Abstract

Globally, with the maturity of information technology, society is now in the information age, magnifying the significance of integrating innovative applications in different financial and other regulatory arenas. The emergence of financial technology (FinTech) based applications has transformed the traditional banking and regulatory systems and enhanced customer satisfaction by providing a balanced environment for protecting its customers from risky behavior or other potential disruptions. Besides these critical applications of FinTech in the financial industry, it is not developed in the Gulf Cooperation Council (GCC) region as in China, United States, and other developed countries. In order to bridge the gaps in the extant by identifying the critical factors involved, this research work presents a systematic analysis of the available literature reported during the period ranging from 2016 to 2021. This systematic mapping of the extant was performed by selecting five different research questions. The key objectives of this systematic research work are, (1) To identify the barriers that restrict the rise of FinTech in the GCC region, (2) Analyze the behavior of different communities regarding the adaptation of FinTech by evaluating the case studies reported, (3) the impacts of FinTech on different communities in the GCC region. (4) The findings of this research work will not only help the state development bodies by encouraging its stakeholders to use FinTech-driven applications in banking, markets, etc. but it will also help the people in maintaining long-term connection with the Ministries of Foreign Affairs, the Dutch regulators, Economic Affairs, the Dutch Central Bank (DNB), as well as with the Authority on Financial Markets (AFM), and (5) this study work will present new research directions for the research community to explore in the near future.

Introduction

During the last few years, the FinTech-driven applications has gained significant attention of the research community and other financial gurus. The key motivation behind this significant attraction is the potential of the FinTech to incorporate supply-chain networks in all business sectors. 1 It is an integration of digital technologies facilitating its users to perform transactions via online and mobile banking. 2 For example, high speed internet connectivity and mobile applications facilitate users to promote financial operations/activities using smart IoT devices, including e-bill payments and direct payroll deposits. These online banking facilities and integration of digital technologies have proposed a secure and efficient business model in place of traditional business models that were mostly error-proven. A good business model especially FinTech-integrated model provides high facilities to its customers and poor communities by restricting corruption and ill-legal fees by providing non-cash community, 3 smart intelligent interface using advanced artificial intelligence and machine learning models, 4 presenting globalized economy, providing a centralized controlling mechanism where the customers can have access from everywhere and every time.

During the research analysis performed by KPMG and H2 Ventures in 2016, 5 it was reported that more than half of the top 50 FinTech “unicorns” were born after 2010. The FinTech has become a buzzword among Silicon Valley entrepreneurs and Wall Street investors, and their investment is considered as the fastest growing investment in this modern technological application. Inspired by this significant interest of the financial industries and research communities, both the government and non-government organizations have shown a keen interest in transforming the traditional banking systems toward FinTech-driven systems. This transformation will not only ensure the higher facilities for their customers but will help in boosting the economy of the country by restricting fraudulent mechanisms and strategies, no-corruption, and helping the poor community to borrow money for their basic needs and new business startups. Inspired from the world, the FinTech is also emerged speedily in the Gulf Cooperation Council (GCC) countries, especially in the State of Qatar. The researchers reported work on FinTech using case studies of MENA region (an English-language acronym describing the Middle East and North Africa).6,7 While some researchers reported work on GCC member countries using FinTech as the point of consideration.8–10

Consequently, the maturity of research on digitization and FinTech begs to systematically analyze the extant that can explicitly identify the materiality, variability, emergence, and richness of FinTech as a phenomenon. The systematic research work is extensively reported in many research fields, including healthcare, 11 intelligent homes, 12 crowdsourcing, 13 network IPv6 domain, 14 navigation assistant, 15 and many others, due to its higher capabilities to analyze the literature in a systematic manner by flushing lights on the gaps in a specific research domain and suggest new research directions by bridging these gaps. To perform this systematic literature review (SLR) process a total of five different research questions are formulated in this systematic analysis to assess the proposed FinTech domain with different perspectives. Five different peer-reviewed online repositories are selected for the accumulation of the relevant articles for the systematic mapping. A total of 91 most relevant research articles are analyzed and systematically assessed in this research work. The prime objectives of this research work include:

The identification of the critical barriers that restrict the rise of FinTech in the Middle East. Identifying these key barriers will help the research community to address these challenges by suggesting new and enhanced solutions to gain customer satisfaction and encourage them toward the use of FinTech-driven applications.

Analyze existing work by identifying the behavior of different communities regarding the adaptation of FinTech by evaluating the case studies reported. Some of the critical problems faced by FinTech during the adoption process are unfamiliar with FinTech, intimidated feelings, and lack of understanding. 16 Although the researchers performed workshops, conferences, and present news reports to encourage people toward FinTech, a large number of the population still show dubious behavior. The second and most important objective of this research work is to identify the residents’ sentiments regarding FinTech and suggest some future research directions based on the assessed information.

The impacts of FinTech on different communities in the Middle East. The findings of this systematic research work will not only help the state development bodies by encouraging its stakeholders to use FinTech-driven applications in banking, markets, etc. but it will also help the people in maintaining lifelong relationships with the Ministries of Foreign Affairs, Economic Affairs, the Dutch regulators, the Dutch Central Bank (DNB), as well as the Authority on Financial Markets (AFM), and

Based on the systematic analysis and findings, this study will present new research directions for the research community to bridge the gaps in the selected FinTech domain.

The rest of the paper is organized by presenting the related work in section 2 of the paper. Section 3 of the paper explains the research protocol followed for the proposed systematic mapping. At the same time, section 4 of the paper presents the quality assessment criteria and systematic analysis. Section 5 of the paper outlines the results and discussion section of the article. Based on the systematic assessment of the literature the future research directions are outlined in section 6 of the paper followed by the conclusion in section 7 of the paper.

Related work

The 21st century has astonished us with its advancement by introducing numerous smart applications ranging from banking system to smart financial systems, 17 routing systems 18 to smart navigation applications, 19 and many others. Surprisingly, its pace is so quick that we obviously raise our hands and desist any feign of watching what is the latest in innovation. This gape, in its own pervasiveness, presents itself in Finance, likely more so thananywhereelse does. It must be noted; we do not allude to Finance as Finance any longer yet FinTech. 20 This idea can be a touch devilishly extended, FinTech itself is at the brink of the redesign as though there was a need. The researchers shown a significant interest in this transition process, initiating from the zephyr of Blockchain darting its wings, which is found to be a hot topic of research in the labs, financial industries, and in research centers.21–23

