Abstract

Affordable housing is a pressing political problem that seems to be fueling social unrest among young people. Rising rents, expensive property prices, and stagnant wages leave young adults with few prospects of entering the housing market without intergenerational financial support. In this article, we examine the role of homeownership, housing unaffordability, and intergenerational transfers in explaining welfare preference and voting behavior of young European adults. We propose the emergence of a new growing interest group composed of financially overburdened young renters and mortgaged homeowners whose welfare is increasingly threatened. We bridged HFCS 2017 and ISSP 2016 datasets through statistical matching and used ordered and multinomial logit models to analyze these trends in Belgium, Germany, France, and Slovakia. We find that homeownership polarizes young adults in terms of their welfare support. Housing unaffordability, however, coalesces young homeowners and renters by increasing redistribution support.

Introduction

In Berlin, driven by decades of rising rents and popular discontent, a local referendum passed for the public acquisition of private institutional investors’ properties (Vasudevan, 2021). In Brussels and Paris, young people and workers have taken to the streets to protest rising living costs and inflation (Méheut, 2022). The widespread nature of housing issues, ranging from concerns about affordability and high rents to investors activities, have prompted protests across Europe with affordable housing specifically fueling social unrest among young people. Does this translate to shifts in political preferences and at the ballot box? This article employs a novel synthetic dataset and shows that while homeownership lowers young adults’ welfare support, housing unaffordability coalesces young homeowners and renters, increasing support for redistribution and voting for center–liberal parties. These trends point to emerging generational differences where housing unaffordability visibly influences the young.

The literature connecting homeownership and welfare state preferences is well-established. Research on the housing-welfare trade off shows that social expenditure decreases as levels of homeownership increase (Castles, 1998; Kemeny, 1981). Micro-level studies find that higher housing wealth and affordability are just as relevant as high income in lowering individuals’ demands from the government, with marked country differences given housing regimes characteristics (André and Dewilde, 2016; Ansell, 2014; Paradowski and Flynn, 2015). Nevertheless, the conventional negative relationship between homeownership and welfare preference has recently faced scrutiny, partly due to the influence of financialization 1 and household debt (Van Gunten and Kohl, 2020). In addition, homeownership, housing wealth, location, and unaffordability play significant roles in explaining voting trends and the electoral success of different political parties. Studies indicate that homeowners in areas with high property values and accumulated wealth tend to support right-wing parties due to their rhetoric on lower taxation and homeownership support (André et al., 2018; Ansell et al., 2022; Paradowski and Flynn, 2015). Conversely, regions excluded from housing wealth gains and renters struggling with housing unaffordability often experience resentment and discontent, leading to increased support for populist voting that capitalizes on these grievances (Adler and Ansell, 2020; Waldron, 2023).

The political relevance of housing becomes even more evident given the stark contrast in which young adults experience the housing market compared to older peers (Dewilde and Flynn, 2021; OECD, 2021). A significant body of literature has developed on the generation rent phenomenon, where young generations are locked out of homeownership and increasingly rely on the rental market, mostly due to financial constraints rather than choice (Byrne, 2020; Waldron, 2023). Young adults face cumulative disadvantages: more insecure positions in labor and pension markets, stagnant wages, and limited mortgage credit access (Aalbers, 2016; Forrest and Hirayama, 2018). In this context, young adults’ access to homeownership and housing wealth increasingly depends on intergenerational support, with family transfers accounting for differences in credit access, tenure type, debt levels, property value, and location (Cohen Raviv and Lewin-Epstein, 2021; Flynn and Schwartz, 2017). Consequently, housing wealth is disproportionately concentrated among high-income young homeowners (Dewilde and Flynn, 2021).

Although housing-related challenges are widespread across Europe, they manifest differently according to local circumstances (Hick et al., 2024). While homeownership, housing wealth, and affordability contribute to economic disparities across geographic areas and generations (Arzheimer and Bernemann, 2024; Hochstenbach and Arundel, 2021; Waldron, 2021), housing policies and broader welfare characteristics can counteract such inequality depending on how effectively they address and distribute social risks (Comelli, 2021). Despite some convergence in housing market developments, variations in housing provision and housing outcomes influence the role and meaning attributed to homeownership, shaping political preferences across welfare and housing regimes, and underpinning the current European political debate (André and Dewilde, 2016; Dewilde, 2018).

Following the research connecting housing and welfare and adding to the growing scholarship on housing and young adults, this article explores how homeownership, housing unaffordability, and intergenerational support influence the political preferences of young adults by addressing two research questions: to what extent do homeownership, housing unaffordability, and intergenerational transfers matter for welfare and political preferences among young adults? Moreover, what are the possible mechanisms that could explain such effects? Implied by the original housing-welfare trade off, young homeowners might oppose redistribution to safeguard their wealth. However, young people who are denied entry into the housing market or are overburdened by rising housing costs might demand greater government support through redistribution. Complicating matters, among both young homeowners and renters, the costs to purchase a house or the financial stress related to rent and mortgage payments are lower and less burdensome for those relying on parental transfers. Taken together, we propose the emergence of a growing new interest group composed of financially overburdened younger renters and homeowners whose welfare and living standards are threatened.

In making this argument, we make three research contributions. First, we overcome significant data limitations by generating a novel synthetic dataset through statistical matching of two high-quality micro-level surveys—the Household Finance and Consumption Survey (HFCS) and the International Social Survey Program (ISSP)—allowing for comparative analysis of how homeownership, unaffordability, and intergenerational transfers affect young adults’ redistributive and voting preferences. Second, we examine four countries (Belgium, Germany, France, and Slovakia) that have pursued diverse policy paths and undergone distinct house price, homeownership access, rental market, and wealth accumulation trajectories. These countries represent different types of housing and welfare regimes, with policy relevance and practical implications of our findings that may be applicable to other European countries (Dewilde, 2018; Wind and Dewilde, 2019). Third, given the distinct levels of financialization in housing regimes, generating uneven wealth accumulation between and within generations and distinct levels of affordability, this article offers a comprehensive analysis of housing unaffordability as a fundamental driver of social stratification. In doing so, it advances social class and asset-based welfare theories by connecting housing status to political attitudes of young adults across housing regimes in comparative perspective.

The article proceeds as follows. The first section describes and connects the literature on homeownership, housing unaffordability, intergenerational transfers, and housing regimes to political preferences of young people, outlining the possible mechanisms, and stating the expectations. The second section describes the analytical strategy, datasets employed, variables of interest, and methods. The third section presents the results and discusses the main findings. The final section concludes.

Theoretical background

Homeownership, welfare, and political support: what is the connection?

The role of housing in social stratification and its link to the welfare state recently gained scholarly traction. Theories on the housing-welfare trade off suggest a negative relationship between homeownership rates and welfare spending, originally observed with pensions and further extended to general welfare provision (Castles, 1998; Kemeny, 1981). The mechanism implies that the initial financial burden of homeownership increases resistance to the higher taxes required for funding a larger welfare state, with clear distinctions between unitary and dual housing systems 2 (Kemeny, 2005). Similarly, more recent research emphasizes the implications of Asset-Based Welfare—ABW (Adkins et al., 2022; Doling and Ronald, 2010). ABW policies promote the access and accumulation of assets, mainly through homeownership subsidies, to overcome economic insecurity, build up wealth, and reduce reliance on public welfare policies (Adkins et al., 2021). However, gradual welfare reforms and advancement of housing market financialization have led to a convergence of high welfare and homeownership rates (Tranøy et al., 2020). Such convergence results from prior policies creating new constituencies and shaping expectations on the state’s role, making homeownership subsidy cuts politically costly (Pierson, 2011; Van Gunten and Kohl, 2020).

The link between individual homeownership, housing wealth, and political preferences primarily hinges on economic factors. 3 According to the “Median voter Model,” redistributive preferences rise with growing income and wealth inequality (Alesina and La Ferrara, 2005; Ansell, 2014; Meltzer and Richard, 1981). In addition, pocketbook models suggest that voters assess their financial situations throughout the electoral cycle and vote accordingly (Lewis-Beck, 1985). Perceived increases in housing wealth tend to favor incumbent, pro-homeownership, and mainstream parties, while housing wealth deprivation fuels resentment and dissatisfaction, increasing support for left-wing or populist parties (André et al., 2018; Ansell et al., 2022; Brännlund and Szulkin, 2023).

Existing studies have recognized the influence of homeownership and wealth on individual welfare preferences (André and Dewilde, 2016; Ansell, 2014). For instance, higher housing wealth decreases overall redistributive support (Ansell, 2014). Across Europe, homeowners are less supportive of redistribution, with the effect varying by age, income, and welfare regimes, being more pronounced among younger cohorts and in financialized countries (André and Dewilde, 2016). This is expected because compared to older cohorts, younger homeowners have purchased relatively pricier properties at higher interest rates (Aalbers, 2016; Dewilde, 2020). They are still experiencing the financial strain of down payments, mortgage loan repayments, and moderate expectations of continual asset inflation (Aalbers et al., 2021), which results in increasing aversion to redistribution (Ansell, 2014).

Economic interests that shape welfare preferences also influence political results. The literature typically associates homeownership and wealth with more conservative-right-wing voting (André et al., 2018; Ansell, 2014; Paradowski and Flynn, 2015). More recently, declines in local house prices have been linked to stronger populist support (Adler and Ansell, 2020; Ansell et al., 2022). Homeowners often favor conservative or mainstream parties, drawn by policies that promote lower taxation, expanded credit, and housing deregulation (André et al., 2018). They also tend to reward mainstream parties for perceived wealth gains (Ansell et al., 2022). However, renters are more inclined toward left-wing parties, attracted by their stance on tenants’ rights, rent control, and social and affordable housing policies (André et al., 2018). They may also gravitate toward populism as a response to their relative financial dissatisfaction (Ansell et al., 2022). Yet, this relationship is more nuanced than a simple left-right political contrast. Longitudinal studies indicate a complex process where socialization and anticipation of homeownership influence house purchase decisions (Lersch and Luijkx, 2015). Interestingly, transitioning into homeownership does not necessarily imply more conservative voting (Hadziabdic and Kohl, 2022). Instead, it reflects a process of “embourgeoisement” of homeownership, where wealthy homeowners support both economically liberal policies and left-wing ideological values, boosting votes for New Left parties (Beckmann et al., 2020). In other words, the causal mechanism could be mediated by the educational level and parental background of homeowners (Beckmann et al., 2020; Hadziabdic and Kohl, 2022; Lersch and Luijkx, 2015).

The literature suggests that the generation into which one is born largely determines the housing market they encounter. Therefore, we anticipate generational differences in the relationship between homeownership and support for redistribution due to shifts in market conditions and welfare policies. While all homeowners deal with high upfront costs that decrease support for redistribution (Kemeny, 2005) and boost right-wing voting (André et al., 2018), younger adults face a less favorable housing market in a context of weaker safety nets (Aalbers, 2016; Dewilde, 2020). Because they purchase more expensive properties with higher initial debt compared to older homeowners, potentially intensifying their motivation to minimize taxes and safeguard house prices, we expect young homeowners to present even lower support for redistribution and more right-wing voting.

