Abstract

Based on a household survey of 210 borrowing households from the state of Tamil Nadu, India, we investigate the extent and determinants of over-indebtedness among microfinance borrowers. Our analysis based on logistic regression framework using three distinct measures of over-indebtedness shows that the extent of over-indebtedness among the borrowing households is relatively widespread. As regards the determinants, apart from the demographic factors, external and lender-related factors contribute more towards over-indebtedness rather than borrower-related factors. Within the lender-related factors informal sources of credit exert a much stronger influence on over-indebtedness than formal sources which includes microfinance. The above findings imply that the policy environment should facilitate easier access to formal sources such as microfinance, along with provision of social security schemes with a minimum guaranteed income and insurance coverage.

Introduction

Experiments of lending to the poor without collateral through a unique set of mechanisms such as group lending, lending to women borrowers, frequent repayment schedules, etc., commonly characterised as microfinance, had reported some encouraging outcomes towards the end of the last century (D’ Espallier et al., 2011; Pitt & Khandker, 1998). This has resulted in the widespread adoption of the practice globally as a promising tool for poverty alleviation. Thus, by the end of the year 2013, the total number of borrowers reached out by microfinance institutions (MFI) has grown to approximately 211 million, out of which 114 million are living in extreme poverty . This reported growth is amply aided by the ability of the unique mechanisms of microfinance to solve information asymmetry problems between lender and borrower without the help of collateral (Besley & Coate, 1995; Ghatak & Guinnane, 1999; Ghatak, 2000) apart from policy and institutional support. However, alongside its popularity, fissures also have started appearing of late, on the consensus of the beneficial effects of microfinance (Banerjee et al., 2015; Roodman & Morduch, 2014).

While the debate remains inconclusive, sporadic incidents of repayment crises were reported from many of its fast-growing and important markets. The revolt of microfinance debtors of Bolivia in 2001, the crisis in Nicaragua in the year 2008, Bosnia and Herzegovina in 2009 and Andhra Pradesh (India) in 2010 are some of the examples of the crises the industry witnessed in the past. Many studies, analysing the crises in their aftermath, have alluded to the possibility of a typical microfinance borrower being over-indebted as one of the main antecedents for the crisis (Mader, 2013; Pytkowska & Spannuth, 2011). Some common observations associated with the crises such as general erosion of lending discipline, same borrowers being targeted by multiple lenders, fast expansion of area of operation as well as lending portfolio and too many borrowers taking in high levels of credit also point to the prospects of a borrower over-indebtedness (Chen et al., 2010).

It is tempting to overlook the issue, given the fact that historically most microfinance programmes have reported enviable repayment rates (Ahlin & Townsend, 2007; Sharma & Zeller, 1996). However, such high reported repayment rates are incapable of reflecting the weak household finances of the borrowers at the time of repayment. Evidence available early on points to the fact that necessity to maintain access to sources of credit as well as the need to avoid social humiliation can act as powerful incentives to maintain repayments even under adverse conditions (Montgomery, 1996; Rahman, 1999). Therefore, in the specific context of microfinance, maintaining repayments under adverse or even deteriorating household financial conditions of the borrower can be treated as a situation of over-indebtedness (Khandker et al., 2014; Shambhavi & Mohan, 2016).

In spite of its importance, the current microfinance literature has not addressed adequately the possibility and consequences of a borrower being over-indebted. Therefore, our aim is to ascertain the extent of over-indebtedness among microfinance borrowers and identify its determinants. We perform the analysis by classifying the borrowers under various categories of over-indebtedness, ranging from not over-indebted to heavily over-indebted. Household financial ratios of repayment to income, borrowing to assets and borrowing to annual income form the basis for classification. We use primary data collected from 210 borrower households from Madurai and Coimbatore districts in the state of Tamil Nadu in India, the second largest microfinance market. Our findings point to fairly widespread incidents of borrower over-indebtedness. Factors that drive over-indebtedness include adverse economic shocks, uncertain income, number of formal and informal sources of credit, apart from demographic factors.

The remainder of this paper is organised as follows. Section II deals with the theoretical background. Section III deals with methodology, sample and data. Section IV contains the empirical results and analysis, followed by conclusions and policy implications in Section V.

