Abstract

One of the reasons why many developing countries struggle to provide basic public services to citizens is a lack of tax revenue owing to corruption and illicit financial outflow transfers. Trade misinvoicing is one of the main channels taxpayers use to evade taxes and transfer money abroad, particularly in developing countries. Although scholars have been cognizant of the gravity of corruption, little empirical evidence exists on tax evasion through trade, which is mostly related to the decline of tax revenues in developing countries. To bridge this research gap, this study examines the impact of governance quality and adoption of the Open Government Partnership on trade-related tax evasion in developing countries. Governance quality and open government initiatives are expected to reduce tax evasion by increasing moral cost and transparency, improving the legitimacy of tax burden and tax expenditure. The results show that government effectiveness, regulatory quality, control of corruption, and adoption of open government contribute to combating trade-related tax evasion. Moreover, the government's adoption of an open government moderates the association between governance quality (regulatory quality) and trade-related tax evasion; that is, governance quality significantly impacts reducing tax evasion in countries where open government initiatives are more prevalent. This study holds several implications for leveraging the nationwide adoption of open government, which may directly and indirectly help governments reduce trade-related tax fraud and improve tax revenue.

Points for practitioners

Governance quality and the adoption of open government initiatives effectively reduce trade-related tax evasion.

The impact of governance quality on reducing tax evasion can be enforced by adopting open government partnership.

Introduction

A high level of tax evasion associated with trade can threaten the domestic resource mobilization of a government by reducing the tax base, free trade and investment, and economic growth, and increasing bribery among government officials (Baker, 2005; GFI, 2020). Tax evasion poses a significant development challenge, especially in developing countries, where domestic revenue mobilization is critical for delivering essential public services (Addison et al., 2018; Alstadsæter et al., 2019; Kar and Cartwright-Smith, 2010). Furthermore, trade-related tax evasion harms government institutions (Lin, 2018; OECD, 2014) by diverting funds from public spending and undermining trust in government. Specifically, trade misinvoicing accounts for a substantial share of measurable tax evasion based on trade, amounting to 60% of the total illicit financial flows. According to the 2018 estimates produced by the Global Financial Integrity (GFI) research institute, the trade-related illicit financial flows from developing countries and to all global partners were estimated to be 1.6 trillion USD, likely accounting for 20.14% of total trade (GFI, 2021). However, although trade-related tax evasion is attracting the attention of governments and international development agencies, there exists little evidence or understanding of the means and factors that can effectively regulate such activities (Thiao, 2021).

In addition to a general need for research on trade-related tax evasion, some researchers highlighted the necessity to improve governance quality (Psychoyios et al., 2021) and modernize public services by adopting e-government and open government initiatives (Nimer et al., 2022a; Uyar et al., 2021). The argument also cites evidence that tax evasion is likely to be easier in low-income countries than in high-income countries, where regulatory capacity and the adoption of digital government are high and the risk of being caught is almost certainly greater (Pomeranz and Vila-Belda, 2019). This suggests that countries with high institutional capacity and benefits from open government initiatives place numerous regulations on tax disclosure and transfer pricing (Brandt, 2022), and the effect of such regulatory policy is likely to be enforced by the administrative benefit of open government, which increases moral cost and transparency by allowing access to quality information, enabling the tracking of tax evasion activities and reducing administrative cost. Moreover, the institutional approach argues that institutional quality and open government initiatives increase tax revenue and compliance by providing legitimacy to tax burden and expenditure (Torgler and Schneider, 2009), allowing open participation in policy and law-making processes (Feld and Frey, 2007; Rashid et al., 2022; Yamen et al., 2018). Although these factors are expected to reduce trade-related tax evasion, our empirical understanding of the antecedents of the effectiveness of governance quality and the adoption of open government remains limited (Benkraiem et al., 2021; Bradshaw et al., 2019; Lin et al., 2017). In particular, which specific governance quality and open government initiatives should be employed to reduce tax evasion remains an unresolved issue in developing countries.

This study addresses these shortcomings and contributes to the literature on institutional capacity by examining how governance quality and the adoption of open government, considered as institutional regulatory tools, actively promote effective resource mobilization and combat trade-related tax evasion. In addition, this study enhances the conceptualization of the causal relationship between institutional capacity and tax evasion by using the deterrence model and the psychological tax contract model, which have been underutilized in previous research. A key distinction between this study and prior research (Nimer et al., 2022b; Yamen et al., 2023) is its specific focus on trade-based tax evasion, a significant contributor to the tax base shortage in developing countries. Thus, this study examines how a lack of government institutional capacity and transparency impedes government revenue mobilization and the allocation of funds intended for vital public services and economic development. To answer this question, this study tests not only the effect of governance quality and the adoption of open government partnership on tax evasion but also their interactive effects.

The remainder of this paper is structured as follows. The second and third sections discuss the theoretical framework of the research and derive the hypotheses from the existing literature. The fourth section explains the research model, methodology, and measures for testing these hypotheses. The fifth section discusses and interprets the empirical results of the analysis. The final section presents the conclusions.

