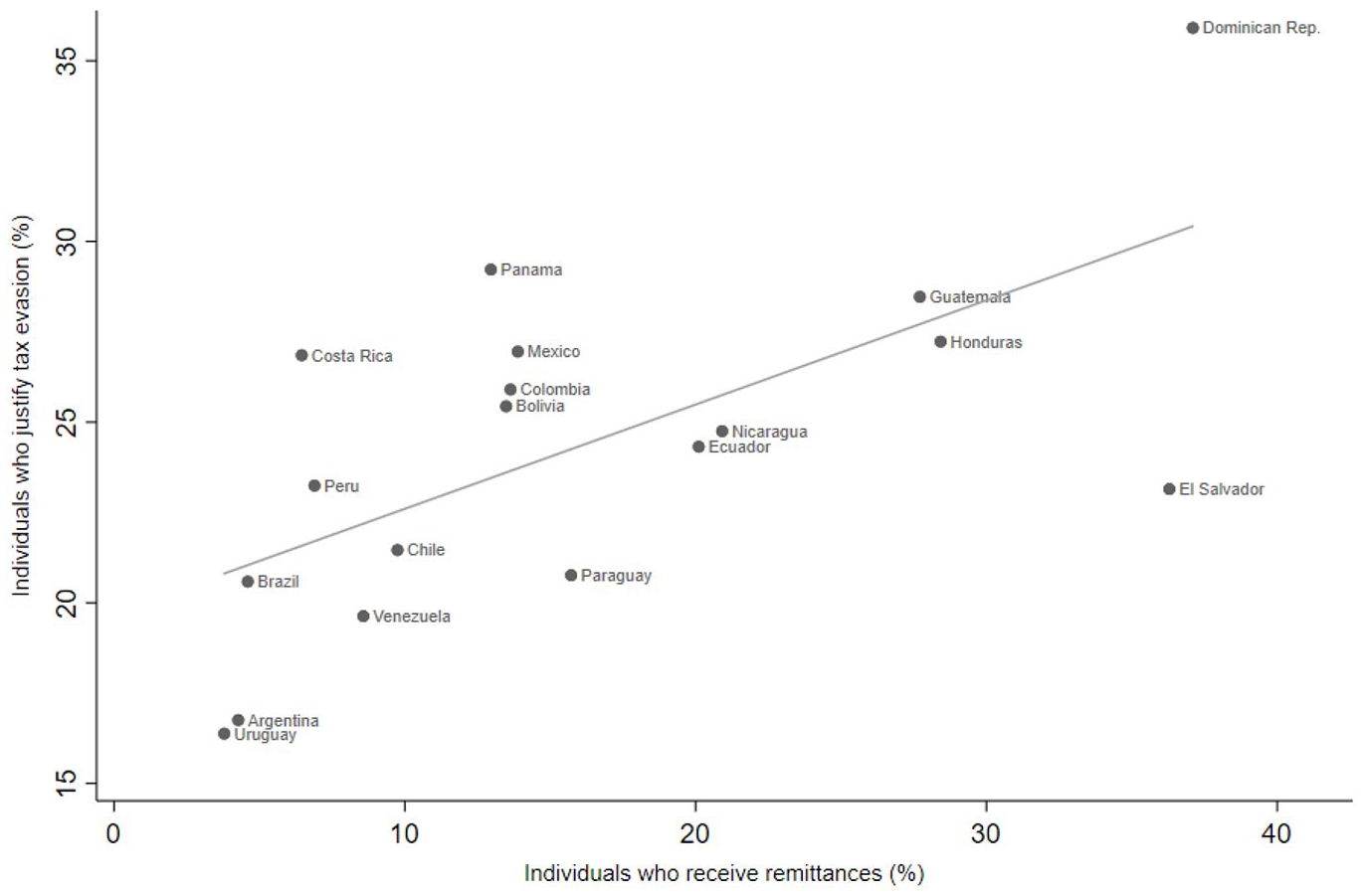

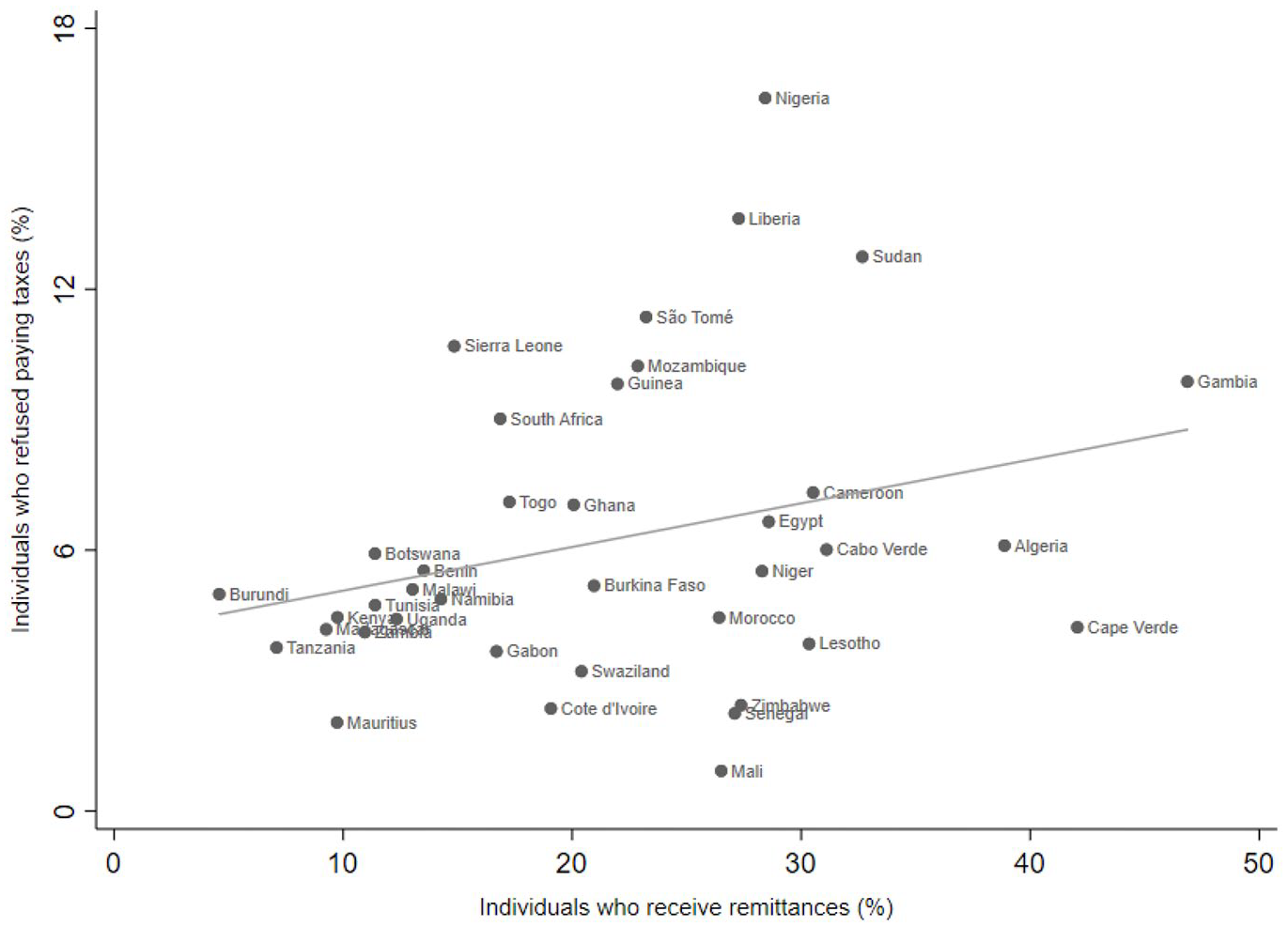

There is significant heterogeneity in levels of remittance receipt and attitudes towards taxes across countries surveyed by Afrobarometer and Latinobarometro, as shown in Figures A1 and A2 in the Online Appendix. At the country level, there is a positive correlation between the proportion of the population who receive remittances and attitudes towards taxation. Figure 1 demonstrates this relationship in Latin America. The Dominican Republic has both the highest proportion of remittance recipients in its population and the highest reported support for tax evasion, while Uruguay has the lowest proportion of both remittance recipients and supporters of tax evasion. The correlation is not as strong in Africa, as shown in Figure 2, but it is also positive. The general pattern in both regions is that the more remittance recipients there are in a population, the greater the support is for tax evasion. In what follows, we estimate a series of regression models to determine whether this pattern is driven by an individual-level relationship between remittance receipt and tax attitudes and behaviours.

Remittance Receipt and Support for Tax Evasion in Latin America.

Remittance Receipt and Tax Refusal in Africa.

Empirical Strategy

To explore the influence of remittance receipt on tax exposure and attitudes, we estimate the following baseline specification:

where ij refers to individual i in country j. Taxationij represents the variables measuring exposure to or attitudes towards taxation that are to be examined. As our main independent variables, we use the remittance-receiving status of an individual, as described above. The vector Xi includes information on a variety of covariates that could influence individual tax attitudes and behaviour. These are: respondents’ experiences with and perceptions of crime and corruption, and levels of trust in tax authorities (Torgler, 2005). To address the possibility of individuals exhibiting negative attitudes towards taxation when they intend to stay in (i.e. not migrate from) their country of origin, models incorporate a binary variable measuring individuals’ plans (or serious considerations) to work or live abroad in the future. This variable is highly correlated with remittance receipt and might capture some of the intrinsic characteristics of the individual as it relates to support of taxation.

We also take into account other socio-economic and demographic attributes that are likely to affect both the receipt of remittances and individual attitudes towards taxation. These are: gender, age, rural/urban residence and educational attainment (reference category: no education). All models control for employment status and a wealth index based on a series of questions about respondents’ possession of various durable goods. Any correlations we identify between remittances and tax exposure and attitudes are therefore unlikely to be driven purely by a resource effect whereby those with greater amounts of resources (including from remittances) are more likely to support or report tax evasion.