Theoretical Background

Concept of Over-indebtedness

The concept of over-indebtedness is complex and multi-dimensional, making it highly challenging to define. It has a negative connotation, implying that the borrower has taken too much debt making him or her worse off. But, minor difficulties in paying off a loan, or even major difficulties faced during a short period of time cannot be considered a situation of over-indebtedness, giving the concept both temporal and spatial dimensions. In short, it is difficult to find a universally acceptable objective answer to the question ‘how much is too much’ in the context of indebtedness. So, various measures are used in various contexts to study the phenomena, and all the measures have their own advantages and shortcomings (Hanna et al., 2012; Gutierrez-Nieto et al., 2017).

Since the debate on over-indebtedness of microfinance borrowers is relatively new, widely accepted measures to represent it are yet to evolve. But, it has seen wide investigation in the context of consumer finance markets of the United States and European countries (Dickerson, 2008; Rowlinson & Kempson, 1994). Such studies use measures such as debt-to-asset ratio, borrowing-to-income ratio, repayment-to-income ratio, etc., to represent over-indebtedness (Betti et al., 2007; Disney et al., 2010). Some studies also use borrower defaults as a variable representing over-indebtedness. Haas (2006) defines over-indebtedness as the inability of borrowers ‘to repay all debts fully and on time’. Based on a review of how the concept has been dealt with in the context of consumer finance, Betti et al. (2007) identify different measures being used for representing over-indebtedness.

As is evident from the foregoing discussion, it is extremely challenging to identify an objective measure to represent the concept of over-indebtedness. Early studies dealing with over-indebtedness in microfinance have attempted to address this challenge by viewing the concept in its different dimensions as mentioned above. Inability to meet total repayment obligations arising from all sources of debt contracted by a particular household at a point of time (Pytkowska & Spannuth, 2011), facing serious problems as perceived by the borrowers in repaying their loans (Shicks & Rosenberg, 2011), using thresholds of ratios constructed from parameters of household finances such as income to repayment, asset to borrowing, etc. (Khandker et al., 2014) are some of the ways in which previous studies have tried to address the challenge.

Determinants of Over-indebtedness: Variables and Hypotheses

We now turn our attention to how the past literature has dealt with the antecedents of over-indebtedness and draw our hypotheses accordingly. Based on a survey of evidence, Schicks and Rosenberg (2011) have classified three major factors influencing over-indebtedness, namely, environmental factors, borrower-related factors and lender-related factors.

External Factors

Adverse economic shocks and income uncertainty constitute the variables forming part of external factors (Disney et al. 2008; Khandker et al. 2014; Stone & Maury, 2006). Adverse economic shocks take the nature of both income and expenditure shocks. Income uncertainty can take many forms such as sudden unexpected dip in income due to illness, accident, business failure, bereavement, etc. Holding income constant, families can experience expenditure shocks in the nature of treatment for illness, accident, loss from natural calamities, etc. This variable is captured dichotomously by asking the respondent households whether they have experienced any such expenditure or income shocks in the immediately preceding one-year period prior to the date of the survey.

Income uncertainty is another factor affecting the finances of the household. If all the income earners of the households belong to the category of casual labourers in urban and semi-urban areas and agricultural labourers in rural areas, then the variable is dichotomously captured as one, otherwise zero.

Therefore, hypotheses forming part of external factors can be stated as:

H1a: Borrower households who have faced adverse economic shocks will be more likely to be over-indebted.

H1b: Borrower households facing uncertain incomes will be more likely to be over-indebted.

Borrower-related Factors (Demand Side)

Many past studies have emphasised the role of borrower-related factors contributing to over-indebtedness (D’ Espallier et al., 2011; Mullainathan & Shafir, 2013; Schicks, 2013). ‘Value of household assets’ is a variable considered here which does not include consumer durables . The other household assets, mostly in the form of house property and jewellery, are captured as approximate market value at the time of the survey. ‘Planned lump-sum non-discretionary expenses (PLNE)’ are captured as such expenses incurred by the households during the immediately preceding 12 months period prior to the date of survey. Aggregate of daily, weekly or monthly wages, salaries or income from other sources earned by all the members of the household captured on monthly basis for ease of recall and extrapolated for the year goes for the recognition of Household income. Essential expenses for maintaining the household such as food, house rentals, energy, clothing, children’s education, etc., are included in ‘Annual household living expenses’.

