Abstract

Classic microfinance loan contracts characterised by rigid weekly repayment schedules used by most microfinance institutions (MFIs) offer little flexibility—and little benefit—to borrowers who are poor and have seasonal income. Previous research has also shown that such contracts can negatively affect the economic well-being of poor borrowers leading to underinvestment of capital, selling of productive assets, over-indebtedness through cross-financing from informal sources, reductions in consumption and income, and in some cases, a deterioration in borrowersʼ mental health arising from stress and worry. If lenders offered more flexibility in loan repayment schedules, would it help to overcome some of these problems? To explore this, we tested whether clientsʼ business outcomes were sensitive to various repayment schedules using primary data collected from the clients of three MFIs, a cooperative society and a few local traders specialising in business lending in a village in North India. We analysed alternatives to the rigid contract model, focussing on the degree of flexibility and the length of gap between repayments in the loan schedule. This study finds that clients repaying their loans monthly invested more in their businesses and earned higher income, compared both to those who repaid weekly and to those with an irregular payment schedule.

Introduction

Microfinance has been traditionally intended to benefit borrowers—especially poor borrowers; however, recent empirical evidence suggests that access to microcredit programmes has only a limited impact on clients’ lives (Armendáriz & Morduch, 2010; Banerjee et al., 2015; Basumatary et al., 2022; Karlan & Zinman, 2009; Meager, 2019; Nakano & Magezi, 2020). This is particularly surprising given the substantial evidence that credit constraints limit the expansions of small businesses (Banerjee & Duflo, 2014) and that borrowers’ returns to capital in microenterprises are high (De Mel et al., 2008). A growing body of evidence suggests that the participation rate in many microfinance programs remains low (Banerjee et al., 2015), dropout rates are high, and the demand for larger loan sizes is less (Meyer, 2002). There is clearly a paradox here: if the borrowers need the loans, and the loans appear to benefit the borrowers, why are the borrowers still reluctant to engage?

One of the reasons cited is that the rigid weekly repayment structures generally offered by microfinance institutions (MFIs) have failed to meet the investment needs of poor borrowers—especially those who have seasonal and irregular income and cash flow. The use of a classic microcredit contract with immediate and frequent (weekly) repayment obligations—in order to reduce defaults and instil fiscal discipline (Armendáriz & Morduch, 2010; Jain & Mansuri, 2003; Meyer, 2002)—may actually inhibit investment and reduce the ability of poor clients to extricate themselves from poverty.

A standard microfinance contract includes a small initial loan, fixed and regular repayments usually starting within a week of first disbursement, progressively larger lending and zero tolerance towards default (Labie et al., 2013). However, MFI clients are almost always poor with irregular income throughout the year. This frequently results in a cash flow disconnect when a repayment is due. Sometimes clients resort to selling productive assets, labour or crops in advance (Khandker, 2012), underinvesting (Field et al., 2010), skipping meals and reducing consumption (Shoji, 2010) only to then borrow from local money lenders at a very high-interest rate (Jain & Mansuri, 2003) in order to repay loan instalments to the MFI. Considering this, there are clear potential benefits for clients in having a loan contract that either lets them align their repayments with their income; or offers a longer gap between repayments.

This paper analyses the effect of various repayment structures on borrowersʼ entrepreneurial outcomes. 1 More specifically, we compare the rigid weekly repayment schedules with two alternatives—first, a monthly repayment schedule instead of a weekly one; and second, a flexible repayment structure tailored to borrowers’ needs. The study utilises a mixed-method approach collecting quantitative and qualitative data from the clients of three MFIs, a cooperative society and a few local traders specialised in business lending in a village in North India.

For the sake of clarity, we should establish some of the key loan characteristics under consideration. Microfinance loans in India are generally intended for poor borrowers with negligible credit history and little financial literacy (Armendáriz & Szafarz, 2011). It has, therefore, been usual for MFIs to design and implement their lending in such a way that helps borrowers learn financial discipline and prudence. In practice, this means that the schedule of repayment must be frequent, and the terms of repayment must be rigid: hence the default repayment scheme for micro-loans is invariably weekly and non-negotiable. The schedule typically requires a borrower to start their repayments immediately after receiving the loan. In this paper, this is what we mean by a ‘traditional’ repayment scheme, and we contrast this approach with other more ‘flexible’ schedules. There is clearly a difficulty in comparing traditional loans with flexible loans, as ‘flexible’ loans may by definition vary widely in their terms, schedules, conditions and rigour. There is no such thing as a single ‘flexible’ loan. We will, therefore, consider two alternatives to the traditional weekly approach—at opposite ends of the flexibility spectrum. The first (direct) comparison is with monthly repayment schemes but we also draw less direct comparisons with the highly flexible credit which is often available from local lenders such as cooperative societies and traders. These lenders—with insight into local market conditions and information on clients’ reputations—can tailor both their products and their repayment terms to individual borrowers’ needs and circumstances over time.

