Abstract

Human activities are responsible for emitting greenhouse gases (GHGs) that contribute to global warming and climate change. As the world's second-largest producer of staple food and the third-largest emitter of GHGs, India has been witnessing an increase in demand for food and energy, resulting in increased emissions. Thus, to achieve net carbon neutrality by 2070, India must focus urgently on climate change mitigation. Its agriculture sector has the potential to transition from being a net emitter to a net absorber of GHGs by adopting sustainable farming practices such as zero tillage, laser-assisted precision land leveling, direct seeding of rice, intercropping, biochar application, use of solar energy, and more efficient management of irrigation water, soil nutrients, livestock feed, and manure. To incentivize climate consciousness, a voluntary carbon credit trading system could be utilized in agriculture, supported by a measurement, monitoring, reporting, and verification platform. This system would also bring about social, environmental, and financial co-benefits for its stakeholders. Specifically, the agriculture sector could substantially reduce the country's annual emissions by 84% from 2019 to 2070. But to realize their potential, the carbon markets must overcome the limitations currently set by policy, economic, cultural, and biophysical factors.

Keywords

Introduction

Increased emissions of greenhouse gases (GHGs) due to anthropogenic activities result in global warming and climate change (UNFCCC, 2022a). Between 1990 and 2019, worldwide annual GHG emissions were ∼ 42 gigatons of carbon dioxide equivalent (GtCO2e), primarily from fossil fuel-based energy plants, transportation, and agriculture (Ritchie and Roser, 2022). About two-thirds of the world's GHG emissions were contributed by 10 countries: China, the United States of America (USA), India, the European Union (EU), Russia, Japan, Brazil, Indonesia, Iran, and Canada (Friedrich et al., 2023; Ritchie and Roser, 2022). While the per capita emissions of developing countries like India (2.77 tCO2e), Brazil (10.03 tCO2e), Indonesia (7.49 tCO2e), and Iran (11.42 tCO2e) were significantly lower than countries in the Global North (an average of 14.21 tCO2e in 2021) (Jones et al., 2023; Ritchie et al., 2023), there has been a surge in emissions from the Global South during recent years (Ritchie et al., 2020).

The dual challenges of climate change and poverty in developing countries can be addressed by transforming domestic agrifood systems. The world's agrifood systems are responsible for feeding a global population of 8.1 billion, of which nearly half of the poor live in middle-income countries, particularly China and India (Mahler et al., 2023; World Economic Forum, 2022). On the one hand, the temperature variations caused by climate change damage the natural and physical resource base and result in increased incidences of disease, unpredictable declines in crop yields, reduced biodiversity, and higher energy demands (Dellink et al., 2019). On the other hand, GHG emissions resulting from the overuse of synthetic fertilizers, livestock production, inefficient water management, deforestation, and food loss and waste, among other practices, contribute largely to climate change (Pathak et al., 2014). As the global population rises, the pressure on agriculture to produce more food using existing resources will increase, and the production process will emit even more GHGs, exacerbating the pace of climate change (Anders and Lokuge, 2022). It is imperative to implement measures to reduce GHG emissions; however, these measures should not compromise system vulnerability or hinder productivity.

Against this context, various technologies, policies, and market mechanisms are being developed to promote sustainable agriculture (Buck and Compton, 2022; Giller et al., 2021). Under the 2015 Paris Agreement, several mitigation and adaptation measures were proposed for agriculture to facilitate carbon sequestration and trade in the carbon market (Rose et al., 2022). However, spreading climate resilience measures among smallholder farmers, who face liquidity constraints and lack access to information, has remained a major challenge for the agricultural Research and Development (R&D) agencies and governments of the Global South (Rapsomanikis, 2015).

Linking carbon markets to farm production and incentivizing emission reduction with the help of tradable carbon credits are lauded as win-win strategies (World Bank, 2023a). For instance, agricultural carbon markets can facilitate the adoption of sustainable agricultural practices (SAPs) such as conservation agriculture, reduced burning of crop residues, organic farming, livestock feed management, and agroforestry. These practices have the potential to sequester carbon in soil and reverse ecosystem degradation before the climate tipping point is reached (Amundson and Biardeau, 2018; Ginkel et al., 2020; United Nations Environment Program, 2020). Private entities (corporations or individuals from the developed world) could buy carbon credits from the voluntary carbon market (VCM) to offset their emissions (Seeberg-Elverfeld, 2010). A share of the revenue generated from the sale of carbon credits could be shared with the farmers, thereby improving their financial status (Jindal et al., 2007). In short, agricultural carbon markets could improve agricultural productivity, food, and income security (United Nations Environment Program, 2020), while facilitating the overall attainment of carbon neutrality.

Carbon markets and the application of carbon credits to spreading SAPs are in the nascent stage (Anders and Lokuge, 2022). Nevertheless, they have already gained significant attention in research and policy arenas. Several informative industry reports explain the concept, evolution, and status of carbon markets at the global scale (Ecosystem Marketplace, 2022a; Food and Agriculture Organization, 2010; South Pole, 2022). However, most existing studies have been geographically skewed, focusing predominantly on developed regions (Buck and Compton, 2022) and leaving the unique opportunities and challenges of the Global South underexplored. Furthermore, there remains a notable dearth of comprehensive research specifically addressing the integration of carbon markets into the agricultural sector of developing countries. Given the significant role that agriculture plays in the Global South, coupled with its vulnerability to the effects of climate change, the need to understand how carbon markets can be effectively leveraged against the specific policy environment of a given country is imperative. Understanding this research gap, we attempt to answer the following research questions: (a) Can carbon credits be generated in Indian agriculture with the help of regenerative agriculture? If yes, then what is the procedure for doing this, and who would participate? (b) What are the possible opportunities and challenges? By answering these questions, we aim to provide a perspective on carbon farming as a solution for combating GHG emissions and generating carbon credits in the agriculture sector of rapidly developing economies such as India. Only a few studies (e.g. Kumara et al., 2023) make a linkage between SAPs and climate change mitigation through participation in carbon markets.

In the rest of this article, we trace the evolution and current state of carbon credit markets and their relevance in the context of SAPs and carbon sequestration, alongside their co-benefits and limitations. In addition, the stakeholders of a carbon farming system and the process of carbon crediting in agriculture are also discussed. Finally, specific emphasis is laid on the role of Indian agriculture in climate change mitigation in terms of its opportunities and challenges.

Evolution of carbon markets and credits

The concept of carbon markets was introduced by the United Nations Framework Convention on Climate Change (UNFCCC) through the Kyoto Protocol (1997) and included mechanisms such as the Clean Development Mechanism (CDM), Joint Implementation (JI), and the International Emissions Trading System (ETS) (Sarkar and Dash, 2011; Sydney et al., 2019). After 2012, because concerns emerged regarding the limited scalability of the mechanisms, an international VCM was introduced in the Paris Agreement (Kossoy and Guigon, 2012; UNFCCC, 2023a) This was intended to address the limitations of the earlier mechanisms and adapt to the evolving landscape of climate action, and the evolution underscores the adaptability and resilience of the VCM as a vital tool in addressing climate change (Ahonen et al., 2022). Projections suggest that carbon markets may facilitate transactions ranging between US$5 and 50 billion by 2030 (Blaufelder et al., 2021). Specifically, the size of the VCM is expected to increase at a compounded annual growth rate of 35%, reaching at least US$15 billion by 2030 (Alexander, 2023). However, the realization of these estimates depends on a complex interplay of factors including evolving policies and market conditions.