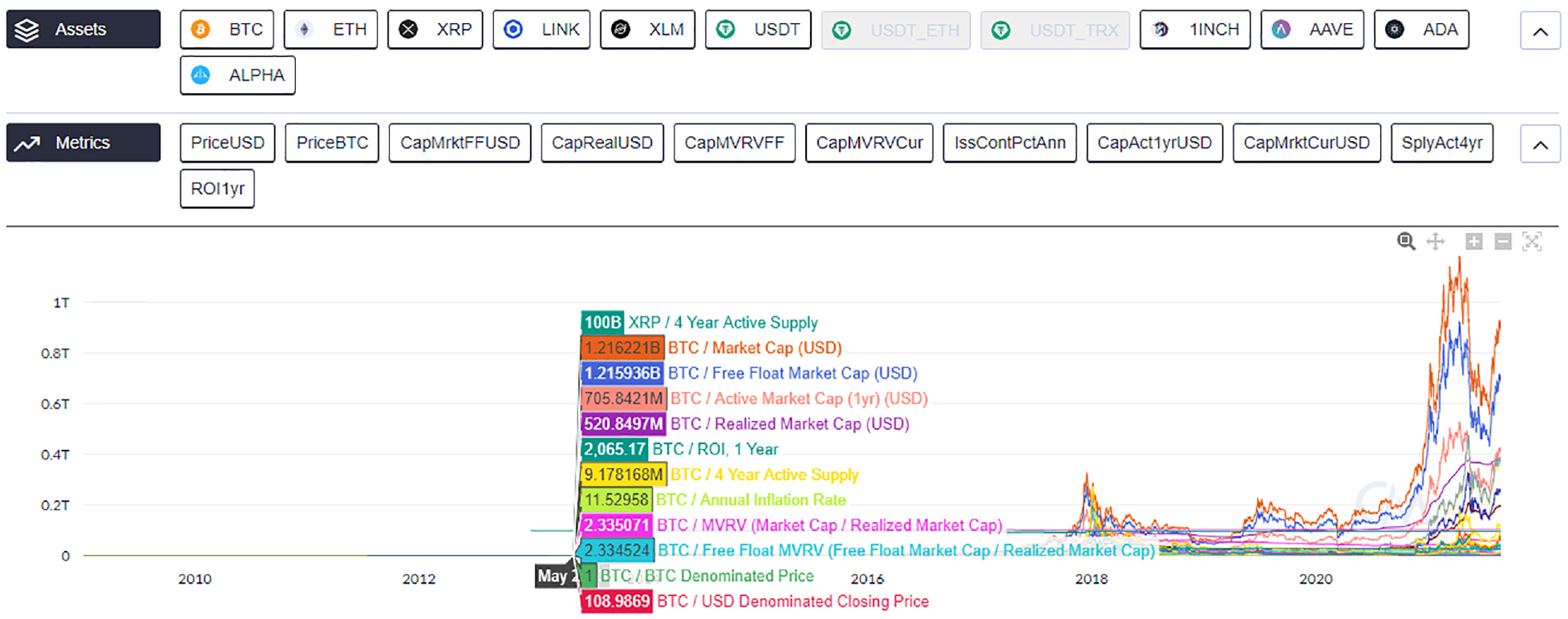

In 2008, Nakamoto (a Japanese researcher) reported an article by presenting a plot that introduced the new advanced money, termed as Bitcoin (XBT or BTC). 24 It is believed that this new advanced money was a reply to the 2008 global financial crisis (GFC), and emanating government bailouts of banks. As Tschorsch and Scheuermann, 25 and Geiger 26 clarified, “Bitcoin is an option in contrast to the current budgetary framework. It expels authority from any single individual or association, and was made in any event incompletely as a reaction to the 2008 GFC,” 27 where the poor judgment of a couple of prompted cutbacks, school graduates without openings for work, and home abandonments universally.” With the help of blockchain, total exchange rates are recorded online, and by using a proof of work model (performed using cash excavators), these replacements are totally asserted. Besides, this blockchain-modeling still there is tendency to face two-fold spending issues.28,29 Another, innovative idea of cryptocurrency is introduced that uses decentralized mechanism for operational purposes. The overall cryptocurrency market capitalization has remarkably risen more than four-folds since 2018; exceeds $30 billion after 2020, as depicted in Figure 1.

Market capitalization record. 30

From Figure 1, it is depicted that Bitcoin is the most prominent cryptocurrency in terms of market capitalization and transactions (average daily number of transactions over the last 4 years) followed by BTC, ETH, XRP, LINK, XLM, Monero, and LTC. Besides this gigantic market contribution, most of the populations show dubious behavior toward Bitcoin or FinTech applications. The researchers around the world put a significant contribution toward the sentiment analysis of the population toward FinTech. Many research researchers reported case studies31,32 to identify population interest, while some researchers33,34 used deep learning and other shallow architectures for sentiment analysis purposes. While other reported survey papers25,35 for identifying challenges and security risks in the FinTech-driven applications. With passage of time this innovative field get matured and China is the best example, where the FinTech-driven models extensively used compared to United States and United Kingdom. 36 Besides this keen interest from the world, the FinTech-driven models are not encouraged in the GCC region, and still they prefer direct financing because money market funds are more popular in this region compared to Japan and Germany etc. Though direct financing is full of fraudulent, corruption, no centralized control mechanism, and many others but still most of the population in this region show a dubious behavior for blockchain, Bitcoin and other FinTech-based applications.

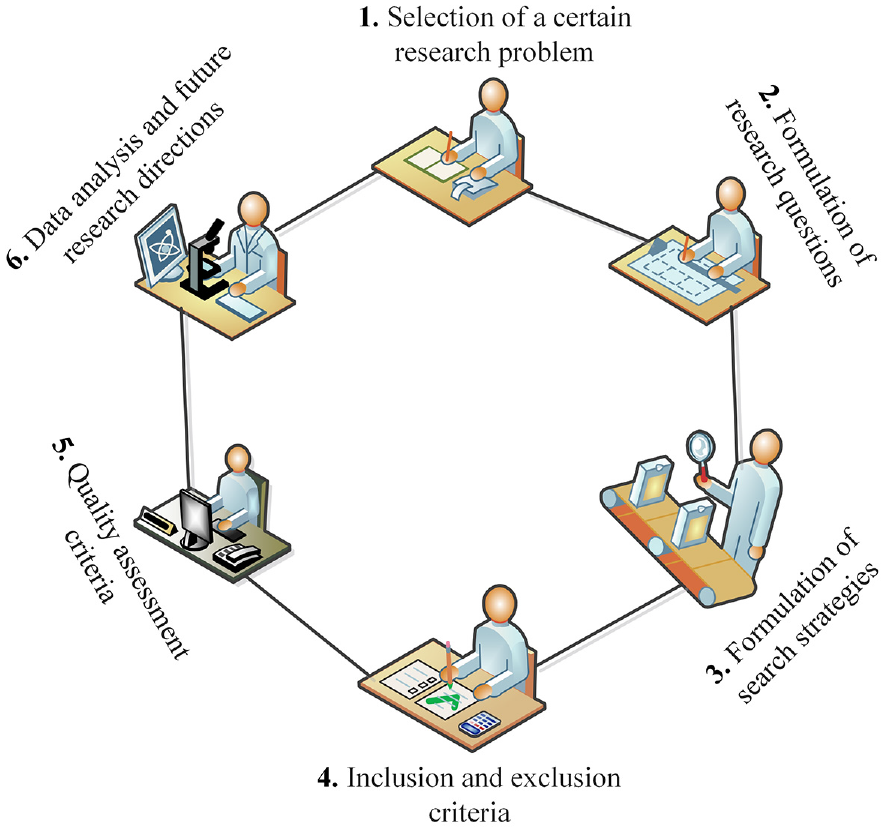

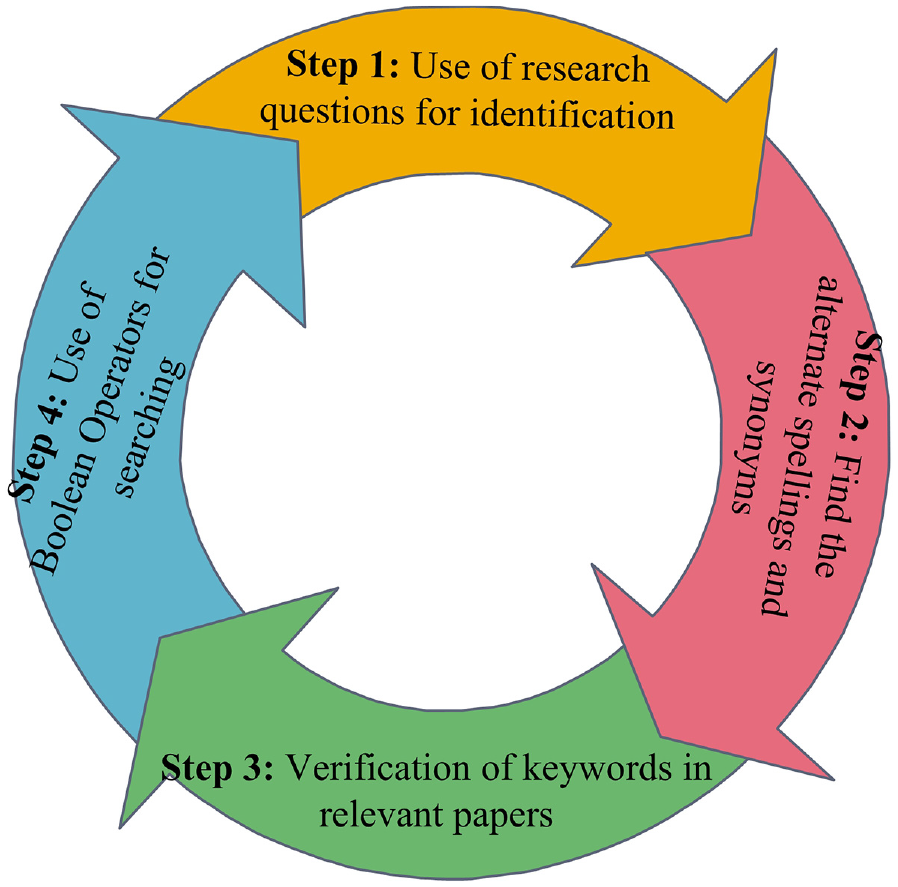

For identifying the core problems that hinders the implementation of FinTech-driven applications in the GCC region, this research work performs a systematic analysis of the extant accumulated from five different peer-reviewed research journals. The systematic literature review (SLR) studies are significantly reported by researchers in diverse domains to get knowledge of new trends and future research direction in the topic of interest. Key steps of an SLR work are depicted in Figure 2. These steps include identification of a research domain, selection of research questions (in our case, we have formulated five research questions to analysis the proposed research field with different perspectives), identification of search strategies, inclusion and exclusion criteria, and finally the assessment and identifying new gateways for future research directions.

Key steps of an SLR work.

If a systematic research work accurately follows these key steps represented in Figure 2 and ensure the PRISM checklist defined by Moher et al., 37 then the accomplished research work will contain a sound knowledge regarding a certain of interest. Keeping in view the importance of these guidelines the extant in the FinTech domain is assessed and analysis were performed to find the gaps in the available literature and suggested new research directions.