Housing unaffordability: rising costs, rising risks

While house price appreciation fosters self-sufficiency creating support for welfare withdrawal among homeowners, it also exacerbates wealth inequality and economic vulnerability (Adkins et al., 2022; Ronald and Arundel, 2022). Expanding upon the previously mentioned mechanism related to homeownership and political preferences, recent research incorporates house price variations to understand redistributive and voting preferences (André et al., 2018; Ansell, 2014; Ansell et al., 2022). Ansell and Cansunar’s (2021) study reveals that regional housing unaffordability, determined by increased house prices, 4 lowers the demand for redistribution among homeowners and renters. Yet, the findings are puzzling and the mechanism is not clear. While homeowners directly benefit from housing unaffordability through the wealth generation function of price appreciation, high-income renters may resist income taxation despite higher rents. The effect is mainly induced by homeowners, who constitute most voters in nearly all European countries. However, the authors note that this pattern may not hold for younger renters excluded from homeownership, which could potentially intensify political polarization.

How do these dynamics affect young adults’ political preferences? Rising inflation and housing unaffordability have changed the living standards for many young households (Aalbers et al., 2021; Dewilde, 2018; Greve et al., 2024; Hick et al., 2022, 2024). While overall housing unaffordability remained stable from 2010 to 2018, it has worsened for private renters and young adults (Hick et al., 2024). Young people are disproportionally in poor-quality housing and experience financial stress with minimal savings and meager pension prospects, thereby promoting feelings of social decline and loss (Dustmann et al., 2022; Hick et al., 2022). Factors such as wage and property price/rent mismatches, social housing disinvestment, affordable housing shortages, high urban demand, and prohibitive costs prevent many young people, particularly renters from non-wealthy backgrounds, from living near economic centers (Dewilde, 2022; Le Galès and Pierson, 2019). This situation considerably limits their social mobility and life opportunities (Inchauste et al., 2018; Winke, 2021). It creates a tradeoff where housing costs are lower and affordable, but access to services, jobs, competitive wages, and favorable career prospects are limited (Mohino and Ureña, 2020).

The affordability challenges faced by young households significantly increase their economic vulnerability and risk perception. This is particularly true for renters entering new tenancies or recent homeowners (Hick et al., 2024). For new entrants, house purchase is more expensive and riskier with no capital gains guarantees (Ansell, 2014; Ansell and Cansunar, 2021). In this context, homeownership can shift from a source of security to a burden if mortgage repayments become challenging (Will and Renz, 2023). Moreover, both young homeowners and renters experience similar vulnerability and lower socioeconomic standings due to high housing costs, decreasing mobility, intensifying spatial segregation, and lowering consumption (Brännlund and Szulkin, 2023; Hick et al., 2024; Winke, 2021). Based on this mechanism, we anticipate that affordability issues will increase demand for redistribution and bolster left-wing voting among young people.

Intergenerational transfers and housing regimes: family and state counterbalancing housing market challenges

If housing unaffordability lowers the living standards and opportunities of young households, family wealth and welfare policies counteract the adverse effects of the housing market. From early financial education to economic support or longer co-residence, families possess varying capacities to guide and support their children according to their social class status. These family dynamics, in turn, influence housing outcomes (Cohen Raviv and Hinz, 2022; Flynn and Schwartz, 2017). The financialization trend and the emergence of credit as a private alternative to the welfare state influence individuals’ strategies in navigating financial risks and capitalizing on housing opportunities (Flynn and Kostecki, 2023). As adjustments in the mortgage markets decrease young adults’ homeownership access, intergenerational wealth transfers have become increasingly common to overcome credit constraints and facilitate home purchases (Dewilde and Flynn, 2021; Galster and Wessel, 2019; Morelli et al., 2021; Nolan et al., 2020).

Financial transfers are also used to pay off existing debts or provide a passive income source, easing the burden of housing costs (Lennartz and Helbrecht, 2018). Comparative research suggests that receiving intergenerational transfers improves young adults’ homeownership prospects (Cohen Raviv and Hinz, 2022). It provides an advantage in securing mortgaged homeownership in highly financialized housing markets, where affordability is lower due to an interaction with housing prices (Flynn and Kostecki, 2023). Like in other domains, families’ resources reinforce patterns of social stratification (Filandri and Semi, 2022), and are known to influence young adults’ consumption, saving behavior, housing, and wealth tax preferences (Bastani and Waldenström, 2021; De Nardi, 2004; Lersch and Luijkx, 2015; Lux et al., 2018). For instance, the expectation of receiving large bequests from parents lowers young adults’ willingness to save (De Nardi, 2004). Support for inheritance taxation decreases as respondents’ net wealth increases (Bastani and Waldenström, 2021). Furthermore, receiving intergenerational transfers and growing up in homeownership is positively associated with being a homeowner later in life (Lersch and Luijkx, 2015; Lux et al., 2018). Following these mechanisms, we anticipate that receiving intergenerational transfers will lower demand for redistribution and increase support for right-wing parties among young people.

Alongside market forces and family dynamics, another crucial aspect in redistributing social risk is the welfare state (Esping-Andersen, 1990). National institutions and political coalitions play a pivotal role in redirecting resources to fund public policy that support affordable housing or rent regulations, which can either mitigate or amplify social and spatial inequality (Dewilde, 2022; Kholodilin, 2024). For example, across Europe, homeowners tend to accumulate more wealth than renters. However, the wealth gap is the smallest in countries with a more affordable rental market, allowing renters to improve their savings (Wind and Dewilde, 2019). Indexation of benefits across welfare states helps people cope with inflation, distributing risks more evenly (Greve et al., 2024). From a housing regimes’ perspective, the relationship between affordability, parental support, and homeownership varies depending on institutional developments that determine levels of housing market financialization, generosity of the welfare state, and regulation of the rental market (Flynn and Montalbano, 2024; Ronald and Lennartz, 2018).

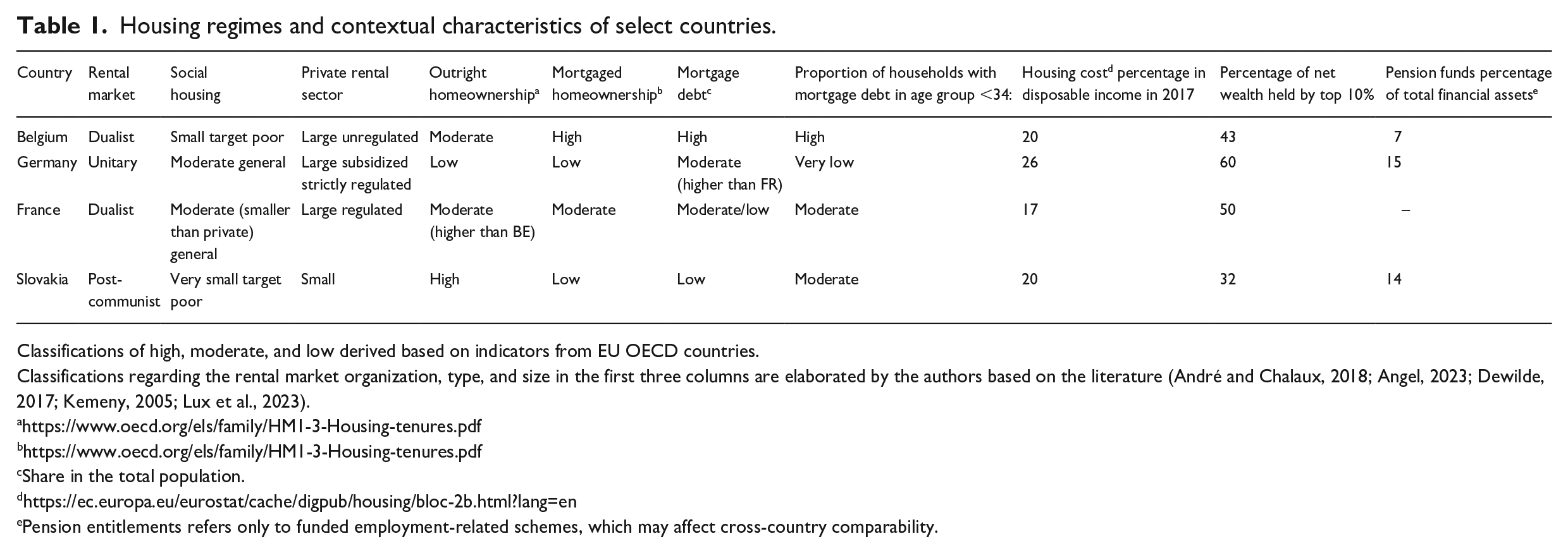

The four countries we analyze in this article exhibit distinct housing provision, allocation, and consumption patterns, influencing housing outcomes and welfare state support (Dewilde, 2020). Germany represents the typical unitary rental market with low homeownership and strict rent regulations (Elsinga and Haffner, 2019; Gabor et al., 2022). Belgium and France 5 exemplify dualist rental markets where homeownership is the prevalent tenure form, each with varying degrees of mortgage credit, social housing, and homeownership incentives (André and Chalaux, 2018; Benites-Gambirazio and Bonneval, 2024; De Decker and Dewilde, 2010; Kemeny, 2005; Le Goix et al., 2021). In Belgium, the private rental market is unregulated and the limited social housing targets low-income households. In contrast, France has a larger social rental sector with broader eligibility criteria and a more regulated private market (Wind and Dewilde, 2019). Despite minimal residualization, income has become increasingly relevant for determining households residing in social housing (Angel, 2023; Beaubrun-Diant and Maury, 2022; Dewilde, 2017). Slovakia completes the selection, representing a post-socialist housing system with high outright homeownership, lower quality housing stock, limited housing finance, and minimal welfare services (Lux et al., 2023; Soaita and Dewilde, 2019; Stephens et al., 2015). These characteristics are summarized in Table 1.

Housing regimes and contextual characteristics of select countries.

Classifications of high, moderate, and low derived based on indicators from EU OECD countries.

Classifications regarding the rental market organization, type, and size in the first three columns are elaborated by the authors based on the literature (André and Chalaux, 2018; Angel, 2023; Dewilde, 2017; Kemeny, 2005; Lux et al., 2023).

Share in the total population.

Pension entitlements refers only to funded employment-related schemes, which may affect cross-country comparability.

