Abstract

In this study, we merge the literature on homeownership regimes, which focuses to a lesser extent on the consequences of wealth and social inequality, with the literature on wealth and social stratification, which overlooks the importance of homeownership regimes in contributing to those inequalities. Within this framework, we examine to what extent homeownership regimes shape class inequality in homeownership among young adults and the mortgage debt burden that usually accompanies it. We first develop an updated typology of homeownership regimes that incorporates the role of the family via intergenerational wealth transfers (IWT) such as gifts and housing assets. This dimension was theoretically underdeveloped and empirically absent from previous homeownership typologies. Second, we employ this typology to investigate class-based gaps in homeownership and mortgage debt burden within and between homeownership regimes. This is done by pooling data for a total of 20 countries from two sources: the European Union Statistics on Income and Living Conditions (EU-SILC) 2013–2014 (EuroStat) for EU countries, and the Household Expenditure Survey 2012–2013 (CBS) for Israel. Using multivariate modeling, we find that homeownership regimes in which IWT in the form of financial support is common practice increase class inequality in homeownership compared to regimes in which IWT of assets is common practice. Contrary to the literature suggesting that liberal mortgage markets advance inclusion, it appears that in the homeownership regime characterized by the most liberal housing finance system (which includes Northern European countries and the Netherlands), class inequality in mortgaged homeownership is the widest but class inequality in mortgage debt burden is the narrowest. Homeownership regimes characterized by IWT of assets (which include Southern and Central Eastern European countries) reveal the opposite patterns. We discuss the implications of our findings for the literature on homeownership regimes and wealth inequality, with a specific focus on young adults.

Keywords

Introduction

Most Western societies have experienced an increase in household wealth, mainly through homeownership expansion. Indeed, housing assets play a key role in the household wealth portfolio and in the process of intergenerational wealth transmission (IWT) (Piketty, 2011). Wealth differs from other sources of social inequality in that it is frequently independent of principles of meritocracy. Wealth tends to be accumulated in the family over generations, and access to wealth is often unrelated to one’s own individual efforts and achievements (Hällsten and Pfeffer, 2017; Spilerman, 2004). Evidence for this claim is provided by the relatively low correlation between household income and wealth across countries (Fessler and Schürz, 2018; Korom, 2018; Pfeffer and Waitkus, 2021).

Over the past several decades, scholars of social stratification have been paying closer attention to wealth inequality and housing assets in particular as important dimensions of social stratification (Killewald et al., 2017; Semyonov and Lewin-Epstein, 2013; Spilerman, 2004). For most households, housing comprises by far the largest share of household wealth, and its economic, social, and symbolic significance set it apart from other forms of wealth (Pfeffer and Waitkus, 2021; Semyonov and Lewin-Epstein, 2013). Hence, investigating the institutional context of achieving homeownership as well as the barriers and opportunities it provides is crucial for a better understanding of socioeconomic inequality. Indeed, a corpus of studies found large differences in levels of homeownership and the level of homeownership inequality across countries (Kolb et al., 2013; Kurz and Blossfeld, 2004; Wind and Dewilde, 2019; Wind et al., 2017), as well as class inequalities in mortgage debt for the young and the elderly (Bicakova and Sierminska, 2008; Lewin-Epstein and Semyonov, 2016; Martins and Villanueva, 2006).

While the above studies considerably advance our understanding of wealth inequality and social stratification more generally, they do not pay sufficient attention to the institutional structures that shape these inequalities. In our view, it is necessary to assess the role of societal arrangements that structure access to housing in order to gain a fuller understanding of differences between countries and inequalities within countries. In order to fill this gap, we turn to a growing body of literature on housing regimes. The literature on housing regimes has illuminated important differences in the housing landscape across countries (Hoekstra, 2003, 2005; Kemeny, 1995; Blackwell and Kohl, 2019; Mulder and Billari, 2010; Schwartz and Seabrooke, 2008), but its potential has yet to be fully realized when it comes to addressing the implications for socioeconomic stratification within and across societies (for exceptions, see Dewilde and De Decker, 2016; and Wind et al., 2017, which focus on the elderly or the rental sector). That is, the literature on housing regimes is focused more on the dynamic between the macro-level institutions (government programs and the mortgage market) that generate different kinds of housing regimes than on how those structures generate homeownership and mortgage debt burden variation at the household level, thus influencing future wealth accumulation.

Our central rationale for reframing a homeownership typology is based on the socioeconomic context in which the present-day generation of young adults is situated. This context includes institutional shifts that pose a significant challenge to access to first-time homeownership, which is an event typically coupled with young adulthood (McKee et al., 2017). The present cohort of young adults lives in a time of greater uncertainty and instability than their parents (Breidenbach, 2018). This particular socioeconomic context includes relatively high unemployment rates (Scarpetta et al., 2010), income stagnation in many Western countries (Vogel, 2017), and shrinking welfare benefits (Taylor-Gooby, 2016). Furthermore, recent decades have witnessed rising housing prices, with more households taking out higher mortgage loans at a time of intensified mortgage market financialization (Aalbers, 2008; Van Gunten and Navot, 2018). Not only do young adults have insufficient net income to keep pace with increasing housing prices, but they also hold higher non-housing debt (mainly student loans) than their parents’ generation (Fuller et al., 2020). Hence, the bulk of studies show that homeownership is less affordable for the current cohort of young adults as compared to earlier cohorts situated in different social contexts, while those who are able to achieve homeownership face a greater mortgage debt burden (e.g. Breidenbach, 2018; Cohen Raviv, 2021; Flynn and Schwartz, 2017; Ronald, 2018). This economic environment intensifies the dependence of young adults on intergenerational assistance and has triggered a shift toward re-familialization (Flynn, 2020; Flynn and Schwartz, 2017; Isengard et al., 2018; Ronald, 2018). This in turn increases intergenerational and intra-generational inequality in homeownership and thus prospects of future wealth accumulation. Young adults who have the benefit of properties or financial transfers from their family are at a great advantage. In our view, these developments underline the need to reframe the relationship between social institutions when studying inequality in homeownership and the mortgage debt burden.

Our two research aims are as follows: first, we aim to investigate the circumstances of young adults vis-à-vis homeownership tenure and mortgage burden and how these circumstances are mitigated by institutional arrangements set in place in various countries. Second, we aim to examine class disparities in homeownership tenure and mortgage burden across different institutional arrangements. By combining the framework of homeownership regimes with the research literature on social stratification, we aim to contribute to the two bodies of scholarship in the following ways: first, we construct a typology of homeownership regimes that accounts for the role of the family (via IWT and its different forms), which was theoretically underdeveloped in and empirically absent from previous homeownership typologies. The purpose of doing so is to address the differentiated circumstances of young adults, typically first-time homeowners, across societies. We do so by introducing the family and IWT into the homeownership regime framework. Our typology is also based on updated macro-level data after the Global Financial Crisis (GFC) period, which also represents the climax of the financialization era thus far, and on an advanced statistical tool. Second, implementing the new homeownership regime typology allows us to investigate the magnitude of class differences in homeownership and mortgage debt burden among young adults within and between homeownership regimes. In doing so, we highlight the role of institutional structures in generating and maintaining inequality in the potential to accumulate wealth. Third, we account for the geographical region of Central Eastern Europe (CEE), which is often neglected in cross-national studies of homeownership and wealth inequality, since it is considered to consist of super-homeownership societies. Yet some of the countries in CEE have witnessed a trend toward increasing wealth inequality comparable to the situation in France and Germany (the latter is one of the most unequal countries in the European Union (EU); Brzeziński et al., 2020), and young adults living in these areas are struggling to access homeownership in the absence of IWT (Makszin and Bohle, 2020; Mandic, 2008). Our research also provides policy-related insights, since we show how class polarization in homeownership and associated mortgage debt differ in accordance with institutional practices in the housing market.

The significance of homeownership for wealth and social inequality

Homeownership increases owners’ stake in society and situates households within the social order (Kemeny, 1995). Homeownership also contributes to higher levels of subjective wellbeing and life satisfaction since it is accompanied by a sense of shelter, stability, and security for the household unit (Elsinga and Hoekstra, 2005; Spilerman, 2004). Moreover, in most advanced economies, the value of housing increases over the long run, and for most families homeownership is a major source of wealth accumulation (Scatigna et al., 2014; Spilerman, 2004). Homeownership also provides economic security against periods of strong inflationary trends (Forrest et al., 1990) and the consequent weakening of the “welfare state.” One significant example of this is the notion of “asset-based welfare,” in which security in old age is ensured through homeownership financed by a housing mortgage rather than a pension (Doling and Ronald, 2010). Given the wealth potential embedded in owning a home, declining rates of homeownership among the young in advanced economies over recent decades is a source of concern (Lennartz et al., 2016). Homeownership is also laden with symbolic power, since homeownership and home value are highly visible representations of status (Bourdieu, 2005: 19). Thus, owning a more valuable home than the average for that age cohort can play an important role in establishing a young household’s status by showing that it is “ahead” in the accumulation of material goods (Henretta, 1984).

Homeownership may also produce financial risks, as is true of markets more generally. The price of housing (and the value of home equity) may decline, or rise, as a result of economic cycles, changes in the attractiveness of a location, and unforeseen external shocks (Killewald and Bryan, 2016). Furthermore, vulnerability to risks associated with homeownership is unevenly distributed among social classes and is influenced by the level of generosity of the welfare state (Beck, 1992; Giddens, 1999). One remarkable example is the GFC in 2008, which led to home depreciation and financial crisis for many households in the United States that relied on leveraged mortgages and changed attitudes toward mortgaged homeownership as a secure investment and a means of accumulating wealth (Dwyer et al., 2016; Wolff, 2016). Yet mortgage loans are the main route of attaining homeownership, especially among young adults from the lower and middle classes who have limited family resources and support. Economic risks notwithstanding, such loans not only provide access to security and stability but are also important drivers of social mobility. Differences in access to mortgages and homeownership are therefore fundamental sources of wealth and social inequality (Kolb et al., 2013; Kurz and Blossfeld, 2004; Lewin-Epstein and Semyonov, 2016). Although homeownership may entail risks of financial loss, it is important to note that housing assets have led to more long-term wealth accumulation than other forms of financial investment across advanced economies (Jordà et al., 2019).

