Abstract

We explore the decisions in Parliament about the Swedish tax deduction for commuting since the 1980s. The aim is to explain the continuity of the tax regulation despite several attempts from motions in Parliament and public investigations to reform it towards environmental goals, e.g., reduced emissions of CO2. When reforms have been proposed, the political majority in Parliament has regardless of political colour voted against and retreated to the original motives for the tax deduction; economic growth and the enlargement of regional labour markets. The interests of Swedish mass motorisation succeeded in finding the arguments to slow down reforms and at the same time reinforce the path dependency by adding new legitimacy to the regulation. If the attempts to reform the tax deduction had been part of a broader reform of the transport sector and the tax system, they might have succeeded in breaking with the old path.

Introduction

The number of cars in Sweden increased almost fivefold in the 1950s. The country attained the highest level of car ownership per capita in Europe in the 1960s. 1 From 1945 to 1965, the Swedish Parliament took important decisions to develop Sweden into a ‘car society’. 2 A road plan, decided by the Parliament in 1959, laid the foundation for a new road transport planning, with projections for further strong growth of cars as the point of departure. The road plan outlined the construction of 13,900 km of trunk roads, including 1,310 km of motorways, and 81,000 km of secondary roads across the country until 1975. No arguments were raised in Parliament against the road plan. 3 According to Falkemark, mass motorisation in Sweden had already in the 1930s developed into a large technical system characterised by institutional path dependency and supported by influence from powerful lobby groups that managed to promote private cars as an alternative superior to public transportation. 4 Although Sweden stands out in a European context with its rapid diffusion of private cars in the 1950s, the negative external effects that emerged with the growth in demand for transport have been recognised. These problems include congestion, safety, air pollution and greenhouse gas emissions. Even though congestion and road accidents were well-known occurrences in Sweden before the 1950s, they reached new heights through the growth of mass motorisation. Lundin focuses on the emergence of a group of planning experts as the key advocates of the idea of the ‘car society’ as the solution to these problems. 5 Congestion and road accidents would be possible to eliminate with urban planning and investments in motorways. Lundin's study ends in the late 1960s, when social engineering and urban modernisation had become challenging, but by then mass motorisation had already been stabilised as a cornerstone of the transport system. However, most governments have since the 1990s set explicit goals for the transport sector to become less fossil fuel dependent, and for the sector's emissions such as nitrous oxides and carbon dioxide (CO2) to decrease. The Governments’ focus has generally been on developing and implementing incentives that make consumers choose either to travel by public transport or to choose a car with less harmful emissions. Several studies have shown that the effects of climate policies often conflict with other political goals such as labour market expansion, economic growth, support to low-income households and support to sparsely populated areas. 6 During recent decades, stronger linkages have developed between national tax systems and environmental and transport sector goals. Potter et al. examined the tax deductions for commuting in Germany, the Netherlands, Switzerland and Norway and concluded that minor changes in the taxation regime did not contribute to reach transport and environmental objectives and may well have ended up with negative results. 7 Attempts to add-on an eco-reform to an otherwise unreformed taxation regime were largely counteracted by other parts of the taxation system. In Sweden, the total carbon dioxide emissions from road transport declined by 4 per cent between 1990 and 2014, but if the traffic volume in passenger kilometres had remained unchanged, emissions would – with otherwise the same vehicle fleet – instead have fallen by 22 per cent. 8 Although a part of this development can be explained by population increase, it is still likely that the Swedish institutional setting for car taxation could have countered the national environmental goals that were introduced in the mid-1990s.

