Abstract

Microfinance has garnered significant attention in development discourse due to its acclaimed potential to reduce poverty. Its role as a poverty reduction tool, however, has yet to be thoroughly examined. A single case study was undertaken through interviews and observations involving 30 Savings and Internal Lending in Communities beneficiaries in Semonkong, Lesotho. The rural populations in Lesotho face poverty due to, among other reasons, a lack of access to microloans necessary for alleviating poverty. The study’s outcome sheds light on the phenomenon of community-led microfinance programme and analyses their contribution to the livelihoods of those living in rural communities. The study found that savings-led microfinancing has effectively increased household incomes among those participating in it thereby amplifying consumption and access to basic needs. Small loans have further facilitated the establishment of small businesses and the acquisition of assets necessary to curb poverty. While there are some negative consequences associated with participating in this activity, the study found that overall the positive impacts outweigh the negative ones. We, therefore, recommend the promotion of savings-led microfinancing as a poverty alleviation tool and envisage that the findings of this study will stimulate policy dialogue and promote advocacy for rural financial inclusion.

Introduction

Microfinance is a predominant poverty alleviation strategy that has spread rapidly and widely across several developing countries in Africa, Asia and Latin America in the last few decades (Ding et al., 2023). Microfinance refers to the provision of financial services to people who are not benefitting from the traditional banking systems because of their lower economic status (Chhorn, 2021). The idea to improve access to appropriate financial services for poor households has traditionally focused on providing credit via formal alternatives following a successful model implemented by Grameen Bank in Bangladesh established by Muhammed Yunus in the 1970s. However, Karlan et al. (2017) noted that due to limited participation and geographic reach of microcredit institutions, especially among the rural poor, efforts were shifted to expanding access to savings. A growing literature shows that microsavings yield strong welfare impacts than microcredit, suggesting a more transformative approach than the common credit programmes. In parallel to the development of microcredit products for the poor, many nongovernmental organisations (NGOs) had begun promoting informal savings-led microfinance groups that followed and improved on the model of informal associations indigenous to many societies called Rotating Savings and Credit Associations (ROSCAs). Although the appeal of the savings-led microfinance approach was shown by the growth of these groups, which reached over 10 million people in more than 70 countries after only a few years of significant expansion efforts, its contribution as a poverty alleviation strategy has been under-explored. Some of the reasons why this model became attractive include the fact that it does not rely on external capital but instead, all funds come from group members’ savings, the funds are managed by the group members themselves and hence improved record keeping and increased transparency. The groups are trained and monitored by a local NGO not a credit-providing institution and adopt flexible repayment schedules structured around seasonal cash flow (Frisancho and Valdivia, 2020). Due to its increased popularity, especially in Africa, several experimental studies have been carried out to find the effects of this model on financial inclusion and the overall welfare of each household.

Despite the abundance of these studies, their results are mixed, and there are conflicting views on their effectiveness (Karlan et al., 2017). Some researchers have considered theory to have moved far ahead of the evidence, while success stories remain unsubstantiated (Beaman et al., 2020). To put this into perspective, no income or expenditure effects are found for savings groups in Ghana, Malawi, Uganda (Karlan et al., 2017) and Mali (Beaman et al., 2014). However, research by Ksoll et al. (2016) reports positive effects on household expenditures, meals consumed per day and number of rooms in northern Malawi. A qualitative assessment of a 4-year implementation of Savings and Internal Lending in Communities (SILC) activity in Haiti by Parker et al. (2017) also found positive effects on loans and share-out funds being invested in businesses, paying school fees, health-related expenses and household consumption. Karlan et al. (2017) and Beaman et al. (2014) found that savings groups help households manage risk through consumption smoothing or food security. In addition, Karlan et al. (2017) found positive effects on women’s empowerment that is absent in the study of Beaman et al. (2014). Furthermore, increased human capital investments are present in India (Baland et al., 2020), but not in Mali (Beaman et al., 2014).

It has been suggested that over 60% of the population in lower-middle-income countries are in rural areas. As such, it is necessary to explore how participation in savings programmes enhances the social and economic well-being of the rural population. This study, therefore, seeks to investigate the extent to which a particular savings-led microfinance programme (SILC) reduces poverty to sustain livelihoods in most rural communities of Lesotho.

Study area

This study was conducted in the Southeastern highland region of the Capital City of Lesotho called Semonkong (see Figure 1). Lesotho is a small, largely mountainous country that is completely surrounded by South Africa. It is mostly rural, with a population estimated at 2,007,201 in April 2016. Among the population, 70% live in rural areas compared to 30% who live in urban areas (Bureau of Statistics, 2016). According to the World Bank Poverty and Equity Brief for Lesotho (2023), poverty is more prevalent in rural areas (estimated at 60.7%) due to limited income opportunities and high vulnerability to environmental and economic shocks. Although the proportion of the population living below the national poverty line in Lesotho fell from 56.6% to 49.7% (almost half of the population) between 2002 and 2017, in the rural areas, poverty remained stagnant at 60.7%, widening an already urban–rural divide.

Map of Lesotho.

