Abstract

Based on a media analysis and a manager survey, we investigate past and intended future strategies of farm supply and grain marketing businesses in Germany. Alliances, diversification and organic growth were among the most popular past strategies and, according to the participants, will be in the future. Nevertheless, the trend towards divestment and fewer locations for grain collection will continue. Large, investor-owned firms prefer a combination of capital-intensive strategies, cooperatives and small and medium-sized enterprises plan to adopt fewer strategies. We outline several potential implications and areas for further research.

Introduction

Farm supply and grain marketing businesses play an important role in mediating between agriculture and industry (Gollisch et al., 2018). 1 They fulfil two central functions: The supply business, that is, selling agricultural inputs to farmers, and the sales business, that is, purchasing crops from farmers. The environment in which agricultural trading firms operate is currently undergoing major changes (see also Batte and Ernst, 2007). This development is also true for Germany and becomes evident in different areas: Firstly, the number of firms continuously decreases while the traditional division into wholesale and retail level seems to dissolve (Bundeskartellamt, 2014). Secondly, structural change in agriculture is leading to fewer and larger firms doing business with agricultural traders. In the course of these developments, agricultural trading firms need to find a strategic orientation. To date there has been little agreement on what a promising strategy for agricultural traders is. Growth, internationalization, diversification and differentiation are much discussed concepts (Gollisch et al., 2018). Besides that, service profiling of the firms is considered important to achieve high customer satisfaction and thus to remain a trading partner for farmers. Otherwise, farmers could start doing business directly with input producers or buyers of cereals (Schulze, 2012). More recently, special attention is being paid to the increased online agricultural trade and its effects on the industry (Batte and Ernst, 2007; Fecke et al., 2018; Zeng et al., 2017). A growing body of research recognizes the need to understand possible consequences of structural change within agriculture and the food processing industry for agricultural traders’ strategies (Gollisch et al., 2018; Höhler and Kühl, 2014; Schulze, 2012; Sexton, 2013).

The few existing studies on agricultural traders’ strategies provide contradictory results. Harling and Funk (1987) identify four attributes of strategies: focus, differentiation, cost leadership and firm size. Based on data on 170 U.S. agricultural trading firms, they show that most firms pursue similar competitive strategies (Harling and Funk, 1987). Höhler and Kühl (2014) analyze strategies of cooperatives in the cereal sector in the EU-27. Half of the firms pursue cost leadership, while 32% aim for differentiation, and 19% for focus. Growth is achieved primarily organically or through domestic merger and acquisition. Gollisch et al. (2018) argue that the structural changes in agriculture leave traders with a limited set of strategies, namely cost reduction or differentiation. They use a discrete choice experiment to categorize strategies. According to their analysis, the majority of the traders would choose a service-oriented or hybrid strategy rather than cost or price leadership. They also divide the surveyed traders into three segments: the “conservatives,” the “service providers,” and the “scale-driven traders.” While the “conservatives” prefer intensive business relationships with rather small farms, the “service providers” focus on offering a high level of service to relatively large farms. The “scale-driven traders” are the group most likely to target business growth (Gollisch et al., 2018).

Surprisingly, the effects of different organizational forms and firm sizes on the strategic position of agricultural trading firms have not been investigated. Research on small and medium-sized enterprises (SMEs) in other sectors has established that they face disadvantages compared to larger firms in terms of both strategic planning and financing growth (Beck and Demirguc-Kunt, 2006; Burke and Jarratt, 2004; Carpenter and Petersen, 2002; Rostamkalaei and Freel, 2016). Due to resource constraints, smaller firms tend to adopt niche strategies, that is, they often try to act as specialized providers for a limited region, a limited number of customers, or a limited product or service portfolio (Bishop and Megicks, 2002; Lee et al., 2001; Wernerfelt and Karnani, 1987). With regard to the differences between organizational forms, it is often assumed that cooperatives and investor-owned firms (IOFs) pursue different objectives (Soboh et al., 2009). While cooperatives seek to benefit their members, IOFs strive to maximize profits. These different objectives could result in different strategies for their businesses (see also Parliament et al., 1990).

A main challenge faced by many researchers is the dynamic nature of strategies. Mintzberg’s (1987) interpretation of strategies as patterns implies that strategies are often only recognizable afterwards as patterns of actions. These actions are both part of the intended strategies of the management and partly emergent. As a result, a comprehensive investigation of strategies as a pattern requires the examination of both actions taken and intended actions. This paper attempts to describe the development of strategies of agricultural trading firms. We are mainly interested in two questions. Firstly, how have the strategies of agricultural traders evolved over time? Secondly, how may strategies develop in the future? Based on the structural developments mentioned above, we assume that product and service differentiation have become more important and will continue to become more important for firms in the future. Based on the above mentioned literature on SMEs and cooperatives, we expect differences between IOFs and cooperatives as well as between SMEs and large firms.

The methodological approach taken in this study is a mixed methodology based on a media analysis and a survey. Our first goal is the description of the past strategic positioning of agricultural trading firms. Thereby we show the evolution of past strategies and also gain a deeper understanding of the industry context (Molina-Azorin, 2012). Like Höhler and Kühl (2019), we understand strategies as the sum of strategic actions. Hence, we analyze 2738 newspaper articles about actions of the nine largest German agricultural trading firms for our strategy analysis. Our second goal is to complement the identified implemented strategies with managers’ assessments on the future. Therefore, managers of agricultural trading firms were surveyed about their intended strategies. The survey results serve to answer our second research question, that is, to show how strategies may develop in the future. We examine differences in intended strategies between firm sizes and organizational forms.

Prior research on agricultural trading firms’ strategies provides contradictory results and neglects the fact that strategies develop over time (Gollisch et al., 2018; Harling and Funk, 1987; Höhler and Kühl, 2014). In addition, no distinction is drawn between the strategies of SMEs and large firms, as well as between IOFs and cooperatives. To the best of our knowledge, this is the first study to undertake a longitudinal analysis of strategies of agricultural trading firms. A detailed examination of their strategies contributes to a better understanding of the sector dynamics and the firms’ reactions to structural changes. The development of strategies is of interest not only to researchers in the fields of strategic management and agricultural economics, but also to competitors within the sector.

