Abstract

“Buy now, pay later” (BNPL) installment payments allow customers to pay for purchases in a series of interest-free installments over a short period of time. This research provides novel insights into how customer adoption of BNPL installment payments impacts spending. The authors leverage customer-level transaction data before and after the introduction of a BNPL installment payment service at a large U.S. retailer. A difference-in-differences analysis indicates that the adoption of BNPL installment payments is associated with (1) an increase in purchase incidence and (2) larger purchase amounts. These effects are statistically and economically significant over time. Moreover, this increase in spending is greater for smaller- (vs. larger-) basket shoppers and for shoppers who relied more heavily on credit (vs. debit) cards before adoption. Three preregistered experiments show that BNPL installment (vs. lump sum) payments increase spending by reducing perceived financial constraints. Specifically, BNPL installments alleviate perceived financial constraints by reducing perceived costs and facilitating budget control. These findings highlight the substantive role of BNPL installment payments in shaping purchase behavior and provide important implications for the management of BNPL payment schemes.

Keywords

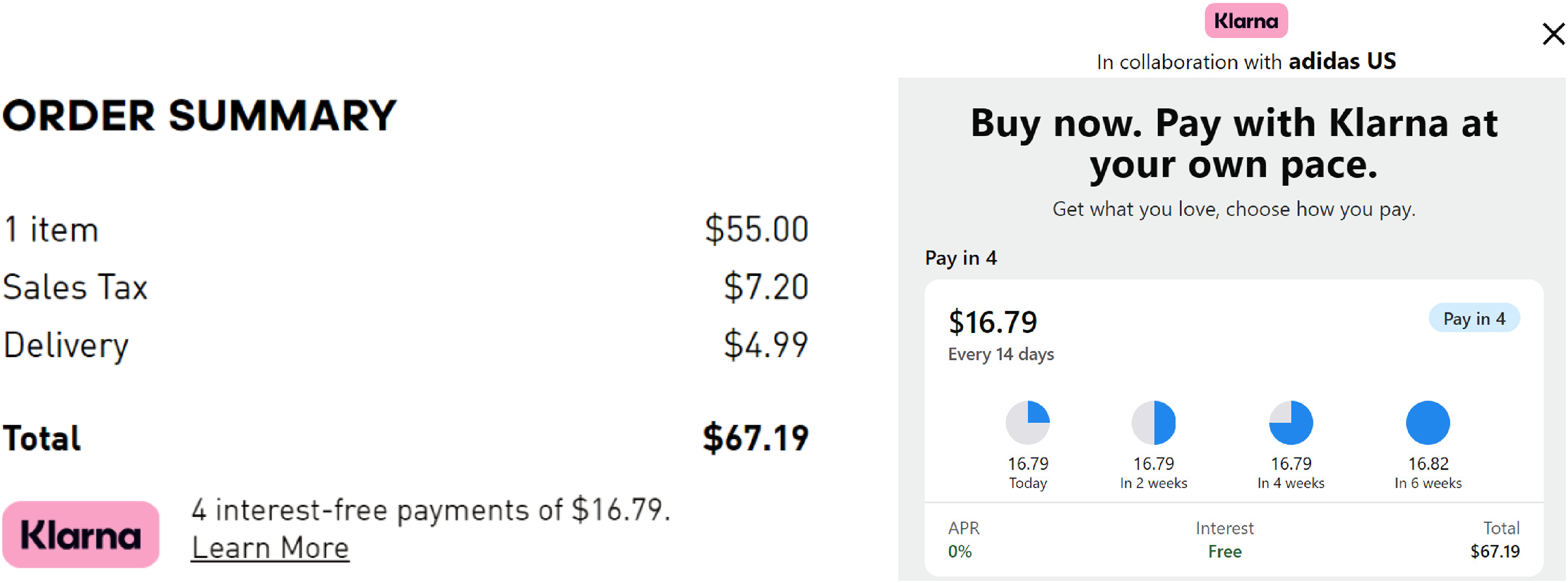

Buy now, pay later (BNPL) has become an increasingly popular payment method at retailers, allowing customers to pay for purchases in interest-free installments over a relatively short period of time, typically within six weeks (Accenture 2021). Over 45 million U.S. customers and over 15 million U.K. customers have adopted this form of payment in recent years (Accenture 2021; Sheikh 2021). Globally, the number of BNPL users reached 380 million in 2024 and is projected to reach 670 million by 2028 (Juniper Research 2024). Worldwide BNPL spending equaled $316 billion in 2023 and is expected to grow to $450 billion by 2027 (Worldpay 2024). Most BNPL installment spending is realized via providers like Afterpay, Klarna, and Affirm (Dikshit et al. 2021). In recent years, a growing number of major retailers (e.g., ASOS, Adidas, H&M, Walmart, Sephora) have partnered with BNPL providers to allow customers to pay for purchases in installments. As illustrated in Figure 1, this enables customers to pay for purchases in installments, such as in four interest-free installments over six weeks (“Pay in four”). 1

Example of BNPL Installments.

Despite the growing popularity of BNPL installment payments, little is known about their impact on retail sales. Furthermore, retailers are uncertain about its long-term effects (Schultz 2022). 2 Prior literature has not studied the effects of BNPL installments, focusing instead on how framing prices in segregated terms affects transaction evaluations (Atlas and Bartels 2018; Bambauer-Sachse and Mangold 2009; Gourville 1998, 1999, 2003). These existing studies on temporal reframing have examined the effects of prices framed in segregated (“$2 a day”) or aggregated (“$60 a month”) terms, with payments remaining aggregate (all customers “pay monthly”). In contrast, BNPL installments go beyond segregated frames and require customers to make actual segregated payments across a specified time (“Pay $60 in four payments of $15 over six weeks”). Thus, BNPL installments involve separate segregated payments (“four payments of $15”) rather than a single lump sum payment (“one payment of $60”).

Our research aims to provide retailers with an understanding of how BNPL installment payments influence retail sales. We propose that segregating payments alleviates perceived financial constraints, thereby increasing spending. We first analyze transactional data from a major retailer in the United States that introduced BNPL installment payments by partnering with a leading BNPL provider for the first time (Study 1). Our difference-in-differences (DID) analysis reveals that adoption of BNPL installment payment plans is associated with an increase in purchase incidence of approximately 9 percentage points and with a relative increase in purchase amounts of approximately 10%. These effects remain statistically and economically significant across the entire postadoption period. An analysis of customer heterogeneity reveals that the effect is stronger among credit (vs. debit) card shoppers and among smaller- (vs. larger-) basket shoppers. Next, three preregistered experiments provide causal evidence for the positive effect of BNPL installment payments on spending and explain why the effect occurs. Consistent with the transactional data, BNPL installment payments increase spending by reducing perceived financial constraints (Studies 2 and 3). Specifically, BNPL installment payments alleviate perceived financial constraints by reducing perceived costs and facilitating budget control (Study 4).

Our article offers several contributions. Substantively, we provide novel empirical insights on the effects of BNPL installment payments on retail sales. Using transactional data, we show that adopting BNPL installment payments positively impacts customers’ purchase incidence and amounts. In addition, we find that these effects remain statistically and economically significant over time. Furthermore, we offer key insights into the heterogeneous impact of BNPL installments across customers. Consistent with our theorizing, our findings imply that the effect of BNPL installments on spending is larger among customers who are likely to be more financially constrained (i.e., among customers who purchased smaller baskets and relied more heavily on credit cards before adoption; Bell and Lattin 1998; Borzekowski, Kiser, and Shaista 2008).

Theoretically, we contribute to the temporal reframing literature (e.g., Gourville 1998, 1999, 2003). Prior work has focused on prices framed in segregated (“$1 a day”) or aggregated (“$30 a month”) terms, while payments remain aggregated (“monthly payment”; Gourville 1998). BNPL installments go beyond segregated price frames and segregate actual payment. We show that segregating payment works beyond existing temporal reframing mechanisms via perceived financial constraints. This happens, at least in part, because segregating payments makes customers feel more in control of their budget. By alleviating perceived financial constraints, segregating payment into BNPL installments is effective when the aggregate cost is salient. Furthermore, the effect occurs even when an aggregate payment is more delayed than the installment payments. It also applies to goods and services consumed on a recurring and one-off basis. Finally, we also contribute to work on perceived financial constraints. While existing research has examined its consequences on consumer behavior (e.g., Dias, Sharma, and Fitzsimons 2022; Paley, Tully, and Sharma 2019; Tully, Hershfield, and Meyvis 2015), we illustrate an antecedent by showing that BNPL installment (vs. delayed lump sum) payments reduce perceived financial constraints.

Theoretical Background

Buy Now, Pay Later

BNPL installments have become a common payment method in recent years (Worldpay 2021). Major players such as Afterpay, Klarna, and Affirm partner with retailers to enable customers to spread the cost of their shopping in interest-free installments (Sheikh 2021). When customers choose BNPL installments at the checkout of a participating retailer, the bill will be paid in full by the BNPL provider to the retailer. Customers pay the BNPL provider for the first installment at the time of purchase and repay the remaining interest-free installments over a short time period.

Prior research has shown that payment methods can affect spending. Customers tend to spend more on credit cards than cash (e.g., Hirschman 1979; Raghubir and Srivastava 2008). The higher spending with credit cards (vs. cash) has been attributed to temporal decoupling, where the purchase is separated from actual payment (Prelec and Loewenstein 1998). By also delaying payment, BNPL installments share payment decoupling characteristics with credit cards. However, in an online retail context, customers predominantly rely on credit cards that already delay payment (PYMNTS 2024). BNPL installment payments are distinct from credit cards in that payments are segregated into smaller installments at the point of sale. We argue that segregating payment into installments can impact spending. Specifically, building on the temporal reframing literature, we postulate that BNPL installment payments affect perceived financial constraints, increasing spending.