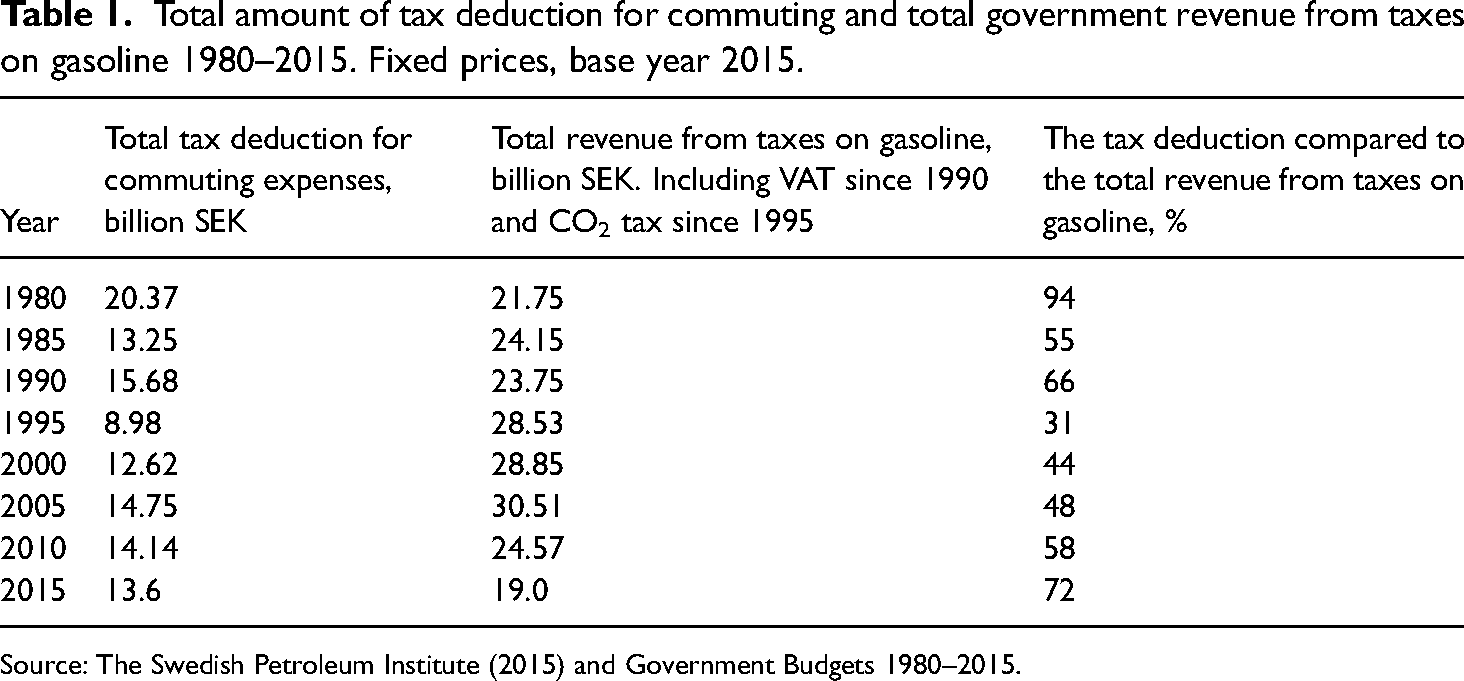

Sweden is not covered in Potter's review, but public investigations have shown that the tax deduction for commuting contributed to increased private car usage also in Sweden and that it increased people's dependency on transportation in general. 9 Although Sweden adopted a carbon dioxide tax both on fuel and vehicle ownership in 1995 and 2006, respectively, the tax deduction for commuting is still in 2022 without a direct incentive to choose a car with less emissions. The average tax reduction for commuting deductions, assuming a marginal tax of 40 per cent, was in 2015 around 6,500 SEK per person and year (equivalent to 750 today's US$). 10 However, the tax reduction was unequally distributed compared to income from work. For just over 30 per cent of the taxpayers with tax reductions, the reduction corresponded in 2015 to between 5 and 20 per cent of their total income from work. Around 7 per cent or just over 7,000 people received a reduction corresponding to more than 20 per cent of their income from work. 11 Furthermore, the tax deduction has corresponded to a substantial part of the total tax income from petroleum sales, including CO2-tax and VAT (Table 1). The tax deduction decreased sharply compared to the total revenue from taxes on gasoline between 1980 and 1985 when changes were made to the tax deduction's regulation. It continued to decrease between 1990 and 1995 mainly due to new climate taxes on gasoline. However, the relative size of the tax deduction has since then increased towards previous levels. Thus, the periods 1980–1985 and 2010–2015 seem to be of special interest for an analysis of the political debates and decisions about the tax deduction for commuting. These periods also coincide with attempts by the Government to reform the tax deduction.

Total amount of tax deduction for commuting and total government revenue from taxes on gasoline 1980–2015. Fixed prices, base year 2015.

Source: The Swedish Petroleum Institute (2015) and Government Budgets 1980–2015.

In 2015, it was possible to deduct costs exceeding 10,000 SEK for commuting to work. 12 For travel by car, a flat rate of 18.50 SEK per 10 km was used. For travel by public transportation, the actual ticket cost was the basis for the deduction. The distance between home and the workplace had to be at least 5 km to get a deduction for travel expenses. To qualify for deductions for travel by car it was necessary to travel at least 5 km, and to regularly gain at least two hours in total per day in travel time, compared to public transport (if available). Even congestion taxes could be deducted, which would offset environmental policies like the Stockholm congestion tax. 13 If public transport was not available in the region, the regulations on the minimum time gain and a distance of at least 5 km did not apply. In 2015, more than 900,000 individuals or 17 per cent of all wage earners received tax deductions for travel expenses. The average deduction for travel to and from work was 14,600 SEK and the total amount of the deduction was 13.6 billion SEK. 14 The reduction in total tax income due to these deductions was about 6.5 billion SEK. Since the 1980s the share of the deduction allocated to travel by public transport has gradually decreased and was in 2015 only 10 per cent. Thus, it is likely that the deduction policy could have offset the effects of climate taxes on private car travel, creating a less effective environmental transport policy. It has on the other hand since the early 1900s been possible for households to deduct the actual costs incurred by income generation. 15 Commuting costs have been handled as private costs in the income tax regulation since they depend on the households’ choice of residential location. However, since these costs have been relatively substantial for many households, there has been an exception to this rule. This exception has caused recurring debates about what parts of the costs of private cars should be deductible. To better understand these policy conflicts, it is necessary to investigate the transport sector's institutional setting during a longer period and analyse the arguments about the deduction policy in detail and within their historical contexts.

Scholars have shown how traditional institutions and practices can be reproduced within new policy contexts showing tendencies of institutional path dependence. 16 The complex and dynamic nature of the transport system is usually characterised by elements of uncertainty, risk, irreversibility, path dependency and lock-in effects. 17 According to a broad and common definition, an institutional setting is path dependent if initial moves in one direction elicit further moves in that same direction with self-reinforcing mechanisms and positive feedback as driving forces. 18 Studies of path dependence usually cover both the origin of the path during an early formative moment when path dependency is established and the mechanisms of self-reinforcement at a later stage. We will focus our investigation on the self-reinforcing mechanisms since the path dependence of mass motorisation according to Falkemark was already in place when the tax deduction for commuting was formally established in the 1950s. Thus, the tax deduction for commuting will represent a subsystem of the path dependency of Swedish mass motorisation, but our study can still contribute with new knowledge of how decisions within a subsystem reinforce the whole system. Tracing this process has so far not been done within this specific policy area. 19

We focus on the periods 1980–1985 and 2010–2015 for the analysis of the debates in Parliament. The first period is motivated by major changes in the regulation of both traffic policy and the commuting tax deduction. The second period is motivated by new taxation of environmentally friendly cars and stronger pressure in Parliament to reform the tax deduction. Both periods cover social democratic and liberal governments (liberal 1980–1982, social democratic 1982–1985, liberal 2010–2014 and social democratic 2014–2015). We will also specifically analyse the major Swedish tax reform of the early 1990s, when the tax deduction for commuting was a part of a broader tax reform agenda.

In general, the results contribute to new knowledge about the difficulties of developing effective environmental policies. The main sources are public investigations and reports, government bills, protocols from Parliament debates and submissions and reports from interest groups in the committee archives at the Swedish National Archive (Riksarkivet).