Semonkong is a small town situated in the Maluti Mountain Range of the country and is about 120 km southeast of the capital city, Maseru, with its altitude ranging from 2500 to 3096 m above sea level. It is home to the second highest single-drop waterfall in Africa, Maletsunyane Water Fall, which plummets almost 200 m into a narrow gorge hemmed by steep green slopes and sandstone cliffs, making it a specular tourist destination. Semonkong is one of the rural areas in Lesotho with a high population, estimated at 7812 and is characterised by limited economic opportunities (Lesotho Household Budget Survey report, 2017/18). Like in many rural parts of the country, poverty is rife in this area and its population is trapped in a vicious circle of poverty, a phenomenon they wish to break through engagement in microfinance activities. Farming is a major livelihood activity in Semonkong, although it is restricted by unreliable climate conditions and the harsh long winter seasons that come with snow. According to Semonkong Rural Development Project report of 1996, there are, on average, only 100 frost-free days during the cropping season, which is obviously a limiting factor for successful agriculture. Even during the short growing season, between mid-September and mid-April, natural hazards like frost, hail, droughts and severe downpours are by no means uncommon. Moreover, there is hardly any flat land for farming in the area as it is very mountainous.

Given the remoteness of many rural communities in Lesotho, accessing formal financial services is and has always been difficult and expensive. FinMark’s study of 2014, through its Making Access Possible (MAP): Lesotho Country Diagnostic Report programme, estimated that only 16.6% of adults got credit from the formal financial sector, with a meagre 3.8% being served by commercial banks in 2013. These banks have largely benefitted from clients with regular income in the form of monthly salaries that are used as collateral. As a result, business aspirants depend on other financing means, which require substantial fees, guarantees and collateral access loans, limiting rural households’ ability to get credit and sustain their livelihoods (Figure 1).

Literature review

Microfinance

Debates about microfinance abound, although its value to the poor is being widely recognised. The varied landscape of perspectives has seen other studies assert that microfinance exacerbates poverty, while others uphold its potential to alleviate it. Rewilak (2017) examined the role of the financial sector in poverty reduction in some developing countries between 2004 and 2015 and found evidence that financial development may be effective in reducing poverty and that economies of developing countries with higher financial inclusion significantly reduced poverty rates and income inequalities. In the context of Vietnam, Linh et al. (2019) investigated the impact of access to credit on rural populations and found that access to credit improves overall household revenue and alleviates poverty. Evidence provided by the World Bank (2014) also demonstrates that the development of the financial sector significantly reduces poverty and inequality as it boosts shared prosperity. In general, existing literature shows that the positive impacts of microcredit include enabling the poor to become micro-entrepreneurs, improving their incomes and levels of education and eventually allowing them to escape the vicious cycle of poverty (Chomen, 2021; Gakpo et al., 2021).

Conversely, an array of studies highlights the inadequacies of microfinance as a sole tool for poverty alleviation. Banerjee et al. (2017), for example, suggested that while microcredit succeeds in improving household expenditure and creating and expanding business, it appears to have no discernible short-term effect on education, health or women’s empowerment as it is claimed to have. Others criticise the mischaracterisation of microfinance as a ‘miracle for the poor’ and warn that it should not be expected to work in all situations (Karlan et al., 2017; Roodman and Morduch, 2014). Similarly, Karnani (2007) posits that microfinance benefits the better-off but is disadvantageous to the poor as borrowers who already have assets and skills are capable of making good use of credit, whereas the poor are less capable of using credit to increase their income. It should also be noted that formal financial services have been targeted at the rich sector of societies due to the commonly held view that the rich have a greater capability to repay loans and preserve their savings while the poor communities have generally remained either underserved or left with informal financial services which provided credit at very high cost (Cull and Morduch, 2014; Owolabi, 2015). An example is the Bangladesh Grameen microcredit model introduced by Mohammed Yunus. Studies have indicated that this model was met with limited participation by the rural poor due to high interest rates and low geographic reach. Ashe (2002), for instance, showed that while microfinance effectively delivers services to cities and densely populated rural areas, it has limited success in rural areas that are more than 1 km from urban centres, owing to high costs.

In light of these debates, the 2012 report on the state of the Microcredit Summit Campaign noted that a different approach to microfinance was necessary (Maes and Reed, 2012). This move saw NGOs starting to promote a highly decentralised, savings-led approach to microfinance that emulates and improves on the model of indigenous ROSCAs. Catholic Relief Services (CRS) specifically designed the SILC. The model has expanded to 27 countries: 6 in East Africa, 8 in West Africa, 7 in Central Africa and 6 in Southern Africa. Lesotho is among the countries where the CRS’s SILC model has been promoted through CRS’s partner organisation CARITAS Lesotho. Meanwhile, a study conducted by Letete (2013) focusing on the poverty reduction prospects of microfinance in Maseru concluded that microfinance was relatively successful in promoting social relations and reducing poverty in Lesotho.

Research on the effectiveness of savings-led microfinance in the country in alleviating poverty, however, is still lacking. This present research intends to unravel the extent of SILC’s influence on poverty alleviation within Semonkong, providing valuable insights into the dynamics that shape the interplay between microfinance and poverty alleviation.

The concept of SILC

SILC is promoted by the CRS and its partners to strengthen the livelihoods of the people they serve and enable them to meet their essential needs in an effort to reduce poverty. Its basic principle is to bring self-selected people (based on proximity, knowledge of each other, trust, and friendships) together to form groups of between 15 and 30 members and save money from which they can borrow. Its agenda is to provide savings, simple loans and insurance to community members who do not have access to formal-sector financial services, either because the services are not available or because they cannot access them (CRS, 2024). This model is implemented through the engagement of field agents who are trained CRS staff responsible for creating awareness among communities about SILC methodology. This involves training groups on leadership and management, elections, record keeping, managing meetings, savings and credit policy development, and SILC constitution. The groups are governed by a management committee of seven people elected among the general assembly. These include a Chairperson, a secretary, treasurer, money counter and three key stakeholders. The groups meet at regular intervals that they choose. All transactions are carried out during the meetings in front of a group to ensure transparency and accountability. The groups agree on contributing to establishing a social fund to cater for unpredicted expenses such as funeral and educational expenses for orphans and medical expenses. CRS has worked in Lesotho since 1976, and through its partner Caritas, it started the implementation of SILC in 2010.

