Abstract

Supreme audit institutions (SAIs) are a component of a nation's institutional system. This article defines the concept of an institutional anti-corruption system centered on the SAI through four main characteristics: independence, accountability, mandate and collaboration. The article aims to assess the impact that the quality of the anti-corruption system has on perceived levels of corruption. Data from the 2019 International Budget Partnership Open Budget Survey covering 117 countries are used for this purpose. The regression results show that the quality of the institutional anti-corruption system centered on the SAI is associated with a low level of perceived corruption. However, other elements must be implemented to create an anti-corruption environment, such as citizens’ involvement as controlling actors.

Points for practitioners

It is important that policy makers recognize and leverage the potential of SAIs in reducing corruption. Contemporary governance and the complexity of corruption require the protection of SAI's independence, but also call for the establishment of collaborative mechanisms that engage civil society and the media.

Keywords

Introduction

Public finances audit is essential for the financial health of governments. Modern governance requires mechanisms to ensure the effective management of these finances, in order to avoid the risks of usurpation, such as corruption. While responsibility for ensuring the integrity of public finances lies with the supreme audit institutions (SAIs), responsibility for countering corruption goes beyond them. As an inherently chameleonic phenomenon, the fight against corruption calls for a holistic approach. Transparency International has enshrined this approach in its notion of a “National Integrity System”.

The National Integrity System is composed of 11 interrelated pillars or governance bodies, working in synergy to reduce corruption. Most countries have such bodies, which interact on various issues. We refer to this array of pillars and their operating rules, established with the aim of reducing corruption, as the institutional anti-corruption framework.

Several studies show, in broad terms, the important role of political and democratic institutions in reducing corruption. Among others, Stapenhurst et al. (2006) demonstrate the essential contribution of parliaments as law-making and executive oversight actors. Imbeau and Stapenhurst (2019) show that the resource capacity of parliamentary oversight committees is associated with lower levels of corruption. Also, according to Lederman et al. (2006), a long exposure to democracy achieves the same result, as does decentralization (Tchitchoua and Onana, 2020). This paper builds on this literature, but also narrows its scope to a more specific exploration, because the quality of relationships established between the different governance bodies within an institutional framework influences the impact that institutions have on corruption. This, to our knowledge, is neither conceptualized nor measured in previous studies.

The angle of analysis places the SAI at the center of the framework. The aim is to study the impact of the quality of the relationship between the SAI and other governance bodies of a given country on its perceived levels of corruption. Although the contribution of SAIs to the fight against corruption is not unanimous in the literature, they are generally acknowledged to have preventive and detection roles (McDevitt, 2020). To fulfil these roles effectively, Santiso (2006) and Henderson (2019) lay down the crucial nature of the relationships that SAIs should establish with other government institutions or social partners, but also certain principles that need to be respected, such as independence, a clear mandate and cooperation. So what effect does the quality of a SAI-centered institutional framework have on the perceived level of corruption? Answering this question provides a new contribution to anti-corruption strategies, as the Transparency International index shows that corruption is still very much present. We argue that, as the quality of the SAI-centered institutional framework increases, the perceived level of corruption decreases. Based on regression analyses conducted on a sample of 117 countries, the results show that the quality of such a framework has a positive and statistically significant effect on the perception of corruption.

The rest of the paper is divided into five parts. The first part shows the importance of a SAI-centered governance framework to fight corruption. The second part presents the construction of the concept of quality of the institutional anti-corruption framework centered on the SAI and the study hypothesis. The third part presents the methodology and data. The fourth part illustrates the results obtained, which are analyzed in the final part.

A SAI-centered governance framework to reduce corruption

Defined as the abuse of power by public officials for private gain (Dye and Stapenhurst, 1998), corruption is a cancer that undermines development efforts, fuels social inequality and destroys people's trust in their institutions (Park and Blenkinsopp, 2011). It diverts about $132 billion annually from European Union Member States and about $1260 billion annually from developing countries (World Economic Forum, 2019). For more than 30 years, many anti-corruption strategies have been developed, ranging from strengthening legislation and promoting sound public financial management to administrative reforms (Dye, 2007; McDevitt, 2020; Rose-Ackerman and Palifka, 2016). In view of the lacklustre success achieved by these strategies (Gans-Morse et al., 2018), a recent body of literature highlights the role of the SAI in the fight against corruption.

