Abstract

In many countries, smallholder farmers play a key role in food crop seed production. So far, the community roles, operational structures, seed production efficiency, aspects of sustainability, and the social and policy environments in which these groups operate have been poorly studied and described. The present study attempts to better understand these factors by drawing cases from twenty-five seed producer groups in five countries (Vietnam, Uganda, Zambia, Niger, and Guatemala) that deal with nine crops in total (rice, maize, sorghum, pearl millet, common bean, cowpea, soybean, groundnut, potato and sweet potato). Results of the study show all groups supply a significant share of seed offered in local markets. It appeared that all groups received major support for capacity development from a broad range of actors including local and national governments, public institutions, national seed companies and development organizations. Several groups operate under seasonal contracts with institutional seed buyers, whereas other groups sell most of their seed in local markets to fellow farmers. To support seed quality and render product branding meaningful, most groups have established subgroups for crop monitoring and seed inspection, and for gathering and using market intelligence. Some, but not all groups depend on formal seed certification. Two key challenges stand out across seed producer groups interviewed. First, most seed producer groups experience difficulties in accessing good-quality early generation seed (EGS) on time, like in the formal seed sector in many countries. Second, in most groups packaging and labelling of the seed produced and offered in local markets is suboptimal, hindering further professionalization. Moreover, groups invariably have a poor understanding of applicable seed policy and legislation. Our observations point at actions that external stakeholders could undertake to strengthen smallholder farmer seed production in recognition of their contribution to food and nutrition security.

Introduction

Smallholder agriculture provides food for a major part of the global population (Tscharntke et al., 2012). For their seed supply, smallholders depend to a large extent on locally produced seeds offered in local seed markets and involving farmers’ varieties as well as registered formal (both public and private) sector varieties. In many developing countries, the informal seed system is much larger than the formal seed system (Kusena et al., 2019). In a meta-study covering six countries, McGuire and Sperling (2016) report smallholder farmers access more than 90% of their seed from their local markets. Local markets are especially important for poorer farmers and in times of stress (Sperling and McGuire 2010; Kansiime & Mastenbroek, 2016). In many countries, the formal seed sector only has a substantial market share in hybrid maize and in global vegetable crops (Sperling and McGuire, 2010). Crop varieties first offered in formal markets do get dispersed in informal seed systems over time, and in the process often undergo modification and adaptation to local conditions (Singh et al., 2020). Farmer seed production responds to specific local demands, especially regarding minor, less profitable crops, and open-pollinated crop varieties, and tends to operate in local markets and areas where commercial seed is often not available or affordable (Mastenbroek et al., 2021). Rural development initiatives have supported the establishment of farmers seed enterprises (CRS, 2017) that serve local markets but also engage in seed production contracts with development projects, non-government organizations (NGOs), government agencies and commercial seed companies (SDC, 2021).

National seed laws have a major impact on the functioning of smallholder seed systems. Seed laws and regulations determine who can produce and sell seeds, which varieties may be offered in the market, and which quality requirements have to be fulfilled for seed lots to be marketed. In a survey conducted by the Food and Agriculture Organization (FAO), it appeared that commercial production and exchange of uncertified seed was permitted for only a limited group of crops in 25 per cent of the covered countries, while 29 per cent of countries explicitly banned the sale of all seed that had not been certified (FAO, 2018). Furthermore, an analysis of the seed laws and policies and regulations across 35 countries in Africa showed that in 23 countries seed laws forbid the trade in unregulated seed. Obviously, government policy and legislation may have negative impacts on farmers’ abilities to engage in seed production and marketing, for staple crops (De Jonge et al., 2020; Gatto et al., 2021).

While guaranteeing the quality of seed in the market, seed laws with more flexible regulatory approaches and practices may allow for more equal opportunities of formal and informal seed systems, and the marketing of high-quality seed of traditional and farmer-adapted varieties (Kuhlmann and Dey, 2021). To boost the quality of smallholder produced seed and to increase the marketing of such seed, FAO developed the Quality Declared Seed (QDS) concept (FAO, 2006), which has been enacted in several countries in sub-Saharan Africa. Other countries introduced legislation based on the related concept of truthfully labelled seed. Both concepts aim at a shift of the burden of quality control from the government to the seed producer, assuming that the seed producer has an interest in brand and/or origin reputation and in keeping clients satisfied with the quality of the seed provided (Spielman and Kennedy, 2016). These approaches may also enhance the use of farmers’ varieties, if these indeed facilitate the marketing of seed of such varieties (FAO, 2021).

Smallholder seed production requires multiple capacities, including technical expertise, market intelligence and access to public services. Thus, in a number of countries farmers have organized themselves in local seed producer groups to produce high-quality seed of crop varieties, often with external support to various extents. This study involved structured focus group discussions with twenty-five seed producer groups in five countries (Vietnam, Uganda, Zambia, Niger and Guatemala) producing seed of nine crops in total (rice, maize, sorghum, pearl millet, common bean, cowpea, soybean, groundnut, potato and sweet potato). The results provide information on the community roles, operational structures, seed production efficiency, aspects of sustainability, and the agroecological, social and policy environments in which these groups operate. Where reference is made to starter seed or input seed, used by the interviewed groups to establish their crop stands for seed production, this may be informally self-produced, or be early-generation seed of various grades obtained from external parties (public or private entities). Such grades may encompass breeder seed, pre-basic and basic seed, whereas the term foundation seed is also used. The seed produced by the interviewed groups may be formally certified or quality-declared seed (QDS). Consequently, quality of the seed used as input and of the seed produced by the groups for the market, may vary considerably in quality aspects.

Methods

The seed producer groups involved in this study were selected based on current or previous involvement in international seed system initiatives managed by the Sowing Diversity = Harvesting Security program coordinated by Oxfam Novib, and by Catholic Relief Services in the framework of the Supporting Seed Systems for Development (S34D) program, in collaboration with national partner organizations involved in these two initiatives. By consequence, the results of this study reflect local development realized through external support. Beyond this sample, external support for local seed production initiatives may take various alternative forms or may be absent.

A structured survey instrument (see

In each of the five countries involved, at least four seed producer groups were interviewed, with one or two meetings per group. Typically, interviews would take between two and three hours. All focus groups comprised both men and women producers and involved at least 10 but not more than 15 participants, in line with national Covid-19 containment measures. Any ambiguity in the original responses was cross-checked with the interviewers who in some cases consulted the communities involved to resolve follow-up questions. A minimum of 10 producers per group provided individual economic information, ensuring representation of women, where possible. Quantitative data was collected and analyzed in Microsoft Excel.

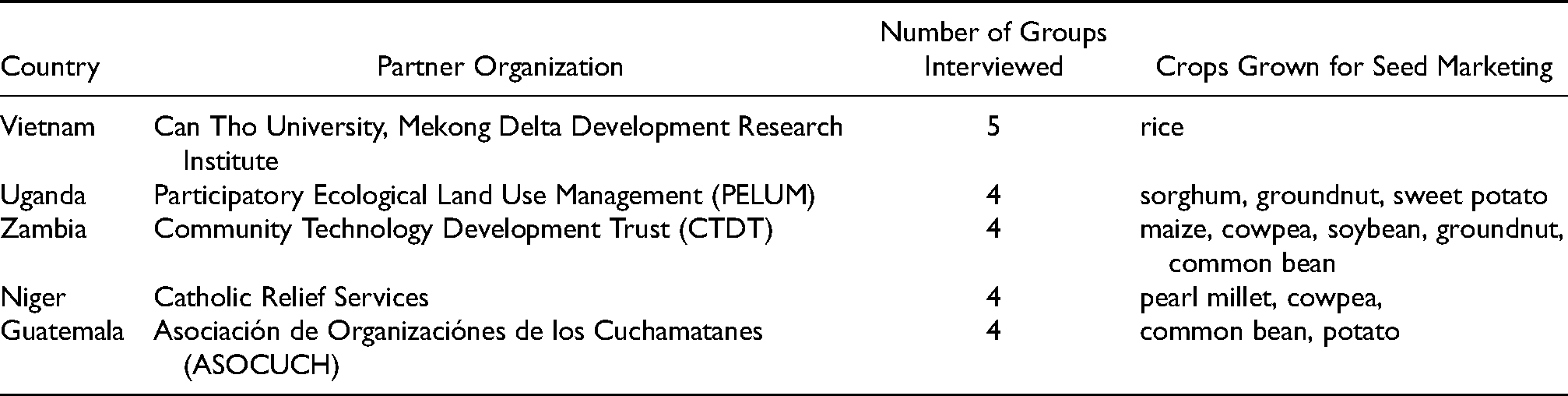

An overview of implementing organizations and number of groups interviewed for the study is provided in Table 1 below.