Theoretical framework and literature review

Deterrence model and psychological tax contract model

Trade misinvoicing is the largest component of illicit financial flows and is typically used to evade taxes and charges. Therefore, this study examines the factors affecting trade misinvoicing through tax evasion theory. The literature on tax evasion describes it as a complicated process that involves several factors, such as tax authorities, businesses, individuals and their tax-paying behavior. According to Riahi-Belkaoui (2004), the theory of tax evasion includes the deterrence and psychological tax contract models. Theories classify the factors associated with tax evasion into three major categories: taxpayer behavior, tax administration, and governance (Nurunnabi, 2018). The deterrence model argues that taxpayers’ behavior is likely to be influenced by institutional factors, suggesting that favorable governance conditions aid in reducing tax evasion. This model emphasizes a cost–benefit framework and argues that rational taxpayers are more likely to engage in tax evasion when they perceive the benefits of tax evasion to outweigh the expected cost of detection (Allingham and Sandmo, 1972).

The psychological tax contract model explains tax morale as a complicated interaction between taxpayers and the government, arguing that tax compliance is governed by psychological tax contracts between taxpayers and the government (Feld and Frey, 2002). The theory states that taxpayers are prepared to pay taxes honestly, despite the fact that they do not get all of the public service in exchange for their tax payment, so long as they believe the political system to be fair and trustworthy (Feld and Frey, 2007). Thus, government policy, the behavior of tax authorities and institutions influence taxpayers’ morale, and when the political system is fair and the outcomes of policies are recognized as effective, taxpayers are willing to accept the tax burden and comply with their tax obligations. Consequently, governance quality increases perceived fairness and trust in government, which may be associated with improved legitimacy of tax burden and expenditure and tax compliance. In addition, the adoption of an open government increases tax compliance by providing transparency and participation in the policy and law-making processes. This indicates that good governance and the adoption of open government reduce tax-related illegal activities by increasing the moral cost and providing legitimizing tax expenditure. Empirically, several recent studies have provided evidence that the deterrence model and psychological tax contract model are both associated with increased tax compliance, suggesting that power enhances enforced compliance, while trust fosters voluntary compliance (Batrancea et al., 2019; Shim et al., 2023).

Hypothesis development

Governance quality and tax evasion

The term governance refers to the integration of ideas concerning political power, the administration of economic and social resources and the ability of governing bodies to make good policies and carry out their duties fairly, effectively and efficiently (Mishra and Momin, 2020; Smith, 2007). The World Bank incorporated Kaufmann et al.’s (2011) seminal work to define and identify governance indicators across countries. The definition indicates that governance is “the traditions and institutions by which authority in a country is exercised. This includes (a) the process by which governments are selected, monitored, and replaced; (b) the capacity of the government to effectively formulate and implement sound policies; and (c) the respect of citizens and the state for the institutions that govern economic and social interactions among them” (Kaufmann et al., 2011). More specifically, they classified and measured governance in six aspects: voice and accountability (VA), political stability (PS), government effectiveness (GE), regulatory quality (RQ), rule of law (RL) and control of corruption (CC).

Good governance is crucial in the creation of capable states with the capacity to manage public affairs and allocate public resources effectively. The deterrence and psychological tax contract models suggest that increasing governance quality reduces tax evasion by increasing the moral cost of being caught and legitimizing the tax burden. Several studies have presented evidence of a negative relationship between governance quality and levels of tax evasion and the informal economy (Dreher et al., 2009; Psychoyios et al., 2021). Torgler and Schneider (2009) found evidence that all six components of governance reduce tax evasion.

Each component of governance affects tax evasion through specific causal mechanisms. First, the evaluation of GE is crucial for taxpayers as they compare the costs and benefits of paying taxes. If taxpayers perceive that their government is inefficient and wasteful in delivering public services, the probability of tax law compliance decreases. Empirical evidence from several studies shows a negative relationship between GE and tax evasion (Nimer et al., 2022b; Yamen et al., 2018).

Second, exercising the right to vote has a favorable impact on tax compliance, as it increases procedural fairness toward tax laws and tax rates. According to Feld and Tyran (2002), rational taxpayers exhibit greater tax morale and increased tax compliance when they believe that the tax code represents their views and the preferences of the majority. Nimer et al. (2022b) have found a significant negative relationship between VA and tax evasion in developed countries.

Third, PS is another predicting factor, contributing to increased tax morale and decreased tax evasion. Throughout times of political turbulence, taxpayers face uncertainty regarding the costs and benefits of paying taxes. When taxpayers are uncertain about the future, they are more likely to hold cash and postpone their tax duties. Prior research has found a negative relationship between political stability and tax evasion (Nimer et al., 2022b).

Fourth, governments’ RQ, associated with clear and fair regulations, reduces tax evasion by simplifying the tax system and promoting more favorable interactions with the government. A good relationship between taxpayers and the government, established through simple and fair regulations, leads to higher tax compliance. Evidence also suggests that tax complexity is positively associated with higher tax evasion (Awasthi and Bayraktar, 2015; Nimer et al., 2022b).

