Abstract

Firms are increasingly facing decisions about operations in markets affected by geopolitical conflicts that attract global attention, but research illuminating the consequences of these decisions remains scarce. In this article, the authors develop a theoretical framework that integrates rational expectations theory with the person-situation framework to explain how investors react to firms’ operational decisions in such markets. Using Russia's war in Ukraine as the empirical context, the authors analyze 289 announcements by 237 firms publicly traded in the United States and United Kingdom during the first month of the conflict. They find that firms announcing a suspension of their operations experience more negative short-term market reactions than firms announcing continued operations. However, these negative reactions are attenuated when suspensions are more anticipated due to prior competitor suspensions, higher public interest in the conflict, larger firm operational footprint in the affected market, and greater preconflict media attention focused on the focal firms. This framework provides important insights for managers faced with both market pressures and stakeholder expectations during geopolitical crises, as well as a theoretical basis for scholars to further examine the consequences of turmoil in firms’ international markets.

In today's connected world, geopolitical crises such as the Russian war in Ukraine, the conflict between Israel and Hamas, or the civil war in Yemen are resonating beyond their geographical borders. These high-profile conflicts present complex dilemmas for international firms operating in the affected regions. Maintaining a presence preserves revenue but may be associated with risks ranging from the safety of employees in the area to the public inferring that firms are taking an ideological position on the conflict. Conversely, market exit leads to immediate revenue loss from that market but eliminates any association with the conflict that could hurt the reputation of the firm in the future. The optimal strategy in such situations is not immediately clear, requiring careful consideration of both financial and reputational factors.

While firms increasingly face these critical strategic decisions during geopolitical conflicts, academic research offers limited guidance on the best course of action. Marketing studies of market exit have focused on competitive dynamics (e.g., Aghaie et al. 2022), regulatory changes (e.g., Moorman, Du, and Mela 2005), or technological disruptions (e.g., Srinivasan, Lilien, and Rangaswamy 2008), often in the context of failing firms (see Karakaya [2000] for a review). In turn, research on firms’ responses to geopolitical crises has typically taken a macro view of risk and overall performance (Dai, Eden, and Beamish 2017; Oh and Oetzel 2011), leaving unanswered how firm- and context-specific characteristics affect firms’ decisions to respond and how those decisions influence firm valuation. Our study addresses this gap by developing a framework to help managers understand and mitigate the valuation losses that firms can incur when withdrawing from conflict-affected markets.

We propose a theoretically grounded framework that identifies how firm- and context-specific contingencies shape stock market reactions to operational suspensions during geopolitical conflicts. Drawing from rational expectations theory (Muth 1961) as our primary theoretical pillar, we argue that investors continuously update their beliefs about firms’ likely responses to conflict based on observable signals, leading to more attenuated market reactions when suspensions are more anticipated. We integrate this overarching theoretical mechanism with insights from the person-situation framework (Dickson 1982), which can help explain why both firm characteristics (such as media visibility and operational footprint) and situational factors (such as competitor actions and public interest) jointly determine market responses. This theoretical integration advances our understanding of how stock markets process information and react to corporate decisions during geopolitical crises by identifying specific contingencies that make operational suspensions more predictable to investors. It can also explain why seemingly similar firms experience different market reactions when suspending operations in conflict zones. For instance, while existing research treats market exit as a uniform event, our framework explains why firms with larger operational footprints or firms making announcements during periods of heightened public interest in the conflict may face different investor reactions compared with smaller firms or those issuing announcements when public scrutiny is low.

We test the predictions of this framework using data pertaining to the conflict between Russia and Ukraine, a major geopolitical event that started in 2022 and that has disrupted global financial markets and commodity prices (e.g., Umar et al. 2022). While emerging literature focuses primarily on the macroeconomic impact of the war itself across industries and economies (e.g., Boungou and Yatié 2022; Yousaf, Patel, and Yarovaya 2022; we summarize this literature in Table WA of Web Appendix A), we examine how international companies that have operations in Russia respond when faced with the prospect of serving a market characterized by high political instability, sanctions, and global public disapproval. This is a current and relevant topic, as firms are increasingly confronted with the prospect of having to abandon markets due to social unrest, conflict, or political upheaval.

We use an event study conducted on a sample of 289 public announcements made by 237 firms publicly traded in the United States and United Kingdom that had business operations in Russia at the beginning of the war in Ukraine. We focus on the first month after the inception of the war in order to more cleanly detect the effect of the conflict itself, as opposed to the effect of adjacent actions such as export controls or disruptions in the supply chain that result from the conflict. We find that investors react negatively to firms’ taking a public stance on the war, and that companies announcing a partial or full suspension experience a more negative stock market response than firms announcing a continuation of operations. However, this negative reaction to suspensions is attenuated when (1) a larger number of competitors have already suspended their operations in Russia, (2) public interest in the conflict is higher, (3) firms have a larger operational footprint in Russia, and (4) firms have higher preconflict media coverage (for partial suspensions). These results validate our theoretical premise that investors react less negatively to operational suspensions when they are more anticipated due to industry pressure, public scrutiny, operational exposure, or information transparency.

Our article differs from prior studies and advances marketing theory and practice in several important ways. First, rather than simply providing a descriptive analysis of the stock market reaction to firms’ actions in the wake of the war in Ukraine, we propose and empirically test an expectations-based theoretical framework that explains how investors react to firms’ announcements regarding their operations in conflict markets. The prior literature offers little consistency in its findings: Studies on earlier conflicts focus more on general market effects than on firm-specific actions, and even recent research on the Russia–Ukraine war yields contradictory findings, with some showing negative investor reactions to exit announcements (e.g., Astvansh et al. 2025; Balyuk and Fedyk 2023; French, Gurdgiev, and Shin 2023) and others showing positive effects (e.g., Kiesel and Kolaric 2023). Moreover, reported effect sizes vary substantially across studies, as summarized in Table WB in Web Appendix B. Our focus on investor responses also complements recent research on consumer reactions, which shows that companies that withdrew from or suspended their Russian operations experienced positive effects on consumer mindset metrics (Fang et al. 2025; Ganesan and Mallapragada 2025).

Second, we address critical methodological limitations prevalent in existing research. Many prior studies rely on convenience samples and secondary data—most notably the widely cited Yale School of Management database (Chief Executive Leadership Institute 2024), which suffers from inconsistencies in data collection, categorization, and temporal precision. Our study overcomes these limitations by implementing a comprehensive sampling approach that captures the full population of affected U.S. and U.K. public firms and applies rigorous verification of announcement dates and systematic classification of firm actions (see Table WC in Web Appendix C).

Third, we develop a novel framework that integrates rational expectations theory with the person-situation framework to explain how financial markets evaluate firms’ responses to geopolitical conflicts. By identifying and empirically validating four key contingencies—competitor actions, public interest, operational footprint, and preconflict media coverage—we go beyond existing knowledge from the market exit literature and offer actionable insights into the factors that shape market reactions to operational suspensions. These findings also provide important managerial guidance showing how firms can better time and communicate operational decisions by leveraging periods of heightened public interest, aligning with industry trends, and using media visibility strategically to manage stakeholder expectations. Though we analyze the Russia–Ukraine war, our theoretical framework applies broadly to investor evaluation of corporate decisions under geopolitical uncertainty in international markets.

How Do Firms React When a Geopolitical Conflict Impacts a Market They Serve?

Scholars have examined firm responses to a variety of exogenous crises, including economic recessions, pandemics, natural disasters, technological disruptions, and terrorism events (Oh and Oetzel 2011; Srinivasan, Lilien, and Sridhar 2011; Tauringana et al. 2021; Wenzel, Stanske, and Lieberman 2021). Our focus is on geopolitical conflicts, defined as disputes, tensions, or clashes between two or more countries or political entities that are rooted in geographical factors, political power dynamics, and strategic interests. We specifically study geopolitical conflicts that attract public attention outside their geography and prompt foreign companies operating in the conflict zone to publicly announce decisions about their ongoing market presence.

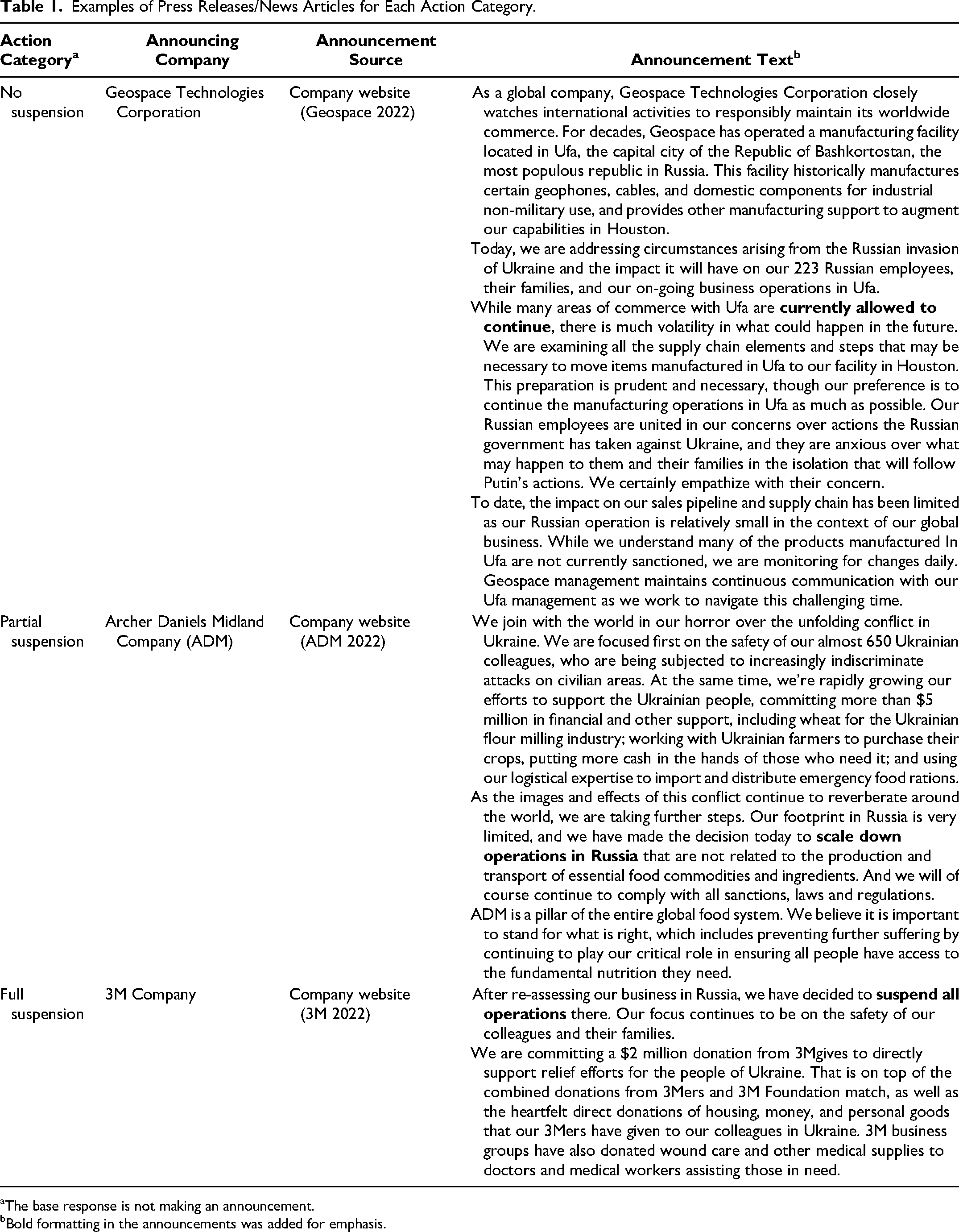

When a geopolitical conflict arises, firms operating in that market must decide whether to take a public stance on their operations in the affected market. These decisions typically fall into one of three categories: (1) full suspension of operations, (2) partial suspension, or (3) no suspension. A full suspension entails complete withdrawal from the market, including closing facilities, halting sales and production, ceasing distribution, withdrawing personnel, and exiting the country. A partial suspension involves limiting specific business functions, such as stopping advertising or new product launches, suspending certain services or product lines, or scaling down operations while maintaining essential services. No suspension reflects continuation of all existing business activities in the focal market without major changes. Examples of each type of action in the context of the Russia–Ukraine war are provided in Table 1.

