Abstract

Many retailers are rushing into the click-and-collect (C&C) format, where shoppers place orders online and pick up the goods themselves later. The authors study the demand implications of C&C and postulate how different ways of organizing this format—each with its own convenience features—appeal to households with different shopper characteristics. Using two data sets, each covering the introduction of two C&C fulfillment types by a major grocery retailer in a large number of local markets, the authors compare the impact of in-store fulfillment (pickup at existing stores), near-store fulfillment (pickup at outlets adjoining stores), and stand-alone fulfillment (pickup at free-standing locations). The authors find that the shift in online consumer spending significantly differs between the three order fulfillment types, as does the impact on total spending. No one order fulfillment type systematically dominates; the effects depend heavily on shopper characteristics. The study’s results provide guidance on which C&C fulfillment type(s) to operate under what conditions and caution retailers not to take the easy in-store route routinely.

Keywords

Although online retail sales boomed over the past decade, grocery retail, representing almost 40% of global retail business, did not follow suit. In the United States, online grocery sales are growing, but still, only a modest 5.9% of grocery spending in 2019 occurred online. In Europe, online made up 7.7% of grocery sales in the United Kingdom, followed by France at 7.4%, with many European countries not exceeding 1% (http://retailinsight.ascentialedge.com).

Probably the biggest obstacle to the success of online grocery shopping is “the last mile” problem, as consumers want fast delivery of their groceries yet are reluctant to pay delivery fees (Chintagunta, Chu, and Cebollada 2012). In response, retailers are launching a new format that can mark the tipping point for online grocery (Galante, López, and Munby 2013): “click and collect,” also known as “buy online, pick up in-store,” “drive-thru,” or “drive.” 1 Click-and-collect (C&C) shoppers place orders online and pick up the goods themselves later. Unlike home delivery, C&C often does not come with an extra fee, while prices online are the same as in-store.

Business analysts believe that C&C may become the road to online success in the grocery industry (Edge Retail Insight 2019a). In the United States, grocery retailers are racing to build C&Cs, with frequent reports of supermarkets across the country venturing into the format. Walmart set out to extend U.S. grocery pickup services to 3,100 stores by the end of 2019, while also Kroger and Albertsons are quickly growing their pickup points (Edge Retail Insight 2019b). The speedy expansion of the C&C format is, however, not necessarily indicative of its viability. Indeed, at the end of the day, the critical question is whether consumers will respond positively (Donato-Weinstein 2015). This consumer response may well depend on the way order collection is organized (Edge Retail Insight 2019b). Realizing this, especially in the pioneering (European) countries, retailers have experimented with three different C&C types—from pickup at existing stores (the “in-store” type) to drive-thru outlets adjoining stores (the “near-store” type, also known as curbside pickup) to free-standing locations with dedicated warehouses (the “stand-alone” type).

A rigorous analysis of consumer response to these alternative fulfillment types is currently lacking, and we intend to fill this gap. Specifically, we address the following questions: (1) How does C&C order fulfillment affect shoppers’ online spending and total spending at a retailer? (2) How do different types of C&C in the form of in-store, near-store, and stand-alone C&C affect these outcomes? and (3) What is the impact of these different C&C types for different types of shoppers? Using two unique data sets, each covering a major grocery retailer’s rollout of two of the three C&C order fulfillment types in a large number of local markets, we find that the demand implications sharply differ between the three types.

Our substantive contribution is threefold. First, despite the almost daily business reports about the potential importance of the C&C format, it has been glossed over in academic research. The single exception is Gallino and Moreno (2014), who home in on the informational function of a “buy online, pick up in-store” format of a consumer durables retailer and find that it mostly serves to inform consumers about item availability before visiting the store. We complement Gallino and Moreno (2014) by focusing on the fulfillment function of the C&C format and analyzing how different ways of organizing C&C fulfillment may affect online consumer demand. Although order fulfillment has been recognized in academic research as a critical channel function (Bell, Gallino, and Moreno 2018) and in the business press as a crucial differentiator that ought to be prioritized (PlanetRetail 2015), it has rarely been studied.

Second, we lay out the different “channel benefits” (Coughlan and Jap 2016) or “service outputs” (Stern and El-Ansary 1988) of (alternative types of) C&C. Building on the shopping convenience typology of Seiders, Berry, and Gresham (2000), we argue that the three order fulfillment types differ in terms of the access, collection, and adjustment convenience they offer to shoppers. We then show how the C&C types are valued differently by shoppers, depending on their need or desire for these convenience features.

Third, we recognize that the impact of C&C is not limited to online and study how the C&C types influence shoppers’ total (i.e., online plus brick-and-mortar) spending at the retailer, and how this extrapolates to retailer revenues in different local markets. As such, we provide a more comprehensive picture of how retailers’ C&C operations affect their overall performance.

Managerially, while “e-commerce is transforming business…for supermarket companies,” even the bigger players (e.g., Kroger in the United States) “struggle with the online grocery upheaval” (Haddon 2019). Our findings may provide grocery retailers with insights on how to avoid mistakes when jumpstarting the introduction of C&C. As retailers are racing to build C&Cs, they are mostly opting for fulfillment within existing stores for the sake of quick, low-cost rollout. Indeed, because in-store C&C can rely on existing infrastructure and processes, it is the easiest to implement (Chaity 2015). However, the pursuit of speed without knowing which type is best in terms of demand may lead to the demise of the format. Besides, while most retailers tend to opt for one type of C&C across all markets, we find that a one-size-fits-all approach is not advisable. Instead, the impact depends on shoppers’ needs for fulfillment convenience and the retailer’s focal performance metric. Our study may help retailers in finding the right mix.

Framework

Retailers launch C&C as an additional channel, next to their existing brick-and-mortar and home-delivery channels, in an attempt to increase online sales by tapping into consumers’ ever-increasing convenience needs (Bronnenberg 2018). We first compare the convenience benefits of the C&C format to a retailer’s prevailing brick-and-mortar and home-delivery channels. Next, we introduce the alternative C&C types—in-store, near-store, and stand-alone C&C—and their distinctive convenience features. We then argue how shoppers value the C&C types differently depending on their need for these convenience features, and how this affects their online spending at the retailer. We conclude by briefly reflecting on the impact of C&C on alternative performance indicators.

The C&C Format and Its Impact on Consumers’ Online Spending at the Retailer

Seiders, Berry, and Gresham (2000) offer a framework that distinguishes different features of shopping convenience: access convenience (i.e., the ease of reaching a retailer), transaction convenience (i.e., the ease of effecting and amending transactions at a retailer), search convenience (i.e., the ease of identifying products at a retailer), and possession convenience (i.e., the ease of obtaining desired products from a retailer). In a C&C setting, where shoppers place orders online and pick up the goods later, access convenience pertains to the time to, at, and from a pickup location, while transaction convenience comprises two distinct aspects: the physical effort to collect the order at the pickup point (which we refer to as collection convenience) and the ease with which shoppers can adjust their online orders, by adding items (“top-up shopping”), or returning or replacing them, upon pickup (denoted by adjustment convenience). Search convenience captures the ease of identifying and selecting groceries online. In a C&C context, possession convenience is mainly subsumed within search convenience, because shoppers are informed about a product being in or out of stock at the time they place their order.

Compared with brick-and-mortar shopping, C&C may enhance consumers’ search and collection convenience by allowing them to select and order the desired items online and by having the order physically prepared for them by store personnel. Moreover, to the extent that C&C can take effect through dedicated lanes in easy-to-reach locations, it may come with higher access convenience than brick-and-mortar shopping.

Compared with the home-delivery channel, C&C may offer more access-convenience benefits. While home delivery provides consumers with the advantage of not having to leave their houses, they do have to wait at home for their order to be delivered. In contrast, C&C may allow consumers to reduce shopping time without having to wait. Besides, to the extent that C&C allows for top-up shopping and item replacement, it may offer more adjustment convenience than home delivery.

By better catering to consumers’ convenience needs, C&C is expected to increase shoppers’ online spending at the retailer. First, previous brick-and-mortar shoppers (at the focal retailer’s or competing retailers’ brick-and-mortar channels) may shift their purchases online (Avery et al. 2012). Second, shoppers at competing retailers’ home-delivery channels may switch to the more convenient retailer’s C&C channel. Third, C&C might even increase shoppers’ online spending at the retailer through its effect on their total grocery spending, because of the time savings (which may lead to extra trips; Bronnenberg 2018) and the reduced shopping effort (which may enhance spending per trip; SKUlocal 2018). As Bronnenberg (2018) indicates, travel time is a fixed cost, and consumers will only travel to a store when their basket size is large enough to amortize this cost. Thus, as the time cost drops, households will shop more often. Moreover, by shifting the task of picking and packing the order to the store personnel, C&C reduces a shopper’s variable shopping cost, which is known to enhance spending per trip (Bell, Ho, and Tang 1998). These changes in shopping patterns may create a “primary-demand effect”: they may increase shoppers’ home inventories and, as a result, their consumption (Ailawadi, Ma, and Grewal 2018; Ailawadi and Neslin 1998; Chandon and Wansink 2002; Wertenbroch 1998) and total grocery spending (Gijsbrechts, Campo, and Vroegrijk 2018).