Theoretical framework

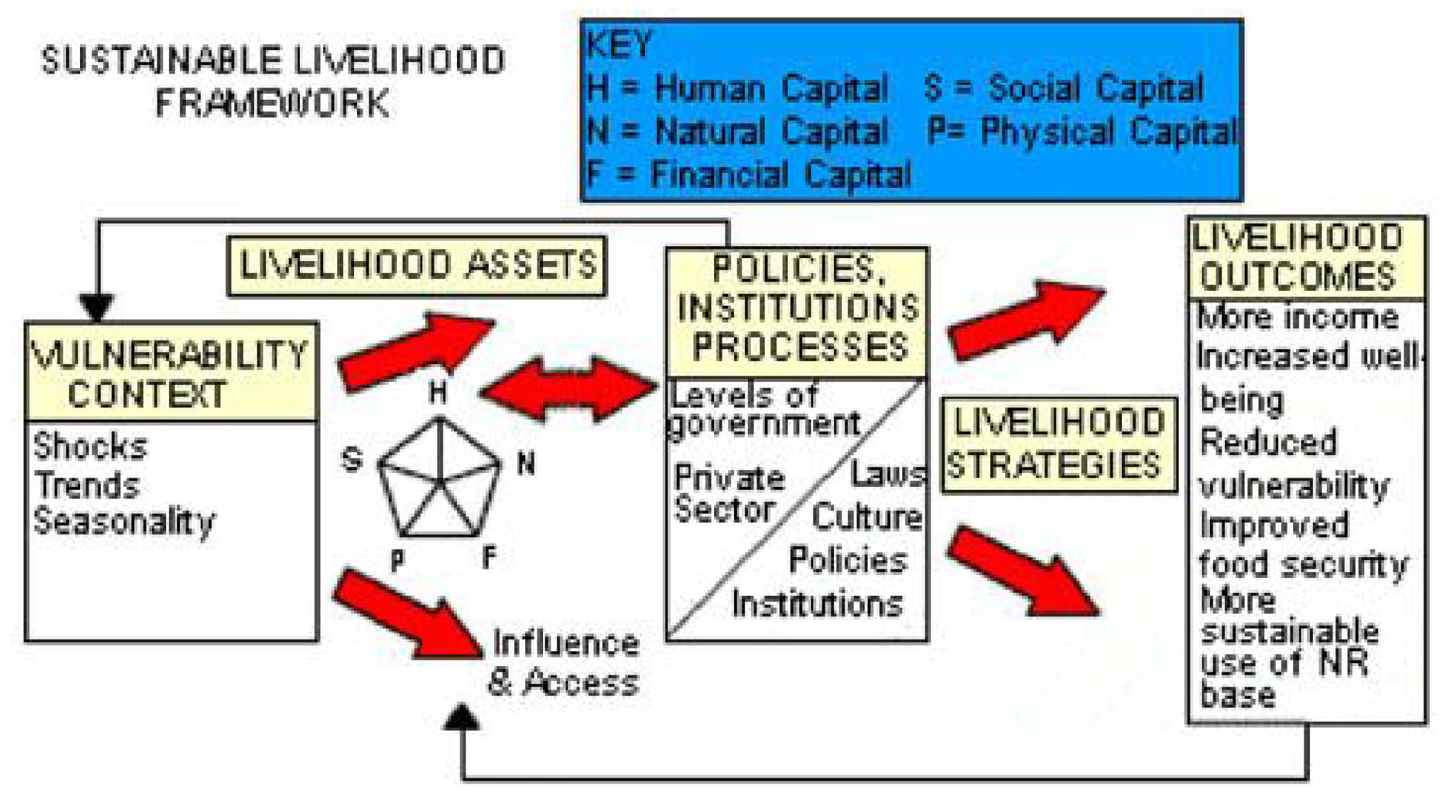

To understand how access to microloans enhances the socio-economic status of the people, our analysis was guided by the sustainable livelihood framework (SLF) developed by the British Department for International Development (DFID) in 1997 with the aim of eliminating poverty in poorer countries. This has since become the most widely used livelihood framework in development practice. The SLF supports the logical understanding that shared values and trust bind community members together and enable the formation of networks that make it possible to escape economic shocks and setbacks (Kollmair and Gamper, 2002). The SLF presents the key factors that affect people’s livelihoods (DFID, 1999) (see Figure 2). In the SLF, the livelihood assets of poor people are classified into five broad categories: human, natural, financial, physical and social capital. These assets are affected by the vulnerabilities that poor people face because if they are more vulnerable to problems, their assets are exposed and affected. To reduce the vulnerability of poor people and enhance their livelihoods, microfinance has played a vital role both as a strategy and a policy for poverty reduction.

Sustainable livelihood framework.

Critics of SLF, however, argue that because poverty is rarely uniformly distributed, selecting a geographical area may not be sufficiently precise to identify the neediest people. Communities usually do not represent such homogeneous collective social units as most development projects tend to assume. The SLF also emphasises transforming structures and processes that have the capacity to provide better opportunities for the poor (DFID, 1999). Mosse (1994) argued that there is a problem of social relations of poverty where issues of inequality and power maintain and reproduce poverty at a local level. In this case, the process of transforming structures is often complicated because informal structures of social dominance in communities influence people’s access to resources and livelihood opportunities. These inequalities are often invisible to outsiders. Examples include inequality that often exists between men and women within a community. Ashley (2000) asserted that it is one thing to ensure that gender is being addressed and another to make it possible for women to express their genuine perceptions, interests and needs about specific livelihood issues in practice.