Thus, the hypotheses for borrower-related factors may be stated as:

H2a: Borrower households with higher asset ownership are more likely to be over-indebted.

H2b: Borrower households with higher incomes are less likely to be over-indebted.

H2c: Borrower households with higher PLNE are more likely to be over-indebted.

H2d: Borrower households with higher household living expenses are more likely to be over-indebted.

Lender-related Factors (Supply Side)

Complex nature of credit markets facing the poor renders it impractical to quantify the structure and conduct of the market. However, the number and type of players occupying the market and the nature of competition among them will ultimately reflect in the number of credit sources facing the borrowers and the ease with which borrowers are able to access these sources. Given the credit constraints faced by the poor, higher supply will translate into higher utilisation, which in turn will reflect in the number of sources accessed by the borrowers (Ghate, 2007; Krishnaswamy, 2007; Vogelgesang, 2003). This can be further classified into the number of formal sources of loans as well as number of informal sources of loans accessed by the borrower.

Hence, the hypotheses for lender-related factors can be stated as:

H3a: Borrower households with more number of loans from formal sources will be more likely to be over-indebted.

H3b: Borrower households with more number of loans from informal sources will be more likely to be over-indebted.

Demographic factors: Household size, age of the household head, literacy levels, occupation and ratio of dependant members are the demographic factors considered in the study. Size is measured by the number of people who permanently stay together in the household. Educational attainment of the household head is measured using three ordinal levels consisting of completion of primary and below, completion of secondary and completion of higher secondary and above. Occupational profile is categorised based on the occupation of the chief wage earner of the family and has three nominal categories consisting of casual labourers as one, salaried employees as two and business or self-employed as three. Gender of the household head is not considered here as most of the sample households have male heads.

H4a: Borrower households of larger size will be more likely to be over-indebted.

H4b: Borrower households with a higher educational attainment for the head will be less likely to be over-indebted.

H4c: Borrower households with an older head will be less likely to be over-indebted.

H4d: Borrower households with larger dependents ratio will be more likely to be over-indebted.

Sample and Data

Sample and Data

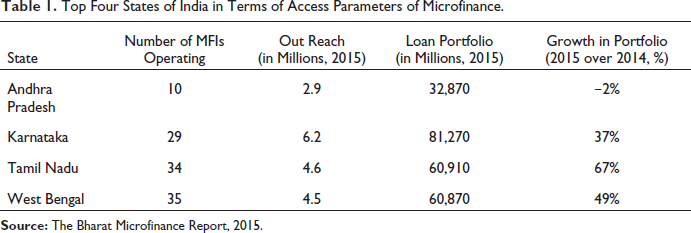

The main research questions are addressed through a unique data set collected using a household survey among microfinance borrowing households in the state of Tamil Nadu during the year 2015. Households who are borrowers from any MFIs for past three years or more prior to the date of survey only have been included as respondents. The sampling technique used was simple random sampling and the samples were drawn from two districts which recorded rapid growth in terms of the number of borrowers and portfolio size in the south Indian state of Tamil Nadu. The choice of the study area can be justified by the fact that South India recorded the fastest growth for the microfinance industry in the Indian sub-continent (Sa-Dhan, 2015), and within Southern India, Tamil Nadu recorded the highest portfolio growth in the recent past (Table 1). Also, the selection of respondents from urban and semi-urban areas was done keeping in view the shifting focus of Indian microfinance towards more semi-urban and urban markets from its earlier focus on rural areas. Sa-dhan, the largest and oldest association of community development finance institutions in India, confirms that by the end of the financial year 2015, 67% of the 37 million microfinance borrowers in India live in urban areas.

Top Four States of India in Terms of Access Parameters of Microfinance.

Top Four States of India in Terms of Access Parameters of Microfinance.

As per the CRISIL (a premier rating agency in the country) inclusive score in 2013, Coimbatore and Madurai, the two districts from where sample respondents are drawn, feature among the top 50 districts in the country with a score of 100 and 89.2 each in terms of financial inclusion.