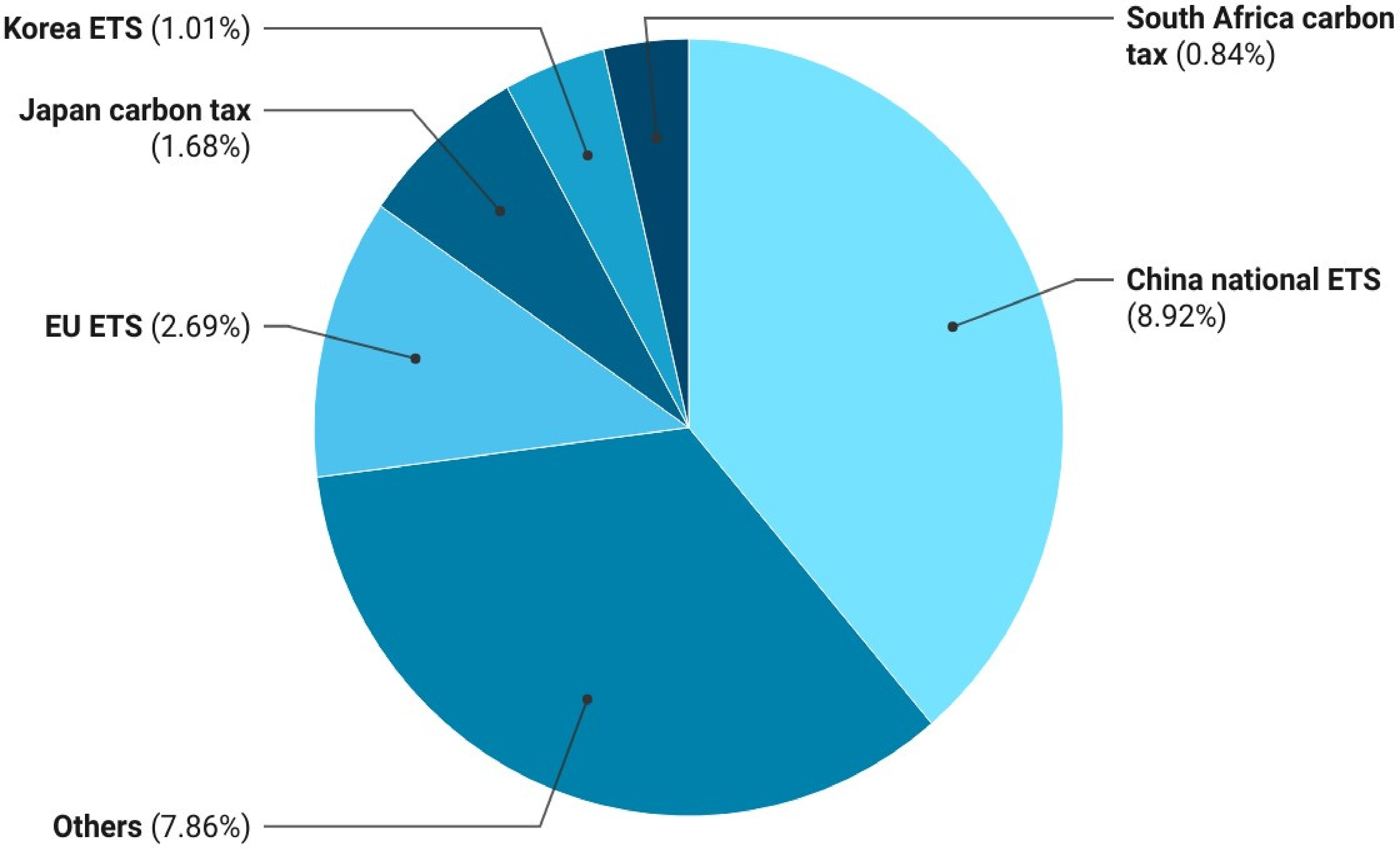

There are two distinct categories of carbon markets: compliance markets and voluntary markets. Compliance carbon markets, established following the Paris Agreement, are mandated and regulated by governments or international organizations. These markets require companies either to achieve prescribed emission reduction targets or acquire carbon credits to offset their emissions (Anders and Lokuge, 2022; Marchant et al., 2022). Regulatory tools, such as carbon taxes, and market-based mechanisms such as cap and trade, offer avenues for emission reduction at the international, national, and regional levels. The introduction of carbon taxes dates back to 1990 when Finland implemented this approach (Dorst, 2021). Following suit, numerous market-based carbon pricing mechanisms were established under the Kyoto Protocol, including the EU ETS and the Regional Greenhouse Gas Initiative (RGGI) (Marchant et al., 2022). As of 2023, 73 initiatives, collectively covering 23% of global GHG emissions (equivalent to 11.66 GtCO2e), have implemented the ETS or carbon taxes (World Bank, 2023b). Among these, China's ETS holds the largest share (8.92%) (Figure 1).

Share of greenhouse gas (GHG) emissions covered by different carbon tax and emissions trading systems (ETS). Source: Compiled from World Bank (2023b).

VCMs contrast with compliance markets, as they involve private entities who volunteer to either offset their carbon emissions or support sustainability objectives without government mandates (Mendelsohn et al., 2021). Voluntarily traded carbon credits are primarily used to fund Reduced Emissions from Deforestation and Environmental Degradation (REDD) projects in developing countries, along with carbon sequestration/removal initiatives encompassing agriculture, renewable energy, waste management, and more (Blaufelder et al., 2021; Mendelsohn et al., 2021). VCMs may contribute to emission mitigation projects that yield supplementary environmental and social benefits, including community development, women's empowerment, and biodiversity conservation. Irrespective of these benefits, such projects must substantiate their tangible and quantifiable contributions to emission reduction (Blaufelder et al., 2021).

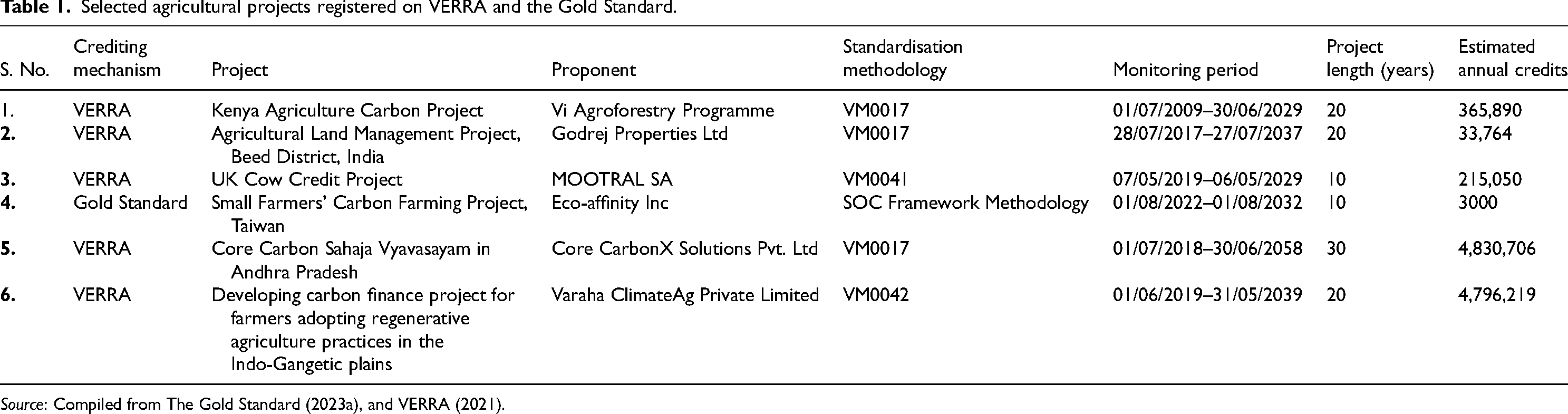

Agricultural carbon credits are actively traded within the framework of VCMs. They adhere to standardized protocols and are issued by carbon crediting mechanisms rooted in Payment for Ecosystem Services (PES) models. The traded credits can incentivize the use of SAPs for carbon storage and removal (Ecosystem Marketplace, 2022a; Food and Agriculture Organization, 2010). Table 1 displays some examples of carbon farming projects.

Selected agricultural projects registered on VERRA and the Gold Standard.

Source: Compiled from The Gold Standard (2023a), and VERRA (2021).

The establishment of a regulatory mechanism for VCMs is imperative to eliminate the possibility of greenwashing, double counting, or leakage of carbon credits. It would ensure the standardized quality of carbon credits, market credibility, and buyer confidence (Ziegler, 2023). Further, it would check for overinflated emission baselines and dubious carbon credits (Netter et al., 2022), as noted in an article by West et al. (2020) about worthless rainforest REDD + carbon credits.

