Abstract

Research examining the antecedents of recalls, instead of their consequences, is relatively sparse and has not considered whether firms’ likelihood to recall products is influenced by legal changes that could induce managerial opportunism, such as those reducing shareholder litigation risk. To examine this question, the authors exploit the staggered adoption of universal demand (UD) laws across several U.S. states as a quasi-natural experiment. UD laws aim to prevent frivolous litigation from disrupting a firm's normal business operations by making it more difficult for shareholders to sue managers for neglecting their fiduciary duties and hold them personally liable. Although UD laws are well-intended, the reduced threat of shareholder litigation disciplining a firm's managers could have unintended negative consequences. Indeed, using a difference-in-differences analysis, the authors find that following the adoption of UD laws, affected firms become less likely to recall products. This effect is weaker in the presence of organizational mechanisms constraining managers’ self-interest-seeking behavior, such as a corporate culture focused on customer needs and interests or the exercise of normative control through monitoring by institutional investors. The authors do not find support for a potential alternative explanation of operational improvement and therefore higher product quality driving their findings.

Suing the directors is a better deterrent than suing the corporation. Directors are going to care more about being held personally liable … than … the company losing a bit more money in shareholder settlements on top of the money it already lost from the bad event itself.

Product recalls are costly, reducing firm value through lost sales, an impaired reputation, and consumer compensation (Chen, Ganesan, and Liu 2009). The publicity of recalls also invites product liability claims (Jones Day 2012). Although, in theory, managers of publicly listed firms should strive to safeguard the long-term value of the firm, in practice, they often face incentives and feel pressures leading to an overemphasis on short-term goals (Mizik 2010), which could motivate them to try to avoid recalls to avert their immediate costs (Eilert et al. 2017). General Motors knowing for ten years about faulty ignition switches before issuing a recall is a case in point (Valdes-Dapena 2014). However, not recalling can jeopardize consumer welfare and hurt the firm's long-term viability (Eilert et al. 2017), exposing managers to the risk of being sued by shareholders for neglecting their fiduciary duties and being held personally liable for compensating the firm for the inflicted damage (Woodruff Sawyer & Company 2014).

The opening quote suggests that this threat of being sued by shareholders for failing to take sufficient action to prevent a product harm crisis could be an effective deterrent to prevent managers from trying to avoid a recall. Indeed, the recent Boeing 737 MAX case—in which current and former directors were sued by shareholders who claimed that the board failed to properly oversee safety matters concerning this airplane—illustrates that such lawsuits are a real risk for managers (Tangel 2021). In this article, we ask what happens when an external shock diminishes managers’ exposure to shareholder litigation risk for failing their fiduciary duties. Will this change in managerial liability affect firms’ subsequent likelihood to recall products? To answer this question, we exploit the staggered adoption of universal demand laws across different U.S. states as a quasi-natural experiment affecting how easy it is for shareholders to file so-called derivative lawsuits.

Derivative lawsuits are brought by shareholders in the name of the firm to enforce managers’ fiduciary duties and make them compensate the firm for any damage they allegedly caused. They are called derivative lawsuits because the firm is the actual plaintiff, whereas the shareholders initiating the lawsuit are the derivative plaintiffs (Bourveau, Lou, and Wang 2018). Derivative lawsuits are costly for managers, as they hurt their reputation and reduce career prospects (Bourveau, Lou, and Wang 2018). Moreover, directors and officers liability insurance does not cover wrongdoings involving dishonesty, intentional misconduct, or breaches in which one reaped a personal gain (Cox 1999). Hence, managers should be motivated to steer clear of actions that could invite derivative lawsuits, such as trying to avoid a product recall.

Against this background, the adoption of universal demand (UD) laws is important, as it imposes a significant procedural hurdle for shareholders to be able to file a derivative lawsuit by requiring them to first demand that the firm's board of directors take legal action against the wrongdoers. As its members are often defendants in the proposed lawsuit, boards typically refuse such requests, leading to the case's dismissal as judges tend to follow the decisions of boards (Bourveau, Lou, and Wang 2018). The adoption of UD laws is driven by the “cardinal precept” of corporate law that directors—rather than shareholders—manage the affairs of the firm. From this perspective, derivative lawsuits are an exception to the normal rule that boards of directors control corporations, and the demand requirement aims to return this power to the board, allowing them to take corrective actions before facing lawsuits that might distract their attention from managing the firm (Erickson 2017). In effect, UD laws aim to prevent frivolous derivative litigation (Erickson 2011) and to sort cases with merit from those without (Erickson 2017), to avoid unwarranted disruption of a firm's normal business operations, which often comes at a great cost to the affected firm (Lin, Liu, and Manso 2021).

Indeed, recent research argues that shareholder litigation risk might prevent some managers from taking bold initiatives, and it finds that UD law adoption is associated with an increase in corporate innovation (Lin, Liu, and Manso 2021). Other research, however, argues that it is exactly these bold initiatives that managers feel more comfortable taking after UD law adoption that can distract their attention and drain company resources away from safety-improving activities, leading to a deteriorated safety climate within firms (Lin et al. 2021). Thus, although UD laws are well-intended and have been linked to some positive consequences, the reduced threat of shareholder litigation as a governance mechanism disciplining a firm's managers could also have unintended negative consequences for a firm. In this article, we develop a conceptual framework examining the possible presence of such unintended consequences in the context of managerial decision making around product recalls.

In particular, we design an empirical strategy to address two main research questions. We first ask whether the adoption of UD laws affects the likelihood of firms to recall products. In this regard, we expect that if an external shock leads to less discipline being imposed on managers, the private incentives to try to avoid a recall to avert its immediate costs could come to dominate their decision making. This expectation is grounded in finance literature documenting agency conflicts in publicly listed firms (Jensen and Meckling 1976) and marketing literature on how such conflicts can induce managerial short-termism (Mizik 2010). We then ask what factors could mitigate the agency conflicts underlying a potential opportunistic response from managers to a reduction in shareholder litigation risk and thus weaken the main effect of UD law adoption on a firm's product recall likelihood.

From a business ethics perspective, two main mechanisms of organizational governance to constrain agents’ self-interest-seeking behavior and reduce the potential occurrence of moral problems in firms are corporate culture and normative control (Husted 2007). Regarding the former, we expect that if a firm's market orientation has a stronger customer focus, the resulting corporate culture (Narver and Slater 1998) will constrain managers’ opportunistic tendency to try to avoid a recall once it is harder for shareholders to sue them for doing so. Regarding the latter, we expect that if a greater proportion of a firm's outstanding stock is owned by institutional investors, the resulting exercise of normative control through the monitoring of managers (Bushee 1998) will constrain their tendency to respond opportunistically to a reduction in shareholder litigation risk, thus again weakening the main effect of UD law adoption on a firm's subsequent likelihood to recall products.

To address our research questions, we compile a comprehensive data set based on all U.S. publicly listed firms included in the Compustat database between 1986 and 2018. We merge these data with information on product recalls from the Consumer Product Safety Commission (CPSC). Since managerial decision making regarding product recalls should only be influenced by the reduced risk of being held personally liable as associated with UD law adoption if managers actually have discretion regarding whether to recall, our main analysis includes only recalls without prior injuries or deaths. 1 Consistent with our conceptual framework, we find a negative relationship between UD law adoption and firms’ subsequent likelihood to recall a product. We also document that the aforementioned relationship is less pronounced for firms with a more customer-focused market orientation or those subject to more stringent monitoring by institutional investors.

