Abstract

This paper sets out to explore the effect of programme budget mechanisms on the efficiency of public spending. To do so, we first conducted an exploratory study among eight officials involved in the preparation and execution of the State budget. This exploratory study then enabled us to construct the variables to produce an analytical model. A survey was carried out among 475 performance chain actors in the central services of 29 ministerial departments of the State of Cameroon. The results obtained using descriptive statistics and simple probit regressions suggest that the mechanisms introduced by the programme budget have a mixed effect on the efficiency of public spending. While, on the one hand, structuring the budget into programmes, actions, activities and tasks, performance measurement indicators and a priori controls on the quality of programmes may have a positive effect on the efficiency of public spending; on the other hand, allocating appropriations according to expected results and costs and a posteriori internal and external budgetary controls have a negative influence on the efficiency of public spending. The study recommends developing the external budgetary controls and introducing internal controls that focus more on performance rather than consistency.

Points for practitioners

This paper contains the first scientific analysis of the effects of programme budgeting mechanisms on the efficiency of public spending in the context of developing countries in general and a sub-Saharan African country, Cameroon, in particular.

The results show that the mechanisms introduced by the programme budget have a mixed effect on the efficiency of public spending.

The study recommends developing the external budgetary controls and introducing internal controls that focus more on performance rather than consistency.

Introduction

The economic growth achieved by Cameroon in recent decades is deemed insufficient to significantly curb poverty. According to Cameroon's National Statistics Institute, the Institut National de la Statistique (2015), although positive, Cameroon's economic growth, which averaged 3.6% between 2001 and 2007 and 4% between 2007 and 2014, fell short of forecasts. Among the factors put forward to explain this underperformance is the low efficiency of public spending 1 (Banque Mondiale, 2018). To remedy these shortcomings, the Government of Cameroon has reformed its public finance system by adopting the programme budget. 2

Previous studies on the programme budget tend to analyse its effects on the rationalisation of public decision-making (Andréani, 1968), allocative efficiency (Craine and O'Roark, 2004) and productive efficiency (Melkers and Willoughby, 2001; Poister and Streib, 1999).

When it was first introduced in the US Department of Defense in 1962, and later in the federal government, the programme budget was designed as an instrument for rationalising public spending (Andréani, 1968; Weber, 1978). By improving the flow of information, this budgetary system solves many problems and also leads to a rationalisation of public decision-making (Andréani, 1968; Hawkesworth and Klepsvik, 2013).

Furthermore, the economic literature shows that programme budgets are conducive to an efficient allocation of resources. Inspired by the theoretical principles of new public management (NPM), the programme budget makes it possible to switch from a logic of means to a logic of results (Gilmour and Lewis, 2005; Jordan and Hackbart, 1999).

In terms of productive efficiency, inspired by the collective choice theory and the incentive theory, the programme budget introduces a budgetary architecture that exposes state preferences (Cho, 2010; Diagne and Faye, 2018; Llau, 2008).

Two observations can be made from the literature review above. On the one hand, to our knowledge, no economic studies exist to date that explore the effect of the programme budget on the efficiency of public spending. Yet, one of the purposes of programme budgeting mechanisms is to increase the efficiency of spending, in particular by linking programme funding to expected results (Pratolo et al., 2020; Robinson and Last, 2009). On the other hand, research on the effects of programme budget mechanisms is still scarce in the context of developing countries in general and sub-Saharan Africa in particular. This paper therefore attempts to address this shortcoming by exploring the effect of programme budget mechanisms on the efficiency of public spending in Cameroon.

The remainder of the paper is organised as follows: the second section presents the literature review, the third section describes the methodology used, the fourth section presents and analyses the results and the fifth section concludes with public policy recommendations.

Programme budget mechanisms: A solution to the problems of bureaucracy and agency to improve the efficiency of public spending

Programme budget mechanisms as a solution to bureaucracy problems

The programme budget has its origins in the budgetary context and the challenges to the effectiveness of traditional public action advanced by both the public choice school (Mueller, 1997) and the new public economy (Laffont, 2000). This is due to the fact that public management is characterised by bureaucratic and discretionary phenomena that encourage the waste of resources, given the absence of instruments to control the opportunism of public officials. To remedy this situation, the programme budget introduces a results-based approach to the State budget through the implementation of a series of measures.