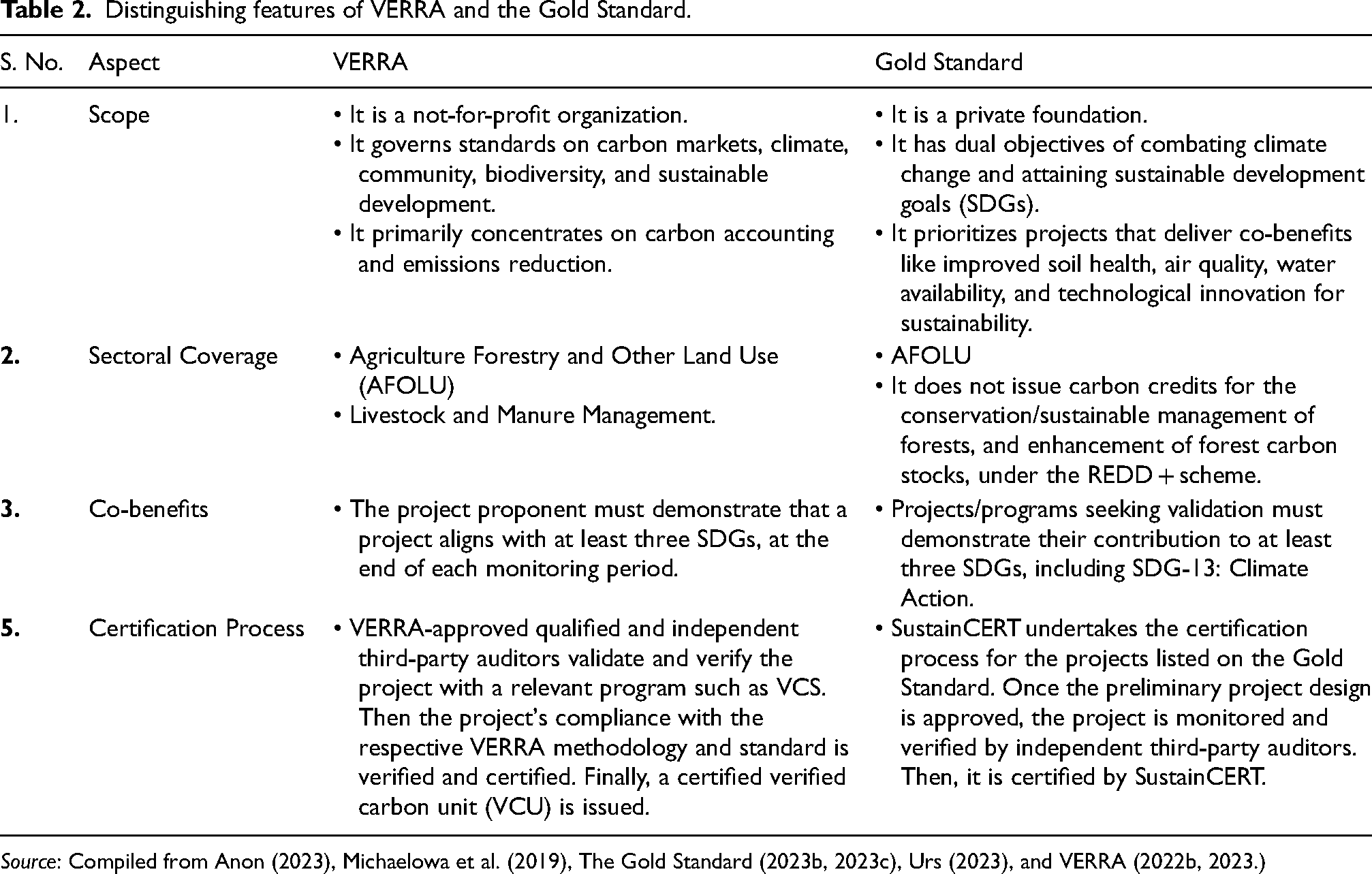

Most agricultural projects in VCMs are covered by the VERRA-administered Verified Carbon Standard (VCS) Program, and the Gold Standard (Netter et al., 2022; VERRA, 2022a). These two carbon crediting mechanisms are key frameworks in the VCM ecosystem. They govern the credibility and transparency of carbon markets, ensuring effective contributions to GHG reductions and the promotion of sustainable practices. While both the Gold Standard and VERRA play significant roles in the carbon market and are globally applicable, their key distinguishing features concerning agricultural carbon credits are tabulated below (Table 2).

Distinguishing features of VERRA and the Gold Standard.

Source: Compiled from Anon (2023), Michaelowa et al. (2019), The Gold Standard (2023b, 2023c), Urs (2023), and VERRA (2022b, 2023.)

Agriculture and allied sectors’ specific methodologies

A detailed examination of carbon crediting methodologies is crucial for a comprehensive understanding of the carbon credit landscape within agricultural projects in VCMs. The VCS program, initiated in 2005, offers individual methodologies such as VM0022 for optimized nitrogen fertilizer use in the USA, VM0041 for reducing enteric methane (CH4) emissions from ruminants globally, VM0042 for agriculture land management and VM0044 for CO2e removal through biochar production. Along with this, since 2003, the Gold Standard has developed methodologies such as afforestation/reforestation for agroforestry projects, the soil organic carbon (SOC) Framework for enhanced agricultural practices, and specific approaches for CH4 emission reduction in dairy cows and water efficiency in sugarcane cultivation. These frameworks highlight the diverse and targeted strategies for carbon accounting and reduction in various agricultural settings, described in Supplemental Material S1. The choice of standard to use depends on the specific goals and priorities of a given project.