The results from this study suggest that borrowers with monthly repayment obligations have a higher level of investment and income compared to those with fixed weekly and flexible repayment schedules. This means that a combination of flexibility and financial discipline—which is better achieved by monthly repayment obligations as opposed to flexible or weekly—is needed for favourable business outcomes for microfinance clients. The qualitative enquiry suggested that weekly repaying clients had less satisfaction with loan products, reported more frequent instances of being stressed before an instalment was due, higher incidence of asking for help in paying instalments from friends and relatives, and delayed expenditure on essentials such as healthcare.

The rest of the study is organised as follows. Section I gives some background on loan repayment structures; Section III describes the data; Section IV presents the methodology used, Section V shows the results, and Section VI contains a summary and discussion of our findings.

Background

In designing microcredit products, MFIs rarely prioritise flexibility. 2 This reflects a widespread belief that flexibility compromises the repayment discipline of borrowers, and can result in higher default rates. However, the evidence linking flexibility and default rates is very mixed. Using a field experiment in West Bengal, India, Field et al. (2010) found that flexibility in microfinance contracts (introducing a grace period of two months before repayment) did indeed significantly increase borrower defaults. On the other hand, Battaglia et al. (2018) found—using data from a randomised control trial (RCT) in Bangladesh—that repayment flexibility improved business outcomes and actually lowered default rates. In a similar study in Madagascar, Weber and Musshoff (2017) found very little difference between the loan delinquencies of farmers with flexible loans (repayment grace periods) and those with standard loans.

It is worth stressing that the high repayment rates proclaimed by the microfinance industry do not necessarily mean that their customers are doing better, nor do they reflect the struggles clients face while repaying their debt obligation through rigid instalments (Prathap, 2017). Often, MFIs resort to coercion and high-pressure tactics for loan recovery (Karim, 2011) which have even, in some instances, resulted in suicide by borrowers in India (Biswas, 2010). Borrowers who default on repayments also face being barred from any future access to loans, as well as a range of further social penalties including humiliation, social pressure, verbal hostility, harassment, shame, and loss of face among community members (Sett, 2015). When potential borrowers have a high level of fear about defaulting, this affects the level of participation: potential borrowers either do not borrow, borrow less, or drop out of the scheme early (Boucher & Guirkinger, 2007; de Janvry et al., 2013). Even when clients do manage to repay weekly instalments on time, the lack of autonomy or loss of control over their actions due to the lack of flexibility in the repayment schedule can lead to sub-optimal task performance, poor motivation and reduced well-being (Chakravarti, 2006; Moller et al., 2006).

The use of frequent rigid repayments in microfinance is also related to over-indebtedness by cross-financing of repayments from informal sources and discouraging credible borrowers from taking out further loans. Jain and Mansuri (2003) found that frequent repayments expanded the volume of informal lending and raised interest rates in the informal sector. Pearlman (2010) argues that a lack of flexibility in microfinance contracts could be the reason for borrowers avoiding using formal credit providers, and instead continue to rely on informal moneylenders. Karlan and Mullainathan (2006) observed that rigid contract schedules constrain loan size and deter some solvent borrowers from taking out loans.

Early initiation of repayment may also lead to entrepreneurs underinvesting in their businesses since they are often obliged to set aside a portion of their loan at the outset for immediate repayment. A rigid repayment structure demanding frequent instalment payments also limits the type of project that can be financed with a microcredit loan, and can deter clients from making an illiquid investment with potentially higher returns. Using a lab-in-the-field experiment with Indian microentrepreneurs, Barboni (2017) found that risk-averse borrowers were more likely to take up rigid contracts with low flexibility. In contrast, Field et al. (2010) show that clients with a grace period of two months were more likely to start businesses and invest in less liquid assets with higher returns if there was a relaxation of liquidity demands in the early phase of the loan cycle. Using an RCT in India, Aragon et al. (2020) found that additional flexibility in repayment terms increased profits of the borrowers.

Flexibility in repayments could also improve a client’s ability to deal with short-term shocks to household income. In an experiment in India on microfinance clients working in dairy farming, Czura (2015) found that flexible repayment schedules significantly improved the ability of the borrower to absorb such shocks and resulted in higher income due to an increase in investment and productivity. In a similar study in Bangladesh, Battaglia et al. (2018) offered vouchers to delay up to two monthly repayments anytime during a 12-month loan cycle and found that treated clients experienced higher sales volatility without an increase in default rates. This suggests that flexible contracts could also act as an insurance mechanism in case of fluctuations in income.

In addition to making life easier for borrowers, some types of flexibility offer clear operational benefits to lenders. Field and Pande (2008) suggest that MFIs can reach up to four times as many clients without hiring additional collection officers, simply by changing the repayment schedule from weekly to monthly. Fewer meetings, fewer collections, and fewer transactions inevitably translate into lower costs. If we accept the central premise that microfinance is a powerful tool for poverty alleviation (Armendáriz & Szafarz, 2011), and that flexibility enables lenders to reach both the poorest and most seasonally-affected borrowers (Khandker et al., 2012) then it is clearly desirable for MFIs to reduce costs, lower interest rates, and service as many clients as possible.