SAIs are not anti-corruption agencies officially tasked with combating corruption. However, theoretical and empirical studies show that SAIs' work has a positive impact on the level of corruption. On the theoretical level, Dye and Stapenhurst (1998) set forth that SAIs have the power to deter public officials from wrongdoing because of the transparency and accountability that audits require. This argument is shared by Dye (2007) and Borge (2001), who contend that SAIs create an environment of integrity through their audits of public finances, and thus help prevent corruption. Chêne (2018) and Kayrak (2008) add that conducting audits allows SAIs to detect corruption, as they have access to all of the documents of the audited organizations. Empirically, Santiso (2006) shows that the audit quality of Latin American SAIs is negatively correlated with corruption. The cross-country study by Gustavson and Sundstrom (2018) shows that a one-point increase in “good auditing” reduces corruption by about four points. Audit quality is dependent on the independence and professionalism of the SAI and the implementation of their recommendations. With statistically significant results, Tara et al. (2016) demonstrate that the existence and volume of SAI audits have a negative effect on the perceived level of corruption, all other things being equal. Finally, Reichborn-Kjennerud et al. (2019) conclude from interviews with SAI members that coercive, normative or mimetic pressures lead to a variation in their role in relation to corruption.

These studies establish the important contribution of SAIs in reducing corruption. However, they do not examine the underlying relational mechanisms of the institutional environment surrounding their work. Specifically, the nature and quality of relations between SAIs and other government institutions are not studied. This is where the “National Integrity System” (NIS) (Pope, 2000) comes into play.

The NIS is noteworthy for three main reasons. First, it addresses the solution to corruption in an institutional approach. It is based on the values of a vigilant society, supported by 11 pillars of governance, and whose goals are sustainable development, respect for the rule of law and improving quality of life. Institutions have a binding power over individuals (Peters, 1999). As corruption is a multifaceted and divergent social phenomenon, institutionalism is a good basis for fighting it. This is corroborated by the adoption of laws and the creation of anti-corruption and monitoring organizations. The NIS is rooted in these values, contrary to Heywood and Johnson's (2017) criticism that cultural factors are not considered. Second, corruption affects all sectors of a nation. The war against it should therefore involve the main institutions, both political and social, as illustrated by the pillars of the NIS. Third, given the complex nature of corruption, reductionist analyses (e.g. focusing on types of corruption) are useful, but insufficient. The NIS provides a systemic response, as it is based on the principle of interdependence of the pillars. After the criticism on the lack of evidence of this interdependence, Heinrich and Brown (2017) compiled evaluations of 38 NISs and show that the interdependence of the pillars is positively correlated with the control of corruption. The application of the NIS therefore brings about positive results. However, while all governance bodies play key roles in the fight against corruption, SAIs are the “linchpin of a country's integrity system” (Langseth et al., 1999). In fact, whatever the type of SAI – parliamentary, judicial or collegiate – it is governed by rules of operation, and is part of a system of relations with the other pillars of the NIS that we the call “SAI-centered institutional anti-corruption framework”.

The SAI-centered institutional anti-corruption framework: construction of the concept

The construction of a concept requires two basic operations (Bélanger and Daigneault, 2021): identification of its fundamental characteristics and their logical linking. Inspired by Jacob (2005), the institutional anti-corruption framework is defined as the set of measures taken in a given state, in terms of organizations and their operating rules, with the aim of reducing corruption. The SAI-centered institutional anti-corruption framework (hereafter IACF/SAI) places the SAI at the center of the framework, and is concerned only with the operating rules between the SAI and the other organizations in the framework. Building on the NIS, four attributes of the IACF/SAI are identified: independence, accountability, mandate and cooperation.

Independence

This means freedom from all forms of influence, whether functional, organizational or financial (INTOSAI, 1998). Supreme audit institutions cannot carry out their work objectively and effectively without independence. The Lima Declaration calls for the establishment of the SAI to be enshrined in the constitutions of states in order to guarantee this independence. In addition, the mechanisms for appointing officials, the freedom of choice of missions or the allocation of the budget are other indicators of independence. Notwithstanding the other bodies, the SAI should be independent of the Executive. There are examples of how the Executive can undermine the work of the SAI by starving it of resources (Kpundeh and Dininio, 2006).

Accountability

This refers to the obligation to answer for one's actions before an entity that has entrusted you with a mandate (Bovens, 2007). Regardless of the type of SAI, it is usually required to report to parliament on its operations and on the entities it audits (Flizot, 2003). The accountability of the SAI is a perfect complement to its independence. Among other things, it helps answer the question: who audits the auditor?