Homeownership regimes—current state of research

We draw on the theoretical construct of “homeownership regimes” to understand how institutional arrangements are linked to stratified housing outcomes for young adults. Homeownership regimes represent ideologically driven power relations between the state, housing-finance systems, and the family that cut across a number of countries. Consequently, one can identify clusters of countries with broadly similar regimes (Dewilde and De Decker, 2017; Kemeny, 1995). Several typologies of housing regimes exist in the literature, some focusing on rental arrangements and others on homeownership. With regard to the former, the most familiar classification in this field was proposed by Kemeny (1995, 2006). He distinguished between integrated rental systems in countries with corporatist social structures and dual rental systems, which exist mostly in countries with liberal social structures (along with several Scandinavian countries). Hoekstra (2003) compared Kemeny’s housing-regime typology with the typology of welfare states (Esping-Andersen, 1990) and found that they did not necessarily overlap as in the case of the Netherlands. Other typologies of housing regimes address aspects of housing affordability and link macro- and micro-level factors (household characteristics) among entire populations (André and Chalaux, 2018) or among the elderly and the poor (Dewilde and DeDecker, 2016; Mulder et al., 2015; Wind et al., 2017), but they also focus primarily on the rental market (both private and public).

A second strand of the housing-regime literature focuses on homeownership. Scholars who develop typologies of homeownership regimes often point to the welfare state–homeownership “trade-off” hypothesis. In countries with poor public welfare provision for the elderly, households are forced to make private provision for old age through homeownership, which is a form of investment. In countries dominated by public housing, by contrast, housing is more likely to be perceived as a social right (Castles, 1998; Schwartz and Seabrooke, 2008). One of the prominent homeownership typologies was proposed by Schwartz and Seabrooke (2008). They founded their typology on two macro dimensions (mortgage debt to gross domestic product (GDP) and homeownership rate) for the period before the GFC. The clustering of countries in their homeownership regimes mostly confirmed the trade-off hypothesis. Furthermore, the housing regimes they proposed partly overlapped with Esping-Andersen’s social democratic and corporatist/conservative groups.

Taking a historical perspective, Blackwell and Kohl (2019) recently developed a housing typology which is constructed along three dimensions across decades and countries: social expenditure from GDP, mortgage debt to GDP, and homeownership rates. On the basis of this typology, they reported two major findings: first, they found a negative correlation across time and countries between homeownership rates and mortgage debt per GDP, although in certain countries this relationship tended to be positive. Second, the correlation between social expenditure as a proportion of GDP and homeownership rates tended to be negative after the Second World War but changed to no correlation or even a positive one from the 1980s on in Western EU countries (Blackwell and Kohl, 2019; Tranøy et al., 2020; Van Gunten and Kohl, 2020). Thus, they suggested that the “trade-off” hypothesis described above slowly fades out. Other researchers proposed housing-regime typologies based on the same dimensions but with more empirical indicators and focused on the elderly population’s homeownership (Mulder and Billari, 2010; Wind et al., 2017).

While the above-mentioned scholarship acknowledges the “latent” role of family when it addresses access to homeownership, it does not fully incorporate it into the theoretical rationale of housing regimes and lacks empirical measures of the role of the family in access to homeownership. Variation in intergenerational economic assistance across countries is an important factor both in the dynamic with macro-level institutions and in the generation of inequality in homeownership at the household level. Since the present cohort of young adults is characterized by greater dependency on their parents’ financial resources through money or asset transfers (Albertini et al., 2007; Isengard et al., 2018; Ronald, 2018), we believe that this dimension ought to be accounted for when constructing a typology of housing regimes as a framework for the study of young adults’ access to housing. Here, we offer a twofold contribution by merging two strands of literature: typologies of homeownership regimes and wealth and social inequality. Therefore, we incorporate the family assistance dimension both theoretically and empirically in the construction of our typology of homeownership regimes.

A multidimensional typology of homeownership regimes

Theoretical dimensions

The homeownership regime typology we constructed incorporates three important social institutions: the state, the (mortgage) market, and the family. Through the policies it develops, the state shapes the forms and mix of housing tenure. As regulator, the state regulates not only the housing market but also the mortgage market. These regulations are embedded in a country’s history, reflecting the cultural values and pervasive ideologies and interests of various social agents with regard to housing tenure. For example, countries with corporatist legacies place greater emphasis on housing as a dwelling unit and the stability associated with renting (Blackwell and Kohl, 2019), rather than on the asset value of housing and its role in building household wealth. Thus, housing policies that heavily regulate and subsidize the rental market make purchasing a home less necessary for families, while a regulated private rental market makes housing assets less attractive for investors (Kholodilin et al., 2018; Wind et al., 2017).

In the Anglo-Saxon countries, citizens are more dependent on the value of their housing as a form of insurance. Hence, when housing prices are inflated they will be less supportive of generous welfare provisions (Ansell, 2014, 2019; Castles, 1998; Kemeny, 1981; Schwartz and Seabrooke, 2008). After the housing bubble burst, however, support for the welfare state increased accordingly among citizens (Ansell, 2014). In rental societies, by contrast, housing costs are more evenly spread over an individual’s life cycle, and thus voters will adopt a more positive stance toward increasing taxes to fund generous welfare programs (Kemeny, 2006). Kohl (2018) found that a homeownership ideology was supported not only by right-conservative parties but also by center-left parties that usually support state-based housing provisions in order to attract voter support. The culture of homeownership, then, is historically shaped by a country’s housing tenure arrangements and at the same time shapes these arrangements through the political process. Furthermore, this culture is transmitted across generations largely through socialization in the family (Aassve et al., 2002; Henretta, 1984; Lersch and Luijkx, 2015).

Countries also vary in the extent to which their mortgage market is accessible and inclusive, which is governed by the level of state intervention. When mortgage loans are easily accessible, they are widely used, which facilitates entry into homeownership, but when they are less accessible and costlier, homeownership based on mortgage loans is likely to be less prevalent (Mulder and Billari, 2010). Different mortgage market practices exist, and they indicate the level of inclusiveness and attractiveness of the mortgage loans in a given country (Fuller, 2015). Some examples are the maximum loan-to-value (LTV) ratio, the highest mortgage loan in relation to the value of the housing bought that the bank is willing to provide a household; tax relief for mortgage loans, which serves as an incentive for buyers to purchase housing assets; mortgage maturity in years, which suggests that when the duration of taking out a mortgage loan is longer, households can lower their monthly mortgage repayment for a longer time, which makes mortgage loans affordable for a larger share of the population; and low taxes on capital gains, which makes it more attractive to purchase an asset for purposes of property speculation (Fuller, 2015; Van Gunten and Navot, 2018). A recent study suggests that due to an institutional shift after the GFC, the mortgage market practices described above are not necessarily a reflection of the level of inclusion but of the level of mortgage market intensification (Van Gunten and Navot, 2018). In other words, after the GFC most countries placed more restrictions on mortgage borrowing, meaning that those able to borrow now bear a higher amount of mortgage loans and thus a higher level of risk.

The third component that is essential for establishing our typology of homeownership regimes is the institution of the family. Its role in shaping the life chances of young adult offspring is gaining in importance, as labor market security is reduced and the welfare state is retracting. Hence, the family’s role with respect to housing should be understood in the context of what is often referred to as the (inter)generational contract or intergenerational solidarity. Generational solidarity has long been present in the discourse on social welfare but is less prominent, although not absent, from research on housing. Importantly, students of the family have noted that the extent and forms of the generational contract change over time (Komp and Van Tilburg, 2010) and vary across cultures and in relation to societal institutional frameworks (Szydlik, 2008). With respect to housing, studies have pointed out that the preference for homeownership is transmitted through family socialization, raising the likelihood that children who grew up in family-owned homes will seek to achieve such a status as well (e.g. Henretta, 1984; Lersch and Luijkx, 2015). More importantly, for the present study, housing is a major axis of the social reproduction of socioeconomic inequality due to the growing role of housing in maintaining and increasing household wealth.

Intergenerational economic support for young adults increases their ability to achieve homeownership both directly, by providing the necessary financial resources, and indirectly, by improving access to mortgage loans. Such financial transfers from parents, or other family members, allow their offspring to purchase a home earlier in life, to make larger down payments, and to acquire higher value property (Spilerman and Wolff, 2012). Hence, the equity accumulated in housing assets is passed down through generations and supports the persistence of inequality (e.g. Pfeffer and Killewald, 2018; Spilerman, 2004). IWT is therefore a mechanism of social reproduction with respect to the accumulation of future wealth. While the above is generally true, it should be noted that the importance of the family with respect to housing tenure varies across countries with different institutional arrangements. The level and form of IWT that is prevalent in a country depends on the relationship between the family, the state, and the housing-finance systems. Taken together, they structure the opportunities available for parents to provide specific forms of financial aid and to meet their children’s needs accordingly (Isengard et al., 2018). The homeownership regimes we generate in the following reflect those differences in IWT patterns.

