Abstract

The author uses Canadian public-sector union contracts from a 30-year period to study the factors influencing wage setting. He also undertakes complementary analyses of contract duration and the use of Cost-of-Living Adjustment (COLA) clauses to examine how variables capturing uncertainty and contracting costs affect contract length and the use of indexing provisions. Findings show that inflation expectations, unemployment rates, wage growth, and COLA clauses are associated with fairly large effects on wage settlements that are much more prominent during the period prior to the Bank of Canada adopting an inflation target (i.e., before 1991). They also indicate that variables capturing inflation uncertainty and contracting costs do not have a large effect on contract duration, but contracting costs do have a larger effect on the use of indexing provisions. Results suggest that indexing provisions are an important inflation coping mechanism for both wage settlements and contract duration, with bargaining pairs willing to trade off smaller base wage changes and longer contracts for them.

Keywords

The public sector is an interesting arena to study wage-setting behavior, as unionization rates and collective bargaining coverage tend to be much higher there than in the private sector. For example, unionization rates in the public sector can be 2 to 4.5 times larger than the corresponding rates in the private sector (Riddell 1993; Uppal 2011). In collective bargaining contracts, nominal wages are fixed and set for some specified period. Expectations of future inflation are thus of great importance to bargaining teams, as higher expectations of future inflation can require larger wage increases to maintain the purchasing power of wages. While bargaining teams might have expectations about future inflation, unexpected changes in prices that erode the purchasing power of earnings are a possible concern. Union contracts can also contain indexing provisions, however, often referred to as Cost-of-Living Adjustment (COLA) clauses, which can offset all or part of these unanticipated changes in prices. COLA clauses, which were more common during the 1970s and 1980s, have been in decline over the past few decades (Labour Program 2015). For public-sector workers who do not have the right to strike and use interest arbitration to resolve bargaining impasses, expectations of inflation are also relevant, as arbitrators consider cost-of-living as a criterion when determining their awards. Consequently, inflation expectations can play a key role in wage setting.

The state of the economy, such as the overall level of wage growth and the unemployment rate, which can reflect the tightness in labor markets, may also affect bargaining positions in contract negotiations. For example, if the labor market is tight (i.e., unemployment rates are low) then unions may negotiate for larger wage increases because the “outside wage option” for workers may also increase. Similarly, unions may observe wage increases in other sectors, which can affect their expectations for wage settlements. Moreover, labor market conditions can also enter into arbitrator decision-making, as arbitrators use the criterion of comparability and consider labor market conditions in related or other markets to determine the wage settlements in their awards.

Another factor that may influence wage setting in the public sector is the political or institutional environment, as governments might move to curb wage growth of public-sector workers. The US state of Wisconsin’s Act 10, which significantly weakened the bargaining power of its public-sector unions, is an example of such an effort. Similarly, the federal and provincial governments of Canada have often implemented legislation to curb wage growth for public-sector workers at various times over the past half century (Thompson and Ponak 1992; Rose 2005). In addition, governments can enact special legislation to intervene directly in a work stoppage.

I study public-sector wage setting using contract data from the Canadian public sector from 1978 to 2008. Union contract data are less likely to be prone to measurement error in wages from individual self-reporting, which is often a problem in labor market surveys. I use data from the federal and 10 provincial jurisdictions and consider the effects of expected inflation, labor market tightness, wage growth in a jurisdiction, COLA clauses, and the Bank of Canada’s inflation-targeting policy on wage settlements. Bargaining pairs may also adapt to rising and uncertain inflation by adjusting the length of contracts and using indexing provisions. Consequently, I also include complementary analyses of contract duration and the use of COLA clauses, which examine how contracting costs and uncertainty can influence the length of contracts and whether contracts contain indexing provisions. Because wage settlements, contract duration, and the use of COLA clauses can be interrelated, my preferred estimates for each of these outcome measures are based on an instrumental variable estimator.

My study period includes high, moderate, and low inflation regimes, unlike earlier studies of contract data that were primarily based on data from higher inflation periods only (e.g., Cousineau and Lacroix 1977; Auld, Christofedes, Swidinsky, and Wilton 1980; Card 1990). The Bank of Canada also adopted an inflation-targeting policy in 1991 to combat high inflation, which divides my data into two policy regimes with respect to inflation. This detail means I can study wage settlements and contract features in both low and stable inflation periods, as well as periods with higher and more uncertain inflation, and determine if any heterogeneity is present in the effects. Along with this variability in inflation, my study period includes several recessions, which provides more variation in labor market conditions than reported in earlier studies. My study period also includes examples of direct government intervention in public-sector collective bargaining in which they used legislative means to limit the wage gains public-sector unions could make while bargaining as well as to intervene in some contract disputes.

Data

The Labour Program at Employment and Social Development Canada collects data on union contract settlements. Unfortunately, the Labour Program no longer makes contract-level data publicly available, as they currently provide only extracts of the data. Consequently, I use the contract-level data studied in Campolieti, Hebdon, and Dachis (2014, 2016), which I believe is the most recent and complete listing of contract data available for Canada.

These data contain information on the annual negotiated settlement rate for wages and other contract details from 1978 to 2008 for bargaining units with 500 or more members. These data include the average annual increase (or decrease) in wages for each contract. The settlement data also include information on the dispute resolution procedure available to a bargaining unit to resolve a bargaining impasse if one were to occur and whether the settlement was legislated. Legislated settlements include two types. On the one hand, some legislated settlements are “back-to-work” orders and reflect that the government in the jurisdiction intervened directly in the work stoppage to end it. In Canada, this sort of intervention occurs when the government perceives a threat to public health and safety or the economy. On the other hand, the legislated settlement variable also captures some broader forms of government restraint that occurred during my study period. Such restraint could cap growth in wages as well as limit access to dispute resolution procedures, such as interest arbitration, for all public-sector workers. I discuss these sorts of initiatives in the next section. The contract data do not distinguish between the back-to-work orders and the broader legislation and only indicate whether there was a legislative restraint of some form, not the form of the restraint. The data also indicate whether the contract contains a COLA clause. Unfortunately, the more recent versions of the contract data do not contain details on the nature of the escalators in the COLA clauses, unlike earlier versions of the contract data that did provide these sorts of details (Christofedes 1987; Card 1990). Finally, the data also provide the effective and expiry dates for a contract, which I use to compute the length of the contract (in months).

I merge information on actual inflation (computed from the Consumer Price Index (CPI), all items), wage growth in a jurisdiction (for all industries), and unemployment rates (both sexes, aged 15 and older) to the contract data. I use the actual inflation rate to create a measure of the expected inflation rate with a time series model (see the Online Appendix for details). This time series model also produces a measure of uncertainty about future inflation expectations, which I refer to as inflation volatility.