The Convenience Features of Alternative C&C Types

Click and collect can be organized in three major ways. In an in-store C&C, store employees pick and pack ordered items and make the order available at the traditional store location. Shoppers are required to go into the store for pickup rather than wait in the car. In a near-store C&C, the fulfillment center is colocated at a retail store. Shoppers pull up to a drive-thru area with a roof overhead, where they find a touch screen kiosk to alert store staffers. The groceries are then loaded up by retail employees, without the shoppers ever having to leave their car. A stand-alone C&C consists of a warehouse and collection point located wholly separate from the grocer’s retail store, but at a convenient site (e.g., a commuting route, a parking lot, or an office block). Professional pickers assemble orders from a dedicated fulfillment center or black store. Shoppers drive up and have the order delivered to their car.

Table 1 summarizes how these C&C types rate on the convenience features. Search and possession convenience pertain to the informational function of C&C and are the same across in-store, near-store, and stand-alone C&C types. In contrast, access, collection, and adjustment convenience originate from the fulfillment function of C&C, and differ across the three C&C types. Consequently, we propose that consumer response to the alternative C&C types rests on a trade-off between these three fulfillment-convenience features.

How C&C Delivers Convenience.

a The possibility to add, return, or replace items is present but requires more effort from the shopper than in-store C&C.

In terms of the differences between the C&C types, stand-alone C&C excels in terms of access convenience, followed by near-store C&C, with in-store C&C being the inferior option. Stand-alone C&Cs typically open in easy-to-reach locations that are part of consumers’ daily journeys, with no congestion from consumers driving up to the regular brick-and-mortar store. Near-store C&Cs are not located in select, easy-to-access locations but still avoid congestion through dedicated pickup lanes. Stand-alone and near-store C&Cs also outperform in-store C&C in terms of collection convenience by eliminating the physical burden of handling shopping baskets. In addition, consumers are not limited to what they can physically carry when using stand-alone or near-store C&C, as their orders are lifted into their cars. Finally, near-store and in-store C&C offer more adjustment convenience than stand-alone C&C, by allowing shoppers to return or replace unsatisfactory products on the spot and to top up on their purchases at the retailer’s on-site brick-and-mortar store. Especially with in-store C&C, top-up shopping is feasible with little extra effort.

Contingency Framework

No C&C type universally excels on all three fulfillment-convenience features. As argued in classic channel texts (Coughlan and Jap 2016, p. 36; see also Stern and El-Ansary 1988), “the very basis of all channel strategies lies in an understanding of the benefits that end-users desire in how they want to buy.” Thus, which of the C&C types yields the highest consumer utility—and therefore demand—depends not just on the convenience features they offer (the supply side) but also on how a specific shopper, with certain shopper characteristics, values each bundle of convenience features (the demand side). Next, we argue how the relative demand effects of the three C&C types vary with shopper characteristics that reflect their fulfillment-convenience needs. Table 2 summarizes our expectations.

Framework Predictions.

Access convenience: rural shoppers and weekend shoppers

Consumers that live in more rural markets and that shop mostly on weekends are more likely to value access convenience. As such, online spending at the retailer may increase if these consumers shift from brick-and-mortar shopping (at the focal or competing retailers) and/or home-delivery shopping (at competing retailers) to the more access-convenient stand-alone shopping at the focal retailer. Rural shoppers may switch as they typically have to travel a longer distance to shop at brick-and-mortar stores and may, therefore, save on driving or waiting time. The same holds for consumers who have higher opportunity costs of time, typically those who shop on weekends and face more crowded stores and congested parking lots (Stratton 2012). In addition, the convenient access of stand-alone C&Cs (on commuting routes, near office blocks, near highway exits) may lead them to incur extra trips (Bronnenberg 2018), as they can stop for pickup on their way home from work with hardly any time loss. These extra trips may spur primary demand, by keeping up continuous and plentiful supply in consumers’ home pantry and, as a result, expanding their consumption (Ailawadi, Ma, and Grewal 2018; Ailawadi and Neslin 1998). Thus, we expect that for rural and weekend shoppers, stand-alone shopping lifts online spending at the retailer more than near-store and, especially, in-store shopping.

Collection convenience: basket size and bulkiness

Large-basket shoppers and shoppers who buy more bulky items are more likely to value collection convenience. As such, they may switch from brick-and-mortar shopping (at the focal or competing retailers) to near-store and stand-alone shopping (at the focal retailer) to reduce the physical onus of shopping. Moreover, the lower physical effort that comes with near-store and stand-alone shopping may stimulate these shoppers to increase their order sizes by purchasing higher quantities (Ailawadi, Ma, and Grewal 2018), which has been shown to increase consumption (Bell, Chiang, and Padmanabhan 1999; Chandon and Wansink 2002; Wertenbroch 1998), especially in the case of large package sizes (Wansink 1996). Thus, we expect that for shoppers with larger and bulkier baskets, online spending at the retailer is higher with C&C types that excel in facilitating transactions (i.e., with stand-alone and near-store compared with in-store C&C).

Adjustment convenience: household size, perishability, and impulse nature

Larger families and shoppers with more perishable and impulse items in their baskets are more likely to value adjustment convenience. As such, they are more likely to switch from home delivery (at competing retailers) to the focal retailer’s near-store and especially in-store C&C. 2 Ceteris paribus (which includes keeping basket size constant), larger households have greater variety needs to satisfy the heterogeneous tastes of multiple household members (Ailawadi, Ma, and Grewal 2018). As they face more complex shopping tasks, they are also more likely to forget items. Near-store and especially in-store C&C allow them to top up in case of forgotten family needs. In a similar vein, consumers who buy more perishable goods—whose expiration dates and freshness can vary a great deal (Chu et al. 2010)—are more likely to shift their purchases to the C&C types that offer adjustment convenience (i.e., in-store and near-store C&C). Moreover, in-store’s and near-store’s option to easily replace unsatisfactory items on the spot decreases the risk to include products of varying quality in their online orders, which may increase their spending per trip. In addition, shoppers who tend to spend larger shares of their baskets on impulse goods may be more attracted to in-store than near-store and stand-alone C&C because of the ability to fulfill their impulse needs when collecting their orders. In all, we expect that larger families and shoppers with more perishable and impulse items in their baskets spend more online at the focal retailer with in-store than with near-store and, especially, stand-alone C&C.

Impact of C&C Shopping on Consumers’ Total Spending at the Retailer

Studying the effect of the C&C types on consumers’ online spending helps shed light on whether C&C may be the route to online success. However, it provides an incomplete account of the implications for the retailer. On the one hand, C&C shopping may lower (i.e., cannibalize) consumers’ brick-and-mortar spending (Avery et al. 2012) and thus total spending at the retailer. Near-store and in-store C&Cs in particular may constitute a mere shift away from the brick-and-mortar store, because the C&C pickup location is the same as the retailer’s brick-and-mortar store. At the same time, stand-alone shopping may lead to more systematic/planned buying and less impulse buying. This may not just shift consumer purchases away from the retailer’s brick-and mortar-stores to the C&C format but also reduce consumers’ order sizes, thereby attenuating shoppers’ total spending lift.

On the other hand, C&C shopping might increase consumer spending at the retailer’s brick-and-mortar stores and thus enhance shoppers’ total spending lift. The adjustment convenience offered by in-store and, to a lesser extent, near-store C&C may create positive spillovers. Once on site to pick up their online orders, in-store and near-store shoppers can engage in top-up shopping at the retailer’s same-site brick-and-mortar store (Ankeny 2017). Moreover, in-store C&C enables shoppers to impulse-buy in response to in-store offers, rather than only use the store as a destination for collection. Extant research has shown that when consumers make more planned purchases (which they do through online ordering), they may balance that type of self-control with other, more indulgent purchases during the same trip (Gijsbrechts, Campo, and Vroegrijk 2018).

Which of these forces prevails is an empirical question that may again be contingent on shopper characteristics. As a corollary, the C&C type that performs best in boosting consumers’ online spending is not necessarily the one that performs best in terms of increasing consumers’ total spending, nor the retailer’s market revenues. We therefore also investigate the impact of the C&C types on C&C shoppers’ total (i.e., online plus brick-and-mortar) spending at the retailer and how this extrapolates to retailer revenues in different local markets.

