Abstract

A bankrupt buyer firm's interactions with its suppliers during bankruptcy have critical implications for both parties and for the broader economy, yet these interactions remain poorly understood. The authors build on research on buyer–supplier relationship dynamics to demonstrate that accommodative and exploitative velocities—the rate and direction of change in the corresponding acts—serve as signals affecting bankruptcy survival. They show how signal characteristics (i.e., the variability in accommodative and exploitative acts) and signaler characteristics (i.e., whether the party undertaking the acts is the buyer or its suppliers) moderate the impact of accommodative and exploitative velocities on bankruptcy survival. Study 1 examines the bankruptcy survival outcome of 310 U.S. bankruptcies over 14 years and finds that a 1% increase in accommodative (exploitative) velocity increases (decreases) the buyer's survival by 39% (33%). Further, variability in accommodative acts weakens their effect, and suppliers' (vs. the buyer's) accommodative and exploitative velocities are less deterministic of the buyer's bankruptcy survival. Study 2 uses a scenario-based experiment to shed light on the mechanism underlying the impact of the two velocities on bankruptcy survival. The findings from both studies demonstrate the key role played by buyer–supplier interactions in a buyer's bankruptcy survival.

Keywords

In March 2023, 548 U.S. firms filed for bankruptcy, 1 a year-on-year increase of 79% from the same month in 2022 (American Bankruptcy Institute 2023). A firm declaring bankruptcy seeks a fresh start by reorganizing—typically, negotiating a debt reduction and/or delayed payment to its creditors—in the shortest amount of time while continuing its business operations (Jindal 2020; Sutton and Callahan 1987). A failure to emerge quickly from bankruptcy hurts not only the debtor-buyer firm but also its creditor-suppliers. Suppliers 2 experience a loss of future revenue and of any relationship-specific investments they may have made, and they bear the cost of finding new buyers (Jindal 2020). In extreme cases, suppliers may be forced to follow their buyer and file for bankruptcy (Pearce and Lipin 2012). Emerging buyers support nearly 28,000 jobs and generate $1.75 billion annually in additional gross domestic product (Druin and Allgrunn 2014). Thus, the likelihood of the buyer's emergence from bankruptcy and its duration in bankruptcy—collectively referred to as bankruptcy survival (Elayan and Meyer 2001; Jindal 2020)—have critical implications for the bankrupt buyer, its suppliers, and the economy at large.

A buyer is keenly aware of the key role its suppliers play in ensuring its bankruptcy survival. Consider the bankruptcy announcement of U.S.-based paper manufacturer Verso Corporation (2016): Today's announcement will have virtually no impact on Verso's day-to-day operations. In turn, we will continue to rely on all of our suppliers. … Amounts owed as of the petition filing date will be settled as part of the company's Plan of Reorganization, and Verso is committed to completing this process as efficiently as possible. … Verso sincerely regrets any near-term hardships its suppliers experience as it works through its restructuring and hopes that its suppliers ultimately will obtain longer-term benefits through a continued relationship with the company. (Italics added for emphasis)

Over the course of the negotiation, the buyer and its suppliers signal their intent by engaging in accommodative acts—behaviors that are intended to allow for or cater to the counterpart's needs (Bello, Katsikeas, and Robson 2010; Cannon and Homburg 2001; Noordewier, John, and Nevin 1990)—and exploitative acts—behaviors that are intended to deny the needs of, extract concessions from, or make demands of the counterpart (Bello, Katsikeas, and Robson 2010; Frazier and Summers 1986; Narayandas and Rangan 2004). 3 Whereas accommodative acts by one party signal to its counterpart the former's intent to cooperate, exploitative acts indicate that the acting party is competitive in its intent (Bello, Katsikeas, and Robson 2010; Montoya-Weiss, Massey, and Song 2001).

Because individual acts by a party provide “an incomplete picture of the signaling phenomenon” (DeKinder and Kohli 2008, p. 84), the counterpart could dismiss them as less credible, one-off events. Indeed, prior marketing research has acknowledged that “relationships between firms evolve over time and are fundamentally dynamic” (Palmatier et al. 2013, p. 13). Decision makers are posited to consider the series of past acts undertaken by their counterpart, infer trends from these multiple acts, and extrapolate these trends into the future, assuming that the acts will continue (Johnson, Tellis, and MacInnis 2005). Building on this notion of information being clearer in trajectories of acts rather than individual acts (Palmatier et al. 2013), we define “accommodative velocity” as the rate (i.e., magnitude) and the direction of change (i.e., whether increasing or decreasing) in a party's accommodative acts over time (Schmitz et al. 2020). Similarly, “exploitative velocity” is the rate and direction of change in a party's exploitative acts over time. We posit that, relative to individual acts, a party's accommodative and exploitative velocities provide a clearer signal of its intent. Yet, their impact on the buyer's bankruptcy survival remains unknown. Thus, the first question we answer is: How do the accommodative and exploitative velocities of a bankrupt buyer and its suppliers impact the buyer's bankruptcy survival?

Inferring a counterpart's intent from its behaviors is inherently ambiguous. Consequently, the impact of parties’ accommodative and exploitative velocities on the buyer's bankruptcy survival may be subject to significant heterogeneity. Building on signaling theory, we identify signal and signaler characteristics (Connelly et al. 2011; Gomulya and Mishina 2017) that likely explain this heterogeneity. We ask: How do signal and signaler characteristics strengthen or weaken the impact of accommodative and exploitative velocities on the buyer's bankruptcy survival? Specifically, we hypothesize variability in acts (the extent to which the parties’ acts diverge from their mean acts; a signal characteristic) (Luo, Raithel, and Wiles 2013; Schmitz et al. 2020) and signaler identity (whether the signaler is the buyer or its suppliers) to moderate the effects of accommodative and exploitative velocities on the buyer's bankruptcy survival.

We test our hypotheses using a two-study multimethod design. Our findings contribute to marketing theory and practice in three ways. First, we demonstrate the influence of parties’ accommodative and exploitative velocities on the buyer's bankruptcy survival. In doing so, we contribute to the limited yet growing literature on buyer–supplier relationship dynamics. Study 1 uses a sample of 310 bankruptcies filed in the United States in three industries from 2001 to 2014. We classify as accommodative or exploitative nearly 10,000 motions filed in bankruptcy courts by bankrupt buyers and their suppliers, accounting for the significant variation in the intensity that is inherent to both types of acts. 4 We find that a 1% increase in accommodative velocity boosts the buyer's bankruptcy survival by 39%; a similar 1% increase in exploitative velocity suppresses bankrupt buyer's survival by 33%. Study 2—a scenario-based experiment—sheds light on the mechanism underlying these two main effects. We report evidence consistent with the notion that a party (1) infers its counterpart's behavioral intent from the latter's velocity of acts and (2) expects this intent, based on the act velocity, to persist in the future. Together, the studies emphasize the critical role played by the dynamic interactions between a buyer and its suppliers in predicting performance outcomes (Palmatier et al. 2013). Our emphasis on relationship trends acknowledges managerial agency in influencing outcomes, thereby extending research on relationship dynamics past its focus on path-dependent relationship stages (Chmielewski-Raimondo et al. 2022; Shamsollahi et al. 2021).

Our second contribution lies in examining buyer's interactions with its suppliers during bankruptcy. Despite the pivotal role that buyer–supplier interactions play in the bankruptcy process, the academic literature remains largely silent on this topic. Instead, this literature has focused on how a firm's state before it filed for bankruptcy determines its survival. Characteristics such as solvency risk (Bryan, Tiras, and Wheatley 2002), firm size (Denis and Rodgers 2007; Moulton and Thomas 1993), debt levels, and marketing expenses (Jindal 2020) have been shown to affect the buyer's bankruptcy survival (see Table 1). We add to this literature by demonstrating that the interactions between the buyers and their suppliers during bankruptcy can impact the buyer's survival and thus bridge the gap between theory and practice.

Representative Multidisciplinary Research on Bankruptcy Survival.

