Abstract

Companies are increasingly held accountable for their corporate social irresponsibility (CSI). However, the extent to which a CSI event damages the firm largely depends on the coverage of this event in high-reach news media. Using the theory of news value developed in communications research, the authors explain the amount of media coverage by introducing a set of variables related to the event, the involved brand, and media outlet. The authors analyze a sample of 1,054 CSI events that were reported in 77 leading media outlets in five countries in the period 2008–2014. Estimation results reveal many drivers. For example, the number of media covering the story may be 39% higher for salient and strong brands. 80% more media report the event if a foreign brand is involved in a domestic CSI event. When a brand advertises heavily or exclusively in a news medium, this reduces the likelihood of the news medium to cover negative stories about the brand. The average financial loss at the U.S. stock market due to a CSI event amounts to US$321 million. However, the market reacts to the event only if 4 or more U.S. high-reach media outlets report on the event.

Keywords

Companies are increasingly held accountable for their social irresponsibility. External stakeholders, including investors, no longer tolerate unethical firm behavior and are demanding proactive social responsibility (e.g., Kang, Germann, and Grewal 2016; Kölbel, Busch, and Jansco 2017). Indeed, events of corporate misbehavior may propel a firm into a severe if not existential crisis. For example, Enron’s accounting fraud in 2001 led to not only its bankruptcy but also the dissolution of its then-auditor, Arthur Andersen. A Wall Street journalist played a major role in the discovery of the Enron scandal and won several media awards for his investigation. The case demonstrates the enormous power of media. By construction, unethical behavior has no consequences until it is revealed and reported in the media. In fact, extensive research on corporate crises suggests that media coverage is one of the most important (if not the most important) accelerators of a brand/firm crisis (e.g., Backhaus and Fischer 2016; Kölbel, Busch, and Jansco 2017; Liu and Shankar 2015). Backhaus and Fischer (2016) show that the immediate loss in brand strength deteriorates from −13% to −21% if 12 instead rather than 6 German media outlets cover a crisis event. In addition, the brand then needs two months longer to recover from the crisis. Kölbel, Busch, and Jansco (2017) study how media coverage of corporate social irresponsibility (CSI) increases financial risk. They find that one additional article may cost a firm up to US$140 million per year. Thus, media coverage is a key factor that shapes the depth and length of a crisis and its consequences for a company. Media coverage of a CSI event, however, can be very heterogeneous. The recent Volkswagen emission scandal reached broad worldwide press coverage, and it was covered by all the leading U.S. newspapers. In contrast, only a few outlets reported on the accused misappropriation of funds by Banorte, a leading bank in Mexico in 2012. In another example, both Goldman Sachs and J.P. Morgan were accused of fraud in 2012 and 2010, respectively. Whereas 9 of the 15 leading U.S. media outlets reported on Goldman Sachs, only 3 outlets covered J.P. Morgan. From the firm’s perspective, it is therefore of utmost relevance to understand and anticipate media coverage in a crisis situation, and scholars have recently called for research in this area (Cleeren, Dekimpe, and Van Heerde 2017).

Research Question and Contribution

Studying the drivers of media coverage of CSI events is the key objective of this study. We develop a model of how journalists and their media outlets decide whether to report on a CSI event. This model includes theory-based drivers of news selection such as the evidence on the event, brand strength, brand origin, and exclusivity of advertising partnership. We acknowledge that there are many sorts of negative publicity about a firm (e.g., product recalls, scandals of sponsored celebrities, CSI incidents); however, it is beyond our scope to cover all of them, and we chose to focus on CSI behavior that relates to environmental, social, and governance issues because although their relevance has risen consistently in recent years, they are less studied than other events such as product recalls.

This research makes several contributions. We develop a conceptual model for understanding when a CSI event becomes news. We draw on the theory of news value (Galtung and Ruge 1965), an established paradigm of news generation in communication research, and significantly extend previous work in journalism, particularly by introducing managerially relevant news selection variables.

We apply the model to a large multicountry data set and quantify the impact of news selection variables on the probability of reporting a CSI event. Specifically, we collect data on CSI events and their coverage during 2008–2014 in the leading online and offline media in five countries: the United States, Mexico, the United Kingdom, Germany, and France. The final sample includes a set of 1,054 CSI events involving 324 brands across diverse industries. Unlike product recalls, which must be reported to authorities, we can only identify CSI events from their coverage in media channels. An important benefit of the multicountry design is that we observe events that were not reported in one country through their media coverage in other countries. Thus, the multicountry data set significantly contributes to the power of the analysis. Furthermore, we uncover important differences between media coverage of a domestic versus a foreign event as well as for a domestic versus a foreign brand. Only in a multicountry data set is there a quasiexperimental variation across domestic and foreign for the same CSI event and the same brand, which supports identification of the related effects. The unique data set also yields substantive and generalizable results that covers both developed and developing countries.

Finally, we investigate the economic consequences of media coverage of a CSI event in a financial event study. Although it is well-known that media attention may influence investor behavior (e.g., Engelberg and Parsons 2011; Fang and Peress 2009; Van Heerde, Gijsbrechts, and Pauwels 2015), we need to demonstrate this for the domain of CSI news to establish practical relevance, which has not been done so far. Together with the analysis of the drivers of media coverage, this analysis sheds light on the financial risks of a CSI event dependent on brand and event characteristics.

This study offers important insights into the world of media and how outlets report on corporate issues. Consistent with the theory of news value, we find that media prefer reporting CSI events for strong and well-established brands. For example, 53% of the leading U.S. media covered a story when Google violated privacy concerns by collecting personal information in Europe in 2010. In contrast, Citibank, a much weaker and less salient brand than Google, was accused of fraud in India in the same year, and no leading U.S. media outlet reported on this event. Media also show a preference for events that happen in the home market, particularly involving foreign brands; however, they tend to cover CSI news less often for their advertising partners. Furthermore, we find that “right-oriented” media are less likely to cover a CSI event compared with “left-oriented” media. This effect becomes weaker when the brand is more present because of recent overall advertising pressure.

Moreover, the event study produces an unexpected finding. If we do not control for media coverage, the analysis suggests that investors do not care about unethical firm behavior. However, we do find evidence for a negative stock market effect when 4 or more media outlets out of the 15 largest U.S. outlets cover the CSI event.

The remainder of this article is structured as follows. The next section gives an overview of related literature. Following that, we introduce the model of CSI news selection. We then develop expectations about news selection drivers. The following sections present the data, the empirical model of news selection, and estimation results. We then introduce the event study to measure the economic impact of media coverage. The final section concludes with a discussion of implications and limitations.

Related Literature

This study extends the marketing literature on brand/firm crises in a new direction. Prior research has studied the effects of negative corporate news on various performance metrics and conditions—for example, sales (Cleeren, Van Heerde, and Dekimpe 2013), advertising effectiveness (e.g., Liu and Shankar 2015), and shareholder value (e.g., Flammer 2013). In addition, researchers have analyzed consequences for customer mindset variables such as attitude toward the brand (e.g., Ahluwalia, Burnkrant, and Unnava 2000), brand equity (e.g., Dawar and Pillutla 2000), brand attention and brand strength (e.g., Backhaus and Fischer 2016), and online word of mouth (WOM; e.g., Borah and Tellis 2016).

Another related stream of research in marketing and economics studies the behavior and outcomes in media markets. Researchers have suggested both theoretical models (e.g., Gal-Or, Geylani, and Yildirim 2012; Xiang and Sarvary 2007) and empirical models (e.g., Gentzkow and Shapiro 2010; Gurun and Butler 2012; Rinallo and Basuroy 2009). The interdependency of media and their advertising partners and how it results in various forms of media biases have been of particular interest in these studies (e.g., Beattie et al. 2020; Gurun and Butler 2012; Rinallo and Basuroy 2009). As a result, the studies typically focus on advertising but do not pay much attention to other variables that also might significantly influence media coverage.

We build on this stream and also study the role of advertising. But advertising is only one among several other variables in our model of media coverage. Specifically, we adapt an established paradigm—the theory of news value (Galtung and Ruge 1965)—to derive a list of important drivers of the coverage of CSI events. Empirical research in this domain has studied a wide range of news topics including international crises (Galtung and Ruge 1965), celebrity news (O’Neill 2012), and protest events (Oliver and Myers 1999). Although the theory of news value is widely accepted in the field of journalism and covered in standard textbooks (e.g., Van Ginneken 1997), empirical research appears to be limited to case studies and qualitative research (e.g., Caple and Bednarek 2016; Dick 2014; Galtung and Ruge 1965; Harcup and O’Neill 2001, 2017; O’Neill 2012). A rare exception is Oliver and Myers (1999), who study the coverage of 382 protest events by two local newspapers in a small U.S. city. Their context with protests on social and political issues in a small city, however, is very different from our nationwide coverage of unethical firm behavior events. The set of driver variables also appears to be limited with a focus on the number of protesters, the type of supporting organization, the location and time of the protest, and the type of protest. Our set of drivers is larger and covers all relevant news factors suggested by the theory of news value. Importantly, we also consider news selection variables that are actionable for managers because they can influence them.

