Abstract

What are the political implications of Chinese loans to borrowing countries? Our argument is that similar to other forms of international finance, loans from China provide leaders with additional resources to maintain their power. The nature of China’s lending practices—characterized by an absence of good governance conditions—offers a unique advantage to political leaders, allowing corrupt leaders who receive loans from China to stay in power for longer periods. To support this argument, we conducted an analysis of a dataset of 115 developing countries from 2000 to 2015, focusing on the relationship between Chinese loans and leaders' political survival. Our findings indicate that Chinese loans positively impact leader survival, with the strongest effects observed in more corrupt regimes. To address endogeneity concerns, we employ a shift-share instrumentation strategy and several additional tests. Our analysis underscores the importance of Chinese lending to both international and domestic politics.

Introduction

At the turn of the twenty-first century, China emerged as a major lender in sovereign debt markets to developing countries. China has reportedly invested or lent over $1 trillion the past two decades (Horn, Reinhart and Trebesch, 2020). Coordinated under the banner of the Belt and Road Initiative (BRI) since 2013, Chinese loans have sparked controversy. Countries like the United States are concerned that the Chinese loans are buying undue influence in partner countries. 1 In addition to China’s ambitions, the sustainability of Chinese loans raises concerns, as over 35 percent of Chinese lending projects experienced major implementation problems, and an increasing number of borrowing countries face financial distress (Malik et al. 2021).

Given concerns about the undue influence of Chinese finance and low-quality projects, it remains unclear why leaders accept Chinese loans. 2 We argue that similar to other types of financial resources, Chinese loans provide leaders with political benefits. Leaders will need to satisfy their key constituents and fend-off opposition groups to stay in power. The nature of China’s lending also provides a unique benefit to leaders: the ability to utilize funds without conventional domestic or international constraints. Given the opaque nature of Chinese loans, countries frequently do not even report these among their official debts, hiding a country’s true indebtedness while allowing funds to be used for political purposes with little oversight (Brown 2023; Horn, Reinhart and Trebesch, 2020). Given these features, we argue that leaders have more discretion when using Chinese loans for political purposes, particularly through underhanded channels. Consequently, we hypothesize that the most corrupt leaders who receive Chinese loans will stay in power longer.

To test our argument, we examine the relationship between Chinese loans and leader survival in a dataset of 115 developing countries in the time span between 2000 and 2015. We find that Chinese debt increases leader survival. This effect is strongest for more corrupt leaders, highlighting the nebulous nature of these sovereign transactions. The analysis addresses concerns about endogeneity using a shift-share instrumental variable design. Several pieces of evidence suggest that Chinese loans allows leaders to pay off key constituents, including elites with close ties to the incumbent leader and politically affiliated constituencies. Specifically, we find a positive relationship between Chinese loans and capital flight into offshore accounts for corrupt leaders but not for non-corrupt leaders. Moreover, we find that Chinese loans increase the re-election probability for leaders and their parties. Conversely, we do not find that Chinese loans affect measures of aggregate demand, government repression, and public goods provision at the national level. These findings help dismiss alternative mechanisms through which Chinese loans might boost leader survival.

Our argument and analysis enhance our understanding of the political consequences of China’s foreign economic policy-making. While researchers have begun to examine the political effects of Chinese lending in borrowing countries—such as project distribution (Dreher et al. 2021), compliance with international organizations' standards (Hernandez 2017; Watkins 2021), and governance (Cormier 2023; Ping, Wang and Chang, 2022)—our study is the first to link the political benefits of Chinese loans to leaders' ability to stay in office. Previous research has shown the political importance of international financial resources to leaders' political survival (DiGiuseppe and Shea 2016; Licht 2010; Yuichi Kono and Montinola 2009). We build off these findings and highlight the unique role that China lending has in international finance and on leaders.

Our argument and results also relate to the literature on China’s international engagement (Braeutigam 2011; Gelpern et al. 2023; Horn, Reinhart and Trebesch, 2020; Petry 2021; Zeitz 2021). Chinese lending dynamics have the potential to affect the recipient country’s economic relations such as trade (Davis, Fuchs and Johnson, 2019) and can even intercede into the aid-conflict nexus (Strange et al. 2017). Our research complements a fast-growing body of literature on the political implications of Chinese lending in developing countries (Braeutigam 2011; Bader 2015; Bunte 2019; Iacoella et al. 2021; Kaplan 2021; Ping, Wang and Chang, 2022).

The Political Economy of Chinese Loans and Leader Survival

Leaders are survival-motivated. To remain in power, they will need to satisfy the demands of their constituents, relying on a pick-and-mix range of private and public goods, which requires access to fiscal resources (Bueno de Mesquita et al. 2003; Bueno De Mesquita and Smith 2010). When leaders are dependent on domestic groups for fiscal resources (i.e., tax revenue), leaders will struggle to use these resources for political gain without making political concessions (Levi 1988, 12). However, non-tax resources allow leaders to spend on key constituents without extracting resources from the general population. In general, access to these non-tax revenues increases the political survival of leaders (DiGiuseppe and Shea 2016; Morrison 2009; Yuichi Kono and Montinola 2009). These resources include natural resource rents, foreign aid, and sovereign credit.

Sovereign credit is a particularly important non-tax resource for leaders, as it allows them to spend more in the short term than they otherwise could. However, in the long term, the incentive to over-rely on sovereign credit can be a double-edged sword, potentially leading to unsustainable debt burdens and economic instability. Consequently, private investors and many official lenders exercise caution in extending substantial credit to developing states lacking a credible credit history. In this context, the entrance of China into the lending market has broadened credit access for many emerging markets and developing countries. China’s lending, predominantly conducted under the Belt and Road Initiative (BRI), has provided access to credit for countries that might not otherwise receive it, or at least not in the same magnitude (Braeutigam 2011; Carney 2023; Dreher et al. 2022; Jenkins 2022).

Theoretically, Chinese lending can enhance leaders' chances of political survival in several ways. Firstly, akin to other financial sources, it relaxes a leader’s fiscal constraints. Therefore, leaders with greater access to Chinese loans can more effectively utilize fiscal resources for their political objectives than those with less access. The availability of Chinese financing, especially for infrastructure projects and other public goods, can significantly free up fiscal space, allowing leaders to reallocate funds that would have otherwise been earmarked for infrastructure (Kaplan 2021). This reallocation enables them to invest in other popular spending programs, further bolstering their political support. Leaders motivated by political survival will allocate these resources in ways that maximize their chances of remaining in power. This often involves expanding the provision of public services and particularistic goods that cater to key constituencies and stimulate local economies (Braeutigam 2011). For example, in Ecuador, access to Chinese financing enabled the Correa administration to increase investment in highly popular government spending programs, thereby bolstering its political support (Lim and Ferguson 2022).

In addition, Chinese loans often finance projects that are relatively visible, large-scale infrastructure developments. For instance, in the case of Angola in 2002, China filled an important financing gap to rebuild the war-torn country in exchange for the country’s oil proceeds, essential to start rebuilding the country after years of conflict and the government’s popular approval (Braeutigam 2011; Corkin 2011; Brütsch 2014; de Carvalho, Kopiński and Taylor, 2022). These types of visible projects can significantly enhance the public’s perception of a leader’s effectiveness.

In addition to these direct effects, Chinese lending can also have indirect effects on leader survival. In particular, since Chinese loan projects may contribute to enhanced domestic investment and economic growth (Dreher et al. 2021; Kern and Reinsberg 2022), they may boost a leader’s popularity. 3 More popular leaders will be more likely to stay in power longer. Such effects would not be unique to Chinese loans: other sources of external finance may also have positive effects on a leader’s popularity, although the effects may be more contextual (Blair and Roessler, 2021; Baldwin and Winters 2020; DiGiuseppe and Shea 2015).