Fifth, law enforcement and citizens’ commitment to following the RL has a considerable impact on tax evasion. The deterrence model suggests that strict law enforcement and effective tax legislation increase the cost of tax evasion. Wahl et al. (2010) argue for a balanced approach where deterrence power and trust in the legitimacy of authority enhance tax compliance. Therefore, taxpayers avoid complying with their tax obligations if they believe that the rule is unfair or unsupported, or that their avoidance will not result in harsh punishment.

Lastly, corruption increases tax evasion by reducing trust in authorities and providing opportunities for taxpayers to cheat on their tax duties and manipulate tax reports. Torgler and Schneider (2009) argue that tax evasion increases when citizens feel cheated, corruption is pervasive and the tax burden is not utilized properly. Controlling corruption increases the cost of bribery, making taxpayers prefer paying taxes rather than evading them (Nimer et al., 2022b). Thus, this study proposes the following hypotheses:

Open government and tax evasion

As the 2000s began, politicians and policymakers gained a great deal of interest in the concept of open government, anticipating that it would provide numerous benefits, including improved efficiency, decreased corruption, enhanced government legitimacy and increased accountability (Meijer et al., 2012). The concept of “open government” commonly pertains to the integration of technological advancements within the public sector, enabling public access to government-held information and participation in the policy-making process (Park and Kim, 2022). Simply put, open government is a concept that encompasses not only information disclosure, but also the openness of the interaction between government and citizens. Open government initiatives are closely associated with issues of transparency, participation and collaboration, which have also been regarded as the three foundations of ideal open government (Geiger and Von Lucke, 2012; Wirtz and Birkmeyer, 2015). The Open Government Partnership (OGP) is an international partnership initiated by the Obama administration as an extension of the Open Government Directive in 2011. It intends to become a global knowledge network that promotes government openness worldwide through innovation and new technologies (Moon, 2020; Piotrowski, 2017; Schnell and Jo, 2019). The OGP countries have agreed to be more transparent, responsible, and responsive to their citizens. To join the OGP, participating nations must accept a high-level Open Government Declaration, adopt a country-level action plan, and submit a progress report.

Although open government reforms offer various democratic or administrative benefits, there may be differences depending on the focus of each government. Although countries, such as many in Europe, emphasize the economic value of an open government, developing countries often focus on transparency, accountability and citizen participation (Gao et al., 2023). This finding is consistent with Meijer et al.’s (2012) argument that an open government provides incentives for integrity. They stated that open government partnership grants the public the opportunity to observe the use of public funds, curb abuse of power and improve the integrity, transparency and accountability of government organizations by improving the closed culture of government organizations to open ones.

Moreover, e-government applications, usable data, trackable systems and disclosure not only improve public sector integrity but also reduce the shadow economy and tax evasion by increasing the risk of getting caught for government officials and taxpayers engaging in unethical activities. Recent studies conducted at the cross-national level revealed that open government or e-government applications impede tax evasion (Nimer et al., 2022a; Uyar et al., 2021) and the shadow economy (Ajide and Dada, 2022; Sacchi et al., 2022). Nimer et al. (2022a) uncovered that e-government services significantly reduced the level of tax evasion by suggesting that innovative practices within public services produce significant societal advantages. Similarly, Uyar et al. (2021) tested the relationship between e-government and tax fraud, with a focus on the moderating effects of information technological maturity. The result suggests that open government initiatives assist in lowering tax evasion.

Moderating role of open government

The effects of governance quality on trade-related tax fraud are likely to be successful with the nationwide adoption of the OGP. The adoption of open government increases transparency, citizen participation and the government's operational efficiency, which increases the likelihood that those who engage in illegal activities and illicit financial transfers will be apprehended. The higher risk for the discovery of tax evasion provides an advantage to the government in successfully regulating and challenging tax evaders in court, as well as forcing them to obey tax duties. This means that the effectiveness of governance in reducing trade-related tax evasion will be strengthened when governments adopt open government initiatives, given that such initiatives reduce the administrative costs of regulating tax evasion and help government officers access information needed for tracking. Moreover, the benefits of transparency, citizen participation and government responsiveness associated with the OGP increase citizens’ trust in the government, which may encourage them to follow regulations and tax duties.

Veiga and Rohman (2017) argued that the application of e-government will allow the government to cut administrative expenses and enable citizens to report misconduct, all of which may eventually reduce tax evasion. Similarly, Kitsios et al. (2022) stated that open government initiatives allow tax authorities to adopt an e-tax system as an extension of e-government implementation that can improve tax compliance and enforcement. Open government initiatives facilitate governments’ operational efficiency and allow them to benefit from more reliable and accurate information in a timely manner. This indicates that a high level of commitment to open government initiatives enhances governments’ operational efficiency by reducing administrative costs and increasing access to accurate information in trade transactions, this increases tax compliance and revenue mobilization efforts.

The adoption of open government can be discussed individually to understand how it moderates the relationships between the six governance dimensions and tax evasion. First, the adoption of open government plays a moderating role between GE and tax evasion by enhancing government operational efficiency through reduced administrative costs and improved access to reliable information in trade transactions and tax reports.