Our third contribution arises from our integration of signaling theory and the relationship dynamics literature in marketing. Academics have, for the most part, leveraged signaling theory to examine signals of quality (Bhattacharya, Morgan, and Rego 2022; Kirmani and Rao 2000; Spence 1973). Our research extends the theory by examining parties’ signals of intent (Connelly et al. 2011). We further identify signal and signaler characteristics (variability in acts and identity, respectively) that moderate the relationship between accommodative and exploitative velocities and bankruptcy survival. We find that at high (low) levels of variability in acts, a 1% increase in accommodative velocity increases bankruptcy survival by 37% (40%). Furthermore, a 1% increase in suppliers’ accommodative velocity raises bankruptcy survival by 32%; yet, a similar 1% increase in the buyer's accommodative velocity enhances bankruptcy survival by 39%. Buyers’ acts also dominate suppliers’ with respect to exploitative velocity, lowering bankruptcy survival by 33% relative to the 28% lower bankruptcy survival attributable to suppliers’ exploitative velocity. The characteristics of the signal and that of the signaler are thus vital in moderating the effects of intent signals.

The following section presents our conceptual background and hypotheses. We then describe Studies 1 and 2 and discuss their results. We conclude with the implications and limitations of our research and offer directions for future research.

Conceptual Background

The Simultaneous Incentives for Making and Seeking Concessions

A buyer's bankruptcy filing represents a significant disruption to its relationship with its suppliers—a key class of creditors (Schmitz et al. 2020). Only if and when the suppliers approve the buyer's debt reorganization plan can the buyer resume business-as-usual operations (i.e., without the oversight of a bankruptcy court) and repay the suppliers (Jindal 2020; see Web Appendix A on the U.S. bankruptcy process). Mindful of its goal of resuming normal operations, the buyer is incentivized to cooperate with its suppliers. For their part, suppliers are cognizant of their potential loss in sales and that they are likely to recover only cents on the dollar if the buyer were to go out of business (Yang, Birge, and Parker 2015), and they therefore make concessions. Both parties thus have the incentive to accommodate (i.e., cooperate with) each other during bankruptcy.

Bankruptcy filing affords the buyer the leeway to continue operating its business, thereby adding value for its stakeholders, including suppliers. The cooperation of the buyer and its suppliers underlies the cocreated value of their relationship during and after bankruptcy. The persistence of this value throughout the bankruptcy process, and the incentives for both parties to accommodate each other, make bankruptcy a non-zero-sum game.

Yet, competing interests are also present. The buyer seeks to renegotiate the repayment terms with its suppliers in order to reduce payments and lengthen the time between payments. Suppliers, antithetically, seek debt recovery as early as possible (Yang, Birge, and Parker 2015). The simultaneous existence of the incentive to make and seek concessions (i.e., pursue the counterpart's and one's own interests, respectively) drives each party—the buyer and its suppliers—to undertake both accommodative and exploitative acts.

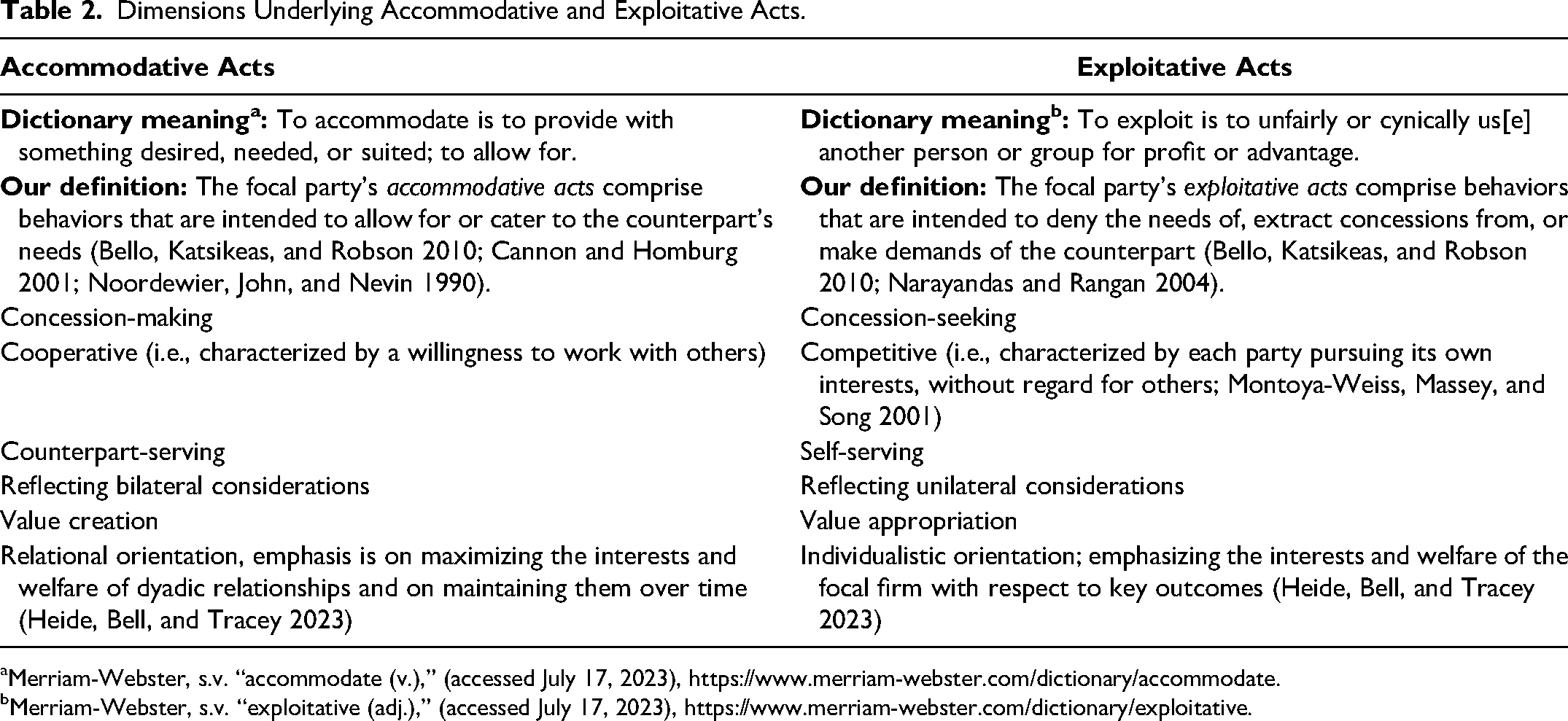

Our discussions with bankruptcy experts and a review of the interorganizational literature yield several dimensions on which accommodative and exploitative acts may differ (see Table 2). Accommodative acts are intended to serve the counterpart by making concessions, reflect the value-creation objective to cocreate value, demonstrate a willingness to work with the counterpart, and emphasize bilateral considerations and a relational orientation. In contrast, exploitative acts are intended to serve the focal party by seeking concessions, reflect value-appropriation objectives and an effort to gain something, and emphasize unilateral considerations and an individualistic orientation. Whereas accommodative acts are other-interest emphasizing, exploitative acts emphasize self-interest even at the expense of the counterpart. Importantly, neither party needs to undertake accommodative acts and exploitative acts to the same extent. Both types of acts range in intensity—the extent to which they emphasize interests of the relationship versus the self. Table W1 in Web Appendix B displays the accommodative and exploitative acts undertaken by the buyer and its suppliers during bankruptcy along with the expert-adjudicated intensity of each act.

Dimensions Underlying Accommodative and Exploitative Acts.

Merriam-Webster, s.v. “accommodate (v.),” (accessed July 17, 2023), https://www.merriam-webster.com/dictionary/accommodate.

Merriam-Webster, s.v. “exploitative (adj.),” (accessed July 17, 2023), https://www.merriam-webster.com/dictionary/exploitative.

The Impetus for Signaling

Because the bankruptcy process requires the buyer and its suppliers to interact with each other via motions filed in the bankruptcy court, each party provides information to its counterpart by undertaking acts that indicate its intentions, motives, or goals (Porter 1980)—that is, by signaling its intent via its behaviors (Stiglitz 2000). The counterpart must, in turn, infer the acting party's intent—cooperative or competitive—from the latter's accommodative and exploitative acts, respectively, undertaken over time. Accommodative acts signal a cooperative intent by making concessions to the counterpart. In contrast, exploitative acts signal a competitive stance, with the signaler emphasizing its intent to seek concessions emphasizing its own interests, even if such concessions may not be in the interests of its counterpart.