Data

Setting

In France, Europe’s largest grocery market and the birth nation of C&C, retailers are extensively experimenting with alternative C&C types (Edge Retail Insight 2018). Ideally, we would study the differences between in-store, near-store, and stand-alone C&C within a retailer, as this allows us to control for price- and assortment-positioning differences between retailers and concentrate squarely on the differences between the three C&C types. 3 However, no retailer operates all three types. Still, two leading retailers each use two types: Intermarché uses in-store and near-store C&C, while Leclerc uses both near-store and stand-alone C&C. To ensure that we do not confound interretailer with C&C-type differences, we analyze the data by retailer.

The two retailers studied are quite similar. Leclerc is the second-largest French retailer, accounting for 14.4% of the grocery market in 2017, operating a network of 1,779 stores (mainly hypermarkets), and generating revenues of approximately €44 billion. Intermarché is the third-largest French retailer, representing 12.8% of the market with 2,806 stores (mostly supermarkets) and revenues of approximately €33 billion (www.planetretail.net). Leclerc, the number-one C&C player in France, opened its first pickup point in 2007 and rolled out the format over the next few years. Intermarché, the number-three C&C player in France, opened its first C&C in 2008. The price positioning of both retailers is below the market average (A3Distrib 2012), with Leclerc perceived as somewhat lower in price than Intermarché (Delvallée 2016). Both retailers maintain a uniform pricing policy: prices in the C&C format and in the brick-and-mortar stores in a given market are identical and, thus, do not affect consumers’ channel choice (for a similar argument, see Chintagunta, Chu, and Cebollada [2012]). Neither retailer adds a service charge.

Sample

We use scanner panel data from Kantar France. The data cover 91 four-week periods between 2008 and 2014. We complement these data with information from the marketing research companies Experian and A3Distrib to identify the opening date of each C&C location, its type (in-store, near-store, or stand-alone C&C), and the local market in which it operates. 4 We focus on markets where the focal retailer operates only one of the three C&C types (which represent over 95% of all markets), and where the first opening by that retailer occurred during our observation window. To allow for a one-year period to assess postadoption effects, we only consider local markets where C&Cs opened before January 2014, resulting in 101 near-store and 82 stand-alone markets for Leclerc and 66 in-store and 212 near-store markets for area Intermarché. Next, we retain households living in these markets that are consistently active in the panel throughout our observation window, which leads to 3,674 and 3,555 households in Leclerc’s near-store and stand-alone markets and 2,224 and 7,667 households in Intermarché’s in-store and near-store markets. Of the Leclerc households, 10.6% and 11.8% started shopping at near-store and stand-alone C&Cs, respectively, whereas 3.6% and 3.8% of the Intermarché households started shopping at in-store and near-store C&Cs. 5

Key Measures

Dependent variable

The dependent variable is online spending (OnlineSpend) at the retailer. It includes all household purchases ordered on the retailer’s website within a four-week period.

Focal independent variables

The dummy variable C&C shopper is one from the time a household adopts C&C shopping and zero otherwise. Households that were merely attracted once (e.g., by trial promotions) but then backed out are not marked as C&C shoppers (for a similar practice, see, e.g., Lambrecht, Seim, and Tucker [2011] and Van Nierop et al. [2011]). The dummy variable Type indicates which C&C type a retailer operates in a local market; it equals 0 for near-store C&C, and 1 for the other type operated by the retailer (i.e., stand-alone C&C for Leclerc, in-store C&C for Intermarché).

Moderators

Rural shopper (Rural) is measured by a dummy variable that indicates whether a household lives in a rural market (1 = rural market, 0 = other), while weekend shopper (Weekend) is operationalized as the fraction of a household’s shopping trips that are made during weekends. Basket size (Basket) is measured as a household’s average number of items purchased per shopping trip. Bulkiness (Bulky) is the average number of bulky items in a household’s shopping basket. Household size (Hhsize) captures the number of members in the household. 6 Finally, perishability (Perish) and impulse nature (Impulse) are measured as the fraction of a household’s shopping basket that is spent on perishables and impulse-natured goods. All moderator variables are measured in the year before the C&C opened and calculated across all retailers. Table 3 provides a detailed description of the operationalizations.

Measurement.

Notes: C&C = click and collect.

aWe calculate the dependent variables by four-week period t.

b We measure the moderator variables in the year before the C&C opens in the household’s local market.

cWe calculate the averages across all four-week periods in the year before the C&C opening.

d Perishability and impulse nature are based on an unpublished 2018 Mturk survey conducted by Gielens and van Lin.

e Since these data were not available at the local-market but at the zip-code level, we matched the local markets to the corresponding zip codes.

Method

We model the extent to which C&C shopping changes a household’s online spending at the retailer. For each retailer, we estimate the online spending model across the different C&C types operated by that retailer, using interaction terms to evaluate the differences between the C&C types while accounting for potential sources of endogeneity.

To estimate the online-spending model, we consider all households in local markets where the retailer opened a C&C within our observation window with at least one year of data available before and after the date of the opening. As such, we can track for each of the households (those who eventually do and do not adopt C&C shopping) their online spending at the focal retailer at least one year before the opening of the C&C until at least one year after the household adopted that C&C (or, in case of no C&C shopping, the end of the data window).

Model Specification

We model the impact of C&C shopping on household online spending at the retailer as

where h captures the household, l the local market, c the C&C type, r the retailer, and t the time period (month).

The interactions between

Control Variables

Household online spending at a retailer may depend on the availability of competing retailers’ C&Cs as well as on the presence of brick-and-mortar stores in the local market. To account for these influences, we control for the number of the focal retailer’s and competing retailers’ C&Cs, their super- and hypermarkets, and independent local retailers at time t in market l (for details, see Table 3). For Stand-Alone C&Cs, we control for the distance to the retailer’s nearest brick-and-mortar store (which is 0 for in-store and near-store). We add a linear trend from the time the C&C pickup point opens in the local market. All continuous variables (except the trend) are mean-centered.

Market Selection Bias

The retailer’s decision to open a particular C&C in a specific market may be driven by variables that also influence households’ online spending at the retailer and, if unaccounted for, may bias our estimates. Insofar as these variables are observable, we can add them as controls to Equation 1. However, some of the variables that simultaneously drive the retailer’s decision to open a certain C&C type and the consumer’s spending decision may be unobservable. To deal with this issue, we use a control-function approach (Wooldridge 2015). We first estimate, per retailer, a multinomial probit selection model across all periods and local markets, including those markets without a C&C. The three choice alternatives are whether the retailer opens one of the two C&C types or none at all, and the explanatory variables are the exogenous variables in Equation 1 plus several instruments. As instruments, we use the number of households living in the local market, and the setup and operational costs of opening a C&C in the market. The setup costs are captured by the availability of construction sites and the average price of both construction sites and real estate in the local market. The costs of running a C&C are reflected in the availability of labor in the local market and labor costs. All six variables are time-varying and meet the criteria for instrument variables (IVs; Wooldridge 2010, p. 112): we expect them to influence the retailer’s decision to open a specific C&C type in a local market but to be uncorrelated with households’ online spending at the retailer. The coefficients of the IVs are statistically significant. Moreover, the likelihood-ratio tests for the restricted (without instruments) versus full model (with instruments) is highly significant for both retailers (Intermarché:

Endogeneity of the C&C Shopping Decision

Unobserved characteristics that drive a household’s C&C shopping decision may also affect its spending. In other words, the adoption variable in Equation 1 may also be endogenous. We therefore estimate a probit model across all households in these markets and all periods in which the C&C type is available, with