We add to the media literature in marketing by building on the theory of news value. Studying the coverage of CSI events has not been the focus before. Our quantitative study includes more than 1,000 events over a period of 6.4 years, 77 media outlets, and five countries. To the best of our knowledge, it is the first study that focuses on specific drivers of media coverage of news that is relevant to marketing managers and other company executives. We acknowledge that recent work in marketing has already addressed the dynamic interplay between news media coverage and other communication channels as well as economic outcomes (Chen et al. 2019; Hewett et al. 2016; Van Heerde, Gijsbrechts, and Pauwels 2015). A key message from these studies is that media coverage plays a significant role that should not be neglected by management. However, these studies do not investigate CSI events, which is our focus here.

A Model of CSI News Selection

In this section, we develop a model that describes the process and drivers of selecting negative corporate news due to an event of unethical behavior. We introduce variables that influence editors’ choice to cover the CSI news and discuss their direction of influence.

Theory of News Value

In a seminal article, Galtung and Ruge (1965) suggest a theory of news value to answer the question “How does an ‘event’ become ‘news’?” This theory has gained wide acceptance to explain the selection process of news across various fields (international politics, entertainment, sports, etc.), though not corporate news. Although researchers have suggested extensions and refinements of the theory (e.g., Harcup and O’Neill 2001; Van Ginneken 1997), it has not lost its relevance and still applies to today’s digital media world (Harcup and O’Neill 2017).

Galtung and Ruge begin with the basic premise that journalists follow ground rules to evaluate an event and put forward a taxonomy of 12 factors describing the newsworthiness of the event. The theory contends that the more factors an event satisfies, the more likely it is to be reported on. Moreover, news factors may compensate each other and altogether have to pass a certain threshold to qualify as news.

We adopt the theory of news value to explain how media outlets assess the newsworthiness of a CSI event. The news factors proposed by the theory describe the reasons for newsworthiness at an abstract level. As a theoretical contribution, we derive explicit news selection variables from the news factors that apply to the specific context of unethical firm behavior. These news selection variables are observable and thus suitable for empirical validation. In the following section, we briefly describe this process before we set up the conceptual model.

Deriving CSI News Selection Variables from the Theory of News Value

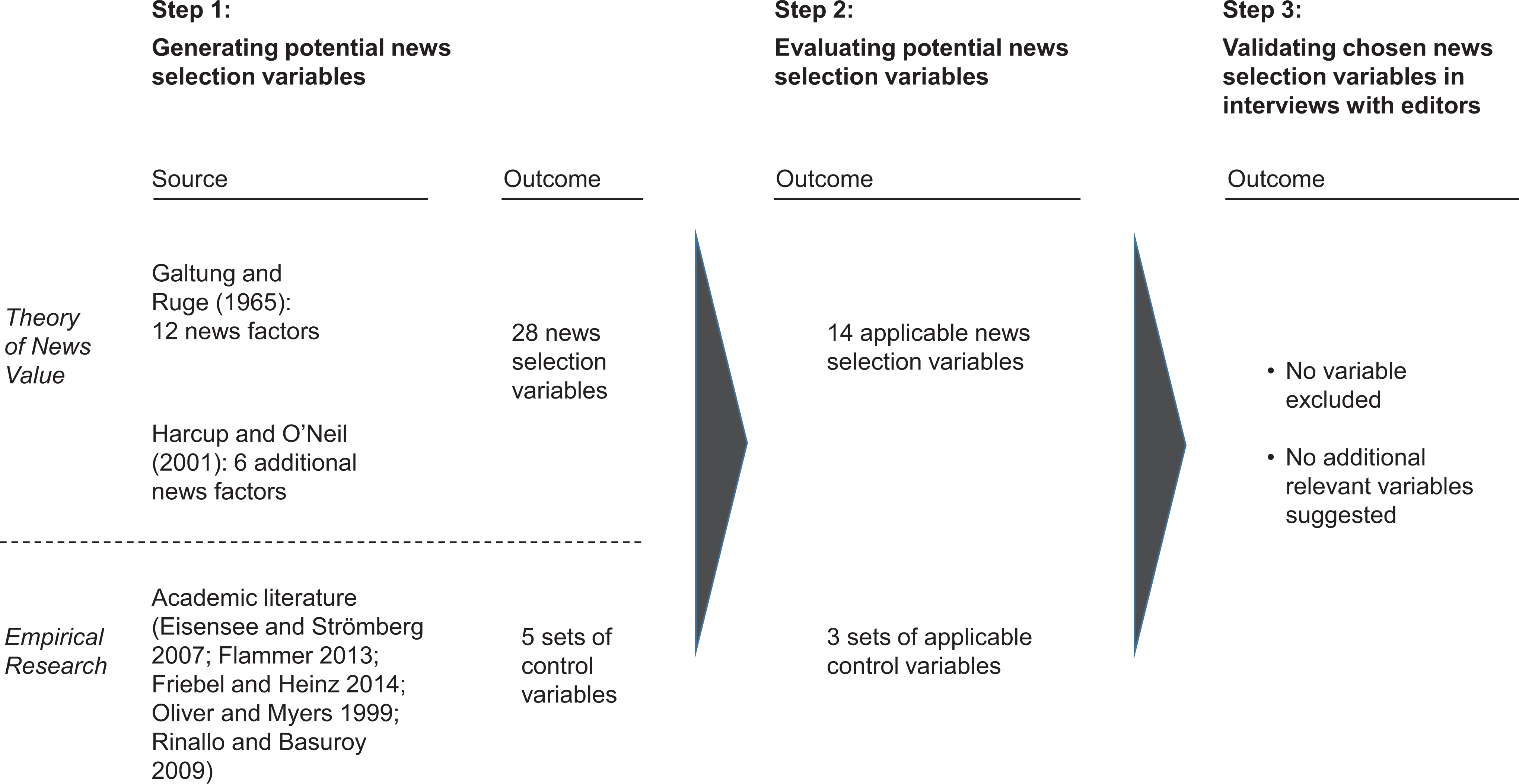

We proceeded in three steps (Figure 1). We began with the original news factors (12) proposed by Galtung and Ruge (1965) and their major extension (+6 news factors) by Harcup and O’Neill (2001). The description of the news factors provides the basis for our understanding of their meaning that we transferred to the context of firms and brands. For example, when Galtung and Ruge refer to power elite as a news factor they describe this as stories involving powerful and well-known individuals, organizations, or institutions. In the corporate world, this can be transferred to brands that are strong (powerful) and salient (well-known). As a result, we consider the two variables brand salience and brand strength as specific news selection variables for our model. Another news factor is unambiguity, which suggests that an event is more likely to be selected if it can be understood more clearly and interpreted without multiple meanings (Galtung and Ruge 1965). To reflect unambiguity, we introduce a news selection variable that measures the evidence base of a CSI event. We ended up with a catalog of 28 potential news selection variables (for a detailed list, see Web Appendix Table WA.1) that represent factors proposed by Galtung and Ruge and Harcup and O’Neill. In addition to the logical generation of news selection variables, the relevant academic media literature in politics (e.g., Galtung and Ruge 1965), journalism (e.g., Harcup and O’Neill 2001), sociology (e.g., Oliver and Myers 1999), economics (e.g., Eisensee and Strömberg 2007), and management (e.g., Friebel and Heinz 2014) helped us identify five sets of potentially relevant control variables.

Process of deriving CSI news selection variables.

In a second step, we evaluated these variables according to their relevance in the context of our study and their measurability, by which we mean that the criterion must be objective and specific enough. Criteria such as positive news do not apply to the context of CSI events. Others, such as a surprising character of the news, are too vague to be clearly operationalized. The second step reduced the set of variables to 14 news selection variables and 3 sets of controls. This set of news selection variables is large and captures a great portion of the heterogeneity of CSI events.

In the third step, we conducted in-depth interviews with four newspaper editors to validate our selection. 1 The editors considered all news selection variables highly relevant on a rating scale from 1 to 5, except for political orientation and advertising relationship. We still kept these variables because the prior literature has documented their influence on editorial decisions (e.g., Gurun and Butler 2012; Larcinese, Puglisi, and Snyder 2011). We also used the interviews to identify new variables that met the aforementioned requirements, but no new variables came up.

