Abstract

Grain legume cultivation in Germany has the potential to benefit agroecological biodiversity, while plant-based proteins are highly demanded. However, grain legume growers face challenges such as climatic variability, uneven political support, and a fragmented market with high transaction costs. Farmers often encounter sales difficulties due to a lack of interest from trading companies and the absence of large, homogeneous lots of consistent quality. Producer organisations (POs) can address these issues by enhancing farmers’ bargaining power, reducing transaction costs, and creating stable regional market structures. Given the limited presence of POs for grain legumes in Germany, we investigate the conditions under which farmers may choose to join a PO and examine farmers’ preferences for an ideal grain legume PO structure. We apply an ordered probit model to identify the factors influencing farmers’ interest in selling the grain legumes they grow on their farms through a PO. Our study reveals that interest in joining a PO increases by 20% when farmers perceive the core objective as achieving better prices. At the same time, provision of additional services, such as advisory support or joint logistics, has little effect. Both small and large grain legume growers show interest in POs, with administrative burdens identified as a major concern against participation. If POs meet farmers’ needs, they have a high potential to encourage grain legume cultivation and, consequently, foster more sustainable agriculture. To unlock this potential, policymakers and PO stakeholders should reduce bureaucratic barriers and promote diverse, farmer-oriented PO models.

Introduction

Many European farmers operate relatively small, independent and typically family-owned farms. In contrast, processing companies and retailers are often organised as larger, horizontally and vertically more integrated entities (Clapp, 2021). This results in a well-known imbalance in bargaining power which makes it challenging for farmers to negotiate on eye-level with other actors in the supply chain (Bonanno et al., 2018). In response to these imbalances, European farmers had long practised the establishment of cooperatives. Based on these experiences, the European Union's Common Agricultural Policy (CAP) has supported the establishment of producer organisations (POs) since 2001 (Michalek et al., 2018).

An important goal behind the establishment of POs in Europe was to directly respond to the necessity for collective bargaining in input and output markets (Bijman and Iliopoulos, 2014; Fałkowski and Ciaian, 2016).

POs help farmers to reduce transaction costs while enabling collaboration in processing and marketing (Bijman and Hanisch, 2012; Đurić et al., 2021). Examples of these benefits include farmers’ enhanced bargaining power due to pooling of quantities supplied, coordinated qualities, improved marketing and joint advertisement, provision of technical and logistical support, assisting with quality management, and facilitating knowledge transfer (Fałkowski and Ciaian, 2016; Hendrikse and Bijman, 2002; Hendrikse and Feng, 2013).

To further increase the number of POs and acknowledge their valuable contribution to economic and ecological sustainability, the CAP also strengthens the establishment and operation of POs within the framework of market structure support (European Commission, 2022): Many EU fruit and vegetable farms as well as dairy farms already organise the marketing of their produce typically via POs (European Commission, 2025). However, not all agricultural sectors have seen the same rise in the share of farmers who join a PO and their impact on agriculture is case-sensitive (Bijman, 2016; Chowdhury et al., 2024). This may indicate the rather difficult process of establishing POs, and the potential disadvantages that farmers may also encounter as part of a PO (Chowdhury et al., 2024).

For niche markets and emerging products or quality lines, such as grain legumes, these difficulties are especially evident (Dal Belo Leite et al., 2014). Historically, several niche crops have successfully transitioned into mainstream production when driven by strong demand forces; in parallel, well-coordinated value chains emerged quickly or provided support if already in place. For instance, rapeseed evolved from a marginal crop to a leading European oilseed after breeding advances improved its quality and policy support fostered biofuel markets (Carré and Pouzet, 2014), while spelt experienced a revival driven by consumer interest in traditional and health-oriented grains. This trend was supported by branding initiatives while on the supply side contract farming schemes evolved quickly (Alvarez, 2021; Cubadda and Marconi, 2002). In contrast, grain legumes lack a comparable consumer-driven demand and cannot rely on integrated supply chains, which may explain their relatively slow adoption despite well-known ecological benefits.

At the same time is the process of forming a PO a relatively under-researched field (European Commission, 2025; Hoehler and Kuehl, 2014). This is also evident in Germany, where, despite being a major producer of grain legumes (Eurostat, 2024), only a few farmer-owned POs explicitly specialise in their marketing (e.g., Rheinweiß Soja w.V. and EZG SO!JA). Instead, cooperative agricultural trade mainly focused on cereals, wine, milk, or fruit and vegetables, which are all products that play a dominant role in the agri-food chain (Deutscher Raiffeisenverband e.V. 2024; Greve, 2001; Kuehl, 2012).

Nevertheless, grain legumes are a vital crop group, offering protein-rich feed for animals and humans (Parveen et al., 2022; Watson et al., 2017) and contributing to sustainable farming systems. Their ability to biologically fix atmospheric nitrogen reduces the need for synthetic nitrogen fertilizers, thereby lowering input costs and greenhouse gas emissions (Barbieri et al., 2023). Additionally, grain legumes enhance soil fertility, improve crop rotation diversity, and can interrupt pest and disease cycles, contributing to more resilient and environmentally friendly farming practices (Stagnari et al., 2017; Watson et al., 2017).

Despite their ecological and agronomic benefits, the cultivation of grain legumes in Europe faces significant barriers (see Magrini et al. (2018) for an analysis of the lock-in situation of grain legumes in Europe). Among the most important are profitability gaps compared to established crops such as wheat or maize. On many farms, grain legume cultivation is only competitive because of targeted subsidies (Sponagel et al., 2021). Without these support payments, legume production would often be less attractive economically compared to cereals or maize, given the yield variability, price volatility, and relatively weak value chains (Mittag and Hess, 2022; Sponagel et al., 2021). This explains why grain legumes are often grown by livestock farms that use them directly as feed or by farms that seek to improve crop rotation for agronomic reasons rather than being motivated by pure market returns (van Loon et al., 2023; Zimmer and Böttcher, 2021). Unlike specialist arable farms, livestock farmers are less dependent on external markets and can integrate legumes into their production system at comparatively lower market risk. Additionally, organic farms represent another important group of grain legume growers, as legumes play a critical role in organic crop rotations because of their ability to add nitrogen to the farm's nutrient cycle. In order to make grain legumes more attractive for other farm types as well, governments have long sought to increase the cultivation of grain legumes due to their sustainability benefits (European Union, 2023; Zander et al., 2016), such as improving soil health and reducing reliance on imported protein sources (Pilorgé et al., 2021; Preissel et al., 2015; Reckling et al., 2020). However, despite these policy efforts, the area under grain legume cultivation remains low and volatile (Eurostat, 2024).

