Abstract

Coronavirus disease 2019 (COVID-19) posed a serious challenge to food production and distribution worldwide. There were major disruptions in supply chains due to mobility restrictions and a slump in demand due to the loss of livelihoods and incomes. What effect do these offsetting movements have on prices? Which commodities experienced price increases/slumps? Were these localised or widespread across regions? What is the relative contribution of sub-groups to the overall trends? We delve into these issues using wholesale and retail price data to understand the price dynamics in India during COVID-19, using the previous four years as the reference point. The analysis revealed that the retail margins were consistently higher in 2020–2021 indicating the persistence of local shortages for all commodities. Owing to government support through procurement and distribution, the effect on cereals’ prices was minimal. Perishables like vegetables and meat/fish marketed in raw form through informal/petty trade networks, faced maximum erratic behaviour, while milk, marketed in processed form by organised intermediaries, experienced a moderate impact on prices. Fruits, a perishable but with high-income elasticity of demand, witnessed muted prices possibly due to income erosion. Pulses and oils/fats, imported in large quantum, saw a sharp price increase due to local supply bottlenecks combined with international trade disruption.

Introduction

A strict nationwide lockdown was imposed on 24 March 2020 to control the spread of the coronavirus disease 2019 (COVID-19) virus in India. This lockdown continued in varying degrees of intensity until 31 May. Upon improvement in the situation, a gradual unlock was done by November 2020.

The growth rate of India’s annual real GDP (2011–2012 prices) in 2020–2021 was −6.2%. All the sectors of the economy, except agriculture, experienced severe contraction. In April 2020, many important policy decisions were taken by the union and the state governments for the agriculture sector. Extended and staggered procurement; enabling farmers to sell and transport directly from registered warehouses and farmer producer organisations (FPOs); designing app-based transport aggregator services; removal of restrictions under the Essential Commodities Act, allowing inter-state trade were some of the important measures undertaken.

These measures helped the agriculture sector record an impressive growth rate of 3.6% in 2020–2021, following a decent growth rate of 3.7% in 2019–2020. There was bumper food production of 309 million tons, which was 4% more than the previous year. Foodgrain stocks were also adequate, even with enhanced food distribution programmes launched during the pandemic.

Despite such positive performance of agriculture and food distribution, consumer food inflation remained a concern. Headline inflation based on the consumer price index (CPI), which was on a downward trend from 2014 to 2018, began to rise thereafter. The CPI inflation which was 4.8% in 2019–2020 (Apr–Mar) rose to 6.2% in 2020–2021. This rise was mainly driven by food inflation, which increased from 0.73% in 2018–2019 to 7.3% in 2020–2021. The weight of food and beverages in CPI is 46% while in the USA it is about 14%–15%. Thus, headline inflation in India is more sensitive to movements in food prices. As per the Economic Survey 2020–21, during 2019–2020 (Apr–Dec) as well as 2020–2021 (Apr–Dec), the major driver of CPI inflation was the ‘food and beverages’ group, with a contribution of 54% and 59%, respectively. The high food inflation since March 2020 points to possible supply chain bottlenecks due to COVID-19-induced disruptions. World food prices, as shown by the Food and Agriculture Organization’s (FAO) food price index, have also recorded a continuous increase from June 2020 to March 2021.

Most countries imposed lockdowns, movement restrictions and closed their borders to trade. Although the lockdown in India was lifted in phases, severe movement restrictions continued until November 2020. The fragmentation of national and international markets due to lockdowns severely impaired all four dimensions of food security. First, the restrictions on transportation and retailing severely affected physical access to food. It also affected the livelihoods and incomes of several workers involved in these sectors. There is evidence of an increase in the market power of local food traders, leading to an increase in prices (Ihle et al., 2021). Both these factors, reduction in incomes and rise in prices, had a negative effect on the economic access of households to food. The uncertainty induced by restrictions on marketing and distribution (of food) has also adversely affected the third pillar of food security, which is stability. Finally, morbidity induced by the disease also affected the absorption capacity of food. Against this backdrop, the main objective of the present analysis is to understand the effect of COVID-19 restrictions on economic access to food1 and livelihoods in India through an analysis of price increases and decreases. The rest of the paper is organised as follows. Section II outlines the research questions and data and methodology, followed by a brief review of the recent literature in Section III. The analysis and discussion of the results are presented in Section IV. Section V concludes.

Objectives and Methodology

Food is marketed at multiple points in India, starting from the point of production or the farm gate to the local village market to the wholesale market to finally the retail market. The main points among these for our present enquiry are the wholesale market and the retail market, for which a continuous record of prices is available. The price movements at the wholesale level largely affect the farmers while those at the retail level affect the consumers.

Food prices can increase because of multiple factors, which include supply shortages, demand upsurges, increases in international prices or a combination of all these (Sekhar et al., 2017). Demand for food products is normally stable while supply conditions may change depending on weather and other agro-climatic factors. However, COVID-19 posed problems on both sides. On the supply side, the problems related mainly to production and marketing, because of the labour shortage due to disease and movement restrictions and, the closure of many markets. On the demand side, the sudden imposition of lockdown left large numbers of workers unemployed or with drastically reduced incomes. This has adverse implications on demand for expensive protein-rich foods like milk, meat and fish. What is the effect on food prices of these mutually offsetting movements on the supply and demand side? This is the main question we explore in this study.