An easing of rigid repayment schedules could also contribute to broader non-economic goals. Since poverty is a multidimensional construct involving both economic deprivation and psychological well-being (Chakravarti, 2006; Narayan-Parker & Patel, 2000), it is logical that if policymakers and MFIs really wish to tackle ‘poverty’, they take a holistic view in designing financial products which address both the poor clients’ fundamental needs of economic prosperity and psychological well-being (Sett, 2015). Repayment flexibility can reduce financial stress as noted by Field et al. (2012), where they found that clients with monthly repayment obligations were less likely to report feeling ‘worried, tense, or anxious’ about repaying; and were more likely to report feeling confident about repaying; and reported spending less time thinking negatively about their loan compared to the weekly repayment clients.

Despite the clear potential to better meet the needs of MFIs and their clients, there is limited evidence on the effects of deviating from the traditional weekly repayment contract’s design and most of it is focused on delinquency and default rates. Not much attention has been given to other important business outcomes such as level of investment, loan amount and income. This research aims to narrow this knowledge gap.

The Study Area and the Data

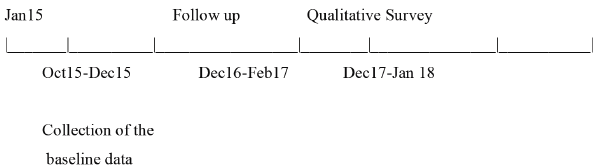

The quantitative study covered a random sample of 211 women who were clients of three MFIs, a cooperative society, and a few local traders collected through two household surveys taken in 2015 and 2016 (see the timeline in Figure 1), in a village in the state of Haryana (see the location in Figure 2). The survey collected information regarding income, loans, investment, health, household composition, education, employment, assets, and other variables. The qualitative research involved semi-structured interviews with 28 clients in 2018.

Timeline of Data Collection.

Timeline of Data Collection.

The village is 90 km away from the state capital, with 1143 households and a population of 6466, of whom 3420 are males while 3046 are females as per the Population Census 2011. Haryana is a relatively prosperous state with only 11 per cent of the population living below the poverty line. The average literacy rate of Haryana is 76 per cent, male literacy stands at 84 per cent while female literacy is at 66 per cent, not far off from the national average. Hinduism is the main religion of the state with 87.46 per cent classified as Hindu. The state is also very agricultural with 65.12 per cent of people living in rural areas. The village is in a very stable region with a fast-growing economy, good infrastructure for irrigation and transportation, and a very low likelihood of being affected by natural disasters such as earthquakes or floods.

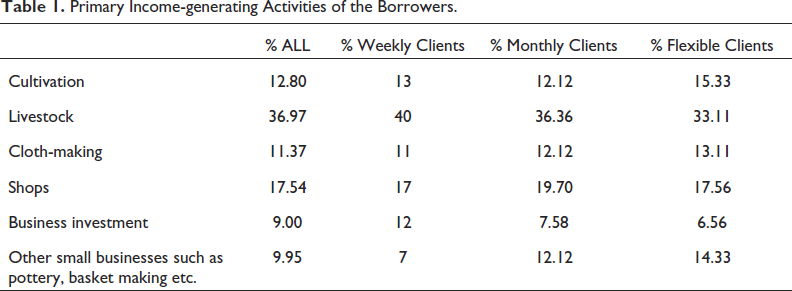

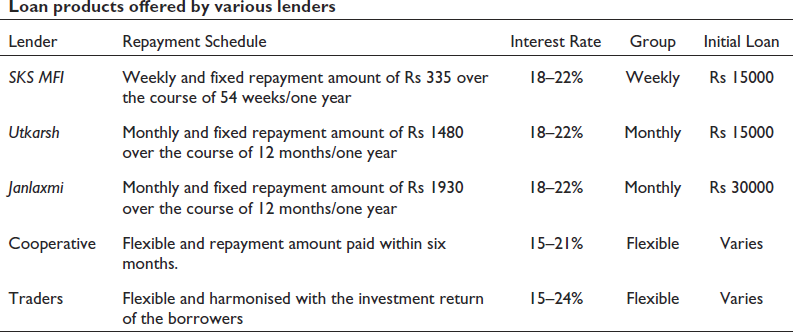

The credit market of the village has been served by three microfinance organisations: SKS (now known as Bharat Financial Inclusion Limited), Utkarsh, and Janlaxmi since 2014. Additionally, there is a government-supported cooperative society and several traders specialising in productive loans. Most women in the sample are self-employed in household businesses such as livestock, agriculture, small shops, and garment making (see Table 1). None of the businesses are registered with the government or have any permanent employees.

Primary Income-generating Activities of the Borrowers.