Methodology

Sampling, data collection and analysis

Data analysed in this study stem from a postgraduate dissertation of the first author, supervised by the second and third authors. The fieldwork for the study was carried out between April and June 2022. The study employed the qualitative research approach and methods. The qualitative research approach was deemed appropriate for this study because it involves exploring a human problem by collecting data and analysing it inductively, building from emerging themes and through the researcher’s interpretation of the data (Creswell, 2009). The approach also allows the researcher to capture the stories and experiences of participants in their own words. The primary data collection method employed in this study was in-depth interviews with 30 SILC members sourced from 6 villages in Semonkong as follows: Ha-Lepae (5), Ha-Lesala (6), Ha-Khonyeli (3), Ha-Moahloli (8), Ha-Leteka (4) and Ha-Lesia (4). Participants were selected using a convenient sampling technique (see Table 1). Due to COVID-19 pandemic safety measures and legal restrictions that were still in force during this study, the researchers were compelled to conduct interviews using remote modes combined with face-to-face interviews. Among these participants, 19 were interviewed face-to-face and the remaining 11 were interviewed using different online platforms such as WhatsApp calls, WhatsApp voice notes and telephone calls. Conducting interviews through WhatsApp and the telephone allowed us to reach a wide geographical area. In-depth interviews were appropriate because the study required detailed accounts of the experiences of the rural poor with SILC as a microfinance programme. With the consent of the participants, interviews were recorded using a phone recorder while the researcher also took handwritten notes. Similarly, a call recorder was used to record word-to-word data from call interviews, while voice notes were used to maintain the accuracy of the data. Each face-to-face session lasted between 45 minutes and 1 hour, a direct call interview lasted between 30 and 45 minutes, while WhatsApp message response turn-around time was longer at 1–3 days due to network connectivity issues or other circumstances that involved lack of electricity to charge phones.

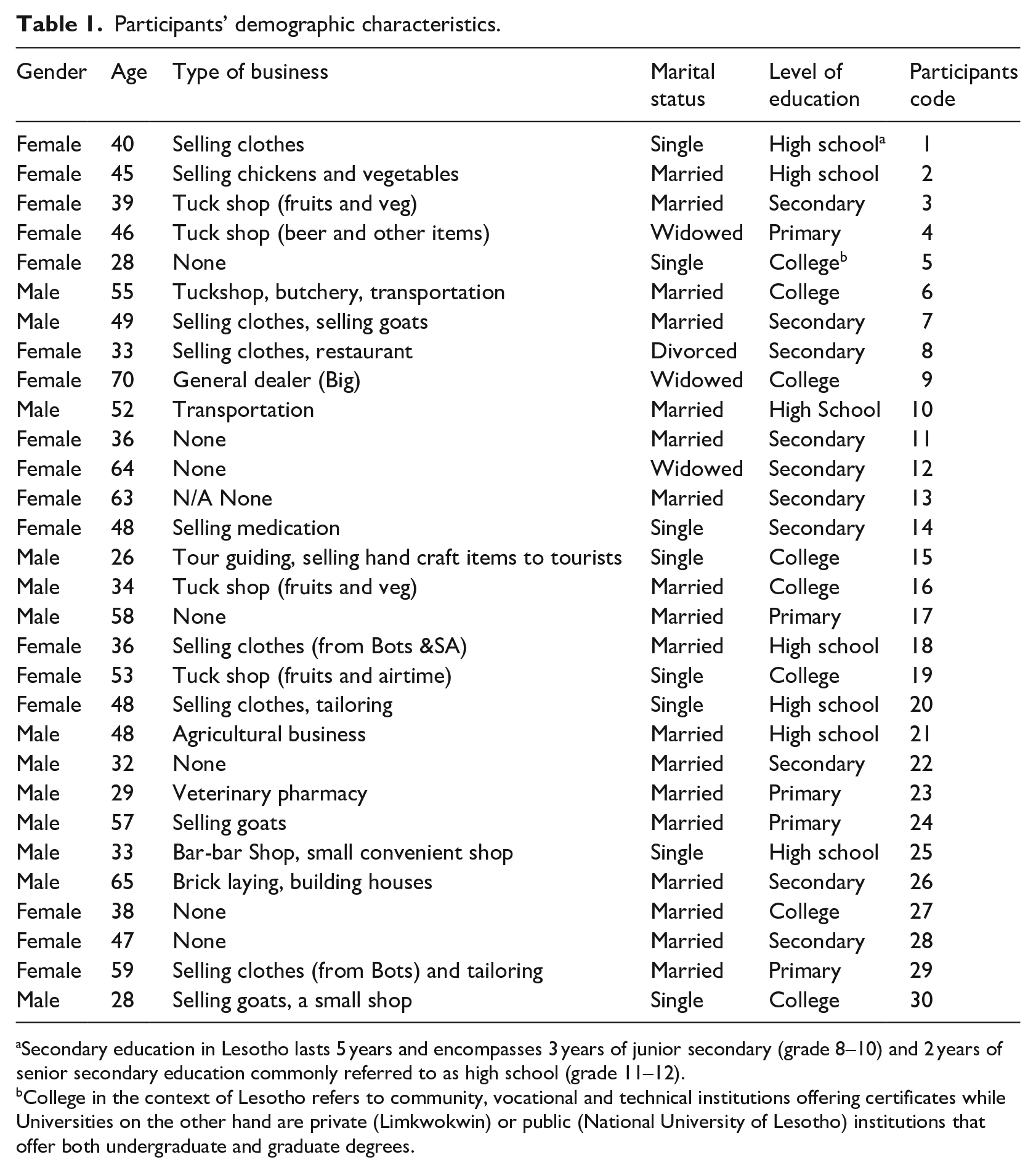

Participants’ demographic characteristics.