The paper proceeds as follows. The following section will examine the relevant literature. Section “Data and method” is concerned with the data and methodology used for this study. Section “Results” presents the results of the media analysis and the survey as well as a comparison. The paper ends with a discussion and conclusion.

Review of the relevant literature

Theoretical background

The strategy term has various definitions. In game theory, the term strategy describes a complete plan in which the decisions to be taken for all possible situations are already determined in advance (Von Neumann et al., 2007). According to Chandler (1990), strategies consist in the definition and pursuit of long-term corporate goals and the associated actions and allocation of resources. Mintzberg (1987) describes strategies as a consistency in behavior. It is even irrelevant whether this consistency was planned ex ante (“deliberate strategy”) or whether it was unplanned (“emergent strategy”). His view of strategies as patterns implies that strategies can be identified in retrospect as patterns of strategic actions. Ansoff (1957) refers to product–market combinations of firms and names market penetration, market development, product development, or diversification as possible growth alternatives (“product-market strategies”). In addition to these growth-oriented strategies, firms may also divest if certain markets decline (Harrigan, 1980).

Porter (2008) distinguishes three generic strategies: cost leadership, differentiation, and focus. In the case of cost leadership, the competitive advantage originates from low costs. In the case of differentiation, the firm offers unique products or services. Focus describes a situation in which a firm focuses on individual customer segments. Porter (2008) argues that a firm can only pursue one strategy at a time because strategies require different strengths and resources. However, there is also evidence that a combination of different strategy types, a hybrid strategy, results in higher performance (Claver-Cortés et al., 2012).

While strategies aimed at achieving competitive advantages over competitors within individual business areas can be called “Competitive Strategy,” the term “Corporate Strategy” refers to the strategic orientation of the entire firm. This orientation includes questions about the business areas in which a firm should operate and how the firm is organized (Porter, 1989). Common to all considered ideas of corporate strategies is that they aim at maintaining or improving the success of the firm. According to the “Resource-Based View,” which was essentially coined by Barney (1991), firms can achieve sustainable competitive advantages by identifying and using internal strategic resources. Achieving competitive advantages is possible by executing value-creating strategies that are not also implemented by competitors. The implementation of such strategies requires the deployment of the firm's own resources. In this model, strategic resources are the source of unique strategies and sustainable competitive advantages. In this way, each firm can have its own strategies, which may also change over time.

Empirical research

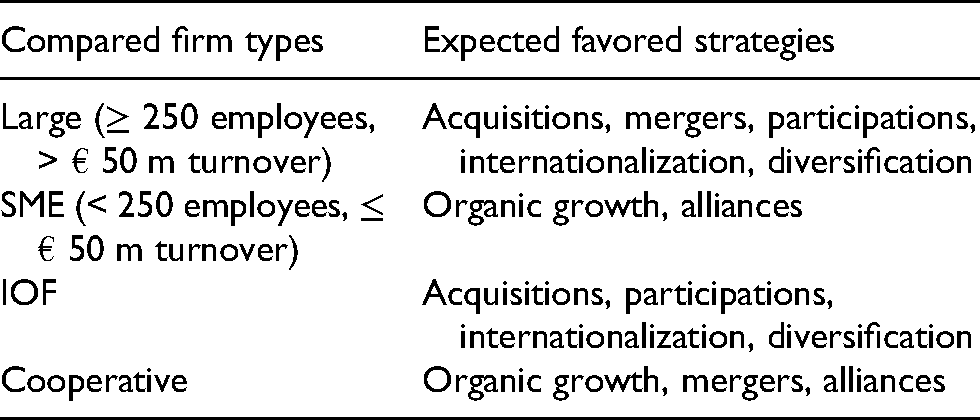

Previous research has established that SMEs focus on niche strategies (Bishop and Megicks, 2002; Lee et al., 2001; Wernerfelt and Karnani, 1987). Because of SMEs’ financial constraints, we assume that they consider incremental or low-cost strategic actions to be more promising. In contrast, more risky or capital-intensive strategic actions (acquisitions, mergers, shareholdings, internationalization, and diversification) tend to be preferred by large firms. Cooperatives and IOFs pursue different objectives (Soboh et al., 2009). We assume that strategic decisions of the cooperative aim at optimizing the procurement of inputs for the local members as well as the marketing of the harvested products. As a result, diversification into new business areas and internationalization could be unattractive steps. Instead, we assume that these are more likely to be pursued by IOFs if they allow the maximization of profits. Previous studies indicate that cooperatives do not pursue equity-intensive strategies such as acquisitions or participations, preferring instead mergers, joint ventures and also other cooperative arrangements. In contrast, IOFs prefer acquisitions and participations, or increases in existing participations (Hardesty, 2005; van der Krogt et al., 2007). Further, cooperatives often appear to be less diversified than other organizational forms (Hendrikse and van Oijen, 2002). Based on the existing evidence, we assume alliances, organic growth and mergers to be particularly frequent strategic actions for cooperatives. For IOFs, acquisitions, diversification and internationalization are more likely to be observed, in line with the literature. Table 1 lists the strategies we expect to be preferred by firms of different sizes and organizational forms.

Expected differences between agricultural trading firms of different size and organizational form.

In the following, we conduct both a media analysis and a survey of strategic actions.