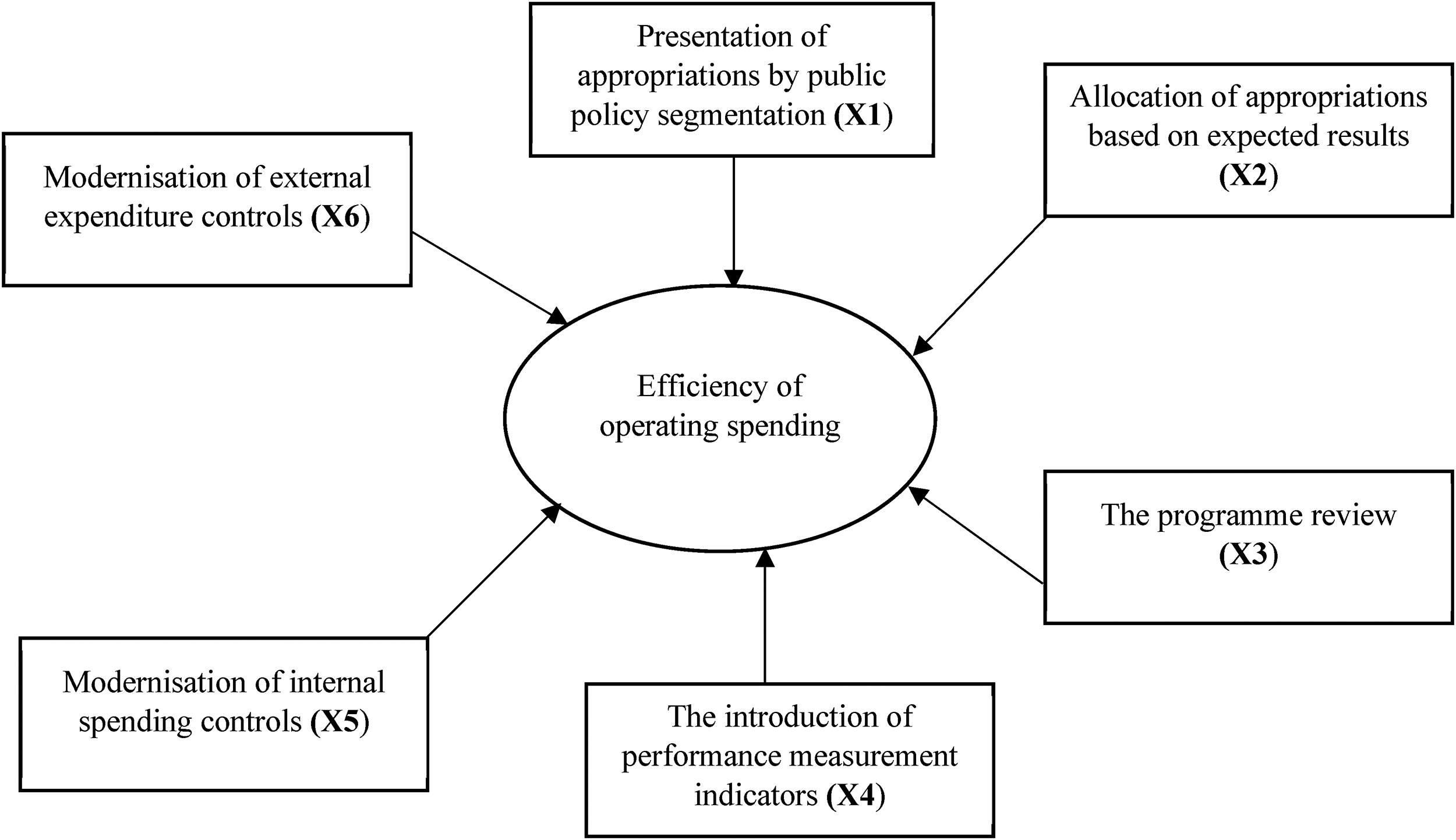

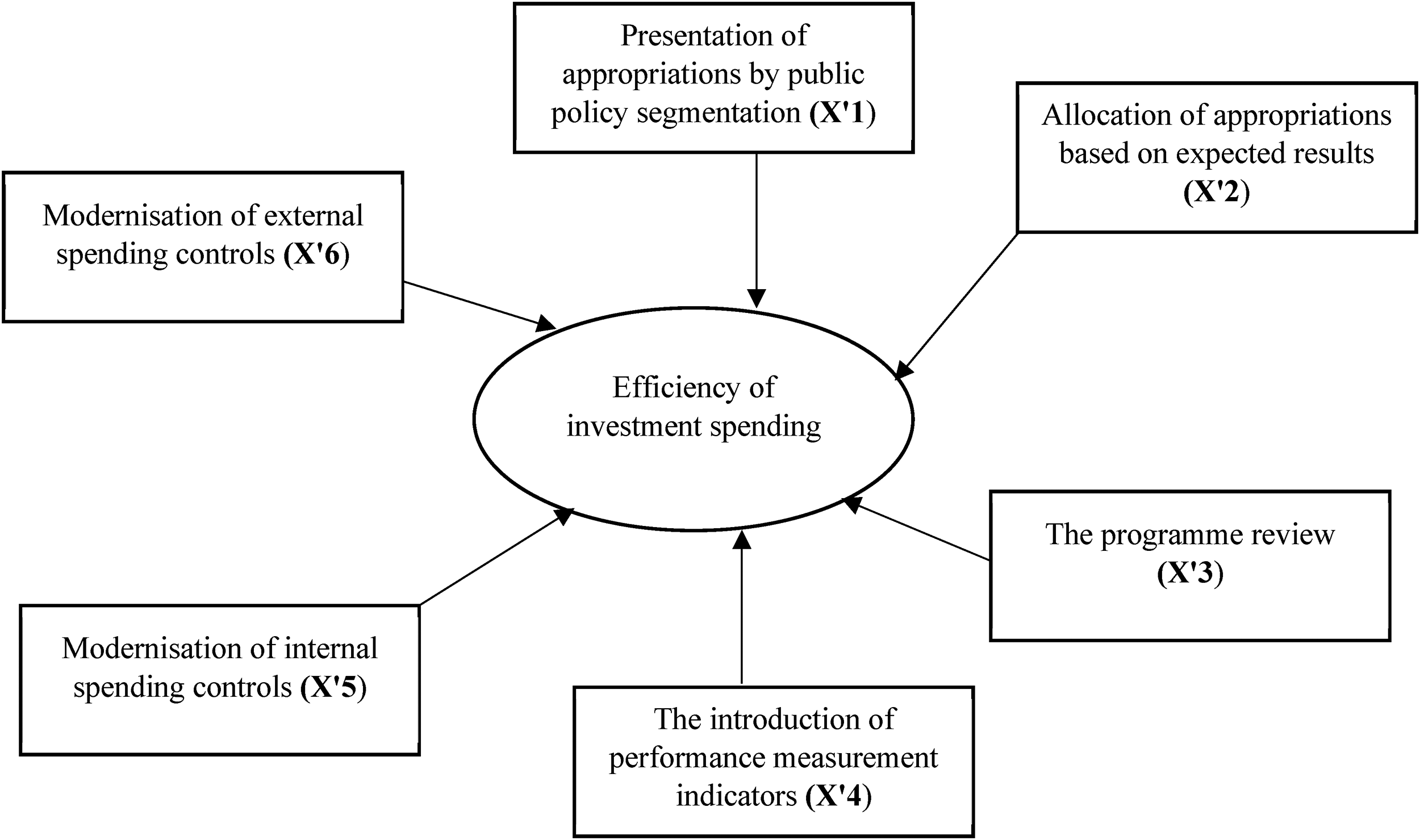

Presentation of appropriations by public policy segment

According to a now recurring formula, the aim of the programme budget is to engineer a shift in State management from a logic of means to a logic of results (Ministère des Finances, 2011). The watchwords of budgetary reform are efficiency and performance in the use of the administration's budgetary resources, with the aim of securing respect for the general interest (Camby, 2002). With the programme budget, appropriations are presented on the basis of their intended use, that is, the purpose for which the spending is incurred. As a result, the old architecture organised around budget headings corresponding to types of spending is be replaced by a new architecture structured around the purposes of the spending (Behn, 2003; Van Stolk and Wegrich, 2008). It is in fact a presentation by segmentation of public policies, the missions constituting the support for public policies and the programmes constituting segments of the latter defined according to an impact (a general interest objective) (Guillaume et al., 2002; Trosa, 2002).

On the basis of these factors, we formulate the following hypothesis:

H1. The presentation of appropriations by public policy segmentation enhances the efficiency of public spending.

Allocation of appropriations according to expected results

Inspired by the theoretical principles of NPM, the programme budget is characterised by a focus on results, considered in terms of efficiency, effectiveness and quality of service (Bouckaert and Halligan, 2008). With the programme budget, budgeting is based, on the one hand, on the segmentation of public policies in order to link the allocation of appropriations to the expected results and, on the other hand, it is focused on the cost of public policies (Banque Mondiale, 2018; Condrey et al., 2001). Policy-based budgeting is based on the allocation of resources according to identified public policies: ‘results-based budgeting articulates budgetary choices around public policy choices (…), it provides an institutional framework and techniques for making trade-offs in the pursuit of several public policies when available resources are limited’ (Holmes, 2000).

On the basis of these elements, we formulate the following hypothesis:

H2. Allocating appropriations on the basis of expected results enhances the efficiency of public spending.

