Abstract

This article has set out to understand why a large number of public–private partnership (PPP) projects delayed stalled and terminated in the largest PPP program in India. Based on quantitative and case-study-based qualitative research, this study finds that the incomplete nature of PPP contracts, uncertainty and information asymmetry leads to adverse selection, moral hazard, opportunism and holdup of the PPP projects. The inefficacious and inequitable allocation of risks among stakeholders and lack of contract management skills in project authorities exaggerated the problems, and the final outcome is a large number of failed projects and no participation from private developers in future projects defeating the very purpose of adopting the PPP model to build public infrastructure. This study proposes a 20-point conceptual institutional framework suggesting policy and project-level measures for effective execution of the future PPP program in India and developing countries with similar socioeconomic environment post-COVID-19 pandemic amid recessionary conditions.

Keywords

Introduction

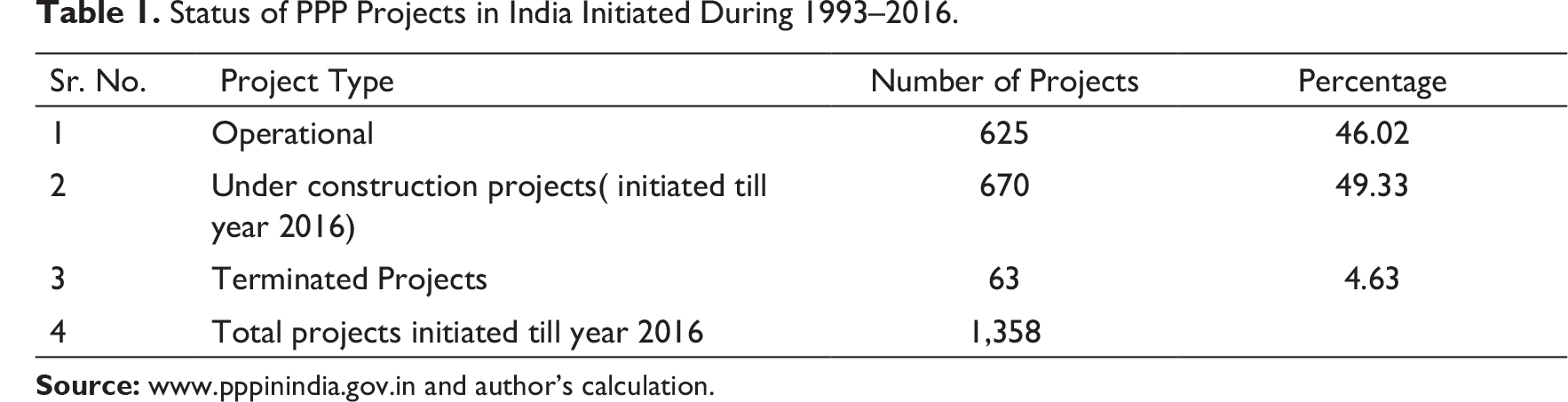

The public–private partnership (PPP) in infrastructure is an innovative structure to build public infrastructure with collaborative efforts from the government project authority and the private developers. A PPP concession is a contract of long duration (20–40 years), which defines all the aspects of partnership such as ownership, responsibilities, risk allocation and contract management. A right is conferred upon the private developer through a contract to design, finance, construct and operate public infrastructure asset. The basic idea is to give incentive to private developers and investors to invest in PPP projects in lieu of attractive financial returns from the project. The PPP model started with great enthusiasm and expectations in India in 1999. A large number of contracts were signed in all the subsectors of infrastructure. By 2010, India has become one of the largest markets of PPP projects globally according to Infrascope Report 2015. The initial euphoria in the PPP model diminished after 2011. During 2011–2019, while the number of new projects reduced drastically, a large number of already started projects were delayed, stalled and terminated. There has been an overall contraction in terms of the number of PPP projects. The private sector players who started enthusiastically and won a number of PPP contracts are now laden with huge debts and are trying to monetise PPP assets by selling operational projects and are shying away from participating in new PPP projects and lenders restrained themselves from lending to new PPP projects due to crisis of corporate defaults and piling of non-performing assets (NPAs) in the Indian banking system. As exhibited in Table 1, out of 1,350 plus projects initiated on PPP basic in India till 2016, only 46% projects have become operational, and the rest of the projects were either terminated, delayed, stalled and could not become functional till end of 2019 just before eruption of COVID-19 pandemic.

Status of PPP Projects in India Initiated During 1993–2016.

Status of PPP Projects in India Initiated During 1993–2016.

Operational Projects

The projects that had been awarded to concessionaires on PPP basis after competitive bidding. The financial closure achieved and then construction was completed, and the projects are in operation phase collecting their revenue in the form of annuity or toll free. Some projects have even completed their contracted life cycle.

