Abstract

We investigate the extent to which (quasi-)colonial ties played a role in the procurement of jet aircraft by airlines in the Global South. Because we do not have access to archival data on the sensitive issue of aircraft procurement, we take an indirect empirical approach. Our investigation is based on a dataset including all Western jet aircraft delivered between 1952 and 1989. We ask if, to what extent, and how long airlines from former British, French, Dutch, and US (quasi-)colonies tended to buy jets from their former or, respectively, most recent colonial master. We compare the (ex-ante) expected geographical distribution of politically unbiased jet deliveries to the (ex-post) actual historical and potentially biased distribution. We find that colonial ties to former colonial masters from Europe especially mattered until the early/mid-1970s when, triggered by the two oil price crises, pure economic motives gained more significance in informing procurement decisions.

Objective and outline

From its beginnings until at least the 1970s, civil aviation was highly politicised, and even today the two most important aircraft manufacturers, Airbus and Boeing, accuse each other of improper government aid. In fact, the development of commercial aircraft has been an extremely costly endeavour ever since and is, ultimately, only profitable if several hundreds of them can be sold. In addition to technology- and labour-related policy motives, national prestige has been playing a key role in establishing and maintaining aircraft manufacturing capacity. Therefore, it is not surprising that governments have repeatedly tried to support the selling efforts of national manufacturers. 1 The incentives for manufacturers and governments – especially if manufacturers are government-owned – to try selling an expensive product by capitalising on political ties and, thereby, circumventing the market mechanism should be considerable. 2

If political pressure plays a role in the sale of aircraft, it stands to reason that this is particularly important in relation to (former) colonies as potential customers. However, when investigating the market for wide-body aircraft, Jopp and Spoerer (2023) find no statistically robust evidence of a positive colonial bias for the period from 1969 (the market launch of the first wide-body aircraft, the Boeing 747) to 1989. 3 Three possible explanations come to mind (with the first two not being mutually exclusive): firstly, the colonial past could have led the decision-makers with the airlines and governments to deliberately back away from doing business with the former colonial master country. Secondly, there might have already been technological path dependencies in place when the decision for or against the purchase of certain wide-body jets was made, which then overcompensated for any (post-)colonial (positive or negative) preferences. For example, those airlines already operating an almost all-Boeing narrow-body fleet might have chosen the Boeing 767 over the Airbus A300. Thirdly, irrespective of any colonial dependencies as well as technological and customer-relations path dependencies, each new model on the market was evaluated anew for its economical usage and for whether it would fit the existing fleet.

To clarify these issues, it is important to look back even further and ask whether colonial or technological dependencies did play a role before the era of wide-body jets. This is the focus of this article. For all Western commercial jet types, we examine to which first-hand customers aircraft manufacturers sold their brand-new aircraft. In a first step, we look at whether commercial jet aircraft were sold disproportionately to (former) colonies, that is, whether there was a positive colonial bias before 1969, the advent of wide-body aircraft; and we argue that there was one indeed. Therefore, in a second step, we clarify when this positive colonial bias lost its significance and which of the above-mentioned reasons apply.

In our view, answering the question of the role of colonial ties or, more generally, political pressure in shaping historical aircraft procurement decisions requires going beyond case studies dominating the literature. As we do not have access to archival data on the sensitive issue of aircraft procurement, we instead pursue an empirical, mass data approach. 4 To this end, we collected data on every Western jet delivered between 1952 and 1989. After having placed our study in the relevant literature in the “Placing the study” section, we describe our dataset in more detail in the “Dataset and methodological issues” section. In the “Assessing some trends” section, we discuss some noteworthy historical trends in the data as to the role of first-hand customers from the Global South (where most of the Western countries’ actual and former colonies lie) as jet aircraft procurers. In the “Colonies and aircraft procurement” section, we present our results, limiting ourselves to methods of descriptive statistics. Finally, the “Conclusion” section concludes the article. The Online Appendix provides Supplemental Material.

Placing the study

Our analysis links with two bodies of literature. The first comprises the many studies produced by economists, economic historians, political historians, and political scientists on decolonisation processes and post-colonialism. This literature has provided ample evidence that past colonial relations have been significant for long after colonies gained their formal independence in many cases.

5

For example, in his 1978 study, Smith concluded that […] the Europeans could nevertheless significantly influence this process [i.e., the decolonization process; the authors] in most cases by their attention to grooming their successors. For virtually every nationalist government harbored a civil war whose divisions allowed the colonial authority a strong voice in local affairs. By deciding with whom they would negotiate, by what procedure they would institutionalize the transfer of power, and over what territory the new regime would rule, Paris and London decisively influenced the course of decolonization.

6

In regards to British colonial legacy specifically, Lange (2004) provides evidence on institutional path dependencies reaching from colonial rule well into the post-colonial era. 7 In addition, other authors clearly suggest that a former colonial master would have wanted to take part in shaping a former colony's future to defend its own economic and security interests in the first place. 8 For Africa's air transport sector, Button et al. (2015) provided statistical evidence that the colonial legacy indeed shaped the sector's long-term development. 9

One way in which a former colonial master could exert influence, if not outright pressure, to pursue national interests may be seen in establishing financial leverage through all sorts of financial flows, especially foreign aid. 10 According to McKesson (1990), for example, France was “the major foreign player on the African scene” around the late 1980s, evidenced by a share in foreign aid to sub-Saharan Africa of 18 per cent, outranking every other donor country or supranational donor organisation. 11 Considering the findings from the various economic and political science studies that ask for the motives of donor countries to provide foreign aid, France's motive, very likely, was to serve its own economic and security interests rather than acting out on an altruistic streak towards her former colonies. 12 To name only one study, Alesina and Dollar (2000) established colonial ties as one important statistical determinant of foreign aid flows; former colonial masters tend to provide more foreign aid to their former colonies than to other potential receivers. 13 Another way of preserving influence was integrating former colonies into a political or economic superstructure controlled by the former colonial master. The Franc de la Communauté Financière d’Afrique (CFA-Franc) zone may be viewed as such a structure as well as may the Commonwealth of Nations. 14

Following Jönsson (1981), four major motives for government intervention have been uniquely coming together in the aviation industry, namely “national defense”, “economic considerations”, “safety”, and “foreign policy considerations” – that is, national prestige (“showing the flag”). 15 The aviation industry may, therefore, be seen as the paragon of a highly politicised economic sector. Thus, it is well imaginable that (former) colonial masters like Britain, France, the Netherlands, and the United States, each commanding over a potent commercial aircraft industry in this study's observation period, viewed (former) colonies as their exclusive marketing zones providing unrivalled demand for their produce. We like to think these are the perfect ingredients for a situation characterised by frequent “political sales” as defined by Jopp and Spoerer (2021) and to be seen in comparison to market-mechanism-based sales guided by economic motives of the aircraft procurer in the first place 16 ; particularly so when considering that corruption seems to be a special, persistent issue with former colonies, 17 very much like with the aircraft industry. 18

At this point, the second body of literature comes into play which is directly concerned with the birth and rise of the commercial aircraft and airline industries and which may, or may not, provide historical evidence on the matter. Notably, in the grand narratives, which are built around the various steps of regulation having shaped commercial aviation to date, the issue of colonial ties and the consequences for aircraft procurement and production decisions is largely neglected. An instructive example is Dobson's narrative, in which there is only one mention of the terms “colony” and “colonialism” each and no mention of the term “decolonization”, at all. 19 The political dimension of selling aircraft is more present in the specialised works on single aircraft manufacturers and particularly in the rivalry between Boeing and Airbus, culminating in several subsidy disputes between the United States and the European Union. 20 However, in this literature as well as other manufacturer-, country-, or airline-centred historical narratives, the question of how many sales deals were politically induced, that is, decidedly circumvented the market mechanism for the manufacturer's benefit, is addressed, at best, at the very surface. The same goes for the colonial ties issue, specifically. 21 Our approach is geared at filling this knowledge gap to some extent.