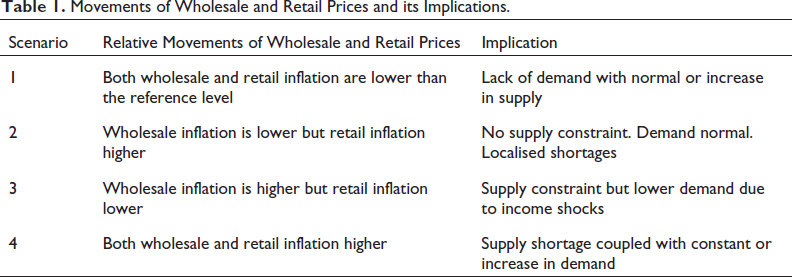

Food prices can differ at the wholesale and retail levels quite substantially. Since demand at the wholesale market is a derived demand emanating from the consumption side, a lower price at the wholesale and retail levels (than the reference price 2 ) would be an indication of depressed demand (possibly due to income shocks) and excess supply in the market. However, if the retail price is higher, then it may be indicative of local supply bottlenecks in the retail markets. On the other hand, if the retail price is lower and the wholesale price is higher, it may be indicative of a production constraint leading to excess demand in the wholesale markets. Finally, a situation of higher prices in the retail and wholesale markets is indicative of a leftward movement of the supply schedule coupled with a constant or a rightward shift of the demand schedule.

These four scenarios can be summarised as follows in Table 1.

Movements of Wholesale and Retail Prices and its Implications.

Movements of Wholesale and Retail Prices and its Implications.

Research Questions

What is the trend in prices at the wholesale and retail level from April 2020 to March 2021? What is the relative movement of specific commodity groups?

What is the relative movement of wholesale price index (WPI) and CPI inflation in 2020–2021?

Which specific commodities within a group have shown maximum change and possible reasons thereof?

What are the implications of the above price movements?

Data Sources and Methodology

Two important indicators of food inflation are used—CPI and WPI. The period of analysis is from January 2016 to March 2021.

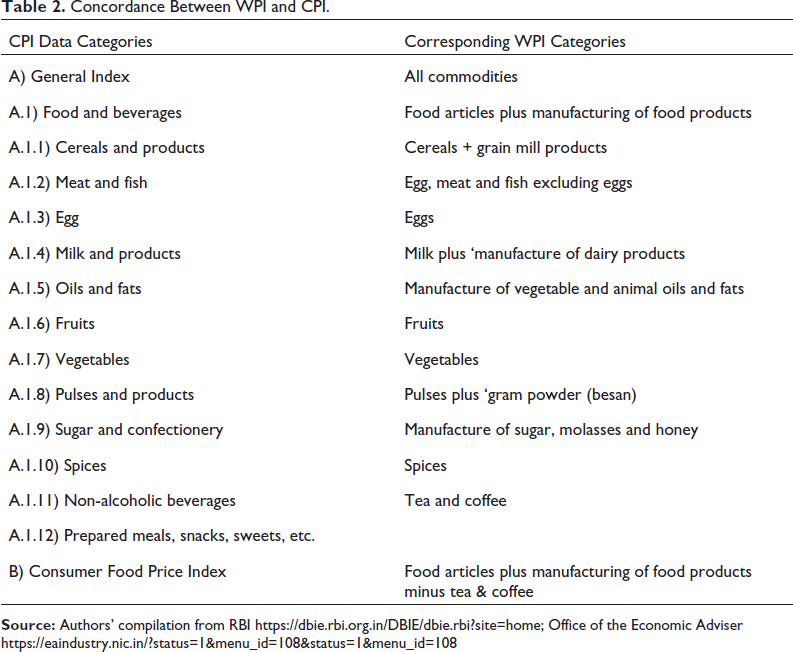

Monthly CPI data (base 2012 = 100) for food categories were extracted from the Reserve Bank of India (RBI) website. 3 Using the combined CPI, the inflation rate was calculated for each month from January 2017 to March 2021 for each food sub-group and major commodities within each sub-group. The monthly WPI data (base 2011–2012 = 100) for food was obtained from the Office of the Economic Adviser, Ministry of Commerce and Industry, Government of India. Prior to calculating the inflation rate based on WPI, for the sake of uniformity and comparison, we worked out the concordance of WPI with CPI using the sub-categorisation of CPI as the benchmark. The details of concordance are provided in Table 2. Using this, the WPI-inflation rate was calculated for the same sub-categories as CPI, from January 2017 to March 2021.

Concordance Between WPI and CPI.

For assessing the effect of the national lockdown in March 2020 on food prices, the average CPI and WPI inflation rates for 2017–2019 (reference prices) were compared with the corresponding monthly inflation rates during the period from April 2020 to March 2021. After identifying the broad food categories that had witnessed a surge post-lockdown, the specific commodities within those categories that could have possibly contributed to higher food inflation have been examined. For this, only inflation rates of commodities with higher weight in the CPI basket were analysed. However, since the CPI data for individual commodities was missing for the months of March, April, May 2020 and March 2021, the analysis of inflation rates of individual commodities was restricted to the period from June 2020 to February 2021.

Tabular and graphical analysis have been used in the analysis. To understand the relative contribution of each of the sub-groups to overall food inflation, a decomposition exercise has been carried out.

Inflation Decomposition

To identify the contribution of each of the commodity sub-groups to overall food inflation, we undertook the decomposition of monthly food and beverage inflation from April 2020 to March 2021 4 on the following lines.