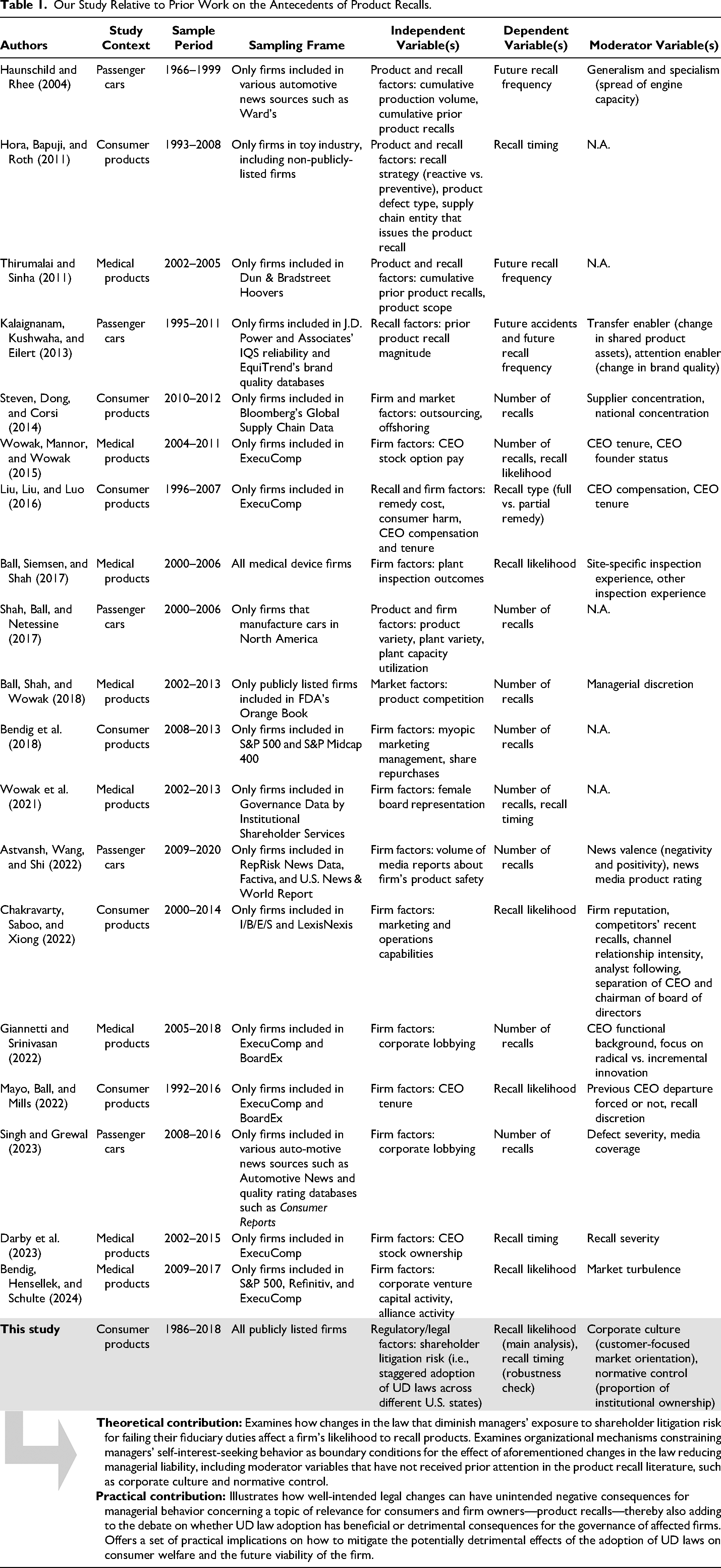

Our article contributes to the literature in several ways. Theoretically, we further our understanding of the antecedents of product recalls in terms of factors driving a firm's decision to recall or not, whereas prior research focuses on the consequences of recalls after they were already decided on. Table 1 positions our study relative to the limited literature on recall antecedents, to which we add by examining how an external shock diminishing managers’ risk of being sued by shareholders for failing their fiduciary duties influences a firm's subsequent likelihood to recall a product. In doing so, we respond to Bendig et al.’s (2018) critique that prior work lacks theory and evidence on precursors of recalls beyond operational issues. Specifically, it has not examined the role of legal changes reducing shareholder litigation risk as a driver of managerial opportunism in regards to recall decisions. Finally, with the majority of previous work coming from the field of operations management, the existing literature does not provide insights about how variables under the influence of the marketing function, such as a firm's customer focus, can act as boundary conditions of potential managerial opportunism.

Our Study Relative to Prior Work on the Antecedents of Product Recalls.

Practically, we offer insights about how changes in shareholder litigation risk, as a corporate governance mechanism, affect managerial behavior concerning a topic of particular relevance for both consumers and firm owners—product recalls. While UD laws are well-intended, our finding that they also reduce the likelihood of firms to recall products suggests unintended negative consequences of imposing less discipline on managers. In this regard, we contribute to the extant literature examining the effects of UD law adoption, which is equivocal on the governance implications for affected firms. To mitigate the potentially detrimental effects of UD law adoption on consumer welfare and the future viability of the firm, the implications of our study include suggested amendments to UD laws for legislators to consider to strengthen consumer protection, guidelines for public policy makers on how to evaluate new legislation, and recommendations for shareholders and consumer advocates on how to structure corporate boards and strategize around the ownership composition of the firm.

Conceptual Framework and Hypotheses

Agency Conflicts and Derivative Lawsuits

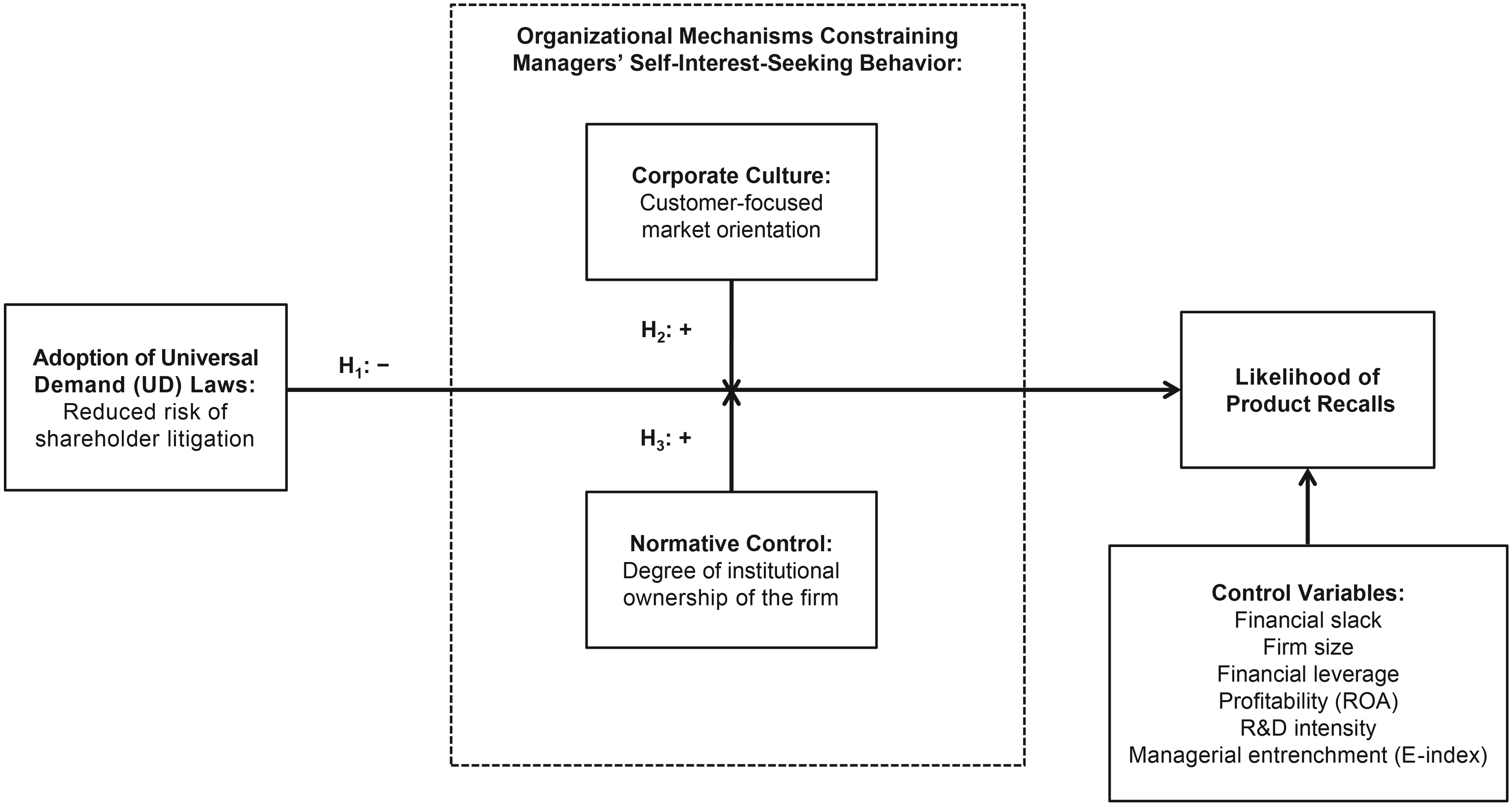

In developing our conceptual framework and corresponding hypotheses on how changes in managerial liability affect a firm's product recall decisions and the boundary conditions of this effect (Figure 1), we rely on arguments from agency theory (Jensen and Meckling 1976) and the business ethics literature (Husted 2007). Our point of departure is the observation that, in publicly listed firms, ownership and control are separated in that the former resides with the shareholders, whereas the latter resides with the managers appointed by the shareholders. This situation introduces the potential for agency conflicts, in which a firm's managers as agents do not act in the best interest of the firm's shareholders as principals, thus neglecting their fiduciary duties to the firm.

Conceptual Framework: Shareholder Litigation Risk and Product Recall Decisions.

To minimize such agency conflicts and to discipline managers, shareholders have a suite of governance mechanisms at their disposal, including the threat to file derivative lawsuits to sue managers on behalf of the firm and hold them personally liable for compensating the firm for any damage their behavior has allegedly caused (Bourveau, Lou, and Wang 2018). The relevance of derivative lawsuits as a corporate governance mechanism is highlighted in prior literature which finds that the incidence of derivative lawsuits is higher for firms where agency conflicts are more likely (Ferris et al. 2007). One instance in which shareholders might want to exercise their right to file derivative lawsuits is when they think that managers are putting the value of the firm at risk by pursuing their private interests instead of those of the firm. For example, this could be the case when managers are overly focused on the immediate instead of potential long-term consequences of their decision making.

In this regard, prior literature on “myopic management” explains that managers often have private incentives to emphasize current-term results at the expense of long-term performance (Mizik and Jacobson 2007). According to this stream of literature, managers might feel pressure to meet quarterly analyst earnings expectations, their job security might depend on short-term stock market reactions, or their performance might be assessed based on current-period accounting measures (e.g., Chung, Low, and Rust 2023). Together, these conditions can cause managers to rely heavily on strategic options that generate immediate results but put the future of the firm at risk, such as cutting discretionary expenditures on advertising and/or R&D (Graham, Harvey, and Rajgopal 2005; Mizik 2010).

We expect similar forces to be at play when managers decide whether to issue a product recall, in that they have incentives to avoid recalls to avert their short-term costs (Chen, Ganesan, and Liu 2009), but doing so might jeopardize the firm's long-term reputation and financial viability (Liu, Shankar, and Yun 2017). However, shareholders might try to keep managers in check and prevent the occurrence of managerial myopia through the threat of filing a derivative lawsuit, in which they hold managers personally liable for any damage that their behavior has caused to the firm (Bourveau, Lou, and Wang 2018).