Empirical Methods and Public-Sector Bargaining

For wage settlements, I focus on estimating specifications of the form

where j denotes a bargaining pair, i denotes jurisdiction, t denotes year,

I estimate Equation (1) using ordinary least squares (OLS) as it provides a useful baseline. I also use a fixed effects (FE) estimator, which includes a bargaining pair–specific fixed effect, as I have longitudinal data on bargaining pairs. The COLA clause is endogenous, however, so the OLS and FE estimators of Equation (1) will be biased if the specification includes an indicator for COLA clauses. To address this endogeneity I also estimate Equation (1) using an instrumental variable (IV) estimator. I follow earlier papers (e.g., Christofedes 1990) and use an indicator for whether the previous contract included a COLA clause as an instrument for the COLA clause in the current contract. 2

Expectations of inflation can factor into contract negotiations, as unions will ask for wage increases to offset the expected decline in their purchasing power. Labor market conditions may also have an effect on wage settlements. The Phillips curve expresses a negative trade-off between wage growth and unemployment (Phillips 1958). In particular, tighter labor markets (with low unemployment rates) can reflect higher wages, while slacker labor markets (with higher unemployment rates) can manifest in lower wages. The wage growth control,

As the use of a strike or interest arbitration to settle a bargaining impasse is endogenous, OLS estimates of their effect on wage settlements will be biased. Consequently, I do not control for how the contract was settled but rather the dispute resolution procedure available to resolve an impasse if one were to occur. For example, 79% of the contracts in my sample have the right to strike, but strikes occur in only 4% of the contracts. Five types of dispute resolution regimes occurred during my study period. First, the right-to-strike designation, which provides unions the (unrestricted) right to strike and employers the (unrestricted) right to lock out workers if a bargaining impasse occurs and the conditions for a legal strike/lockout are met. Second, compulsory interest arbitration, whereby a bargaining pair must use interest arbitration to resolve a bargaining impasse. Third, the choice-of-procedure designation, in which a bargaining unit can pick either a strike or interest arbitration as a dispute resolution procedure prior to beginning bargaining. Fourth, the essential-service designation, which limits or restricts a bargaining unit’s right to strike. 3 Fifth, the duty-to-bargain designation, in which case the bargaining unit has the right to bargain but does not have access to any dispute resolution procedures if it reaches an impasse. The duty-to-bargain regime includes only four contracts, as it was replaced by formal dispute resolution procedures as the study period progresses.

As discussed earlier, governments can also intervene in collective bargaining, which can limit wage settlements. A few types of legislated settlements occurred during my study period. Some of the legislated settlements occur because there were a few periods when the federal and provincial governments used legislation to curb wage settlements in the public sector. For example, the “6-and-5” program, which limited public-sector wage increases during 1982 and 1983 to 6 and 5%, respectively. During 1982 and 1983 inflation was double-digit and the caps on wage settlements proscribed by the 6-and-5 program were used to dampen the wage price spiral, as wage growth would slow and thus weaken inflation. The federal government as well as the provincial governments in British Columbia, Ontario, Quebec, Newfoundland and Labrador, Nova Scotia, and Prince Edward Island passed this legislation. 4 Note that under the provisions of the 6-and-5 program, bargaining units could lose access to interest arbitration to settle bargaining impasses on wages (Campolieti and Riddell 2020). In addition, following the recession of 1990–1992, the Canadian economy entered a period of limited growth, which strained the fiscal resources of provincial governments. In response, many of these governments implemented a series of expenditure-reducing measures, which also included limiting public-sector wage growth. The Canadian jurisdictions that passed this sort of legislation included Quebec, Ontario, Nova Scotia, Newfoundland and Labrador, Prince Edward Island, Saskatchewan, Manitoba, and Alberta. Finally, as discussed earlier, the government in a jurisdiction can intervene directly in the negotiations with back-to-work orders, which end a strike or lockout.

The fiscal position of various levels of government could also vary across the business cycle. For example, collective bargaining–restraint legislation may occur at times the fiscal resources of the government are strained. This suggests that the estimates of the effect of legislated settlements on wage settlements may have a negative bias. Moreover, the federal and provincial governments may use back-to-work orders to end some contentious strikes, and unions may not necessarily be able to gain favorable wage gains in these negotiations. Ellwood and Fine (1987) and Currie and McConnell (1994) argued that including year and state (jurisdiction) effects could lessen these concerns about the potential endogeneity of legislative variables. Although I am able to include year effects in all the specifications I estimate, I am unable to include jurisdiction effects, as many of my control variables vary at the jurisdiction level only and would be collinear with the jurisdiction-specific effects. Consequently, my estimates for the legislated settlement variable could reflect some bias. However, I am able to estimate a FE model with bargaining pair–specific effects, which could lessen some of the potential bias and shed light on the extent of this bias when compared with the estimates produced by the OLS and IV estimators.

Adjusting the length of a contract and including indexing provisions is another way bargaining pairs could adjust and cope with rising and uncertain inflation expectations (Cousineau and Lacroix 1977). Gray (1978) posited that contract duration is influenced by contracting costs and uncertainty. More specifically, greater uncertainty could require a decrease in contract duration and larger contracting costs could be associated with an increase in contract duration. I estimate the following specification for contract duration

where

I also estimate a linear probability model for the presence of COLA clauses

where

I cluster the standard errors for the estimates of Equations (1), (2), and (3) by jurisdiction as some of the control variables vary at the jurisdiction level only. The provincial jurisdictions would include public-sector workers who work for municipal governments, the provincial government, or provincial crown corporations, but the federal jurisdiction would include only those who work for the federal government or its crown corporations. 7 As I have a very small number of clusters (11 jurisdictions), I use the Wild bootstrap with the Webb weighting scheme to obtain p values for t statistics with proper size (MacKinnon, Nielsen, and Webb 2023; Webb 2023). 8

