Abstract

This study investigates the influence of macroeconomic variables on the volatility of Islamic stock indices in India (Nifty 50 Shariah) and China (FTSE Shariah China) using the generalised autoregressive conditional heteroskedasticity–mixed data sampling (GARCH–MIDAS) model. We analyse monthly data from July 2010 to December 2023, focusing on the impact of inflation (consumer price index [CPI]) and short-term interest rates (91-day T-bill rate for India and the interbank rate for China) on the long-term volatility component. Utilising the GARCH–MIDAS model, this research seeks to identify how macroeconomic variables affect the instability of Islamic stock indices within India’s Nifty 50 Shariah and China’s FTSE Shariah China. We examine monthly data between July 2010 and December 2023, focusing on the effect of inflation (CPI) and short-term interest rates (91-day T-bill rate for India and interbank rate for China) on long-run volatility component. We have found out that there is a strong positive correlation between short-term interest rates and long-term volatility in both markets, which means that perhaps Muslim investors are using conventional interest rates to determine their Islamic investments. But the effect of CPI differs between them, as it has an insignificant effect in India and a marginally significant but negative impact in China. This difference shows how essential it is to look at national factors when studying the volatility of Islamic stock exchanges. It is noted here that in both locations there is evidence of the leverage effect, so that bad news greatly influences volatility compared to good news. Also, we did not find any regular pattern when comparing Islamic stock returns and traditional interest rates while conducting a benchmark study. The above findings have important implications for those who invest or manage funds or make policies in these new economies—showing them how they should adapt their investment and risk management plans to specific situations.

Introduction

Volatility in financial markets is a critical concern for investors, policymakers and regulators, particularly in rapidly developing economies like India and China. Fluctuations in asset prices can impact investment decisions, risk management strategies and overall economic stability. As these two nations emerge as global economic powerhouses, understanding the dynamics of their financial markets becomes increasingly important. Within this context, Islamic finance has witnessed significant growth in both India and China, presenting a unique and ethically driven investment alternative. In India, the Islamic finance sector has grown at an estimated annual rate of 18% over the last decade, according to a report by the PHD Chamber of Commerce and Industry (2023). While in China, the volume of Islamic finance transactions doubled between the period 2019 and 2023 with a growth rate of 23% over the past decade, according to a recent report by the State Council Information Office of the People’s Republic of China, 2024.

This growth necessitates a deeper understanding of the factors that drive volatility in Islamic stock markets and how they may differ from conventional counterparts. This study aims to bridge this knowledge gap by analysing the impact of key macroeconomic variables on the volatility of Islamic stock indices in India and China. This study specifically examines the impact of two pivotal macroeconomic variables: inflation and short-term interest rates. Inflation, as measured by the consumer price index (CPI), reflects the general price level in an economy and can influence investor sentiment and corporate profitability. High inflation can erode the real value of investments, leading to increased market volatility (Fama, 1981). Short-term interest rates, reflecting the cost of borrowing, can impact investment decisions and corporate financing costs. Changes in interest rates can alter discount rates used in asset valuation, thereby influencing stock market volatility (Campbell, 1987). While numerous factors can affect market volatility, we focus on inflation and interest rates due to their fundamental roles in macroeconomic policy and their established influence on financial markets, particularly in emerging economies (Alam et al., 2009; Alexakis & Apergis, 1996).

Specifically, this study aims to determine whether inflation and short-term interest rates significantly influence the long-term volatility of Islamic stock indices in India and China, and to investigate any country-specific differences in these relationships. Furthermore, we examine the presence of the leverage effect, where negative news may have a disproportionate impact on volatility, and explore whether the volatility of Islamic stock indices in these markets can be benchmarked against conventional interest rate benchmarks.