Systematic mapping protocol

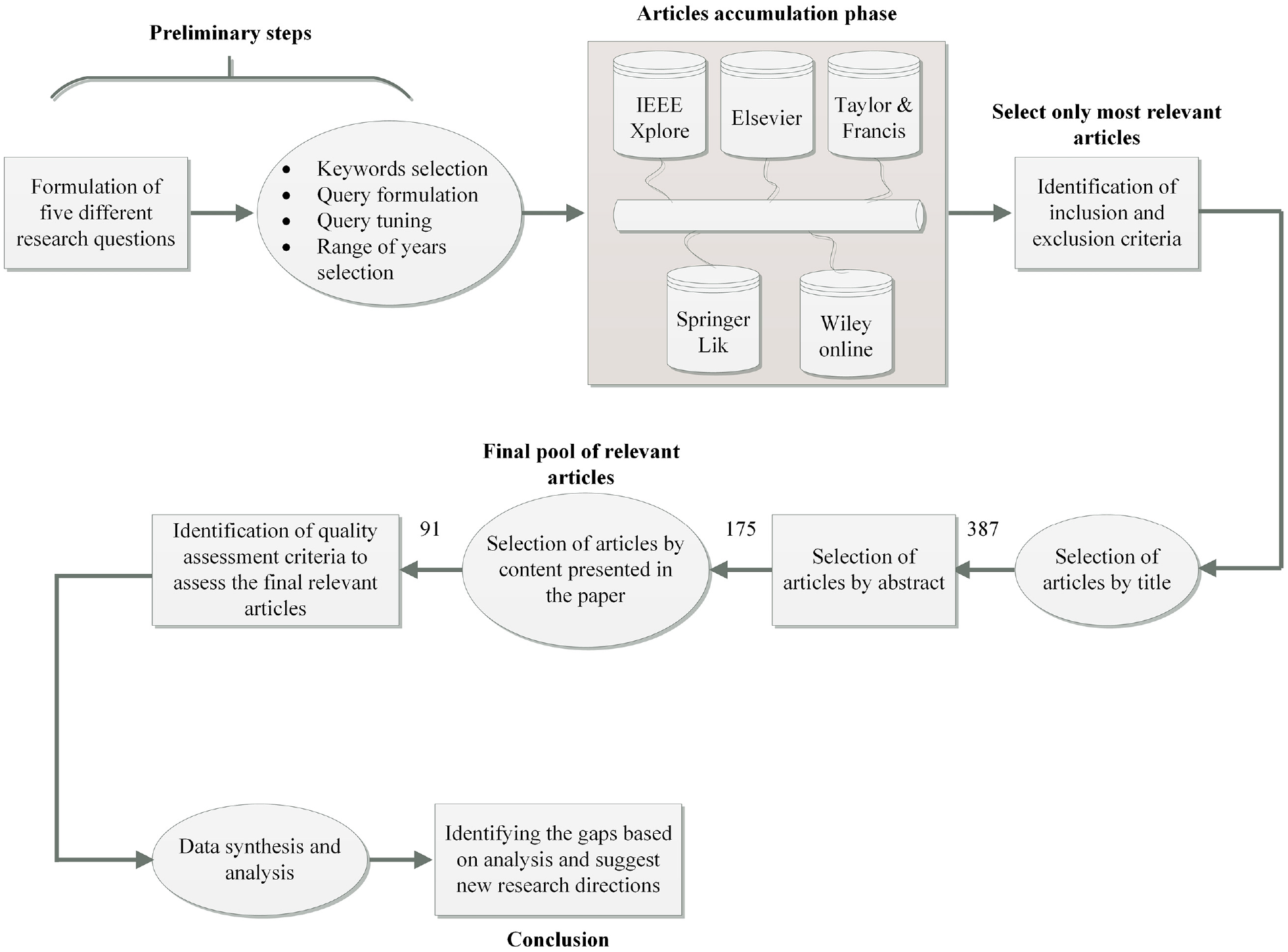

A systematic literature review aims to identify, select and critically assess the extant in order to answer a well formulated research question. 38 The systematic research work should follow an audibly determined protocol where the selection criteria is clearly stated earlier to the systematic mapping. It is an absolute, unequivocal search conducted over multiple online repositories and gray literature that can be cloned and replicated by other researchers. 39 It involves formulating a cognoscible search strategy which has a definitive focus or answers a specific research question. The review evaluates the type of information retrieved, appliqued and published within known timeframes (in our case 2016–2021). The search terms, searching strategies (including repository names, platforms, interval of search), and limits all need to be comprised in the review process. Figure 3 diagrams the systematic mapping protocol used for the proposed SLR work.

Proposed systematic research protocol.

From Figure 3 it is evident that the first step in our research work is to formulate the most relevant and well-defined research questions, because this is the key step in any SLR work and acts like a corner stone for the lateral assessment process. For this systematic analysis we proposed five research questions. Based on these research question keywords are identified that helped in formulating the queries to download relevant articles from the targeted libraries (ACM, Springer Link, Elsevier, Taylor & Francis, and Wiley online library). These articles are then scrutinized based on title, abstract, and contents presented in the paper. After completing the inclusion and exclusion process a final set of relevant articles is developed for the systematic analysis. It consists of 91 relevant articles. All these steps are discussed in details below.

Preliminary steps

These are the prime steps of any SLR work and considered as the backbone for the systematic mapping work. These steps consist of:

Research questions

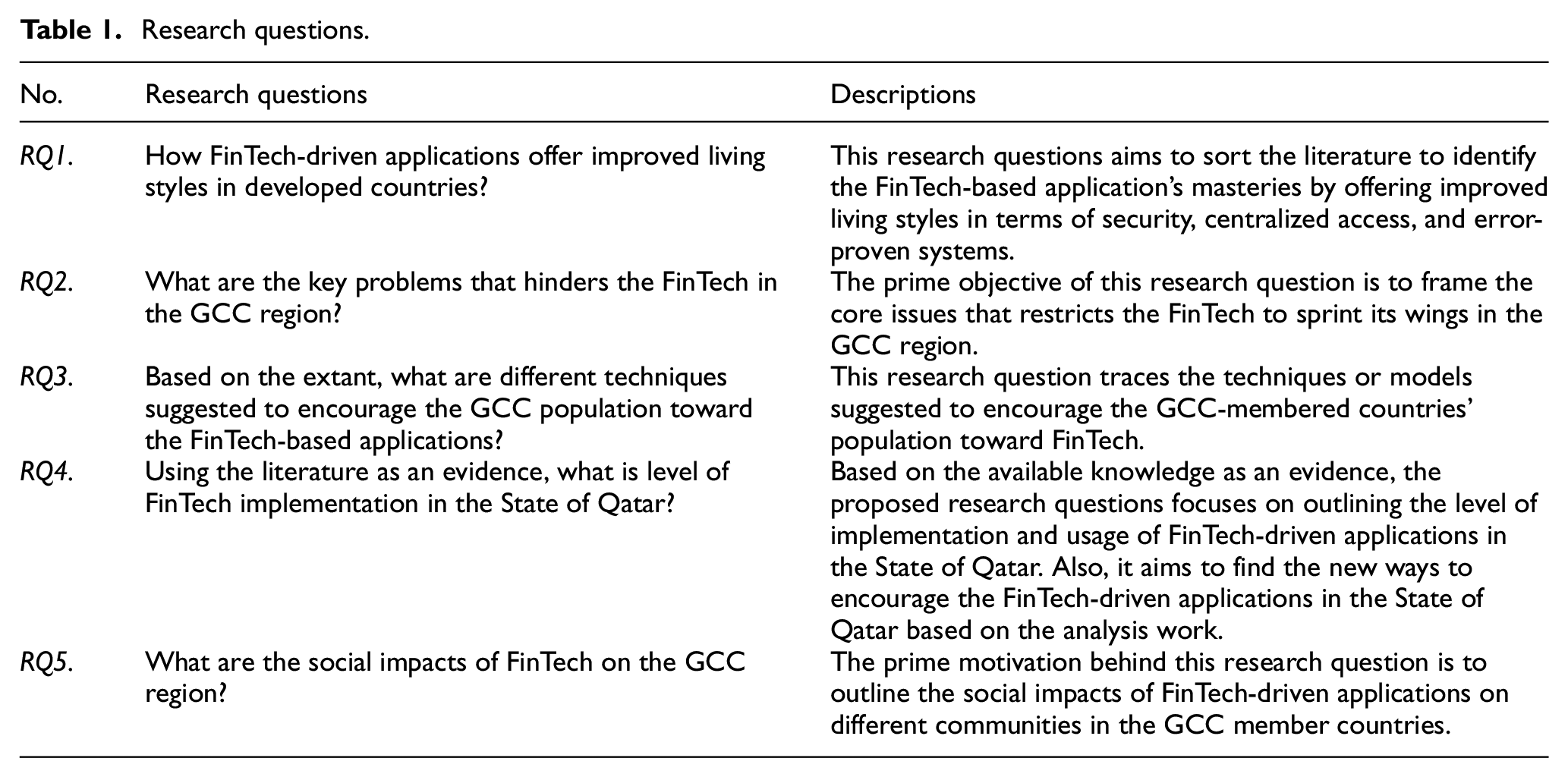

For committing this systematic mapping, we couched five different research questions (RQs), depicted in Table 1. These research questions were framed by keeping the goal in mind to analyze the FinTech domain with different perspectives.

Research questions.