All three MFIs use a version of the Grameen group lending model. Like a Grameen model, borrowers are asked to form a group of five and, subsequently, the group members are expected to monitor each other’s repayment as well as share some coordination activities (such as collection of repayments) to reduce the operational costs of the MFI. However, they all can receive as well as repay the loan at the same time (instead of taking turns to do the same). Eligibility to receive a second loan depends on both the individual and the group repayment record. Repayment of 50 per cent dues makes one eligible for a second loan. The group is expected to meet every week/month for a short meeting during which the members pay their dues and repeat their pledge to the group to maintain honesty and continue to repay on time. Thus, the group offers both a screening device and partial monitoring, but the liability remains individual. During the study period, there was no case of default or expulsion from a group.

There is some difference between the MFIs in terms of the repayment cycle. The repayment cycle of SKS is weekly which starts within a week of the loan disbursement, whereas Janlaxmi and Utkarsh use a monthly cycle of repayment, which starts after a month of the loan disbursement. SKS and Utkarsh have similar loan products where a new borrower starts with a loan limit of Rs 15,000 ($215), which is then increased by an additional Rs 15,000 ($215) in the second loan cycle, and then by Rs 20,000 ($285) in the third loan cycle, and finally by Rs 30,000 ($430) in the fourth until to reach the overall cap of Rs 80,000 ($1145) is reached. For Janlaxmi, the first loan starts at Rs 30,000 ($430) and the second loan can be up to Rs 50,000 ($615). The repayment is collected by a loan officer during the weekly/monthly meeting of the group, and a record is kept in individual passbooks. Hence, the clients of SKS meets 54 times a year to pay their instalment compared to only 12 times a year for Utkarsh and Janlaxmi clients.

The cooperative society and traders are very flexible both with their loan amount and repayment cycle. Usually, a cooperative loan is to be paid back within six months with agreed monthly instalments of variable amount. Instalments can be adjusted in difficult times, but failure to pay the loan on time can invite penalties in the form of higher interest charges on the outstanding amount and/or being barred from future loans. The ‘flexibility’ in lending from traders varies depending on the borrower’s relationship with them. These lenders in the samples, also known as aadthis, are a special category of professional money lenders in the village who are grain traders but also serve the function of lending in the absence of concrete formal financial infrastructure. They provide facilities for both credit and savings and act as a village bank. Due to heavy competition in the village lending sector, their interest rates are usually the same as the MFIs. The loans are usually seasonal and for productive purposes, and lenders prefer to be paid just after the profits from the investment are realised. One of the clear benefits of borrowing from these two groups is that the repayment schedule can be harmonised with the occurrence of investment returns.

