Abstract

Using the accounting process framework, we illustrate the varied attempts preparers have taken with regard to making accrual accounting and reporting (AAR) useful and useable for prospective users. Our longitudinal analysis, spanning the years 2008–2021, centres on the experiences of Organisation for Economic Co-operation and Development (OECD) member countries. The data were gathered from observations and informal conversations at meetings of the OECD Senior Budget Officials Network on Financial Management and Reporting, and a review of corresponding publicly available official documents and presentations. Our findings cast light on the reasons for the diversity in the practice and the use of AAR among the OECD member states, although guided by the same norms cascaded down from the accounting environment. Preparers in member states are shaping AAR differently within their own contexts than those prescribed by the accounting environment, as they have learned from their experience of dealing with users and their information needs. The scale of this diversity is determined by the extent to which AAR reforms correspond to the member states’ accounting contexts. The harmonisation of AAR thus appears a more elusive goal owing to the varied approaches that the preparers have chosen to make AAR useful and useable within their local settings.

Points for practitioners

Accrual accounting and reporting (AAR) reforms proposed by standard setters, international organisations, practitioners and the accounting profession have often proved to be very technical and overwhelming, overlooking both the contextual requirements and the users’ capacity and information needs. In addition, preparers have to deal with a plethora of inputs from the local side. Having learned from these experiences, advanced preparers are now involved in the contextualisation of AAR reforms, e.g. through simplification, alternative presentation formats and reducing information overload on users. This, coupled with the approaches they have taken to promote the use of AAR, has resulted in diversity in its adoption across countries. Hence, it is important to understand the communicative dimension of AAR reforms as driver of such diversity.

Introduction

This study sheds light on the adoption of accrual accounting and reporting (AAR), with a focus on attempts of preparers of making AAR useful and useable. A major trend within the public sector worldwide over the past few decades has been the adoption of AAR. A recent status report showed that a total of 120 countries will adopt some aspects of AAR at different administrative levels by 2030 (IFAC/CIPFA, 2021). The International Public Sector Accounting Standards are widely used examples of AAR that were either adopted by a substantial number of governments or are being considered for potential adoption (Polzer et al., 2020). Academic and professional debates about the implementation of AAR in the public sector and its perceived benefits have persisted and are still ongoing (Adhikari and Gårseth-Nesbakk, 2016; Stewart and Connolly, 2025). For instance, the accounting profession, practitioners and standard setters have continually propagated the benefits of AAR, in terms of generating more reliable and comprehensive information beyond cash receipts and payments, and thus improving transparency and decision-making (IFAC/CIPFA, 2021).

With some exceptions (e.g. Andriani et al., 2010), AAR has, however, been contested at the academic level, owing to its profit-oriented neoliberal objectives, inherent technicalities and, more recently, its inability to account for and discharge accountability in relation to issues of wider social significance such as climate change, social equity and financial resilience (Grossi et al., 2023; Steccolini, 2019). A focal point of criticism concerns the extent to which accrual information is actually understood and used by the prospective key groups of users, in particular the politicians and public administrators, who are in a position to approve such information (Ezzamel et al., 2005; Haustein et al., 2019; Oulasvirta, 2023; van Helden and Reichard, 2019). For instance, van Helden (2016) argues that politicians’ approval or appreciation of accrual information does not mean that they will use it in practice. Increasingly, claims have been made in favour of adopting a user perspective when studying the implementation of AAR (Haustein et al., 2019; Oulasvirta, 2023).

However, making accrual accounting information accessible to different groups of users, or the ‘demand side’ of information as it is referred to by Hammerschmid et al. (2013), has proved to be challenging within the public sector (Polzer et al., 2020). While some studies argue that it takes time for users and preparers to understand and be convinced of the usefulness of AAR (Andriani et al., 2010; Ezzamel et al., 2005), other studies have provided evidence that users’ interest in accrual information lags behind the promises made by the promoters of AAR and therefore it remains largely inapplicable (Haustein et al., 2019).

It is often argued that preparers of financial statements (i.e. the ‘supply side’ – see e.g. Hammerschmid et al., 2013) can play an important role in designing (better) systems for communicating accrual information by making it more easily understandable and applicable for users. Surprisingly, such a perspective on the ‘preparation’ of statements as a crucial antecedent of their ‘use’ has so far received scant attention in the public sector accounting literature and, until recently, has lagged behind in comparison with the ‘use’ perspective (Oulasvirta, 2023). Only recently have a few studies begun to address the ‘usability’ of performance information for different user groups (although in a somewhat abstract way), for example with respect to understandability and user needs (Jethon and Reichard, 2021). A recent study by Bracci et al. (2023) illustrated the attempts made by preparers of financial reports in an Italian municipality to translate public sector accountability into practice. Apart from these examples, investigating the ways in which preparers attempt to link accrual information to users has constituted an important gap in the public sector accounting literature.