Following the conditional-cooperation theory of taxation, support of taxation is contingent on other people paying taxes (Torgler, 2005). That is, individuals who think that fellow citizens evade taxes are less willing to pay them themselves. Hence, we also include in our models a variable measuring respondents’ perception of tax compliance in society. From R6 of the Afrobarometer, we use a binary variable that takes the value of 1, if the respondent thinks that fellow citizens always pay taxes and 0 otherwise. From the Latinobarometro survey, we use a variable that measures respondents’ perceptions of tax compliance. It is derived from the question: ‘Based on what you have heard, what is the proportion of citizens who pay taxes properly?’ This is an ordinal variable, ranging from 0 to 3 with poles of ‘none’ and ‘all’.

As additional controls in the models using data from Africa, three variables that can influence tax attitudes and compliance are included: (1) a binary variable measuring whether the respondent thinks the survey was sponsored by the government, (2) a binary variable measuring whether the respondent thinks that it is difficult to find information about what taxes and fees to pay and (3) a binary variable measuring whether the respondent thinks that in their country it is difficult to avoid paying taxes. 2

Finally, γj are country effects to control for any unobserved or unmeasured differences across countries, such as formal and informal institutions and norms about tax morale and compliance.

To test the hypotheses that the receipt of remittances influences tax attitudes and behaviours and national political identification, we estimate a series of regression models. We use logit and ordered logit estimators depending on the nature of the dependent variable. We estimate two models for each dependent variable. The first represents a baseline model, including basic socio-economic and demographic control variables and the second adds all other control variables.

Matching Strategy

As noted above, members of remittance-receiving households may have specific unobservable attributes which could affect the probability that they will send relatives abroad as well as their attitudes towards taxation. In this context, omitted variables that are correlated with both the receipt of remittances and taxation attitudes and perceptions may bias our estimates. To mitigate the problem of ‘selection on observables’, we use matching such that treated and control groups have similar covariate distributions (Ho et al., 2007). Specifically, we employ the coarsened exact matching (CEM) method developed by Iacus et al. (2012). CEM is a non-parametric matching method that reduces the imbalance between treated and untreated groups and is less susceptible to model misspecification than other matching techniques such as propensity-score matching.

In this study, the treatment group is made up of respondents who receive remittances. They were matched on the pre-treatment variables of age, gender, size of place of residence, years of education, employment status and wealth. Using CEM, we ensure that the treatment and control groups are similar in terms of the matched covariates, and that the results are not driven by self-selection based on these characteristics. We then include the additional previously discussed covariates as controls to address any remaining differences in terms of (non-matched) characteristics and increase statistical power. Our approach hence allows us to separate the effect of remittances from other factors shaping individuals’ support of taxation. To compensate for the different sizes of the treatment and control groups, we use weights in our regressions. One caveat is the loss of observations (and hence statistical power) to obtain balance, but the inclusion of additional controls increases statistical precision.

