Abstract

Growth and innovation are primary arguments for firms that aim to go public and access resources from the stock market. So it is ironic that going public is, for a majority of firms, associated with a pronounced slump in breakthrough innovation. This article proposes an actionable, marketing-related explanation for why some firms that go public manage to beat the post–initial public offering (IPO) innovation slump: innovation imprinting. The authors argue and demonstrate that firms that engage in innovation imprinting before going public attract a segment of concordant investors whose risk preferences are more supportive of breakthrough innovation than investors at large. These investors, in turn, reward the firms’ continued introduction of breakthrough innovations after they have gone public. By analyzing the innovation patterns of 207 firms in the consumer packaged goods sector before and after an IPO, the authors observe that one-third of firms are able to maintain or beat their pre-IPO levels of breakthrough innovations after going public. By studying their actions, the investors they attract, and their financial performance and survival rates, the authors provide empirical evidence for the importance of innovation imprinting and concordant investors in helping firms beat the post-IPO innovation slump.

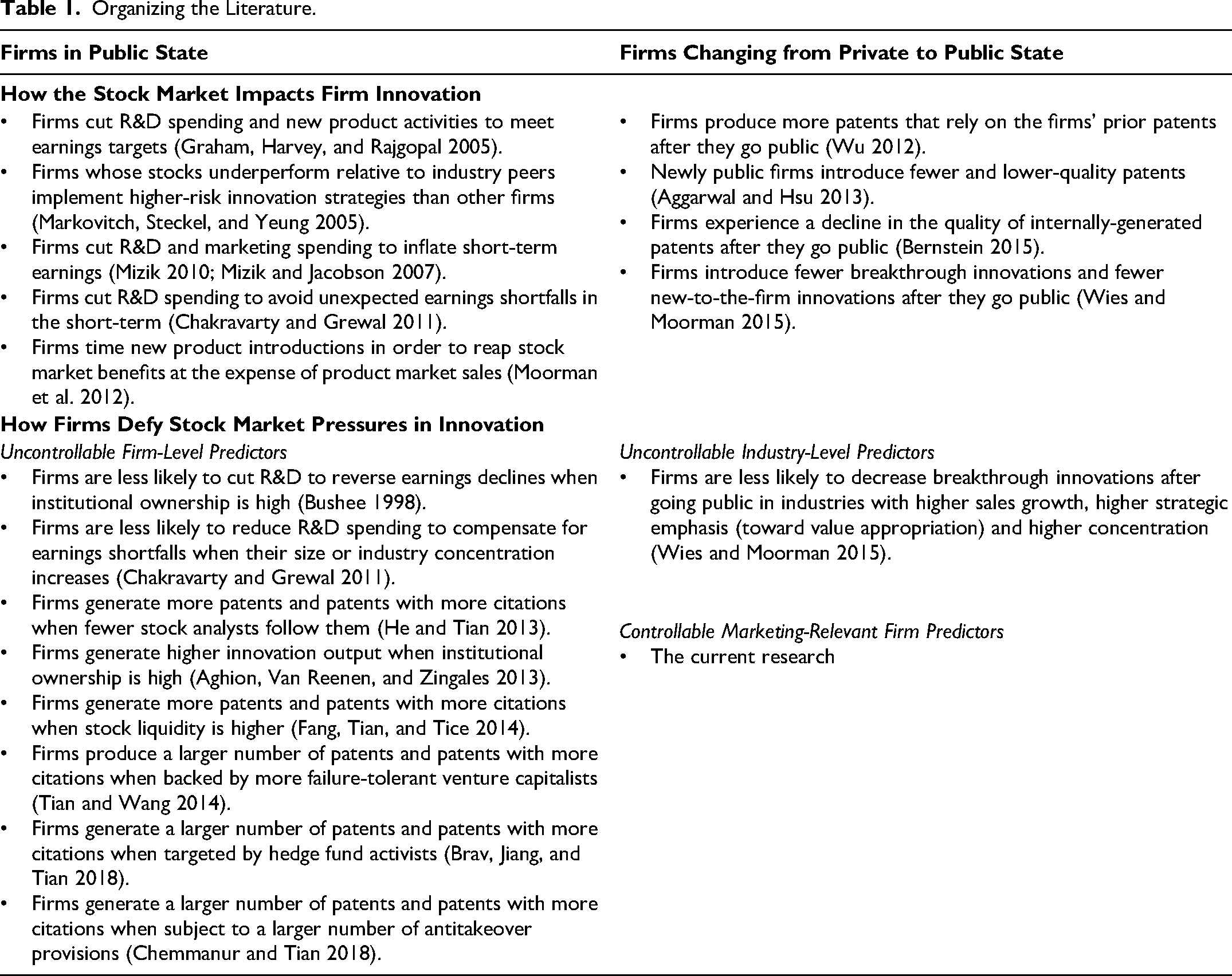

Business commentators repeatedly warn that “once companies go public … [they] have pretty much started the inevitable death of innovation” (Deeb 2014). Those who manage public companies lament that when striving to meet Wall Street's quarterly demands, it is “not always possible to focus on innovating for customers” (Dell 2014). A growing body of academic research reinforces these concerns by finding that once companies go public, they reduce their research and development (R&D) and marketing spending (Chakravarty and Grewal 2011; Mizik and Jacobson 2007), take less risk in innovating (Markovitch, Steckel, and Yeung 2005), and time the introduction of new products to maximize stock market, rather than product market, impact (Graham, Harvey, and Rajgopal 2005; Moorman et al. 2012). Other studies document declines in patent innovativeness (Aggarwal and Hsu 2013; Bernstein 2015) and in the introduction of risky innovations (Wies and Moorman 2015) after companies undergo an initial public offering (IPO). Overall, these studies suggest that going public is associated with a pronounced reduction in breakthrough innovation; a phenomenon we refer to as the “post-IPO innovation slump.”

The post-IPO innovation slump is especially striking because the purported logic for accessing public markets is often one that involves growth and innovation (Kim and Weisbach 2008). As Bodnaruk et al. (2008, p. 2818) note, an IPO allows the firm to “raise funds to finance new growth opportunities,” and investors buy shares in newly public companies in part to reap the benefits of this growth. If a substantial slump in innovation is inevitable among firms that go public, then the implications for these firms—and their investors—are discouraging.

However, there are reasons to believe that not all firms that go public are doomed to experience a post-IPO innovation slump. Empirically, the literature largely focuses on average effects across firms and industries to reach pessimistic conclusions about the slump. But averages might conceal much variance, and exceptions can be insightful (Gould 1991). Although many firms succumb to this slump, others do not. It could be instructive to understand what differentiates the latter from the former. The existing literature emphasizes the role of stock market pressures to explain why managers reduce innovation investments after they go public and thus cause harm to their firms in the long run (e.g., Mizik 2010). Though pressures from stock markets could indeed play a role in discouraging innovation, research shows that these same markets also reward innovation by publicly listed firms (Sorescu and Spanjol 2008; Tellis, Prabhu, and Chandy 2009). The literature offers few explanations for this apparent paradox.

Remarkably, no prior research has examined actions that managers can take to beat the post-IPO innovation slump (see Table 1), though studies have offered insights into industry-level factors that explain why some firms are able to do so. For example, Chakravarty and Grewal (2011) find that industry concentration reduces the slump, while Wies and Moorman (2015) observe that industry incentives such as strong sales growth weaken it. Other research, mostly in finance, has identified firm-level factors that are not under managers’ direct control, including stock liquidity (Fang, Tian, and Tice 2014), institutional ownership level (Bushee 1998), and antitakeover provisions (Chemmanur and Tian 2018).