Results

Descriptives and Model-Free Evidence

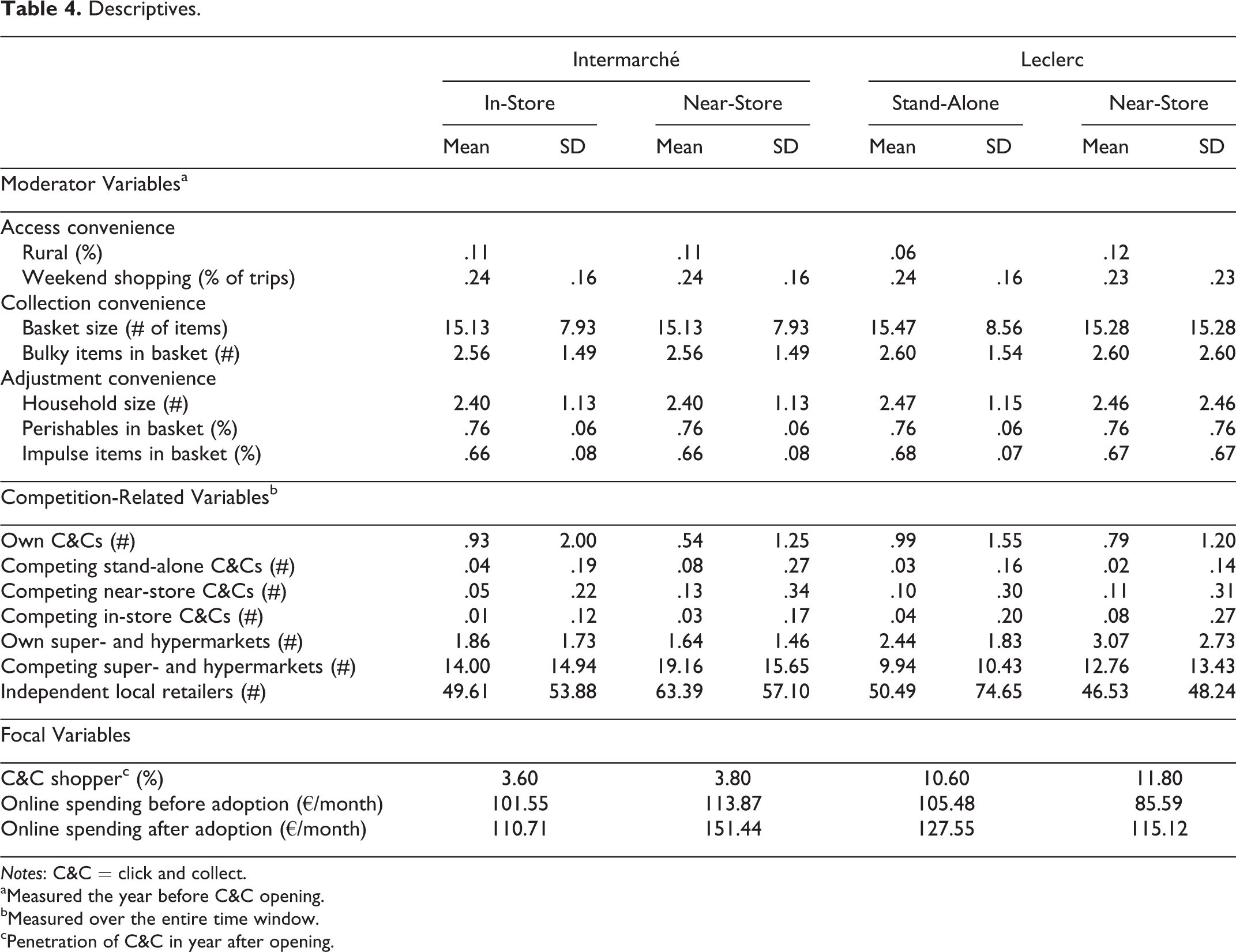

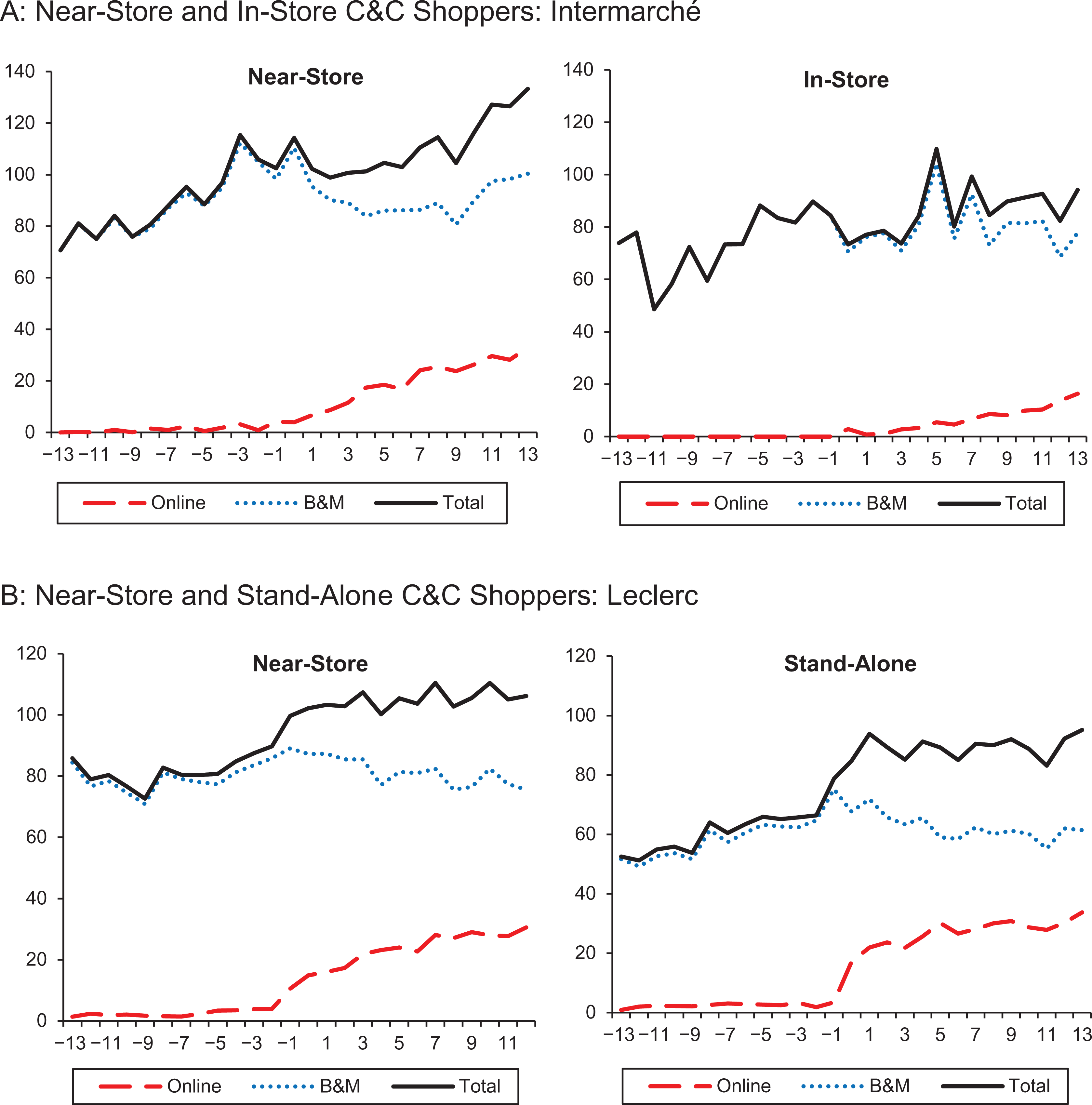

Table 4 provides descriptives for both Intermarché and Leclerc markets. None of the moderator or control variables differ systematically between markets with different C&C types. Figure 1 portrays the average C&C shopper’s (1) online, (2) brick-and-mortar, and (3) total spending at Intermarché (Panel A) and Leclerc (Panel B) in the year before and after they started C&C shopping. Regardless of the retailer and C&C type involved, C&C shopping leads to a clear upswing in online spending and a weaker increase in total spending at the retailer. Brick-and-mortar spending at the retailer remains rather stable. These plots should, however, be interpreted with caution: they do not control for factors that concurrently change with the retailer’s C&C opening or the households’ decision to start C&C shopping, nor for possible endogeneity in these decisions. Moreover, they cannot reveal differences in spending effects between shoppers with different convenience needs. Our model accounts for these issues.

Descriptives.

Notes: C&C = click and collect.

aMeasured the year before C&C opening.

bMeasured over the entire time window.

cPenetration of C&C in year after opening.

Average four-weekly online, brick-and-mortar, and total spending at the retailer by click and collect shoppers before and after adoption.

Does C&C Shopping Affect Online Spending at the Retailer?

Table 5 shows the effects of C&C shopping on online retailer spending. The coefficient of the “CC shopper” variable captures the impact of near-store shopping (the reference case in both models) on online spending at the retailer, for the average household in our sample. This effect is positive and significant for both retailers (Intermarché:

The Effect of C&C Shopping on Consumer Spending at the Retailer.

*p < .10.

**p < .05.

***p < .01.

Notes: Two-sided tests of significance. CF = control-function regressor. All models include household and time fixed effects. The reference C&C type is near-store. The “alternative C&C type” is in-store for Intermarché, and stand-alone for Leclerc.

Do Online-Spending Effects of C&C Shopping Depend on Shoppers’ Convenience Needs?

Access convenience: rural shoppers and weekend shoppers

Rural shoppers show a below-average spending lift after they start shopping at near-store C&Cs (Intermarché:

Collection convenience: basket size and bulkiness

The online spending lift from near-store shopping is higher for shoppers with larger baskets (Intermarché:

Adjustment convenience: household size, perishability, and impulse nature

Near-store shopping leads to a larger increase in online spending for larger households (Intermarché:

Robustness Checks

We performed multiple robustness checks. First, as an alternative way to correct for market selection, we reestimated the market selection model on pooled data across the two retailers using four choice options (no C&C opening or an opening of one of the three C&C types). We then used the generalized residuals from this analysis as control-function regressors in Equation 1. Second, to alleviate the concern that serial correlation in the unobserved household components would overstate the significance of our effects, we ran a simple before–after spending model to measure the impact of C&C shopping on online spending. Following Bertrand, Duflo, and Mullainathan (2004) and similar to Ailawadi et al. (2010), we removed the time dimension by collapsing the time-series data for each household into a pre- and posttreatment period. Third, we used a difference-in-difference approach with propensity score matching (Rosenbaum and Rubin 1983) to compare the change in online spending of households who adopt C&C shopping with that of control households (i.e., nonadopters with a similar adoption propensity). Fourth, instead of assessing the impact of a household’s C&C adoption, we reran our models with the local opening of a C&C pickup point as the treatment variable. Finally, consumers’ online spending may well evolve over time as they gain more experience, or as the execution of the format improves. Adding an extra interaction between the adoption variable and time-since-adoption points to a small negative effect. Thus, after the initial upswing, consumers slightly shift some of their purchases back to the store.