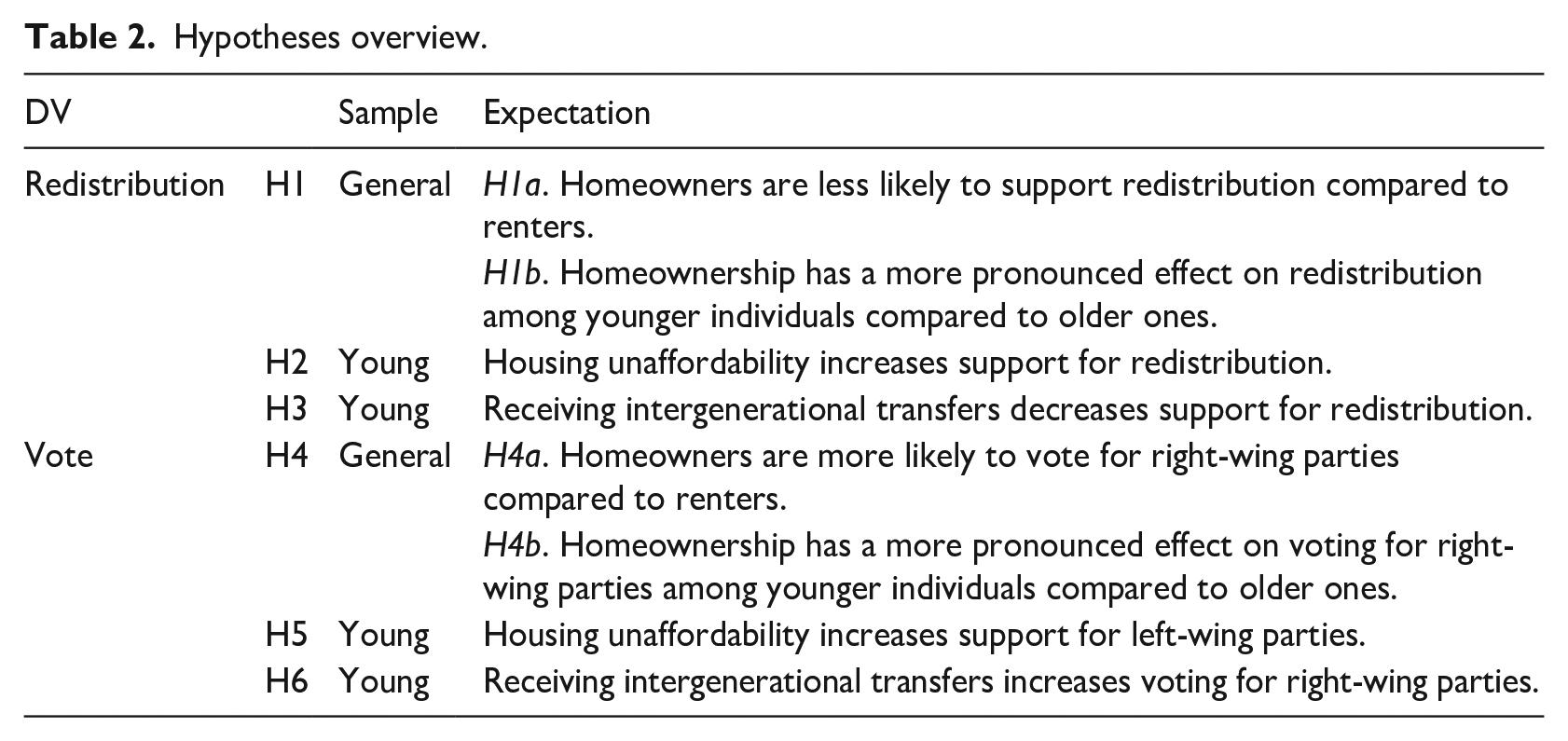

Hypotheses

Together, these literature strands argue that homeownership, housing unaffordability, and intergenerational transfers are politically relevant in shaping demand for welfare redistribution preferences and voting behavior, our two key dependent variables. We summarize the conceptual relationships for each outcome variable in Table 2, deriving six hypotheses from the literature. While hypotheses 1 and 4 focus on the contrast between younger and older generations, hypotheses 2, 3, 5, and 6 narrow their focus to the young subsample to investigate the effect of unaffordability and intergenerational transfers within this demographic.

Hypotheses overview.

Empirical analysis

Data and methods

To investigate our research questions, we statistically matched the HFCS 2017 and ISSP 2016—Role of Government (RoG) module V datasets applying a random hot-deck technique (Andridge and Little, 2009; Donatiello et al., 2016). The HFCS gathers detailed information on households’ balance sheets in a representative repeated cross-sectional survey. It employs a multiple imputation (MI) procedure to handle missing values, creating five imputations (ECB, 2020). The ISSP is an annual survey with rotating modules. The RoG module provides valuable data on political attitudes regarding government size, social policies, redistribution, taxation, and voting (ISSP Research Group, 2018). We use randomly selected units from a subset of all available data donors with complete observations in ISSP to stochastically impute an existing donor’s observed value to the missing records of similar units in the receiving dataset, HFCS.

The statistical matching approach has gained importance in the social sciences (D’orazio et al., 2012; Leulescu and Agafitei, 2013). For instance, it has been used to merge data on household consumption and income with data on voting behavior, migration, and well-being, thereby enhancing analytical capabilities and enabling cost-effective research on new questions (Albayrak and Masterson, 2017; Ayala et al., 2022; Donatiello et al., 2016). The technique relies on matching similar respondents’ sociodemographic characteristics within each country rather than directly observing all variables from the same person (Kim and Rao, 2012).

To ensure a reliable synthetic dataset, a series of sensitivity analyses using different matching approaches and parameters were conducted, showing no significant differences in the direction or statistical significance of key indicators. Detailed information about the surveys, variables, and matching approach is available in the Supplemental Online Material, with key points noted here.

The analyses follow the HFCS user guide, which specifically addresses the problem of high non-response rates regarding questions about wealth. HFCS oversamples the wealthiest households and applies multiple imputations to estimate the missing values of non-responding households. All estimations combine the five implicates to provide accurate estimates and standard errors following Rubin’s (1986) rule. All analyses consider the survey’s complex design, weights, and bootstrap variance estimation (1000 replications). Given the nature of the dependent variables, we adopted ordered and multinomial logistic regressions, deploying pooled country-fixed effects and country-specific models. Following Mize (2019), we present the results in terms of the odds ratio, predicted probabilities, and average marginal effects (AMEs).

Sample

Our hypotheses include comparisons between younger and older individuals as well as hypotheses specific to young people. We accordingly conduct our analyses on two samples. We start our analysis by including all available observations, comparing younger (22–42) and older (43 and above) respondents in a total sample of 18,700 individuals. The smallest sample is in Slovakia (1,661) and the largest is in France (11,121). Next, we limit our focus to households with young adults aged 22–42 aligning with prior research (e.g. Dewilde and Flynn, 2021) and considering the delayed transition to homeownership (Dewilde, 2020). Drawing from housing and inequality studies, the unit of analysis is the individual within their household (e.g. Dewilde, 2018). The young subsample sizes range from 404 observations (Slovakia) to 3,239 observations (France). Descriptive statistics before and after the statistical matching are available in the Supplemental Online Material for the total sample and per country.

Variables

We analyze two dependent variables: welfare preference and vote choice. Welfare preference is measured using the statement, “It is the responsibility of governments to reduce differences in income between the rich and the poor.” Responses range from 1 to 4, where a higher score indicates a stronger belief in government responsibility. This question is widely used in sociology and political economy research to gauge attitudes toward the welfare state, including existing work on housing and redistribution (Adler and Ansell, 2020; Ansell, 2014). While the question asks about income and not wealth, research using ISSP data indicates that perceptions of income and wealth inequality are significantly associated (Gonthier, 2023).

To capture voting preferences, we use the question, “Can you tell me for which candidate you voted in the last country Election?” ISSP converts vote choice to a five-point left-right scale, increasing to the right. The scale is party-based and is classified based on expert judgment. The specific criteria ISSP uses to classify parties (e.g. based on economic or cultural stances) are not explicitly stated. To enhance confidence in understanding the left-right scheme, we cross-referenced information with the Global Party Survey 2019 (Norris, 2020). The Supplemental Online Material provides more information about the left-right scheme.

Our three key independent variables are homeownership, individual housing unaffordability, and receiving an inheritance or financial gift. Homeownership is a binary variable 6 based on housing and mortgage debt indicators. Housing unaffordability refers to monthly rent or mortgage cost in euros relative to gross income, forging the housing expenditure-to-income ratio variable. Following the HFCS documentation, housing cost ratios equal to or above the 40 percentage threshold indicate affordability problems. The intergenerational transfers variable is derived from the question regarding the receipt of inheritance 7 or substantial gifts, coded as zero for non-recipients and one otherwise.

To test for the interactions, the general models include the product between homeownership and age, while the young subsample models include the product term between homeownership and unaffordability. Tests of the interactions involved additional steps. In logistic regression models, the distribution of the outcome variable is not linear, and the interaction term cannot be directly interpreted. It is advisable to use tests of the predicted probabilities and the average marginal effects (contrast or second difference) to determine significant differences of the effect of one predictor across levels of the other (Mize, 2019).

We control for geographic region, the amount spent on utilities, income, education, marital status, and age. Geographic region refers to the area of residence of the household and is nationally coded for Germany, France, and Slovakia. It is included as a factor variable in the country-specific regressions except for Belgium, where the variable is unavailable. Amount spent on utilities includes electricity, water, gas, telephone, Internet, and television. Income is in thousands of euros and refers to the equivalized gross annual income from all resources. Education is based on the highest ISCED level attained (UNESCO, 2012) and grouped into primary-lower, secondary, and tertiary education. Age is a continuous variable indicating the household representative’s age. Marital status is categorical in which one denotes “single,” two is “married/consensual union on a legal basis,” and three means “divorced, separated or widowed”—in the case of young adult households, the percentages in the last category were very low. 8