Search strategy

After crafting the research questions, the next step is to define a search strategy for collecting relevant research articles. The search strategy followed for the proposed research work is depicted in Figure 4 below. During the articles accumulation process, all the articles are downloaded from the library using a search query (based on the finalized research keywords). This query was furtherly tuned and refined based on the library requirements and results. In case if more non-relevant articles retrieved then the query was more refined and become more specific to the topic of interest (this not only ensures the accumulation of most relevant articles but it also makes the inclusion/exclusion process more simpler; as there are no more redundant or non-relevant articles to exclude).

The search process.

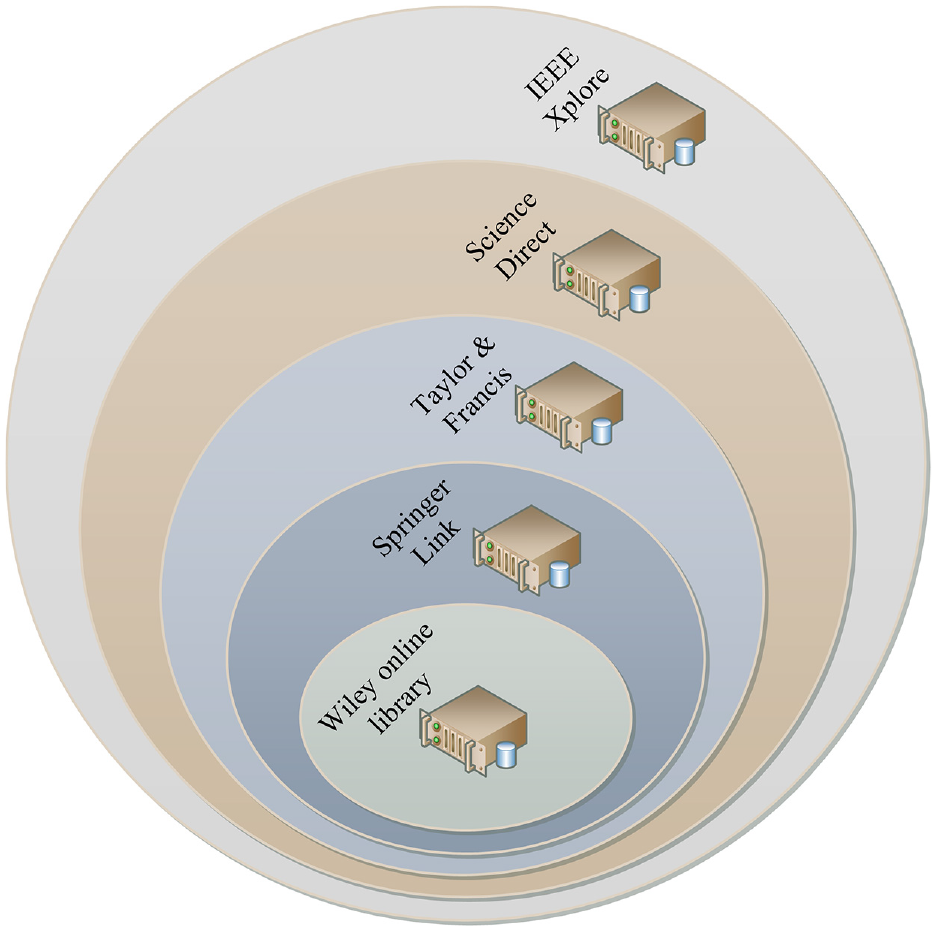

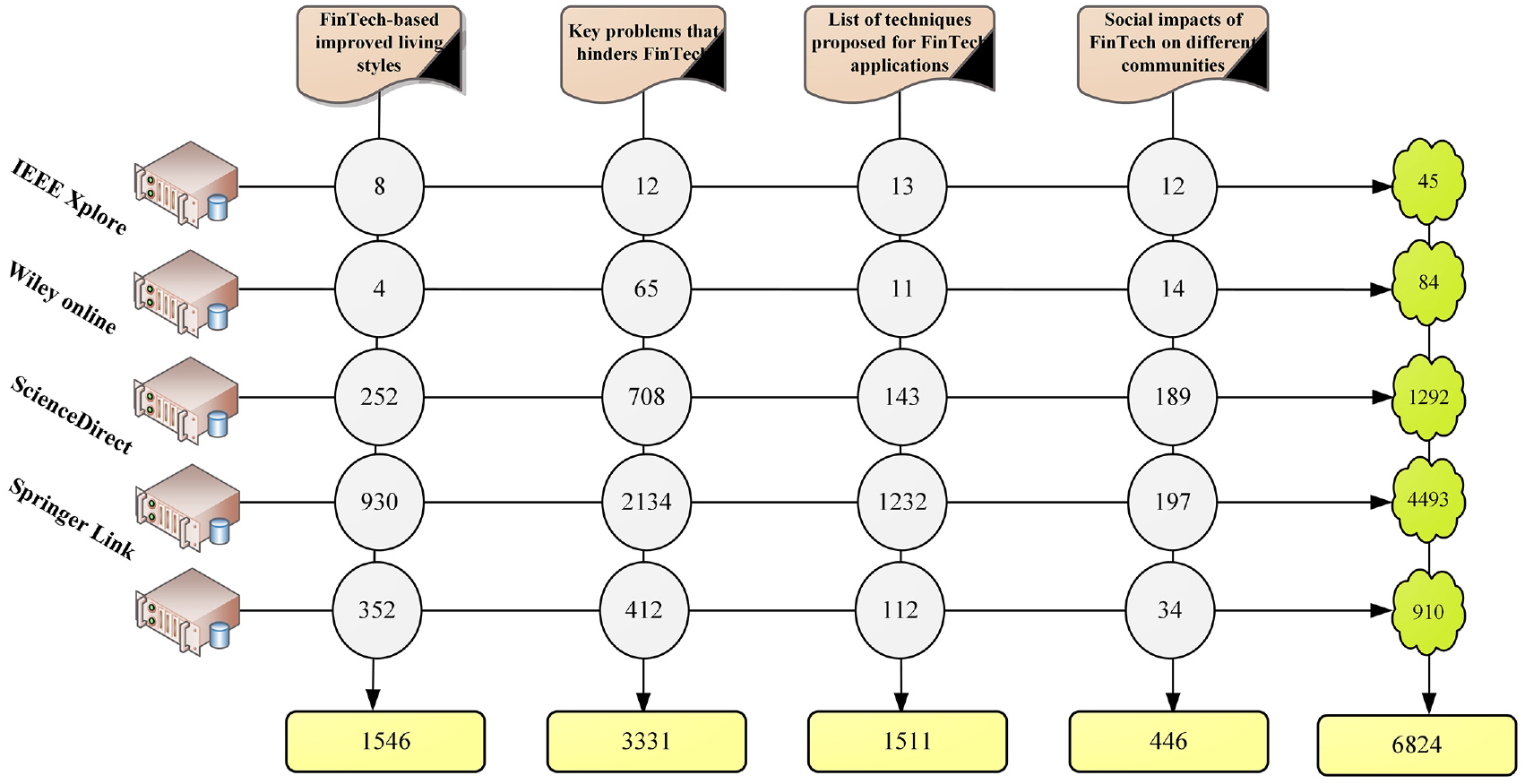

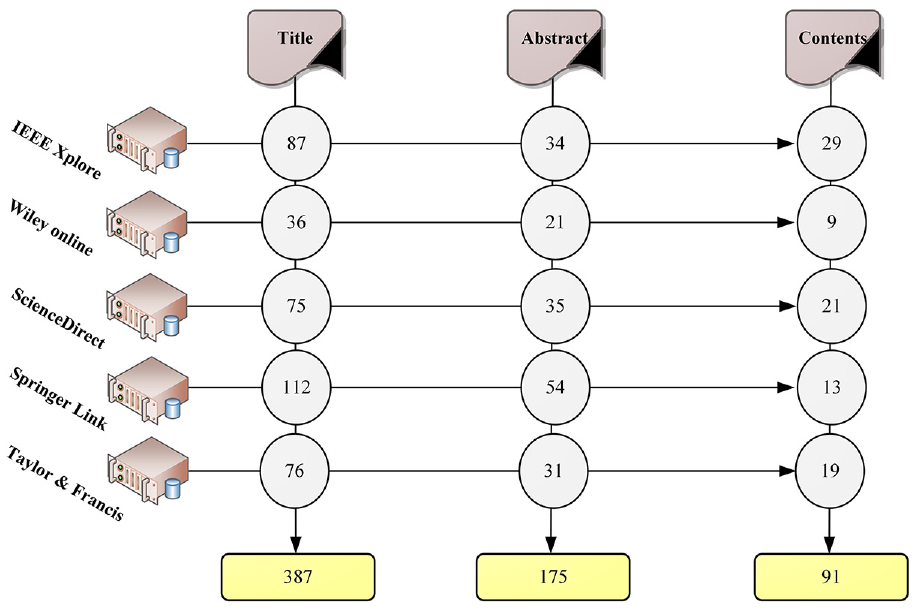

After finalizing the search process (to download relevant articles), the next step is to target the peer-reviewed online repositories to accumulate relevant articles. In our case we selected IEEE Xplore, ScienceDirect, Taylor & Francis, SpringerLink, and Wiley online library as depicted in Figure 5. Based on the RQs, the keywords were identified, and then queries were framed to download articles from the targeted online repositories. The queries were tuned based on the search results and relevant articles. Snowballing 40 was used to ensure the accumulation of each article. A total of 6824 articles were accumulated during the search process as depicted in Figure 7.