Empirical indicators and empirical strategy

Representing the institutional dimensions

Keeping in mind the theoretical considerations described above, we now turn to the operationalization and the empirical strategy for deriving our homeownership typology. We operationalized the three dimensions above using two indicators for each of them (six indicators in total). State policies and cultural preferences that advance homeownership are proxied by the share of homeowners in a given country on the one hand (Hypostat, 2012–2015) and by regulations that protect the rental sector on the other (hereafter, rent control). The latter is a quantitative variable that measures the extent to which the government regulates initial rent levels and the ongoing rent increase that landlords can demand from tenants (ranked 1–5 by the OECD, 2016). A higher score on this dimension means that higher rent controls are imposed by the state; a lower score means that the initial rents and ongoing rents are freely negotiated between landlord and tenant. 1

In order to capture the mortgage-market dimension, we used two indicators that take account of differences in mortgage-market activity/intensity and accessibility, permitting between-country comparisons. The measures are the ratio of total outstanding residential loans to GDP and the maximum LTV ratio for first-time home buyers (Hypostat, 2012–2015; additional sources are detailed in Table 7 in Appendix 1). The ratio of total residential loans to GDP indicates how active/intensive the mortgage market is within a country (Benchetrit and Carmon, 2006).

A higher residential loan to GDP ratio indicates that homeownership is mainly achieved by mortgage loans, while lower levels indicate alternative means of attaining homeownership, such as IWT. The maximum LTV ratio represents the level of liberalization and the risk that housing-finance institutions are willing to absorb in the case of default (Fuller, 2015, p. 255). Higher maximum LTV ratios enable lower-income population access to the housing market with relatively low levels of initial equity. Housing finance systems with a higher maximum LTV ratio are therefore more inclusive (Wind et al., 2017). Although these dimensions are quite similar, the latter relates to mortgage-finance conditions, while the former indicates the final results of the mortgage market (e.g. the same country can have a relatively high maximum LTV ratio and a relatively low residential loan to GDP ratio).

We used two indicators at the country level to capture the role of the family institution and how it interacts with the state and the mortgage market to structure housing opportunities for young adults. Both indicators capture the prevalence of resource flows across generations. The first measure is a macro indicator of the share of young adults in the country that received monetary transfers (gifts or inheritance) from family members. The second measure indicates the share of young adults in a given country that received housing assets from family members (HFCS database, 2017; self-calculated). Although both are a form of IWT, financial transfers are generally quite small in terms of home purchase and would still require access to the mortgage market, whereas transfers of housing assets usually have higher wealth values and also provide a housing solution. Unlike IWT in the form of financial assistance, the transfer of housing assets provides a domicile, typically eliminates mortgage payments, and provides an asset that may appreciate in value in tandem with the housing market (Isengard et al., 2018; Killewald and Bryan, 2016).

Constructing the typology

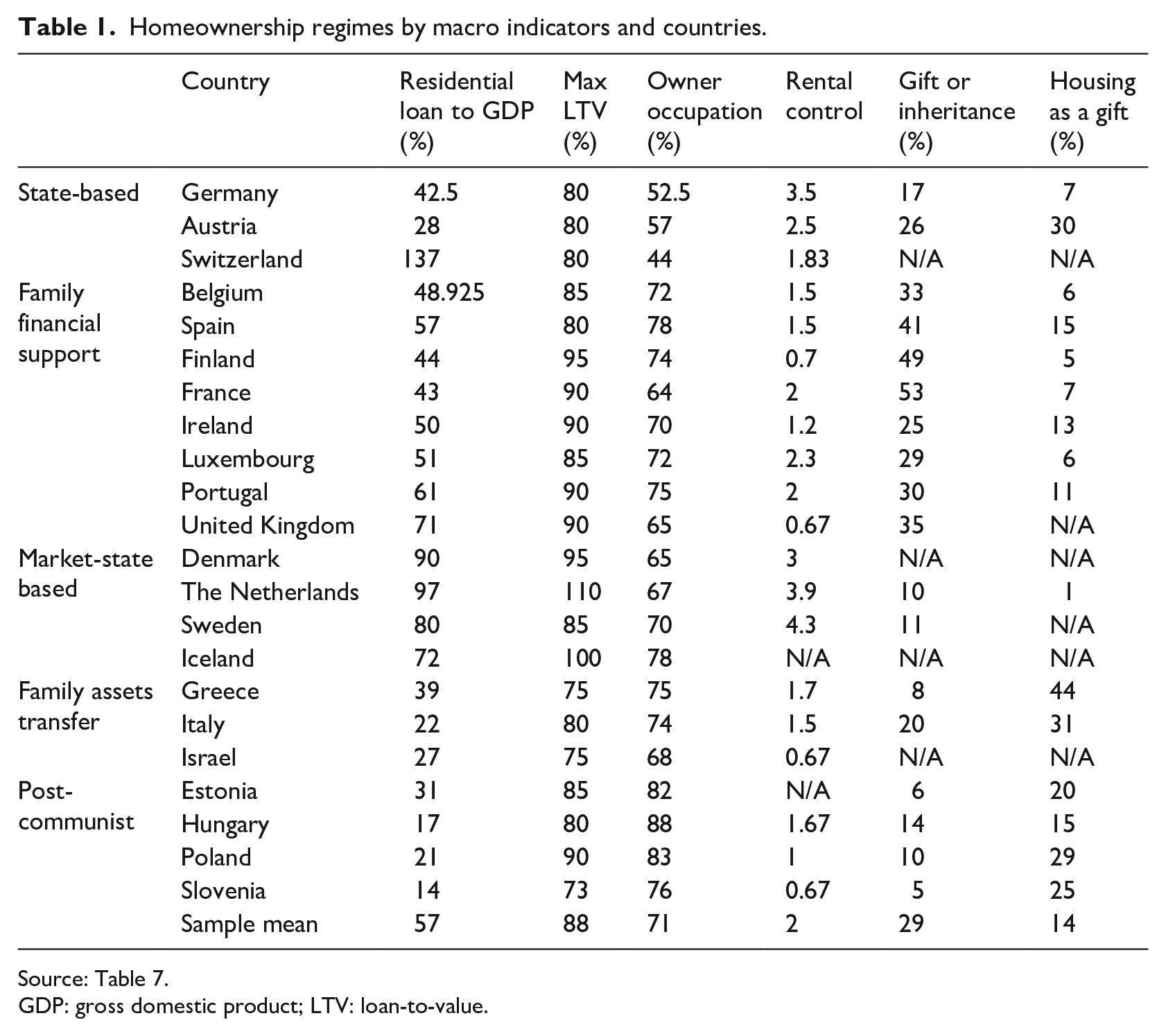

The reader should bear in mind that a typology of homeownership regimes aims to depict fairly distinct institutional arrangements and to classify countries into groups on the basis of similarities with regard to these institutional arrangements. Our strategy was to consider the three institutions and their measurements simultaneously, as well as to determine how countries are grouped with respect to these institutions. To do so, we employed cluster-analysis techniques. This is the most suitable method for creating an appropriate statistical grouping of the countries that are most similar to one another along these dimensions. Because the typology includes indicators on different scales, we standardized all indicators via z-scores. We used K-means cluster analysis to ascertain empirically how the countries were grouped on the basis of their distance from the mean (centroid) on each of the six dimensions. The K-means algorithm identifies the optimal k number of centroids and then allocates every observation to the nearest cluster, while keeping the distances from the centroids as small as possible (Morissette and Chartier, 2013). Hence, the most similar countries are grouped together and are distinguished from other countries that cluster in other groups. 2 To measure the similarity between observations, we used squared Euclidian distance metrics, which is the most common method. 3 The analysis resulted in five distinct clusters (i.e. homeownership regimes) characterized by different scores on the state, mortgage market, and family dimensions. The results are presented in Table 1.

Homeownership regimes by macro indicators and countries.

Source: Table 7.

GDP: gross domestic product; LTV: loan-to-value.

Table 1 shows the list of countries included in the analysis and the regimes to which they were classified on the bases of their institutional characteristics. The names given to the regimes best describe the way in which homeownership is acquired. We referred to the first cluster as the state-based regime, which includes Austria, Germany, and Switzerland. In this regime, the mortgage market is relatively less accessible for young adults with a relatively low maximum LTV ratio, which means that a high down-payment is needed for first-time homeownership. It is also characterized by the lowest homeownership rate among European countries, alongside a highly controlled rental market, which results in relatively low residential loans to GDP ratio. Switzerland is an exception with respect to the latter measure, as it had the highest residential loans to GDP ratio in the sample. This high level of activity of the Swiss mortgage market is not a result of accessible mortgage loans for young adults but a combination of a high housing price and extremely low interest rates (negative even in 2014), which attracts investors to the housing market (Baselgia and Martínez, 2020). Gifts and housing inheritance are less customary in the German-speaking countries as well. Austria, by contrast, has a high housing inheritance rate. This can be explained by the increase in housing prices in Austria coupled with decreasing public housing subsidies in the last decade (Wagner, 2014). The countries in this regime were classified into different regimes in the typology of Schwartz and Seabrooke (2008; “corporatist-market” and “statist-developmentalist”) but clustered similarly to the regime suggested by Wind et al. (2017; “regulated rental”).

The second regime is the family financial support regime. It is the largest cluster and consists of mostly Western countries but also some southern European countries and Finland. It is characterized by high percentages of IWT of gifts and low percentages of asset transfer, which explains the classification of these countries here. This regime is also characterized by a generous mortgage market represented by high maximum LTV ratios but with medium-low activity on the mortgage market. Homeownership rates are at medium-high levels, and so are the rent-control levels. In Western EU countries, the welfare state is generous, the economic security of the elderly and children is seen as the state’s responsibility, and the rental market is highly regulated (Albertini and Kohli, 2013; Albertini et al., 2007; Isengard et al., 2018; Ronald, 2018). Thus, parents are more financially secure and can provide their children help in the form of gifts (inter-vivo financial transfers) to make down payments on mortgage loans or to deal with adverse life events. This enables young adults to leave the parental home at an earlier stage compared to the Mediterranean countries. Renting is considered an acceptable alternative to ownership in some of the countries included in this regime.