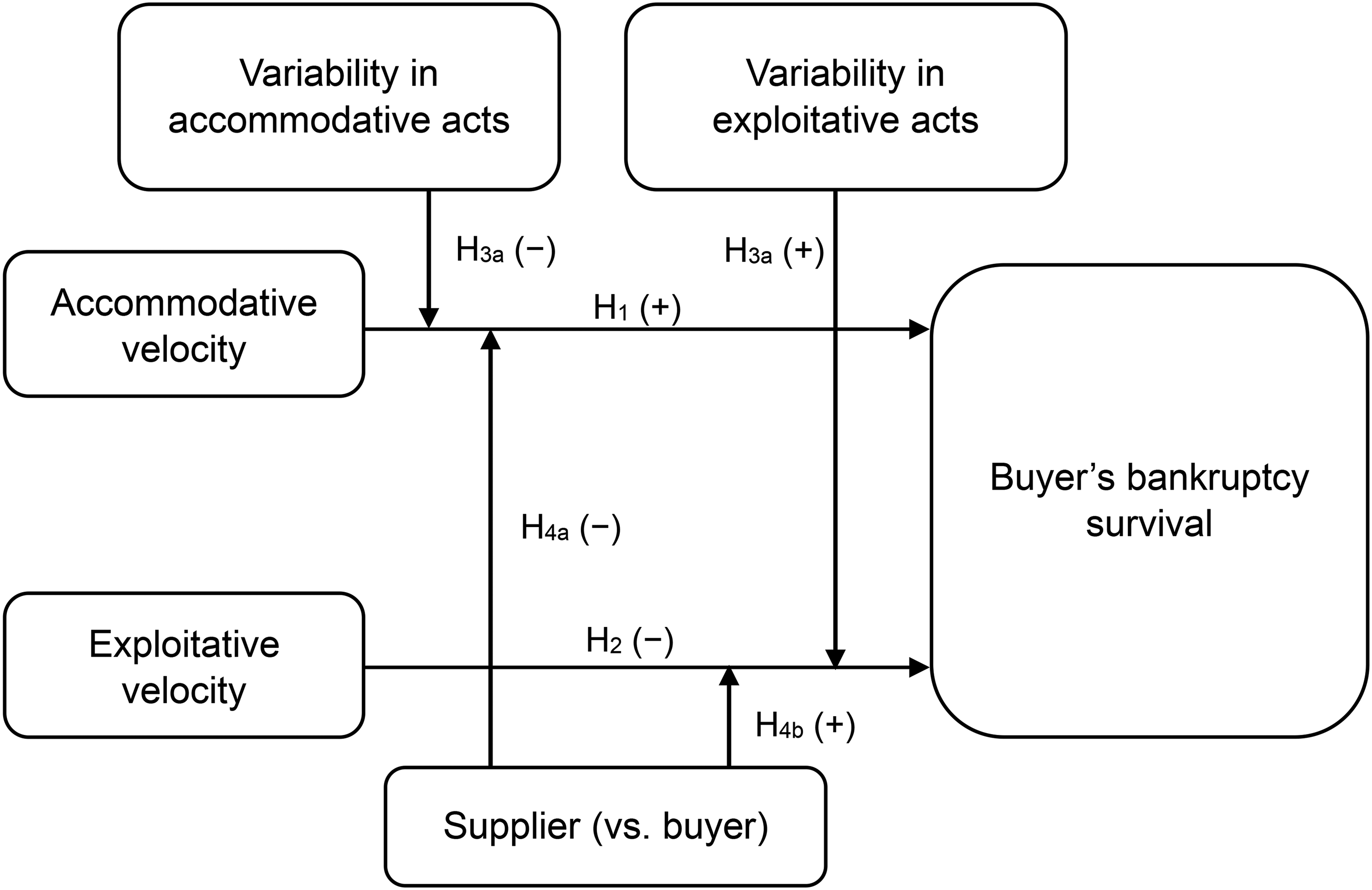

Figure 1 presents our conceptual framework. We integrate insights on relationship dynamics (Palmatier et al. 2013; Shamsollahi et al. 2021) with the literature on signaling intent under information asymmetry (Connelly et al. 2011) to link both parties’ behaviors to bankruptcy survival (see Table 1). Studies on signaling acknowledge that individual acts have limited signaling value because they occur at a singular point in time (DeKinder and Kohli 2008) and the signal recipient thus has lower confidence that these acts will persist over time (Connelly et al. 2011). Research on evolving interfirm relationships emphasizes the greater information provided by trajectories of acts (Connelly et al. 2011; Narayandas and Rangan 2004; Shamsollahi et al. 2021). Both streams of research converge on the insight that, relative to individual acts that may be dismissed as one-off events, parties’ behavioral trajectories provide a clearer signal of intent.

Conceptual Framework.

We thus posit the velocity (i.e., the rate and change) of the buyer's and its suppliers’ accommodative acts to signal the cooperative intent of both parties. Similarly, the velocity of their exploitative acts signals their competitive intent. The counterpart infers the focal party's high levels of accommodative (exploitative) velocity as reflective of concession-making (concession-seeking) and extrapolates the trend in the acts to persist in the future (DeKinder and Kohli 2008). We posit this extrapolation and the superior signal value it provides as a mechanism that underlies the impact of both parties’ accommodative and exploitative velocities on the buyer's bankruptcy survival.

We further consider signal and signaler characteristics that are likely to increase or decrease signal noise—the part of the signal that is noninformative about the underlying intent (Gomulya and Mishina 2017)—thereby weakening or strengthening the effects of the accommodative and exploitative velocities on bankruptcy survival. The greater the noise in the signal, the lower the recipient's confidence in inferring the signaler's intent. High variability in the counterpart's prior acts lowers the focal party's confidence in its inference of the counterpart's behavioral intent from these acts (Table 3 displays the juxtaposition of the velocity and variability of both types of acts). We also hypothesize the signaler's identity (i.e., whether the acting party is the buyer or its suppliers, a signaler characteristic) to moderate the impact of accommodative and exploitative velocities on bankruptcy survival.

Velocity and Variability in Acts.

Notes: Velocity is the rate and the direction of change in either accommodative acts or exploitative acts over time. This is the slope of the line in the table's examples. Variability in acts is the extent to which parties’ acts diverge from their mean acts. The stars indicate the intensity of acts and show whether they are close to or scattered away from the line. Further, the lowest level of accommodative (exploitative) velocity is reflected in a steep negative slope of the line.

Hypotheses

Main Effects of Accommodative and Exploitative Velocities on Bankruptcy Survival

Accommodative velocity

Accommodative velocity is the rate and direction of change in accommodative acts—behaviors that are intended to allow for or cater to the counterpart's needs (Bello, Katsikeas, and Robson 2010; Cannon and Homburg 2001; Noordewier, John, and Nevin 1990). A party's accommodative acts indicate the importance it places on its relationship with the counterpart and its motivation to continue the relationship (Anderson and Weitz 1992; Axelrod 1984). Individual accommodative acts vary in intensity (see Table W1 in Web Appendix B). For example, the buyer's motion to allow a supplier's new claim (i.e., the court-defined motion is “allow claim”) is a higher-intensity accommodative act. Likewise, a supplier motioning to dismiss an adversary proceeding (i.e., court-defined motion = “dismiss adversary proceeding”) is a lower-intensity accommodative act.

The focal party's accommodative velocity signals to the counterpart the former's cooperative intent (Bello, Katsikeas, and Robson 2010). High accommodative velocity enables the counterpart to infer the focal party's desire to cooperate by considering not only the current accommodative act but also its recent past behavior in the same vein (DeKinder and Kohli 2008). Importantly, if the focal party's accommodative velocity is higher, the counterpart is likely to extrapolate the positive trend inherent in the focal party's accommodative velocity, infer its persistence in the future (Johnson, Tellis, and MacInnis 2005), and assess the relationship as growing (Palmatier et al. 2013). In contrast, lower levels of accommodative velocity suggest that the rate of change in accommodative acts is slow, and the counterpart expects the intent to cooperate to change at a slower rate.

The greater the counterpart's expectation of the focal party continuing to allow for or cater to its needs, the more likely it is to reciprocate with relationship-building accommodative acts of its own (Heide and Miner 1992; Hoppner and Griffith 2011). With both parties perceiving their relationship to be growing, there is an increased expectation of relationship continuity likely eliciting a virtuous cycle of cooperation. In such a climate, the buyer and its suppliers are more likely to converge on a reorganization plan that is agreeable to both parties. Thus,

Accommodative velocity increases the buyer's bankruptcy survival.

Exploitative velocity

Exploitative velocity is the rate and direction of change in exploitative acts—behavior intended to deny the needs of, extract concessions from, or make demands of the counterpart (Bello, Katsikeas, and Robson 2010; Narayandas and Rangan 2004). Exploitative acts reflect the focal party's focus on achieving outcomes of value to itself, even if such outcomes may hurt its counterpart. The focal party's exploitative acts thus likely damage its relationship with its counterpart. Like the accommodative acts, exploitative acts also vary in intensity. For example, a buyer's motion to disallow a supplier's claim (court-defined motion = “disallow claim”) is highly exploitative act, whereas suppliers’ motion of complaint (court-defined motion = “complaint”) is less so (see Table W1 in Web Appendix B).