Temporal Reframing

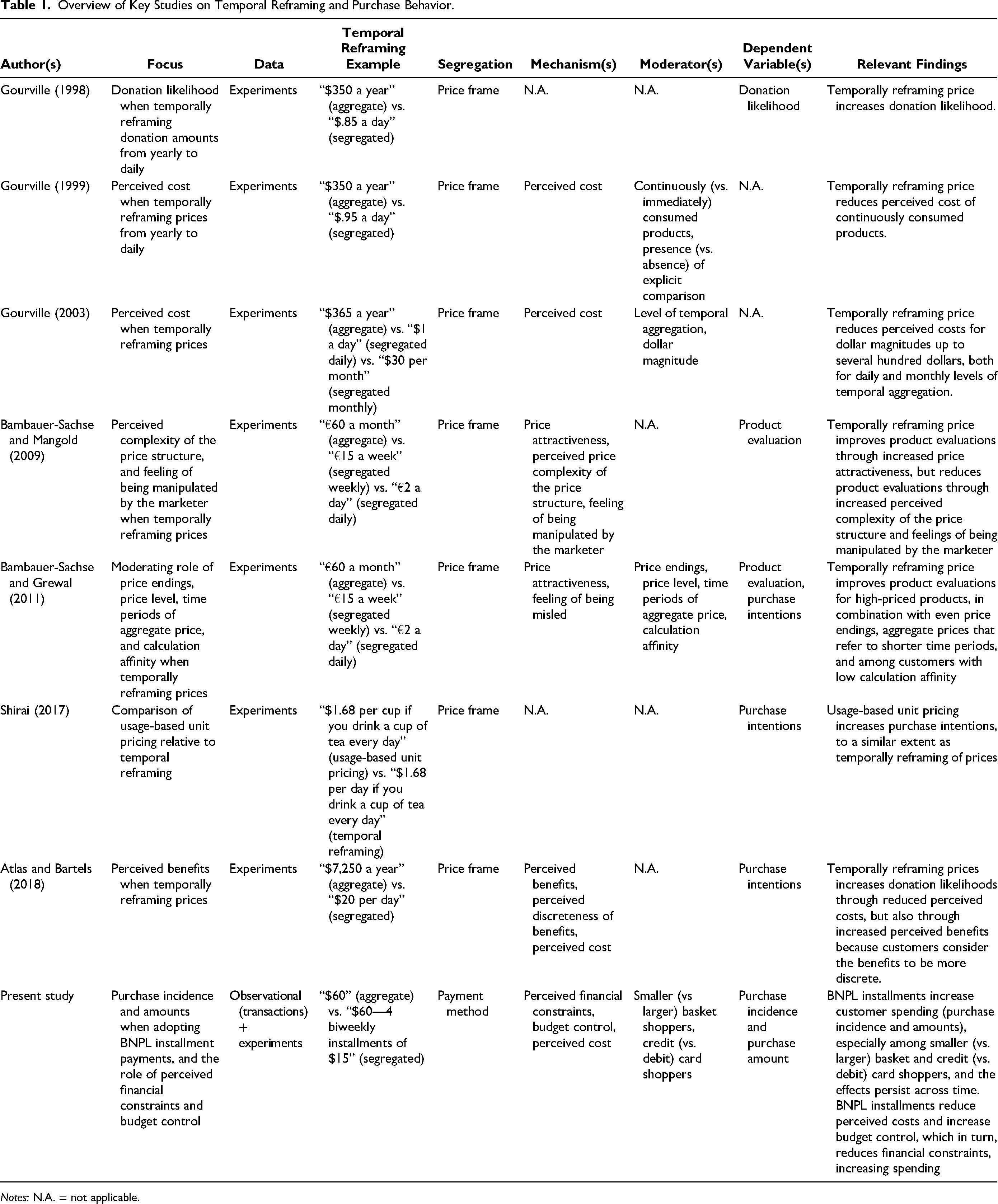

Temporal reframing refers to the presentation of prices over varying time periods (Gourville 1998, 1999, 2003). For instance, prices can be framed in aggregate terms (“$60 a month”) or segregated terms (“$15 a week”). Objectively, framing equivalent prices in segregated terms (“$15 a week”) or aggregate terms (“$60 a month”) should not affect purchase intentions, as the underlying cost remains the same (Kahneman and Tversky 1979). Nonetheless, the temporal reframing literature demonstrates that segregating versus aggregating prices has consequential effects on perceptions and purchase intentions (Table 1). Gourville (1998) first showed that donation likelihood was higher when prices were framed in segregated (“$1 a day”) than in aggregated terms (“$365 a year”). This effect has been generalized to different temporal frames (e.g., weekly instead of daily) and various recurring consumption contexts (e.g., a car lease, gym membership; Atlas and Bartels 2018; Bambauer-Sachse and Grewal 2011; Bambauer-Sachse and Mangold 2009; Shirai 2017).

Overview of Key Studies on Temporal Reframing and Purchase Behavior.

Notes: N.A. = not applicable.

The temporal reframing literature has identified several mechanisms explaining the effects of segregated prices on purchase intentions. Prior research has revealed how segregating prices affects perceptions of recurring costs and benefits. According to the “pennies-a-day” framework, segregating prices (“$1 a day”) reminds customers of other small and trivial expenses (Gourville 1998). Thus, segregated prices are perceived as more palatable and attractive than aggregated prices (Bambauer-Sachse and Grewal 2011; Bambauer-Sachse and Mangold 2009; Gourville 2003). Gourville (1999) further theorizes that temporal reframing is particularly effective for products consumed on a recurring basis (e.g., subscriptions) due to the overlap between segregated prices and prototypical petty cash expenses. Segregating prices can also help customers appreciate the recurring benefits of a purchase, thereby increasing perceived benefits and purchase intentions (Atlas and Bartels 2018).

Previous work has also identified mechanisms that attenuate the effects of temporal reframing. Bambauer-Sachse and Mangold (2009) revealed that customers found segregated (vs. aggregated) prices complex and became skeptical of the marketer's motives. Correspondingly, segregated (vs. aggregated) prices can elicit greater feelings of being misled, reducing product evaluations (Bambauer and Grewal 2011).

Our work differs from previous studies on temporal reframing in several ways. First, prior work frames prices in either segregated (“$15 a week”) or aggregated terms (“$60 a month”) with actual payments kept constant. 3 BNPL installments go beyond segregated price frames and require customers to make actual segregated payments across the specified time periods (“Pay $60 in 4 biweekly installments of $15”). Second, prior work examines the effects of temporal framing on purchase intentions using experiments. Our research leverages transactional retailer data to study how segregating payments into BNPL installments impacts customers’ actual spending over time. This further enables us to answer managerially relevant questions on which shoppers will likely change their spending (i.e., depending on historical basket size and credit card use). Third, we show that segregating payment works beyond the existing temporal reframing mechanisms via perceived financial constraints. Specifically, we theorize that segregating payments makes customers feel more in control of their budget, alleviating perceived financial constraints. By working through additional mechanisms, our effects not only apply to recurring consumption (e.g., car leases) but also generalize to purchases consumed on a one-off basis (e.g., a flight).

The Effect of BNPL Installment Payments on Perceived Financial Constraints and Spending

We predict that segregating payment into BNPL installments decreases perceived financial constraints, increasing spending. Perceived financial constraints reflect “the extent to which people believe that their financial situation restricts desired consumption” (Tully, Hershfield, and Meyvis 2015, p. 60). While customers can feel financially constrained if their income is insufficient to satisfy their consumption desires, perceived financial constraints reflect a “psychological state that does not necessarily imply poverty or a literal absence of money” (Paley, Tully, and Sharma 2019, p. 890). Even among customers of similar objective wealth, perceptions of financial constraints can differ (e.g., Paley, Tully, and Sharma 2019; Sussman and Shafir 2012). Put differently, perceived financial constraints can occur among lower- and higher-income customers. 4

We theorize that segregating payment into BNPL installments reduces perceived financial constraints for two reasons: (1) decreasing perceived costs and (2) increasing budget control. First, perceived costs reflect the extent to which people evaluate costs as small and trivial (Atlas and Bartels 2018; Gourville 1998). According to the “pennies-a-day” framework, segregating prices decreases perceived costs by reminding customers of other small and trivial expenses, such as a cup of coffee (Gourville 1998). Thus, prices framed in daily terms (“$1 a day”) are perceived as less costly than monthly terms (“$30 a month”), which, in turn, are perceived as less costly than yearly terms (“$365 a year”; Gourville 2003). Similarly, Atlas and Bartels (2018) found that perceived costs were lower when prices were framed in segregated terms (“25ȼ a day”) compared with aggregated terms (“$90 a year”). While prior work frames prices in either segregated (“$15 a week”) or aggregate terms (“$60 a month”), our payment context jointly presents the aggregate and segregated terms (e.g., “$60 in four installments of $15”). Thus, customers are typically aware of the total cost.

We argue that segregating payment can still reduce perceived costs in the presence of the aggregate term. According to the numerosity heuristic, people tend to infer a greater quantity from higher numerosity at the expense of relevant contextual information (Pelham, Sumarta, and Myaskovsky 1994). Numerosity refers to the number of units that a stimulus is quantified by (Pelham, Sumarta, and Myaskovsky 1994). For example, weight can be measured in kilos (e.g., 1 kg; lower numerosity) or grams (e.g., 1,000 g; higher numerosity). The numerosity heuristic occurs when people focus on the number and consider 1,000 g heavier than 1 kg. This heuristic also extends to costs, where people often focus on the sheer numerousness of cost information (Bagchi and Davis 2016).

In the context of BNPL installments, customers might focus on the segregated terms (“four installments of $15”) and judge these as smaller than the aggregate term (“total cost of $60”). Furthermore, the numerosity heuristic is not due to the inability to understand and process numbers (Weller et al. 2013). Highly numerate people have been found to be more prone to this heuristic, as they focus more on numeric information (Cadario, Parguel, and Benoit-Moreau 2016). Moreover, the effects generalize to highly educated and experienced customers. For instance, master of business administration students evaluated the cost of a magazine subscription more favorably when its price was segregated (“$1 per day”) than aggregated (“$365 per year”; Atlas and Bartels 2018). Hence, we postulate that customers would evaluate payment more favorably when it is segregated into BNPL installments despite being cognizant of the aggregate term.

Prior work on partitioned pricing has shown that this segregation effect persists even when the total cost is clear (Carlson and Weathers 2008). Despite being aware of the total cost, customers had higher purchase intentions when costs were presented in segregated terms (“base price + shipping costs”) than in aggregated terms (“total costs”; Xia and Monroe 2004). Thus, BNPL customers may focus on the segregated payment (“four installments of $2.50”) at the expense of the aggregate payment (“$10”) and perceive the amount to be less costly, even when they are aware of the total cost (“$10”). These findings suggest that segregating payments into BNPL installments lowers perceived costs.

By lowering perceived costs, BNPL installment payments should impact perceived financial constraints. Financially constrained customers perceive that their consumption desires exceed their financial means (Paley, Tully, and Sharma 2019). Put differently, perceived financial constraints are a subjective assessment of wealth where customers evaluate the adequacy of their financial resources relative to one or more reference points (Tully, Hershfield, and Meyvis 2015). For instance, reminding participants of reference points such as mortgages, bills, and limited savings made people feel more financially constrained (Tully, Hershfield, and Meyvis 2015). Segregating payment into BNPL installments (“four installments of $2.50”) could lower the reference point, where one evaluates their financial means against the installment payment (“$2.50”) rather than the total cost (“$10”). By making the payment for desired consumption seem less costly, BNPL installments increase the likelihood that customers feel that their financial means are sufficient to fulfill their consumption desires, alleviating perceived financial constraints.

Second, we argue that BNPL installment payments increase budget control, reducing perceived financial constraints. Budget control refers to perceptions of control over allocating financial resources and tracking expenses against a budget (Kidwell and Turrisi 2004). By earmarking money for expenses, budgeting enables customers to assess if their income is sufficient to satisfy their consumption desire (Heath and Soll 1996). Prior work suggests that temporal frames affect how people budget (Spiller 2011; Ülkümen, Thomas, and Morwitz 2008). Specifically, individuals found it easier to estimate budgets for shorter time frames (“next month”) than for longer time frames (“next year”; Ülkümen, Thomas, and Morwitz 2008). Unlike traditional credit card payments (“a single lump sum due at the end of the month”), installment payments are segregated into shorter time frames (“four weekly payments”). Hence, we propose that BNPL installments make it easier for customers to estimate their budgets, increasing budget control. Consequently, BNPL installment payments should impact perceived financial constraints. For instance, prior work found that individuals with higher budget control felt less financially constrained than their counterparts with lower budget control, even when they shared the same income (Gasiorowska 2014).