Organizing the Literature.

In this article, we adopt a distinctive approach, which is to focus on firm-level, externally visible, marketing-relevant actions 1 that managers can take to beat the post-IPO innovation slump. In particular, we examine the marketing actions that managers can take before they go public to ensure that their firms continue to innovate even after the IPO. Consistent with this approach, we study firms as they transition from private to public—an approach that remains rare in this literature (see Table 1)—which allows us to account for the long reach of each firm's early history. We focus on breakthrough innovations, defined as new products that incorporate new technologies and/or fulfill key customer needs substantially better than existing products (Chandy and Tellis 2000), which have been shown to drop off after the IPO.

We aim to make three contributions to the literature in marketing, innovation, and the marketing–finance interface. First, we propose a managerially actionable explanation for why some firms that go public beat the post-IPO innovation slump: innovation imprinting. In our context, innovation imprinting refers to marketing-relevant actions by firms that establish product priorities and build market capabilities associated with breakthrough innovation before they go public. We argue that innovation imprinting establishes aspirations and routines within the company that support its ability to resist potential stock market pressure to shift priorities and capabilities away from breakthrough innovation after going public.

Second, we offer an explanation for the apparent contradiction in the effect of the stock market in encouraging or discouraging innovation in public firms. We argue that it is important to consider investors not as a homogenous whole—as the marketing literature tends to do—but as segments that have varying preferences (see Bushee 1998). Specifically, we propose that firms that engage in innovation imprinting attract a segment of investors whose risk preferences are more supportive of innovation than investors at large. We refer to these investors as “concordant investors.” Innovation imprinting

Third, we document that the innovation slump is by no means inevitable among firms that go public. By analyzing the innovation patterns of 207 firms in the consumer packaged goods (CPG) sector before and after an IPO, we observe that almost one-third of firms are able to maintain or beat their pre-IPO levels of breakthrough innovations after going public. To explain this effect, we present a theoretically driven measure of innovation imprinting that capitalizes on publicly available data on private firms—thereby overcoming one of the key challenges of empirical research on this topic. We show that this metric helps predict whether firms are likely to beat the post-IPO innovation slump after they go public. Moreover, we provide evidence for the mechanism we propose to explain why this occurs: innovation imprinting attracts concordant investors, who reward firms for persisting at breakthrough innovation. Our findings challenge the idea that the stock market causes an inevitable adoption of a risk-averse view that discourages breakthrough innovation. Instead, results suggest that managers can help their firms remain innovative by planting the seeds of innovation before they go public.

Conceptual Framework

Why do some firms remain innovative after they go public? We argue that the answer might lie in the innovation activities that they engage in before they go public. Following a long tradition of research on the origins of firm strategy (see Simsek, Fox, and Heavey 2015), we propose that these early activities—formally referred to as innovation imprinting—help establish innovation priorities and capabilities that support a firm's ability to resist potential stock market pressure to shift toward more incremental innovation after it goes public (see Figure 1). This view extends prior literature, which has tended to focus on how firms maintain or adapt their early identity over time. In addition, we extend the literature by advocating for a novel mechanism by which the firm maintains the activities and outcomes of its past. Specifically, we suggest that the firm's pre-IPO innovation imprinting signals to and ultimately attracts a set of investors who are less risk averse and who will support the firm's focus on breakthrough innovation. Once attracted, these investors buffer the firm from the short-term focus of the stock market and enable it to continue to innovate at pre-IPO levels. We illustrate this in Figure 1 by the mediating role that these investors play in beating the post-IPO innovation slump. Beating the slump, we predict, leads to positive and consequential outcomes—both for investors and for firms that yield higher financial returns as well as lower odds of bankruptcy.

Conceptual Framework.

This section outlines the core tenets of our proposed framework by linking the three constructs depicted in Figure 1: (1) the post-IPO innovation slump, (2) pre-IPO innovation imprinting, and (3) the role of concordant investors. We discuss each construct in turn, and then present a series of hypotheses arising from the associated framework.

Beating the Post-IPO Innovation Slump

As we have noted, the post-IPO innovation slump—a reduction in the introduction of breakthrough innovations among firms that go public—is well-documented. A key reason for this slump is that after firms go public, managers perceive pressure from the stock market that reduces their incentives to invest in breakthrough innovation. This is the case because breakthrough innovation is an inherently risky activity, and investments may fail to pay off or to do so within a predictable timeline. These aspects of breakthrough innovation are at odds with expectations from many stock market investors, who impose strict quarterly earnings targets and judge firms by their short-term performance. These investor expectations create incentives that prompt managers to optimize investments for the short term (Mizik 2010). One way to secure short-term performance is to reduce their firms’ focus on breakthrough innovation and instead fund more incremental innovation activities, which are less risky and more predictable in their outcomes. A theory of how firms beat the post-IPO innovation slump should therefore offer a mechanism that weakens this short-term stock market pressure. We introduce innovation imprinting and the attraction of concordant investors as this mechanism.

Imprinting and Breakthrough Innovation

Imprinting is a concept with a long history in the organizational sciences (Stinchcombe 1965). 2 This literature has broadly examined three types of questions. First, what are the sources of imprinting? Scholars in this area have pointed to the many different early influences—environmental, organizational, or individual—that can have a formative effect on how companies develop (Marquis and Tilcsik 2013). For example, Snihur and Zott (2020) find that founders’ tendency to engage in search outside their industry for novel stimuli leads to imprinting that facilitates business model innovation later in the firm's life. Second, what are the consequences of imprinting on strategy choice and firm performance? Simsek, Fox, and Heavey (2015) suggest that these effects can be wide-ranging (see also Marquis and Tilcsik 2013). The most common consequences at the firm level are growth, survival, and strategic change or new market entry (Simsek, Fox, and Heavey 2015. Third, what are the organizational processes and dynamics that maintain or weaken the effects of imprinting? For example, Suddaby et al. (2020) describe how imprinting facilitates the sensing of opportunities and the seizing of opportunities, while Erodogan, Rondi, and De Massis (2020) highlight how firms adopt both forward- and backward-looking approaches to balance the dual goals of maintaining tradition and achieving innovation.

We draw from and extend the literature on imprinting to develop and test marketing-related explanations for why some firms beat the post-IPO innovation slump in several ways. First, we introduce to the literature the construct of innovation imprinting, which (as we noted previously) refers to activities by firms that establish product priorities and build market capabilities associated with breakthrough innovation before they go public. In focusing on and delving deeply into innovation-specific aspects of the phenomenon of imprinting, we aim to go beyond the existing literature, which has largely addressed generic aspects of imprinting (e.g., recombination; Gioia et al. 2010) or imprinting on dimensions that are distinct from innovation (e.g., employment models; Baron, Hannan, and Burton 1999).

Second, we introduce the important role of external actors (in our case, the stock market) to explain the dynamics of imprinting. Importantly, we suggest that the external actors are a key reason why the effects of imprinting are maintained over time. Specifically, we argue that innovation imprinting attracts a segment of risk-tolerant investors who give the firm license to maintain its breakthrough innovation even after it goes public. This view is distinctive from the focus of the great majority of imprinting research, which ignores the impact of imprinting on external entities such as investors (Kimberly 1975).

Third, we highlight the role of marketing activities in imprinting. In our review of the imprinting literature, we were hard pressed to find examples of how marketing-relevant imprints have played an influential role in the firm's evolution; indeed, the literature is currently devoid of a marketing focus. We present arguments for why marketing-relevant imprints, as manifested in a firm's pre-IPO product priorities and market capabilities, can help the firm sustain its innovation outcomes. We build on these points of contribution in the following subsections.