Drawing on the accounting process framework (Mellemvik et al., 2005), we address this gap in the current study, highlighting the preparers’ views and experiences with AAR and their attempts to make it more useable. A key aspect of the accounting process framework concerns the delineation of variations in accounting practice and use, taking into account the learning that emanates from the accounting process. We ask the following question: what are the challenges that preparers have encountered in implementing AAR and what attempts have they taken to making AAR useable and useful within their own contexts?

The relevance of the research is underlined by observations that the preparers of AAR have encountered multiple challenges in adopting AAR, not least because information needs, accounting traditions, government policies and the required staff competences are rarely, if ever, the same in the public sector as in the private sector (Steccolini, 2019). In this respect, the annual symposia of the ‘Organisation for Economic Co-operation and Development (OECD) Senior Budget Officials Network on Financial Management and Reporting’, the empirical setting for this study, offers a fruitful arena for gathering information about challenges that preparers in different member states encounter with respect to perceived user needs, and their attempts to address these challenges.

The remainder of the paper is organised as follows: the next section discusses the accounting process framework and its significance for the study. We then outline the research methods. The fourth section presents an overview of the key public sector accounting issues discussed within the OECD. The findings are then presented, followed by a discussion. The final section outlines the contributions made by the study.

Theoretical orientation: The accounting process framework

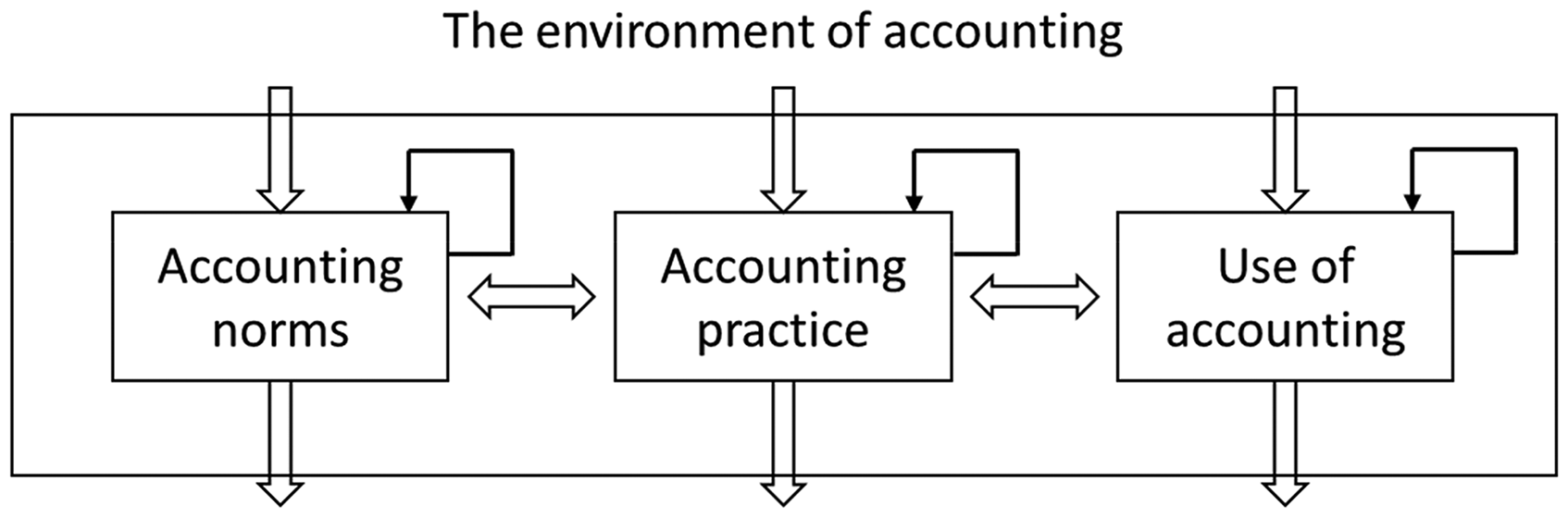

Prior work on AAR has demonstrated that reforms prescribed in the wider accounting environment are often ‘contextualised’ and ‘glocalised’ when they are cascaded down to adopting countries (Baskerville and Grossi, 2019). An underlying principle of the accounting process framework (Figure 1) involves explaining the reasons for this, i.e. how accounting ideas and practices are adjusted to the ‘targeted contexts’, to obtain legitimacy (Mellemvik et al., 2005). As compared with many other frameworks which focus on user needs, usability and use of accounting information (see e.g. van Helden and Reichard, 2019), this framework identifies and differentiates the three levels affecting the process of accounting – ‘accounting norms’, ‘accounting practice’ and ‘use of accounting’. Activities at the level of accounting norms include the adoption of global accounting principles in the form of national laws and regulations, i.e. stating how things should be according to theory and standards. ‘Accounting practice’ comprises both day-to-day accounting activities (such as entering transactions in the accounting books) and periodic tasks (such as preparing reports). Mellemvik et al. (2005) explain that the ‘use of accounting’ relates to both internal users (e.g. managers) and external users (e.g. politicians, journalists and citizens) and the manner in which they apply accounting information in relation to decision-making and accountability.