Results

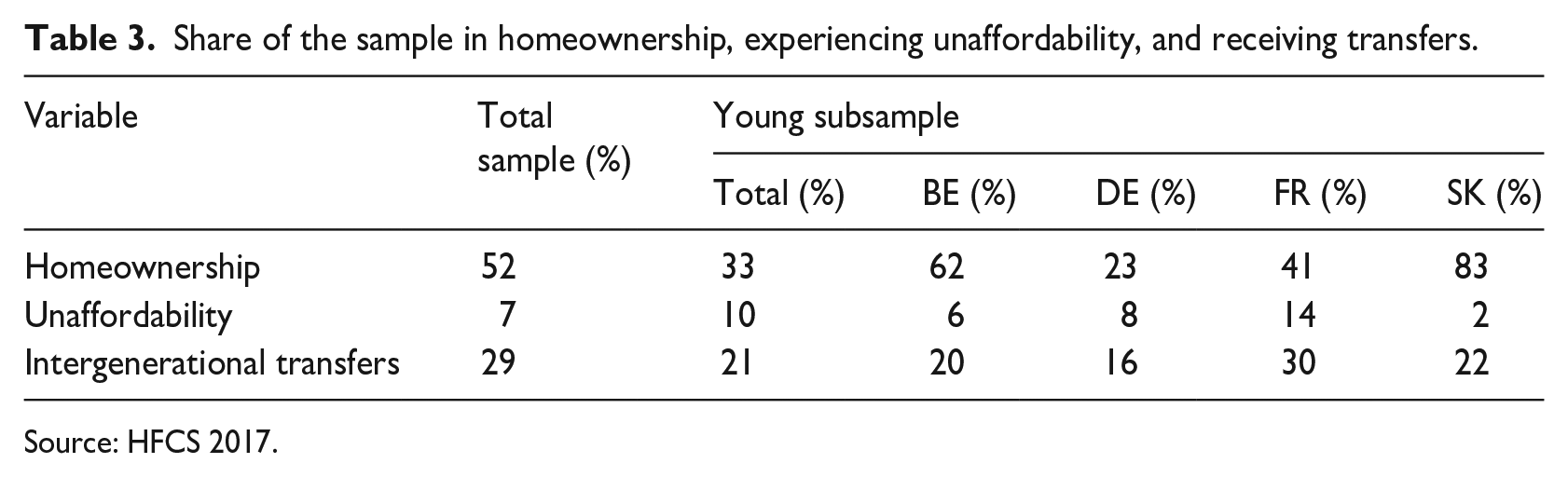

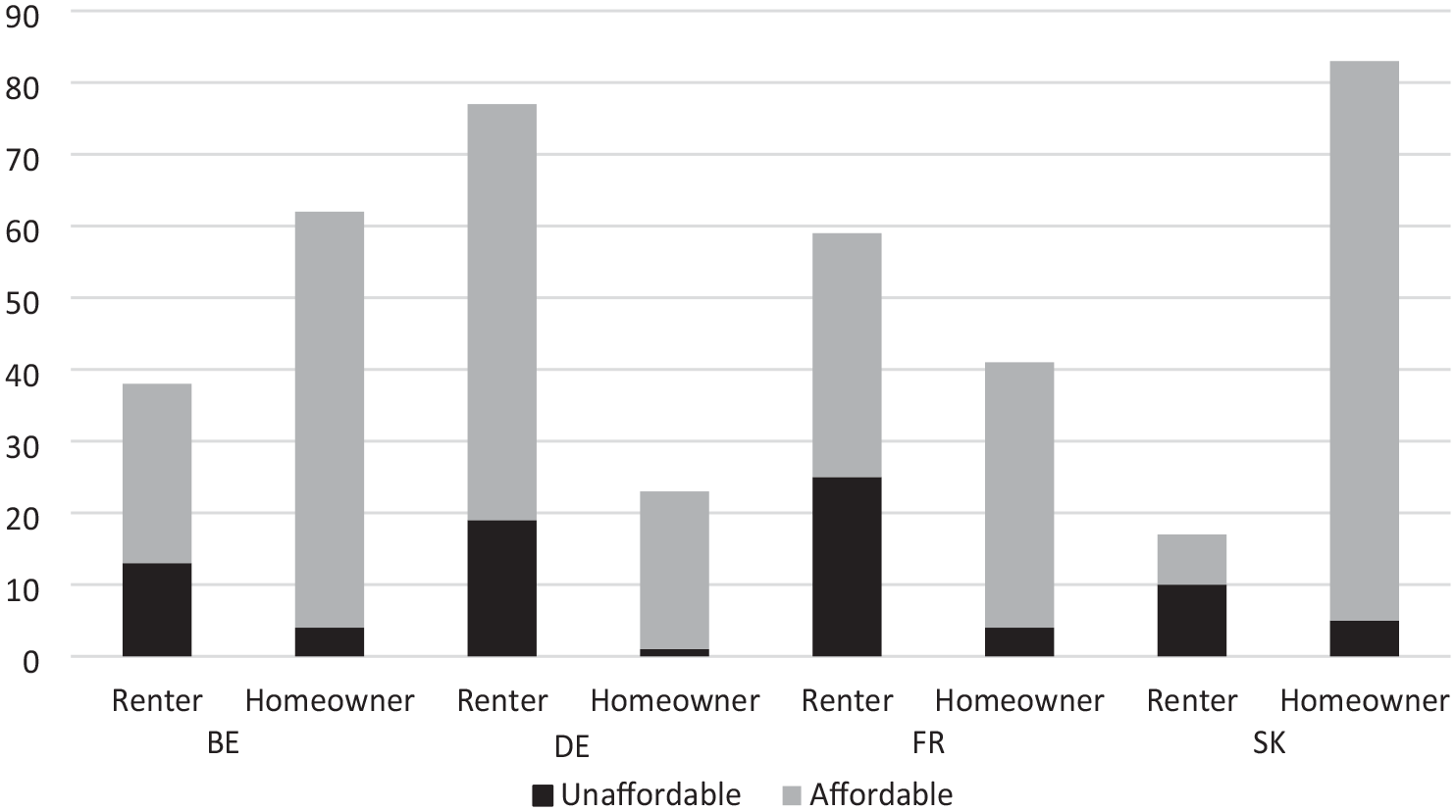

This section discusses the hypotheses for the two dependent variables, redistribution, and voting, in turn. Table 3 demonstrates the differences across the two samples and across countries for the key independent variables of this article. Figure 1 illustrates the share of the young subsample in unaffordability among homeowners and renters in each country. While homeownership prevails for older individuals, young people are mostly renters. The tenure distribution nonetheless aligns with the housing regimes literature, with, for instance, young renters more prevalent in Germany and young homeowners more prevalent in Slovakia. Tables A1 and A2 in Appendix A show the complete descriptive statistics for the entire sample and young subsample.

Share of the sample in homeownership, experiencing unaffordability, and receiving transfers.

Source: HFCS 2017.

Share of the young subsample in unaffordability among homeowners and renters in each country.

Support for redistribution

Total sample

We begin by examining our first general hypothesis of whether homeownership has a negative association with redistribution (H1a) followed by whether young homeowners are even less supportive of redistribution (H1b). The pooled model includes all independent variables, the interaction term between homeownership and the age-centered continuous variable, controls, and country-fixed effects. 9 Results with the odds ratio and AME of all coefficients are displayed in Table A3 in Appendix A. The main association of homeownership and age on support for redistribution is not statistically significant, and we do not find support for H1a. The lack of statistical significance suggests that neither homeownership nor age alone influence support for redistribution, as confirmed in the AME. However, results suggest a significant interaction between tenure and age. To test whether there is a moderating role of age in the relationship between homeownership and support for redistribution (H1b), we turn to the differences in AME (Mize, 2019). The difference in AME captures how the relationship between homeownership and support for redistribution varies across age and if differences between them are statistically significant.