Results

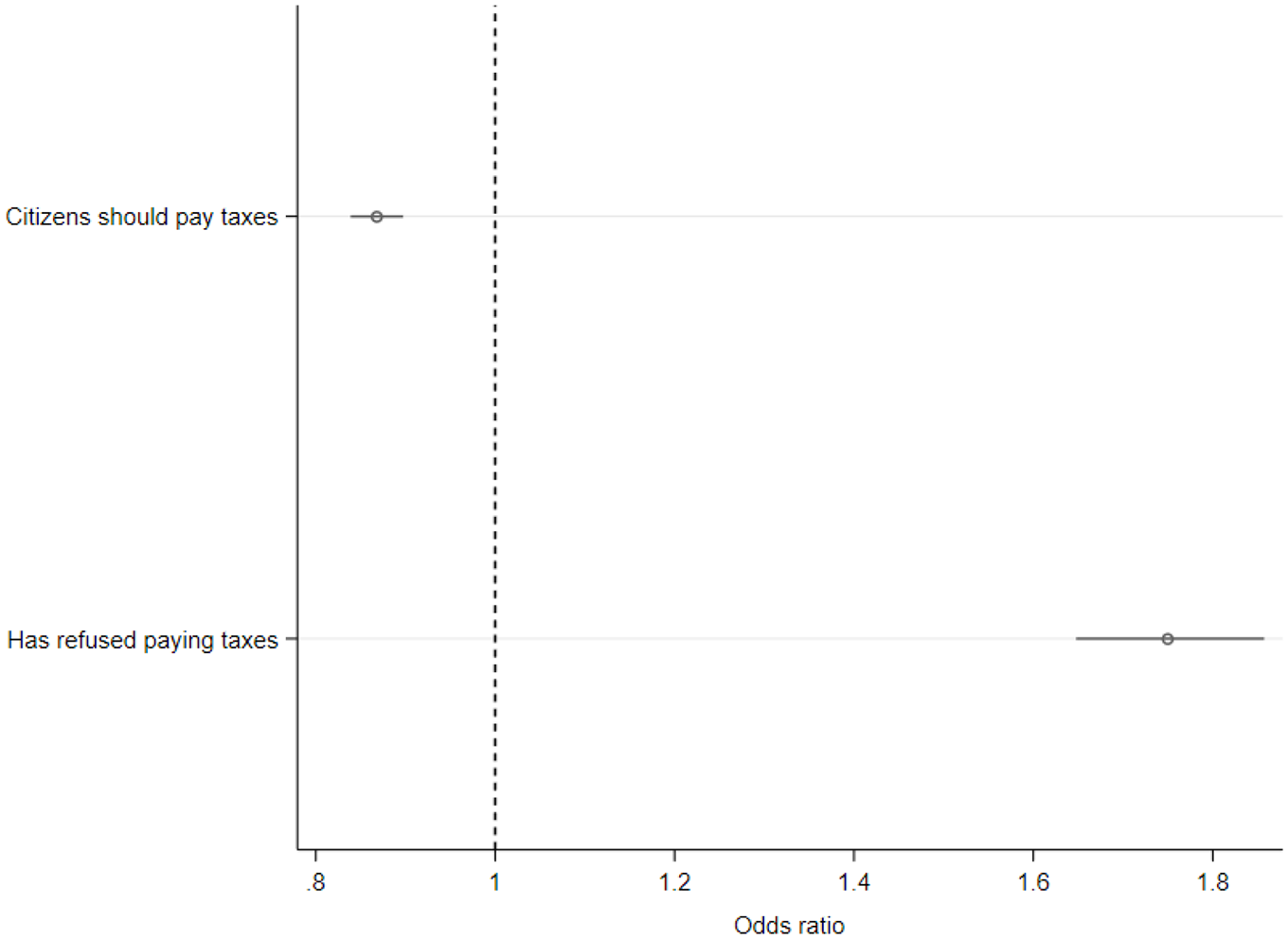

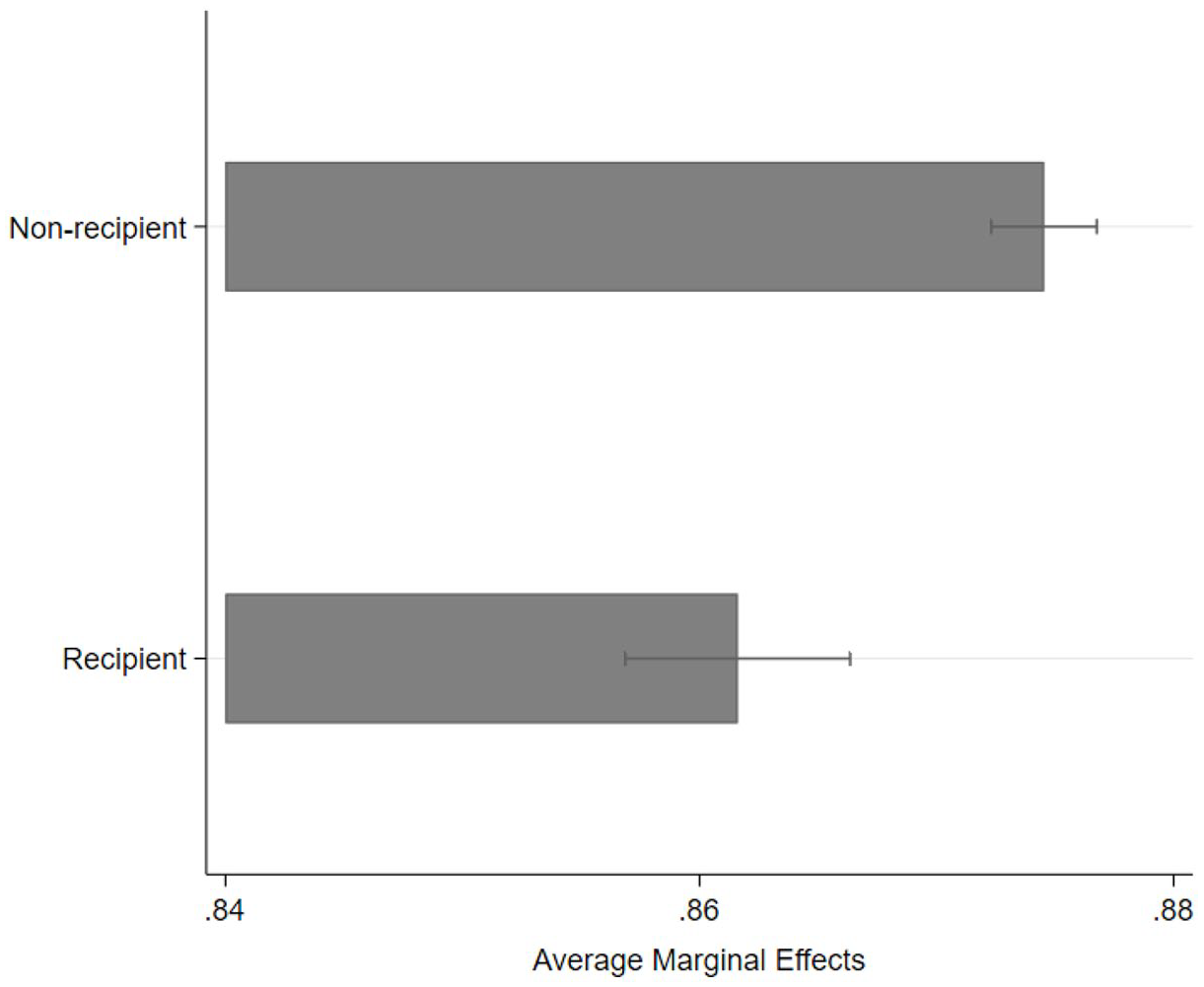

We begin by testing the hypothesis that remittance recipients are less supportive of taxation using data from R4, R6 and R7 of the Afrobarometer. We pool the data and include wave-fixed effects to control for temporal variation. Our models show that remittance recipients are significantly less likely to agree with the idea of citizens having an obligation to pay taxes to the government than non-recipients. Those who receive remittances are also more likely than non-recipients to report having refused paying taxes when asked to do so. The full results of these models are reported in the Online Appendix, and the exponentiated coefficients of the remittance variable are displayed graphically in Figure 3. Receiving remittances is associated with a 14% decrease in the likelihood of an individual agreeing that citizens should pay taxes to the government, and an increase of 61% in the probability of refusing to pay taxes. These results provide evidence to support our hypothesis that the receipt of remittances lowers tax morale and increases support for and the practice of tax evasion.

Effect of Remittances on Tax Attitudes and Behaviour in Africa.