By examining the impact of inflation and short-term interest rates on the volatility of Islamic stock indices in India and China, this study contributes to the growing body of knowledge on Islamic finance in emerging markets. Specifically, it provides empirical evidence on whether the macroeconomic drivers of volatility in Islamic stock markets differ from those in conventional markets. The comparative analysis of India and China, two of the world’s largest emerging economies, offers valuable insights into the country-specific nuances of Islamic finance. Furthermore, the application of the GARCH–MIDAS model, which effectively captures both short-term and long-term volatility dynamics, enhances the methodological rigour of this investigation. The findings have implications for investors seeking portfolio diversification and risk management strategies, as well as for policymakers aiming to foster financial stability in these rapidly growing economies. Our analysis reveals that short-term interest rates are a significant driver of long-term volatility in both markets, while the impact of inflation varies, being insignificant in India and marginally negative in China. We also find evidence of the leverage effect, and our benchmarking analysis suggests that Islamic stock volatility in these countries is not directly linked to conventional interest rates.

Literature Review

Researchers have been fascinated by how stock prices, inflation and interest rates interact with each other for decades. The complex relationships among these three elements have been the subject of much scholarly literature, dating back to the work of Fama (1981), who claimed that inflation contributes negatively to stock market returns, explaining that increasing inflation reduces profits made by companies, leading to a decrease in gains realised by investors. In contrast, though, he maintained that only over extended periods of time would changes in basic factors help reduce this negative effect.

On this topic, Schwert (1989) went further, showing how general macroeconomic conditions relate to stock market fluctuations. He asserted that variations in price levels and cost of borrowing, among other things, affect company earnings predictions as well as the rates used to discount them. That is why it is said that unpredictability in share values continues to exist.

Stock market instability is significantly influenced by financial leverage and interest rates. According to Campbell (1987), there exists a negative correlation between the market price of a company’s share and the prevailing interest rates. More so, it has been found out by him that an increase in capital cost, which in turn translates to increased borrowing rates, will result in a decline in firms’ worth, thus increasing market price fluctuations.

Impact of Macroeconomic Variables in Emerging Markets

In emerging economies, macroeconomic variables’ specific role on stock market instability has become the subject of a growing body of research. Inflation uncertainty has been shown by Alexakis and Apergis (1996) as negatively correlated with stock prices in some of the emerging economies, emphasising their inclination to respond to inflationary movements. This was also recast by Alam et al. (2009), who found that emerging economies experiencing rising inflation tend to have higher discount rates and less investment, hence increased stock market volatility. Bhuiyan and Chowdhury (2020) similarly found that macroeconomic factors impact the volatility of the Indian stock market.

GARCH–MIDAS Models and Macroeconomic Volatility

Conventional GARCH models are suitable for dealing with short-term volatility clustering; however, they usually fail when low-frequency macroeconomic variables are incorporated. To solve this problem, Ghysels et al. (2006) proposed the mixed data sampling (MIDAS) model, which allows for the integration of data with different frequencies. A hybrid approach combining the strengths of both models, the GARCH–MIDAS model has become popular in recent times (Conrad & Loch, 2015; Engle et al., 2013; Fang et al., 2020). Yarovaya and Lau (2016) also emphasise the importance of macroeconomic factors when analysing the volatility of stock markets in G7 countries.

Various studies have used GARCH–MIDAS to explore how macroeconomic variables affect fluctuations in share prices. Conrad and Loch (2015) observed that long-term stock market swings can be well anticipated by such factors as unemployment rate, profits made by firms and term spreads. According to the findings of Engle et al. (2013), there is a substantial connection between manufacturing output in the economy and the changes in share prices, especially over an extended period.

Islamic Finance and Market Volatility

The Islamic stock market research, although it is expanding, continues to be quite constrained. Numerous studies have examined several parts of Islamic finance, such as risk-return features (Hussein & Omran, 2005) and investor psychosocial effects (Danila et al., 2021). In contrast, there are few studies examining the macroeconomic forces that cause volatility in these markets, especially in developing nations like India and China.