As China’s lending is built around the principle of domestic non-interference, leaders have substantial discretion in using these loans for political gain and reward key constituents (Dreher et al. 2021, 2022; Kaplan and Thomsson, 2017). For instance, Dreher et al. (2021) report that Chinese investment projects benefited regions where a country’s leader or their spouses were born. Similarly, China’s lending is less discerning about fiscal management in the borrowing state than other sources of sovereign credit. This is exemplified by the fact that Chinese loans do not always immediately show up on country’s debt balance sheet (Brown 2023; Horn, Reinhart and Trebesch, 2020).

Finally, Chinese loans do not contain clauses mandating sound macroeconomic policymaking or good governance practices, providing leaders with more leeway to increase public spending in ways that boost their political popularity (Cormier 2023; Dreher et al. 2022; Kaplan 2021). Furthermore, Chinese loans can provide financial means to extend control over national media and communication channels, thus becoming a potent tool for influencing voter sentiment (Carter and Carter 2022). In contrast to Western donors, Chinese lenders often overlook domestic political interference by leaders, ensuring a steady flow of credit that helps them remain in power, even under significant political and economic pressures.

Given these fiscal and political benefits of Chinese loans, we expect that more Chinese loans should help leaders stay in power compared to having access to fewer Chinese loans. We formulate this expectation in our first hypothesis:

Chinese loans increase leader tenure.

The first hypothesis posits that Chinese loans are similar to that of other non-tax revenues: the greater the amount, the more beneficial it is for leaders. Nevertheless, there are additional characteristics that distinguish the political and fiscal advantages of Chinese loans from other types of non-tax revenue. We anticipate that these unique features will be particularly advantageous to more corrupt leaders as compared to their non-corrupt counterparts. In general, a corrupt leader will be more likely to misappropriate public funds for personal gain than a non-corrupt leader. We argue that the lack of transparency and the lack of governance conditions associated with Chinese loans will facilitate that potential misappropriation for corrupt leaders more so than other types of non-tax revenue.

First, a key feature of Chinese finance is the lack of transparency around loan dealings (Brown 2023; Cormier 2023; Dreher et al. 2022). The opacity surrounding Chinese loan dealings will particularly benefit corrupt leaders. The “hidden” nature of Chinese loans helps leaders in two ways. First, if Chinese debt is not reported, investors are more likely to underestimate a state’s credit risk, allowing leaders to access other streams of credit when they otherwise could not. Second, if Chinese loans are not reported in official budgets, leaders will have more discretion on how to use those funds for political purposes. Chinese loans are even subject to non-disclosure agreements, which can facilitate corruption (Dreher et al. 2021; Gelpern et al. 2023; Horn, Reinhart and Trebesch, 2020). For example, $1.163 billion in loans from China to Congo went “missing, with no evidence that the money had been disbursed for infrastructure projects.” 4

Second, Chinese loans lack governance conditions, which allows leaders to potentially engage in kickback schemes and political manipulation. For instance, leaked Chinese contracts reveal the diversion of funds and creation of fictitious services (Gelpern et al. 2023). The New York Times highlighted that officials in Kenya’s Standard Gauge Railway, financed by a $4.7 billion Chinese loan, were implicated in fraudulently channeling over $2 million for non-existent land claims along the railway route. 5 Numerous scandals tied to China-financed projects across various countries underscore the potential misuse of Chinese loans (Corkin 2016; Wang 2022).

We also note that the distinct features of Chinese loans, namely their lack of transparency and governance conditions, set them apart from other non-tax revenue sources. For instance, bond issuances or international bank loans typically involve international contracts that mandate the public disclosure of a country’s private debt obligations. In addition, official debt from international financial organizations like the World Bank is not only more transparent than Chinese loans, but comes with additional fiscal obligations, ranging from reporting requirements to fiscal management changes. Therefore, while alternative non-tax revenue sources, like private credit, may help leaders retain power, they do not disproportionately benefit corrupt leaders over non-corrupt ones.

Hence, we expect corrupt leaders to benefit the most from these unique features of Chinese loans, allowing them to use Chinese loans for their own political benefit with limited repercussions. Non-corrupt leaders, on the other hand, will be less likely to misuse Chinese loans. While this lending might still benefit non-corrupt leaders because of the expansion of available fiscal resources and the potential popularity of China financed projects, we expect corrupt leaders to benefit the most from Chinese loans. From this discussion, we expect the following conditional relationship:

Chinese loans increase leader tenure more for corrupt leaders than non-corrupt leaders.

In summary, we argue that Chinese lending—similar to other sources of finance—will help leaders hold on to power. In addition, considering the opaque nature of these loans, we anticipate that the impact on political survival will be most pronounced among highly corrupt leaders.

Empirical Analysis

To test our propositions, we construct a dataset of 539 leaders from 115 developing countries from 2000 to 2015, with leader-year as the unit of observation. 6 We focus on developing countries for several reasons. First, developed countries have more domestic fiscal resources to support investments and resolve debt crises. Thus, they do not necessarily need China to cover these financial needs. In addition, China’s investment projects are rarely observed in developed countries. In a high-profile exception, Italy signed a memorandum of understanding with China’s BRI in 2019, but this never materialized into any loans or investment (Ghiretti 2021).

Second, developed countries have better credit access in international capital markets. Higher incomes, established credit histories, and representative institutions attract bond investors, allowing developed countries to increase debt without relying on international financial institutions or other countries. Again, this lessens the probability that a developed country needs Chinese loans.

Finally, even when global liquidity constraints limit sovereign borrowing, developed countries have alternative means to address debt crises. Most notably, liquidity swap lines from the U.S. Federal Reserve during the 2007–2009 financial crisis and the early months of COVID-19 helped maintain global economic stability (McDowell 2019). These funds almost exclusively targeted developed countries, with Singapore and Brazil being the only two recipients that are not OECD members (Tooze 2017). As a result of this, we limit our sample to non-OECD countries. 7