Examples of Press Releases/News Articles for Each Action Category.

The base response is not making an announcement.

Bold formatting in the announcements was added for emphasis.

These decisions involve complex trade-offs. While suspensions lead to immediate revenue losses, maintaining operations risks reputational damage, political instability, sanctions, and external criticism. Firms that suspend operations often must make public announcements, as stakeholders and media can quickly bring such actions to the public's attention. Firms continuing operations may avoid public statements unless external pressure compels a response.

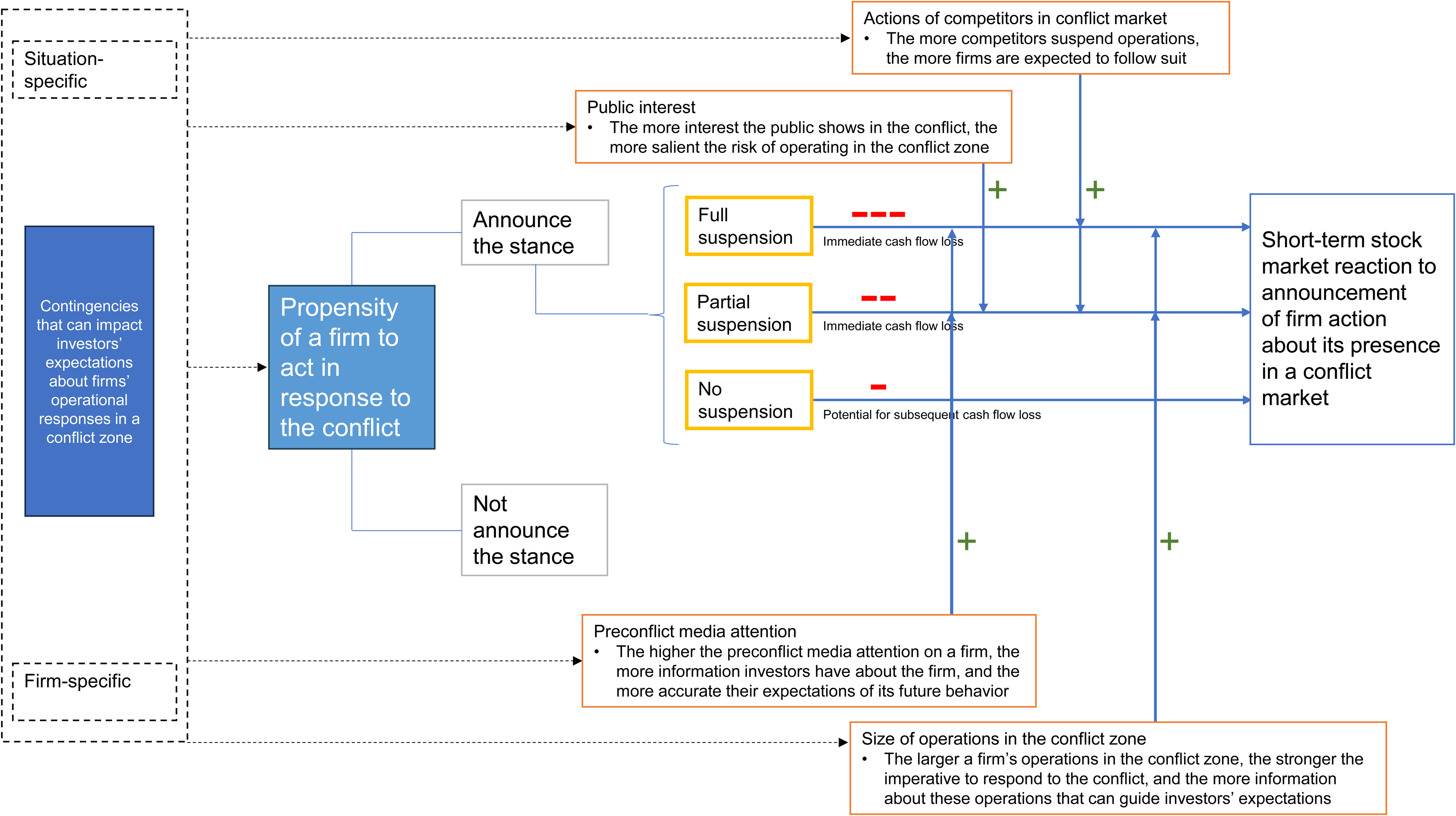

Our study systematically analyzes these operational announcements. Specifically, we develop and test a theoretical framework that explains how investors react to firms’ announcements of operational decisions in conflict markets and how these reactions are shaped by four firm- and context-specific contingencies: competitor actions, public interest in the conflict, operational footprint in the affected market, and preconflict media attention. Figure 1 presents the conceptual model, which illustrates both the direct effect of announcement type on stock market reactions and the moderating effects of these contingencies.

Theoretical Framework of Investor Expectation Formation and of the Short-Term Investor Reactions to Firms’ Announcements of Operational Decisions in Geopolitical Conflict–Affected Markets.

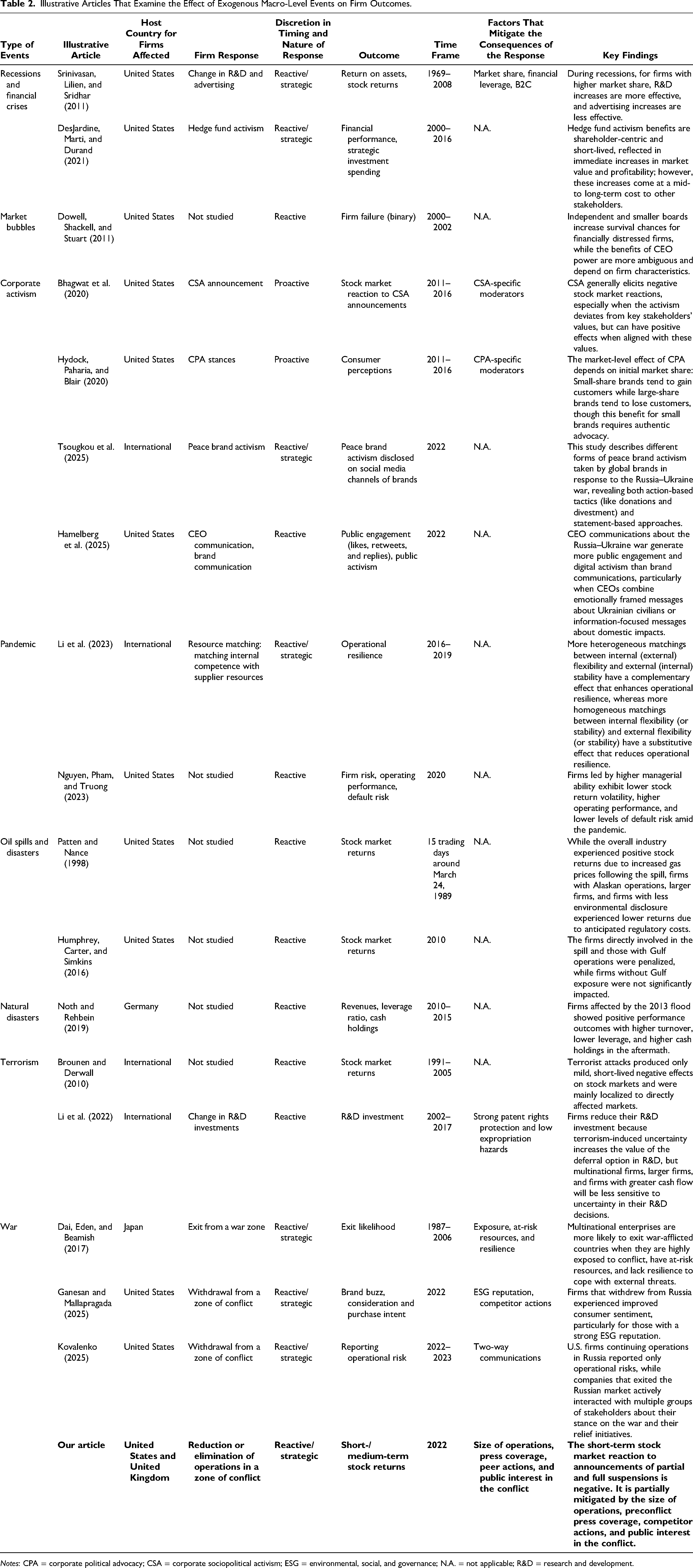

This research contributes to two major streams of literature: (1) market exit and (2) firm behavior in times of crisis. While prior marketing literature has largely focused on the competitive consequences of market exit (e.g., Ozturk, Venkataraman, and Chintagunta 2016) or on exit drivers in stable market settings (e.g., Dixit and Chintagunta 2007), our study extends this work to firms’ withdrawal decisions under geopolitical conflict. Similarly, while research on crisis responses has addressed firm-level resilience and investor reactions to extreme events such as terrorist attacks and natural disasters (Brounen and Derwall 2010; DesJardine, Bansal, and Yang 2019; Karolyi and Martell 2010), we focus on a previously underexplored managerial dilemma: how firms’ voluntary operational decisions in conflict markets are evaluated by investors. Table 2 summarizes how our study differs from prior literature across both streams. 1

Illustrative Articles That Examine the Effect of Exogenous Macro-Level Events on Firm Outcomes.