Data and method

Media analysis of past strategic actions

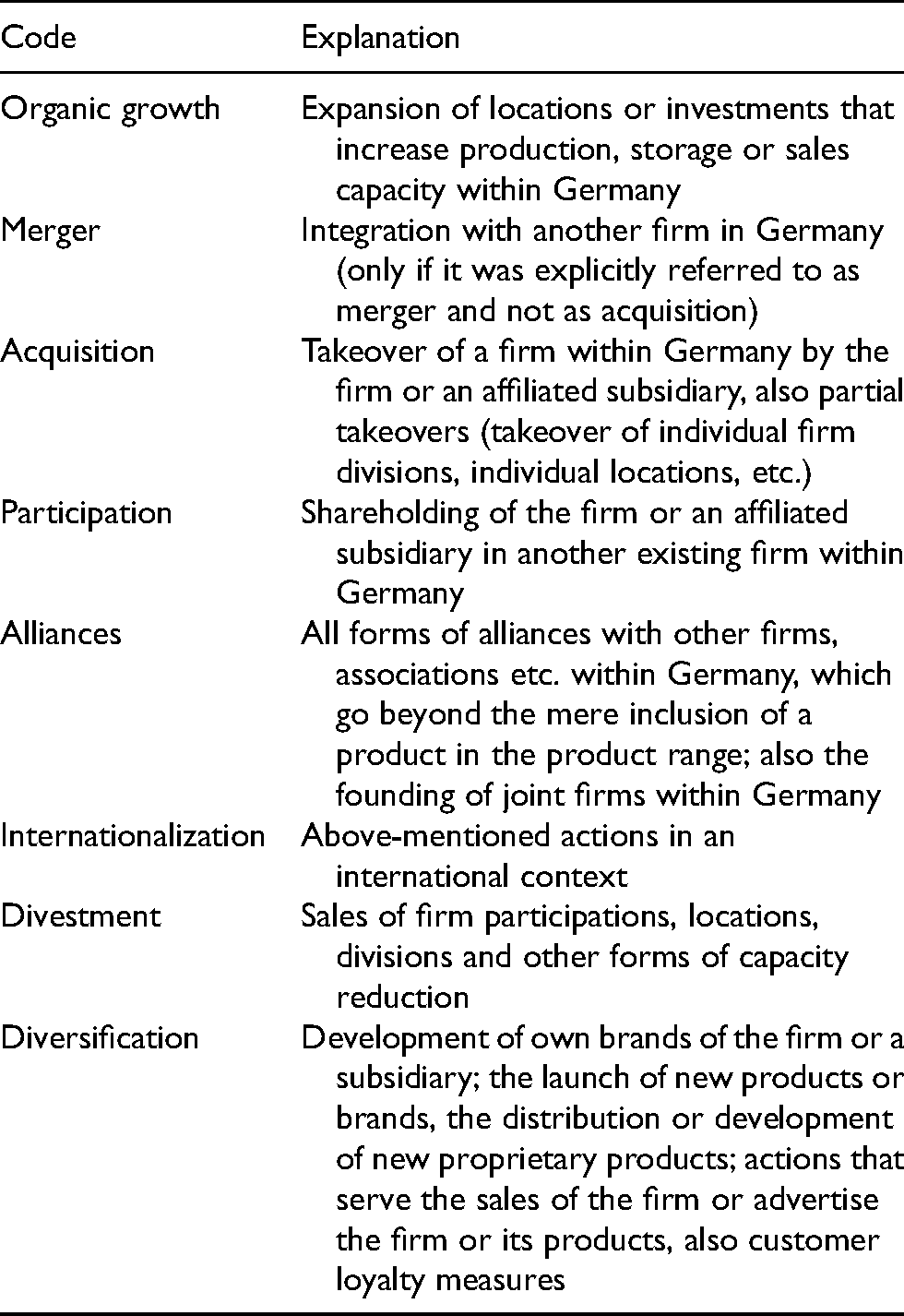

Data for this study were collected using a search portal for newspaper articles. The search was limited to articles published in “Agrarzeitung,” a trade journal that is widely distributed in the industry and regularly reports on strategic actions of the firms. A small sample of large firms was chosen because of the expected difficulty in obtaining full information on the strategic actions of smaller firms. Therefore, the names of the nine largest firms were entered as search terms (BayWa, Agravis, HaGe, RWZ, Raiffeisen Waren GmbH, ZG Raiffeisen, Beiselen, ATR, Getreide AG). A total of 2738 newspaper articles were found. All articles published between 1 January 2010 and 31 December 2019 were analyzed. The time span was chosen with regard to the subsequent survey of managers, which also covers a period of 10 years. The content of each article was screened for information on one or more strategic actions of one of the firms. To classify the strategic actions, categories were formed to which the different actions were assigned as codes. The selection of the relevant actions is based on existing work (Gollisch et al., 2018; Harling and Funk, 1987; Höhler and Kühl, 2014). Following Ansoff (1957), we distinguish between market-oriented actions (organic growth, mergers, acquisitions, participation, alliances, internationalization, and divestment) and product-oriented actions (diversification). Table 2 provides an explanation of the different codes:

Coding of the strategic actions.

Mentions of strategic actions were manually coded by a research assistant according to a previously developed manual (e.g. see Appendix Table A1). Actions were assigned to the year in which they took place. Some actions were given multiple codes. If, for example, the joint distribution of a new product was started in an alliance with another firm, this action was coded as “diversification” and as “alliance.” However, to avoid duplication, the same event was only coded once if it was mentioned several times. In total, 628 actions were coded.

Survey of intended strategic actions

For the second part of the study, we developed a questionnaire on the basis of the relevant literature and an expert interview with a former manager of an agricultural trading firm. The aim of the survey was to complement the results of the media analysis with an assessment of managers’ opinions on intended strategies. To ensure that the questionnaire was understandable and given answers would be meaningful, the survey was tested with a representative of an agricultural trading firm. The survey was conducted as an online survey, mainly due to its easy distribution. The link was distributed in 2020 via a newsletter of a training firm for staff of agricultural traders and to a list of firms collected via a web search. A reminder was sent in both cases. As a result of the data collection, it is not possible to determine the number of firms reached and the response rate. As an incentive for participation, a report with the most important results was offered.

The questionnaire was divided into four parts:

General information on the firm. Participants should provide information on the size and legal form of their firm as well as their position within the firm. Developments in the next 10 years. Statements were developed both from the previous media analysis and from the expert interview. The statements should be evaluated by the participants for their firm on a scale with the points “increases,” “stays the same,” and “decreases” (see also Appendix Table A2). Strategic actions of the respondents’ firms. Different strategic actions should be evaluated according to the time horizon in which they were perceived as relevant for the firm. The different time horizons (3, 5, or 10 years) should reflect a short, medium, and long-term period. In addition, it was possible to indicate that strategies were not relevant (see Appendix Table A3). Possible future developments in the industry in general. Participants were asked to express their agreement to previously developed statements on a six-point Likert scale (see Appendix Table A4).