Delayed/Under Construction Projects

The projects were awarded on PPP basis before 2016. But projects could not be completed till date due to failure in achieving financial closure, delay in land acquisitions, environment permissions, legal disputes between parties, inefficient contractors and change in design and scope. Normally, it takes maximum three years for completion of infrastructure projects like roads, seaports, airports, metro-rail and power projects. Hence, we have studied projects that were awarded prior to 2016 and till date their construction is not completed. There are projects that are delayed by 8–10 years. On paper, they are designated as under operational projects and they are not cancelled till date. Most of these projects are stalled, and there is very low possibility of their revival.

Terminated Projects

The projects that were delayed stalled and with legal disputes are officially cancelled by either the project authority or the private concessionaire based on the terms in the concession agreement (CA).

The rest of the article is structured as follows: Section I discusses the prevalent dismal state of PPP projects in India. Section II discusses literature on PPP. Section III details the research methodology. Section IV presents quantitative data and its analysis. Section V discusses 10 case studies. Section VI presents the analysis. Section VII proposes a 20-point framework to be used for effective implementation of future PPP projects.

Physical infrastructure like roads and airports and social infrastructure like schools and hospitals are essential for economic growth and form the basis of providing a better standard of living for the citizen of the country. The governments worldwide build infrastructure through budgetary provisions, but many governments in developing countries which are not in a fiscal position to meet mammoth spending requirement build infrastructure through partnership with private partners and the PPP (Ross & Bettignies, 2004). The government builds cost-effective infrastructure in collaboration with the private developers in PPP modality using project management expertise of private developers without raising government debt or imposing taxes on citizens (Chan et al., 2011).

The incomplete contract theory is discussed in detail by Grossman and Hart (1986) and Hart and Moore (1990) suggesting giving property ownership right to the private investing party to incentivise them to invest in public infrastructure projects and further protect the investor appropriation from the government authority and encourages innovation to reduce life cycle cost of the project. The allocation of two or more activities of a project to a private partner called as ‘bundling’ induces the private developer to use more cost-effective and innovative designs reducing the project life cycle cost and enhance returns to private partner (Daniels & Trebilcock, 2000). A PPP project requires a technically expert and financially sound private developer with adequate technical knowhow, capable project team, effective project organisation structure and past experience in executing infrastructure projects and public authorities should select a competent private partner in procurement stage to ensure completion of project on time and within assigned budget (Dada & Oladokun, 2012).

A risk is an uncertainty about future outcome, and risk management is bunch of activities and measures to deal with risks to control the project (PMBOK, 1996). A risk allocation and management is essential for PPP project management (Irwin, 2007), and risk allocation between the projects partners while creating maximum value should carefully manage issues like adverse selection, moral hazard and project hold up arising due to incomplete nature of PPP contracts and should be allocated to a partner who can manage and mitigate it by aligning interests of all involved stakeholders and meticulously drafting the CA taking into consideration that PPP is largely an incomplete contract. The time and cost overrun lowers the benefit and destroy the economic value of the project. The poor outcomes of individual PPP projects due to poor contract and risk management result into poor economic welfare (Ansar et al., 2016).

The government transfers risks to the private sector as they are expert and experienced in building infrastructure assets (Cheung et al., 2012). The private party should manage and adequately price the risks, which are under their control, and the public authority should take charge of those risks, which cannot be controlled by private party (Cheung et al., 2012; Zhang, 2005). The allocation of risk among parties along with the adequate compensation to offset the accepted risk is discussed, negotiated and contracted during the PPP procurement process (Abd Karim, 2011).

The private equity investors take risk of investing with the expectation of higher rate of returns resulting into higher cost of PPP projects than public procurement projects. The lenders act as a monitoring agency for PPP projects to safeguard their interests and investments (Jefferies et al., 2002). A project structured on the sound principles of project financing optimally allocates risks among the parties along with project cost optimisation (Akintoye, 2003). A certain and stable cash flow is prerequisite for the project finance as lenders have recourse only to the cash flows and assets of the project (Zhang, 2005).

The risk management involves monitoring of risk of the project throughout the entire life cycle of the project. The private sector investors prefer to become party to PPP projects, wherein revenue risk is mitigated through certainty of revenue to cover the project’s costs and generate risk adjusted returns, while the government attempts to lower the cost of building public infrastructure by allocating some risks to a private partner (Grimsey & Lewis, 2004). The risk should be managed on life cycle basis by identifying risks in the earlier stages of the project and proactively managing them on continuous basis (Zou et al., 2008). But the private developers succumbed to underestimating the cost (Cantarelli, 2011) and the overestimation of the profits from PPP projects, which is termed as ‘optimism bias’ in the literature (Flyvbjerg, 2009).