In this study, we focus on grain legumes commonly cultivated in Germany for feed and food purposes, specifically field peas, faba beans, soy beans and lupins. While these crops may differ in end uses, they share similar agronomic characteristics and face comparable challenges in terms of value chain organisation, price fluctuations, and market access (Mittag and Hess, 2022; Soisontes et al., 2023). These challenges combined with the fragmented and niche nature of grain legume markets (Kezeya Sepngang et al., 2018; Mittag and Hess, 2022) often result in difficulties for individual farmers to achieve stable and profitable production at the farm level(Sponagel et al., 2021; Zimmer and Böttcher, 2021).

This raises the critical question of whether POs could enhance the attractiveness of grain legume cultivation and, if so, why they have not yet emerged in this sector. Understanding the economic and social barriers to forming POs for grain legumes is essential for addressing this knowledge gap.

Therefore, this paper focuses on grain legume production in Germany, one of the leading producers of these crops in the European Union (Eurostat, 2024). We aim to address the following research questions:

RQ1: What factors influence farmers’ willingness to market their grain legumes through a PO?

RQ2: How should such a PO be structured to effectively support farmers and enhance the viability of grain legume cultivation?

By examining these questions, this study seeks to clarify the potential role of POs in overcoming market fragmentation and supporting the economic and environmental sustainability of grain legume production. By focusing on the case of grain legume production in Germany, this study provides novel insights into the institutional and economic challenges of organising producer cooperation in a fragmented and niche market. It contributes to the academic discourse by shedding light on why established policy instruments, such as POs, have so far failed to take root in this sector ‒ despite the clear ecological and political will to promote it.

The research design combines primary data collection through a structured survey of grain legume farmers in Germany with the estimation of a structural ordered probit model. The model is used to identify the effect of farmer-specific characteristics, perceptions, and structural farm features on their willingness to market grain legumes through a POs. The survey was conducted in-person at a trade fair in June 2024 and targeted both conventional and organic farmers across different regions, resulting in a diverse sample. Through its empirical analysis and conceptual framing, the paper advances the understanding of how market organisation can support more resilient and sustainable value chains for protein crops in Germany and potentially other European contexts.

Structural model

We assume that a farmer, as part of a regional sample of i = 1,…,N farmers, has a limited land endowment

Grain legumes often lack well-functioning domestic markets, and therefore the price that farmers receive is determined by broader on-farm and marketing conditions rather than by a single, homogeneous market-clearing price. We model the farm-gate price as:

The competitiveness of grain legumes relative to alternative crops for i = 1,…,N farm locations, in turn, is determined by the value of the marginal product:

The value of the marginal product describes, as one part, the physical marginal productivity of grain legumes at each location. This is the first derivative of the production function

Secondly, the value of the marginal product links marginal physical productivity

Thus, the profitability of grain legumes

Within our analytical framework, the profitability of grain legumes relative to alternative crops is represented as:

We capture the opportunity cost of land use through the profit gap relative to alternative crops:

This profit gap influences the incentive to adopt grain legumes and to join a producer organisation. If

We hypothesise that membership in a PO may lower farm-specific marketing costs by reducing/improving the price determining components, thereby increasing the price received, enhancing profitability and hence competitiveness of grain legume production.

Hence, the farmer's expected profit from marketing via a PO versus non-membership is:

Here,

To capture intertemporal preferences, we define the net present value (NPV) of expected profits over a planning horizon T:

The latent utility difference for farmer i is:

We define the latent preference for PO membership as:

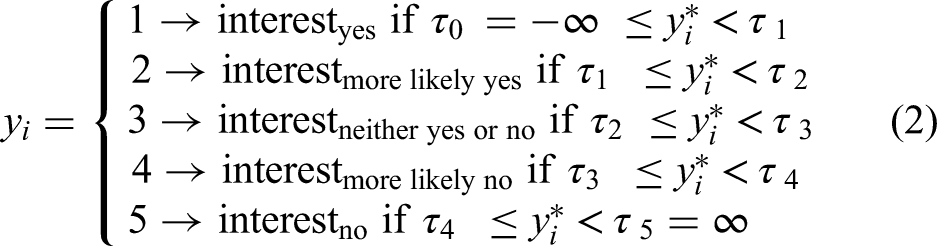

The observed outcome, however, is not binary. Instead, it will be measured on an ordinal scale that indicates the farmer's level of interest in selling through a PO, ranging from 1 (very interested) to 5 (not interested). Therefore, we model the observed ordinal decision for a POi using an ordered choice model described in the next section.

This structural framework allows us to link theoretical profitability considerations to observable stated preferences for PO membership and to identify key drivers influencing farmers’ willingness to participate in collective marketing schemes.

Data and methods

We use primary data collected through a farmer survey conducted at the DLG-Feldtage agricultural trade fair in Germany in June 2024. Farmers were approached directly on-site and invited to participate, which helped reduce self-selection bias commonly associated with online surveys and ensured a more diverse pool of respondents. Due to data protection regulations, a complete list of the target population was not available. The trade fair was chosen as the survey location because it attracts a broad cross-section of German farmers, including both conventional and organic producers, as well as farmers with and without prior experience in grain legume cultivation.

However, it must be acknowledged that farmers attending such events are not representative of the general German farming population. Participants are likely to be more innovation-oriented, better connected, and more open to new production systems or cooperative approaches. This introduces a potential source of sampling bias, particularly with regard to farmers’ openness toward joining a PO. As a result, the findings may overestimate the general willingness to participate in collective marketing initiatives. Similar challenges in farmer survey recruitment and sampling bias have been discussed in Mergenthaler et al. (2025), which highlights the importance of survey context and access strategies for data quality and generalisability. Against this backdrop, the results should be interpreted as indicative of relevant patterns and motivations rather than statistically representative of the broader farming population in Germany.