Mandate

To carry out its activities and ensure that they have an impact, the SAI works within a mandate defined by national legislation. These laws and regulations define the type of audit to be carried out (financial, compliance, performance, etc.), as well as the scope of coverage of the public administration (ministries, public agencies or types of expenditure subject to audit). The scope of the SAI's mandate has an impact on its ability to curb corruption, including the possibility of auditing sensitive sectors (Khan and Chowdhury, 2007). As auditors of public finances, SAIs should be able to audit the entire public administration and monitor public funds where they are spent. Withholding some public expenditure from auditing increases the risk of corruption (Wang and Rakner, 2005). The boundary with the private sector is also taken into account when the SAI is brought in to audit public procurement contracts. Corruption is very prevalent in this sector (Prebissy-Schnall, 2020).

Cooperation

The SAI's interaction with bodies such as the judiciary, civil society, the media and international bodies enhances its effectiveness within the institutional framework. As such, the judiciary supports the SAI by following up its audits (in case of detection of anomalies of a criminal nature). Regarding civil society, the importance of their implication is shown, for example, in the context of transparency in areas such as public procurement or budgeting (Dye, 2007). The media is a key player in governance. They support SAIs in monitoring public administration and raising citizens’ awareness (Reichborn-Kjennerud et al., 2019). As an international partner in terms of auditing standards and good practice, the International Organization of Supreme Audit Institutions (INTOSAI) plays an essential supporting role.

The quality of the IACF/SAI thus depends on the degree to which the attributes are effectively applied. Depending on this level of application, the IACF/SAI will be of high, medium or low quality. For example, a IACF/SAI will be of higher quality if:

the budget of the SAI is decided by a competent body other than the Executive (independence); a parliamentary committee examines the audit reports submitted by the SAI (accountability); the SAI has the power to audit the whole of government (mandate); the SAI involves civil society in its work, uses the INTOSAI guidelines, maintains relations with the media and receives support from the judiciary when needed (cooperation).

An additive combination of these attributes creates the ideal conditions for a high-quality institutional anti-corruption framework. The attributes have been chosen in line with previous studies such as those of Gustavson and Sundstrom (2018) and Santiso (2006), and the INTOSAI recommendations. Each of the IACF/SAI attributes is important. However, the absence of one attribute does not undermine the existence of the overall framework. Taking the example of Russia or Nigeria presented by Kpundeh and Dininio (2006), the absence of SAI independence does not preclude the existence of an institutional framework in these countries. However, the quality of the framework and its influence on the control of corruption will depend on it. Yet what impact does the quality of such a framework have on the perceived level of corruption?

Hypothesis

The concept of governance promotes a systemic framework in which all stakeholders contribute to the resolution of a collective problem (Chevallier, 2003). In new public governance, the state becomes plural (the existence of several interdependent stakeholders) and pluralist (several processes) in the management of social problems (Osborne, 2010). These logics are equally beneficial in countering corruption. The four attributes of IACF/SAI bring together different stakeholders to solve a collective problem. This gives rise to the following hypothesis:

As the quality of the SAI-centered anti-corruption institutional framework increases, the level of corruption decreases

Methodology

A cross-sectional empirical approach is adopted to test the study hypothesis.

Dependent variable

The dependent variable is the level of control of corruption, as measured by the World Bank's Control of Corruption Index (CCI). It is a better corruption perception index in terms of internal validity, stable over time and highly correlated with the index produced by Transparency International (Chabova, 2017). The CCI is a continuous variable, varying between −2.5 and +2.5: −2.5 indicates a high level of corruption while +2.5 indicates a low level of corruption. The index has been produced since 1996 by the World Bank based on the compilation of several data sources (Kaufmann et al., 2007). We use the CCI for the year 2020.

Independent variable

The independent variable is the quality of the IACF/SAI. It is a variable composed of four sub-variables representing each of its attributes. The sub-variables used are taken from the International Budget Partnership (IBP) database. The IBP conducts an Open Budget Survey (OBS) every two years, which aims, among other things, to assess the role of supervisory institutions in opening up the budget process. The 2019 OBS covers 117 countries. The process of obtaining data brings on board civil society or academic researchers, peer reviewers and governments (IBP, 2019). However, aspects related to the collaboration between the SAI and the judiciary, the media or the private sector are not addressed. The sub-variables selected to construct the IACF/SAI are presented in the supplementary research material (Table 1, see online). The use of a single database for the independent variable ensures the consistency of its content.