Dataset and methodological issues

Aviation still attracts many enthusiasts, so for practically every commercial aircraft ever flown information on the complete chronology of owners, that is, from the first customer to purchase the brand-new aircraft to the last operator buying it second-hand and eventually retiring it one way or the other (by scrapping, preserving, or write-off), is available somewhere on the internet. While for some types of aircraft, we directly consulted publications reporting production lists, 22 we mostly drew on several online databases. 23

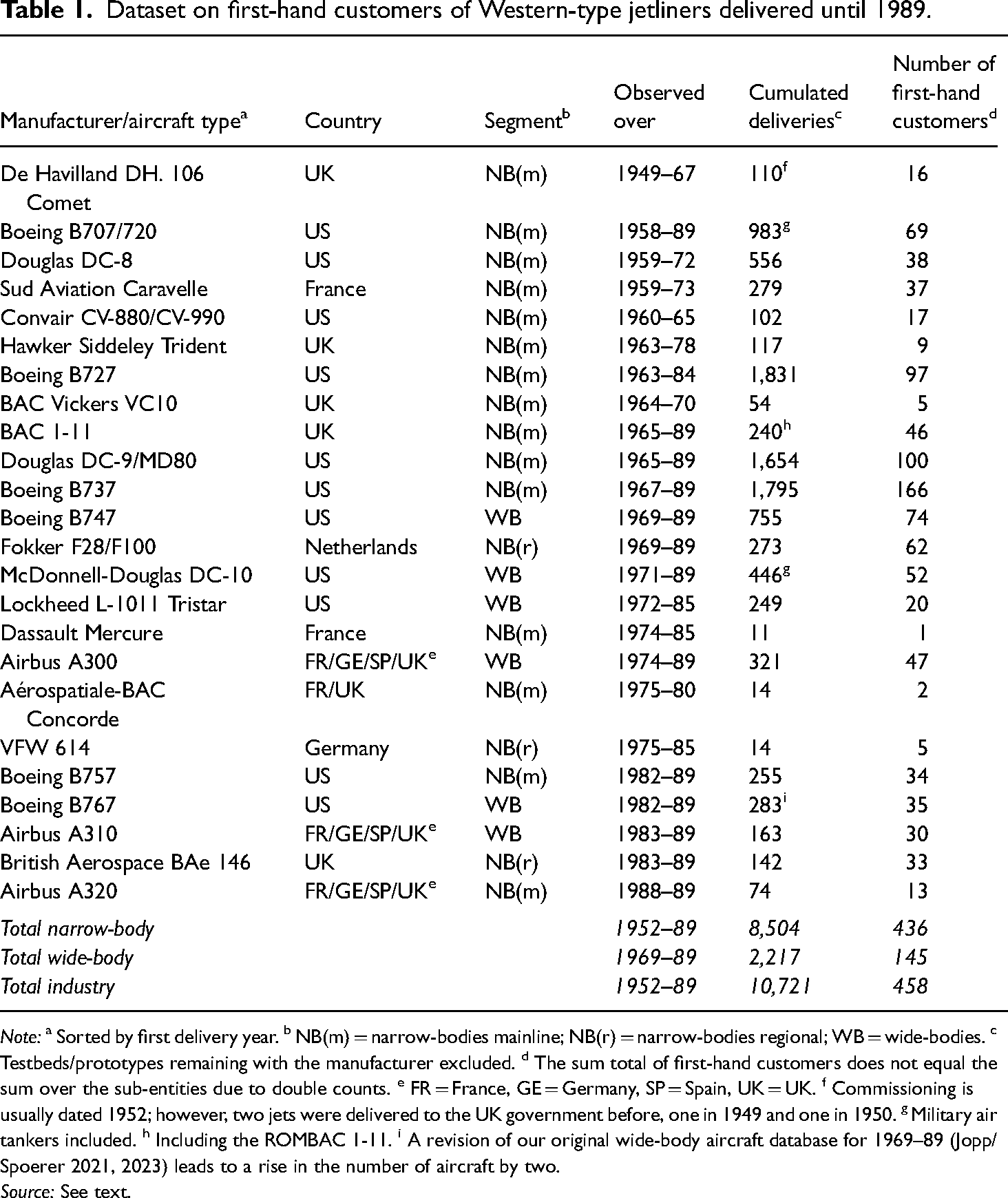

From these databases, we have collected information on every commercial jet aircraft produced and delivered between 1952 and 1989 that was not of Soviet design. 24 Table 1 provides an overview of all 24 types of jet aircraft in our dataset. Given are the type of aircraft and manufacturer in column one; the manufacturer's home country in column two; the market segment in column three; the period of delivery in column four; the number of cumulated deliveries until and including 1989 in column five; and the number of different first-hand customers by type in column six.

Dataset on first-hand customers of Western-type jetliners delivered until 1989.

Note: a Sorted by first delivery year. b NB(m) = narrow-bodies mainline; NB(r) = narrow-bodies regional; WB = wide-bodies. c Testbeds/prototypes remaining with the manufacturer excluded. d The sum total of first-hand customers does not equal the sum over the sub-entities due to double counts. e FR = France, GE = Germany, SP = Spain, UK = UK. f Commissioning is usually dated 1952; however, two jets were delivered to the UK government before, one in 1949 and one in 1950. g Military air tankers included. h Including the ROMBAC 1-11. i A revision of our original wide-body aircraft database for 1969–89 (Jopp/Spoerer 2021, 2023) leads to a rise in the number of aircraft by two.

Source: See text.

In total, according to our count, 10,721 jets were delivered to 458 different first-hand customers (including but not limited to commercial passenger and cargo airlines) in the observation period, thereof 8,504 narrow-bodies, most of which may be reasonably seen as designed to serve mainline routes, and 2,217 wide-bodies, appearing on the scene with the first deliveries of the Boeing 747 in 1969. 25 In fact, our dataset is covering the entire pre-1990 first-hand market for Western jet aircraft.

To be precise, the dataset created for the purpose of this article is an extension of our dataset on wide-body jet aircraft introduced in Jopp and Spoerer (2021, 2023) for the much larger narrow-body segment. For the baseline variables created per wide-body jet and subsequently also for each narrow-body jet, we kindly refer the reader to the overview in Jopp and Spoerer (2021). The information per jet we do need for this analysis is the following: (a) manufacturer (e.g. Boeing), type (B707, B727, etc.), and market segment (e.g. narrow-body mainline); (b) the delivery year (e.g., 1970); (c) the first-hand customer (e.g. American Airlines or Dutch government) and its home country (e.g. the United States of America and the Netherlands) 26 ; (d) whether the first-hand customer's home country belonged to the Global South during the observation period (0-1-coded dummy variable); 27 (e) whether it was a (former) colony of either Britain, France, the Netherlands, or the US (0-1-coded dummy variables), which are the relevant manufacturer countries; or (f) whether it lay in Latin America and, thus, establishes what we call a quasi-colony of the US (0-1-coded dummy variable), relating to the agenda that was set by the Roosevelt Corollary of 1904. In a few cases, we also identified quasi-colonies of Britain.

Assigning countries to the Global South and Global North and deciding whether a country was a (former) colony, and to which colonial master, needs explaining. We provide this methodological discussion in the Online Appendix. Summarising our assignment process, Table A1 in the Online Appendix lists the countries we consider having had a recent (quasi) colonial history with the aircraft manufacturers’ home countries. Besides the country and (former) colonial master, we report the country group (Global South or North), the date of independence from colonial rule, and the year in which the first brand-new jetliner was procured by an operator from the respective country.