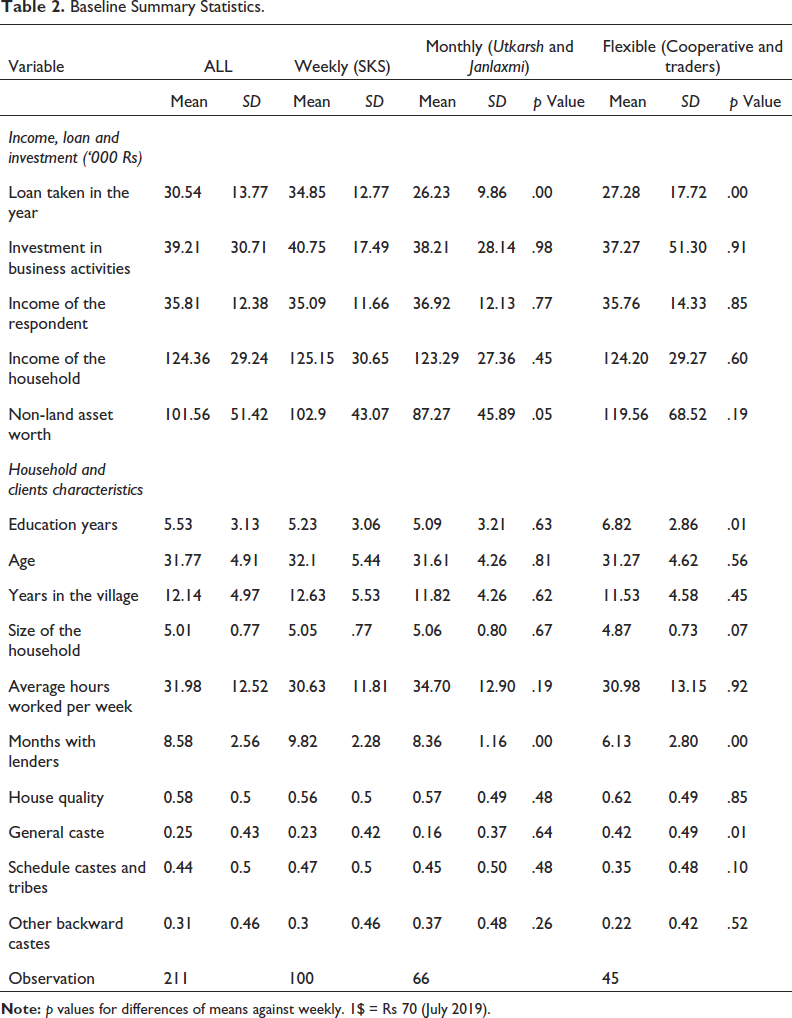

The descriptive statistics of the participants at baseline are provided in Table 2. The average woman in our sample is 31.77 years old and has completed 5.5 years of education and lived in the village for 12 years. The average client has a total loan size of Rs 30.53 ($430), an income of Rs 35810 ($515), saves Rs 690 ($10) every month, consumes food worth Rs 3400 ($48.64) every month and owns Rs 101,560 ($1452) worth of non-land assets. On average, clients have invested (business spending on items such as inventory, raw material, labour, and land) Rs 39210 ($542) while working 32 hours per week. Information regarding expenditure on health, children’s education, house quality, 3 and other personal characteristics was also collected in the survey.

Baseline Summary Statistics.

To assess the impact of flexibility in repayments on business outcomes of microfinance clients, this study uses a mixed-method approach, which includes a questionnaire survey for quantitative data and semi-structured interviews with randomly selected borrowers.

We divide the analysis into various categories of business outcomes. Our primary focus is on the level of investment, income and loan amount. Due to the relatively small sample size, it was not feasible to compare rates of default—in fact, during the course of the study, the default rate was zero in our sample.

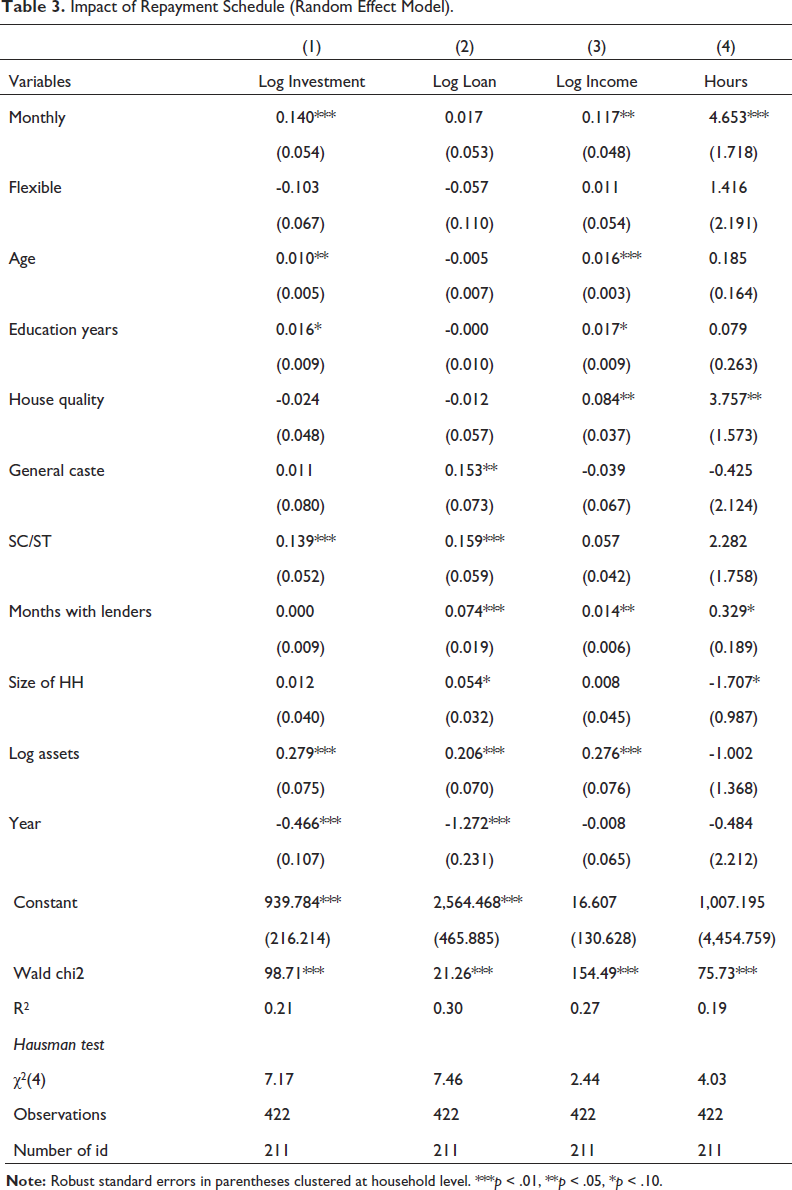

For the quantitative analysis, the study uses panel data collected from two rounds of household surveys in 2015 and 2016. To identify which empirical methodology—fixed effects or random effects model—is most appropriate, we perform the Hausman specification test (Hausman, 1978). A rejection of null hypothesis in the Hausman test statistic would imply that the random effects estimators are inconsistent and that fixed effects estimates are more appropriate. In our case, the Hausman specification test failed to reject null hypothesis (see Table 3) and suggests support for the random effects model. 4

Impact of Repayment Schedule (Random Effect Model).