Interview sample.

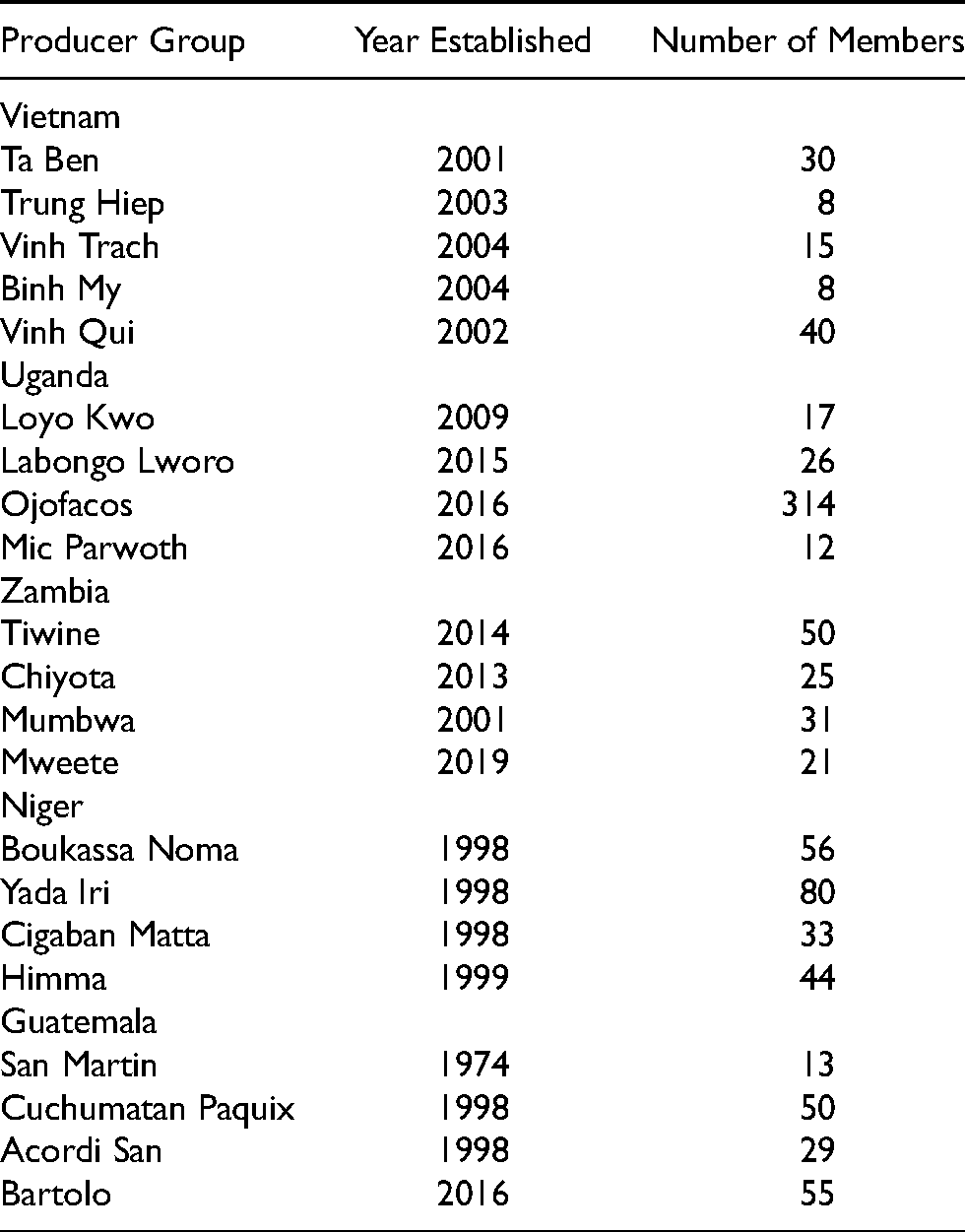

Most of the interviewed seed producer groups have been operating over many years. Most producer groups in the Mekong Delta in Vietnam, widely known as seed clubs and focusing exclusively on rice production, were established two decades ago. Membership of the individual groups ranged from 8 to 40, whereas participation of women and youth was generally low. In Uganda, groups producing Quality Declared Seed (QDS) were established between 2009 and 2016. Membership ranged between 17 and 30, more than 50% of the producers are women, and three of the four groups have witnessed an increase in the participation of youth over time. One group has developed into a cooperative which has grown substantially, now involving over 300 members (not all involved in seed production). In Zambia, QDS producer groups were established between 2001 and 2014, and ranged from 21 to 50 members in size. On average 15% of the members was below 30 years of age. Participation of women was especially significant in administrative and marketing activities. In Niger, large farmer producer groups of up to 80 members were established 10 to 20 years ago, participation of women and youth being substantial, but varying between groups. In Guatemala, work on potato started in 2000, work on beans in 2015, with groups sizes ranging from 20 to 55. Details on the seed producer groups are summarized in Table 2.

Details on the seed producer groups sampled.

Results

In the sample of seed producer groups involved in this study major commonalities and distinctions between individual seed producer groups and countries could be distinguished, as presented below. The agro-ecological settings of the various seed producer groups varied but on average appeared well suitable for seed production. Only groups in Vietnam reported that they had access to irrigation. High altitudes in Guatemala favoured potato seed production. The agro-ecosystems in Vietnam and Uganda allowed two cropping seasons per year, agro-ecosystems in the other countries were characterised by only one growing season. Most but not all groups had good access to roads, and some groups (Vietnam, Niger) appeared to sell across political borders.

Results of the focus group discussions are presented according to the value chain, addressing group organization and within-group operations, capacity building and training, choice of crop varieties and marketing, access to starter seed, seed volumes produced, seed packaging and labeling options, and price setting for seeds produced. In addition, results regarding a few themes that cut across the value chain are presented, in particular roles played by external stakeholders, strengths and weaknesses as perceived by the groups, impact of national seed policies and laws, and impact of the Covid-19 pandemic on group functioning.

Group organization

In all countries, selection of group members was primarily based on individual qualities as a farmer and access to basic inputs. Farmers could announce their own candidacy. In most cases, farmer members needed to have access to good-quality land, but in Niger large communal plots served to produce seed. All members in the farmer producer groups felt they act as a group, although some activities (especially sales of part of the seed in local markets) may be undertaken as individuals. By exception, the members of the QDS groups in Zambia reported that they look at the membership as being a personal affair, yet they reported group decisions on the selection of crops and varieties, as well as on seed inspections and marketing. In Guatemala, groups engaged in production planning and identifying input requirements, whereas the seed production itself was regarded an individual responsibility. In Niger, a common plot of land was used for seed production, and all activities were planned and implemented as a group.

The role of women in informal peer-to-peer field inspections varied from low (Vietnam) and variable (Guatemala) to high (Uganda, Niger), and sometimes included marketing (Guatemala). All groups valued the role of women (e.g. for their specific knowledge on seed selection and food quality) and youth (needed for long-term sustainability of the group; better educated, better connected outside the community, and interested in marketing aspects). Training of young people was considered important, but it was noted that – as for women - they often have no access to, nor own land, and may therefore have limited access to credit, which in turn may influence their position in the groups and hamper their full participation in seed production.

Within-group operations

All seed producer groups interviewed had formed a subgroup on seed monitoring and inspection, providing peer review during the growing season, and many groups a marketing intelligence subgroup. All groups undertook internal peer-to-peer field inspections, often provided by an appointed field inspection committee, sometimes by outsiders (community seed bank committee in Uganda).