In sum, by reducing perceived costs and facilitating budget control, we posit that segregating payment into BNPL installments alleviates perceived financial constraints. Subsequently, BNPL installments should increase spending, as previous research has shown that lower perceived financial constraints increase purchases (Karlsson et al. 2004, 2005; Tully, Hershfield, and Meyvis 2015). For instance, households that felt less financially constrained reported more purchases (Karlsson et al. 2005). Next, we present evidence from the field in which we explore how adopting BNPL installment payments impacts spending, followed by experimental evidence providing stronger causal evidence and studying the proposed mechanism.

Overview of Empirical Studies

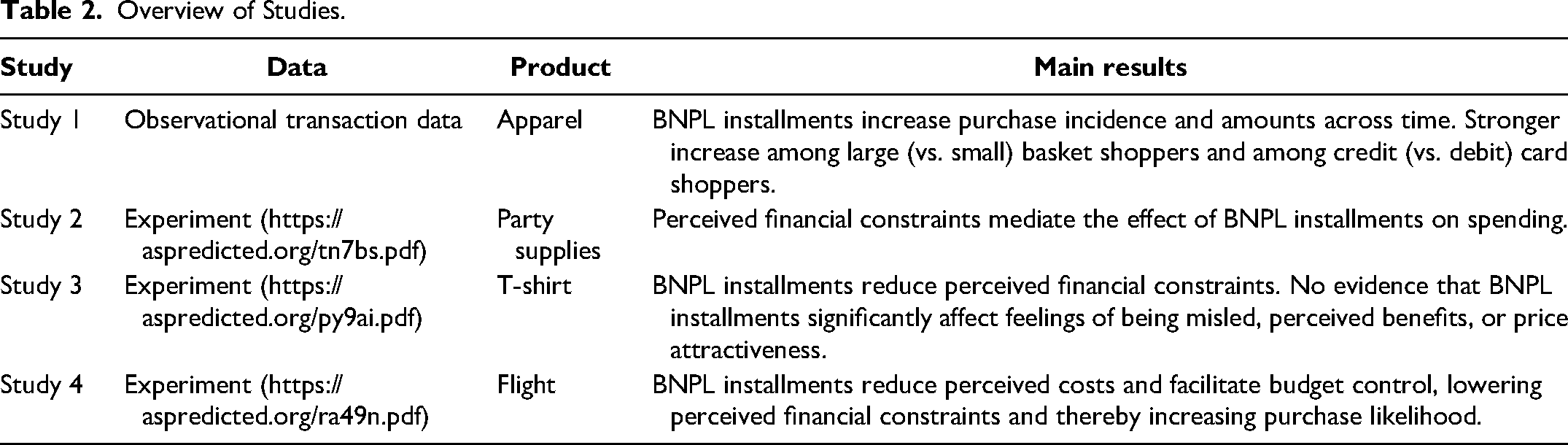

We investigate the BNPL installment effect in four studies, as summarized in Table 2. Study 1 uses a DID analysis to analyze observational data for a large sample of customers at a major U.S. retailer. We also conduct a vast range of robustness checks for Study 1 (Web Appendix B) and explore customer heterogeneity in the effect. Study 2 is a randomized online experiment to validate Study 1, and it tests the mediating role of perceived financial constraints. Study 3 examines the effect of BNPL installments on perceived financial constraints and tests the role of alternative mechanisms. Study 4 examines the full model, whereby BNPL installments reduce perceived costs and facilitate budget control, reducing perceived financial constraints and, in turn, increasing purchase likelihood. 5 All stimuli, data, syntax, preregistrations for Studies 2 to 4, and supplementary studies are available on Journal of Marketing's Dataverse (https://doi.org/10.7910/DVN/JR278J).

Overview of Studies.

Study 1: The Impact of BNPL Installment Payments on Customer Spending in the Field

To examine how the adoption of BNPL installment payments impacts purchases, we leverage data on the introduction of BNPL installment payments by a reputable U.S. retailer that prefers to remain anonymous. We exploit the fact that after the retailer made BNPL installment payments available to its customers, only a selection of customers adopted the service. Our identification of the BNPL installment payment effect relies on the change in purchases by adopters of BNPL installment payments after the retailer's introduction of BNPL installment payments, relative to a control group of nonadopters in the same period. The objective of our analysis is to explore how purchase behavior differs between adopters and nonadopters in the period after the introduction of BNPL installment payments. To mitigate possible bias due to self-selection of adoption, we use matching on observable factors to increase the comparability of adopters and nonadopters. We estimate a DID model on the matched sample to identify the effect of customers’ adoption of BNPL installment payments on their spending.

Empirical Context and Data

We obtained transaction data from a retailer that introduced BNPL installment payments for the first time during our sample period. Our dataset covers total weekly spending from a major apparel retailer at the customer level within the United States between April 2020 and April 2021. In October 2020, the retailer partnered with a leading BNPL installment payment service provider for the first time, which enabled customers to buy and pay later in a series of installments. 6 The availability of the new BNPL installment payment method was communicated on the retailer's webpage. Specifically, it indicated that customers could “pay in 4 installments” using the BNPL installment payment service provider immediately below the “add to bag” button on the retailer's website. In line with common practice in retail, the product's full price remained visible above the “add to bag” button. The ability to pay in four installments was visible to all customers on the website. No targeting was involved around BNPL, and the retailer did not make any strategic price adjustments in response to the introduction of BNPL. The introduction of the BNPL installment payment method allowed customers to purchase products immediately and pay with four equal repayments for the first time at the focal retailer. The retailer receives the payment in full from the BNPL provider shortly after the transaction, while the customer repays the BNPL provider over four installments. The first installment must be paid at the time of purchase, and the three remaining installments are due two, four, and six weeks after the purchase, respectively. The installments the customer pays go to the BNPL provider and are interest-free. In exchange for the service, the retailer pays the BNPL installment payment provider an undisclosed flat transaction fee and a variable fee.

Our dataset spans 52 weeks of data, 22 weeks before and 30 weeks after the retailer's introduction of BNPL installment payments. To examine the change in customers’ purchase behavior after adopting BNPL installment payments at the focal retailer, we focus on existing customers who made at least one purchase from the retailer's online store prior to the retailer's introduction of BNPL installment payments. In line with common practice, our main analysis focuses on a cohort of customers who adopt around the same time (Iyengar, Park, and Yu 2022). Specifically, from the retailer's pool of existing residential customers, we obtain a random sample of 25,000 customers who adopt within four weeks after the retailer's introduction of BNPL installment payments. In the robustness checks, we report similar effects across later cohorts of adopters. As a control group of nonadopters, we obtained a random sample of 200,000 existing residential customers who did not adopt during the entire study period and made at least one purchase before the retailer's introduction of BNPL installment payments.

Matching

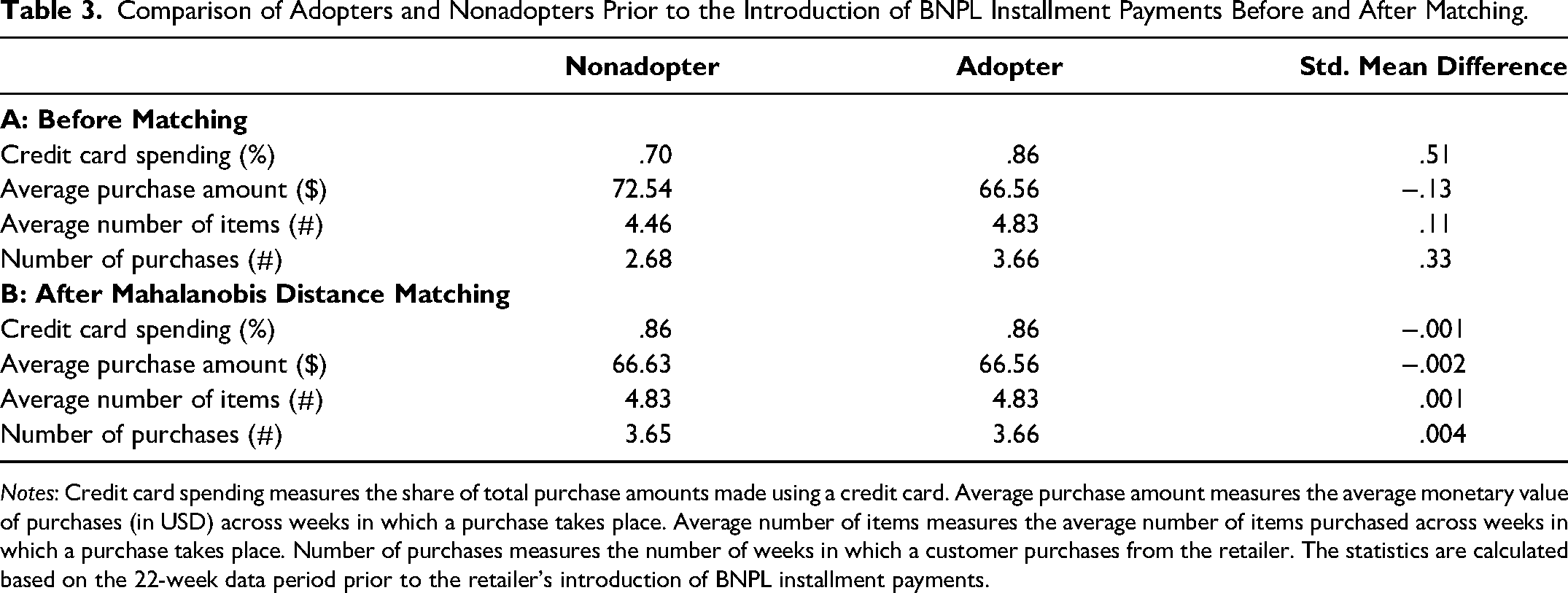

A potential concern is that our data lacks randomization on who adopts. If adopters differ systematically from nonadopters, this may lead to biased estimates in our DID analysis. To improve the comparability of adopters and nonadopters, we match each customer who adopts BNPL to a similar customer who does not adopt based on observed characteristics. To assess whether nonadopters were similar to adopters before the introduction of BNPL installment payments, we compare both groups during the 22-week period prior to the retailer's introduction of BNPL installment payments.

BNPL may be more appealing to customers facing financial constraints. For example, higher-income groups are less likely to adopt BNPL (Shupe, Li, and Fulford 2023). Although customers’ financial constraints are not directly observable, certain behavioral characteristics could serve as proxy variables. Previous studies indicate that individuals with lower incomes tend to purchase in smaller amounts and are more likely to use credit cards rather than debit cards (Bell and Lattin 1998; Borzekowski, Kiser, and Shaista 2008; Noble et al. 2017). Additionally, customers who shop more frequently at the focal retailer may have greater exposure to its introduction of BNPL, potentially increasing their likelihood of adoption. Therefore, we consider the following four observable measures: (1) credit card spending, (2) average purchase amount, (3) average number of items, and (4) number of purchases. Credit card spending measures the percentage of total purchase amounts made using a credit card. Average purchase amount measures the average weekly monetary value of purchases (in USD) across weeks in which a purchase takes place. Average number of items measures the average number of items purchased across weeks in which a purchase takes place. Number of purchases measures the number of weeks in which a customer purchased from the retailer. All four characteristics are calculated over the 22 weeks before the retailer's introduction of BNPL installment payments. Based on these characteristics, we calculate the Mahalanobis distances among customers and select the match with the smallest distance (Datta, Knox, and Bronnenberg 2018). 7 This results in a sample of 25,000 adopting customers and 25,000 nonadopting customers. In the robustness checks, we report similar effects when using the entire sample of nonadopting customers (N = 200,000) without matching.