High levels of exploitative velocity signal a competitive or even confrontational tone by the party engaging in the behavior. Such an inference is likely to escalate tension between the two parties, leading to distrust and conflict (Frazier, Gill, and Kale 1989; Geyskens, Steenkamp, and Kumar 1999). The ensuing conflict elicited by the expectation of similar behavior in the future may prolong the bankruptcy, as the confrontational approach will make it difficult for the buyer and its suppliers to resolve their disagreements. The counterpart may also engage in “tit-for-tat” behavior, anticipating continued exploitative acts by the focal party (Hibbard, Kumar, and Stern 2001), with both parties engaging in exploitative acts suggesting that the buyer–supplier relationship is decaying. The focus on seeking concessions is likely to make the suppliers less amenable to supporting the buyer's reorganization plan, in turn posing a challenge to the buyer's bankruptcy survival. Thus, Exploitative velocity decreases the buyer's bankruptcy survival.

Contingency Effects of Variability in Accommodative and Exploitative Acts

The variability in the parties’ acts, whether accommodative or exploitative, refers to the extent to which the acts diverge from their mean (Luo, Raithel, and Wiles 2013). Such divergence implies a lack of consensus (Cialdini 1993) and raises doubt about the signal's credibility (Helm and Mark 2007; Herbig, Milewicz, and Golden 1994). The lack of consistency (high variability) in acts reduces the counterpart's confidence in its ability to predict the signaler's future intent (Gomulya and Mishina 2017). In particular, the deviation reduces the counterpart's conviction that the trend of the focal party's acts will continue, and thus makes the signaler's future behavior less reliable (Johnson, Tellis, and MacInnis 2005). We expand this logic to propose how variabilities in the two types of acts work as contingency factors.

The high variability in accommodative acts reflects a lack of “a consistent thread of meaning” (Keller 2008, p. 641) and raises doubt in the counterpart regarding the signaler's cooperative intent. The counterpart is relatively less likely to extrapolate the positive trend inherent in the focal party's accommodative velocity to infer its persistence in the future (Johnson, Tellis, and MacInnis 2005) and to assess the relationship as growing (Palmatier et al. 2013). The likelihood of the counterpart reciprocating with relationship-building accommodative acts of its own is therefore reduced (Heide and Miner 1992; Hoppner and Griffith 2011), and the signaler's accommodative velocity is less likely to elicit a virtuous cycle of cooperation. The result is a less cooperative climate and a reduced likelihood of the suppliers agreeing to the buyer's debt reorganization plan. In contrast, low variability in accommodative acts suggests that the acts are consistent over time, giving greater confidence in their persistence.

Just as for accommodative velocity, variability in exploitative acts gives the counterpart pause for thought with respect to the signaler's competitive intent. The value of the signal inherent in a trend of exploitative acts is diluted when no clear pattern emerges, thanks to their variability (Gomulya and Mishina 2017). The variability in the exploitative acts instead suggests a lack of commitment to exploitative behavior and erodes the counterpart's ability to clearly predict that the focal party will continue to act exploitatively over time. Under such uncertainty, the counterpart is less likely to reciprocate the signaler's confrontational tone (Hibbard, Kumar, and Stern 2001). A conflict spiral is therefore less likely to develop, and both parties’ competitive resolve is likely weakened, relative to exploitative velocity with low levels of variability. Because the variability would give them hope that the exploitative velocity may not persist in the future, suppliers become more amenable to supporting the buyer's reorganization plan. Thus,

The greater the variability in accommodative acts, the weaker the positive effect of accommodative velocity on the buyer's bankruptcy survival.

The greater the variability in exploitative acts, the weaker the negative effect of exploitative velocity on the buyer's bankruptcy survival.

Contingency Effects of Signaler Identity (Supplier vs. Buyer)

“The U.S. bankruptcy code is debtor [buyer] oriented, allowing the management of the bankrupt firm to stay in control and to continue operating the firm during reorganization” (Yang, Birge, and Parker 2015, p. 2320). Specifically, U.S. bankruptcy law affords control to the buyer and confers it significant discretion in its day-to-day business operations (Pearce and Lipin 2012). Such discretion includes but is not limited to the buyer having the exclusive ability to extract value from favorable relationships and to renounce unfavorable ones (Ayer, Bernstein, and Friedland 2003). The buyer may decide which suppliers receive priority payment and which supplier relations should be (dis)continued as part of the bankruptcy process. These and other such legally conferred rights make the bankruptcy process debtor-oriented (Yang, Birge, and Parker 2015). The buyer's greater agency implies, and its acts are more likely to be attributed to, such agency (i.e., an internal attribution) rather than to the bankruptcy.

Although suppliers retain the right to agree with or oppose the buyer-proposed bankruptcy reorganization plan, they play a supporting rather than leading role, relative to the buyer. The relatively lesser discretion afforded to suppliers in the bankruptcy reorganization, in turn, results in their accommodative and exploitative acts being more likely to be attributed to the exigencies of the buyer's bankruptcy reorganization (i.e., an external attribution).

As Prabhu and Stewart (2001, p. 65) state, “When behavior can be explained sufficiently by external or situational factors, the behavior is attributed to the situation, and no inference is made about the dispositions of the sender” (emphasis added). Consistent with attribution theory and the associated discounting principle, when the suppliers’ behavior is attributed to the buyer's bankruptcy filing (an external situation), their acts are discounted and the buyer is less confident that these acts will persist in the future. This external attribution likely causes the buyer to discount the suppliers’ competitive intent and to infer relatively lower persistence of the latter's exploitative acts. The buyer's external attribution of suppliers’ acts also elicits less clarity about the suppliers’ accommodative velocity and its inferred persistence. A likely dilution of the impact of suppliers’ accommodative and exploitative velocities on bankruptcy survival occurs, relative to the buyer's acts’ velocities.

In contrast, the buyer's exploitative (accommodative) acts are internally attributed. That is, the buyer's behavior is considered strategic in intent as it tries to manage the bankruptcy process. The buyer's acts may “contribute to the development of a reputation” consistent with their signals (Prabhu and Stewart 2001, p. 65), as the behavior is internally attributed. High levels of exploitative velocity indicate a clear competitive stance, whereas high levels of accommodative velocity indicate a more cooperative stance for the buyer, as its internally attributed behavior is likely to persist in the future. Thus,

The positive effect of accommodative velocity on the buyer's bankruptcy survival is weaker for suppliers’ acts than for those of the buyer.

The negative effect of exploitative velocity on the buyer's bankruptcy survival is weaker for suppliers’ acts than for those of the buyer.

Empirical Context

Our empirical context comprises U.S. public firms’ efforts to reorganize their debt via Chapter 11 bankruptcy, the legal status that allows them to renegotiate the debt they owe their suppliers and other unsecured creditors. This renegotiation occurs via a series of motions—submissions that the buyer and its suppliers file in a bankruptcy court. Such motions by the two parties (the buyer and its suppliers) comprise our measures of accommodative acts and exploitative acts.

We test our conceptual framework using two studies. Study 1 tests our hypotheses using a unique database of bankruptcy motions filed in U.S. courts. Study 2 is a scenario-based experiment that replicates H1 and H2 and provides evidence on the mechanism underlying the effects of accommodative and exploitative velocities on the buyer's bankruptcy survival.

Study 1

Data Collection and Unit of Analysis

We assess bankruptcy survival of buyers in three industries: manufacturing, retail and wholesale trade, and services. These industries are characterized by significant buyer–supplier relations and are thus appropriate for our research. We integrate data from three archival sources. New Generation Research's Bankruptcy Data database provided us with a list of all U.S. public firms (in manufacturing, retail and wholesale trade, and services industries) that filed for reorganization bankruptcy between 2001 and 2014. The list includes the name of the firm, the date it filed for bankruptcy, and name of the bankruptcy court where the firm filed for bankruptcy. We cross-reference these firms with Standard & Poor's Compustat – Capital IQ North America Fundamentals Annual database to obtain data on accounting variables. To these data, we add information on motions (i.e., acts) by the buyer and its suppliers from the U.S. judiciary's Public Access to Court Electronic Records (PACER) database. This database provides the Docket Activity Reports (for details, see Figure W2 in Web Appendix B for details), which list the individual motions filed by the buyer and its suppliers during bankruptcy. We download Docket Activity Reports for each bankruptcy in our sample. These steps yield a sample of 421 reorganization bankruptcies filed by U.S. public firms from 2000 to 2014.