We created a questionnaire that asked primarily about the farmers’ interest in selling the grain legumes they grow at their farms through a PO. Additionally, farmers had to state which advantages and disadvantages this would have from the perspective of their farms. Demographic and farm-specific characteristics were asked as well. After a pre-test of the questionnaire with five farmers, slight modifications have been made to the language and wording. The final questionnaire was answered by 120 farmers, of which 119 completed questionnaires remained after data cleaning.

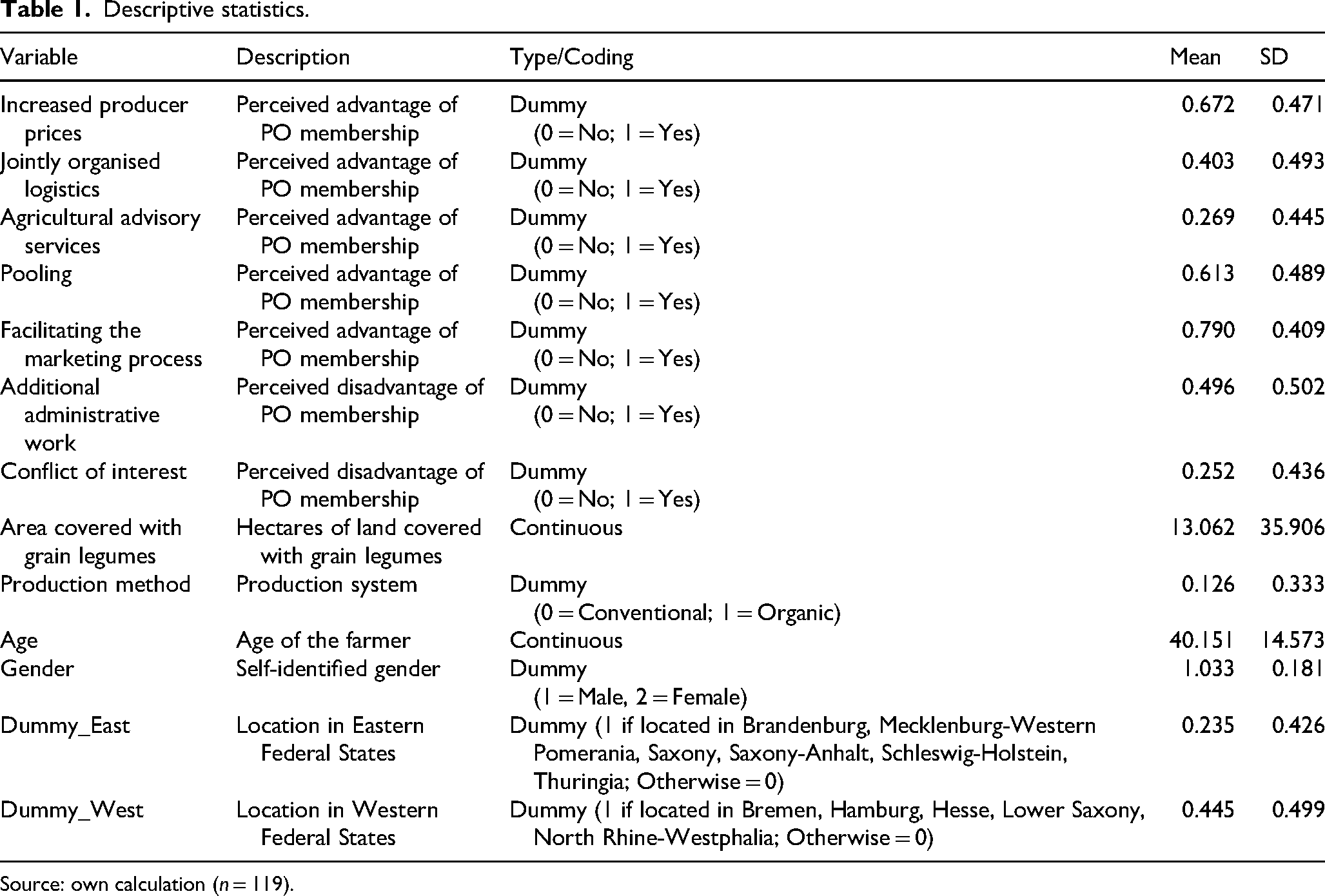

Table 1 provides the descriptive statistics of the variables used in the analysis, including farmers’ perceptions of advantages and disadvantages of PO membership, as well as socio-demographic and farm-specific characteristics.

Descriptive statistics.

Source: own calculation (n = 119).

Initially, the list of advantages and disadvantages was longer, but due to multicollinearity and high correlation, some variables had to be dropped before the final model estimation. We assessed multicollinearity using pairwise correlation matrices and Variance Inflation Factors (VIFs). Variables with high pairwise correlation (ρ > 0.75) and VIF values above conventional thresholds (VIF > 5) were reviewed. Among those, we retained variables that either had a clearer theoretical grounding or showed more substantial variation in the responses. We dropped those that were either highly redundant or conceptually overlapping, such as ‘General Market Information’, which was highly correlated with ‘Agricultural Advisory Services’.