Control variables

The control variables are those cited by the literature as having demonstrated their impact on the level of corruption. Ernst (2020) shows a correlation between the level of economic development and corruption. To control for this factor, we use the 2019 gross domestic product measured by the World Bank. Secondly, several studies show the importance of women in government in reducing corruption. A 10% increase in female representation in parliaments reduces corruption by 1.58 according to Esarey and Schwindt-Bayer (2019). We use the percentage of women in parliaments to control for this factor, 2019 data produced by the Inter-Parliamentary Union. Political stability and respect for individual freedoms are essential for reducing corruption (Lederman et al., 2006), and for engaging civil society (Khan and Chowdhury, 2007). These elements are assessed using the World Bank's 2019 governance indicators: Voice and Accountability; Political Stability; and Respect for the Rule of Law. Finally, the ability to read and write is necessary for a population to interact with its government. This factor is controlled for by the literacy rate, as measured by the United Nations Educational, Scientific and Cultural Organization. In the absence of a recent measurement, we use the 2017 literacy rate.

Empirical strategy

The empirical process takes place in three stages. In the first, we perform a factor analysis using the selected OBS variables to ensure the reliability of the construction of the concept. This is done by constructing an additive scale. In the second step, we investigate the bivariate relationship between IACF/SAI quality and the perceived level of corruption. The last step is a multivariate study using multiple linear regression with respect to the nature of the variables.

As the institutional framework focuses on SAIs, the presentation of descriptive statistics uses the SAI as the unit.

Results

Quality of the SAI-centered institutional anti-corruption framework

The factor analysis performed on the quality of the IACF/SAI is reliable. The three reliability indicators are effective: a Cronbach's alpha greater than 0.6; factor loadings greater than 0.3; and the variance expressed by the first eigenvalue greater than 1. The IACF/SAI quality of each country takes a value between 0 and 100. To facilitate the categorization of countries, we have established a three-range scoring system: 1 a low-quality IACF/SAI is scored between 0 and 49; medium quality between 50 and 75; and high quality between 76 and 100. Removing the missing data results in a final sample of 114 countries, of which 12% have a high-quality IACF/SAI, 39% a medium-quality and 49% a low-quality IACF/SAI (Table 2, see online).

The analysis shows that 48% of the sample has a SAI that is independent of the Executive branch in setting its budget. Accountability to parliament is on average respected by 47% of SAIs. On average, 67% of SAIs have a mandate that allows for all three types of audit and coverage of the whole of government. These findings are in line with the results of the INTOSAI survey presented below. Finally, only 38% of SAIs have formal mechanisms for citizen participation in their audit processes.