In previous typologies, Spain and Portugal were classified into a familial regime together with other Mediterranean countries that are characterized as favoring asset transfers over money transfers to their children (Mulder and Billari, 2010; Wind et al., 2017). The classification of these countries into this regime type reflects changes in IWT patterns in Spain and Portugal. This might be explained by the fact that the housing construction boom and housing price increases benefited the elderly prior to the GFC, enabling them to make inter-vivo transfers to their children (Hoekstra et al., 2010), while the post-GFC period forced a large share of young Spanish adults into the rental sector (Azevedo et al., 2019). The United Kingdom, with its neoliberal political economy, and Finland, with a social democratic political economy, are also classified here due to a high prevalence of family financial support. The clustering of this mix of countries from different geographical EU areas with diverse political economies illustrates the importance of taking into account the role of family when classifying countries into homeownership regimes. Incorporating the institution of the family into the construct of housing regimes highlights certain similarities across countries not captured in previous typologies. Here, countries are classified differently than in previous homeownership typologies (Blackwell and Kohl, 2019; Castles, 1998; Mulder and Billari, 2010; Schwartz and Seabrooke, 2008; Wind et al., 2017). It is also an indication that family economic support to offspring is increasingly being extended into young adulthood.

The third regime is the market-state regime, which includes most northern EU countries and the Netherlands. It is characterized by high levels of mortgage accessibility, high homeownership rates, and high rent control. At the same time, countries associated with this regime have relatively low levels of IWT of both gifts and assets. In this regime, homeownership is normalized through a generous housing-finance system, alongside tightly controlled public rental housing provided for the majority of the population, with a specific focus on the lower class in Sweden and Denmark (Jensen, 2013). Housing-finance systems in the countries included in this regime have been extensively liberalized since the financialization of housing in the 1980s (Aalbers and Christophers, 2014). For example, LTV ratios of over 100 percent became common in Denmark, Sweden, and the Netherlands at the beginning of the 21st century, as financial institutions were allowed to pass on risks to third parties in the form of residential mortgage-backed securities (RMBS) (Wind et al., 2017). Although interest-only mortgages became the most popular means of financing housing in the Netherlands (Scanlon et al., 2008), homeownership is not considered the norm, and renting is seen as an acceptable and suitable alternative (Mulder and Billari, 2010). A recent study argues that the generous welfare states in the northern EU countries increase creditworthiness and have thus encouraged financialization of housing. This in turn undermines the solidaristic structure of these countries, resulting in mortgage accumulation and re-familialization (Tranøy et al., 2020).

The fourth regime is the family asset transfer regime. It includes Mediterranean countries and is characterized by low residential loans to GDP, low maximum LTV ratios, low levels of rent control, and relatively high rates of homeownership. Most importantly, it is characterized by high rates of IWT of housing assets and low rates of IWT of gifts. In Mediterranean countries, housing-finance systems are strict and public spending on family benefits are relatively low (OECD, 2019a). These countries also display a legacy of homeownership, while the rental market is tight and expensive, due to a mismatch between supply and demand, exacerbated by stagnating incomes (Azevedo et al., 2019; Modena and Rondinelli, 2011). This in turn increases the dependency of children on their parents’ resources. Thus, it is more common in the Mediterranean countries to provide IWT in the form of housing assets or space (co-residence). In this regime, young adults leave the parental “nest” at an older age (Aassve et al., 2002), and the family serves as a “shock absorber” for economic and employment downturns (Moreno and Marí-Klose, 2013).

The fifth cluster comprises post-communist countries. It shows the lowest level of residential loans to GDP and maximum LTV ratios, together with low rent control levels. Yet these countries also have the highest homeownership rates in the sample, with high rates of IWT of housing assets and low rates of IWT of gifts. This cluster of countries resembles the previous cluster, but with significantly higher homeownership rates. It is also exceptional in the sense that homeownership in these countries did not run through the financialization process but was due to the fall of the communist regimes and the privatization of social housing. With the fall of the communist regimes and the transition to the free market, tenants were given the opportunity to purchase their homes below market prices. This was a widespread practice, which created the super-homeownership societies in the CEE region we are witnessing today (Stephens et al., 2015). However, because mortgage markets remain relatively underdeveloped and the rental market is kept marginal, young adults are mainly dependent on their family resources to provide access to homeownership, as in Mediterranean Europe (Makszin and Bohle, 2020; Mandic, 2008). One implication of this situation is that young adults make the transition to first-time homeownership later in life, postponing their family formation stage, which also leads to decreasing fertility rates in the CEE region (Makszin and Bohle, 2020).

We used our typology to examine homeownership tenure inequality among young adults. Specifically, our aim was to investigate class disparities in homeownership and mortgage burden within and across homeownership regimes.

We chose to signify class location in the stratification system using Weber’s (1978) definition of “class,” according to which the possession of material resources, accumulated through advantages in the market, results in distinctive standards of living. We therefore focused on “income class” as the main mechanism influencing homeownership tenure pathways and mortgage debt at the household level. Moreover, we also considered income class since household income is often the main criterion for receiving mortgage loans from financial institutions (“income class” and “class” will be used interchangeably here). Given the attributes of the various homeownership regimes described above, we expected that they would result in the following systematic differences in the extent of class-based gaps in young adults’ housing tenure and their mortgage debt burden:

Hypotheses

(H1) In the homeownership regimes characterized as family-asset transfer and post-communist, we expected relatively narrow class-based gaps in the probability of mortgaged homeownership, since mortgage loans are a less common practice in those regimes for the majority of the population. We also expected the highest share of outright ownership in these regimes due to the common practice of IWT of housing assets. This in turn should contribute to a narrow class-based gap in outright ownership compared to other regimes. We also expected a high share of mortgaged homeownership in the family financial support regime, with the parental cohort providing financial aid with mortgage down payments. However, we expected households that did not benefit from IWT of gifts to have less access to mortgage loans. Therefore, we expected that this would in turn result in a relatively wide class-based gap in mortgaged homeownership in this regime compared to other regimes.

(H2) Due to the high level of liberalization and generosity of the housing finance system in the market-state regime, we expected high class-based gaps in the level of mortgage debt burden in this regime, as those from the lower class would be able to receive relatively large mortgage loans compared to similarly placed households in the family-asset transfer and post-communist regimes. In the latter regimes, housing finance systems are more conservative, access to mortgage loans is relatively restricted, and mortgage loans are more carefully tailored to individual means. Thus, we expected narrower class-based gaps in the level of mortgage debt burden among the family asset transfer and post-communist regimes. Since the state-based regime is coupled with a conservative housing finance system and a lack of family financial aid, we expected a low class-based gap in the level of mortgage debt burden as well.

Data and sample

Our analysis was carried out on 19 European countries and Israel. For the empirical analyses, we used the cross-national EU-SILC (European Union Statistics on Income and Living Conditions) surveys for 2013 and 2014. The European Statistical System (ESS) has been conducting the survey since 2004. The objective of this survey is to collect multidimensional microdata on income, poverty, social exclusion, and living conditions. The EU-SILC covers a wide range of EU countries with information on homeownership and household mortgage debt intensity (for comparison, the HFCS of the ECB lacks information on Northern EU countries and the United Kingdom). We chose these particular years to represent the period after the GFC in 2008. For the purpose of the present study, the unit of analysis is the household, because housing tenure and mortgage debt is best viewed as a characteristic of the household rather than of the individual (Lewin-Epstein and Semyonov, 2016; Spilerman, 2004). We included in our sample 19 European countries which have a sufficient number of observations of young-adult household heads: Switzerland, Denmark, Luxemburg, the Netherlands, Sweden, the United Kingdom, Austria, Belgium, Finland, France, Ireland, Iceland, Greece, Spain, Italy, Estonia, Hungary, Poland, and Slovenia. We combined the 2013 and 2014 waves to increase the sample size. In the EU-SILC, financial information for the household was reported by one or two members of the household, who were designated as “responsible for the accommodation.” The first respondent was chosen as the household’s financial representative. Our study focused on the cohort of young adults in the age range 25–40. 4 The total sample size for both years was n = 32,949 households.

Israel was added to the analysis due to the similarity of its political, economic, and welfare structures to those of the Mediterranean European countries (Gal, 2010). Data for Israel were drawn from the Household Expenditure Survey for the years 2012–2013. This survey, which is conducted by the Israel Central Bureau of Statistics (CBS), is a repeated, cross-sectional survey that collects data on households’ standards of living. It was possible to merge the Israeli data with the European data due to similarities in the meanings and manipulations of the variables. For the purpose of the present study, we collected data only from the household’s financial representative. The final Israeli sample size for both years is n = 1793 households. After merging the Israeli sample with the European sample, we obtained a final sample size of 20 countries and 34,742 households.

Variables

We constructed two variables to assess the prevalence of homeownership among young adults and the size of their mortgage debt burden. The first is housing tenure and includes three categories: renter, mortgaged homeownership, and outright ownership. The second variable, relative repayment, captures the household’s mortgage debt burden and measures the monthly repayment of mortgage debt and mortgage interest on the main residence as a proportion of the household’s total disposable income. For ease of interpretation, we multiplied the proportions by 100. Total disposable household income refers to household net income from all sources. We used disposable household income rather than gross household income in order to reduce the effect of differences in tax policies between countries, thereby making the data more comparable. The variable relative repayment was created solely for households with both mortgage debt and income.

As previously mentioned, the main predictor variable in our analysis is income class. The literature proposes various ways of operationalizing income classes, mainly by defining the middle class through a measure of households situated above the poverty line and by grouping income percentiles or quintiles (Pressman, 2015). Following Estache and Leipziger (2009) and Atkinson and Brandolini (2013), we used the “income polarization definition,” which highlights the extremes by defining the low and high classes as relatively small, homogeneous categories. In this formulation, the middle class is made up of the three central quintiles of income distribution (i.e. 60% of the population), whereas the lower and the upper classes are made up of the lowest and highest quintiles, respectively. This relative definition of income class makes it possible to compare those in similar (relative) class positions across countries, taking into account differences in individual countries’ purchasing power parity.