Prices of carbon credits in the VCM

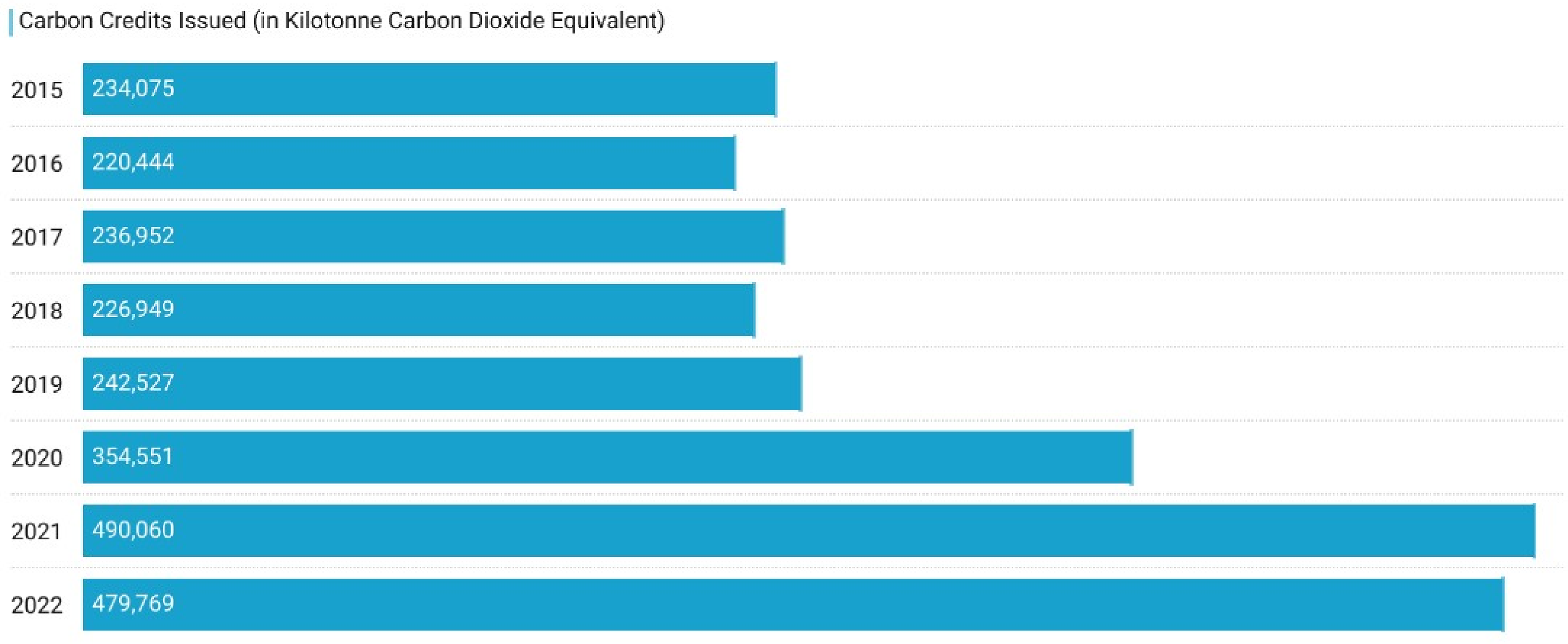

The VCM witnessed a substantial 252% increase in carbon credit retirements in 2022, compared to the level recorded in 2017 (South Pole, 2022). The heightened commitment to decarbonize, in alignment with the Paris Agreement, may increase the annual global demand for voluntary offsets, estimated at 1.5–2 GtCO2e by 2030 and 7–13 GtCO2e by 2050 (Blaufelder et al., 2021; The United Nations, 2023). Against this potential demand, carbon markets continue to supply an increasing number of carbon credits (Figure 2), with a notable surge in forestry-based credits against agriculture-based credits (World Bank, 2021). By avoiding deforestation, encouraging reforestation, minimizing landfill emissions, and applying technology to remove CO2, the annual supply of carbon credits is anticipated to be between 8 and 12 GtCO2e annually (Blaufelder et al., 2021).

Carbon credit issuance over years. Source: Compiled from World Bank (2023c).

The nature-based voluntary carbon credits are traded in online commodity exchanges such as the Carbon Trade Exchange and the Voluntary Climate Marketplace (TCVCM), or over-the-counter (OTC) in the case of occasional or low-volume trading and non-standardized contracts (Chen et al., 2021; Ecosystem Marketplace, 2022b; Perdan and Azapagic, 2011). The market price of carbon credits can be determined in two ways: (a) internal (cost-based) pricing, which factors in the social costs of GHG emissions, the costs of abatement technologies, and the present and future value of emission allowances; and (b) external (market-based) pricing, which balances the supply and demand of emission units to establish a price for carbon credits through a cap and trade or baseline-and-credit system (Opanda, 2023; World Bank, 2023c). These methodologies contribute to the overall pricing framework in carbon markets. Therefore, the choice between these pricing approaches is highly relevant, as it impacts the valuation of carbon credits while incentivizing emission reduction and maintaining economic growth (UNFCCC, 2023b). In addition, the price of carbon credits is influenced by the project location, type of program, underlying standards, year of issuance, co-benefits beyond carbon reduction such as sustainable development goals (SDGs), regulatory mechanism, traded volume, and market supply and demand (Opanda, 2023). For instance, credits associated with carbon removal tend to command higher prices (US$19 per credit) than avoidance-based credits (US$8 per credit) (World Bank, 2022a). Meanwhile, due to the regulatory obligations faced in the compliance market, the weighted price of a carbon credit is traded at around US$35 (CarbonCredits.Com, 2023). This is higher than the price of agriculture projects in the VCM that hover around an annual average of US$8 per tCO2e (Ecosystem Marketplace, 2022b). For the most part, voluntary carbon credits are traded OTC, at a premium. Specifically, agricultural carbon credits traded OTC in India are priced significantly higher at US$12–40 (e.g. climes.io sells voluntary carbon credits priced at US$24) than those traded on exchanges, which are priced at US$1–6.

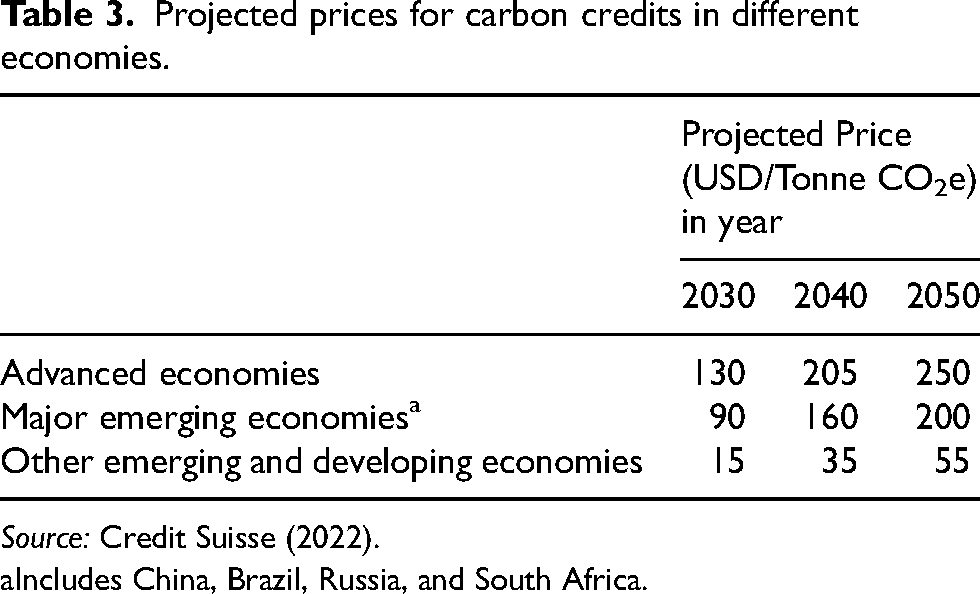

Some researchers have pointed out that to incentivize decarbonization, carbon prices (US$28 in the compliance market and US$7 in the voluntary market per tCO2e) should increase (Boever, 2023; Credit Suisse, 2022) (Table 3). Notably, the Taskforce on Scaling VCMs (TSVCMs) conservatively predicts that the price of voluntary carbon credits will range between US$10 and US$20 per tCO2e in 2030 (Credit Suisse, 2022). Shifting from business-to-business (B2B) to business-to-consumer (B2C) business models can boost the demand for carbon credits and, thus, increase their price. For instance, notable companies like Amazon, Flipkart, Walmart, and Zomato have begun to purchase carbon credits to offset their GHG emissions stemming from packaging and home delivery operations in India, which collectively amount to ∼1.5–5 million deliveries per day (Marcel, 2023). In 2022–2023, Zomato procured 500,000 carbon credits from the VCM and offset 18% of its deliveries by adopting eco-friendly transportation like bicycles and electric vehicles (Zomato Limited, 2022). Likewise, Perfora, an oral care company, offers climate-neutral products in collaboration with Climes that sells carbon credits to customers and has in this way offset 3 tCO2e to date (Climes, 2023). Moreover, blockchain technology is being utilized by Unilever's Ben & Jerry's, an ice-cream manufacturer, to (a) make carbon credits more accessible even to small buyers, unlike the current carbon offset markets that sell bulk credits to large corporate buyers, and (b) simplify the carbon credit trading process with enhanced transparency (Sherry, 2018).

Projected prices for carbon credits in different economies.

Source: Credit Suisse (2022).

Includes China, Brazil, Russia, and South Africa.

The dynamic interplay of increasing supply and demand for carbon credits has the potential to exert upward pressure on their price (Ernst and Young, 2022). In fact, carbon prices rose by 40% between 2021 and 2022 (South Pole, 2022).

While carbon markets hold significant promise, they face an issue of asymmetric pricing information (Blaufelder et al., 2021). A single carbon credit can exhibit divergent pricing across regions, with examples of compliance carbon credit prices at US$11 in Korea, US$29 in California, and US$35 in Austria (World Bank, 2023b). Similarly, voluntary carbon credit prices range widely from US$1 to US$119 (CarbonCredits.Com, 2023). This pricing inconsistency extends to several online platforms, including Quantum Commodity Intelligence and Ecosystem Marketplace, which report varying carbon credit prices for identical activities. The lack of a clear and uniform pricing mechanism in carbon markets contributes to limited global engagement, and these markets often favor developed countries (Buck and Compton, 2022; Favasuli and Sebastian, 2021). Other probable reasons for low global participation include a lack of public awareness about climate change, high administrative costs, limited approved methodologies for estimating carbon saved from an intervention, and insufficient quality assessment of credits. This results in non-transparent measuring, reporting, and verification (MRV) (Marchant et al., 2022; Smith et al., 2019).