Abd Karim (2011) analysed various risk factors of PPP project such as political, legal, economic and concluded that delay in project approval and getting various permissions, change in law and land acquisition are the most observed issues in PPP. The study by Pickrell (1992) found that rail projects in the US wrongly anticipated the traffic and revenue during operational phase, which resulted into revenue risk and lowered benefits. Engel et al. (2007) stated that in highway PPP project, forecasting traffic precisely is difficult, which leads to revenue risk during operation phase. In Indian context, Akalkotkar and Malek (2016) cited budgetary constraint of government as a cause to introduce PPP program in infrastructure on large scale. Lakshmanan (2008) mentioned problems like opaque procedures, faulty risk allocation, inadequate project selection, cost and time overruns. Mathur (2017) cited land acquisition delay budget overrun and demand risk as major risks. Baruah and Kakati (2016) described land acquisition, demand risk and financial risk as the prime issues. Harisankar and Sreeparvathy (2013) blamed faulty arbitration system in India. As per Gupta (2015), the cost overruns for Mumbai airport and Delhi airport was 113% and 50.5%, respectively. Iyer and Jha (2006) have described project participant’s commitment and sponsors competency as the success factors and miscommunication and lack of trust among project parties as causes of failure for PPP projects. Pathan and Pimplikar (2013) investigated that a BOT project gets affected by various parameters like structure of toll, revision in toll and its schedule, capital grant from government and suggested that the project authority and the concessionaire should decide about sharing of risks for effective risk mitigation.

The significant causes for failure of the PPP model in developing countries are absence of sound institutional mechanism and effective and transparent policies (Akintoye & Matthias, 2009). A sound and sensible legal and regulatory framework is requisite for dealing with the issues in PPP implementation, and such a framework should be transparent, fair and highly predictable supported with an efficient, procurement process (Harris, 2008). Such a sound framework can attract local as well as foreign investors (Adetola et al., 2011; Kumaraswamy & Zhang, 2001).

Research Methodology

This study uses a mixed methodology method incorporating quantitative and qualitative analysis. In the first stage, a quantitative study of 149 PPP projects in India (53 terminated and 96 delayed and stalled projects) is conducted. The data of all individual PPP projects in the sample are collected, which had been initiated as PPP project, CA was signed and contract was awarded to bid winning party, and subsequently, these projects were delayed, stalled and terminated or cancelled. The data are collected from the sources like www.pppinindia.gov., which is an official database of PPPs in infrastructure in India maintained by the Ministry of Finance, Government of India, annual reports and credit rating reports of project SPVs. For each individual PPP project, data such as special purpose vehicle (SPV) name, project description, sponsor, contract signing date, the terminating party, reason for termination or delay of project are obtained and analysed.

We have used a case study method to support the quantitative analysis and address the research question of how and why the PPP model has failed in India. Ten cases of failed PPP projects are thoroughly analysed. The cases are selected based on the logic of incomplete contract theory and literature replication. The in-depth structured and semi-structured interviews were also conducted with senior professionals involved in these projects. More than 1,000 pages of project documents including CAs are examined.

A detailed examination is done after triangulating the quantitative data and insights from case studies, interviews and project documents based on the various parameters like information asymmetry, uncertainty and contract and risk management discussed in PPP literature. A 20-point framework for improving performance of future PPP projects post COVID-19 is proposed.