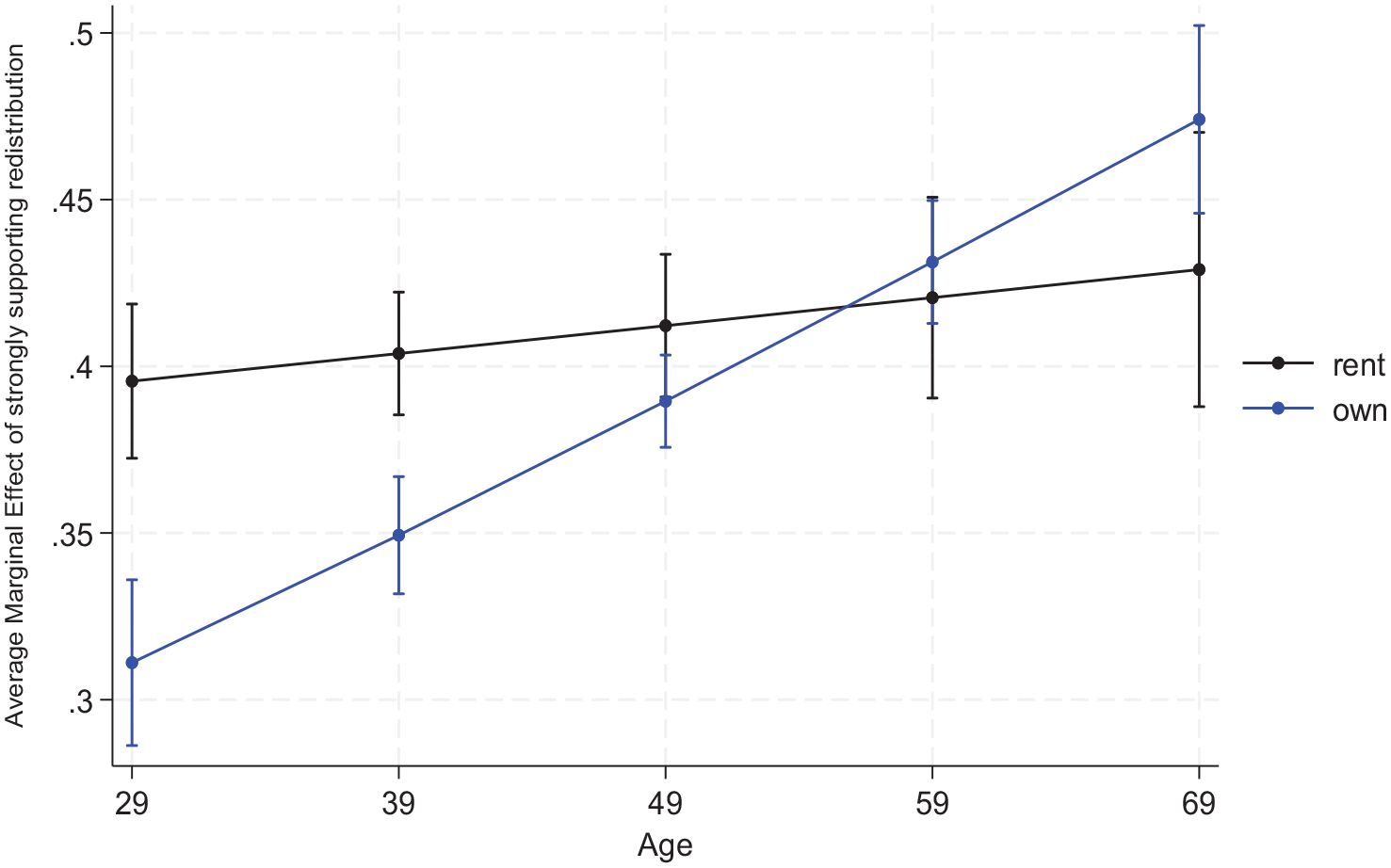

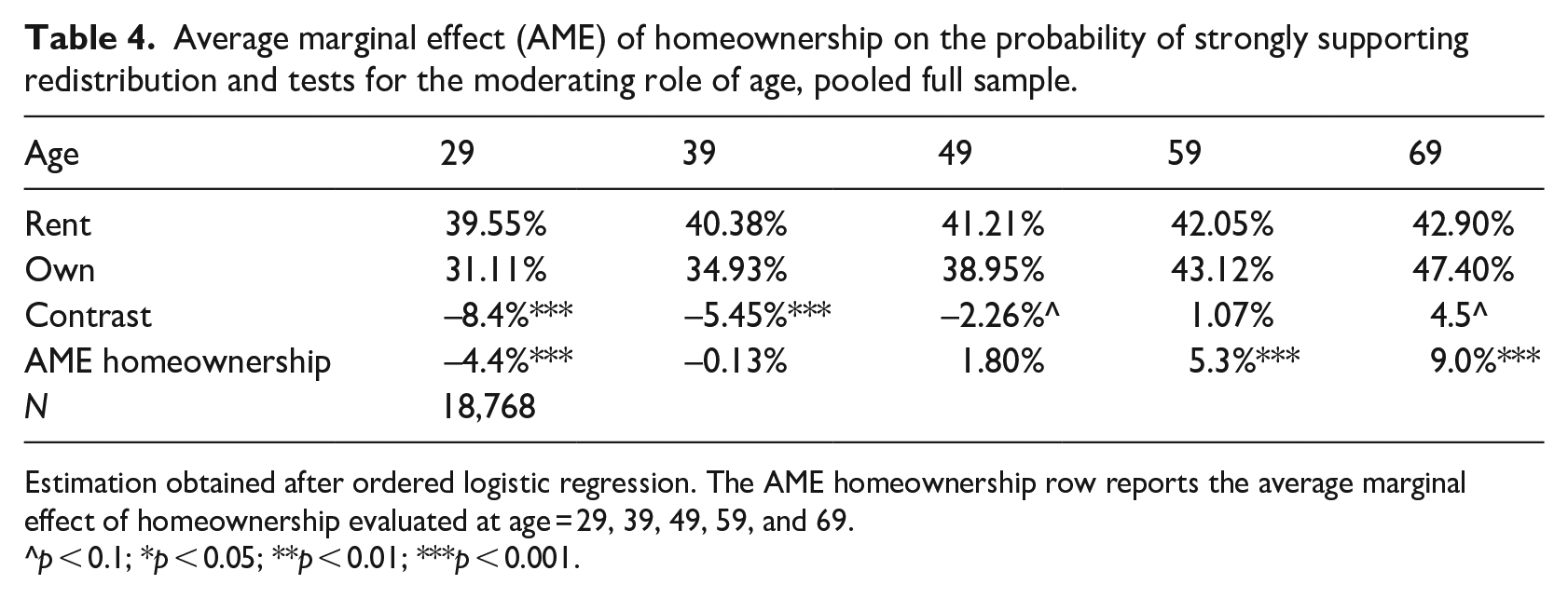

To facilitate interpretation, we illustrate and compare the AME for homeowners and renters of strongly supporting redistribution (a value of four on the four-point scale). Figure 2 illustrates the marginal effects of strongly supporting redistribution at different points of age for homeowners and renters using the parameters presented in Table 4. There, the first and second rows were obtained splitting the sample between homeowners and renters and calculating the AME for each group separately across different levels of age. The third row takes the first difference between homeowners and renter within each age point, while the fourth row reports the AME of homeownership evaluated at age = 29, 39, 49 (mean), 59, and 69. We observe that homeowners at age 29 are on average associated with a 4.4 percentage (p < 0.05) decline in strongly supporting redistribution. This confirms H1b, since among the youngest in the sample, support for redistribution is lower. Differences between homeowners and renters are also significant with homeowners being less inclined to support redistribution compared to renters within the same age group. As age increases, we observe a shift: the increase in support for redistribution is higher for older homeowners (indicated by the steeper line in Figure 2). Specifically, older homeowners (at age 69) have on average a 9 percentage higher probability of strongly supporting redistribution. The situation for older homeowners is the opposite to what is expected in the traditional literature, indicating a possible convergence in homeownership-welfare support at the micro level, which is more aligned with recent findings (Van Gunten and Kohl, 2020). Results are similar for the other categories of the dependent variable. Country-specific regressions consistently show a similar trend of lowest support among young homeowners compared to the older cohort, with statistical significance observed in Belgium, Germany, and France, as shown in Tables A3 and A4 in Appendix A.

Average marginal effects of the interaction between tenure and age on support for redistribution, adjusted predictions for pooled total sample with country-fixed effects (N = 18,768).

Average marginal effect (AME) of homeownership on the probability of strongly supporting redistribution and tests for the moderating role of age, pooled full sample.

Estimation obtained after ordered logistic regression. The AME homeownership row reports the average marginal effect of homeownership evaluated at age = 29, 39, 49, 59, and 69.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

Young subsample

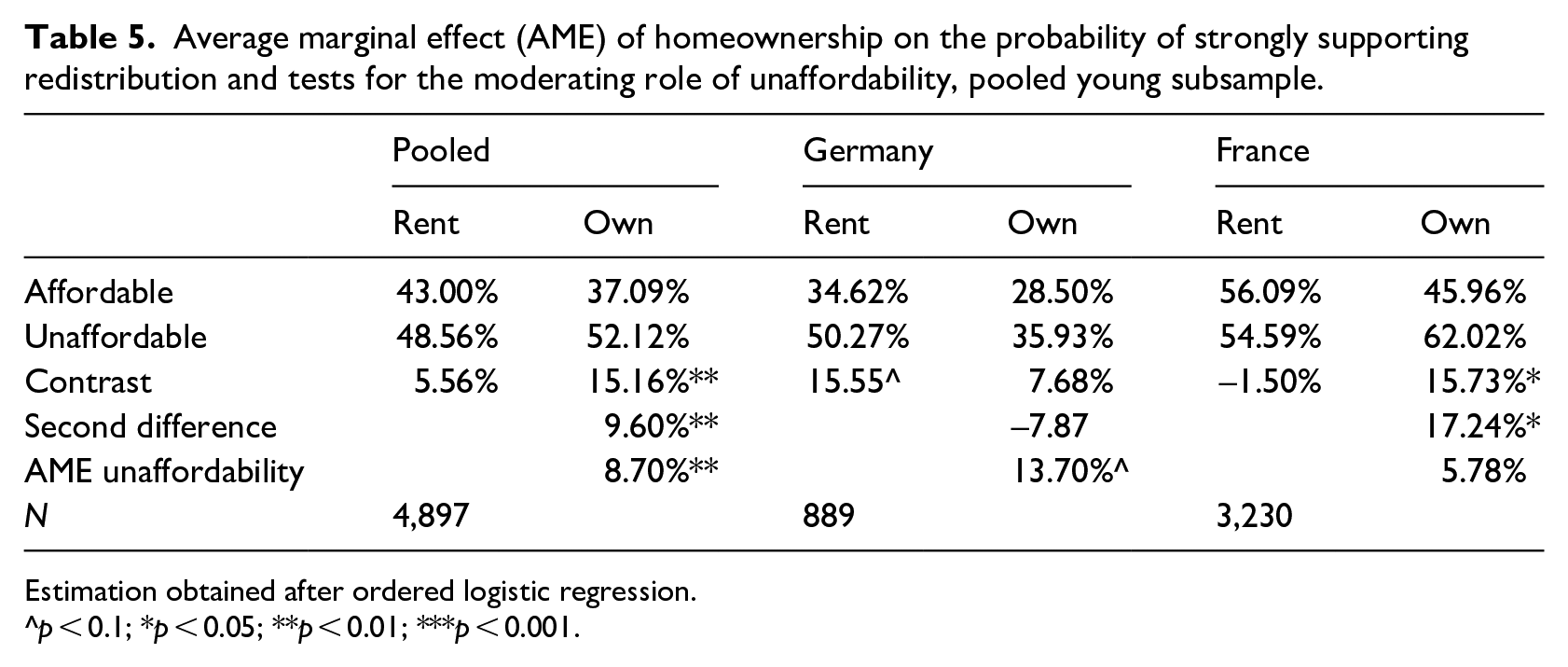

To investigate H2; whether housing unaffordability increases support for redistribution and H3; whether receiving intergenerational transfers decreases support for redistribution, we narrow our focus to the young subsample. Results of the ordered logistic regressions are presented in Table 5. We show AMEs and their differences between levels of homeownership and unaffordability to test for the interaction term included in the model.

Average marginal effect (AME) of homeownership on the probability of strongly supporting redistribution and tests for the moderating role of unaffordability, pooled young subsample.

Estimation obtained after ordered logistic regression.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

In favor of H2, our results suggest that housing unaffordability correlates with more support for redistribution. As observed in the Pooled Model 1 in Table A5 of Appendix A, the odds ratio of 1.33 and AME of 0.069 (p <0.1) are statistically significant. While the significance level is marginal, the magnitude of the association warrants attention. Once we include the interaction between homeownership and unaffordability in the Pooled Model 2, the AME of unaffordability remains statistically significant and increases to 0.087 (p < 0.05), confirming H2. Directly interpreting the odds ratio (Table A5 of Appendix A) can be challenging, therefore, we turn to predicted probabilities and AMEs (Table 5) for an easier and more intuitive understanding of the relationship between housing unaffordability and redistribution. Combining data from all countries, young homeowners and renters experiencing unaffordability show, on average, 8.7 percentage higher probability of supporting redistribution than their young counterparts in affordable housing situations. 10 In other words, unaffordability has a main influence increasing support for redistribution among young homeowners and renters. The analysis of the interaction term shows that the difference in strongly supporting redistribution due to unaffordability is statistically significant for homeowners (15.16%, p < 0.01) but not for renters.

To provide a comparative analysis, we now turn to the country-specific regression results also displayed in Table 5. Our findings indicate that housing unaffordability correlates with greater support for redistribution among young people in two of the analyzed countries: Germany and France. In the regression results for Belgium and Slovakia, neither homeownership nor housing unaffordability correlate with support for redistribution in the subsample of young people.

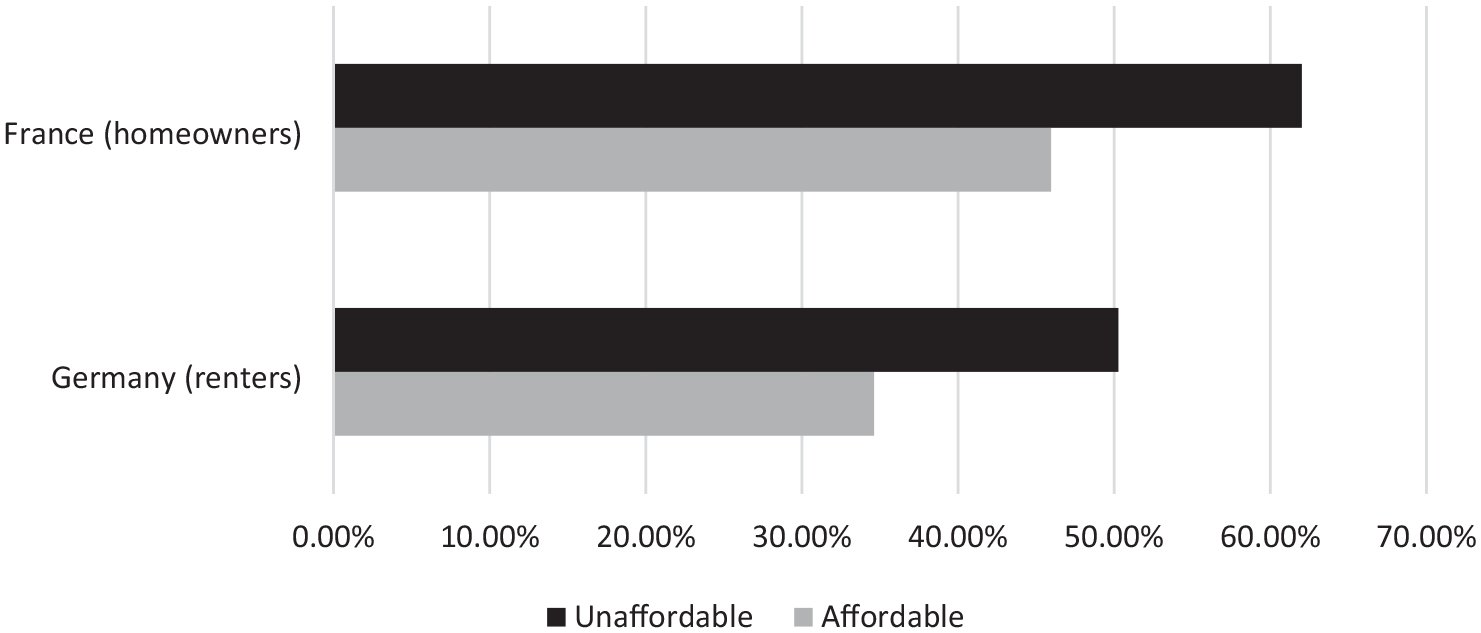

As presented in Table 5, housing unaffordability in Germany has an AME of 0.137 (p < 0.1), indicating a significant association with greater support for redistribution. 11 Both renters and homeowners facing unaffordable situations tend to express increased support for redistribution, however, the difference is statistically significant only for renters (15.55%, p < 0.1). German renters in unaffordable situations are 15 percentage points more inclined to strongly support redistribution compared to those whose housing costs do not exceed 40 percent of their income. In France also, young homeowners exhibit different patterns of support for redistribution. On average, renters are more supportive than homeowners, but unaffordability does not play a role for this group. This is evident in Table A5 where the AME for homeownership is statistically significant. However, housing unaffordability affects these two groups differently as indicated by the analysis of the interaction term between homeownership and unaffordability in Table 5. The interaction term highlights a divergence in support among homeowners based on unaffordability. Specifically, homeowners facing unaffordability tend to express 16 percentage points (p < 0.1) higher support for redistribution, while homeowners without the cost overburden exhibit even less redistributive support. Figure 3 illustrates the statistically significant differences between renters in Germany and homeowners in France due to the influence of unaffordability.