Let Pi , Pi–12 be the CPI of food & beverages in the month i and in the same month of the previous year (that is i–12), respectively.

where ‘i’ is the month (i = 1, 2, 3…12) and ‘j’ is the commodity group such as cereals and pulses (j = 1, 2, 3…). wj is the weight of the group in the CPI basket, which is constant over the study period. Pji is the price index of the jth commodity in the ith month of a particular year. Pj( i –12) is the price index of the jth commodity in ith month of the previous year.

Food & beverage inflation in time i is given by

In this manner, the overall inflation of the food & beverages group can be decomposed into contributions of the individual j sub-groups.

The inflation of the consumption basket in 19 countries of the euro area fell by more than 40% from February to March 2020 (Harmonised Index of Consumer Prices (HICP), Eurostat 2010). However, food expenditures experienced a y-o-y increase (+2.4%) as well as for the previous month (+14%). The COVID-19 policies in the European Union (EU) had a disruptive effect on food supply chains (Ihle et al., 2020). Akter (2020), combining the EU’s HICP with the Stay-at-Home Restriction Index (SHRI) dataset for January–May 2020 and using a series of difference-in-difference regression models, finds the severity of stay-at-home restrictions increased overall food prices by 1% in March 2020, compared to January and February 2020. The effects on food prices of SHRI were significant even after controlling for cross-country effects.

Laborde et al. (2021) project a global recession of 5%–7% during 2020 and that around 150 million people could fall into extreme poverty due to the impact of COVID-19. They account for the differential impacts on employment, incomes and prices across economic sectors, types of workers, and groups of households. These distributional effects, which are not factored in other studies (World Bank, 2020 and Sumner et al., 2020), explain more than one-third of the overall poverty impact.

The impacts of COVID-19 supply disruptions on food production and value chains differed by product and region though (Laborde et al., 2020). Government support can also make some difference. In India, the marketing of staple crops was relatively less affected because of public procurement, compared to perishables like fruits and vegetables. Ceballos et al. (2021a) find that government intervention in grain markets has helped stabilise grain markets in Haryana, India while lack of similar support has rendered tomato producers vulnerable. Varshney et al. (2020) also highlight the role of government intervention in mitigating supply chain disruptions through public procurement as well as agricultural market reforms that helped in protecting farmers from a price crash. Pulses and vegetable oils, for which India depends upon imports, have been affected adversely by a rise in international prices.

Supporting the evidence on the vulnerability of perishable commodity farmers, Hirvonen et al. (2021) find that the supply of vegetables in Ethiopia’s urban markets was severely affected by disruptions in transport and supply of key farm inputs. Minten et al. (2020) find that smaller-sized vegetable farms in Ethiopia are less affected than medium-sized farms by COVID-19 disruptions, as smaller farms rely less on hired labour. This is consistent with Reardon et al. (2020), who hypothesise that vulnerability due to reduced labour supply shows an inverted U-shape with farm size. It increases initially with a relatively higher dependence of medium-sized farms on hired labour. As the farm size increases further, significant economies of scale kick in along with the financial capacity to use more capital.

As COVID-19 disrupts markets for non-staple, and perishable foods more than staple foods, these disruptions aggravate income-related problems and lead poor households to shift their consumption away from protein-rich foods, reducing dietary diversity and adversely affecting nutrition. Laborde et al. (2021) confirm the strong shifts in the composition of food demand. Their global scenario analysis forecasts that the COVID-19 recession induces substantial food demand shifts away from more nutrient-rich non-staples to lower-quality staples across regions and countries. Ceballos et al. (2021b) also show that income declines cause increases in food insecurity and particularly a reduction in more expensive foods like fruits, vegetables and animal-sourced foods. This is consistent with Hirvonen et al. (2021), who found that reductions in household food consumption in Ethiopia involved cutting down the intake of foods such as fruit, meat, eggs and dairy. Tata-Cornell Institute (2020) show a disproportionate rise in the price of non-cereals in India compared to cereals which could distort consumer spending resulting in inadequate intake of protein-rich food, particularly by the vulnerable population. Narayanan and Saha (2020) find that smaller cities have witnessed a sharp increase in retail prices particularly of pulses, oils and perishables such as tomatoes and onions.