Data Analysis and Findings

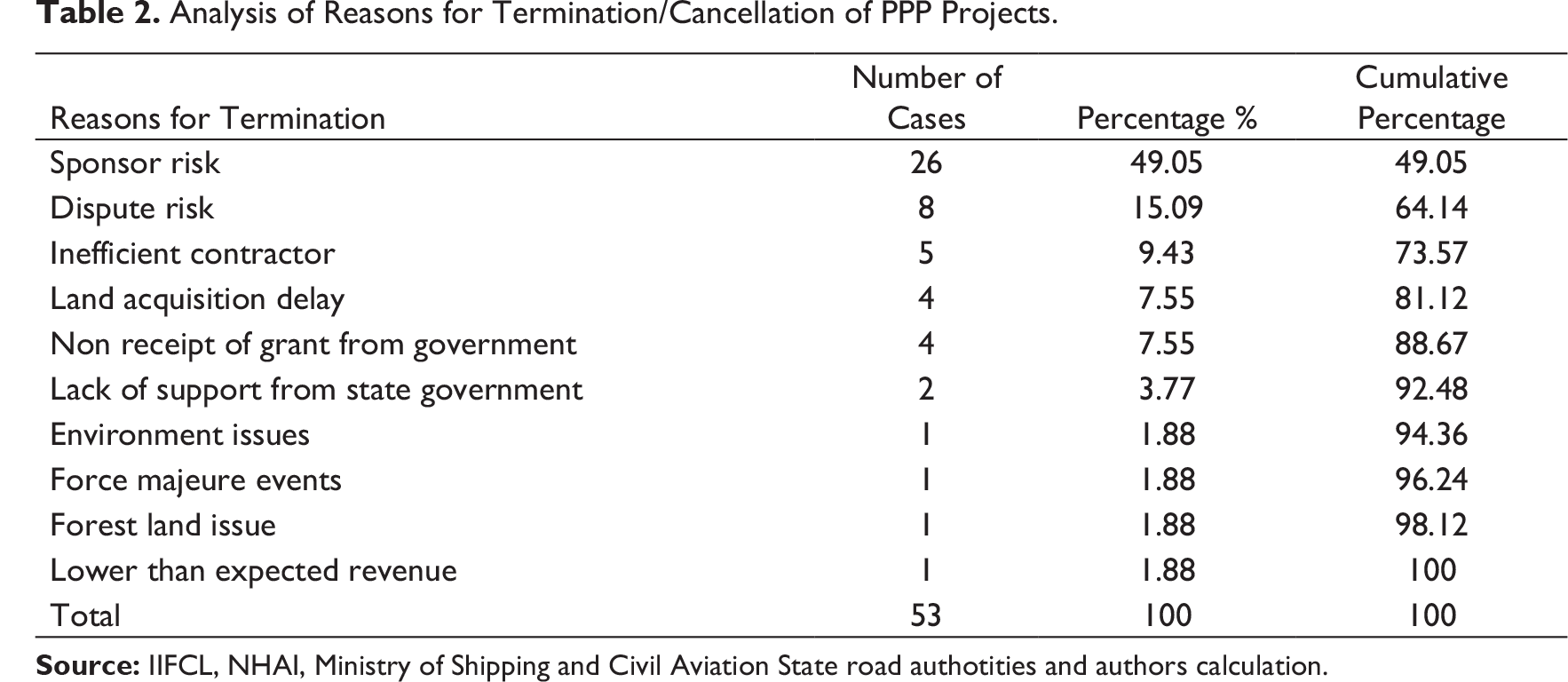

Analysis of Reasons for Termination/Cancellation of PPP Projects.

Analysis of Reasons for Termination/Cancellation of PPP Projects.

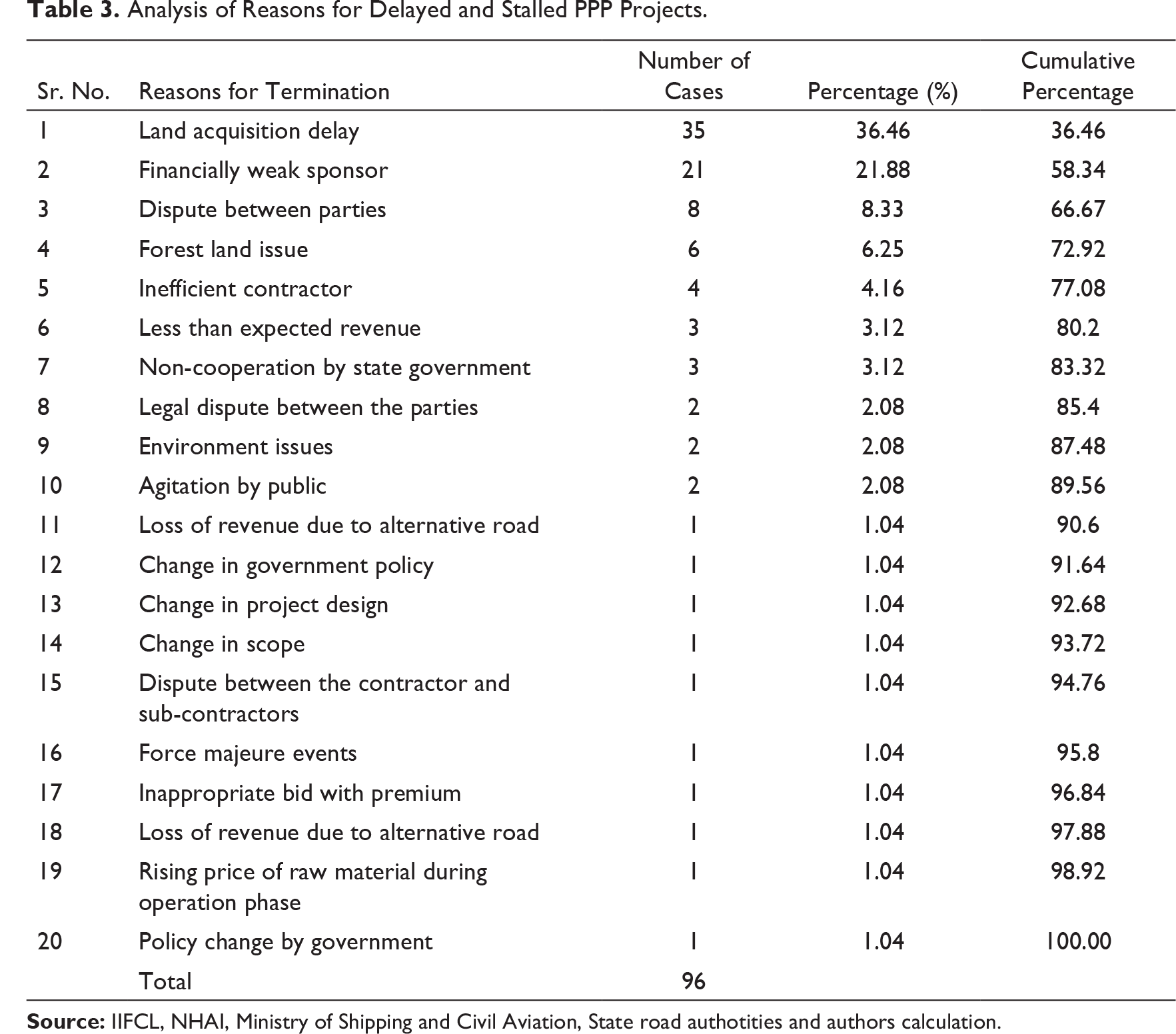

Analysis of Reasons for Delayed and Stalled PPP Projects.