To assess whether nonadopters were similar to adopters on these observable characteristics before the introduction of BNPL installment payments, we compare both groups on their purchase behavior during the 22-week period prior to the retailer's introduction of BNPL installment payments. Table 3 summarizes the averages before matching (Panel A) and after matching (Panel B) for the observed covariates used in the matching procedure. Most notably, adopters rely more heavily on credit cards to pay for purchases (Madopter = 86%, Mnonadopter = 70%) and show a higher number of purchases (Madopter = 3.66, Mnonadopter = 2.68). We also observe lower average purchase amounts (Madopter = $66.56, Mnonadopter = $72.54) among adopters but not a lower number of items (Madopter = 4.83, Mnonadopter = 4.46). Overall, these descriptive statistics are consistent with the intuition that adopters may be relatively more financially constrained than nonadopters and are, therefore, more likely to purchase for smaller amounts using credit cards. After matching, the groups of adopters and nonadopters are comparable in all characteristics (Table 3, Panel B).

Comparison of Adopters and Nonadopters Prior to the Introduction of BNPL Installment Payments Before and After Matching.

Notes: Credit card spending measures the share of total purchase amounts made using a credit card. Average purchase amount measures the average monetary value of purchases (in USD) across weeks in which a purchase takes place. Average number of items measures the average number of items purchased across weeks in which a purchase takes place. Number of purchases measures the number of weeks in which a customer purchases from the retailer. The statistics are calculated based on the 22-week data period prior to the retailer's introduction of BNPL installment payments.

Difference-in-Differences Analysis

We employ a DID specification to examine the impact of BNPL installment payment adoption on customer purchases:

Our main analysis distinguishes between two outcome measures of customer purchases of key interest to retailers: whether a purchase is made in a given time period (purchase incidence) and how much is spent conditional on purchase incidence in a given time period (purchase amount in USD). In line with prior work, we distinguish between these two measures because adoption may impact both metrics differently and because they have differing implications for retailers (Iyengar, Park, and Yu 2022). Similar to prior literature, we estimate a two-part model (Ailawadi and Harlam 2009; Chesnes, Dai, and Jin 2017). The purchase incidence part captures the customer's decision to purchase from the retailer and is estimated as a logit model. The purchase amount part captures the customer's decision on how much to spend and is estimated as a log-linear model using observations in which the customer purchases from the retailer. 12

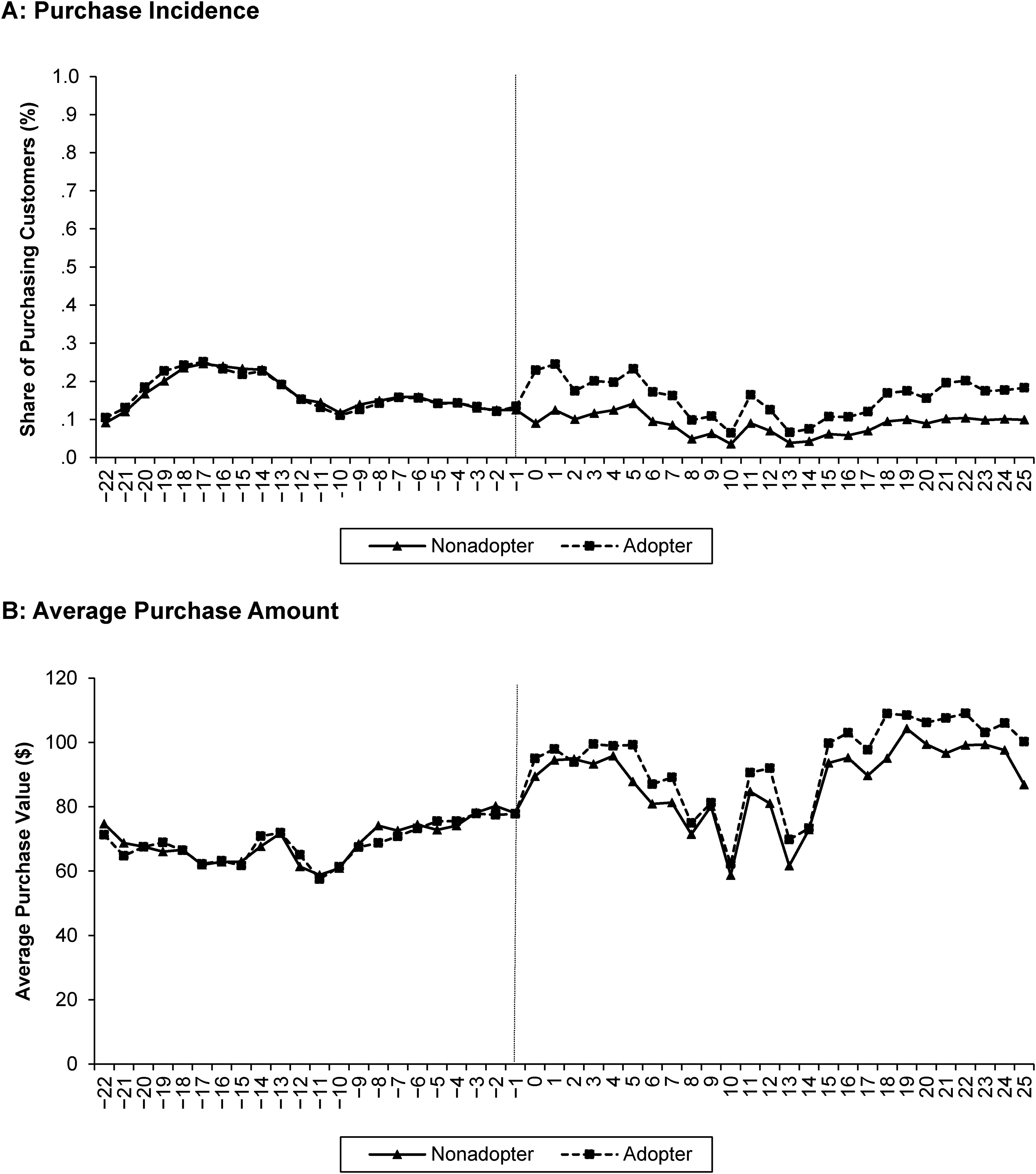

The identification assumption underlying DID is that in the absence of adoption, there would have been no differential changes in purchase behavior between the treatment and control group (Angrist and Pischke 2008). Because postintroduction counterfactual trends are unobservable, we assess the presence of parallel trends in the preintroduction period between adopters and nonadopters. In Figure 2, we provide visual verification that the trends in purchase behavior follow similar patterns between adopters and nonadopters prior to the introduction of BNPL installment payments. Specifically, we plot the percentage of adopting versus nonadopting customers making a purchase in each week to understand whether purchase incidences are on average similar between adopters and nonadopters (Figure 2, Panel A), and their average weekly purchase amount conditional on purchase incidence (Figure 2, Panel B). The results in Figure 2 indicate that behaviors were similar in the preperiod across adopters and nonadopters.

Comparison of Purchase Incidence and Average Purchase Amounts Between Adopters and Nonadopters.

Model-Free Evidence

To gain an initial understanding of the effect of the adoption of BNPL installment payments on purchase incidence and purchase amounts, we calculate purchase incidences and average purchase amounts before versus after the retailer's introduction of BNPL installment payments among adopters and nonadopters. Table 4 summarizes the results of this before-and-after calculation. It reveals that adopters, on average, make about two purchases (M = 1.83) more than nonadopters across the period after adoption. It also reveals a differential increase in purchase amounts of $6.88 among adopters compared with nonadopters, which is an average increase of approximately 10% compared with the average purchase amounts of an adopter prior to adoption (i.e., $6.88/$66.56). Next, we discuss the estimation results from our DID model that controls for potential customer- or time-varying confounders.

Before-and-After Analysis of Adopters and Nonadopters.

Notes: “Before” refers to the 22-week period prior to retailer's introduction of BNPL installment payments, and “After” refers to the 26-week period after the retailer's introduction of BNPL installment payments.

Main Estimation Results on the Impact of the Adoption of BNPL Installment Payments on Customer Purchases

Table 5 contains the estimates on the impact of adopting BNPL installment payments on customer purchases, obtained from the DID model specified in Equation 1. In line with the model-free insights, the effect on purchase incidence (PI) is significantly positive (β1,PI = .778, p < .01). This effect reflects the impact of adoption on purchase incidence after the first purchase. Thus, adopters are more likely than nonadopters to purchase from the retailer in the period after adopting the BNPL installment payment option. The effect of adoption on purchase amount (PA) is also significantly positive (β1,PA = .100, p < .01). In line with our model-free evidence, these results indicate that customers who adopted BNPL installment payments are more likely to make a purchase from the retailer and purchase for a larger amount after adoption compared with customers who did not adopt.

Main Impact of BNPL Installment Payment Adoption on Purchase Incidence and Purchase Amount.

***p < .01.

Notes: Standard errors clustered at the customer level appear in parentheses. The adjusted R2 for the purchase amount model equals .19.

Effect Sizes

To understand the economic significance of our estimation results, we calculate the effect size based on the estimates. For the purchase incidence model, we calculate the average marginal effect. This indicates that the probability of purchase, on average, increases by 8.96 percentage points (i.e., the average purchase probability of 16.64% before adoption increases to an average of 25.60% after adoption). For the purchase amount model, because of the log-linear link between purchases amount (which is natural log-transformed) and the dummy capturing the adoption effect (which enters the model linearly), the effect size translates to an average increase of approximately 10.52% (i.e., exp(.100) − 1) in dollar value (i.e., the average purchase amount of $66.56 before adoption increases to an average of $73.56 after adoption).

Robustness Checks

We conduct a series of robustness checks to verify the robustness of our main effects (Goldfarb, Tucker, and Wang 2022). We summarize and motivate these robustness checks in Web Appendix B and report detailed results. Overall, we find that our results hold up across a vast range of possible models, with evidence of robustness against (1) using alternative nonadopting (control customers), (2) using alternative adopting (treatment) customers, (3) using an alternative dependent variable (number of items purchased), and (4) possible selection on unobservables. 13 In addition, we show that the effect persists over time and is not driven by short-term adjustments in spending. In Web Appendix C, we further illustrate that the effect was not significantly influenced by the number of COVID cases during our sample period.

Heterogeneity in the Effect of BNPL Installment Payments on Purchase Incidence and Amount

Our main analysis suggests a positive and significant effect of BNPL adoption on purchase incidence and amount. Now, we extend our analysis by exploring heterogeneity in the effect. Heterogeneous effects can be used to shed light on behavioral mechanisms (Goldfarb, Tucker, and Wang 2022). Specifically, a moderation analysis can provide initial insights into the proposed mechanism by “identifying which groups would be affected by a certain mechanism that would display the causal effect of interest” (Goldfarb, Tucker, and Wang 2022, p. 15). Furthermore, a moderation analysis can provide managerially relevant insights into which customer groups may be more responsive to BNPL installment payments.