Relationship between IACF/SAI quality and level of corruption

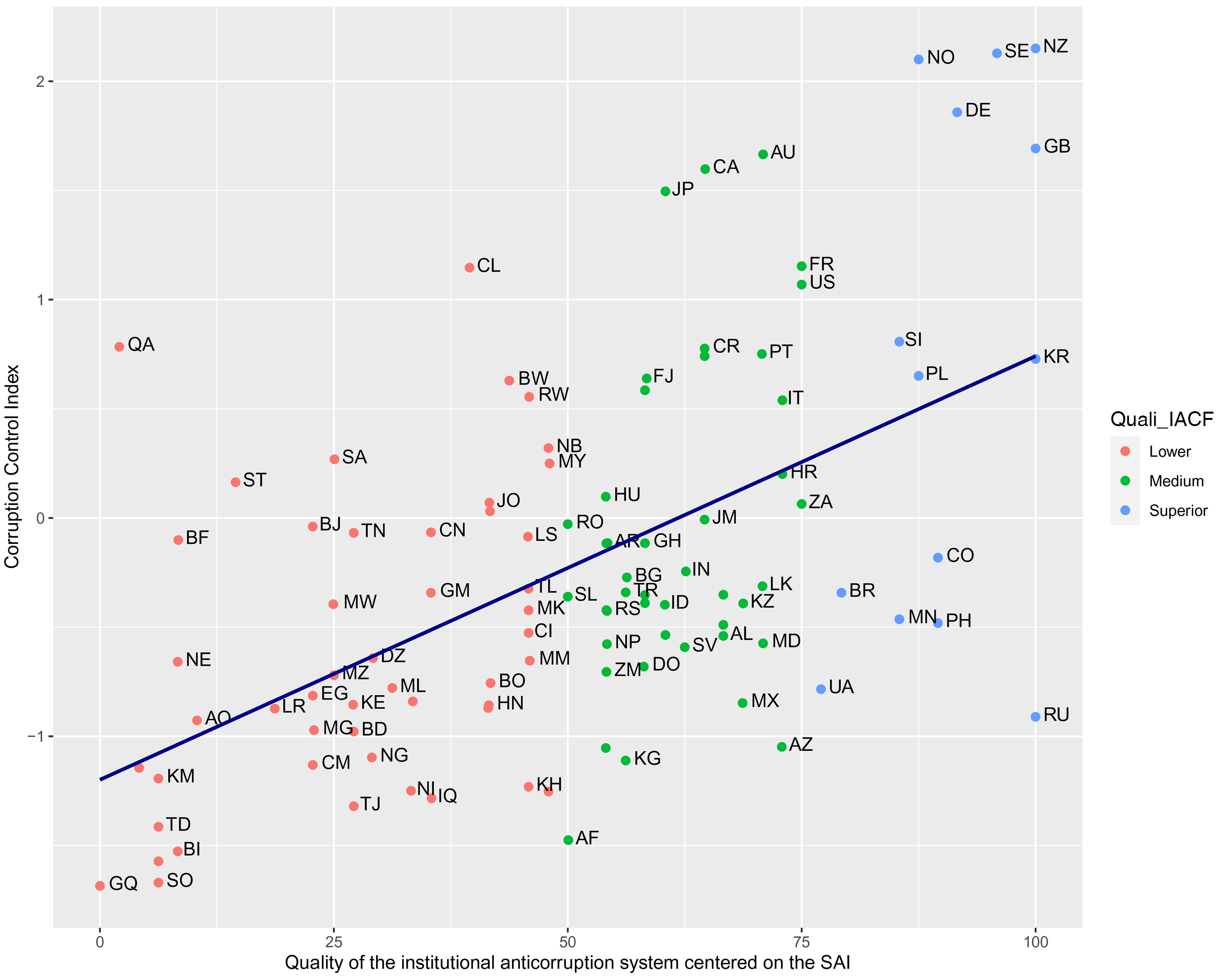

The correlation between the quality of the IACF/SAI and the CCI is positive and stands at 0.55. At the left and right ends of Figure 1, countries with a lower quality IACF/SAI have a higher level of corruption, while those with a higher-quality IACF/SAI have an irregular level of corruption. This irregularity requires the combination of additional factors that can explain the level of corruption.

Relationship between the quality of the institutional system and the level of corruption.