Online databases used for articles accumulation purposes.

The pool of relevant articles

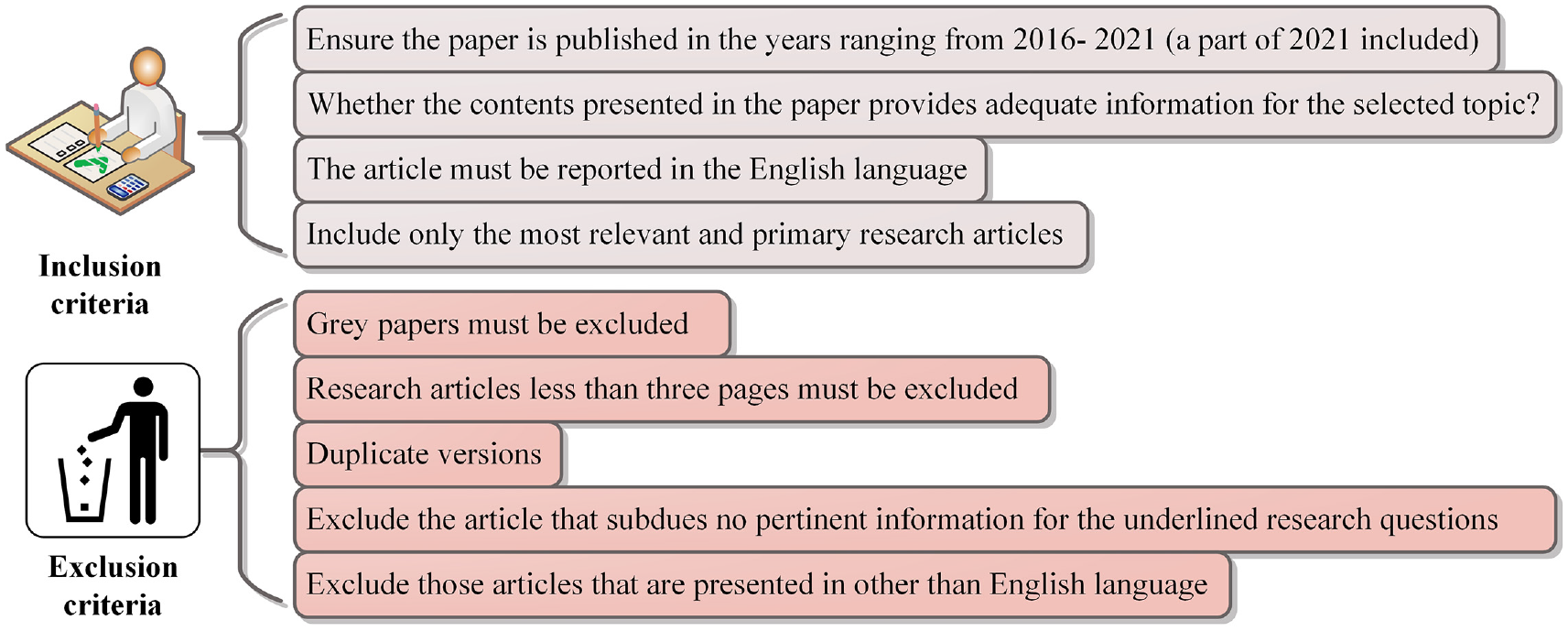

To develop a final pool of relevant articles, inclusion and exclusion criteria is defined as depicted in Figure 6 below. It is the most hectic job in an SLR work to decide for whether an article should be included in the final pool or not? As this step laterally ensures the quality of a systematic research work. To address this problem, we (the authors) combinedly searched each library and downloaded articles. A manual voting mechanism is followed to validate the relevancy of a certain research article with the selected topic. For the inclusion or exclusion of an article, if more than half were agreed, then that paper was included, otherwise excluded from the final pool of relevant articles.

Articles selection criteria during the search process.

After searching the libraries and follow the search criteria represented in Figure 6, the number of articles retrieved are depicted in Figure 7 below.

Number of articles retrieved during the initial search process.

During this initial search process, we retrieved a huge number of articles for each research question. Still, the prime objective of this step is only to select the most relevant research articles. So, the accumulated themes were further refined and assessed based on the title, abstract, and description (contents) presented in the paper. The corresponding results of this filtering process are depicted in Figure 8. A total of 91 articles were finalized for the assessment and analysis purposes.

Contribution of research articles in the final pool.

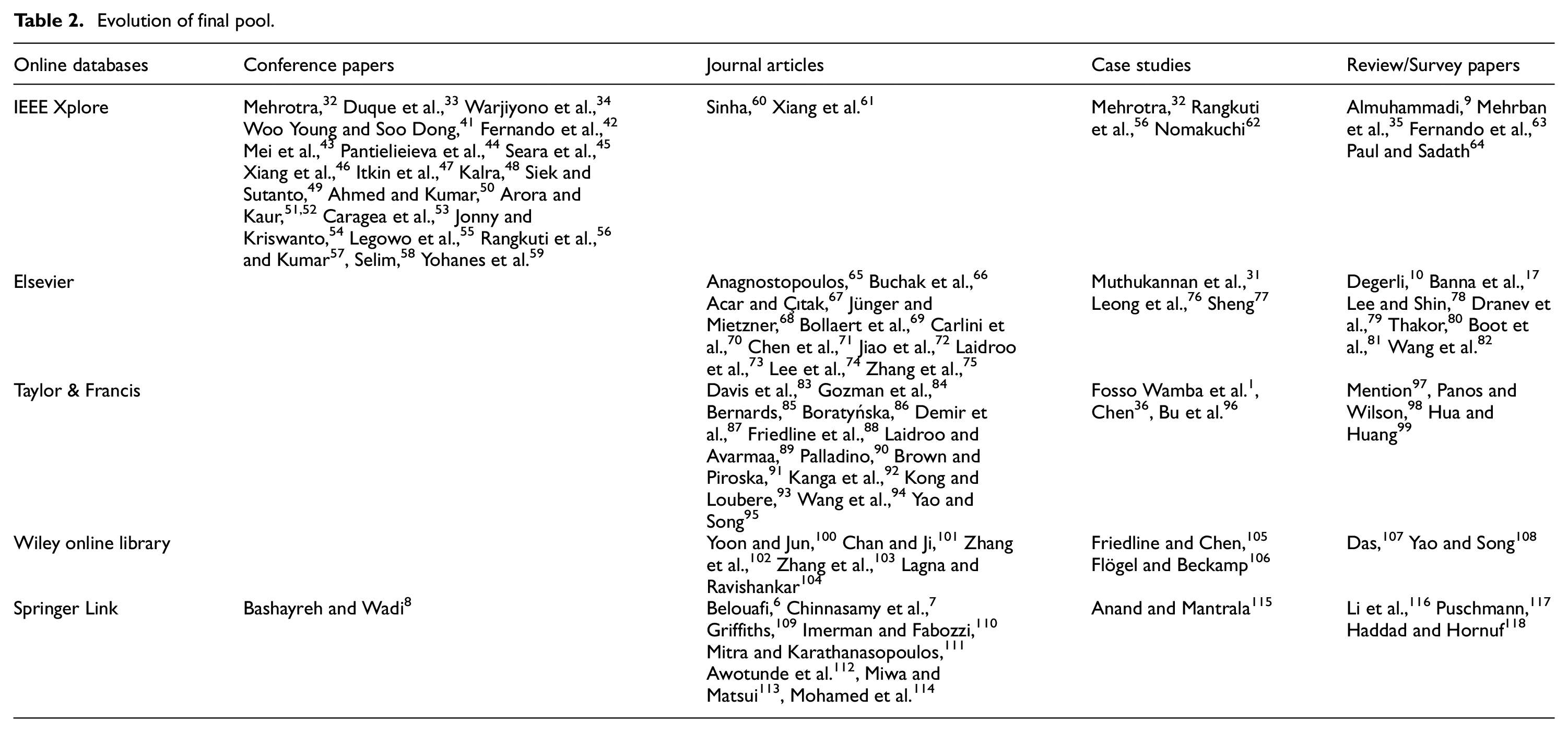

The details regarding number of journal articles, conference papers, case studies, and review articles contributed in the final pool is depicted in Table 2.

Evolution of final pool.

Quality assessment criteria

After developing a final set of relevant articles, the next important step is to analyze each article against each research question using a certain quality criterion. A grading mechanism is ensued to validate all 91 research articles. The grading mechanism followed for this systematic assessment process is : (1) If an article exactly answers a specific research question, then it is allotted a weighted numerical value of 1, (2) If a certain research article fragmentarily satisfies a research question, then it is allotted a numerical weighted value of 0.5, and (3) If a research papers fails in satisfying a research question then it is assigned a value of 0 (this represents the irrelevancy of an article with that particular research question).