Empirical Findings and Discussion

Descriptive Statistics

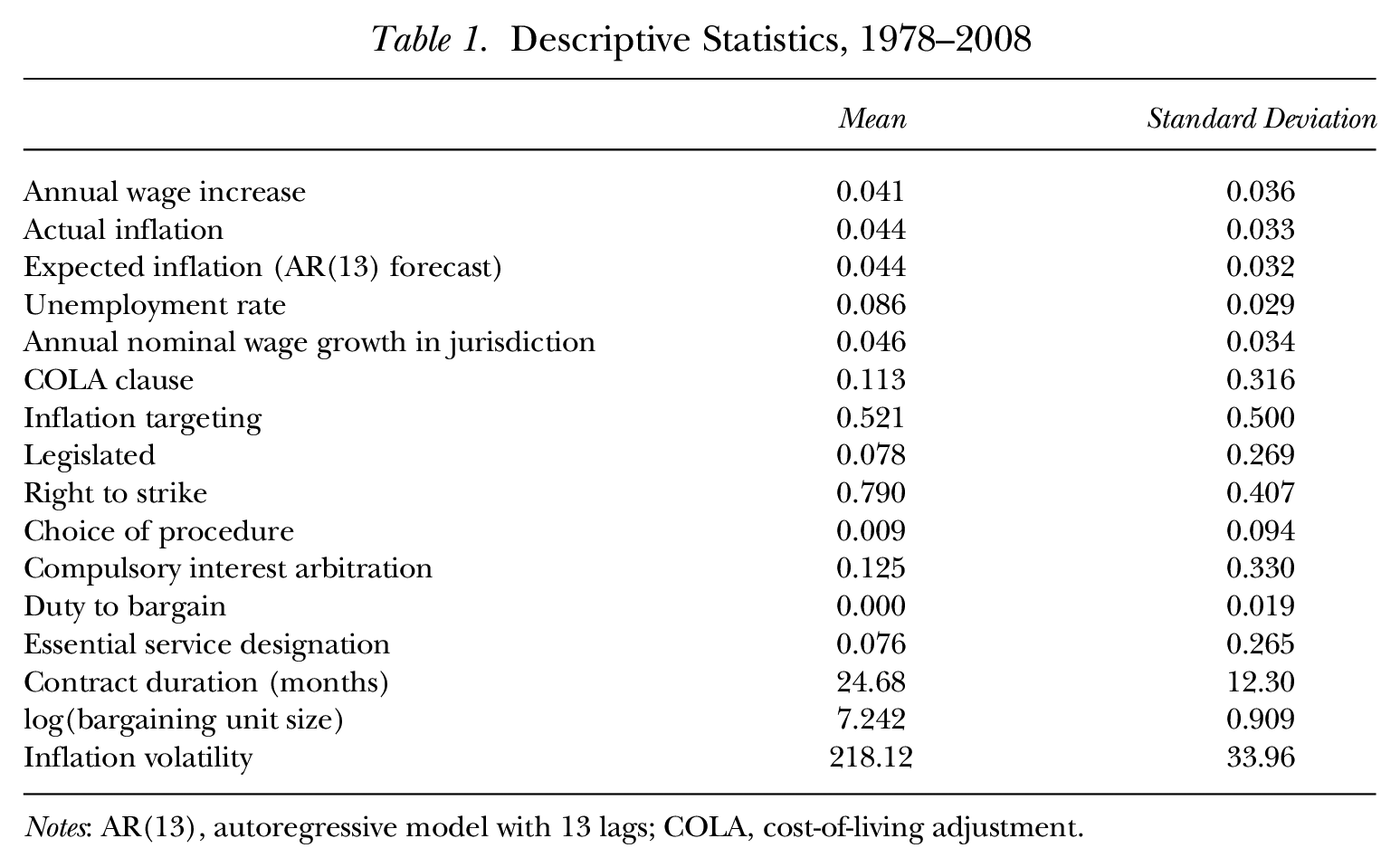

Table 1 contains descriptive statistics for the data. The mean annual increase in contract wages is approximately 4.1%. The mean of actual and expected inflation are both 4.44%. The measure of inflation volatility does not appear to have a great deal of dispersion. As can be seen in Figure A.1 (tables and figures prefaced with an “A.” may be found in the Online Appendix), the data include a large number of contracts from the 1970s, 1980s, and early 1990s, when inflation rates were quite elevated. The indicator variable for inflation targeting, which takes the value 1 for the period when the Bank of Canada adopted an inflation target, has a mean of approximately 0.5, so I have a similar number of contracts in each of these two monetary policy regimes. Unemployment rates average 8.6% during the study period and overall annual wage growth in a jurisdiction has a mean of about 4.6%. COLA clauses are present in 11% of the contracts. Most of the contracts in my sample are covered by the right-to-strike legal structure. Compulsory interest arbitration is the next most common dispute resolution procedure available (12.5%), followed by the essential-service designation (7.6%). The choice-of-procedure and duty-to-bargain designations are much less common. Government-restraint legislation of some form occurs in approximately 8% of contracts. Contract duration has a mean of about 24.7 months.

Descriptive Statistics, 1978–2008

Notes: AR(13), autoregressive model with 13 lags; COLA, cost-of-living adjustment.

Wage Settlement Regressions

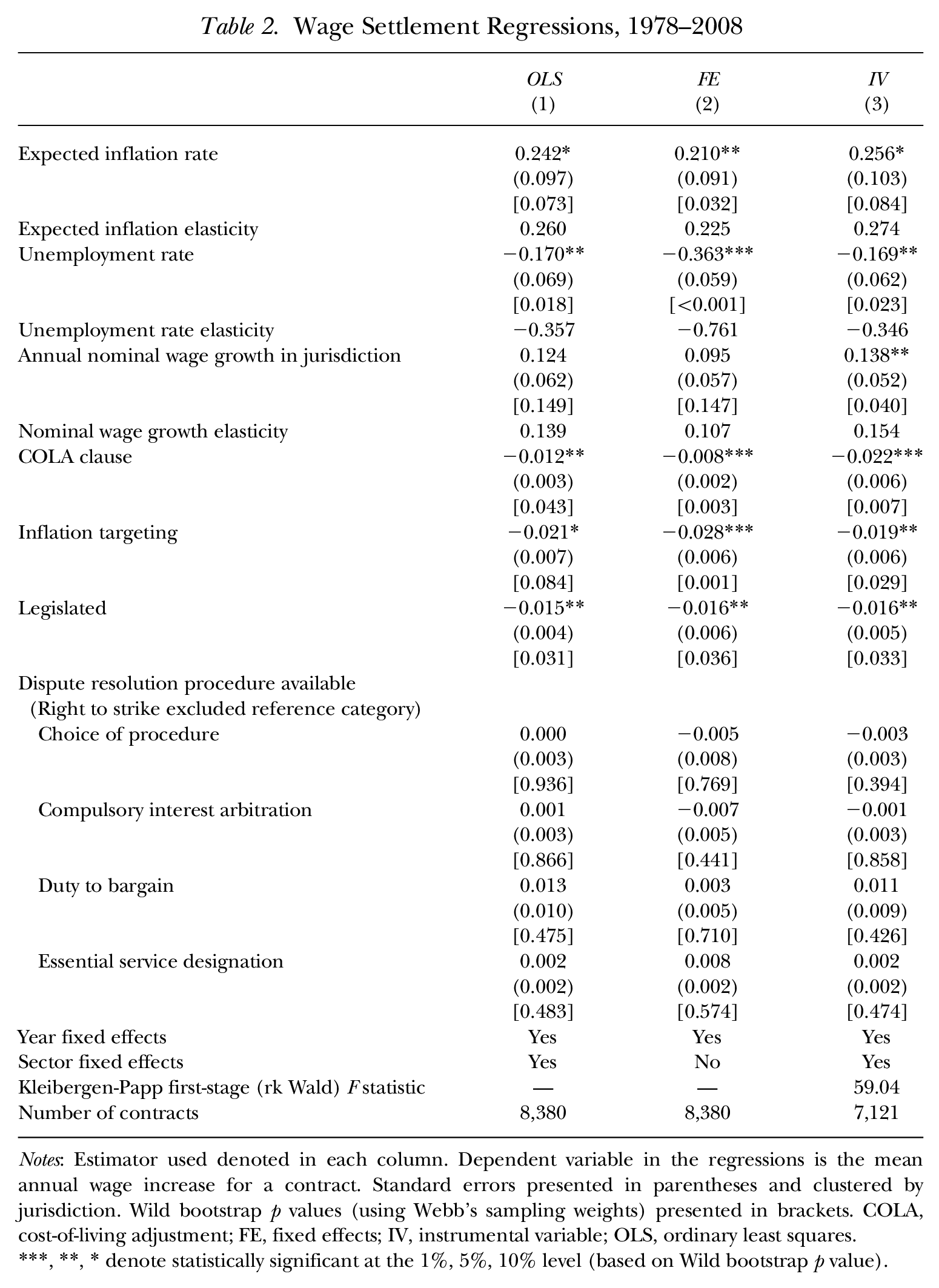

I present estimates for the wage settlement regressions in Table 2. As COLA status is endogenous, my preferred estimator is an IV estimator (column (3)). However, I still present and discuss estimates based on OLS and FE estimators to illustrate the differences and similarities between these estimators and the IV estimator. This sort of approach has also been used in earlier papers (e.g., among others, Hendricks and Kahn 1986).