In response to these financial, technical, and accounting challenges, some developing countries, such as Kenya and China, have taken mitigative action. The Kenya Agricultural Carbon Project proposed a collective approach for small farmers to sequester carbon, earn credits, and drive rural development (Siedenburg and Brown, 2015). Similarly, China established a Green Carbon Fund in 2007 and engaged in carbon credit trading, with credits valued at US$3 per tCO2e (Zhu et al., 2014).

Quality of carbon credits

To achieve the broader adoption of agricultural carbon credits, a critical imperative is quality enhancement, which is more than an abstract notion. High-quality carbon credits represent ecological integrity and promise a sustained, credible impact on the environment and economy, making them more appealing to buyers (DiMarino and Wright, 2023). Certain project characteristics indicate the quality of a carbon credit. Firstly, the principle of additionality emphasizes that carbon projects must lead to emission cuts over and above the baseline scenario. Secondly, the concept of permanence stresses the durability of these credits. Carbon removal or storage activities must prevent leakage and ensure that the net carbon captured does not inadvertently find its way back into the atmosphere. For instance, if a farmer reverts to conventional tillage from no-till, the sequestered carbon could be released back into the atmosphere, thus disturbing the permanence of the initially generated credits. Furthermore, carbon offset programs must accurately estimate that the number of credits retired corresponds to the volume of emissions reduced, avoiding pitfalls such as double counting or transfer redundancies. Lastly, it is crucial to align the carbon credits with established standards, such as those set by VERRA or the Gold Standard, so that they are inherently recognized as being of high-quality (The Gold Standard, 2023d; VERRA, 2022c). Initiatives such as the core carbon principles have been recently released by the Integrity Council for the VCM to improve the quality of voluntary carbon credits and market standards (Alexander, 2023).

Besides financially incentivizing SAPs, high-quality carbon credits also provide significant co-benefits for society and the environment (Buck and Compton, 2022; Fleming et al., 2019). Co-benefits are the additional positive impacts of climate mitigation actions and can be categorized into financial, social, and environmental dimensions (Fleming et al., 2019; Tang, 2016; White, 2022). From a financial standpoint, they offer an additional stream of revenue for farmers and create opportunities for climate traders and aggregators. On the social front, the benefits range from food security, enhanced farmer livelihoods, and women's empowerment, to poverty alleviation, improved rural infrastructure, community development, and the emergence of new markets for green products. Environmentally, the advantages encompass reduced GHG emissions, bolstered biodiversity, and public health benefits. However, empirical studies often neglect these co-benefits of carbon farming, leading to an underestimated GHG mitigation potential and insufficient compensation for farmers (Tang, 2016).

Acknowledging these co-benefits could further incentivize carbon farming. However, the inclusion of co-benefits in carbon pricing mechanisms is challenging. Firstly, quantification methodologies for estimating co-benefits lack consistency as they are context-specific (Lou et al., 2022). Thus, the collection, measurement, and inclusion of their data in carbon pricing mechanisms is tricky (Vrsatz et al., 2014). Even when they are quantified, the co-benefits may be unequally distributed between communities or individuals due to the absence of internationally recognized criteria for them (Hultman et al., 2020). Moreover, conflicting political and stakeholder interests may result in uncertainty regarding the co-benefits reaped (Hultman et al., 2020). Finally, policy formulation to incorporate co-benefits in carbon pricing faces political and bureaucratic hindrances at the global, national, sub-national, and local levels. Often, this results in the target players not benefiting from the policy (Spencer et al., 2016). Despite these challenges, efforts are being made to incorporate co-benefits into carbon pricing mechanisms to address short and long-term socioeconomic and environmental concerns. To encourage this, VERRA mandates project proponents to map their project's benefits to the relevant SDGs (VERRA, 2023).

Key players and pathways: Navigating carbon farming stakeholders and implementation steps in agriculture

While stakeholder engagement is crucial for the success of carbon farming projects, its complex nature is often not fully addressed in academic studies (Smit and Pilifosova, 2018). One may check Supplemental Material S2 for the various stakeholders in carbon farming. The stakeholders play a crucial role in the design, implementation, and success of a carbon farming project in agriculture, and its sequence of steps is explained in Figure 3.

Simplified flowchart of steps in carbon crediting. Source: Authors’ compilation from Smith et al. (2019), VERRA (2022b, 2023) and World Bank (2022b).

The project proponent drafts a document detailing the design of the carbon farming initiative, outlining its goals, operational scale, timeframe, geographic setting, the specific carbon farming techniques to be utilized, and the baseline scenario for comparison. This document also defines the roles and responsibilities of the project stakeholders, the provisions for building their capacities, and a plan for the monitoring and expansion of the project (UNFCCC, 2022b). Thereafter, the project activities that reduce GHG emissions and/or sequester SOC are implemented by the farmers (Smith et al., 2019). They are then validated by accredited third-party auditors following standardized methodologies (VERRA, 2022b) and the estimated baseline (VERRA, 2023). After the implementation and validation of the project, emission reductions are estimated and verified by project developers (Agtech companies), either through direct visits or using remote sensing technology (World Bank, 2022b). Accordingly, carbon credits are issued to the project by VERRA or the Gold Standard and sold to buyers (VERRA, 2022c). For instance, Boomitra proposed a carbon farming project in East Africa in 2019, covering 100,000 acres across Kenya, Rwanda, Tanzania, and Uganda. The intention is to sequester 1,249,417 tCO2e in 20 years by deploying regenerative agricultural practices, and the initiative requested registration on VERRA under the VM0042 methodology. In the project area, Boomitra collaborates with implementation partners to promote zero tillage (ZT), crop residue retention, manure application, improved water management, agroforestry, etc., through training and technical support to farmers (Boomitra, 2023).

In general, the generation and sale of carbon credits can be a tedious task, especially for small and marginal farmers, due to insufficient technical assistance for adopting SAPs and administrative, legal, and technical costs incurred during sale in carbon markets (Buck and Compton, 2022; Raina et al., 2024). Therefore, carbon companies like Boomitra, Varaha, Grow Indigo, and Core CarbonX can collaborate with Farmer Producer Cooperatives, Non-governmental organizations (NGOs), and local community leaders in rural areas to implement carbon projects and increase farmers’ participation in carbon farming (Nozaki, 2021).

Constraints to reap carbon credits from agriculture

Agricultural carbon credits face demand side challenges like (a) low buyer confidence and trust due to the complex and non-transparent process of carbon sequestration, hampering the authenticity of credits, (b) numerous certification labels like VERRA, Gold Standard, Plan Vivo, Puro.earth, etc., flooding the carbon markets and creating confusion and reducing buyer interest, and (c) skepticism surrounds corporations’ long-term emission reduction pledges (Wongpiyabovorn et al., 2023). As a cumulative effect, agricultural carbon credits are currently low-priced in the market (Nozaki, 2021). Additionally, on the supply side, the low potential for carbon credit generation from small landholdings in the Global South inadequately incentivizes farmers to adopt SAPs (Girish and Trivedi, 2022; Ishtiaque et al., 2024) and reduce their emissions. Meanwhile, insufficient farmers’ awareness and training on SAPs, no contact with the carbon company, and non-receipt of promised carbon credit payment discourage the continuation of SAPs, and the risk of reversibility of captured SOC persists (Cariappa and Birthal, 2023; Wongpiyabovorn et al., 2023). 1 , 2 Furthermore, variations in atmospheric temperature, precipitation, soil properties, topographic factors, and vegetation result in high spatial variability of soil carbon storage (Wang et al., 2021). Another major challenge faced by carbon projects is the generation of accurate MRV, which is costly and time-consuming, depending on the technology adopted by farmers and the region of intervention. For data collection, field surveys are often expensive, and satellite surveillance is challenging, especially during bad weather and cloud cover (Jayaraman et al., 2023). Besides, quantification of SOC using prediction models for a particular soil type/vegetation may be inaccurate, especially for small and marginal farmers of the Global South. 3