Impact of Repayment Schedule (Random Effect Model).

The random effect model is proposed in the following form:

Where Yit denotes an outcome variable for a client i at the time t, M is a dummy for a monthly repayment schedule and F is the dummy for a flexible repayment schedule, X is a vector of the borrower’s individual and household characteristics such as age, education, condition of the house, size of the household, the value of assets and caste. Ui is an household-specific unobservable effect,

Parallel to the quantitative analysis, a series of interviews were carried out with 28 women 5 (10 participants from weekly, 10 participants from monthly and eight from flexible group), who were randomly selected from the survey sample. 6 The questions relating to client’s reasons for joining the lender, their feedback (pros and cons) of the lending product, satisfaction with the lending terms, and effect of the product on client’s business were asked. In terms of analysing the information in the interviews, transcripts and notes were first coded into categories. For example, comments on the level of investment were grouped together. Similarly, other categories were formed—income, loan amount, consumption and other relevant information. This helped us to understand the differences in the viewpoints of participants between and within various repayment groups on how the repayment structure is affecting the above categories.

Endogeneity

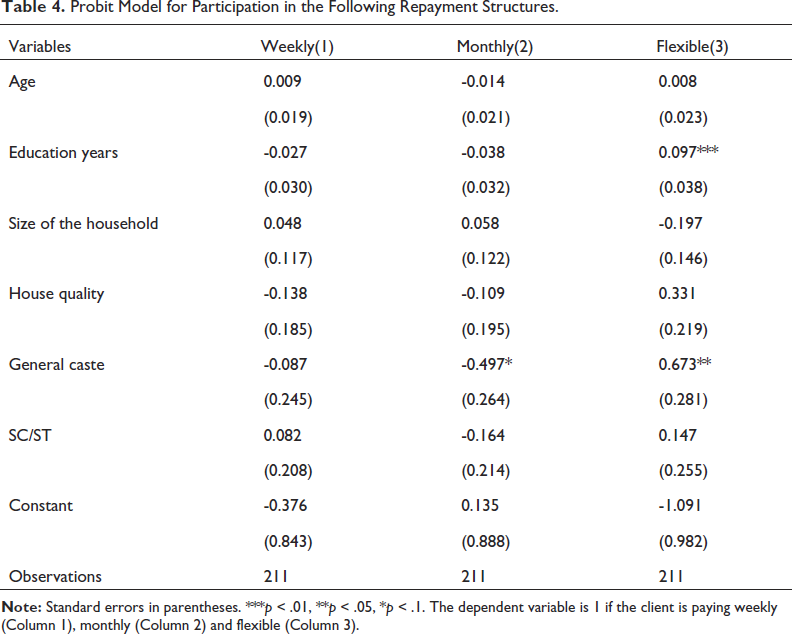

The choice of repayment structure was exogenous for both the MFIs and the borrowers. All three MFIs offer the same repayment structure and loan products regardless of the region they operate in, implying that the repayment scheme has no relationship with the location or the borrowers’ characteristics. The borrowers of MFIs are indifferent to the repayment structure, which is verified using a probit model (see Table 4) on the probability of participation in any of the repayment structures at the first round. We find MFI borrowers’ characteristics (except being from general caste significant only at 10 per cent) have no influence on the participation in either monthly or weekly. Hence, it can be argued that neither the MFIs nor their borrowers chose this scheme considering the borrowers’ characteristics in the area. However, higher educated clients and those who belong to general castes are more likely to participate in flexible repaying lending giving arise to the problem of self-selection. Our qualitative enquiries suggest that the clients felt indifferent to the credit repayment structure, and simply getting a loan was the most important factor in joining the MFI or other lenders. Most of the clients of MFIs were introduced by their friends or joined because their friends were already members. Prospective clients first express their interest in getting a loan, then a loan officer goes to the client’s house and evaluates if the client fulfils all the criteria for the loan. If the client agrees to all the loan conditions and has a guarantor, a contract is signed between MFI and the client.

Probit Model for Participation in the Following Repayment Structures.

The results show that the client’s investment behaviour is sensitive to the design of debt contracts. The study finds a significant increase in business investment for the monthly repaying group (see Table 3) investing roughly 14 per cent on average more on business items compared to weekly clients. The study also finds that clients with monthly repayment schedules increased their income by 12 per cent; however, no effect was found with flexible repayments (see Table 3). These results are consistent with the predictions that by reducing the liquidity needs in the early phase of a client’s loan cycle, monthly repayment should increase the client’s investment in business. In contrast, rigid weekly repayment may require the client to keep some money from the loan amount to pay for the instalment due to start immediately after the loan disbursement. In this case, clients are more likely to (under)invest in a less risky and liquid asset with low returns and hence, limit the likelihood of potential income growth.