Secondary education in Lesotho lasts 5 years and encompasses 3 years of junior secondary (grade 8–10) and 2 years of senior secondary education commonly referred to as high school (grade 11–12).

College in the context of Lesotho refers to community, vocational and technical institutions offering certificates while Universities on the other hand are private (Limkwokwin) or public (National University of Lesotho) institutions that offer both undergraduate and graduate degrees.

The in-depth interviews were supplemented with key informant interviews, field observations and documentary research. The key informant interviews involved three SILC field agents and the Caritas Country Director in Lesotho. The lengths of the key informant interviews and the transcription process were similar to those of the in-depth interviews. Field observations were conducted during the face-to-face in-depth interviews and meetings with the research participants. A field diary and notes were used during the field observation. Documentary research was also used as a supplementary research method in which the researcher reviewed SILC project-related and relevant NGO reports.

This study received ethical clearance from the Institutional Review Board (IRB) of the University of Botswana with reference number UBR/RES/IRB/SOC/GRAD/459.

Results and discussions

Socio-demographic characteristics of respondents

Socio-demographic factors that include participants’ age, gender, educational attainment, economic status, education level and household size were considered important because they could have implications for understanding an individual’s living conditions and their development trends. The study, therefore, explored participants’ sociodemographic characteristics as shown in Table 1. Total membership for groups investigated varied between 9 members and 25 members, which were aggregated to 51 women and 34 men for all the 6 villages investigated. The number of respondents sampled were 17 females representing 56.7% and 13 males representing 43.3% of the total sample size. The study results showed that the majority of respondents (60%) were married, while 26.7% were single, 3% divorced and 10% widowed (see Table 1). From the qualitative data collected, the high percentage of married people was attributed to the belief that married adults were likely to be more responsible in the repayment of loans. Besides, it was mentioned that marriage presents an opportunity for both partners to work and therefore contribute richly to the growth of SILC. The majority of respondents (73.3%) were engaged in small businesses as their main occupation, while 10% of respondents were undertaking professional work or formal employment, 10% were farmers and 3.3% were either not working or retired. All respondents were literate, with nearly 40% having attained secondary education. The youngest respondent in this study was 20 years old and the oldest was 70.

Data analysis

The interviews were conducted in Sesotho, the main language spoken in the rural areas of Lesotho. Interviews were then transcribed and translated into English, where key themes were drawn to offer a framework for thematic analysis. Three stages of coding and classification of data were followed. The first stage was open coding which facilitated the search for categories and phrases related to how financial access benefitted the participants and the challenges. The second was the axial coding phase, where the level of conceptual abstraction was increased, and the relevance of the categories guided by the research questions was determined to form sub-themes. The third phase was selective coding, which involved identifying connections between categories based on the research objectives and guided by the SLF. For instance, Kanbur and Squire (1999) clearly state that the human capital assets, health and education, are essential building blocks to help the poor increase their income and thus reduce vulnerability, while capital assets, in combination with the structures available, determine the achievements of certain outcomes which can have impacts on the livelihood.

In this research, financial capital, human capital and physical capital were combined under one inclusive theme called economic empowerment. Furthermore, we combined risk mitigation strategies with social capital to form a social empowerment theme. Finally was the psychological strain theme which was a combination of anxiety and low self-esteem that was observed among participants who failed to repay the loans. This is an outcome of a lack of or limited access to the capital assets necessary to attain quality livelihoods.

Economic empowerment

Ability to start businesses

Economic empowerment was assessed based on the ability to start businesses and enhancement of the already exciting ones which in turn would lead to increased household income, capital investment and enhanced education opportunities further building on human capital. The results of the study indicate that joining SILC promoted entrepreneurship among the participants as more than half of the respondents (73%) were engaged in small businesses. Business ownership is essential because, as Moll (2005) explains, a productive enterprise increases the capacity of members of a microfinance scheme to first deal with risk through the withdrawal of savings and obtaining more credit in case of emergencies. It also improves the management of consumption over the years to maintain adequate nutrition and provides opportunities to invest in more assets. Indeed, this was confirmed during in-depth interviews when participants mentioned having a business generates profits which help in paying off the monthly contributions and savings which in turn allow them to borrow more loans whenever need arises. People who own profitable businesses contribute more to the social security fund making it easy for members who might need it for things such as funerals, disaster recovery incidences, health and other unexpected social need. Over 60% of business owners in this study reported purchasing more business equipment, buying vehicles and investing in the education of their children after a share-out period. Emphasising the benefits of business ownership, one female participant (Participant 3) provided the following narrative:

After joining the SILC, I was able to start a business. I can say that owning a business affords me an opportunity to save any amount that I have at the time of the meeting; meaning that if my business is not good, I save less, but when business recovers and makes more profits, I save more money and collect more funds at the end of the cycle which I use to buy additional equipment for my business and assets such as furniture for my family.

Entrepreneurship is a fundamental basis of microfinance approach to poverty alleviation. Bruton et al. (2013) ascertain that entrepreneurship offers the best opportunity to create substantial and significantly positive change within poverty settings. The idea of promoting economic activities among the rural poor was also the central theme of Grameen Bank, which focused mainly on getting loans to the poor with explicit focus on poverty reduction and social change.