A total of 83 persons took part in the survey, 62 persons completed the survey. The number of respondents is somewhat lower than in Gollisch et al. (2018) but represents at least 10% of the total population according to their data. Most of the participants (57 persons) indicated to be the managing director or to have management responsibility. The sample includes small enterprises (1–4 employees and 0–4.9 million euro turnover), medium, and large enterprises (over 250 employees and over 500 million euro turnover). Most of the firms operate under the legal form of a cooperative or a limited liability company. Of the 62 firms, 20 classify as Non-SMEs while 42 classify as SMEs. The sample consists of 17 cooperatives and 45 IOFs. We compare the strategic actions across firm sizes and organizational forms by using Pearson's Chi-squared tests.

Results

Media analysis of past strategic actions

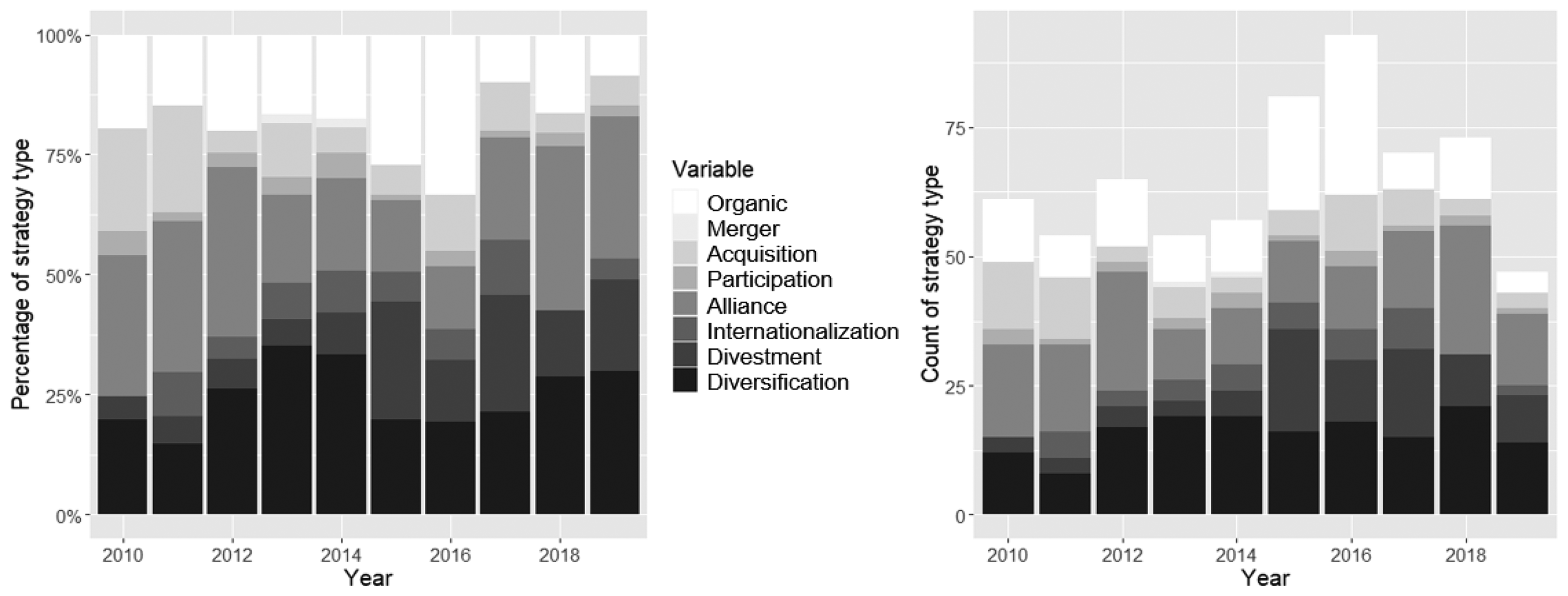

First, we examine the distribution of the total number of strategic actions over time. Figure 1 shows the share and total number of the different strategic actions over the years. Among market strategies, alliances seem to dominate in most years, followed by organic growth. Diversification also occurs frequently in all years. Trends can be seen with regard to divestment and acquisition. While acquisitions tended to decline in the second half of the period under review, divestments increased during this period. No clear trends can be identified for the other strategies.

Distribution of strategic actions per year and per category, percentage and count.

Survey of intended strategic actions

In part 2 of the survey about developments in the next ten years, most of the managers indicated that personnel costs (40 out of 62), the provision of digital services (54 out of 59) and cooperation with non-cooperatives (32 out of 54) as well as with cooperatives (32 out of 52) will increase. 2 The majority plan to increase the number of business lines (27 respondents) or to keep it constant (22 respondents). The answers do not give a clear picture of the future development of traded volumes, sales, margins, and profits. While some respondents assume increasing figures, others anticipate stagnation or decline. The results are clearer in the case of planned strategic actions. The majority of the participants (30 out of 55) expect to reduce the number of locations for grain collection in the future. Only four managers are planning to reduce the range of consulting or digital services.