Notes: CPA = corporate political advocacy; CSA = corporate sociopolitical activism; ESG = environmental, social, and governance; N.A. = not applicable; R&D = research and development.

The Short-Term Stock Market Reaction to Firms’ Announcing Their Stance Regarding Their Operations in a Geopolitical Conflict Market

We examine the short-term stock market reactions to announcements about operational changes in conflict zones because these actions impact a wide range of stakeholders, and traditional accounting measures may not fully capture this broad impact. Stock prices, in contrast, reflect investors’ collective assessment of how firms’ decisions affect their expected future cash flows (Fama 1970). This assessment incorporates both the immediate financial impact of operational changes and investors’ expectations about how various stakeholders will respond to firms’ decisions (Grossman and Stiglitz 1980). Short-term price movements (within one to ten days) offer a clean signal of investor expectations and can influence firms’ cost of capital, debt covenants, employee compensation, and institutional investor evaluations (Brown and Warner 1985).

Our theoretical framework is grounded in rational expectations theory (Muth 1961), which posits that investors form expectations based on available public information and update them as new signals emerge. In this context, a firm's announcement to suspend or continue operations affects forecasts of future cash flows. Suspension decisions, which signal immediate revenue losses, typically prompt negative stock market reactions. However, if such actions align with prior external signals and are anticipated, the negative impact is reduced.

The main theoretical pillar of our research—rational expectations theory—and prior research on investor responses to firm announcements (e.g., Chen, Ganesan, and Liu 2009; Loewenstein and Prelec 1992) suggest a clear baseline effect: Firms that announce partial or full suspensions of operations in a conflict zone will, on average, experience more negative short-term stock market reactions than firms announcing a continuation of operations. The greater certainty of revenue loss explains the sharper negative response to suspension announcements.

However, the extent of this negative reaction can vary considerably across firms and contexts. To identify which factors most strongly shape investor expectations and thus moderate the baseline effect, we draw on the person-situation framework (Dickson 1982), which has been extended to the organizational level in research on crisis response, legitimacy, and stakeholder reactions (e.g., Bundy and Pfarrer 2015; Johns 2006). This framework highlights the importance of both enduring firm-level characteristics (“person”) and contextual or environmental pressures (“situation”) in explaining how organizations respond to external events. Applied to our setting, this framework helps guide the selection of moderators that influence the degree to which a firm's decision is expected or surprising to investors.

Consistent with this logic, we propose and test four moderators: two situational (competitor actions and public interest in the conflict) and two firm-level (operational footprint in the affected market and preconflict media visibility). These variables influence the informational environment surrounding firms’ suspension announcements and thereby shape how investors process the news. We next turn to the specific hypotheses, detailing the mechanism through which these factors moderate the market response to firms’ decisions.

Actions of competitors

Rational expectations theory suggests that investors closely monitor industry patterns to form expectations about firms’ likely responses to geopolitical conflicts (Muth 1961). When a significant number of competitors suspend operations in a conflict zone, such actions become viewed as an appropriate and expected industry response, similar to how peer effects influence decision-making in other business contexts (Shi, Grewal, and Sridhar 2021; Sunder et al. 2017). This perception influences how investors evaluate subsequent suspension announcements, as a continued presence in the conflict zone becomes increasingly difficult to justify to stakeholders (Deephouse 1996; Deephouse and Carter 2005).

This expectation formation process operates through two mechanisms. First, prior suspensions by industry peers provide investors with information about the likely financial implications of such decisions, reducing the uncertainty associated with estimating changes in future cash flows for firms affected by the conflict (Grossman and Stiglitz 1980; Shi, Grewal, and Sridhar 2021). Second, as more firms suspend operations, investors may begin to anticipate that remaining firms will take similar actions to avoid being singled out as condoning the conflict. This continuous updating of expectations means that when firms announce suspensions in industries where many peers have already done so, the market reaction is likely to be more muted since the decision has become more anticipated and the consequences better understood.

Public interest in the geopolitical conflict

Rational expectations theory also explains how investors may assess the impact of public attention to a conflict on firms’ likely responses and their financial implications. When public interest in a geopolitical conflict is high, investors recognize that firms face increased scrutiny of their operational decisions in the conflict area. This heightened attention makes operational and reputational risks of maintaining operations in conflict zones more salient and quantifiable for investors (Tetlock 2007).

In addition, the level of public interest serves as a key signal through which investors form expectations about firms’ decisions. As public attention to a conflict intensifies, investors begin to incorporate the increased probability of operational suspensions into stock prices (e.g., Barber and Odean 1998; Huberman and Regev 2001). They recognize that high public interest creates pressure for strategic responses that protect firms’ reputations, making suspension decisions more predictable. This dynamic applies broadly to conflicts where there is evidence of public disapproval, even if only from a segment of the population. Consequently, when firms announce suspensions during periods of elevated public interest, the market's reaction tends to be more moderate since investors have already partially anticipated such decisions and their implications for firm value.

Size of firms’ operations in a market involved in geopolitical conflict

The size of firms’ operations in a conflict market is likely to be a key factor considered by firms’ investors. First, for firms with larger operations in conflict-affected markets, investors are more likely to anticipate potential operational disruptions and incorporate these expectations into stock prices before any formal announcements are made (Kim and Verrecchia 1991). While a larger footprint in the conflict zone potentially gives firms more resources to mitigate disruptions, it also increases their exposure to risks. By the time the actual suspension announcements occur, these risks are already reflected in stock prices, decreasing marginal information content and resulting in a more muted market reaction.

Second, firms with substantial operations in conflict zones typically provide more detailed risk disclosures and market-specific information in their financial reports. As market participants continuously learn about firms’ risk exposures and likely responses to risk, this increased information flow enables investors to form more precise expectations about potential operational changes, reducing the surprise element of suspension announcements (Diamond and Verrecchia 1991; Doshi, Kumar, and Yerramilli 2018).

Third, market participants recognize that larger operations create stronger imperatives for strategic response (Johns 2006). This understanding leads investors to view suspension decisions by firms with larger operations as more carefully considered and strategically necessary, resulting in more measured market reactions to such announcements.

Preconflict firm-specific media attention

Another factor that can significantly impact investors’ informational load and expectation formation is the preconflict media coverage that firms receive. First, firms with higher preconflict press coverage operate in a richer information environment that enables market participants to develop and continuously update their expectations about potential operational decisions during conflicts (Bushee et al. 2010). When suspension announcements occur for these highly visible firms, the marginal information content is lower as investors have already incorporated expectations into stock prices, resulting in more muted market reactions compared with firms with limited preconflict coverage.

Second, extensive media coverage creates greater transparency about a firm's stakeholder relationships in the affected market (Fang and Peress 2009). This visibility helps investors better understand the complex web of local partnerships, customer relationships, and political connections that influence both the necessity and implications of operational decisions during conflicts. As investors learn more about these stakeholder relationships through media coverage, they can better anticipate how firms might respond to geopolitical tensions, further attenuating market reactions when suspensions are announced.

Data and Method

We examine firms’ decisions to operate in markets experiencing geopolitical crises through the context of the Russia–Ukraine war that began on February 24, 2022. Using an event study methodology, we analyze the stock market reaction to companies’ announcements about their Russian operations made in February and March 2022. Our analysis accounts for potential selection bias in firms’ decisions to take public stances and the endogeneity of specific firm actions. While we focus on announced actions, we note that in highly scrutinized conflicts, unannounced actions are typically publicly visible and thus reported by the press, which would lead to them being captured in our analysis. Actions neither announced nor publicly visible are classified as “no action” since they cannot impact stock prices.

We examine the first month of the war (February 24 to March 26, 2022), when firms’ actions were most directly attributable to the conflict rather than to other strategic factors or external pressures. Our analysis focuses on firms publicly traded in the United States and United Kingdom, allowing for English-language archival searches while extending findings beyond a U.S.-only context. To build our sample, we need three types of data: (1) information about the commercial presence of firms in Russia, (2) information about the actions they took in response to the war, and (3) data on firm and industry-level characteristics that can help us put these actions into context.

Sample Construction

Identifying firms’ Russian footprint

We started with 3,830 firms publicly traded on U.S. and U.K. exchanges since 2021 with available data from Bloomberg, Compustat, and Refinitiv Eikon. Using Orbis and Mergent Intellect databases, supplemented by Factiva searches, we identified 587 firms with Russian operations—540 with physical branches or subsidiaries and 47 operating without a physical presence. 2 From the 587 publicly traded firms that had a business presence in Russia at the beginning of the war, we excluded two companies with significant Russian ownership, Yandex NV and Evraz PLC, because of their close ties with the country that started the conflict.

Identifying the actions that firms took in response to the war

For the remaining 585 companies, we conducted comprehensive Factiva searches using the keyword “Russia” for the first month following the war's onset, supplemented by Google searches combining each firm's name with “Russia” to capture all relevant announcements and press mentions. These comprehensive archival searches ensure that (1) our analysis is based on the full information set available to investors regarding the actions that these firms took in response to the war, (2) we accurately captured the dates when firms announced their stance, and (3) we obtained the full details of their actions.

We collected news articles and announcements reporting business actions regarding Russian operations, along with external callouts, or calls from an external entity directed at firms with a Russian presence, asking them to act or condemning them for not doing so. The announcements in our sample came through press releases, news reports of company actions, management statements, or public CEO letters to employees.

The archival searches resulted in a sample of 333 news or announcements made by 253 firms. From this sample, we excluded six observations by four firms that had a large volume of daily news, which made extracting the effect of their actions relative to the war in Ukraine difficult: Alphabet, Meta Platforms, JPMorgan Chase & Co., and London Stock Exchange Group. We also excluded 38 announcements as follows: all announcements made by the same firm within two days of each other (a total of 25 announcements), and 13 announcements made on the same day as a callout, as the effects of such concurrent events cannot be disentangled.

Obtaining firm and industry data for the empirical analysis

We obtained stock price information from Bloomberg, Yahoo Finance, CRSP (Center for Research in Security Prices), Compustat Global, and Kenneth French's website (French 2025). Financial and accounting data came from Compustat US and Compustat Global, details on board characteristics from BoardEx, and press coverage from RavenPack. We obtained data on firms’ corporate social responsibility (CSR) reputations in the human rights arena from Refinitiv Eikon. Since the events took place in March 2022, the covariates in our analysis are measured as of the end of 2021.

Final sample

Our final sample contains 289 events—announcements and news reports—about the stance that 237 firms (publicly traded in the United States and United Kingdom) with Russian operations took regarding their commercial presence in Russia. As these statistics indicate, some firms made more than one announcement in the first month following the war, sometimes changing their original position and other times reiterating it. 3 In addition, our analysis also accounts for the 332 firms that had a Russian presence but chose to not take any public actions. Table WD in Web Appendix D presents in more detail all the steps we took in constructing the sample.