Assessing some trends

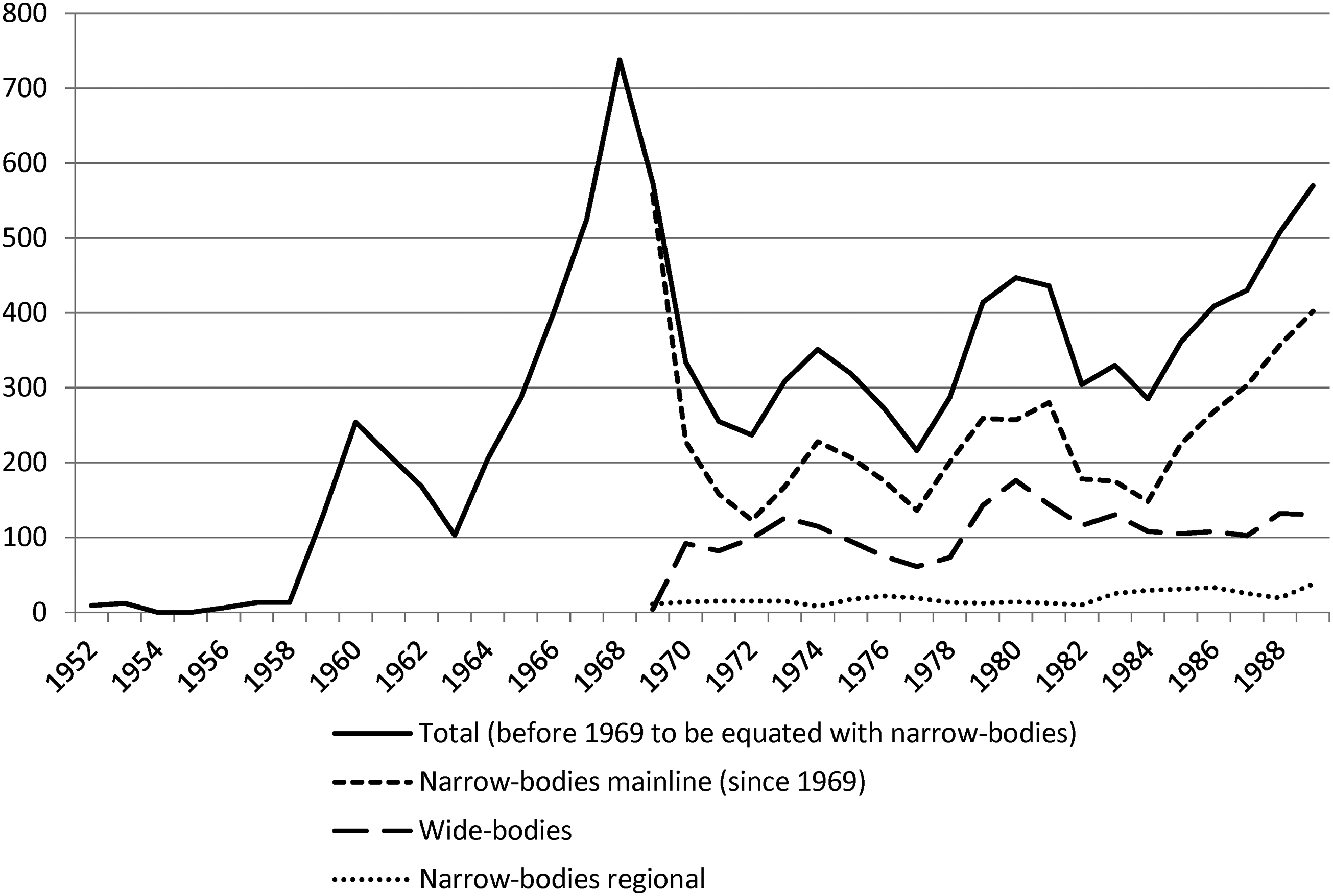

In this section, we want to briefly review some trends as to jet aircraft procurement in the Global South and the Global North. To begin with, Figure 1 illustrates the overall trend in deliveries of Western-type jets by market segment. Clearly visible is the strong rise in the first phase of the market ending in the late 1960s. Narrow-body jets were state of the art in the 1950s and 1960s and experienced a nearly uninterrupted boom initially. When wide-bodies entered the market in 1969, the market for narrow-bodies seemed saturated; their sales were plummeting and recovered only in the second half of the 1980s. There is no doubt that the two oil price shocks of the 1970s and early 1980s heavily influenced airlines’ and other operators’ procurement decisions. 28

Annual deliveries of brand-new Western-type jetliners by segment, 1952–89. Note: On the composition of the segments, see Table 1. Source: Authors’ dataset; see the “Dataset and methodological issues” section.

The first oil price crisis in 1973/74 brought about a doubling of the price for kerosene, a rise markedly surpassed by the crisis in 1981 with an almost ten-fold increase compared to the start of 1973. Consequently, total jet sales dropped, and the production of kerosene-thirsty jet types such as the Caravelle, the Trident, and the supersonic airliner Concorde was stopped; especially for the latter, France's and Britain's prestige project, there had not been demand for brand-new jets from airlines other than Air France and British Airways. Airlines operating the Boeing 720 or the Convair Coronado threw their aircraft on the secondary market, where they found demand located in the periphery, at best, or retired them straight away. As for the wide-body segment, the first types of aircraft to heavily lose in significance due to fuel inefficiency were the triple-engined aircraft, Lockheed's Tristar, and McDonnell Douglas's DC-10. Because Lockheed did not find new customers for its Tristar, production finally ceased in 1985. Jets offering more favourable fuel consumption per passenger profited, like Airbus's A300 and later Boeing's B767. In addition, the FAA eased ETOPS regulations, allowing twin-engine jets to cross the North Atlantic for commercial flights beginning in 1985. 29

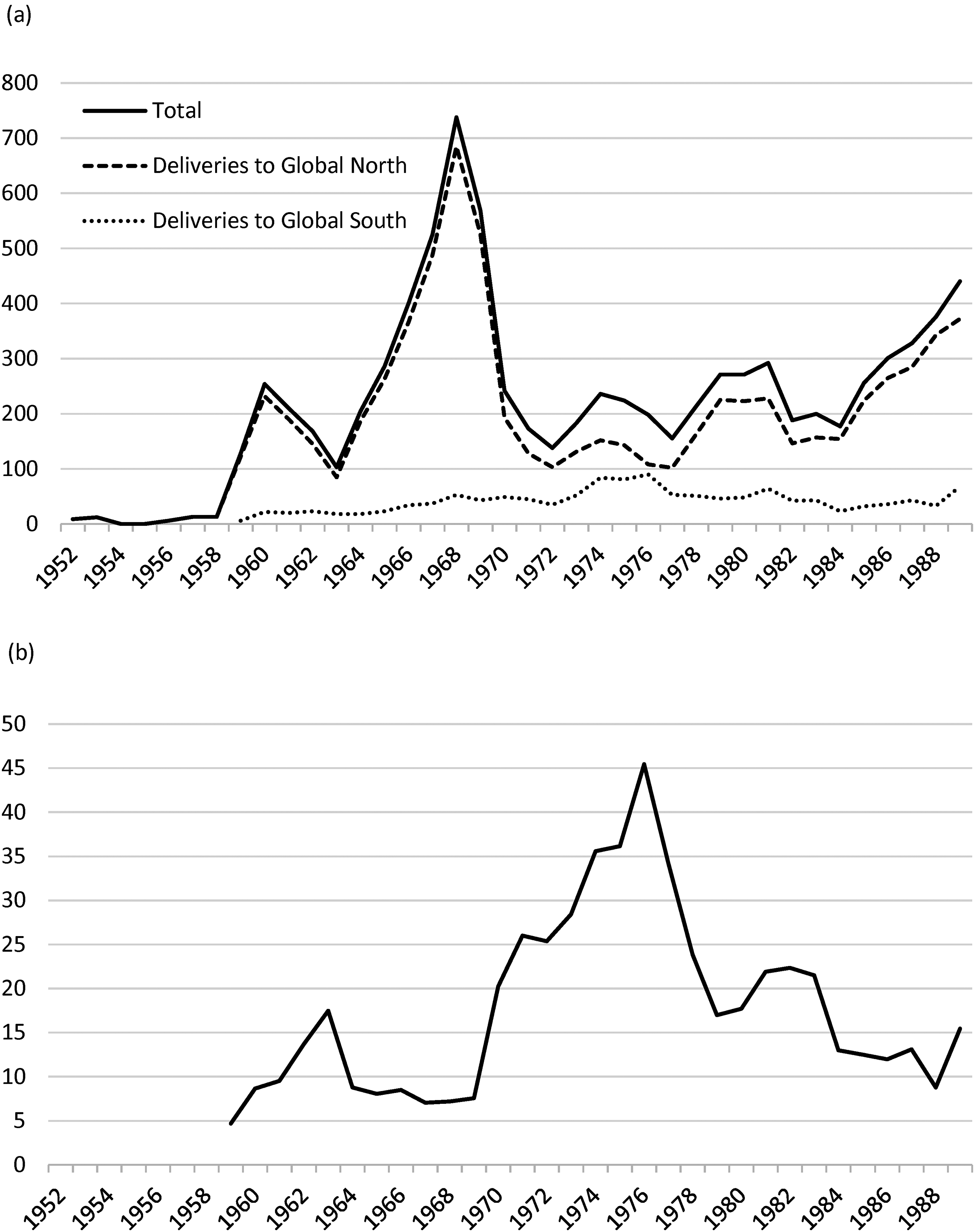

Figure 2 breaks down the overall number of deliveries by segment into brand-new jets delivered to the Global North and the Global South; while panels (a) and (c) show the absolute figures for narrow-body and wide-body aircraft like in Figure 1, panels (b) and (d) report the Global South's percentage share in both segments. The very first jetliner to be delivered to a commercial customer was the De Havilland DH-106 Comet I with registration G-ALYS, bound for British Overseas Airways Corporation (BOAC) and delivered on 4 February 1952. Fifty-one more aircraft – 40 Comets and 11 Boeing B707 – had been delivered until early in 1959, before the first operator from the Global South saw its first delivery of a brand-new jet. This was a Comet IV (reg. LV-PLM) handed over to Aerolíneas Argentinas on 27 January 1959. The Argentinian flag carrier received another two Comets that year (in March and May), followed by VARIG from Brazil as the Global South's initial first-hand customer of the Sud Aviation Caravelle III (two jets delivered in mid-September and early December). For the sake of completeness, the very first jet delivered to an operator from the Global North that had a formal colonial background with the manufacturer's home country was a Comet I, and the operator was Canadian Pacific Air Lines (CP Air) to which the jet (reg. CF-CUN) was handed over on 2 March 1953. 30