Conceptual Model

Drawing on the theory of news value and the interviews with the editors, we suggest a model of how the media cover CSI events and how this affects the stock market (see Figure 2). We assume that a CSI event comes to the attention of a media outlet through various sources (e.g., own research, news agencies, press releases, social media). We do not investigate these sources further. The editorial team evaluates each event in terms of its newsworthiness. To be reported, the news must pass a certain threshold. The news selection variables determine the extent to which this threshold is crossed. We have derived these variables from the theory of news value as explained previously and shown in Figure 2. We distinguish three groups of variables that are specific to the brand, the CSI event, and the media outlet. Table 1 summarizes each news selection variable and its impact on media coverage in the first two columns. Columns 3 and 4 show the connection to the related higher-level news factor and its abstract meaning from which the variable was derived. We discuss details on measurement of the news selection variables subsequently.

Media coverage of CSI news and its impact on the stock market.

News Selection Variables for CSI Events and Their Correspondence to Original News Factors.

a News factor added by Harcup and O’Neill (2001).

Notes: News factors are based on Galtung and Ruge (1965) and Harcup and O’Neill (2001).

The main effects of the news selection variables appear in column 2 of Table 1. In line with insights from theoretical models (Gal-Or, Geylani, and Yildirim 2012), we also consider a special condition in which the advertiser concentrates its effort exclusively on one media outlet. This is called a selective advertising partnership. Finally, we allow for the possibility that the impact of CSI-related and media outlet–related variables depends on brand characteristics. However, the theory of news value is not sufficiently developed to advance a comprehensive set of moderators and a priori expectations on their influence. We therefore test for potential interaction effects and follow Steenkamp and Geyskens (2014) by using inductive reasoning to explain these effects. This inductive approach is also philosophically supported by Bass (1995).

Brand-Related News Selection Variables

Brand salience (+), brand strength (+), and brand presence (+)

We consider three dimensions of a brand’s role and perception in the population: brand salience, brand strength, and brand presence. The first two constructs result from long-term processes of information processing, learning, and evaluation. They constitute the two key dimensions of brand knowledge according to Keller (1993) and cover both volume and valence. Brand salience reflects the prominence or level of activation of a brand in long-term memory (Alba and Chattopadhyay 1986). Brand strength builds on these knowledge structures but adds a directional meaning by integrating cognition, emotions, and behavioral intentions. Strong and salient brands should lead to higher media coverage when involved in a CSI event.

Brand presence refers to the fact that a brand may also be more or less present in short-term memory at a specific point in time. This presence fluctuates over time, as it is driven by short-term influences such as advertising pressure, rumors, viral activities, and so on. We identified two news selection variables that reflect brand presence in terms of recent brand advertising expenditures and relative online interest in the brand (Google Trends). The more present the brand is, the higher the press’s likelihood of reporting on the brand.

Negative WOM (+)

Negative WOM on a brand leads to more news articles on that brand. Hewett et al. (2016) show this phenomenon for banks in a complex multimedia system of communication. We expect the same for our context of CSI events.

Domestic brand (+)

The interviewed editors emphasized that stories on a domestic brand are more likely to be published, simply because domestic brands are more relevant to the average citizen. Readers will pay more attention to culturally similar items and take less notice of culturally distant items.

Brand CSI history (+)

If a topic has already been covered in the media, it is likely that it will continue to be defined as news for the near future. The reason is that the topic has become familiar and easy to interpret by the potential reader.

CSI Event–Related News Selection Variables

Domestic CSI event (+)

Events characterized by CSI occur in every corner of the world. An event that happens in the home country is closer to the people than an event outside the country, in line with the previous argument that cultural proximity increases the relevance of an event.

Evidence (+)

Ambiguity about the facts and consequences of an event hinders a clear interpretation of the event and also may undermine the credibility of newspapers. Thus, media outlets have a strong preference for clear and unambiguous stories (Galtung and Ruge 1965).

Other brand news (−)

Editors strive for a balanced composition of news to meet the demand of their readers for variety (Galtung and Ruge 1965). Therefore, the threshold for reporting on the CSI event of a brand will be higher if other brand news competes for space at the same time.

Media Outlet–Related News Selection Variables

Frequency: daily frequency (+)

Frequency of publication is an important variable that corresponds to the news factor frequency. The occurrence of a CSI event is much more in sync with a daily frequency and may be outdated to report on in a weekly or monthly magazine.

Political orientation [to the right: (−)]

Newspapers have their own editorial line, competitive strategies, and relationship with advertising partners that influences their business decisions (e.g., Gal-Or, Geylani, and Yildirim 2012; Larcinese, Puglisi, and Snyder 2011). Harcup and O’Neill (2001) summarize such considerations under the newspaper’s own agenda. We argue that the general political orientation of a media outlet shapes the editorial line and therefore may lead to more or less coverage of CSI stories. The left versus right contrast is the only scheme of political orientation that applies across countries. Profit-oriented companies and their representatives are the natural enemy of left-oriented ideologies. Their power and focus on profit maximization are considered the key source for exploitation of the workforce and unequal distribution of wealth (Marx 1867). News about corporate misbehavior therefore is most welcome in the fight against the power of these companies, which fits into the frame of reference for readers of left-oriented newspapers. In contrast, right-oriented media outlets tend to be more sympathetic toward private enterprises and capitalism as a whole. Consequently, we expect that left-oriented media are more likely to report on a CSI event.

Advertising relationship with media outlet (−)

Another potentially influential factor on editorial decisions is the relationship to advertising partners. Outlets rely on advertising money and want to maintain good relationships with their advertisers. News selection decisions are vulnerable to the interests of advertising partners (e.g., Gurun and Butler 2012; Rinallo and Basuroy 2009; Xiang and Sarvary 2007). Thus, we expect a negative effect of advertising on media coverage.

Selective advertising partnership with media (−)

In a theoretical analysis under the assumption of heterogeneous customer preferences and differentiated products, Gal-Or, Geylani, and Yildirim (2012) show that it may be rational for firms to place their advertisements exclusively in one media outlet. Moreover, their analysis implies that the outlet introduces even more positive reporting in favor of the advertiser compared with a situation in which the advertiser targets more than one outlet. This result suggests a negative effect of advertising investment on media coverage that is even stronger than for a nonselective partnership.

Impact on Stock Market Response

Finally, we consider the economic consequences of a CSI event in terms of its stock market response (see Figure 2). Prior research has produced mixed results. Whereas Flammer (2013) reports a negative stock market effect of environmental issues, other authors do not find a significant stock market response to CSI events (e.g., Groening and Kanuri 2013; McWilliams and Siegel 1997). None of these studies, however, analyzes the role of media coverage. We consider media coverage in our framework as a potentially important driver of the impact of a CSI event on stock returns. Because the news selection variables may also influence the investors’ reaction to a CSI event, we include both their potential direct effect and the indirect effect (mediation via media coverage).

Data

Sampling and Search Strategy

We apply our research framework (Figure 2) to five countries: the United States, Mexico, the United Kingdom, France, and Germany. We wanted to investigate countries that are relevant to the global economy, that represent different continents, and for which we have sufficient linguistic expertise to understand and rate news articles. The countries account for 38% of the world’s gross domestic product and even include an emerging economy (Mexico). The observation period covers 6.4 years from 2008 to mid-2014.

Sampling brands

We define the brands of YouGov’s BrandIndex database as our population. This database offers representative attitudinal brand information for a wide range of brands on a daily basis and has been used in prior research (e.g., Hewett et al. 2016; Luo, Raithel, and Wiles 2013). Across the five countries, we cover 2,300 brands. 2

Sampling media outlets

Using published data for 2012, we identify the media outlets with the largest print circulation and the leading online newspapers (based on website traffic; see https://www.alexa.com/siteinfo) in each country. Given that reach is the main driver of impact on society, consumers, and investors, the focus on leading newspapers should not be a critical limitation (Hewett et al. 2016; Kölbel, Busch, and Jansco 2017). Articles for most of the outlets were searchable in the LexisNexis database; if not, we looked for other publicly accessible archives. As a result, we analyze 77 outlets that include between 13 and 18 outlets per country (for the list of outlets, see Web Appendix 2).

Sampling CSI events

Unlike for product recalls, there is no requirement to report CSI events, and thus, no publicly accessible database is available. Therefore, it was necessary to uncover CSI events ex post on our own. We searched for potential CSI events within the sample of YouGov brands and media outlets country by country (for a similar strategy, see Flammer [2013]). We are aware that this strategy comes at a cost: we might overlook a few CSI events that were considered by all outlets in the selection stage but not reported by any of them in any of the five countries. This limitation should be less of an issue for the international brands that are part of YouGov’s brand list. At the country level, we repeatedly observe that media in one country report on a CSI event for an international brand (e.g., McDonald’s in the United States) but do not do so in other countries (e.g., McDonald’s in France). Through this mechanism, we also effectively uncover events that were not reported at all in a specific country.