Imprinting and product priorities

We first consider the imprinting role of the firm's strategy, which establishes its priorities and aims to build a consensus around goals and appropriate actions (Boeker 1989). Given this role, past strategic choices can frame the mental model that influences how managers perceive the firm and its environment going forward, including what is aspirational and achievable (Marquis and Huang 2010). Consistent with this view, Boeker’s (1989) study of the semiconductor producers in Silicon Valley observes that priorities established at company founding tend to be maintained over time.

In the same way, we expect that a firm's priorities regarding the development and introduction of breakthrough innovations before it goes public will have a formative effect on its post-IPO actions. Although they may manifest themselves in multiple ways, we focus on two product priorities that are under the manager's control, marketing-relevant, and transparent to the stock market. The first priority is the level of emphasis placed on the development and introduction of breakthrough innovations relative to more incremental innovations (see Sorescu, Chandy, and Prabhu 2003). The prioritization of breakthrough innovations over incremental innovations establishes the firm's acceptance of the risk associated with this focus.

A second priority pertains to the pacing of breakthrough innovations, which reflects the degree to which the development and introduction of breakthrough innovations is a consistent instead of a more sporadic feature of the firm's strategy (Brown and Eisenhardt 1997; Sharma, Saboo, and Kumar 2018). A consistent pacing of breakthrough introductions pre-IPO is a strong indicator of a company's strategy to prioritize risky innovation.

Imprinting and market capabilities

Capabilities reflect bundles of skills, accumulated knowledge, and resources that enable a firm to carry out its activities (Moorman and Day 2016). Capabilities are developed over time and form powerful routines that are deeply institutionalized in the organization's processes. As such, they are difficult to disrupt. For example, Marquis and Huang (2010) observe the persistence of acquisition capabilities from actions taken during the founding of U.S. commercial banks. Following our focus on capabilities that are under managers’ control, externally visible, and marketing-relevant, we focus on two market capabilities that meet these criteria. In both cases, the focus is on capabilities related to commercializing breakthrough innovation (Sorescu, Chandy, and Prabhu 2007).

The first capability is a firm's bundling capability (Sirmon, Hitt, and Ireland 2007), through which it combines breakthrough innovations with related incremental innovations to create platforms for future growth. For example, Home Bake extended its breakthrough product “Scoop & Bake Cookie Dough”—the first shelf-stable, nonrefrigerated cookie dough—by creating a line of related products including brownies and fudge. By building a platform for future growth, a bundling capability increases the firm's ability to manage the commercial risks associated with breakthrough innovation.

The second capability is the firm's leveraging capability which involves applying its own resources and those owned by other firms to extract value from its breakthrough innovations. Specifically, engaging in marketing alliances allows firms to leverage others’ resources to introduce breakthrough innovations across markets (see Sirmon, Gove, and Hitt 2008; Sirmon, Hitt, and Ireland 2007). A leveraging capability increases the firm's ability to reach customers across markets and to use partnerships to do so efficiently.

Summary

These arguments describe how innovation imprinting—as manifested in pre-IPO product priorities and market capabilities—can help firms manage the risks involved in developing and commercializing breakthrough innovations. This innovation imprinting increases the likelihood firms will beat the post-IPO innovation slump.

The Role of Concordant Investors in Beating the Post-IPO Innovation Slump

Our discussion thus far has offered an internal account of imprinting that is consistent with the literature. In this subsection, we add to this view by describing an external signaling mechanism that contributes to this effect. Specifically, we predict that the firm's pre-IPO innovation imprinting actions send important signals to the investor community regarding the firm's future, including its product priorities and market capabilities that are likely to persist over time (Bebchuk and Stole 1993; Moorman et al. 2012). Because investors can observe these amassed aspects of a firm's breakthrough innovation efforts, they interpret these as indicators of the firm's future innovation potential, including the ability to manage risks.

The idea of signals utilized by investors to gauge a firm's future economic value has a long research tradition in finance (e.g., Carter and Manaster 1990). Because of information asymmetries between firm owners and investors, and because owners might have incentives to misrepresent the firm to investors, research has suggested that investors will tend to ignore unsupported claims released by owners (Cohen and Dean 2005). Instead, the firm must use actions to transmit credible information about its strategy important to forming expectations for the future of the venture (Downes and Heinkel 1982), including innovation activities (e.g., Audretsch, Bönte, and Mahagaonkar 2012).

However, investors are not a homogenous group. Some have a greater affinity for risky innovation than others. We propose that the signals inherent in innovation imprinting attract a segment of concordant investors, meaning they share the firms’ tolerance for risk. They value the potentially high returns to breakthrough innovation and are commensurately more forgiving of the risk associated with these innovations relative to other investors. These characteristics make them highly compatible with the risk-taking associated with breakthrough innovations. Hereinafter, we refer to these concordant investors as “risk-tolerant investors.”

Recent work in finance points to the advantages of matching firms and investors with compatible risk profiles. Kaplan, Sensoy, and Strömberg (2009), for instance, describe how investors make their IPO investment decisions based on the IPO firm's prior business strategy, which they expect to persist in the post-IPO state. Pointing to a two-sided matching mechanism, Sørensen (2007) highlights that young firms advertise to and pick those venture capital investors who have the best strategic fit, even if it is not the best financial offer at the time of matching. Lungeanu and Zajac (2016) document the positive long-term effects of firm–investor fit on firm performance.

As risk-tolerant investors assess IPO firms, they look for credible signals that the firms align with their own innovation preferences and will persist in breakthrough innovation in the long term. The logic we have articulated suggests that firms that have engaged in innovation imprinting will be more likely to offer such signals. This increases the likelihood that they will attract risk-tolerant investors once they go public.

Together, H1 and H2 imply that the attraction of risk-tolerant investors is an important mechanism by which innovation imprinting increases the likelihood that firms will beat the post-IPO innovation slump. We predict the following:

Long-Term Effects of Beating the Post-IPO Innovation Slump

What is the impact of beating the post-IPO innovation slump on long-term performance outcomes of the firms in question? Does it help them improve their financial performance and survive over the long run? We examine both outcomes next.

Financial performance

A significant body of literature has examined the returns to innovation (Sorescu, Chandy, and Prabhu 2003; Sorescu and Spanjol 2008; Srinivasan et al. 2009). This literature indicates that the stock market rewards persistent breakthrough innovation by firms. The stock market values breakthrough innovations because they offer new customer benefits that grow markets and form barriers to entry for competitors.

However, and relevant to our article, this literature has not considered the performance impact of breakthrough innovation in the context of IPO firms. Further, our question is not whether breakthrough innovation is per se a predictor of financial performance. Instead, we focus on whether maintaining or exceeding pre-IPO breakthrough innovation levels after going public is noticed and rewarded by investors. We think the answer is yes for two reasons. First, firms that beat the post-IPO innovation slump are likely to have attracted risk-tolerant investors who will disproportionally reward the introduction of breakthrough innovations. Second, consistent with our signaling story, maintaining or exceeding the level of breakthrough innovation relative to pre-IPO levels represents a strong signal of firm strategy, confidence, and competitive viability that should be rewarded by these risk-tolerant investors.