Wage Settlement Regressions, 1978–2008

Notes: Estimator used denoted in each column. Dependent variable in the regressions is the mean annual wage increase for a contract. Standard errors presented in parentheses and clustered by jurisdiction. Wild bootstrap p values (using Webb's sampling weights) presented in brackets. COLA, cost-of-living adjustment; FE, fixed effects; IV, instrumental variable; OLS, ordinary least squares.

***, **, * denote statistically significant at the 1%, 5%, 10% level (based on Wild bootstrap p value).

Because I cluster my standard errors, I use the Kleibergen-Papp first-stage (rk Wald) F statistic to assess whether my instrument is weak (Kleibergen and Papp 2006). As can be seen in Table 2, the (rk Wald) F statistic (59.04) exceeds 10, so the instrument is not weak (Staiger and Stock 1997).

The IV estimate in column (3) indicates that expected inflation is associated with an increase in wage settlements. Based on the very conservative Wild bootstrap p values, expected inflation is statistically significant at the 10% level of significance. I should emphasize that my approach to inference, using the Wild bootstrap p values, is a much more conservative approach to inference than that in earlier papers, which used critical values from the normal distribution and did not cluster standard errors. Hence, it is not possible to directly compare statistical significance in my estimates with earlier papers, as statistical significance is greatly overstated in the earlier papers. 9 To better assess the effects of expected inflation (as well as the other continuous control variables, i.e., the unemployment rate and wage growth in a jurisdiction) on wage settlements, I computed elasticities. 10 The expected inflation rate has an elasticity of approximately 0.27, which suggests that a 10% increase in expected inflation would be associated with an increase of 2.7% in wage settlements. Earlier papers (e.g., Cousineau and Lacroix 1977; Riddell 1979; Auld et al. 1980; Card 1990) considered periods characterized by rising or persistently high inflation rates, but my study period also includes contracts from low inflation periods as well as a secular decline in inflation. The OLS and FE estimates in columns (1) and (2) suggest similar effects on wage settlements (elasticities of 0.260 and 0.225, respectively).

The unemployment rate, which captures tightness in the labor market, has a negative estimate in column (3), which is statistically significant at the 5% level of significance. This negative relationship between wage settlements and unemployment rates has also been observed in earlier papers (Riddell 1979; Auld et al. 1980) and is interpreted as consistent with a Phillips curve trade-off. The elasticity of wage settlements with respect to the unemployment rate is –0.35, so that a 10% increase in the unemployment rate would be associated with a 3.5% decline in wage settlements. Whereas the OLS estimate in column (1) is similar to the IV estimate, the FE estimate in column (2) is more than two times larger. The FE estimate suggests a much stronger trade-off between unemployment and wage settlements.

The growth in wages in the jurisdiction is associated with a somewhat smaller effect (an elasticity of about 0.15) on wage settlements relative to expected inflation and is statistically significant at the 5% level of significance based on the Wild bootstrap p value. The OLS and FE estimates (elasticities of 0.14 and 0.11) in columns (1) and (2) are not statistically different from zero.

The IV estimate for the COLA clause in column (3) is associated with a statistically significant (at the 1% level of significance) decline of 2.2 percentage points in wage settlements. This effect is considerably larger than those based on the OLS and FE estimates in columns (1) and (2). Cousineau and Lacroix (1977) also included an indicator for indexing provisions in their OLS analysis of public-sector contracts and they found that COLA clauses would be associated with a decrease in wage settlements. My OLS estimate fits into the lower end of the range of OLS estimates presented in Cousineau and Lacroix (1977) for the Canadian public sector. This result suggests there is a large bias in my OLS and FE estimates as well as the OLS estimates in the earlier literature, which would understate the effects of COLA clauses on wage settlements. The IV estimate indicates a strong trade-off between COLA clauses and wage settlements. In particular, bargaining pairs are willing to accept lower up-front nominal wage increases if they receive indexing provisions. The indexing provisions in the COLA clause would remove most (if not all) of the uncertainty attributable to future inflation. Consequently, workers would be willing to exchange smaller nominal predetermined wage increases for contingent wage increases. Hendricks and Kahn (1986) observed a similar trade-off in their wage regressions using US data and argued that it could reflect a compensating wage differential that risk-averse workers pay for protecting themselves against inflation.

The coefficient estimate on the indicator for the inflation-targeting policy by the Bank of Canada is quite large (1.9 percentage point decline in wage settlements, or a decrease of approximately 45% relative to the mean annual wage settlement). This estimate is statistically significant at the 5% level of significance. The OLS and FE estimates suggest a somewhat larger effect on wage settlements.

The control for legislated settlements, which includes back-to-work orders as well as more general legislation that limits settlement terms, is associated with a 1.6 percentage point decline in wage settlements. This estimate is statistically significant at the 5% level of significance (based on the very conservative Wild bootstrap p values). Since the mean annual increase in wage settlements is 4.1%, a legislated settlement can substantially reduce wage growth as the coefficient estimate suggests a 39% decrease (relative to the mean annual wage increase during my study period) in wage settlements. The OLS and FE estimates in columns (1) and (2) are similar to the IV estimate in column (3). As discussed earlier, the estimates for the effects of legislated settlements could have a negative bias if governments are likely to use these legislative restraints when their fiscal resources are under great strain. My estimates of the legislated settlement variable are similar to those in earlier papers (e.g., Currie and McConnell 1991; Campolieti et al. 2016), which may better control for the potential bias from the legislated settlements occurring during periods the fiscal resources of governments are strained. This finding suggests there is likely little bias in the legislated settlements estimates.

As discussed earlier, I do not control for the actual use of dispute resolution procedures to resolve bargaining impasses, but rather the type of dispute resolution procedure that is available to resolve a bargaining impasse if one were to occur. Interest arbitration is widely believed to increase wage settlements in the public sector (Olson 1980; Delaney 1983; Feuille and Delaney 1986; Currie and McConnell 1991). However, the indicator for the availability of compulsory interest arbitration as a dispute resolution procedure does not have a statistically significant estimate in Table 2. In addition, the estimate is quite small in magnitude, suggesting little if any effect on wage settlements relative to contracts for bargaining units that have the right to strike. In other words, I report no difference in wage settlements between contracts in the compulsory interest arbitration and the right-to-strike legal structures. My estimates for the availability of other types of dispute resolution methods also indicate no statistically significant differences relative to the right to strike. The OLS and FE estimates in columns (1) and (2) provide similar findings.