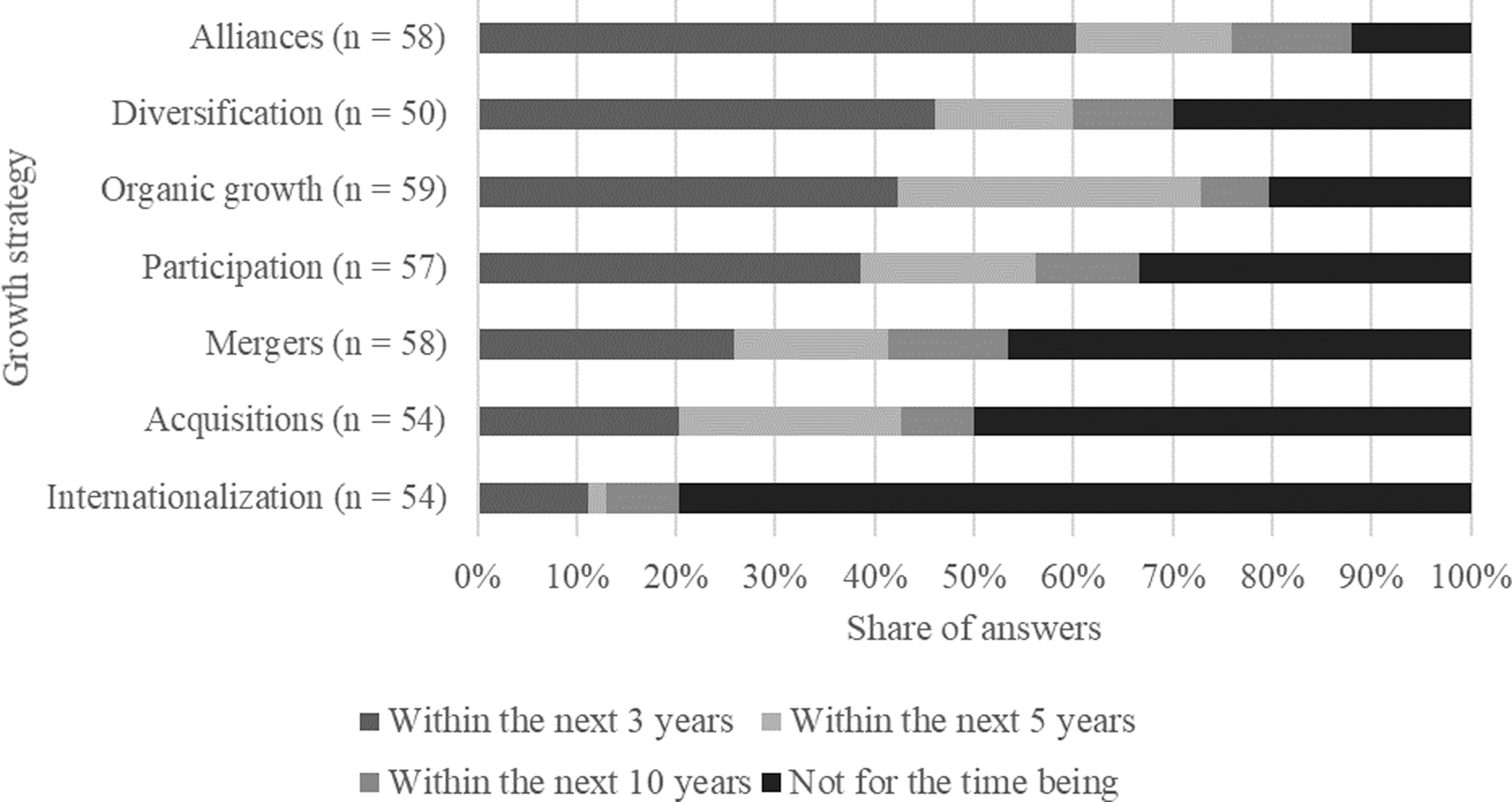

Asked about strategic actions for the next ten years in part 3 of the survey, participants favored alliances (see Figure 2). In contrast, internationalization was the least preferred strategy. The majority of the firms represented are aiming for organic growth in the short and medium term (i.e. in 3 and 5 years). More diversification is expected to occur in the short term as well as in the medium and long term. Approximately 50% of the participants perceived mergers and acquisitions as promising for their firm within the next ten years, while a similar share stated that they have no such plans.

Respondents’ preferred strategic actions for the coming ten years. Note: Sample sizes differ as a result of missing answers.