Second, open government facilitates the impact of VA on tax compliance by enabling more open and wider citizen participation, which reflects the views and opinions of most taxpayers.

Third, the adoption of open government strengthens the impact of political stability on tax evasion by increasing predictability in uncertain times through transparency.

Fourth, open government also strengthens the relationships between RQ and tax compliance by improving the efficiency of the tax system and granting taxpayers with accessible and simplified tax payment processes (Kitsios et al., 2022).

Fifth, open government promotes citizen participation, which is positively associated with citizens’ trust in the government, thereby encouraging taxpayers to abide by the RL and fulfill their tax obligations.

Lastly, the adoption of open government initiatives provides advantages to the government and citizens in controlling corruption by increasing the risk of discovering tax evasion and bribery through accessible and transparent information needed for tracking (Veiga and Rohman, 2017). Therefore, this study suggests the following hypotheses:

Methods and data

In this study, the effects of governance quality and the adoption of open government partnership on trade-related tax evasion in developing countries were investigated. Research data from several sources, namely the GFI, the Worldwide Governance Indicators project, the OGP report and the Center for Systemic Peace Polity Project, were collected. Longitudinal data were collected from 2009 to 2018 for 112 developing countries, which served as the unit of analysis for the study.

Trade misinvoicing is the dependent variable, which is the largest component of measurable tax evasion. Data retrieved from the Global Financial Integrity 2021 report that measured 134 developing countries’ trade misinvoicing from 2009 to 2018 were used. According to the report, the data measurement utilized the United Nations Comtrade bilateral trade database to identify discrepancies or value gaps between what two countries reported having traded. Trade misinvocing happens when importers and exporters misrepresent the reported value of commodities on invoices presented to the respective customs agency to escape tax and customs duties, conceal earnings in offshore bank accounts and illicitly transfer funds across borders (GFI, 2021). The data used in this study were the total value gaps identified in the trade between 112 developing countries and all their trading partners, measured as a percentage of total trade. 1 During the 10-year period, Gambia had the largest average value gap as a percentage of their total trade with all trading partners, at 51.9%, followed by Sierra Leone at 35.4% and Togo at 29.2%.

This study considers the following independent variables: governance quality and open government partnership adoption. To measure governance quality, this study used six World Bank Governance Indicators that evaluate various aspects of governance. The first is GE, which measures the perceived quality of public services, the level of its autonomy from political tensions, the efficacy of policy implementation and the government's credibility in upholding promised policies. Second is VA, which measures the perceived public participation in the process of selecting their governing body. Third, PS measures the perceived probability of encountering political instability or acts of violence driven by political motivations. Fourth, RQ reflects the perceived capacity of the government in formulating and implementing robust policies and laws that enable and facilitate the growth of the private sector. Fifth, RL measures an agent's perceived trust in and adherence to societal laws, including property rights, law enforcement, contract enforcement and the functioning of the judicial system. Last, CC measures the perceived level to which public authority is used for personal benefit (World Bank, 2022). All the six dimensions of governance quality indicators range from approximately −2.5 to +2.5 and higher scores represent a higher level of government effectiveness, accountability, political stability, regulatory quality, rule of law, and low level of corruption.

To measure adoption of open government initiative, this study used OGP data. The OGP was established in September 2011 as an international project with the goals of transparency, accountability, citizen involvement, technology and innovation (Piotrowski, 2017). To join the OGP, a country must sign a high-level Open Government Declaration, present a country action plan, and submit progress reports. In the last 10 years, the OGP has welcomed over 70 new countries. Open Government Partnership membership was used as a dummy variable. Therefore, it was coded 1 when a country joined the Open Government Partnership and remained an active member in a specific year. Otherwise, it was coded as 0.

Several control variables were also considered. First, for measuring the level of democracy, the Polity index updated using the Polity5 project and obtained from the Center for Systemic Peace (Marshall and Gurr, 2021) was used. The Polity index measures concomitant qualities of democratic and autocratic authority in governing institutions. It delineates three categories, ranging from autocracies (−10 to − 6) to anocracies (−5 to +5 and three special values: −66, −77 and −88) and democracies (+ 6 to +10). Special values were coded as 0. Second, GDP per capita (current USD) is the gross domestic product divided by the midyear population, which represents economic development. Finally, population is the country's total population, which measures all residents. The GDP per capita and population data were retrieved from the World Bank dataset.

In this study, the feasible generalized least squares regression was applied for estimation (Greene, 2003; Kmenta, 1986) to account for possible autocorrelation and heteroskedasticity. 2