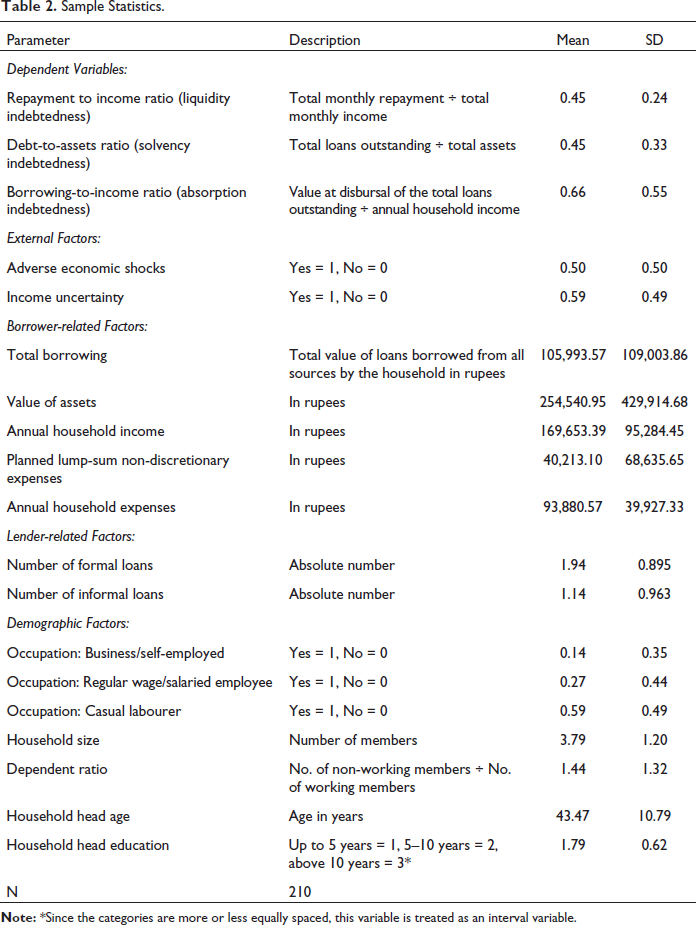

Descriptive Statistics

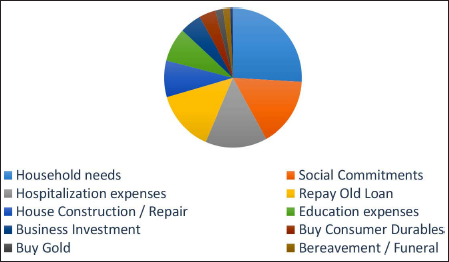

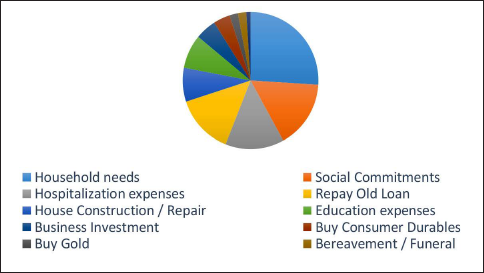

Table 2 shows the descriptive statistics of the variables considered in the study. Total borrowings by each household as at the date of survey has an average of ₹1.06 lakhs and a standard deviation of 1.09 lakhs. The distribution of these loans both by number and percentage of value is given in Figures 1 and 2, respectively. The sources of loans include loans from MFI, gold loans, money lenders, friends and relatives (MLFR) and other formal and informal sources such as banks, cooperative banks and chit fund loans, which are broadly categorised into formal and informal loans for the purposes of analysis.

Sample Statistics.

Distribution of Loans by End Use (Number).

Distribution of Loans by End Use (Percentage of Value).

Further, repayment to income ratio with a mean of 0.45 indicates that on an average, a representative borrower household spends 45% of monthly income on loan repayment commitments. Debt-to-asset ratio representing the level of solvency of the household has an average 0.45 and a standard deviation of 0.33. The high variability of this measure reflects the variability of asset holdings of the borrowing household. For borrowers staying in own houses, the value of the self-occupied house accounts for a major share of the asset holding, whereas this will be absent for those staying in rented accommodations. Families who have migrated from rural areas in search of job opportunities in towns account for most of the borrowers staying for rent and their low asset holding explains the relatively high level and variability of debt-to-asset ratio. Borrowing-to-income ratio shows the average debt level of about 66% of the annual income of the borrowers.

Incidence of income or expenditure shocks seems to be fairly widespread with around 50% of the sample households reporting to have faced some such shocks at least once during the preceding 12 months of the survey. Prevalence of income uncertainty, which is at a fairly high level of 59%, is also consistent with this observation, since uncertain incomes can also contribute to economic shocks. The occupational profile of sample respondents, where 59% of the respondents are casual labourers, lends credence to both the above observations.