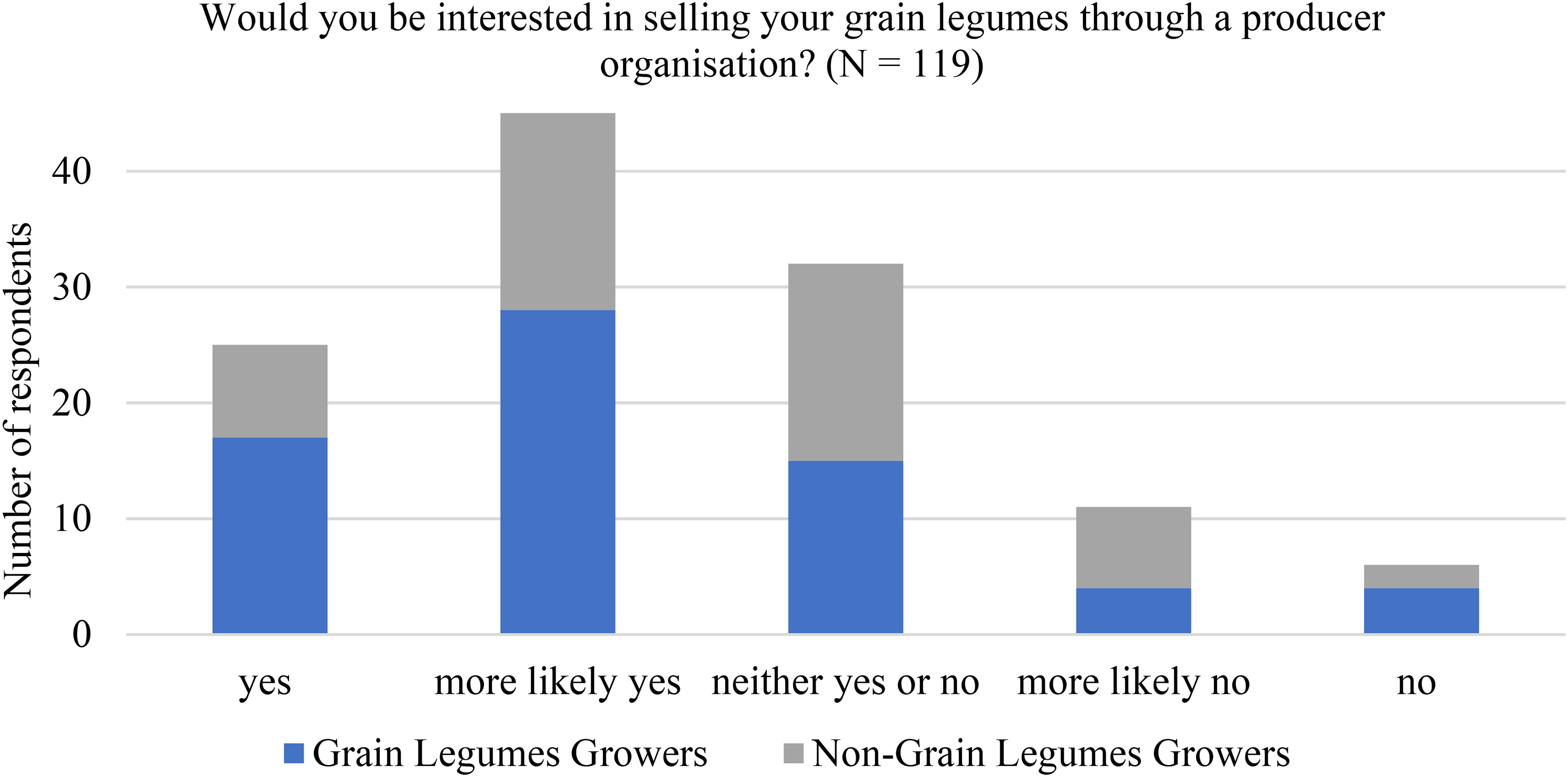

Figure 1 shows the distribution of the dependent variable ‘Would you be interested in selling your grain legumes through a producer organisation?’. It was answered on a 1–5 Likert scale, where each number represents a distinct level of interest.

Distribution of the dependent variable.

Furthermore, the graph indicates that there is only little distinction between the interest levels of farmers who currently cultivate legumes and those who do not. This is supported by the Mann‒Whitney U-test, which yields a p-value of .731 at a 5% significance level.

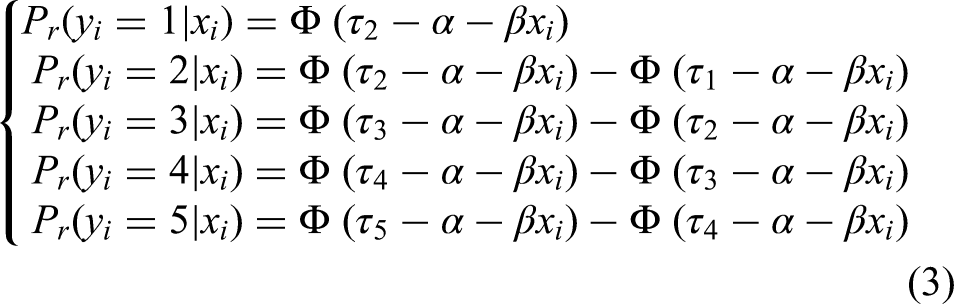

The literature employs ordered logit and ordered probit models to analyse such ordinal data. The choice between the two models largely depends on convenience and the model most commonly applied in the respective field of research (Long and Freese, 2006). This study utilises the ordered probit model due to its broader applicability in analysing the ordinal characteristics of the dependent variable. The ordered probit model is appropriate in this context, as it accounts for the ranked nature of responses without assuming equal intervals between categories (Long and Freese, 2006). Hence, the ordered probit model allows us to examine how covariates influence both the direction and thresholds of farmers’ ordinal responses.

Following Long and Freese (2006) and Greene (2010), the model is specified as:

The observed y is related to

The model parameters specified in equation (3) are estimated using the maximum likelihood method. Nevertheless, the model's coefficient interpretation is not entirely clear: Neither the sign nor the magnitude of the estimated coefficients receives a direct interpretation.

For instance, the dependent variable comprises five categories, whereas the model incorporates a single unknown threshold parameter (Greene, 2010). This necessitates the partial change or marginal effect, which can reveal the effects of independent variables on the probability of five distinct levels of interest in selling grain legumes through a PO, each considered individually. A partial change is observed in the predicted probability of the outcome m for a continuous variable, within the interval

Furthermore, the change in the predicted probability for a discrete change in

The questionnaire also asked for the characteristics and the structure of an ideal PO from the perspective of the respondents. These characteristics, such as ‘regional’, ‘small number of members’, or ‘individual contracts’, were stated using a semantic differential. Respondents were then asked to rate the characteristics of the PO on a series of bipolar adjective pairs using a five-point numerical scale. The analysis of the survey results in this respect will be represented descriptively via a bipolar profile diagram contrasting different characteristics of a PO. Due to the small sample size, additional short telephone interviews were conducted with members of already established POs for other crops (e.g., rapeseed, spelt) to triangulate the results. These interviews were used to validate the respondents’ assessments of the potential role of POs for grain legumes.