Data and Variables

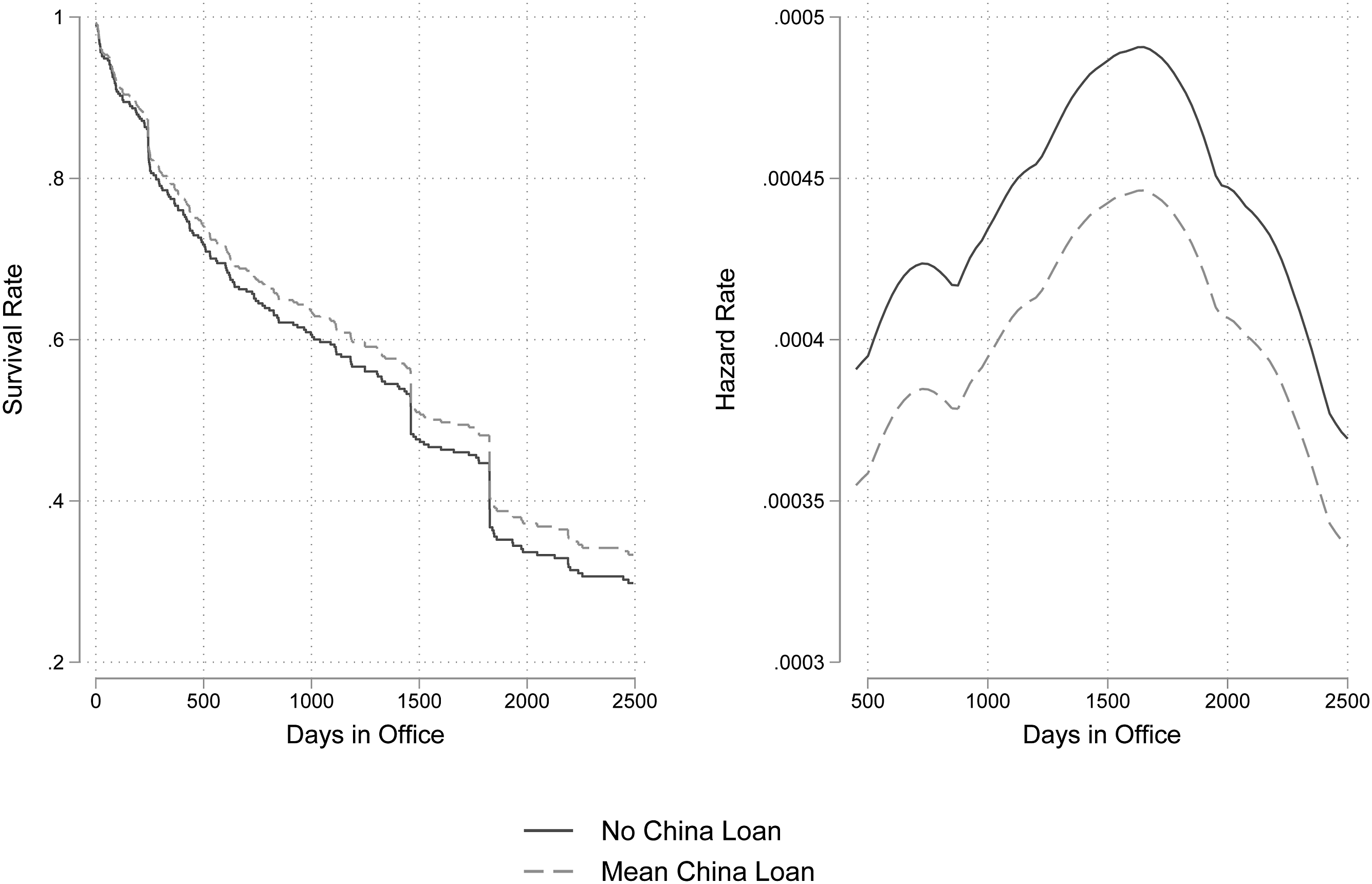

Our main outcome variable is binary, capturing whether a leader has exited office in a given year. We focus on politically driven exits from office, excluding exits due to illness, death, and voluntary retirement. As is common practice in survival analysis, the sample includes spells of leaders as long as they are in office and—if they leave—until the year in which they leave office. We draw this information from the Archigos dataset (Goemans, Gleditsch and Chiozza, 2009). 8 The sample includes 375 leader exits, 137 of which involve China lending.

Our main independent variable is Chinese loans. We measure the stock of debt owed to Chinese creditors as a percentage of the borrower’s output (Horn, Reinhart and Trebesch, 2020). While estimates of Chinese loans differ due to their opaqueness, we believe Horn, Reinhart and Trebesch (2020) offers the most comprehensive account given that they build off of several existing data sources, such as AidData (Malik et al. 2021; Tierney et al. 2011). In addition, the authors use a ‘consensus’ method to reconcile accounts of the same transactions by different data sources. To account for skewness and expected marginal declining effects, we take the natural logarithm of this variable. To demonstrate the robustness of our results, we also use project data from AidData in our analysis (Custer et al. 2023; Dreher et al. 2022). We focus on the number of new China-led investment, loan, or aid projects in a given year. 9

To address potential confounders, we include control variables that may explain why countries receive Chinese loans and may explain leader survival as well. To identify these confounders, we rely on previous political economy research focused on leader survival to build a parsimonious model (DiGiuseppe and Shea 2015; Dreher and Gassebner 2012).

We begin with economic indicators that may predict whether states need external credit and the economic competence of leaders. For example, higher growth rates lessen the need for states to seek external financing, while leaders are generally rewarded for higher growth (Treisman 2015). We also control for the log of GDP per capita, as Chinese lending tends to be more concentrated among low-income countries (Gelpern et al. 2023; Reinsberg et al. 2019). In addition, constituents should reward leaders when wealth levels increase (Casper 2017; DiGiuseppe and Shea 2015; Williams 2012). Growth and wealth data are from the World Development Indicators (WDI 2020).

Next, we control for a country’s debt burden. States with higher debt may be viewed as credit risks by private investors, prompting these states to turn to China for financing. In addition, debt crises are a risk to leader survival (DiGiuseppe and Shea 2015). Debt data are drawn from the IMF Global Debt database (Mbaye, Badia and Chae, 2018). Like the China lending data, these data are in percent of a borrower’s GDP. We also take the natural log to account for skewness and expected marginal effects.

We also control for natural resource rents. Leaders that receive fiscal resources from natural resources are better able to reward constituents (Morrison 2009). In addition, these states are more attractive to private investors, decreasing the need to turn to China. Since China’s lending is predicated on natural resource extraction, it may provide more attractive lending terms to these states (Gelpern et al. 2023). Natural resource rent data is from the World Bank (WDI 2020).

Finally, we consider the political characteristics of the state. We include a measure of regime type, given the different survival dynamics in democracies compared to autocracies (DiGiuseppe and Shea 2015, 2016; Williams 2012). We rely on the V-Dem polyarchy index, which measures the extent to which a country qualifies as electoral democracy (Coppedge et al. 2016). Next, we include a measure of civil conflict, as this may dissuade all types of external financing while threatening the survival of leaders. We use PRIO’s Armed Conflict Dataset (Gleditsch et al. 2002). An observation is coded as one if a state experiences an intrastate conflict in a given year, otherwise as zero. The Armed Conflict Dataset defines intrastate conflict as violence (with at least 25 battle deaths) between a government and an organized rebel group.

Part of the analysis focuses on potential scope conditions that moderate the effects of China lending. These moderators will help identify the mechanisms that connect China lending to leader survival. We begin by testing whether Chinese loans have heterogeneous effects across corrupt administrations. More corrupt leaders are better able to use state resources for personal gain, allowing these leaders to stay in power. Leader corruption data are taken from V-Dem (Coppedge et al. 2016). These data have several advantages over other measures of corruption. To begin, V-Dem’s executive corruption measure is tied specifically to a leader rather than focusing on a regime as a whole. We expect that there is heterogeneity in corruption levels across leaders within a country. In addition, corruption is a difficult activity to observe. V-Dem’s Bayesian latent modeling approach leverages country expertise, producing a latent measure. While expert-based measures are not immune to error, previous research on expert-coded variables finds that even with a substantial error, expert-coded indices are robust and that error tends to attenuate estimates rather than exaggerate estimates (Marquardt 2020).

Next, we examine whether potential economic benefits from Chinese loans help leaders stay in power. If Chinese loans promote growth, then leaders with Chinese loans and higher growth may stay in power longer. Similarly, leaders may be rewarded for using Chinese loans for growth-potential activities. For example, large infrastructure projects may build the foundation for higher growth in future activities. To proxy for this, we condition Chinese loans on public goods provision, as measured by V-Dem (Coppedge et al. 2016). Leaders that use Chinese loans to provide more public goods may be rewarded by their constituents more than leaders that use Chinese loans for particularistic or political purposes.

Instead of using Chinese loans for corrupt purposes or public goods provision, leaders may use these financial resources to bolster the coercive apparatus of the state. Therefore, leaders with more Chinese loans and higher coercive capacity will be able to stay in power longer. To test that possibility, we condition Chinese loans on two coercive indicators: military spending (data drawn from the World Bank) and repression levels (data taken from Fariss et al.’s (2020) latent measure of repression).