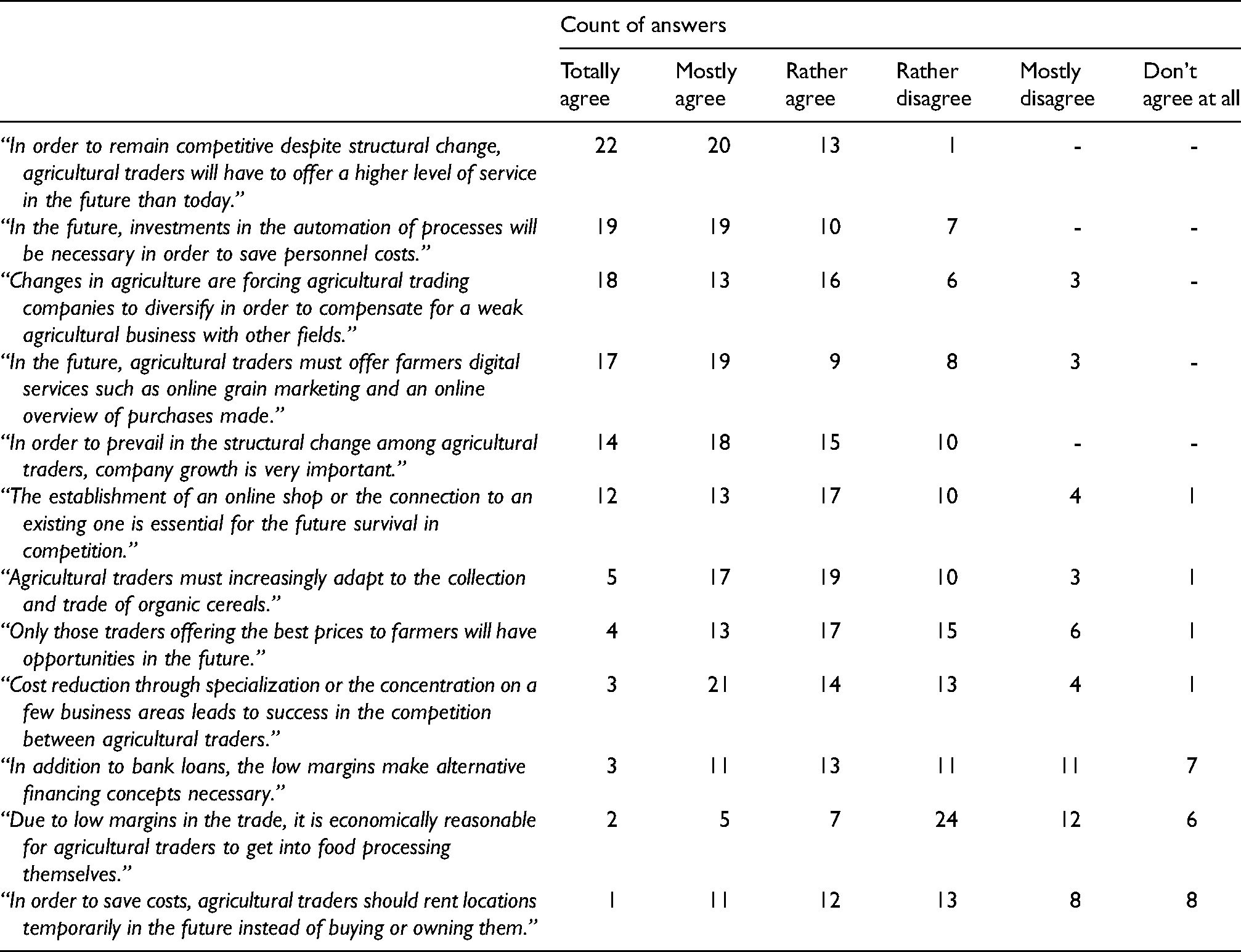

Regarding the general developments in the industry (see section “Introduction”), the statement that trading firms need to offer a higher level of service in the future received the most support (for the detailed results, see also Appendix Table A4). In addition, most participants see a need for diversification and further firm growth as well as a need for the expansion of digital services and the automation of processes. While 55 respondents agreed that “In order to remain competitive despite structural change, agricultural traders will have to offer a higher level of service in the future than they do today,” only 34 respondents agreed that “Only those traders with the best prices for farmers will have a chance in the future.” At the same time, a high level of service was considered more important than offering the best prices. It is also interesting to note that the majority of the respondents did not expect alternative financing concepts, the temporary renting of locations or entering the food processing industry in the future.

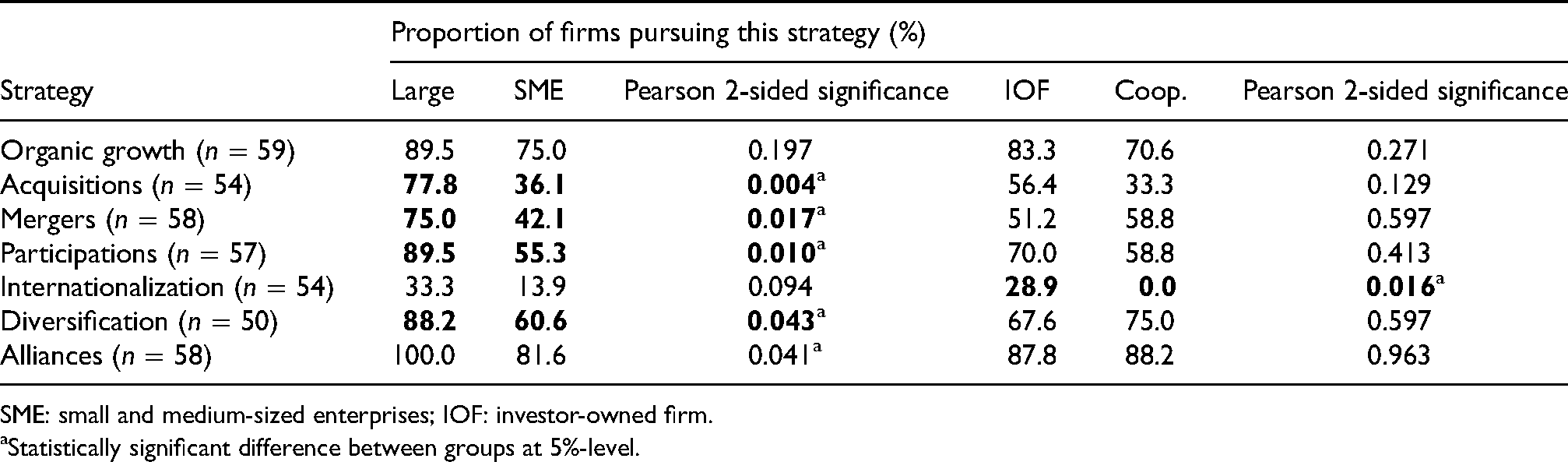

Table 3 presents differences between the firms regarding size and organizational form. We limit our investigation to whether the respondents considered the respective strategic action to be promising for their firm or not, regardless of the time period. Bold cells show strategic actions whose proportions match our expectations (see Table 1).

Differences in strategic actions between types of agricultural trading firms.

SME: small and medium-sized enterprises; IOF: investor-owned firm.

Statistically significant difference between groups at 5%-level.

Based on a two-sided Pearson's chi-squared test, we observe statistically significant differences between large firms and SMEs in the cases of acquisitions, mergers, participations, diversification, and alliances. While 77.8%, 75%, 89.5%, 88.2%, and 100% of the surveyed large firms’ managers are aiming to pursue these strategies, only 36.1%, 42.1%, 55.3%, 60.6% and 81.6% of the SMEs’ managers are doing the same. Overall, managers of large firms intend to adopt more strategic actions than those of smaller firms. With regard to the organizational form, statistically significant differences could only be detected for internationalization, which is favored by 28.9% of the IOFs but only by 0% of the cooperatives.