Another interesting dimension was that the utilisation of loans for business had a great gender difference in that men generally used their loans for multiple business initiatives, while most women mainly engaged in one or two types of businesses at a small scale. Multiple business ventures that men were engaged in included agricultural activities, which are a common cultural signifier of wealth in rural areas, transport, butchery and tour guiding. Their focus is ownership and control of big assets. On the other hand, women generally focused on small but regular income flows like selling fat cakes. This is confirmed by research conducted by the U.S. Department of Commerce (2010), which suggested that women generally chose smaller businesses because of the lack of start-up capital, the need for flexibility and shorter working hours due to family caregiving responsibilities. Other studies have suggested that giving loans to women as the marginalised section of the society helped them develop entrepreneurial skills, start their own microenterprises and, in the end, support themselves and their families (Bansal and Singh, 2020).

Moreover, being involved in microfinance improved women’s involvement in household decision-making and facilitated women to become self-reliant, a situation which according to Sarjekar (2019) improves well-being of women and the possibility to bring about wider changes in gender inequality. Over 70% of women interviewed for this study had started a business after receiving microloans. In general, microloans improved the well-being of women, as highlighted by Participant 29 in the extract below:

Having a business has provided me with the flexibility and the freedom that I need as a woman. I remember when I was pregnant, my clients knew that I would sometimes open late and that the baby is here, I am able to come with my child to work. If I was employed, I would incur the costs of hiring a helper to stay with my child at home while I came to work, which would in turn limit my capability to save.

The above account also shows how microloans empower self-reliance. If people are empowered, they release their maximum potential and create their own version of development and hence deal effectively with their situation in terms of poverty reduction and taking control of the issues that impinge on their quality of life (Abiche, 2004).

Increased household income levels

All households in the study sample had had access to loans and had earned extra income at the end of a pre-determined time (typically 8–12 months) over the years. Overall, respondents reported that before joining a SILC group, their income levels were low and that they were subjected to borrowing from their extended family members or loan sharks in which case they paid high interest rates. A high number of participants, 26 out of 30 (86.67%), agreed that SILC had immensely contributed to their family income through access to small loans, the social fund and the final share-out at the end of the period, thereby empowering them. Through access to loans, they were able to attend to their basic needs, including food items, clothing, cosmetics, payment of school fees and health expenses, as indicated in the statement below from Participant 3:

SILC gave me an opportunity to meet my financial needs and avoid exorbitant charges from money lenders relatives. And unlike in the past, I am able to have money that sustains the family on a daily basis . . .

In line with this finding, Adu-Okoree (2012) found that microfinance had a positive impact on household income and welfare, leading to improved standards of living and enhanced opportunities to save money. Another study by Jahns (2014) in El Salvador further indicated that savings groups helped participants manage and plan their household finances better, buy better-quality food, build a cushion for emergencies and enjoy greater peace of mind. For instance, Participant 6, a male respondent in his sixties, pointed out that when he joined SILC, he did not have much but ever since he has been able to increase his income and invest into more businesses, he reported to have been able to financially support his family as a result. The following is his account:

After joining SILC in 2015, I borrowed money to buy a new breed of goats and a ram. My farm has grown immensely as a result, and now I am able to supply my butchery without having to depend on other farms. I have also started a restaurant where we sell food, particularly our own meat, to the locals and visitors at the bus rank. Additionally, I took a M50 000.00 loan recently and bought a mini truck to help in the businesses. I occasionally use it also to do ‘Nkukele business’ (nkukele literally means carry my belongings), where I transport other people’s belongings for a fee.

To demonstrate further, Participant 2 mentioned that his first deposit to SILC was M300 and that he contributed the same amount for 12 months without borrowing. At the end of the cycle, he had M3600 in the fund plus interest of M1800 which add up to M5400 as take-home. But he was quick to point that other members invested more and therefore had their income doubled at the end of the cycle. The following is what he said:

. . . but other members, especially those with successful businesses contribute huge amounts monthly, and there was a time when someone collected a total of M54,000 at the end of the cycle. This is such a big opportunity for families to grow their income and improve their lifestyles.

In addition, data obtained from Caritas indicated how household income for poor communities of Semonkong increased due to accessing microloans as it was found that although the savings could be as little as M20.00 1 per month, the participants enjoyed a significant take-home amount after 12 months due to accrued interest and money generated from fines imposed on those who do not pay on time or miss official monthly meetings. For example, data showed that 16 groups, with a membership of 318, in Semonkong managed to save M296,284.20 at the end of a cycle. It was, therefore, estimated that each group had 20 members, each of whom earned M925.90 to add to their household income at the end of the period. These amounts vary per area, as seen in the example of Kanana Council in one of the reports, which indicated that there were 6 groups in Kanana with a membership of 107. Together, they had saved M270,037.20 by the end of the cycle. It was also estimated that each group had 18 members, each taking M2500.00 at the end of the period. During the cycle, members rotationally borrow loans which are calculated using a formula based on their savings. For instance, if member X had saved M200.00, she or he would qualify to borrow a maximum amount of M1000 and less for the period of that cycle (M200 × 5 = 1000).

Enhanced education opportunity

Many SILC members consider children education as an important investment for their families because there is a general expectation that children will support their parents as they age. Participants in this study mentioned paying school fees for their children as one of the expenses that SILC helped them to meet. As such, some loans taken from the SILC were used for the education of children. This was explained by one of the participants (Participant 17), who stated,

When my son was completing secondary education in 2016, I took a loan to pay his examination fees because I couldn’t afford to pay them from my pocket. It was so frustrating for me because if I had not paid, that would have meant his future would be bleak. Now that I paid, we are so hopeful that he will have money in future, which will enable him to take care of us and reverse the poverty trajectory of this family.