Results and Discussion

Trends in Food Prices

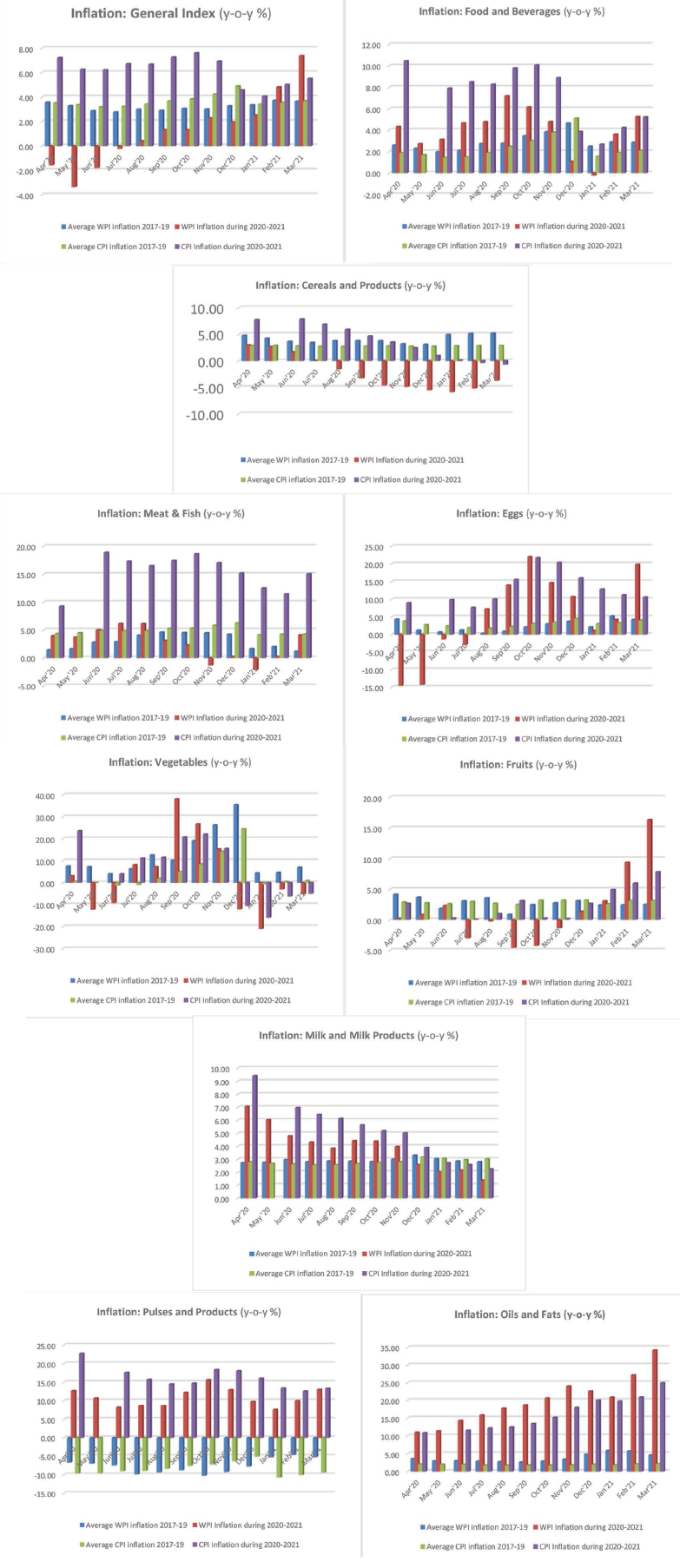

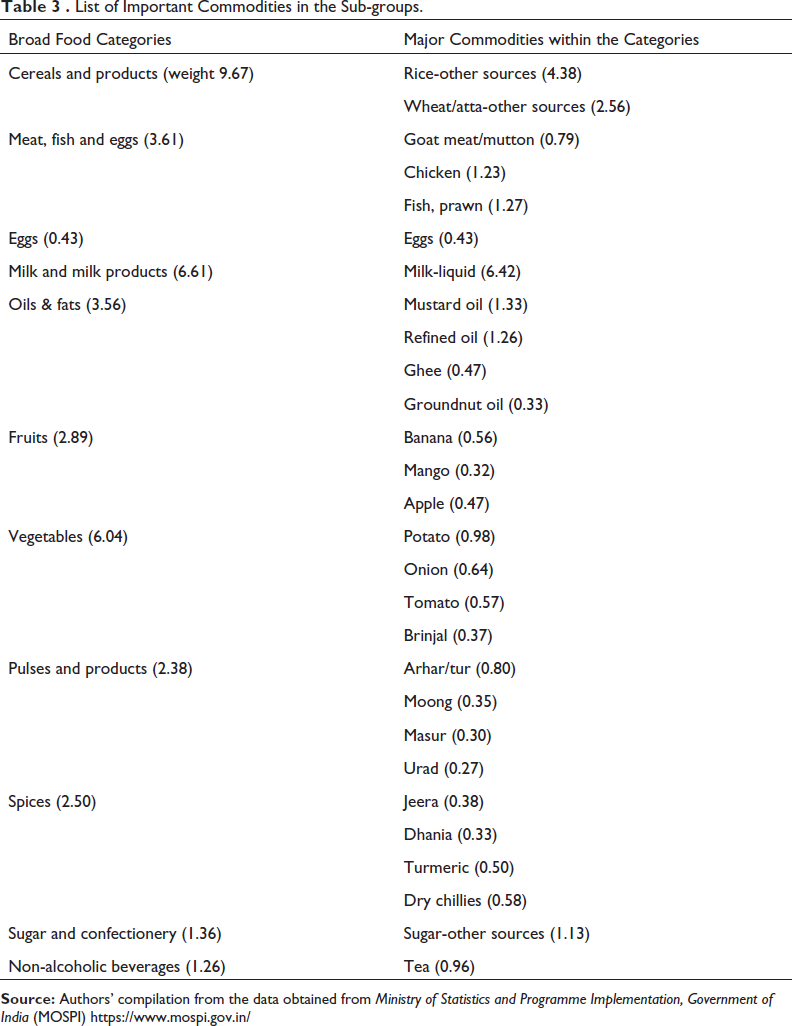

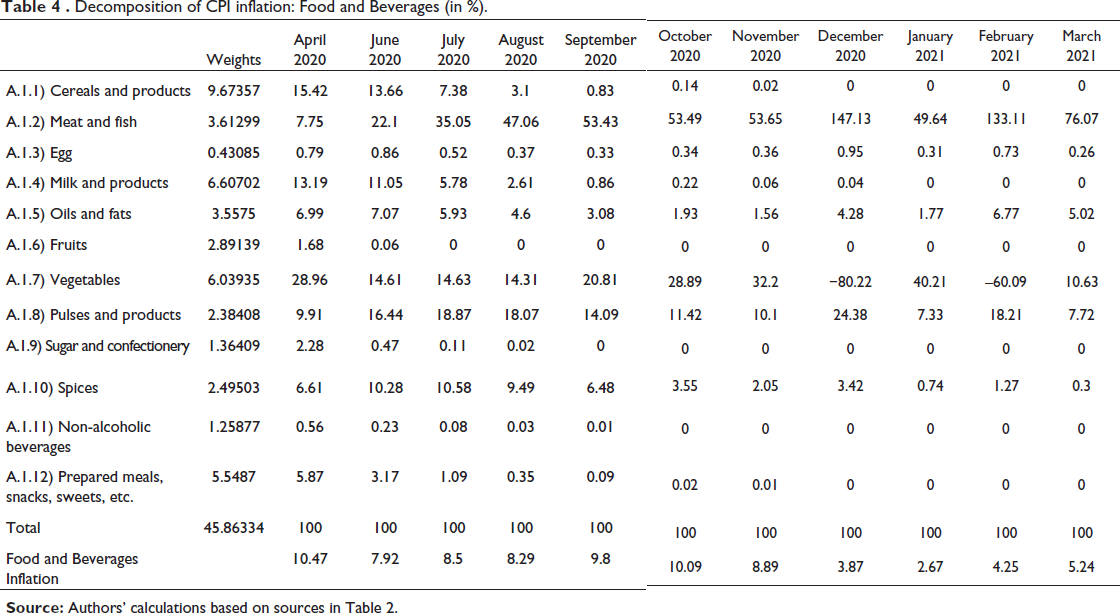

Based on WPI and CPI inflation rates, the following section analyses the trends in food prices after the lockdown from April 2020 to March 2021 (Figure 1). The analysis aims to identify the main sub-groups that experienced higher/lower inflation in 2020–2021 as compared to the reference level (average inflation of 2017–2019). In the next step, to understand which specific commodities have contributed to these observed inflation trends in the sub-groups, CPI inflation of specific commodities that have a major share (Table 3 and Figure 2) in the weight of each sub-group has been examined.

5

Following the lockdown, there was an increase in prices at the wholesale (WPI inflation) as well as at the retail level (CPI inflation) for most of the food commodities during 2020–2021. Also, the rise in retail prices has been much higher than wholesale prices in most of the months for the majority of the commodities (except oils and fats and non-alcoholic beverages). This indicates that the margins in retail trade increased vis-à-vis the wholesale trade possibly due to movement restrictions, which led to localised shortages and an increase in market power of local retail traders.

6

Retailers’ margins also increased for some commodities due to sizable reductions in wholesale prices. These trends show that growth in retailers’ margins took place at the expense of consumers as well as producers. Immediately after the lockdown, wholesale prices of a few commodities showed deceleration, which was pronounced for eggs, fruits and vegetables. This deceleration continued until July 2020, although it continued much longer for fruits. Cereals and Products: CPI inflation of ‘cereals