Differences in average marginal effects of housing unaffordability for homeowners in France and renters in Germany.

Examining H3 and the relationship between intergenerational transfers and support for redistribution in the young subsample, we observe in Table 5A (in Appendix A) that while in the pooled ordered logistic regression the AME failed to reach statistical significance, in Belgium and Germany different patterns emerged. In Belgium, the regression results align with our expectations for H3, suggesting a 11 percentage points lower likelihood (p < 0.1) of support for redistribution among young individuals who have received intergenerational transfers. In Germany, however, the AME shows that receiving intergenerational transfers increases the probability of support for redistribution by 8 percentage points (p < 0.1), which opposes our expectation.

To contextualize the observed variation in support for redistribution across countries and the findings combined for H1, H2, and H3, we draw upon the housing regimes framework as done by prior research. As we have argued previously, the country’s social, political, and economic context are likely to influence and be influenced by citizens’ political preferences (André and Dewilde, 2016). Germany stands out as a rental-oriented society with one of Western Europe’s lowest homeownership rates and one of the highest wealth inequality levels (Dewilde and Flynn, 2021). In contrast to other countries, the German housing finance system retained a conservative approach and buying property remains particularly difficult without receiving intergenerational financial assistance (Cohen Raviv and Hinz, 2022).

Loan-to-value and loan-to-income ratios stayed low, requiring substantial down payments for homeownership, making it significantly harder for the lowest social group (Wind and Dewilde, 2019). Their integrated rental market, characterized by its robust tenant protection, has historically provided a viable and long-term option across all income levels (Dewilde, 2018). However, incremental changes in the rental stock, including the conversion of social into private rentals contributed to affordability challenges, especially in metropolitan areas (see Elsinga and Haffner, 2019 for a complete discussion). This particularly affects newer tenants who encounter less favorable rents (Hick et al., 2024), potentially bolstering calls for redistribution.

As depicted in Figure 1, in our German sample, 25 percent of young renters face unaffordable housing, compared to only three percent of homeowners. This situation increases economic vulnerability and risk perception among young households, especially renters, influencing their demand for redistribution. Despite housing unaffordability being prevalent among the young, especially renters, we did not observe a corresponding increase in demand for redistribution in this group in the analyzed countries, except for Germany.

In France, we find that renters, on average, express greater support for redistribution than homeowners. Figure 1 illustrates that 59 percent of young people in France are renters, of which 42 percent experience housing cost overburden. Housing unaffordability does not influence renters, but it does polarize homeowners. Challenging prevailing views in the literature (André and Dewilde, 2016; Ansell, 2014), we found that overburdened homeowners tend to demand greater government support, probably in response to their economic strain, seeking relief from their financial burden.

The French government has actively encouraged homeownership through state-financed mortgages (André and Chalaux, 2018; Wijburg, 2019). However, due to the regulated housing finance system, characterized by moderate down payments and amortization requirements, homeownership expansion has remained limited to the middle and upper classes. This has resulted in increased social selectivity, notably evident in the strong divide between securely and insecurely employed individuals (Dewilde, 2017; Lersch and Dewilde, 2015). Despite widening disparities between property prices and household incomes with historic levels of unaffordability, the real estate market remained strong (Le Goix et al., 2021). Uncertainty about the retirement system, the perception of declining living standards, and the rising value of property have elevated homeownership to nearly indispensable for maintaining a decent lifestyle. Consequently, average-income households are willing to accept greater debt and assume heavier financial burdens to secure homeownership, aiming to reduce uncertainty during retirement (Benites-Gambirazio and Bonneval, 2024).

Belgium features a dualist rental market where government policies actively promote mortgage-based homeownership (André and Dewilde, 2016; Dewilde, 2020). This approach decreases the attractiveness of the private rental sector and stimulates homeownership as an alternative form of social security (De Decker and Dewilde, 2010). Our results show that while receiving intergenerational transfers is associated with less support for redistribution among young adults, housing unaffordability does not have any influence despite the substantial proportion of young households experiencing costs overburden, as illustrated in Figure 1. One key reason for this lack of influence is that wealthier individuals have a tangible opportunity to transition into mortgaged homeownership in a context of a more financialized housing market (Lennartz et al., 2016). As property is increasingly seen as a partial retirement asset, they become hesitant toward supporting redistribution. Results should be interpreted with caution due to our inability to control for geographic regions, however.

Slovakia has a more equalized distribution of housing asset ownership among the population. However, the housing stock is often of low quality, resulting in high housing-related costs and potential financial risks (Stephens et al., 2015). Homeownership does not necessarily indicate housing wealth, and mobilizing housing assets for personal welfare needs or investment strategies remains challenging (Cohen Raviv and Hinz, 2022; Wind and Dewilde, 2019). In Slovakia, like other post-socialist countries, the residual welfare state, widespread homeownership inherited through families, and low mortgage debt likely shape young adults’ views toward market solutions over state provision (Lux et al., 2023). Linking the findings to social stratification, private homeownership continues to hold ideological and economic significance in both Belgium and Slovakia. Its prevalence among young people, although with varying forms of access (credit market or the family), still indicates compliance with the expected tenure status. Therefore, fulfilling tenure expectations, particularly for the middle class through market mechanisms or family assistance, may limit demand from the government in those countries.

Analyzed together, results about redistribution show that homeownership is associated with lower welfare support among young adults, while housing unaffordability coalesces young homeowners and renters, increasing support for redistribution with remarkable country differences. In financialized systems where young people have broader access to mortgage markets, like Belgium, or where families assist in providing homeownership, as in Slovakia, our data suggests that despite high levels of unaffordability among renters, there is no significant influence on demand for redistribution. Conversely, in countries with high housing costs, especially among young households in the primary tenure type, such as homeownership in France or the rental sector in Germany, there is an influence on the demand for redistribution due to increase economic vulnerability and risk perception.

Vote choice

Total sample

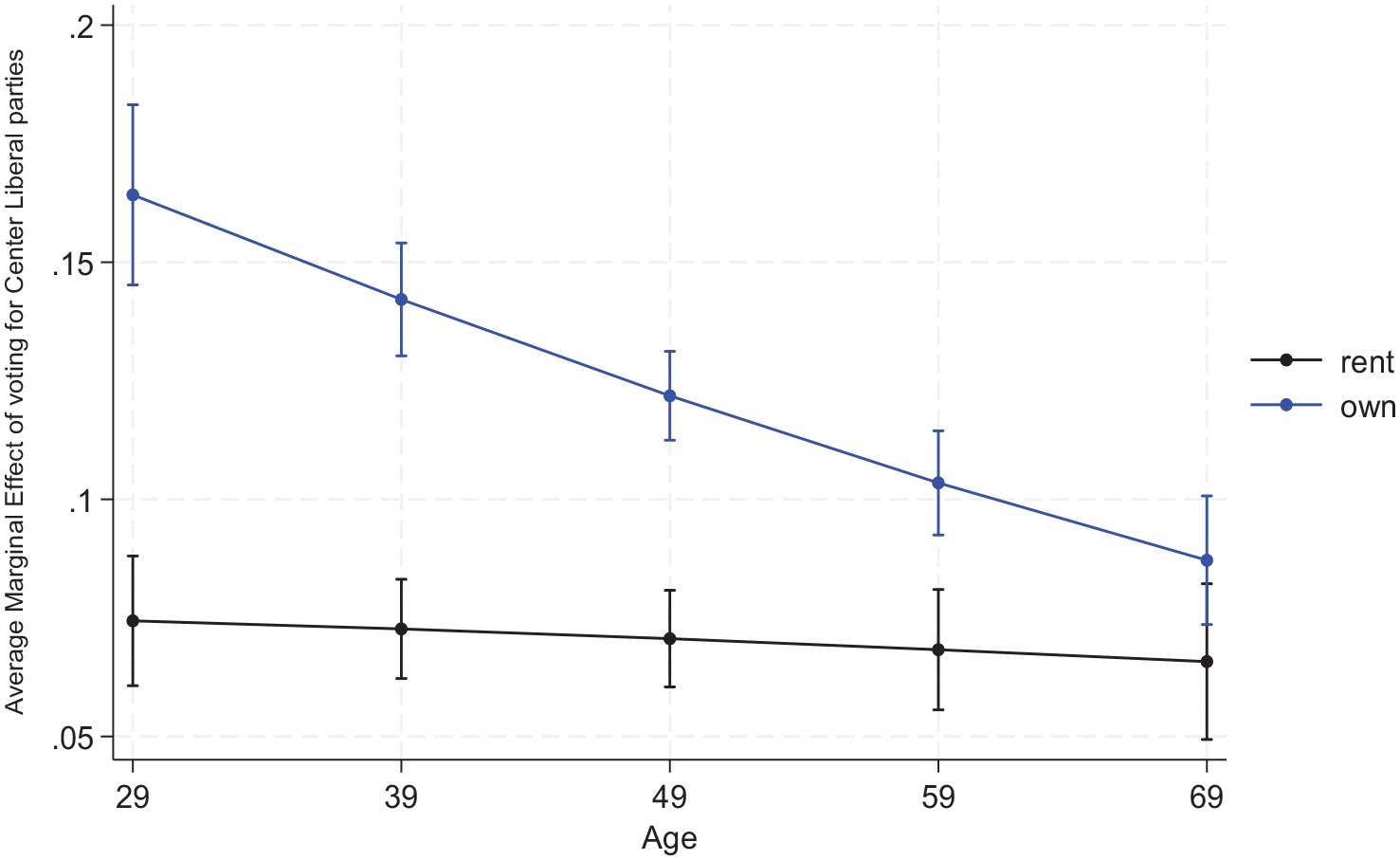

With respect to our second dependent variable, voting, we test whether homeowners are more likely to vote for right-wing parties (H4a), with a more pronounced effect on younger people (H4b). Table A6 and A7 in Appendix A show the relative risk ratio and AME for the multinomial logistic regressions for the total sample across all countries for voting outcomes relative to the far-right category. From the tables, we observe that the relative risk ratio of homeownership is not statistically significant across any of the party categories. Hence, we reject H4a since there is no evidence of homeownership influencing voting behavior in our sample. Examining H4b, results suggest that, compared to the older group, younger respondents are more likely to vote for center–liberal parties than for the far right. 12 Multinomial logit coefficients are not interpretable alone. Therefore, Figure 4 illustrates the predicted probabilities in terms of the AME as shown in Table 6 of voting for center-liberal parties (the only coefficient that was statistically significant in the model in Table A6) across age while holding all other variables constant at their mean values. The predicted probability of a respondent voting for a center–liberal party is significantly higher for younger homeowners and decreases as age increases. While age differences are visible, we reject H4a because we do not find homeownership to have a significant association with voting. Moreover, we cannot confirm H4b because of lack of evidence in homeownership increasing right-wing voting especially among young people.