Survival

The aforementioned financial returns provide the resources to innovative firms to further develop their innovation pipelines, thus setting the stage for a potential virtuous cycle of innovation and returns. Such a cycle should also bode well for firm survival. Because breakthrough innovations generate larger revenues and profits (Pauwels et al. 2004), beating the post-IPO innovation slump in breakthrough innovation should help firms compete more effectively, leading to better odds of survival in competitive markets. We predict the following:

Data and Measures

Empirical Context and Data Sources

An ideal empirical context to test our hypotheses would fulfill three criteria. First, IPOs and breakthrough innovations should be widely prevalent in the context, thus ensuring an adequate sample size for rigorous tests of our hypotheses. Second, objective and reliable information should be available on each of the constructs of interest. Importantly, information on the imprinting factors should be available when firms are privately held (and not required to disclose information) and over a period of time that is long enough to assess the impact on long-term outcomes. Third, the context should be economically significant and yet should not be constrained by unique regulations (such as in pharmaceuticals) that might limit generalizability.

The U.S. CPG sector meets each of these criteria. First, the CPG sector is one of the largest sectors in the United States, and it is economically significant, supporting one in ten U.S. jobs and contributing over $2 trillion to the U.S. gross domestic product (PwC 2019). Second, CPG firms have traditionally aimed to innovate as a source of growth, and data sources are available over time (e.g., through ProductLaunch Analytics). 3

To test our predictions, we assemble a data set using several secondary sources: (1) Datamonitor's ProductLaunch Analytics for new products, (2) EDGAR and SDC Platinum for IPOs (Global New Issues Database) and alliances (Mergers, Acquisitions and Alliances Database), (3) Compustat for financial data, (4) Thomson Reuters Institutional 13f Holdings for risk-tolerant investors, (5) ReferenceUSA and the Center for Research in Security Prices for firm age, (6) Factiva for firm size, and (7) IRI's Marketing Factbook for category controls.

Sample

Our predictions are tested on a sample of 207 CPG firms that went public between 1980 and 2011. This sample reflects 4,312 firm-year observations with an unbalanced number of years before and after the IPO. We restrict our sample to firms for which we have at least three years of data pre- and post-IPO to examine firm innovation behaviors before and after the IPO. In the process of building the sample, we identified firms that remained private during this period. We used these firms to build a sample of 158 private firms, reflecting 3,591 firm-year observations, for endogeneity corrections and robustness tests.

Measures

Breakthrough innovations

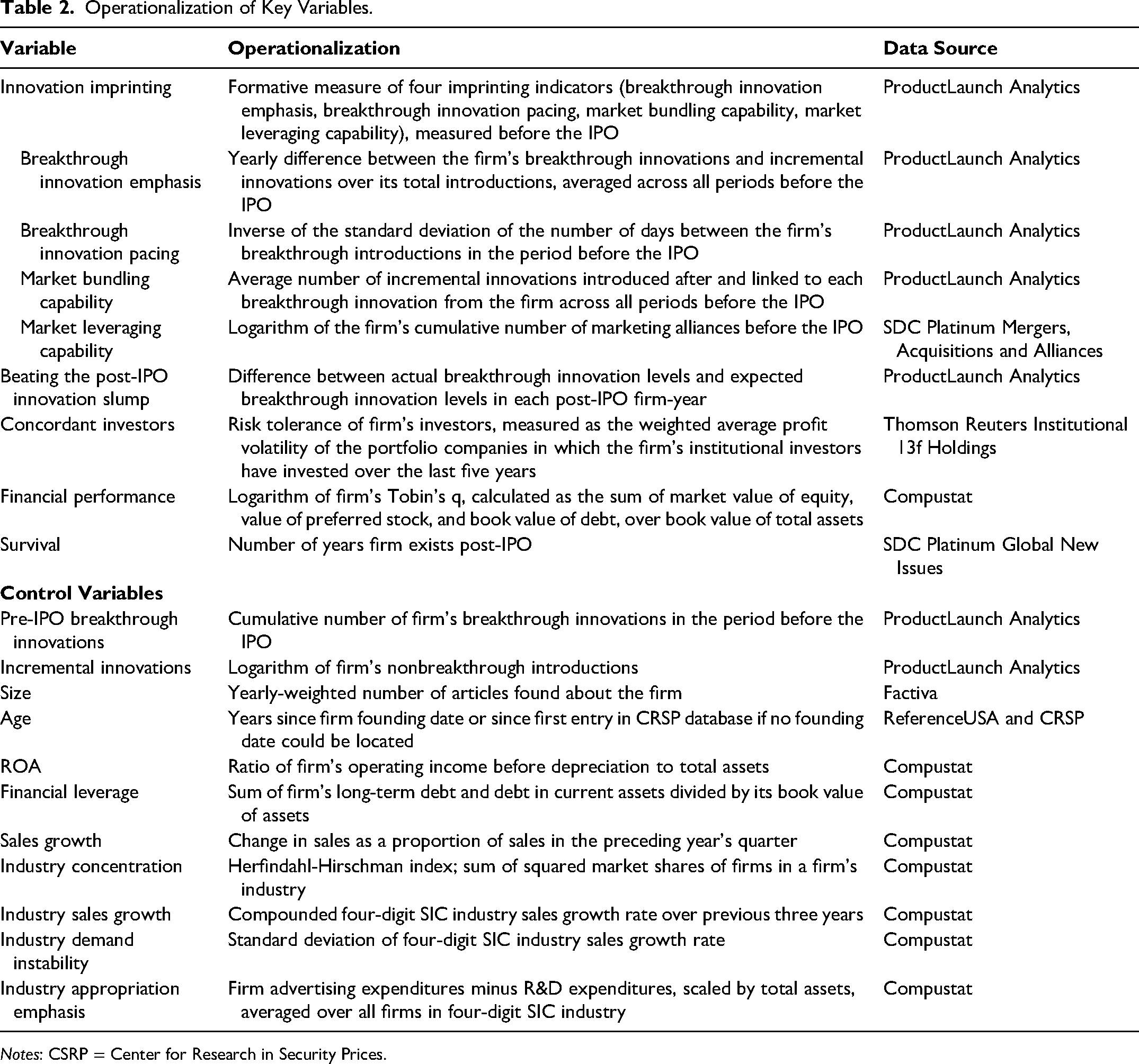

We collect the number of firm breakthrough innovations introduced by U.S. firms into U.S. food, drug, and mass channels using Datamonitor's ProductLaunch Analytics. ProductLaunch Analytics counts each new product introduction as an innovation and defines an innovation as “breakthrough” if it targets a new market and/or offers a substantially new consumer benefit through product positioning, merchandising, packaging, formulation, or technology (Sorescu and Spanjol 2008). We count the number of firm breakthrough innovations per year and take the logarithm given its skewed nature, adding 1 when zero products are introduced to avoid losing observations. Examples of breakthrough innovations include, in packaging, DFV Wines’ bag-in-box wine equipped with a tap technology to keep the wine fresh after opening (2011); in technology, Unipath Diagnostics’ digital pregnancy tests (2003); and in the new market area, Big Heart Pet Brands’ dog treats that prevent gum disease (2013). Table 2 summarizes our key variables’ data sources and operationalizations.

Operationalization of Key Variables.

Notes: CSRP = Center for Research in Security Prices.

Pre-IPO innovation imprinting

Innovation imprinting refers to pre-IPO actions by firms that establish product priorities and build market capabilities associated with breakthrough innovation. Given our theoretical focus on imprinting actions that are under managers’ control, are externally visible before the IPO, and have a marketing focus, we wanted to balance conceptual comprehensiveness with empirical feasibility. Four measures were qualified as relevant to breakthrough innovation, reflecting two dimensions of product priorities (emphasis and pacing) and two dimensions of market capabilities (bundling and leveraging).