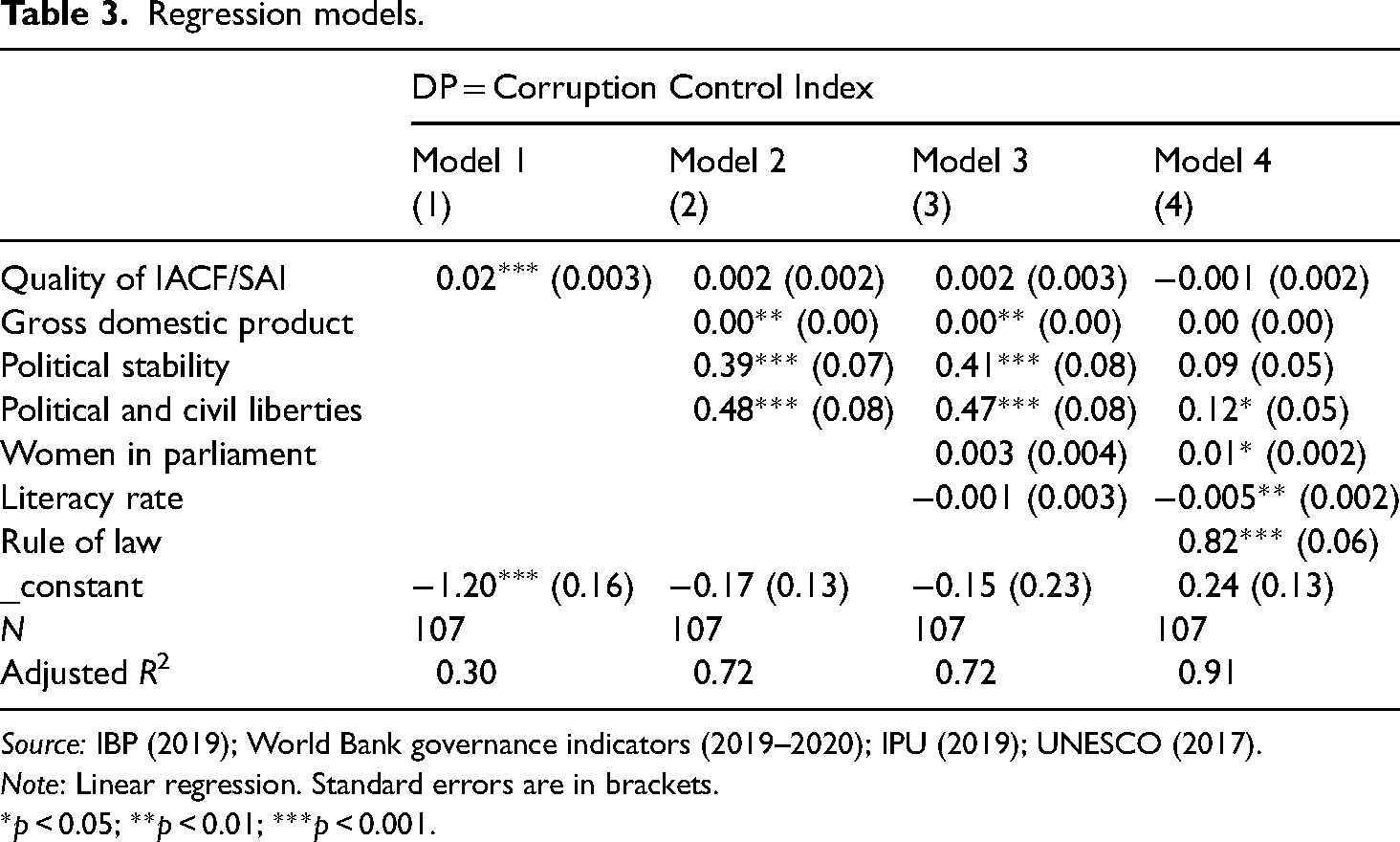

Table 3 presents four regression models analysing the relationship between IACF/SAI quality and the level of corruption. Model 1 shows a significant relationship (p-value < 0.001) between the two variables. An increase of one quality unit in IACF/SAI reduces the level of corruption by 0.02. However, the model has an explanatory power for variability of 30% (adjusted R2). Controlling for other variables, the economic level measured by GDP is significant (p-value < 0.01) in both model 2 and model 3. However, its degree of influence on the variability of the level of corruption is reduced (coefficient equal to 0.00). The absence of violence and respect for political and civil liberties, on the other hand, are contributors to the reduction in the level of corruption by 0.39 and 0.48 in model 2 and 0.41 and 0.47 in model 3 respectively. The presence of women in parliament in model 3 contributes to the reduction of corruption by 0.003. The surprising effect relates to the literacy rate, where an increase of one point leads to a reduction in the CCI of 0.001. One would tend to expect that increased literacy skills would lead to a better understanding of the political system, and hence to a reduction in corruption. Compliance with the rule of law reduces the level of corruption by 0.82, which is significant at 99%. However, this, in model 4, invalidates the study hypothesis.

Regression models.

Source: IBP (2019); World Bank governance indicators (2019–2020); IPU (2019); UNESCO (2017).

Note: Linear regression. Standard errors are in brackets.

*p < 0.05; **p < 0.01; ***p < 0.001.

Analysis of the results

The analysis covers three main findings drawn from the results: compliance with standards, improved quality of parliamentary-type IACFs/SAIs and the combination of means to reduce corruption.

SAI operating standards are not met

The results show that 88% of the countries in the sample have a low- or medium-quality IACF/SAI. This means that the principles of independence, a clear mandate, links with the government and parliament or the clarity of the scope of control of the public administration are not fully applied. These principles have been enshrined since 1977 in the INTOSAI Lima Declaration, to which the SAIs of more than 195 countries have signed up.

According to the INTOSAI report (2020), almost all SAIs (99%) have a legal framework to carry out the three traditional types of audits, 61% table an annual report in parliament and the scope of audit coverage varies. The report reveals that 48% of SAIs are not financially independent, 38% report interference in the choice of their missions and 65% do not communicate with citizens.