By segregating costs, we proposed that BNPL installment payments reduce perceived financial constraints, increasing spending. Because well-off customers are less sensitive to financial constraints, we would expect that financially constrained customers will perceive more benefits from BNPL installment payments. Hence, the effect of BNPL installment payments may be stronger among financially constrained customer groups. As customers’ financial constraints are unobserved, we draw on prior literature to identify two possible observable proxy variables. First, previous research suggests that reliance on credit (vs. debit) can serve as a proxy variable for customers’ financial constraints. Specifically, more financially constrained households are more likely to use credit (vs. debit) cards than less financially constrained households (Borzekowski, Kiser, and Shaista 2008). Second, prior research suggests that a customer's typical basket size can also serve as a proxy for financial constraints. For instance, Bell and Lattin (1998) examine differences between small- and large-basket shoppers and find that small-basket shoppers are significantly more financially constrained. Similarly, average basket sizes tend to be smaller for more financially constrained customers (Noble et al. 2017). Thus, financial constraints can possibly be proxied by credit card spending and basket size (Bell and Lattin 1998; Borzekowski, Kiser, and Shaista 2008; Noble et al. 2017). Empirically, we examine whether the adoption of BNPL installment payments has a differential impact on purchase incidence and purchase amount depending on two customer characteristics: (1) heavier (vs. lighter) credit card shoppers and (2) smaller- (vs. larger-) basket size shoppers. We construct the first measure based on a customer's historical reliance on credit (i.e., their share of historical spending by credit vs. debit; average credit sharei; M = 83.76, SD = .33) across the preintroduction window. We construct the second measure based on a customer's historical basket sizes (i.e., the average dollar value of their basket; average basket sizei; M = 66.59, SD = 45.54) across the preintroduction window. 14

We investigate whether BNPL installment payments have a significantly differential impact between customers by estimating Equation 1 with additional interaction terms (Goldfarb, Tucker, and Wang 2022). Specifically, we estimate Equation 2, in which we allow interactions between the focal parameter of interest and a customer's historical average credit share and purchase amount:

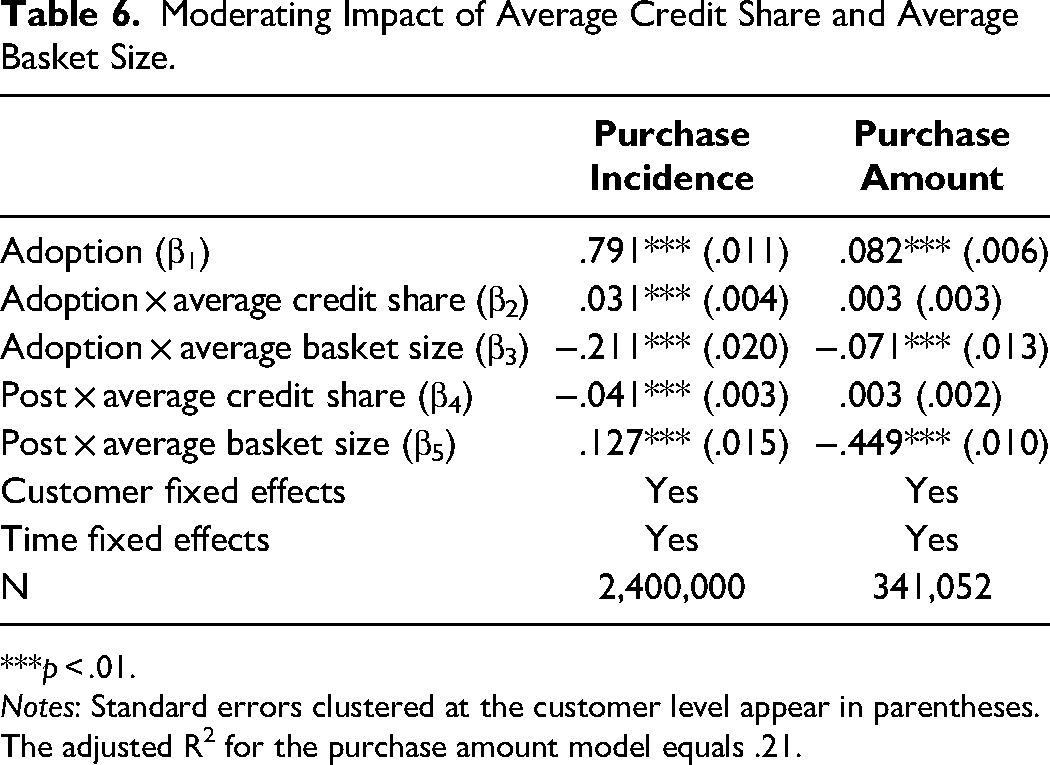

Table 6 reports the results, indicating negative and significant interaction effects between adoption and average basket size in the purchase incidence model (β3,PI = −.211, p < .01) and in the purchase amount model (β3,PA = −.071, p < .01). In line with our expectations, this indicates that the positive effects of adoption on purchase incidence are less pronounced among larger-basket shoppers than among smaller-basket shoppers. The results also confirm an expected positive and significant interaction of adoption and average credit share in the purchase incidence model (β2,PI = .031, p < .01) and a positive but insignificant interaction effect in the purchase amount model (β2,PA = .003, p = .29). A simple slope analysis further reveals that the effects remain statistically significant at high and low level of average basket size and credit share (see Web Appendix D).

Moderating Impact of Average Credit Share and Average Basket Size.

***p < .01.

Notes: Standard errors clustered at the customer level appear in parentheses. The adjusted R2 for the purchase amount model equals .21.

Study 1 Discussion

Study 1 indicates that the adoption of BNPL installment payments is associated with increases in customer's purchase incidence and purchase amount. The effect is economically and statistically significant over time and is robust against using alternative groups of adopters and nonadopters. Our analysis of heterogeneity shows that the effect is more pronounced among smaller- (vs. larger-) basket size shoppers and credit (vs. debit) credit card shoppers.

Although the analyses in Study 1 indicate that BNPL installment payments are associated with increased spending, Study 1 is subject to two key limitations that we seek to address in subsequent studies. First, in an ideal setting, the retailer would have randomly assigned a customer to a single payment condition, which was infeasible in this context. Therefore, Study 1 relied on matching on observables to improve the comparability between adopting and nonadopting customers. The absence of unobservable characteristics (e.g., income) in the matching may bias our results if such characteristics affect both adoption and purchase behavior. Matching on behavioral characteristics may in part mitigate this concern (e.g., due to correlation between behavior and income). To alleviate concerns about selection on unobservables, we conducted a robustness check that replicates the analysis using within-adopter variation, where late adopters (instead of nonadopters) act as a control for early adopters (Iyengar, Park, and Yu 2022; Yan, Miller, and Skiera 2022). This can mitigate possible selection on unobservable customer characteristics that are shared by early and late adopters. A potential solution to deal with an unexplained part of the adoption decision related to our outcome measures would be to estimate a selection model. However, this is “only useful for causal inference in the presence of a strong credible exclusion restriction” (Goldfarb, Tucker, and Wang 2022, p. 13). We were unable to implement a selection model because we do not have strong and credible observables that only affect adoption but not the outcome variable. Thus, we lack exogenous variation in the adoption decision, which we note as a caveat of this study. Second, Study 1 provides limited insight into the impact of BNPL installment payments on customers’ perceived financial constraints.

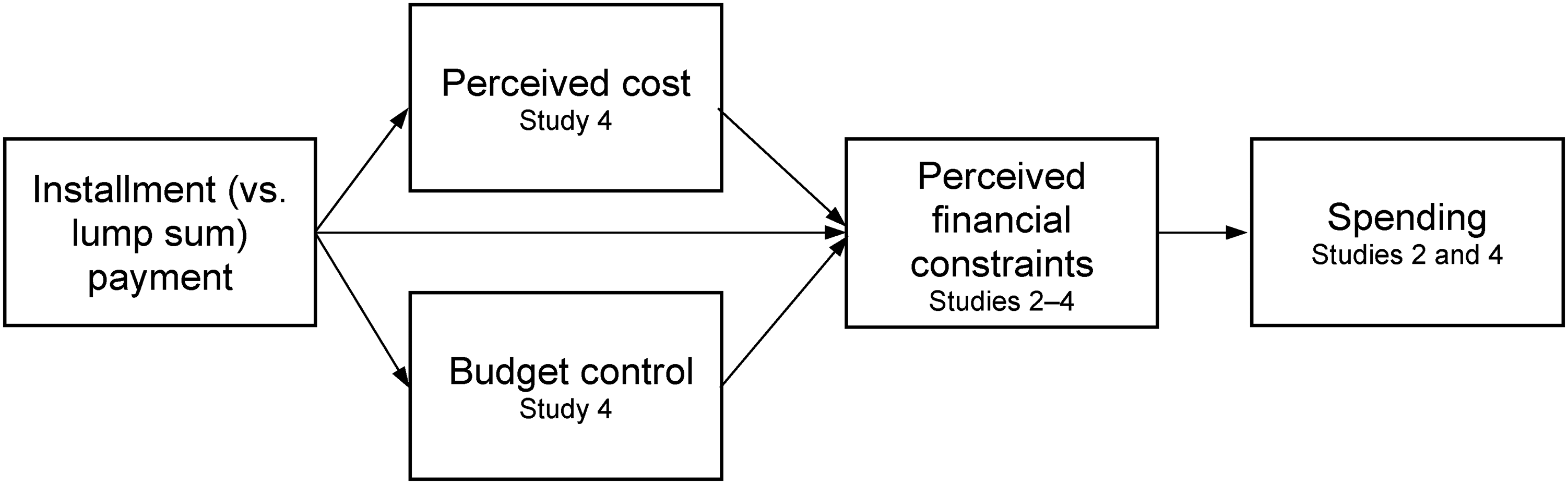

Our experiments address these limitations through (1) random assignment of payment methods and (2) testing the underlying mechanisms. By independently manipulating payment methods, the experiments test the causal effect of BNPL installment payment on spending in a more controlled setting. We also shed more light on the mechanism proposed in our conceptual framework (see Figure 3). Specifically, the experiments show that perceived financial constraints mediate the effect of BNPL installments on spending (Studies 2 and 4) while addressing alternative explanations (e.g., price attractiveness, feelings of being misled, perceived benefits, construal level; Studies 3 and 4). We also demonstrate that BNPL installments alleviate perceived financial constraints by reducing perceived costs and boosting budget control (Study 4). The experiments indicate that the effect of BNPL installments is robust across different products (e.g., party supplies, apparel, flights) and number of installments (e.g., three installments, four installments, six installments).

Conceptual Framework and Overview of Experiments.

Study 2: The Mediating Role of Perceived Financial Constraints

We propose that BNPL installment (vs. lump sum) payments reduce perceived financial constraints, increasing spending. To test these predictions in a more controlled setting, we created a shopping task where participants were randomly assigned to an installment or lump sum payment condition. In the lump sum payment condition, payment was delayed such that full payment was due at the end of six weeks. Prior research has shown that delaying payment increases spending (Raghubir and Srivastava 2008). If delaying payment is the sole driver for our effect, we would expect participants in the delayed lump sum payment condition to spend more than their counterparts in the installment condition, since payments need to be made earlier in the installment than in the delayed lump sum payment condition. However, if segregating versus aggregating costs contributes to the effect, we would expect participants in the installment condition to spend more than those in the delayed lump sum condition.

Method

We preregistered this experiment using AsPredicted (https://aspredicted.org/tn7bs.pdf). Four hundred participants were recruited on CloudResearch in exchange for a small monetary payment. Participants who failed the attention checks were excluded from the analysis, leaving a final sample of n = 391 (52.4% male, 47.6% female; Mage = 40.59 years). We randomly assigned participants to one of two payment conditions: lump sum or installment payment.