Considering the product priorities, we measure level of emphasis on breakthrough innovation in a manner analogous to Mizik and Jacobson’s (2003) measure of strategic emphasis. Specifically, we calculate the average of the following ratio before the IPO:

We capture pacing of breakthrough innovation by the inverse of the standard deviation of the number of days between the firm's breakthrough introductions in the period before the IPO. A lower value indicates higher variability in introducing breakthrough innovations, and a higher value indicates a more consistent pace of breakthrough introductions.

Regarding market capabilities, we measure bundling of breakthrough innovation as the pre-IPO average number of incremental innovations introduced after and linked to each breakthrough innovation from the firm. To form this measure, we searched in ProductLaunch Analytics for the number of bundled incremental innovations the firm introduced as an offspring of the breakthrough innovation. To qualify as part of the breakthrough innovation bundle, an incremental innovation needed to satisfy two conditions: the product had to be introduced (1) within the following 12 months of the original breakthrough innovation and (2) under the same brand name and in the same category as the original breakthrough innovation.

Recall that leveraging is an aspect of a firm's breakthrough innovation capability that addresses the extent to which the firm can apply breakthrough innovations beyond its own market boundaries. We measure leveraging of breakthrough innovation as the logarithm of the firm's cumulative number of marketing alliances before the IPO.

We view these four variables as indicators of the formative measure of innovation imprinting. We therefore create our measure following standard procedures for formative measures (see Web Appendix A for details). Using the unweighted average of the four standardized indicators as our main measure, we validate the robustness of our results using alternative weighting schemes and operationalizations.

Concordant investors

Recall that concordant investors share the firm's tolerance for risk and predisposition toward breakthrough innovation. We derive investors’ tolerance for risk by studying their past investment behavior. This approach is similar to Abarbanell, Bushee, and Raedy (2003) and Bushee and Goodman (2007), who derive investors’ preference for growth based on their past trading behavior. First, we identify a firm's investors using the Thomson Reuters Institutional 13f Holdings database. For data availability reasons, we focus on the firm's institutional investors. This choice is also conceptually reasonable because institutional investors have a larger impact on firm behaviors than retail investors (Basak and Pavlova 2013). Second, for each investor, we retrieve their portfolio of companies over the last five years, as captured in the Thomson Reuters Institutional 13f Holdings database. We then proxy the riskiness of each company in this portfolio by its profit volatility, measured as the industry-adjusted standard deviation of profits in the prior five years (e.g., Myers, Myers, and Skinner 2007). We construct this measure based on the view that if an investor holds a stake in companies with high profit volatility, they are less likely to exert short-term performance pressure on the focal firm than other investors. We average the profit volatility across all firms an investor holds in their portfolio to proxy an investor's risk tolerance. Finally, to arrive at our firm-level measure, we average the risk tolerance of the firm's investors, weighted by the investors’ shares in the firm.

Financial performance

We measure financial performance by the firm's Tobin's q, an established proxy for firm performance in the marketing literature (e.g., Rao, Agarwal, and Dahlhoff 2004). Following Chung and Pruitt (1994), we calculate Tobin's q as the logarithm of TQi,t = (MVEi,t + PSi,t + BVDi,t)/TAi,t, where MVEi,t is the market value of equity, PSi,t is the value of preferred stock, BVDi,t is the book value of debt, and TAi,t is the book value of total assets for firm i in year t.

Survival

The firm's survival duration is measured in number of years it exists post-IPO. We code each year as 1 in which the firm still operates, and code it as 0 if the firm's legal status is bankruptcy or liquidation. We classify firms that were acquired by other firms as surviving firms (although results hold if we code the acquired firms as dead).

Control variables

We include a comprehensive set of firm and industry control variables as described in Web Appendix B and listed in our model descriptions that follow.

Modeling and Estimation Approach

We describe four sets of models associated with our research questions. First, we model the degree to which firms beat the post-IPO innovation slump. Second, we model whether innovation imprinting helps explain this outcome. Third, we model how innovation imprinting attracts concordant investors and test the mediating mechanism we outline in our hypotheses. Finally, we model the rewards associated with beating the innovation slump after going public in terms of firm financial performance and survival.

Do Firms Beat the Post-IPO Innovation Slump?

We begin by examining whether firms can actually beat the post-IPO innovation slump—that is, whether they continue to introduce breakthrough innovations after the IPO. To do so, we compare the actual breakthrough innovation levels in each post-IPO year with the expected breakthrough innovation levels in each post-IPO year. As our test, we build a breakthrough innovation prediction model based on a firm's pre-IPO observations to determine the predicted level of breakthrough innovations for each post-IPO firm-year. Using only the pre-IPO observations, we estimate the following fixed-effects autoregressive model:

Table 3 contains results of this model estimation, which is significant (χ2 = 1465.75, p < .01). We use the estimated coefficients from this pre-IPO regression to predict breakthrough innovation levels for the post-IPO firm-years (t > T(IPOi)) and to compute the difference between the actual and predicted number of breakthrough innovations for each post-IPO firm-year:

Breakthrough Innovation Prediction Model.

*p < .10.

**p < .05.

***p < .01.

Notes: Robust standard errors in parentheses. All variables are at the firm level unless noted as industry level. All variables are measured in period t unless specified as (t − 1).

This variable reflects the degree to which the firm beats the post-IPO innovation slump in a given year and is a key measure in testing our hypotheses. It is continuous and positive if the firm exceeds the expected level of breakthrough innovations in a given post-IPO year, negative if not, and zero if the firm exactly meets the expected level of breakthrough innovations.

Does Innovation Imprinting Help Firms Beat the Post-IPO Innovation Slump?

To test the idea that innovation imprinting helps firms beat the post-IPO innovation slump, several modeling options exist with differing strengths and weaknesses. We present the strongest test here and offer two more as robustness checks. Following Equation 2, our selected approach uses the degree to which the firm beats the innovation slump in a given post-IPO year as the dependent variable. We estimate

Our empirical setup has an important implication for estimating Equation 3. Given our focus on beating the post-IPO innovation slump, we observe the difference between actual and predicted breakthrough innovation levels only for firms that have gone public. To prevent the estimated coefficients in our model from being influenced by potential selection biases associated with the decision to go public, we employ a two-stage Heckman-type approach in which we first model the firm's choice to go public. To do so, we add the sample of 158 private CPG firms identified in ProductLaunch Analytics that did not go public in the observation period. We estimate the firm's likelihood of going public with a Probit model:

Using this exclusion restriction, we compute the inverse Mills ratio (IMR) as λ = ϕ(β′Xi,t)/Ф(β′Xi,t), where ϕ and Ф are the probability density function and cumulative density function of the normal distribution, respectively, and add it as a predictor in Equation 3. Web Appendix C offers further evidence regarding why we are not concerned about the potential endogeneity of firm choice to go public in our modeling setup.

Does Innovation Imprinting Attract Concordant Investors?

To test whether innovation imprinting helps attract more risk-tolerant investors, we estimate the following model:

To examine whether the attraction of risk-tolerant investors mediates the relationship between innovation imprinting and the ability to beat the post-IPO innovation slump, we test a mediation model following the bias-corrected procedure suggested by Zhao, Lynch, and Chen (2010) with 5,000 bootstrapped samples.

Are Firms Rewarded in the Long Term for Beating the Post-IPO Innovation Slump?