Navi Mumbai Airport

To address the congestion in Mumbai International airport, the government decided to construct a new airport in New Mumbai in the vicinity of existing airport in 1998. But till date even the construction is not started due to delayed environment permissions as proposed site is part of sensitive coastal regulation zone and delay in land acquisition from the local farmers. The project cost escalated as the farmers are paid four times the market price of land as per new land acquisition bill. After acquiring the land, the City and Industrial Development Corporation, the project authority had done earthworks at the project site before commencement of the construction. In a global competitive bidding in 2017, GVK infrastructure, the current operator of the existing Mumbai airport was selected as a concessionaire but till date the construction is not started, and due to current COVID-19 pandemic, the project will get further delayed. In the meanwhile, due to legal issues, Adani Infrastructure has been appointed as a concessionaire replacing GVK Infrastructure in August 2020. As the capacity of the existing airport in Mumbai saturated in 2018, the plan to develop Mumbai city as an aviation hub did not materialise, resulting into severe economic loss for the city.

Chennai Port—Maduravoyal Expressway

The project was conceived by the National Highways Authority of India (NHAI) to provide connectivity between Chennai port and nearby state and national highway, and its bidding was done in 2010. The authorities faced severe opposition from local farmers and delayed environment permissions due to vicinity of river bed area to the project site. The construction was started in 2013, but till that time, since very small portion of required land was acquired, the work progress at a snails speed and NHAI had to pay the idle charges for labour and machines of the contractor. Finally, the NHAI terminated the project in 2015. All the stakeholders in the projects severely impacted financially due to part of the work, which was already done before the cancellation of the project which points to faulty planning and preparation of the project.

Kishangarh–Udaipur–Ahmedabad Highway

Kishangarh–Udaipur–Ahmedabad highway was a six-lane 550-km highway awarded on PPP basis by the NHAI to the concessionaire GMR Infrastructure in 2011 through competitive bidding as GMR offered highest premium of USD 90 million per annum. But, after 2013, the economic conditions in India deteriorated and GMR realised that it would be difficult to pay such a high premium if the project revenue fall during operations. Hence, GMR dropped out of project citing the delay in getting environmental permissions for the project and subsequently in 2013 requested again to renegotiate the premium to start project work. The case points towards aggressive bidding by the developer.

Yamuna Expressway

The project is 165-km six-lane state highway connecting Noida to Agra in Uttar Pradesh state with concession period of 36 years till 30 April 2044 at project cost of ₹14,000 Cr. Yamuna Expressway Industrial Development Authority initiated the project and Jaypee Infratech Ltd. was appointed as the concessionaire. The project included construction, operation and maintenance of the expressway and right of developing 6,200 acres of land along Yamuna expressway.

The sponsor company Jaypee Enterprise Ltd. (JAL) had defaulted on ₹525 Cr of loans outstanding to IDBI bank. The Supreme Court directed JAL to deposit ₹2,000 Cr with court to safeguard interest of homebuyers. JAL had submitted to court a proposal to sell Yamuna expressway to a prospective buyer who was willing to pay ₹2,500 Cr for the expressway. The court had restrained the directors of Jaypee Infratech and JAL from travelling abroad without permission. Allahabad bench of NCLT has ordered liquidation proceedings against Jaypee Infratech under IBC 2016.

Shivpuri Dewas Expressway

The NHAI awarded this 300-km national highway on BOT toll basis to the concessionaire GVK Infrastructure in 2011. But due to economic slowdown, the company failed to raise equity and the financial closure was not achieved. The company pulled out of the contract citing delay in getting the environment clearance and the dispute reached to Delhi high court. Finally, the NHAI terminated the project in 2014. In 2015, the NHAI restructured the project and awarded the project in three stretches of 100 km to three developers.

Three Seaports for Trans-shipment in the Vicinity

The shipping industry in India wanted to build a strong, alternative container trans-shipment terminal to help send and receive cargo without routing them through neighbouring hub ports such as Colombo, Singapore and Jebel Ali. To cater this need, the port operations started from 2011 at Vallarpadam by the Union-government-owned Cochin Port Trust in Kerala. Another such facility was started at Colachel in 2016, and barely two months after that, the work began on a new trans-shipment terminal at Vizhinjam. Colachel and Vizhinjam are just 36 km apart. Vizhinjam is 225 km from Vallarpadam.