Similar to this finding, Dungey and Ansell (2020) examined how the idea of survival motivates education in Lesotho and found that young people were expected to both relieve their parents of the burden of their care and actively support them as they grew older; hence, parents have a vested interest in their children’s education. Microfinance has been found to eliminate poverty in households where children could not afford to pay school fees and other educational expenses. Odero (2018) concluded in his study that microfinance enables students who face challenges of paying tuition fees, living costs and other educational costs to access education for the betterment of their lives and their families.

Participant 26 echoed the same idea as he stated,

. . . Ke batla a be le mokhoa boiphiliso ka thuto e se be mokopakopa (. . . I want him to live a good life and be able to meet his own needs without being a beggar)

The above statement reflects the common belief among Basotho that education is key to success, lucrative jobs, health, social security and wealth for the entire family. The reference to ‘family’ in the above statements reflects the importance of a child’s education to the whole family’s survival. To illustrate this point, we use the story of Thabo (not his real name) to show how SILC provides an opportunity for people to improve their lives through getting an education. Thabo was a 26-year-old young man with two younger sisters. Their parents had died, a circumstance which forced him, as the eldest sibling, to drop out of school and find work to take care of his sisters. Thabo revealed in an interview that he occasionally worked at a local lodge to transport tourists with his horses to the nearby waterfall and other places. He explained that it was very difficult to get clients and that some clients did not want to pay for his services which made his income unstable and unreliable. As a result, he asked the elder of his sisters to drop out of school and find work so they could help each other and take care of the youngest sibling. When he was unable to raise enough money for their needs, especially the school fees for his youngest sister, he would resort to borrowing from bo machonisa (the loan sharks or illegal money lenders), who charged him exorbitant interests and often subjected him to various forms of abuse and threats when he delayed payment. This was until he met a friend who introduced him to SILC. Since he joined SILC, he has been able to send his sister back to school. Thabo stated that he also took advantage of the credit facility available to him to start a small business to supplement the income he was getting from his job at the lodge. He stated,

I buy men’s jeans, t-shirts and shoes from town for resale, and the profit I make gives me enough to save with the group on a weekly basis when we meet.

He further explained that with the loans he obtained from the group and proceeds from his business, he is able to pay school fees for his sisters. He hoped that his sisters’ completion of their education would change the future trajectory of his family.

Social empowerment

Social empowerment refers to the use of social capital and risk mitigation strategies to develop autonomy, confidence, power and other necessary means that bring change and pave the way for a better future. During the interviews, participants expressed their improved social relations through networking and information sharing among members through regular meetings. Microfinance meetings served as a communication platform where members shared information regarding issues relating to health, family, church and politics. Through such interactions, social relationships were built and nurtured. Participant 23 pointed out that

Support has become the motto of our SILC group, and the more we meet, the more we bond to become family. These groups are not just about money; they are about the general well-being of the members.

For others, meetings have helped them to come out of their ‘shells’. Participant 29 explained,

I always considered myself reserved until I joined this group, and now I am able to express myself freely, knowing that we are brothers and sisters, and I can freely share my aspirations and fears for the future without being judged.

Similarly, Participant 11 pointed out that before joining SILC, she was already a member of a church group but would never make any contributions during meetings because she was shy. This participant also reflected on one important aspect of the programme in strengthening her human capital through learning of new skills such as accountability, book keeping and lending policies and procedures. She said,

I would normally be silent during meetings and pray, deep down in my heart, that someone would raise some of my concerns. Now I am a different person, I am free to express my opinions and I am not shy to express how I feel. I have also been able to use some of the financial skills acquired from the SILC trainings in my church and other platforms, such as extended family meetings.

Studies show that microfinance significantly shapes and enhances social relations between members and their communities. Rohini and Feigenburg (2010) reported a similar finding, suggesting that regular group meetings enhance social capital because as people interact, they get to know one another better and as a result, group meetings boost trust among members. Many participants of this study reported that their active engagement in SILC activities also boosted their public speaking and financial management skills. This was attributed to regular trainings and support provided by SILC field agents who train members on bookkeeping, leadership, general accountability and management skills.

In one of the meetings, we observed that before the commencement of the formal meeting, members gathered in small groups of two or more just to chat. In one of the small groups, a member was giving an update about the husband of another member who had been unwell for a while. The group then decided to visit that family after the meeting. This made it apparent that the groups were not just meeting to discuss financial matters but also for members to provide psycho-social support to each other. Between meetings, members continued to interact with one another. This promotes trust among members and strengthens their relationships. One family had an opportunity to access the social fund, which is aimed at addressing any emergencies or educational costs for orphans in the community. Participant 17 explained,

When my father passed away in early 2017, I accessed the emergency fund and was allowed to take an additional loan, which assisted me with most of the funeral costs. This was indeed a kind gesture, which helped me a great deal when I was in desperate need of money . . . Funeral expenses can stretch one’s finances but at the same time, every child wants to give their parents a dignified burial, no matter how much money is required to do so.

Many participants highlighted health as an important consideration that required regular financing. In an effort to increase equitable access to healthcare, the government of Lesotho controls the fees for health service provision in government health institutions to ensure that such services are accessible even to the poor. However, many people resort to private healthcare providers, despite their exorbitant fees, citing poor service provision at public health institutions. The results show that healthcare, especially among households with elderly parents or individuals with chronic illnesses, has heightened spending, necessitating the need to borrow money. Participant 24 stated,

. . . despite the low cost of services at public health care centres, I recently took my mum to a private doctor due to private doctors’ reliability and quick response as opposed to public health centres . . .