The programme review

The programme review involves exploring possible solutions in order to discover the most effective and therefore least costly way of achieving the objectives pursued. This stage of the programme budget should, in particular, force the various services to no longer consider their activities as ends in themselves, but rather as a means to achieving the objectives set. This implies that they should effectively challenge all activities and play them off against other possible means that may prove more effective (Weber, 1978). This programme review, which some refer to as ‘zero-based budgeting’, is crucial if we are to move away from the practice of making marginal changes to the previous budget, a practice that does not provide for any fundamental revision of the structure of the budget and that focuses budgetary decisions exclusively on marginal changes to the level of previous spending. Programme reviews allow existing programmes to be called into question if they are obsolete (Merewitz and Sosnick, 1971).

These factors allow us to formulate the following sub-hypothesis:

H3. Programme reviews improve the efficiency of public spending.

The introduction of performance measurement indicators

Another way in which programme budgeting has been used to drive performance in the public sector is through the introduction of performance measurement tools (Bevan and Hood, 2006). Indeed, given the economic inefficiency of the public sector, considered as the result of bureaucratic, discretionary phenomena specific to public administrative management, leading to a waste of budgetary resources due to the absence of mechanisms to channel the opportunism of agents, the theoretical corpus of NPM recommends introducing performance measurement tools (Bouckaert and Halligan, 2008). The assumption made by this school of thought is that introducing quantitative performance indicators makes it possible to clarify specific decisions, create benchmarks, determine budget allocations, improve communication and feedback, serve as an input for motivation systems, career development and the promotion of individuals and, finally, make objectives clearly explicit (Askim, 2007; Behn, 2003; Nomm and Randma-Liiv, 2012; Pollitt and Bouckaert, 2004).

These factors allow us to formulate the following hypothesis:

H4. Performance measurement indicators enhance the efficiency of public spending.