When Vizhinjam will become operational, all three trans-shipment ports will get crowded in and around the same region. The shipping ministry has decided to spent ₹1,700 crore to create infrastructure for developing Vizhinjam as a national trans-shipment hub. Another container trans-shipment terminal at Vizhinjam with viability gap funding (VGF) from the government is not recommended. The scarce resources of the government like the VGF cannot be spent on a project, which will basically eat into another project on which considerable government funds have already been spent. Setting up of a trans-shipment terminal at Vizhinjam will result in both Vallarpadam and Vizhinjam fighting for the same cargo and thus making both ports unviable in the process.

Water PPP in Karnataka

The Karnataka state government initiated a project to provide drinking water supply to the water-scarce regions of Belgaum. The project was budgeted at ₹250 crores to be spent over a period of four years between 2004 and 2008. Appropriate regulatory and legal framework was established by the government to ensure better service delivery at affordable tariff and timely maintenance. However, the project was faced with acute hurdles. The tariff was set at very high levels in order to recover the project costs. Availability of water depended on the monsoon rains and the flow of water from the Mandavi River in Goa.

The water disputes between the two states led to drying up of the Neer Sagar reservoir, from which this water supply was being sourced. Several citizen and civil society groups protested that the government’s decision to upscale the project was taking without the local population into confidence and the ambiguity related to the tariff and costing of the project. Thus, an ambitious yet genuine people welfare project was dealt a significant blow due to mismanagement of the stakeholders. The project has proved to be too costly for the state government, and the overall benefits from the project did not reached the population for which it was set up.

Ranchi Expressway Ltd.

Ranchi Expressway Ltd. was a 163-km national highway connecting Ranchi to Jamshedpur, for which the NHAI awarded contract to Madhucon Projects Ltd. in 2011. The total estimated project cost of ₹1,655 crores with a debt of ₹1,150 crores and equity of ₹500 crores. Out of the equity, it was mandatory for the promoters of Madhucon Projects Ltd. to contribute 25% of equity, that is, ₹125 crores before first drawdown date from consortium of banks led by Canara bank. But the promoter draws down ₹1,030 crores without providing the equity and misused the bank funds. They did not carry out any project work, and the project was terminated in 2018. When the enquiry was made by serious fraud investigation agency SIFO, it was revealed that the promoters siphoned total ₹265 crores drawn from banks. The investing agency CBI arrested the CMD and other directors of the company in a fraud case in March 2019.

Delhi–Gurgaon Toll Road Project

The project was awarded on the BOT basis to the sponsor DSC Ltd. in 2002 and completed in 2008. Since the concessionaire DSC Ltd. could not carried out the maintenance work as per the contract terms and up to the expectations of the project authority, NHAI, the project was terminated by the NHAI in 2013. But the consortium of bankers led by IDFC bank had lent more money than the estimated project cost by the NHAI without consulting the NHAI, and hence, the NHAI rejected to pay more than earlier decided termination payment to banks putting banks to incur a big loss. The issue is also referred to enforcement directorate (ED) and chief vigilance commissioner to investigate any siphoning of the funds done by the project developers.

Airport Metro Line Project

This project was proposed to connect Delhi Airport to the city and outskirts in conjunction with the existing Delhi Metro. Reliance Infrastructure Ltd. was the sponsor, and its subsidiary Delhi Airport Metro Express Pvt Ltd. was the concessionaire for the project. The project was commissioned in February 2011. The consortium of banks led by Axis Bank lent a loan of ₹2,220 crores against a government-approved debt of ₹1,247 crores without consulting the government authority. The lenders took a hit on this account as the sponsor walked out of the project. The project was terminated, and bankers had to incur loss of ₹1,000 crores due to reckless lending without considering the termination payment terms in the concession and against the principles of project financing.

Analysis and Discussion

Following the detailed quantitative analysis of sample of 150 failed projects corroborated by analysis of 10 cases of failed projects, we have derived following propositions.

A large number of stakeholders with conflicting interest were involved in the PPP project. The lack of data sharing and the hiding of the private information made the projects susceptible to uncertainty and information asymmetry. Due to information asymmetry and inadequate project monitoring and lack of information, the project authorities could not resolved the issues occurred during construction and operation phase due to heightened uncertainty. The resulting opportunism, moral hazard, adverse selection and hold-up issues proved detrimental to the outcome and intended objectives of the PPP projects.

The project authorities could not handle the uncertainty and information asymmetry due to lack of contract and risk management skills. That coupled with inadequate contract monitoring led to delay, time and cost overrun and even termination of the projects. In case of New Mumbai airport and Chennai port expressway projects, the project authorities failed to deliver their own contractual obligations such as providing land and environmental permissions on time. The project planning and preparation was inadequate in these cases.

In cases of Kishangarh and Shivpuri expressway projects, the adequate enforceable performance measures were observed to be missing in the CA. The authorities failed to monitor the construction and operation of works resulting into loss of quality and increased cost. The authorities failed to knot penalties with the contract clauses and incorporate quantifiable performance indicators to stimulate better enforcement of projects.

Ideally, a good CA can encourage innovation and efficiency in the project by the concessionaire. But the concessionaire used loopholes in the contracts for its own benefit and opportunistically skipped their obligation due to lack of clear demarcation in terms of performance limits in the CA. The PPP contracts failed in specifying justified reasons for renegotiations, which resulted into failing of the renegotiation in reaching to logical conclusions.