Our unit of analysis comprises the buyer firm and its suppliers. We view the suppliers as a collective rather than as separate entities. This view is consistent with the bankruptcy process, which emphasizes the suppliers as a group (Jindal 2020). Furthermore, the PACER data do not identify the individual creditor that filed a motion. For each bankruptcy, we use the information contained in the Docket Activity Report to distinguish the motions filed by the buyer and its suppliers from motions filed by other bankruptcy stakeholders, such as the bankruptcy court, banks, and employee unions. The U.S. bankruptcy courts classify the buyer's and suppliers’ motions into 23 types. Using the definitions of accommodative acts and exploitative acts, a bankruptcy attorney classified each of the 23 types of motion listed in the Docket Activity Report as an accommodative, exploitative, or neutral act. The expert also rated each motion's intensity on a scale of 1 (lowest) to 7 (highest) (Hibbard, Kumar, and Stern 2001; see “Determining and Classifying Motions Filed During Bankruptcy” in Web Appendix B). Per this classification, 15% of motions in our sample are accommodative, 77% are exploitative, and 8% are neutral.

Measures

A party (i.e., either the bankrupt buyer or its suppliers) often files multiple motions to which the counterpart responds. Consider Figure 2, which illustrates the motions filed by Amcast Corporation—one of the buyers in our sample—and its suppliers. Amcast filed three motions: reject contract, complaint, and pay prepetition debt. At this point, one of Amcast's suppliers filed an objection motion. Amcast's prior three motions comprise a “sequence” s. A sequence, therefore, is a time-ordered set of uninterrupted motions filed by the same party. Next, we sum the weight of each exploitative motion in s to compute the intensity of exploitation in s. Sequence s has two exploitative motions: “reject contract,” with a weight of 6 (on a scale of 7), and “complaint,” with a weight of 4. Therefore, the intensity of exploitation in s is 6 + 4 = 10. Similarly, we calculate the intensity of accommodation in the sequence s. Because s comprised a single accommodative motion of “pay prepetition debt” with a weight of 4, the intensity of accommodation in s is 4.

A Prototypical Example of the Sequences of Acts by a Buyer and Its Suppliers.

Following the objection motion by one of Amcast's suppliers, Amcast filed further motions, interrupting its suppliers’ behavior. This interruption helps us group the suppliers’ prior single motion into sequence s + 1. Next, we compute the intensity of exploitation and the intensity of accommodation in suppliers’ sequence s + 1. Because objection is exploitative and has a weight of 5, the intensity of exploitation in suppliers’ sequence s + 1 is 5. Because s + 1 has zero accommodative motion, the intensity of accommodation in s + 1 is 0. We repeat this process until Amcast's bankruptcy proceeding ends. Our structuring of the individual motions into sequences means that the sequences alternate between the buyer and the suppliers. For example, in Amcast's case, sequence s is the buyer's, s + 1 is the suppliers’, s + 2 is again the buyer's, and so on.

Our data set comprises all sequences s within bankruptcy i. However, 110 of the 421 bankruptcies had three or fewer sequences of interactions between the buyer and its suppliers, too few to calculate acts’ velocities and variability. We therefore excluded these bankruptcies. An involuntary bankruptcy—one in which the creditors request the debtor to file for bankruptcy—was also dropped. Our estimation sample thus comprises 310 bankruptcies filed between 2001 and 2014. Table W2 in Web Appendix B lists the number of bankruptcies in our sample by industry and by year.

Dependent variable: Bankruptcy survival

Our dependent variable (DV) is a categorical measure with three values: 1, 2, and 0. First, we are interested in predicting the survival of the bankrupt buyer. Therefore, consistent with prior research on bankruptcy (Elayan and Meyer 2001; Jindal 2020), the DV equals 1 if the buyer maintains its legal status after bankruptcy or is acquired by another firm (i.e., survives or emerges from bankruptcy). Second, the bankruptcy may end in the liquidation of the buyer's assets, which is an unfavorable outcome because the buyer sought reorganization and not liquidation (Chapter 11 vs. Chapter 7, respectively, in the United States). Bankruptcy survival equals 2 for such bankruptcy cases. Third, the bankruptcy court may dismiss a case if the buyer fails, for example, to submit to the court the required documents timely or attend the required meetings. We set Bankruptcy survival to 0 for such bankruptcy cases. Across the 310 bankruptcies in our final sample, 49% of the firms survived (i.e., DV = 1), 44% were liquidated (i.e., DV = 2), and 7% were dismissed (i.e., DV = 0).

Predictor variables

We measure a party's accommodative velocity in sequence s by the change in the intensity of its accommodation over the current sequence and its prior two sequences. Consider the example of Amcast Corporation, whose bankruptcy proceeding began with the latter (i.e., the buyer) filing the first motion. Suppose we are in sequence #9. Because sequence #1 belonged to Amcast, sequence #9 also belongs to it (see Figure 2). We compute the velocity of Amcast's accommodation in sequence #9 by considering Amcast's behavior in the prior two sequences and the current sequence—that is, sequences numbered 5, 7, and 9. We create a counter variable that takes the value of 1 for sequence #5, the value of 2 for sequence #7, and the value of 3 for sequence #9. Next, we regress the intensity of accommodation in these three sequences on the counter. The slope coefficient estimate serves as our measure of the focal party's accommodative velocity (Palmatier et al. 2013). The standard error of the slope coefficient is our measure of the variability in the focal party's accommodative acts (Bommaraju et al. 2019). We repeat the preceding process to compute the focal party's exploitative velocity and the variability in its exploitative acts. The signaler dummy variable equals 1 for the supplier and 0 for the buyer.

We control for three groups of variables. First, because neutral acts may dilute the attention that a party pays to its counterpart's accommodation and exploitation, we control for the parties’ neutral acts in the focal bankruptcy. Second, we control for several accounting characteristics of the buyer, each of which might impact its bankruptcy survival. The amount the buyer owes the suppliers serves as a proxy for the suppliers’ influence, which can determine bankruptcy outcomes (Jindal 2020). We therefore include the debt owed (accounts payable divided by total debt) as a control variable. Bankruptcy research suggests a strong association between the bankrupt firm's liquidity and its bankruptcy outcomes (Jindal and McAlister 2015). We accordingly control for the buyer's average cash over the six years preceding the year of the bankruptcy filing in millions of dollars. Lastly, following Jindal (2020), we control for the buyer's solvency (total debt divided by total assets), asset size (log-transformed), and profit (earnings before interest, taxes, depreciation and amortization divided by sales).

We further control for two bankruptcy-specific decisions that the buyer makes. Bankruptcy research in finance and law suggests that the New York–Southern and Delaware bankruptcy courts are more effective and efficient in resolving bankruptcies (LoPucki and Doherty 2002). Consequently, we control for whether the bankruptcy was filed in New York–Southern or Delaware (NYDE = 1) or elsewhere (NYDE = 0). Further, following prior research (Flynn and Farid 1991), we also control for whether the bankrupt buyer designates its CEO (as opposed to a CFO, a restructuring officer, etc.) as the primary contact during bankruptcy (CEOPRIMARY). Lastly, we include fixed effects to account for unobserved heterogeneity specific to the buyer's industry (INDUSTRY) and the bankruptcy-filing year (YEAR). Table 4 reports descriptive statistics for the variables and their pairwise correlation coefficients.

Study 1: Descriptive Statistics and Correlation Coefficients.

Natural log-transformed.

Notes: All correlations greater than the absolute value of .04 are significant at p < .10 (two-tailed). n = 3,160.