Balanced agency relations: Modernising budget execution controls

Programme budgeting is also based on the principal–agent relationship (Folscher, 2007). An agency relationship exists when the principal delegates authority to managers in order to manage an organisation or resources on their behalf (agent) (Jensen and Meckling, 1976). As far as the public sector is concerned, it is also an agency relationship that is established at two complementary levels. On the one hand, parliamentarians represent the people who have entrusted them with a mandate to manage areas of public action on their behalf. On the other hand, Parliament, by passing the Finance Act, delegates to the administration the power to implement public action tools or to manage specific areas within the framework of strategic orientations that have been approved by the electorate (Charreaux, 1999; Jensen and Meckling, 1976). Folscher (2007) also highlights various relational problems between principals and agents that are potentially problematic in the public sphere. The relationship between finance ministries and sector ministries, for example, is generally problematic in this respect, with covert information and actions often persisting (Hou et al., 2011).

The presence of an agency relationship expresses two problems. The interests of the principal and the agent may diverge. There may also be an informational asymmetry between the principal and the agent. More often than not, the latter is better informed than the principal, both about external factors and about actions taken (Charreaux et al., 1987).

Consequently, as soon as an agency relationship is established on a long-term basis, it is necessary to set up instruments capable of guaranteeing that the agents’ actions meet the wishes of their principals (Fama, 1980; Jensen and Meckling, 1976). Therefore, to keep a check on agency problems within the public administration and to ensure that the actions of agents respond appropriately to the wishes of their constituents, the programme budget improves external controls (parliamentary and jurisdictional controls) and internal controls over public spending (Desmoulin, 2004; Lascombe and Vandendriessche, 2006; Robert, 2001; Santiso, 2006).

These elements of the literature allow us to formulate the following two hypotheses:

H5. Modernising internal controls enhances the efficiency of public spending. H6. Modernising a posteriori external controls on budget execution improves the efficient management of public spending.

Methodological approach

Sample and data collection

Mixed methods research was used in this paper, with two different data collection methods. Firstly, we conducted an exploratory study through eight semi-structured interviews with officials involved in budget preparation and execution in the following government departments in Cameroon: a representative of the National Assembly's Finance Committee; an official from the Ministry of Finance's Budget Reform Division; an official from the Ministry of Finance's Directorate General in charge of the Budget; an official from the Public Investment Programme Directorate of the Ministry of the Economy, Planning and Regional Development; two directors of general affairs from ministries with portfolios; two deputy budget directors from ministries with portfolios. These interviews, which took place between 6 and 17 March 2023, lasted an average of 1 hour. The topics covered in this guide are presented in the Appendix.

To process the data from these semi-structured interview guides, we used thematic content analysis as defined by Paillé and Mucchielli (2021), which enables us to identify and examine the effect of programme budget mechanisms on the efficiency of public spending.

At the end of this exploratory study, a survey questionnaire was drawn up and randomly administered to performance stakeholders 3 in the central services of 29 ministerial portfolio departments in Cameroon. The choice of these public administrations is justified by the fact that they are pioneers in the implementation of programme budgeting in Cameroon. Since 2013, the budgets of these ministries have been prepared and executed according to the programme model. The questionnaire was administered to 750 people, but only 475 questionnaires were returned fully completed.

The questionnaire had two main sections. The first section aimed to gather information on the ministry (name and size of the budget) and the respondents’ profiles (age, gender, level of education, position and number of years’ experience). The second section aimed to obtain respondents’ perceptions of the effects of programme budget mechanisms on the efficiency of public spending. We based our choice of mechanisms on the literature presented in the second section.

Formalising the model

Our aim is to examine the effect of programme budget mechanisms on the efficiency of public spending. To do so, we draw on Park's (2019) model. This model represents a probit regression expressed in the following probability form:

Effects of programme budget mechanisms on the efficiency of operating spending.

Effects of programme budget mechanisms on the efficiency of investment spending.