Managerial Liability and Recall Decisions

Under some conditions, initiating a product recall could be beneficial for firms in the long run, for example by creating goodwill with customers and regulators when taking responsibility for product failures proactively (Ahluwalia, Burnkrant, and Unnava 2000; Dawar and Pillutla 2000) or by fostering organizational learning to prevent future mistakes (Haunschild and Rhee 2004). However, recalls themselves have numerous negative implications, which may motivate managers to “seek to avoid recalls when possible” (Mayo, Ball, and Mills 2022, p. 743). In particular, recalls are associated with damage to the firm's financial performance and market value (Chen, Ganesan, and Liu 2009) as well as sales losses (Cleeren, Van Heerde, and Dekimpe 2013). In addition, they involve the costs of repairing or replacing recalled items (Shah, Ball, and Netessine 2017), potential legal actions (Daughety and Reinganum 1995), and recall-related negative media coverage (Liu and Shankar 2015).

As these negative consequences of product recalls reflect badly on managers’ perceived skills—and thus their value in the market for managerial talent—they prefer not to be associated with them (Mayo, Ball, and Mills 2022). Moreover, the immediate costs of a recall means that managers might not be able to meet analyst earnings expectations or other key performance indicators linked to current-period accounting measures, therefore inducing a myopic tendency to try to avoid recalls as per the predictions of the myopic management literature (Chung, Low, and Rust 2023; Mizik 2010). While one could argue that the aforementioned potential positive aspects of a product recall in terms of organizational learning and/or customer and regulator goodwill could prevent managers from trying to avoid them, based on prospect theory, it is well-known that “losses loom larger than gains” when making decisions under risk (Kahneman and Tversky 1979). Hence, we expect that in a manager's mind, the potential (long-term) benefits of a product recall will not outweigh its (short-term) costs.

Nevertheless, while Chen, Ganesan, and Liu (2009) find that, in the short-term, stock markets may punish firms for recalling “too early,” Liu, Shankar, and Yun (2017) find that, in the long term, the negative effect of recalls are more pronounced for firms recalling “too late.” This pattern of findings can be explained by investors updating their beliefs of the impact of a recall on future cash flows over time and a correction of any under- or overreaction in the long run (Liu, Shankar, and Yun 2017). Indeed, the long-term damage to a firm of not recalling a product in terms of the opportunity costs of lost future sales due to impaired brand equity or regulatory fines can far exceed the short-term damage of a recall in terms of the associated immediate sales losses or costs to replace faulty items (Eilert et al. 2017). Hence, shareholders concerned about the long-term value of the firm might file a derivative lawsuit to hold managers personally liable for compensating the firm for the damage of trying to avoid a recall.

Against this backdrop, we argue that when deciding whether to issue a product recall, managers of publicly listed firms face a trade-off between (1) the private incentives to avoid its immediate costs and (2) the risk of being sued by shareholders for neglecting their fiduciary duties in terms of ensuring the long-term viability of the firm when doing so. We expect that the external shock of UD law adoption—which diminishes managers’ exposure to the threat of shareholder litigation—leads the incentives to avoid recalls to gain prominence in the aforementioned trade-off and come to dominate managerial decision making. This line of reasoning is supported by Liu, Liu, and Luo (2016), who document that CEOs often appear to act out of personal interest when making product recall decisions, leading to undesirable outcomes for consumers. We hypothesize:

Boundary Conditions of the Effect of UD Law Adoption

Given the argument that agency conflicts between shareholders and managers underlie managers’ opportunistic response to UD law adoption in terms of them trying to avoid product recalls, our investigation of the boundary conditions of this main effect will be guided by insights from prior literature on organizational mechanisms that can mitigate such agency conflicts. The business ethics literature distinguishes two main governance mechanisms to constrain the self-interest-seeking behavior of agents and reduce the occurrence of moral problems in organizations—corporate culture and normative control (Husted 2007). This literature considers corporate culture as a means for interest alignment and a solution for business ethics problems that operates by attempting to eliminate the underlying conflict of interest (Husted 2007). Normative control, in contrast, works by monitoring through a higher authority, which makes it harder for managers to hide the consequences of their actions from stakeholder scrutiny (Husted 2007), thus aligning the agent's behavior with the principal's objectives. A key distinction between these two solutions to agency conflicts is thus that the former relies on managers intrinsically wanting to do “the right thing,” while the latter is based on extrinsically forcing them to do so by means of formal accountability to a higher authority. Next, we discuss our expectations on how corporate culture, in terms of a firm's relative focus of its market orientation on customers versus competitors (Slater and Narver 1994), and the exercise of normative control, in terms of monitoring of a firm's managers by institutional investors (Bushee 1998), will shift the main effect of UD law adoption on product recall likelihood.

Corporate culture

A firm's market orientation describes its organizational culture in terms of the norms and behaviors that are prioritized while aiming to create ongoing superior performance (Narver and Slater 1990). The market orientation construct encompasses multiple dimensions, with the literature often juxtaposing a firm's customer orientation against its competitor orientation (Homburg, Grozdanovic, and Klarmann 2007). Day and Wensley (1988) argue that organizational success requires a balanced mix of a customer and competitor orientation, but they also state that, in practice, most firms tilt toward one or the other. Indeed, Slater and Narver (1994, p. 48) distinguish between firms having a customer focus and those having a competitor focus, depending on the relative emphasis of their market orientation.

In this regard, Deshpandé, Farley, and Webster (1993, p. 27) contend that “a competitor orientation can be almost antithetical to a customer orientation when the focus is exclusively on the strengths of a competitor rather than on the unmet needs of the customer.” Moorman and Day (2016) interpret a customer orientation as the belief that an organization should place customers’ interests first in every decision it makes. Since the fundamental purpose of a product recall is to protect customers and compensate them for the purchase of a faulty product (Liu, Liu, and Luo 2016), we expect that if a firm's market orientation has a stronger customer focus, this will weaken the extent to which a reduction in shareholder litigation risk induces an opportunistic response by managers in terms of them trying to avoid recalling a product as described in our H1.

This expectation is supported by recent finance literature arguing that corporate culture is relevant because managers often face choices that cannot be properly regulated in advance, noting that “corporate culture acts as a constraint” (Guiso, Sapienza, and Zingales 2015, p. 61). Based on a large-scale survey of U.S. executives, Graham et al. (2022) document that executives link corporate culture to a wide range of actions and decisions, including ethical choices around compliance and myopic behavior that boosts short-term stock prices at the expense of long-term value. Importantly, Graham et al. highlight a customer orientation as an important cultural value that firms can have, while Cravens and Guilding (2000) argue that the focus of a market orientation on providing superior customer value implies a long-term perspective. Hence, we expect that if a firm's market orientation has a stronger customer focus, the resulting corporate culture will constrain managerial myopia and the opportunistic tendency to try to avoid a product recall once it is harder for shareholders to sue managers for doing so, and thus weaken the main effect of UD law adoption. We hypothesize:

Normative control

We previously argued that the threat of filing a derivative lawsuit is a way for shareholders to try to impose discipline on managers and prevent myopic behavior that could damage the firm. However, this is not the only way that shareholders can intervene when they suspect that a firm's management is engaging in value-destructive actions. Another option to express dissent is using one's “voice” (Hirschman 1970). Shareholders can do so by raising issues in private discussions with management, submitting formal shareholder proposals, or voting against them at annual general meetings, with the threat to “exit” and sell their shares if managers do not listen, which could depress the firm's stock price. Managers are more likely to listen to shareholders whose voice is more salient because they have more power, such as institutions holding a substantial stake in the firm (Wies et al. 2019).

Indeed, the extant finance literature argues that institutional investors play an important monitoring function in corporate governance (Lin, Ma, and Xuan 2011), noting that such investors have the incentives and ability to monitor managers and, if necessary, intervene to safeguard the long-term value of the firm (Shleifer and Vishny 1986). In consideration of this, we expect that if institutional ownership of a firm is more pronounced, this will weaken the extent to which a reduction in shareholder litigation risk induces the managerial opportunism as described in H1. Institutional investors will be aware of the value-destructive effect of trying to avoid a recall (Eilert et al. 2017, p. 113) as they are more sophisticated and better informed than the average individual investor (Cheong, Hoffmann, and Zurbruegg 2021). Their monitoring will help ensure that managerial decision making is guided by considerations of the firm's long-term prospects instead of a myopic focus on meeting short-term earnings goals (Bushee 1998). Accordingly, we expect that if a greater proportion of a firm's outstanding stock is owned by institutions, the corresponding exercise of normative control will constrain managers’ opportunistic and myopic tendency to try to avoid a product recall once it is harder for shareholders to sue them for doing so, and thus weaken the main effect of UD law adoption. We hypothesize:

Method

Data Sources and Sample

We begin our data collection by considering all U.S. publicly listed firms included in the Compustat database between 1986 and 2018. The start of our sample period is motivated by having a control period before UD laws are adopted for the first time, with the earliest adoption taking place in the state of Georgia in 1989. The end of our sample period is motivated by the fact that the most recent UD law adoption took place in 2015 in the state of Louisiana, and we need to ensure that firms have had the opportunity to incorporate this change in the law in their managerial decision making.