Identifying CSI events

We proceeded as follows to identify CSI events (see also Flammer [2013]). We searched country by country for potentially relevant media reports on unethical behavior in all outlets using LexisNexis and online archives. We submitted the brand or company name together with up to 500 keywords per language on typical environmental (e.g., pollution, animal mistreatment), social (e.g., child labor, discrimination), and governance (e.g., fraud, corruption) issues. We identified more than 50,000 articles including a huge set of articles that were not related to CSI events. Therefore, one coauthor and six graduate students (among them native speakers in English, Spanish, French, and German) read and content-analyzed all articles. Using a set of criteria to identify a CSI event (for more details, see Web Appendix 3), we ultimately identified 1,054 CSI events. We assigned each event to one of the three categories of environmental, social, and governance issues. There was no disagreement for the majority of assignments (95%), and the few cases of disagreement were resolved by discussion.

We required that a media report must have occurred within 14 days after the first published report to be counted as coverage (see also Eisensee and Strömberg 2007; Oliver and Myers 1999). This time frame is more than sufficient to identify all reporting media outlets (see also Web Appendix 4 for a related robustness check). Note that we do not count the number of articles per outlet but only whether the outlet has reported on the CSI event.

Variable Operationalization

In this section, we describe how we measured the selection variables. We combined various databases to build the data set for estimation. We provide further details on the operationalization of news selection variables in Table 2 and correlations in Web Appendix 5. Variance inflation factors are less than the critical value of 10. Thus, we find no indication of collinearity issues.

Details on the Operationalization of the Variables.

a For more details on data collection and the exact items, see Web Appendix 6.

Brand measures

YouGov, a global market research company specializing in online panels, provided us with access to its BrandIndex database (for details, see Web Appendix 6). This unique database offers a representative measurement of brand attitudinal variables at the daily level. The brand variables have been used in prior research, albeit with different labels (e.g., Backhaus and Fischer 2016; Hewett et al. 2016; Luo, Raithel, and Wiles 2013).

Brand strength (YouGov’s BrandIndex) is a multidimensional index that runs from −100 to +100 (Backhaus and Fischer 2016; Luo, Raithel, and Wiles 2013). Brand salience measures the depth of brand knowledge and runs from 0 to 100. We used YouGov’s buzz metric and reverse-coded it to measure negative WOM (Hewett et al. 2016). The metric computes the number of respondents who heard something positive about the brand minus the number who heard something negative in the last two weeks relative to the total number. Using Google Trends data (Stephen and Galak 2012), we measured relative online interest in the brand to capture brand presence. To avoid reverse causality issues, we measured all variables before the CSI event. This ensures, for example, that negative WOM is not confounded by WOM created by the event itself. We measured recent advertising pressure, our second brand presence variable, with a stock variable. Ebiquity, an international market research company, provided us with advertising data across offline and online media (note, however, that advertising data were only available to us for the United Kingdom, France, and Germany). Brand CSI history of the recent past measures the number of CSI events for the focal brand in the 12 months preceding the current CSI event. Domestic brand is a dummy variable. It varies by country because McDonald’s is a domestic brand for U.S. outlets but a foreign brand for all other outlets in the sample.

CSI event measures

Domestic CSI event refers to the origin of the crisis event and is a dummy variable. Evidence is a dummy variable measuring whether a CSI event is based on rumor or on evidence. We measured other brand news using a dummy variable that explains whether other brand-related news was announced within a time window of three days before and seven days after the CSI event date (for a detailed list of events, see Web Appendix 7).

Media outlet measures

We measured political orientation of media outlets using a left–right scheme on a five-point rating scale (Fuchs and Klingemann 1990). Public sources such as worldpress.org provide political classifications (e.g., conservative, liberal) for a wide range of outlets. We converted these classifications in a first step into ratings on a five-point scale and asked 20 experts in politics to validate the ratings in a second step. We represented a brand’s advertising relationship with the media outlet using advertising stock, as with brand presence; the difference here is that we only considered advertising in the focal outlet. We identified a selective advertising relationship as one in which the focal brand has advertised in the focal outlet exclusively for the six months previous to the CSI event. Frequency of publication refers to weekly or daily online and offline issues.

Descriptive Statistics

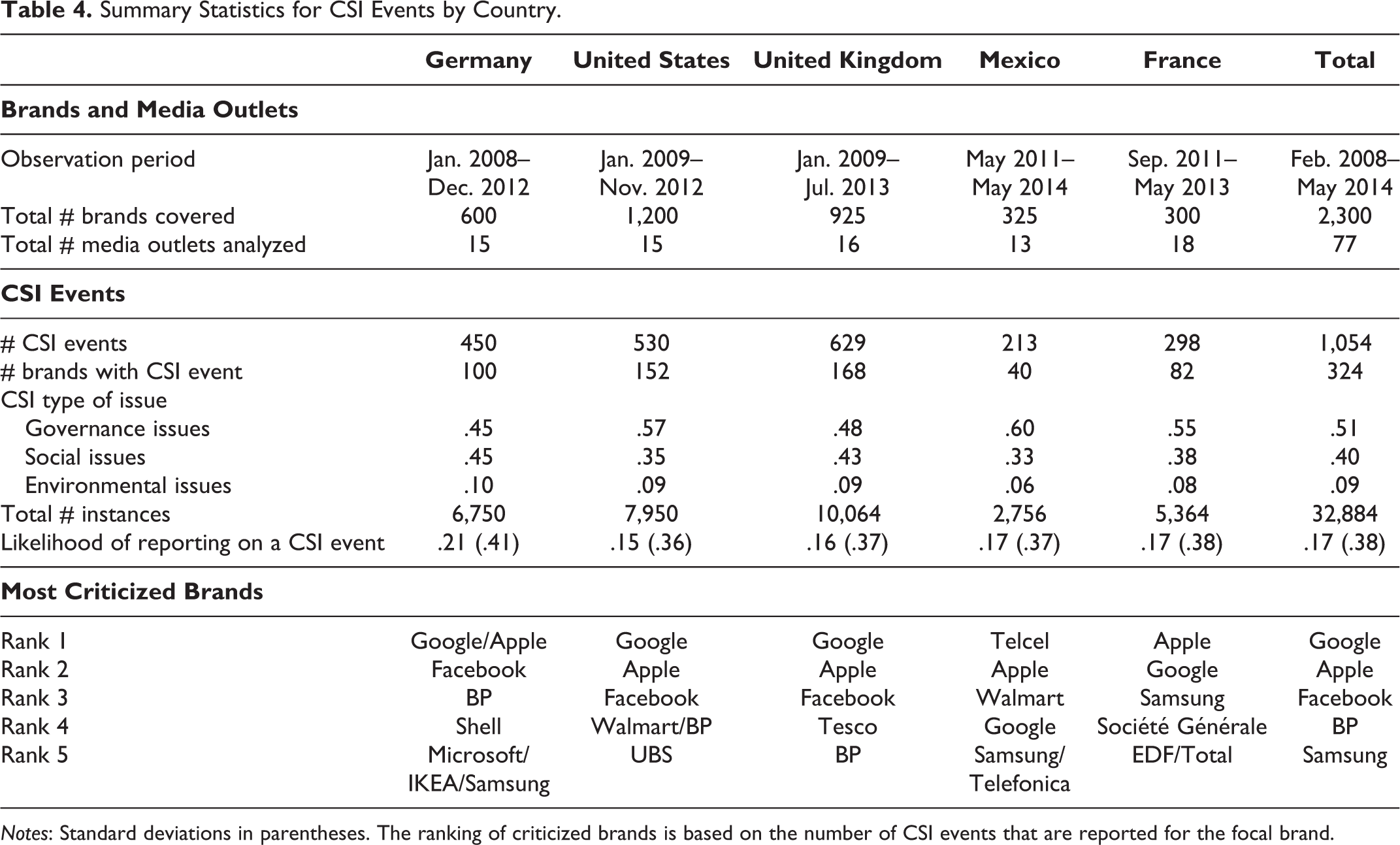

Table 3 presents descriptive statistics of the news selection variables. In Table 4, we show a summary of our search for CSI events. Note that our observation period differs somewhat across countries because YouGov started collecting its BrandIndex data at different points in time. From 2013 on, YouGov introduced a change in its methodology across markets. Even though the change was modest, we ended our observation period by country with this change to ensure a consistent measurement of the brand data.