In the multivariate analysis, we controlled for a number of household socio-demographic variables that have been found to be highly correlated with housing tenure and mortgage debt (Lewin-Epstein and Semyonov, 2016). Education level is based on the highest ISCED level attained (International Standard Classification of Education, 2011) and is grouped into three categories: “non–high school graduation,” “high school” (including vocational education and non-academic tertiary education), and “academic education.” Marital status is a binary variable for which a value of 1 denotes “married” and a value of 0 “otherwise” (i.e. single, divorced, separated, or widowed). In the case of young adult households, the percentages in the last three categories are very low. 5 Employment status is a binary variable for which 1 denotes “employed households” and 0 denotes “unemployed or not in the labor force.” (The sample characteristics are exhibited in Table 2 in Appendix 1.) Nationally is a binary variable for which 1 denotes “European nationality” (or Israeli nationality in the case of Israel) and 0 denotes “non-European nationality” (or non-Israeli nationality in the case of Israel). Gender is a binary variable for which 1 denotes “female” and 0 “male.” Age (centered) is a continuous variable indicating the age in years of the household representative and is mean centered. Household size (centered) is also a continuous variable indicating the number of individuals living in the household and is mean centered. In the multivariate models, we also controlled for country dummies to address macro-level differences among countries with similar housing regimes. 6

Findings

Descriptive statistics of housing tenure and mortgage debt burden by income class

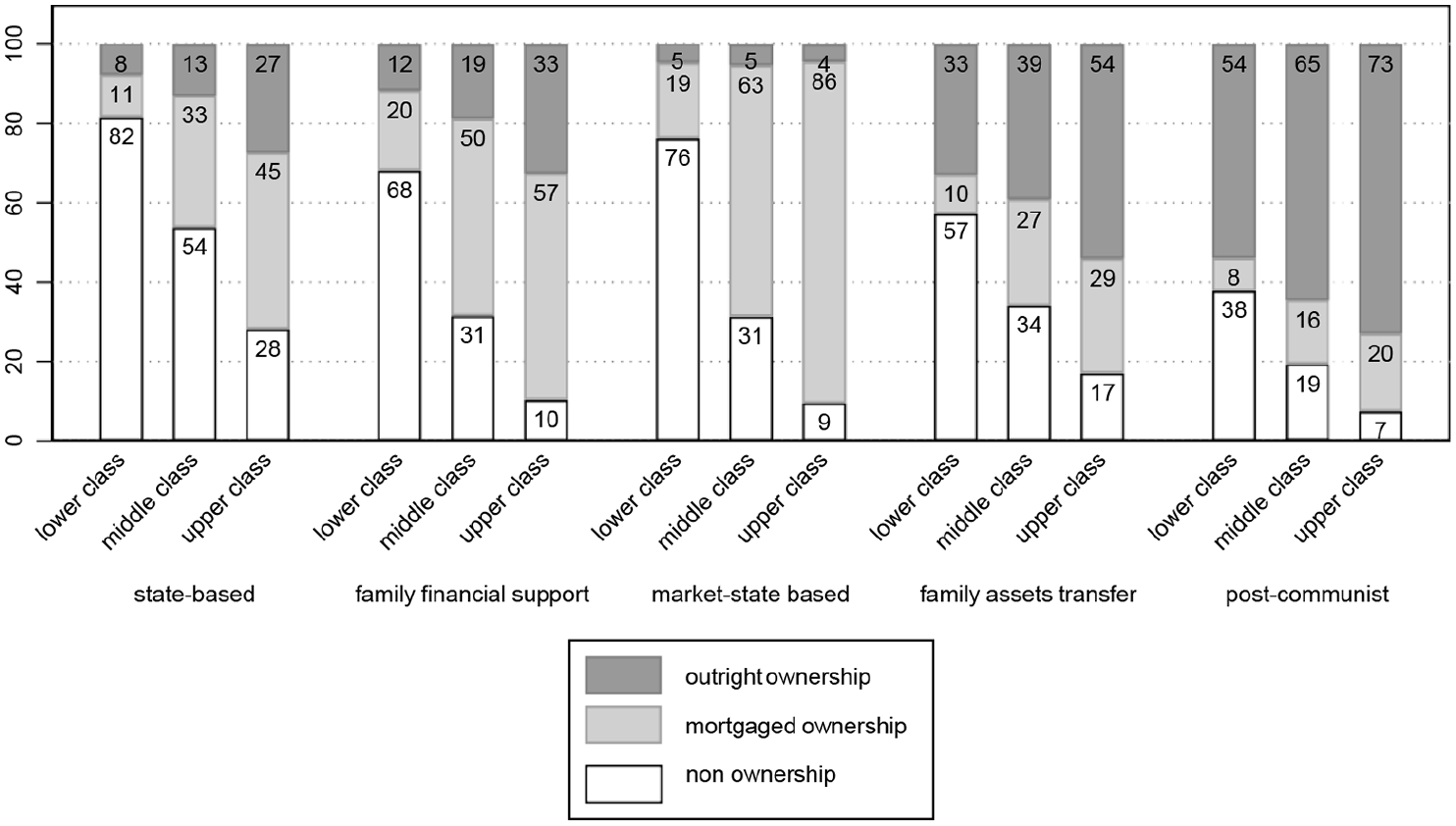

Figure 1 shows the rates of the different housing tenure categories according to income class and homeownership regime. The figure reveals a stratified pattern of outright ownership or mortgaged homeownership according to income class for all regimes. That is, in all five regimes, young households in the upper class are more likely than those of other classes to own a home, with or without mortgage debt, followed by the middle class, and then the lower class. However, class-related patterns of the different categories of housing tenure are structured distinctively within the homeownership regimes.

Percentage of housing tenure, by income class and homeownership regimes.

As expected, the post-communist regime reveals the highest percentages of outright ownership among all income classes, with more than 50 percent of young adults from the lower class and more than 60 percent of young adults from the middle class owning their home outright. The common practice of transferring family assets among the CEE countries makes the distribution of asset ownership far more equal in the stage of young adulthood than in other regimes. The family-asset transfer regime displays the next highest prevalence of outright ownership across income classes, even among the lower class, one-third of whom own their home outright. The family financial support and the state-based regime, however, reveal that the upper class has a considerable advantage in outright ownership compared to the middle and lower classes. This is an indication of the more rigid class structure in countries characterized by those regimes, which produces greater class inequality in homeownership in the stage of young adulthood. By contrast, the state-market-based regime exhibits the lowest rate of outright ownership for all income classes. This is related to the fact that the practice of family-asset transfer is uncommon in this regime.

Access to homeownership through mortgage loans is clearly more limited in the post-communist regime, followed by the family asset transfer regime. They have the lowest rates for all classes across regimes (lower class 8%, middle class 16%, upper class 20%; and lower class 10%, middle class 27%, and upper class 29%, respectively). By contrast, the market-state regime has the highest share of mortgaged homeownership for all classes (lower class 19%, middle class 63%, and upper class 86%), revealing the impact of an accessible and inclusive mortgage market in these countries. The family financial support regime also displays a relatively high share of mortgaged homeownership across all classes, which was expected due to the financial aid that is customary in the countries included in this regime. Once again, the state-based regime displays a strong advantage for the upper class in mortgaged homeownership, reflecting the more rigid class structure in countries characterized by that regime. Hence, homeownership with or without a mortgage is less likely in the state-based regime than in other regimes and is primarily the privilege of young adults in the upper income class.