Web Appendix W3 provides details on the various robustness checks. With one exception, results remained substantively the same, thereby underscoring the robustness of our findings. Only for bulkiness did the interaction with in-store C&C shopping become insignificant (instead of positive and significant) in a number of instances, indicating that this effect (which was unexpected to begin with) should be interpreted with caution.

Effect Sizes: The Monetary Value of C&C Shopping

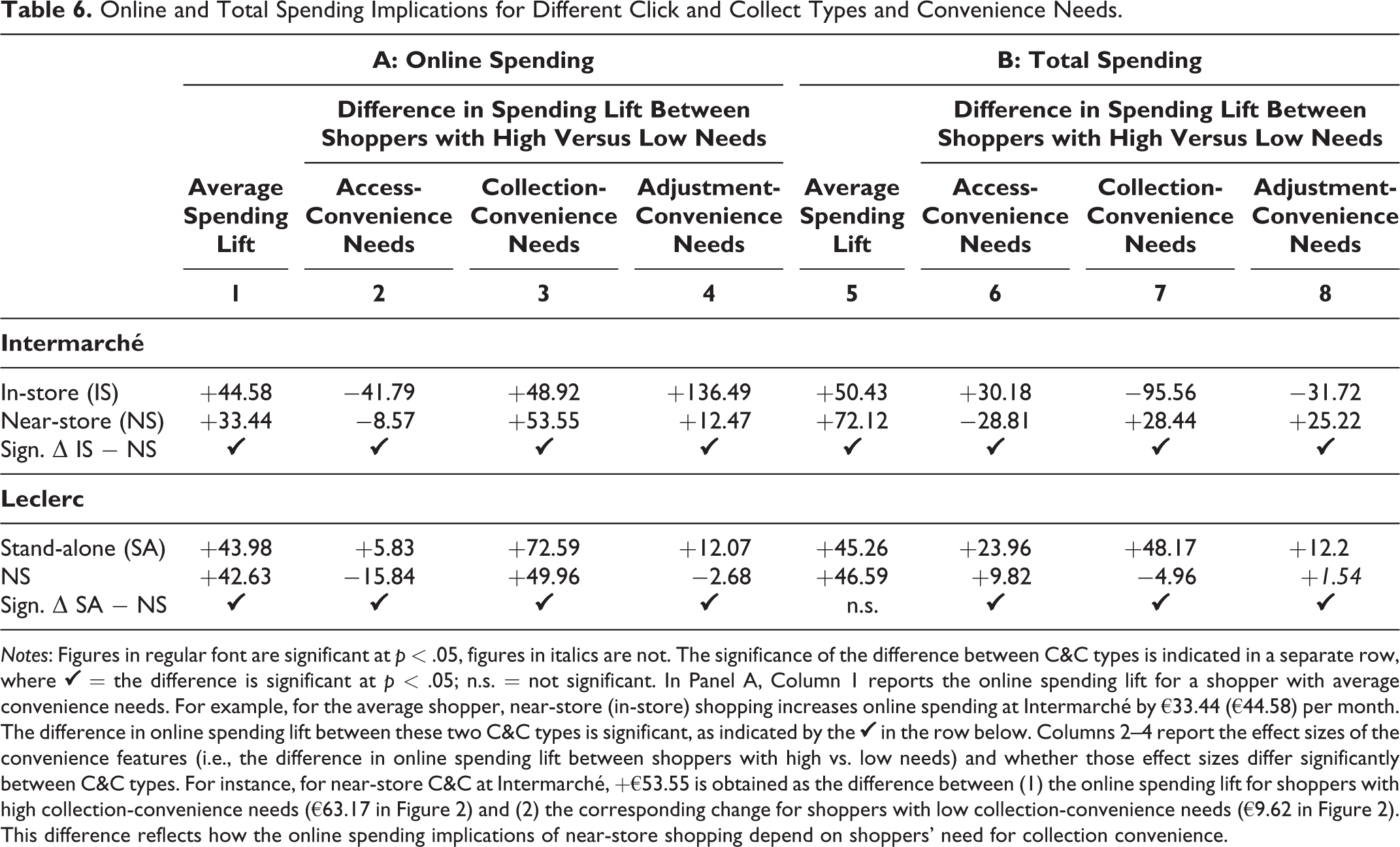

To glean more insight into the economic significance of the findings, we use the estimates from Table 5 to calculate the effect sizes. Column 1 in Table 6, Panel A, reports the average change in online spending after households start C&C shopping. On average, households spend about €40 extra online per month at the retailer. While the spending lift is significant for each C&C type, it is highest for in-store C&C. At first sight, this seems to validate the (many) retailers that are investing in in-store C&C. However, closer inspection reveals a more nuanced picture.

Online and Total Spending Implications for Different Click and Collect Types and Convenience Needs.

Notes: Figures in regular font are significant at p < .05, figures in italics are not. The significance of the difference between C&C types is indicated in a separate row, where ✔ = the difference is significant at p < .05; n.s. = not significant. In Panel A, Column 1 reports the online spending lift for a shopper with average convenience needs. For example, for the average shopper, near-store (in-store) shopping increases online spending at Intermarché by €33.44 (€44.58) per month. The difference in online spending lift between these two C&C types is significant, as indicated by the ✔ in the row below. Columns 2–4 report the effect sizes of the convenience features (i.e., the difference in online spending lift between shoppers with high vs. low needs) and whether those effect sizes differ significantly between C&C types. For instance, for near-store C&C at Intermarché, +€53.55 is obtained as the difference between (1) the online spending lift for shoppers with high collection-convenience needs (€63.17 in Figure 2) and (2) the corresponding change for shoppers with low collection-convenience needs (€9.62 in Figure 2). This difference reflects how the online spending implications of near-store shopping depend on shoppers’ need for collection convenience.