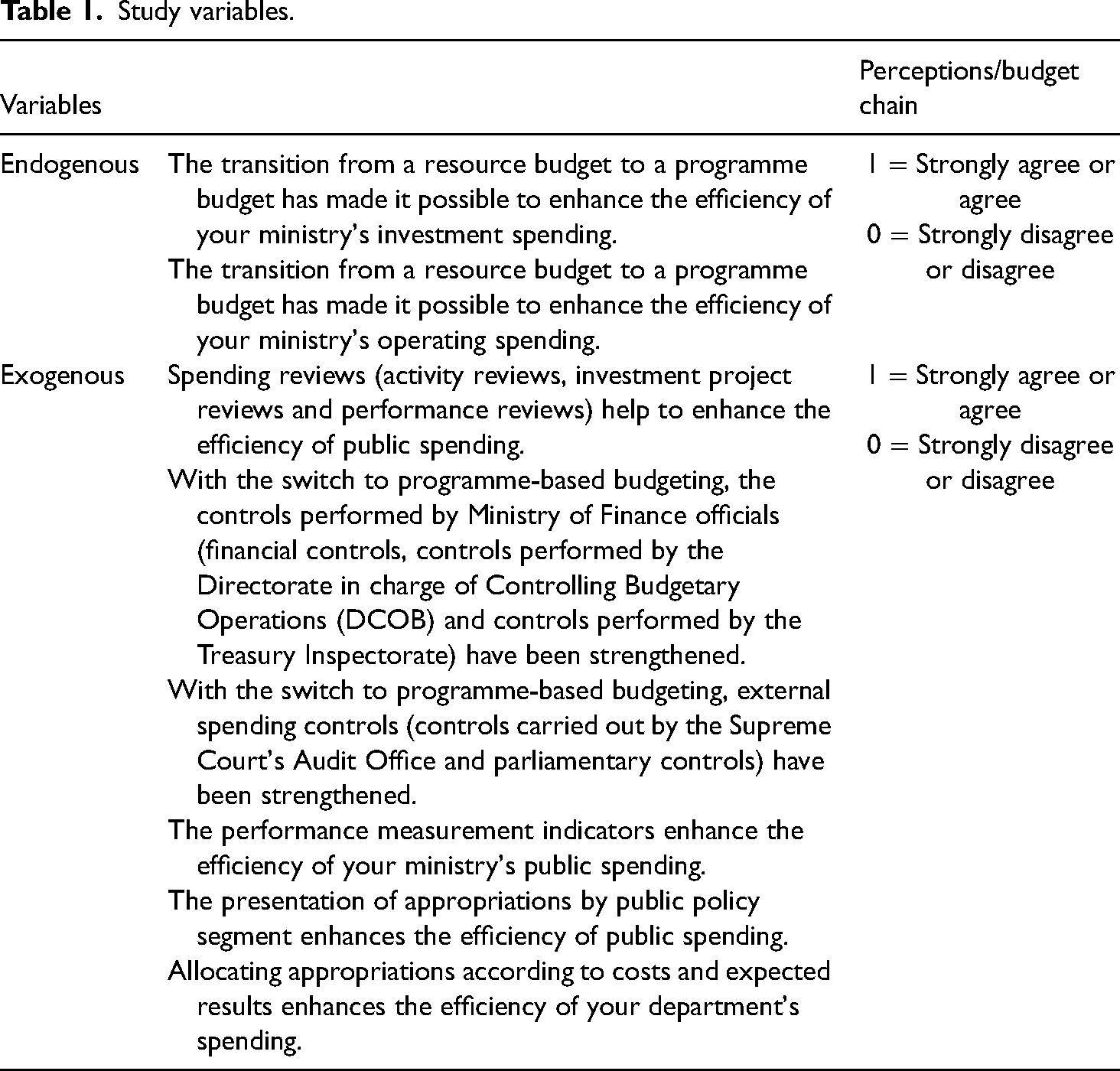

Definition of study variables

In this research, we used programme budget mechanisms as exogenous variables and the efficiency of public spending as an endogenous variable. A Likert scale from 1 to 4 was used to measure responses. In this research, our dependent variable represents the perception of the level of efficiency of public investment and operating spending by performance stakeholders. As public spending is made up of operating and investment spending, our dependent variable will be made up of two indicators. The first represents the level of efficiency of public investment spending. The second indicator refers to the level of efficiency of public operating spending.

The choice of these two indicators is justified by the fact that, in economics, efficiency refers to the ability of a production unit to obtain maximum output from a given set of factors or, conversely, to use as few production factors as possible for a given level of output. In other words, an efficient producer could produce the same outputs with at least fewer inputs, or use the same inputs to produce more outputs. Thus, efficiency can be seen from the point of view of minimising the number of inputs used (input orientation) or maximising the number of outputs (output orientation) (Coelli, 1996). In the light of this definition, we have equated the costs of producing public assets within a ministerial department with the level of efficiency of its operating and investment spending.

Programme budgeting mechanisms refer to one of the modern budgeting approaches, which are systematic approaches to budgeting in public sector organisations, formulated around specific performance and output targets and aimed at improving the effectiveness and efficiency of public spending. These variables were assessed using a questionnaire adapted from Sofyani (2018) and Pratolo et al. (2020). The construction of the programme budget includes six indicators, namely the presentation of appropriations by public policy segmentation; performance evaluation through a programme review; the use of standard cost analysis in budgeting; the introduction of performance indicators; and the modernisation of internal and external spending controls. Table 1 summarises the study variables.

Study variables.

Results

Results of the exploratory analysis

The semi-structured interviews revealed that the programme budget mechanisms have a positive influence on the efficiency of public spending. However, this effect can be improved for certain mechanisms.

Assessing the efficiency of public spending with the transition from resource-based budgeting to programme-based budgeting

The results of the interviews conducted in the field indicate that the transition from resource-based budgeting to programme-based budgeting has improved the efficiency of public spending. In fact, the respondents, in particular (R1, R2, R3, R4, R5, R6, R7), emphasise that the transition from the resource budget to the programme budget has made it possible to enhance the level of efficiency of the investment and operating spending of their ministerial departments in that the purpose of the programme budget is to systematically reconcile the costs and results of the adopted programmes. In addition, they believe that efficiency in the allocation of resources is one of the cornerstones of the programme budget. These verbatim accounts clearly show that the programme budget, by virtue of its purpose and characteristics, considerably increases the efficiency of spending by Cameroon's portfolio ministerial departments, given that they all unanimously agree that ‘the effects are visible in terms of the results obtained during the implementation of programme budgets’.

Performance measurement indicators

The results of the interviews conducted in the field also suggest that performance measurement indicators improve the efficiency of public spending. For interviewees (R1, R2, R3, R6, R8), the ex-ante and ex-post evaluations of public spending, through clear and measurable indicators, make it possible to improve the effectiveness of public action. In other words, the improvement in the efficiency of public spending thanks to performance measurement indicators is indisputable. Interviewee (R5) rightly states that: To date, it can be said that these instruments have helped to change the behaviour of civil servants, not only through the evaluations that are generally carried out, but also through the ratings that are often made public. As a result, each programme manager is required to perform a self-evaluation on a regular basis.