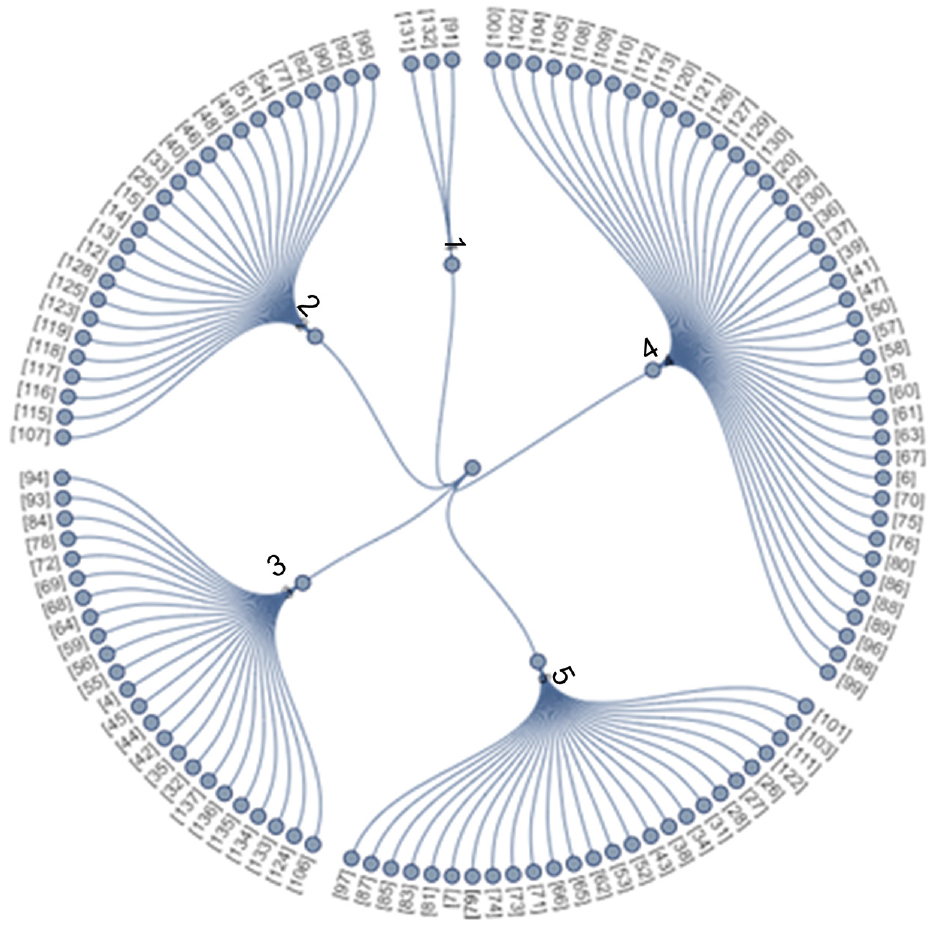

After accomplishing the quality assessment process, the relevancy of each article along with aggregate score (by adding all the grading scores for each article). The underlined results are depicted in Figure 9 below.

Relevancy of each article with the proposed research problem.

The highest aggregate value represents the most relevancy of an article with the selected research domain.

Results and discussions

With the unremitting flux of digital and technological transformation, we are now avouching rampant disruptions in financial and banking sectors that are considered the most aching sectors nowadays. Especially with the emergence of FinTech, a fat umbrella term that portrays disruptive technologies in the financial services sector. Globally, total investments in the FinTech have grown exponentially from $1.8 billion in 2010 to $19 billion in 2015.119,120 Keeping in view the interest of business tycoons in the FinTech-driven applications, the researchers paid a significant attention toward the development of smart FinTech-based applications. This section of the paper aims to analyze the published research work by identifying the gaps in the literature and bridge these gaps by suggesting new gateways for future research directions.

How FinTech-driven applications offer improved living styles in developed countries?

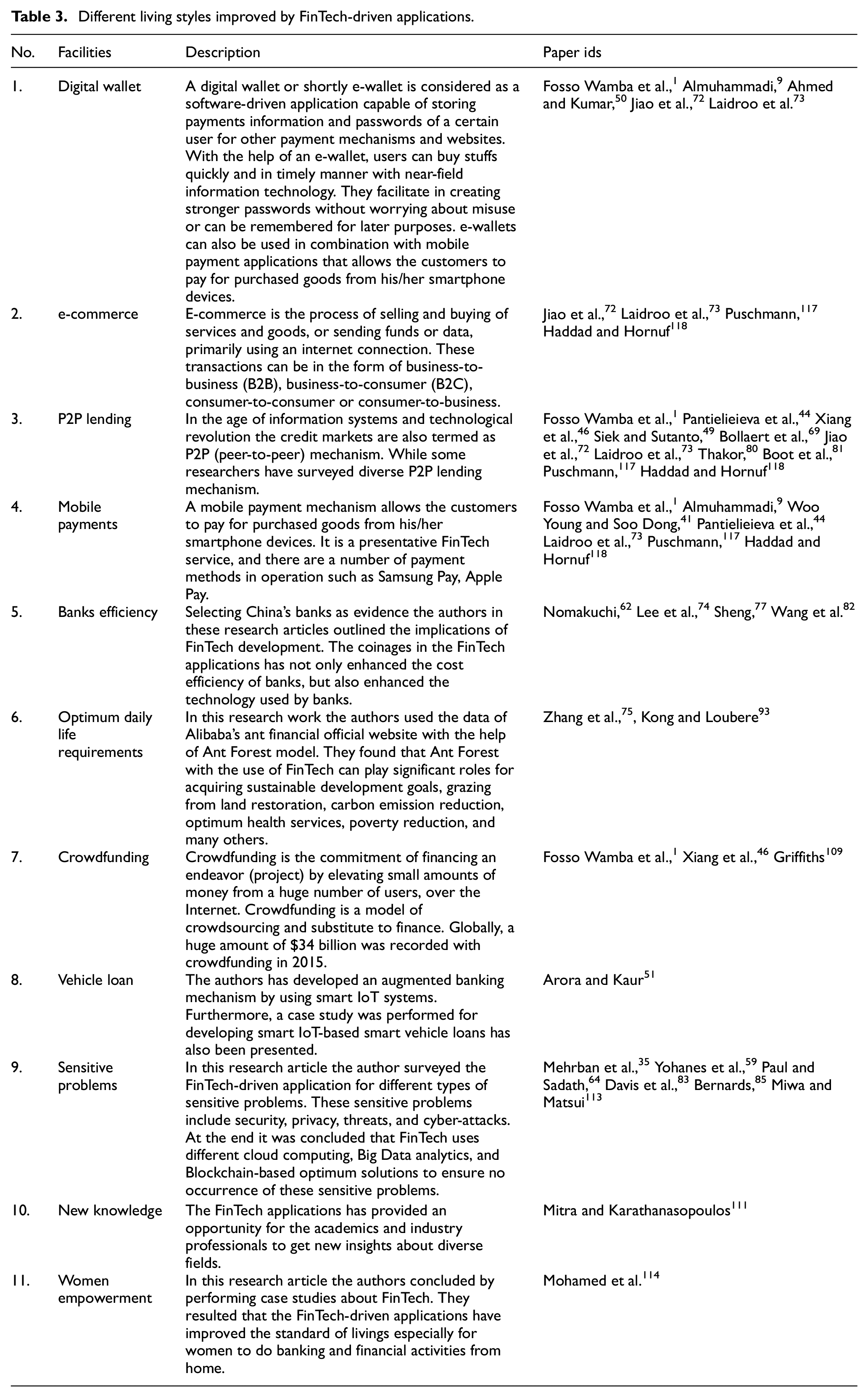

After scrutinizing the extant it was concluded that the countries that cognate with the advents in the information system and FinTech-driven applications were nowadays considered as the developed countries in the world like United States of America, China, United Kingdom, and a few others. In contrast, the countries they tried to adapt these technologies, but face challenges are nowadays listed as the developing countries such as India, Pakistan, Iran, etc. Laterally the countries shown less interest or left far behind from the aforementioned categories are listed in underdeveloped countries such as South Sudan, Central African Republic, and many others. Gearing these smart financial applications, the developed countries have mostly the non-cash communities and an easy access interface for the poor people to start new business startups, etc. Some of the improved living styles that were recorded in the published research work are depicted in Table 3.

Different living styles improved by FinTech-driven applications.

After assessing the final relevant articles, it was concluded that FinTech-driven applications have staged an improved living styles for its users with the help of Blockchain assisted smart solutions. These smart solutions ensure integrity of sensitive information, frugality of new knowledge, women empowerment, easier transaction and mobile payment interface, borrowing money from banks for cars, homes, and other basic needs.

What are the key problems that hinders the FinTech in the GCC region?