The accounting process framework (Mellemvik et al., 2005).

Central to the framework is the assertion that the linkages between the levels are not linear or one-way. For instance, not only is accounting practice shaped by accounting norms, but the former is also affected by other factors beyond the changes in accounting norms. Another example for linkages is that users may also use accounting information in a way that adheres to their own ideas, and thus call for changes in relation to accounting practices (such as changes in formats or complexity of accounting reports). The process of accounting delineated in the framework also implies that it is both influenced by and influences the environment, which consists of international organisations, lobbying groups, the profession itself and shareholders, among others.

The framework has embedded elements of learning to provide more clarity about how the process of accounting operates. The thin recursive arrows in Figure 1 indicate learning emanating from each process through the experience of the individuals involved. The thick arrows represent three different learning situations – between sub-processes and from the environment to each sub-process and vice-versa. Following the framework, accounting norms may alter owing to the learning experience of those involved in the processes, as well as in respect to the experiences of others. This in turn may affect the accounting environment, in particular the way in which pressure for reform is exerted. The framework therefore demonstrates how each accounting process is influenced through its own experience, as well as the experience of other processes and how the accounting environment can learn from the experience of and interaction with the accounting processes.

As stated previously, we draw on the above framework to better understand the multifacetedness in the adoption of AAR across OECD member states. The extent to which accrual information is actually drawn upon by prospective key users is decisive in terms of determining the extent to which the adoption of AAR can be regarded as successful (Haustein et al., 2019; van Helden and Reichard, 2019). Thus, adopting countries and government actors involved in the process, as the preparers of financial statements, have a strong incentive to link ‘accounting practice’ and the ‘use of accounting’ to legitimise the adoption of AAR. Consequently, we argue that a key task for preparers of financial statements is to cater to the (perceived) information needs of different user groups (illustrated by the horizontal arrow in Figure 1 that runs from right to left from ‘use of accounting’ to ‘accounting practice’). Thus, preparers may attempt to identify users’ information needs and tailor financial statements with respect to the format and content in the process of adopting AAR. It is therefore particularly important for them to edit and re-visit the requirements of AAR according to the information needs of the ‘demand side’ within the target context and to contribute to consensus building. However, how this is achieved, i.e. what preparers’ concerns are regarding the perceived accounting information needs of users and what they do to engage with users’ needs, is an open question that we address in this study. In other words, while the framework illuminates the complex settings in which the preparers are situated (by suggesting that influence may come from users, from standard setters and from the institutional context), what we do not know from the existing literature is what the preparers do in such situations of complexity, as well as their learnings – and this is what we are exploring and discussing in this article.

We argue that the presentations and debates that preparers engage in at the OECD reveal the outcomes of the ‘learning circle’ from the preparers’ perspective, and reflect the way in which user-related issues are perceived by preparers and the approaches taken to address them.