Hypotheses

Building upon the existing literature, this study examines the following hypotheses:

The influence exerted is as a result of inflation (CPI), which will bear greatly on the long-term volatility in Islamic stock indices found in India and China. This proposition concurs with the Irving Fisher hypothesis that asserts that actual asset earnings adapt to expected inflation, thereby rising nominal returns and enhancing volatility in times of inflation (Joubert, 2021). In India as well as in China, short-term interest rates will have a negative and significant effect on the long-term volatility of Islamic stock indices. The idea behind this hypothesis is that an increase in interest rates raises the cost of capital, which lowers firm valuations and thereby leads to higher stock market volatility. The leverage effect is anticipated to be a characteristic of the Indian and Chinese Islamic stock markets. According to this hypothesis, future volatility is expected to be more sensitive to negative returns than to positive returns, which echoes the fact that investors tend to react asymmetrically to news.

Hypothesis Development

Based on the existing literature and theoretical framework, we develop the following hypotheses regarding the impact of macroeconomic variables on the volatility of Islamic stock indices in India and China.

H1: Inflation (CPI) will have a positive and significant impact on the long-term volatility of Islamic stock indices in India and China.

This hypothesis is rooted in the Irving Fisher hypothesis, which posits that real asset returns should adjust to anticipated inflation. In periods of rising inflation, nominal stock returns are expected to increase to compensate investors for the loss of purchasing power. This adjustment process can lead to higher volatility in stock prices (Joubert, 2021). Furthermore, inflation uncertainty can negatively affect corporate profitability and investor sentiment, further contributing to market volatility (Fama, 1981).

H2: Short-term interest rates will have a negative and significant impact on the long-term volatility of Islamic stock indices in India and China.

This hypothesis is based on the fundamental relationship between interest rates and asset valuation. Higher interest rates increase the cost of capital for companies, potentially reducing their profitability and investment. This, in turn, can lead to lower stock valuations and increased market volatility (Campbell, 1987). Changes in short-term interest rates can also affect investor expectations and discount rates, further impacting stock market volatility.

H3: The leverage effect will be present in both the Indian and Chinese Islamic stock markets.

The leverage effect, first proposed by Black (1976), suggests that negative shocks to stock returns (bad news) tend to increase volatility more than positive shocks (good news) of the same magnitude. This asymmetric response is often attributed to increased financial leverage and heightened uncertainty during periods of market decline. We hypothesise that this effect will also be present in the Islamic stock markets of India and China.

Methods

This research article examines how macroeconomic factors influence the fluctuations in Islamic stock market indices in India and China using GARCH–MIDAS model. This technique was developed by Engle et al. (2013), which allows adding information with different frequencies to explore the effect of slow-moving economic indicators on fast-moving share prices. The GARCH–MIDAS model is particularly well-suited for this analysis because it allows us to directly incorporate low-frequency macroeconomic variables (like monthly CPI and interest rates) into the model for long-term volatility, while still capturing the high-frequency dynamics of daily stock returns with the GARCH component. This separation of short-term and long-term volatility components is crucial for understanding the specific influence of macroeconomic factors, which may not be evident in traditional GARCH models that only use high-frequency data (Engle et al., 2013).

Data

Data Description and Sources.

Data Description and Sources.

GARCH–MIDAS Model Specification

The GARCH–MIDAS model decomposes volatility into two components: a short-term component captured by a GARCH(1,1) process and a long-term component driven by macroeconomic variables.

Short-term Component

The short-term component is modelled using a GARCH(1,1) process with an asymmetric term to capture the leverage effect:

where:

gi,t represents the conditional variance on day i in month t. ri,t is the daily stock return on day i in month t. µ is the mean daily stock return. α, β and γ are the ARCH, GARCH and asymmetry (leverage effect) parameters, respectively.

Long-term Component

The long-term component, denoted as τt, is modelled using the MIDAS specification:

where:

m is a constant term. θ is a vector of coefficients that measure the impact of each macroeconomic variable on long-term volatility. ωk(w1, w2) are the MIDAS weights that determine how much the past macroeconomic values influence present volatility. We make use of beta weights with a diminishing character, such that recent observations carry more weight. The way to calculate Beta weights is as follows:

where:

K is the maximum lag considered for the macroeconomic variables. w1 and w2 are parameters that govern the shape of the weights. Xj,t–k represents the macroeconomic variables (CPI and interest rate) at lag k.