We do not find any significant difference between weekly and flexible client’s income and investment. This suggests that microfinance clients need a combination of discipline and flexibility for their businesses to grow, which is better achieved by monthly repayment obligations as opposed to flexible or weekly. In this regard, these findings are in contrast to Barboni and Agarwal (2018), Battaglia et al. (2018), Czura (2015) and Field et al. (2012). 7

The qualitative data analysis confirms the plausibility of the quantitative analysis that clients with weekly repayment schedules kept a portion of their loan to allow repayment of their first few instalments, reducing the funds available to the business.

One of the clients who has a sweet shop in the survey confirmed underinvesting in their business. She said:

…I got a second loan for stocking up sweets to sell during Diwali. A part of that loan went for advance payment to the supplier to confirm my bulk order. The rest of it was set aside to pay for the weekly instalments since it will take weeks to sell enough sweets to make a profit – weeks in which I still have to make regular repayments on loan. This adds to the cost of borrowing [Interviewed in January 2018].

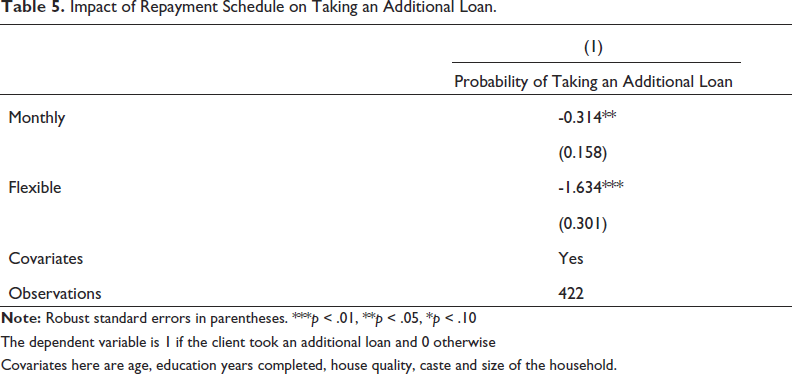

We do not find any significant differences in the amount of loans taken by various repayment groups. However, the use of monthly and flexible repayments reduced the probability of taking an additional loan from an external lender by 31.4 percent and 163.4 percent, respectively (see Table 5). The qualitative enquiries suggest that these additional loans are usually taken from small moneylenders who charge a very high interest rate and sometimes to pay for repayments of the initial MFI loan. These findings are comparable to Jain and Mansuri (2003) study which shows that the use of regularly scheduled repayments in microfinance loans may be a reason why informal lenders still thrive in regions where microcredit has been firmly established.

Impact of Repayment Schedule on Taking an Additional Loan.

Impact of Repayment Schedule on Taking an Additional Loan.

The dependent variable is 1 if the client took an additional loan and 0 otherwise

Covariates here are age, education years completed, house quality, caste and size of the household.

The interviews suggest that some women who are struggling to pay their instalments turn to the informal sector for help. This phenomenon was echoed by one respondent who pays their instalment weekly:

...our business (agriculture) is seasonal, and we are poor with no savings. It is hard to pay every week when there is no source of income during the low season. We have to borrow from neighbours, friends or informal lenders (quick loans at a very high interest rate) in order to pay the weekly instalments. Borrowing from some people could be very humiliating and stressful since they will keep reminding you about the money [Interviewed in December 2017].

Microfinance is seen as a tool to protect the poor from village moneylenders (also known as loan sharks) who usually charge a very high interest rate. However, rigid and inflexible microcredit contracts may have helped them survive by taking advantage of the information symmetry between MFIs and clients (Jain & Mansuri, 2003).

One woman did not increase her loan size after being given a choice and linked weekly instalments with stress as illustrated by the following statement:

…finding money for the repayment every week causes me real worry and stress. Until I have money for the instalment, I feel anxious and agitated all the time. Taking a bigger loan and paying even higher instalments will make it worse [Interviewed in December 2017].

The study also finds that monthly repayment clients work 4.6 hours more per week than weekly repaying clients (see Table 3). This shows that the increase in investment is complemented by an increase in the hours worked.

The qualitative enquiries suggested that women with weekly repayment schedules have lower satisfaction with the loan product compared to monthly and flexible repayment borrowers. Lack of time to attend weekly meetings was also given as the reason for somewhat less satisfaction. Women with weekly repayment schedules reported higher incidences of being stressed on the day before an instalment was due. On the other hand, monthly group members reported making business purchases in bulk more frequently compared to the women in the weekly group. Incidents of delaying expenditure on healthcare reported were also higher in the weekly group.

Weekly repaying women also emphasised the importance of the social interactions in the regular weekly meetings: particularly valuable experience given the traditional norms of female isolation in the region. Social interaction for the women with a monthly repayment was rare outside their group. Research by Feigenberg et al. (2013) shows that more frequent meetings can increase social capital. The qualitative enquiry suggests that more women from the weekly group reported asking for help to pay instalments from their group members. This might be due to an increase in social capital and economic cooperation among women.