However, much remains to be done as, according to interviewee (R5): ‘Some of the results indicators used do not provide sufficient information on the activity of the programmes, while others only partially describe the performance of the State's action’. Similarly, for interviewee (R7): ‘Some indicators are not relevant because statisticians had no real say in their design’.

The programme review

The first step when drawing up the programme budget is to carry out a review of each programme. This review is used to assess the achievements of the previous financial year, to evaluate the relevance of the activities budgeted for the current year, to determine the progress of ongoing investment projects and, finally, to plan the activities to be programmed for the following financial year (N + 1). Respondents generally agreed that the programme review has undeniably improved the efficiency of public spending. In this respect, interviewees (R4, R5, R7, R8) believe that the programme review provides an opportunity to take stock of the attainment of programme and action objectives (values set by indicator), with a view to identifying shortcomings and proposing corrective solutions to optimise programme management.

Allocation of appropriations

The feedback received from the respondents reveals that allocating appropriations according to costs and expected results helps to improve the efficiency of public spending insofar as it is inherently based on a precise and global assessment of the activity to be carried out. In this respect, interviewees (R2, R3, R7) believe that allocating appropriations according to costs and expected results does indeed help to improve efficiency, as it makes it possible to link the budgeting of funds to the results that are to be achieved. However, for respondents (R4, R6, R8), the influence of this method of allocating appropriations on the efficiency of spending is still low. Moreover, they add that, despite the effectiveness of budgetary programming by programme, the majority of appropriations are still allocated on the basis of the structure of the services and not on the basis of expected results. Medium-term financial planning is still at the experimental stage.

Modernising internal controls

With regard to the modernisation of internal controls, two trends can be identified in the light of the interviewees’ comments. On the one hand, some believe that the various internal spending controls are part of the tools used by the programme budget to achieve the best possible results with the resources available (R1, R2, R3, R6, R8). For others, internal controls are more often than not focused on consistency and compliance, with little or no attention paid to performance aspects (R4, R5, R7).

Modernising external controls

The effect of external spending controls on improving the efficiency of investment and recurrent spending in Cameroon is mixed. This observation is confirmed by the comments of respondents (R1, R3, R4, R5, R6, R8). According to these interviewees, the Audit Chamber of the Supreme Court of Cameroon plays its role, but its work is hampered by the fact that its recommendations are rarely followed. What is more, public accountants do very little accountability reporting. This idea is also shared by respondents (R1, R2, R3, R4, R5, R6, R7), who believe that the Parliament of Cameroon effectively carries out its task of voting on the budget review and also makes recommendations. However, this mission of parliamentary control is not yet sufficiently thorough, as the Cameroonian Parliament does not have a department specialising in budgetary research. What is more, parliamentarians do not have enough time to examine the draft budget and vote on it.

The presentation of budget appropriations by programme

The stakeholders interviewed (R1, R2, R3, R4, R5, R6, R7, R8) all agree that presenting budget appropriations according to programme undoubtedly improves the efficiency of investment and operating spending. To this end, they indicate that structuring appropriations into programmes, actions, activities and tasks contributes to achieving the best results with the budgetary resources available in terms of investment and operations.