Estimation and Diagnostics

The GARCH–MIDAS model is estimated using maximum likelihood estimation. To ensure the model’s validity and reliability, we conduct a series of diagnostic tests:

Residual heteroskedasticity: We analyse whether there is any remaining heteroskedasticity in the standardised residuals using the ARCH lagrange multiplier (LM) test. If it is absent, that implies the model can adequately explain volatility dynamics. Model fit: We evaluate the model fit by visually inspecting the standardised residual plots and analysing the significance of the estimated parameters.

Benchmarking Analysis

In order to know if Islamic stock markets in India and China can be compared to conventional interest rates, we compare the returns of Islamic indices with their respective benchmark rates (repo rate for India and lending rate for China). A trend and correlation analysis is visually conducted to identify possible benchmarking relationships.

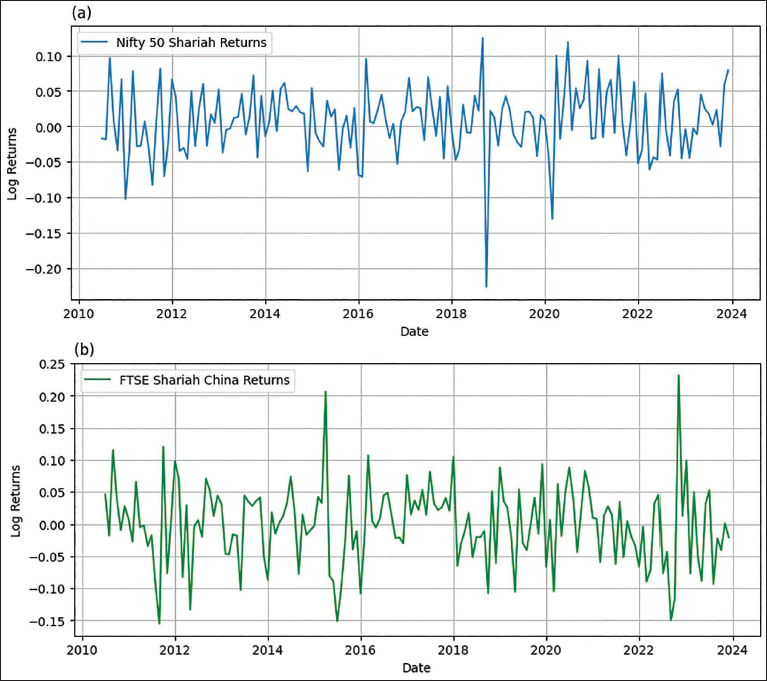

Figure 1 illustrates the monthly log returns of the Nifty 50 Shariah Index for India and the FTSE Shariah China Index, highlighting periods of heightened volatility. This is the report for our analysis; therefore, we will look at how inflation and short-term interest rates affect variations in Islamic stock indices in India and China. Additionally, we examine whether there exists a leverage effect and investigate if it may be possible to use conventional interest rate benchmarks as a basis for measuring volatility within the Islamic stock market.

JII Returns. (a) Monthly Log Returns of Nifty 50 Shariah (India). (b) Monthly Log Returns of FTSE Shariah China.

JII Returns. (a) Monthly Log Returns of Nifty 50 Shariah (India). (b) Monthly Log Returns of FTSE Shariah China.

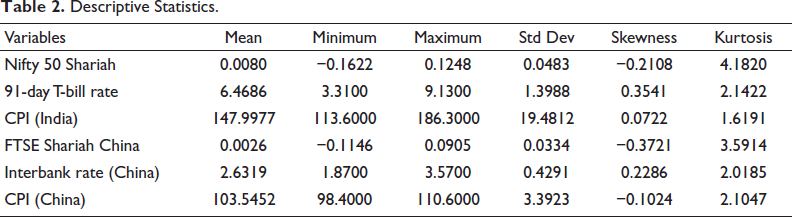

Descriptive Statistics

Descriptive Statistics.