Table A.1, contains estimates from various other specifications that show my findings are robust. I also examine the robustness of my findings to an alternative measure of expected inflation and obtain estimates similar to those I present in Table 2 (see Table A.3). 11 I also find in an analysis of private-sector contracts (Table A.2), that wage setting in the private and public sector are influenced by many of the same factors. 12

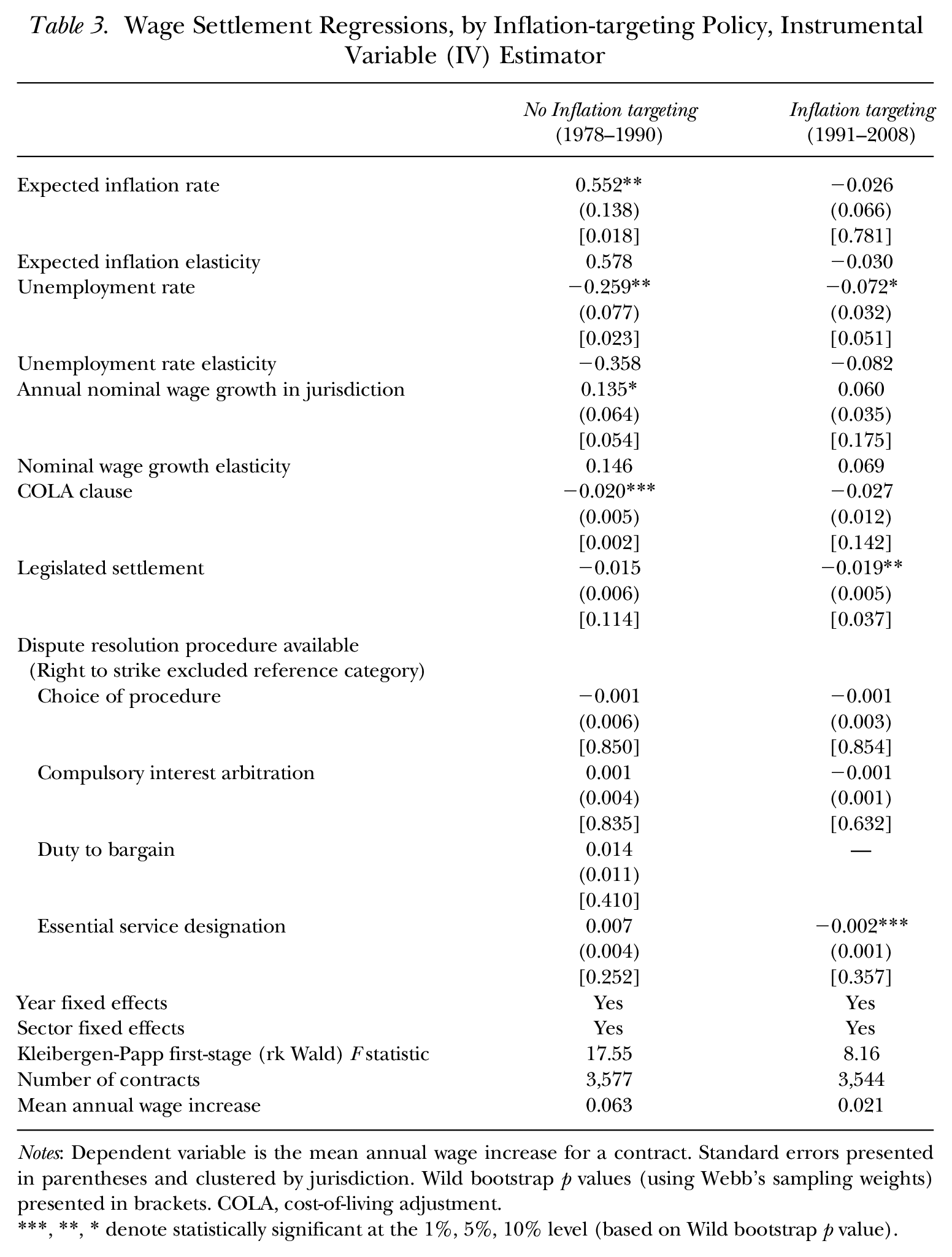

My study period spans four decades, some of which had much lower inflation than the other decades. I use 1991 as the demarcation point between the higher and lower inflation periods because the Bank of Canada adopted an inflation-targeting policy in February 1991, and present IV estimates of the wage settlement regressions by monetary policy regime in Table 3.

Wage Settlement Regressions, by Inflation-targeting Policy, Instrumental Variable (IV) Estimator

Notes: Dependent variable is the mean annual wage increase for a contract. Standard errors presented in parentheses and clustered by jurisdiction. Wild bootstrap p values (using Webb's sampling weights) presented in brackets. COLA, cost-of-living adjustment.

, **, * denote statistically significant at the 1%, 5%, 10% level (based on Wild bootstrap p value).

I report the differences in the estimates on the control variables across these two monetary policy regimes in Table 3. For the period before the Bank of Canada adopted an inflation target the elasticity of wage settlements with respect to expected inflation is 0.58, but this elasticity falls to –0.03 during the inflation-targeting period. The estimate for the expected inflation rate prior to the adoption of the inflation target is statistically significant at the 5% level of significance. This finding suggests that expected inflation plays a stronger role in wage setting prior to the inflation-targeting regime, which had relatively high and uncertain inflation. During the inflation-targeting regime, which had low and stable inflation rates, changes in expectations of future inflation are associated with little effect on wage settlements. While my wage settlement elasticities for expected inflation in Table 2 are smaller than those in the earlier literature, my expected inflation elasticity for the 1978–1990 period in Table 3 is similar to the elasticity estimates presented in Cousineau and Lacroix (1977), which range from approximately 0.56 to 0.84.

The estimates in Table 3 also indicate that the negative trade-off between wage settlements and unemployment rates is stronger during the period prior to inflation targeting. The unemployment rate estimate from the period prior to the Bank of Canada adopting an inflation target is statistically significant (at the 5% level of significance based on Wild bootstrap p values) and it implies an elasticity of –0.36. In contrast, the estimate from the period with an inflation target implies a much smaller elasticity (–0.08). While earlier papers have found a strong inverse relationship between wage settlements and labor market tightness (e.g., Riddell 1979; Auld et al. 1980), this relationship appears to be much weaker after the adoption of the inflation target.

I also find that nominal wage growth in the jurisdiction is associated with a large effect on wage settlements, which is statistically significant at the 10% level of significance, in the period prior to the adoption of the inflation-targeting policy by the Bank of Canada. In the period before inflation targets, the elasticity of wage settlements with respect to wage growth is 0.15. In contrast, during the period with inflation-targeting, nominal wage growth in the jurisdiction has an elasticity of approximately 0.07 and is not statistically significant.

The indicator for COLA clauses also has an estimate that is statistically significant and suggests a somewhat large effect on wage settlements in the period prior to inflation targeting. In particular, a COLA clause is associated with a 2 percentage point, or 32%, decline in the average annual increase in wage settlements (the mean annual wage increase in a contract was 6.3% in the period prior to the adoption of an inflation target). During the period with the inflation-targeting policy, the coefficient estimate for COLA clauses is not statistically significant. The estimate for the COLA clauses for the period with inflation targeting should be interpreted with caution, however, as the Kleibergen-Papp first-stage (rk Wald) F statistic is below 10. One interpretation of my findings in Table 3 is that bargaining units are willing to compromise on the size of the annual wage increase if they receive indexing provisions for their wages during periods with high and more variable inflation.

I find that the dispute resolution procedures available to settle bargaining impasses tend to have negligible effects on wage settlements and are not statistically different from zero. The estimate for the legislated settlements indicator is associated with a larger effect on wage settlements during the period with inflation targeting. This finding suggests possible heterogeneity in the effect of legislative restraints by inflation-targeting regime.