and products’ in 2020–2021 was high from April 2020 to Oct 2020 compared to the reference price. Then it started tapering down and turned negative from Jan 2021. But WPI inflation remained lower throughout 2020–2021. In fact, the WPI inflation rate was negative since August 2020 following the relaxation in lockdown.

List of Important Commodities in the Sub-groups.

These trends indicate that the demand was lower during the initial months possibly due to reduced incomes due to lockdowns and storage of staples by the households. This lowering of demand, coupled with supply gluts due to fresh wheat harvests, has pushed the WPI inflation of this sub-group to lower levels than in 2017–2019. 7 However, the retail prices continued to remain higher because of local shortages due to restrictions on the physical movement of goods and people and also due to panic buying of essential goods, leading to higher prices at the retail level. 8 These trends were moderated to some extent later due to massive procurement by the government of wheat and rice and also the distribution of grains by the government to households through Public Distribution System (PDS) and other special schemes (Pradhan Mantri Garib Kalyan Yojana (PMGKY)). This resulted in a much lower level of prices, as indicated by inflation falling into the negative zone, during the latter part of the study period. These trends are also corroborated by Ceballos et al. (2021) and Varshney et al. (2020), who find that wheat farmers suffered minimal losses as their output prices were guaranteed through state-led wheat procurement at fixed prices. However, this support aggravated existing inequalities and further worsened the vulnerabilities of producers not receiving such support and facing difficulty to access markets, such as tomato farmers, as we shall see later in this section.