Recent developments in the agricultural carbon markets

The future landscape of agriculture carbon markets is shaped by a combination of governmental initiatives, shifts in stakeholders’ mindsets, technological advancements, and international collaborations (Lelechenko, 2023). For instance, the Carbon Border Adjustment Mechanism (CBAM) proposed by the EU aims to levy a carbon tax on imports from countries with less stringent climate policies (Park et al., 2023). This mechanism is expected to decrease worldwide carbon emissions by < 0.2% compared to an emissions trading scheme with a carbon price of 100 euros (US$108) per metric ton and without a carbon tariff (Asian Development Bank, 2024). It could also impact Indian carbon markets as follows: (a) Indian exports of iron, steel, aluminum, and other high carbon footprint products may face a competitive disadvantage in the EU due to the additional carbon tax, (b) although agricultural produce is currently not covered by CBAM, the EU plans to extend its scope, and (c) CBAM could incentivize Indian industries to reduce carbon emissions and adopt cleaner technologies, potentially leading to a domestic carbon pricing system or other decarbonization measures (European Parliament, 2022). This mechanism could lead to an increased demand for carbon credits, including those from agricultural activities, as part of domestic compliance markets, and enhance green investments in low-carbon technologies and SAPs (European Parliament, 2022).

Another important game changer could be the increased government intervention in carbon markets to ensure quality, transparency, and integrity in the transactions. For instance, the World Bank Engagement Road map for High-Integrity Carbon Markets showcases the role of international cooperation in boosting transparent and inclusive carbon markets, benefiting developing countries first (World Bank, 2023d). Governments like that of Singapore set out the Eligibility Criteria to ensure the high environmental integrity of International Carbon Credits (ICCs) under its carbon tax regime. These eligibility criteria, developed in consultation with a wide range of stakeholders, reflect a commitment of governments to transparency, additionality, and environmental integrity (National Environment Agency, 2023). Another similar example is the Indian Government's Green Credit Program, launched in October 2023, which incentivizes environmental conservation across various sectors, aligning with the broader “Lifestyle for Environment” movement to promote sustainable practices (Press Information Bureau, 2023). India also introduced a framework on VCM in Indian agriculture in January 2024, to encourage SAPs that reap tradeable carbon credits for the farmers (Ministry of Agriculture and Farmers Welfare, 2024). Government involvement may harmonize standards, leverage technology for transparency, develop supportive policy frameworks, engage the private sector, and foster international cooperation. Such developments and associated institutional changes suggest a rapid evolution of a multifaceted approach to fully realize the potential of carbon markets, and it can be more beneficial for agricultural sectors, where the emissions are not concentrated, making the credit provision more challenging.

Indian agriculture: Role and opportunities in climate change mitigation

Developing countries (with 85% of the global population) are expected to surpass the GHG emissions of developed countries by 2050. While the per capita emissions may still show significant contrast, some researchers indicate that the whole Global South could play a significant role in climate change (Chandler et al., 2002). Against this context, the case of India, as a rapidly developing agrarian economy, is particularly noteworthy. Its population is projected to grow at an average annual rate of 1.12% from 2022 to 2031, exceeding the global average growth rate of 0.96% (The United Nations, 2022). This demographic trend is set to escalate nutritional and energy demands. Economic growth in India is likely to lead to increased incomes, resulting in dietary shifts towards the greater consumption of dairy and meat products with a higher carbon footprint (Organization for Economic Cooperation and Development, 2023a). Such changes are expected to intensify pressure on India's agricultural production. India's per capita CO2 emissions could potentially double, increasing from 1.53 tCO2e in 2013 to 2.98 tCO2e in 2030 (Narain, 2021; World Bank, 2022c; World Economic Forum, 2022).