Results and discussion

Descriptive statistics

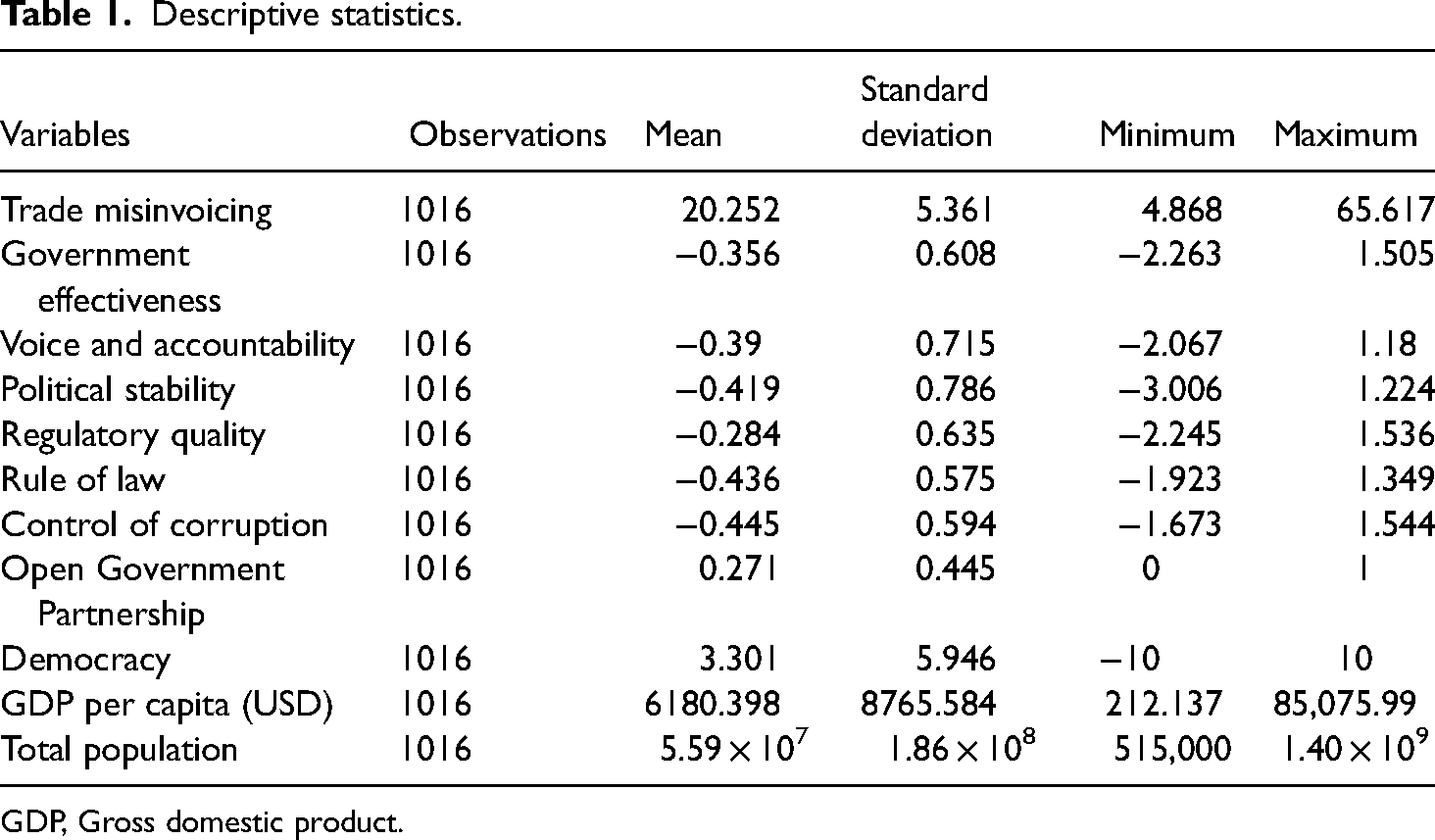

Table 1 provides a comprehensive overview of descriptive statistics. As shown in Table 1, the average trade misinvoicing rate is 20.2% of the total trade, and it increases to 65.6% of the total trade. Based on a rating scale of −2.5−2.5, the means of the six indicators of governance quality are slightly lower than the moderate level: whereas the mean of RL is −0.436, the mean of CC is −0.445, the mean of GE is −0.356, the mean of RQ is −0.284, the mean of VA is −0.39 and the mean of PS is −0.419. The mean count for government partnerships is 0.271. Three control variables were used, which generated the following means: democracy is 3.301, GDP per capita is US$6180.398 and total population is 55.9 million.

Descriptive statistics.

GDP, Gross domestic product.