Summary Statistics of News Selection Variables.

a We report the frequency of selective partnerships here. Of 296 brands, 49 advertised in only one media outlet for the last six months before the brand was involved in a CSI event. For model estimation, we use the advertising stock invested into the specific outlet.

Summary Statistics for CSI Events by Country.

Notes: Standard deviations in parentheses. The ranking of criticized brands is based on the number of CSI events that are reported for the focal brand.

In total, we identified 1,054 CSI events within the 6.4 years. Given the unbalanced data set, this leads to 32,884 instances in which a media outlet could have reported on a CSI event. They chose to do so in only 5,685 instances, which results in an average reporting rate of 17.29%. Of the 2,300 brands covered in our analysis, 324 were involved in these events, which represents a share of 12% (in total), or 1.9% per year. Note that the total number of events and brands is smaller than the sum across countries because of the significant overlap in brands and, thus, crisis events. As Table 4 shows, Google and Apple are among the top five most criticized brands in each country.

Model and Estimation

Econometric Model Specification

According to the theory of news value, news factors of an event add up in a compensatory, additive manner and collectively need to pass a threshold to become news. We do not observe the difference between the perceived newsworthiness and the threshold but only whether the threshold was passed and the news reported. Assuming that the error term of the latent evaluation of newsworthiness is independently, identically distributed extreme value gives rise to the binary logit model that we apply to the data.

Specifically, let

with

where

By specifying an event-specific constant αi, we control for event-specific news factors that are unobservable to us. Specifically, we capture their joint influence in the unobserved term μi that is assumed to be normally distributed with zero mean and variance

Equation 1 also includes two random error terms, vj and wk, which we assume to be normally distributed with zero mean and a variance to be estimated. By incorporating these error components, we account for unobserved effects that are specific to the outlet and the brand. Note that this specification allows the errors to be correlated within outlets and within brands.

Vector

We also considered including prior coverage of the CSI event by other outlets as a control. Although it seems plausible to assume that editors use competitors as sources of information, it also implies that editors reiterate the news of others, which goes against their principles of exclusivity and timeliness. The analysis of the diffusion of media reports in Web Appendix 4 suggests that there is no strong direct dependency among outlets. Media report the event either immediately or not at all.

We estimated the model with simulated maximum likelihood. We used the estimator implemented in LIMDEP 10.0, which approximates the integral to obtain the unconditional likelihood function by Monte Carlo simulation (see also Greene 2012, pp. 629–33, 733f).

Identification and Endogeneity

The large number of CSI events and media outlets creates an effective sample size of more than 32,000 observations. We exploit the rich variation of our focal variables across and within CSI events, brands, and media outlets (see Table 3) to identify the effects of interest. A CSI event is a rare and exogenous shock and occurs unexpectedly. Equation 1 models the media outlet’s endogenous decision process of whether to report on the event. We subsequently discuss potential endogeneity issues that involve advertising variables and other brand news.

Research on product recalls (e.g., Rubel, Naik, and Srinivasan 2011) suggests that firms may change their advertising expenditures ex ante in expectation of lower economic performance after a recall announcement. Because a recall is predictable and is certain to happen, firms have an incentive to do so. In contrast, it is not a given that CSI-related firm behavior will be revealed. Indeed, senior management might not even be aware of a CSI issue. Therefore, a proactive change in advertising prior to the disclosed CSI event is not very likely. Employing Granger causality tests, we do not find evidence that CSI events Granger-cause advertising, which does not prove exogeneity but is consistent with this assumption (see Web Appendix 8).

Endogeneity concerns might also be related to the variable other brand news, which can be interpreted as similar to a “confounding” event known from event studies. In these studies, observations with confounding events are simply removed from the sample so that they do not interfere with the event of interest. Our estimation results and conclusions are robust when we follow this procedure and exclude observations with other brand news (see Web Appendix 8).

However, we also have an interest in estimating the impact of other brand news on the reporting likelihood. Therefore, we must determine the extent to which a potential simultaneity between our dependent variable and the coverage of other brand news affects estimation. For this purpose, we adopted both an instrumental variables approach and a structural approach. The instruments are strong according to the incremental F-statistic (Angrist and Pischke 2009) and valid according to the overidentification Sargan–Hansen J-test (Wooldridge 2016). The Hausman–Wu test (Wooldridge 2016), however, does not support the assumption that other brand news is endogenous. Because instrumental variables estimation produces less efficient estimates, we do not focus on these results here, but we do report them in full detail, including statistics on the strength and validity of instruments, in Web Appendix 8.

Results

We present the results of model estimation in Table 5. In the first column of data, we report estimation results by using the full data set across all five countries. The second column of data shows the analysis for those countries for which we also have advertising data available. Following our conceptual model (see Figure 2), we also tested for possible interactions of brand-related variables with CSI event-related and media outlet-related variables. To be included, the interaction variable had to be statistically relevant (likelihood ratio test: p < .05), meet standards for collinearity statistics (variance inflation factor < 10), and not affect the stability of other estimated coefficients in the model (for similar approaches, see Bijmolt, Van Heerde, and Pieters [2005] and Edeling and Fischer [2016]). Specifically, we first tested for the significance of each interaction effect separately. In the following steps, we sorted out those interactions that did not pass the likelihood ratio test or caused severe collinearity issues after we included all interaction variables together. From this procedure, we identified and added four additional interactions to the model. Web Appendix 9 describes the four-step selection process in detail.

Drivers of Media Coverage of CSI Events (Estimation Results for Equation 1).

**p < .05.

***p < .01.

Notes: One-sided t-test only for expectations, two-sided t-test otherwise.

Brand-Related News Selection Variables

We find support for the relevance of all brand-related news selection variables. Estimated parameters associated with these variables are significant. Brands that show a higher salience level (β1 = .0133, p < .01) and have greater brand strength (β2 = .0055, p < .01) are more likely to be reported when they are involved in a CSI event. This probably explains the difference in coverage of the U.S. fraud case in our introductory example. Goldman Sachs is by far the stronger and more salient brand. Therefore, three times more media reported on Goldman Sachs than on J.P. Morgan. We also find evidence for a higher likelihood for brands that are more present, as reflected in their recent advertising pressure (β3 = .9 × 10−5, p < .05) and online interest (β4 = .4 × 10−4, p < .01). In 2012, 60% of the leading German news outlets reported on L’Oréal, which was accused of illegal campaign donation in the presidential elections. Being a strong and salient brand, the unusual high media coverage for a foreign brand involved in a foreign governance issue event might be also explained by the strong brand presence of L’Oréal due to the extraordinary high advertising expenditures around the event.

The results suggest that the level of negative WOM about a brand before the CSI event increases the chance that a media outlet reports on that event (β5 = .0091, p < .01). The chance is also greater if the brand is a domestic brand and if the brand has had more reported CSI events in the past (β6 = .0795, p < .01). Note that we use domestic brand as a reference category to allow for the identification of the interaction effect of foreign brand with domestic event and other variables. Therefore, we report a negative parameter estimate for foreign brand in Table 5 (β7 = −.5464, p < .01).

CSI Event–Related News Selection Variables

All expected relationships are supported with respect to our CSI event–related variables. A media outlet is more likely to cover a story on a domestic CSI event (β8 = .7181, p < .01). Conversely, this means that foreign events are less reported, which could be the reason for the low coverage of Apple’s use of underage interns in India. Despite the high popularity of the brand, only 13% of U.S. media covered the story. The results also show that a CSI event is more likely to be covered if it is based on evidence (β9 = .3024, p < .01). The existence of other brand news around the event date, however, reduces the chance that the CSI event will be reported (β10 = −.3732, p < .01).

Media Outlet–Related News Selection Variables

Media outlet characteristics also have an influence on the chance that a CSI event is reported. If the media outlet is issued at a higher frequency (e.g., daily versus weekly: β11 = 1.5006, p < .01), the likelihood of reporting the CSI event is greater. The last column of Table 5 shows that the parameter estimate for political orientation of the outlet is consistent with our expectation for the subsample of countries where we also control for advertising (β12 = −.0301, p < .05). Thus, left-oriented media are more likely to report on a CSI event. A deeper recent advertising relationship of an outlet with a brand involved in a CSI event reduces the likelihood of being reported in that outlet (β13 = −.0001, p < .05). As expected, the effect is even stronger when the advertising partnership with the brand is selective (β14 = −.0141, p < .01).

Interaction Effects

Being a foreign brand appears to make a difference for the role of news selection variables. We detect three significant interactions of variables with this brand characteristic and one more interaction between total advertising and political orientation. We discuss the results next.