In Vietnam, the Provincial Agricultural Technical Service Center was hired to assess and inspect the seed quality and to assess varietal purity and seed health. Many but not all groups aimed for formal certification of the seed produced by government certification agencies, involving field and seed inspection. In Vietnam, in case seed clubs produced seed of varieties under plant variety protection, seed was informally monitored but nevertheless by government agencies (regional seed centers). In Zambia, inspection was either a personal or a group affair, and certification to meet QDS requirements was done by the Seed Control and Certification Institute (SCCI). In Zambia and Niger, private contracting companies carried out their own inspections as well. In Niger, only one of the four cowpea producer groups did not aim for formal certification, all other seven groups (cowpea and pearl millet) did. In Guatemala, potato seed was certified by the government agency, field monitoring was an added informal and internal affair. No formal certification of bean seeds was in place, and this remained a responsibility of the producer groups with support of the ASOCUCH cooperatives.

Seed groups producing certified seeds or QDS were inspected by the proper seed regulatory agencies (Ministry of Agriculture in Niger, Seed Control and Certification Institute (SCCI) in Zambia, Ministry of Agriculture (MAGA) in Guatemala). Typically, the marketing subgroups gathered information about market preferences by paying visits to local markets, through informal exchanges with other seed producer groups, and by following up on radio and phone messages from government authorities (both national and local).

In summary, the seed produced was either informally marketed or underwent certification by national authorities, but all groups maintained informal peer-to-peer inspections of the crops grown and the seed produced.

Capacity building and training

Every seed producer group in the study sample had received formal and/or informal trainings. Multiple trainings were typically provided either by actors in development projects, but also by the National Agricultural Research System (NARS), local government extension agencies, farmer organizations and private sector entities. Trainings were mostly provided and paid by external parties. The length of the trainings varied from a few days to season-long, and single to multiple trainings on various topics were involved, including on agronomic practices, integrated pest management, seed selection, post-harvesting methods and storage, business and marketing, and financial management. In all groups members received a training in seed production, whereas only few trainings covered seed policies and regulations. Obviously, peer-to-peer assistance between group members formed an additional major component in capacity building, as may also be deduced from the establishment of sub-groups for field inspection and market intelligence. All seed production groups regarded capacity building as an essential element of their activities. Sometimes, as in Niger, producer group members undertook a learning trip to Burkina Faso as part of the trainings.

Markets and crop and variety choices

The groups in Vietnam focused on rice seed production only, and the groups in Niger either on cowpea or pearl millet, in Guatemala either on potato or beans, whereas the groups in Zambia and Uganda produced several crops simultaneously (see Table 1). Across all countries, market demand was the strongest factor influencing for which crops and varieties to produce seed. Markets and customers were highly variable and ranged from institutional buyers (public and private, including government programmes and NGOs) to fellow farmers in local markets, either through direct sales or through middlemen (agro-dealers, kiosks, motorbike sellers).

All groups sold some of their produce in local and regional markets even if they had been contracted by institutional buyers. The share in national markets was low. Groups that operated under contract with wholesale buyers did not undertake market research (in particular in Vietnam, Zambia). Other groups often undertook market visits and market intelligence as a group, normally through the activities of a marketing subcommittee. Some also sold through seed fairs (Uganda). Sometimes, the choice of varieties for which seed was produced, was determined by the availability of starter seed (Zambia). In Guatemala, bean seed from smallholder producer groups was sold to NGOs and local agro-services, which would buy 70% of the total production. In general, where seed producer groups produced seed under contract with institutional buyers, they were provided with starter or input seed by the contracting party.

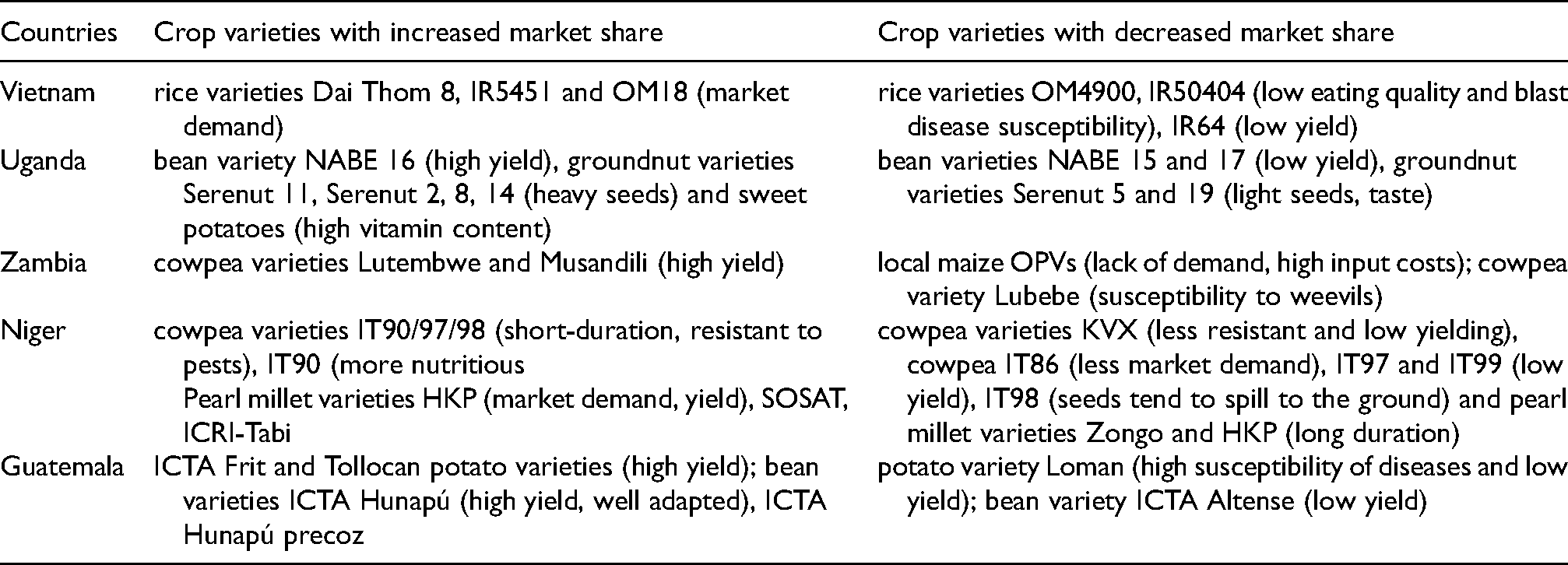

Over the years, the varieties and even the crops grown for seed production have changed in response to market request and changing climate conditions. In Niger it led to a change in crops, from pearl millet to cowpea, and in Zambia, seed producers shifted from the production of maize OPV seed to groundnuts and cowpeas. In Guatemala, susceptibility to diseases and low yield resulted in decreased seed production of a particular potato variety. At the same time, it appeared cumbersome to introduce seed of new varieties with unknown traits into local markets, since this presented a production risk for the buyer. Most popular varieties under the seed producer groups shared some common and well-recognized features: they were resistant to pests and diseases, stress-tolerant and often early-maturing in response to current climate conditions, and ideally also high-yielding, whereas palatability, nutrient-richness, and easy food preparation were traits being more popular amongst female seed producers. The preferences of the seed producer groups thereby closely followed the preferences of the smallholder farmer communities at large. Table 3 below provides examples of changes in varietal preferences over the last few years. The numbers of crops and varieties grown appeared to be limited, groups in Vietnam, Guatemala and Niger focusing on a single crop, and the total number of varieties for a particular crop grown by a single producer group not exceeding four.

Responses to variety demand.

Gender appeared to be associated with the crops for which seed was produced, the production of seed for crops that were grown by male mainly also being a male affair (such as rice in Vietnam and potato in Guatemala). The assessments in Zambia and Zimbabwe showed maize, sorghum, and millet to be “men’s crops” whereas the legumes groundnuts and cowpeas appeared to be “women’s crops”. Many female group members suggested that they participated as group members with the consent of their male partners. Gender also influenced variety preferences. Attributes such as taste, flavour, ease of processing, low cooking time and low flatulence were more important factors for women than men who were more concerned about yield, and yield stability under various agroecological conditions.