Average marginal effects of the interaction between tenure and age on voting for center–liberal parties, adjusted predictions for pooled total sample with country-fixed effects (N = 18,768).

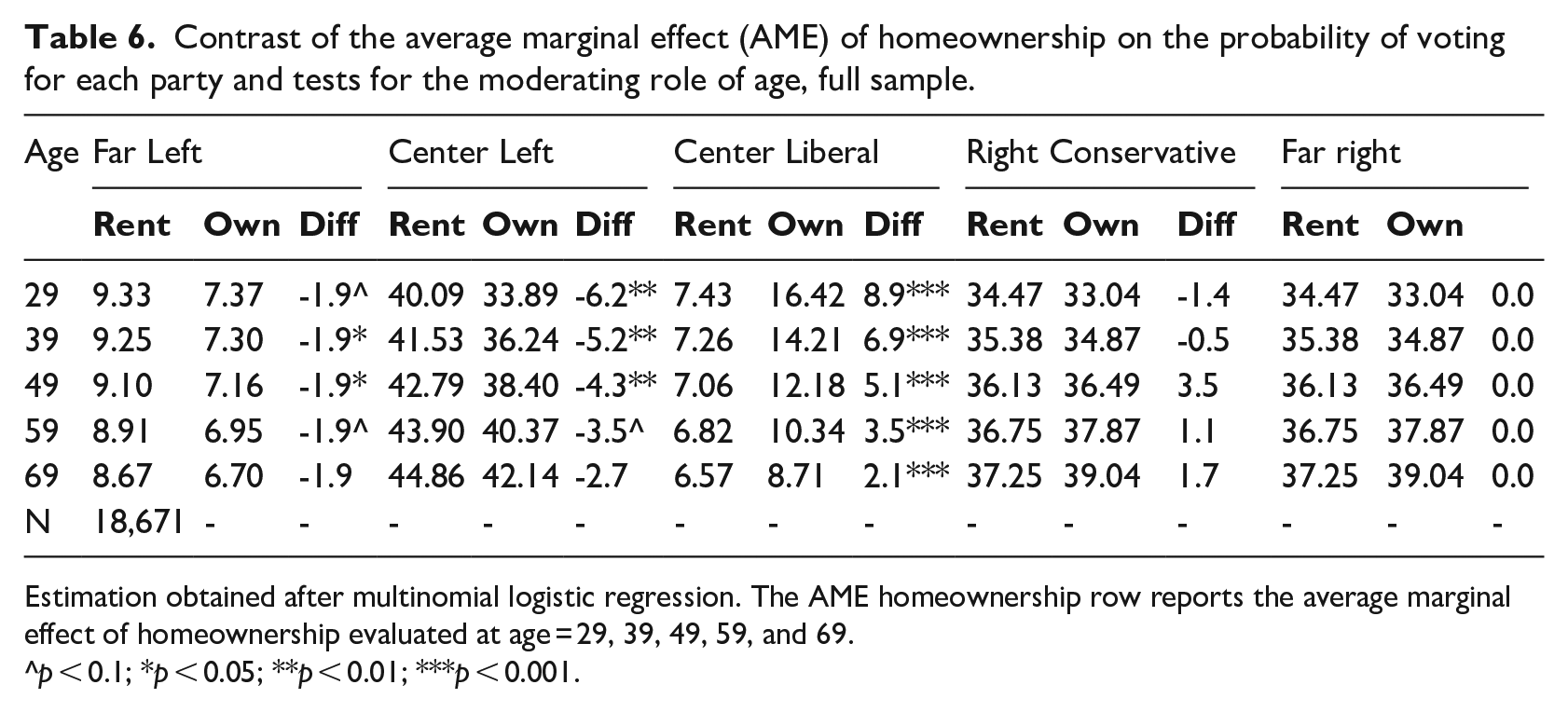

Contrast of the average marginal effect (AME) of homeownership on the probability of voting for each party and tests for the moderating role of age, full sample.

Estimation obtained after multinomial logistic regression. The AME homeownership row reports the average marginal effect of homeownership evaluated at age = 29, 39, 49, 59, and 69.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

Young subsample

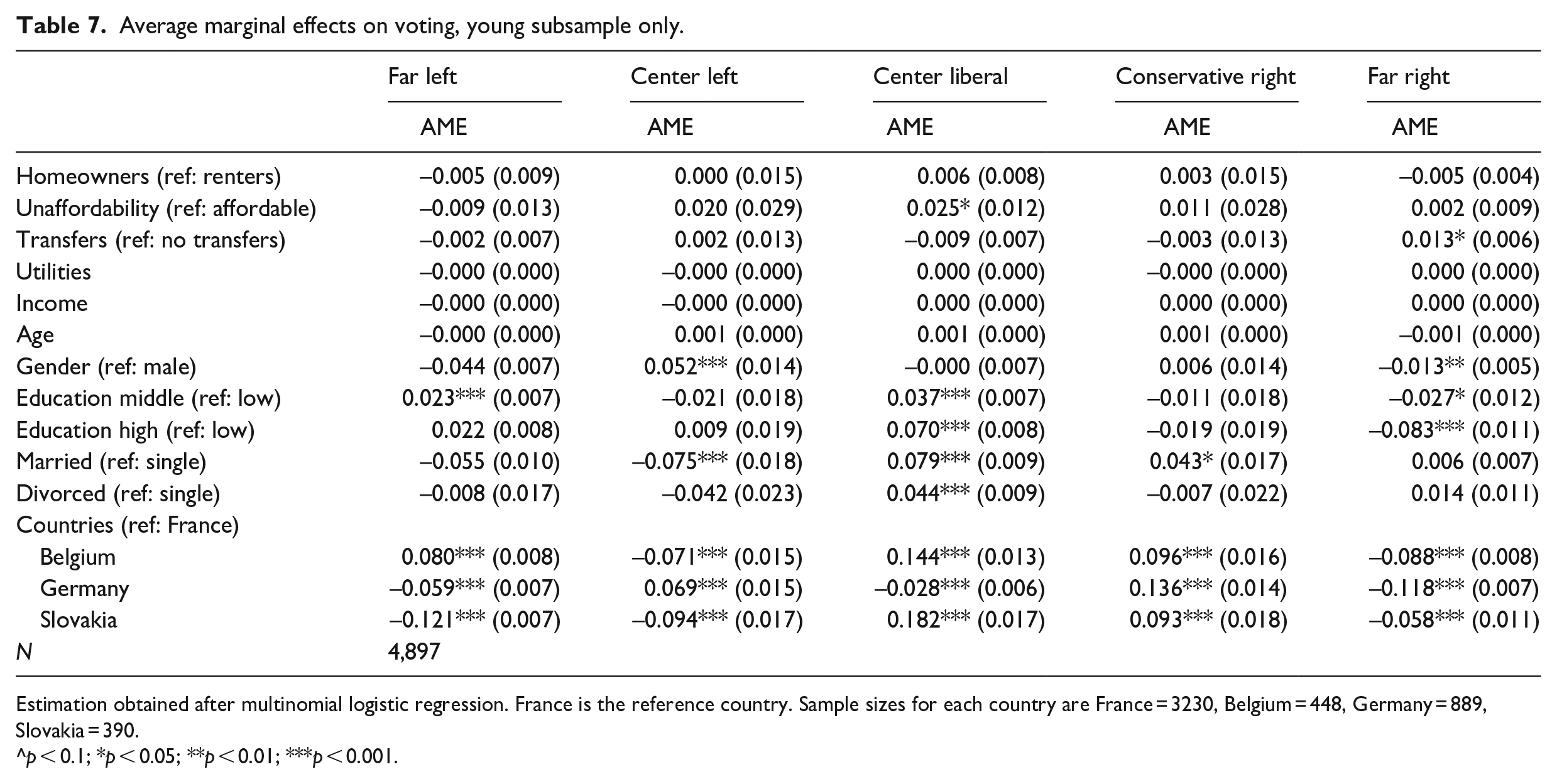

We now turn to examine our fifth hypothesis of whether housing unaffordability increases support for left-wing parties among young adults (H5). Table 7 presents the AME of the multinomial logistic regressions for the young subsample across all countries, comparing vote outcomes relative to the far-right category.

Average marginal effects on voting, young subsample only.

Estimation obtained after multinomial logistic regression. France is the reference country. Sample sizes for each country are France = 3230, Belgium = 448, Germany = 889, Slovakia = 390.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

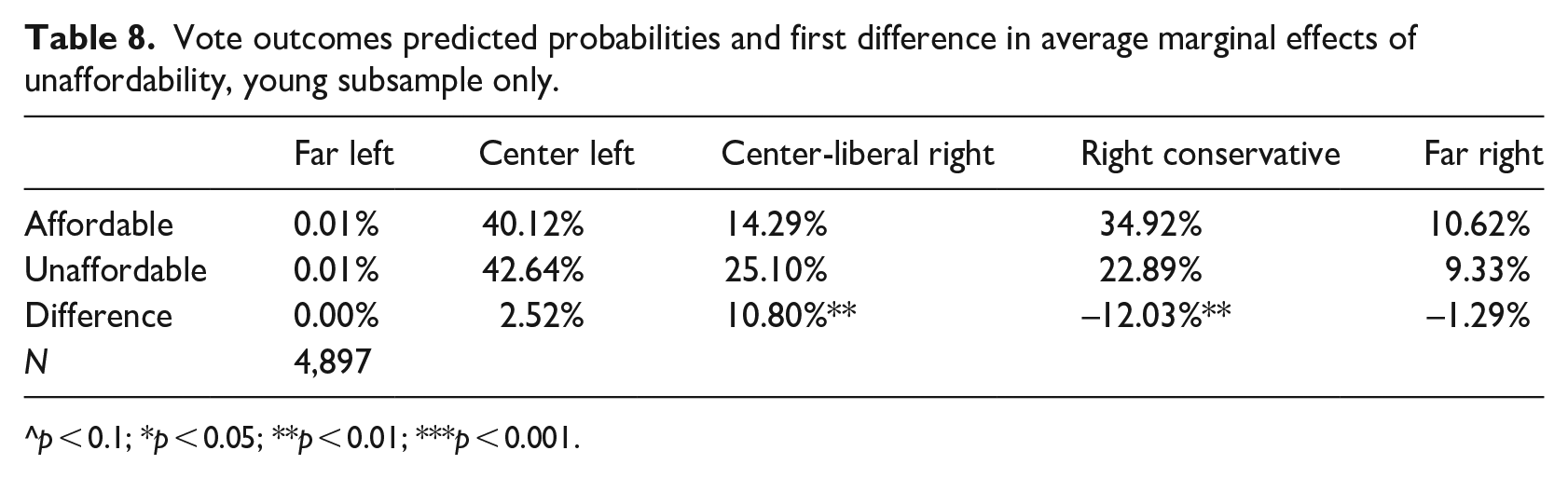

As observed in Table 7, unaffordability enhances the likelihood of young respondents voting for center–liberal parties relative to the far right, compared to those in affordable housing. Examining the first difference 13 in the predicted probabilities displayed in Table 8, on average, young households facing housing unaffordability are 11 percentage more likely to vote for center–liberal right parties and 12 percentage less likely to vote for right-conservative parties than young people in affordable conditions. However, we did not find enough evidence to affirm that unaffordability leads young adults to vote for left-wing parties. Hence, we reject H5.