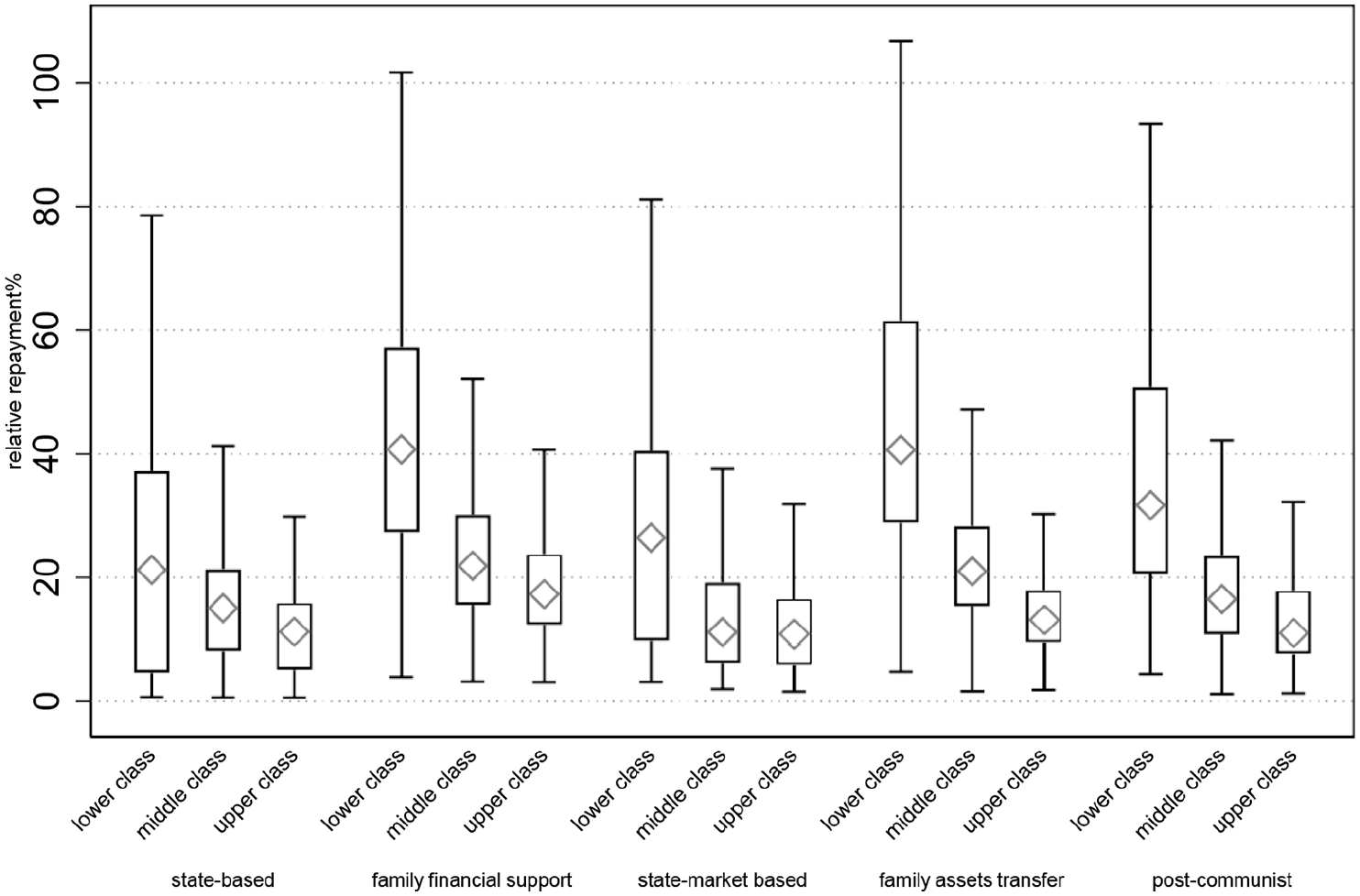

As noted above, the main mechanism for achieving homeownership in most Western countries is via mortgage loans. However, the size of relative repayment can become a source of financial strain for young adults, especially in lower income classes in different institutional contexts. To examine how relative repayment varies by income class and homeownership regime, we calculated the median and the interquartile range of relative repayment by income class for each of the five regimes. Figure 2 presents the results of this analysis (Table 3, in Appendix 1).

The median and interquartile range of relative repayment by income class and homeownership regimes.

The findings reveal that in all regimes the lower class has both the highest median and the largest dispersion (interquartile range) of relative repayment. While this comes as no surprise, the question we addressed concerns the extent of class-based gaps in relative repayments. They appear to be narrowest in the state-based (where the median relative repayment of the lower class is 21%, as against 15% for the middle and 11% for the upper classes) and market-state regimes (where the median relative repayment is 26% for the lower class, as against 11% for the middle and upper classes). In addition, the values of the third quartile (q3) of the relative repayment for the lower class in the family-asset transfer, family financial support, and post-communist regimes are 62 percent, 57 percent, and 51 percent, respectively. This points to the fact that any kind of family financial support (money or assets) increases class inequality in mortgage debt burden, whereas in the state-based and market-state regimes the values for relative repayment do not exceed 40 percent. These findings provide an indication that when an accessible or inaccessible mortgage market is coupled with an alternative in the shape of a protected rental market and a stable labor market, which are characteristics of the market-state regime and the state-based regimes, class inequality in mortgage debt burden is likely to be narrower than other sets of institutional arrangements. This in turn has a great impact on the experience of and the risk associated with mortgage debt burden placed on young adults in parallel homeownership regimes.

Multivariate estimation of class disparities by homeownership regime

To investigate income-class patterns of housing tenure and mortgage debt burden more rigorously, we considered a wider range of household factors using multivariate analysis. This involved estimating the probability of being in a particular category of housing tenure via multinomial logistic regression modeling. We estimated average marginal effects (AME) to reflect the percentage-point difference in the dependent variable (housing tenure) associated with a one-unit change in the independent categorical variable, net of control variables at their observed values (Williams, 2012). An important advantage of AME is that it can be compared across regimes. 7 While these analyses enabled us to statistically test the class-based gap within homeownership regimes, we also ran a post-estimation command to statistically test differences among regimes (as will be detailed further).

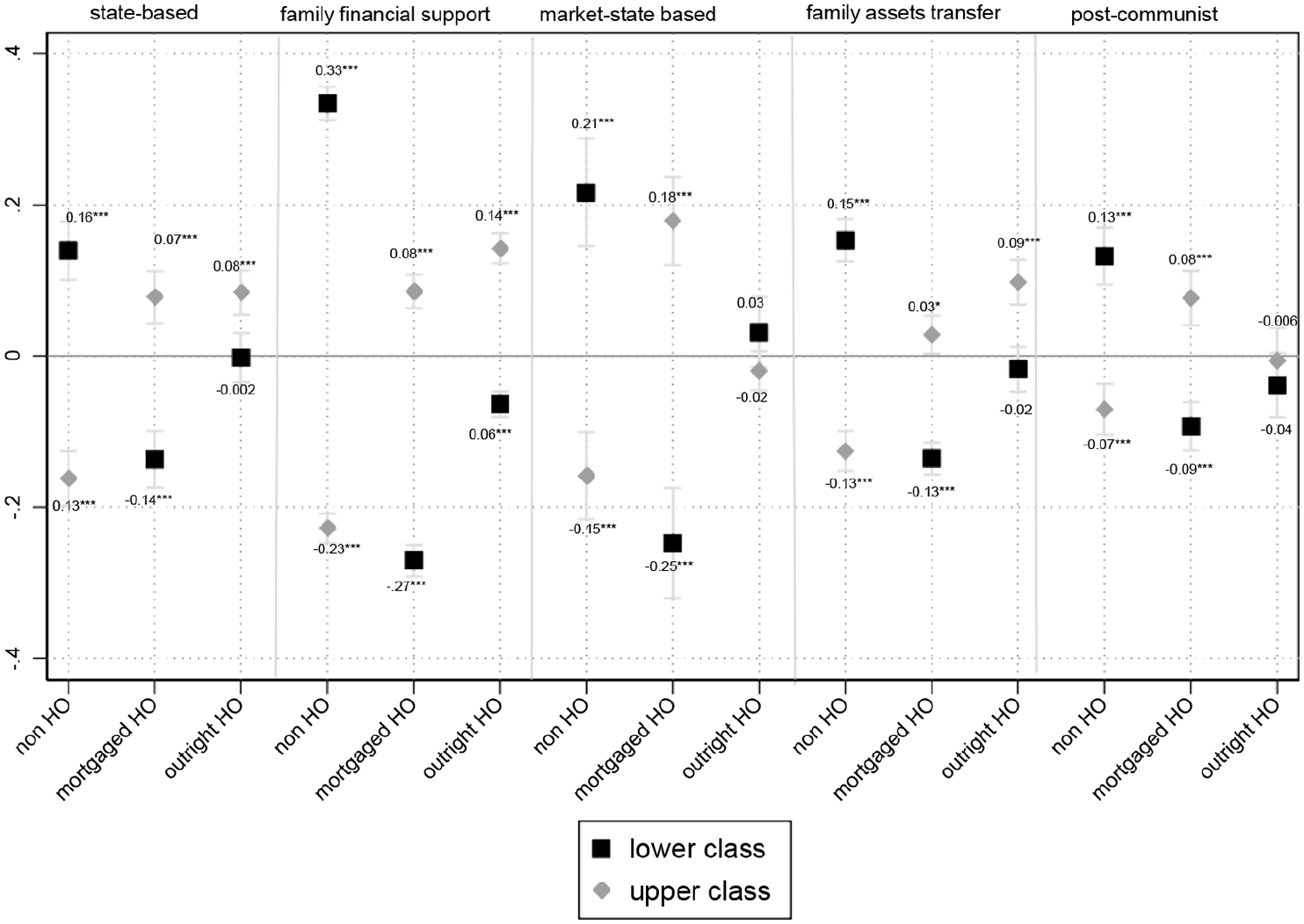

For the sake of simplicity, the central findings of the multinomial logistic regression models are presented in Figure 3, in which we take housing tenure as a function of income class and household socio-demographic attributes, controlling for country dummies and age(centered) in each of the homeownership regimes (Table 4 in Appendix 1 displays the multinomial logistic regression models). In the figure, the horizontal line with the value of 0 represents the middle class and serves as the reference. The squares represent the percentage-point difference in the dependent variable (the reference category is mortgaged homeownership) between the lower and middle classes. The diamonds represent the percentage-point difference in the dependent variable between the upper and middle classes.

AME predicting the difference in probability of housing tenure between the lower or upper class and the middle class and 95% confidence intervals, by homeownership regime.

Overall, Figure 3 presents a stratified pattern of the probability of being in any of the categories of housing tenure according to income class across all regimes. As for differences within regimes, with regard to mortgaged homeownership, the narrowest income-class-based gap for the probability of having mortgaged homeownership is found in the post-communist and family asset regimes, net of household socio-demographic attributes and country fixed effects and age. We expected this result due to the underdeveloped housing markets and limited accessibility of mortgage loans in these countries, which in turn contributes to lower percentages of mortgaged homeownership in this regime across all income classes, thus reducing the gaps between them. On the other hand, the family financial support regime displays the widest gap between the middle and the lower classes in mortgaged homeownership and a relatively wide gap between the middle and the upper class compared to other regimes. This indicates a strong effect of the family in this regime, as the transfer of financial aid from parents to their children in countries associated with this regime extends the gap between IWT beneficiaries and non-beneficiaries. However, the market-state based regime exhibits the largest class-based gaps in mortgaged homeownership, which is surprising, since it comprises countries with the most generous housing finance systems and egalitarian labor markets. Perhaps this can be explained by the existence of a highly controlled public rental market of a relatively high quality in these countries, which makes rental an appealing alternative for the lower and the middle class, as evident from the relatively high rate of non-owners in the market-state regime. The relatively wide income-class-based gap in mortgaged homeownership is in line with previous reports on the high levels of wealth inequality in these countries (Korom, 2018; Pfeffer and Waitkus, 2021).