Methodology

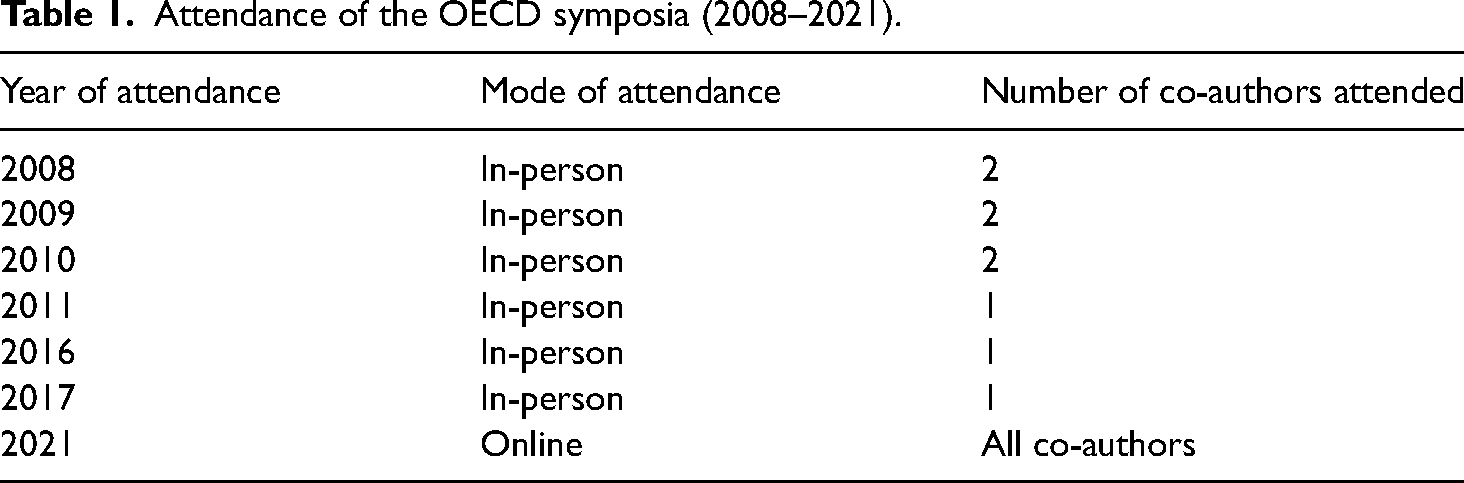

Since its inception in 2001, the symposia of the ‘OECD Senior Budget Officials Network on Financial Management and Reporting’ have become an annual event. These symposia provide a forum for key stakeholders involved in public sector accounting, including standard setters, international organisations, policy makers, practitioners and preparers (mainly budget and treasury officers and senior accountants representing member states and other invited countries) (Adhikari and Gårseth-Nesbakk, 2016; Blöndal, 2003). To highlight the concerns of preparers, we conducted a longitudinal qualitative study, spanning the years from 2008 to 2021. While the year 2008 marked the beginning of the financial crisis, further rationalising the importance of AAR and its adoption by member states, the COVID-19 pandemic which began in 2020 introduced several new issues and priorities within public sector accounting beyond the implementation of AAR, including recovery packages, digitalisation, social equity and sustainability reporting (e.g. Grossi et al., 2023). By placing special emphasis on the years at the beginning and the end of the observation period, we have thereby covered the periods in which the focus was on extending the implementation of AAR across member states and elevating its usefulness and applicability for adopting governments.

The OECD symposia are closed events and thus formal interviews with participants are prohibited. To ensure the richness of the data, we therefore adopted a triangular approach, involving: (a) analysis of the publicly available symposia materials; (b) observations of the symposia; and (c) informal conversations with symposia attendees (Ahrens, 2022; Patton, 2015). We started our data collection in 2008 by analysing the agendas, documents, presentation slides and reports of earlier symposia which are publicly available on the OECD webpages. We repeated this process during the data collection period. In addition, we collected hard copies of such documents, slides and reports in those years in which we attended the symposium in person (see Table 1). While reviewing these documents, we were guided by two key objectives, mirroring our research questions: first, to obtain insights into the plans and strategies for advancing the AAR reforms (e.g. by analysing the distribution of topics on the agendas) and areas/issues that were regarded as challenges; and second, to identify the approaches to making AAR useable and useful (e.g. by studying best practices referred to in the presentation slides).

Attendance of the OECD symposia (2008–2021).

In total, we attended seven symposia during our study period (Table 1). Extensive notes were taken in each session to capture the views of representatives. These were then cross-checked when more than one co-author was involved in taking the notes, and discussions were held between the co-authors who had attended the symposium to ensure consistency in our understanding of the issues/topics discussed in each session. Informal conversations were held mostly with the representatives of member states (preparers) whenever the opportunity arose, especially during break times. In total, we were able to talk with more than 40 representatives during our study period, and each conversation lasted between 5 and 30 min. Given the informal nature of the conversations, we assured each representative that full anonymity would be maintained. Our aim in facilitating the informal conversations was to obtain the views of diverse actors and country representatives attending the symposia. For instance, following the OECD's categorisation of members in terms of their adoption of accrual accounting – high intensity accrual adopters, medium-intensity adopters and low-intensity adopters (Adhikari and Gårseth-Nesbakk, 2016; Blöndal, 2003) – our focus was on selecting representatives from each category. Such differences between the member states in terms of the adoption of AAR were also notable during our observations, helping us identify the representatives for informal conversations.

The content of our conversations focused mainly on understanding preparers’ views on AAR reforms, the challenges they encountered during the implementation process, their experiences of dealing with different groups of users and their attempts to making AAR useful and useable for decision-making. The views expressed by representatives were immediately added to the field diary and discussed by all co-authors until a consensus was reached. It is worth noting that these views were largely shaped by the stage of reform that their countries were currently at. Being able to collect data through observations and informal conversations was particularly important, as this enabled us to capture the preparers’ viewpoints as they naturally emerged from the debate, rather than issues being artificially introduced in a formal interview setting. The pertinence of such ‘naturally occurring data’ has been particularly highlighted in qualitative research owing to its ability to strengthen the validity of the results (Ahrens, 2022; Steccolini, 2023).