Annual deliveries of brand-new jetliners to operators from the Global South and Global North by segment, 1952–89. (a) Narrow-bodies – absolute figures. (b) Narrow-bodies – annual share of deliveries to the Global South in per cent. (c) Wide-bodies – absolute figures. (d) Wide-bodies – annual share of deliveries to the Global South in per cent. Note: On the composition of the segments, see Table 1. Source: Authors’ dataset; see the “Dataset and methodological issues” section.

As follows from Figure 2, Panel (a), jetliner deliveries to the Global South peaked in 1976 (90 jets), right between the two oil price crises, and then followed a downward trend. In the late 1980s, a reversal loomed on the horizon. Expressed in a percentage, first-hand customers from the Global South accounted for roughly half the effective market for narrow-bodies at the peak in the mid-1970s; that percentage would shrink to around 15 per cent in 1989. The picture for the wide-body-segment is different and especially owes to the growth of four airlines, namely Singapore Airlines, Saudia, Korean Air Lines, and Thai Airways. The peak-year was 1980 with 56 jets delivered, accounting for 32 per cent of the effective market. Interestingly, when focusing entirely on the percentages, wide-body deliveries to the Global South also peaked in 1976, with an effective market share of around 43 per cent. In the following years, as with narrow-bodies, deliveries followed a less steeply declining trend. It seems that, in relative terms, airlines from the Global South were more important to the principal aircraft producers as consumers of wide- than of narrow-bodies.

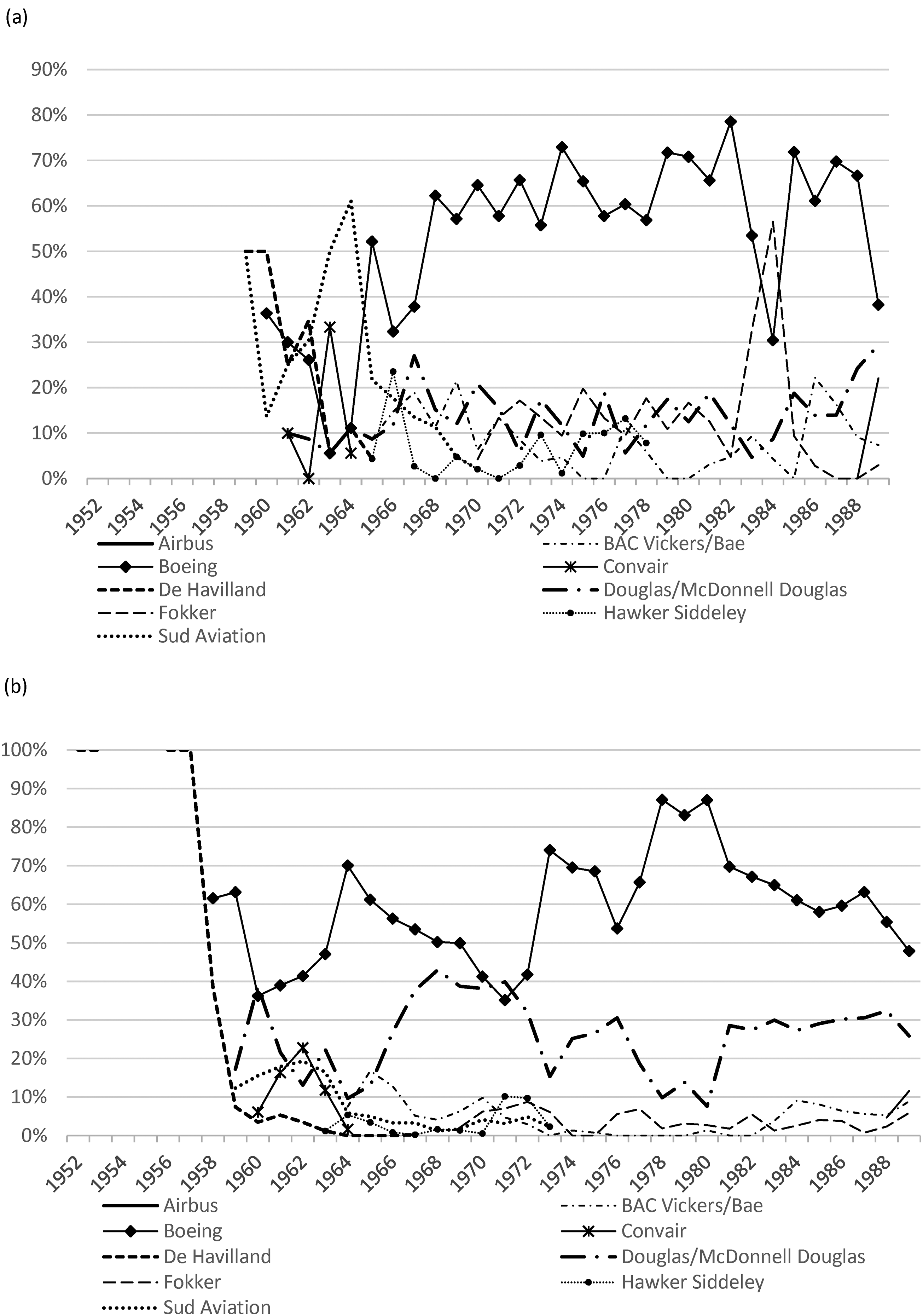

Figure 3 details the picture from the perspective of the aircraft producers in that it depicts the effective market shares by segment and country group. In the early 1960s, the typical jet used by an airline of the Global South (if it had jets at all) was the comparably small and cheap twin-engined Caravelle. But since the mid-1960s, Boeing aircraft dominated. While this holds for the Global North as well, Boeing fared disproportionately better in the South when compared to its most important rival, Douglas (see Panels a and b of Figure 3). Boeing's short- and medium-range jets, the B727 introduced in 1963 and the somewhat smaller B737 (1967) sold much better in the Global South than the DC-9 (1965). Boeing's dominance over the commercial aircraft market held well through to the early 1980s, when the Airbus 300/310 began to gain significant shares in the market for wide-bodies below the capacity of the B747, which was too large for many airlines, especially in the Global South. Only the B767 introduced in 1981 competed successfully with the Airbus A300/310 family.

Manufacturers’ annual effective market shares in the Global South and the Global North, 1952–89. (a) Global South – narrow-bodies. (b) Global North – narrow-bodies. (c) Global South – wide-bodies. (d) Global North – wide-bodies. Note: Aérospatiale, Dassault, and VFW omitted due to the negligible number of deliveries. Source: Authors’ dataset; see the “Dataset and methodological issues” section.

Referring to our mentioning of Singapore Airlines and others a few lines back, it might be interesting to see which operators from the Global South did buy Western-type jets and to which number. To this end, Table 2 ranks the top 20 first-hand customers from the Global South by the number of jets delivered to them over the whole period of investigation. 31 These airlines account for 1,055 of 1,854 jets delivered to 169 operators from the Global South in total, equalling a share of 57 per cent. Garuda Indonesia, the leading airline in terms of procured brand-new jets, ranks 26th when looking at the full ranking including operators from the Global North. As an appetiser for the subsequent analysis, it is noteworthy that more than half of the jets procured by Garuda, namely 56 according to our counting, are Dutch-manufactured Fokker F28.