Empirical Model

Bankruptcy survival

Our interest lies in the buyer's likelihood and speed of emergence from bankruptcy, that is, its bankruptcy survival (DV = 1). However, this outcome competes with the alternate outcome of liquidation (DV = 2). We thus estimate a competing-risks regression (Fine and Gray 1999; Jindal 2020), which helps us model the hazard of bankruptcy survival, controlling for the competing outcome. Simply stated, the competing-risks regression models firm i's hazard of survival (our outcome of interest) at time t, provided the firm has neither survived until time t nor has experienced the competing outcome of liquidation. The bankruptcy survival subdistribution hazard function for a competing-risks model is expressed as

Endogeneity correction

Our hazard function may have omitted variables that may impact the parties’ behaviors and directly affect the buyer's bankruptcy survival. For example, the buyer may exhibit values that emphasize resilience in the face of adversity, thus prioritizing reorganization over liquidation. Such culture—unobservable to us—may influence the buyer's behaviors and directly impact its bankruptcy survival. Omitting such variables renders the accommodative velocity and exploitative velocity (i.e., AVis and EVis) potentially endogenous to our hazard function, biasing our estimates. We follow standard methods to control for the endogeneity of accommodative velocity and exploitative velocity. First, we include industry-fixed effects that control for the unobserved industry-specific factors that do not vary over time and can impact a firm's bankruptcy survival. Similarly, the year fixed effects control for the unobserved macroeconomic variables that may influence bankruptcy survival.

Second, we use the control function method (Petrin and Train 2010) to correct for potential endogeneity. To identify instruments that meet the relevance criterion (i.e., correlated with the velocities) and exclusion restriction (i.e., uncorrelated with the omitted variables), we rely on recent marketing research on bankruptcy (Jindal 2020) and research on the contagion effect of bankruptcy (Ferris, Jayaraman, and Makhija 1997; Jindal and Slotegraaf 2023).

Bankruptcy motions are filed and made publicly available almost immediately. Thus, the attorneys working with their clients (buyers and suppliers) have access to information on industry norms. That is, peers’ average behaviors may determine the focal party's acts. We confirm this logic through two means. First, we consulted a bankruptcy counsel who advised us on the Chapter 11 process. The counsel told us that “there is a precedential effect of one (bankruptcy) case on another. If one … [party] … is in proceedings in which motions are necessary, the next … [party] … that files might look to the earlier case in considering how it might approach proceedings in the second case.” Second, BankruptcyData.com provided us with a data file with the names of counsel that the debtor and the committee of unsecured creditors in manufacturing bankruptcies had retained. Consistent with our expectation, the counsel names were repeated within the industry. The repetition supports our reasoning that counsels within an industry generate institutional knowledge, which they appropriate by using prior behaviors of the same type of party (i.e., buyer or suppliers) to determine the current behavior. We thus reason that our instrument meets the relevance criterion. Further, we argue that peers’ accommodative and exploitative acts do not correlate with omitted variables such as the focal buyer's values (Jindal 2020); that is, the instruments meet the exclusion restriction.

Accordingly, we instrument the parties’ accommodative (exploitative) velocity in bankruptcy i by the average of the accommodative (exploitative) velocity of the parties in other bankruptcies in the buyer's industry in the 90 days prior to the filing year of the focal bankruptcy i. In addition, we use a second instrument, time to bankruptcy filing (the years elapsed between the firm being publicly listed and the year of bankruptcy filing), to correct for endogeneity (Antia, Mani, and Wathne 2017). Web Appendix B details the instrument validity checks, and Table W3 presents the estimates from the first-stage regression.

Results

Model-Free Evidence

We perform a median split on accommodative velocity and conduct a log-rank test, where the null hypothesis is that the survival functions are equal for low and high levels of the variable. We conduct a similar test for exploitative velocity, variability in accommodative and exploitative acts, and whether the signaler is the suppliers or the buyer. We reject the null of equal survival functions for accommodative velocity (p < .05), exploitative velocity (p < .05), variability in exploitative acts (p < .1), and supplier identity (p < .05). However, we could not reject the null of equal survival functions for the variability in accommodative acts. These findings provide preliminary support for our model.

Survival Analysis Results

Table 5 reports estimates from the competing-risks model. The positive coefficient estimates indicate that the predictor increases the hazard of bankruptcy survival, whereas a negative coefficient estimate indicates a decrease in the hazard. That is, a positive coefficient indicates an increase in the likelihood of the buyer's emergence from bankruptcy and a decrease in its bankruptcy duration. In contrast, a negative coefficient indicates a lower likelihood of emergence and higher duration.

Study 1: Competing-Risks Model Estimates (N = 3,160).

*p < .1. **p < .05. ***p < .01 (two-tailed).

Natural log-transformed.

Notes: Regression estimates are shown with z-statistics in parentheses.

H1 posits that the accommodative velocity is positively associated with the buyer's bankruptcy survival. We find support for H1, as parties’ accommodative velocity increases the buyer's bankruptcy survival (α1 = 38.73, p < .01). Averaged over the duration of a bankruptcy, a 1% increase in accommodative velocity increases the hazard of bankruptcy survival by 39%. H2 hypothesizes that exploitative velocity decreases the buyer's bankruptcy survival. We find marginal support for this hypothesis as well (α1 = −33.27, p < .1). Over the bankruptcy duration, a 1% increase in exploitative velocity decreases the hazard of survival by 33%.

H3a predicts that the variability in accommodative acts weakens the positive effect of the accommodative velocity on the buyer's bankruptcy survival. H3a is supported (α6 = −.97, p < .01). H3b states that the variability in exploitative acts weakens the negative effect of the exploitative velocity on the buyer's bankruptcy survival. We find no support for this hypothesis (α7 = −.24, n.s.). H4a predicts that the positive effect of accommodative velocity is weaker for suppliers’ (vs. the buyer's) acts. This hypothesis is supported (α8 = −7.22, p < .05). We also find support for H4b, which states that the negative effect of exploitative velocity is weaker for suppliers than for the buyer (α9 = 5.16, p < .05).

Turning to the control variables, we find that solvency (α13 = 1.57, p < .01), size (α14 = .18, p < .05), and CEO as the primary contact (α17 = 1.26, p < .05) are positively associated with the buyer's bankruptcy survival. The buyer's cash is negatively related to its bankruptcy survival (α12 = −.00, p < .05). Parties’ neutral acts (α10 = .17, n.s.), the amount the buyer owes its suppliers (α11 = −.00, n.s.), profit (α15 = −.00, n.s.), whether the case is filed in the more efficient courts of New York–Southern or Delaware (α16 = −.04, n.s.), and whether the buyer is in the retail (α18 = −.18, n.s.) or services (α19 = −.11, n.s.) industries are not associated with the buyer's bankruptcy survival. The residuals for the accommodative velocity have a weakly significant association with bankruptcy survival (α32 = −31.98, p < .1). However, the residuals of the exploitative velocity are not related to survival (α33 = 29.33, n.s.), suggesting that this velocity is likely not endogenous to the specification of bankruptcy survival (Tan, Chandukala, and Reddy 2022). Web Appendix C provides details on seven robustness checks (Tables W4–W9) and two additional analyses (Tables W10 and W11) we conducted. Our results remain robust across all analyses.

Post Hoc Analysis of the Moderators

Following Aiken and West (1991), we conduct simple slopes analysis to further assess the significant interactions between accommodative velocity and the variability in accommodative acts. At high and low levels of variability (±2 SD), the positive slope of accommodative velocity was 37.05 and 40.37, respectively. That is, at high levels of variability, a 1% increase in accommodative velocity causes a 37% increase in bankruptcy survival. In contrast, at low levels of variability, the increase is 40.37%.

Next, we compute the effect sizes by the signaler identity: suppliers versus the buyer. A 1% increase in the buyer's accommodative velocity boosts bankruptcy survival by 38.73%, whereas a similar increase in the suppliers’ accommodative velocity raises bankruptcy survival by 31.5% (38.73 − 7.22). Next, a 1% increase in the buyer's exploitative velocity suppresses bankruptcy survival by 33.27%, whereas a similar increase in the suppliers’ exploitative velocity decreases bankruptcy survival by 28.1% (−33.27 + 5.16). The insight is that the buyer's acts are more impactful than the suppliers’.

Study 2

Objective

Study 2 aims to (1) replicate the main effects from Study 1 that parties’ accommodative (exploitative) velocity helps (hinders) the buyer's bankruptcy survival and (2) test the proposed mechanism—that the counterpart anticipates the focal party to persist in its accommodative or exploitative acts in the future—underlying the main effects.

Design

We employed a one-factor, three-condition (accommodative, exploitative, and neutral velocity) between-subjects design. In designing the experiment, we consulted four marketing academics and two bankruptcy law experts on the scenario wording and response formats. Web Appendix D describes the scenario text common to the three conditions and the text manipulating the velocities: accommodative, exploitative, and neutral.

Procedure

We recruited from Prolific Academic 224 U.S.-located individuals with managerial experience to participate in a study about a supplier dealing with a bankrupt buyer. The average age of the participants was 40.9 years, and the average managerial experience was 19.5 years. The participants had prior experience in a broad range of industries: manufacturing (n = 26; 11.61%), retail and wholesale trade (n = 38; 16.96%), and services (n = 81; 36.16%). Fifty-two percent of participants were female, 47% were male, and 1% did not disclose their gender.