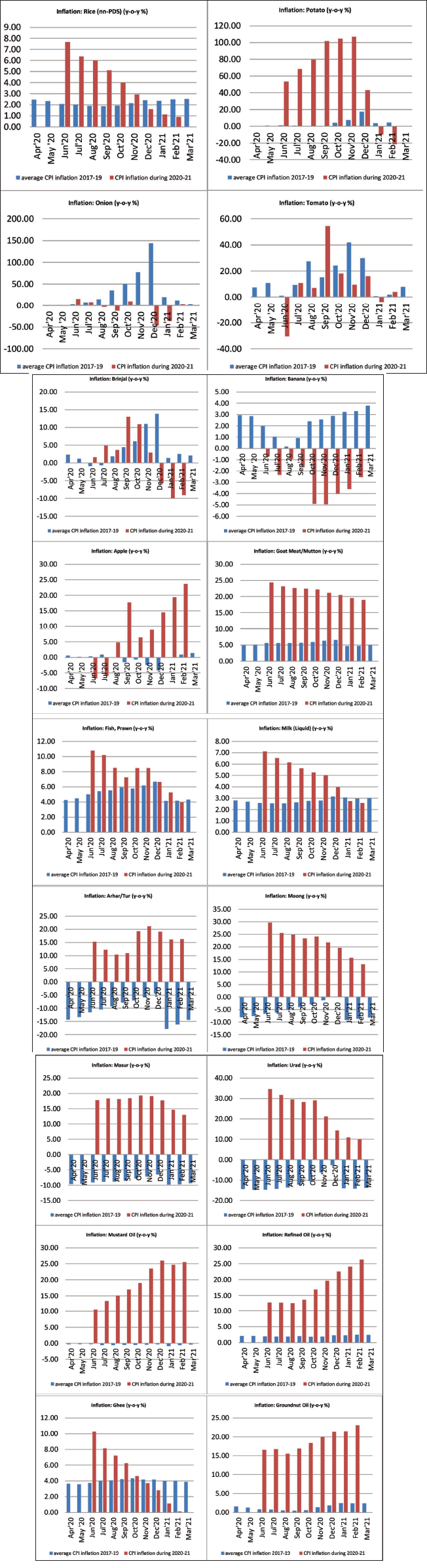

The trend in the CPI inflation of the cereals and products sub-group is mainly driven by the non-PDS rice, which has a weight of 45% in the sub-group. The CPI inflation of rice for 2020–2021 was higher than the reference price from June to November 2020 (it was more than double from June to September). It was only from December 2020 onwards that the CPI inflation of rice (2020–2021) moved below the reference level.

1. Perishables: The prices of perishables showed a mixed trend. The CPI inflation was consistently higher than the reference level. However, there were differences in the behaviour of wholesale prices. Fruits, vegetables and eggs showed a decline in wholesale prices immediately after the lockdown while those of meat/fish and milk and products continued to hold up.

a. The WPI inflation of vegetables fell drastically in the initial months after the lockdown (April, May and June 2020) and remained lower during the period except in July, September and October 2020. On the contrary, the CPI inflation remained higher than the reference level from April 2020 to November 2020. After the complete lifting of the lockdown, the CPI inflation (2020–2021) also showed a declining trend. These trends indicate that there were short-term gluts in the wholesale markets during the strict lockdown from April to June 2020 while there were local shortages in the retail markets at the same time. These led to a steep fall in WPI inflation and a high CPI inflation. The CPI inflation eased after November when most of the movement restrictions were lifted. Ceballos et al. (2021) in a comprehensive study show that tomato producers in the state of Haryana suffered severe losses due to a steep fall in their sale prices, as they were forced to shift from wholesale to local retail markets during the lockdown.

In this sub-group, there are no predominant commodities in terms of weight. Therefore, we have considered four important commodities for detailed analysis – potato, onion, tomato and brinjal. For potatoes, as compared to the reference level, the CPI inflation in 2020–2021 experienced a massive increase in the months following the lockdown period. It varied in the range of 43%–107% from June to December 2020. In fact, the inflation of potato prices in 2020–2021 was over 100% for the consecutive months of September to November 2020, mainly due to a 62% decline in market arrivals in August 2020. Thereafter it experienced a fall due to policy measures by the government and a negative trend ensued for January and February 2021. In the case of onion, contrary to the reference level inflation which was as high as 144%, CPI inflation in 2020–2021 did not witness such an increase. The CPI inflation for 2020–2021 was lower than the reference level for most of the months and it was negative too. The former exceeded the latter only for the month of June and July 2020, mainly because of a decline in market arrivals by 74% in April 2020. In the case of tomatoes, except for the months of July 2020, September 2020 and February 2021, the CPI inflation of tomatoes (2020–2021) was lower than the reference level. The CPI inflation of brinjal in 2020–2021 exceeded the reference level during the initial months of the lockdown from June 2020 to October 2020. Thereafter, from November 2020 to February 2021, it was lower. It was, in fact, negative for December 2020 (−5.68%), January 2021 (−9.94%) and February 2021 (−9.07%).

Thus, the trend in retail prices of important vegetables was broadly similar; an increase during the first few months of the lockdown, which remained elevated in double digits from July to November 2020 and a decline thereafter. The rise in inflation appears to be on account of a decline in the arrival of potatoes and onions during the lean season. In the case of onions, arrivals declined by 74% in April 2020 and in the case of potatoes by 62% in August 2020. However, immediate steps taken by the Government resulted in a steep decline in vegetable inflation in December 2020.

b. Both WPI and CPI inflation of fruits for 2020–2021 remained lower than the reference levels from April to December 2020, showing a decline in demand. The erosion of incomes during the lockdown period may have led to the decline in the prices of fruits, which have a high-income elasticity of demand. The decline in prices (WPI and CPI) continued until December 2020 but prices started firming up in January 2021 when all movement restrictions were lifted.