Top 20 first-hand customers of Western-type jetliners from the Global South, 1952–89.

Note: a If not otherwise indicated, the founding date – not to be confused with the date when an airline's operation actually started – is taken from https://www.planespotters.net (accessed: 18 April 2023). b Percentage share in all deliveries to the Global South (N = 1,854) in parentheses. c Taking Soviet aircraft into account, slightly changes the picture: TAROM would enter with 43 jets (17 of Soviet and 26 of Western origin; Romania was considered as part of the Global South since 1976, see the Online Appendix), as well as would Cubana with 31 procured Soviet jets; CAAC (+ 17) and United Arab Airlines/Egyptair (+ 8) would climb in the ranking. d Origins date back to 1946; given is the year when Malaysia-Singapore Airlines (MSA) was split into Malaysian Airline System and Singapore Airlines (https://de.wikipedia.org/wiki/Singapore_Airlines; accessed 18 April 2023).

Source: Authors’ dataset.

Colonies and aircraft procurement

We now take a more detailed perspective and focus on aircraft sales of producers located in the former colonial master countries. Therefore, we divide the buyer countries into the (former or quasi) colonies as defined above (see “Dataset and methodological issues” section and the Online Appendix) – British former and quasi colonies in the Global South and Global North, French colonies, Dutch colonies, former and US quasi-colonies, and the remaining countries of the Global South – and look for whether we find evidence that both characteristics – the origin and destination of brand-new jets – are stochastically dependent. Statistically speaking, that would be our alternative hypothesis (H1). If, historically, colonial ties do not play a role in how jets distribute over destination countries, both characteristics can be considered stochastically independent (H0). To determine whether we can reject H0 in favour of H1, we use contingency tables, a convenient descriptive statistical tool to assess stochastic independence.

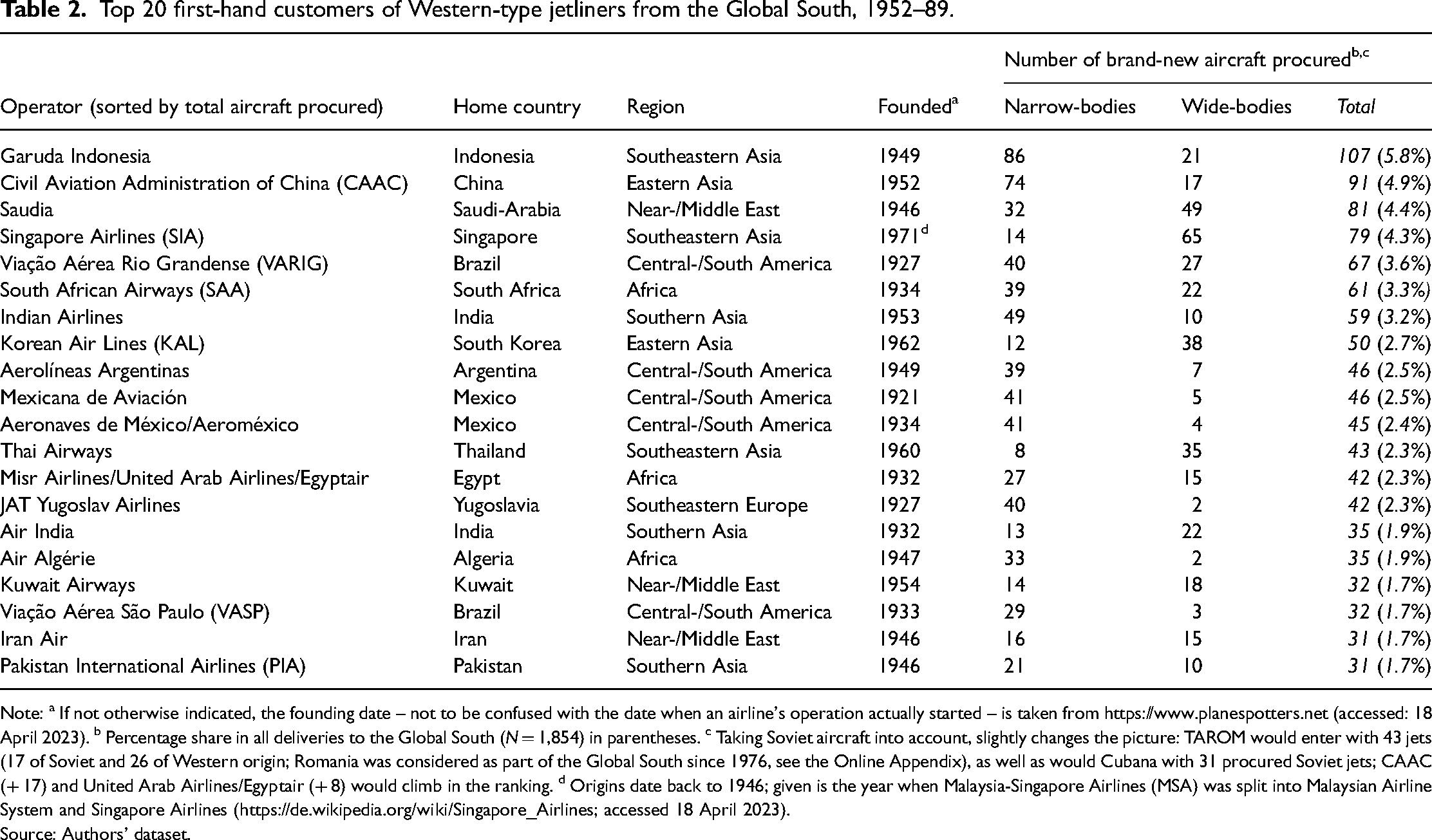

Tables 3 to 5 provide such contingency tables for both market segments in the periods 1952–69 and 1969/70–89. The distinction between these two periods is informed by the fact that wide-bodies appeared on the scene in 1969; we chose to distinguish these sub-periods to make the narrow-body segment directly comparable. Because we know for each manufacturer i (rows in Tables 3 to 5) and for each country group j (columns in Tables 3 to 5) the number of delivered jets, we can calculate the expected distribution in the cells in between. 32 The expected sales sijexp in panel A are compared to the actual historical sales sijhis in panel B, and sijhis/sijexp = cbij is the relation of historical to expected sales (panel C). Technically, it holds that if cbij is different from zero, then the manufacturer i has sold disproportionally in country group j, which implies both characteristics are stochastically dependent. For the sake of the argument, we label a sufficiently large positive deviation from expectations for the relevant manufacturer country-country group of destination-combination a “positive colonial bias” and vice versa. 33

Contingency tables for the narrow-body-segment – expected versus actual deliveries, 1952–69.

Note: Expected sales rounded to one decimal place. Figures printed in italics are not entering the row and column totals in bold print. The annotation “excl. RR” and “RR only” means “excluding aircraft powered with Rolls-Royce engines” and, respectively, “aircraft powered with Rolls-Royce engines only”. For the logic behind this distinction, see the explanation in the text.

Source: Authors’ computations.