Finally, we consider the heterogenous effects of China lending. It may be that corruption, public goods provision, and repression are all proxying for regime dynamics. Democracies and non-democracies implement different rules for leader removal, with democratic leaders usually having shorter tenures because the costs of leader removal are lower in democracies. In addition, leaders in different regimes may have different incentives or different discretion on using external financial resources (DiGiuseppe and Shea 2015; Licht 2010; Yuichi Kono and Montinola 2009). Because of these dynamics, previous political economy research has focused on the heterogeneous effects of loans and aid on leader survival. To examine these same possibilities in the context of Chinese loans, we test for moderation effects across V-Dem’s polyarchy measure and Boix et al.’s (2013) binary measure of democracy.

Empirical Strategy

Our key dependent variable is the duration of days before a leader exits office, t. Therefore, we opt for a survival analysis design. Specifically, we rely on Cox proportional hazard models, which allow us to estimate the determinants of the hazard rate of leader failure, h(t). In our context, ‘failure’ is defined as a leader’s exit from office for political reasons. Leaders are included in the sample as long as they are at risk of being removed from office but leave the sample in the event of losing office. Unlike other survival models, the Cox model makes no assumptions about the functional form of the baseline hazard rate of leadership failure (h0t) while assuming proportional hazards (Box-Steffensmeier and Jones, 2004). We illustrate this model here for Hypothesis 1:

where h(t) is the hazard of a leader leaving office as a function of some baseline hazard rate (h0t), Chinese loans, and a set of control variables (X) designed to block confounding pathways. We also estimate conditional effects of Chinese loans, where leadership survival may be more affected by Chinese loans when leaders are corrupt:

The advantage of the Cox survival model over other survival estimators is that we need no additional parametric assumptions about the baseline rate. Leaders may have an increased risk of losing power, a decreased risk of losing power, or some non-monotonic combination of both. Like other parametric estimators, however, the Cox estimators are sensitive to confounders. If some observable or unobservable factors existed that affect both China lending and leader survival, then the estimator would be biased. Leaders are strategic and survival-motivated. Thus, any agreed-upon Chinese loan will be scrutinized through the political lens of whether it helps a leader or not. To address this endogeneity problem, we also employ an instrumental variable (IV) model. There are two issues with this strategy. First, Cox survival models are not conducive to instruments. Second, we need valid instruments.

On the first issue, we can treat our data as discrete duration panel data, where the dependent variable is the binary outcome of whether a leader leaves office or not in a given year instead of the duration of time until a leader leaves office. This data structure can be analyzed by standard regression techniques or IV estimations. To account for temporal dependencies in the data, we include time trends, using the linear, squared, and cubic trends of time since a leader left office in a given country.

10

For our purposes, we estimate a probit model:

To ensure that our data can be transformed into discrete duration panel data, we estimate a probit model and compare the probit to the Cox estimations. 11 We find similar results (see model 3, Table 1 for a comparison). With this estimator, we can utilize standard IV approaches.

Next, we need valid instruments for the IV models. Two assumptions of a valid instrument are that (1) it has a strong association with the endogenous regressor and (2) the instrument is uncorrelated with the outcome model error term. The first assumption can be tested directly, while the second cannot.

To instrument for Chinese lending, we use a shift-share or Bartik estimation strategy (Goldsmith-Pinkham, Sorkin and Swift, 2020; Lang 2021; Dreher et al. 2022). This design has two parts. First, we identify a “shift” variable that explains the supply of Chinese loans but is plausibly exogenous to leader survival: currency reserves in China. Chinese currency reserves proxy China’s general financial liquidity, where we expect that higher reserves should increase the likelihood that China issues a loan to a given country. 12 Leaders in borrowing countries should have no impact on Chinese reserves. However, Chinese reserves may be associated with other global factors that change over time and that may subsequently affect a potential borrower’s economic conditions. If that were the case, reserves would not meet the exclusion restriction assumption. One solution to confounding temporal variables would be to use time-fixed effects. Since reserves do not vary across units in a given year, however, this is not an option for our design.

Thus, the second part of the estimation strategy is to interact the “shift” variable with the “share” component, which is the leader’s propensity to receive a loan. To capture a leader’s propensity to receive a loan, we use the percentage of previous leader-years that involved a Chinese loan in a given country. The interaction between reserves and a leader’s likelihood of receiving a Chinese loan provides two design advantages. First, the interaction models the heterogeneous effects of China’s reserves on lending. For example, some countries that are either geopolitically or economically important to China are probably less affected by changes in reserves than a country that may provide marginal benefits to China. We expect that more China reserves will prompt China to increase its lending portfolio, conditional on the baseline level, to borrow from China in the first place.

Second, the interaction creates variation within countries over time, allowing us to include both country and year-fixed effects into the models, resulting in the following first stage model:

where α i represents country-specific intercepts and ν t represents year effects. The resulting estimator for the interaction term (γ3) is akin to a difference-in-difference design with a continuous estimator. We assume that China’s reserves only affect a leader’s political survival through Chinese loans, conditional on a country’s likelihood of receiving a loan and other model components.

It is possible that China’s reserves are associated with China’s other external economic policies that could subsequently affect a country’s economic conditions. Given the model, this possibility is not likely for several reasons. Year fixed effects address any global specific changes to economic conditions that may be associated with reserves and leadership change. In addition, the first stage of the instrumental variable model will control for economic and political conditions that are typically associated with leadership survival and global economic effects. Thus, in order for China’s reserves to affect leaders' political survival through an alternative pathway, that pathway would require that heterogeneous effects across countries exist in a way that is also correlated with the likelihood of a country receiving a Chinese loan. This alternative is not obvious to us. Thus, we assume that the interaction plausibly meets the exclusion restriction. While this assumption cannot be tested, we implement a series of falsification tests in the appendix to provide an empirical and theoretical defense of our assumptions.

Finally, we cluster standard errors at the country level given expectations that errors may be correlated within countries given norms and political expectations of leadership turnover. 13