UD laws are the result of a national initiative by the American Bar Association's Business Law Section to revise Subchapter D: Derivative Proceedings of the Model Business Corporation Act (MBCA) by adding a universal demand requirement (Lin et al. 2021). While not every state in the U.S. has adopted this provision for shareholders having to make a written demand to the board of directors before being able to file a derivative lawsuit, for those adopting it, it is the same. Web Appendix A provides an overview of which states adopted UD laws and in what year. At the end of the sample period, 25 out of 50 U.S. states had adopted UD laws. Note that a firm's state of incorporation determines whether it is subject to a UD law or not—the location of its shareholders is irrelevant. 2

The next step in our data collection is to obtain information on product recalls from the CPSC website and match the corresponding firms to those available in Compustat. 3 In total, we can match 1,442 product recalls made by 197 unique publicly listed firms for which we have complete data on all the control variables. Web Appendix B highlights the top 40 firms in terms of number of recalls, which together account for around three-quarters of the total number of recalls. Web Appendix B also distinguishes recalls without prior injuries or deaths from the overall sample. To do so, we hand-collect information from the recall descriptions about these events having occurred or not. For about 60% of the overall sample, namely 868 recalls, there are no prior injuries or deaths. This is where firms will have the greatest managerial discretion on whether or not to issue a recall, and from a theoretical perspective, this subset of recalls is therefore most appropriate for testing our hypotheses and will be the focus of our analyses. Note that this does not imply that the recalls we examine are inconsequential or that there is no risk of injury or death occurring if a recall would not be initiated. For example, our sample of recalls includes power mowers at risk of their blades breaking, potentially injuring users and bystanders, and recreational off-road vehicles whose steering wheel can separate, thus posing a crash hazard.

Following standard procedures in prior literature using the difference-in-differences (DiD) methodology to study product recalls (Kini, Shenoy, and Subramaniam 2017), we include in our analysis all firms from every two-digit Standard Industrial Classification industry in which there was at least one recall during the sample period. To ensure that we do not omit observations where there might have been a need for a product recall (i.e., an instance of a defective product) but the firm decided not to issue one, we also include all firms from industries in which, during the sample period, there was an incident report filed by consumers with the CPSC through its “Safer Products” website, indicating that they experienced an issue with an unsafe product. The final sample includes a total of 2,693 unique firms and 30,679 firm-year observations. 4

Measures

Dependent variable

Our dependent variable is PRODUCT_RECALL, which is an indicator variable that is equal to 1 if a firm announces a product recall in the current year, and 0 otherwise. If a firm has more than one recall in a given year, we treat these as a single observation. Accordingly, the 868 recalls mentioned previously result in 504 recall events in terms of PRODUCT_RECALL. Web Appendix C plots the evolution of PRODUCT_RECALL, indicating a peak in 2008, followed by a decline, which could be due to the passing of the Consumer Product Safety Improvement Act in that year. A robustness check shows that our baseline results are not driven by this legislation.

Moderator variables

The first moderator variable is the measure CUSTOMER_FOCUS, which reflects whether the market orientation of a firm focuses more on customers versus competitors. This measure is based on text analysis of firms’ 10-K reports as submitted to the Electronic Data Gathering, Analysis, and Retrieval system (EDGAR), using the validated dictionary from Zachary et al. (2011), as also employed in the recent work of Bhattacharya, Misra, and Sardashti (2019) and Srivastava, Kashmiri, and Mahajan (2023). Web Appendix D provides details on the operationalization of this measure. 5

The second moderator variable in our regressions is the measure INST_OWNERSHIP, which reflects the fraction of a firm's total outstanding common stock that is held by institutional investors. This measure is based on information from the Thomson Reuters Institutional (13F) Holdings database and is operationalized as per Cheong, Hoffmann, and Zurbruegg (2021).

Control variables

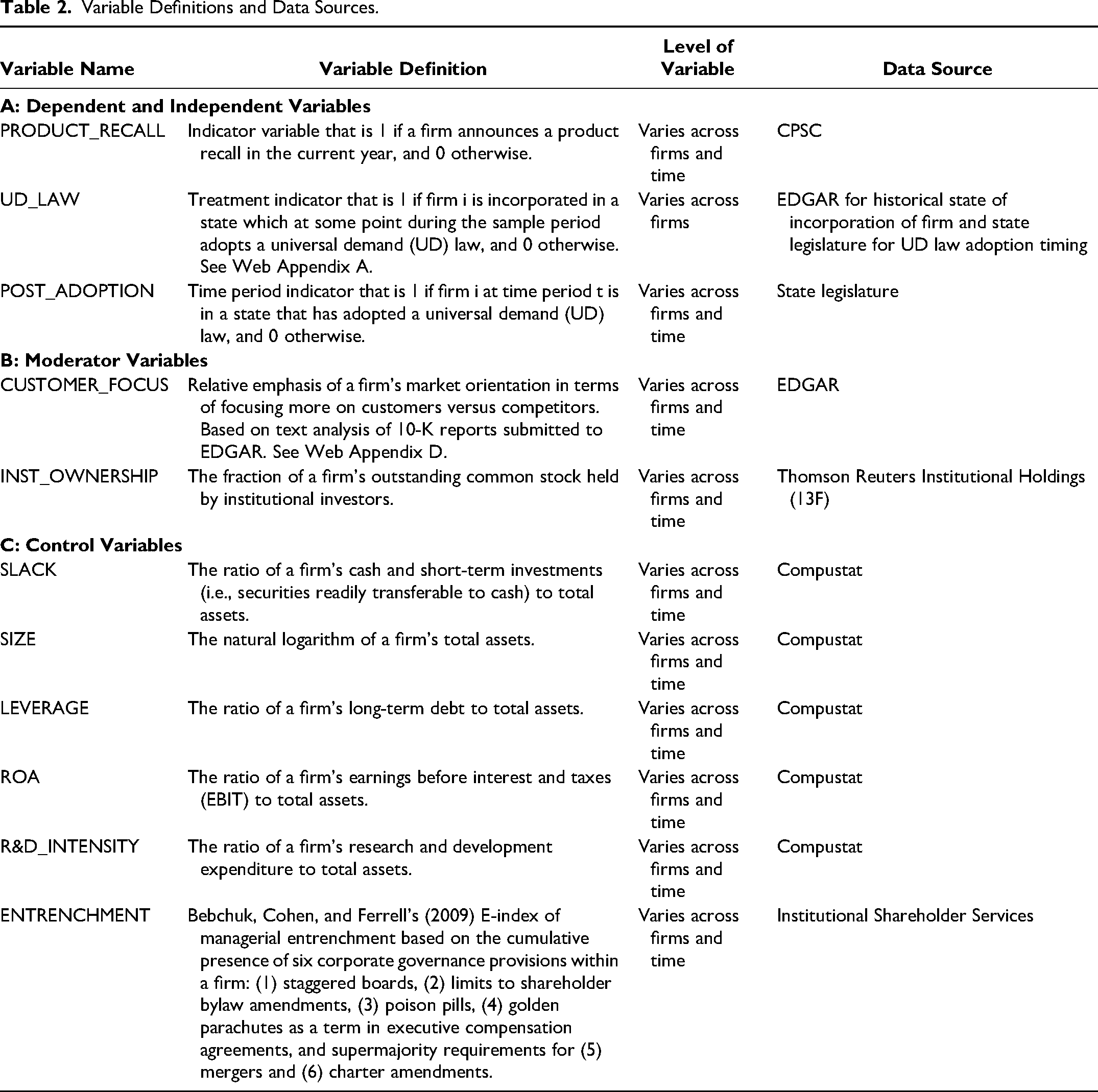

We include a set of commonly used control variables that could also influence firms’ ability and willingness to make a product recall to reduce the possibility of observing a spurious relationship between shareholder litigation risk and product recall likelihood. First, we control for financial slack (SLACK) to acknowledge that firms with more cash and securities that are readily transferable into cash have more financial resources to deal with the immediate costs of recalls (Kalaignanam, Kushwaha, and Eilert 2013). Second, we account for firm size (SIZE) as a measure of the financial resources that firms could mobilize to deal with the longer-term costs of product recalls (Kashmiri, Nicol, and Arora 2017). Third, we add firm leverage (LEVERAGE) as a control since greater financial leverage can decrease firms’ flexibility to invest in product safety initiatives (Kashmiri, Nicol, and Arora 2017). Fourth, we control for firm profitability through return on assets (ROA) given that firms with better financial performance are more likely to allocate resources to product reliability improvement (Kalaignanam, Kushwaha, and Eilert 2013). Fifth, we include R&D intensity (R&D_INTENSITY) as a control, as it has been argued to capture firms’ long-term investment in product quality (Kini, Shenoy, and Subramaniam 2017). Sixth, apart from moderating the effect of UD law adoption, institutional ownership could also have a direct effect on a firm's product recall likelihood because firms with higher institutional ownership score better on the product quality and safety dimensions of corporate social responsibility (CSR) ratings (Chen, Dong, and Lin 2020). Consistent with recent literature (Darby et al. 2023), we therefore control for institutional ownership in all our models. Finally, we control for a firm's corporate governance quality to capture the alignment of incentives between managers and shareholders, which could influence a firm's product recall decisions (Liu, Liu, and Luo 2016). Specifically, we include Bebchuk, Cohen, and Ferrell's (2009) E-index of managerial entrenchment (ENTRENCHMENT). This index refers to six governance provisions. As listed in Table 2, these provisions either provide managers with some form of protection from removal from the firm by placing constitutional limits on shareholder voting power, such as supermajority requirements, or reduce the financial consequences of being removed by including terms in executive compensation agreements, such as golden parachutes. The E-index is particularly relevant to include given Appel's (2019, p. 17) argument that its provisions “impede the ability of shareholders to exert governance in ways that may substitute for litigation rights.” Further, the E-index is negatively associated with pay-for-performance sensitivity (Fahlenbrach 2008) and, thus, the extent to which executive compensation is tied to the future value of the firm (Hartzell and Starks 2003), which could also influence recall decisions (Liu, Liu, and Luo 2016).