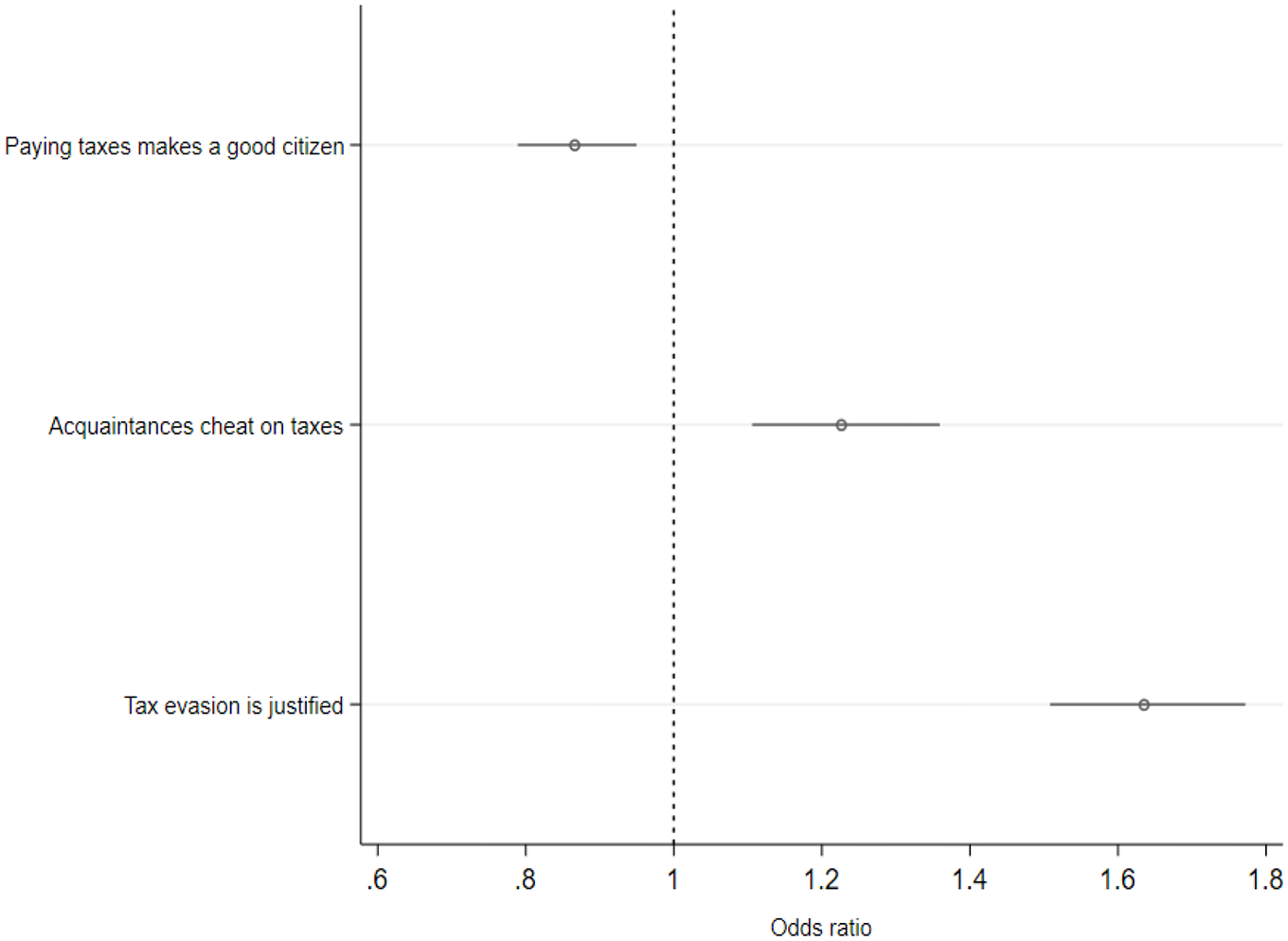

We find similar headline results when examining data from Latin America. The full regression tables for models using the Latinobarometro survey appear in the Online Appendix and are graphically presented in terms of average marginal effects in Figure 4. As in Africa, remittances in Latin America are associated with lower support for taxation in general and greater knowledge and approval of tax evasion. Holding all other variables constant, we estimate that receiving remittances leads to an 11% decrease in the likelihood of supporting the idea that paying taxes makes a good citizen, a 13% increase in the probability of having an acquaintance who cheats on taxes and a 51% increase in the likelihood of justifying tax evasion. Evidence from both Latin America and Africa therefore supports our primary hypothesis that remittance recipients are less likely to support the fiscal contract than non-recipients.

Effect of Remittances on Tax Attitudes and Behaviour in Latin America.

In both the Afrobarometer and Latinobarometro models, our results are robust to the inclusion of socio-demographic controls and potentially confounding variables measuring emigration plans and considerations, trust in authorities, and perceptions of and experiences with corruption and crime.

To ensure that our results are not driven by outliers, we estimated separate models in which countries with very high levels of remittance recipients were excluded from the sample: Cape Verde, Algeria, Gambia, El Salvador and the Dominican Republic. The effects of remittances on tax behaviour and attitudes (reported in the Online Appendix) remain similar in the reduced sample.

To control simultaneously for the individual-level characteristics and country-level factors that may influence tax attitudes and behaviour, we also estimate a series of multilevel models with individual respondents nested in countries across which intercepts vary. Our models include the following country-level predictors: remittance inflows as a percentage of gross domestic product (GDP) from the World Bank’s World Development Indicators (as a proxy for both country levels of economic development and dependence on remittances); direct taxes as a percentage of the GDP from ICTD/UNU-WIDER Government Revenue Dataset 3 ; and the control of corruption index from the World Bank (as a proxy of corruption). Results from these mixed models are reported in the Online Appendix. 4 Although the variance is statistically meaningful across models, indicating that there is a significant amount of between-country variability in the outcome, the coefficient for the receipt of remittances remains significant. Thus, even after accounting for a country’s level of public corruption, remittance recipients are more likely than non-recipients to refuse paying taxes or justify tax evasion. Results are consistent when using the corruption perception index from Transparency International as alternative country-level predictor of corruption. 5

Mechanisms

To examine the mechanisms behind our results, we perform a series of analyses to examine the relationships between remittances, national political identification and the payment of taxes and fees to protect assets and investments. The full regression tables are reported in the Online Appendix, and we display the key results graphically in the main text.