The number of crops and varieties produced by a single seed producer group appeared to be small relative to numbers in farmers’ fields. However, given the multiple options for smallholder farmers to ensure access to seed, and the many considerations smallholder farmers have in choosing their crops and varieties (Joshi et al., 2006), the impact of “specialisation” on total crop diversity in the communities served can be regarded limited. When asked, seed producer groups did not consider the impact of their operations on total crop diversity. From a biodiversity maintenance perspective, the relatively small number of varieties marketed by the seed producer groups that farmers may choose from may negatively affect the total crop diversity in farmers’ fields. Such impact may be similar to the impact of limited crop and varietal choice offered by the formal sector on total crop diversity in smallholder agriculture.

Starter seed, production volumes and quality levels

Production volumes appeared to be determined by market demand, availability of suitable production fields, and access to starter seeds. Volumes differed to a large extent between groups. In 2020 and 2021 the five seed clubs interviewed in Vietnam jointly produced 2300 MT and 2000 MT rice seed per year, ranging from 90 to 1200 MT per year between individual groups. The share of the five seed clubs in the local market (village and community level) was more than 50% over a period of more than 10 years. Seed quality was informally inspected by local and provincial authorities, but not formally certified as a sizable proportion of the seed produced involved varieties under plant variety protection. Starter seed from which the seed clubs produced their own stocks were variously obtained from provincial seed centers and private seed companies.

By contrast, all four seed producer groups interviewed in Zambia produced QDS and/or certified seed. The annual production of the groups ranged from 12 MT to 32 MT for various crops. QDS was produced using third generation certified seed (Class3) or higher as starting material. In Guatemala, the smaller groups who produced bean annually supply an average of 2.5 MT of bean seeds, whereas the larger groups producing potato seed tubers delivered 240 MT of certified seed potatoes annually. Starting material (potato tubers) was obtained from the Institute of Agricultural Science and Technology (ICTA). The major differences in seed volumes produced seemed to reflect the roles that seed producer groups play and the markets that they serve locally.

Packaging and labeling

For most of the seed producer groups packaging and labeling presented a challenge, an issue that was obviously mostly relevant if a major portion of the seed was sold directly in local markets rather than to institutional buyers. Nevertheless, labeling appeared relevant since it shows the identity of the producer or producer group and knowing the identity of the producer and expected quality played a major role in local markets.

Some of the seed clubs in Vietnam did not package their seed at all but sold the harvested seed wholesale to the Provincial Seed Centers that also took care of drying the seed. For direct sales, most of the seed clubs packaged the rice seed in 40 kg per bag, according to seed packaging regulations, and in line with farmers’ preferences regarding this staple crop. Most bags remained unlabeled, since many varieties of which seed was produced were protected by plant variety rights. Unprotected varieties (e.g. those originating from IRRI) did get labeled, and all labels contained information on the producer groups.

In Zambia where institutional buyers absorbed a major share of the seed produced, legume seeds were packaged in 50 kg bags. Only in one seed production group, bags were tagged with names of the farmer producer for sales in local markets. In Niger, seeds were labeled, presenting the name of the crop variety and its characteristics, as well as the name of the seed producer group, year of production, and expected yield of the variety in farmers’ fields.

In Guatemala, potato seed was offered in 22 kg/50 pounds wooden boxes, for easy exhibition and movement, and in bags of 45 kg/100 pounds. Bean seed was offered in packages of 3, 5, 25 and 100 pounds. One potato group had started labeling, and in 2021 a label for product registration was introduced. On the label the following information was included: variety, weight, seed category, production date, code, or producer name. In general, the market required different package sizes, depending on to whom it was sold.

Setting seed price

The price of seed produced was set in either of two alternative ways: through contracts with institutional buyers before production onset, or at local marketing at the end of the production season by examining actual expenses (input costs) and current market prices. Contracting before and price setting at the start of the growing season appeared to limit market risks for the individual seed producer.

In Vietnam, most seed clubs produced under contract with seed centers and/or seed companies, whereas many individual producers sold smaller portions of their produce via kiosks, motorbike distributors and agro-dealers, in local and regional markets to individual farmer buyers. Local market prices would typically be proposed by the marketing subgroup and agreed with the group leaders. The price of seed produced by the seed clubs was considerably lower than the price of seed marketed by the private sector.

In contrast, in Uganda, the seed produced was primarily sold in local markets, often by members of the marketing subgroups, although NGOs would also buy and market part of the seed produced. The price of the seed would be set by considering actual production costs at the end of the growing season.

In Zambia, setting the seed price for local markets was largely the decision of individual seed producers, although actual sales could also be done collectively. In one group in Zambia, the enterprise Afriseed purchased all seed produced and provided starter seed. Other groups in the country also sold to seed companies, rendering the commercial sector the major buyer of the QDS produced by these groups. All groups except one negotiated the price for institutional buyers prior to the production process, in which process the supply of starter seed by the institutional buyer influenced the agreed price.

In Niger, a major proportion of the seed of pearl millet was marketed directly in local markets by the farmer producer groups, either collectively or individually. Quite exceptionally, for pearl millet the government appeared to determine the price through the Agricultural Market Information System, which was communicated by radio messages. In some cases, development, and relief partners (such as the World Food Programme) would buy all pearl millet seed. Institutional buyers purchased seed of both crops. A higher proportion of the cowpea seed was sold to private entities under contract.

In Guatemala, the price set for seed potatoes was largely based on production costs of previous years of growing potatoes for seed purposes. The local farmers’ cooperative to which the seed producer group members belong established the price through a payment agreement with the individual seed growers. Whereas the price of consumption potatoes fluctuated, the price for seed potatoes remained more stable since it was largely based on production costs.

Analysis of the seed/grain price ratio showed major differences between crops and countries. For example, the ratio for common bean is substantially different for Zambia and Guatemala, but similar for cowpea in Niger and Zambia. The lowest ratio is the one for rice in Vietnam, possibly explained by large production volumes and major competition, and highest for seed of maize OPVs. Table 4 provides an overview of the calculated seed/grain price ratios.

Seed-grain price ratio by crop and country.

Some groups mentioned that they did not ask a maximum price or a price set for commercially produced seed in the market, suggesting a social role, a position for which the members of the seed producer groups may obtain respect and status from their communities in return, and that may help them in securing external support from local authorities. This could explain the low seed-grain price ratios.