Domestic CSI event × foreign brand (+)

A domestic CSI event increases the likelihood of reporting. This likelihood is even greater if a foreign brand is involved in the event (β15 = .5754, p < .01). From a theoretical perspective, this finding is consistent with the idea of ethnocentrism (Shimp and Sharma 1987). According to this idea, consumers tend to behave patriotically and want to protect their domestic economy. Catering to the preferences of patriotic consumers, media outlets are more critical toward foreign brands when these brands are involved in a potential scandal in their home country. A prominent recent example is the Volkswagen pollution scandal, which was covered in 100% of the leading U.S. media.

Other brand news × foreign brand (+)

We find that the negative effect of other brand news is weaker for foreign brands (β16 = .0951, p < .05). We draw on the notion of consumer patriotism to explain this result. Editors seem to be less willing to substitute the CSI event for other news on the foreign brand because a negative event associated with the foreign brand reinforces beliefs about the strength of the home economy that needs to be protected.

Advertising relationship with media outlet × foreign brand (+)

The attenuation effect of advertising appears to be weaker for foreign brands (β17 = .0006, p < .01). For an explanation, we again follow the line of argument that consumers tend to favor domestic brands over foreign brands and want to protect their domestic economy. Catering to the preferences of patriotic consumers conflicts with outlets’ strategic interest to protect their advertising relationship. Compared with domestic brands, this strategic interest weighs less for foreign brands.

Political orientation × total advertising (+)

Left-oriented media outlets are more likely to report on a CSI event, but this effect becomes weaker for brands with higher advertising pressure (β18 = .5 × 10−5, p < .01). Conversely, although right-oriented media might be less prone to report on a CSI event, their editors cannot ignore characteristics that cater to the preferences of their readers. Particularly, when a brand is more present among readers because of high advertising expenditures in the recent past, not reporting the news may backfire and threaten the credibility of the outlet.

Control Variables

We also find that several of our control variables influence the likelihood of covering a CSI event in the media. Unsurprisingly, the likelihood has increased over time (β19 = .0008, p < .01), confirming the view that companies are increasingly held accountable for their social and environmental footprint. Social issues tend to be less covered in the media (β20 = −.2210, p < .01) relative to governance and environmental issues. We also observed differences in the level of CSI news coverage across countries (e.g., Germany vs. United Kingdom, β21 = .4374, p < .01).

Classification Performance

Table 6 shows three classification statistics computed for different thresholds of classifying an event as being reported. The model user needs to decide about the threshold level for the predicted probability on which an event is classified as being reported. Note that we face a highly unbalanced sample, with only 17.3% of “positive” reporting events. This makes it difficult for any model to beat the maximum chance criterion where each event is classified as unreported or “negative,” yielding a classification rate of 82.7%. Therefore, measures such as precision, recall, and the F1 score are more informative about the classification performance of the model.

Model Classification Statistics.

Notes: Model statistics are based on Sample I (the United States, France, Germany, Mexico, and the United Kingdom). Threshold defines the predicted probability from which on an event is classified as being reported. Recall computes the number of correctly identified reporting events relative to all reporting events in the sample. Precision computes the number of correctly identified reporting events relative to all predicted reporting events. The F1 Score measures the harmonic mean between recall and precision.

Precision focuses on the power of the model to correctly classify events as being reported. For example, if our model predicts 20 reporting events and 15 of these predictions are correct, the precision is 75% = 15/20. Assuming that the total sample included 40 reporting events, the model would have identified 37.5% = 15/40 in total, which is the recall rate. Recall, therefore, is a measure of completeness. It depends on the context and objectives of the user of the model, which type of performance is more important. Table 6 shows that the model performance changes with the threshold in different directions for the two metrics. The F1 score is a compromise because it considers both precision and recall (harmonic mean of both statistics). For our model, it is largest at a threshold of .10 and achieves a reasonable classification score of .404, whereas 1.0 represents perfect prediction.

Robustness Checks

We performed several additional analyses to determine whether our estimation results are robust. For the sake of brevity, we cannot report all results here but refer to Web Appendix 10.

First, we tested alternative model specifications. We substituted a count variable of the number of media outlets reporting on the CSI event for our dependent variable and estimated a linear regression model and a zero-inflated Poisson model. Results are highly consistent with our focal model’s results (see columns 2 and 3 in Table WA10.2). However, we do not use these models, because they restrict us in investigating the media-specific variables. In another specification, we included fixed effects for brand and outlet in Model 1 instead of their respective error components. The results do not change substantially.

Second, we used alternative ways to operationalize news selection variables. We measured the variables brand salience, brand strength, advertising stock, selective advertising partnership, and brand CSI history differently. The results in Table WA10.3 do not suggest anything different.

Third, we added new, potentially relevant variables—specifically, brand strength dispersion (Luo, Raithel, and Wiles 2013), square of brand strength, a dummy for business newspapers as outlet (e.g., Financial Times), and several financial variables for listed companies from Compustat. Likelihood-ratio tests indicate that none of these variables are relevant (p > .05).

Fourth, we performed three analyses to check for the robustness of our sampling strategy for CSI events and brands. We deleted the 50 weakest brands (15%) on the basis of their brand strength rating from the sample and reestimated our model. By this analysis, we simulate a possible sampling effect arising from a concentration on well-established, larger brands. Table WA10.5 (column 2) shows that results are consistent with our focal sample.

In another analysis, we randomly deleted one outlet that reported on a CSI event for each event and reestimated the model. By this procedure, we simulate that the information about the event has been uncovered by an exogenous source and not by an outlet included in the model estimation. Results are again stable (see Table WA10.5, column 3).

In our final analysis, we restrict our sample to include only those brands that are covered by YouGov in more than one country. By this restriction, we minimize the possibility that we exclude important events, because they have not been reported by any outlet in one country. The proportion of these nonreported events in a country is fairly high in this subsample with 39%. The results based on this subsample in Table WA10.5 (column 4), however, do not suggest a different conclusion.

Event Study

In this section, we investigate the capital market impact of a CSI event. We adopt the established event study methodology to test the effects in a subsample of 97 brands/firms and 347 CSI events for which we have U.S. stock market data available.

Model and Data

We use the Fama–French–Carhart four-factor model to measure the abnormal returns (Carhart 1997; Fama and French 1993). This model accounts for four risk factors to explain daily stock returns and has been extensively applied in marketing research (e.g., Borah and Tellis 2016). The premise is that daily abnormal returns are due to the unanticipated CSI event and driven by its media coverage and news selection variables (see Figure 2). Abnormal returns are given as follows:

where Rkt is the stock return of a firm that owns brand k on day t and E(Rkt) denotes the expected return from a regression of Rkt on the risk factors. These risk factors are Rmt for the stock return of the benchmark market portfolio, SMBt for excess return of small over big stocks, HMLt for the difference in returns between high and low book-to-market ratio stocks, and UMDt for the momentum factor. The

To estimate the Fama–French–Carhart model, we need data from the U.S. capital market. This restricts our sample to firms that are primarily listed at U.S. stock exchanges. It applies to 97 brands and 347 CSI events, which creates a healthy sample size that is comparable with prior event studies. We obtain data on the risk factors from the Kenneth R. French online data library. The benchmark portfolio includes all NYSE, AMEX, and NASDAQ stocks (for details, see https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/). Stock return data are obtained from Thomson Reuters.

Following previous research (e.g., Hsu and Lawrence 2016), we use an estimation window of 250 days until 15 days prior to the CSI event to estimate the return equation. We select a three-day event window [−1 to 1] to calculate cumulative abnormal returns (CARs). This window has been used in prior studies to account for lead and lagged effects of stock market response (e.g., Borah and Tellis 2014; Dinner, Kushwaha, and Steenkamp 2019). The results are fully robust to other windows [−1 to 0], [−1 to 2], and [−1 to 3] (see Web Appendix 11).

Estimated CARs [−1, 1] are the dependent variable in a second step, in which we regress this variable on media coverage (measured as a count variable: 0–15), our news selection variables, aforementioned control variables, and additional financial control variables that have been used in previous research (e.g., Dinner, Kushwaha, and Steenkamp 2019). Specifically, we estimate the following equation:

where ∊ik is an i.i.d. error term, and the δ parameters are to be estimated. Note that we cannot include the publication frequency dummies. By definition, media coverage is the sum of the reporting frequencies across daily and weekly outlets scaled by the total number of outlets. We test for the inclusion of firm-specific effects to control for unobserved brand/firm heterogeneity. The Baltagi–Li Lagrange multiplier test (Baltagi and Li 1990), however, rejects this assumption (χ2(1) = .1323, p > .70).