Citizen involvement is the aspect of IACF/SAI quality that needs further improvement. Any democratic country should recognize the people as the principal of government action (Gustavson and Sundstrom, 2018). However, considering the resources it requires, the implementation of mechanisms to engage civil society in the work of SAIs should no longer be considered only as good practice. It should be an integral part of any political system. Current digital developments could be used to this advantage, as an informative tool and a means of collecting citizens’ opinions, but also as a means of disclosure (Park and Kim, 2020). Some SAIs already do this, such as the Auditor General of Quebec. 2

Implementing the principles of the Lima Declaration would be an effective way of improving the quality of the IACF/SAI. However, this work cannot be done by the SAIs alone. It requires a commitment from all parties involved (executive, parliament, judiciary, public administration, society, etc.), as part of a real political will for change. Depending on the societal evolution of each country, this change will take more or less time, as it requires human, material and financial capacities, but above all a change in the political and administrative cultures in which the institutional frameworks are embedded. The majority of countries have a SAI for the audit of their public finances, with heterogeneous operating principles. Notwithstanding the contextual differences, this study shows that the quality of the IACF/SAI has a positive effect on the perceived level of corruption.

Countries with a parliamentary-type SAI have a better quality IACF/SAI

The positioning of countries such as Botswana and Rwanda is noteworthy. Despite the lower quality of the IACF/SAI, these English-speaking sub-Saharan African countries have a lower level of corruption than French-speaking sub-Saharan African countries. The SAIs of these two countries have adopted parliamentary-type operating rules. The results of studies by Blume and Voigt (2011) or Imbeau (2014) confirm these findings, that countries with a parliamentary-type SAI are perceived as less corrupt and more transparent. This position is also true for countries in other geographical areas such as Canada, Austria or Norway, compared with France, Portugal or Italy.

The parliamentary system is seen to be conducive to a high-quality IACF/SAI. In relation to the principle of independence, for example, the INTOSAI report (2020) states that 100% of the North American 3 SAIs surveyed are parliamentary in nature and have the necessary resources for their audits. This proportion is 84% for European countries, 28% for English-speaking sub-Saharan Africa and 16% for French-speaking sub-Saharan Africa. Similar results are obtained for reporting to parliament, coverage of whole-of-government or the publication of reports. However, there are other factors that complement this finding. For example, Rwanda is the country with the highest percentage of women in parliament in the world (IPU, 2019). These findings are also confirmed by the regression results. However, one question that emerges from this analysis is why countries with parliamentary systems have an institutional framework that favours the implication of different actors in solving public problems. One potential answer is the interlocking of the Executive with the Legislative.

In the parliamentary system, the population votes for members of parliament and the Executive simultaneously. The Executive, which is formed by the parliamentary majority, is accountable to parliament. The principle of accountability is emphasized. Thus, the individual who voted for a member of the government may find their interests represented in the law proposal and enactment circle (parliament); and, with a little more luck, these same interests may be found in the policy-making circle (Executive). If the individual voter is active in a civil society organization supporting a particular cause – depending on the degree of openness of parliamentarians, the rules of lobbying and the collaborative mechanisms in place – that cause is more likely to be heard. Despite its imperfections, the parliamentary system establishes an a priori collaboration from the electoral base to the political summit, unlike the presidential system where the strict separation of powers is certainly beneficial, but does little to encourage this sharing. It should be noted that the presidential system also offers the possibility of collaboration. Jurisdictional SAIs, which are mostly found in countries with a presidential or semi-presidential regime, have a close relationship with the judiciary. In France, for example, the SAI called Cour des comptes has a public prosecutor attached to the Court, which facilitates the referral of cases of corruption and other matters to the criminal courts.

The quality of IACF/SAI is insufficient to counter corruption

Figure 1 shows that countries with a lower quality IACF/SAI have a higher level of corruption, while countries with a higher quality IACF/SAI have a scattered level of corruption. While the overall effect is positive, there are disparities on both sides.

Countries with a lower quality IACF/SAI such as Chad, Equatorial Guinea or Somalia are ranked 160th, 174th and 179th (out of 180) respectively in the Corruption Perceptions Index 2020. Although significant, the regression results showed that the level of economic growth has little impact. From this perspective, the difficulty of these two French-speaking sub-Saharan African countries is not necessarily related to their economic level, but rather to governance mechanisms such as the transparency of government activity, the accountability of public officials or the quality of natural resource management. Weak institutions are one of the main causes of corruption prevalence in developing countries (Imbeau and Stapenhurst, 2019). The importance of financial transparency is even more important when the country is highly dependent on natural resources (Imbeau, 2014). Thus, the absence of these oversight mechanisms, for which the SAI serves as guarantor, leads to an inadequate allocation of resources and a proliferation of corruption. Corruption cases in Equatorial Guinea, for example, are mostly related to political figures and the management of oil revenues. In excessive cases such as Somalia, political instability contributes to deterioration of the social and economic environment because of wars. The quality of the institutional anti-corruption framework can thus be seen as a guarantee of peace.