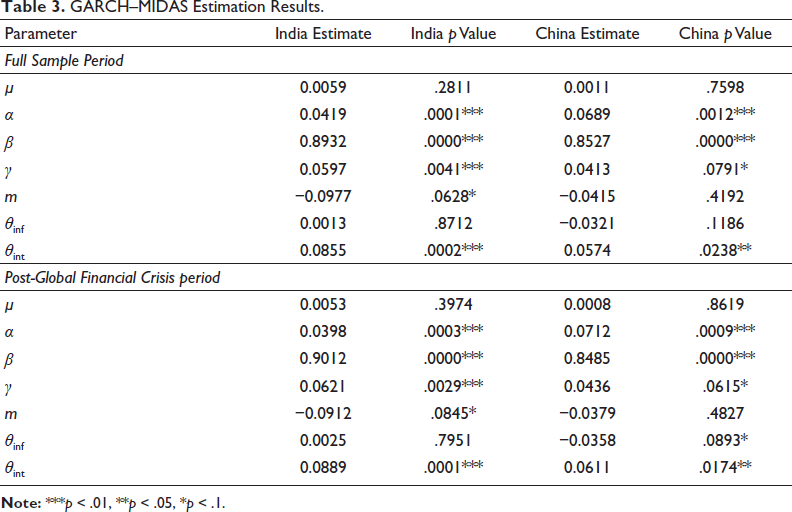

Macroeconomics Variables on Islamic Indices Returns

GARCH–MIDAS Estimation Results.