All participants were first asked to imagine that they were employed as managers of a firm supplying inputs to a buyer firm (named TKS Associates) for more than five years, and that the buyer firm had been unable to pay its last invoice and had filed for bankruptcy (see Web Appendix D). They were further informed that their employer and the buyer firm were required to interact with each other solely via motions filed in a bankruptcy court. The scenario also mentioned the implications of the supplier's interactions with the buyer firm for the latter's bankruptcy survival, and what the survival meant for each party.

The participants were randomly assigned to one of the three experimental conditions (accommodative velocity n = 75, exploitative velocity n = 72, neutral velocity n = 77). Each participant viewed TKS Associates’ three recent acts and was expected to infer trends (velocity) from these multiple acts (Johnson, Tellis, and MacInnis 2005). We next asked the participant to indicate their likelihood of approving the buyer firm's bankruptcy debt restructure plan (i.e., our DV). The participant next answered a series of questions regarding their belief that their buyer partner would persist with accommodative and exploitative acts in the future (i.e., our mechanism variable). We randomized the order of presentation of statements about their beliefs. Lastly, we checked the manipulation and concluded by collecting participants’ demographic information (age, gender, years of managerial experience, and industry worked in).

Measures

Web Appendix D lists the items we used to measure participants’ anticipation of their buyer partner firm's future accommodative and exploitative acts. We modified Bello, Katsikeas, and Robson’s (2010) measures of accommodative acts to arrive at a five-item Likert-type scale reflecting the extent to which the participant anticipated the buyer to undertake accommodative acts in the future. We developed analogous items of participants’ beliefs regarding their buyer partner firm undertaking exploitative acts in the future. We also controlled for respondents’ age, gender, years of work experience, and industries.

Attention Check and Manipulation Checks

Of the 224 participants originally recruited, three failed our attention check items and were excluded from the study. We undertook checks of our manipulations by examining means across treatments to the statement “TKS Associates’ recent motions have accommodated [or exploited] my company” for the 221 participants. The checks indicate that our manipulations were successful, with the accommodative velocity scenario significantly increasing perceptions of the accommodativeness of TKS's recent acts compared to the neutral scenario (Maccommodative − Mneutral = 2.19; t = 13.24, p < .00), and the exploitative velocity scenario (Maccommodative – Mexploitative = 3.96; t = 23.06, p < .00). In addition, the exploitative scenario significantly increased participants’ perceptions of the exploitative velocity of TKS's recent acts compared with the neutral scenario (Mexploitative − Mneutral = 1.36; t = 5.92, p < .00) and the accommodative scenario (Mexploitative – Maccommodative = 3.21; t = −16.48, p < .00).

Results

To assess the effects of the buyer's accommodative and exploitative velocities, we first regressed the likelihood of participants approving TKS Associates’ debt restructure plan (i.e., our DV) on a three-level categorical variable (accommodative and exploitative conditions, with the neutral condition specified as the baseline). Table 6 displays the regression results with and without the inclusion of covariates. Consistent with H1 and H2, accommodative velocity significantly increases the supplier's likelihood of approving the buyer's debt restructure plan, whereas exploitative velocity significantly decreases this likelihood.

Study 2: Regression Results.

*p < .1. **p < .05. ***p < .01 (two-tailed).

Notes: Robust standard errors are in parentheses.

We further argued that suppliers’ perceptions of the buyer's future accommodative intent mediate the effect of accommodative velocity on their likelihood of approving the buyer's debt restructure plan. To test this argument, we used PROCESS Model 4 (Hayes 2018) and found that perceived future accommodative intent partially mediates the path between the buyer's accommodative velocity and suppliers’ likelihood of approving the plan. The total effect of accommodative velocity on the supplier's approval (c = 1.89, p < .00) comprises an indirect effect through perceived future accommodative intent (a = 1.36, p < .00; b = .54, p < .00; a × b = .73, CI = [.43, 1.06]) as well as a significant direct effect (c′ = 1.16, p < .00). The indirect effect is 38.86% ([1.36 × .54] ÷ 1.89) of the total effect.

We also argued that the negative association between the buyer's exploitative velocity and the supplier's approval is mediated by the supplier's perceptions of the buyer's future exploitative intent. The evidence is consistent with this expectation. Perceived future exploitative intent partially mediates the path between the buyer's exploitative velocity and the suppliers' likelihood of approving the plan. The total effect of exploitative velocity on the supplier approving the buyer's plan (c = −2.06, p < .00) comprises a significant indirect effect through perceived future exploitative intent (a = 1.16, p < .00; b = −.54, p < .00; a × b = −.63, CI = [−.93, −.36]), as well as a significant direct effect (c′ = −1.43, p < .00). The indirect effect is 30.41% ([1.16 × −.54] ÷ 2.06) of the total effect.

The experiment supports our hypotheses that a bankrupt buyer's accommodative (exploitative) velocity significantly increases (decreases) the likelihood of the supplier approving the buyer's plan, and that these effects are partially explained by an increase in suppliers’ perceptions of future accommodative (exploitative) intent.

Discussion

Our research responds to the call for an “interactive approach to interorganizational relationships” (Heide and Miner 1992, p. 265). Relying on the novel context of buyer–supplier interactions occurring in 310 bankruptcies filed by buyer firms in three industries over 14 years, Study 1 demonstrates that the velocities of a bankrupt buyer's and its suppliers’ accommodative and exploitative acts impact the buyer's bankruptcy survival. These effects are contingent on the variability in these acts and whether the signaler is the buyer or its suppliers. Study 2 demonstrates an underlying mechanism: the extent to which one party's acts shape its counterpart's expectations of similar behavior in the future. The convergent results from a longitudinal-observational study and a scenario-based experiment demonstrate that “prior relationship dynamics determine future relationship developments” (Schmitz et al. 2020, p. 72) and influence the buyer's bankruptcy survival. In what follows, we discuss the theoretical and managerial implications of our findings.

Theoretical Implications

Contributions to research on dynamics of buyer–supplier relations

Research on interorganizational relationship dynamics has examined the stages and cycles of relationship development (Shamsollahi et al. 2021) and emphasized that these relations follow a predefined trajectory in their evolution over time. However, the marketing discipline has little understanding of how temporal changes in relational behaviors influence firm performance (see Palmatier et al. [2013] for a notable exception). One reason for the lack of research on the relationship trends is the difficulty in observing buyer–supplier interactions over time. The bankruptcy court filings provide a unique opportunity to observe how the parties’ behaviors evolve. By studying two relational constructs that change over time (i.e., accommodative and exploitative velocities) and their impact on the critical outcome of a firm's bankruptcy survival, we extend prior acknowledgments of the importance of examining different relationship velocities and of quantifying their effects on performance (Palmatier et al. 2013).

Integrating the relationship dynamics literature with signaling theory, we show how parties’ (the buyer's and its suppliers’) acts convey information about their intent (Porter 1980). We build on Prabhu and Stewart's (2001, p. 63) contention that “through repeated interaction, receivers first form beliefs about senders and then use these beliefs in making decisions.” In addition, we identify variability in accommodative acts as a significant moderator of the effect of accommodative velocity on bankruptcy survival. When one party's accommodative velocity is characterized by high variability, its accommodative velocity is not considered a credible signal. Counter to our hypothesis, though, variability in exploitative acts does not moderate the effect of exploitation velocity on bankruptcy survival. These findings suggest asymmetry in the effects of accommodative and exploitative velocities and the variability in the acts. Exploitative velocity appears to elicit a greater expectation of persistence, despite variability in it. Each party would do well to be mindful of this asymmetry.

We also hypothesize and find evidence that parties’ identities matter. In the present context, suppliers’ acts are discounted more than a buyer's acts. We attribute this differential discounting to the fact that bankruptcy procedures offer less discretion to suppliers, resulting in their acts being attributed to external factors (Prabhu and Stewart 2001; Ross and Anderson 1982). In contrast, the buyer strategically and voluntarily files for bankruptcy to reorganize and start afresh and thus has greater discretion. Consequently, the effects of suppliers’ accommodative and exploitative velocities on the buyer's survival are weaker than those of the buyer. The asymmetric moderating impact of the signaler identity on the buyer's bankruptcy survival emphasizes the importance of the context in which the parties interact.