Research questions:

1. How did the tax deduction's regulation develop over time and how was it allocated since the 1980s?

2. What were the main political arguments in Parliament and in public investigations and submissions from interest groups concerning the tax deduction since the 1980s?

3. How did the political decisions and arguments about the tax deduction adapt to the path-dependent development of mass motorisation and contribute to its self-reinforcement?

The tax deduction for commuting 1980–1992

The fact that the tax deduction for commuting has been in place in its current form since before the 1980s suggests that it has been subject to a variety of driving forces since the economic and political framework in society during this period have changed fundamentally. 20 In this section, we will compare the debates about the tax deduction during two periods characterised by different political and economic frameworks.

In 1979, the Parliament decided on a new Swedish traffic policy that was implemented during the following years. The reform brought with it a fundamental change regarding how the socio-economic costs should be distributed.

21

Since the 1920s, rail and road traffic, in general, should cover their socio-economic costs, including investments in rails and roads. According to the bill, both rail and road traffic should in the future only contribute to the socio-economic marginal cost, while the cost for infrastructure should be covered by the State budget. Even though a liberal government was installed in 1976 for the first time in 44 years, there was still a broad consensus in Parliament between the Social Democrats and the liberal government about these reforms. Falkemark argues that the main motive behind the reform was to increase the railways’ competitiveness, but the new economic principles also supported increased road traffic.

22

However, the Parliament debated measures to reduce private car travel and increase public transport use. The minister of communications, representing the liberal government, argued that a reduction in the tax deduction could affect public transport, car use and settlement structures favourable: Behind the commuting deduction are regional policy, labour market policy and gender equality policy. In addition, the direct economic impact for the individual, state and municipality should also be mentioned. A change in car travel deductions could contribute to increased awareness of the real costs associated with car travel. Both the structure of building settlements and public transport and car utilization could be influenced in a favourable direction from energy and traffic policy. However, after consulting the manager of the budget ministry, I am at this moment not ready to propose any change of the regulation for deduction of costs for commuting.

23

The Minister believed that the tax deduction was an important instrument to reach the goals of regional policy, labour market policy and equality between men and women. The argument about gender equality is not explained further and is not present in other Parliament sources and public investigations during this time. 24 Since the effects of a reduced tax deduction for commuting were seen as negative for the general economic development and could have consequences for the State's and the municipalities’ finances, in the long run, the budget ministry had the final say and the tax deduction remained unchanged.

However, the negative consequences of the tax deduction became clearer in public investigations and government bills in the 1980s. According to a Government bill in 1980, the design of the tax deduction was questionable from several perspectives. 25 The Minister in the liberal government stated that there were strong arguments to regard commuting costs as private living expenses, especially if the costs depended on the taxpayer's decision to settle further away from the workplace. The minister also argued that the tax deduction offset some of the goals of traffic policy, since it favoured commuting by private car and discouraged carpooling and travel by public transport. Other issues concerned the administrative problem of controlling the time-gain rule since there had been several disputes between taxpayers and tax authorities. The Minister for the first time proposed several limitations in the tax deduction's regulation. Firstly, the time-gain rule was increased from one and a half hours to two hours. Secondly, travel costs up to 1,000 SEK (2,000 SEK in 2015 fixed prices) were regarded as personal living expenses, i.e., only costs above this level became deductible. 26

In 1983, the regulation was reformed to only cover variable costs, but this time during a social democratic government. Previously, the tax deduction covered both fixed costs (i.e., the capital cost of purchasing a car, the annual vehicle tax, insurance and garage) and variable costs (i.e., fuel, repairs and maintenance) based on average costs for a smaller car. 27 Fixed costs were regarded as private costs of living, as people normally obtained a car essentially for private use. The deduction per kilometre was set to 1.20 SEK. 28 The only (formally documented) input from interest groups and other organisations during these reforms came from the County Administrative Boards (Länsstyrelsen) of Stockholm and Skåne. 29 The regions argued in favour of the proposal since it would promote public transport. The bill was not connected directly to a public investigation which could explain the absence of formal input from other organisations at this time.

In 1989, a comprehensive public investigation of a major income tax reform suggested that the time-gain rule should be abolished and that the tax deduction should be made dependent only on the distance between home and work and only if the distance to the workplace exceeded 30 km. 30 Thus, the size of the tax deduction would no longer be affected by the choice of transport mode and would give the same benefit for travel by private car or public transport. This would have been a radical change in the regulation, but the investigation's proposal was not included in the government bill. The Minister of communications in the social democratic government argued that large groups of taxpayers, particularly in sparsely populated regions, were depending on car to get to and from work with reasonable commuting times. 31 The investigation's proposal would also, according to the minister, result in a significant and lasting economic hardship for these groups, since it would be difficult for many to move closer to work. Since the bill proposed a fundamental reform of the Swedish income tax system, the tax deduction for commuting was one of many tax issues that were addressed by the proposal. Many interest groups had objections to parts of the tax reform, but only a few mentioned the tax deduction for commuting, and most of them supported the investigation's proposal. 32 Similar proposals would return in the late 1990s and stir up a lot more activity from interest groups.

The first part of the historical overview has shown that up until the early 1990s, the arguments in public investigations and government bills about the tax deduction for commuting were related to geographic and economic accessibility to commuting, and specifically towards supporting households in sparsely populated parts of the country. The main arguments for reforming the tax deduction were that it favoured commuting by private cars, discouraged carpooling and public transport, and that car ownership to a large extent was a private expense that should not be eligible for a tax deduction.

The tax deduction for commuting 1993–2015

Although the main principles for the tax deduction for commuting did not change during the 1990s, there were minor adjustments to the regulation that shows how it was gradually adapted to new circumstances. The tax deduction was reformed with a stricter time-gain rule and a higher cut-off for deductible commuting costs. The major Swedish tax reforms at the beginning of the 1990s did not directly affect the tax deduction, but they caused a push for reform since the changes in income taxation also covered deductions of all kinds. The first public investigation specifically about the tax deduction was presented in 1993. According to the investigation's directives, it should not only propose a simplified regulation but also suggest how the proposals from the former investigation could be implemented in a way that did not reduce the deduction for those with long distances between home and work that could not use public transport.