Results

Chinese Loans and Leader Survival

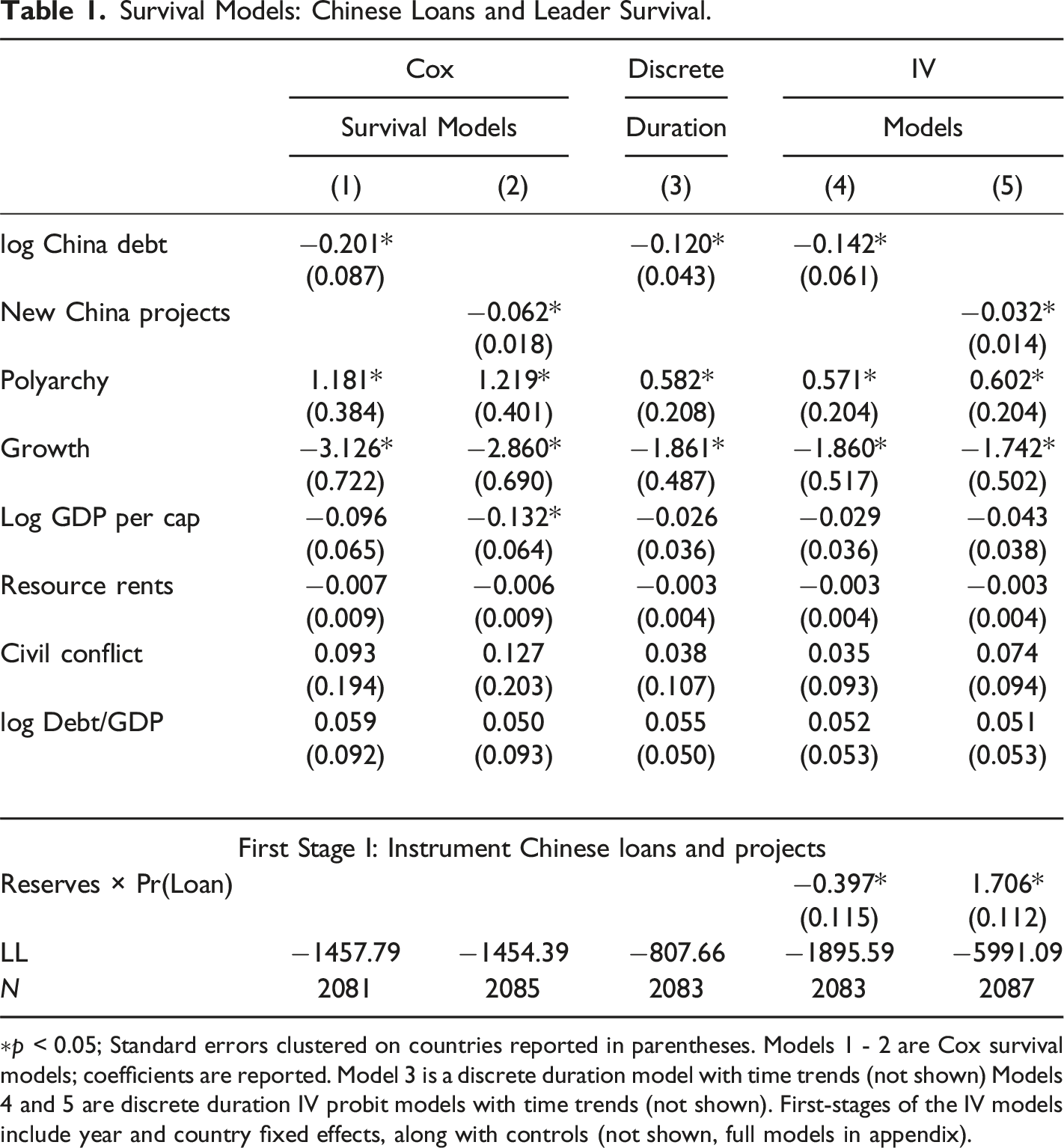

Survival Models: Chinese Loans and Leader Survival.

∗p < 0.05; Standard errors clustered on countries reported in parentheses. Models 1 - 2 are Cox survival models; coefficients are reported. Model 3 is a discrete duration model with time trends (not shown) Models 4 and 5 are discrete duration IV probit models with time trends (not shown). First-stages of the IV models include year and country fixed effects, along with controls (not shown, full models in appendix).

The coefficients of control variables are in line with expectations. In particular, democratic leaders have significantly shorter tenures compared to autocratic leaders. Given that the controls are designed to block confounding pathways between China borrowing and leader tenure, we hesitate to interpret their effects further (Keele, Stevenson and Elwert, 2020). Diagnostic tests, however, suggest that democracy is violating the proportional hazard assumption. We address this potential problem through time-varying estimation and shared frailty estimations. These variations did not change the main coefficient. We discuss these tests in more detail in the appendix.

As discussed above, Chinese loans may be caused by the same factors that can keep a leader in office. For example, natural resource rents can both attract China investment while helping leaders satisfy key supporters. We control for observable confounders in models 1 and 2, but other factors may exist that confound the relationship of interest. To address unobservable confounders, we use the interaction between China’s currency reserves and the likelihood that a leader receives a loan to instrument Chinese loans. We estimate the instrumental variable model using a conditional-mixed process framework, with a OLS regression in the first stage(s) and a probit model for the outcome stage. Leaders' survival as a function of Chinese loans.

For comparability, we replicate the Cox model results in model 1 using a discrete duration probability model in model 3. This duration model estimates the probability that a leader exits office in a given year and includes a time trend since the last leader exit (and its squared and cubic forms). We observe substantively similar results in model 3 as in model 1, which is consistent with econometric theory (Beck, Katz and Tucker, 1998; Box-Steffensmeier and Jones 2004).

With the discrete model as our foundation, we employ our instrumental variable estimation strategy. To reiterate, we interact China’s currency reserves with the probability that a country receives China finance in the first stage of the instrumental variable model. We include country and year fixed effects in the first stage to account for unit and temporal heterogeneity. Because currency reserves do not vary across the countries in the sample and the probability of receiving a loan does not vary over time for each country, the additive components of the interaction drop out by design due to collinearity. We are left only the interaction term, which we assume is plausibly exogenous to the model.

While we cannot test the exclusion restriction empirically, we use falsification tests to rule out some potential threats to our assumption. For example, we examine whether the control variables in our main models are associated with the interaction instrument. In addition, we identify conditions under which the association between the instrument and the endogenous regressor should not exist: countries that recognize Taiwan and countries that have close security ties to the United States (Dreher et al. 2022). A lack of empirical association in these tests does not prove our assumptions, but any empirical association would call those assumptions into doubt (see Tables A4 and A5 in the appendix for more details). We find no evidence of these empirical associations.

With our plausible instrument, we find that Chinese loans (instrumented by Reserves*Pr(Loan)) decrease the likelihood that a leader exits office in a given year in model 4. Model 5 replicates model 4, but instruments for the number of new China financed projects instead of loans. Using a similar instrumental variable strategy, we interact reserves by the probability of a new project in a given year. We find substantially similar results in model 5 as we did in model 4 and in the Cox survival models.

In summary, we have found that Chinese loans boost leader survival. This finding helps motivate why leaders are eager to receive China finance and suggests that leaders make use of Chinese loans for political purposes. We now further examine how leaders turn China finance to their political advantage.

Chinese Loans and the Survival of Corrupt Leaders

The above analysis demonstrates that Chinese loans provide leaders with political benefits, resulting in longer tenures. A remaining question is how: How do these loans benefit leaders? We argue that Chinese loans provide leaders with more funds to implement public projects or reward important constituents. We expect that the latter is of particular importance to leaders' survival, given that leaders cannot prevent non-supporters from enjoying the benefits of public goods. Being able to funnel funds directly to key supporters (and excluding non-supporters) should have more impact on survival and create loyalty among supporters.