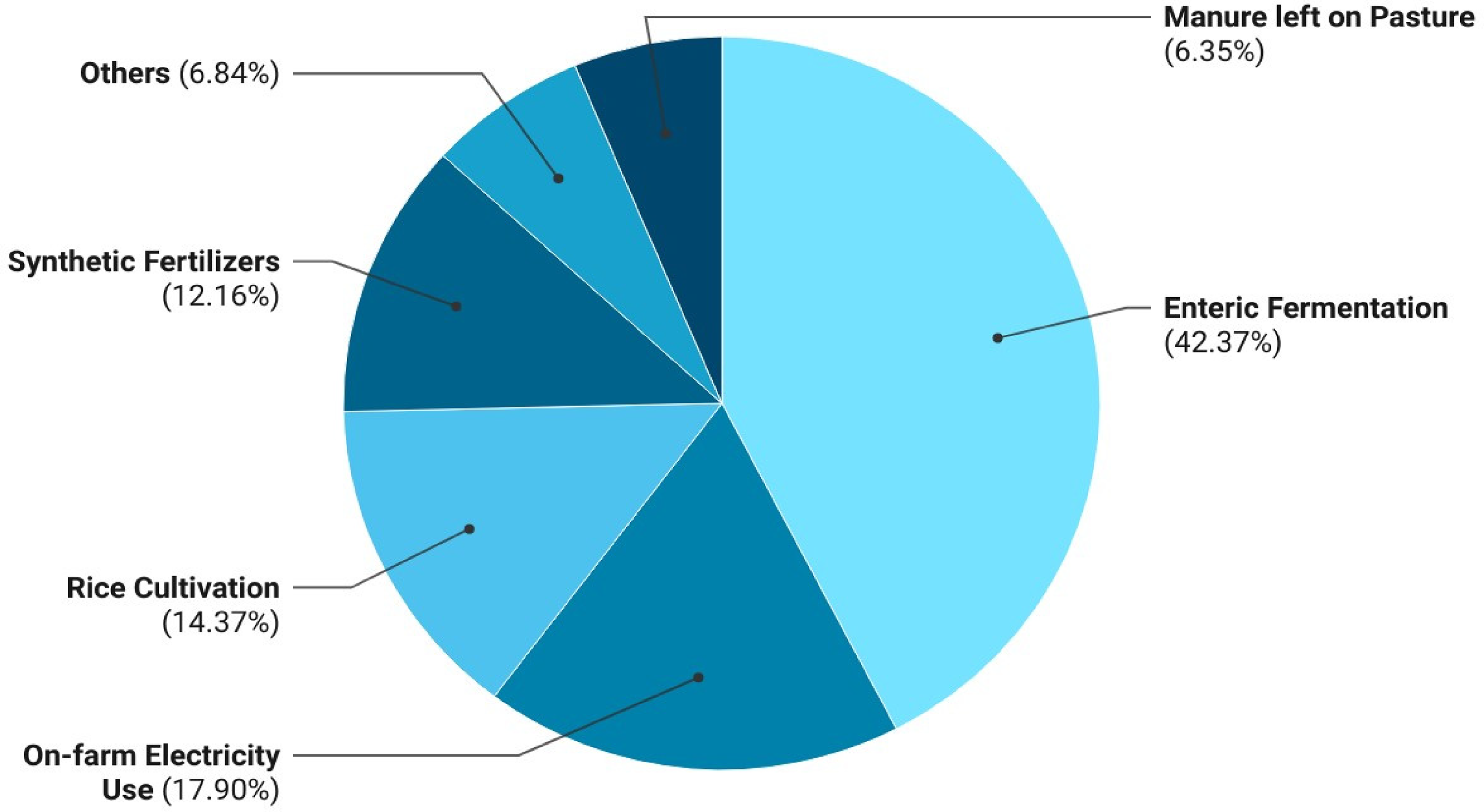

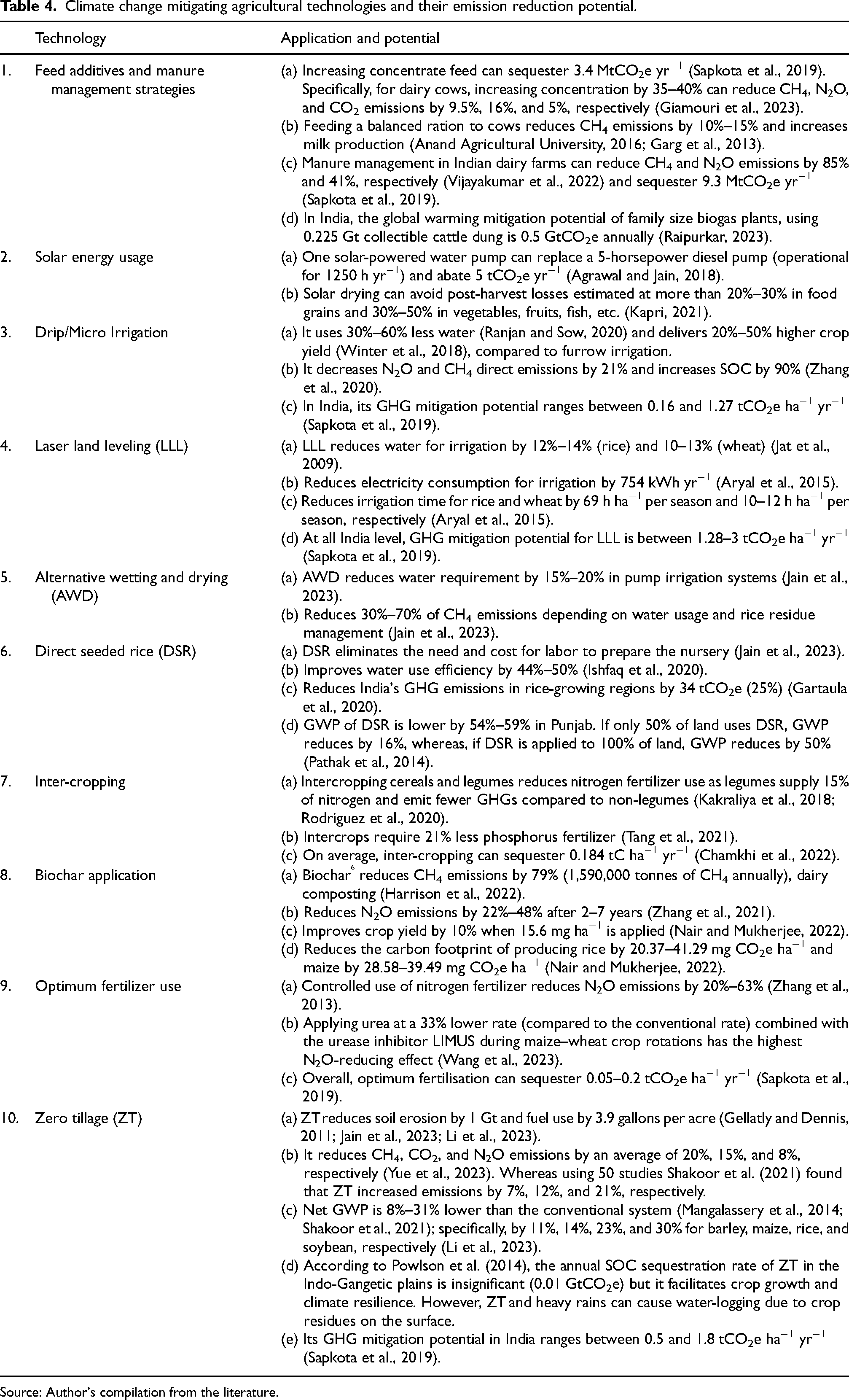

The agriculture sector accounts for 14% of India's GDP and 17% of its national GHG emissions (Chand and Singh, 2023; Ministry of Statistics and Programme Implementation, 2023). Figure 4 provides a detailed breakdown of emissions from the agriculture sector. The evolving food industry, employing inefficient technology and non-renewable energy sources in food processing, transportation, packaging, and retailing, is likely to further elevate GHG emissions (Mrowczynska-Kaminska et al., 2021). This pattern underscores the urgency to explore climate change mitigation strategies within the agriculture sector. Farmer adoption of SAPs offers a particularly promising solution. Implementing SAPs can significantly reduce India's annual emissions, potentially lowering them from 11.8 GtCO2e in 2019 to 1.9 GtCO2e by 2070 (Bhattacharya, 2019; Gupta et al., 2022). Certain SAPs that can be deployed in India are tabulated in Table 4.

Breakdown of agricultural emissions from different sources in India in 2020. Source: Compiled from Food and Agriculture Organisation (2020).

Climate change mitigating agricultural technologies and their emission reduction potential.

Source: Author's compilation from the literature.

As indicated in Table 4, SAPs have a lower global warming potential (GWP) than conventional practices. This is due to their positive environmental and economic impacts, such as reductions in soil erosion, water and electricity consumption for irrigation, use of synthetic fertilizers, enteric emissions from livestock, and cost of agricultural labor, while potentially improving crop yields. According to Sapkota et al. (2019), Indian agriculture is expected to emit 515 Megaton (Mt) CO2e per year (yr−1) by 2030, out of which SAPs can mitigate 85.5 MtCO2e yr−1. Specifically, ZT, efficient fertilization, and water management for rice production can collectively sequester 43 MtCO2e yr−1 (Sapkota et al., 2019). For instance, ZT alone sequesters 0.5–1.8 tCO2e per hectare (ha−1) yr−1 (Sapkota et al., 2019). Assuming a conservative carbon price of US$10 per credit and project developers distributing 60% of carbon credit sales revenue to farmers, a farmer practicing ZT could earn ∼ INR 250–900 ha−1 yr−1. Similarly, the GHG mitigation potential of laser-assisted precision land leveling (LLL) ranges between 1.28 and 3 tCO2e ha−1 yr−1 (Sapkota et al., 2019). Following LLL technology could yield a farmer ∼ INR 600–1500 ha−1. These figures are based on conservative estimates, and actual earnings could be 1.2–4 times higher, as carbon credit prices in OTC deals range between US$12 and 40.

Such opportunities can be realized if all the stakeholders collaborate and mobilize market information, input supplies, and technical services for farmers (Kumara et al., 2023; Ministry of Agriculture, 2013). However, small and marginal farmers are less likely to adopt SAPs due to their lack of awareness and the high implementation cost of technology. For instance, LLL and drip irrigation have high up-front costs, but small and marginal farmers lack economies of scale and adequate access to credit and risk-bearing abilities (Ruzzante et al., 2021; Ishtiaque et al., 2024). The government extension agencies and self-help groups offer only limited information to facilitate the adoption of the SAPs. The absence of a secure land tenure is another challenge as then the farmer prefers investing in agricultural practices offering immediate returns over long-term investments in SAPs (Ruzzante et al., 2021). Presently, in India, carbon farming policies are in an early development stage. Nonetheless, the recently announced framework on VCM in Indian agriculture and schemes such as the Green Credit Program, Promotion of Alternate Nutrients for Agriculture Management Yojana (PM-PRANAM), and the Mangrove Initiative for Shoreline Habitats and Tangible Incomes (MISHTI) among others, incentivize green growth (Ministry of Agriculture and Farmers Welfare, 2024; Gazette of India, 2023; Press Information Bureau, 2023). Furthermore, regular consultations with carbon farming stakeholders including project developers, certifiers like VERRA and the Gold Standard, international agricultural R&D organizations, the Integrity Council for the VCM, the Carbon Market Association of India, and carbon credit rating agencies can facilitate holistic policy formulation (Singh and Chaturvedi, 2023). 4

The role of Indian agriculture in climate change mitigation is growing. In terms of the number of agricultural carbon credit projects, India with 46 projects is second to China (279) and is leading in emission reduction among countries with Agricultural Land Management (ALM) projects on VERRA (Nozaki, 2021; VERRA, 2021). However, policy uncertainty, imprecise MRV, inefficiencies, and variations in sequestration conditions (Tripathi, 2023) should be accounted for while striking a balance between sustainability and economic development.