Contract Duration Regressions

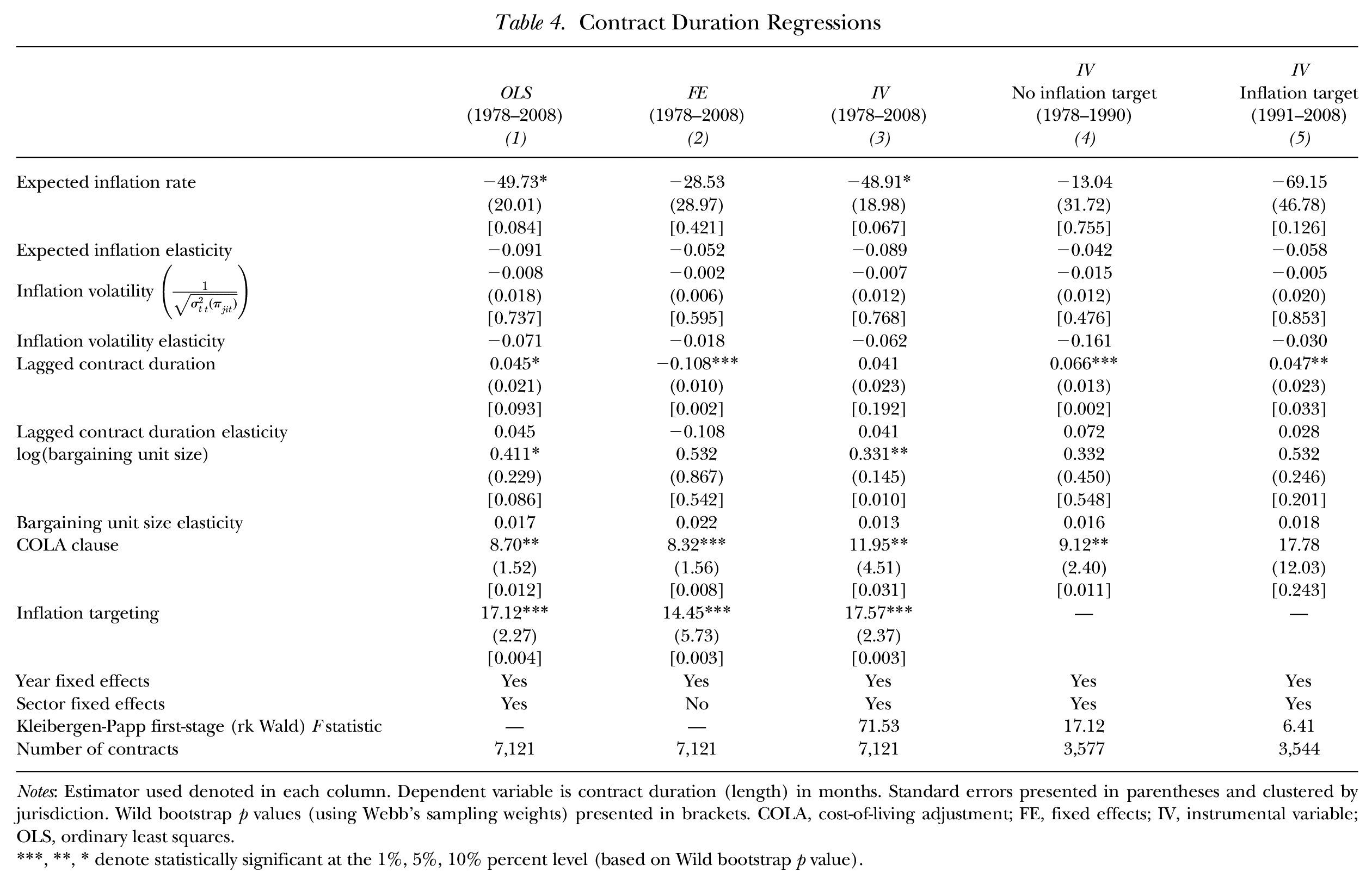

I present the estimates for the contract duration regressions in Table 4. Because the specifications I estimate for contract duration include an indicator for a COLA clause, the IV estimator (presented in column (3)) is my preferred estimator. As in the wage settlement regressions, however, I also present and discuss OLS and FE estimates. The Kleibergen-Papp first-stage (rk Wald) F statistic for my IV estimates (presented in Table 4) also exceeds the benchmark of 10 used in the literature (Staiger and Stock 1997), so my instrument for COLA status is not weak.

Contract Duration Regressions

Notes: Estimator used denoted in each column. Dependent variable is contract duration (length) in months. Standard errors presented in parentheses and clustered by jurisdiction. Wild bootstrap p values (using Webb's sampling weights) presented in brackets. COLA, cost-of-living adjustment; FE, fixed effects; IV, instrumental variable; OLS, ordinary least squares.

, **, * denote statistically significant at the 1%, 5%, 10% percent level (based on Wild bootstrap p value).

In column (3) of Table 4, which presents the IV estimates, increases in expected inflation are associated with a decrease in contract duration (at the 10% level of significance), but the effect is quite small. In particular, the elasticity for contract duration with respect to expected inflation is –0.09, which suggests that a 10% increase in inflation expectations is associated with a 0.9% decrease in contract duration (approximately 0.2 months). Inflation volatility, is not statistically significant, and the elasticity also indicates a negligible effect on contract duration. The OLS estimates in column (1) and FE estimates in column (2) for expected inflation and inflation volatility are largely similar to the IV estimates in column (3). My estimates for expected inflation and inflation volatility, which capture the effects of inflation uncertainty on contract duration, differ from earlier studies that have found inflation uncertainty has a large effect on contract duration (Christofedes and Wilton 1983; Murphy 1992; Rich and Tracy 2004). This outcome could reflect some structural change in contracting behavior, as inflation fell and became less uncertain during my study period.

As did Christofedes and Wilton (1983), I find the lag of contract duration is associated with an increase in current contract duration, but only the OLS and FE estimates are statistically significant. Christofedes and Wilton (1983) posited a partial adjustment mechanism allowed bargaining pairs to try to obtain the optimal or desired contract length over time, by gradually eliminating the difference between desired and actual contract lengths. The elasticities I compute suggest that these sorts of effects would be negligible in my sample.

Earlier papers (e.g., Christofedes and Wilton 1983; Rich and Tracy 2004) that have studied contract duration in the private sector use bargaining unit size to capture economies of scale in contract negotiations, in which larger bargaining units have lower contracting costs. While the size of the bargaining unit does have statistically significant IV estimate in Table 4, the elasticity suggests negligible effects on public-sector contract duration. This result suggests that scale economies in contracting costs would have little effect on contract duration in the public sector. Perhaps this reflects that the bargaining units in my sample are quite large (500 or more members) and many are affiliated with the largest public-sector unions in Canada (e.g., among others, the Canadian Union of Public Employees and the Public Service Alliance of Canada, which have also concentrated union membership over time (Campolieti 2020)). By contrast, many of the bargaining units in the private sector considered in earlier work are smaller and tend to have a much more diverse set of union affiliations. The elasticities for the OLS and FE estimates are slightly larger (0.017 and 0.022, respectively) than the elasticity for the IV estimate.