Leverage Effect

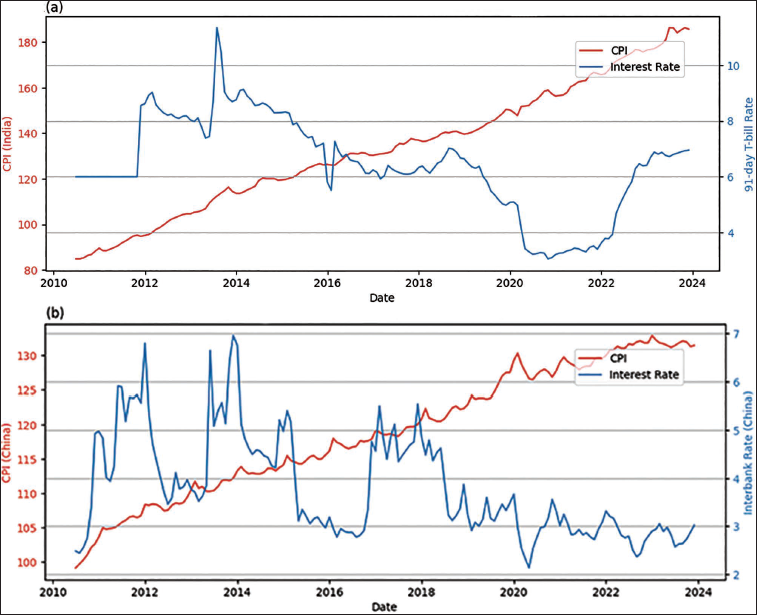

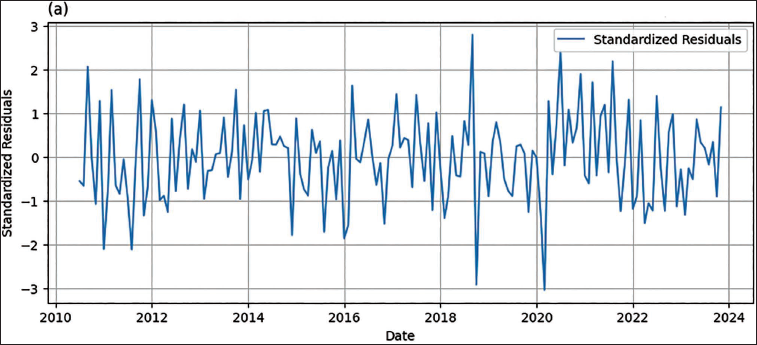

The big and good coefficients for both India and China in all the sample periods (see Table 3) indicate that there are strong signs of leverage in both Islamic stock markets. This is in line with H3, which states that future volatility is affected more by negative news than by positive news. For example, in the Indian market, a 1% decline in Nifty 50 Shariah Index brings about higher future volatility than a 1% rise does. Such asymmetric reactions could be due to investor behaviour where negative news results in more uncertainty and risk aversion (Black, 1976). Figure 2 depicts the evolution of inflation (CPI) and short-term interest rates in India and China over the sample period. Figure 3 shows the standardised residuals from the GARCH–MIDAS model, indicating the adequacy of the model in capturing volatility dynamics.

(a) Inflation (Consumer Price Index [CPI]) and Interest Rate (India). (b) Inflation (Consumer Price Index [CPI]) and Interest Rate (China).

Standardised Residual Plots. Standardised Residuals from GARCH–MIDAS Model (India).

Interest Rate Impact

The results consistently indicate that short-term interest rates form a vital predictor of long-term volatility in both Indian and Chinese Islamic stock markets. The positive and statistically significant θint coefficients support this argument as they imply that whenever there is an increase in short-term interest rates, there is an accompanying rise in long-term volatility. Nonetheless, these findings contradict H2, which suggested a negative relation. This positive relationship, that has come to us as a shock, can be explained possibly by the fact that Muslim investors in these markets rely on traditional short-term interest rates as the basis of their investments when it comes to Shariah-compliant tools (Majid & Yusof, 2009). Due to such rising rates, among other factors such as opportunity costs, therefore, they may require more from Islamic investments, hence increasing their volatility through the engaged trading activities, which in turn will lead to price fluctuations.

Inflation Impact

There exists a mixed picture when it comes to the effect of inflation (CPI) on long-term volatility. In the Indian case, there is no statistically significant effect of CPI, either in full sample or post-crisis periods. These findings contradict H1, which expected a positive correlation. It implies that CPI may not necessarily be a pivotal force behind long-term volatility in the Indian Islamic stock exchange.

Interestingly, in the Chinese market, CPI shows a slightly significant negative link with long-term volatility in the period after crisis. This result contradicts both H1 as well as the findings for the Indian market. The implication may be due to an active role played by the Chinese government over inflation management. According to Yiu et al. (2012), effective control measures may reduce stock market volatility (2012).

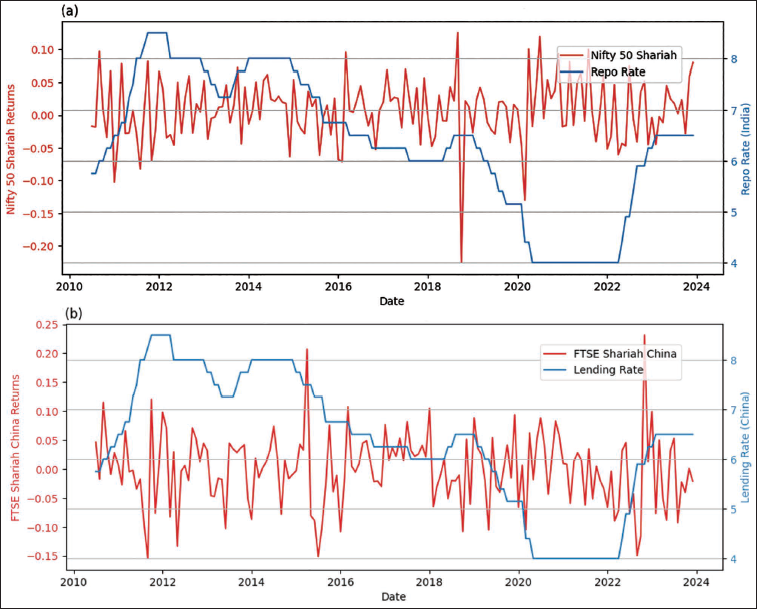

Benchmarking Analysis

Our benchmarking analysis, comparing the returns of Islamic indices with conventional interest rate benchmarks, did not reveal a clear and consistent relationship.