33

The investigation proposed that the cost of commuting between home and work was of a private nature and that the tax deduction therefore should be abolished completely. But since the Government's directives to the investigation gave no room to suggest that it was abolished, the investigation presented a model with different tax deduction amounts for various travel distances.

34

If the distance between the home and the workplace (single journey) was up to 15 km, no deduction should be allowed. If the distance was between 15 and 30 km, a deduction of SEK 0.80/km should be allowed – regardless of the means of transport. If the distance was longer than 30 km, deductions should be allowed for the distance between 15 and 30 km with SEK 0.80/km and for the part of the distance exceeding 30 km with SEK 1.40/km. For taxpayers that were forced to use a private car due to age, illness or disability, deductions would be allowed with actual cost, but not more than SEK 2.30/km. There should also be deductions allowed for road, bridge and ferry charges. However, these reforms did not appear in the bill. The Minister in the liberal government argued that the issues of the former public investigation's proposal were still not dealt with: As can be seen from the investigation's in-depth analysis of the problems, it is hardly possible to replace the current time limit with distance limits without relatively sharp disadvantages occurring for certain groups with limited access to public transport. The proposal presented by the inquiry can be said to be a modification of the former investigation's proposal, which also meant that the right to deduct was related to a system with distance limits. The disadvantages of e.g., sparsely populated areas with poor communications are mitigated by the investigation's proposal in relation to the former proposal but are still largely present. The modifications have also been made at the cost of a much more complex system of rules.

35

Furthermore, the Minister argued that some groups would be able to receive a larger tax deduction than the actual travel cost. 36 The Minster also referred to the criticism from interest groups, especially from the Swedish Road Federation. 37 This was until now the most ambitious proposal from the government to reform the tax deduction for commuting. The investigation's referral received 58 responses from different organisations and government authorities. We will now have a closer look into their arguments.

Most respondents preferred the existing tax deduction regulation or an even more generous deduction for private cars use, but for different reasons. 38 The major national trade unions LO (Landsorganisationen) and TCO (Tjänstemännens Centralorganisation) supported that public transports should be favoured by the reform but were against the reduced deduction for private car commuting since many of their members usually could not travel by public transport to work (construction workers were explicitly mentioned by LO). Organisations such as the County Administrative Boards (Länsstyrelser) and the Swedish Municipal Association (Svenska Kommunförbundet) were against the proposal as they believed it to be even more bureaucratic than the existing tax deduction. The Car Industry Association (Bilindustriföreningen) wanted the tax deduction to include commuting by company car, which was to be excluded from the tax deduction. Otherwise, there were no comments from interests representing the car manufacturers, despite Sweden's dependence on the car manufacturing industry (Volvo and SAAB) for exports and employment. The Swedish Automobile Association (Motormännens Riksförbund) was strongly against the proposal and argued that the tax deduction should compensate for all costs for commuting by private cars. They suggested an increased deduction of 3 SEK/km. The Swedish Road Federation (Svenska Vägföreningen) opposed the proposal since it would in practice reduce the deduction by 50 per cent for commuters that travelled longer than 30 km single journey. The Swedish Road Federation did not see any arguments to justify the reform and argued that the tax deduction instead should be increased to correspond to the actual cost of commuting by private cars. The Motor Drivers’ Sobriety Association (Motorförarnas Helnykterhetsförbund) was against the proposal for the same reasons as The Swedish Road Federation. On the other hand, the Swedish Local Traffic Association (Svenska Lokaltrafikföreningen) supported the proposal but argued that the increase of the deduction for travel by private car on distances over 30 km should be modified so that both travel by private car and public transport received the same deduction. They also argued against the proposed deductions for road, bridge and ferry charges and justified their arguments with the goals of climate policy.

The responses show that those in favour of the proposal referred to climate policy goals for the transport sector in general, while the arguments against the proposal focused on more specific issues like the needs of certain groups in the labour market or within parts of the country. These differences in arguments will also appear in the investigation of the motions from MPs in the second part of this article.

In 2008, the Government decided to increase the tax deduction with the explicit motive to compensate for an increase in environmental taxes on gasoline and diesel: The income tax deduction for travel expenses between the home and the workplace reduces the expenditure on commuting for many women and men living in rural areas. This is especially true for the areas that are characterized by long distances and where public transport is not expanded nor is it possible to expand. The deduction therefore provides significantly greater opportunities for those who live and work in these areas to find a job without having to move. The deduction also increases the availability of labour for the companies, primarily within the local labour market region. The Government has raised the deduction for commuting by car by 0.05 SEK to 1.85 SEK per kilometre. The increase is a compensation for increased carbon dioxide tax and increased energy tax on diesel.

39

The argument to compensate for higher environmental taxes is related to both higher taxes on gasoline and diesel and the reformed Swedish car tax regulation that was introduced in 2006 and made the annual car tax dependent on the individual car's emissions of CO2.