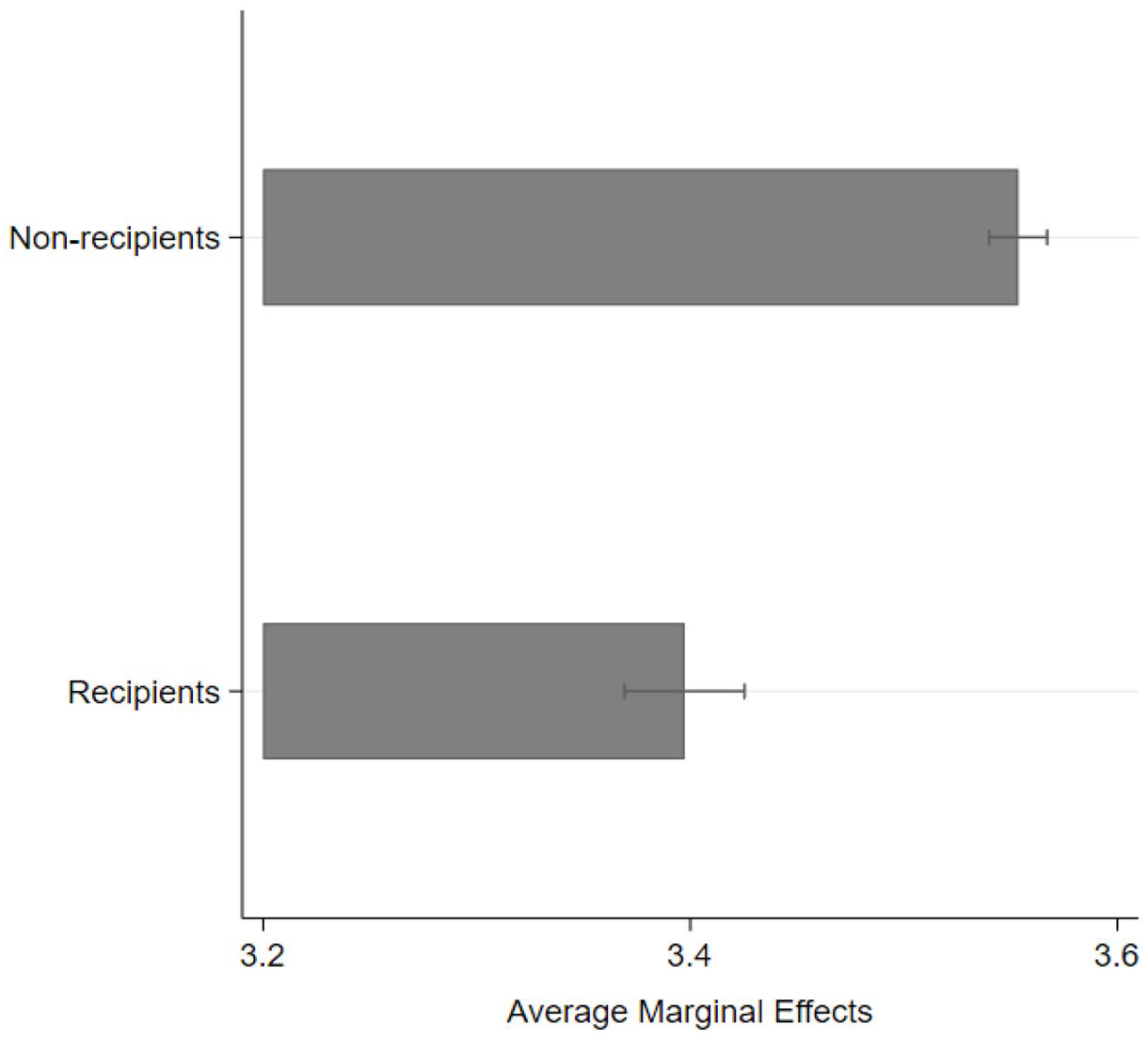

We first test our hypothesis that remittances weaken support for taxation because recipients have weaker feelings of national identity. Figure 5 plots the predicted probabilities of feeling identified more with one’s nation than with the ethnic group for a set of hypothetical individuals who vary only on whether or not they receive remittances. As expected, feelings of national identity are weaker among individuals who receive remittances. Models (reported in the Online Appendix) show that once we control for feelings of national identity, the (Y-standardised) coefficient for remittance receipt remains positive and statistically significant, but decreases across models. This is consistent with our hypothesis of remittances working (partially) through that channel. Figure 6 plots the average predicted probabilities of tax refusal for average hypothetical individuals who vary only on their national identification and whether or not they receive remittances. In line with our theory, the stronger the feelings of national identity the less likely individuals are to report having refused to pay taxes to the government, while those who receive remittances are more likely to report tax refusal than non-recipients. Having a high level of national political identification can mitigate the effect of remittances on tax refusal to some extent, but as we saw above, remittance reduces these feelings.

National Identification by Remittance Recipient Status in Africa.

Tax Refusal, Remittances and National Identification in Africa.