The fact that media outlets differ in their decision to report on the CSI event does not create a selection bias because these decisions are aggregated in our focal media coverage variable. But it could be that unobserved variables influence both investors’ reaction and media coverage. This would introduce a potential correlation of predictors with the error term and thus bias the results. By including the news selection variables in the event model, we reduce the danger of an omitted variable bias, but we cannot rule it out. We therefore test for the exogeneity of media coverage by using the Hausman–Wu test (Wooldridge 2016). By employing two alternative sets of outside instruments, the test does not suggest endogeneity. Consequently, we estimate the model with ordinary least squares. For the sake of brevity, we report details on instruments and tests in Web Appendix 12.

Results

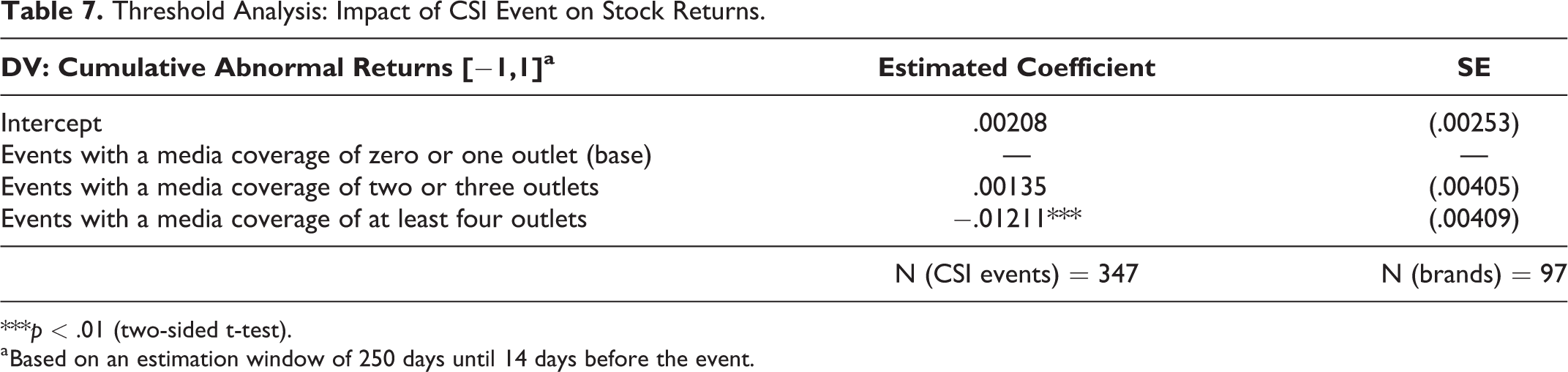

Threshold analysis

The analysis reveals a nonsignificant main effect of the average cumulative abnormal returns (

Threshold Analysis: Impact of CSI Event on Stock Returns.

***p < .01 (two-sided t-test).

a Based on an estimation window of 250 days until 14 days before the event.

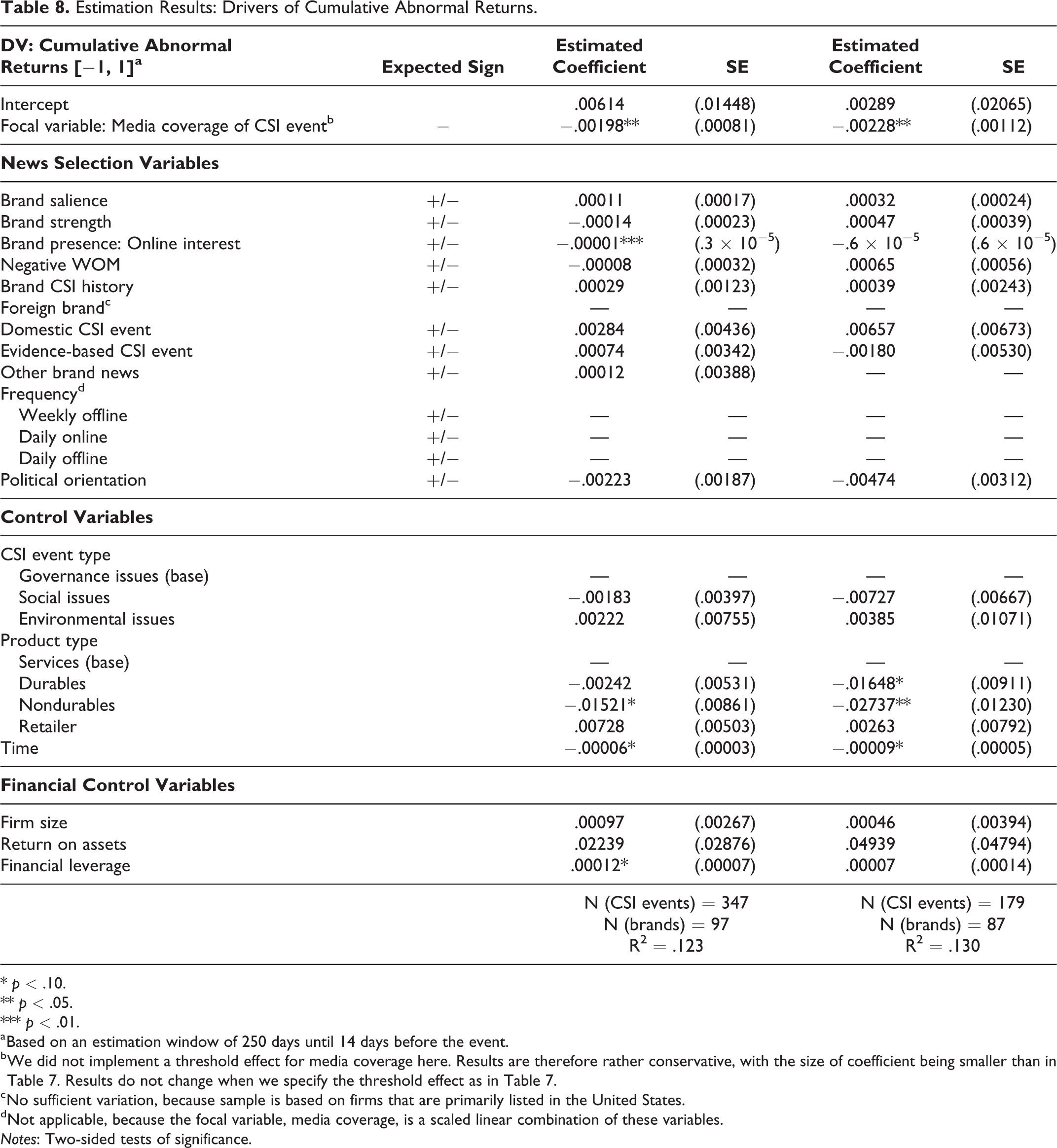

Driver analysis

Table 8 shows the results from estimating Equation 3. We include the events with other brand news in the first results column but exclude them as confounded events from the sample in the second results column. We find a significant negative effect (

Estimation Results: Drivers of Cumulative Abnormal Returns.

* p < .10.

** p < .05.

*** p < .01.

a Based on an estimation window of 250 days until 14 days before the event.

b We did not implement a threshold effect for media coverage here. Results are therefore rather conservative, with the size of coefficient being smaller than in Table 7. Results do not change when we specify the threshold effect as in Table 7.

c No sufficient variation, because sample is based on firms that are primarily listed in the United States.

d Not applicable, because the focal variable, media coverage, is a scaled linear combination of these variables.

Notes: Two-sided tests of significance.

Discussion and Conclusions

The empirical findings lend strong support for the relevance of the theory of news value to explain the coverage of unethical firm behavior. In this section, we discuss managerial implications and contributions to marketing theory. Before discussing implications, however, we must first examine the practical size of the effects.

Magnitude of the Influence of News Selection Variables

Because estimated parameters cannot be directly compared to evaluate the relative importance of news selection variables, we use Models 1 and 3 to simulate the effect of a change in a news selection variable on media coverage and stock return. The stock return effects reflect the impact of media coverage because we find no significant direct effects for the news selection variables. As a baseline (base scenario), we define a situation in which all variables are set to their sample average. The reporting likelihood is 17.3% in the base scenario. For simulation, we either increase a metric variable by two standard deviations or set a dummy variable to 1. We always apply parameter estimates of the larger sample when available (see Table 5). Changes are expressed in percentage points (unless stated otherwise) in the following subsections and in Figure 3.

Impact of news selection variables on likelihood of reporting (in percentage points) and on stock returns.