Bananas, apples and mangoes together have a share of nearly 47% of the total weight of the sub-group. The data on mango prices was available for only a few months. Thus, we could only analyse the data on bananas and apples. Banana has the highest weight and its CPI inflation in 2020–2021 remained negative compared to the reference level throughout the period of study. The CPI inflation 2020–2021 apple was lower than the reference level in the months of June and July 2020 and was even negative during those months. However, in the subsequent months, it showed a sharp increase and varied in the range of 5% to 24%.

c. The CPI inflation of eggs has remained consistently higher than the reference level, showing that there were persistent local shortages in supply. However, wholesale prices showed a decline immediately after the lockdown similar to fruits and vegetables. WPI inflation 2020–2021 was negative during the period of strict lockdowns from April to July 2020 compared to the reference level. It started increasing thereafter and remained higher. The CPI inflation of (2020–2021) was much higher compared to the reference level. The increase was very steep from September to December 2020 when inflation was almost seven times the reference level.

The price of meat and fish, particularly CPI inflation (2020–2021), was higher than the reference level throughout the period under study. WPI inflation 2020–2021 was also higher than the reference level but only during the initial months of strict lockdowns from April to August 2020, after which it registered a fall. These trends indicate that the supply shortages at the wholesale and retail level during the period of strict lockdowns were the possible reasons for higher inflation, as demand was largely muted because of income shocks. Further, CPI inflation in 2020–2021 was relatively higher than WPI inflation in 2020–2021 showing higher margins for retailers vis-à-vis the wholesalers.

The trend in the CPI inflation of this sub-group is mainly due to three commodities—mutton, chicken and fish/prawn—which together have about 90% of the total weight of this sub-group. The CPI inflation of mutton for 2020–2021 remained almost four times higher than the reference level throughout the period under study—ranging from 19% to 24%. A marked increase in the CPI inflation rate (2020–2021) of chicken is observed compared to the reference level in the months following the lockdown. It varied in the range of 16% to 31%. For fish/prawns, CPI inflation 2020–2021 was higher than the reference level for a major part of the study period except for December 2020 and February 2021 when there was only a slight difference between the two indicators.

For milk and milk products, in the initial months following the lockdown (April to November 2020), both WPI and CPI inflation 2020–2021 was higher than the reference level, showing possible supply shortages at the wholesale as well as retail levels. Thereafter, particularly from January to March 2021, the price rise for 2020–2021 (both WPI and CPI inflation) was slightly lower than the reference level.

The CPI inflation of this sub-group is almost entirely driven by liquid milk which has about 97% of the total weight. The CPI inflation of milk (2020–2021) was found to be tapering off over the months. It was higher than the reference level for the months of June to December 2020 and it was lower from January to February 2021.

2. Two sub-groups—pulses and products and oils and fats have not shown any decline in wholesale prices even in the months immediately following the lockdown. The prices of these sub-groups (both WPI and CPI 2020–2021) have remained quite high relative to their reference levels. 9 In April 2020, there was a sudden spike in the prices of pulses to 22.8% possibly due to movement restrictions and also stocking of pulses by households. The price rise of pulses and oils could also be due to major dependence on imports as restrictions on international trade in many countries during the pandemic led to a firming up of international prices of these commodities. The CPI inflation was much higher than the WPI inflation for pulses and products but in the case of oils, the trend is reversed. It is worth highlighting that for pulses, the inflation (WPI and CPI) during 2017–2019 was in the negative zone but it shot up in 2020–2021 to a very high level immediately after the lockdowns. We try to explore below the price trends of major commodities in each sub-group.

a. Pulses and products: CPI inflation of this sub-group is driven by major pulses—arhar, masur, urad and moong—which together have a share of about 72% in total weight. The CPI inflation of arhar witnessed a sharp increase in 2020–2021 as compared to the reference level in the months after the lockdown. As opposed to the negative inflation of 2017–2019, arhar/tur dal experienced CPI inflation in 2020–2021 in the range of 10% to 21% during the study period. The trend was the same for moong dal, wherein CPI inflation in 2020–2021 hovered in the range of 13%–30%. Similarly, for masur (lentils), CPI inflation during 2020–2021 was consistently higher than the reference level in the months following the lockdown. While the former varied in the range of 13%–19%, the latter experienced a negative trend. The trend was no different for urad. While inflation in 2017–2019 had a negative trend, the CPI inflation in 2020–2021 experienced a sharp increase varying in the range of 10% to 35%. The spike in prices of masur and urad could be due to lowered production. Although the production of total pulses increased in 2019–2020 and 2020–2021, the production of urad and lentils declined in 2019–2020 compared to the previous year. Also, the supply bottlenecks in international markets resulted in the tightening of imports in 2020–2021, leading to a decline of 15% in the quantum of pulse imports and an increase in landed price by 37% compared to the previous year as per the Directorate General of Commercial Intelligence and Statistics (DGCIS) data.

b. Oils and fats: The CPI inflation in this sub-group is mainly determined by the trends of four commodities—mustard oil; refined oil (includes soybean oil, sunflower oil and saffola, etc); ghee and groundnut oil—which together have a share of 95% of the total weight. While the reference level inflation for mustard oil was negative, the CPI inflation in 2020–2021 varied in the range of 11%–26%. The story was no different for refined oil. The reference level inflation varied in the range of 2%–3% whereas the CPI inflation 2020–2021 varied between 13% and 26% for the consecutive months from June 2020 to February 2021. Though the CPI inflation 2020–2021 of ghee was tapering off over the months, it remained much higher than the reference level from June to October 2020. The CPI inflation of groundnut oil in 2020–2021 varied in the range of 16%–23% while the reference level inflation was in the range of 0.47%–2.44%.