The observed figure of annual income of approximately ₹1.70 lakhs per annum is almost equivalent to ₹15,000 per month, which translates to rupees 500 per day for each household on an average. This observation is consistent with wage levels for urban workers observed in the contemporary national sample surveys of urban households. The high volatility exhibited by the value of asset holding is reflected in the high variations in the debt-to-asset ratio. PLNE of approximately ₹40,000 is in line with the annual income of the borrower households. Annual household recurring expenses of approximately ₹1.63 lakhs are below the annual income of ₹1.70 lakhs, but indicate the small surplus available for the households after necessary household expenditures are met. This is indicative of the situation of scarcity discussed in Guérin et al. (2014) and Mullainathan and Shafir (2013).

Lender-related factors show that an average borrower has equal access to both formal and informal loan markets which is indicative of the competitive nature of the markets. The number of informal loans accessed by the borrower being marginally higher than the number of informal loans accessed shows the ease with which the borrower can access the informal sources.

Head of a typical borrower household has an average age of less than 45. The average educational attainment of the head is between primary and secondary levels, with very few completing the secondary levels. Fifty-nine per cent of the sample households have their heads working as casual labourers with mean income uncertainty accounting for 0.59. This is also indicative of the household head being the main wage earner of the household in most cases. The chances of a household head being a stable income earner or a salaried employee are only 29%.

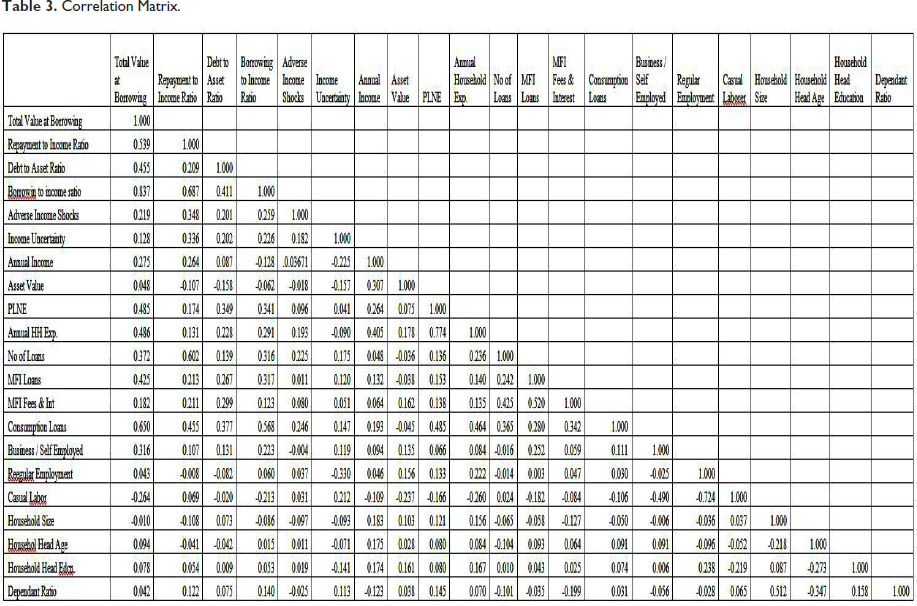

The correlation matrix of the variables given above is presented in Table 3. It can be noted from the table that none of the explanatory variables are showing a significant correlation between themselves, signifying a lack of multi-collinearity.

Correlation Matrix.

Extent of Over-indebtedness

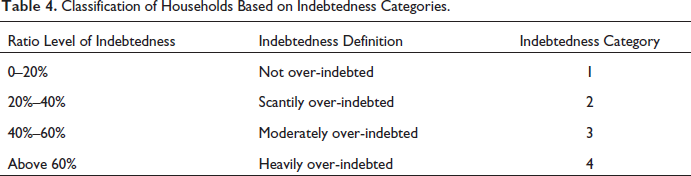

As discussed above, we propose to use income- as well as asset-based measures to proxy the level of over-indebtedness. Specifically, we use three measures to represent the liquidity situation of the household, the debt absorption capacity and the solvency level of the household. The financial ratios used to represent the measures are monthly loan repayment to monthly income of the household, total borrowings to annual income of the household and total outstanding borrowings to total assets of the household. The monthly repayment to monthly income ratio is the standard debt-to-income ratio. This ratio may be incapable of representing the real state of indebtedness of microfinance borrowers since they resort to borrowing from many informal sources also. Such sources may or may not insist on structured repayment schedules. Hence, we include two more measures which take into account the total borrowings of the household from all sources. The measures we use to identify over-indebtedness and its descriptions are given in Table 4.