However, there are some unusual cases such as Qatar. Despite the low quality of its IACF/SAI, its level of corruption is less critical. Qatar is an absolute monarchy. Its governance indicators on transparency, democracy or public participation are not so good. 4 However, unlike some so-called “free states”, its level of corruption is considered low. The country has experienced strong economic growth in recent years through the efficient exploitation of its natural resources. This exceptional case again raises questions about the measurement of corruption, including the use of perception indicators. Indicators for measuring corruption have varied over time, but it is clear that perception indices are still the most widely used. Thus, despite the lack of individual freedoms, Qatar could be perceived as less corrupt because of its economic growth or the degree of satisfaction of Qataris with their government. However, the Qatargate scandal that broke in December 2022 about possible corruption cases involving the country and members of the European Union could justify an image that does not live up to its corruption perception level.

The disparity in results is more pronounced for countries with a higher quality IACF/SAI. The UK and New Zealand, for example, stand apart from Russia, for example. New Zealand ranks first in the Corruption Perceptions Index 2020, with a score of 88 out of 100. Together with the UK, these are countries with a parliamentary-type SAI. Their governance systems are characterized by the principles of transparency, accountability and citizen participation (Mawer, 2006). The World Bank's governance indicators classify them as developed, politically stable countries where the rule of law and individual freedoms are respected. Some of these characteristics are transposable to Russia, notably economic development. However, its level of corruption is higher. Russia scores 30 out of 100 on the corruption perception index, yet it has anti-corruption legislation. 5 The audit chamber carries out audit work, but without real independence (Kpundeh and Dininio, 2006). The lack of independence of the SAI could be compounded by the absence of civil liberties and political rights. 6 Preventing civil society and the media from exercising their right of vigilance deprives the government of oversight actors. Russian governance confirms that the mere existence of anti-corruption laws is not enough. Subject to other explanatory factors, this analysis would be similar for Brazil or Colombia, countries with high IACF/SAI quality and high levels of corruption.

Conclusion

The complexity of the phenomenon of corruption, as reflected in Transparency International's notion of a National Integrity System, requires the involvement of different autonomous and interdependent institutions working together towards a common goal. The IACF/SAI is built on the institutional foundations of the SAI's mandate and its control over the public administration, independence from the Executive, accountability to parliament and the implication of civil society. Using the Open Budget Survey data, bivariate analysis shows that a high-quality IACF/SAI is associated with a low perceived level of corruption. Policy makers should therefore focus on the application of institutional rules that promote a high-quality IACF/SAI such as the involvement of social actors in public financial oversight mechanisms.

However, the effect of IACF/SAI quality on the level of corruption is weak according to the multiple regression. There are two main reasons for this marginal contribution. The first relates to the construction of the IACF/SAI concept. The latter was to consist of the set of rules governing the relationship between the SAI and all other pillars of the national integrity system (i.e. 11 pillars). The unavailability of data reduced the construction of the concept to five institutions. Important indicators are lacking, such as the SAI's cooperation with the judiciary, the media or international actors. This opens up avenues for research to supplement and improve this study, in order to obtain an overall picture. The second reason is the complexity of the fight against corruption as a social phenomenon. Social phenomena are characterized by values and social structures that change and diverge from one context to another. No single factor can capture the whole phenomenon. A high-quality IACF/SAI should be associated with an environment free of violence, where individual rights and freedoms are respected, where citizens are implicated in political decision-making circles, and where the rule of law is applied. This requires a change in social culture.

Supplemental Material

sj-docx-1-ras-10.1177_00208523231155385 - Supplemental material for Public auditing: What impact does the quality of the institutional framework have on the level of corruption?

Supplemental material, sj-docx-1-ras-10.1177_00208523231155385 for Public auditing: What impact does the quality of the institutional framework have on the level of corruption? by Eriole Zita Nonki Tadida in International Review of Administrative Sciences

Footnotes

Acknowledgements

I would like to thank Professors Pierre-Marc Daigneault and Eric Montigny for their comments and their improvements to this manuscript. I am also grateful to Téma Francklin, Mohamed Awal and Yvelin Gansou for their guidance. Special thanks go to the reviewers whose suggestions helped to improve this paper.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.