The IV estimate for COLA clauses in column (3) of Table 4 is associated with a somewhat large (12-month) increase in contract duration. The OLS and FE estimates in the first two columns are about 33% smaller, statistically significant increases of 8.7 and 8.3 months in contract duration. This result suggests a downward bias in the OLS and FE estimates of the effects of COLA clauses on contract duration. My estimate suggests that reducing the effects of unexpected inflation with indexing provisions would be associated with an increase in contract duration. This estimate is consistent with earlier empirical work (Christofedes and Wilton 1983; Murphy 1992; Rich and Tracy 2004) as well as theoretical work (Gray 1978). As is the case with wage settlements, bargaining pairs may be more willing to trade off a longer contract when they have more protection from unexpected increases in inflation. Likewise, the indicator for the inflation-targeting regime, with lower and less variable inflation rates, would be associated with an increase of approximately 17.6 months in contract duration (as shown in column (3)). This estimate suggests a more stable and lower inflation environment would be associated with longer contracts as bargaining pairs may perceive less uncertainty about future inflation and its costs. The OLS and FE estimates for the inflation-targeting regime indicator are somewhat smaller (17.1 and 14.5 months), but still suggest sizeable increases in the length of contracts.

I also present some estimates for contract duration by inflation-targeting regime in columns (4) and (5) of Table 4 based on the preferred IV estimator. While some large differences in the IV coefficient estimates on the control variables are evident in columns (4) and (5), the elasticities suggest negligible effects on contract duration that do not differ across monetary policy regimes. Of note, the indicators for COLA clauses have estimates that differ a great deal across the two monetary policy regimes. However, the Kleibergen-Papp first-stage (rk Wald) F statistic for the specification using data from the inflation-targeting regime is below 10, which indicates that the estimate from the inflation-targeting regime should be interpreted with caution because the instrument is weak.

The Online Appendix contains an analysis of private-sector contract duration. Comparing the private- and public-sector regression results suggests that uncertainty and contracting costs have similar effects on contract duration in both sectors, that is, they would be associated with negligible effects on contract duration, and they would not differ by monetary policy regime.

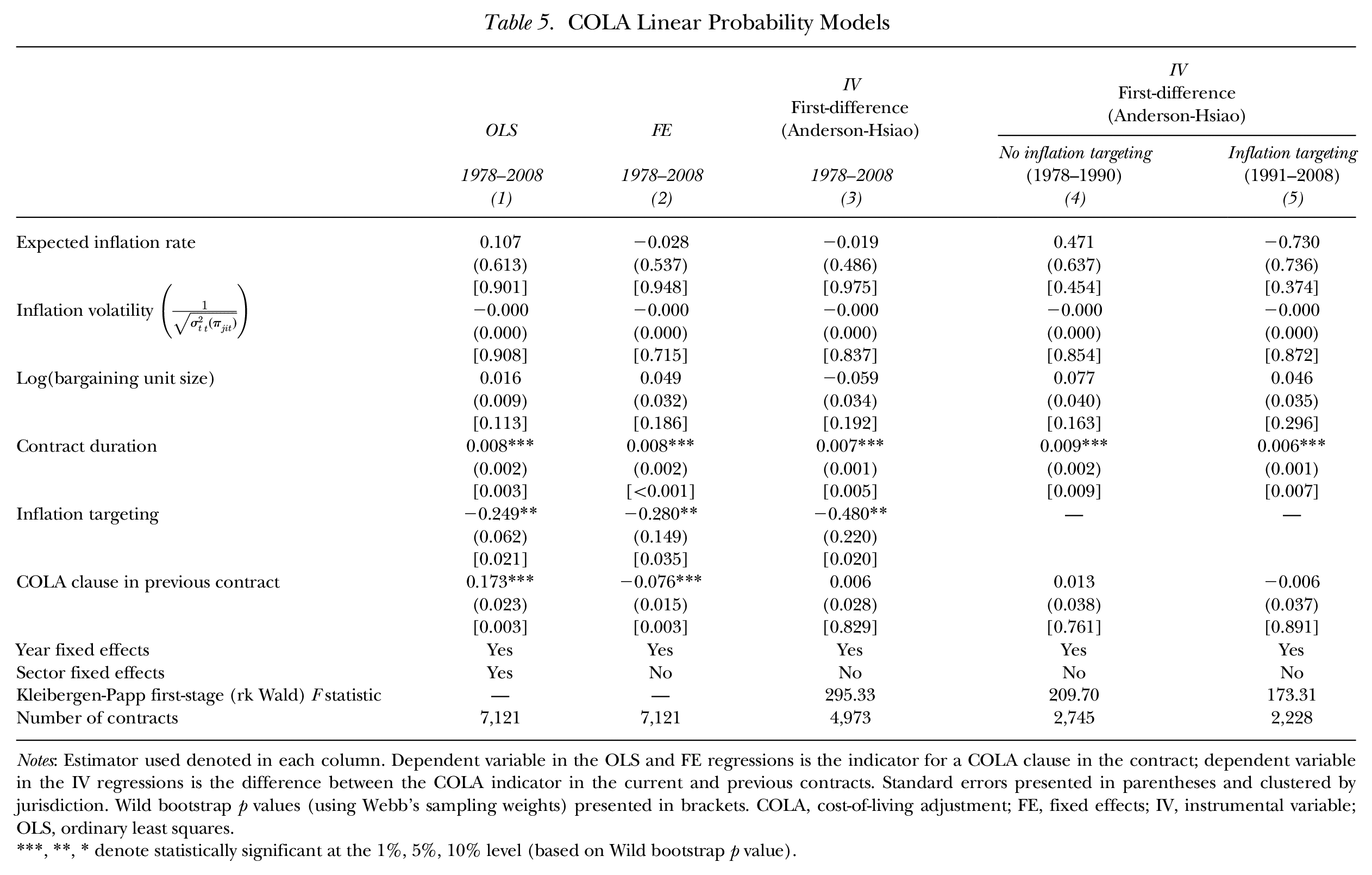

COLA Clause Linear Probability Models

I also provide some estimates for the incidence of COLA clauses in the public-sector contracts in Table 5. I estimate these regressions as linear probability models. As with the wage settlements and contract duration regressions, I present some OLS and FE estimates but the IV estimates are my preferred estimates. However, my IV estimates for the linear probability models are for a first-differenced model as discussed in Anderson and Hsiao (1981) and used in various papers (e.g., among others, Schnell and Gramm 1987; Campolieti and Riddell 2019).

COLA Linear Probability Models

Notes: Estimator used denoted in each column. Dependent variable in the OLS and FE regressions is the indicator for a COLA clause in the contract; dependent variable in the IV regressions is the difference between the COLA indicator in the current and previous contracts. Standard errors presented in parentheses and clustered by jurisdiction. Wild bootstrap p values (using Webb's sampling weights) presented in brackets. COLA, cost-of-living adjustment; FE, fixed effects; IV, instrumental variable; OLS, ordinary least squares.

, **, * denote statistically significant at the 1%, 5%, 10% level (based on Wild bootstrap p value).