Classification of Households Based on Indebtedness Categories.

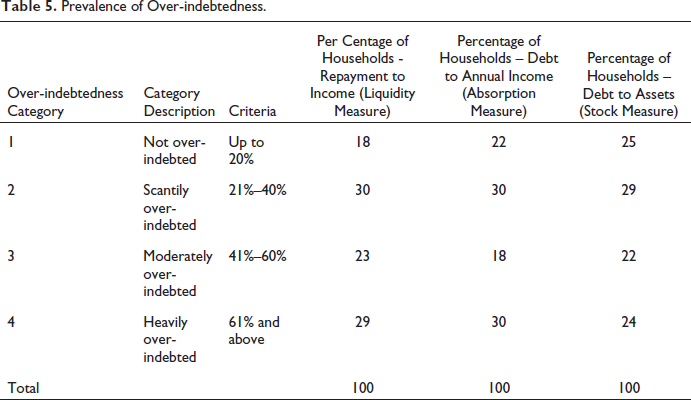

Table 5 exhibits the extent of over-indebtedness among the sample borrowers.

Prevalence of Over-indebtedness.

Percentages in the table represent the proportion of households that fall into a respective category of over-indebtedness as measured by the given criteria in Table 4. Fifty-two per cent of the borrower households fall in the category of moderately and heavily indebted as per the liquidity over-indebtedness measure. Comparable figures for absorption and stock measures are 48% and 46%.

Among all the three measures, the ratios are more or less consistent across all three measures, which confirms the level of over-indebtedness among the borrowing community by different yardsticks. These figures are indicative of the fact that over-indebtedness among microfinance borrowers is arguably widespread, which requires serious attention.

Since the primary aim of the study is to identify the determinants of over-indebtedness by classifying the microfinance borrowers into various categories of indebtedness, the dependent variable we use is categorical in nature as mentioned in Table 4. We, therefore, use the multinomial logit regression technique. Since the over-indebtedness categories defined as above have a natural order to them, ranging from not over-indebted to highly over-indebted, we use the ordinal variant of multinomial logit regression (Agresti, 2010; Norusis, 2012). Specifically ordinal regression is used for ascertaining the odds related to each of the households to fall into a higher category of over-indebtedness based on the explanatory factors.

Thus, specifically for over-indebtedness, the estimation model is:

where: Y is a measure representing the level of indebtedness; j denotes indebtedness categories which can take values of 1, 2, 3 and 4; and ‘x’, ‘m’, ‘n’ and ‘p’ are external, borrower-related, lender-related and demographic factors pertaining to borrower household ‘i’.

Results of ordinal regressions using three different measures of over-indebtedness are presented in Table 6.

Results of Ordered Logit Regression on Over-indebtedness (Log Odds).