Results of the quantitative approach

Results of the descriptive analysis

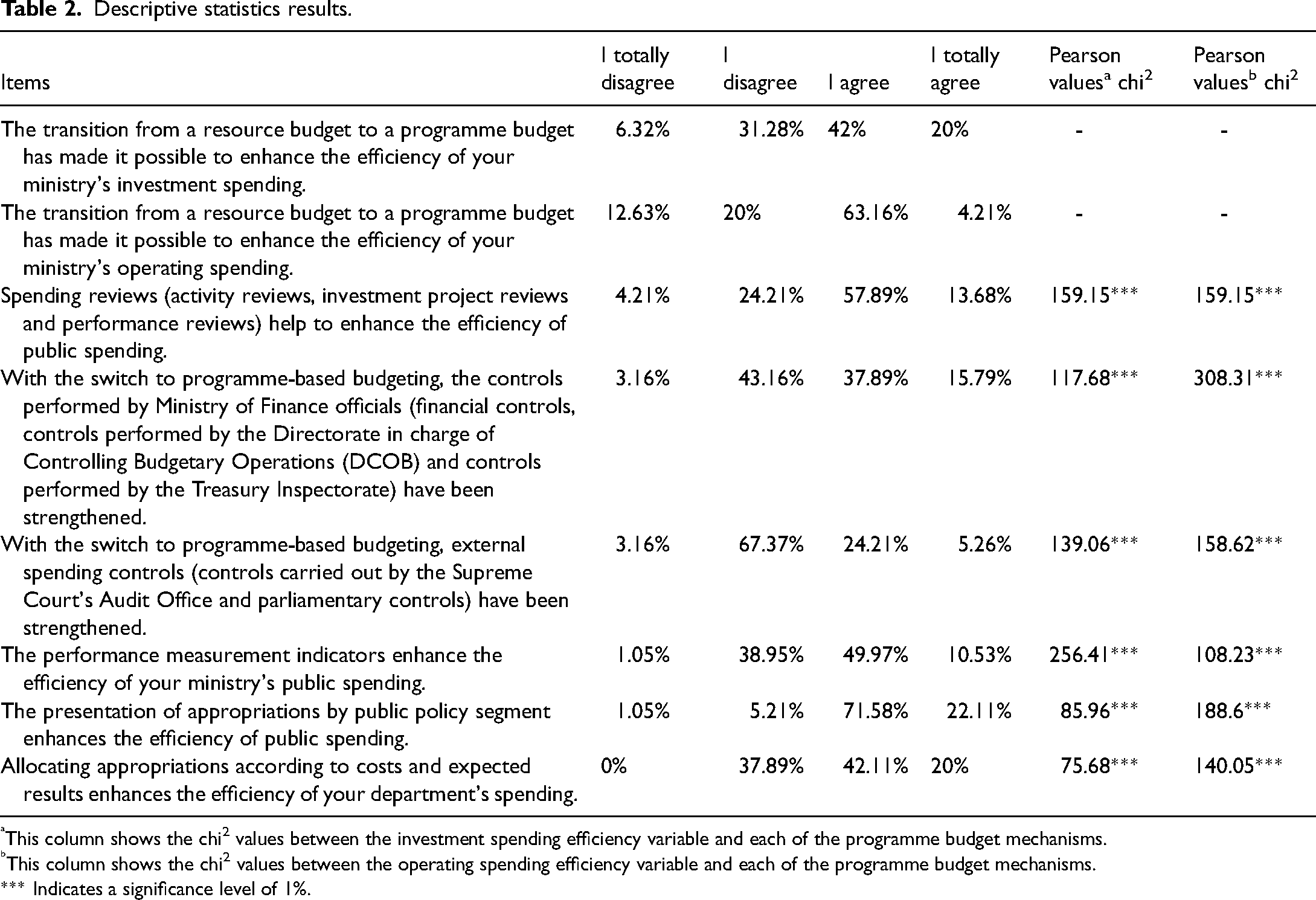

Table 2 shows the results of the descriptive statistics for the study variables. Generally speaking, the majority of actors in the performance chain interviewed consider that, with the exception of external spending controls, the other five programme budget mechanisms improve the efficiency of spending by Cameroon's portfolio ministries. The results of the chi2 test presented in the last two columns of Table 2 reveal an interdependence between the level of efficiency of public spending and each of the programme budget mechanisms.

Descriptive statistics results.

This column shows the chi2 values between the investment spending efficiency variable and each of the programme budget mechanisms.

This column shows the chi2 values between the operating spending efficiency variable and each of the programme budget mechanisms.