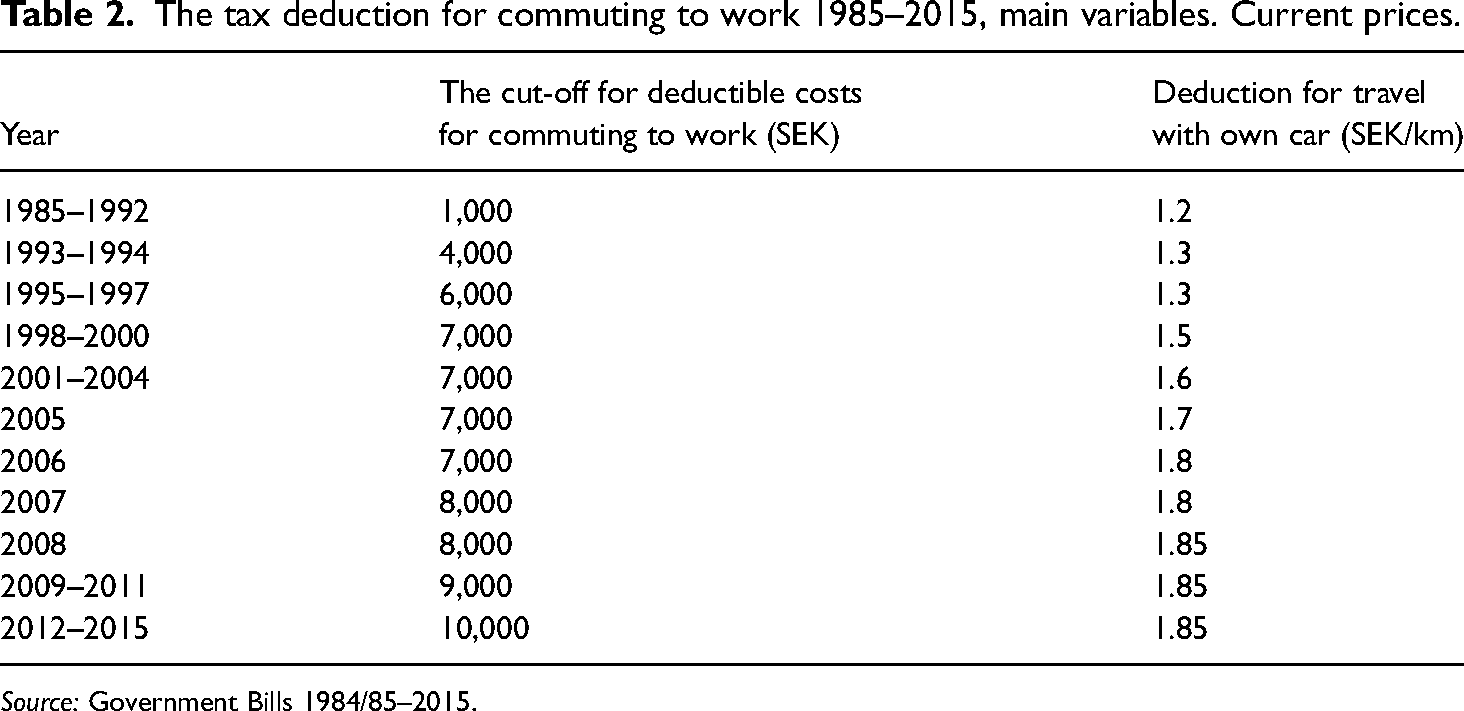

In 2012, the so-called ‘Capacity Investigation’, an investigation carried out by the Swedish Transport Administration, suggested as a part of its ‘climate package’ that the tax deduction for commuting should be reformed within five years to better support the transition towards a carbon dioxide neutral car park in 2030. 40 In 2013, a public investigation about fossil-free transport proposed that a new public investigation should be appointed to analyse the effects of the current tax deduction more deeply and propose either a distance-based system or that the tax deduction is abolished altogether. 41 The most recent public investigation about the tax deduction for commuting was presented in 2019 and proposed a completely reformed tax deduction to better support the transition towards a carbon dioxide-neutral car park. 42 However, when the report was published, the Government directly passed it on to the Government authority Transport Analysis (Trafikanalys) to further study the effects on sparsely populated parts of the country. A summary of the main reforms of the tax deduction regulation since the 1980s shows that it has been a fine-tuning of the regulation rather than fundamental reforms (see Table 2).

The tax deduction for commuting to work 1985–2015, main variables. Current prices.

Source: Government Bills 1984/85–2015.

The cut-off as well as the reimbursement per kilometre have been adjusted several times, although the overall design of the tax deduction has been the same since the 1980s. The cut-off of 1,000 SEK in 1985 corresponds to approximately 2,000 SEK in 2015 in fixed prices. The reimbursement of 1.2 SEK/km in 1985 corresponds to 2.45 SEK in 2015 in fixed prices. Thus, the cost of the tax deduction in the Government budget has been controlled by the Government by adjusting the levels to fit the Government budget. On the other hand, both the costs for congestion charges, bridge tolls and ferry charges have been deductible since the late 1990s. Thus, when the Stockholm congestion charge was introduced in 2007, the cost was deductible for all car owners that were eligible for a tax deduction for commuting, although the congestion charge itself only excluded so-called ‘green cars’ (mainly ethanol/E85 fuelled cars). 43