An additional critical insight we provide stems from our experiment. We show that trajectories of acts—both accommodative and exploitative—increase the counterparts’ confidence that the acts will persist. Moreover, these beliefs in the persistence of acts explain the supplier's decision to influence the buyer's bankruptcy survival efforts. In establishing the mechanism underlying the impact of accommodative and exploitative acts on bankruptcy survival, we provide confidence in the results we observe in situ over 14 years of bankruptcies.

Contributions to signaling theory

We make two significant contributions to signaling theory. First, although the signaling theory acknowledges that a firm's stakeholders lack information about not only its (and its offerings’) quality but also its behavioral intent (Stiglitz 2000), the empirical evidence has focused on the former (Acar et al. 2021; Cao et al. 2023; Chase and Murtha 2019). Our focus on understanding how parties use acts to signal intent thus represents an important contribution to the signaling literature. Specifically, Study 1 yields evidence consistent with our hypothesizing the signaling value of accommodative and exploitative act velocities. Study 2 further demonstrates that signals do provide information of the sender's intent. That is, upon receiving the sender's accommodative (exploitative) acts, the receiver believes that such accommodation (exploitation) will likely continue. This inference about the sender's intent in turn influences the buyer's bankruptcy survival.

Second, the extant signaling literature has focused overwhelmingly on positive signals. However, signals can also be negative (Connelly et al. 2011). In examining parties’ exploitative acts and the receiver's inference of these acts, we emphasize the need to be cognizant of the acts’ repercussions. Our focus on signaling intent via accommodative and exploitative acts significantly extends the scope and application of signaling theory to vital managerial decisions.

Contributions to the marketing–finance interface

We also make an important contribution to research on the marketing–finance interface (Srivastava, Shervani, and Fahey 1998). In considering bankruptcy survival pursuant to buyer–supplier interactions, we extend the nascent literature examining the link between marketing actions and bankruptcies (Antia, Mani, and Wathne 2017; Jindal and McAlister 2015; Jindal and Slotegraaf 2023). Academics in economics, finance, marketing, and law have provided robust insight into how a firm's financial status before it files for bankruptcy impacts its bankruptcy survival (see Table 1). We extend this literature by demonstrating that buyer–supplier acts during bankruptcy also determine the buyer's bankruptcy survival. The demonstrated influence of both parties’ acts during bankruptcy bridges the gap between the theory and the practice of bankruptcy. Importantly, our findings demonstrate that marketing can help a firm's financial outcomes not only in steady state but also in crises (Edeling, Srinivasan, and Hanssens 2021; Fang, Palmatier, and Steenkamp 2008).

Managerial Implications

In a postpandemic world characterized by macroeconomic instability and geopolitical uncertainty, firm bankruptcy is unfortunately not a rare incident (American Bankruptcy Institute 2022). Bankrupt firms often leave their customers, suppliers, and employees stranded. Just as importantly, bankrupt firms experience financial losses they are particularly ill-suited to weather. The Chrysler Corporation, for example, lost $100 million each day that it remained in bankruptcy (Selbst 2009). The firms we studied had assets worth $8 billion, on average. Moreover, on average, medium-sized firms spend about 3% of their assets and 648 days in bankruptcy (Rosen 2016). We therefore estimate that bankruptcy costs amounted to $370,000 per day for firms in our sample. Notably, successful and speedy emergence from bankruptcy enables the buyer to make and act on decisions without the court's supervision, providing additional incentive for managers to seek early survival.

We find that a 1% increase in a party's accommodative velocity increases bankruptcy survival by 39%, while a 1% increase in its exploitative velocity decreases bankruptcy survival by 33%. Each party would do well to note that accommodative velocity has a greater effect on bankruptcy survival even though these acts represent only 15% of the motions filed during bankruptcy. We also find that the variability in acts mitigates the positive effect of accommodative velocity, but not that of exploitative velocity. These asymmetrical moderating effects suggest two simple yet important pieces of advice to buyers and their suppliers: (1) undertake accommodative acts increasingly and consistently over time, because they aid bankruptcy survival, and (2) reduce exploitative acts over time. These findings underscore managerial agency, particularly the insight that the buyer's fate is not solely determined by its financial status prior to filing for bankruptcy.

Our findings also have implications for suppliers. Although suppliers’ acts are less influential with respect to bankruptcy survival than the buyer's, their effect is nevertheless substantial. Specifically, a 1% increase in suppliers’ accommodative velocity increases bankruptcy survival by 32% (for the buyer's accommodative velocity, the increase is 39%). Similarly, a 1% increase in suppliers’ exploitative velocity decreases bankruptcy survival by 28% (for the buyer's exploitative velocity, it is 33%). Our findings indicate that the suppliers’ velocities influence bankruptcy survival, albeit to a lesser extent than the buyer's velocities. This difference is more pronounced for accommodative velocity than exploitative velocity. The latter findings imply that suppliers should consider the marked bankruptcy survival outcomes consequent to their use of accommodative and exploitative motions in court.

From a public policy perspective, suppliers’ participation is a desirable feature of bankruptcy laws. However, suppliers do not always participate in the bankruptcy proceedings because of the costs or a general sense of apathy (Tomasic 2006). The findings from our research indicate that suppliers’ acts over time influence buyer's bankruptcy survival. Policymakers can use the findings from our research to encourage suppliers to engage in accommodative acts at a faster rate and reduce the rate of exploitative acts to support a buyer's efforts to emerge from bankruptcy.

Limitations and Research Directions

Our research does have limitations, each of which merits future attention. The U.S. Chapter 11 bankruptcy law assigns priority levels to a firm's creditors based on whether the debt provided is secured or unsecured (Jindal 2020). Because all suppliers provide unsecured debt to a buyer firm, their claims fall under the same priority level. However, we cannot rule out the possibility that bankruptcy laws in other countries may assign different levels of priority to suppliers. Nor can we rule out the possibility that other non-supplier-undertaken motions might impact buyers’ bankruptcy survival. Future research may explore non-U.S. settings and non-supplier-undertaken motions and test our theory. In addition, the court-provided PACER data do not usually identify the specific supplier, especially for motions filed by the buyer. Relatedly, while the Securities and Exchange Commission requires a U.S. public firm to disclose its major customers, no such mandate exists for the firm's major suppliers. As a result, we are unable to examine heterogeneity in buyer–supplier interactions as a function of supplier characteristics. Future efforts to remedy this limitation, perhaps in non-U.S. contexts, could prove fruitful.

The archival data preclude us from observing out-of-court negotiations, settlements, and/or disagreements that could determine the court-filed motions. Future research that complements the PACER data with surveys of the buyer, suppliers, and/or their counsel measuring out-of-court interactions could be valuable. Furthermore, we do not observe the extent to which suppliers attribute blame for the buyer's bankruptcy to its financial mismanagement or to the external business environment. Because this blame attribution could also influence how signals are inferred and, in turn, influence bankruptcy outcomes, future research should examine blame attribution and its implication on the bankruptcy survival. Lastly, although we acknowledge that buyer–supplier power, dependence, and reciprocity likely influence bankruptcy survival, they are either unobservable or lie outside the scope of this study. Future research could examine these and other buyer–supplier relationship constructs and their effect on bankruptcy survival.

Supplemental Material

sj-pdf-1-jmx-10.1177_00222429231193994 - Supplemental material for Buyer–Supplier Relationship Dynamics in Buyers’ Bankruptcy Survival

Supplemental material, sj-pdf-1-jmx-10.1177_00222429231193994 for Buyer–Supplier Relationship Dynamics in Buyers’ Bankruptcy Survival by Sudha Mani, Vivek Astvansh and Kersi D. Antia in Journal of Marketing

Footnotes

Acknowledgments

The authors thank participants of the AMA's Winter Academic Conferences and the B2B Research Online Seminar Series. They acknowledge research assistance from Areej Alshamrani, Neetu Astvansh, David Jack Bunce, Hoorsana Damavandi, Angela Newman, Lisette Sotelo, and Upma Tiwari. They thank Richard McLaren and Kevin McElcheran for their expertise regarding legal aspects of bankruptcy, and June Cotte, Jan B. Heide, Jessica Hoppner, Zuzanna Jurewicz, Ethan Milne, Harmen Oppewal, and Kenneth H. Wathne for their comments on this research. They are also grateful to Ben Schlafman from New Generation Research Inc. (BankruptcyData.com) for answering questions on the bankruptcy phenomenon.

Associate Editor

Hari Sridhar

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Monash Business School’s COVID-19 Disrupted Research Grant Scheme.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.