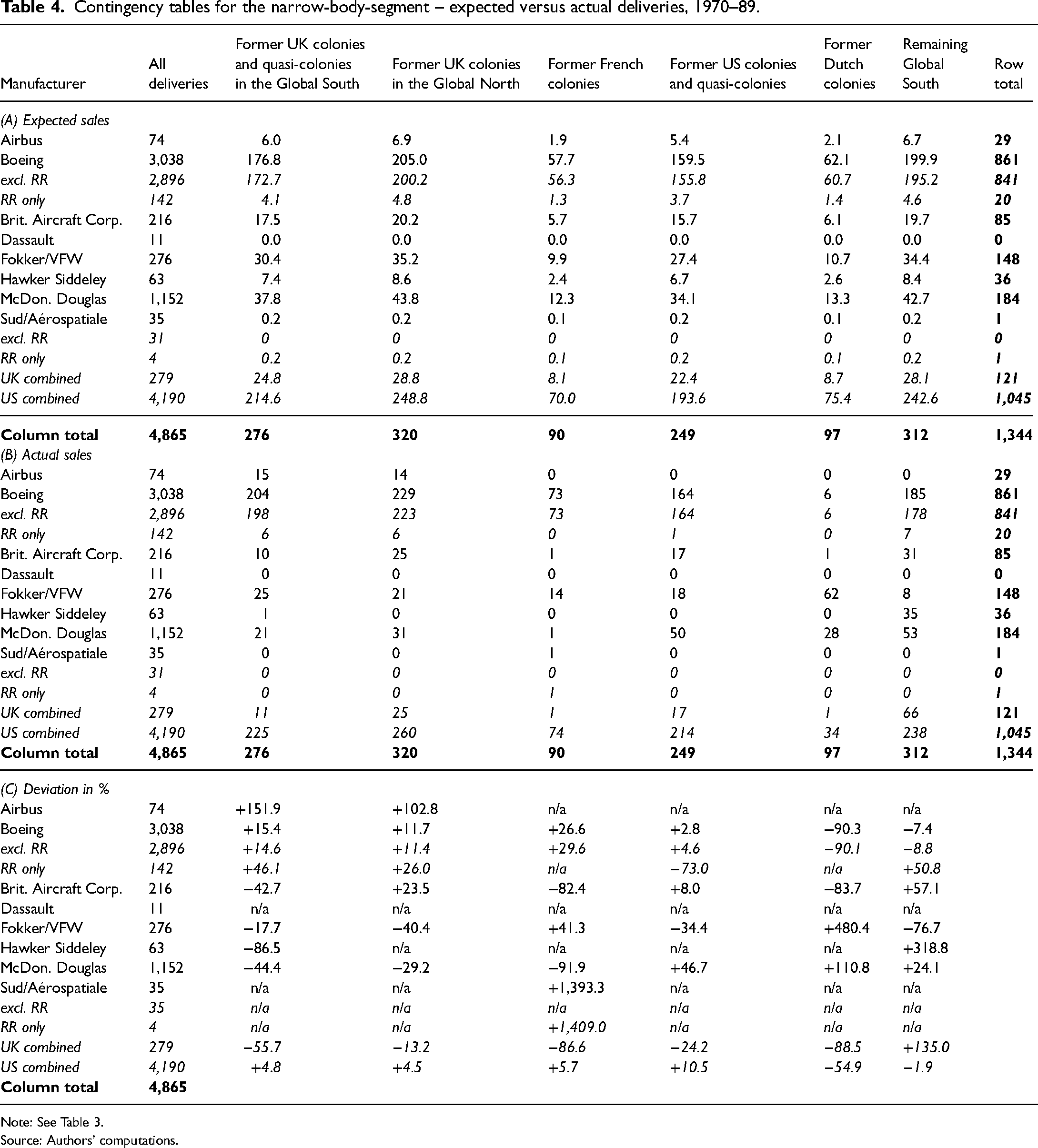

Contingency tables for the narrow-body-segment – expected versus actual deliveries, 1970–89.

Note: See Table 3.

Source: Authors’ computations.

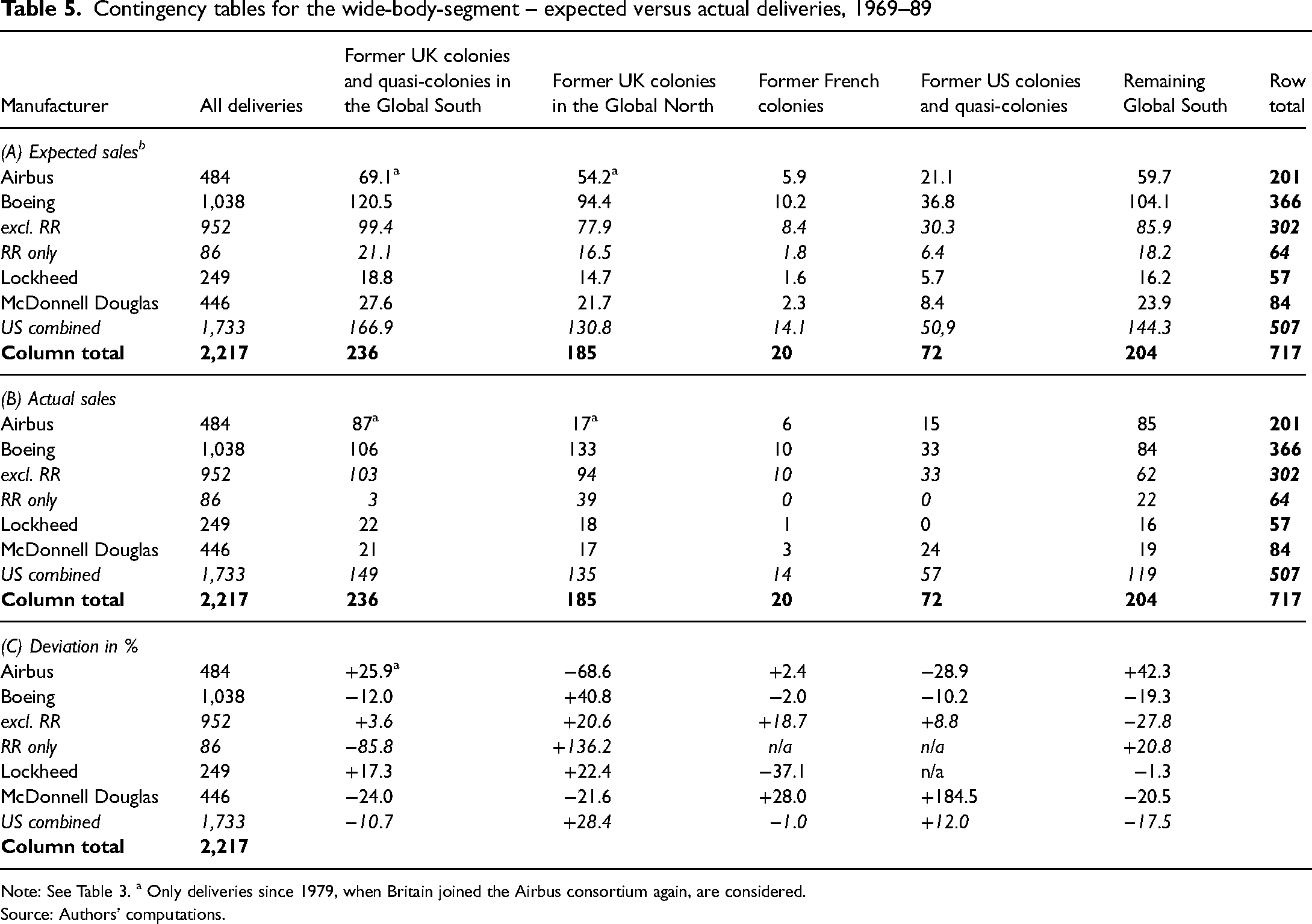

Contingency tables for the wide-body-segment – expected versus actual deliveries, 1969–89

Note: See Table 3. a Only deliveries since 1979, when Britain joined the Airbus consortium again, are considered.

Source: Authors’ computations.

Thus, the value for cb11 in the first cell of panel C for the period 1952–69 (see Table 3) indicates that Boeing's actual sales to former UK colonies in the Global South were 30.9 per cent higher than one could have expected a priori. This, however, is not a positive colonial bias because Boeing's home country, the United States, is obviously not considered in our framework to be the relevant colonial master; the figure does certainly have information content in that it can tell from where (former) UK colonies, if not from Britain, procured jets. Of actual interest in this country group are the sales of British manufacturers to (former) UK colonies. Whether cb21=+ 27.0 for BAC should already be interpreted as a colonial bias is discussable; we tend to take modest deviations from zero in either direction to still be compatible with the idea of stochastic independence (i.e. we like to interpret the figures more conservatively to not fall for overinterpretation). But the values for De Havilland and particularly Hawker Siddeley are higher than + 100 per cent, that is, the number of actual sales is more than twice the number of expected sales. If, for the sake of convenience, we take “>100 per cent” as a benchmark, we find that colonial ties certainly did matter in the case of British aircraft before 1970. This holds for the French Caravelle (+ 468 per cent), too. The only other values higher than 100 per cent are cb34=+ 162.1 and cb35=+ 2,888.0 for the Convair Coronado of which only nine aircraft were sold to the Global South. But the actual sale of six rather than two aircraft to former and quasi-colonies, as predicted, is not too spectacular and might be an outlier. Taken together, we do find a positive British and French colonial bias for narrow-body sales in that first period, but not for US sales to former and quasi-colonies.