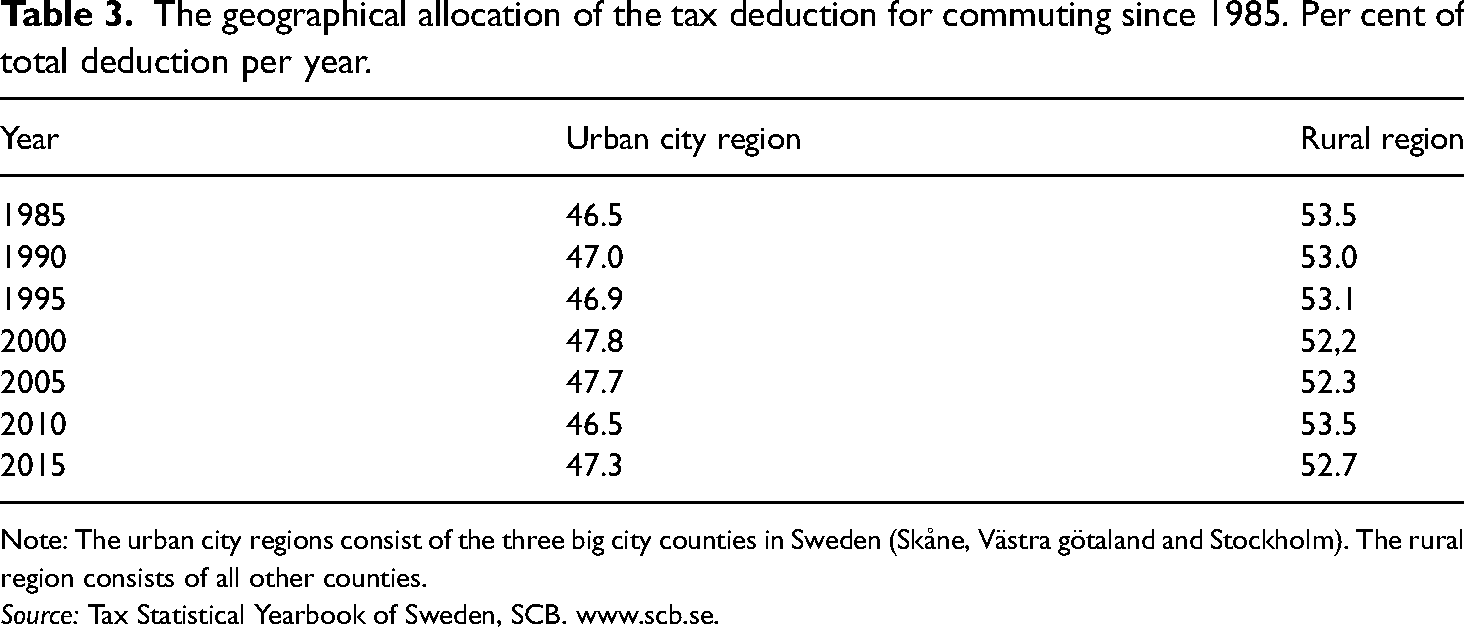

A recurring argument for the tax deduction has been to support commuting in the sparsely populated parts of Sweden that have limited access to public transport. In public investigations, the three big city regions have been compared to the other parts of the country to analyse the geographical allocation of the tax deduction. 44 Table 3 shows the allocation of the tax deduction for commuting for these two regions. The urban city region consists of the three Swedish big city counties (with the cities of Stockholm, Gothenburg and Malmö). The rural region consists of the other more sparsely populated counties.

The geographical allocation of the tax deduction for commuting since 1985. Per cent of total deduction per year.

Note: The urban city regions consist of the three big city counties in Sweden (Skåne, Västra götaland and Stockholm). The rural region consists of all other counties.

Source: Tax Statistical Yearbook of Sweden, SCB. www.scb.se.

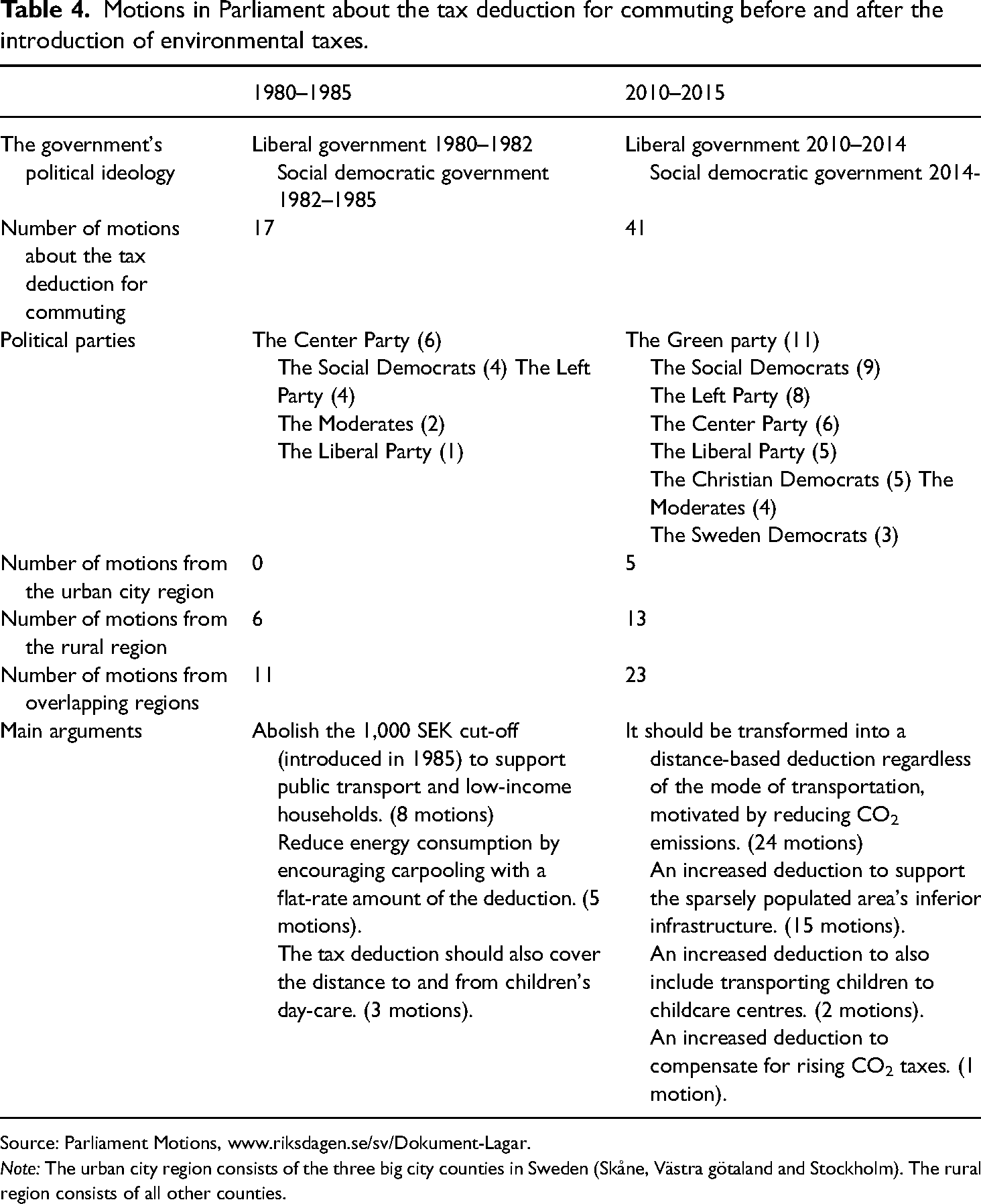

The stability of the regional shares between 1985 and 2015 is not surprising, since the main parts of the regulation have been unchanged since the 1980s. However, the regional shares of the tax deduction are even more stable when compared to the development of the relative shares of the population in these regions. The urban city region that accounted for 48 per cent of the population in 1985 had increased its share to 52.6 per cent in 2015. 45 Thus, the tax deduction shares per capita had a small increase in the more sparsely populated rural region. The frequent arguments for national cohesion, regional development and support for sparsely populated parts of Sweden are still in contrast to the relatively large part of the tax deduction allocated to the urban city regions. Therefore, we need to study the Members of Parliament's (MP's) arguments about the tax deduction with respect to their geographical belongings. The arguments in motions in Parliament during periods before and after the introduction of national environmental taxes in the transport sector are compiled in Table 4.