Variable Definitions and Data Sources.

While not applicable to our baseline analysis that focuses on determining the probability of a product recall occurring, we do include several recall characteristics as additional control variables when, in a robustness check, we examine if UD law adoption also impacts firms’ recall timing.

Table 2 defines the variables included in our analyses. Table 3 provides descriptive statistics and correlations, which are well below .8, mitigating multicollinearity concerns (Cleeren, Van Heerde, and Dekimpe 2013). 6

Descriptive Statistics and Correlations.

Notes: To facilitate interpretation, SIZE is reported in its original units before the log transformation (as described in Table 2). All descriptive statistics are at the firm-year level and for the full sample of 30,679 firm-year observations, with the exception of CUSTOMER_FOCUS, for which data is only available from 1994 onwards and which is thus based on 25,230 firm-year observations. All correlations that are not within parentheses are significant at p < .01 or better (two-tailed).

Identification Strategy

We follow Goldfarb, Tucker, and Wang’s (2022) guidelines about conducting research in marketing with quasi-experiments. In this section, we explain our identification strategy and verify that its underlying assumptions are satisfied. Our identification strategy relies on statewide differences in the adoption timing of UD laws, leading to differences in shareholder litigation risk across U.S. states. Accordingly, we rely on a staggered DiD approach. The staggered timing of the adoption of UD laws in different states offers the benefit of having control firms in states that either have not yet adopted the law or will never adopt the law. While our theoretical argumentation centers on the reduced threat of managers being sued by shareholders for failing their fiduciary duties as the underlying driver of the impact of UD law adoption on product recalls, as a “manipulation check” we note that prior literature also finds that the actual number of derivative lawsuits filed in states adopting UD laws declines significantly (Appel 2019; Chu and Zhao 2021; Lin, Liu, and Manso 2021). Importantly, while the adoption of UD laws per se might not be random, the timing of their adoption is (Goldfarb, Tucker, and Wang 2022, p. 4). Furthermore, Appel (2019, p. 20) demonstrates that UD law adoption does not affect firms’ incorporation choices. Accordingly, previous literature considers the staggered adoption of UD laws as an exogenous shock to litigation risk for managers of publicly listed firms (e.g., Bourveau, Lou, and Wang 2018; Huang, Ozkan, and Xu 2023; Manchiraju, Pandey, and Subramanyam 2021). 7

In the regression models of our DiD analysis, our explanatory variable of interest is the interaction term UD_LAW × POST_ADOPTION. UD_LAW is a treatment indicator that is equal to 1 if firm i is incorporated in a state that at some point during the sample period adopts a UD law, and 0 otherwise. Hence, control firms are those incorporated in a state that does not adopt a UD law at any time during the sample period. POST_ADOPTION is a time period indicator that is equal to 1 if firm i at time period t is in a state that has adopted a UD law, and 0 otherwise.

Before estimating our regression models, we present model-free evidence and explore the raw data to assess whether the quasi-experiment of the staggered adoption of UD laws appears to have an effect on the dependent variable, as per Goldfarb, Tucker, and Wang’s (2022) recommendation. In particular, we examine the variation in the mean value of the PRODUCT_RECALL variable between those firm-year observations that come from when firms are (vs. are not) exposed to UD laws. As expected, Table 4 shows that the recall likelihood PRODUCT_RECALL is significantly lower (at the 99% level of confidence) for the former compared with the latter group of firm-year observations.

Exploring the Raw Data: UD Law Adoption and Product Recalls.

***p < .01 (two-tailed).

Notes: Variable of interest is highlighted in bold. Reported statistics are at the firm-year level and for the full sample of 30,679 firm-year observations.

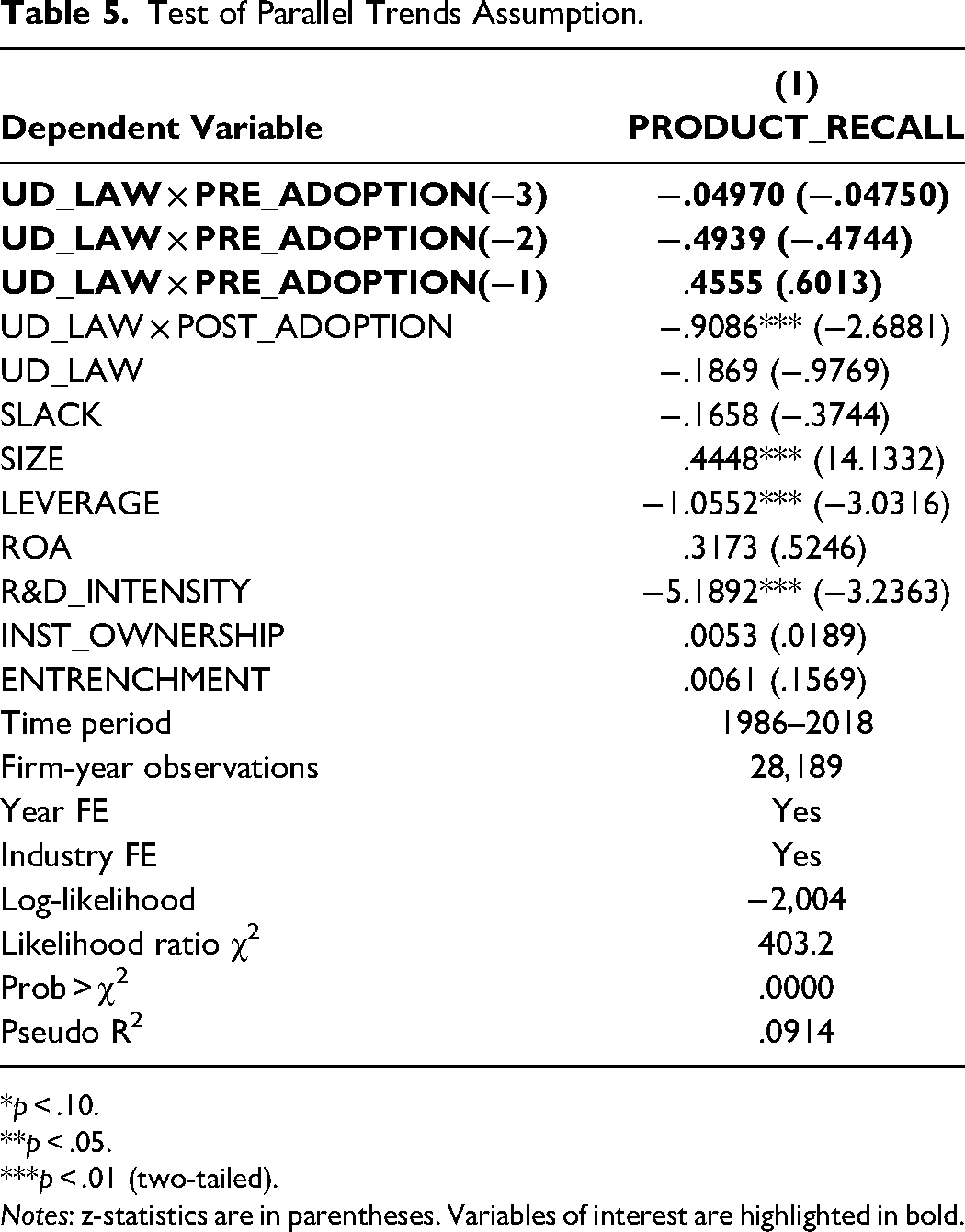

Next, the validity of our DiD approach requires that the parallel trends assumption is upheld (Goldfarb, Tucker, and Wang 2022). This assumption entails that the trends in the dependent variable for the treatment and control groups follow parallel paths prior to the treatment. In the context of our study, this means that we should find no systematic differences between treatment and control group firms in the likelihood of issuing product recalls before UD law adoption. To test this notion, we add three time period indicators to our model besides the POST_ADOPTION variable—one for each of the three years prior to when a state actually adopts a UD law, named PRE_ADOPTION(−3), PRE_ADOPTION(−2), and PRE_ADOPTION(−1), respectively. 8 To show that the change in PRODUCT_RECALL for the treatment and control group firms within the pretreatment regime does not exhibit different trends, we interact each of the PRE_ADOPTION time period indicators with the treatment group indicator UD_LAW. Evidence of a pretrend would reveal itself through any of these three interaction effects being significant. Table 5 shows no evidence of a pretrend, as none of the interaction effects between UD_LAW and the preadoption indicators is significant.

Test of Parallel Trends Assumption.

*p < .10. **p < .05. ***p < .01 (two-tailed).

Notes: z-statistics are in parentheses. Variables of interest are highlighted in bold.

Finally, our identification strategy is based on the assumption that, coinciding with the adoption of UD laws across different U.S. states, there was no systematic change in firms’ likelihood to recall products in those states independent of the introduction of these laws. To test this assumption, we conduct a falsification test as per Janakiraman, Lim, and Rishika (2018) to verify that our baseline results are not spurious. This test involves creating a group of placebo treatment firms by randomly assigning a firm's state of incorporation to another state (i.e., where the UD law adoption occurs at a different time), reestimating the regression models, saving the z-statistics, and repeating the exercise 1,000 times. If our results are driven by unknown state-based factors other than the UD law adoption, then the exercise using this “fake” group of treatment firms (Janakiraman, Lim, and Rishika 2018, p. 101) would still deliver a significant result. However, the histogram of z-statistics in Figure 2 shows that only in 31 out of the 1,000 cases, the z-statistic of this placebo test is the same or more negative than the actual z-statistic from when firms are assigned their correct state of incorporation, again supporting the validity of our DiD approach.