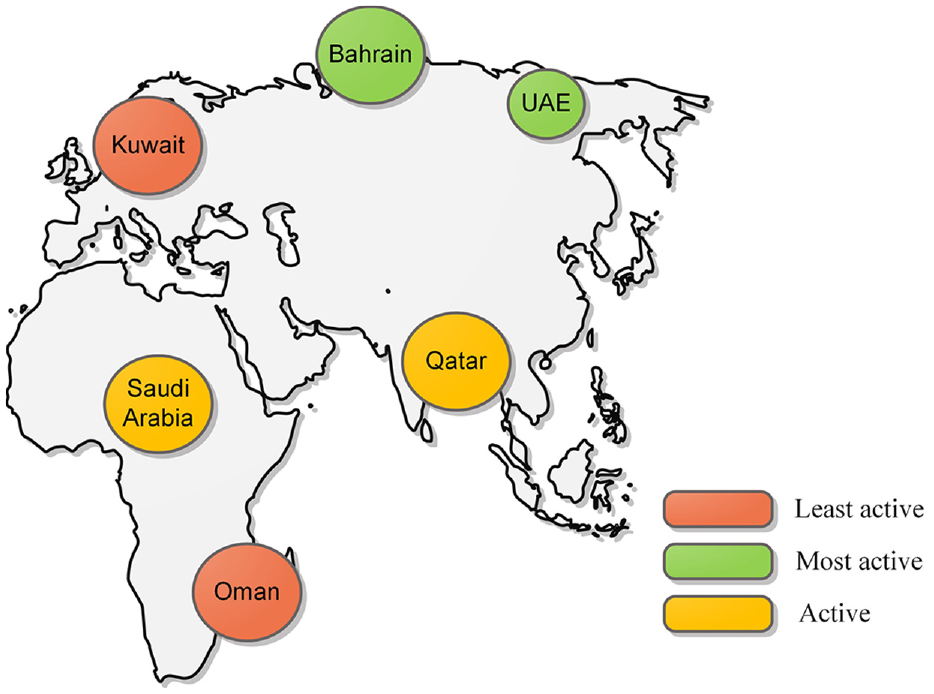

Based on the IMF reports the GCC member countries (including six countries named Bahrain, Kuwait, Oman, Kingdom of Saudi Arabia (KSA), United Arab Emirates (UAE), and the State of Qatar) are listed in developing countries list.121,122 After thoroughly analyzing the extant, it was concluded that some of the GCC member countries like Turkey, KSA, UAE, Bahrain and the State of Qatar have reported significant work and encouraged FinTech-based revolution in their financial and banking sectors but still there is a lot of work to do to track the FinTech and meet with the digital revolution. A survey report 123 aired in 2017 has shown the level of regulation activity in the middle east including GCC region. Figure 10 represents the GCC member countries regulation report.

Level of FinTech regulation in GCC region.

Some of the key problems that hinders the FinTech to open its headwings with full capacity in the GCC region are listed below.

These are some of the prime reasons that restricts the FinTech to open its wings with full strength in the GCC region. If these problems are addressed on priority basis then FinTech can be emerged in this region with full hype. Resultantly, the living styles of the population living in this region will be enhanced.

Based on the extant, what are different techniques suggested to encourage the GCC population toward the FinTech-based applications?

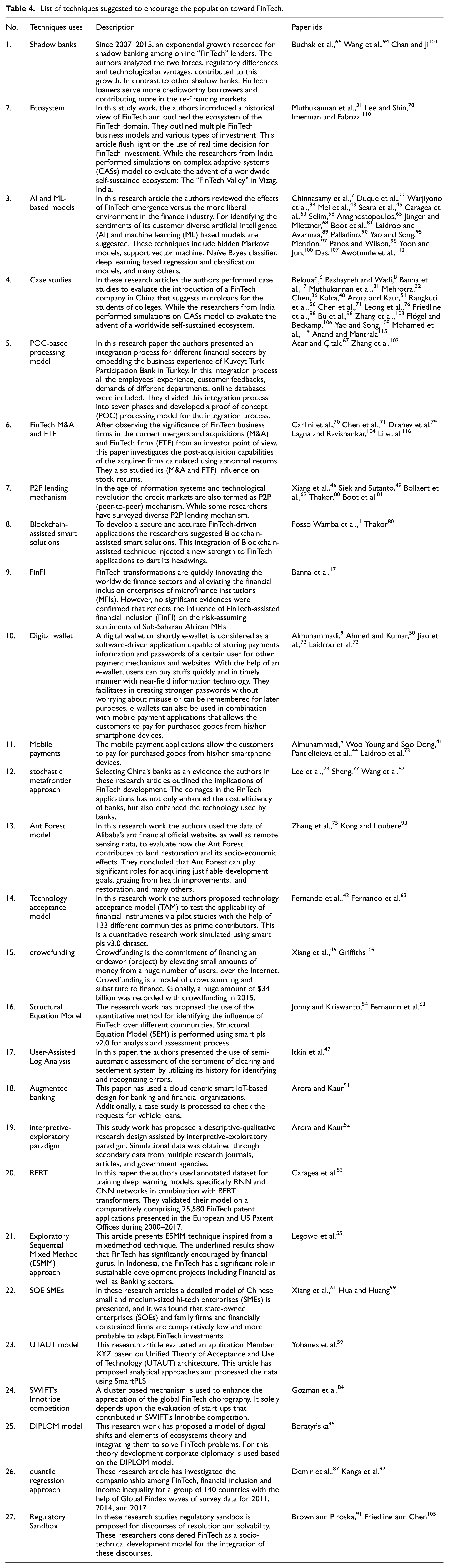

From the literature it was concluded that numerous models and techniques were adapted to develop smart FinTech applications by using mathematical and analytical applications. Some of the researchers performed case studies to inform people about FinTech applications and flaws in the traditional business models. While some researchers inspired from the extensive applications of machine learning techniques in diverse domains (healthcare, 124 internet security,125–127 text recognition domain,128–130 and many others) suggested machine learning models during the development of FinTech-driven applications to analyze the sentiments of the population regarding FinTech applications. List of other models and other techniques suggested are depicted in Table 4 below.

List of techniques suggested to encourage the population toward FinTech.

From the above discussion presented in Table 4 it is concluded that the researchers paid a significant attention toward the machine learning models to analyze the behavior of multiple user regarding FinTech applications. Though a lot of work has been reported from the developed countries but comparatively there is no significant work reported from the GCC member countries.

Using the literature as an evidence, what is level of FinTech implementation in the State of Qatar?

After analyzing the literature it was concluded that United Arab Emirates, 131 Turkey,10,132 Saudi Arabia, 133 and the State of Qatar134–136 has shown a keen interest in adopting FinTech-driven applications in high regulation sectors including banking and financial sectors. This keen interest in adopting the new technologies has strengthen the abilities of these countries to face the hard challenges of Covid-19 pandemics compared to other GCC member countries. Although Kingdom of Bahrain has also shown interest by encouraging its population especially women to follow FinTech-driven applications.50,114

From the extant it is concluded that a lot of research work must be carried on from this region (GCC) by introducing a Blockchain driven, and venture capitalist facilitated ecosystem. This research work will help in: (1) creation of new markets and new startups; (2) improved deliverables costs; (3) better processes; (4) commercial evaluation of trades and professions; (5) innovative workflows; (6) smart revenue and regulation scheme; (7) skill evaluation of an institution per unit area; (8) reduction in the OPEX and CAPEX of state development bodies; and (9) achievement of new knowledge regarding blockchain and crowdfunding-based FinTech applications.

What are the social impacts of FinTech on the GCC region?