As per the government guidelines, the total project cost was to be calculated as the sum of the bank lending and equity money infused by the private developer. In cases of Delhi–Gurgaon Highway and Delhi Airport Metro Express line projects, banks had lent more than the Government evaluated cost to SPVs of projects without consulting the project authorities. Since the projects were cancelled, banks had taken a hit as the liability of the Government in such cases was limited to the project cost defined by it and termination payment in proportion to project cost. The banks hesitated to remove errant promoters due to lack of the expertise to run the business. Such projects subsequently classified as NPAs.

The basic objective of the PPP model was to make effective utilisation of private finance and efficiencies of developers, but few private players misused the PPP model for own benefit to the detriment of the taxpayers. In cases like Ranchi Expressway, the concessionaires borrowed large funds from the banks and diverted these funds to their other subsidiaries or siphoned the funds off to both India and overseas, while themselves bringing in little or no committed equity. The grant received from the project authority or loan from banks was paid as mobilisation advances to subcontractor belonging to same sponsor group who in turn round-tripped the same back to concessionaire and showed as promoter’s equity. The large payables were created by obtaining over-invoiced materials at inflated prices, which were converted into equity of the sponsor using forged invoices.

The loan monitoring processes of the banks were inadequate to verify the source of real equity infused by sponsors and prevent any fraud from the developers. Some concessionaires inflated the total project cost many times the original project costs estimated by the project authority during bidding stage with anticipation of reviving more grant during renegotiation in future. This resulted into entire funding of the project with public funds while zero equity from developers. The diversion of funds to other businesses and lack of equity funds significantly delayed financial closure of many projects and termination even before the start of the construction.

The policy paralysis by government has often been cited as the main culprit for the slowdown in both the economy and the infrastructure sector, but the private sector arguably deserves its share of the blame. Some players participated in a bid process with the aim of winning the project with little regard for project economics. Faced with a project that is commercially unviable from the outset, the winner attempts to get the government to add sweeteners to the contract after the bidding has ended. It results in the so-called ‘gold plating’ of costs and the loading of the project with much more debt than it can bear, making a ‘restructuring’ of the loan a few years down the road almost inevitable. As per economic theory, infrastructure projects are ‘long gestation’ projects where returns take years to fructify, in reality the promoter, unofficially, retrieves a handsome de facto return on his investment within a relatively short span of time. An aggressive bid was excuse to load the project with excessive debt and siphon off surplus funds. The companies bid aggressively in a bunch of projects so as to build a large portfolio of deals in a short time, which can then be sold to the public market in an IPO, enabling the promoter to exit. Such projects eventually failed to achieve financial closure.

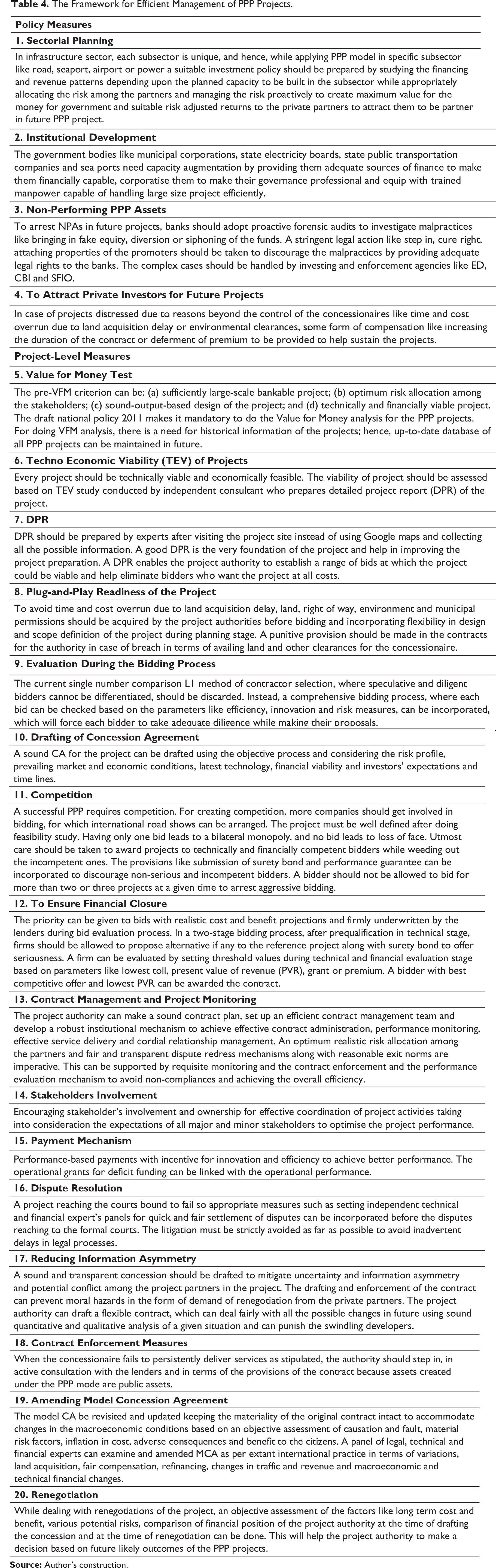

Suggestions

The Framework for Efficient Management of PPP Projects.