Financial performance

This model examines whether beating the post-IPO innovation slump is associated with a stronger firm financial performance:

Firm survival

Finally, we test whether the degree of beating the post-IPO innovation slump affects firm survival with an accelerated failure-time (AFT) model:

Results

Do Firms Beat the Post-IPO Innovation Slump?

Beginning with a test of whether firms beat the post-IPO innovation slump in a given year, we corroborate prior research and find that the majority of firms innovate at lower breakthrough levels than their pre-IPO levels would predict. Figure 2 shows the distribution of the degree to which firms manage to beat their predicted breakthrough innovation levels post-IPO (Beat_Innovation_Slump, Equation 2). Negative values indicate that the firm did not meet its predicted post-IPO level, zero indicates that the firm did reach its predicted post-IPO level, and positive values mean that the firm beat this level. The mean level of −.068 (SD = .394) confirms that most firms succumb to the post-IPO innovation slump. Specifically, in 69.6% of firm-year observations, firms fail to meet their predicted levels of breakthrough innovations (i.e., negative realizations) while firms beat these predicted levels (i.e., positive realizations) in 30.4% of observations. We do not observe any firm-years in which predicted levels are met exactly.

Distribution of Degree of Beating the Post-IPO Innovation Slump.

A second set of descriptive analyses examines whether firms persistently beat the innovation slump across their post-IPO years. Figure 3 displays the kernel density plot of the proportion of years each firm beats the innovation slump measured as a count of the number of post-IPO years in which firm i beats the post-IPO innovation slump (i.e., has positive realizations of Equation 2) divided by the total number of the firm's post-IPO years. If succumbing (beating) to the innovation slump is persistent, we should observe this ratio's observations clustered close to zero (one). As the clustered observations close to zero show, most firms rarely meet or exceed their predicted breakthrough innovation levels in any of the public-year observations. The lower spike towards the right end of the distribution, however, suggests that some firms manage to do so consistently across post-IPO years. Table 4 summarizes further descriptive features of our sample firms and presents correlations among the variables of interest.

Frequency of Firms Beating the Post-IPO Innovation Slump.

Descriptives and Correlations.

Notes: All correlations above .022 are significant at p < .05. All variables are at the firm level unless noted as industry level.

Does Innovation Imprinting Help Firms Beat the Post-IPO Innovation Slump?

Having established that some firms beat the post-IPO drop in breakthrough innovations, we turn to the role of innovation imprinting as a predictor that influences this outcome. Table 5 shows our results. Column 1 provides our focal model employing the overall innovation imprinting measure. The model's adjusted R2 (R2 = .51) and Wald statistic (χ2 = 1,865.37, p < .01) point to satisfactory explanatory model power and fit. A variance inflation factor below ten suggests that multicollinearity is not a concern. In support of H1, we find that pre-IPO innovation imprinting helps firms beat the post-IPO innovation slump (β1 = .159, p < .01).

Innovation Imprinting Helps Firms Beat the Post-IPO Innovation Slump.

*p < .10.

**p < .05.

***p < .01.

Notes: Column 1 tests the composite innovation imprinting measure, Column 2 tests the four individual measures of innovation imprinting, and Column 3 repeats the individual test using standardized coefficient estimates. Robust standard errors in parentheses. All variables are at the firm level unless noted as industry level.

Column 2 of Table 5 provides results using the four separate imprinting indicators. Similar to the composite measure, we find that all four indicators increase the firm's likelihood of beating the post-IPO innovation slump. Column 3 reports standardized results of the four separate indicators, which is helpful in interpreting their magnitudes.

Does Innovation Imprinting Attract Concordant Investors?

We next consider the role of concordant investors in explaining how innovation imprinting helps firms beat the post-IPO innovation slump. H2 posits that innovation imprinting attracts more risk-tolerant investors, and Table 6 reports results from the test of this hypothesis. Results indicate good model fit (R2 = .145, χ2 = 912.91, p < .01). As we predicted, imprinting has a positive effect on the attraction of more risk-tolerant investors (β1 = .051, p < .01).

Innovation Imprinting Attracts Concordant Investors.

*p < .10.

**p < .05.

***p < .01.

Notes: Robust standard errors in parentheses. All variables are at the firm level unless noted as industry level.

H3 hypothesizes that innovation imprinting attracts more risk-tolerant investors, who in turn grant the firm leeway to persist at breakthrough innovation once it has gone public. This structure reflects a mediation model, which we test using the guidelines in Zhao, Lynch, and Chen (2010). We find that innovation imprinting has a positive effect on attracting risk-tolerant investors. The risk-tolerance of investors, in turn, increases the firm's likelihood of beating the innovation slump after it goes public (indirect effect = .003, p < .01, 95% confidence interval: [.001, .005]).

In addition to testing the mediating mechanism, this estimation approach (reported in Web Appendix D) also serves as a robustness check because it models the equations simultaneously (as opposed to each equation separately, as we do in the main analysis).

Are Firms Rewarded in the Long Term for Beating the Post-IPO Innovation Slump?

Tobin's q

We begin with model-free evidence to test H4. Specifically, the difference in Tobin's q between firms beating and succumbing to the post-IPO innovation slump is substantial—in the first year, Tobin's q is 57% higher for firms that beat the slump.

Table 7 presents the results of estimating Equation 6 to test the effect on Tobin's q. Confirming our expectation (H4), we find that firms that beat the post-IPO innovation slump have a higher Tobin's q (β1 = .609, p < .01). For instance, a firm that beats its expected level of breakthrough innovations (two) by one additional breakthrough innovation increases Tobin's q by .25—amounting to an average increase of 12% in Tobin's q. This insight extends prior research, which has been limited to showing that breakthrough innovations have a stronger effect on firm performance than incremental innovations (Srinivasan et al. 2009).

Beating the Post-IPO Innovation Slump Improves Tobin's q.

*p < .10.

**p < .05.

***p < .01.

Notes: Robust standard errors in parentheses. All variables are at the firm level unless noted as industry level.

Finally, although not theorized, when combined, our predictions imply a serial mediation model in which pre-IPO innovation imprinting increases the attraction of more risk-tolerant investors, which, in turn, increases the likelihood of beating the post-IPO innovation slump and ultimately Tobin's q. Our results support this serial mediation model (indirect effect = .003, p < .05, 95% confidence interval: [.0003, .005]).

Survival

H5 predicts that firms that beat the innovation slump will have a higher survival likelihood. Table 8 displays the results of estimating Equation 7. In line with H5, beating the post-IPO innovation slump increases firm survival likelihood (β1 = .401, p < .01). To facilitate interpretation of the magnitude of this effect, we transform the coefficient [100 × (exp(β1) − 1)] to calculate the percentage change in expected survival time when firms beat the post-IPO innovation slump. For instance, a firm that beats its expected level of breakthrough innovations of two by one additional breakthrough innovation can increase its likelihood of survival by 20%. 6

Beating the Post-IPO Innovation Slump Improves Firm Survival.

*p < .10.

**p < .05.

***p < .01.

Notes: Robust standard errors in parentheses. All variables are at the firm level unless noted as industry level.

Additional Analyses and Robustness

Do Results Hold Up to Alternative Modeling, Timing, and Measurement Choices?

Alternative models

We assess the robustness of our key finding that imprinting increases the likelihood of beating the post-IPO slump with two approaches. First, we repeat our analyses using a new sample that includes both the IPO and private firm samples and model the post-IPO innovation slump as an interaction with firm's private or public state. We estimate the following:

In a second robustness check, we use innovation imprinting to predict the ratio of post-IPO years in which the firm beats the innovation slump to the total post-IPO years:

Alternative timing specifications

We examine the impact of different timing specifications and find all of our results replicate (for details, see Web Appendix F).