Empirical analysis

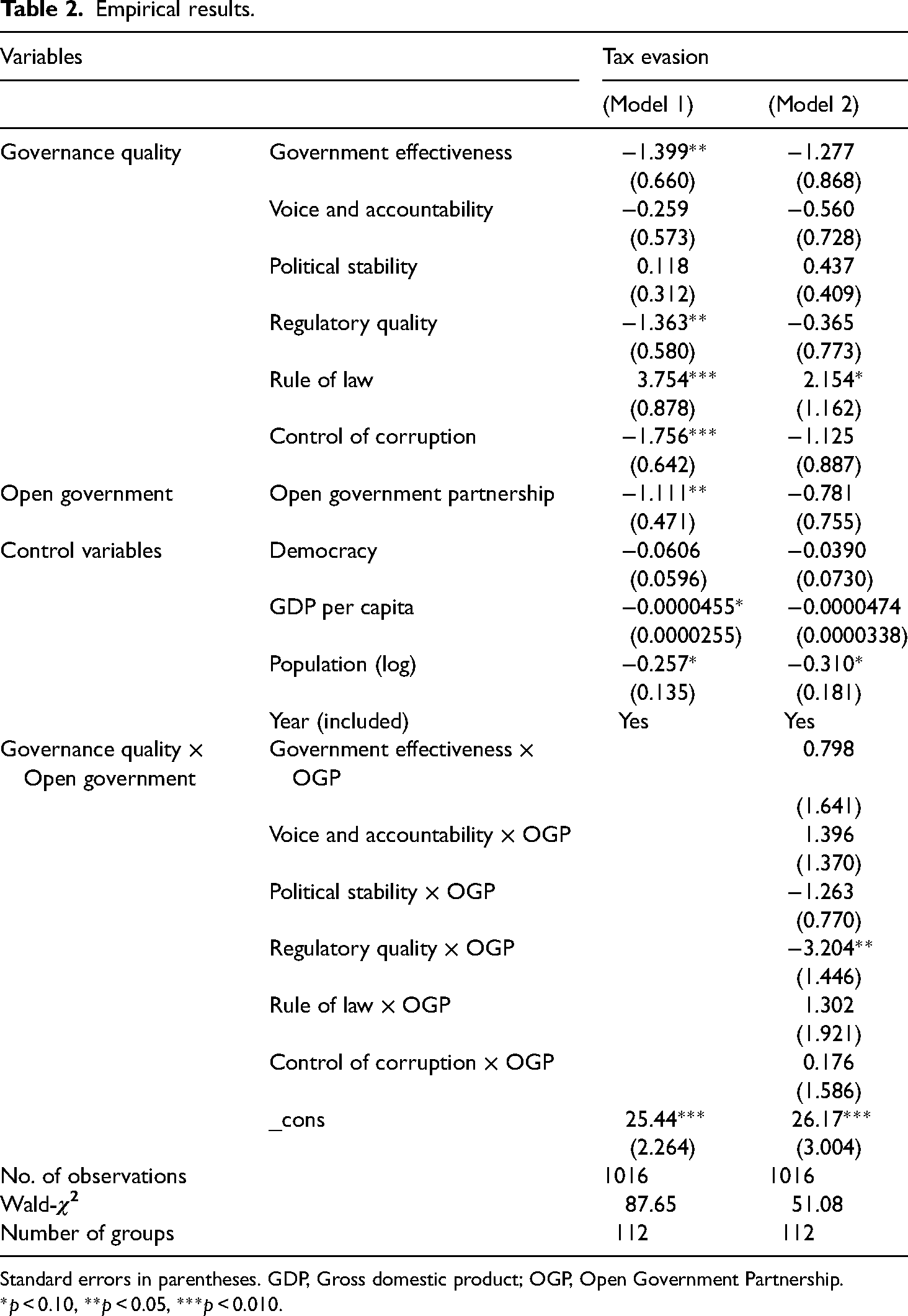

Table 2 presents the results of the panel regression models. This study employed two panel data regression models for analysis. The regression of the basic result is summarized in Model 1, whereas the result including moderation effects is detailed in Model 2. 3 The basic model shows that GE (β = −1.399, p < 0.05), RQ (β = −1.363, p < 0.05) and CC (β = −1.756, p < 0.01) are negatively associated with trade misinvoicing, whereas the RL (β = 3.754, p < 0.01) is positively associated with trade misinvoicing. As hypothesized, the adoption of the OGP (β = −1.111, p < 0.05) reduces the level of trade misinvoicing. Therefore, these findings provide empirical evidence for the validity of four hypotheses, namely, H1a, H1d, H1f and H2a. However, the results fail to confirm the three hypotheses that VA, PS and RL significantly reduce tax evasion.

Empirical results.

Standard errors in parentheses. GDP, Gross domestic product; OGP, Open Government Partnership.

*p < 0.10, **p < 0.05, ***p < 0.010.

The findings imply that developing countries with higher levels of GE, RQ, CC and commitment to open government initiatives are more likely to have increased tax revenues or higher-level resource mobilization. This, in turn, enables these countries to better provide public services and alleviate poverty. Alternatively, this study provides evidence that trade-related tax evasion will decline as developing countries improve their governance by building up their administrative effectiveness, improving regulatory quality, controlling corruption, and modernizing their public services through the adoption of open government initiatives. This finding is consistent with the findings and arguments of previous studies on tax evasion, tax compliance and the shadow economy. The main argument is that countries with higher institutional quality or good governance have effective tools to combat trade-related tax evasion by implementing effective regulations, whereas in countries with lower levels of governance quality, such regulations are less common and have little effect owing to limited administrative capacity (Brandt, 2022; Pomeranz and Vila-Belda, 2019; Torgler and Schneider, 2009; Verdugo Yepes, 2011). The other argument is that effective governance enhances the government's capacity to deliver improved public services to citizens, enhancing government effectiveness, establishing regulations and controlling corruption, and taxpayers feel motivated to fulfill their tax duties and willingly contribute to the payment of taxes (Feld and Frey, 2007; Rashid et al., 2022; Yamen et al., 2018). Contrary to our intention, this study found that the rule of law among governance dimensions had a positive relationship with tax evasion, which is the opposite result from most previous studies. However, some studies argued that an equilibrium is needed, as a strong law enforcement can be linked to complicated and vague tax laws, which can further increase tax evasion (Pickhardt and Prinz, 2014). The findings of this study provide evidence for the arguments of Pickhardt and Prinz (2014).