Microfinance has been hailed as one of the most innovative and productive tools for fighting global poverty, providing financial services for those with no access to traditional banking. However, recent evaluations of microfinance products have found limited evidence of the transformative effects claimed by its proponents. Anecdotally, many borrowers blame the contract models used to manage their loans. Most MFIs follow a rigid non-negotiable contract model where every client must repay in the same way: fixed weekly instalments starting immediately after disbursement of the loan. These offer no flexibility to borrowers who are poor and have seasonal income. Such contracts can also negatively affect the economic well-being of poor borrowers leading to underinvestment of capital (Field et al., 2010), selling of productive assets (Khandker, 2012), over-indebtedness through cross-financing from informal sources at a higher interest rate (Jain & Mansuri, 2003), reduction in consumption (Shoji, 2010), income (Czura, 2015), and increases in financial stress (Field et al., 2012). A shift away from a rigid weekly repayment schedule can overcome some of these problems. Based on the results, this study makes a case in favour of monthly loan repayment contracts. The findings suggest that a monthly repayment structure can break the cycle of low investment in microenterprises by borrowers as well as boost their income. The qualitative enquiries suggest that weekly repaying clients invested less of their loan amount, had less satisfaction with their loan products, reported more frequent incidences of being stressed before an instalment was due, higher incidences of asking for help in paying instalments from friends and relatives, and more frequently delayed expenditure on healthcare.

Considering this, MFIs have an opportunity—arguably a responsibility—to build financial products aligned with the needs of their consumers; and they can achieve this without sacrificing their core objective of reducing poverty in a profitable and sustainable manner. Such a model may require MFIs to work more closely with their consumer to understand their requirements and build customised products depending on the consumers’ cash flows. If lenders wish to overcome the barriers which their current operating model presents, there is a pressing need to shun the ‘one size fits all’ approach to rigid microfinance contracts. Longer gaps between repayment may deteriorate payment incentives; however, MFIs can use sanctions (such as barring from future loans) and rewards (such as an increased loan size and reduced interest rates) and collect more detailed information on its clients (Labie et al., 2013). MFIs could take advantage of informal financial channels to collect information on prospective borrowers (Hamp & Laureti, 2011) or hire local payment collectors from the same area to the clients to facilitate screening, and to monitor and mitigate moral hazard problems 8 (Labie et al., 2013). The optimal combination of flexibility and discipline would require lenders to innovate their product design, lending technologies, and risk management strategies and to dramatically improve their information base (Sett, 2015). Although less-frequent repayment schedules may result in some higher costs for MFIs—e.g., through deploying more staff in the field to monitor clients and acquiring information on clients to evaluate their preferences and repayment capacity—there are potential benefits for those lenders too. MFIs can lower costs by reducing the frequency of repayment-collections and may be able to lower interest rates, scale up operations, and reach additional clients in remote or previously under-served locations.

Although the present study confirms the general benefits of flexibility in terms of longer repayment gaps, this approach is not easy for most microfinance organisations to implement because an MFI needs to instil and maintain repayment discipline among its clients. Nevertheless, the benefits are real, and the challenge rests with the microfinance organisations to seek ways of transferring these benefits to the formal sector, by more efficient and effective design of loan contracts.

Until now, MFIs have largely ignored the demand for monthly repayment financial products; however, increasing competition in the microfinance industry may encourage MFIs to rethink their product design. For them to continue growing, it is essential to pay attention to their clients’ needs, preferences, behaviours and well-being. We hope this study will help MFIs to rethink and refocus their lending approach and help them make the shift away from rigid loan contracts.

Although this paper draws a clear conclusion—that a traditional rigid weekly repayment structure is not the best option—the scope of this research to date does not allow us to state with confidence what the best option actually is. We conclude that flexibility is best, but ‘flexibility’ is a broad term, which includes the introduction of grace periods (Field et al., 2010), clients’ involvement in choosing their preferred repayment structure (Barboni & Agarwal, 2018), as well as simply requiring less frequent repayments (monthly rather than weekly) and offering a greater range of loan products to cater for a wider range of client needs. Or, of course, any mixture of these. Both further qualitative and quantitative research are needed to understand in detail the cash flow and other challenges faced by poor clients in repaying debt obligations, and to seek the elusive balance between maximising economic benefit for the client while minimising economic risk to the lender.

Despite the results put forward in this research, the question regarding the impact of repayment flexibility remains critical for further studies. Future studies should focus on more enhanced versions of flexibility, comparing financial products differing in their degree of flexibility, and understanding the conditions under which flexibility works well. Future studies should also try to overcome the limitations of this research in terms of a small sample which has been complemented with qualitative data to make the results robust. Since our findings are based on the sample of women in Haryana, North India, we do not recommend generalising the results beyond this selected group of women.

Finally, this study recommends qualitative research, along with quantitative analysis, to understand the challenges (economical and psychological) clients face while repaying debt obligations through rigid instalments, and how flexibility in loan contracts can improve business outcomes for borrowers. In this regard, the qualitative research set this study apart from the past literature on repayment schedules and has been instrumental to our understanding of the obstacles to progress created by the enforcement of rigid weekly microfinance contracts.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.