We analysed the data adhering to the underlying ideas of ‘directed qualitative content analysis’ (see e.g. Hsieh and Shannon, 2005) and ‘generalisability’ in qualitative accounting research (see e.g. Ahrens, 2022; Steccolini, 2023). This allowed us to capture diverse issues relating to the use of AAR by engaging with the literature, theory and practice and the approaches taken by preparers’ to make AAR useful and useable. To begin with, taking into account the key ideas underpinning our analytical framework (Figure 1), in particular the learning process, we carefully reviewed the texts of the publicly available symposia materials, highlighting those relating to users and uses of AAR. Mirroring these interests, our initial coding categories therefore incorporated issues such as concerns about users, as discussed in the symposia as the ‘accounting environment’, key challenges associated with the adoption of AAR, approaches recommended to member states/governments, and preparers’ experience and learning gained via the process of implementing AAR. In a next step, after reviewing the notes taken during our observations and informal conversations, several new coding categories were identified. These included, amongst others, preparers’ experiences of dealing with the technicalities of AAR and (re-)defining and contextualising the key concepts, elucidating the importance of AAR to users, understanding the capacity and competence of users and lessons learned in terms of making AAR useful and useable. Following an iterative procedure, we revisited the initial coding categories, deleted the overlapping ones and added new categories. The initial and revised categories were subsequently discussed following the coding rules, as outlined by Miles et al. (2014), and finalised with the agreement of all the co-authors. In a final step, the finalised categories, relevant quotes and findings were then analysed to flesh out the attempts preparers have taken with regard to making AAR useful and useable for users.

Empirical context: The ‘environment of accounting’ and concerns about users

Implementing AAR across different countries has proved to be a major issue in the wider environment of public sector accounting, not least the OECD (OECD/IFAC, 2017). Among the major actors at this level, influencing countries’ efforts to implement AAR, are the standard setters (e.g. International Federation of Accountants [IFAC], International Accounting Standards Board [IASB], European statistics, statistical office of the European Union [EUROSTAT], Federal Accounting Standards Advisory Board [FASAB]), regional policy makers and think tanks (e.g. European Commission [EC], OECD), international monetary organisations (e.g. International Monetary Fund, World Bank), the professional associations (e.g. Chartered Institute of Public Finance and Accountancy [CIPFA]) and accounting firms (e.g. PricewaterhouseCoopers [PwC], Ernst & Young [EY]). These actors have regularly participated in the OECD symposia, championing their success in terms of disseminating AAR across member countries, as well as highlighting the challenges they have encountered. Our experience of observing the symposia during its early years was that a large number of AAR-related issues remained unsettled, and that the standard setters were falling behind in terms of meeting their schedules and deadlines. The situation was further exacerbated in the immediate aftermath of the financial crisis as governments were hesitant to embrace many elements of AAR, such as fair value. Numerous discussions took place about allegedly difficult accrual concepts such as accounting entities, financial instruments and fair value and the challenges faced in terms of explaining the importance of these concepts to users (primarily governments).

Identifying users and their information needs was another issue repeatedly discussed in the symposia. Our early observations showed that a specific public sector conceptual framework outlining key users was absent during this time, and questions were therefore raised about the actual users of public sector accrual information and whether accrual information is useful to them. Opinions were divided in terms of identifying the types of information that users would prefer, as well as the piecemeal adoption of standards (that were themselves still under development) and reforms introduced by governments. Implicit in the discussion were concerns about the extent to which such initiatives would allow governments to reap the full benefits of AAR. We observed that, despite emphasising a holistic adoption of AAR, actors in the environment quickly became aware of the issues relating to users’ capacity for consuming information and the consequences of producing excessive information. Concerns were raised with the caveat that an overflow of information may erode users’ interest in AAR and slow down the pace of adoption.

During the period under investigation, discussions continued regarding several areas and aspects of AAR in relation to which the views of participants remained divided. Such ambiguities were particularly observed in relation to the treatment of social insurance programmes (e.g. pensions), recognising certain contingent liabilities (e.g. in PPPs), dealing with accuracy and volatility associated with non-cash items (e.g. depreciations), measuring heritage assets, sustainability issues and adopting accruals for budgeting. Towards the end of our observation period, the discussion primarily shifted to public finances after the COVID-19 pandemic, as well as the question of how digitalisation initiatives can contribute to addressing users’ information needs. We observed that, in the later stages, the understanding of who constitutes a ‘user’ of accounting information became broader, and has now also extended to citizens and the media, for example.

Findings: Dealing with AAR users from the preparers’ perspective

Identified issues by preparers regarding usefulness and useability of AAR

Convincing different groups of users of the benefits of ambitious AAR reforms proved to be challenging for a large number of country representatives attending the symposia. Many of the accrual concepts and standards introduced were perceived as ambiguous and preparers were therefore uncertain about the extent to which these would actually be useful in addressing users’ needs and expectations. For instance, a representative of a member state in Central Europe shared his country's experience: ‘One challenge is that there is no full agreement and one standard. […] It is important for us that we will not be accused [by users] of manipulating the figures [due to different systems of asset valuation that operate in parallel]’.