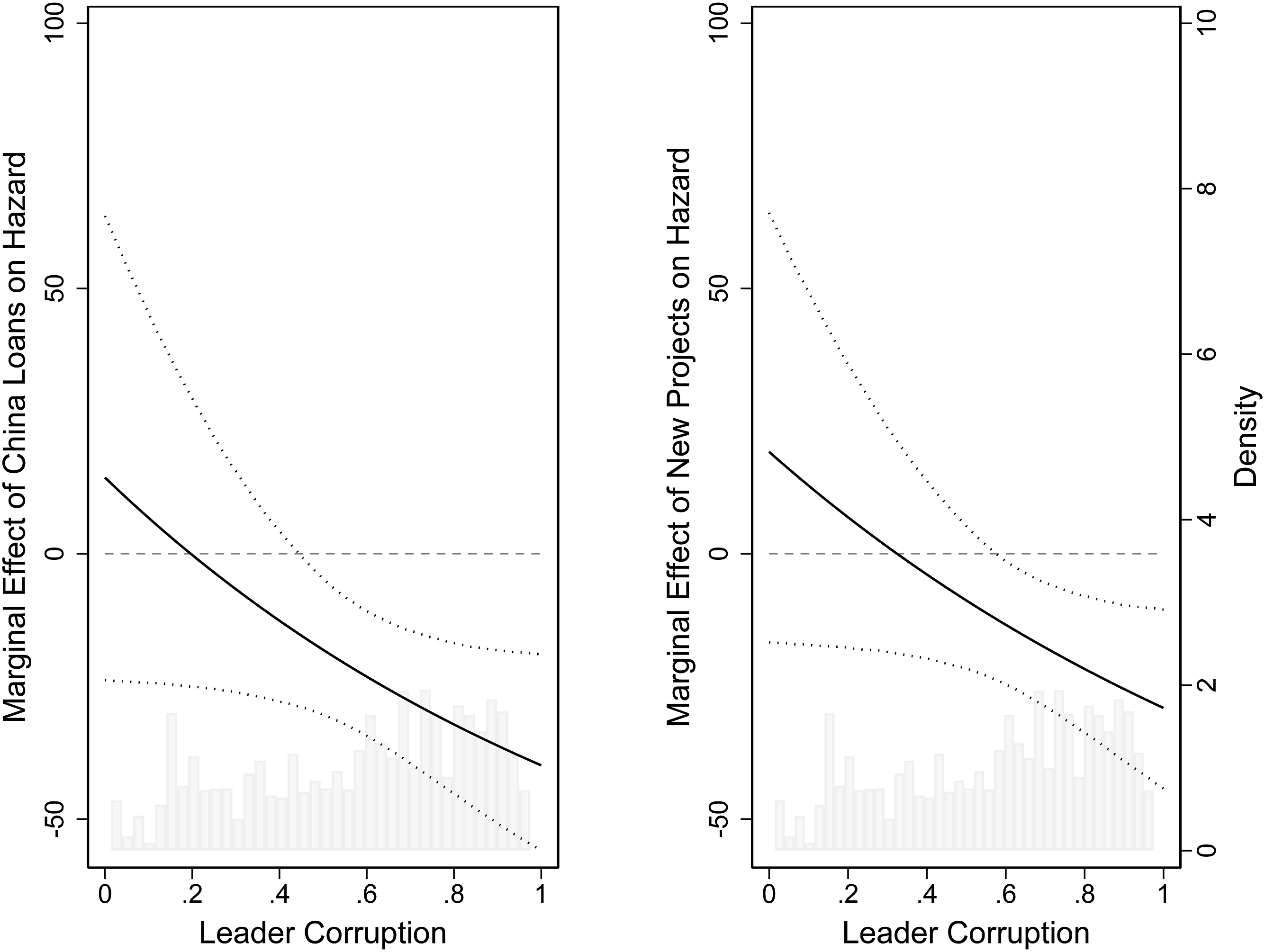

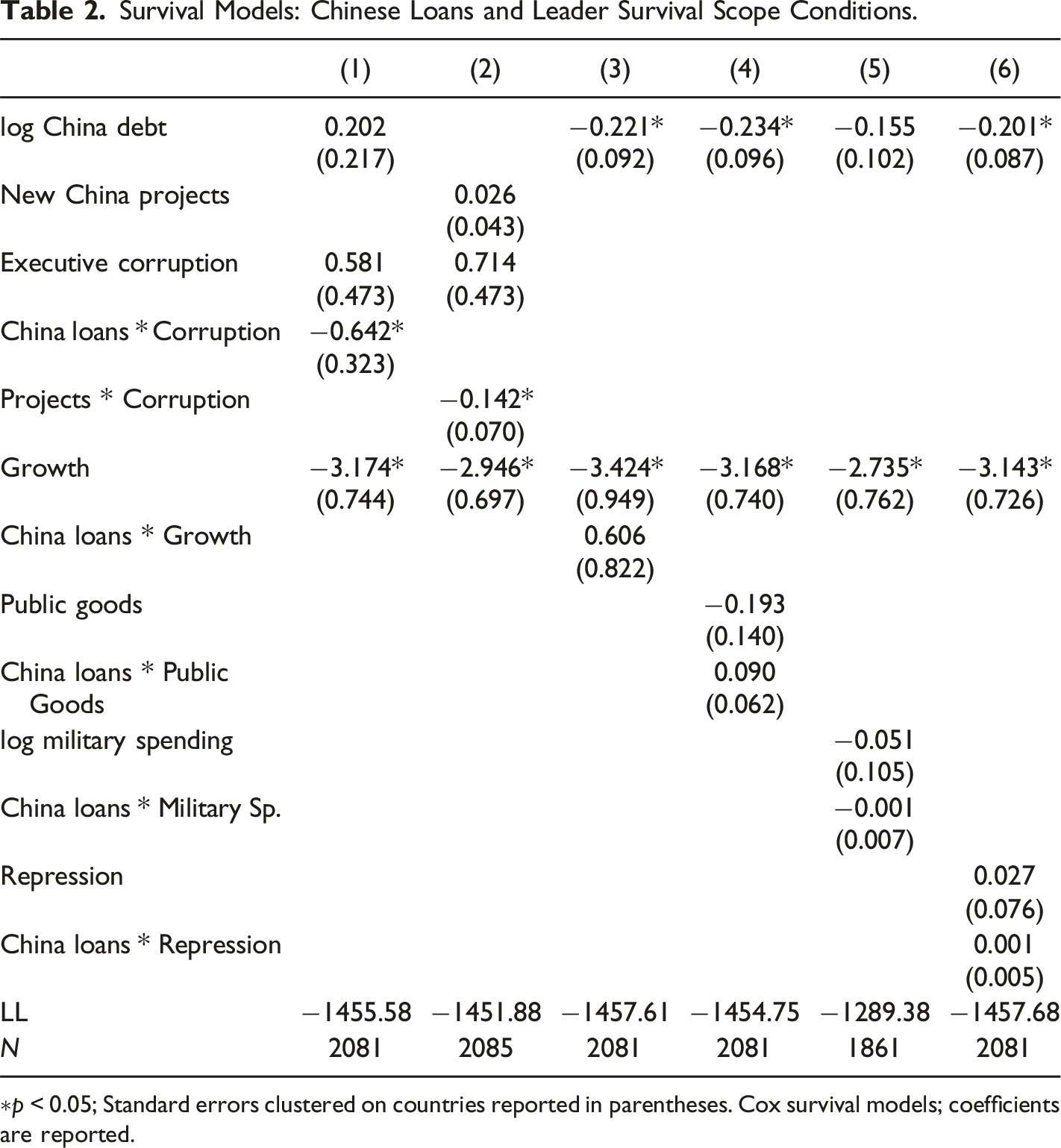

Chinese loans are particularly useful for these political transactions because these loans do not necessarily show up in the official budgeting processes (Brown 2023; Dreher et al. 2022). Therefore, leaders can use traditional fiscal processes to reward supporters publicly and use Chinese loans to reward supporters privately. We expect that the most corrupt leaders will make the most use of China’s lending. To illustrate this point, we interact Chinese loans with leaders' corruption levels in model 1 in Table 2. We observe that Chinese loans reduce leaders' hazard of leaving office more for corrupt leaders. To ease interpretation, we plot the interaction in the left panel of Figure 2. We also replicate this finding when we interact with new China projects with corruption levels in model 2 (see right panel of Figure 2). Marginal effects of Chinese loans on leader survival conditional on corruption. Note: Percent change in the hazard of leader failure resulting from a one standard deviation logged unit change in China lending (left panel) and one standard deviation change in new China projects (right panel) conditional on corruption, holding controls at mean value. The dotted lines represent the 95 percent confidence intervals around the simulated estimates (solid line), resulting from 10 000 draws of betas and the variance-covariance matrix. Density plot of corruption in background. Survival Models: Chinese Loans and Leader Survival Scope Conditions. ∗p < 0.05; Standard errors clustered on countries reported in parentheses. Cox survival models; coefficients are reported.

Models 1 and 2 in Table 2 show that Chinese finance is most politically beneficial to corrupt regimes. Given that the terms and conditions of Chinese loans are often obfuscated, corrupt leaders can use this obfuscation to direct the finance towards themselves and important elites. While the results demonstrate the importance of corruption in explaining the political importance of Chinese loans, they do not rule out other possibilities. For example, it may be that Chinese loans provide economic benefits to the country as a whole and constituents rewards their leaders for these economic benefits. To test for this possibility, we interact Chinese loans with growth and find no statistically relationship in model 3. The political benefits of Chinese loans are the same for leaders in countries experiencing high economic growth and low economic growth. In a variant of this test, we interact Chinese loans with public good provision, with the possibility that constituents reward leaders that are providing more public goods in conjunction with China projects. However, we find no evidence of this dynamic in model 4.