Motions in Parliament about the tax deduction for commuting before and after the introduction of environmental taxes.

Source: Parliament Motions, www.riksdagen.se/sv/Dokument-Lagar.

Note: The urban city region consists of the three big city counties in Sweden (Skåne, Västra götaland and Stockholm). The rural region consists of all other counties.

The tax deduction has been debated in Parliament almost every year since the 1980s, since it has been a part of the government’s yearly budget bill. Table 4 shows that in the early 1980s the most frequent argument about the tax deduction in Parliament motions was that the 1,000 SEK cut-off should be abolished to support low-income households (eight motions). Although the cut-off was gradually increased to 10,000 SEK in 2012, there were no motions during the period 2010–2015 that argued that it should be abolished. Rather a cut-off was believed necessary for budget reasons during the second period. Furthermore, MPs from the Left Party and the Social Democratic Party argued that ‘it would be a failure for distribution policy to raise the cut-off to 1,000 SEK, as public transport passengers are disadvantaged’.

46

Also, MPs from the Moderate Party representing both the urban city and rural regions opposed the proposed cut-off in the deduction: The proposal means that when calculating the deduction only variable costs are to be considered. /…/ The reason for the proposal is that individuals normally buy a car for essentially private use. Even in such cases, there is no reason not to deduct for depreciation or insurance, both of which increase with the mileage. We therefore reject the proposal to increase the cut-off of the commuting deduction.

47

The second-most frequent argument was that carpooling should be stimulated with a flat-rate amount of the deduction (five motions). MPs from the Center Party representing both the urban city and rural regions argued that this was an urgent matter: ‘especially in the sparsely populated areas it is unfortunately often impossible to use collective means of transport for commuting. Unfortunately, according to surveys, the number of persons (including drivers) in these cars is only about 1.25. Therefore, from both energy and environmental considerations, it is particularly important to seek to achieve increased carpooling’. 48

The third-most frequent argument was that the tax deduction also should cover the distance to and from children's day-care (three motions). This argument was put forth by MPs from parties all over the political scale. MPs from the Moderate Party representing both the urban city and rural regions wrote motions every year in the 1980s arguing that ‘the time required to drive children to and from day-care should be taken into consideration when determining the time to be used for commuting’. 49

To sum up the debates in Parliament in the early 1980s, MPs from all parties in Parliament signed motions about the tax deduction for commuting and were generally in favour of an increase in the tax deduction. On the other hand, within the context of the energy crisis in the 1970s and 1980s, some MPs did propose a flat-rate deduction to promote carpooling, although that would not have reduced the cost for the deduction. None of the demands in the motions were supported by Parliament.

However, the idea of a different kind of tax deduction regulation gained momentum in the early 2010s as a response to the increasing threat of carbon dioxide emissions. The most frequent argument in Parliament motions was that the tax deduction should be distance-based and not dependent on the mode of transportation, to give an incentive to reduce CO2 emissions (24 motions). MPs from the Social Democratic Party representing the rural region argued that this was an urgent matter: The main traffic movement for households is commuting. Today, the tax deduction for commuting benefits travel with harmful emissions. We therefore mean that the government should consider designing a proposal with vehicle-neutral travel deductions to benefit those travelling by public transport or bike. The deduction could be a fixed amount per kilometre for the distance between the workplace and the household.

50

MPs from the Green Party in the rural region argued along similar lines: ‘To promote travel by public transport or by bike, we want to explore the possibility of introducing a transport-neutral, distance-based tax deduction for commuting’. 51 Also, MPs from the Moderate Party in the rural region favoured a distance-based deduction although for other reasons: ‘The commuting deduction's time rule, i.e., saving at least two hours travelling by car, is difficult to control, leading to many incorrect deductions. If this time limit is removed and the travel deduction is based on the distance between the workplace and the home, then travel by car, bike and public transport should be treated equally’. 52

Furthermore, 15 motions argued that an increased tax deduction for commuting was necessary to compensate for sparsely populated area's inferior infrastructure. MPs from the Liberal Party proposed ‘a reallocation of the deduction for commuting in order to increase its regional accuracy and reduce the possibilities of cheating’. Thus, the MPs suggested that the travel deduction should be more generous in municipalities where public transport was less developed, while deductions should be decreased in municipalities with a higher possibility of using public transport. 53 The Sweden Democrats argued along similar lines when MPs from both the urban city and rural regions ‘were concerned about the government's lack of understanding that many people are directly dependent on the car to get to and from work’, and that ‘many people in our country simply live where there are no public transport at all’. These MPs wanted to dramatically increase the commuting deduction to 2.25 SEK/km. 54 One MP from the Green Party commented on the results of a recent public investigation, arguing that ‘one can say that the typical tax deducting commuter is a highly paid man in the outskirts of the metropolitan regions who deliberately cheats on his deductions’. 55 The MP argued that the tax deduction did not specifically support sparsely populated regions in its current form but that it still should be increased since there were no alternative ways to support these transports.