Modeling the Stock Market Reaction to Firms’ Responses to the War

We classified the various positions that firms took when they responded to the war in Ukraine using a content analysis of the 289 events in our sample. The announcements fall into one of the three previously described categories: (1) no suspension—the announcement indicates that the firm will continue its existing operations in Russia; (2) partial suspension—the announcement indicates that the firm will take partial actions to limit its business in Russia, such as stopping advertising and future investments in the region, suspending some of its operations or nonessential business activities, or suspending new sales but still serving existing accounts; and (3) full suspension—the announcement indicates suspension of all operations in Russia or complete exit from the region. All announcements, as well as the heuristics that the authors used to classify them, are presented in Web Appendix E.

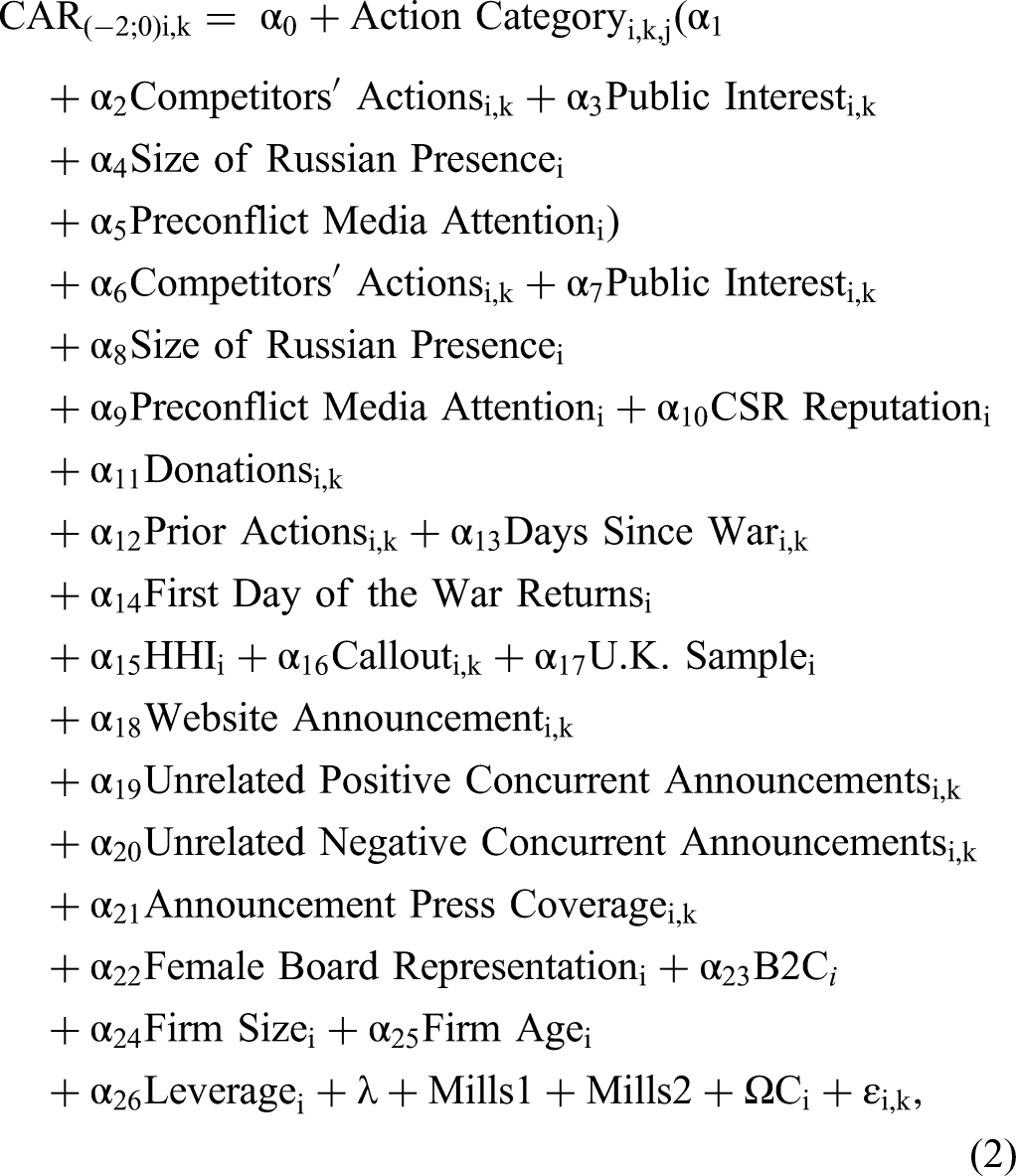

To investigate investors’ reaction to these actions, we use a short-term event study with the market model (MM) and the Fama–French four-factor model (FF) as benchmark models. Short-term event studies have been extensively used in business research because they provide cleaner identification of causal effects, minimize confounding events that could bias results, and enable more precise measurement of the market's interpretation of specific firm actions. We calculate abnormal returns (ARs) as the difference between expected and realized rate of returns (see Sorescu, Warren, and Ertekin [2017] and Fama and French [2015] for the four-factor model), and obtain cumulative abnormal returns (CARs) around each announcement during the (t1, t2) period:

To select the appropriate time window for the analysis, we follow prior research and calculate CARs for several windows around the event and choose for our analysis the window with the most significant t-statistic: (−2, 0) (Ertekin, Sorescu, and Houston 2018; Swaminathan and Moorman 2009). CAR measurement windows that include days preceding the event are common in the literature—for example, Agrawal and Kamakura (1995) use (−1, 0), Homburg, Vollmayr, and Hahn (2014) use (−1, 0), Wiles and Danielova (2009) use (−2, 0), and Bhagwat et al. (2020) use (−2, 2)—and suggest that news of some of these announcements may have leaked before they were formally made. We use the CARs as the dependent variable in a model of the determinants of the stock market reaction to companies’ response to the war in Ukraine:

Focal Independent Variables and Control Variables

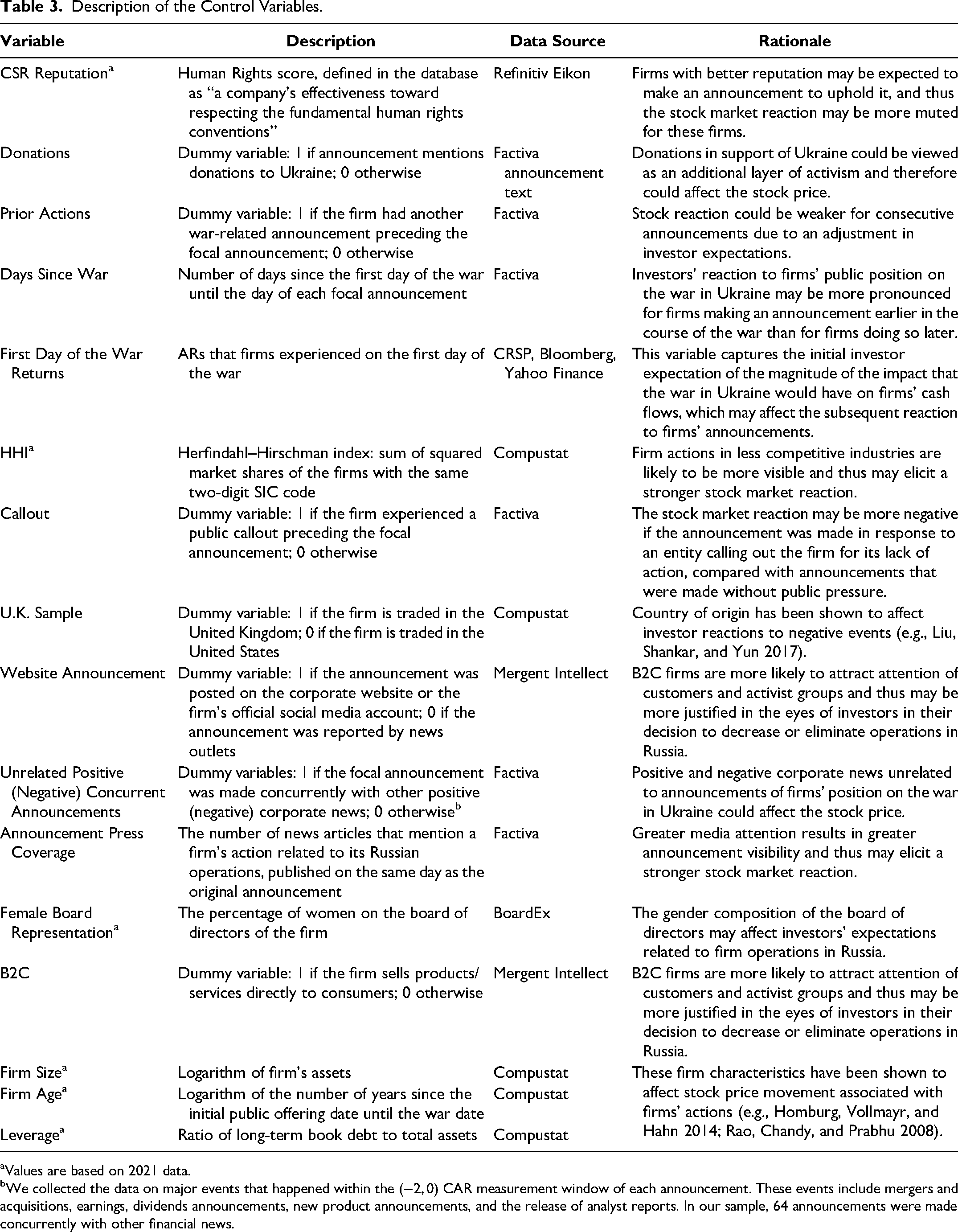

Competitors’ Actions is the logarithm of the number of firms operating within the same two-digit Standard Industrial Classification (SIC) code that announced a partial or full suspension of their operation in Russia in response to the war. Public Interest is the Google Trends index that reflects the volume of public internet searches for the term “War in Ukraine” during the week of a firm's announcement. The index is normalized on a scale from 0 to 100, where 100 represents the peak popularity for the term. Size of Russian Presence is the logarithm of the number of Russian subsidiaries each firm has, obtained from Mergent Intellect and Orbis databases. Preconflict Media Attention is the total number of publicly available news articles and media reports mentioning a firm during the six months preceding the start of the war in Ukraine. The news data are obtained from the RavenPack database and capture the total volume of publicity associated with the firm in the prewar period. Table 3 presents the rationale, operationalization, and data sources for the control variables included in our models.

Description of the Control Variables.

Values are based on 2021 data.

We collected the data on major events that happened within the (−2, 0) CAR measurement window of each announcement. These events include mergers and acquisitions, earnings, dividends announcements, new product announcements, and the release of analyst reports. In our sample, 64 announcements were made concurrently with other financial news.