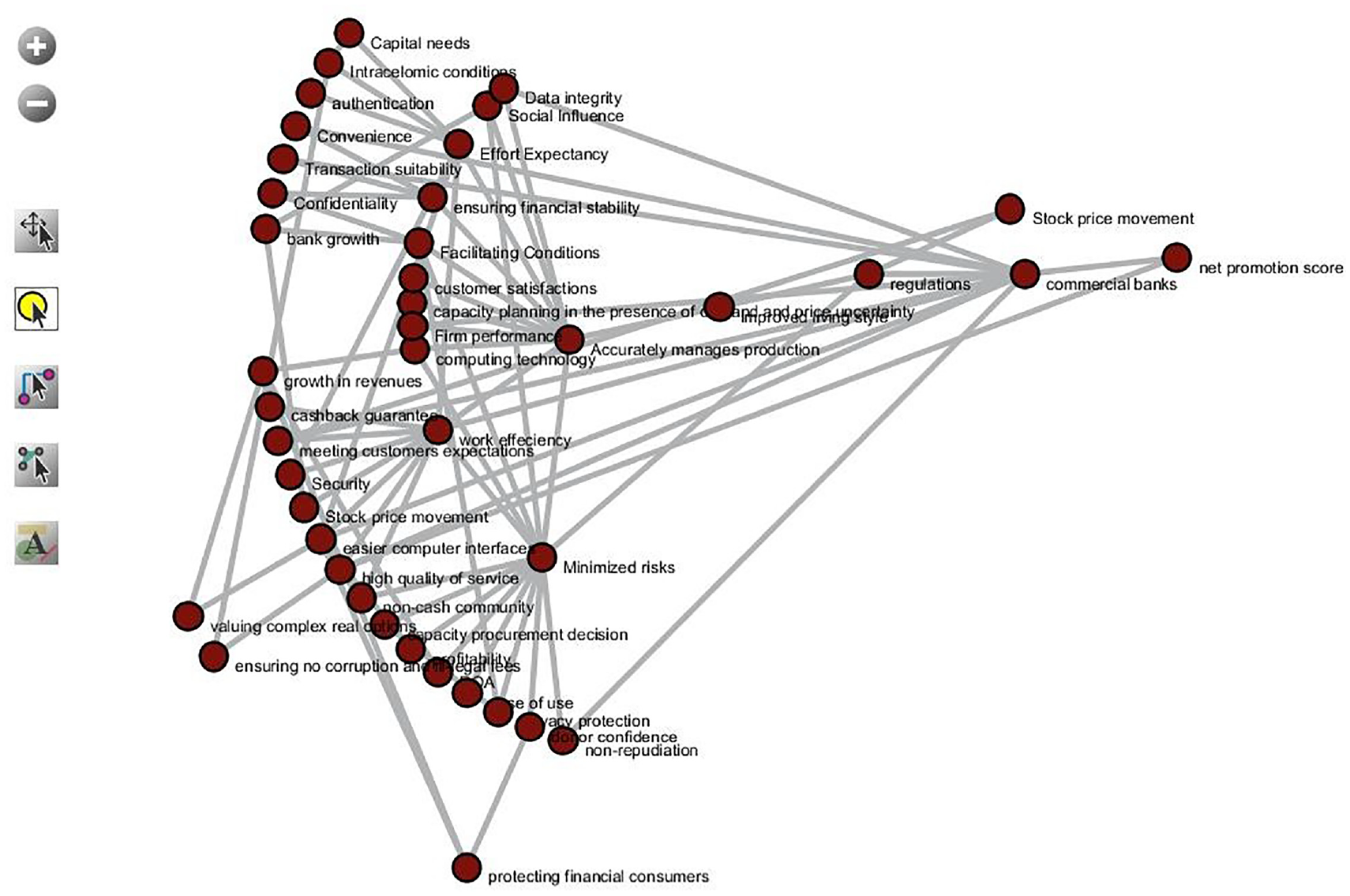

After boning the reported research work in the FinTech domain, it was concluded that the countries that cultivates smart applications especially the FinTech-driven applications in their business and financial sectors, they provided an easy interface for serving both the poor and rich communities. Assisting the poor community by providing an easy access to borrow money for their basic needs including education, new business startup, or building homes etc. On the other hand, profiting the richer community by providing a safe and secure model where they can invest, can authenticate, availability of error proven systems etc. Also these FinTech driven applications ensures no provides high facilities to its customers and poor communities by restricting corruption and ill-legal fees by providing non-cash community, 3 smart intelligent interface using advanced artificial intelligence and machine learning models,137,138 presenting globalized economy, providing a centralized controlling mechanism where the customers can have access from everywhere and every time. A huge number of social impacts that influences our lives are depicted in Figure 10 below. Sci2 Tool 139 is used to sketch the Figure 11.

Social impacts of FinTech applications.

On the other hand the GCC member countries (Yemen, Syria, and others) that do not follow or show interest (due to unstable environment or some other reasons) in adapting these FinTech based applications (in their high regulation sectors including banks and financial organizations) are extensively influenced from corruption, instability, money laundering, imbalance transfer of money in different hands, no centralized control, no authentication and integral interface, cash oriented exchange services (that are full of fraudulent, black money, fake currency notes etc.), poverty, voracity, and many others.

In order to control these key problems in the GCC member countries a significant attention is required from both the research communities and financial organizations. The research community must work on identifying the easiest ways by selecting venue for workshop or case studies to encourage people to participate and encourage them toward the FinTech-driven applications to improve their living styles. While the financial sectors do invest on these poor communities to assist them by providing an easy access to borrow money for their basic needs.

Future research directions

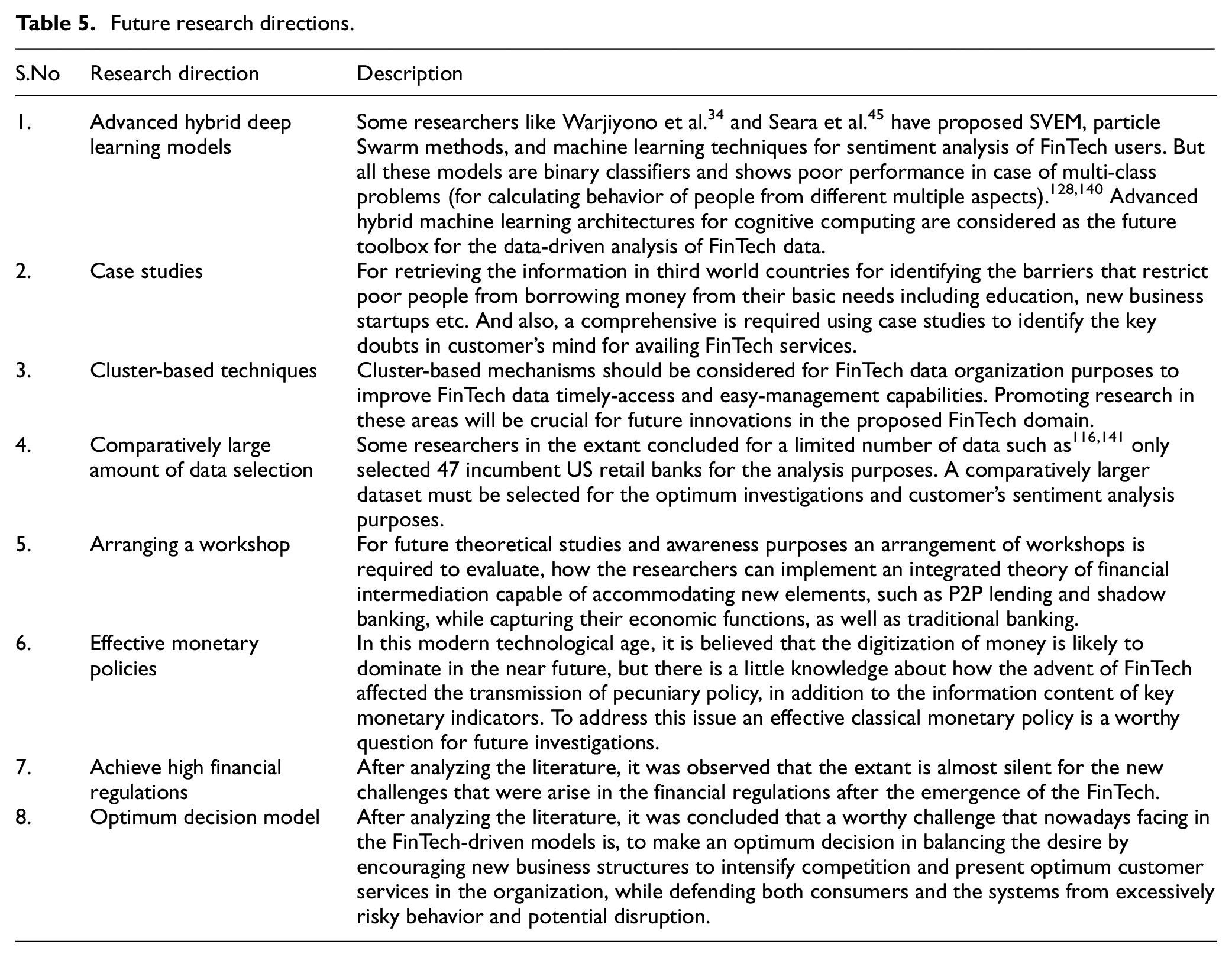

After polishing this systematic analysis, some future research directions are endorsed in this SLR work. These new research directions will cheer no heterogeneity among payment schemes in different payment processes, meliorates the financial inclusion of previously excluded market segments, present the strategic capabilities for a firm to occupy a market niche in financial sector, make the poor community in the GCC region able to borrow money for their basic needs (education, cars, safe resident environment, new business startup etc.). Some of the few research directions are depicted in Table 5.

Future research directions.

Conclusion

The emergence of FinTech is deliberated as a new paragon for providing potent financial services by integrating smart IoT devices. Payment is an imitable FinTech service, and there exists innumerable payment stratagem in operation. However, there exists a potent variegation among payment strategies in the form of payment processes, transaction settlement schemes, and software agent deployments. Accordingly, for any two different payment strategies a payment cannot be established. The gamut of doable financial stability risks graveled by FinTech, which claims a systematic analysis by entities presenting financial stability, is deceived. The demand for presenting a reliable level of information security of financial intermediation, taking into account a digitalization on the basis of new information and communication technologies and info-communication systems, is substantiated. To address these problems, a systematic monitoring work is performed, where a total of 91 most relevant research articles analyzed based on five different research questions. The findings of this research work will not only help the state development bodies by encouraging its stakeholders to use FinTech-driven applications in banking, markets, etc. but it will also help the people in maintaining great connections with the Ministries of Foreign Affairs, Economic Affairs, the Dutch regulators, the Dutch Central Bank (DNB), as well as the Authority on Financial Markets (AFM), This systematic mapping offers new research directions for the research community to explore in the near future.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Qatar University Internal Grant No. QUHI-CBE-21/22-1 funded this publication.