Comparison of past and intended strategic actions

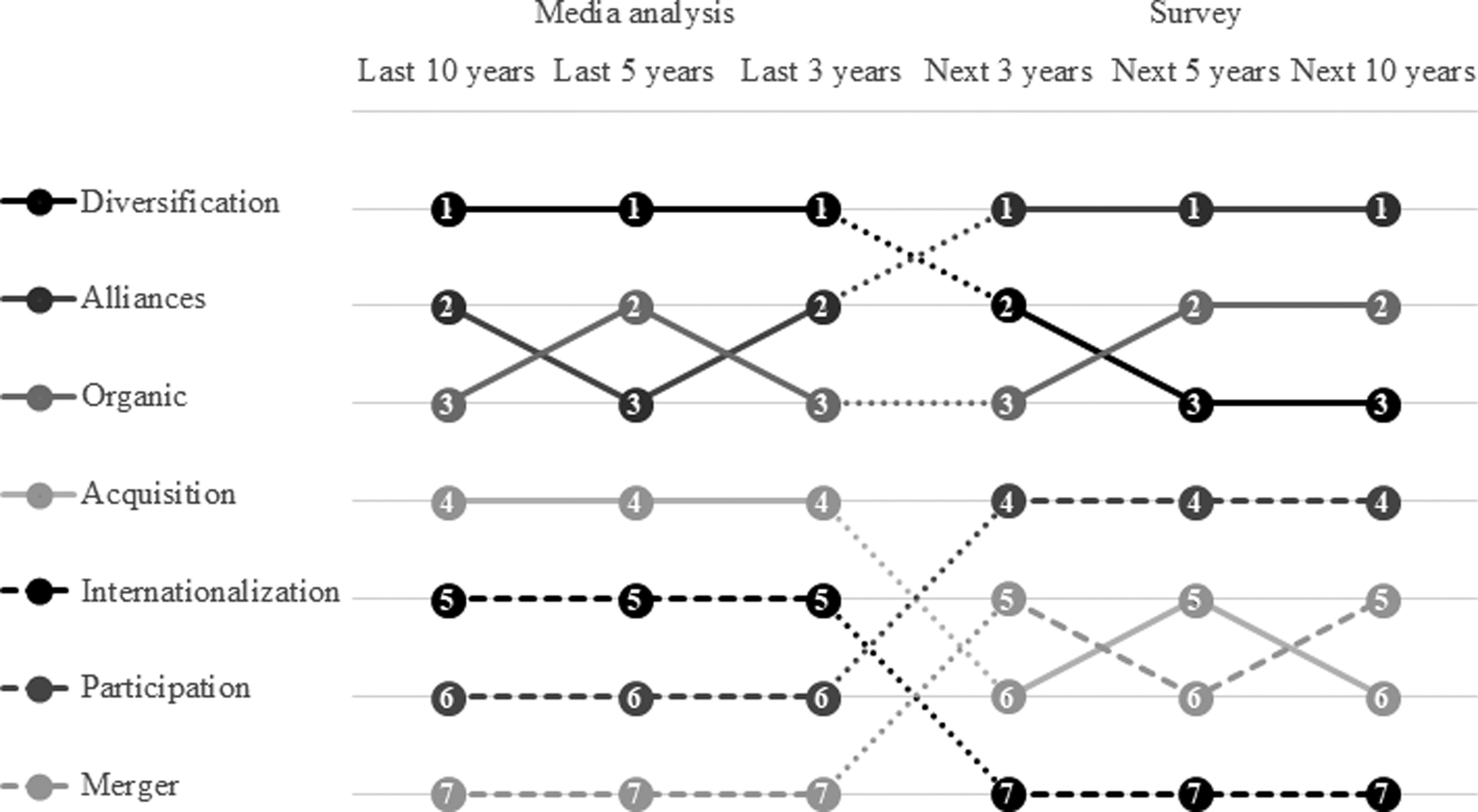

Figure 3 shows an aggregated ranking of the different growth strategies in the media analysis and in the survey (part 3). The results of the both analyses were summarized in such a way that the category “next five years” (“next ten years”) also includes the category “next three years” (“next five years” and “next three years”). For the media analysis, the ranking is based on frequency; for the survey, it is based on agreement ratings.

Comparison of preferred strategic actions in the past and in the future.

The comparison must be viewed with caution, as the media analysis only includes large firms, while the survey also includes managers of many small and medium-sized firms. While diversification has emerged as the most important strategic action in the media analysis over the last ten years, the managers surveyed intend to focus on alliances over the next ten years. Diversification is nevertheless, next to organic growth, among the TOP 3. While internationalization was fifth most common in the media analysis, it is last in the survey. Conversely, participation occurs more frequently in the survey than in the media analysis.

Discussion

Past and intended strategies

Farm supply and grain marketing businesses have had different ways of responding to transformational pressures over the past ten years. Diversification, organic growth and alliances were the most frequently used strategic actions. While no clear trend was evident for most strategic actions, divestment seemed to increase over time. At first, this seems to be a contradiction to the growth trends. However, it may also be an expression of increasing efforts for efficiency, which is reflected in growth at a few selected locations as well as alliances between firms. The observed combination of different strategic actions supports the findings of Gollisch et al. (2018), who highlighted the importance of hybrid strategies. Further work needs to be done to establish whether and how a combination of strategic actions leads to a superior performance as suggested by Claver-Cortés et al. (2012).

Surprisingly, although most of the respondents stated that corporate growth was important, the majority plan to reduce the number of locations for grain collection within the next ten years. Divestment is a popular strategy in declining markets (Harrigan, 1980) and is likely related to structural change in agriculture. In both the media analysis and the survey, only few firms and managers were in favor of internationalization. There are several explanations for this result. First, the market environment in other countries could be similarly characterized by overcapacities, meaning that firms do not expect any advantages from entering the market. Second, current trends toward greater protectionism could discourage firms from further internationalization. Third, the survey took place at the time of the Corona pandemic, making internationalization unattractive due to supply chain disruptions. The media analysis further indicates that acquisitions have become less important over the last ten years. This finding is consistent with the survey results, which also indicate that acquisitions will not be among the most relevant strategies in the future. The consistent results suggest stable trends in the development of strategies. Strategies have not changed as much as one might assume due to the changing business environment.

Differences between media analysis and survey can be seen in the category of participation. While this strategy was less popular in the past, it seems to become more likely in the future. This difference may be due to changes in the business environment. The digitization of internal processes and the growing online trade are cited by many respondents as the main challenges for the future (see also Fecke et al., 2018). Participation could be seen as an opportunity to meet these challenges. Another possible explanation is that the firms surveyed differ from the firms in the media analysis both in terms of size and legal form. A further difference between past and future exists in terms of diversification. While diversification was one of the most frequently documented strategic actions in the media analysis, the question regarding its future implementation shows mixed results. This discrepancy could be attributed to different understandings of diversification. While many participants stated that they want to keep the number of business lines constant in the next ten years; they also stated that the provision of digital services will increase. To develop a full picture of diversification as a strategy, additional studies will be needed that differentiate between different types of diversification.