Identification Strategy

We account for two sources of bias in our model. First, we account for the potential selection bias associated with the choice to take a public stance versus stay silent and not publicly share the firm's plans regarding its operations in Russia. Second, for the firms that do take a public stance, we account for the endogeneity of the choice of the type of stance adopted by firms: not suspend, fully suspend, or partially suspend operations. 4

Accounting for the sample selection bias associated with taking a public position against the war

To address potential selection bias from unobservable factors driving firms’ decisions to take stances on the war, we employ a Heckman approach (Heckman 1979). Using all firms with a Russian presence, both those that made and did not make war-related operational announcements, we specify a probit model predicting the probability of firms making public announcements about their Russian operations:

To satisfy the Heckman model's identification requirement, we use Leadership Communication Focus as our exclusion restriction, calculated as the log of the total number of the focal firms’ senior leadership positions (e.g., directors, officers, senior managers) that include communication-related responsibilities or titles. Specifically, we searched for all senior roles with titles that include the following words: “communications” (e.g., corporate communications, external communications, strategic communications), “relations” (e.g., public relations, media relations, external relations, stakeholder relations), “corporate affairs,” and “public affairs.” A high number of communication roles within senior management indicates a strong emphasis on communication in the leadership structure and the presence of communication expertise within the leadership team. We therefore expect that Leadership Communication Focus verifies the relevance condition because firms with formal communication positions among their leadership are more likely to announce their strategic positions, including their operational stance toward the conflict. We also argue that Leadership Communication Focus is exogenous with respect to the outcome because it should not directly affect investor reactions to war-related announcements. Investors respond to the news content itself rather than the organizational structure that facilitated its release, which was known to them ahead of time.

All other variables in the selection model are firm-level variables included in the main CARs model and have been defined in the previous section. Announcement-level variables from the CARs model do not have observations for the firms that did not take a stance on the war and thus are not included in the selection model. We estimate Equations 2 and 3 jointly using maximum likelihood estimation and use robust standard errors clustered at the firm level. The maximum likelihood estimation procedure jointly estimates all parameters by maximizing the full likelihood function that accounts for the selection and outcome equations simultaneously.

Accounting for the endogeneity associated with the choice of stance against the war

To address potential endogeneity in firms’ choices between full, partial, or no suspension of Russian operations, we estimate a multinomial logit model predicting the probability of each action type. The dependent variable, the type of action taken by the firm, has three levels: Level 0, no suspension, is the base category; Level 1 is a partial suspension; and Level 2 is a full suspension. Using this model, we obtain two generalized inverse Mills ratios that are included in the CARs model to correct for endogeneity (Bourguignon, Fournier, and Gurgand 2007; Wooldridge 1995). The Mills ratios are

where Pij is the probability of a firm announcing one of the three actions regarding its operations in Russia. This probability is given by

where εij is an error term and

where i denotes the firm, k denotes the announcement, and j denotes the action type taken by firm i. All variables, except the two instruments discussed subsequently, are as described previously. Announcement Press Coverage is not included in the action choice model due to its temporal distance from the decision-making process, such that announcement-specific media coverage becomes apparent after a certain action is announced and thus cannot determine a firm's choice among the three action types.

Peers-of-Peers Russian Market Prevalence (PRMP) and Ownership Concentration serve as instruments accounting for the endogeneity of the choice of firm action. PRMP captures the prominence of the Russian market for the second-degree peer firms of each focal company (Shi, Grewal, and Sridhar 2021). Peer firms are all companies that operate in the same two-digit SIC codes as the focal firms, and second-degree peers are all firms that operate within the same two-digit SIC codes (primary and secondary) of the peers. We focus on two main two-digit SIC industry codes associated with the focal firm in defining the peers and computing the instruments. Specifically, we use the primary and secondary two-digit SIC codes obtained from the Orbis database 5 and calculate PRMP as the average number of second-degree peers (competitors’ peers) that have a presence in Russia.

The second instrument, Ownership Concentration, captures the degree of independence of each firm from its shareholders, and it is available in Orbis. It takes a value of 1 when no shareholder has more than 25% of direct or total ownership of the company, implying that ownership is dispersed among various shareholders, and 0 otherwise.

To support the validity of the proposed instruments, we must establish both relevance and exogeneity (instruments predict the endogenous variable but affect the dependent variable only through this mechanism). We expect that higher PRMP (greater Russian market prominence) increases the suspension probability as these industries face greater scrutiny and pressure during the war. We verify that this is true and report in the next section a more negative stock market reaction for firms with a presence in Russia on the day when the war started than for firms without Russian operations. Conversely, higher Ownership Concentration likely decreases the full suspension probability, as dispersed ownership reflects diverse investor views, and decisions are less influenced by the interests of a few dominant shareholders, making radical stances (i.e., full suspension of operations) less likely.

Both instruments should meet the exclusion restriction by being uncorrelated with unobservable shocks affecting stock market reactions to announcements. Following Shi, Grewal, and Sridhar (2021), we argue that peer-of-peer instruments meet this criterion as second-degree peers lie outside the focal firm's immediate peer group and are unlikely to share idiosyncratic shocks with the focal firms. Similarly, Ownership Concentration is publicly known and should be incorporated in baseline stock prices, affecting market reactions only through its influence on the choice of action announced.

Results

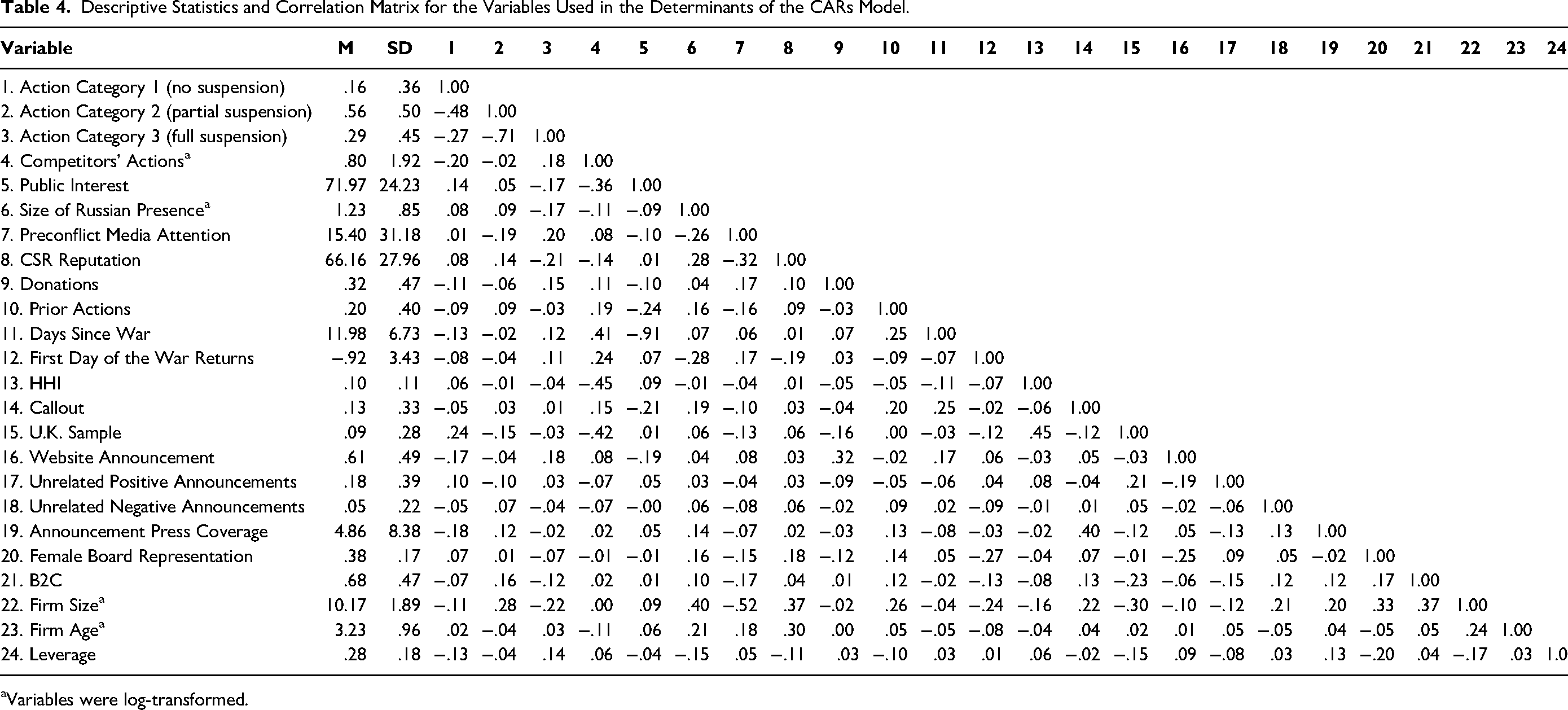

Descriptive Statistics

Descriptive statistics for the variables used in the CARs model are presented in Table 4, and those for the data used in the selection bias correction model are presented in Table WF of Web Appendix F. Out of 289 announcements in our sample, 45 (15.6%) state the intention to continue with existing operations with no changes (no suspension); 161 (55.7%) suggest a partial suspension of Russian operations, and 83 announcements (28.7%) indicate a full suspension/exit from the Russian market. On average, firms in our sample had five subsidiaries in Russia at the start of the war and were mentioned in the news 15 times during the six-month period before the beginning of the war in Ukraine. In our sample, 32% of announcements discuss company donations to Ukraine; 20% of announcements were preceded by another public action by the same firm, and 13% were preceded by a callout.

Descriptive Statistics and Correlation Matrix for the Variables Used in the Determinants of the CARs Model.

Variables were log-transformed.