The picture changes if we look at sales of narrow-body jets in the wide-body era starting in 1969 (see Table 4). Although the market continued to grow, British aircraft manufacturers sold fewer aircraft in the period 1970–89 than before. The positive colonial bias for British-manufactured jets vanishes completely. In contrast, both the French Caravelle and the Dutch Fokker 28 profited from a pronounced positive colonial bias of 1,393.3 per cent and 480.4 per cent, respectively. As KLM nearly exclusively relied on Douglas jets at the time and provided Garuda (Indonesia) with technical assistance, Douglas also has a high cb-value. As with the first period, we do not find evidence for a positive US quasi-colonial bias. A special case in this second period in both segments is Airbus because it involved, among others, France and, since 1979, Britain as owner countries. Since Airbus initially sold no A320 jets to airlines from former French colonies, there clearly cannot be a related positive colonial bias. However, there clearly is a positive bias regarding both former UK colonies from the Global North (Ansett Australia) and South (Indian Airlines). A part of this bias should certainly be attributed to Britain; we will come back to the how in a few lines.

Switching to the wide-body segment (see Table 5) leads to results that are very similar to those of Jopp and Spoerer (2021, 2023). Only for (McDonnell) Douglas do we find a cb value larger than 100, tellingly linked with the US's former colonies and quasi-colonies. But Boeing and Lockheed were less successful in Latin America so the combined value for the US manufacturers is low. The results for Airbus are also low and, thus, within the limits of what might still be in line with stochastic independence, so that we can confirm our earlier results.

Up to here, we neglected all rows indicated by “excl. RR” and, respectively, “RR only”. These rows are a special feature in our contingency tables we have yet to explain. According to, for example, Keith Hayward, the market for aero engines was at least as competitive and tight as the market for airframes, with engines being a vital and valuable part of any aircraft. 35 Therefore, it seems reasonable to look for a colonial bias based on the provision of engines to foreign-manufactured aircraft, too. The British aero engine manufacturer Rolls Royce is an instructive case. Besides all British-manufactured jets, Rolls Royce was the exclusive engine provider for Fokker's F28 and F100, Sud Aviation's Caravelle I/III/VI series, Boeing's B707-420 series, Douglas's DC-8-40 series as well as for Lockheed's Tristar. 36 Moreover, Rolls Royce engines were optional regarding certain series of the B747, B757, and B767. To capture this aspect, the contingency tables also provide figures disaggregated by engine provider, that is, Rolls Royce (“RR only”) and the rest (“excl. RR”).

Did jets equipped with Rolls Royce engines sell disproportionally well in former UK colonies? As for the narrow-body segment up until 1969, there is evidence that Boeing could do so in former UK colonies located in the Global South (cb = + 156.3), while Douglas could do so in the Global North (cb = + 150.3). We cannot make such a case for Fokker or Sud Aviation, though. Looking at the narrow-body segment after 1969, we only observe a modest positive deviation regarding Boeing and still no case for Fokker or Sud Aviation. Finally, as for the wide-body segment, Boeing could sell B757-jets equipped with Rolls Royce engines disproportionately well in former UK colonies in the Global North (while selling disproportionately worse in the Global South, though). 37 Taken together, we may also speak of some colonial bias towards the United Kingdom from the perspective of engine provision. 38

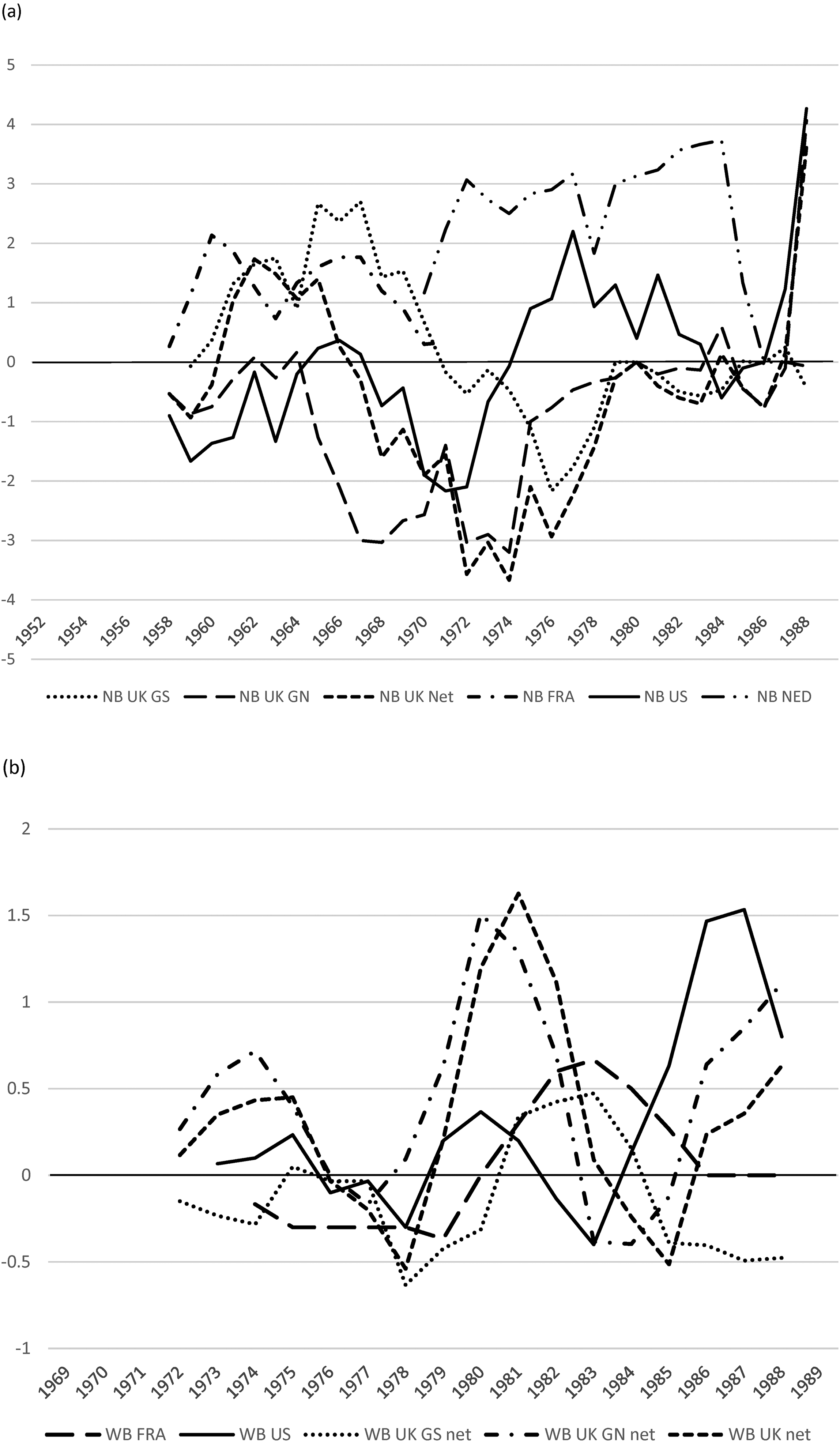

Finally, we seek to depict the colonial bias per producer country year-by-year to be able to locate when precisely the tide for especially UK manufacturers turned. Figure 4 illustrates in two panels the development of the colonial bias. To construct the time series, we had to compute contingency tables for each year and segment (tables not displayed), expressing the bias not as a percentage deviation but as the absolute number of jets sold beyond, or short of, expectations. The straight lines show the colonial bias for Britain, France, the Netherlands (not in panel B), and the United States. For Britain, we also computed a net effect over the Global South (GS) and the Global North (GN). A difficulty for the computation of the bias arises from the fact that Airbus was owned partly by France (37.9 per cent) and since 1979 also by Britain (20.0 per cent; the remainder falling on Germany, 37.9, and Spain, 4.2 per cent). We therefore attributed only 37.9 per cent of Airbus's colonial bias vis-à-vis former French colonies to France, and we did accordingly for Britain regarding Airbus's bias towards former UK colonies. We also consider that Rolls-Royce provided the engines for several foreign-built aircraft. We attributed a flat 50 per cent of Boeing's, Douglas's, Fokker's, and Sud Aviation's (positive or negative) bias towards former UK colonies to Britain; the percentage seems defendable because the engines certainly are an important construction piece.

The development of the colonial bias over time. (a) Narrow-bodies. (b) Wide-bodies. Note: Depicted is a three-year centred moving average of the annual estimates. The bias is reported in terms of jets sold beyond expectations (positive bias) or, respectively, short of expectations (negative bias). Source: Authors’ own computations.