*** Indicates a significance level of 1%.

Results of the econometric estimates

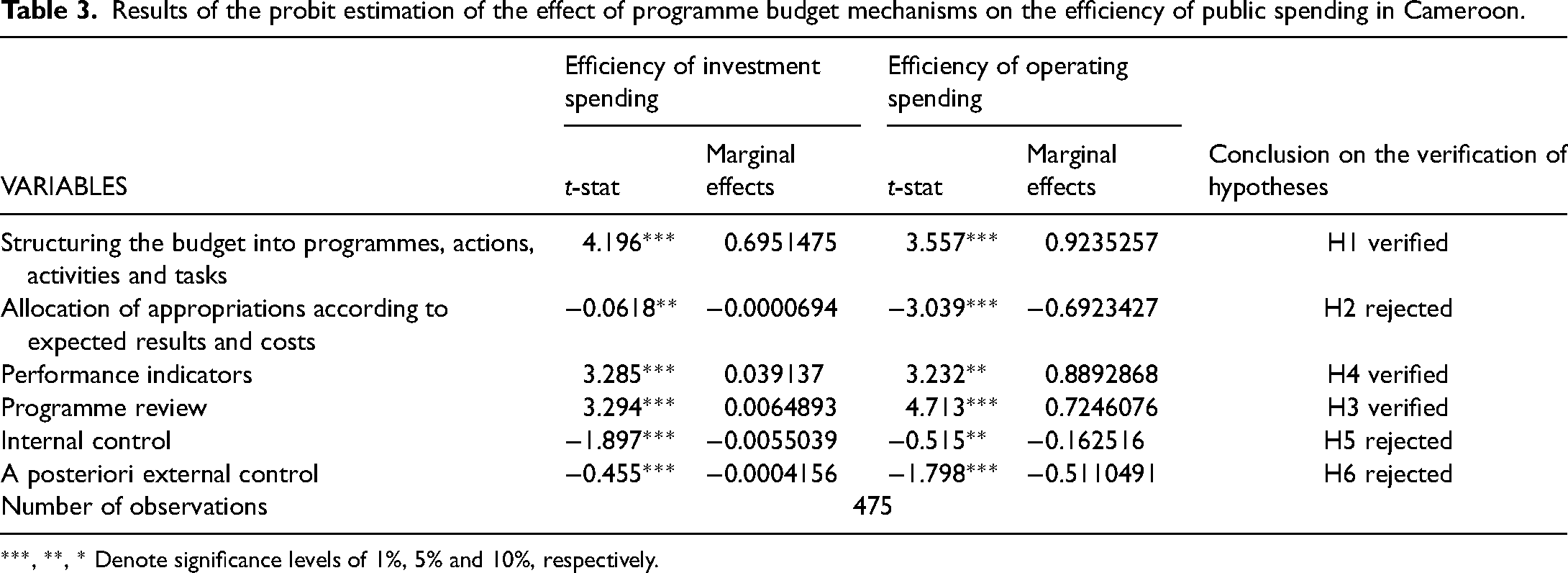

Table 3 presents the results of the probit regression estimates. The estimates of these models are valid, as the validity tests before and after estimation confirm the good quality of the regression. These robustness tests involve the chi2 globality test (first estimate) and the post-estimate significance test (Hosmer and Lemeshow test and classification test). The chi2 globality test, which is the likelihood ratio test, checks whether the model containing the list of predictors represents a significant improvement in the fit compared with the model without predictors. This test indicates a significant improvement over the base model, as the significance threshold of the diagnostic test (c² = 563.41; p < 0.01) is 1%. The Hosmer and Lemeshow test (c² (9) = 9.82) is insignificant, indicating that the estimated model is appropriate for the data and no longer has any variables that could improve its estimation quality. The determination coefficient (R2 = 0.12) indicates that the estimated predictors hold 12.4% of the information in the model. With regard to classification, the regression correctly predicted 72.3% of the responses sought.

Results of the probit estimation of the effect of programme budget mechanisms on the efficiency of public spending in Cameroon.

***, **, * Denote significance levels of 1%, 5% and 10%, respectively.

Discussion of the results

Overall, it appears that the mechanisms introduced by the programme budget have had a mixed effect on the efficiency of public spending in Cameroon. Econometric estimates show that structuring the budget into programmes, actions, activities and tasks has a positive and statistical significance level of 1% on the efficiency of investment and operating spending. This result corroborates the analyses of Camby (2002) and Llau (2008) who, inspired by the economic theory of collective choice, believe that the programme budget introduces a budgetary architecture that clarifies and exposes to a greater degree the definitions of the aims, objectives and missions pursued.

Allocating appropriations according to the expected results and costs of public policies has a negative effect and a statistical significance level of 1% on the efficiency of operating spending and a negative and statistically significant effect on the efficiency of investment spending. This result, which does not corroborate the conclusions of Melkers and Willoughby (2001), means that, in Cameroon the allocation of appropriations is not yet linked to the expected results, nor is it focused on the cost of public policies, as predicted in the literature on programme budgeting.

Performance indicators have a positive effect and statistical significance level of 1% on the efficiency of investment and current spending. This result, which is in line with the conclusions of Askim (2007), Bouckaert and Halligan (2008), Ho (2011), Melkers and Willoughby (2005) and Poister and Streib (1999), suggests that the introduction of result indicators through the programme budget enables the State of Cameroon to instil performance in the public sector.

The programme review has a positive effect and statistical significance level of 1% on the efficiency of investment spending and operating spending. This result, which is consistent with that of Riahi (2007), means that the activity review, the investment project review and the performance review constitute consultation frameworks that, by improving budget preparation, minimise the production costs of public assets.

Internal controls on public spending have a negative effect and a statistical significance level of 5% on the efficiency of investment spending and on the efficiency of operating spending. This result, which contradicts the findings of Wakiriba et al. (2014), could be explained by the fact that, in Cameroon, internal controls are more focused on consistency and compliance and hardly address performance aspects.

External controls on public spending have a negative effect and statistical significance level of 5% on the efficiency of investment spending and on the efficiency of operating spending. This result, which is not in line with the conclusions of Santiso (2006), could be justified by the fact that, in Cameroon, parliamentary controls are not yet thorough, while the budgetary control powers of the financial jurisdiction are still weak.

Conclusion

The aim of this paper was to examine the effect of programme budget mechanisms on the efficiency of public spending. This qualitative and quantitative research in the Cameroonian context reveals that the mechanisms introduced by the programme budget have a mixed effect on the efficiency of public spending. The mechanisms of the programme budget, which are the structuring of the budget into programmes, actions, activities and tasks, the performance measurement indicators and the a priori controls on programme quality, may well have a positive effect on the efficiency of public spending. On the other hand, the allocation of appropriations according to expected results and costs and internal and external a posteriori budgetary controls have a negative impact on the efficiency of public spending.

The study recommends that Parliament's power of budgetary authorisation be strengthened. The legislature should also have sufficient time to examine and vote on the draft budget. As far as internal controls are concerned, we recommend that they be more performance-based. As a result, the ministry in charge of supreme state audit should carry out more performance audits. We have observed that public spending is not yet sufficiently performance-driven. To remedy this, we suggest that the budgetary authorities first define a strategic line, and then the total level of spending.

Footnotes

Declaration of conflicting interests

The author has no conflicts of interest to declare.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Notes

Appendix: Interview guide

Has the transition from a resource budget to a programme budget enhanced the efficiency of your department's investment and operating spending? What impact will the introduction of performance measurement indicators have on the efficiency of investment and operating spending? What is the contribution of the spending review (activity review, review of investment projects and performance review) to the efficiency of investment and operating spending? Does the allocation of appropriations according to costs and expected results enable your department to improve the level of efficiency of its investment and operating spending? Since the switch to programme-based budgeting, have the controls carried out by Ministry of Finance officials enabled your department to enhance the efficiency of investment and operating spending? Since the switch to programme-based budgeting, have external spending controls (controls by the Audit Office of the Supreme Court and parliamentary controls) enabled your ministry to enhance the efficiency of its operating and investment spending? Does the presentation of budget appropriations according to programmes, actions and activities have an impact on the efficiency of investment spending?