Results

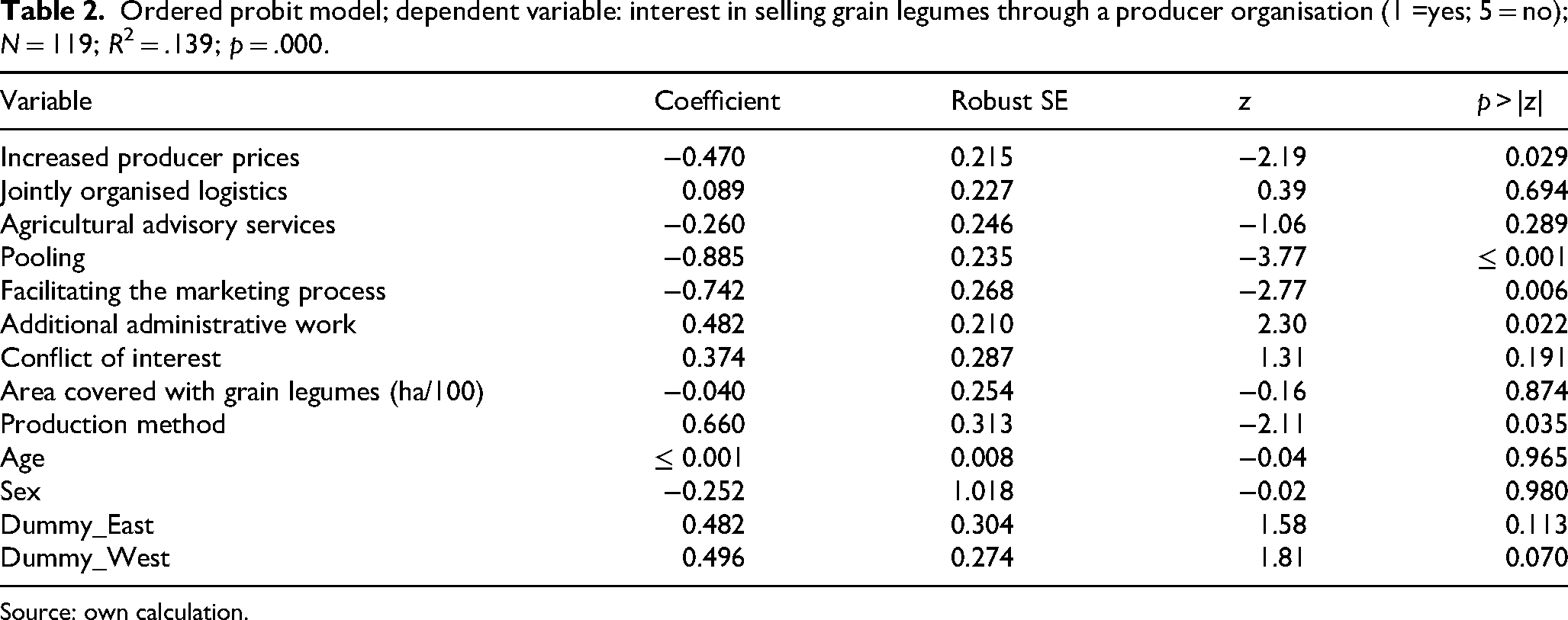

The estimation strategy outlined was used to analyse the determinants of interest in selling grain legumes through a PO. The results of the final ordered probit model are shown in Table 2.

Ordered probit model; dependent variable: interest in selling grain legumes through a producer organisation (1 =yes; 5 = no); N = 119; R2 = .139; p = .000.

Source: own calculation.

A farmer's interest in selling grain legumes through a PO significantly depends on the perceived advantages, such as the POs's ability to pool the production volumes or higher producer prices. In terms of perceived disadvantages, farmers are particularly concerned about the additional administrative work involved in joining a PO.