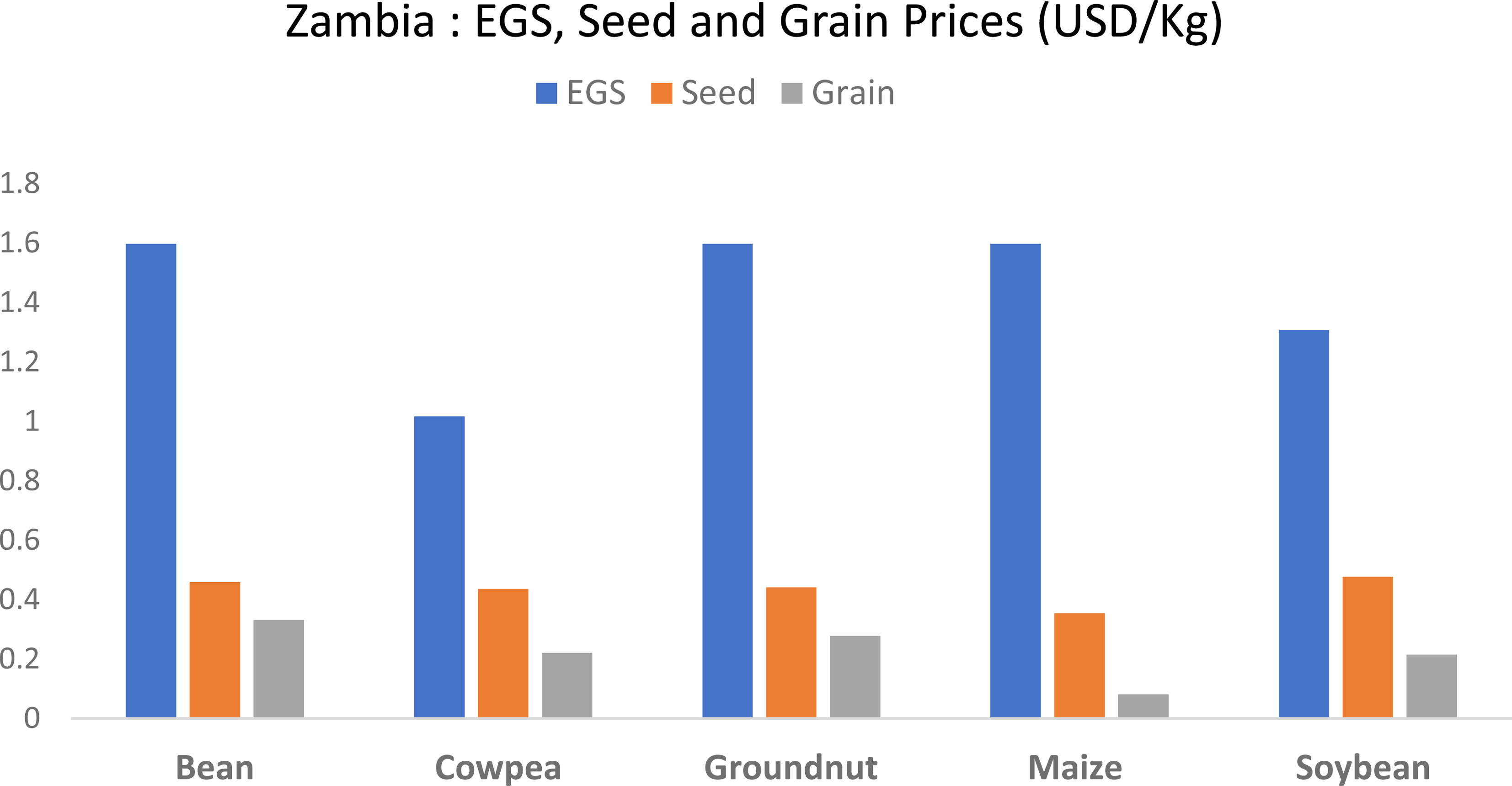

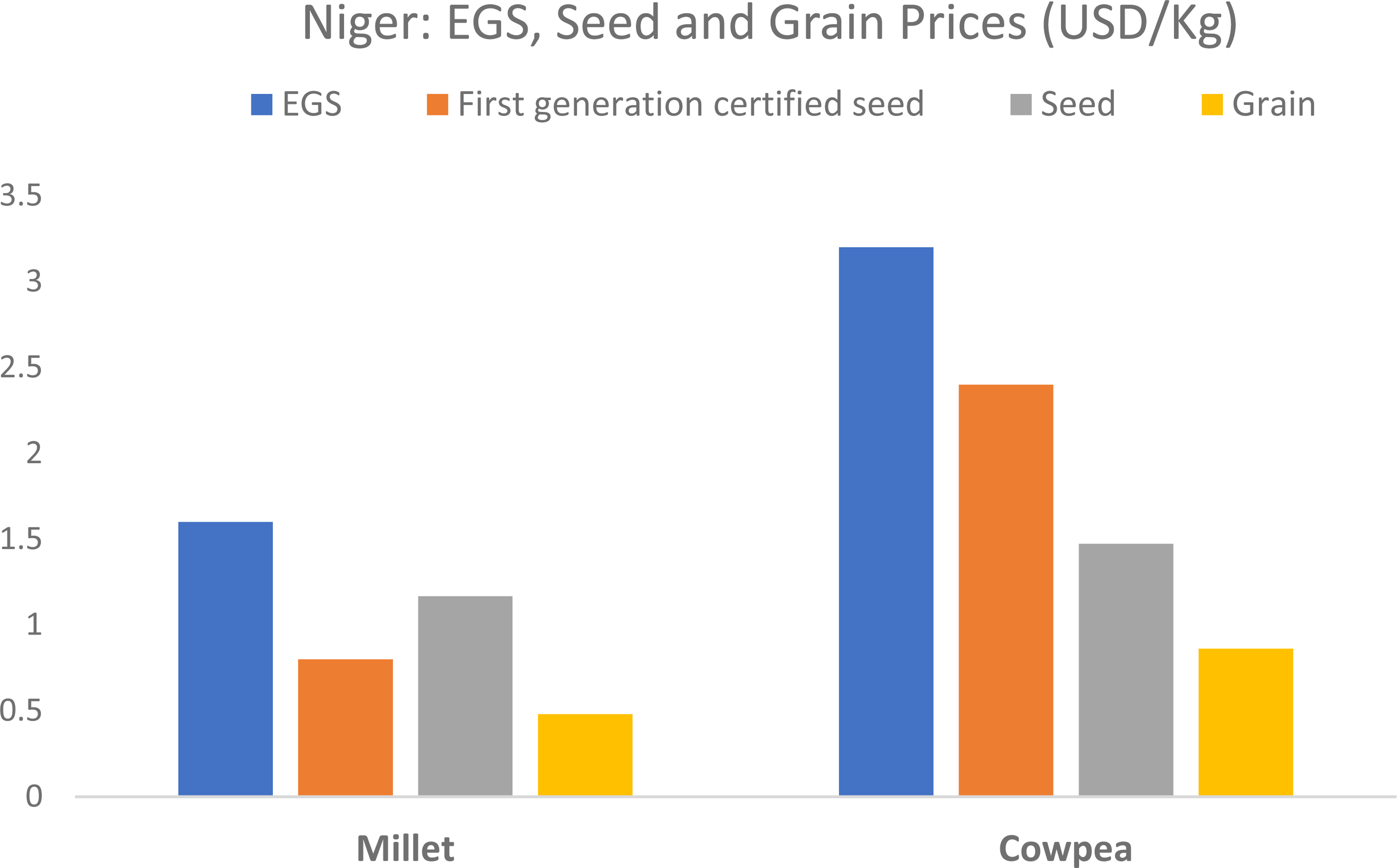

As detailed below a comparison between seed and grain prices on the one hand and the price that farmers pay for input seed on the other, revealed that in Zambia (Figure 1a) and Niger (Figure 1b) farmer producers were confronted with rather smaller margins distinguishing seed from grain prices in their local markets, whereas the price for starter seed they needed to start seed production appeared considerably higher. In Niger, either EGS or first generation of certified seed was used as starter input seed.

Comparing input seed, produced seed and grain prices in Zambia* *Note. Currencies were converted using https://www.xe.com/currencyconverter/ accessed on June 29, 2022

Comparing input seed, produced seed and grain prices in Niger* *Note. Currencies were converted using https://www.xe.com/currencyconverter/ accessed on June 29, 2022