Results of the Short-Term Event Study

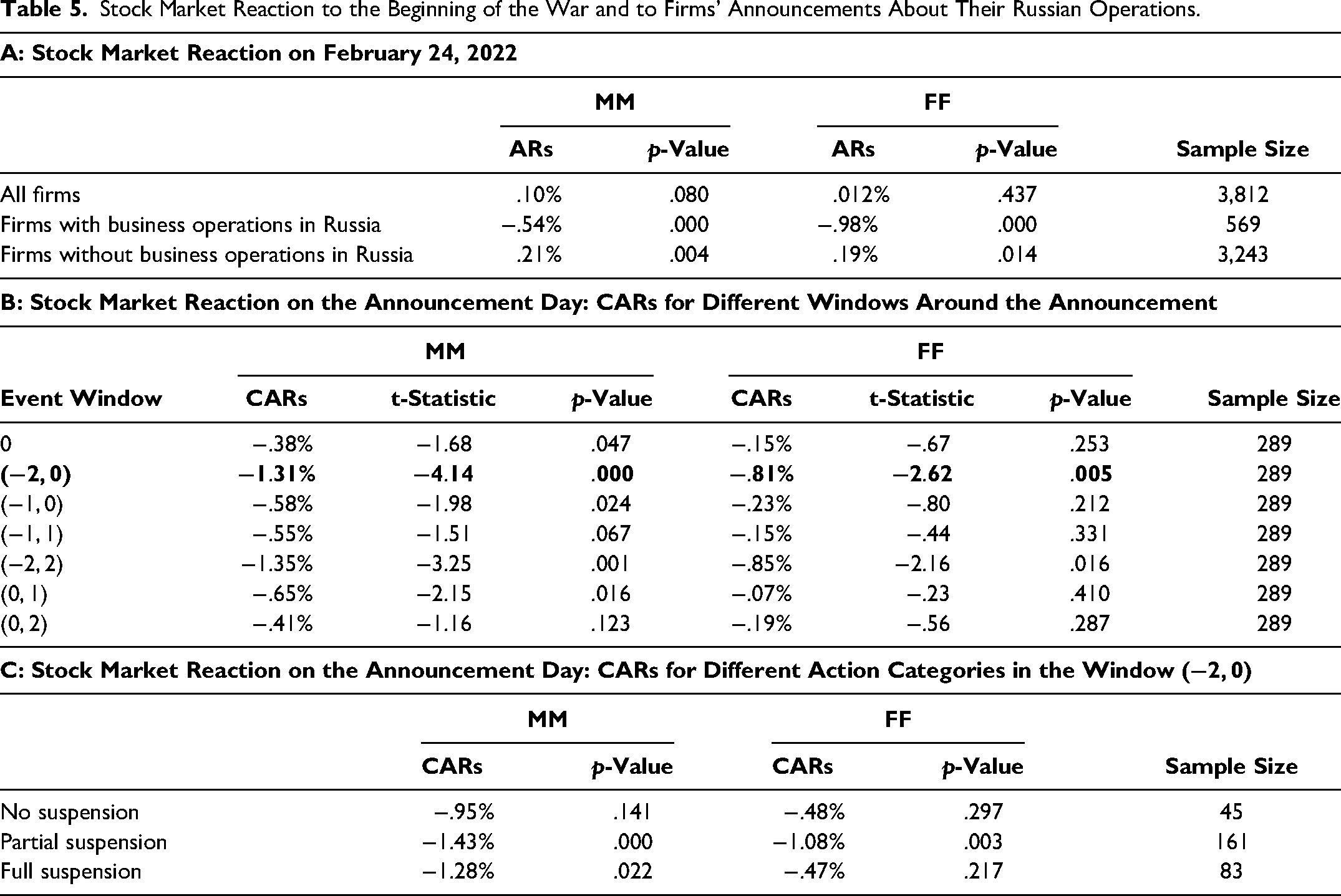

Table 5, Panel A, presents evidence of the stock market reaction on the first day of the war. Overall, the stock market did not experience significant abnormal returns on February 24, 2022 (MM: ARs = .10%, p = .080; FF: ARs = .012%, p = .437). However, not surprisingly, we find that the stock market reaction on the day of the war depends on whether the companies had business operations in Russia at the time. Specifically, for firms with business presence in Russia, the ARs are negative and significant (MM: ARs = −.54%, p = .000; FF: ARs = −.98%, p = .000), while for the companies that did not have operations in Russia, the ARs are positive (MM: ARs = .21%, p = .004; FF: ARs = .19%, p = .014). This highlights the validity of our sample and of our expectation-based theoretical support, as it appears that investors anticipated a loss in cash flow for firms operating in Russia as early as the day the conflict started.

Stock Market Reaction to the Beginning of the War and to Firms’ Announcements About Their Russian Operations.

Firms that made any announcement about their operations in Russia experienced, on average, significant negative CARs across several windows around this event. The results are summarized in Table 5, Panel B. As explained in the “Data and Method” section, we use the window (−2, 0) with the most significant t-statistics for subsequent analyses.

The stock market reactions to the three different action categories, presented in Table 5, Panel C, reveal that firms announcing partial or full suspension of their operations in Russia experience negative CARs (partial suspension: MM: CARs = −1.43%, p = .000; FF: CARs = −1.08%, p = .003; full suspension: MM: CARs = −1.28%, p = .022; FF: CARs = −.47%, p = .217). The FF CARs for the full suspension do not attain significance, possibly because of the small size of the subsample of firms that made these announcements. We do not observe a significant stock market reaction to announcements that indicate an intention to continue with existing Russian operations (no suspension: MM: CARs = −.95%, p = .141; FF: CARs = −.48%, p = .297).

Cross-Sectional Analysis of the Short-Term CARs

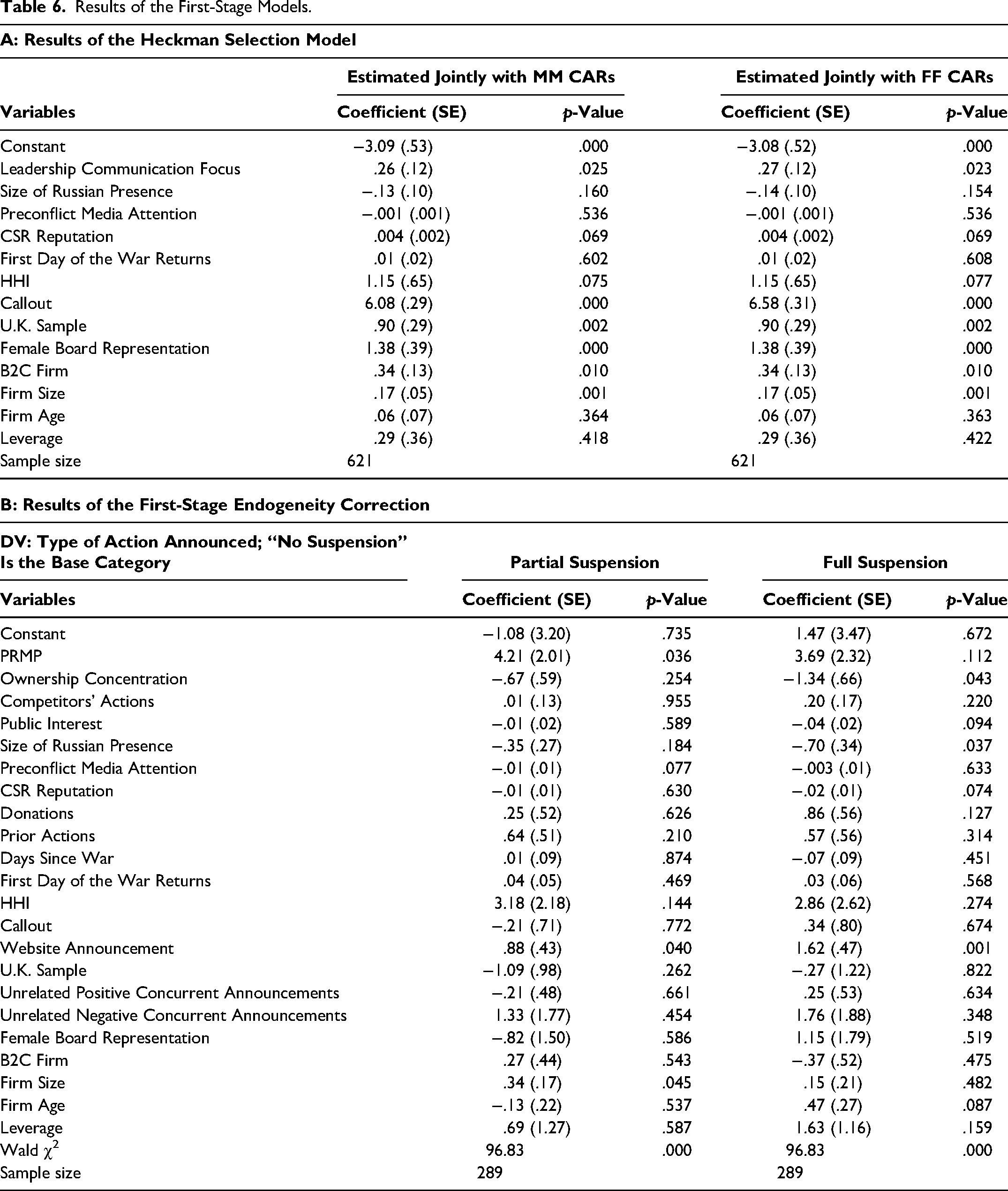

Results of the cross-sectional analysis are presented in Tables 6 and 7. Table 6, Panel A, summarizes the findings of the selection model. Since Equations 2 and 3 are estimated jointly, the estimates of Equation 3 vary slightly across the two specifications of the CARs model (MM and FF CARs, respectively, as a dependent variable).

Results of the First-Stage Models.

Determinants of CARs to Announcements of Actions Pertaining to Russian Operations.

Notes: Standard errors are in parentheses. Industry dummies are omitted for parsimony. Wald χ2 represents a joint statistic for the selection and the determinants of the CARs models.

In the first stage of the selection model, we find that the exclusion restriction, Leadership Communication Focus, has a significant positive effect on the probability of a firm making a public statement in response to the war in Ukraine (Leadership Communication Focus: MM: β = .26; p = .025; FF: β = .27; p = .023), underscoring the validity of using it to control for the possibility of selection bias. Other significant determinants of the propensity to make an announcement include whether or not firms experienced a callout; the ones that do are more likely to take a stance in regard to their business in Russia (Callout: MM: β = 6.08; p = .000; FF: β = 6.58; p = .000). This suggests that public callouts are a powerful tool to pressure companies to respond. We also find that companies with a higher percentage of women on their board of directors are more likely to take a stance against the war (Female Board Representation: MM: β = 1.38; p = .000; FF: β = 1.38; p = .000). This finding could be explained by prior research linking female board representation to more ethical corporate decisions (e.g., Bernardi and Threadgill 2010; Wowak et al. 2021). Finally, larger firms and B2C companies are more likely to make a war-related announcement, possibly due to their higher visibility and greater public scrutiny compared with B2B firms and smaller companies (Firm Size: MM: β = .17; p = .001; FF: β = .17; p = .001; B2C: MM: β = .34; p = .010; FF: β = .34; p = .010).

The results of the multinomial model of the determinants of the type of action announced by the firm, which we use to obtain endogeneity correction factors, are presented in Table 6, Panel B. We find that both PRMP and Ownership Concentration have a significant effect on the choice of the announcement made, which verifies the relevance of these two variables as instruments. PRMP is significant in the model comparing the probability of partial suspension to no suspension (partial suspension: γ = 4.21; p = .036), suggesting that firms operating in industries with a greater number of peers with Russian presence are more likely to partially suspend their operations, potentially due to increased visibility of such industries. In line with our expectations, we also find that firms with low Ownership Concentration are less likely to announce a more radical stance (full suspension: γ = −1.34; p = .043). In addition, our results indicate that larger firms are more likely to announce a partial suspension (γ = .34; p = .045), while firms that make announcements on their corporate websites or official social media accounts (rather than through media outlets) are less likely to announce a continuation of operations (partial suspension: γ = .88; p = .040; full suspension: γ = 1.62; p = .001).