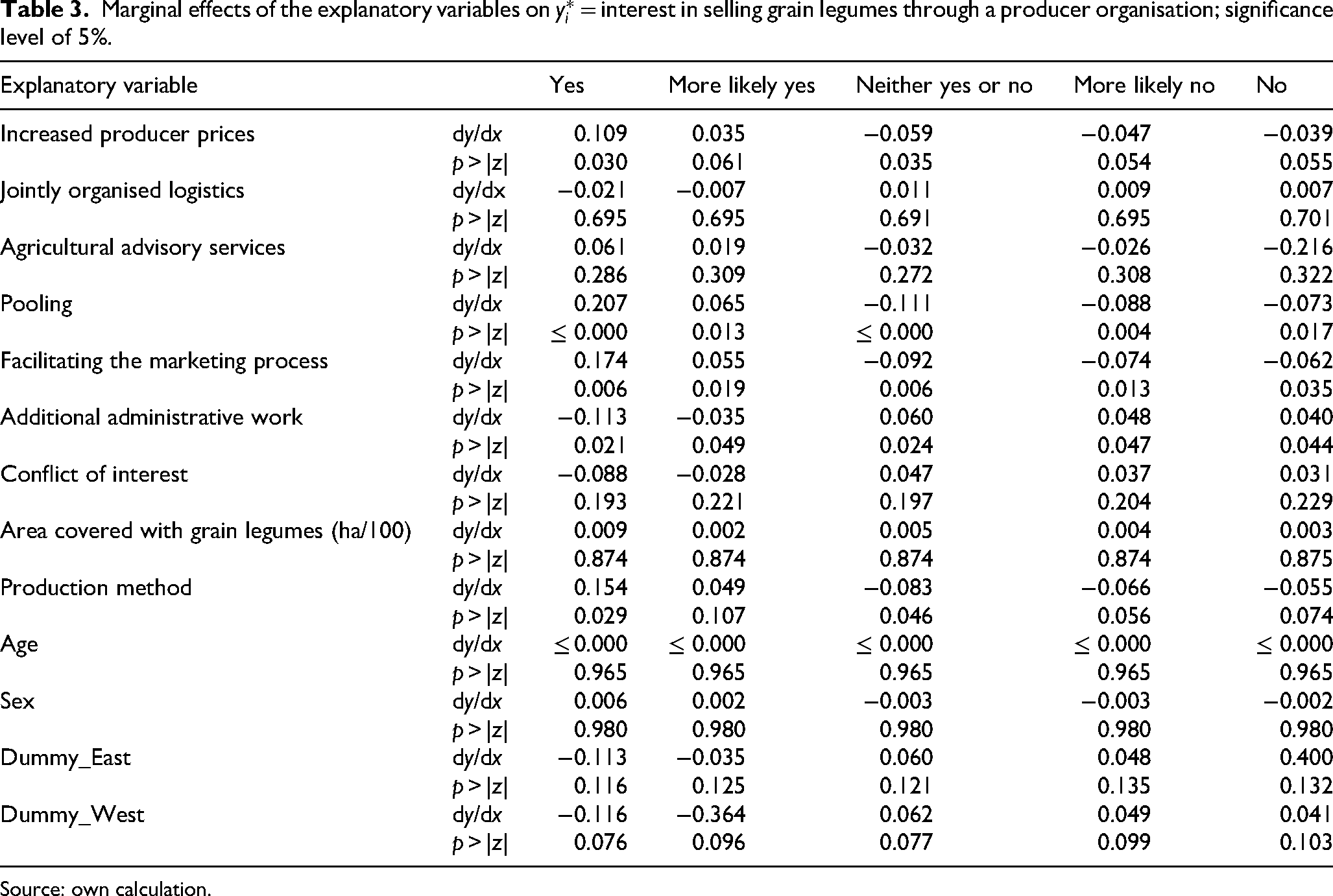

Table 3 shows the estimated marginal effects of the explanatory variables on the farmers’ interest in selling their grain legumes via a PO (see previous section). The marginal effects derived from the ordered probit model provide detailed insights into how various perceived advantages and disadvantages influence farmers’ willingness to market grain legumes through a PO.

Marginal effects of the explanatory variables on

Source: own calculation.

Perceived benefits play a significant role in shaping farmers’ attitudes. Most notably, the perception of pooling advantages substantially increases the probability of strong agreement with collective marketing. Specifically, farmers who view pooling as beneficial are, on average, 20.7 percentage points more likely to respond with ‘Yes’ (p ≤ .001). Similarly, facilitating the marketing process increases the likelihood of a positive response by 17.4 percentage points (p = .006). The expectation of higher producer prices is also positively associated with agreement, increasing the probability of full agreement by 10.9 percentage points (p = .030). In addition, farmers’ production method (e.g., organic vs. conventional) appears to be a relevant determinant, with a statistically significant and positive marginal effect of 15.4 percentage points (p = .029) on full agreement.

In contrast, certain perceived disadvantages act as barriers. The perception of additional administrative burden significantly reduces the likelihood of full agreement by 11.3 percentage points (p = .021) and increases the probability of more neutral or negative responses. Although the perception of conflicts of interest has a negative sign, the effects are not statistically significant across any response category (p > .1).

Other variables such as jointly organised logistics, agricultural advisory services, and the area under legume cultivation show no statistically significant association with farmers’ marketing preferences. Likewise, age, gender, and regional location (East/West Germany) do not have a meaningful influence, except a weakly significant effect for the West dummy in isolated response categories (p ≈ .07–.10).

While the analysis primarily highlights the marginal effects for the extreme response categories (‘Yes’ and ‘No’), it is important also to consider how the explanatory variables influence the intermediate levels of agreement. The categories ‘More likely yes’, ‘Neither yes nor no’, and ‘More likely no’ provide additional nuance in understanding farmers’ marketing preferences. For instance, the perceived benefits of pooling and facilitating marketing not only significantly increase the likelihood of selecting ‘Yes’, but also significantly reduce the probabilities of selecting more hesitant categories such as ‘Neither yes nor no’ and ‘More likely no’ (e.g., pooling: dy/dx = −0.111, p ≤ .001 for ‘Neutral’; dy/dx = −0.088, p = .004 for ‘More likely no’). This indicates that these benefits play a decisive role in shifting attitudes from indecision or mild opposition toward a strong preference for collective marketing.

Conversely, the perception of additional administrative burden increases the likelihood of neutral and negative intermediate responses (e.g., dy/dx = + 0.060, p = .024 for ‘Neither yes nor no’), while reducing the probability of ‘Yes’. Notably, for several variables such as logistics, advisory services, and conflict of interest, the marginal effects across all five categories are statistically insignificant and symmetrically distributed around zero. This suggests that these factors do not systematically push respondents in either direction on the agreement scale.