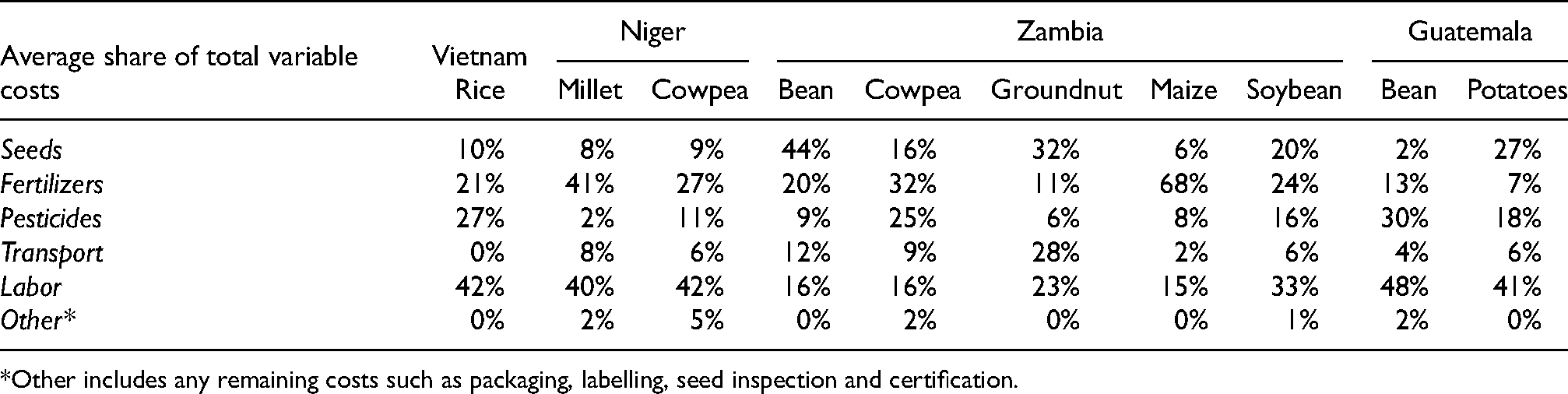

Somewhat surprisingly, a review of the costs of all inputs in seed production revealed that the share of costs for input seeds was relatively small compared to all other inputs. Table 5 below shows the shares of the input costs to total variable costs of production. SM Figures 2 through 5 in the supplementary material show these shares in more detail. The share of the costs of input seeds was much smaller than that of each other component, including fertilizers, pesticides, transport, and labour, and averaged at 10% of all input costs approximately, ranging from 2% to 44%. A partial explanation for this observation may be that starter seed provided under a contractual agreement is seemingly free of costs or provided at a subsidized rate, whereas for groups mainly producing for local markets special cost arrangements may apply as well. When comparing between crops and countries, seed costs were relatively higher for seed potatoes in Guatemala and for bean seed in Zambia, probably associated with higher production costs. An alternative explanation for differing price ratios between starter seed and output seed produced by the farmer groups may be differences in grades and qualities of the starter seed. In some cases, when the seed produced is collected by the buyers directly from the fields, transport costs are absent (example – Vietnam).

Support services provided to seed producer groups.

Average share of input costs to total variable cost of seed production (in %).

*Other includes any remaining costs such as packaging, labelling, seed inspection and certification.

In summary, revenues of farmer seed producers were modest, given the seed-grain price ratio was relatively low, probably since otherwise smallholder buyers would be averted from buying seed and turn to grain as production input instead. For many producer groups the price of input seed seemed not to be of major relevance, probably because the true price is either integrated in the seed produce selling price (when operating under contract) or subsidized in other ways, as in the case of seed provided by development organizations or public authorities.

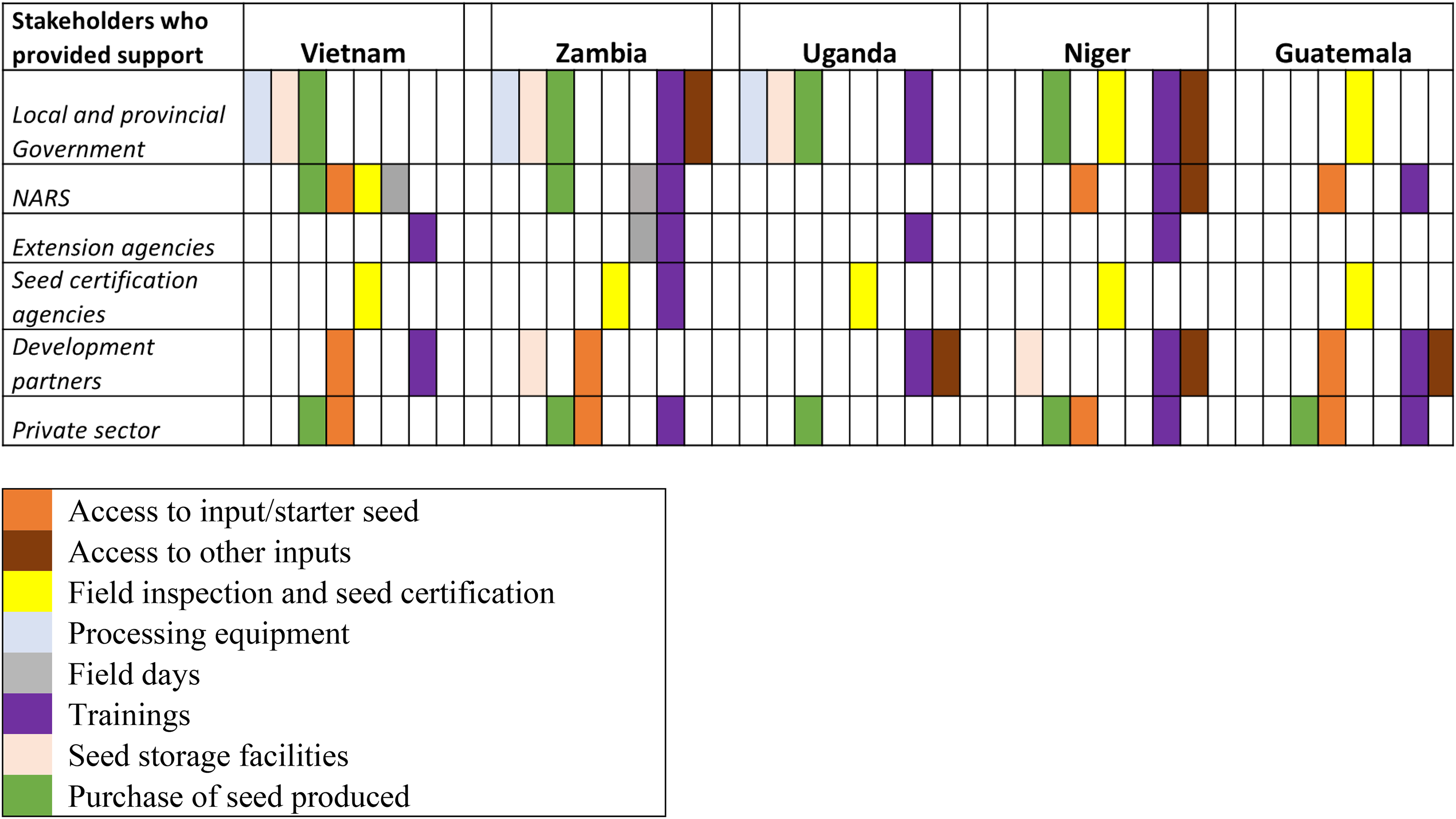

Roles played by external stakeholders

External stakeholders have routinely supported seed producer groups in various ways. Some of the same services were provided by different stakeholders across countries and over time, in particular the provision of trainings, of input seed, and of other agricultural inputs. Input seed was regularly provided by government agencies and programs (Vietnam, Uganda, Zambia, Guatemala), development organizations (Niger) and private sector seed companies (Vietnam, Zambia). In all countries, the seed produced by the farmer groups was purchased by multiple parties, both institutional buyers (seed centers, private companies, NGOs) and fellow farmers. Seed certification agencies inspected and certified seed lots to qualify for QDS and for regularly certified seed classes. An overview of support services is provided in Figure 2 below.

Strengths and weaknesses perceived by group members

When asked about their strengths, the members of the seed producer groups often mentioned their technical skills related to seed production, the support they obtained from fellow members, and good knowledge of crop and variety preferences of their fellow farmers. Access to trainings and to good-quality land were also regarded major assets of group members. Moreover, they mentioned their good reputation as seed providers in serving local markets and communities, and some reported that formal certification of seed lots might contribute to enhancing customer confidence.

Only some groups claimed a role in maintaining crop diversity and in coping with climate change effects in crop production in their agroecosystems. All groups reported as a main strength that they operate as a group and that they benefit from group spirit and a division of tasks within the group. Almost all seed producer groups reported that their operations are sustainable, except for few groups in Zambia and Guatemala. A group in Zambia had halted seed production by lack of access to input seed, whereas bean producing groups in Guatemala tended to gain very little profit over their seed sales, possibly caused by the low reproduction rates of bean seed.

The major weakness of many groups, in particular groups selling a major part of their produce in local markets, appeared the ability to deal with market fluctuations, in terms of volume demand, variety preference, and price received. Monitoring the market for changes in demand and price was deemed as a challenge for these groups.