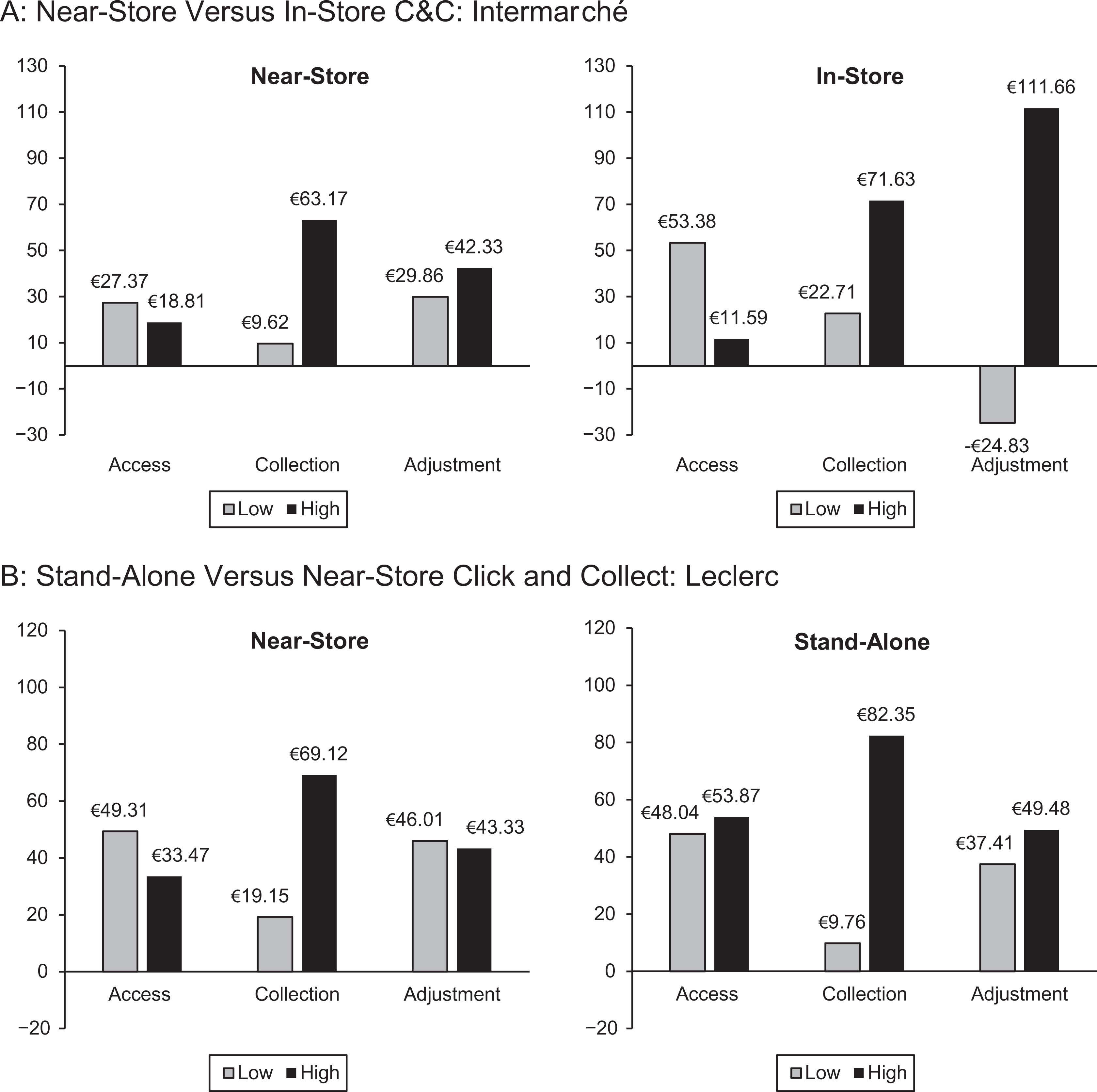

Impact of shoppers’ convenience needs on online spending at the retailer.

The spotlight analysis in Figure 2 displays the changes in online spending following C&C shopping, by C&C type, for shoppers with low versus high needs for each convenience feature. 9 Columns 2 to 4 in Table 6, Panel A, report the corresponding effect sizes of the convenience features (i.e., the difference in online spending lift between shoppers with high vs. low needs) and whether those effect sizes differ between C&C types. Shoppers with a high access-convenience need (weekend shoppers, shoppers in rural areas) spend less online than shoppers low on that need when near-store shopping (Intermarché: €18.81 vs. €27.38, a difference of −€8.57; Leclerc: €33.47 vs. €49.31 = −€15.84) and especially in-store shopping (−€41.79), but more so when stand-alone shopping (+€5.83). This difference between C&C types stems mostly from rural shoppers. Shoppers with higher collection-convenience needs (those with large and bulky baskets) always spend more online, regardless of the C&C type, but significantly more so when near-store than in-store shopping (Intermarché: near-store = +€53.55, in-store = +€48.92) and when stand-alone than near-store shopping (Leclerc: stand-alone = +€72.59, near-store = +€49.96). While we find that the online spending lift across C&C types is mostly driven by basket size, bulkiness drives the extra lift for stand-alone C&C. Shoppers who score higher on adjustment-convenience needs (large households shopping more perishables and impulse goods) spend significantly more online when in-store shopping (+€136.49), while the difference between low- and high-adjustment-need shoppers is less pronounced for stand-alone and near-store C&Cs. The complexity of household needs plays a role here: larger households in particular spend more online when in-store shopping, which enables them to purchase forgotten items upon pickup. Basket composition, too, matters: shoppers with more perishable and impulse items in their baskets spend much more online when in-store shopping and less so when near-store or stand-alone shopping.

In all, we find that C&C shopping boosts online spending at the retailer. On average, in-store shopping produces the highest online spending lift, especially among shoppers with high adjustment-convenience needs. For shoppers with high access- or collection-convenience needs, stand-alone shopping yields the highest online-spending gain.

Does C&C Shopping Increase Total Spending at the Retailer?

Click-and-collect shopping enhances households’ online spending at the retailer. However, if C&C shopping cannibalizes brick-and-mortar spending, the retailer’s gain may be negligible. To explore this, we reestimate Equation 1 with shoppers’ brick-and-mortar and total spending at the retailer as the dependent variables. We summarize the estimation results in Table 5. Table 6, Panel B, and Figure 3 document the ensuing changes in total spending.

Impact of shoppers’ convenience needs on total spending at the retailer.

For households with average convenience needs, C&C shopping enhances total spending at the retailer. For stand-alone and in-store shopping, the online and total spending lift do not significantly differ, while for near-store shopping, the increase in total spending significantly exceeds the online lift (Intermarché: €72.12 compared with €33.44, p < .01; Leclerc: €46.59 compared with €42.63, p < .05,). Thus, cannibalization does not appear to be an issue, and positive spillovers from C&C to brick and mortar can occur.

However, this average picture conceals substantial shopper heterogeneity. The impact of shoppers’ convenience needs on their total spending at the retailer (Table 6, Panel A, columns 6–8) is very different from that on their online spending (Table 6, Panel B, columns 2–4). In a similar vein, Figure 3 shows that across shoppers with different convenience needs, the pattern of changes in total spending does not mimic that of changes in online spending displayed in Figure 2. For households that value access convenience, the total spending lift (in Figure 3) always exceeds the online lift (in Figure 2), suggesting positive spillovers to the retailer’s brick-and-mortar stores. The time savings of C&C shopping may attract access-oriented shoppers to the retailer and, having become familiar with the retailer or being on-site for C&C order collection, they may use some of the saved time to seek out additional items at the retailer’s brick-and-mortar stores. A higher collection-convenience need typically leads to lower total than online spending lifts, indicating that part of the household’s online spending lift is at the expense of brick-and-mortar spending. Such cannibalization appears especially prevalent with in-store C&C. For this C&C type, the online spending lift (€71.63, see Figure 2) is entirely dissipated by the fact that shoppers with high collection-convenience needs spend less at the retailer’s physical outlets (leading to a total spending lift of −€1.56; see Figure 3). Likewise, for households with high adjustment-convenience needs, the total spending lift from in-store shopping (€40.50, see Figure 3) is far lower than the online spending lift (€111.66, see Figure 2), suggesting strong cannibalization. While adjustment-oriented shoppers tend to be impulse-driven, the ability of controlling their impulse tendencies online results in a relatively larger brick-and-mortar loss.

In summary, C&C shopping not only affects a household’s online but also affects its brick-and-mortar spending at the retailer in ways that critically depend on the C&C type and that household’s convenience needs. Thus, which C&C type to operate in a local market should be guided by the total (online plus brick-and-mortar) spending implications and the local shopper profile.