Falsification Test: Histogram of z-Statistic Distribution of Placebo Test.

Modeling and Estimation Approach

In our conceptual framework, we specify the relationship between the adoption of UD laws and the associated reduction in shareholder litigation risk and the likelihood of firms to issue a product recall and outline relevant boundary conditions of this relationship. To empirically assess this relationship, we rely on statewide differences in the adoption timing of UD laws and employ a staggered DiD approach. DiD approaches are an established identification strategy in marketing to overcome endogeneity concerns and establish causal effects in a quasi-experimental setting like ours (Goldfarb, Tucker, and Wang 2022). We implement our DiD approach by estimating a conditional logit panel model (Greene 2003). Conditional logit models, also known as fixed-effects logit models, are a useful framework to estimate binary panel regressions that account for unobservable characteristics within the data.

We control for unobservable time-variant factors by including year fixed effects (YEAR_FE), and we include industry fixed effects (INDUSTRY_FE) to control for unobservable time-invariant factors.

9

It is worth noting that it is not possible to include firm fixed effects because of the way our data is structured. That is, our sample includes a set of firms that never issue a recall but are in the same industries as the firms that do issue a recall. This implies that there is no variation, at the firm level, for these nonrecall firms in the dependent variable, and the firm fixed effects would thus be perfectly collinear with the dependent variable. For this reason, prior literature on product recalls with a comparable empirical setting as ours focuses on year and industry fixed effects (Kini, Shenoy, and Subramaniam 2017). We first estimate a panel regression model to examine the main effect of UD law adoption on the subsequent likelihood that firms issue product recalls (H1):

Next, following the reduced-form model approach of Schmitz et al. (2020),

11

we estimate a panel regression model to examine the interaction effects that constitute the two boundary conditions (H2–H3):

Results

UD Law Adoption and Product Recalls

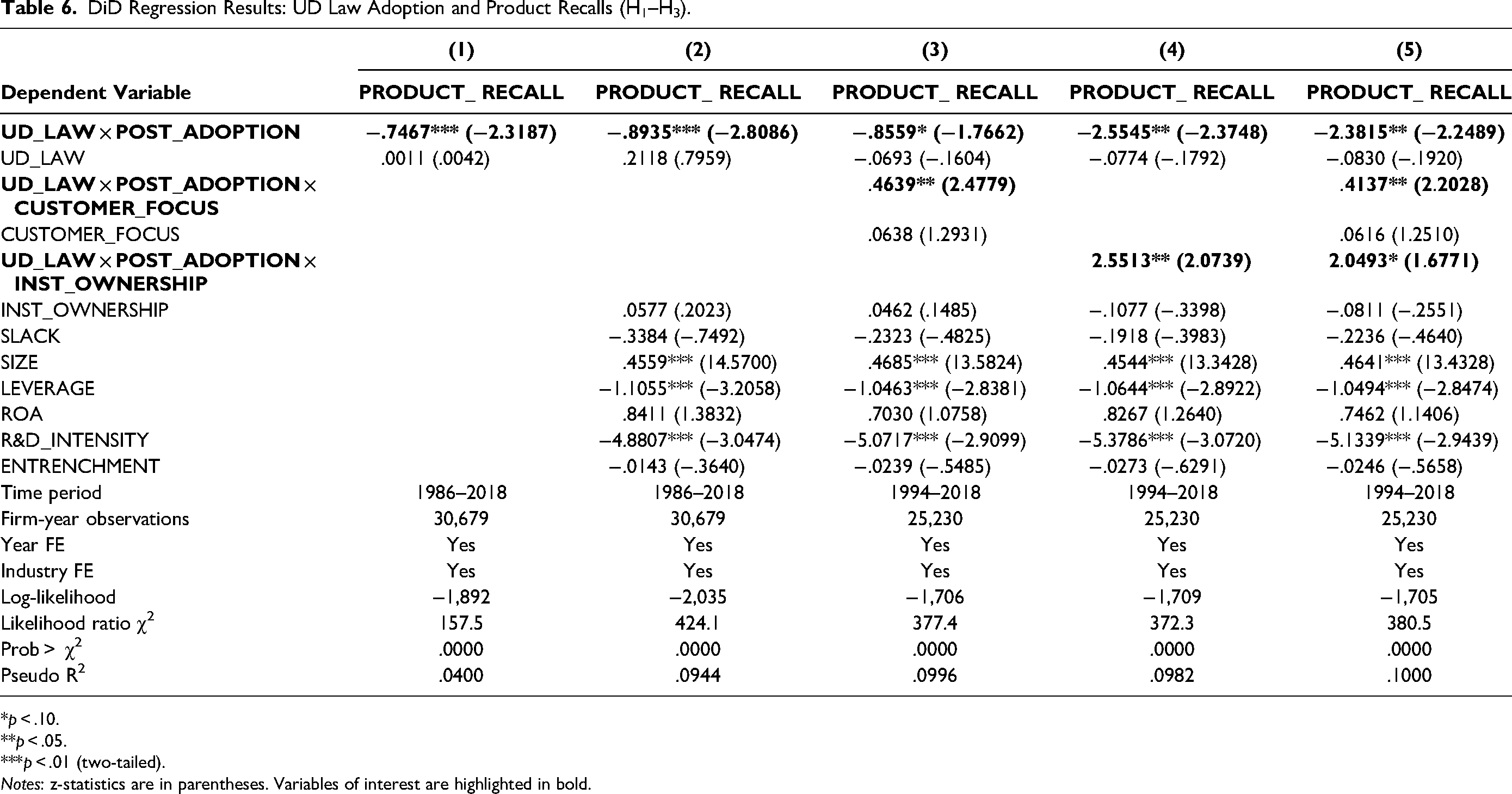

H1 predicts a negative association between the adoption of UD laws and the likelihood that firms will issue a product recall. We present the regression results of Equation 1 in Table 6. For robustness, Columns 1 and 2 show models without and with control variables, respectively. Across the alternative model specifications, the effect of UD_LAW × POST_ADOPTION on PRODUCT_RECALL is consistently negative and significant, supporting H1. For the economic interpretation of the results from these logit regressions, we focus on the odds ratio of the variable of interest. The odds ratio for the UD_LAW × POST_ADOPTION coefficient in Column 2 is .4093, implying that firms in UD law states are, on average, 29.04% less likely to announce a product recall relative to firms headquartered in states that have not adopted UD laws. 12 While the reduction in recall probability associated with the adoption of UD laws is sizeable in relative terms, the absolute change in probability is more modest given the low average base probability of any firm experiencing a product recall during the sample period (1.64%; see Table 3). However, as the consequences of trying to avoid a recall can be very serious for firms and consumers (Chen, Ganesan, and Liu 2009; Eilert et al. 2017), we document an important effect.

DiD Regression Results: UD Law Adoption and Product Recalls (H1–H3).

*p < .10. **p < .05. ***p < .01 (two-tailed).

Notes: z-statistics are in parentheses. Variables of interest are highlighted in bold.

In Web Appendix E, we show results for those recalls where there has been an injury or death reported prior to the recall announcement and find no effect of UD law adoption, consistent with our theoretical expectations. In Web Appendix F, we show that the baseline results are robust across different sample subperiods. Among others, we confirm that the negative impact of UD law adoption on a firm's product recall likelihood is not driven by the passing of the Consumer Product Safety Improvement Act in 2008. In Web Appendix G, we show that the baseline results are robust to using an alternative, continuous measure of the number of product recalls as the dependent variable, paired with an ordered logit panel model specification. Finally, in Web Appendix H, we show that UD law adoption also leads to a delay in recall timing, demonstrating the robustness of our quasi-experimental investigation by considering an alternative dependent variable as per the recommendations of Goldfarb, Tucker, and Wang (2022).

Boundary Conditions of the Effect of UD Law Adoption

We next move our attention to examining the boundary conditions of the effect of UD law adoption on product recall likelihood as per our H2 and H3. Note that as CUSTOMER_FOCUS relies on text analysis of firms’ 10-K reports, which are only widely available from 1994 when EDGAR electronic filing started (Asthana, Balsam, and Sankaraguruswamy 2004), the sample period and size available for testing the boundary conditions are smaller than those available for testing the baseline results. To address multicollinearity issues, in Columns 3 and 4 of Table 6 we first report regression results of models where we add each of the moderators separately, before presenting the results of the full model of Equation 2 in Column 5. While both moderator variables remain significant when they are included simultaneously, the significance levels are higher when each is included separately.

Corporate culture

H2 predicts that the negative association between the adoption of UD laws and firms’ likelihood to recall a product is weaker for firms whose market orientation focuses more on customers. In support of H2, the coefficient of the interaction term UD_LAW × POST_ADOPTION × CUSTOMER_FOCUS in Column 5 of Table 6 is both positive and significant. The positive coefficient indicates that the negative baseline effect of UD law adoption on the probability that a firm will recall a product is less pronounced when a firm's corporate culture prioritizes customer needs and interests. For an economic interpretation of this result, we examine the effect size of the moderator by generating average predicted probabilities across the sample distribution of the CUSTOMER_FOCUS variable. We calculate the difference in average predicted probabilities when changing the value of CUSTOMER_FOCUS from that representing the 25th percentile to that representing the 75th percentile. Moving from less to more customer-focused firms in this way reduces the impact of UD law adoption on product recall likelihood by 10.56%.