Moreover, the result validates prior studies’ negative correlation between adopting open government initiatives and tax evasion (Nimer et al., 2022a; Uyar et al., 2021). The main argument is that adopting an OGP increases tax compliance by providing legitimacy to tax duty through transparency and participation. Furthermore, it allows access to usable data and information, increasing the traceability of trade-related transfers and tax payments, leaving little opportunity for taxpayers and government officials to manipulate tax duties.

To explore whether the nationwide adoption of open government partnership moderates the association between governance quality and tax evasion, this study included moderation effects. As reported in Model 2, adopting an open government partnership has a significantly moderated relationship between the one governance quality components and trade-related tax evasion.

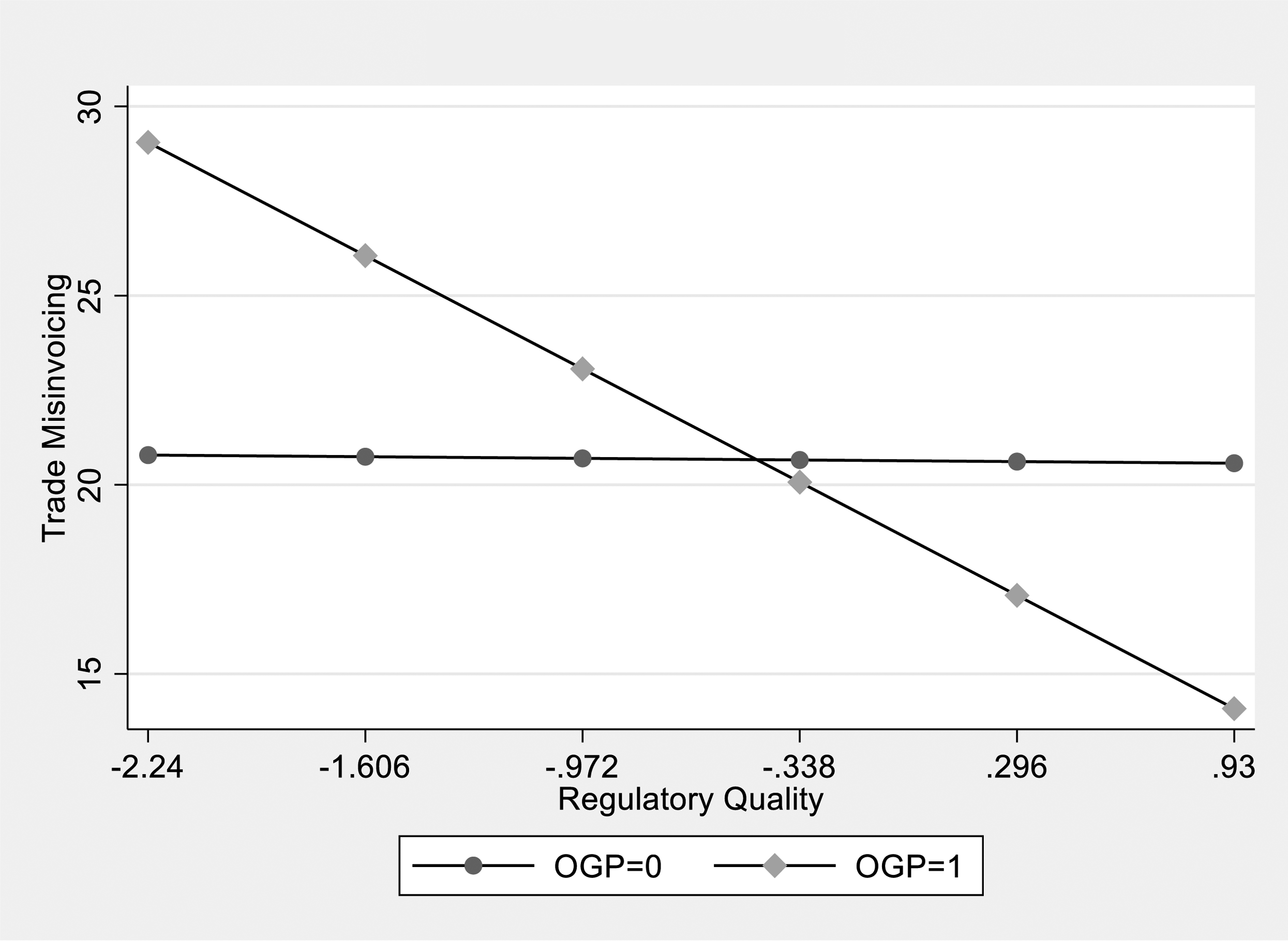

Figure 1 exhibits the moderating effects of adopting an open government partnership on tax evasion. The results show that regulatory quality (β = −3.204, p < 0.05) is probably more likely to have a greater impact on decreasing tax evasion among countries with high levels of commitment to open government initiatives. Therefore, this supports the hypothesis, namely, H3d. On the contrary, the findings from moderation analysis does not support H3a, H3b, H3c, H3e and H3f.