Another caveat, highlighted by several representatives especially during our early observations, concerned potential misinterpretation of accrual standards and statements by prospective users. With the exceptions of the Anglo-Saxon countries, understanding of key concepts, such as the adjustments required on balance sheets, was limited. Such challenges made preparers in a number of member states, mainly in Europe, reconsider the timeline for implementing reforms, in particular by slowing down the pace of adoption. In a few member states, the reforms were paused altogether. In fact, debates around key concepts and how they could be applied to the context of the public sector continued for many years, as a representative of one European member state confirmed during our later observations: ‘The concept of net assets/equity in particular has a different meaning for the central government compared with a company [causing possible confusion among users]’. The challenges faced in dealing with such items have also been outlined in several previous studies (Adhikari and Gårseth-Nesbakk, 2016; Blöndal, 2003).

The need to report on a multiple set of accounts (e.g. accrual consolidated statements and statistical reports) was another issue that captured the attention of preparers in multiple member states. This requirement put them in a difficult position as they had to convince the users of which set of accounts are to be used and for what purpose. Although discussions were ongoing regarding harmonisation issues between public sector accounting standards and statistical guidelines (e.g. ESA and GFSM), a consensus was yet to be reached. During our early observations, a representative from an Anglo-Saxon member state commented: ‘The bigger problem was a confusion for the readers of having two statements. Which one was right?’

A large number of country representatives were of the view that the media reporting of AAR had become another challenging factor for them in terms of both convincing and dealing with the politicians and administrators. For instance, a representative of an Anglo-Saxon member state remarked at a symposium that ‘the media only focuses on surplus, not the balance sheet’. In the following year, the same representative shared his experience of dealing with the media: ‘[We] need to be clear when talking with the media about what is and what is not an estimate’. During our informal conversations, representatives were more critical about how the media reported on AAR at times, accusing them of undermining their efforts to elucidate the importance of AAR to users.

While emphasising the importance of being aware of the needs of different user groups, representatives from European member states were particularly cautious about their expectations of the user groups. A key concern raised was whether they (representatives) were expecting too much from the users or, alternatively, whether they have failed to clearly consider what would be of specific interest to different groups of users. A representative from a central European member state recounted the experience of introducing fiscal sustainability reporting in his country: ‘We backed away from an indefinite time horizon because it is a nightmare to explain it to people. We struggle with convincing people that we are not [financially] healthy’.

The majority of Anglo-Saxon member states had already adopted AAR by the beginning of the twenty-first century (see e.g. Adhikari and Gårseth-Nesbakk, 2016). The preparers in these countries were particularly concerned about the importance of education and competence building as the adoption of AAR turned out to be very technical. During both the symposia discussions and informal conversations it was mentioned that civil servants at different administrative levels initially often had an insufficient understanding of the new accounting and budgeting principles introduced. This, in turn, impaired an efficient dealing with requests by users for specific information. In fact, this appeared to be an even more severe problem in other member states, as the following statement by a representative of one Scandinavian country illustrates: ‘Getting the new rules to work in practice has […] proven to be a great challenge. The need for education of the administrators must […] not be underestimated. Insufficient understanding of the new rules for accounting and budgeting affects the whole decision-making process’.

A further issue experienced across the majority of member states was a limited readership of financial statements, which resulted in accrual information having a limited impact on fiscal policy decision-making. Such concerns have also been raised in the existing literature (Haustein et al., 2019; van Helden and Reichard, 2019). The need to facilitate research was particularly emphasised so as to increase the use of accrual information, as shown by the following statement from a representative of one Asian member state: ‘The disclosures provided to users are sometimes unclear, redundant or immaterial [alongside information being] scattered across different reports. We need to research how to better use accrual financial information with reference to international practices’.

Attempts of preparers of making AAR useful and useable

At the time we started observing the symposia, several initiatives had already been implemented by Anglo-Saxon member states to draw users’ attention to AAR and some important lessons had been learned. Such initiatives were targeted at reducing the information burden on users by simplifying the financial statements and other disclosure notes and making sense of accounting information. Representatives of these member states (Anglo-Saxon countries) were well aware of the fact that users are interested in having access to more timely, simple and accessible information and therefore their preference would be for budget and planning documents rather than technical accounting issues and statements. Alternatives were proposed to simplify the process, asserting that this could be achieved through the reworking of reporting practices, especially by the provision of shorter statements (mitigating information overload) and better presentation of the accounting information (improving clarity). Views were expressed during our informal conversations that the simplification of the practices and statements would also ease the existing tensions in relation to meeting the accountability expectations of diverse users.