The OLS and FE estimates, which are not first-differenced, are presented in columns (1) and (2) of Table 5. The OLS and FE estimates indicate that expected inflation, inflation volatility, and bargaining unit size are not associated with a statistically significant effect on the likelihood of a COLA clause. However, contract duration is associated with a statistically significant increase in the incidence of COLA clauses. If longer contracts mean that workers face more uncertainty about future inflation and the greater erosion of their wages, then it seems reasonable to expect that risk-averse workers would be more likely to obtain COLA clauses that would protect their purchasing power. My estimates suggest that a 12 month increase in contract duration would be associated with a 9.6 percentage point increase (12 months multiplied by the point estimate of 0.008) in the likelihood the contract contains a COLA clause. The OLS and FE estimates for the lagged COLA clause indicator differ in sign. The FE estimate suggests that a COLA clause in the previous contract would be associated with a decrease in the incidence of COLA clauses, whereas the OLS estimate suggests that a COLA clause in the previous contract would be associated with an increase in the incidence of COLA clauses. It seems more likely to expect that the presence of COLA clauses in the previous contract would increase the likelihood of these sorts of clauses in the current contract, as the previous agreement on these provisions could serve as a template for future indexing provisions. The Kleibergen-Papp first-stage (rk Wald) F statistics from the IV regressions for wage settlements and contract duration suggest this assumption is plausible. The indicator variable capturing the Bank of Canada’s inflation target is associated with a decline in the incidence of COLA clauses. As discussed earlier, during the period with an inflation-targeting monetary policy, inflation was much lower and less variable and COLA clauses have become less prevalent (Labour Program 2015). Consequently, COLA provisions might not be as necessary as there is less uncertainty about future inflation.

The preferred Anderson-Hsiao (first-differenced) IV estimates are presented in column (3) of Table 5. Because the IV estimates are first-differenced they capture the change in whether the current and previous contract include COLA clauses, unlike the estimates in columns (1) and (2), which capture whether the current contract includes a COLA clause. The Anderson-Hsiao IV estimates in column (3) for expected inflation, inflation volatility, and bargaining unit size are imprecisely estimated, as are their OLS and FE counterparts in the first two columns of Table 5. Hendricks and Kahn (1983) found that bargaining unit size increased the likelihood of a COLA clause, but they did not present their probit estimates as marginal effects so it is difficult to determine the size of this effect. The IV estimate for the inflation-targeting variable is negative and statistically significant at conventional levels of significance. Hendricks and Kahn (1983) used a probit model to estimate the use of COLA clauses and found increases in expected inflation were associated with an increased prevalence of COLA clauses. My estimate for the inflation-targeting indicator suggests that stable inflation periods are associated with a decline in the use of COLA clauses, which is consistent with the findings in Hendricks and Kahn (1983). The IV estimate for contract duration is similar in magnitude to the OLS and FE estimates as well as statistically significant at the 1% level of significance. However, the IV estimate for the lagged COLA clause is 0.006 and has a p value of 0.83, which suggests that the presence of COLA clauses in previous contracts has little effect on the use of COLA clauses. The Kleibergen-Papp first-stage (rk Wald) F statistic for the IV regression (295.33) is substantially above the threshold of 10.

Finally, I also estimated the COLA linear probability model by inflation-targeting regime and observe little difference in the estimates and findings (see columns (4) and (5) of Table 5).

Concluding Remarks

I study wage settlements, contract duration, and the incidence of COLA clauses in the Canadian public-sector contracts during a 30-year period, which has a great deal of variability in inflation and economic conditions as well as government policy toward collective bargaining.

I find that expectations of future inflation are associated with an increase in wage settlements. I also find unemployment rates are associated with a statistically significant decline in wage settlements, which suggests that wage settlements are inversely related to labor market tightness. I also find that wage growth in a jurisdiction is associated with an increase in wage settlements. When I consider contracts from the private sector I obtain similar findings, which suggests that inflation expectations and economic conditions play a similar role in wage-setting behavior in the private and public sector. I also find COLA clauses can have a sizeable effect on public-sector wage settlements, which suggests that bargaining teams may be willing to trade off smaller annual wage increases for more indexing on future inflation. When I split my data by monetary policy regime, I find that inflation expectations and wage growth in a jurisdiction as well as labor market tightness have a much more substantial effect on wage settlements during the period before the Bank of Canada adopted its inflation-targeting policy. I also consider the effects of the dispute resolution procedures available to resolve a bargaining impasse and find no statistically significant differences between these methods on wage settlements relative to the right-to-strike legal structure. However, I find that government-restraint legislation is associated with a decline of approximately 1.6 percentage points in annual wage increases, or 39%, relative to the mean wage settlement during my study period.

My contract duration regressions include measures of uncertainty and contracting costs, which have a negligible effect on contract duration. The contract duration elasticities for these measures of uncertainty and contracting costs also do not appear to vary with monetary policy regime. I do find, however, that COLA clauses and the inflation-targeting indicator are associated with substantial increases in contract duration. These findings suggest that the indexing provisions in COLA clauses and having an environment with lower and more stable inflation are associated with reductions in uncertainty about future inflation and contribute to an increase in the length of contracts. Likewise, the linear probability models I estimate for the use of COLA clauses suggest that longer contracts would be associated with an increase in the use of COLA clauses and that a more stable inflation environment would be associated with a decrease in the use of COLA clauses.

My findings offer a few implications for research and collective bargaining. First, a return to higher and more uncertain inflation could alter how bargaining pairs approach negotiations. In particular, expectations of future inflation, labor market tightness, and wage growth could have a much greater influence on wage demands when inflation rates are higher and more variable than when they are lower and less variable. Second, my results point to the role COLA clauses can play in both wage settlements and contract duration. In particular, bargaining pairs may be willing to trade off smaller base wage increases and longer contracts for these indexing provisions. In addition, the use of COLA clauses can increase as contract length increases. While the frequency of COLA clauses in contracts has been in decline during the past few decades, the return to a higher inflation environment suggests they could be of greater importance in these more uncertain times.

Supplemental Material

sj-pdf-1-ilr-10.1177_00197939251323234 – Supplemental material for Collective Bargaining and Public-Sector Wage Setting

Supplemental material, sj-pdf-1-ilr-10.1177_00197939251323234 for Collective Bargaining and Public-Sector Wage Setting by Michele Campolieti in ILR Review

Footnotes

This research did not receive any specific grant/financial support from funding agencies in the public, commercial, or not-for-profit sectors.

For general questions as well as for information regarding the data and/or computer programs, please contact the author at

2

3

In the essential-service designation some workers in a bargaining unit are designated as essential and do not have the right to strike.

4

During the years of the 6-and-5 program the province of New Brunswick froze the wages of public-sector workers.

6

More specifically, I instrument

7

Provincial crown corporations can include liquor store workers, and federal crown corporations can include postal workers at Canada Post.

8

These p values are obtained with the boottest ado file (Roodman, Nielsen, MacKinnon, and Webb 2019).

9

Many of the estimates in my tables would be statistically significant, as are those in earlier papers, if I computed t statistics with the clustered standard errors and used the t distribution with 10 degrees of freedom for the critical values.

10

The elasticities for the wage settlement regressions are computed as

12

In preliminary work, I also considered the effects of unanticipated past inflation on wage settlements and found that it had a negligible effect on wage settlements. Including this additional inflation measure did not alter the results for the other controls.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.