Effect on media coverage

Figure 3 shows the results of the simulation. Overall, the impact of news selection variables is quite substantial. Several variables produce a relative change in the likelihood of reporting of 30% and more. Considering brand-related variables, four variables stand out in their capacity to increase the likelihood of reporting. First, the level of brand salience increases the likelihood by 6.7%, the level of brand strength by 3.5%, and the level of negative WOM by 4.7%. For the simulated higher brand salience, this means that 39% more media cover the CSI event (rise of base likelihood from 17.3% to 24%). When the involved brand is a domestic brand, the reporting likelihood rises by 5.5%. It also increases by 4.3% for brands with more CSI events in the recent past. Salient, strong national brands appear to be at a substantial disadvantage when it comes to media coverage of a CSI event.

Among CSI event–related drivers of media coverage, two essential drivers stand out: domestic event and its interaction with a foreign brand. The likelihood of reporting rises by 7.7% for a domestic event. The increase is even larger for a foreign brand (13.9%), implying that 80% more media report on the event (rise of base likelihood from 17.3% to 31.1%).

Considering media outlet-related variables, the frequency of publication plays an important role. Unsurprisingly, a daily frequency raises the likelihood by 3.6% (online) and 3.9% (offline). The effects of political orientation and advertising relationship are relatively small. However, we find a strong impact of a selective advertising partnership. Such a partnership lowers the reporting likelihood by −7.8%, to a level as low as 9.5%.

Effect on stock returns

The second column of Figure 3 shows the simulated effects on stock return. On average, a firm loses US$321 million as a result of a CSI event when four or more media outlets in the United States report on the event. This is a substantial financial loss. The analysis of the news selection variables suggests that this loss is significantly larger under several conditions. For salient and strong brands, the loss increases by US$216 million and US$114 million, respectively. A higher negative WOM also expands the loss by US$154 million. The largest impact, however, arises from a domestic CSI event and one that involves a foreign brand. Here, the financial damage rises by US$246 million for a U.S. brand involved in an event in the U.S. and US$426 million for a foreign brand involved in an event in the U.S., respectively, to −US$567 million and −US$747 million, respectively. This represents a substantial burden for any company. Note that evaluating the financial effect of a selective advertising partnership is not meaningful, because the lower reporting likelihood applies by definition to only one outlet.

Implications for Marketing Theory

This study makes important theoretical contributions to research on corporate misbehavior. While it is well known that media coverage aggravates the negative effects of CSI and product recalls on various firm outcomes (e.g., Backhaus and Fischer 2016; Kölbel, Busch, and Jansco 2017; Liu and Shankar 2015), we do not know much about when and why the media cover such corporate news. This study is a first step toward answering these questions and extends the literature on CSI and firm crisis events.

Stock market effect of media coverage

Although prior research in marketing points to the power of the media to drive stock market effects (e.g., Van Heerde, Gijsbrecht, and Pauwels 2015; Gao et al. 2015) it has not been established for the coverage of CSI events. The results of our study, however, suggest that coverage in a single high-reach outlet is insufficient to drive stock market response. Rather, there is a critical mass of at least four high-reach outlets in the U.S. that need to report the CSI event. Adding to this result, we find that, on average, a CSI event does not provoke a stock market reaction (

Brand shield effect

It has been long argued that strong brands may shield the company from the negative impact of a CSI event. Researchers used both experimental data (Ahluwalia, Burnkrant, and Unnava 2000; Klein and Dawar 2004) and observational data (Backhaus and Fischer 2016) to demonstrate the shield effect with respect to brand-related consumer metrics. The effect, however, is less studied in terms of stock market reactions.

We do not find evidence for a direct effect of brand salience and brand strength on stock market response. However, because they significantly drive media coverage, their indirect effect via media coverage is negative. Consequently, companies with strong brands suffer more from a CSI event. This finding challenges the view that a strong brand generally protects the company from the negative impact of a crisis event.

Foreign brand effects

We also extend the literature on international marketing. This study shows that the extent of media coverage largely depends on whether the brand is a foreign or a domestic brand and whether the CSI event occurs in the home market or a foreign market. As a result, the potential harm effects on brand equity are not uniform across countries, which adds to the complexity of building and maintaining international brands. Being a foreign brand backfires in various ways. Initially, it appears to be an advantage in terms of the main effect on media coverage. The likelihood of reporting is higher by 5.5% for a domestic brand (see Figure 3). Yet our analysis also points to several interaction effects with respect to foreign brands. According to the results, it hurts more to be a foreign brand that is involved in a domestic CSI event. In addition, foreign brands do not benefit as much as domestic brands from the attenuation effects of other brand news and advertising investments.

Coverage due to political orientation and total advertising

Although the focus of our study is generally on the various drivers of media coverage and not on media bias, we consider two variables, political orientation and advertising, that have been studied in the media bias literature (e.g., Gurun and Butler 2012; Larcinese, Puglisi, and Snyder 2011). Both variables have not been considered in the context of reporting on events of CSI, yet. For political orientation, we find evidence in support of our expectation that left-oriented media are more inclined to report on unethical firm behavior. However, we also show that this difference reduces the larger the total advertising spending of the brand. The higher the current presence of the brand due to its total advertising spending across all media channels, the higher the likelihood that a right-oriented media outlet covers a CSI story.

We also add to the literature on advertising and media relationships. Prior research has suggested that advertisers have a strong influence on media outlets to cover their products more often and in a favorable manner (e.g., Gentzkow and Shapiro 2010; Rinallo and Basuroy 2009). We extend this knowledge and document that advertisers may also have the power to deter media from covering negative stories about their brands. While the effect is comparatively modest in general, it becomes larger provided that the advertiser and media outlet are in an exclusive relationship.

Implications for Firms

What are the implications for firms and managers? First, our study educates managers that CSI events are not equally covered in the media. While many of them might have real-world examples available, suggesting differences in coverage of CSI events, it remains difficult to predict when an event will be broadly covered in the press. This study can help managers predict and anticipate media attention so they can prepare their organizations to better handle the risks. It would be particularly helpful to predict whether a CSI event has the potential to exceed the threshold of four media outlets for the impact on the U.S. stock market. Managers of investor relations might then think about useful measures to deal with the expected increased attention of investors and their likely need for more information. Further research could answer the question of what kind of information and measures this would be.

Companies might also consider the strategic launch of other neutral or positive brand news when being confronted with the possible reporting of a CSI event. Other brand news has the power to crowd out negative CSI event news, as the analysis suggests. International brand managers should be aware of the higher likelihood of media coverage if their brand is involved in a CSI event in a foreign market. While this alone can hardly be the main reason to adopt a local brand-name strategy, it should be considered in these often-difficult strategic decisions.

Furthermore, the results show that advertising investment—and in particular, investments in selective partnerships—helps shield against broader media coverage of a CSI event. This finding points to an overlooked role of advertising investment in traditional, high-reach newspapers, which have come under increasing pressure from digital media channels. The rather tiny marginal effect of advertising in Figure 3 may create the impression that it is of only marginal relevance to the firm. However, even a tiny effect could cause a CSI event to cross the threshold of coverage in four media outlets, which differentiates between no financial market impact and an average loss of US$321 million.

Limitations and Future Research

This study is not without limitations that may stimulate future research. Although we cover several important Western economies, we do not know the extent to which our results extend to other important economies such as China, India, or Japan. Because of cultural differences, not all or possibly additional news selection factors may play a role, which would be interesting to test for in a further study. We also focus on CSI issues, but we acknowledge that there are many other potentially negative firm events (e.g., celebrity scandals). These events would be worthwhile to study. Finally, we consider the coverage of single CSI events. Future work could study the dynamics and evolution of a broader CSI issue that often encompasses a string of several single CSI events and related media stories.

Supplemental Material

Supplemental Material, Media_Coverage_CSI_Events_Web_Appendix - When Does Corporate Social Irresponsibility Become News? Evidence from More Than 1,000 Brand Transgressions Across Five Countries

Supplemental Material, Media_Coverage_CSI_Events_Web_Appendix for When Does Corporate Social Irresponsibility Become News? Evidence from More Than 1,000 Brand Transgressions Across Five Countries by Samuel Stäbler and Marc Fischer in Journal of Marketing

Footnotes

Acknowledgments

The authors are grateful to the vice editor-in-chief of Bild Zeitung, the managing and business editor of Rheinische Post, and the business editor of taz-die tageszeitung for their cooperation. They thank YouGov for providing access to their BrandIndex database and Ebiquity for providing advertising data. They also thank participants of the 2018 Media Economics Workshop; seminars at Massey University of New Zealand, University of Auckland, Auckland University of Technology, and University of Groningen; the EMAC Conference 2017; and Marketing Science Conference 2016 for helpful discussions. The authors thank six research assistants who helped read and content-analyze the data. Finally, the authors thank Marnik Dekimpe, Els Gijsbrechts, Johannes Münster, and John Roberts for insightful comments on earlier versions of the article.

Associate Editor

Jan-Benedict Steenkamp

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.