The Framework for Efficient Management of PPP Projects.

As per ADB’s report ‘Meeting Asia’s Infrastructure Needs’ India requires $4.5 trillion to cater India’s infrastructure demand by 2030, which is possible if both the private sector and the government together invests in public infrastructure. The COVID-19 pandemic and nationwide lockdown have severely impacted Indian government’s budget, and the government needs to shift back to the PPP model such as BOT or toll-operate-transfer (TOT) projects funded by private players in place of current hybrid annuity and EPC models funded entirely by the government.

India’s response to Corona pandemic needs elevating the public and private spend in Infrastructure sector through PPP. It is the right time to put in place a progressive plan to kick start the PPP model with a new approach by addressing the core structural issues such as inadequate contractual frameworks and NPAs that have plagued the infrastructure sector for two decades while addressing the concerns of the stakeholders with appropriate risk allocation and de-risking the private sector and addressing issues like availability of capital, bankability of the projects, tech innovations, changing market conditions. The robust financial and technical plans with optimum risk allocation structure and involving the lenders with an acceptable credit risk to drive PPPs with large-scale private investment without burdening the banking system with further NPAs.

The development financial institutes in India can forge innovative partnerships with foreign FIs to ensure flow of capital. To improve the confidence of the private equity players, a sound pipeline of bankable projects is required supported by innovative financial products and funding models along with emphasis on project planning and regulatory framework to enhance the viability of PPP projects in India. In the absence of many sector-specific regulators, a central legislation as adopted by South Korea and even a separate ministry to deal with problem of slow ‘decision-making’ which had paralysed PPP projects in the past is recommended. India needs to start PPPs in digitisation, healthcare, railways to attract international companies and supply chains to switch over their facilities to India.

The study contributes towards the growing body of knowledge on contract and risk management in PPP projects by suggesting a framework of policy and project level measures for effective implementation of future PPP projects. The findings of this study will help the project authorities to spot the probable bottlenecks during the planning phase of the project and drafting of the CA to handle the uncertainty and information asymmetry in the projects and take corrective measures during construction and operation phase to improve the project performance. The study proposes a 20-point conceptual institutional framework for improvement in the prevailing PPP policy. India, which was leading country in terms of the number and value of PPP projects from 2007 to 2011, had lost the track, and by the end of 2019, before eruption of corona pandemic, there were no takers for PPP projects offered by the Indian government. This research is an attempt to study these phenomena in detail to find the root causes for such a large number of failed projects. This study represents PPP market behaviour in India and, therefore, is of significant relevance to other developing economies sharing socio-economic similarities with India.

Future Areas of Research

Several interesting areas for research emerged as we explored depth in this study. This research studied the PPP projects awarded till 2016 on PPP basis to account the delays in the projects. Post 2016, new PPP models such as hybrid annuity model and TOT were introduced by the government. The projects based on these models can be evaluated for their performance in future. The preliminary contribution of this research requires further validation through multiple cases of projects post 2016. It will be interesting to study the impact of corona pandemic on the PPP model. The findings in India can be compared with other developing countries like South Korea, Indonesia, Thailand and Vietnam who had shown remarkable performance in PPP projects in the last five years.

Conclusion

This study is conducted to understand why a large number of PPP projects delayed, stalled and terminated in the largest PPP program in the world implemented in India. Based on the quantitative and 10 case studies, this study finds that the incomplete nature of PPP contracts and uncertainty leads to adverse selection, moral hazard, opportunism and holdup of the projects.

The inefficient and inequitable allocation of risk among stakeholders, lack of contract management skills in the project authorities in terms of tying contractual performance norms with payment mechanism and ineffective monitoring while aggressive bidding by the concessioners, the excessive funding by the banks and misuse of the PPP model by some private developers defeated the objective to the detriment of public, and the PPP model became instrument for the privatisation of profits and nationalisation of losses. The final outcome is a large number of failed projects and no participation from private developers in future projects defeating the very purpose of adopting the PPP model to build public infrastructure by making effective use of funds and expertise from private sector.

The study proposes a 20-point conceptual institutional framework suggesting policy and project-level measures such as sectorial planning, institutional development, efficient and transparent procurement process creating competition, designing bankable projects and de-risking them by taking measures like awarding plug-and-play ready projects in terms of land acquisition and various permissions to avoid delays in financial closures and time and cost overrun, setting a fair and transparent alternative dispute redressal mechanism based on arbitration, mediation and conciliation, rewarding efficiency and punishing dishonesty will attract the private developers and financial investors for future PPP projects. A world-class infrastructure will help to attract supply chains and foreign investment in India and achieve its dream to become 5 trillion dollar economy post corona pandemic.