Potential pitfalls of carbon farming in India

Policy barriers preventing the emergence of carbon farming in India

In the context of global public goods, such as climate change mitigation and environmental conservation, well-crafted policies are essential for addressing problems in collective action, promoting sustainability, and fostering international cooperation (Garg et al., 2007). Otherwise, the result is mismanagement and the irresponsible use of shared resources and negative externalities (Robe, 2014). In India, policy-related challenges are a central barrier to the adoption of carbon farming. They result from the unequal implementation of agri-environmental policies and the conflicting goals of various stakeholders in the agricultural sector. For instance, stubble burning is legally prohibited in Punjab, Haryana, Uttar Pradesh, and Rajasthan (Deshpande et al., 2023), which makes it ineligible to be included in carbon credit projects (VERRA, 2022a). Moreover, developing nations are disproportionately burdened with the responsibility for carbon sequestration and climate change mitigation, raising concerns of “environmental colonialism” (Wittman and Karon, 2009). 5 This inequity can hinder the enthusiasm for carbon farming initiatives in India. Besides, the risk of carbon leakage, as outlined by Bohringer et al. (2017) is a critical aspect. For instance, the EU's unilateral enforcement of CBAM might shift its emission-intensive industries to developing nations with weaker regulations, such as India (Kawasaki, 2023). As a result, India would experience a rebound effect by nullifying the emission reductions achieved in the EU, paving the way for carbon leakage. 6 Consequently, environmental challenges can arise, highlighting the need for coordinated global efforts in carbon farming. A common price for carbon credits is also necessary to genuinely reduce emissions and avoid such unintended consequences (Eckersley, 2010; European Commission, 2023).

Educational, operational, and economic roadblocks to carbon farming in India

Without collective participation, carbon farming in India is costly and unappealing because the majority of its farming population are smallholder farmers who lack information and financial and technological resources (Chute et al., 2022; Krishnan and Singhal, 2023). Thus, India could face educational, operational, and economic challenges during the implementation of carbon farming. Firstly, communication gaps between the farmers and the farmer producer organizations, local human resources (e.g. community networks), and agritech companies pose educational barriers for the farmers of India (Nozaki, 2021). Insufficient and asymmetric information about project locations, GHG mitigation technologies, yield and cost changes, input requirements, carbon credit calculation methodologies, market channels, and training for carbon farming can thus cause VCM inefficiency (Harriss-White et al., 2019; Sharma et al., 2021). Secondly, precise MRV is costly and time-consuming for farmers, resulting in the risk of dubious credit sales (Kooten, 2009). Additionally, the majority of farmers in India are hesitant to adopt digital technology since they do not receive immediate benefits (Krishnan and Singhal, 2023). Besides, due to these technical constraints faced by farmers, third-party verification using cloud computing, smart sensors, and blockchain encryption is unfeasible, hindering transparent real-time carbon credit generation (Vives, 2023; Woo et al., 2021). These roadblocks reduce buyer confidence, demand, liquidity, and prices in the carbon credit market (Blaufelder et al., 2021). Global carbon prices were below the required level of US$40–80 per tCO2e in 2020 and must rise to US$50–100 per tCO2e by 2030 (High-Level Commission on Carbon Prices, 2017).

Farm and farmer characteristics hindering the adoption of carbon farming in India

Even when agricultural carbon farming is implemented, the comparability of the carbon credits generated can be difficult due to variations in farm properties such as soil type, biomass availability, and crop residue removal and, thus, varying sequestration conditions across regions (Buck and Compton, 2022; Kooten, 2009; Payen et al., 2023). For instance, agroforestry systems have a carbon sequestration potential of between 0.87 and 8.92 megagrams (Mg) ha−1 yr−1. On the one hand, legume-based systems in Punjab can sequester 0.87 Mg ha−1 yr−1, while those in Uttar Pradesh sequester 3.4 Mg ha−1 yr−1. This disparity could be accredited to biophysical variations that must be considered (Chavan et al., 2023). Furthermore, cultural barriers like lack of stakeholders’ awareness, personal interest, and attitude cause apprehensions about carbon farming (Singh and Chaturvedi, 2023; Sharma et al., 2021). In developing countries, especially in Africa and South Asia, women are often excluded from decision-making in agriculture due to intrinsic gender inequality (Lee et al., 2015; Raghunathan et al., 2019). Men often control finances and choose profit over sustainability (Raghunathan et al., 2019). For instance, the household-level survey conducted by Aryal et al. (2014) in Bihar and Haryana found that decisions regarding farm practices and, specifically, the adoption of SAPs are taken by the males of the households. Females undertake laborious tasks in agriculture and, thus, can be more receptive to SAPs that result in higher output and co-benefits and are less laborious. But they become the decision makers only in cases of the emigration of male heads for alternative employment or their demise. In the Gangetic plains of Bihar, Aryal et al. (2018) highlighted that the adoption rate of SAPs, such as crop diversification and the use of high-yielding seed varieties by female-headed households is 0.42% higher than that of male-headed ones (Mishra et al., 2023; Raghunathan et al., 2019).

Conclusion

In summary, the evolution of carbon markets and credits has been marked by the introduction of various mechanisms under the Kyoto Protocol and the Paris Agreement. The VCM has emerged as a flexible and resilient tool, with projections indicating substantial growth in transactions. Distinct from compliance markets, VCMs involve private entities voluntarily engaging in the offsetting of emissions, including projects in agriculture. Agricultural carbon credits play a crucial role in VCMs, adhering to standardized protocols like the VCS Program and the Gold Standard.

The pricing of carbon credits in the VCM is influenced by various factors, including project location, type, standards, and market dynamics. Agricultural carbon credits, traded over the counter in India, often command higher prices compared to exchange-traded credits. The increasing global demand for voluntary offsets and efforts by major companies like Amazon, Flipkart, and Zomato to purchase carbon credits indicates a positive trend. However, challenges such as asymmetric pricing information and the lack of a uniform pricing mechanism persist, impacting global engagement.

The quality of carbon credits is a critical consideration for their broader adoption. High-quality credits, aligned with recognized standards, contribute to climate mitigation and offer significant co-benefits for society and the environment. These co-benefits, ranging from improved livelihoods to biodiversity conservation, are often overlooked and present challenges in quantification and inclusion in carbon pricing mechanisms. Specifically, to generate agricultural carbon credits, government initiatives can encourage SAPs by increasing awareness and technological advancements while addressing their potential limitations. In the context of Indian agriculture, the country plays a significant role in global emissions, and SAPs are identified as a promising solution for climate change mitigation. The adoption of SAPs in India faces challenges related to policy barriers and educational, operational, and economic roadblocks, as well as farm and farmer characteristics. Initiatives like the Framework on VCM in Indian agriculture and the Green Credit Program aim to incentivize sustainable growth, but a reduction in policy uncertainties and the need for coordinated global efforts remain crucial for the success of carbon farming initiatives in India. In other words, while carbon markets hold promise for climate change mitigation, addressing challenges related to pricing, quality, and global cooperation is essential for their effective implementation, particularly in the context of agricultural practices in India.

Supplemental Material

sj-docx-1-oag-10.1177_00307270241240778 - Supplemental material for Shaping India's climate future: A perspective on harnessing carbon credits from agriculture

Supplemental material, sj-docx-1-oag-10.1177_00307270241240778 for Shaping India's climate future: A perspective on harnessing carbon credits from agriculture by Ananya Khurana, Dilip Kajale, Adeeth AG Cariappa and Vijesh V Krishna in Outlook on Agriculture

Footnotes

Acknowledgements

This study is also strategically aligned with the One CGIAR Regional Integrated initiative Transforming Agrifood Systems in South Asia (TAFSSA) to support actions that improve equitable access to sustainable healthy diets, improve farmers’ livelihoods and resilience, and conserve land, air, and water resources in South Asia.

Data availability

The data used in the article is freely available in the public domain and can be sourced from the World Bank, the Food and Agriculture Organization (FAO), and the International Energy Agency. All data sources are appropriately referenced within the text.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethics approval statement

This article does not involve new research on human beings or animals. The analysis and discourse presented herein are based on already published studies.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported through the CGIAR Regional Integrated Initiative Transforming Agrifood Systems in South Asia or TAFSSA (https:// www.cgiar.org/initiative/20-transforming-agrifood-systems-insouth-asia-tafssa/). We acknowledge and appreciate the One CGIAR Donors (![]() ).

).

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.