Next we consider the possibility that leaders are using Chinese loans for nefarious, coercive purposes. Instead of funneling financial resources to key supporters, leaders may be using Chinese loans to build the coercive power of the state. With this added coercive power, leaders can repress opposition and hold onto power by force. To test this possibility, we interact Chinese loans with military spending to examine whether leaders with Chinese loans and higher military power are able to stay in office longer. Model 5 shows no support for that expectation. Similarly, when we interact Chinese loans with a latent measure of repression, we find no conditional effects in model 6. Leaders benefit from Chinese loans whether they repress or not.

The analysis in this section shows that Chinese loans benefit leaders along one particularly pathway: corruption. More corrupt leaders use Chinese loans towards their political advantage better than less-corrupt leaders. We do not find similar conditional effects across growth, public goods provision, or repression. In addition, we show below that the corruption interaction does not hold for other types of external finance. These null results highlights the uniqueness of Chinese finance within the realm of international political economy.

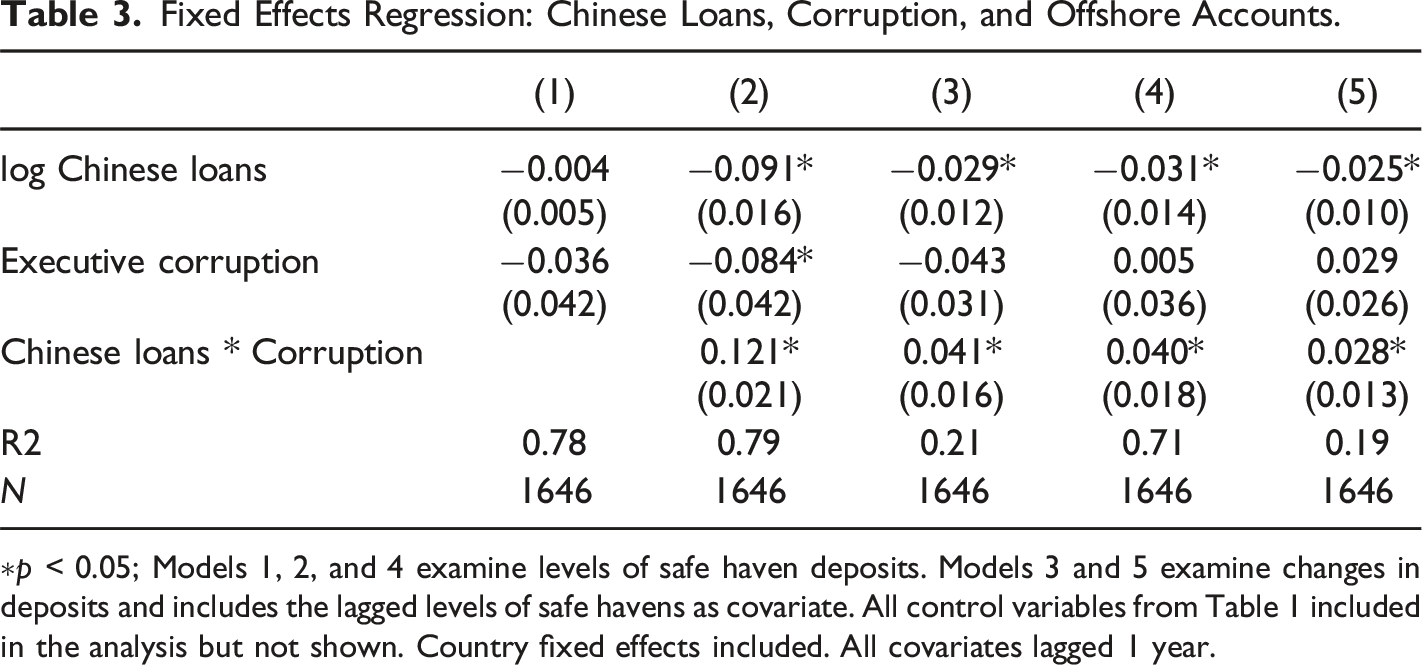

An additional observable implication of our argument is an increase in bank deposits into offshore financial safe-havens. Corrupt leaders and their supporters have incentives to build financial “parachutes” to provide financial resources in case of ouster and exile, without fear that this money can be seized or frozen by domestic or international actors. Safe havens provide leaders a way to store money until an emergency. Drawing on data on bank deposits from the Bank of International Settlements (BIS 2020), we measure the deposits in safe-haven countries as a share of total deposits abroad. 16 We expect that more corrupt leaders will funnel Chinese loans towards safe havens rather than non-safe-haven accounts. In other words, the effect of corruption on safe havens deposits should increase as countries have more access to Chinese loans.

Fixed Effects Regression: Chinese Loans, Corruption, and Offshore Accounts.

∗p < 0.05; Models 1, 2, and 4 examine levels of safe haven deposits. Models 3 and 5 examine changes in deposits and includes the lagged levels of safe havens as covariate. All control variables from Table 1 included in the analysis but not shown. Country fixed effects included. All covariates lagged 1 year.

We test the robustness of these results with different model specifications. Model 3 in Table 3 looks at the changes in bank deposits and includes the lagged value of safe-haven deposits. We observe a similar dynamic to model 2: more China lending increases the change in safe haven deposits for more corrupt regimes. Models 4 and 5 use (Andersen et al., 2022) categorization of safe havens as the dependent variable, and we observe similar results. 18 These results are only suggestive, of course, given that we cannot prove that Chinese loans are the ones being siphoned off for private gain. This system of finance is designed to hide the money trail, so we cannot definitely tie leaders to these accounts. The results, however, are consistent with our expectations that Chinese loans are more likely to be misappropriated by more corrupt leaders.