As part of simplifying the presentation and dissemination of accrual information, a number of country representatives provided examples of the specific initiatives that they had undertaken. These included launching separate webpages and providing a short illustrative brochure, nicknamed the ‘citizen’s guide’. For instance, during our observations, a representative of an Anglo-Saxon member state revealed: ‘the full report, 267 pages, I send 17–18 sections of that each year to a fixed list of recipients. [However,] the citizens guide: I ship thousands of that thin brochure’. In addition, during our informal conversations, representatives of Anglo-Saxon member states highlighted the holistic approaches they have pursued as a result of having learned lessons from their AAR experience. Such approaches not only emphasised the users’ needs but also considered the challenges they themselves had encountered in the process of implementing AAR and making accrual accounting information useable. The focus was on identifying examples of good accounting practices by engaging closely with the user groups and seeking their feedback. For instance, representatives pointed out that the AAR was supplemented by the incorporation of narrative statements (aimed at helping users to understand concepts more easily via better explanations, highlighting key priorities and cross-referencing key information) and by improving the presentation of accounting information (i.e. information reduction, consistency and visualisation). A representative of one Anglo Saxon member state commented: ‘[W]e have started to make more use of graphical illustrations so as to make governmental reports more reader-friendly’.

During the period under investigation, several important lessons have been learned in relation to the process of dealing with users and the challenges faced in implementing AAR. For instance, during our observations of a later symposium, a representative of one Anglo-Saxon member identified three lessons they had learned during their 25 years’ of experience with AAR in a presentation: ‘1. Target users’ needs and objectives, 2. Welcome the pain and use it!, 3. Moving from stability to resilience [i.e. their ability to fend off financial crisis, fluctuations and turmoil]

The above statements illustrate the extent to which the public sector accounting environment has influenced accounting norms, practice and use (Mellemvik et al., 2005). A key issue underlying the adoption of AAR concerns improving transparency and accountability by serving user groups with enhanced accounting information. As outlined in prior work (Adhikari and Gårseth-Nesbakk, 2016), the pace of the AAR reforms proposed has apparently proved to be demanding. However, the preparers have been forced to adopt them following several adjustments and simplifications. With some exceptions among Anglo-Saxon member states, the level of adoption of AAR therefore varied significantly, resulting in the public sector accounting environment having to readjust the implementation plans, strategies and timelines for AAR reforms on several occasions. The implications of these results are outlined in the following section.

Discussion

Using the longitudinal setting and drawing on the accounting process framework (Mellemvik et al., 2005), we have identified the challenges that preparers in OECD countries encountered in implementing AAR regarding a perceived lack of user orientation and the attempts they have made to accrue information that is useful and useable in the contexts of their own countries. The literature shows an increasing proliferation of AAR across countries (IFAC/CIPFA, 2021; Polzer et al., 2023). For many years, one of the academic criticisms targeted at AAR centred on aspects relating to the users, mainly delineating how accrual technicalities and other factors such as capacity and resource constraints have limited its application by politicians and administrators (Haustein et al., 2019; Oulasvirta, 2023; van Helden and Reichard, 2019), as well as the length of time that users need to adjust to AAR (Ezzamel et al., 2005).

However, as our findings show, issues relating to AAR users are neither new nor unknown to the actors within the environment of public sector accounting who participated in the OECD symposia. For instance, continued discussions were held in the symposia about making users aware of technical accrual concepts, such as fair value and heritage assets. The consequences of information overload of users were widely acknowledged. Following our findings, a number of contributions have been made.

First, the application of the accounting process framework (Mellemvik et al., 2005) has enabled us to shed light from a different perspective on the challenges that the preparers reported at the OECD symposium regarding their attempts to making AAR useful and useable. An underlying idea of the framework is that the linkage between the accounting norms, practices and use functions in a dialectic manner, being influenced by the learning emanating from each level. By using the framework, our findings have therefore cast light on the causes of the perceived diversity in the practice of AAR among the OECD member states, despite being guided by the same norms cascaded down from the environment. Indeed, the scale of this variation is determined by the extent to which the AAR reforms correspond to the member states’ accounting contexts. With this, the study adds to research addressing the different variations of AAR practices and use (e.g. Baskerville and Grossi, 2019), especially by showing that preparers across countries face an arduous and sometimes conflicting duality, namely attempting to mix international AAR developments with local contextual specificities. While the existing literature is so far largely silent on what the preparers do in such situations of complexity, as well as their learnings, our analysis of the presentations and debates that preparers engage in at the OECD symposia reveal the outcomes of the ‘learning circle’ from the preparers’ perspective, and reflect the way in which user-related issues are perceived by preparers and the approaches taken to address them. In particular, the results show how preparers attempt to develop national AAR practices that serve multiple interests, namely those brought about by information needs of different types of users, by national political priorities and by international standard setting recommendations.