All participants were given a shopping task where they imagined that they were planning a Halloween party and needed to get some supplies. In the lump sum condition, participants adopted a payment method where they paid for the entire amount in six weeks. In the installment condition, participants paid in four biweekly installments where they paid the fourth installment in six weeks. In both conditions, the payment methods incurred no interest and no fees if they were paid on time.

Next, participants made five decisions where they could purchase several items for each product category (e.g., decorations, games, sweet treats). To mimic a real-life shopping environment, participants had four to six items to choose from and could pick more than one item for each decision. Prices were shown for every item. In the installment condition, these prices were also split into four installments (e.g., Halloween Party Deco Kit $10—four installments of $2.50). All participants indicated the items they wished to purchase. After the shopping task, participants in the lump sum condition were shown the total cost of the selected items. In the installment condition, we also showed the total cost split across four biweekly installments. The manipulations are included in Web Appendix E.

After completing the shopping task, we measured perceived financial constraint with the following three items adapted from Paley, Tully, and Sharma (2019): (1) “To what extent does this payment method make you feel financially constrained?” (1 = “not at all financially constrained,” and 9 = “very financially constrained”), (2) “To what extent does this payment method allow you to spend as much as you like?” (reverse-coded, 1 = “not at all, and 9 = “very much”), and (3) “To what extent does the payment method help with your financial situation?” (reverse-coded, 1 = “does not help at all,” and 9 = “very helpful”). Finally, participants responded to an attention check and completed the manipulation check and the demographic measures.

Results

Manipulation checks

Consistent with our manipulations, participants in the installment condition described the payment more as ongoing installments compared with their counterparts in the lump sum conditions (Minstallment = 8.00, SD = 1.96 vs. Mlump sum = 2.22, SD = 2.32; t(389) = −26.56, p < .001, Cohen's d = −2.69). Participants in the lump sum condition regarded the payment as more deferred than their counterparts in the installment condition (Minstallment = 7.53, SD = 1.92 vs. Mlump sum = 8.12, SD = 1.91; t(389) = 3.03, p < .001, Cohen's d = .31). This is consistent with the manipulations, as the installment condition required payments to be made sooner than the lump sum condition.

Perceived financial constraints

The three items assessing financial constraints were averaged such that a higher number indicated greater perceived financial constraints (α = .58). 17 As predicted, participants in the installment condition felt less financially constrained than their counterparts in the lump sum condition (Minstallment = 4.09, SD = 1.69 vs. Mlump sum = 4.83, SD = 1.79; t(389) = 4.14, p < .001, Cohen's d = .42).

Spending

As predicted, participants in the installment condition purchased more items than their counterparts in the lump sum condition (Minstallment = 9.92, SD = 4.18 vs. Mlump sum = 9.27, SD = 3.07; t(389) = −1.74, p = .082, Cohen's d = −.18). We also examined the effect of the payment method on the total amount of money participants spent in the shopping task. As expected, participants in the installment condition spent more money than those in the lump sum condition (Minstallment = $89.42, SD = $40.95 vs. Mlump sum = $77.46, SD = $30.86; t(389) = −3.27, p = .001, Cohen's d = −.33).

Mediation

We then examined if perceived financial constraints mediated the effect of payment method on the number of items purchased using PROCESS Model 4 (Hayes 2017). Consistent with our predictions, perceived financial constraints mediated the effect of installment payment on the number of items purchased (indirect effect = .31, 95% CI: [.12, .57], 10,000 resamples). We also examined if perceived financial constraints mediated the effect of payment method on the total amount spent using PROCESS Model 4 (Hayes 2017). Consistent with our predictions, perceived financial constraints mediated the effect of installment payment on the total amount spent (indirect effect = 3.31, 95% CI: [1.27, 6.05], 10,000 resamples). These results show that perceived financial constraints are an underlying mechanism for the effect of BNPL installments on spending.

Study 2 Discussion

Study 2 provided causal evidence that BNPL installment payments increased spending compared with an equivalent lump sum payment. 18 Moreover, differences in perceived financial constraints explained the effect of BNPL installment payments on spending. Specifically, participants who paid in installments (vs. lump sum) felt less financially constrained and spent more. In this experiment, both payment methods did not incur any interest, limiting the possibility that participants thought they had more money to spend in the installment payment condition due to the lack of interest. Furthermore, both payment methods were deferred. Participants perceived the installment condition (i.e., four installment payments over six weeks) as less deferred than the lump sum condition (i.e., one lump sum payment in six weeks). This mitigates the possibility that participants spent more in the installment (vs. lump sum) condition due to the delay in payment.

Study 3: The Effect of BNPL Installment Payments on Perceived Financial Constraints and Alternative Mechanisms

Study 2 demonstrated that BNPL installment payments (vs. a delayed lump sum payment) are perceived to be less financially constraining. The goal of Study 3 is to examine alternative mechanisms for the effect of segregating payment. First, segregating prices has been shown to increase perceived benefits and, in turn, purchase intentions (Atlas and Bartels 2018). Correspondingly, segregating payments into BNPL installments could have a similar effect. Second, segregated prices have been found to elicit feelings of being misled as customers find segregated prices more complex and become skeptical of the marketer's motives (Bambauer-Sachse and Mangold 2009; Bambauer-Sachse and Grewal 2011). Similarly, segregating payments into BNPL installments could be deemed complex and misleading. Third, segregating prices into smaller terms has been found to enhance price attractiveness. Specifically, segregated prices (“€2 per day”) were deemed as more well-priced and a better deal than aggregated prices (“€60 per month”; Bambauer-Sachse and Grewal 2011). Although the aggregate term was present, segregating payment into smaller installments could increase price attractiveness. Therefore, we measured perceived benefits, feelings of being misled, and price attractiveness to explore whether they might play a role in our context.

Furthermore, prior research has shown that consumers prefer payment schemes that match the pattern of benefits they gain from purchases (Auh, Shih, and Yoon 2008). Since Study 2 used supplies for an upcoming party, its pattern of benefits could be relatively short. Thus, BNPL installments might increase purchase likelihood as it requires an up-front payment, aligning the benefits of the purchase with its payment scheme. Therefore, Study 3 uses a product for which consumption should exceed the payment period (i.e., a T-shirt, which on average lasts about 2.20 years; Kale 2019).

Method

As preregistered on AsPredicted.org (https://aspredicted.org/py9ai.pdf), 600 participants were recruited on Prolific in exchange for a small monetary payment. Participants who failed the attention checks were excluded from the analysis, leaving a final sample of n = 599 (35.6% male, 64.1% female, .3% others; Mage = 41.50 years). All participants read a hypothetical scenario where they bought a T-shirt with a price of $24. Spending was kept constant across conditions to isolate the impact of installment payments on the mechanisms (i.e., to minimize the possible influence of spending on the mechanisms). They were randomly assigned to one of three payment conditions: (1) an up-front lump sum condition (i.e., pay $24 now), (2) a delayed lump sum condition (i.e., pay $24 in 30 days), or (3) an installment condition (i.e., pay in three installments of $8). All payment conditions incurred no interest and fees if they were paid on time.

Next, perceived financial constraints were measured using four items: “To what extent does the payment method …” (1) “make you feel less financially constrained?,” (2) “allow you to spend as you like?,” (3) “improve your financial situation over others?,” and (4) “help with your financial situation?” (1 = “Not at all,” and 9 = “Very much”; α = .85; adapted from Paley, Tully, and Sharma [2019]). These items were reverse-coded and averaged such that a higher number indicated higher perceived financial constraints.

To examine alternative mechanisms, we also measured perceived benefits of the purchase on the following four items: (1) “I would get a lot of pleasure from this purchase,” (2) “I would miss out on benefits if I did not have this purchase,” (3) “I would benefit a lot from having this purchase,” and (4) “This purchase would not be very beneficial for me” (reverse-scored) (1 = “strongly disagree,” 9 = “strongly agree”; Atlas and Bartels 2018; α = .77). We assessed feelings of being misled on five items: (1) “The presentation of the price is unclear,” (2) “I cannot understand the price at a glance,” (3) “The price information is quite complex,” (4) “My friends would judge this price as an unfair price,” (5) “This seller has the intention of misleading customers” (1 = “strongly disagree,” and 9 = “strongly agree”; Bambauer-Sachse and Grewal 2011; α = .79). Price attractiveness was also measured on the following three items: (1) “In general, this product is well-priced,” (2) “The product price is attractive,” and (3) “Compared to similar products’ prices, this price is a good deal” (1 = “strongly disagree,” and 9 = “strongly agree”; Bambauer-Sachse and Grewal 2011; α = .95).

As manipulation checks, participants also indicated how they regarded the payment method on two items (1 = “lump sum,” and 9 = “ongoing installments”; 1 = “now,” and 9 = “deferred”). We measured cost awareness by asking participants to indicate the price of the T-shirt on a slider scale, ranging from $0 to $50. Finally, participants responded to an attention check and reported their demographic details (see Web Appendix G for stimuli and measures).

Results

Manipulation checks

A one-way ANOVA revealed a significant difference across payment conditions on the perceptions of ongoing installments (F(2, 595) = 601, p < .001, η2 = .67). Consistent with our manipulations, participants in the installment condition described the payment more as ongoing installments than their counterparts the lump sum conditions (Minstallment = 8.31, SD = 1.33 vs. Mup-front lump sum = 1.43, SD = 1.50 and Mdelayed lump sum = 3.09, SD = 3.00; t(596) = −32.10, p < .001, Cohen's d = −2.78). As expected, there are also significant differences across payment conditions on whether the payment is deferred (F(2, 595) = 1349, p < .001, η2 = .82). Post hoc comparisons using a Tukey honestly significant difference (HSD) test indicated that the installment condition was regarded as significantly more deferred than the up-front lump sum condition (Minstallment = 7.67, SD = 1.64 vs. Mup-front lump sum = 1.33, SD = 1.19, p < .001), but less deferred than the delayed lump sum condition (Minstallment = 7.67, SD = 1.64 vs. Mdelayed lump sum = 8.30, SD = 1.57; p < .001). These findings were consistent with the manipulations. Participants did not differ significantly across conditions on cost awareness (F(2, 595) = .07, p = .935, η2 = .00), with participants indicating an average of $24 in all three conditions (Minstallment = $24.00, SD = 2.60; Mdelayed lump sum = $24.00, SD = .76; Mup-front lump sum = 24.00, SD = .24).

Perceived financial constraints

As predicted, there were significant differences in perceived financial constraints across payment conditions (F(2, 595) = 12.19, p < .001, η2 = .039). Participants in the installment condition felt less financially constrained than their counterparts in the lump sum conditions (Minstallment = 5.48, SD = 2.29 vs. Mdelayed lump sum = 6.05, SD = 2.23 and Mup-front lump sum = 6.51, SD = 1.71; t(596) = 4.42, p < .001, Cohen's d = .38). Post hoc comparisons using a Tukey HSD test also indicated that participants in the installment condition felt less financial constrained than their counterparts in the delayed lump sum condition (Minstallment = 5.48, SD = 2.29 vs. Mdelayed lump sum = 6.05, SD = 2.23; p = .018) and up-front lump sum condition (Minstallment = 5.48, SD = 2.29 vs. Mup-front lump sum = 6.51, SD = 1.71; p < .001).