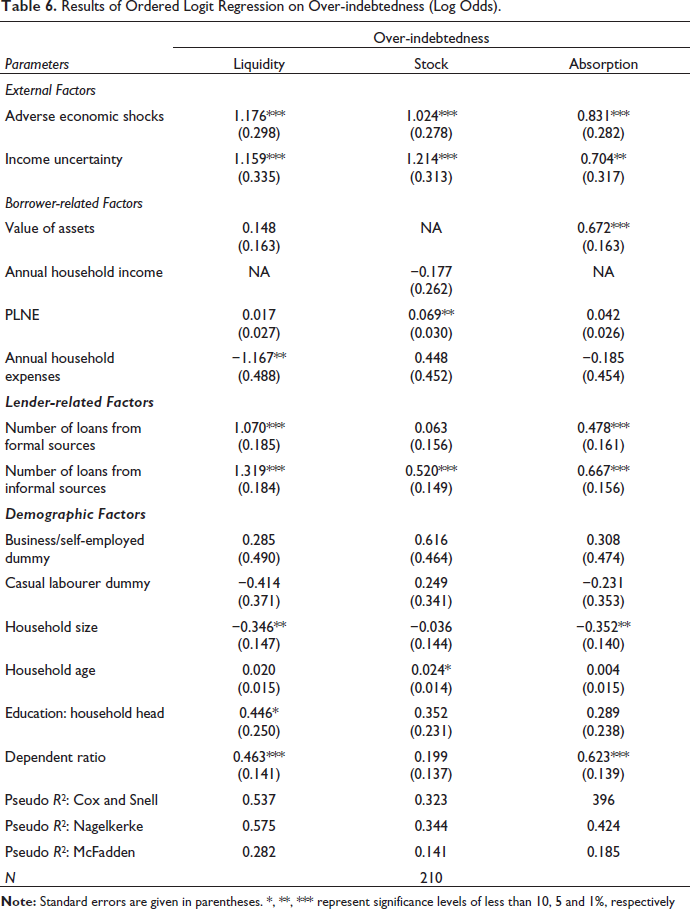

Coefficients of income uncertainty and adverse economic shocks are significant for all three regressions, at less than 5% levels of significance, showing the importance of environmental factors. This finding is well in line with the previously observed evidence in Stone and Maury (2006), Disney et al. (2008) and Khandker et al. (2014).

Among borrower-related factors, the value of assets is highly significant in absorption over-indebtedness. But it is not so for liquidity and stock over-indebtedness. Another variable which shows significance in the borrower-related factors is PLNE in stock over-indebtedness, sign and significance of which is in hypothesised lines. A third variable which shows significance in borrower-related factors is annual household expenses. Negative sign of the variable here may be indicative of the possibility that over-indebted households are cutting down their expenses, which is in line with the observation in Schicks (2013).

On the lender-related factors, both variables show significance at less than 5% levels. Between them, the number of loans contracted from informal sources shows a relatively stronger influence than the number of loans contracted from formal sources in all three regressions. This is significant at less than 1% level across all regressions. Its coefficient of 1.319 in liquidity over-indebtedness implies that one more source of informal loan added to the borrowing portfolio of the household increases the odds of the household moving to a higher category of over-indebtedness by a factor of 3.74 times. For absorption and stock over-indebtedness, the odds are increased by factors of 1.95 and 1.68, respectively. It can also be observed from the sample statistics (Table 2) that the average number of informal loan sources accessed by a borrowing household is comparatively lower at 1.14 as against 1.94 for formal loans. This may be clearly indicative of the inadequacy of the formal sources in meeting the demands of the households, and thus exposing them to higher risks of over-indebtedness.

Demographic factors of the borrower households which show significance is the dependency ratio across two measures of over-indebtedness. Sign of the variable is in expected lines. Household size is significant at 5% levels across two measures. Its negative significance may be indicative of the presence of more earning members in larger households. Education of the household head is positively significant at 10% levels in the liquidity measure of indebtedness. Since the average education of the household head is less than ten years, this relationship may not be indicative of the impacts higher levels of education can have on over-indebtedness.

Across the world, all microfinance markets which had undergone crises had reported high repayment rates, till the crisis had erupted. There is a possibility that such high repayments are brought about by worsening household finances of the borrowing households while keeping the repayment current. Findings from our study confirm this reality in two aspects. First, a sizeable proportion of the borrowers are facing high repayment obligations in relation to their ability to service the same. Second, and more importantly, reinforcing the previous finding, borrowings driven by external factors as well as lender-related factors rank high among drivers of over-indebtedness. The key differentiating factor in our study is the significance observed in lender-related factors. Within lender-related factors also, the relatively higher influence of informal sources, representing mainly money lenders, is indicative of the dependence of the poorer households on them. Considering the fact that the state of Tamil Nadu has the third highest financial inclusion score at the end of 2013 (79.2 out of 100, against the national average of 50.1), our results show the ground yet to be covered by formal financial sector in reaching out to the poor and marginalised.

The significance observed in environmental and institutional factors is also in line with the dynamics observed in the run-up to the crises in different microfinance markets (Chen et al., 2010; Khandker et al., 2014; Schicks, 2013). Hence, the above findings imply that the policy environment should facilitate easier access to formal sources such as microfinance, along with the provision of social security schemes providing income and insurance.

One limitation of the study is the small sample size. However, the selection of sample households was carried out with ample care, who would well represent the borrower category. Adding similar households would only have increased the sample size, without any material change in the study findings.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.