India is the largest importer of edible oils and more than 60% of the domestic consumption requirements are met through imports. Demand for edible oils is rising while domestic production is almost stagnant. Imports in 2020 were affected as Malaysia and Indonesia imposed export tariffs on crude palm oil, which affected domestic prices of palm oil from January to June 2020. There was also a large spike in international prices with inflation using the Food and Agriculture Organization (FAO) oil price index rising to 32% for nine months, from June 2020 to March 2021. This spike was particularly severe from January 2021 to March 2021 when the inflation touched 53% on average. With India’s large dependence on edible oil imports, this massive increase in world prices was reflected in domestic prices too.

Another important factor is the shortfall in domestic production in recent years. Although production of total oilseeds is estimated to have increased in 2019–2020 and 2020–2021, production of soybean and mustard declined significantly in 2019–2020. The production of sunflowers has been declining continuously over the years except in 2019–2020.

In conclusion, it is evident that the retail prices of a majority of food items have consistently increased following the lockdown. Further, CPI inflation was higher than WPI inflation. These trends point towards the presence of local supply bottlenecks particularly in the food retail chain. The pre-existing bottlenecks seemed to have been exacerbated following the lockdown. Commodities such as food grains, which benefitted from the significant intervention of the government either in the form of procurement or food distribution, seem to have experienced moderate inflation. Milk and products, which are perishable but are processed and marketed mostly through organised private traders or milk cooperatives like Amul, have managed to avoid the slump in wholesale prices. This is in contrast to other perishable commodities like fruits and vegetables and eggs which involve little processing and are marketed mainly through informal channels and petty traders.

Relative Contribution of Different Sub-groups to Consumer Food Inflation

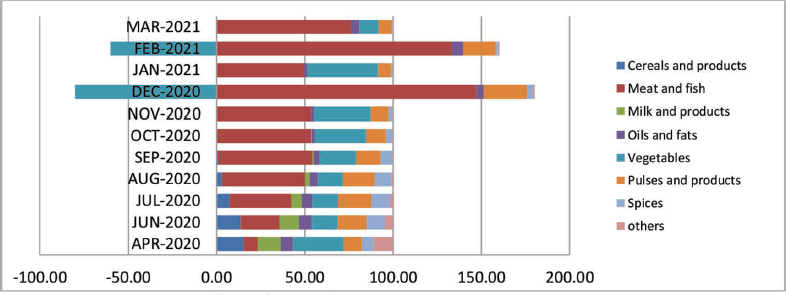

The CPI inflation of food and beverages remained in the range of 8%–10% from June to November 2020. The contribution of various commodity sub-groups to food inflation is summarised in Table 4 and Figure 3. Nearly 82% of the food inflation during 2020–2021 was on account of three commodity groups—meat and fish; pulses and products and vegetables (Table 4). Meat and fish alone had a share of about 62% followed by pulses and products (14%) and vegetables (6%). Spices (5%); milk and products (4%); cereals and products (4%) and milk and products (3%) contributed the rest. The share of meat and fish was relatively low at the start of the year (8% in April 2020) but increased very rapidly (Figure 3). The share of cereals and products, which was relatively high at the start of the year at 15%, fell rapidly and reached less than 1% by September 2020, indicating the effectiveness of procurement and distribution programs. A similar trend can be seen in milk and products, indicating the effect of a reduction in movement restrictions. Prices of vegetables fluctuated widely as reflected in their share, indicating the perishability of the product and lack of processing and organised marketing. The share of pulses was high and more or less steady, except in January and March 2021, when it dipped slightly.

Decomposition of CPI inflation: Food and Beverages (in %).

In some months, contributions of different commodity groups offset one another. For example, in December 2020 and February 2021, a very steep rise in the prices of meat and fish seemed to have been offset by a sharp decline in the prices of vegetables, leading to a fall in overall food inflation during those months.

Conclusions

The lockdowns had a differential impact on the supply and prices of different food commodities due to various factors which include government support; perishability (of the product); organised marketing; processing; and international prices. The retail margins were consistently higher in 2020–2021 showing that local shortages were persistent. The effect on prices of commodities such as cereals was minimal because of active government support in the form of procurement and distribution. Perishable commodities like vegetables, which are mostly marketed in raw form through informal and petty trade networks, faced the maximum price movements. On the other hand, milk which is marketed in processed form by organised intermediaries like milk cooperatives and private traders experienced a moderate movement in prices. Fruits, which are also perishable but have a high-income elasticity of demand, have seen muted prices in 2020–2021 because of the erosion of incomes owing to the pandemic. Meat and fish showed higher inflation due to the supply shortages at the wholesale as well as the retail level during the period of strict lockdowns, although the demand was largely muted due to income shocks. Finally, pulses and products and oils and fats, which are imported in large quantum every year, have seen a sharp increase in prices possibly due to the disruption of international trade.

The following broad policy implications can be drawn from the study. The findings point to the importance of the role of government intervention in procurement and distribution which helped maintain price stability in food grains during COVID-19-induced uncertainty. Stabilising the incomes of producers of perishable commodities such as vegetables, meat and fish, which are marketed mostly through informal networks, needs special attention. The development of efficient infrastructural facilities in the form of cold chain and logistics could be one option. Minimising dependence on imports for pulses and edible oils could help in moderating domestic price volatility. On the demand side, strengthening the existing social safety nets and developing new ones could aid the recovery process of vulnerable populations.

Footnotes

Disclosure Statement

The authors report there are no competing interests to declare.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.