Alternative mechanisms

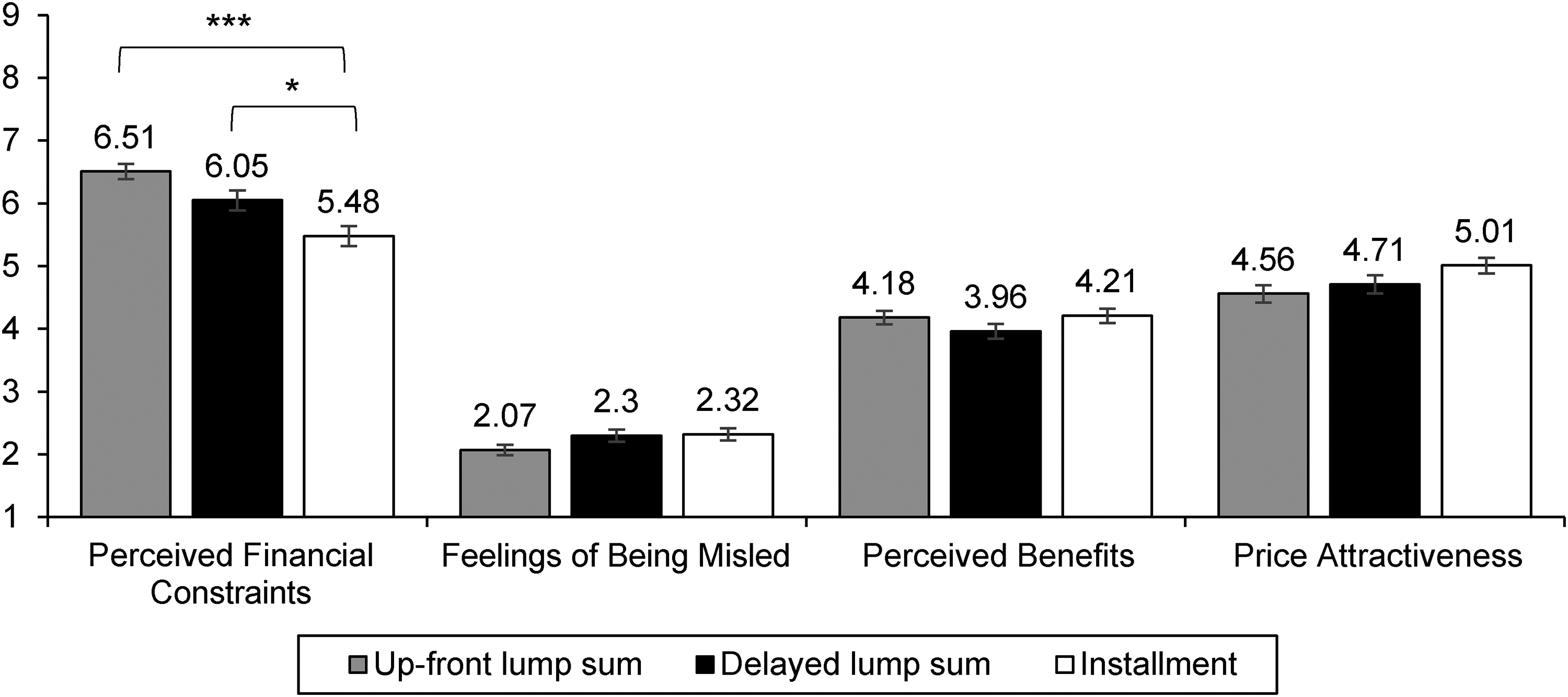

There were no significant differences across payment conditions on feelings of being misled (F(2, 595) = 2.35, p = .096, η2 = .008), perceived benefits (F(2, 595) = 1.50, p = .224, η2 = .005) and price attractiveness across payment conditions (F(2, 595) = 2.83, p = .060, η2 = .009). Post hoc comparisons using a Tukey HSD test revealed no significant differences between the installment condition and the delayed lump sum condition in feelings of being misled (Minstallment = 2.32, SD = 1.40 vs. Mdelayed lump sum = 2.30, SD = 1.36; p = .983), perceived benefits (Minstallment = 4.21, SD = 1.62 vs. Mdelayed lump sum = 3.96, SD = 1.65; p = .246), or price attractiveness (Minstallment = 5.01, SD = 1.77 vs. Mdelayed lump sum = 4.71, SD = 2.06; p = .269). There were also no significant differences between the installment condition and the up-front lump sum condition on feelings of being misled (Minstallment = 2.32, SD = 1.40 vs. Mup-front lump sum = 2.07, SD = 1.17; p = .122), perceived benefits (Minstallment = 4.21, SD = 1.62 vs. Mup-front lump sum = 4.18, SD = 1.51; p = .973), or price attractiveness (Minstallment = 5.01, SD = 1.77 vs. Mup-front lump sum = 4.56, SD = 1.97; p = .052) 19 (Figure 4).

Perceived Financial Constraints, Feelings of Being Misled, Perceived Benefits, and Price Attractiveness by Payment Condition (Study 3).

Study 3 Discussion

Study 3 showed that segregating payment into BNPL installments alleviated perceived financial constraints. This study also explored several potential alternative mechanisms. Customers might have failed to understand how BNPL payments worked and felt misled. We did not find evidence for this alternative explanation. Participants were aware of the purchase cost and did not differ in feelings of being misled across payment conditions. This finding suggests that participants were just as cognizant of the costs in BNPL payments as lump sum payments. We also did not find significant differences in price attractiveness between the delayed lump sum and the installment condition. This implies that segregating payment does not significantly affect price attractiveness.

Moreover, segregating payment did not significantly impact perceived benefits. Prior work on temporal reframing has partly attributed its effectiveness to perceived benefits. Atlas and Bartels (2018) found that framing prices in segregated terms (“25ȼ a day”) helped customers appreciate the recurring benefits of the contract than if the same price was framed in aggregated terms (“$90 a year”). Since BNPL is restricted to a specific number of payments for a short time (“six weeks”), segregating payment into BNPL installments could have a limited impact on perceived benefits.

BNPL installment payment decreased perceived financial constraints, even after controlling for these alternative mechanisms (see Web Appendix G for details). Overall, our findings suggest that segregating payment alleviates perceived financial constraints, even when participants know the purchase cost, are not misled, and perceive similar benefits from the purchase.

Study 4: Testing the Full Model

While Studies 2 and 3 demonstrated that BNPL installment payments reduced financial constraints, Study 4 aimed to unpack the link between BNPL installment payments and perceived financial constraints by examining two plausible underlying constructs. We proposed that segregating payment into BNPL installments lowers perceived financial constraints by making purchases seem less costly and facilitating control over one's budget. 20 Thus, Study 4 was designed to examine the full model, whereby BNPL installment payments reduce perceived cost and increase budget control, thereby reducing perceived financial constraints and, in turn, increasing purchase likelihood.

Study 3 demonstrated the effect of BNPL installments for products whose benefits exceed the payment period. Study 4 aimed to generalize the effect of BNPL installment payments on purchase intentions when benefits do not exceed the payment period (i.e., for a flight booked six weeks in advance).

Study 4 also aimed to examine two alternative explanations for our effect. One alternative explanation is the pattern alignment hypothesis: “Consumers prefer payment schemes that match the pattern of benefits and payments in each period, rather than a scheme that encompasses an entire financing period” (Auh, Shih, and Yoon 2008, p. 292). To examine if the pattern alignment hypothesis drives our effects, Study 4 utilized a flight booked six weeks in advance as it offers a one-off benefit six weeks later. Since BNPL requires an up-front payment with additional installment payments before consumption, some payments are made before the benefits occur. In contrast, the pattern of benefits is more aligned with delayed lump sum payment as both the flight and payment are due in six weeks. By showing that BNPL installment still works in this context, we illustrate that our effects are not just driven by a preference to align payment with the pattern of consumption benefits (Auh, Shih, and Yoon 2008). Second, we also investigated the possibility that installment (vs. delayed lump sum) payments could induce different mental construals to influence spending (Chen, Xu, and Shen 2017).

Method

As preregistered on AsPredicted.org (https://aspredicted.org/ra49n.pdf), 400 participants were recruited on Prolific for a small monetary payment. Participants who failed the attention checks were excluded from the analysis, leaving a final sample of n = 399 (50.6% male, 48.6% female, .8% others; Mage = 42.50 years). All participants read a hypothetical scenario where they were planning for an upcoming trip that was happening in six weeks and found a flight for $59.10. They were randomly assigned to either a delayed lump sum (i.e., pay $59.10 in six weeks) or installment (i.e., pay six installments of $9.85) payment condition.

Next, purchase likelihood was assessed on two questions on an 11-point scale (0 = “Not at all,” and 10 = “Very much”; adapted from Atlas and Bartels [2018]; α = .86). We then measured perceived financial constraints using four questions (e.g., “To what extent does the payment method make you feel less financially constrained?”; reverse-coded, 0 = “Not at all,” and 10 = “Very much”; α = .93; adapted from Paley, Tully, and Sharma [2019]), perceived cost using four questions (e.g., “To what extent does the payment method make the cost of the product trivial?”; reverse-coded, 0 = “Not at all,” and 10 = “Very much”; α = .89; adapted from Atlas and Bartels [2018]), and budget control using four questions (e.g., “To what extent does the payment method give you the ability to maintain a budget?”; 0 = “Not at all,” and 10 = “Very much”; α = .98; adapted from Kidwell and Turrisi [2004]). Participants also completed the Behavioral Identification Form to test for the role of construal level (Chen, Xu, and Shen 2017; adapted from Vallacher and Wegner [1989]). Finally, they completed the manipulation checks regarding the payment methods and reported their demographic details (see Web Appendix I for stimuli and measures).

Results

Manipulation checks

Consistent with our manipulations, participants in the installment condition described the payment as more ongoing installments than their counterparts in the lump sum condition (Minstallment = 9.37, SD = 1.43 vs. Mdelayed lump sum = 3.58, SD = 4.28; t(397) = −18.09, p < .001, Cohen's d = −1.81). As expected, participants in the delayed lump sum condition regarded their payment as more deferred than their counterparts in the installment condition (Mdelayed lump sum = 9.13, SD = 1.79 vs. Minstallment = 8.54, SD = 2.23; t(397) = 2.90, p = .004, Cohen's d = .29).

Purchase likelihood

As predicted, purchase likelihood was higher in the installment condition than in the delayed condition (Minstallment = 6.35, SD = 3.30 vs. Mdelayed lump sum = 5.67, SD = 3.55; t(397) = −2.00, p = .046, Cohen's d = −.20).

Perceived financial constraints

In line with our predictions, participants in the installment conditions felt less financially constrained than their counterparts in the delayed lump sum condition (Minstallment = 4.50, SD = 3.09 vs. Mdelayed lump sum = 5.19, SD = 3.21; t(397) = 2.20, p = .028, Cohen's d = .22).

Perceived cost

As expected, participants in the installment condition perceived payment as less costly than their counterparts in the delayed lump sum condition (Minstallment = 4.51, SD = 2.94 vs. Mdelayed lump sum = 5.54, SD = 3.01; t(397) = 3.43, p < .001, Cohen's d = .34).

Budget control

Participants in the installment condition perceived higher budget control than their counterparts in the delayed lump sum condition (Minstallment = 6.57, SD = 3.12 vs. Mdelayed lump sum = 5.60, SD = 3.36; t(397) = −3.00, p = .003, Cohen's d = −.30).