To examine whether Islamic stock market returns in India and China are benchmarked against conventional interest rates, we visually compare their trends over the sample period. Benchmarking, in this context, would imply a consistent relationship or co-movement between the Islamic index returns and the conventional interest rates (e.g. repo rate for India and lending rate for China).

Therefore, one can say that the level of Islamic stocks in India and China might not be directly related to traditional interest rates, unlike the case with Indonesia’s Muslim stock market (Danila, 2023). Global market trends, changes in the price of crude oil, as well as investors’ mood, may influence the price variability in these marketplaces. Figure 4 presents the benchmarking analysis comparing Islamic stock index returns with conventional interest rate benchmarks for India and China.

(a) Benchmarking Analysis (India). (b) Benchmarking Analysis (China).

Discussion

Our analysis indicates that there are many captivating discoveries concerning the macroeconomic engines of Islamic stock market volatility in India and China. The existence of the leverage effect indicates asymmetrical news effect on the volatility, while the negative startling relationship between interest rates and volatility could mean that Muslim investors tend to benchmark their investment decisions. On the other hand, these different effects of CPI stress on the need to take into account variables unique to each country, like governmental regulations and market processes.

Our investigation examines the elements that cause fluctuations in the Islamic stock markets of India and China by using the GARCH–MIDAS model, as it examines how short-term interest rates and inflation (CPI) affect long-term volatility. The outcomes from this research provide important insights for investors, portfolio managers and decision-makers.

News negotiations involve an overarching leverage effect across both markets. This underscores the Josephs’ improbability theory, meaning that issues like risk should be taken care of by their governments. A notable fact is that our findings are contrary to the general assumption we have held for so long that stock market levels fall when interest rates rise. Long-term volatility in India and China has a positive correlation with long-term interest rates, which gives the impression that Muslim investors could be using the standard rate of return on investments as a yardstick for Shariah-compliant products. More research must be done on this possible virtuous circle between conventional finance and Islamic banking systems within these nations.

However, the relation between CPI and long-term volatility varies in different areas. The Indian market does not feel any impact, while a negative influence is marginally evident on the Chinese market, and it might be due to the success that China has achieved in controlling inflation. Therefore, these findings highlight that Islamic stock market volatility should be analysed with regard to particular countries’ contexts.

According to our benchmark analysis comparing Islamic indices with conventional interest rate benchmarks, there was no persistent association observed, indicating that the fluctuations experienced by Moslem stock exchanges in these countries could not be attributed to usual rates. The research needs to be extended for understanding any other potential cause(s) of fluctuations in such markets, like global market moods, prices of oil and political happenings.

Our research provides significant insights regarding the dynamics associated with Islamic stock exchanges in developing countries. This calls for an elaborate understanding towards investment strategies and risk management techniques that are applicable to these markets, given that they are characterised by enormous macroeconomic changes, diverse investor behaviour, combined with complicated regulatory structures.

Limitations

Our study acknowledges certain limitations:

Data frequency: The use of monthly data might not fully capture short-term volatility dynamics. Future research could employ higher-frequency data for a more comprehensive analysis. Limited macroeconomic variables: Focusing only on short-term interest rates and CPI could limit the analyse; if we include other studios like exchange rate (RER), oil prices, economic policy uncertainty (EPU) and so on, then we may get a more comprehensive analysis.

Future Research

Future research could explore:

Microstructure analysis: Explore how trading actions, order flow and market liquidity contribute to volatility in Islamic stocks globally. Behavioural finance: Examine the role of investor sentiment, herding behaviour and overreaction to news in driving volatility. Comparative analysis: A comparative study of Islamic stock market volatility should be conducted to highlight similarities and differences across regions and countries in their macroeconomic drivers.

Footnotes

Declaration of Conflict of Interests

The author declares no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.