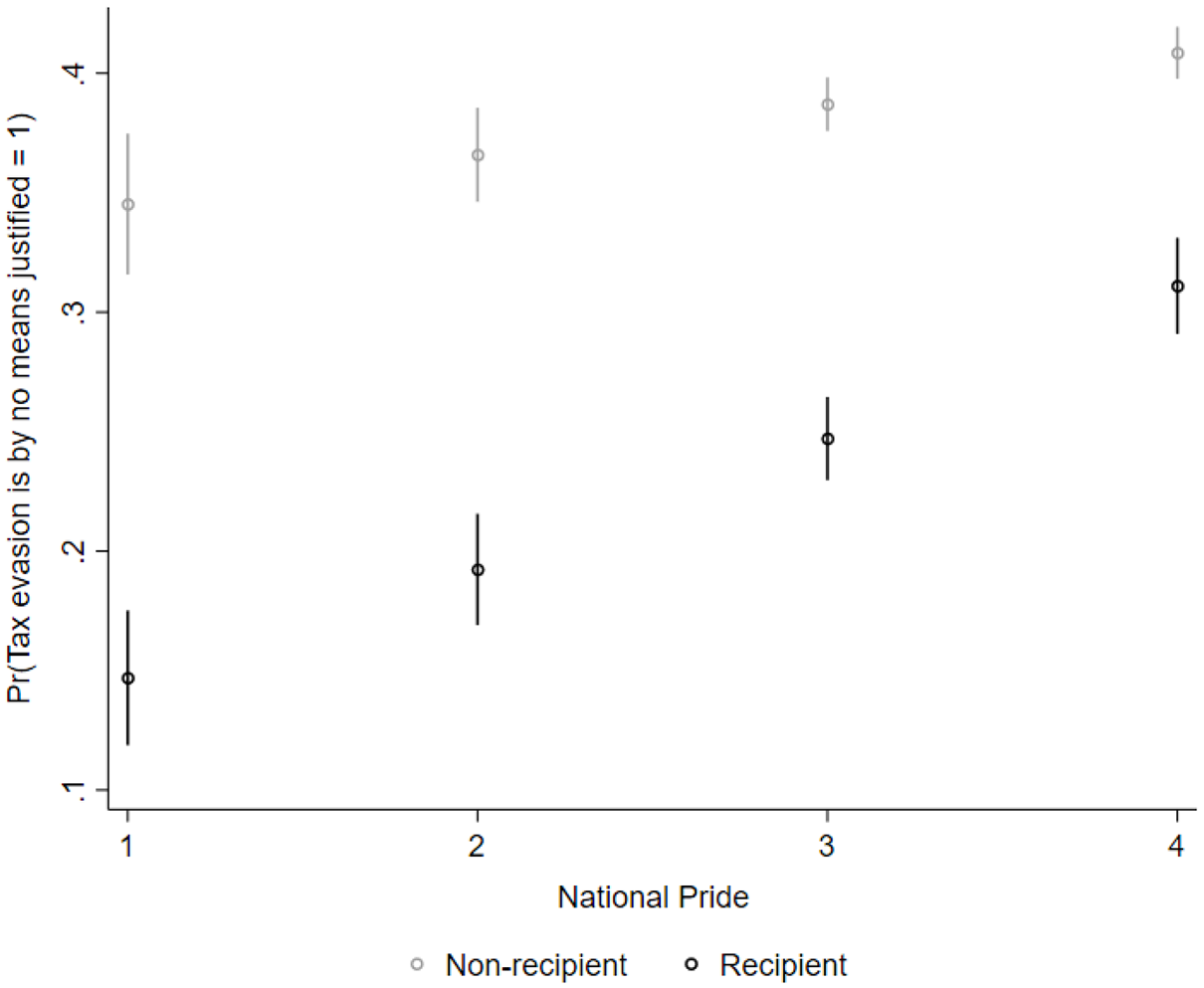

We find similar results in Latin America which are reported in Figures 7 and 8. Remittances are correlated to weaker feelings of national pride, and reduced levels of national pride are associated with a lower probability of opposing tax evasion. Increasing levels of national pride can somewhat mitigate the negative effect of remittances, but remittances recipients with the highest level of national pride are nevertheless more supportive of tax evasion than non-recipients with the lowest level of national pride. The evidence from Africa and Latin America thus supports our hypothesis that the receipt of remittances affects the fiscal contract by weakening feelings of national political identification.

National Pride by Remittance Recipient Status in Latin America.

Support for Tax Evasion, Remittances and National Pride in Latin America.

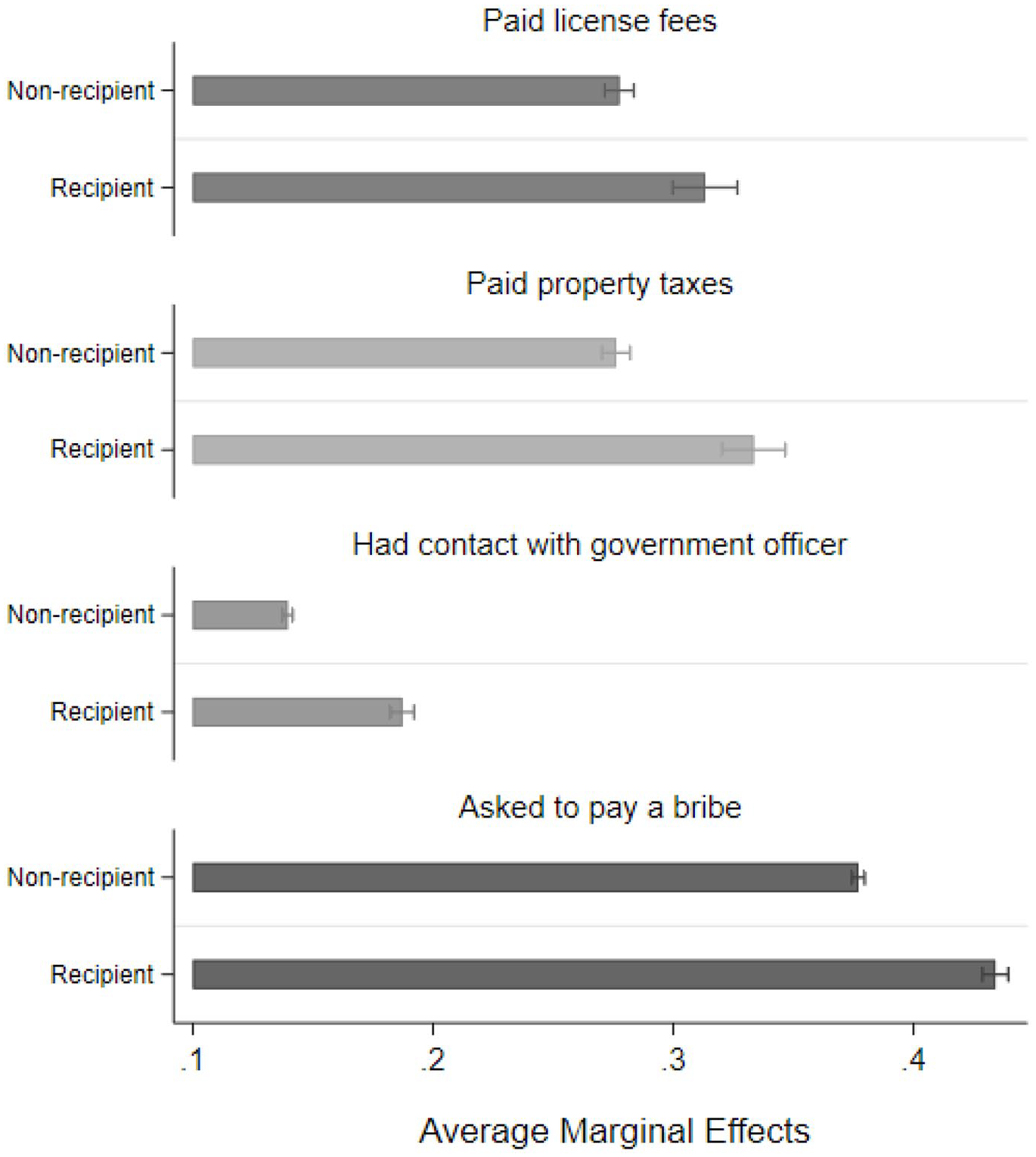

We also test the hypothesis that remittances promote a transactional relationship with the state by examining whether recipients are more likely to pay licence fees and property taxes. The headline results of models using Afrobarometer data are reported in Figure 9, with full regression tables available in the Online Appendix. Relative to non-recipients, remittance recipients are more likely to report both having paid licence fees and having paid property taxes to the government in the 12 months prior to the survey. These results provide evidence that remittance recipients must pay fees to register and protect the investment goods that they purchase with the remittances they receive. These taxes and fees are paid for a specific service – protection of assets – rather than to support the provision of state-funded welfare services.

Average Marginal Effects by Remittance Receipt with 95% Confidence Intervals.

We examine whether the receipt of remittances increases individual contact with state authorities, which might be expected if individuals develop a transactional relationship with the state. As noted earlier, in developing societies, like those in Africa, bribes are regularly paid when dealing with state authorities to secure public goods and services, speed up bureaucratic processes and avoid punishment. Thus, we measure exposure to state authorities in two ways: reported contact with state authorities and reported bribe solicitations. Figure 9 also corroborates our contention that remittances make recipients more likely to interact with government officers and be solicited for bribes. These results indicate that remittance recipients are more likely to have contact with state authorities, which can be attributed to their greater propensity to purchase durable and investment goods. To register and profit from these goods, contact with the state is necessary and licence fees and bribes are frequently paid. Models (reported in the Online Appendix) confirm that the effect of remittance receipt on tax support and compliance travels (partly) through individual exposure to bribery. Futhermore, both contact with state officers and the payment of bribes magnify the influence of remittances on tax refusal.

To further explore this mechanism, we examine how trust (and perception of corruptions) in the bureaucracy influence the relationship between remittances and support of taxation (Kirchler et al., 2008; Wahl et al., 2010). Using data from R6 of the Afrobarometer, we find that there are no meaningful differences across remittance recipients and non-recipients in their levels of trust in, and perceptions of corruption among tax authorities. Moreover, at all levels of trust and perceived corruption in tax officers, remittance recipients in Africa are less likely to think citizens should pay taxes to the government and are more likely to report having refused paying taxes than non-recipients. Similar results are found in Latin America; remittance recipients do not differ significantly from non-recipients in their levels of trust in the public administration. They are also less likely to disapprove of tax evasion than non-recipients at all levels of trust in the public administration That is, the receipt of remittances makes individuals less supportive of taxation above and beyond their trust in the bureaucracy, or perceptions of corruption in it. These results are shown in the Online Appendix.