Construal level

There were no significant differences between payment conditions on construal level (Minstallment = 8.65, SD = 6.08 vs. Mdelayed lump sum = 9.21, SD = 6.42; t(397) = .91, p = .37, Cohen's d = .09), suggesting that participants perceived both installment and delayed lump sum payment just as concretely.

Serial mediation

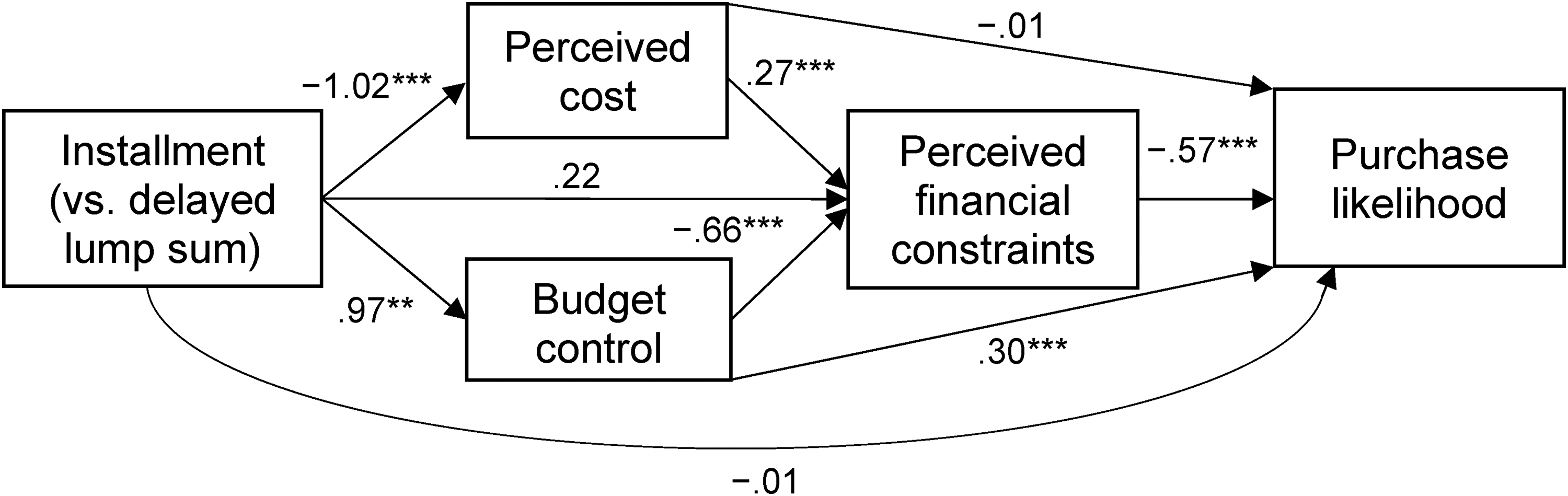

As preregistered, we used the serial mediation bootstrapping methodology (Hayes 2017; Model 80) with payment conditions as the independent variable, perceived cost and budget control as the first mediators, perceived financial constraints as the second mediator, and purchase likelihood as the dependent variable (Figure 5). The serial mediation was significant. BNPL installment payments made costs seem more trivial, reducing perceived financial constraints, and increasing spending (indirect effectperceived costs = .16, 95% CI: [.06, .28]. BNPL installment payments also increased budget control, reducing perceived financial constraints, and increasing spending (indirect effectbudget control = .37, 95% CI: [.12, .65]) (see Web Appendix I for additional details on the analysis).

Serial Mediation Model (Study 4).

Study 4 Discussion

Study 4 provided evidence for our full model. We showed that BNPL installment payments reduced perceived costs and facilitated budget control, thereby reducing perceived financial constraints, which in turn, increased purchase likelihood. This effect emerged with a product whose benefits would only materialize in six weeks. Hence, this study showed that the effect of BNPL installment generalized to purchases where the benefits and payment period were not aligned. We also examined if installment payments affected construal level and found no differences across payment conditions on how customers construed their purchases.

General Discussion

A growing number of retailers, such as ASOS, Adidas, Walmart, and Sephora, have introduced BNPL installment payments in recent years. However, the impact on customers’ spending remains unclear (Digital Commerce 360 2023; Schultz 2022; Tijssen 2021). Our research takes the first step to examine the effects of BNPL installment payments on customers’ spending. A DID analysis indicates that BNPL installment payments increase purchase incidence and purchase amounts. These effects remain statistically and economically significant over time. Moreover, this increase in spending is greater for smaller- (vs. larger-) basket shoppers and for shoppers who relied more heavily on credit (vs. debit) cards before adoption. Three preregistered experiments elucidate the underlying mechanisms, showing that BNPL installments decrease perceived costs and increase budget control, alleviating perceived financial constraints and thereby increasing spending.

Practical Implications

Our findings provide several novel insights to retailers and address uncertainties about the impact of BNPL installments on customer spending (Digital Commerce 360 2023; Tijssen 2021). We demonstrate that retailers benefit because adoption of installment payments leads to more frequent purchases and larger basket amounts. These effects are economically significant, with an increase in purchase incidence of approximately 9 percentage points and a relative increase in purchase amounts of approximately 10% in our context. In addition, we find that these effects persist over time, extending across the entire 26-week postadoption period observed in our study. By documenting continued increased spending among customers after adopting BNPL installments, we alleviate retailer concerns about the long-term effects of BNPL (Schultz 2022). This finding is significant for retailers as (1) the introduction of BNPL installment payments typically incurs costs, and (2) fees on installment transactions are higher than those on credit card payments (Tijssen 2021).

Moreover, our studies provide retailers with insights into why these effects occur. Specifically, customers perceive paying in segregated installments (“Pay $60 in four biweekly installment payments over six weeks”) as less financially constraining than paying in an interest-free delayed lump sum (“Pay $60 in six weeks”). This is at least in part because BNPL installments make customers feel more in control of their budget. We reveal that BNPL installments alleviate perceived financial constraints across a broad range of goods and services, irrespective of whether consumption occurs on a recurring (e.g., clothing) or a one-off (e.g., a flight) basis.

Furthermore, our analysis of customer heterogeneity illustrates how retailers can leverage BNPL installment payments to maximize gains. Basket size and credit card usage are two behavioral characteristics commonly observed by retailers. Previous research suggests that smaller basket shoppers and heavier credit card users are, on average, more financially constrained (Bell and Lattin 1998; Borzekowski, Kiser, and Shaista 2008; Noble et al. 2017). Consistent with our theorizing, we find that increases in spending are larger among customers who tend to purchase smaller (vs. larger) baskets and tend to rely more heavily on credit (vs. debit) cards. Retailers could, for example, target communication about the availability of BNPL installment payments to customers who typically purchase smaller amounts. Such a targeted approach could help optimize the financial impact of BNPL offerings.

Finally, our insights may also be of practical relevance to policy makers. Regulators are increasingly concerned about the potential impact of BNPL installment payments on customers’ purchase behavior. However, there is a lack of research on the topic that can inform regulators about the effects of BNPL on actual spending. We observe that BNPL installment schemes can substantially impact customers’ spending. Furthermore, our secondary data analysis suggests that more financially constrained customer groups (e.g., small-basket shoppers and credit card shoppers) are more likely to rely on BNPL and increase their spending. Regulators and responsible retailers should ensure that BNPL installment payments do not have adverse implications for customers by ensuring that the provided credit is affordable.

Theoretical Implications

Our research offers novel theoretical insights into the impact of payment segregation on customers’ purchase behavior. Prior literature on temporal reframing has considered the impact of framing prices in segregated terms while keeping payments aggregated (e.g., Gourville 1998, 1999, 2003). In contrast, our research examines the effects of segregating actual payments into installments. We show that segregating payment works beyond existing temporal reframing mechanisms by affecting perceived financial constraints. 21

By alleviating perceived financial constraints, segregating payment is effective in various contexts. First, segregating payment into BNPL installments impacts behavior even when aggregate terms are salient to customers. Whereas prior research presented segregated versus aggregate frames independently, our findings apply to real-world contexts where both terms are presented together. Second, previous studies on temporal reframing of price primarily found effects in ongoing consumption contexts (e.g., subscriptions) but not for one-off consumption (Gourville 1999). We demonstrate that segregating payment is effective for products and services, including one-off consumption (e.g., a flight in Study 4). Third, our research shows that the effect persists even when aggregate payments are perceived to be more delayed than installment payments. Fourth, while prior work focused on cross-sectional effects using experiments, we leveraged transactional data to show that the impact of segregating payments remains statistically and economically significant over time. Fifth, we find consistent support for our effect across various categories, including durable and nondurable purchases (e.g., party supplies, flights, clothing). We also find support across varying numbers of payments (e.g., three, six) and different repayment periods (e.g., 30 days, 6 weeks).

Finally, we contribute to work on perceived financial constraints. While existing research has examined its consequences on consumer behavior (e.g., Dias, Sharma, and Fitzsimons 2022; Paley, Tully, and Sharma 2019; Tully, Hershfield, and Meyvis 2015), we illustrate an antecedent by showing that segregated installment (vs. delayed lump sum) payments reduce perceived financial constraints.

Limitations and Future Research

Our research takes a first step toward understanding the impact of BNPL installment payments.

Future research should examine to what extent our results generalize across (1) retailers and industries, (2) later adopters of BNPL installment payments, and (3) time periods. 22 More research is needed to determine how the magnitude of the effect is moderated by financially constraining times such as economic recessions and periods of high inflation. As BNPL grows in popularity, future work could examine how the maturity of installment payments affects its impact. For example, research on cashless (vs. cash) payments has shown that the positive effect on spending has diminished in size over the years (Liu and Dewitte 2021; Schomburgk, Belli, and Hoffmann 2024). The impact of BNPL maturity might also depend on (1) the extent to which BNPL decreases spending from other retailers in the same category (i.e., substitution between retailers) and (2) the extent to which BNPL increases total category spending across retailers (i.e., expansion). Access to data from multiple retailers could help identify potential substitution versus expansion effects. 23 Another promising research area would be to investigate the impact on the types of products customers purchase. For instance, prior work on perceived financial constraints suggests that financially constrained customers are more likely to spend their money on material rather than experiential purchases (Tully, Hershfield, and Meyvis 2015).

Moreover, we do not observe the costs of the BNPL program. While sales revenues increase, the profitability of BNPL installment payment services depends on whether the increase in revenue outweighs the additional cost of the service. Future work should also examine whether and how BNPL installments may impact return behavior. Additionally, while adopters heavily rely on BNPL installment payments at the focal retailer, future work could identify what drives customers to use a given payment method at a particular point in time. For instance, this may depend on customers’ credit card billing cycle, available credit, and the nature of the purchase (e.g., its necessity and its alignment with the timing of benefits obtained from consumption; Auh, Shih, and Yoon 2008).

Future research could examine the roles of alternative mechanisms and theories, including those related to mental accounting (Thaler 1985, 1999, 2008), liquidity constraints (Beltramo et al. 2015), and net present value. 24 Additionally, future work should investigate whether BNPL has adverse implications for customers by exploiting financial decision-making biases. For instance, future research could examine whether people are overly optimistic about future payments by studying the role of intertemporal discounting (Prelec and Loewenstein 1998).