In comparison to the growth strategies described by Höhler and Kühl (2014) for cooperatives in the cereal sector, it is striking that organic growth was frequently chosen as a growth strategy in our sample as well. In contrast to their study, which does not include alliances as a strategy, we show that alliances have been an almost equally important strategy in recent years. Gollisch et al. (2018) found that the opportunity for cooperation is welcomed by traders with different types of strategies. This preference for alliances with other firms is confirmed in this study. For managers, alliances offer growth opportunities that may not have been fully exploited to date. Expansion through alliances has so far been little studied among agricultural traders and also in agribusiness as a whole. Further work is needed to fully understand the implications of alliances for the competition in this sector. Of further interest is how these alliances take place and how they affect the performance of the firms.

Firm size and organizational form

The observed differences in intended future strategic actions between firms of different size and organizational form are mostly in line with our expectations. Cooperatives and SMEs are less likely to carry out acquisitions, participations and internationalization. Cooperatives are slightly more likely to merge than IOFs, though the difference is not statistically significant. Contrary to our expectations, managers of SMEs and cooperatives do not plan to grow organically or ally more often than managers of large firms and IOFs. These results may be due to the fact that many firms grow organically and ally to a certain extent. An additional query on the quantity of projected growth and alliances could have provided additional insights here. Overall, large firms pursue the examined strategic actions more frequently than SMEs do. Our results suggest that Porter’s (2008) classic classification into cost leadership, differentiation or focus falls short of the mark. Further research might explore the reasons for the varying degrees of strategic action use and its effects.

Conclusion

Our main goal was assessing the development of agricultural trading firms’ strategies in the past and in the future. To account for the dynamics of strategies and also to consider both past and intended strategies, two methods, media analysis and survey, were combined. Media analysis was used to examine strategies in the past ten years. We find that some strategic actions, namely diversification, organic growth and alliances, were applied more frequently than others over the last ten years. Our survey results indicate that some of the patterns identified in the media analysis are likely to continue. While the most popular strategic actions in the past appear to remain relevant in the future, the trend towards divestment and fewer locations for grain collection will continue.

While previous studies only examined the strategies at one point in time, we present a long-term study of the strategies using two different methods. The combination of media analysis and survey represents a possibility to examine both past and intended strategies. The two approaches mutually serve to contrast and validate the results. The method shown here can be transferred to other industries and countries. In addition, it can be extended to other media and firms, allowing statements on the whole population of agricultural trading firms.

The generalizability of these results is subject to certain limitations. For instance, the sample size of the firms in the media analysis is relatively small, although it covers a large part of the market in terms of market share. Small and medium-sized enterprises could not be included in the media analysis due to the lack of reporting on their activities. In contrast, firms of various sizes participated in the survey. A self-selection of the participants can be assumed, which may impact our results. Monetary incentives for participation could counteract this in future studies. Further work is also needed to fully understand the development of strategies over time.

By identifying both consistencies and differences in past and intended strategies, this study lays the foundation for further research in the area of strategy development.

Supplemental Material

sj-docx-1-oag-10.1177_00307270211053342 - Supplemental material for Farm supply and grain marketing businesses: A mixed methods investigation of past and intended future strategies

Supplemental material, sj-docx-1-oag-10.1177_00307270211053342 for Farm supply and grain marketing businesses: A mixed methods investigation of past and intended future strategies by Laurin Spahn and Julia Höhler in Outlook on Agriculture

Supplemental Material

sj-docx-2-oag-10.1177_00307270211053342 - Supplemental material for Farm supply and grain marketing businesses: A mixed methods investigation of past and intended future strategies

Supplemental material, sj-docx-2-oag-10.1177_00307270211053342 for Farm supply and grain marketing businesses: A mixed methods investigation of past and intended future strategies by Laurin Spahn and Julia Höhler in Outlook on Agriculture

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

Appendix

What do you think about the following statements about German agricultural trade?

| Count of answers | ||||||

|---|---|---|---|---|---|---|

| Totally agree | Mostly agree | Rather agree | Rather disagree | Mostly disagree | Don't agree at all | |

| “In order to remain competitive despite structural change, agricultural traders will have to offer a higher level of service in the future than today.” | 22 | 20 | 13 | 1 | - | - |

| “In the future, investments in the automation of processes will be necessary in order to save personnel costs.” | 19 | 19 | 10 | 7 | - | - |

| “Changes in agriculture are forcing agricultural trading companies to diversify in order to compensate for a weak agricultural business with other fields.” | 18 | 13 | 16 | 6 | 3 | - |

| “In the future, agricultural traders must offer farmers digital services such as online grain marketing and an online overview of purchases made.” | 17 | 19 | 9 | 8 | 3 | - |

| “In order to prevail in the structural change among agricultural traders, company growth is very important.” | 14 | 18 | 15 | 10 | - | - |

| “The establishment of an online shop or the connection to an existing one is essential for the future survival in competition.” | 12 | 13 | 17 | 10 | 4 | 1 |

| “Agricultural traders must increasingly adapt to the collection and trade of organic cereals.” | 5 | 17 | 19 | 10 | 3 | 1 |

| “Only those traders offering the best prices to farmers will have opportunities in the future.” | 4 | 13 | 17 | 15 | 6 | 1 |

| “Cost reduction through specialization or the concentration on a few business areas leads to success in the competition between agricultural traders.” | 3 | 21 | 14 | 13 | 4 | 1 |

| “In addition to bank loans, the low margins make alternative financing concepts necessary.” | 3 | 11 | 13 | 11 | 11 | 7 |

| “Due to low margins in the trade, it is economically reasonable for agricultural traders to get into food processing themselves.” | 2 | 5 | 7 | 24 | 12 | 6 |

| “In order to save costs, agricultural traders should rent locations temporarily in the future instead of buying or owning them.” | 1 | 11 | 12 | 13 | 8 | 8 |

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.