Alternative measure of Tobin's q

We discuss the appropriateness of Tobin's q as measure of firm performance in Web Appendix G and show the robustness of our results to alternative model specifications and to using Total q.

Do Post-IPO Resources Influence Results?

We examine the impact of four post-IPO resources as additional controls in Equation 3. First, we include the level of IPO proceeds and the percentage of equity sold to capture the financial resources available to firms undergoing an IPO. Second, we control for resource slack that might enable firms to invest in breakthrough innovation, including ROA, financial slack, excess cash, and human resource slack. Third, we add advertising and R&D expenses given that they should influence innovation. Fourth, we control for post-IPO executive turnover in the top management team. Our results replicate across all models (see Web Appendix H).

Does the Stock Market Reward Pre-IPO Innovation Imprinting?

Our H5 results show that investors reward firms for beating the post-IPO innovation slump. Next, we offer three additional tests that support the view that investors reward firms for pre-IPO innovation imprinting both at the IPO and after the IPO when they introduce new products, while punishing firms less severely if they report a sales drop post-IPO.

Investor response at the time of the IPO

We examine whether innovation imprinting influences two measures of investor valuation when the firm goes public. IPO trading is the number of shares traded relative to the total number of shares available on the first day when stocks are listed in financial markets. Higher IPO trading indicates strong interest for a stock. IPO underpricing is the extent to which a firm's stock closes at a price higher than the initial offering price on the first trading day (Ritter and Welch 2002). The larger the gap between closing price and offering price, the more the stock is underpriced. We respectively regress IPO trading and IPO underpricing on pre-IPO innovation imprinting and control variables. Results in Table W14 in Web Appendix I suggest that innovation imprinting is associated with higher IPO trading but not IPO underpricing, though the effect is in the expected direction. These results offer partial support for the stock market's positive response to innovation imprinting. A larger sample of IPOs would be required for a more definitive test of these effects.

Investor response after the IPO: introducing breakthrough innovations

Investors should also reward the firm for introducing breakthrough innovations when it has engaged in pre-IPO innovation imprinting. To test this, we calculate abnormal returns for breakthrough introductions after the IPO using an event study, and regress these returns on the firm's pre-IPO innovation imprinting level. Results in Table W15 in Web Appendix J support this view.

Investor response after the IPO: reporting sales drop

We also expect investors to be more forgiving when firms that have engaged in pre-IPO innovation imprinting report a post-IPO drop in sales. We test this idea by regressing yearly stock returns on an interaction of sales drop and innovation imprinting and the covariates from Equation 3. Sales drop is equal to 1 if the firm reported negative revenue growth and 0 if the firm reported zero or positive revenue growth. Results indicate that engaging in innovation imprinting weakens the negative effect of sales drop on stock returns (β = .052, p < .05, Table W16 in Web Appendix K).

Does Pre-IPO Innovation Imprinting Influence Firm Risk?

There are two ways pre-IPO innovation imprinting could be related to firm risk. On the one hand, innovation imprinting is associated with higher breakthrough innovation activities, which is likely to increase overall firm risk. On the other hand, innovation imprinting is a way of managing and reducing innovation risk, which is likely to decrease overall firm risk. Testing these possibilities, we find no significant impact of innovation imprinting on firm risk (Table W17 in Web Appendix L). We also test whether beating the post-IPO innovation slump is associated with higher firm risk but find no significant effect (Table W17).

Is the Post-IPO Innovation Slump the Outcome of a Strategic Value Extraction Choice?

Our article is premised on the view that the post-IPO innovation slump occurs because firms succumb to short-term stock market pressures after they go public. However, an alternative view is that firms make a strategic choice to stop engaging in breakthrough innovation after going public. Decision makers in the firm may do so to monetize their existing innovations or to simply cash out and to seek other pursuits. Although such a choice is conceivable, our arguments and results show that such a choice would lead to negative and consequential outcomes for both investors and firms. It would therefore not be an especially astute choice for the firm.

Indeed, our arguments and results suggest that the strategic choices that firms make early in their lives to invest in innovation imprinting yields persistence in innovation outcomes even after these firms go public. Specifically, firms that engage in value creation through innovation imprinting early in their lives tend not to switch to value extraction mode after they go public. This is because they draw a group of concordant investors who share their tolerance for risky innovation activities. Furthermore, we find that decision makers in firms that engage in innovation imprinting are no more likely to leave their companies after the IPO than those in firms that do not engage in such imprinting. Specifically, we find no difference in top management turnover at the time of the IPO between firms engaging in innovation imprinting and those that do not (Mhigh_imprinting = 1.69 vs. Mlow_imprinting = 1.63; t = −.72, n.s.). Web Appendix M presents additional evidence to rule out that the post-IPO innovation slump is the outcome of a strategic value extraction choice.

Discussion

Our research addresses an important puzzle: Why do some firms remain innovative after they go public, whereas going public yields a slump in innovation for many others? A substantial literature—in marketing, management, and finance—focuses on the explanations for the latter half of the question. We aim to offer an answer to the puzzle as a whole with a particular emphasis on the former half of the question. We predict and find that the seeds of success or failure in breakthrough innovation among firms that go public are sown early. We propose a parsimonious, managerially actionable, and marketing-centric framework to explain the differing fates of firms that succumb to the post-IPO innovation slump relative to those that beat it.

To do so, we introduce a new theoretical construct—innovation imprinting—and outline a coherent set of actions associated with this construct that managers can take before their firms go public to help them beat the post-IPO innovation slump. A key reason for the beneficial outcomes of innovation imprinting rests in the idea that firms that engage in innovation imprinting are able to signal to and attract a concordant segment of risk-tolerant investors. These investors, in turn, support the continued introduction of risky innovations after the firm's IPO. Moreover, firms that are able to beat the post-IPO innovation slump are rewarded financially and are more likely to survive over the long term. Next, we discuss the implications of our findings while acknowledging limitations and offering future directions for research.

Theoretical Implications

Exceptions can suggest new rules

Previous research on the impact of going public suggests a general rule: breakthrough innovation declines once firms go public because many firms succumb to stock market pressures that seemingly discourage risky, long-term investments (e.g., Markovitch, Steckel, and Yeung 2005; Moorman et al. 2012). Our research highlights the insights to be gained from studying the exceptions to this rule—the firms that continue to introduce breakthrough innovations after they go public. By documenting the actions of these firms—not the averages—we offer insights to help managers prevent their firms from falling prey to this effect. Our perspective is similar in spirit to Chandy and Tellis (2000), who challenge the seemingly inevitable status of the incumbent's curse by understanding the conditions under which existing industry members continue to innovate. This perspective also responds to recent calls to develop “strategy to beat the odds” by identifying actions that challenge industry norms and endowment effects (Bradley, Hirt, and Smit 2018). We hope our findings will encourage more research that adopts this focus on helping firms beat the average as a means to add more value to customers and investors (Pascale, Sternin, and Sternin 2010).

Early imprints have profound consequences

We introduce the concept of innovation imprinting to the marketing literature and articulate a simple set of reasons why imprints set before the firm goes public can have long-term consequences. Our arguments and results show that strategic choices made fairly early in a privately owned firm's life can determine later outcomes that occur under the glare of stock markets. Indeed, we argue and show that the consequences of imprinting are far from trivial: they include outcomes as fundamental as the persistence of breakthrough innovation, financial performance, and the very survival of the firm.