Normative control

H3 predicts that the negative association between the adoption of UD laws and firms’ likelihood to recall a product is weaker for firms with higher institutional ownership. In support of H3, the coefficient of the interaction term UD_LAW × POST_ADOPTION × INST_OWNERSHIP in Column 5 of Table 6 is both positive and significant. The positive coefficient indicates that the negative baseline effect of UD law adoption on the likelihood to recall a product is less pronounced when the normative control exercised through institutional investor monitoring is greater. For an economic interpretation of this result, we examine the effect size of the moderator by generating average predicted probabilities across the sample distribution of the INST_OWNERSHIP variable. We calculate the difference in average predicted probabilities when changing the value of INST_OWNERSHIP from that representing the 25th percentile to that representing the 75th percentile. Moving from firms with lower to higher institutional ownership in this way reduces the impact of UD law adoption on product recall likelihood by 10.01%.

As a final sensitivity analysis, we explore whether there are conditions where corporate culture and normative control do not just weaken the effect of UD law adoption on a firm's product recall likelihood, but can effectively “switch it off.” In this regard, we find that when the values of CUSTOMER_FOCUS and INST_OWNERSHIP are both at or above those representing the 90th percentile, the negative effect of UD law adoption on PRODUCT_RECALL is neutralized. However, note that due to the limited overlap of the distributions of CUSTOMER_FOCUS and INST_OWNERSHIP, only for 1.67% of all the firm-year observations, both cutoff levels are concurrently met. In other words, the effect of UD law adoption extends to almost all firms.

Examining Operational Improvement as a Potential Alternative Explanation

While we theorize that managerial opportunism driven by the decreased risk of being held personally liable by shareholders following the adoption of UD laws underlies our finding of a reduced recall likelihood, there could also be an alternative operational explanation—namely, an improvement in product quality. That is, it is possible that we observe a lower recall likelihood after UD law adoption because there is less need for recalls when shareholder litigation risk is reduced. This could be the case if the greater willingness of firms to innovate and invest in R&D after the adoption of UD laws as reported previously by Lin, Liu, and Manso (2021) would translate into improved product quality and thus reduce the likelihood of instances where products need to be recalled. Although in our regression models, we already control for firms’ R&D intensity—which has been argued to capture firms’ long-term investment in product quality (e.g., Kini, Shenoy, and Subramaniam 2017)—we now formally test for this alternative explanation as per the approach of Mayo, Ball, and Mills (2022).

In particular, we develop a continuous OPERATIONAL_IMPROVEMENT measure through text analysis of firms’ 10-K reports using Mayo, Ball, and Mills’s (2022) dictionary, which includes such phrases as “operational improvement,” “product improvement,” and “quality improvement” (full dictionary and operationalization are in Web Appendix I). According to these authors, a firm that more frequently mentions operational improvement phrases is more likely to experience an increase in product quality.

Next, we include OPERATIONAL_IMPROVEMENT as a control variable in all our regression models of Table 6 to check whether our previously reported results are robust. We also check if there is an interaction effect of UD_LAW × POST_ADOPTION with OPERATIONAL_IMPROVEMENT to examine whether the effect of UD law adoption on firms’ likelihood to recall is influenced by the aforementioned measure of operational improvement, which according to Mayo, Ball, and Mills (2022) would indicate that at least part of one's findings may be explained by an increase in product quality. The results in Column 1 of Table W9 in Web Appendix I do not support such an alternative explanation for our baseline results, as the negative effect of UD_LAW × POST_ADOPTION on PRODUCT_RECALL remains significant after the inclusion of the aforementioned variables, while the interaction term UD_LAW × POST_ADOPTION × OPERATIONAL_IMPROVEMENT itself is not significant. 13 The moderation effects also continue to hold, although significance is again higher when we examine them separately in Columns 2 and 3 instead of simultaneously in Column 4.

In sum, we do not find support for an alternative explanation of operational improvement and thus higher product quality driving our results. That is, it is unlikely that the documented effect of the reduced threat of managers being sued by shareholders on firms’ likelihood to recall is an artefact of a lower need for recalls instead of reflecting a lower willingness of managers to recall.

Sensitivity Analysis Addressing the Distribution of Recalls Across Firms

Finally, one might be concerned about our results being influenced by the fact that a few firms, such as Walmart, Target, and Home Depot, account for a substantial proportion of the number of recalls. Hence, as a sensitivity check, we exclude these top three recall firms—together accounting for 23% of all recalls—from our sample and reestimate our models. Table W10 in Web Appendix J confirms that our baseline results continue to hold, and so do the moderation effects when examined separately. When including both moderators simultaneously, the interaction effect of customer focus remains significant, while that of institutional ownership only just fails to reach significance at conventional levels (z-statistic = 1.62). In sum, we conclude that our results are generally robust.

Discussion

There has been substantial interest in the marketing literature for the consequences of product recalls for firms in terms of, for example, their reputation, stock market value, or sales (e.g., Chen, Ganesan, and Liu 2009; Eilert et al. 2017; Mafael, Raithel, and Hock 2022). However, so far, the marketing literature has paid only scant attention to the antecedents of product recalls in terms of the factors driving a firm's decision to recall in the first place, with the majority of existing studies in this regard being from the field of operations management (see Table 1 for an overview). However, it is important to also understand how nonoperational factors influence recall decisions, with Bendig et al. (2018) arguing that the extant literature lacks theory and evidence in this regard.

We answer the aforementioned call for research and add to the marketing literature by showing how external shocks in the form of legal changes affecting managers’ risk of being held personally liable by shareholders affect publicly listed firms’ decisions to recall. In doing so, we extend prior literature on the antecedents of product recalls that suggests that managerial opportunism can play a role in these decisions (Liu, Liu, and Luo 2016; Wowak, Mannor, and Wowak 2015) but that has not considered legal changes affecting managerial liability as a potential driver of recall decisions.

In particular, using a quasi-experimental DiD analysis, which helps determine the presence of a causal relationship (Goldfarb, Tucker, and Wang 2022), we find that when it is more difficult for shareholders to sue a firm's managers for alleged wrongdoings due to the adoption of UD laws, firms subsequently become less likely to recall products. Given that we theorize that agency conflicts underlie the observed myopic and opportunistic response of managers to UD law adoption, we draw from the business ethics literature to examine the moderating role of organizational mechanisms that can constrain the self-interest-seeking behavior of agents when assessing boundary conditions of the main effect. In doing so, we find that the effect of UD law adoption is weaker for firms whose corporate culture is characterized by a customer-focused market orientation, as well as for those that are subject to more normative control through monitoring by institutional investors.

Theoretical Implications

Drawing from agency theory and guided by a business ethics perspective, we broaden the theoretical dialogue in the literature on product recalls and shed light on the role of legal changes as an antecedent of a firm's decision to recall a product. Leveraging the insights from the aforementioned literature streams helps us better understand the potential trade-offs underlying managers’ decisions to issue recalls and the situations in which legal changes reducing the threat of them being sued for negligence by a firm's shareholders will have a differential effect on their decision making. While the existing marketing literature has focused on studying recalls after they were already decided on, we open up the “black box” and proverbially “look under the hood” of these impactful decisions by investigating why and when firms might decide to recall a product or not in the first place.

Our results documenting an opportunistic response by managers to a reduction in shareholder litigation risk imply that, going forward, the limited literature on recall antecedents should indeed move beyond investigating operational issues (Bendig et al. 2018, 20) and incorporate the insights from agency theory to better understand other drivers of these decisions—including factors related to the self-interest-seeking behavior of a firm's managers. At the same time, our findings show the relevance and importance of employing a business ethics perspective as a theoretical lens to increase our insights regarding the boundary conditions of the role of managerial opportunism in firms’ response to legal changes. In particular, doing so helped identify corporate culture and normative control as relevant moderators that weaken the negative effect of UD law adoption on product recall likelihood. Other research in marketing dealing with moral problems in managerial decision making (e.g., deceptive advertising) might also find our theoretical lens and the associated moderators useful to better understand the circumstances in which the tendency to engage in dubious marketing practices can be kept in check. Doing so is important, as the public exposure of such practices can induce a negative stock market response (Tipton, Bharadwaj, and Robertson 2009; Wiles et al. 2010).

Our results also have implications for the literature on myopic marketing management, which to date has focused on examining the effect of managerial short-termism on unexpected budget cuts to advertising and R&D (e.g., Chung, Low, and Rust 2023; Mizik 2010). This stream of literature should consider broadening its scope to also examine other variables of interest to the marketing function and of importance to consumers, such as product recalls. At the same time, research on UD law adoption might also examine aforementioned budget cuts as a relevant outcome variable. Furthermore, our observation that having a market orientation with a customer focus can be an antidote to managerial myopia around recall decisions not only is encouraging for the marketing literature by signaling the importance of the marketing function within the firm (Verhoef and Leeflang 2009) but also suggests that the relative emphasis of a firm's market orientation (Slater and Narver 1994, p. 48) is a relevant variable to explore in future research on myopic management.

Finally, our results add to the ongoing debate in the finance literature on the governance implications of UD law adoption (Lin, Liu, and Manso 2021; Lin et al. 2021). In particular, we provide further nuance to the question if and when changes in shareholder litigation risk as a governance mechanism might benefit or harm the firm (Chu and Zhao 2021). Indeed, while “an overemphasis to play it safe” by managers to avoid a derivative lawsuit (Kinney 1994, p. 175) might be detrimental from a corporate innovation perspective (Lin, Liu, and Manso 2021), our findings suggest that, all else equal, doing so might actually be beneficial from a consumer protection perspective—consistent with previous observations regarding the effect of UD law adoption on employee safety (Lin et al. 2021).