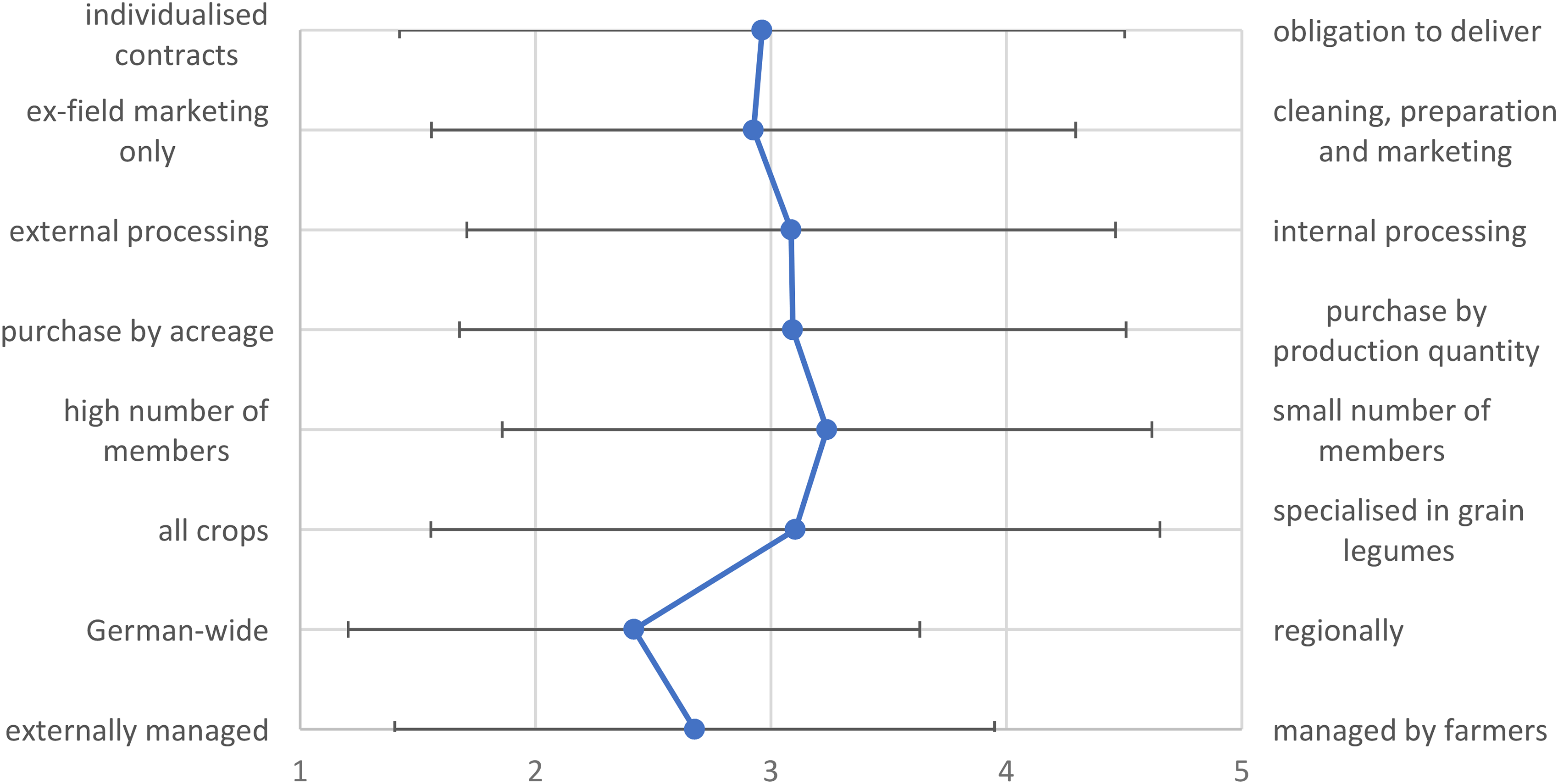

To answer the second research question about the structure and characteristics of the desired PO, we visualised the answers in Figure 2. It presents a bipolar profile diagram contrasting characteristics of a PO for grain legumes. It indicates the tendency toward either pole (e.g., ‘externally managed’ vs. ‘managed by farmers’), while values range from 1 = strong preference for the left-hand option to 5 = strong preference for the right-hand option, with 3 = neutral. Each row represents a different attribute (e.g., scale, management style, product scope), with endpoints showing opposing approaches (left vs. right). The scale indicates the degree of alignment with either model, where intermediate values highlight the spectrum between two idealised strategies. Attributes range from operational features (e.g., ‘external processing’ vs. ‘internal processing’) to structural traits (e.g., ‘high number of members’ vs. ‘small number of members’).

Semantic differential of the PO; blue dots = mean, black lines = standard deviation; 1 = strong preference for the left-hand option, 5 = strong preference for the right-hand option, 3 = neutral; N = 119.

In general, it can be seen that there is a strong tendency towards the mean for all bipolar adjective pairs, whereby the standard deviations are also very high for all pairs. No clear tendencies concerning specific characteristics of the PO can, therefore, be derived from the averaged responses of all respondents in the sample.

To complement these inconclusive survey results, additional short telephone interviews were conducted with members of existing POs for other crops, such as rapeseed and spelt. These interviews offered further insights into farmers’ motivations and expectations regarding POs. Participants highlighted that they mainly joined the PO to strengthen their market position and to benefit from collective bargaining power. Also, shared logistics and knowledge exchange were drivers to join. They particularly valued services like joint marketing activities and transparent pricing structures, although some respondents pointed to bureaucratic processes and slow decision-making as potential downsides of PO membership. Challenges that were raised included balancing individual flexibility with collective rules and ensuring fair benefit distribution among members. Looking ahead, interviewees suggested that POs should be farmer-led but professionally supported, small enough to foster trust and cohesion, yet large enough to maintain market relevance. Greater flexibility in membership conditions and more customised services were seen as ways to make participation more appealing to other farmers.

Discussion

The production of grain legumes in Germany represents a niche market with a rather challenging and fragmented market structure. Production volumes per farm are comparatively small, and traders are usually not interested in small lots (Kezeya Sepngang et al., 2018; Soisontes et al., 2023). The joint marketing of grain legumes seems obvious as farmers can increase their bargaining position and present a more concentrated reaction to market volatility and pressure.

Based on a heterogeneous sample of 119 farmers from all over Germany, we used an ordered probit model to identify potential factors in the farmers’ interest in selling grain legumes through a PO. Marginal effects from the estimated model reveal that farmers’ interest in the PO increases by about 20% if they perceive the core objective of a PO as to their advantage. Farmers generally see the PO as a pooling organisation to facilitate marketing, which goes hand in hand with higher producer prices compared to individual marketing. This is in line with Hendrikse and Bijman (2002). Additional services like agricultural advisory services or joint logistics do not significantly increase the farmers’ interest. This confirms the findings of Verma et al. (2019) and Ragunath et al. (2023), who state that these services of a PO are not the main reason for joining a PO but are nevertheless favourably received by farmers.

The connection between the perceived advantages and disadvantages of POs and the influencing factors of our structural model can be outlined as follows: Increased producer prices and factors that are facilitating the marketing process are directly linked to the general market price (p), which benefits from improved demand and efficient marketing of POs. Pooling and jointly organised logistics enhance market access (m) by enabling larger, more uniform lots and streamlined supply chains. Transportation costs (k) are addressed through jointly organised logistics, reducing expenses and logistical challenges. Lastly, the bargaining situation (c) is improved through collective action, reflected in increased producer prices, though challenges like conflict of interests may arise within the organisation. This linkage highlights the mechanisms by which POs influence economic outcomes for farmers.