Our approach has at least three benefits from a theoretical perspective. First, we focus on a set of imprinting-related actions that firms can take before they go public. This proactive view extends the marketing–finance literature, which has tended to focus on firms that have already gone public (see Table 1). Once firms go public, however, the die could already be cast—in other words, expectations from investors are set, and pressures on managers to conform to these expectations are high. Our research emphasizes the importance of studying actions taken when firms have not yet gone public—and, therefore, before perceptions of their product priorities and market capabilities have solidified in the minds of internal and external stakeholders.

Second, the imprinting-related actions we highlight are under the direct control of managers. This agentic view is an important shift in theoretical focus, because prior research (see Table 1) has tended to focus on industry factors or firm factors not under managers’ direct control. Importantly, we find that the industry factors become less significant when innovation imprinting is added as explanatory variable. This implies that managers are not necessarily passive recipients (or indeed victims) of pressures from the stock market. Our research therefore points to the value of studying ways in which managers can be agents of their own destiny, even when confronted with shareholder pressure to take myopic or misguided actions.

Third, we focus on product priorities and market capabilities that are closely linked to the role of marketing in the firm. This marketing-relevant approach goes beyond the existing literature on imprinting, which tends to focus on generic organizational processes and not on the content of the firm's innovation activities.

Segmentation applies to investors too

A fundamental contribution of marketing thinking to the world of business is the idea that consumers are not a homogenous whole: there exist segments among consumers who have different preferences and propensities to purchase products. Thus, it is especially remarkable that marketing scholars have rarely applied this fundamental principle to explain the behavior of investors. Investors, much like consumers, are not a homogenous whole: there exist segments among investors who have different preferences and propensities to purchase stocks from companies (see Bushee 1998; Tian and Wang 2014). Moreover, just as marketing-related actions by a firm can attract segments of customers who share its values and support its actions, so can marketing-related actions by the firm attract segments of investors who share its values and support its actions toward innovation. Introducing this idea to the marketing literature is a central contribution of this research. Relatedly, and another key contribution, is the suggestion that attracting a concordant segment of risk-tolerant investors who are more forgiving of the risk associated with breakthrough innovations serves as a mechanism by which innovation imprinting helps firms beat the post-IPO innovation slump.

Innovation imprinting has many audiences

Research has tended to view the power of imprinting from the lens of its effects on internal stakeholders. We highlight the power of imprinting on external stakeholders. Although we have focused on investors, it is conceivable that innovation imprinting influences other groups of external stakeholders too. These groups could include consumers and channel intermediaries who witness the firm's imprinting actions, thus predisposing them to have a favorable response to the firm's breakthrough innovations. Barone and Jewell (2013) refer to this idea as “innovation credit” and find that it gives firms greater license to innovate by violating category norms. The same may hold true for competitors who could be dissuaded from entering sectors that house firms with strong imprinting. This view is consistent with Suddaby et al.’s (2020, p. 530) point that managers can use the firm's imprinting to “construct convincing scenarios of the future” and “enroll key stakeholders in the industry to support a strategic direction that advances the firm's strategic goals.”

Substantive Implications

Assert agency over the post-IPO future

Our research offers managers four actions they can take before they go public that should offer more agency over beating the pre-IPO innovation slump than prior literature has surfaced. We focus on imprinting actions that are under managers’ direct control and are embedded in the firm's product priorities and market capabilities. Importantly, these actions are also individually valuable, indicating that managers have choices regarding how they might foster imprinting depending on firm resources.

Target segments of concordant investors

Our findings also point to the importance of attracting risk-tolerant investors who are in sync with the firm's focus on breakthrough innovation. This concordance enables the firm to focus on the long run—a horizon that is necessary when managing breakthrough innovations—and not to worry that transitory sales drops might be punished by investors. Because this mechanism is one means by which firms can beat the post-IPO innovation slump, it is important that firms offer sufficiently clear and strong signals to the investing community regarding their product priorities and market capabilities. Consistent with prior research (Bebchuk and Stole 1993), our research focuses on observable actions of underlying priorities and capabilities. Future research could extend this work by offering additional insight into how firm reporting and other communication strategies might support the ability to signal the firm's focus on breakthrough innovation.

Future work might also expand the approach to segment investors. We focus on classifying investors based on their tolerance for profit volatility. This choice has conceptual appeal, because earnings management is considered a key obstacle for innovation. Future research could explore other approaches, such as those based on growth/value (see Abarbanell, Bushee, and Raedy 2003)—an approach that was not suitable for our single-sector CPG context.

Don't overlook the strategic value in incremental innovations

Our results suggest an important role for incremental innovations. Specifically, we identified the firm's bundling capability, through which it combines breakthrough innovations with related incremental innovations to create platforms for future growth. This points to a heretofore unacknowledged strategic role for incremental innovation. Instead of reinforcing the view that incremental and breakthrough innovations require resource trade-offs and should be managed as separate processes, our findings indicate an important complementarity that should be managed by firms working to build a strategy on breakthrough innovation.

Limitations and Additional Future Research

There are several limitations associated with our article that also offer opportunities for future research. The first limitation is that our measure of innovation imprinting, while focused on observable marketing-related factors under the control of managers, does not include all possible pre-IPO strategic actions. It could be expanded to include other actions that are visible to investors before the IPO, including value protection mechanisms such as patents and trademarks that could help the firm beat the slump. 7 If observable beyond financial disclosures, research could examine the role of business model innovation, brand introductions, and novel advertising investments. Non-marketing-related factors are also likely important in determining which firms can beat the slump. Access to financial resources, such as the presence or reputation of venture capitalists, for instance, might encourage firms to pursue breakthrough innovation.

Second and relatedly, we offer an investor-attraction mechanism that helps explain why innovation imprinting can protect the firm from the post-IPO innovation slump. We acknowledge that this mechanism is but one mediating path. Future research should explore additional mechanisms. Finally, our findings pertain to the CPG sector. Although this is a large and important sector that relies on innovation, future research should also investigate the generalizability of our findings to other sectors.

Conclusion

Going public is an important event in the life of a firm. The firm enjoys access to more capital but also faces pressures that affect its willingness to develop and introduce breakthrough innovations. We find that CPG firms beat the post-IPO innovation slump in only 30% of observations. Our findings indicate that firms are more likely to do so when they have engaged in innovation imprinting before they go public. These imprinting actions improve the odds of beating the post-IPO innovation slump, in part, because they attract more risk-tolerant investors who believe the firm can effectively manage the risks associated with breakthrough innovations. These investors reward these firms with stronger valuations, and the firms survive longer.

Supplemental Material

sj-pdf-1-jmx-10.1177_00222429221114317 - Supplemental material for Innovation Imprinting: Why Some Firms Beat the Post-IPO Innovation Slump

Supplemental material, sj-pdf-1-jmx-10.1177_00222429221114317 for Innovation Imprinting: Why Some Firms Beat the Post-IPO Innovation Slump by Simone Wies, Christine Moorman and Rajesh K. Chandy in Journal of Marketing

Footnotes

Acknowledgments

Special thanks to Bernd Skiera, Raji Srinivasan, Richard Staelin, and seminar participants for their recommendations on a previous version of this article.

Associate Editor

Satish Jayachandran

Note

This manuscript was submitted to JM before Christine Moorman’s tenure as Editor in Chief. When manuscript processing transitioned from the previous editorial team to the new team, Ronald Paul Hill, AMA Vice President of Publications, took over as the editor charged with processing this article through review and final acceptance, per the AMA policy on submissions by journal editors.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Parts of this project were funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation; project number 41915910) and the Leibniz Institute for Financial Research SAFE.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.