In general access to all inputs was a challenge, but the severe one cited by all twenty-five seed producer groups in the study sample was access to sufficient volumes of starter seed on time. In most cases, the input seed was provided by either local research institutions, seed centers, development projects, and/or seed companies, often at low cost or as part of production contract arrangements. Only few groups produced their own input seed, e.g., for common bean in Guatemala and for pearl millet in Niger.

Furthermore, all groups found it a challenge to adequately package and label the seed produced. The implied cost of packaging seeds presented a barrier. Moreover, many producer groups were not aware of labeling options and requirements, or failed to recognize potential advantages of proper labeling, and were unable to arrange for labeling due to lack of labeling material and packaging equipment (such as sewing machines).

A typical challenge in Vietnam appeared that the seed clubs interviewed (as well as many other seed clubs in the Mekong Delta), produced seed of varieties under plant variety protection, a situation accepted by the regional authorities because of the major share of the seed clubs play in the overall rice seed production for the Mekong Delta (Tin et al., 2011).

Some of the challenges mentioned above became apparent only when development projects ended. For example, the provisions created by projects to access starter seed (or EGS) often did no longer function once development project support was discontinued.

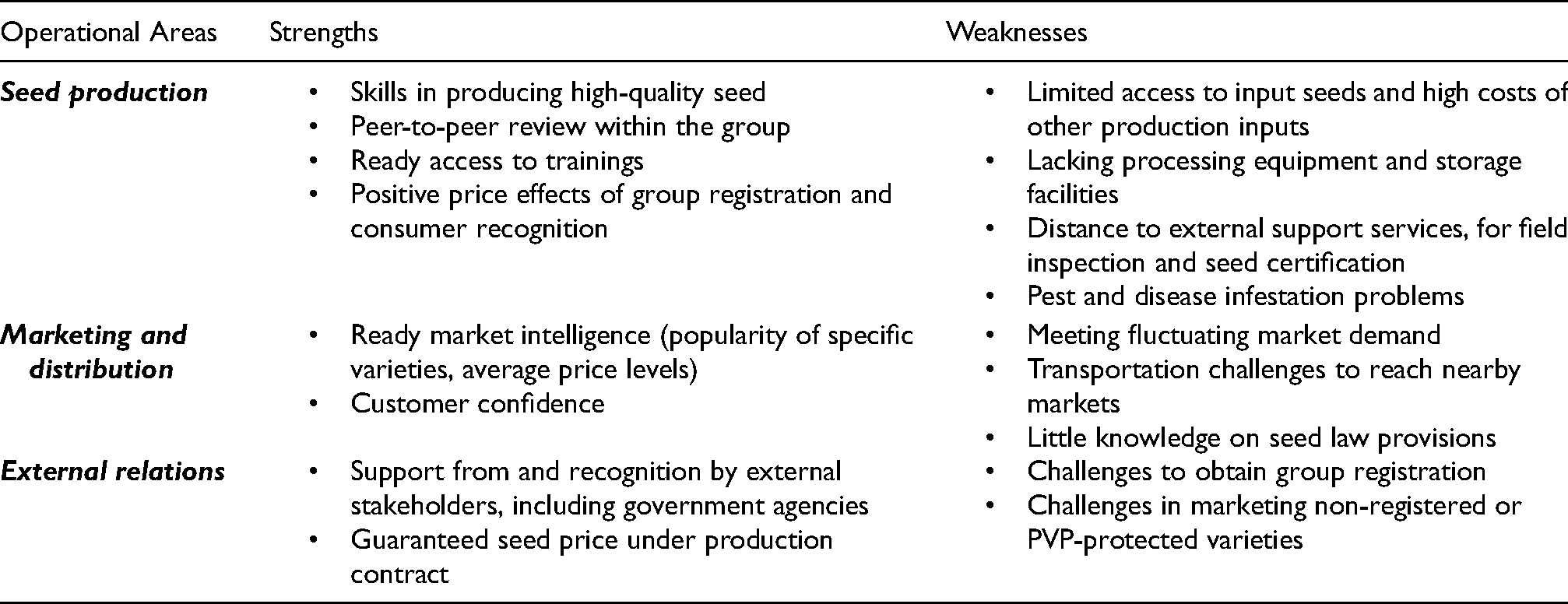

Table 6 provides an overview of all major strengths and weaknesses as identified by the members of the seed producer groups.

Strengths and weaknesses identified by seed producer groups.

Coping mechanisms during COVID-19 pandemic

Government measures to contain the Covid-19 pandemic affected the operations of farmer seed producer groups in each of the countries. Travel and meeting restrictions temporarily halted group meetings, which often delayed group decision-making. In some cases, producer groups were able to meet in smaller groups, and peer review continued by use of mobile phones or tablets. Furthermore, field inspections by certification authorities were delayed or cancelled, affecting the marketing of the seed produced. Travel restrictions also hindered sales to institutional buyers, causing the producer groups to look for alternative outlets in local markets and/or to reduce seed production levels, and as a secondary response to adapt the crop portfolio. In some cases, due to supply chain disruptions, input prices (labour, chemicals) increased, causing a reduction in net income from seed sales, and occasional disruption of group activities. In summary, the pandemic did severely affect group operations, but also provoked appropriate responses of the seed producer groups thus adapting to circumstances caused by the pandemic.

The impact of national seed policy and legislation

Seed producer groups surveyed recognized that seed regulations affect their work, but the exact nature of these impacts and their basis in policy and legislation was insufficiently clear. Most farmers involved appeared to have a limited understanding of what is allowed or obliged under current seed policy and legislation. This resulted in guesswork without a proper understanding of rights and restrictions to produce, label, and market seed. Trainings seemed to pay insufficient attention to legal and policy issues, although some groups (for example, in Vietnam) noted the need for greater collaboration amongst farmers, researchers, and government agencies to deal with legal requirements. The limited access to and interaction with government seed inspectors seemed to maintain this problem in all countries under the study. In Vietnam the tension between the use of protected varieties by the seed clubs and plant variety protection legislation was recognized but unresolved.

Discussion

As experienced smallholder seed producers have since long been major providers in local seed markets (Thijssen et al., 2008; FAO, 2010; Louwaars & De Boef, 2012; McGuire and Sperling, 2013, 2016), one may argue that seed producer groups only exhibit a next level of organisation rather than a higher level of seed production capacity. Self-organisation as described in this study may strengthen the role and position of smallholder seed producers in the seed value chain (e.g. in accessing input seed, obtaining training, improving on quality, increasing market access) and this potential warrants investment in their capacities as outlined above and discussed below. The higher quality and larger volumes of the seed produced distinguish seed production in organized groups from family-based seed production and marketing.

This study provides detailed information about the functioning of 25 smallholder seed producer groups operating in five countries with diverse agro-ecosystems, national economic development levels and policy and legal contexts. All groups were selected based on prior contacts with development organizations, and these have supported the establishment of the seed producer groups based on a keen interest in the communities concerned to engage in seed production and marketing. Therefore, although current support from these organizations was limited (or even absent as in the case of Vietnam), the results presented above sketch some major features of smallholder seed production but cannot necessarily be taken as representative for the average smallholder seed producer group worldwide.

Much of the success of the farmer seed production groups appears to depend on social cohesion of the group as well as proper training and further support by external stakeholders, and the ability of producer groups to access markets and respond to market demands. As seen in Table 4 above, these groups could function with smaller price margins and therefore could cater to a wider range of crops and varieties that profit-maximising private sector entities might hesitate to offer. National policy and government support set further conditions for the potential of seed producer groups. Groups appeared to be self-confident and mostly economically viable and have often been in existence for many years. Major challenges included reliable access to input seed as well as to other production inputs, and the ability to sell the seed either in local markets or to institutional buyers. The long history and intermittent support levels currently provided to most of the interviewed groups by development organisations suggests a high level of sustainability of their operations.