Therefore, if farmers experience the identified advantages through the PO, the farm-specific marketing costs

Regarding the disadvantages of being a PO member, farmers fear additional administrative work, whereas conflicts of interest with other farmers are not a concern. Due to the high burden of bureaucracy, German farmers have to deal with (El Benni et al., 2022), the PO should minimise it as much as possible and assist. To achieve this, the PO could centralise administrative tasks, provide simplified documentation methods, and utilise digital platforms for efficient management. By assuming these administrative responsibilities, the PO could allow farmers to concentrate on their production while still benefiting from organised cooperation. Consequently, this may enhance the PO's appeal, making membership more preferable to non-membership (see structural model).

In terms of farm-specific characteristics, the interest in joining a PO does not depend on the farms’ acreage of grain legumes. Both small-scale and large-scale grain legume growers are interested in selling their grain legumes through a PO. This somewhat contradicts Davidova and Thomson (2014) who state, that mainly smaller farms join together to form co-operatives in order to improve their market position. One potential explanation lies in the sampling context of this study: the survey was conducted at a major agricultural trade fair, which may have attracted a more innovative and market-oriented subset of farmers. This could lead to a sample in which even larger-scale producers are open to collective marketing solutions, thereby attenuating the expected effect of farm size on PO interest. Nevertheless, the finding is in line with Fałkowski and Chlebicka (2021) and Fałkowski and Ciaian (2016) who suggest that larger farms may also engage in collective arrangements to diversify sales channels and enhance economic resilience. In the niche market of grain legumes, both small and large farmers in Germany face similar challenges ‒ such as price volatility, fluctuating demand, and fragmented market structures ‒ which make the benefits of POs relevant across farm sizes. Unlike in more established sectors, the need for collective action is more universal. Small farms may seek logistical and knowledge support, while larger farms aim to strengthen their bargaining power. Thus, in this context, farm size plays a less decisive role in the willingness to join a PO than suggested by findings from other agricultural sectors.

In addition to the ordered probit model, we asked for the farmers’ desired structure of a PO. Results in this respect may reflect the effects of averaging responses across all participants, potentially obscuring differences within subgroups. It is, therefore, worth considering whether distinct groups or clusters exist among the respondents that may exhibit specific patterns or tendencies, which may indicate the farmers’ indecisiveness or unknowingness regarding the specialities of a PO. Several private and public initiatives try to encourage farmers to increase the share of grain legumes in their crop rotation, among others by setting up a PO. Namely, Legunet (2024) actively promotes both agronomic and ecological advantages of grain legume production in Germany and has published guidelines for establishing a PO. By doing so, Legunet offers extension and advisory services to overcome potential knowledge gaps and information barriers.

Our study's sample size of 119 farmers requires critical evaluation regarding representativeness and the application of an ordered probit model. The sample for our study, collected during a national trade fair attended by farmers from across Germany, aims to reflect the country's primary agricultural production structure. This approach ensures a geographically diverse representation, capturing variations in farm size and the proportional distribution of specialised crop producers, specialised livestock farms, and mixed operations. Additionally, the sample accounts for the balance between conventional and organic farming practices, which are notably heterogeneous across different regions. Despite the use of sampling on site, there remains a risk that specific groups of farmers are over- or underrepresented, for example, those who are more likely to attend trade fairs or are more open to innovation and research participation. As such, the resulting sample may not be fully representative of the overall population of German farmers.

The ordered probit model's application to a sample of 119 observations offered valuable insights, mainly due to the ordinal nature of our dependent variable. However, we must acknowledge some methodological restrictions based on our relatively small sample size. Maximum likelihood estimation, commonly used in ordered probit models, can yield less precise parameter estimates in small samples, potentially increasing standard errors and reducing statistical power (Long and Freese, 2006). While a sample size of 119 is modest, it is not uncommon in fields where data collection is resource-intensive or restricted by practical constraints (Williams, 2006). Despite the limitations of small sample sizes, the ordered probit model remains a robust choice for analysing ordinal outcomes, particularly when applied thoughtfully. Its strengths in capturing the structure of ordinal data justify its application here, provided that the results are interpreted with due consideration of the sample size.

Future research should explore the potential clustering of farmers with distinct preferences for PO characteristics to better tailor PO models to the needs of different subgroups. Moreover, expanding the sample size and exploring the perspectives of a broader range of stakeholders would provide a more comprehensive understanding of the drivers of PO participation.

Conclusion

Producer Organisations have a high potential to increase the attractiveness of grain legume cultivation due to their ability to mitigate the economic, social, and logistical constraints that farmers commonly face. Notwithstanding this fact, in Germany - a major producer of grain legumes - there are only a few farmer-owned POs explicitly specialising in marketing of these crops, despite the strong presence of cooperative agricultural trade in the agri-food chain. We asked for factors influencing farmers’ willingness to market their grain legumes through a PO. The findings of this study highlight that farmer interest in selling grain legumes through a PO is significantly shaped by perceived advantages such as increased producer prices and the ability to pool production volumes. Farmers are motivated by the potential to strengthen their bargaining power and improve the marketing in grain legume markets.

A major barrier to participation is the concern over additional administrative burdens, which must be mitigated to increase PO membership. The results also suggest that both small-scale and large grain legume growers express interest in POs, challenging the conventional view that only small-scale farms seek collective action for better market positioning. This finding underscores the evolving role of POs as a strategy for smaller and larger agricultural enterprises seeking to diversify their sales channels and strengthen their market presence. From a policy perspective, reducing the administrative complexity and bureaucratic burden associated with POs is crucial. Supporting POs with streamlined processes, digital tools, and adequate administrative support could encourage broader participation. Given the heterogeneity in farmer preferences regarding PO structure, policymakers should consider fostering diverse POs, accommodating different farm sizes and production systems. Furthermore, as the grain legume sector in Germany is still rather a niche, efforts to raise awareness about the agronomic and ecological benefits of grain legumes should be supported through networks like Legunet, which promote cultivation, processing and market integration of these crops.

In conclusion, POs can play a vital role in improving the economic viability of grain legume production in Germany. Their success, however, depends not only on addressing the perceived (dis)advantages of membership, reducing administrative burdens, and promoting the benefits of collective action but also on enhancing market demand and awareness among buyers, thereby contributing to closing existing profit gaps relative to alternative crops.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

The datasets generated and analysed during the current study are available from the corresponding author on reasonable request.