Vote outcomes predicted probabilities and first difference in average marginal effects of unaffordability, young subsample only.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

Crucially, when examining the broader distribution of votes across all parties (see Figure C8 in Appendix C), it is evident that most young people vote for center-left and conservative-right parties. While housing unaffordability notably influences support for center–liberal parties, it is essential to acknowledge that this does not encompass the entirety of youth voting patterns, and the situation in France may primarily drive the overall findings. For robustness, an additional model excluding France (see Table A9 in Appendix A) revealed that unaffordability was not statistically significant, while homeownership was associated with increased likelihood of voting for all other parties compared to the far right, indicating the need for a cautious interpretation of the results. 14 Unlike Ansell and Cansunar (2021), we do not find that young adults experiencing housing cost overburden turn to populist parties. Regarding H6 and the expectation that intergenerational transfers increase right-wing vote among young people, we did not find this variable to influence the outcomes, and thus reject H6.

The combined vote outcome results suggest that while homeownership does not directly associate with conservative voting, it appears to be influenced by a complex interplay of political, social, and economic factors that our models do not fully capture. Based on cross-referenced information of the ISSP voting variable with the Global Party Survey 2019 (Norris, 2020) – and considering party values, issue positions, and rhetoric – the center–liberal parties in ISSP typically align as economically right-leaning on matters such as privatization, taxes, regulation, government spending, and the welfare state. However, they tend to adopt socially liberal stances on issues like immigration, nationalism, and environmental protection.

Analyzing our findings through a pocketbook voting framework, we observe that housing unaffordability influences voting behavior by affecting perceptions of economic stability and security among overburdened mortgaged homeowners in France. The emergence of new partisan allegiances and the appeal of center–liberal parties, which advocate for free-market economic policies supporting homeownership and opposing high taxation while promoting liberal cultural values praised by the youth, play a significant role in shaping this dynamic. These factors likely contributed to defining our results. Despite shedding some light on voting behavior and homeownership dynamics, the use of pooled regressions with country-fixed effects limits our ability to examine country-specific nuances thoroughly.

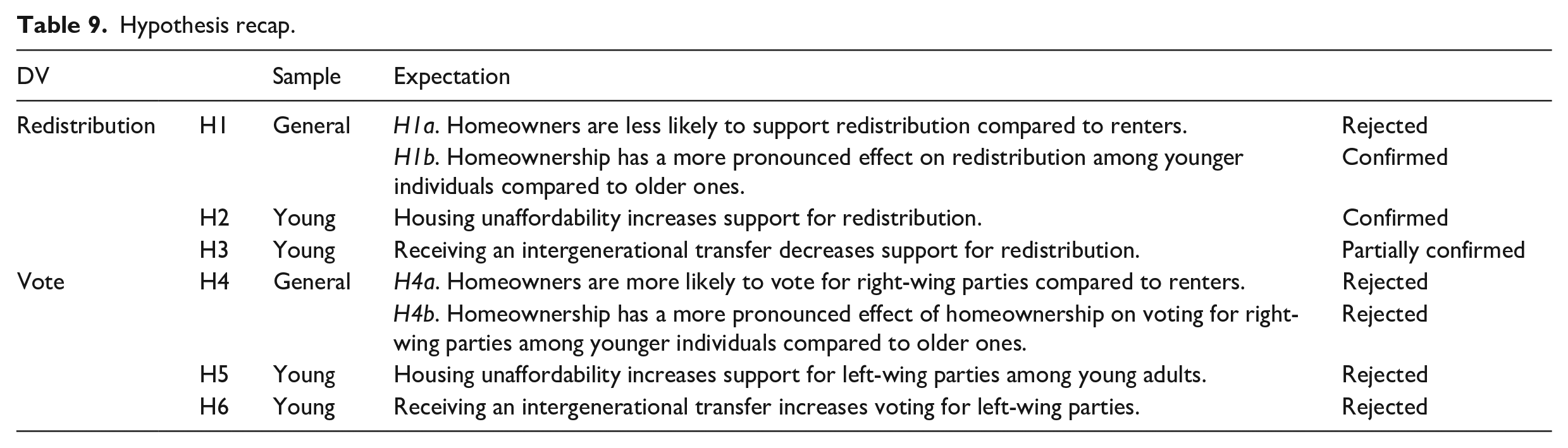

Table 9 recaps the hypotheses and summarizes the results.

Hypothesis recap.

Conclusion and discussion

This article investigated the effect of homeownership, housing unaffordability, and intergenerational transfers on young people’s welfare preferences and political choices in four European countries using a novel synthetic dataset. Our analysis adds to the existing literature emphasizing the role of homeownership, primarily housing unaffordability, in shaping both the demand for social policies and political outcomes. Our findings suggest that while homeownership lowers young adults’ overall welfare support, housing unaffordability connects young homeowners and renters, increasing redistribution support with notable country specificities. Unaffordability also influences voting, heightening support for center–liberal parties at the expense of support for the far-right. Despite partially confirming the predominant literature (André and Dewilde, 2016; Ansell, 2014), our results are intriguing and cast some questions on the conventional housing-welfare trade off and its underlying mechanisms.

Homeownership emerges as a great divider, lowering young people’s redistributive preferences compared to previous generations in three of four countries. Consistent with recent research, our results suggest that the relationship between homeownership and welfare support is not only conditional on the life-cycle stage but also loses relevance for the young group amid growing housing unaffordability and restrictive access to homeownership. We mainly observe a trend of high homeownership at the micro level combined with robust welfare provision preference for a select group (Van Gunten and Kohl, 2020). These findings update the broader debate on housing-based class and social inequality theories by showing that homeownership alone is not sufficient to fully explain preference changes among younger cohorts. Instead of the typical economic divide between homeowners and renters complementing the class system, housing unaffordability seems to produce new forms of social re-stratification, while creating divisions within social classes that fit into the broader picture of current socio-political tensions. Housing had begun to disrupt social classes, even before housing affordability challenges extended to the middle class. When homeownership expanded to less affluent groups, thereby increasing social mobility among older cohorts, it brought into question the shifting identities and fragmentation of the working class under the guise of expanding the middle class, arguably weakening support for more adequate housing policies (Adkins et al., 2021; Forrest and Hirayama, 2018).

In terms of party choice, our findings do not support the conservatizing effect of homeownership as found in most of the traditional literature (Adler and Ansell, 2020; Ansell, 2014; Paradowski and Flynn, 2015). They align however with more recent findings connecting political parties’ realignment and the housing issue explaining the lack of effect or its reverse influence undermining the conventional renter-homeowner divide along the left-right political spectrum (Beckmann et al., 2020; Hadziabdic and Kohl, 2022). Against our expectations, our results suggest that a shift in the constituency structure—primarily composed of overburdened renters—does not necessarily alter the existing power balance unless it also affects wider income groups’ aspirations and wealth accumulation. The political relevance of such findings lies in how housing unaffordability intersects with the interests of young homeowners, splitting them from one another and thereby strengthening the pro-redistribution coalition, albeit with distinct ramifications depending on the circumstances. In specific contexts, tenure loses its stratification power while aspects of housing unaffordability gain greater significance and are positively associated with support for redistribution and center–liberal party voting. With relatively few countries, some caution is needed in interpreting those findings.

What policy implications arise from our findings? Political preferences and voting patterns are pivotal in shaping housing policies and guiding political parties’ adjustments to align with the demands and expectations of their constituents. While housing unaffordability generally correlates with increased support for welfare redistribution, voters favor center–liberal parties, possibly motivated by shared social values and the belief that economically neoliberal policies benefit new mortgage holders by boosting sales and house prices or advancing credit markets to fill homeownership aspirations. These factors, combined with young renters’ lack of economic and political power in more financialized housing systems, might exacerbate their disadvantage, emphasizing the need for alternative housing solutions.

Our findings update theories on asset-based welfare by indicating that mortgaged homeownership associated with unaffordability might not produce the economic security commonly used to justify such policies. Housing unaffordability generates a sense of economic vulnerability and status loss that ultimately challenges the benefits of asset-based welfare for younger cohorts. This development was a component of a wider transition from public to private debt, cementing a belief of self-sufficiency. This approach is unsustainable for young cohorts confronting a tougher economic landscape and a less favorable policy setting, particularly for those who cannot rely on parental help and for whom renting has become an extended or even indefinite tenure.

Moreover, our research advances the discussion on the emerging sociology of housing field and comparative welfare research by underscoring how housing affordability and its distribution is shaping social stratification and electoral outcomes across different housing systems. The housing market is a complex system embedded in social relations, where competing actors leverage state power to influence and direct it (Bourdieu, 2005). It has historically created precarity and disadvantage for disenfranchised groups. However, the political consequences only become more apparent when housing market pressures extend beyond marginalized groups and begin to affect the middle class. While mortgaged homeowners in unaffordable situations are potentially excluded from the traditional economic gains expected from homeownership, renters are excluded from living in areas where labor prospects are strong, but housing is no longer affordable to them. Both end up experiencing significant insecurity amid economic volatility. The housing cost/household income mismatch intersects with the social, wellbeing, health, economic, spatial, and political aspects of young adults’ lives. It threatens their material status and upward social mobility, hence, young voters seek more social protection. Housing unaffordability likely has a more substantial effect on young adults than indicated here, as our findings do not capture those living with their parents or in other alternative arrangements due to financial constraints. Another critical limitation is the impossibility of considering the urban–rural divide that might account for significant variation.

Further research should explore the impact of affordable housing policies on young adults’ housing outcomes, political and institutional trust, and policy-specific desires. If the desire for homeownership motivates young people’s political engagement, it may lead to outcome contradictions, as deeper mortgage markets have not necessarily increased homeownership much further but are associated with higher housing prices and less affordability.

Supplemental Material

sj-docx-1-cos-10.1177_00207152241295976 – Supplemental material for Housing unaffordability and political preferences among young people in Europe

Supplemental material, sj-docx-1-cos-10.1177_00207152241295976 for Housing unaffordability and political preferences among young people in Europe by Julia Furtado and Lindsay B. Flynn in International Journal of Comparative Sociology

Supplemental Material

sj-docx-2-cos-10.1177_00207152241295976 – Supplemental material for Housing unaffordability and political preferences among young people in Europe

Supplemental material, sj-docx-2-cos-10.1177_00207152241295976 for Housing unaffordability and political preferences among young people in Europe by Julia Furtado and Lindsay B. Flynn in International Journal of Comparative Sociology

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Luxembourg National Research Fund (FNR) [14345912].

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.