As for outright ownership, the findings show that the narrowest income-class-based gap is found in the market-state-based and post-communist regimes, net of control variables. In the former, housing prices are relatively high, and IWT in the form of housing assets is less common, making access to outright ownership almost impossible for all income classes. Thus, the income-class-based gap in outright homeownership is narrower in the market-state-based regime. In addition, as revealed above (see Figure 1), the percentage of outright ownership is very low in this regime, resulting in a very narrow class-based gap in outright ownership. On the contrary, in the latter regime housing assets are a common form of family financial support among all classes, therefore decreasing the class-based gap in outright ownership. The largest class-based gap in outright ownership is observed among the family financial support regime. The middle class in this regime has a statistically significant 6 percentage-point higher probability of outright ownership compared to the lower class, and the upper class has a statistically significant 14 percentage-point higher probability of outright ownership compared to the middle class. The class-based gap in outright ownership in this regime reflects the advantages of households with more family resources over others, even though this regime is characterized by a relatively generous mortgage market.

As for renters (non-homeowners), the narrowest class-based gap is in the post-communist and family asset transfer regimes. The rental market is relatively marginal in those regimes and is thus not an attractive alternative. The proportion of renters is relatively low, resulting in a narrower class-based gap in the rental sector than in other regimes.

So far, we have conducted the analyses within each of the five regimes. In order to evaluate whether class-based differences vary significantly across regimes, we combined all of the regimes in a single regression equation to produce a simultaneous (co)variance matrix with robust standard errors (using the post-estimation suest command, Williams, 2015, p.10). Then, we separately compared (using chi-square tests) the class-based gap with regard to the probability of being in each category of housing tenure across regimes (Van Solinge and Henkens, 2008, p. 425; Institute for Digital Research and Education, UCLA, n.d.) (Table 8 in the Online Appendix). The overall results confirm the patterns in housing tenure revealed in Figure 3. They show that the gap between the lower and the middle classes in mortgaged homeownership is significantly wider in statistical terms in the family financial support regime than in all other regimes (state-based; χ 2 = 16.4, p < 0.000, market-state-based; χ 2 = 6.46, p < 0.05, family asset transfer; 24, p < 0.000; post-communist; χ 2 = 7.50, p < 0.05), and the gap between the upper and the middle classes in mortgaged homeownership is significantly wider in statistical terms in the family financial support regime than in all other regimes, (state-based; χ 2 = 11, p < 0.005; market-state-based χ 2 = 10.10, p < 0.001; family asset transfer; χ 2 = 31, p < 0.000; post-communist; χ 2 = 32, p < 0.000).

An indication of the more rigid class structure in countries characterized by the family financial support regime is also revealed, as the gap between the upper and middle classes in this regime is wider and statistically significant with respect to the probability of having outright ownership than the gap in the state-based and family asset transfer regimes (χ 2 = 4.4, p < 0.05, χ 2 = 6.03, p < 0.05, respectively). In addition, a wider gap between the lower and the middle class in outright ownership was found in the family financial support regime than in the state-based regime (χ 2 = 6.63, p < 0.05). Thus, our first hypothesis (H1) is mostly supported, since the narrowest income-class-based gap in the probability of achieving mortgaged homeownership was found in the post-communist regime, while the widest class-based gap in the probability of having mortgaged homeownership was found in the family financial support regime. We will elaborate on these findings in the discussion.

Class differences in mortgage debt burden by homeownership regimes

We estimated ordinary least squares (OLS) linear regression models to examine the magnitude of the correlation between income class and the level of relative repayment for each homeownership regime, taking additional household characteristics into consideration with country dummies and age. Hence, the analysis only includes households with mortgaged homeownership. The purpose of the analysis was to estimate the actual effect of income class on the burden of relative repayment within and between homeownership regimes (using suest post-estimation, as detailed above). Figure 4 displays the findings by income class and homeownership regime (Table 5 in Appendix 1).

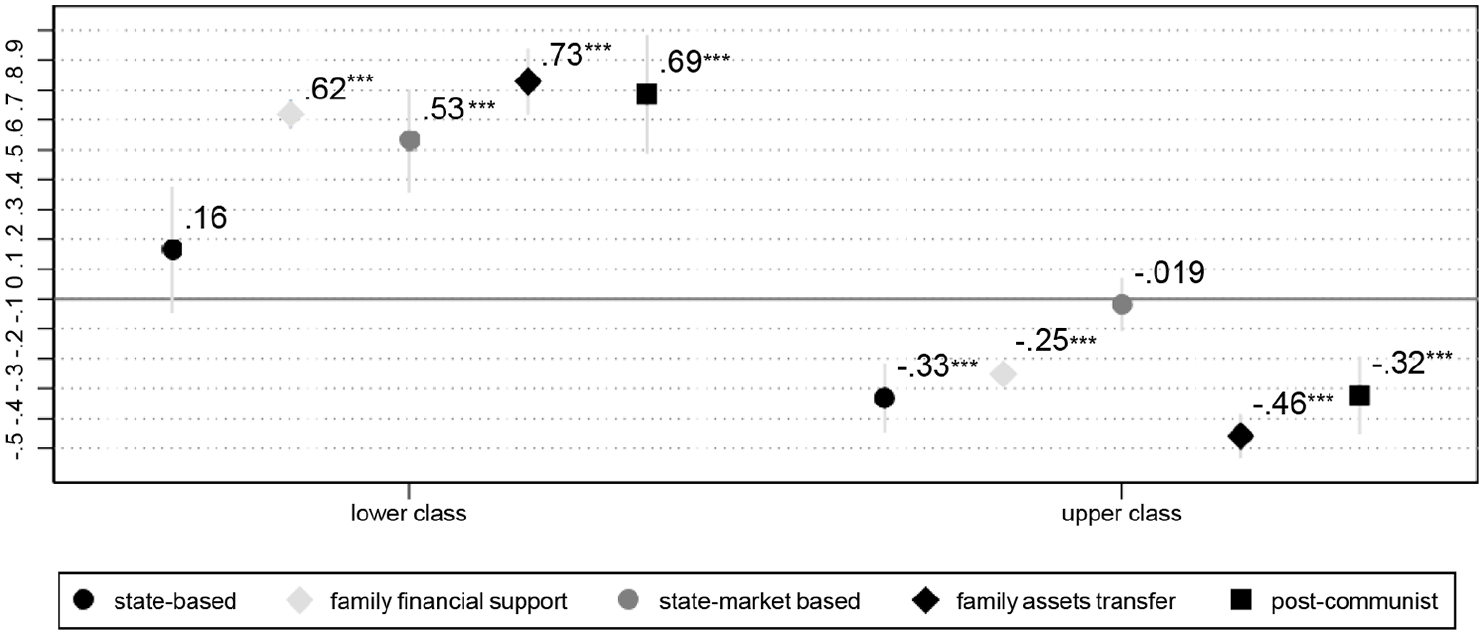

Coefficient estimates representing deviations of the upper and lower class from the middle class, obtained from OLS regression models predicting the (ln) relative repayment, by homeownership regimes.

The findings reveal that in all homeownership regimes, with the exception of the state-based regime (b = 0.16, p > 0.05), the lower class has a higher average level of relative repayment than the middle class, net of control variables, and that these differences are statistically significant within each homeownership regime. The insignificant differences in the size of relative repayment between the lower and middle class in the state-based regime may be due to its conservative housing finance system and the lack of family financial aid, which reduces the middle class advantage in this context. Similarly, within all homeownership regimes, with the exception of the market-state-based regime, the upper class has a lower average relative repayment level than the middle class, net of control variables. The advantage of upper class with regard to having a lower mortgage burden in varying contexts can be linked to the overall widening of income inequality and the erosion of the middle class. However, more central to our argument is the fact that the magnitude of the class-based gaps in relative repayment is context dependent. In the market-state-based regime, the income class gap is quite small, and in fact the middle class does not carry a larger debt burden than the upper class (b = −0.019, p > 0.05). In a similar vein, class disparities in mortgage debt burden are also relatively small in countries with state-based housing regimes, where the coefficient distinguishing the lower from the middle class is not statistically significant. At the same time, the class-based gap in relative repayment is most extreme in the family-asset transfer (b = 0.73, p < 0.000; b = −0.46, p < 0.000) and post-communist regimes (b = 0.69, p < 0.000; b = −0.32, p < 0.000).

The patterns of class differences in the level of relative repayment found within homeownership regimes are also confirmed by statistical tests comparing differences between regimes. The gap between the lower and the middle class in the state-based regime is narrower than the gap between the lower and the middle class in all other regimes and is also statistically significant (Table 9 in the Online Appendix (family financial support; χ 2 = 0.8, p < 0.001, market-state-based; χ 2 = 3.73, p < 0.05, family asset transfer; χ 2 = 12, p < 0.001; post-communist χ 2 = 8, p < 0.05)), and the gap between the upper and the middle class is narrower in the market-state-based regime than in all other regimes and is also statistically significant (state-based; χ 2 = 19, p < 0.000; family financial support; χ 2 = 23, p < 0.000; family asset transfer; χ 2 = 53, p < 0.000; post-communist; χ 2 = 16, p < 0.000). Thus, the lower and middle classes experience less mortgage burdens in the countries classified as having a state-based or market-state-based regime relative to their counterparts in other contexts. For the sake of brevity, further insights about the meaning of those findings and their implications will be presented in the next section.

The above results mostly contradict our second hypothesis (H2), since class-based gaps in the level of relative repayment were narrowest in the market-state-based and state-based regimes (on average) and widest in the family-asset transfer and post-communist regimes, with the family financial support regime situated somewhere in the middle. The widest class-based gap in the level of relative repayment in the family-asset transfer and post-communist regimes can be explained by the combination of underdeveloped mortgage markets and weak presence of the state in the housing sector, which results in a stronger impact of family background. We will discuss this in more detail in the next section. As a sensitivity test, we reanalyzed the data with five income quintiles as an alternative to the “income class polarization” definition we used. Once again, the findings revealed a statistically significant negative correlation between income quintiles and the level of relative repayment in which the burden of relative repayment increases with the downward shift in class position, except in the market-state-based regime. The latter shows the narrowest class-based gap in mortgage debt burden, as the differences in the level of relative repayment between the middle and the upper quintiles are statistically insignificant (Table 6 in Appendix 1).