In comparing the various seed producer groups, some similar features stand out. All groups interviewed have established bodies and procedures arranging for peer field monitoring and inspection of the standing crop and the harvested seed, as well as for processing and marketing activities. Furthermore, all groups show self-confidence, and exhibit a strong group feeling, and almost all perceive their efforts to be economically sustainable. All farmer producer groups use part of their own produce for use at the own farm, sell a sometimes limited, sometimes major volume in local markets, whereas some groups engage in production contracts with public or private entities. We were unable to establish to which extent the seed producer groups also fulfilled a social function, by offering their fellow farmers seed at an affordable price. The recent spread of the Covid-19 pandemic may have convinced more stakeholders of the advantages of short seed supply chains and the role that farmer seed producer groups fulfil in situations in which timely transportation of adequate seed volumes is uncertain (Sperling et al., 2020b).

The trait preferences of men and women interviewed in our study clearly differed based on different roles that men and women tend to play in the household, as has been reported before (SDC, 2021). However, gender influences the opportunities of female and male seed producers in various ways beyond trait preferences. Only few women have the necessary enablers including land title, access to credit and input supplies, as well as to information and technology (Ojiewo et al., 2018) to independently act as seed producers. Whereas this issue was not specifically addressed in our interviews, secondary information based on prior involvement with the communities in which the seed producer groups operate, tends to confirm that the influence of gender reaches beyond processing and diets and into civil rights of women in general.

Reliable access to input seeds in developing countries has been reported before as a wider challenge, and apparently is not typical for smallholder producer groups but a bottleneck for all seed producers (De Boef et al., 2016; Cramer, 2019). Our findings only reconfirm how this situation hampers not only seed production in the private and public sectors but also in smallholder seed production. One can only expect that it will also limit the options for smallholders individually producing seed for local markets.

In addition, our results show that the interviewed producer groups were supported by various stakeholders in multiple ways and appeared to be well-connected. It can be assumed that this ability to connect is essential for the sustainability of the seed production groups. In this context, it is of major relevance that a sizable number of the groups are contracted to produce seed by institutional buyers, which will have an interest in the capacity of the producer groups involved to produce high-quality seed. Our results show that these contractual buyers may provide trainings, input seed and other necessary inputs, and may be involved in field and seed inspection, and encompass the public and private sectors as well as civil society.

Another group of major stakeholders of all seed producer groups consist of entities with an interest in and/or responsibility for high-quality seed for food production purposes and in regional development. Our findings suggest that strong support is often provided by local governments, probably fuelled by direct exposure to the roles that seed producer groups play, to the positive livelihood effects and to personal connections. Support from the national government takes place through agencies and public institutions, in particular extension services, universities, and breeding institutions. External support is of major importance for the development and sustainability of farmer seed producer groups (David, 2004). Finally, seed certification agencies are involved on a formal basis, and whereas access by smallholders to these agencies appears not always to be straightforward, these agencies play a role in helping individual farmers to meet the conditions set for seed certification.

Our results confirm that national seed laws set stringent conditions to smallholder seed production and marketing, as has been reported before (Herpers et al., 2017; De Jonge et al., 2020). Like in most countries, the seed laws in the countries involved set stringent conditions to either the identity and capacity of seed producers (education, access to processing and storage facilities), as well as for varieties to be formally registered to be marketed, and these conditions may be difficult to meet and only with support from some of the external stakeholders. In that context it is relevant that local governments in Vietnam and farmers’ cooperatives in Guatemala provided seed producer groups with access to facilities, whereas institutional buyers often provided input seed of registered varieties. Interestingly, whereas timely availability of inspectors for the purpose of formal certification of the produced seed was reported as a challenge, meeting the certification requirements was almost invariably within reach of the individual members of all seed producer groups. Based on the above, we argue that national seed laws still need adaptation in recognition of the role of smallholder seed production in contributing to national food and nutrition security. In the past, an increased role of smallholder seed production has met resistance based on the assumption that such seed would not be able to meet minimum quality requirements.

More recent research into the quality of seed produced by smallholder farmers has shown that purity and germination rates of farm-produced seed were not significantly different from that of formal sector seed (Bishaw et al., 2013; Kusena et al., 2017; Ndinya et al., 2020), and showed absence of major seed pathogens (Kusena et al., 2017). Given reports on poor and inconsistent relationships between molecular data, variety names and morphological traits in several crops and countries circulating in smallholder agriculture (Maereka, 2020). more attention for proper labeling and regular checks on seed identity may further improve the quality of seed produced by smallholder farmers.

External stakeholders should seek ways to leverage smallholder seed production capacity by promoting options for decentralized seed quality inspection and seed certification to tackle the bottleneck of insufficient numbers of seed certification agency inspectors. Alternatively, national seed policy and legislation may include options to allow for producer-assured labeling and truth-in-labeling of the seed produced, especially under circumstances where seed producers and fellow farmers customers tend to be known to each other.

Another major challenge, for groups that produce to a substantial extent for local seed markets, is the limited knowledge about proper packaging and labelling of the seed, allowing proper branding of its produce by the seed producer group. Branding will allow individual groups to strengthen their position in existing marketplaces and to access wider markets, in case customers do not personally know the seed producer(s), but instead depend on the status of the brand name. Labelling of seed with adequate information about its attributes allows traders who play a role in accessing such wider markets (Sperling et al., 2020a), whereas larger markets served by smallholder producer groups will also increase their potential importance as providers of improved varieties containing novel traits moving, including in remote markets. Generating awareness and providing training on what is required and allowed to be included on the label, how both packaging and labelling may increase market share and income and providing infrastructure and capital (such as sewing machines and printing devices), which could even create off-farm employment opportunities, seems of major importance. Improving market transparency and highlighting and discussing the seed-grain price ratio with both seed producers and farmer buyers may help both improved quality production of existing varieties and the diffusion of new varieties. Development partners and international organizations may seek to support market intelligence needed by seed producer groups, allowing the groups to adequately respond to changing customer preferences and to seek ways to diffuse varieties with new traits based on customer needs and preferences.

Conclusions

This study reports the close linkages between smallholder seed producers on the one hand, and actors in the public, private and civil society sectors on the other, and how input seed as well as seed produced by smallholders pass between each of those sectors. In other words, it shows how at the local level the lines between the public, private and civil sector, as well as farmer producers, between the formal an informal sector become blurred. The dichotomy between formal and informal seed systems disappears in farmers' fields.

Strengthening the ties between all these actors appears crucial to facilitate smallholder seed producers to access good-quality input seed of existing and new varieties and to scale up local seed production. Sustainable partnerships driven by market incentives would ensure continuity long after development projects end. Seed of varieties that are pest and disease-resistant, stress-tolerant and climate change-resilient, those that exhibit culinary properties like easy processing, short cooking times, and good taste should - steer varietal choice by seed producer groups, guide government agencies and research institutes focusing on input seed supply, and provide input to international and national breeding institutes in developing the product profiles of new varieties.

The major role of formal seed sector actors in providing such seed should be considered (1) in reviewing mandates and budgetary resources of government agencies involved, including agricultural research and breeding institutes, extension agencies and seed centers, (2) in private sector strategies involving smallholder seed producers, and (3) in elaborating support by the National Agricultural Research Systems.

Supplemental Material

sj-docx-1-oag-10.1177_00307270221115454 - Supplemental material for Strengths and weaknesses of organized crop seed production by smallholder farmers: A five-country case study

Supplemental material, sj-docx-1-oag-10.1177_00307270221115454 for Strengths and weaknesses of organized crop seed production by smallholder farmers: A five-country case study by B Dey, B Visser, HQ Tin, A Mahamadou Laouali, N Baba Toure Mahamadou, C Nkhoma, S Alonzo Recinos, C Opiyo and S Bragdon in Outlook on Agriculture

Footnotes

Acknowledgements

The authors wish to thank the generous inputs by the smallholder seed producers interviewed for this publication. Part of this work was funded by the United States Agency for International Development (USAID) under Agreement 7200AA18LE00004 as part of the Feed the Future Supporting Seed Systems for Development. Another part of the work was funded by the Swedish International Development Cooperation Agency Sida (grant number 1001534) and fits in the Funding Strategy of the FAO International Treaty on Plant Genetic Resources for Food and Agriculture. Any opinions, findings, conclusions, or recommendations expressed here are those of the authors alone.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Styrelsen för Internationellt Utvecklingssamarbete, United States Agency for International Development, (grant number 1001534, 7200AA18LE00004).

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.