Two motions argued that the tax deduction should be expanded to also include transports that are not directly related to commuting. In this case, MPs from the Moderate Party in the urban city region argued that there are still ‘many necessary car trips that have to be done; children going to day-care, leisure activities, visiting friends and the health care centres, etc’. 56 MPs from the Liberal Party in the rural region believed that it was ‘important to take into consideration that most (people) still drive fossil fuel cars’, and that ‘the high petrol price strikes extremely hard against municipalities with large distances where many depend on the car for commuting’, and that the tax deduction, therefore, should ‘include transports to and from childcare’. 57

One joint motion from the Social Democrats, the Left Party, and the Green Party in both the urban city and rural regions proposed that the overall carbon tax on gasoline should be ‘increased by 0.10 SEK in 2011 and another 0.07 SEK in 2012 per litres’. /…/ to compensate for those who need the car to commute, and for those who use the car at work, we raise the commuting tax deduction by 0.75 SEK per 10 km in 2011 and 1.5 SEK in 2012. 58 This motion was not supported by the liberal government and not accepted by Parliament. Perhaps the most unexpected support for this proposal came from the Green Party which had been actively working for increased environmental taxes in several areas of the economy. In this case, however, the need to compensate people living in the countryside seems to have outweighed the importance of increased overall carbon dioxide taxes on transports. As already noted, the same arguments were used in 2008 in a liberal government bill that argued for an increased commuting tax deduction to compensate for the increased carbon dioxide tax and energy tax on diesel. Since the Social Democrats, the Left Party, and the Green Party were in the opposition between 2006 and 2014, both sides of the Parliament seem to have had a consensus regarding these issues, although the social democratic motion did not pass, probably due to the budget situation in the aftermath of the financial crisis.

To conclude this part of the investigation, there have been three major shifts in the Parliament motions about the tax deduction between the 1980s and the 2010s. Firstly, the total number of motions related to the tax deduction increased from 17 to 41. This probably reflects both a broader political interest in the tax deduction's regulation and an increased conflict regarding the consequences of the regulation. The latter is partly a consequence of the Green Party's entrance into Parliament, since the Green Party stood behind several motions regarding the deduction regulation in the 2010s. Secondly, new arguments appeared during the 2010s. Several motions argued that the deduction should be distance-based regardless of the mode of transportation, motivated by a reduction in CO2 emissions. Furthermore, one motion argued that the deduction should be increased to compensate for rising CO2 taxes, while 15 motions argued that an increase was necessary to support sparsely populated area's inferior infrastructure. Thirdly, the regional representation of active MPs shifted. During the 1980s, most active MPs represented the sparsely populated regions and overlapping regions. In the 2010s, the picture became more complex, with several motions from both regions and an increase in motions from overlapping regions. This suggests that MPs from both regions formed alliances to boost support for more radical changes in the tax deduction, i.e., a change towards a distance-based tax deduction.

Barriers to sustainable transport: a concluding discussion

The first question concerned how the tax deduction's regulation developed and how it was allocated since the 1980s. We have found that the regulation remained relatively unchanged between 1980 and 2015 with only minor adjustments to the minimum level for the deduction and the amount of deduction per kilometre. Furthermore, the geographical allocation has been stable with around 50 per cent to big city regions and the other half to more sparsely populated regions. Although the relative size of the deduction compared to the income from gasoline taxes decreased during the 1990s, it has since then returned to previous levels. This is in line with Falkemark's argument that mass motorisation in Sweden has been characterised by a favourable traffic policy backed up by strong interest groups.

The second question concerned the political arguments about the tax deduction in Parliament and in submissions from interest groups to public investigations. The tax deduction's effect on the regional labour markets has been a persistent argument for the deduction. Labour market mobility has been a frequent argument in motions and government bills and has often been used in connection to goals for regional growth. Since the 1980s there have also been several arguments in public investigations for decreasing or abolishing the tax deduction; environmental concerns, increasing congestion, discrimination of public transport, regional inequality, favouring men over women, expensive for the State budget and difficult to control. The arguments in favour of the tax deduction have been fewer (aspects of labour market mobility) but apparently, they have had a stronger legitimacy over time in Parliament. Those who proposed reforms of the tax deduction did not manage to back their demands with support from other broader political agendas e.g., environmental policy. This conclusion supports one of Falkemark's main arguments that mass motorisation in Sweden (both private cars and trucks) in total has not carried its social costs due to modest taxes and generous subsidies. The broader goals of environmental policies usually receive weaker political mobilisation compared to specific and short-term political goals such as labour market expansion and regional development. 59

The third question concerned how the political decisions and arguments about the tax deduction adapted to the path-dependent development of mass motorisation and contributed to its self-reinforcement. There has been a difference in policy impact between motions in Parliament and government bills. The tax deduction's historical development and the supporting arguments from other sectors of the economy, i.e., labour market policy and regional economic development, legitimised it in Parliament even when demands for environmental adaptation were explicit in several motions. One reason for the lack of reforms may be that MPs submitted most of the motions when their parties were not in a majority in Parliament. Furthermore, the negotiations between the parties that constituted the government appear to have favoured the continuity of the tax deduction's regulation although most motions in Parliament from all parties argued for it to be reduced or abolished. The political majority on each occasion has attached greater importance to economic growth and the enlargement of regional labour markets regardless of political colour. This suggests that regional enlargement has been a strategy for managing a trend towards an ever-increasing spatial mismatch between the geography of the jobs and the geography of the settlements. 60 There are thus many voters to annoy by reducing the commuting deduction. This is a historical circumstance that strengthened the self-reinforcement of the tax deduction, since the very first argument for the policy became even more important for a larger part of the population, and therefore, gained a stronger political influence.

In line with the findings of Potter et al, our investigation also shows that attempts to add-on an eco-reform to an otherwise unreformed taxation regime have been largely counteracted by other political decisions. If the attempts to reform the tax deduction for commuting had been a part of a broader reform of the transport sector and the tax system, it might have weakened the self-reinforcement of the old path of mass motorisation and opened up for other developments.

Footnotes

Acknowledgements

This research was made possible by a research grant to all authors from The Swedish Foundation for Humanities and Social Sciences (Riksbankens Jubileumsfond), P11–0339.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Riksbankens Jubileumsfond (grant number P11-0339).