To rule out other mechanisms, we examine whether there are heterogeneous responses of remittances according to individual evaluations of the household and the national economy. Previous studies have found that remittances are associated with better evaluations of the household and national economy and hence lower levels of disapproval of authorities (Ahmed, 2017; Germano, 2018; Ratha, 2006; Tertytchnaya et al., 2018; Yang and Choi, 2007). One might expect that individuals with positive evaluations of the household or national economy are more supportive of taxation. Although the receipt of remittances is a positive predictor of assessments of the national and domestic economy,” we find, however, that at all levels of economic evaluations, remittance recipients have a lower tax morale than non-recipients (as reported in figures in the Online Appendix). This holds even when considering retrospective, present, and prospective evaluations of the household and national economy. The causal chain from remittances to tax attitudes therefore does not work through the enhanced pocketbook and sociotropic perceptions of the economy generated by receiving remittances.

We also looked at whether remittance recipients are willing to shoulder a heavier tax burden provided the government uses the money to improve public services and goods provision. From R6 of the Afrobarometer, we examine this by examining responses to the question: ‘Would you pay higher taxes to increase health spending?’ It is coded 1, if the respondent (strongly) supports paying more taxes to increase health spending, and 0 otherwise. We find that people who receive remittances from abroad do not differ meaningfully from non-recipient individuals in their support to increase their tax contributions even if it is for universal public services, such as health. 6

In addition, we examine how plans (or serious considerations) to emigrate influence remittance recipients’ tax attitudes and behaviour. We use data from R7 of the Afrobarometer and the 2009 wave of the Latinobarometro, since these are the only survey waves that include questions on both tax attitudes and behaviour and emigration plans (and serious considerations). Across both regions, we find that although remittances and emigration plans weaken support for taxation, the influence of remittances does not vary significantly with individual emigration plans. Evidence from Africa and Latin America thus suggests that the receipt of remittances influences tax attitudes and behaviour does not operate through an exit channel, even among individuals with emigration plans.

Heterogeneity Analysis

Finally, we explore whether the relationship between remittance receipt and tax attitudes and behaviour exhibits heterogeneous responses by the socioeconomic and demographic characteristics of individuals. Although non-employed individuals might be less supportive of (or exposed to) taxation, and non-employed remittance recipients might be more dependent on remittances than employed recipients, we find that employment status has no influence on tax attitudes and behaviour among remittance recipients. We also find that at all wealth levels, the receipt of remittances has a negative influence on tax behaviour and morale. This result suggests that the influence of remittances does not merely consist of recipients (becoming wealthier and hence) paying more tax and therefore disliking tax. Neither do we find heterogeneous responses by age or gender. Results of these analyses are available in the Online Appendix.

In sum, the results of the statistical analyses suggest that receiving remittances makes individuals more likely to justify and practice tax evasion. Although remittance recipients are self-selected and differ along a series of socioeconomic and demographic characteristics from non-recipients, our baseline results remain robust after matching individuals on observable characteristics and controlling for a set of potential confounders. Estimates also hold true after excluding outliers from the sample and controlling for variables at the country-level of analysis. As for the mechanisms, we do not find heterogeneous effects depending on levels of trust and perceptions of corruption in tax authorities, economic assessments, emigration plans and employment status, wealth, age or gender – factors that theoretically can affect tax attitudes and behaviour. This alleviates the possibility that the receipt of remittances is capturing unobservable heterogeneity that is not controlled for in our models.

However, we do find evidence that relative to non-recipients, remittance recipients are less likely to develop feelings of reciprocity towards or identification towards the state as the embodiment of the national community. Our analysis also confirms that remittance recipients are more likely to interact with and be solicited for bribes by state authorities and that interacting with or being solicited bribes by state authorities significantly lowers tax morale among remittance recipients. We therefore conclude that the foreign source of remittances and their use to purchase investment goods are the most likely explanations of why remittance recipients are less likely to support and comply with the fiscal contract. Relative to non-recipients, remittance recipients are less reliant on the state and hence less likely to develop feelings of reciprocity towards or identification towards the state as the embodiment of the national political community. Instead, recipients develop a transactional relationship with the state which involves paying licence fees, property taxes and bribes to register and protect investment goods purchased with remittances. Such interactions further reduce support for general taxation among remittance recipients.

Conclusion

How do remittances influence the extractive capacity of the state in migrants’ homelands? In this article, we have found robust evidence from Africa and Latin America that the receipt of remittances reduces individual willingness to support taxation or pay taxes, thereby hindering the development of a robust fiscal contract in migrant-sending countries. Remittances insulate and disconnect recipients from the national political economy which reduces their national political identification. Rather than supporting the idea of funding the state to improve general public welfare, recipients develop a more transactional relationship with the state by paying fees, taxes and bribes for the specific service of protecting investment goods purchases with remittances.

Our findings raise important normative concerns. One of the most elementary state functions is the ability to collect taxes (Martin et al., 2009). Without sufficient revenue, governments (whether democratic or not) cannot achieve their goals: they cannot monopolise the use of violence, provide public goods or enforce property rights. Where tax collection is limited, individuals are more likely to emigrate and send remittances back home. However, if remittance income lowers the support of recipients for taxation, this can further undermine the capacity of the state to collect resources, leading to a vicious circle that is difficult to escape from. Potential policy responses might be to restrict emigration, tax remittances directly or provide better public services without the need for taxation. Unfortunately, such measures are either unlikely to work – restricting legal emigration will encourage the illegal kind and taxing formal remittances will increase informal transfers – or fiscally difficult for governments without alternative sources of revenue. Furthermore, many regimes may be content with allowing high levels of emigration if doing so allows them to channel what limited resources they control towards supportive constituencies rather than undertaking the long-term project of developing robust taxation-based social contracts. Rather than a boon for development by providing a counter-cyclical source of foreign currency, remittances might trap countries in a cycle of underdevelopment.

We would expect our argument to apply to all less developed countries which have not developed a robust fiscal system combining a high level of taxation with strong public services. We have found evidence for our argument in Africa and Latin America, two regions that vary in contemporary level of development, political institutions and colonial legacies. Future research could examine how the links between remittances and taxation attitudes play out in other regions around the globe, such as Eastern Europe, Asia or the Middle East.

Analysing how migrant remittances influence origin-country governments’ tax-policy choices constitutes another promising avenue for future research. Given that norms are important correlates of support of taxation (Alm and Torgler, 2006; Persson et al., 2015), it would also be fascinating to explore how the political and social norms that migrants send back home influence the motivation to pay taxes by those left behind (Boccagni et al., 2016; Krawatzek and Müller-Funk, 2020). These future undertakings could help us to further understand how remittance recipients’ relations with the state can contribute to the fiscal contract in their homelands.