Negative psychological effects

Despite the positive effects presented above, loans taken from SILC seem to have some unintended negative psycho-social effects among the participants. These include increased levels of stress and anxiety. In trying to ensure the repayment of loans taken from SILC, some members acted as monitors over others, resulting in strained relationships and the erosion of trust among group members. This was pointed out by a Caritas field agent working in the area, who said that this occurred mostly when members feared default by a group member, forcing them to engage in the surveillance of a member after a loan was taken. According to the field agent,

. . . Some of the groups have experienced incidences of non-payment of loans and have had to involve the courts to resolve their cases, and so this has engendered mistrust amongst members causing them to employ different monitoring mechanisms to ensure adherence . . .

This finding is in accord with previous findings indicating that the poor go without proper nourishment to repay their loans (Hammill et al., 2008). While microfinance clearly helps increase household incomes and improve social relations, this study noted that microfinance may lead to negative psycho-social challenges due to constant pressure and stress concerning loan repayments. This often creates a feeling of powerlessness and vulnerability owing to failure to pay. As indicated by Banerjee and Jackson (2017), rather than reducing it, microfinance may also exacerbate vulnerability and poverty because of the increased debt burden on individuals and households.

Another participant (Participant 6) also mentioned that there were some members who took loans for their friends or family members under their names and then failed to repay such loans. He explained,

Some of our members were found to have obtained loans through false pretenses and later failed to repay them, resulting in tensions among members and gossip and mistrust.

Some respondents referred to a disturbing trend where members borrow money from relatives or other societies to repay the loans instead of raising funds from their own businesses, a practice that defeats the whole purpose of SILC. This sentiment was expressed by a 56-year-old woman (Participant 12) sharing her own experience:

I took a loan once in 2016 from a SILC group and failed to pay back because my potato harvest was not good that year; hence I did not sell as much as I had anticipated. I then borrowed money from my daughter-in-law’s society so I could clear my name from the SILC group. Unfortunately, at the time, her husband, whom we both trusted would rescue the situation, lost his job, and the pressure to pay back the loan from the society mounted. All I can say is that I’m not in good terms with my children right now because I failed to raise funds to pay back the loan.

Conclusion and recommendations

Poverty is a fundamental problem that confronts Lesotho, particularly its rural, mainly mountainous areas including Semonkong. The government is working with NGOs to implement programmes that aim at providing poor rural communities with financial services to improve their socio-economic conditions and livelihoods. This study aimed to investigate the extent to which SILC as a savings-led microfinance contributed to the socio-economic conditions of the rural poor in Lesotho in relation to household income, education and health. The study aimed to assess how SILC enhanced opportunities for members to acquire assets and start businesses, identify challenges that resulted from borrowing and document some of the experiences as a result. The results indicate that SILC has been effective in increasing household income and smoothing consumption, enhancing education and increasing access to health services. Further findings show that microfinance programmes indeed make poverty survivable through secure means of savings and lending at a low interest rate among community members. The findings show that involvement with SILC initiative has instilled a better savings culture among rural-based communities; hence, they are highly effective and favoured by the rural communities as a sustainable livelihood activity. The initiative has also provided for accumulation of assets aimed at leveraging the means of living. Respondents were found to have previously used riskier saving mechanisms such as keeping money under the floor mat or anywhere in the house and were used to borrowing money from expensive money lenders who charged ridiculously high amounts of interests. The results further show that involvement in a microfinance scheme enhances social skills such as public speaking, leadership, book keeping and accountability, which are a critical tool to drive interventions aimed at reducing poverty and enhancing livelihoods. On the contrary, strained relationships among community members, stress, shame, powerlessness and fear still prevailed as a result of increased debt incurred by some members. This was mostly attributed to failed businesses or unprofitable business ventures. This is in line with Bayrasli (2012) who ascertains that access to microfinance does not automatically make people entrepreneurs; it requires interest and effort to start a business, skills and commitment.

Recommendations

While the data found some well-established and potential entrepreneurs among the poor communities in Semonkong, the findings suggest, however, that there are some challenges for successful entrepreneurship aimed at reducing poverty. Some of the participants may still not possess creative skills required for a successful entrepreneur even after trainings conducted by Caritas. The study recommends that besides accountability and bookkeeping skills, beneficiaries be trained on business proposal writing to help them pitch to prospective clients and demonstrate the value of their businesses and why they are best in the competition. They could also be trained and supported on exploring different entrepreneurial opportunities to help them diversify new products, markets and services as well as ignite their creativity and competitiveness in the market. For such a holistic intervention, we recommend that policy makers evaluate the market environment and analyse whether it may be financially viable for NGOs and even commercial banks to develop innovative financial products and technologies to target such populations. This will help those with mature microenterprises who might demand larger savings service and loans to grow their enterprises more. In this way, microfinance will lead to creation of full-time or part-time employment opportunities in an economically disadvantaged community.

Footnotes

Author contributions

Conceptualization: M.M., G.F., F.M.; methodology: M.M., G.F., F.M.; data collection: M.M.; data verification: G.F., F.M.; preliminary analysis: M.M.; final analysis: M.M., G.F., F.M.; writing – original draft preparation: M.M.; writing – review, editing and final preparation: M.M., G.F., F.M.; data visualisation: M.M. All authors have read and agreed to the published version of the manuscript.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.