Moderating effect of open government partnership.

The effects of regulatory quality on reducing trade-related tax evasion would be greater in countries where governments adopted open government initiatives and promoted open government practices nationwide. This suggests that the impact of governance quality in reducing tax evasion, the shadow economy or corruption may be enhanced through the benefits of open government initiatives.

Discussion and conclusions

This study examined the effectiveness of governance quality and the adoption of open government partnership as institutional tools to reduce trade-related tax evasion. Using longitudinal data from 112 developing countries, this article aimed to test the impacts of governance quality, open government initiatives and how the adoption of an open government partnership moderates the effects of governance quality in reducing trade misinvoicing.

The results suggest the following conclusions. First, government effectiveness, regulatory quality, and control of corruption have a significant direct impact on reducing trade-related tax evasion in developing countries. These results confirm that institutional quality plays an essential role in reducing the size of trade-related tax evasion by increasing the risk of being discovered and punished through the placement of effective regulations on trade and tax, or increasing the fairness of the institution through reduced corruption and effective policies. This supports the argument that, on the one hand, the quality of the institution affects reducing tax evasion by increasing the risk of being caught when engaging in illegal tax activities, but on the other hand, it reduces the tax evasion rate by strengthening the legitimacy of the tax burden and tax expenditure.

Second, contrary to the assumption, the rule of law has been found to be positively associated with trade misinvoicing, which requires more careful explanation and future analysis. These positive relationships may signify that the hard deterrence approach through one-sided law enforcement increases tax complexity, tax ambiguity and the excessive burden of the need to comply, which, in return, undermines tax compliance (Borrego et al., 2016). The complexity of tax law enables officials to abuse their discretionary authority and corrupt the system. In addition, tax auditors and taxpayers benefit from the tax system's complex rules, ambiguous laws and processes (Ajaz and Ahmad, 2010). This means a balanced approach in the rule of law is warranted to reduce tax evasion.

Third, adopting an open government partnership has been found to be positively associated with a lower level of tax evasion. The countries that adopted the open government initiative agreed to be more transparent, accountable and responsive to their citizens, allowing the public to observe corruption and increasing the government's accountability. Such a mechanism in return increases trust in the government and tax compliance. Moreover, adopting the OGP along with modernized technologies, data disclosure and trackable systems reduces administrative costs and allows authorities to access the quality of information provided by third parties or other authorities regarding tax compliance and trade prices, leaving little opportunity to evade tax duties and manipulate prices.

Lastly, moderation analysis shows that the association between governance quality and tax evasion is negatively moderated by governments’ commitment to the OGP. Specifically, when countries adopted the Open Government Partnership, the impact of regulatory quality to reduce trade misinvoicing was further strengthened. This finding is confirmed by the present study that open government initiatives and digitalization of public services at the national level may enhance the transparency and reliability of the government and increase government tax revenue. Likewise, its benefits on revenue mobilization become greater when the government has a high level of regulatory quality.

This study holds a few noteworthy theoretical and practical implications. First, the finding of the analysis validates the argument that governance quality and open government initiatives are effective regulatory tools for reducing tax fraud. Second, this study reveals that open government has both a direct and interactive effect on tax evasion. In the relationship between governance quality and trade-related tax evasion, open government acts as a moderator, enhancing the effectiveness of regulatory quality in reducing tax fraud. Thus, from a practical perspective, a combined approach that promotes institutional regulatory tools (government effectiveness, regulatory quality, and control of corruption) alongside open government initiatives may prove more effective in increasing tax revenue.

This suggests that governments must first recognize the severity of trade and customs-related tax evasion, which negatively impacts tax revenue and accounts for the largest share of tax evasion. Second, governments should genuinely strive to improve governance quality and maintain a commitment to advancing open government initiatives. Third, to fully leverage the benefits of adopting open government practices, practitioners should design tax systems and policies that facilitate access to and tracking of information while reducing management costs. Finally, policymakers should strive to improve relationships with taxpayers and foster a trustworthy environment. This can be achieved by introducing an effective tax payment and reporting system, rather than relying solely on strengthening power and deterrence to reduce tax evasion.

The study has some limitations that should be addressed in future studies. First, this study used only trade misinvoicing as measure for tax evasion. Incorporating other measures of tax evasion would provide insights into the effectiveness of governance and open government partnerships across different tax evasion channels. Second, this study did not use controlled variables such as the country's level of educational attainment, human development indexes and trade-related indexes, primarily owing to limited sampling. Considering these variables in future studies is important to obtain a more comprehensive understanding of the relationship. Moreover, future research should consider focusing on the effectiveness of revenue mobilization in countries and the accessibility of budget information and processes for citizens from an institutional perspective.

Footnotes

Acknowledgements

I would like to thank Naufal Virindra for assisting with data coding and two anonymous reviewers for their valuable comments and feedback on the paper.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.