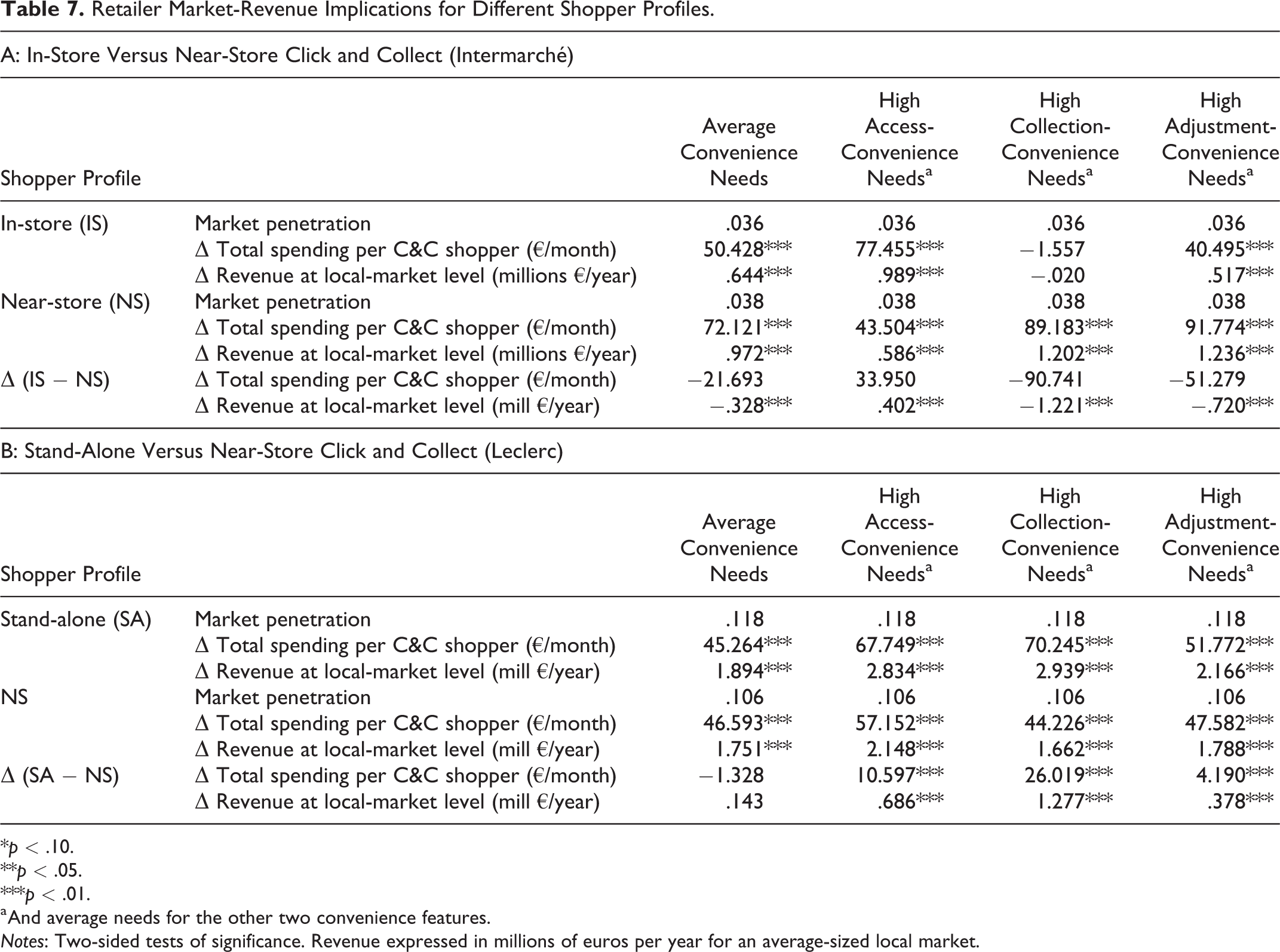

To get a feel for these local-market implications, Table 7 extrapolates the four-week household-level total spending effects to yearly market-level retailer revenues for each retailer and C&C type, and for different shopper profiles. Market-level revenues are obtained by multiplying the C&C shoppers’ total spending with the observed penetration rates for the considered C&C type and retailer. These figures are extrapolated to the local-market level by multiplying with the number of households in an average-sized market. The table shows that when shoppers in a local market have average convenience needs, stand-alone C&C is the highest-performing option: it yields slightly higher market revenues than near-store C&C (+€143,000), which, in turn, strongly outperforms in-store C&C (+€328,000). Interestingly, whereas in-store C&C outperforms the other two types in terms of online spending, it leads to the smallest market-revenue lift for the retailer.

Retailer Market-Revenue Implications for Different Shopper Profiles.

*p < .10.

**p < .05.

***p < .01.

a And average needs for the other two convenience features.

Notes: Two-sided tests of significance. Revenue expressed in millions of euros per year for an average-sized local market.

Stand-alone C&C yields especially higher market revenues than near-store when the shoppers in a local market strongly value collection convenience (a €1,277,000 revenue advantage) or access convenience (a €686,000 revenue advantage). In turn, near-store C&C outperforms in-store C&C for all shopper profiles, except those oriented toward access convenience. When, on average, the shoppers in a local market highly value adjustment convenience, the market-revenue advantage of near-store over in-store C&C amounts to €720,000. For such a shopper profile, in-store C&C generates the largest boost in online spending, but mostly at the expense of the retailer’s brick-and-mortar stores. Thus, when it comes to the retailer’s market revenue, local markets with this shopper profile are better served with near-store and especially stand-alone C&C.

Discussion

With order fulfillment as a major impediment for growth in online grocery, C&C has been advanced as the new fulfillment mantra. Accordingly, many retailers have rushed (or are rushing) into this format to secure their piece of the online grocery pie. However, C&C remains a relatively young phenomenon, and its demand-side effects are not well documented. Moreover, because “the last mile is fast becoming the ultimate battleground” (Post&Parcel 2016), retailers are looking for advice on whether and how to implement these programs. Drawing on two data sets, each covering the introduction of different C&C types by a major grocery retailer, we tracked the spending implications of three C&C types. Our study centered on the following questions: (1) How does C&C order fulfillment affect shoppers’ online spending and total spending at a retailer? (2) How do different types of C&C in the form of in-store, near-store, and stand-alone C&C affect these outcomes? and (3) What is the impact of these different C&C types for different types of households?

Marketing Implications

Spending impact of the C&C format

As to the online spending impact of the C&C format, we find that C&C can be an effective means to boost online spending at the retailer. Thus, C&C may indeed be the long-awaited road to online success for grocery retailers (Craft 2019), overcoming the last-mile problems associated with home delivery. As to the total spending impact of the C&C format, consultants have long thought that “the increase in…click-and-collect will come primarily at the expense of brick-and-mortar sales” (Post & Parcel 2016; see also, e.g., Ankeny 2017; Espiner 2015). In contrast, we find cannibalization to be minimal. Overall, this bodes well for C&C. By blending the convenience features of home delivery and brick-and-mortar channels, C&C enhances households’ total spending at the retailer. The C&C format thus constitutes a valuable addition to a retailer’s channel mix.

Alternative C&C types and shopper convenience needs

When it comes to fulfillment, not all C&Cs are alike. While we find that the C&C format has a significant impact on consumer spending at the retailer, the effects are strongly shaped by (1) the C&C type and (2) shopper characteristics. In-store shopping typically produces the highest online spending lift. As expected, this holds especially among shoppers with high adjustment-convenience needs (i.e., larger households that buy more perishables and impulse items). Interestingly, this lift also stems from an increase in shopping frequency, as these shoppers complement their C&C order collection with store purchases. Stand-alone shopping yields the highest online spending gain among shoppers with high collection-convenience needs (i.e., those buying bulky and large baskets), and especially access convenience (i.e., rural and weekend shoppers). This C&C type does, indeed, come with lower shopping effort than in-store C&C and allows for more time-efficient order pickup than both in-store and near-store order fulfillment.

Looking beyond the online-spending effects, we find that in-store shopping has the most pronounced impact on the retailer’s brick-and-mortar sales. However, depending on shoppers’ convenience needs, the brick-and-mortar effect can go both ways—either attenuating or enhancing the total spending lift. For shoppers with high access-convenience needs, in-store C&C generates positive spillovers for the retailer’s brick-and-mortar stores. Especially for rural shoppers, in-store C&C shopping goes along with higher spending in the retailer’s brick-and-mortar stores and, thus, an increase in total spending. In contrast, for shoppers with high collection-convenience needs, in-store shopping strongly cannibalizes brick-and-mortar sales. When using this C&C type, large-basket shoppers for bulky items seem to merely shift their purchases from brick-and-mortar to online, such that total spending at the retailer hardly goes up. Also for shoppers with high adjustment-convenience needs, the total spending effects of in-store shopping are not promising. Especially for large households buying more impulse items, in-store C&C shopping goes along with a dramatic reduction in brick-and-mortar spending. Thus, the C&C type that yields the biggest boost in online spending at the retailer (i.e., in-store C&C) is not necessarily the best-performing option for the retailer overall.

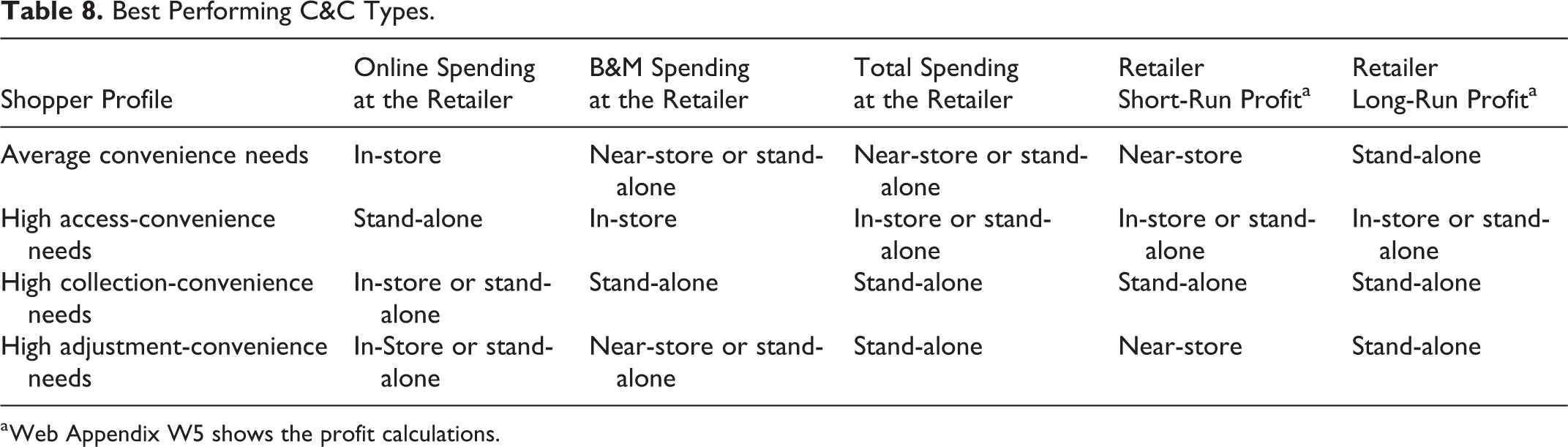

These insights can be useful for retailers setting up or expanding their C&C operations. Table 8 lays out which C&C type performs best depending on the shoppers’ characteristics and the retailer’s key performance metric (i.e., shoppers’ online spending, brick-and-mortar spending, or total spending). Because C&C types differ in terms of setup and order-preparation costs, a possible concern is that even if stand-alone (or near-store) C&Cs yield higher market revenues, these may be offset by higher costs. To shed some light on this issue, we perform back-of-the-envelope calculations to trade off each C&C type’s market revenues (calculated using our estimates) against their costs (taken from industry reports; Capital 2018; Caussil 2013; Editions Dauvers 2013a, b). We then compare the profitability of the C&C types in the short run and the long run (i.e., after the set-up investments have been depreciated) and add these insights to Table 8. Web Appendix W5 shows the underlying profitability calculations.