Practical Implications

Trying to avoid a product recall can harm both a firm's customers and its shareholders. Recently, this was illustrated when Peloton finally announced a recall of its treadmills, reversing course just weeks after saying there was “no reason” to stop using their exercise machines (Reuters 2021). Upon Peloton's eventual recall announcement, its shares fell as much as 15.8% and multiple customers had been injured, with one child reported to have died in an accident with one of their machines. CEO John Foley was forced to admit that “Peloton made a mistake in our initial response to the CPSC's request that we recall the Tread+,” adding that “We should have engaged more productively with them from the outset. For that, I apologize.” Security analyst Youssef Squali noted, “This recall will likely result in significant near-term one-time financial costs and operational disruption, with potential reputational damage” (Reuters 2021). Indeed, another major news outlet revealed that the recall and how Peloton handled it would reduce its sales by about $165 million (Gurman and Bloomberg 2021). Given these negative consequences of trying to avoid recalls, increasing our understanding of the antecedents of these decisions is practically relevant. Our findings on the role of changes in shareholder litigation risk as a corporate governance mechanism have several implications, offering insights for legislators, public policy makers, consumer advocates, and the firm's shareholders.

First of all, it is important for these stakeholders to realize that while UD laws are well-intended, our finding that their adoption is associated with a reduction in product recall likelihood suggests unintended negative consequences of this legal change, which imposes less discipline on a firm's managers. If a reduced risk of being held liable results in managers being more likely to try to avoid product recalls to avert their immediate costs, this can both harm consumer welfare and impair the long-term viability of the firm, as illustrated recently by the Peloton case. To enhance consumer protection in the near term, a case could therefore be made for overhauling UD laws to allow shareholders to claim demand futility when bringing a lawsuit that concerns consumer safety. Demand futility enables shareholders to avoid the demand requirement if they can allege with particularity that demand will be futile because the directors have a conflict of interest, and this was a way to circumvent the demand procedure prior to the adoption of UD laws (Erickson 2017).

More generally, our findings suggest a need for public policy makers to take a more holistic view when considering and implementing legal changes. Legislators in charge of revising corporate law should coordinate with regulators in charge of consumer protection to determine the possibility of the kind of unintended consequences that our study documents and develop mechanisms to prevent damage to consumers and/or firms. The field of evaluation science could provide lessons for how policy makers should evaluate new legislation and try to predict its potential implications, including unintended and/or undesirable ones. For example, Oliver, Lorenc, and Tinkler (2020) recommend the use of a broad range of methods to explore how policies could play out, use theory to plan evaluations, and discuss both methods and theory with relevant stakeholders to make these as useful as possible. These authors also note that adverse unintended consequences of well-intentioned policies can induce strong emotional reactions among policy makers, which can lead to pressure to ignore inconvenient evaluation findings. Hence, it is important to ensure high-level political support when planning the evaluation of legal changes and the remediation of potential unintended consequences.

Consistent with these insights from academia, best practice principles for regulatory impact assessment by the Organization for Economic Cooperation and Development (2019) stress the importance of identifying all groups of stakeholders who could be impacted by proposed new legislation, assessing potential disproportionalities in these impacts, and leveraging insights from behavioral economics to try to predict how outcomes can differ from those expected. Here, the strategic use of decision-making approaches such as dialectical inquiry and devil's advocacy could help challenge one's assumptions and incorporate different perspectives (Schweiger, Sandberg, and Rechner 1989).

Next, the moderators included in our analyses provide practical insights on the boundary conditions of the extent to which a firm's managers might respond opportunistically to changes in the incentives to recall a product as associated with a reduction in the risk of being held personally liable by shareholders. In particular, it is relevant for consumer advocates as well as firm shareholders to know that for firms with a greater customer focus, the negative effect of UD law adoption on product recall likelihood is attenuated. This result implies that it would be in the best interest of these stakeholders to raise the issue of a firm's customer focus at annual general meetings and in private discussions with management. In support of this notion, customer-related issues are beginning to be incorporated in risk assessments and environmental, social, and governance scores by credit rating agencies, with Fitch Ratings (2022) recently stating that “evolving regulations are accelerating the materiality of several customer-related issues, including customer welfare [and] product safety.” This finding also has implications for how corporate boards ought to be structured. Specifically, given Kashmiri, Nicol, and Arora’s (2017) observation that greater marketing department power increases a firm's customer orientation, and our finding that a customer-focused market orientation helps restrain managerial opportunism regarding recall decisions, it is important to create awareness among board members about the benefits of appointing marketing executives to the board, such as a chief marketing officer.

Finally, our other finding that normative control in terms of monitoring by institutional investors reduces an opportunistic response of managers to the adoption of UD laws suggests that aforementioned stakeholders should try to convince institutions to take a meaningful ownership stake in the firm, which both motivates them to invest resources in monitoring managers and makes such monitoring more impactful (Benton 2019; Bushee 1998). Investor relations consulting firms can assist in attracting the desired type of institutional investors that can mitigate agency problems between firm owners and managers (Bushee and Noe 2000, p. 172). Recognizing that investor relations is about marketing the firm (Hanssens, Rust, and Srivastava 2009; Hoffmann, Pennings, and Wies 2010), such consultants can help establish and maintain relationships with high-quality institutional investors (Rose and Co. 2022).

Conclusion and Limitations

Although we open up a new area of research in the marketing literature by focusing on legal changes as an antecedent of a firm's product recall decisions, our type of study has some inherent limitations that warrant discussion. In particular, we relied on archival evidence to show how the likelihood to recall products changes in response to a firm's managers becoming less likely to be held personally liable by shareholders. While we examined several boundary conditions of the effect of such changes in managerial liability on recall decisions, we ultimately only observed the eventual outcomes of managers’ decision-making process in terms of a firm recalling a product or not. To increase our understanding of the underlying process of these decisions, future work could build on our quantitative approach by means of a qualitative approach (e.g., in-depth case studies). Moreover, while our empirical evidence regarding the moderator variables is consistent with agency problems underlying the main effect of UD law adoption on product recall likelihood, there could also be other reasons driving this relationship, and we should note that our current work neither aims nor claims to be able to fully explain the mechanism underlying the main effect of UD laws.

Furthermore, data availability limitations prevented us from including some variables in our analysis. For example, executive compensation structure in terms of the extent to which managers are paid in cash versus equity influences the alignment of their objectives with those of shareholders and could thus affect their product recall decisions (Liu, Liu, and Luo 2016). While this information is available from ExecuComp, that database only covers the subset of large firms included in the S&P 1500 index, which excludes 72% of the recalls in the CPSC database during our sample period, introducing sample selection concerns. Furthermore, since ExecuComp only started to cover the compensation structure of this subset of firms from 1994 onward, relying on it would also have meant that we would not have been able to cover the entire period of UD law adoption in our baseline analysis, which ranges from 1989 to 2015. However, we were able to include the E-index as a corporate governance measure that does not suffer from these limitations and that proxies for executive compensation structure given its known correlation with pay-for-performance sensitivity (Fahlenbrach 2008). 14

Similarly, a firm's concern for the interests of a broader group of stakeholders as captured by its CSR performance (Peloza and Shang 2011) could also affect managerial opportunism regarding product recall decisions. While this information is available from the Kinder, Lydenberg, and Domini (KLD) database, which starts in 1991, the overlap with the firms included in our sample is even more limited than for the ExecuComp database, because for the first ten years, KLD only covered S&P 500 firms. However, as both the E-index (Jo and Harjoto 2012) and institutional ownership (Chen, Dong, and Lin 2020) correlate with a firm's KLD score, our set of control variables already includes proxies for CSR. Furthermore, our customer focus measure should pick up at least part of a firm's commitment to CSR, given the positive correlation between customer orientation and CSR reported in prior literature (Korschun, Bhattacharya, and Swain 2014).

Finally, one could argue that, ideally, we would only have used observations in our analysis where there are defective products to begin with and thus an identified need for a recall. However, while we were able to prevent our sample from omitting such observations, it was not possible to exclusively rely on them, because the CPSC's Safer Products website only tracks consumer incidents from 2011 onward, and there has only been a single UD law adoption since (in Louisiana in 2015), rendering the aforedescribed analysis unviable. Ultimately, the change in our dependent variable could thus reflect a combination of a change in the need for a recall and the willingness of a firm to recall a defective product. However, our analysis on operational improvement and thus higher product quality (as per Mayo, Ball, and Mills [2022]) did not support a theory of the need for product recalls explaining our results.

Supplemental Material

sj-pdf-1-jmx-10.1177_00222429241231236 - Supplemental material for So, Sue Me…If You Can! How Legal Changes Diminishing Managers’ Risk of Being Held Liable by Shareholders Affect Firms’ Likelihood to Recall Products

Supplemental material, sj-pdf-1-jmx-10.1177_00222429241231236 for So, Sue Me…If You Can! How Legal Changes Diminishing Managers’ Risk of Being Held Liable by Shareholders Affect Firms’ Likelihood to Recall Products by Arvid O.I. Hoffmann, Chee S. Cheong, Hoàng-Long Phan and Ralf Zurbruegg in Journal of Marketing

Footnotes

Acknowledgments

The authors thank the JM review team for their thoughtful guidance and constructive feedback that strengthened the paper. The authors also thank Dominique Hanssens, Sascha Raithel, Armando Corsi, Alex Belli, Alison Joubert, and Beatriz Pereira as well as seminar participants at Maastricht University, UNSW Sydney, the 2022 UNSW/USYD/UTS Joint Marketing Research Forum, Victoria University Wellington, La Trobe University, the University of Missouri–Columbia, Freie Universität Berlin, Monash University, the Stevens Institute of Technology, and the University of Groningen for helpful comments that improved the paper.

Coeditor

Vanitha Swaminathan

Associate Editor

S. Sriram

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research has been partly funded by the University of Da Nang, School of Economics.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.