Second, as outlined in prior work (Adhikari and Gårseth-Nesbakk, 2016), our findings also demonstrate the domination of Anglo-Saxon member states in the adoption and implementation of AAR. However, preparers in these countries have continually expressed their concerns, particularly when dealing with users such as politicians, administrators and media and elucidating the technicalities inherent in accrual concepts to them, such as the rationale for pursing multiple reporting models (i.e. statistical and accrual-based statements). For instance, the media has often been keen to demonstrate ‘surplus’ rather than highlighting other elements of the balance sheet, thereby questioning the significance of the time and effort expended on preparing financial statements. Implicit within the views expressed by preparers representing non-Anglo-Saxon member states was the fact that AAR reforms have often followed ambitious paths, thereby overlooking both the contextual requirements and the users’ capacity and information needs.

Lastly, the findings showcase the varied approaches that preparers, mainly in Anglo-Saxon member states as the most advanced ones in terms of AAR reforms, have drawn on by learning from their experiences and their attempts to fine-tune accrual information so as to make it useful and usable for users. While many non-Anglo-Saxon members have continued to be preoccupied with technical implementation issues, several attempts have been made in Anglo-Saxon member states to reduce the information burden on users by simplifying the presentation of financial statements and disclosure notes, developing illustrative brochures and webpages, and embedding more narrative statements and graphical examples.

Indeed, simplification seems to be a key way in which the preparers from most advanced reformers have tried to deal with and resolve the many inputs they have received on AAR initiatives. The study thus contributes to the accounting process framework (Mellemvik et al., 2005) by highlighting the communicative dimension that is key to accounting reforms. Although the framework arguably captures important dimensions for investigating reforms, it does not put sufficient emphasis on the communicative dimension of AAR. Our results provide some evidence that the most experienced preparers are becoming increasingly aware of the importance of this aspect of accounting.

There was also evidence of a more holistic approach being pursued in advanced countries, seeking feedback from politicians and administrators during the preparation of financial statements and identifying good accounting practices. In this way, we have illustrated how the learning emanates from the accounting process through preparers, influencing both public sector accounting practice and the use of accounting information. Ongoing discussions within the public sector accounting environment at the OECD symposia regarding making AAR more accessible and applicable to users, and initiatives launched, such as roundtable discussions with users, also provide some evidence of the influence that preparers have had at the level of ‘accounting norms’, as well as within the wider ‘environment’ (Figure 1) of public sector accounting (Mellemvik et al., 2005). Such influence is, however, fairly minimal compared with the influence of the accounting environment and is the privilege of only a few – mainly Anglo-Saxon – member states. The voices and influence of many non-Anglo Saxon members states have yet to penetrate the public sector accounting environment.

Concluding remarks

A limited number of extant studies has examined AAR reform initiatives from the preparers’ perspectives (Bracci et al., 2023). Preparers’ concerns are often marginalised within the existing public sector accounting literature, and therefore their perspectives on AAR and the initiatives they have instigated to make accrual information useful and usable can offer additional ways of understanding AAR and its applicability in the public sector (Oulasvirta, 2023; van Helden and Reichard, 2019). The current paper has addressed this knowledge gap in the literature by fleshing out preparers’ concerns about the information needs of (prospective) users of AAR and their attempts to make AAR useful and useable in their country contexts.

Next, by using the accounting process framework (Mellemvik et al., 2005), we have also unfolded the way in which learning processes emanate, thereby shedding light on the reasons and causes that will continue to create diversity in the adoption and implementation of AAR across countries. Despite ongoing discussions about the harmonisation of public sector accounting (Baskerville and Grossi, 2019), the role of preparers in the harmonisation process has continued to be somewhat overlooked here. Preparers are involved in shaping AAR in their own contexts in different ways, having learned from their experience of dealing with users and deviating from what is expected from the accounting environment. Although the scale of variations in the adoption and implementation of AAR is somewhat limited in Anglo-Saxon countries, the discourse of AAR harmonisation emanating from the accounting environment therefore appears to be more of an elusive goal owing to the varied approaches that the preparers have undertaken to make AAR useable and useful in their own contexts.

Lastly, the triangulation approach used to collect the data has enabled us to reinforce the validity of our findings in the absence of formal interviews, making it possible to capture a large amount of data (Ahrens, 2022). Against the backdrop of the limitations of the study, an important avenue for continuing the research has been identified. The fact that preparers in different contexts are encountering different types of challenges and undertaking varied approaches, increasingly dialogic approaches to consider pluralism (Grossi et al., 2023; Steccolini, 2019), implies that we have only been able to focus on a few major issues relating to the adoption and implementation of AAR. Further research could therefore explore other institutional, technical, linguistic and dialogic issues, influencing the preparers in different contexts and the manner in which they are dealing with these issues, as a crucial part of making AAR useful and usable.

Footnotes

Acknowledgments

The authors would like to thank the anonymous reviewers and the journal's editorial team for their very helpful comments and advice. Open access funding provided by WU Vienna/Kooperation E-Medien Österreich, Austria, is gratefully acknowledged.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.