The British (former) colonies are an interesting case: for the (former) British colonies that fall under the Global North category, there is a pronounced negative deviation after 1964 and up until the mid-1970s, when looking at the narrow-body segment. In contrast, we do find a profoundly positive colonial bias in those (former) British colonies who belonged to the Global South in the 1960s and into the early 1970s. We find the same result for the French Caravelle. Both biases peter out shortly after the first oil price crisis of 1973–75. In contrast, the Dutch regional jet Fokker F28 sold disproportionally well in former Dutch colonies – Indonesia in the first place – all over its lifetime of production. For the US manufacturers, the picture is mixed. Relative sales to the Global South were low in the 1960s but increased during and after the first oil price crisis when the British and French models had left the market.

The picture in the wide-body segment looks different. Here we find the aforementioned combined Jumbo-Tristar-effect in the late 1970s and early 1980s connected with airlines from former UK colonies in the Global North. While the graph for the (former) French colonies hovers quite stably around the zero-line – no colonial bias for the Airbus models in either direction – the one for the US manufacturers goes up in the second half of the 1980s, when the Boeing B767 fared quite well in Latin America.

Conclusion

Our main results are that we do find a positive colonial bias for British narrow-body jets until ca. 1973 as well as for the Lockheed Tristar and the B747 (if equipped with British Rolls-Royce engines) from ca. 1977 to 1985. For both the French Caravelle and the Dutch Fokker 28, we also find a clear positive colonial bias over the models’ entire production cycle. Concerning wide-body jets (introduced in 1969) the colonial effects are, apart from the result for the RR-equipped B747 and the Tristar, no longer apparent. Jets of the A300/310 family were not sold disproportionately well to former French and British (after 1979, when British Aerospace joined the Airbus consortium) colonies, and American jets, both narrow- and wide-bodies, were not particularly popular with Latin American airlines except for the last years of our observation period (and the DC-10). Our interpretation of these findings is that colonial ties to former colonial masters from Europe especially mattered until the early/mid-1970s when apparently triggered by the two oil price crises, economic motives became more important than colonial ties in informing procurement decisions. 39

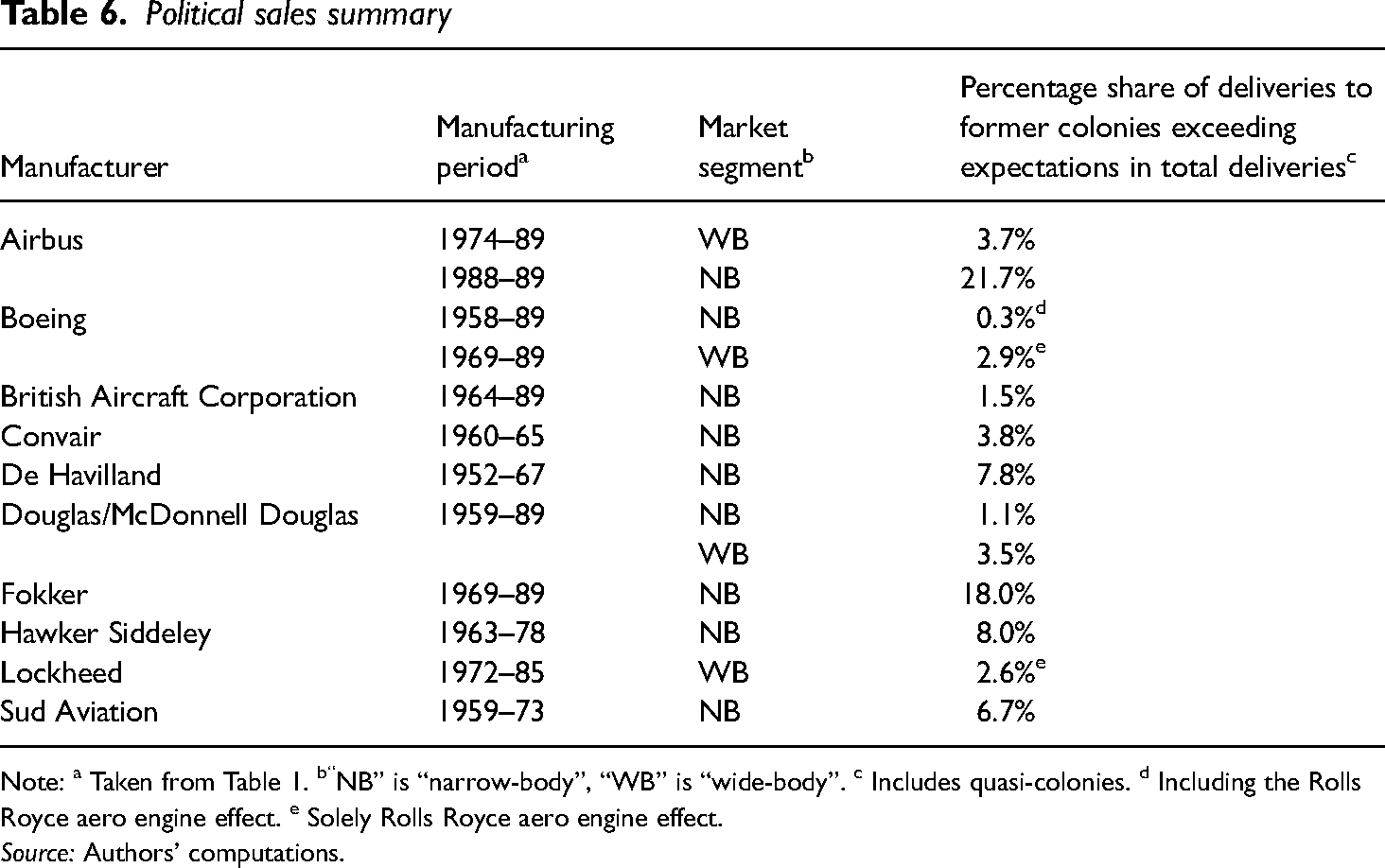

By a simple rearrangement of our quantitative findings, we can put forward an additional notion and link up with the first efforts to determine the percentage of “political sales” in the commercial aircraft industry in its formative period (see the “Placing the study” section). For each manufacturer, Table 6 reports the percentage share of those deliveries to former (quasi-) colonies exceeding expectations according to our contingency table framework (see the “Colonies and aircraft procurement” section). Take the example of the Convair Coronado: The unexpected sales to former (quasi-) colonies of the US amount to 3.8 per cent of all Coronado deliveries in our observation period. We suggest this percentage to be a lower bound estimate of the historical percentage of deliveries up to 1989 that are highly suspicious of having the nature of a political, non-market-induced sale; we call this a “lower bound estimate” because, so far, we only have looked at such political sales potentially arising from colonial ties, specifically. It is quite remarkable that (quasi-) colonial ties played less of a role for American manufacturers than for the Europeans: While the values for the American manufacturers range from 0.3 per cent to 3.8 per cent, those for the Europeans vary (with one exception) between 3.7 per cent and 21.7 per cent.

Political sales summary

Note: a Taken from Table 1. b“NB” is “narrow-body”, “WB” is “wide-body”. c Includes quasi-colonies. d Including the Rolls Royce aero engine effect. e Solely Rolls Royce aero engine effect.

Source: Authors’ computations.

Our findings bear several implications regarding the broader literature on colonial legacy and the special literature on the development of the commercial aircraft industry: firstly, our empirical evidence supports the idea that former colonial ties shape the political and economic relationships between the former colonial master and its colonies beyond formal independence of the latter; in other words, colonial heritage creates path dependence that is reaching well into the post-colonial period and is not easily broken. Secondly, we show this for the example of the air transport sector in the context of which two events of truly worldwide impact – the two oil price crises – seem to have contributed to breaking the path. Finally, thirdly, there seems to be a need for extending the grand narratives of the commercial aviation industry for the role of colonial ties and political sales in the narrower sense of the word.

Supplemental Material

sj-docx-1-jth-10.1177_00225266241265345 - Supplemental material for Civil aircraft procurement and colonial ties: Evidence on the market for jetliners, 1952–89

Supplemental material, sj-docx-1-jth-10.1177_00225266241265345 for Civil aircraft procurement and colonial ties: Evidence on the market for jetliners, 1952–89 by Tobias A. Jopp and Mark Spoerer in The Journal of Transport History

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.