Best Performing C&C Types.

a Web Appendix W5 shows the profit calculations.

Overall, while in-store C&Cs excel at increasing (especially adjustment-convenience-oriented) shoppers’ online spending at the retailer, they lead to lower total spending. Stand-alone C&Cs yield the highest total-spending increase for households with high collection- or adjustment-convenience needs. As to profit, stand-alone C&C appears to be the more profitable option. Many retailers have jumped the bandwagon by quickly setting up the in-store type. Our results caution managers not to take this easy route routinely.

Primary-demand impact of the C&C format

In laying out our expectations, we argued that C&C shopping may increase primary demand through larger baskets and/or extra shopping trips. To deepen our insights, we reestimated Equation 1 with households’ (1) total grocery spending (across all retailers), (2) total number of trips (across all retailers), and (3) spending per trip as the dependent variables (for the estimates, see Web Appendices W4-A, W4-B, and W4-C). For both retailers, we find that, on average, C&C shopping positively affects households’ total grocery spending, and this manifests in an increase in both total trip frequency and spending per trip. These findings contradict the common fear that online shopping may be detrimental for primary demand because of lower impulse and unplanned purchases. Instead, our additional probe suggest that the time convenience leads households to shop more often while the reduction in shopping effort drives up order sizes, thus increasing consumption and spending (Ailawadi, Ma, and Grewal 2018; Chandon and Wansink 2002; Gijsbrechts, Campo, and Vroegrijk 2018; Wertenbroch 1998). Thus, C&C shopping can also increase the size of the grocery pie.

Our insights may be particularly relevant in the light of the COVID-19 pandemic, which has accelerated the shift to online that was already taking place. Fulfillment options with limited contact, such as C&C, have become increasingly popular as shoppers feel wary of walking store aisles. According to the Adobe Digital Economy Index, “buy online, pick up in store” orders in the United States surged in 2020 by 62% between February 24 and March 21, compared with the same period a year earlier (https://www.adobe.com/experience-cloud/digital-insights/digital-economy-index.html). With the adoption rate of C&C spiking, many retailers have accelerated the rollout of C&C pickup points or have added C&C to their channel mix. Because the pandemic created urgent demand for C&C, retailers predominantly turned to fulfillment options that they could quickly launch or expand (i.e., in-store C&C and curbside, near-store options). With the sharp increase in demand, online orders fulfilled with store inventory increasingly risk out-of-stocks on store shelves (Edge by Ascential 2020). Thus, as retailers try to permanently convert the increased C&C demand, they should carefully (re)consider which C&C type performs best depending on their performance outcome of interest and their local markets’ shopper characteristics.

Theoretical Implications

Extant research has focused on internet channels with home delivery (e.g., Campo and Breugelmans 2015; Chintagunta, Chu, and Cebollada 2012; Chu et al. 2010), with several studies investigating the effects of online channel usage on consumer shopping behavior (e.g., Campbell and Frei 2009; Gensler, Leeflang, and Skiera 2012). While home delivery does not require shoppers to travel to a store and queue up, it also has disadvantages: consumers have to commit to delivery times, and returning products can be challenging. The C&C format does not suffer from these drawbacks. We contribute to the online-channel literature by laying out how different C&C fulfillment options rate differently on different convenience features and how consumers value these features. In so doing, we expand the shopping convenience typology of Seiders, Berry, and Gresham (2000) by distinguishing two aspects of transaction convenience that are particularly relevant in a C&C setting: the physical effort to collect the order at the pickup point (collection convenience) and the ease with which shoppers can adjust their online orders, by adding, returning, or replacing items upon pickup (adjustment convenience). In doing so, we recognize that efficient order fulfillment has become an ever more important shopper convenience need that is no longer obscured in the supply chain but has moved to the forefront to capture, delight, and retain shoppers in an omnichannel retail world.

Our findings are consistent with classic channel texts that advise no single channel is best (Coughlan and Jap 2016; Stern and El-Ansary 1988). Rather, consumers differ in how they want to buy. We contribute by adding that it is better to excel in one convenience feature (and score low on others) than to rate average on all features. Indeed, near-store C&C seldom comes out as the best option. Thus, while no single C&C option is best, the “middle” option is definitely worst—conforming to Porter’s (1980) “stuck-in-the-middle” principle.

Furthermore, prior research has studied whether online and offline channels are complementary or synergetic (e.g., Avery et al. 2012; Deleersnyder et al. 2002; Pauwels and Neslin 2015; Wang and Goldfarb 2017). In their synthesis of the literature, Liu, Lobschat, and Verhoef (2018) conclude that substantial channel differentiation may alleviate cannibalization occurring between similar channels (e.g., mobile and online channels). However, such differentiation also leads consumers to perceive lower consistency in the retailer’s channel mix and a less seamless experience during multichannel shopping, which may reduce retailer performance. Thus, Liu et al. (2018) conclude that finding the right balance between channel cannibalization and synergy is a major unresolved issue. We demonstrate that whether the online and the offline channels are cannibalistic or synergetic depends on matching C&C order fulfillment types with shoppers’ convenience needs. By tailoring the C&C type to the local-market shopper profile (e.g., by not setting up in-store C&Cs in markets where consumers have, on average, high collection- or adjustment-convenience needs), retailers can avoid cannibalization while maintaining a consistent channel offer and substantially enhance their market revenues and profit.

Limitations and Future Research

Our study is subject to several limitations, some of which open up new questions that warrant further research. First, our model includes household fixed effects, which ensures that cross-sectional household-specific components are removed. It is still possible, though, that there is some serial correlation left in the errors within each household, which may overstate the significance of the effects. Still, the simple before–after model in which the time dimension is aggregated out reassures us that our effect identification is not biased by (higher-order) temporal error correlation within households (Bertrand, Duflo, and Mullainathan 2004).

Second, we analyzed the impact of three C&C order fulfillment types in two data sets, each involving one retailer. In doing so, we join empirical work in multichannel research that analyzes a single retailer (e.g., Chintagunta, Chu, and Cebollada 2012; Gallino and Moreno 2014). Our focus was on three C&C types with distinct fulfillment modalities. Future studies, across more retailers, could formally investigate to what extent retailer characteristics, such as their price and quality positioning and their assortment breadth and depth (factors that were constant in our comparisons), affect demand for the C&C types.

Third, our focus was on comparing alternative C&C types. Given that the option to order online with home delivery was scarcely used by the panelists in our data set in the country and period considered, we did not consider that option in our analysis. Future studies could compare the C&C types with a broader set of options to buy not purely inside the store, including home delivery. In addition, the uptick in retailers experimenting with various autonomous delivery options to crack the last-mile problem due to COVID-19, including self-driving robots and drones (Dekimpe, Geyskens, and Gielens 2020), provides numerous research opportunities.

Fourth, based on the convenience features of the different C&C types, we conjectured which shoppers would be most inclined to value these features and empirically assessed their behavioral response without intermediate “process” measures. Future studies could directly verify which consumer segments attach more importance to access, collection, and adjustment convenience and how this relates to their preference for alternative C&C types.

Finally, our empirical results reflect the current market situation. The size of the spending lift may well evolve as more retailers roll out their C&C operations, and new types of C&C order fulfillment gain way. We leave the analysis of these developments, including the study of competitive reactions, as a fruitful topic for future research.

Supplemental Material

Supplemental Material, Web_Appendices_--JM-18-0623-R5--_Navigating_the_Last_Mile_in_Grocery_Shopping_PDF - Navigating the Last Mile: The Demand Effects of Click-and-Collect Order Fulfillment

Supplemental Material, Web_Appendices_--JM-18-0623-R5--_Navigating_the_Last_Mile_in_Grocery_Shopping_PDF for Navigating the Last Mile: The Demand Effects of Click-and-Collect Order Fulfillment by Katrijn Gielens, Els Gijsbrechts and Inge Geyskens in Journal of Marketing

Footnotes

Acknowledgment

The authors are indebted to AiMark for providing the data.

Associate Editor

Kusum Ailawadi

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.