Discussion and conclusion

In this study, we combined recent developments in the research on social stratification and wealth inequality with insights from the literature on homeownership regimes. The former provided the premise of the centrality of housing as a form of wealth and its importance in positioning young-adult households within the system of stratification. The latter provided the foundations for introducing the diversity of institutional arrangements that form distinct housing regimes and shape housing tenure and different levels of mortgage debt burden. Given the institutional changes that have taken place in recent decades, the present-day generation of young adults is facing more barriers in the transition to first-time homeownership than previous generations of young adults in diverse contexts (Cohen Raviv, 2021; Flynn and Schwartz, 2017; Fuller et al., 2020; Ronald, 2018). This in turn increases the dependency of young adults, even when they form their own households, on the resources of their family of origin. Thus, we found it necessary to reframe the homeownership typology by accounting theoretically and empirically for the role of the family (via IWT in its different forms), which was theoretically underdeveloped in and empirically absent from previous homeownership typologies (Blackwell and Kohl, 2019; Hoekstra, 2003, 2005; Kemeny, 1995; Mulder and Billari, 2010; Schwartz and Seabrooke, 2008; Wind et al., 2017).

Unlike previous typologies, the typology developed in this study utilizes recent macro-level indicators that postdate the GFC of 2008 and was constructed on the basis of testable statistical analysis. We then implemented this new typology in order to examine how homeownership regimes and the opportunity structures they represent shape economic class disparities in homeownership (therefore providing potential for future wealth accumulation) and the mortgage debt burden ownership often entails. This allowed us to examine how and to what extent inequality in the ownership of the most valuable asset most households will possess during their lives is modified by the institutional context in which young adults mature.

Our suggested homeownership typology builds on previous theoretical explanations, such as housing market financialization (Blackwell and Kohl, 2019; Fuller, 2015; Kohl, 2018; Schwartz and Seabrooke, 2008) and government housing programs (Flynn, 2020; Kholodilin et al., 2018) in access to homeownership, but also impels authors of housing studies to take more seriously the role of family means in this regard (via IWT and its forms), which is receiving growing attention in the wealth and stratification literature. By introducing the institution of the family, our analysis revealed, for example, that family intergenerational assistance cuts across countries with diverse political economies and welfare state regimes, clustering them in the same homeownership regime, that of family financial transfer. Those countries were classified differently in previous housing typologies (Blackwell and Kohl, 2019; Mulder and Billari, 2010; Schwartz and Seabrooke, 2008; Wind et al., 2017). This finding suggests a loosening of the relationship between political economies and housing regimes. One important implication of this finding is that as long as disposable incomes from labor fail to keep up with housing price inflation and alternative housing opportunities are not available to or affordable for young adults, the family will play a growing role in structuring homeownership inequality. Indeed, countries characterized by different regimes may follow similar patterns if states withdraw or further limit their involvement in the housing market.

This may have a ripple effect, since the growing dependency of young adults on family resources in access to homeownership also means a delay in first-time homeownership for those who lack financial assistance or receive it to a lesser extent. A delay in the transition to first-time homeownership also means a delay in family formation, which can also translate to decreasing fertility rates at the national level (Makszin and Bohle, 2020; Mulder and Billari, 2010).

Our findings on variation in class disparities in homeownership and mortgage debt burden that emerge in distinct homeownership regimes reveal the unique contribution of IWT in perpetuating socioeconomic inequality. In the regimes characterized by family housing transfers (Southern European and CEE countries), both mortgaged and outright homeownership inequality are actually reduced, while their conservative mortgage markets increase inequality in the level of mortgage debt intensity and the risk associated with it. In the market-state regime (which includes Northern European countries and the Netherlands), by contrast, where family financial support is low or absent and mortgage markets are highly liberalized, there are noticeable class-based gaps in mortgage homeownership, but class-based gaps in mortgage debt burden are low. This can be explained by the presence of alternative highly controlled and high-quality public housing in the countries of this regime, which is an appealing option for young adults from the lower and middle classes, especially in times of rapidly increasing housing prices. This in turn widens the class-based gap in mortgaged homeownership, as young adults with more financial means invest in housing properties without bearing heavy mortgage debt burden. One important implication of the above findings for inequality among young adults in different housing regimes is that taking out a mortgage loan is more a constraint than a choice for young adults in the family-asset transfer and post-communist regimes, whereas it is more a choice than a constraint for those in the market-state regime.

As for the form of class inequality in homeownership and the mortgage debt burden in the state-based regime (comprising German-speaking countries), it lies somewhere between the two former regimes. It resembles the market-state regime with respect to a lower prevalence of IWT in any form and a legacy of a protected rental market based on the foundation of corporatist social structures in which the state has a role in safeguarding its citizens from financial shocks and significant income inequality (Kemeny, 2006; Kohl, 2018). This leads us to conclude that when households can better rely on government institutions to provide a protected and stabilized rental sector, the social norm of wealth accumulation—which is sacred in neoliberal countries—is weakened. In this context, the “privatization of risk” (Beck, 1992; Giddens, 1999) represented by mortgage debt burden is also more evenly distributed among different classes. This in turn reduces the phenomenon of “asset-based welfare.”

While this study makes a number of novel contributions, it does have several limitations. Information about the preferences of those who are not homeowners—whether because they have been refused mortgage loans or because they lack the necessary capital—was unavailable. Such information would have provided further insight into the dual impact of class inequality and regime differences. Future research would benefit from a larger sample of countries upon which to perform multilevel analysis. Information on housing values was unfortunately unavailable in the EU-SILC dataset. This limited our investigation of net wealth directly.

Finally, there is growing concern in many countries over growing wealth inequality. This study aims to spotlight homeownership as a central mechanism that perpetuates inequality among families. Societies concerned about wealth inequality, particularly the hardships now experienced by the young adult generation, must seriously confront this reality. The market-state and state-based regimes teach us that high state involvement in the housing market provides secure housing alternatives, thus also decreasing class inequality in mortgage burden for those who take out mortgage loans. Hence, there is a need for expending state-provided alternatives if inequality is to be contained. At the same time, there is a need for developing easier access to mortgage loans and easier mortgage terms in countries with less developed mortgage markets (family asset transfer and post-communist regimes). This can be achieved via a higher maximum LTV ratio, which eases access for young adults to the first step to homeownership and provides them tax relief (such as of property transfer tax), deductibility of mortgage interest, grants for financing first-time home buyers, and more (OECD, 2016).

Supplemental Material

sj-xlsx-1-cos-10.1177_00207152211070817 – Supplemental material for Homeownership regimes and class inequality among young adults

Supplemental material, sj-xlsx-1-cos-10.1177_00207152211070817 for Homeownership regimes and class inequality among young adults by Or Cohen Raviv and Noah Lewin-Epstein in International Journal of Comparative Sociology

Supplemental Material

sj-xlsx-2-cos-10.1177_00207152211070817 – Supplemental material for Homeownership regimes and class inequality among young adults

Supplemental material, sj-xlsx-2-cos-10.1177_00207152211070817 for Homeownership regimes and class inequality among young adults by Or Cohen Raviv and Noah Lewin-Epstein in International Journal of Comparative Sociology

Supplemental Material

sj-xlsx-3-cos-10.1177_00207152211070817 – Supplemental material for Homeownership regimes and class inequality among young adults

Supplemental material, sj-xlsx-3-cos-10.1177_00207152211070817 for Homeownership regimes and class inequality among young adults by Or Cohen Raviv and Noah Lewin-Epstein in International Journal of Comparative Sociology

Supplemental Material

sj-xlsx-4-cos-10.1177_00207152211070817 – Supplemental material for Homeownership regimes and class inequality among young adults

Supplemental material, sj-xlsx-4-cos-10.1177_00207152211070817 for Homeownership regimes and class inequality among young adults by Or Cohen Raviv and Noah Lewin-Epstein in International Journal of Comparative Sociology

Footnotes

Appendix 1

Sources for Table 1.

| Indicator | Source | Notes |

|---|---|---|

| Residential loan to GDP ratio

EU countries Israel |

Hypostat, 2019 (for years 2012–2015: 124). https://hypo.org/app/uploads/sites/3/2019/09/HYPOSTAT-2019_web.pdf Bank of Israel 2016; CBS 2016. |

Self-calculated averages for those measurements between 2012 and 2015. Israel: Self-assessed relaying on these two databases. |

| Homeownership rate EU countries Israel |

Hypostat, 2019 (for years 2012–2015: 127). https://hypo.org/app/uploads/sites/3/2019/09/HYPOSTAT-2019_web.pdf

CBS 2012. |

Self-calculated averages for those measurements between 2012 and 2015. |

| Max LTV | OECD (2015, p7) Economic Surveys Switzerland. ESRB 2018, p.96. Annex 2: Active residential real estate instruments in Europe Housing Finance Network (2016). Bank of Israel 2012. Wind et al. (2017) |

|

| Switzerland |

||

| Rent control |

OECD, 2016. Affordable Housing Database. | No data were available for Iceland |

| Housing as a gift |

HFCS database 2017 (Household Finance and Consumption Survey). | Self-calculated for households in the age range: 25–40: |

| Gift or inheritance |

HFCS database 2017. Self-calculated for age range: 25–40. |

Self-calculated for households in the age range: 25–40: |

GDP: gross domestic product; CBS: Central Bureau of Statistics; LTV: loan-to-value.

Acknowledgements

The authors are grateful to Yasmin Alkalay (may she rest in peace) for her endless devotion and dedication for Or Cohen Raviv PhD dissertation and assistance in the data analysis. They are also grateful to Moshe Semionov, Michael Shalev, and Tally Katz-Gerro for their helpful comments and insights on this study.

Correction (December 2023):

Article updated online to correct the reference Flynn LB and Schwartz HM (2020) to Flynn LB (2020) in the text and reference list.

Declaration of conflicting interests