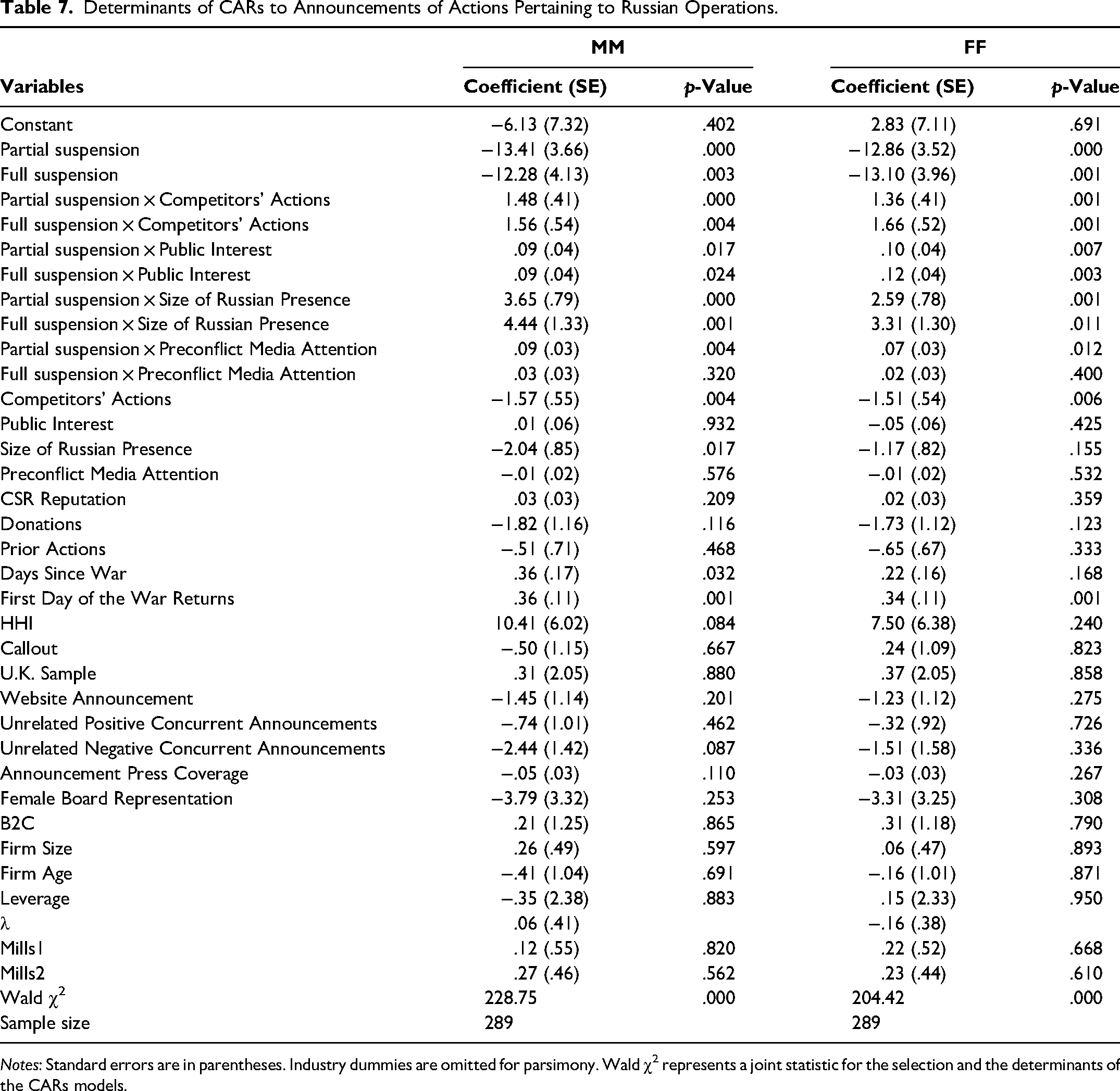

Table 7 summarizes the results of the model assessing the financial consequences of taking a stance on the war. The findings indicate that firms choosing to suspend operations—either partially or fully—experience, on average, a more negative stock market reaction compared with firms announcing that they intend to continue operations in Russia without any changes (partial suspension: MM: α = −13.41, p = .000; FF: α = −12.86, p = .000; full suspension: MM: α = −12.28, p = .003; FF: α = −13.10, p = .001). However, this negative effect is moderated by two situation factors: competitors’ actions and public interest in the conflict, and two firm-level (“person”) factors: the size of Russian presence and preconflict media attention.

Consistent with H1, we find that investors’ reaction to announcements of partial or full suspensions is less negative when firms align their decisions with competitors’. Specifically, firms that announce suspension of operations experience less negative stock market reactions if their competitors have also reduced or eliminated their presence in Russia (partial suspension × Competitors’ Actions: MM: α = 1.48. p = .000; FF: α = 1.36, p = .001; full suspension × Competitors’ Actions: MM: α = 1.56, p = .004; FF: α = 1.66, p = .001). Similarly, in line with H2, the stock market reacts less negatively to partial and full suspensions when public interest in the conflict is high. Under conditions of high public attention and scrutiny, firms making suspension announcements experience less negative CARs compared with firms opting to maintain their operations in Russia (partial suspension × Public Interest: MM: α = .09, p = .017; FF: α = .10, p = .007; full suspension × Public Interest: MM: α = .09, p = .024; FF: α = .12, p = .003). The negative effect associated with partial and full suspension is also partially mitigated by the size of the firm's Russian presence. Specifically, in support of H3, the interactions between partial suspension or full suspension, respectively, and the size of the firm's Russian presence are both positive and significant (partial suspension × Size of Russian Presence: MM: α = 3.65, p = .000; FF: α = 2.59, p = .001; full suspension × Size of Russian Presence: MM: α = 4.44, p = .001; FF: α = 3.31, p = .011), suggesting that firms with a greater Russian presence experience less negative CARs if they announce a partial or a full suspension of Russian operations as a result of the war, compared with firms that announce no suspension. Finally, we find that preconflict media attention also moderates the stock market response to firms’ suspension announcements, but its effect varies by the type of suspension. Firms with high preconflict media attention receive a more positive reaction when announcing partial suspensions (partial suspension × Preconflict Media Attention: MM: α = .09, p = .004; FF: α = .07, p = .012). However, this effect does not hold for firms announcing a full suspension (full suspension × Preconflict Media Attention: MM: α = .03, p = .320; FF: α = .02, p = .400), providing partial support for H4. 6

Robustness Checks

We conduct several robustness checks and present the results in Tables WG1 and WG2 of Web Appendix G. Several firms in our main sample made more than one announcement. We considered all these announcements in our main analysis. To check whether our results are robust to using only the first war-related announcement issued by each firm in the sample, we reestimate the models on a sub-sample of first news only. We find that our main results remain consistent with the results obtained on the full sample, with all coefficients of interest similar in direction, magnitude, and significance.

We also estimate our models on a subsample that only includes the last action announced within our sample period. We find that all previous results replicate. The only exception is the coefficient of the interaction between Partial Suspension and Public Interest, which became marginally significant (p = .058) in the MM CARs model only.

To test the robustness of our results to alternative measures of the size of the firm's Russian presence, we created an alternative measure using Orbis's subsidiary size classifications (small = 1, medium = 2, large = 3, very large = 4). We calculated the size of Russian presence as the log sum of size values of all subsidiaries owned by each firm in our sample. Though available for only 208 companies, this alternative measure yielded similar results, with coefficients consistent in direction and magnitude with our main findings at 10% significance or better.

Finally, several announcements in our sample were made concurrently with other corporate news. Prior research has shown that concurrent announcements do not bias, on average, the results of event studies (Sorescu, Warren, and Ertekin 2017) and should not be excluded from analysis. While in the main analysis we control for the potential confounding effects of these news by including indicator variables, we also present robustness checks that altogether exclude these concurrent announcements from the sample. Results are substantially similar to those from the main analysis, confirming the robustness of our findings.

Additional Analyses

Medium-Term Reaction to Announcements of Actions Pertaining to Russian Operations

The negative short-term reaction to Russian operation suspensions suggests investors initially focused on the loss in cash flows associated with a partial or a full suspension of operations. However, in widely opposed conflicts like Russia's war in Ukraine, this perspective may shift as the conflict persists beyond the short term. In such cases, public opposition to the conflict and favorable opinion toward firms that took a stance against it will likely become more salient to investors. As a result, firms that aligned their actions with stakeholder values may potentially gain support and improve performance through enhanced reputation (Neilson 2010).

To examine potential reaction reversals, we calculate buy-and-hold abnormal returns (BHARs) over one- and three-month windows after the announcement. These medium-term windows are appropriate as they allow sufficient time for stakeholder responses to materialize while avoiding confounding events that could impact longer horizons. Such reversals do not necessarily violate market efficiency, as investors may need some time to understand and incorporate into valuations the complex interplay between ethical stances and financial performance, particularly when stakeholder reactions evolve. In line with common practice, for the companies that made more than one announcement during our sample period, we consider only the last announcements to avoid confounding effects within the estimation window (e.g., Ertekin, Sorescu, and Houston 2018). We calculate BHARs as follows:

where i is the firm, t is the month, Rit is the rate of return of firm i in month t, and Rmt is the return of the S&P 500 market index in month t. The measurement starts on the day after the announcement.