Supplemental Material

sj-docx-1-psx-10.1177_00323217211054657 – Supplemental material for Migrants’ Remittances, the Fiscal Contract and Tax Attitudes in Africa and Latin America

Supplemental material, sj-docx-1-psx-10.1177_00323217211054657 for Migrants’ Remittances, the Fiscal Contract and Tax Attitudes in Africa and Latin America by Ana Isabel López García and Barry Maydom in Political Studies

Footnotes

Acknowledgements

We would like to thank the anonymous reviewers, Melina Altamirano, Sarah Berens, Tim Betz, Gustavo Flores-Macías, Katrina Maydom, Ari Ray and Erik Snel for their helpful comments and suggestions on previous versions of the manuscript. We also extend our gratitude for the feedback received at the 2021 Annual Conference of the Swiss Political Science Association, the 2021 Annual Meeting of the Midwest Political Science Association, the ECPR Joint Sessions Workshop “Diaspora Mobilization and Homeland Politics” (May 2021), the 2021 Annual Meeting of the European Political Science Association, the 2021 Annual IMISCOE Conference, the 2021 Annual Meeting of the German Political Science Association (DVPW), the “Micro-level Dynamics of Migrant Transnationalism” (MITRA) Symposium at Maastricht University (September 2021), and the 2021 Annual Meeting of the American Political Science Association. We acknowledge the use of data made publicly available by the Afrobarometer and the Latinobarometro. All errors remain our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

Supplemental Material

Variables included in the regression analysis

Codebook – Afrobarometer R4, R6, R7

Codebook – Latinobarometro 2009

Figure A1. Remittance Receipt and Tax Attitudes in Africa

Figure A2. Remittance Receipt and Tax Attitudes in Latin America

Figure A3. Tax Refusal, Remittances and National Identity in Africa

Figure A4. Support for Taxation, Remittances and National Identity in Africa

Figure A5. Tax Evasion, Remittances and Affinity with Nationals in Latin America

Figure A6. Affinity with Nationals by Remittance Recipient Status in Latin America

Figure A7. Tax Evasion, Remittances and National Pride in Latin America

Figure A8. Payment of Taxes by Remittance Recipient Status

Figure A9. Support for Taxation, Remittances and Contact with Authorities in Africa

Figure A11. Support for Taxation, Remittances and Bribery in Africa

Figure A12. Tax Refusal, Remittances and Bribery in Africa

Figure A13. Trust in Tax Authorities by Remittance Recipient Status

Figure A14. Support for Taxation, Remittances and Trust in Tax Authorities in Africa

Figure A15. Refusal to Pay Taxes, Remittances and Trust in Tax Authorities in Africa

Figure A16. Support for Taxation, Remittances and Perceptions of Corruption in Africa

Figure A17. Refusal to Pay Taxes, Remittances and Perceptions of Corruption in Africa

Figure A18. Trust in Authorities by Remittance Recipient Status in Latin America

Figure A19. Tax Evasion, Remittances and Trust in the Public Administration in Latin America

Figure A20. Tax Evasion, Remittances and Trust in the Government in Latin America

Figure A21. Support for Taxation, Remittances and Employment in Africa

Figure A22. Tax Refusal, Remittances and Employment in Africa

Figure A23. Tax Evasion, Remittances and Employment in Latin America

Figure A24. Support for Taxation, Remittances and Wealth in Africa

Figure A25. Tax Refusal, Remittances and Wealth in Africa

Figure A26. Tax Evasion, Remittances and Wealth in Latin America

Figure A27. Tax Refusal, Remittances and Age in Africa

Figure A28. Tax Evasion, Remittances and Age in Latin America

Figure A29. Support for Taxation, Remittances and Gender in Africa

Figure A30. Tax Refusal, Remittances and Gender in Africa

Figure A31. Tax Evasion, Remittances and Gender in Latin America

Figure A32. Tax Refusal, Remittances and Retrospective Sociotropic Evaluations in Africa

Figure A33. Support for Taxation, Remittances and Retrospective Sociotropic Evaluations in Africa

Figure A34. Tax Refusal, Remittances and Comparative Pocketbook Evaluations in Africa

Figure A35. Support for Taxation, Remittances and Comparative Pocketbook Evaluations in Africa

Figure A36. Tax Refusal, Remittances and Present Sociotropic Evaluations in Africa

Figure A37. Support for Taxation, Remittances and Sociotropic Evaluations in Africa

Figure A38. Tax Refusal, Remittances and Pocketbook Evaluations in Africa

Figure A39. Support for Taxation, Remittances and Pocketbook Evaluations in Africa

Figure A40. Tax Refusal, Remittances and Prospective Sociotropic Evaluations in Africa

Figure A41. Support for Taxation, Remittances and Prospective Sociotropic Evaluations in Africa

Figure A42. Support for Taxation, Remittances and Prospective Sociotropic Evaluations in Africa

Figure A43. Tax Evasion, Remittances and Retrospective Sociotropic Evaluations in Latin America

Figure A44. Tax Evasion, Remittances and Retrospective Pocketbook Evaluations in Latin America

Figure A45. Tax Evasion, Remittances and Present Sociotropic Evaluations in Latin America

Figure A46. Tax Evasion, Remittances and Present Pocketbook Evaluations in Latin America

Figure A47. Tax Evasion, Remittances and Prospective Sociotropic Evaluations in Latin America

Figure A48. Tax Evasion, Remittances and Prospective Pocketbook Evaluations in Latin America

Figure A49. Refusal to Pay Taxes, Remittances and Emigration in Africa (R7)

Figure A50. Tax Evasion, Remittances and Emigration in Latin America

Figure A51. Support for Taxation, Remittances and Crime in Africa

Figure A52. Tax Refusal, Remittances and Crime in Africa

Figure A53. Disapproval of Tax Evasion, Remittances and Crime in Latin America

Table A5: Payment of Taxes and Remittance Receipt in Africa (R4), Logit Models

Table A6: Taxation and Remittance Receipt in Africa (R6), Logit Models

Table A7: Taxation and Remittance Receipt in Africa (R7), Logit Models

Table A8: Payment of Taxes and Remittance Receipt in Africa (R4), Unmatched Sample

Table A9: Taxation and Remittance Receipt in Africa (R6), Unmatched Sample

Table A10: Taxation and Remittance Receipt in Africa (R7), Unmatched Sample

Table A11: Taxation and Remittance Receipt in Africa (R4-R7), excluding outliers

Table A12: Taxation and Remittances in Latin America, Logit Models

Table A13: Taxation, Remittances and National Affinity in Latin America, Logit Models

Table A14: Taxation and Remittance Receipt in Latin America, Unmatched Sample

Table A15: Taxation and Remittance Receipt in Latin America, excluding outliers

Table A16: Remittance Receipt and Support for Taxation in Africa, Multilevel Logit Models

Table A17: Remittance Receipt and Tax Refusal in Africa, Multilevel Logit Models

Table A18: Remittance Receipt and Tax Evasion in Latin America, Multilevel Ordinal Logit Models

Table A19: Remittance Receipt and Willingness to Pay Higher Taxes to Increase Welfare in Africa (R6), Logit Models

Table A20: Remittance Receipt and Willingness to Pay Higher Taxes to Increase Welfare Spending in Latin America (LAPOP), Logit Models

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.