Benchmarking the Effect of Chinese Loans

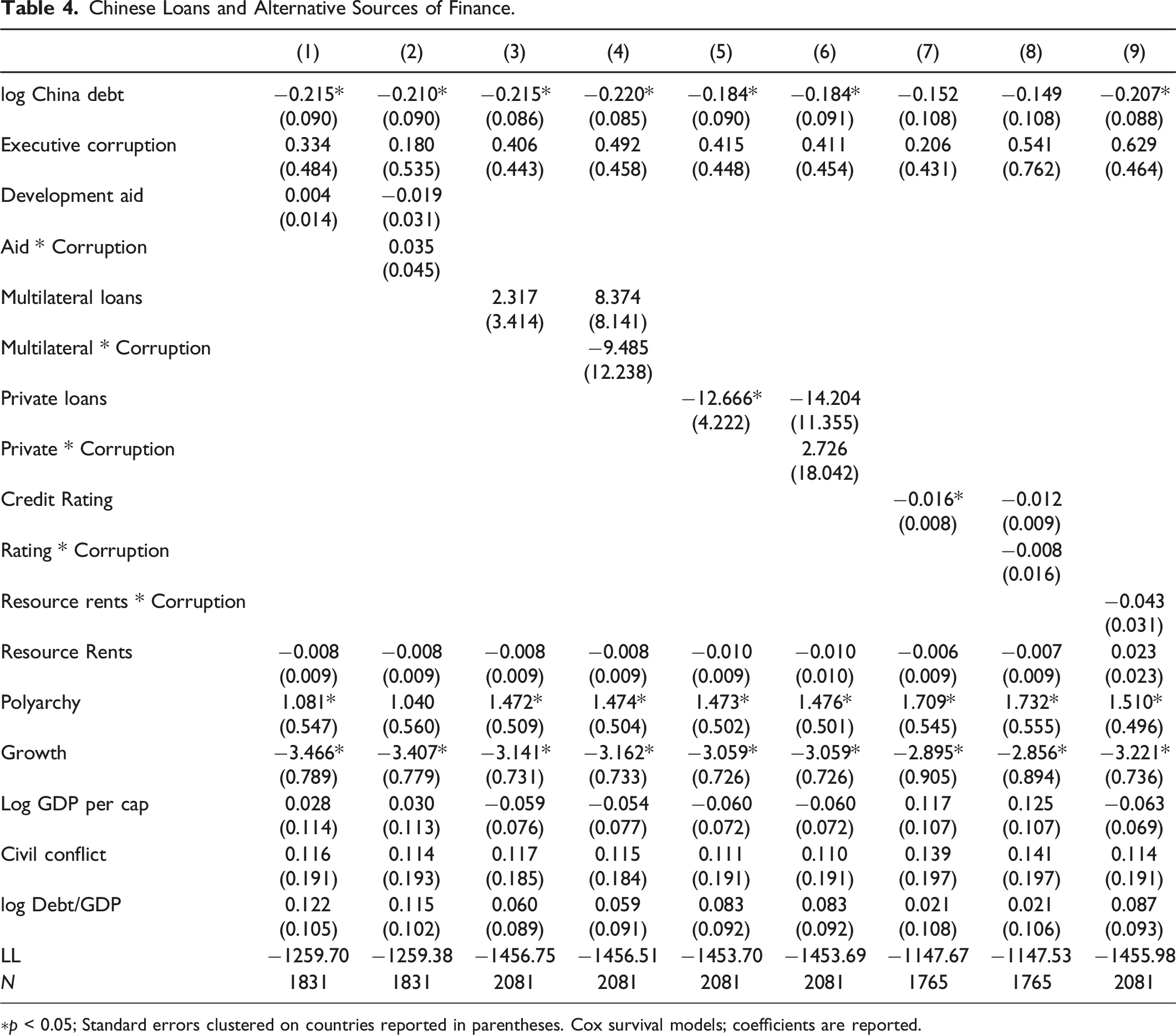

In this section, we conduct additional analysis comparing Chinese loans to alternative sources of finance. Including alternative sources of finance in our models serves two purposes. The first is to exclude the possibility that our results are driven by other sources of finance rather than Chinese finance. The second is to demonstrate the unique political economy of Chinese lending, which benefits more corrupt leaders. We find that alternative sources of finance do not have the same conditional effects as Chinese loans.

Chinese Loans and Alternative Sources of Finance.

∗p < 0.05; Standard errors clustered on countries reported in parentheses. Cox survival models; coefficients are reported.

Additional Analysis

We carry out additional analysis to ensure that our results are robust to various model specifications and measurement choices. The results from these tests do not diverge from our main inferences, so we delegate them to the appendix and briefly discuss them here. First, we perform a number of extensive tests to ensure that corruption, and not regime type, is the key moderating variable. Across different estimation methods and measures of democracy, we find that democracy does not condition the relationship between Chinese loans and leader tenure (section A11, appendix). We do find, however, that Chinese loans appear to increase the likelihood of electoral victory (section A10, appendix). This suggests that these projects have some electoral benefits, in line with our argument.

Our results also remain qualitatively unchanged when we include leader-level characteristics like experience and age as well as their interactions with Chinese loans in the model (section A14, appendix).

We also consider the sensitivity of the survival models and the IV model to various model assumptions. For example, we conduct additional falsification tests in the IV model. We show that the covariate means do not vary significantly across levels of the instruments and are never more imbalanced than comparative levels of the endogenous regressors (section A3, appendix). For the survival models, we implement a variety of diagnostic tests to test the validity of the proportional hazard assumption.

We consider alternative explanations that connect Chinese loans to leader survival. Following Cormier (2023) we examine the role of transparency. We find that controlling for transparency does not change our main inferences about the main effect or the conditional effect of Chinese loans via corruption (section A5, appendix).

Considering alternative measurement and sample choices, our results are unchanged when including OECD countries in the analysis (section A6, appendix). Using project dispersal amounts rather than project numbers also yields similar results (section A7, appendix). Considering alternatives to the corruption measure, we replicate our findings using institutional markers of good governance, notably judicial independence, and rule of law, available from the VDem dataset (section A8, appendix).

Finally, we begin to exploit heterogeneity in project sectors of Chinese development finance. Building on previous work, which shows that corruption is concentrated in specific sectors such as mining, energy, infrastructure, and government procurement (Watkins 2021; Ping, Wang and Chang, 2022), we examine the relationship between Chinese finance projects and leader survival separately for these sectors. Our analysis reveals that projects in corruption-prone sectors are more likely to help leaders stay in power than non-corrupt project sectors (section A9, appendix).

Conclusion

Many emerging markets and developing economies have increasingly relied on non-traditional lenders like China to fund their public spending and investments (Braeutigam 2020; Carney 2023; Kaplan 2021; Kern and Reinsberg 2022). Our findings indicate that Chinese debt positively impacts leader survival, particularly in more corrupt regimes. Given the importance of leader tenure and leader turnover on both domestic and international politics, our findings suggest avenues for future research. For example, leader tenure affects both conflict initiation and duration (Smith and Spaniel 2019; Uzonyi and Wells 2016). Thus, our findings suggest an indirect pathway that connects Chinese loans and conflict behavior that should be further explored.

In addition, our findings do not rule out the possibility Chinese loans have alternative political consequences on states. For example, Chinese loans may inadvertently lead to bad governance practices that undermine development. Alternatively, by providing credit to countries that may not otherwise be able to borrow, China could have larger consequences for global governance (Broz, Zhang and Wang, 2020; Weiss and Wallace 2021; Weinhardt and Ten Brink 2020; McNally and Gruin 2017). And, in general, Chinese loans may affect conflict behavior, given that debt shapes how leaders approach war (DiGiuseppe 2015; Shea and Poast, 2018). Furthering our understanding of how Chinese loans disrupt the political economy of international finance represents an important avenue for future research.

From a policy perspective, our findings have several implications. Although Chinese loans have the potential to lengthen the reign of corrupt and suppressive regimes, this does not apply to all countries. By providing financial access for vital infrastructure projects in developing countries, China has filled loopholes that international investors have left open for years (Braeutigam 2011; Dreher et al. 2022). In many instances, Chinese loans have provided financing for transportation, electricity, and infrastructure to millions of people, which has helped governments lift their populations out of poverty. Thus, deciphering these differences and their political implications is important.

Supplemental Material

Supplemental Material - China Lending and the Political Economy of Leader Survival

Supplemental Material for China Lending and the Political Economy of Leader Survival by Patrick E. Shea, Bernhard Reinsberg, and Andreas Kern in Journal of Conflict Resolution

Supplemental Material

Supplemental Material - China Lending and the Political Economy of Leader Survival

Supplemental Material for China Lending and the Political Economy of Leader Survival by Patrick E. Shea, Bernhard Reinsberg, and Andreas Kern in Journal of Conflict Resolution

Footnotes

Acknowledgements

We thank the reviewers and Paul Huth at JCR for their valuable input. We are also grateful for the generous suggestions that we received from Ariel Ben-Yishay, Jonas Bunte, Timm Betz, Marc Busch, Cameron Ballard-Rosa, Bill Clark, Matthew DiGiuseppe, Jane Duckett, Sayantan Ghosal, Mirko Heinzel, Ted Lasso, Ning Leng, Saliha Metinsoy, Irfan Noorudin, Brad Parks, Jon Pevehouse, Thomas Pluemper, Amy Pond, Dennis Quinn, Nita Rudra, Carole Sargent, Holly Snape, James Vreeland, Christian Wagner, and the participants at DebtCon6 and IPES 2023 at Georgetown University. Yash Dhuldhoya, Marwa Katir, and Markandeya Karthik provided excellent research assistance.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.