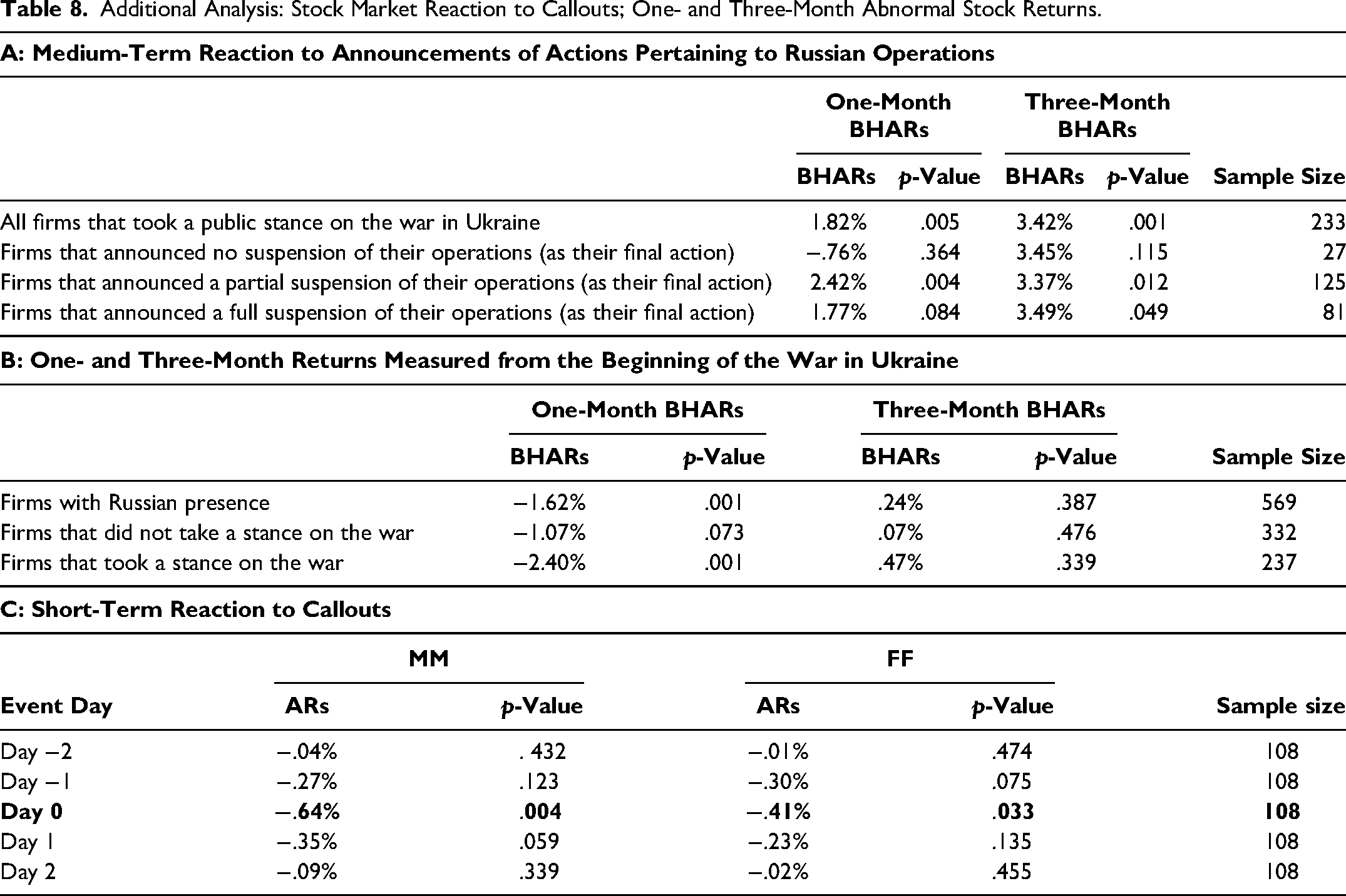

Results in Table 8, Panel A, show that firms taking war-related stances experienced positive average BHARs at one month (BHARs = 1.82%, p = .005) and three months (BHARs = 3.42%, p = .001) after the announcement. However, this effect is driven by firms announcing operational suspensions, with both partial suspensions (one-month BHARs = 2.42%, p = .004; three-month BHARs = 3.37%, p = .012) and full suspensions (one-month BHARs = 1.77%, p = .084; three-month BHARs = 3.49%, p = .049) showing positive returns. Firms announcing no suspension showed no significant BHARs (one-month BHARs = −.76%, p = .364; three-month BHARs = 3.45%, p = .115). This reversal of initial negative short-term reaction likely reflects investors recognizing reputational benefits for firms opposing the conflict, though such effects may not occur or may be less pronounced in conflicts lacking significant public opposition. 7

Additional Analysis: Stock Market Reaction to Callouts; One- and Three-Month Abnormal Stock Returns.

BHARs Measured One Month and Three Months After the Beginning of the War

To examine how the war affected firms that remained silent, we analyze one- and three-month BHARs from February 24, 2022, the start of the war, for all firms publicly traded in the United States and United Kingdom. Results in Table 8, Panel B, show that firms with Russian operations experienced negative BHARs in the first month (BHARs = −1.62%, p = .001). This result appears to be driven by firms that took a stance on the war. These firms experienced significant negative BHARs in the first month (BHARs = −2.40%, p = .001), while firms that did not make any announcements experienced only marginally significant BHARs lower in magnitude (BHARs = −1.07, p = .073). There is no significant effect observed over the three-month period, suggesting that investors fully incorporated war-related cash flow implications within one month. This further validates the window used to collect the announcements for our empirical analysis. We emphasize that this analysis illustrates investors’ expectations associated with the effects of the war and not firms’ responses to the crisis, which are examined with BHARs calculated from the day of each announcement and presented previously in the article.

Short-Term Stock Market Reaction to Callouts

As the war in Ukraine unfolded, many companies with commercial operations in Russia were publicly criticized for continuing their operations in the region and were called on to stop any business in Russia. These callouts were initiated by different entities such as activist groups, customers, companies’ own employees, and politicians. Many of these callouts made headlines and attracted a lot of attention from the press.

To understand how such external public criticism affects stock prices, we conducted a short-term event study on a sample of 108 callouts experienced by the firms with Russian operations within one month from the beginning of the war. The results are presented in Table 8, Panel C. We find that firms experience significant negative ARs on the day of the callout (MM: ARs = −.64%, p = .004; FF: ARs = −.41%, p = .033), suggesting that investors believe that public pressure can have negative consequences on the future cash flows of firms.

Discussion

Our research examines how investors react to firms’ operational decisions in markets affected by geopolitical conflicts, and how both firm-specific and situational factors shape these reactions. Using data from the Russia–Ukraine war, we uncover a complex pattern of market responses that varies based on several key contingencies. First, the short-term stock market reaction to both partial and full operational suspensions is negative, as investors likely focus on immediate revenue losses over potential strategic benefits. Second, this negative reaction is moderated by industry dynamics and public attention: Markets penalize suspensions less severely when competitors have already suspended operations or when public interest in the conflict is high. Third, firm characteristics matter: Companies with larger operational footprints and higher preconflict media attention (for partial suspensions) face less negative stock market reactions.

Contributions to Research

Contribution to the market exit literature

Our study advances marketing theory by extending the market exit literature into the underexplored context of geopolitical conflict. Prior research on market exit has largely examined exit decisions based on declining market attractiveness, competitive dynamics, or regulatory pressures (e.g., Dixit and Chintagunta 2007; Ozturk, Venkataraman, and Chintagunta 2016). We enrich this domain by showing that market exit under geopolitical conflict differs fundamentally: It is evaluated by investors not only on the basis of expected financial performance but also through the lens of stakeholder expectations and public legitimacy. By identifying four moderating factors—competitor actions, public interest, operational footprint, and media visibility—we explain why some firms experience less negative market reactions to exit decisions than others. Our expectation-based framework thus provides a novel, contingency-driven perspective on how investors interpret market exit signals under conditions of high external scrutiny.

Contribution to crisis management and stakeholder response research

We also contribute to the marketing literature on crisis management and stakeholder reactions to firm decisions (e.g., Brounen and Derwall 2010; Karolyi and Martell 2010). Prior work has primarily focused on investor responses to catastrophic events such as terrorist attacks, natural disasters, or pandemics. Our study addresses a different, managerially controllable decision: whether to suspend or continue operations amid political conflict. We demonstrate that investors penalize suspension decisions due to immediate revenue losses, but that this penalty is attenuated when suspensions are anticipated by the market. These findings offer new insights into how managers can manage stakeholder expectations and reduce market penalties through timing and signaling strategies.

Contribution to research on corporate sociopolitical activism

Finally, our work enriches the emerging literature on corporate sociopolitical activism (e.g., Bhagwat et al. 2020; Ganesan and Mallapragada 2025). While prior research has shown that consumers reward firms for taking stands on controversial social and political issues, we extend this conversation to the investor domain. We show that investor reactions to corporate activism in the form of market exit depend on contextual and firm-level contingencies that influence expectations. Our results suggest that firms can mitigate investor backlash by following peer signals, capitalizing on high public awareness, and leveraging strong media presence. This nuanced understanding contributes to ongoing debates about the risks and rewards of corporate activism in international markets.

Contributions to Practice

Our findings provide important insights for managers navigating geopolitical crises. First, our results show that while market suspensions typically trigger negative investor reactions due to anticipated revenue losses, this penalty is not uniform. Managers can strategically mitigate the adverse market response by aligning their timing and communication with industry signals. Specifically, following competitors’ suspension decisions reduces the perceived risk of acting alone and signals adherence to evolving industry norms (“safety in numbers”).

Second, we find that suspensions announced during periods of heightened public interest in the conflict are less harshly penalized by investors. This insight suggests that managers can improve outcomes by proactively monitoring public attention and selecting announcement windows when global scrutiny is high.

Third, our study shows that firms with a larger operational footprint and strong preconflict media visibility experience less severe market penalties when announcing suspensions. These findings suggest that long-term investments in building media relationships and maintaining transparent stakeholder communications can create resilience against market penalties in times of crisis.

Finally, our research helps managers balance the tension between taking stakeholder-pleasing actions (such as suspensions in response to geopolitical events) and safeguarding shareholder value. By offering a clear, empirically grounded framework to anticipate market responses, our study equips decision-makers with evidence-based strategies to minimize risk when making complex operational decisions under geopolitical uncertainty.

Future Research Directions

Our research suggests several promising avenues for future investigation. First, extending our findings across different types of geopolitical crises would be valuable, particularly those with different types of stakeholder expectations than the Russia–Ukraine war. Second, our results reflect the actions of firms headquartered in Western, English-speaking countries, which responded to public interest shaped by Western values. Extending our findings to firms based in countries with non-Western cultures, or examining how investors’ reactions may differ in collectivistic versus individualistic cultures, is a promising avenue for future research. Third, future research could further explore the optimal response timing, particularly in response to stakeholders’ increasing expectations for CSR (Dai, Liang, and Ng 2021; Theis 2020). Fourth, while we document market reaction reversals over three months, examining longer-term consequences for brand equity, customer loyalty, and employee engagement would be valuable. Finally, our theoretical framework could be extended to examine market reactions to other corporate decisions involving complex stakeholder considerations, such as responses to environmental crises or social movements.

Supplemental Material

sj-pdf-1-jmx-10.1177_00222429251355956 - Supplemental material for Investor Reactions to Firms’ Announcements of Operational Decisions in Markets Involved in Geopolitical Conflicts

Supplemental material, sj-pdf-1-jmx-10.1177_00222429251355956 for Investor Reactions to Firms’ Announcements of Operational Decisions in Markets Involved in Geopolitical Conflicts by Larisa Kovalenko, Priya Rangaswamy and Alina Sorescu in Journal of Marketing

Footnotes

Coeditor

Detelina Marinova

Associate Editor

Rajdeep Grewal

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.