Abstract

While matter clearly matters to organization theory, its absence from the study of organizational ethics is striking. Despite the obdurate materiality of the workplace, critical scholarship on organizations and morality sees ethics as interpersonal, subjective and embodied. Organizations, meanwhile, are characterized by moral anomie and dysfunction. This article advances our understanding of the material entanglements of organizational morality, drawing on the science and technology studies inflected study of markets to show how moral orders arise in dialectic between the social and the material. It argues that moral orders are entangled in the material infrastructures of organizations. Its empirical case is the founding and development of a small-company focused stock exchange, OFEX, launched in London in 1995, accessed through elite interviews and documentary work. The article seeks to develop our understanding of morality in critical organization studies, to further defend the Weberian notion of ‘ethics of office’ by emphasizing the sociomaterial dimension of organizational morality, and to contribute to an ongoing renaissance of the study of morality as a sociological phenomenon. There are implications for managers and engaged scholars alike.

Keywords

Introduction

We did what we thought was right . . .We should do what is right for the market. (Jonathan Jenkins, OFEX chief executive)

Current scholarship on organizations and ethics is often distrustful of organizational rationality. 1 Critically minded scholars have pointed out the morally alienating nature of institutional formal-rational calculation (Bauman, 1989; MacIntyre, 1992), with its toxic organizational cultures (Brannan, 2017) and self-justificatory narratives (Collins and Wray-Bliss, 2005; Whittle and Mueller, 2012). Organizational norms are corrosive: Jackall (2010: 204) suggests that ‘bosses’ determine ‘moral rules-in-use’, and that subordinates must simply conform. As the corollary of this position, contemporary organization theory has increasingly understood positive ethics as an individual challenge. Organizational anomie is set against a ‘socially contingent and self-reflexive’ process of individual self-constitution through ethics (Ailon, 2015: 78); doing ‘the right thing’ becomes an act of rebellion and self-affirmation against the structures of the institution. Ethics emerge from this writing as embodied, subjective, affectual and emotional (Pullen and Rhodes, 2015; Rhodes, 2012), part of the work of constituting one’s own moral subjectivity (Munro, 2014). The ethical practitioner is the reflexive one (Hibbert and Cunliffe, 2015); the ethical impulse is interpersonal and relational (Tyler, 2019).

This decidedly un-sociological account of ethics as a subjective, individually embodied property reflects a more general neglect of the topic within mainstream sociology. Talcott Parsons is often blamed for the long exile of morality from sociology; the study of morality was, before Parsons, central to the sociological endeavour. Durkheim (1957) regarded the moral turpitude of industry as a problem of organization, specifically the presence of certain kinds of social arrangements based around competition. Against the backdrop of a more elaborate account of the division of labour and the emergence of variegated professional ethics in society, Durkheim advocated the organization of industrial processes into corporations capable of reintegrating the moral realm with the economic (Steeman, 1963). Max Weber had understood morals as social facts amenable to empirical investigation and an important part of the discipline’s remit (Hitlin and Vaisey, 2013). With the discipline growing averse to grand theory, ‘because morality was identified so strongly with Parsonian theory, it went down with the functionalist ship’, as Hitlin and Vaisey (2013: 53) neatly put it. The psychological sciences, meanwhile, have pursued a vigorous research programme that conceptualizes morality as an evolutionary adaptation. Bykov (2019: 203) reviews this literature and concludes that it ‘leads to a considerable fragmentation of the very idea of morality, which now looks like just little more than a capacity to evaluate hypothetical scenarios’. Eroded from all sides, the sociological content of morality is at stake, and scholars have begun to call for a ‘new sociology of morality’ that takes seriously the divergence of morality across groups, places and times (Hitlin and Vaisey, 2013).

Disciplinary antecedents in classical sociology, a more modern sociological aversion to theorizing morals, a distrust of organizational settings and – related to this – a contemporary account of individualized ethics that draws from postmodern theory and feminist critique (Collins and Wray-Bliss, 2005; Pullen and Rhodes, 2015; Tyler, 2019) have led to a position where the literature has scarcely begun to explore the material dimensions of morality. This absence is striking in view of the increased attention that scholars of organization have paid to materiality in recent years. Authors from the science and technology studies tradition (Haraway, 1985; Latour, 1999; Mol, 2002) and mainstream organizational theory (Barad, 2003; Fotaki et al., 2014; Leonardi, 2013b; Orlikowski, 2007) have sought to emphasize the importance of the material, stressing in different ways its agential and ontological entanglement with the social. Increasingly, matter matters to organization theory (Carlile et al., 2013); when it comes to the analysis of organizational morality, however, matter does not yet seem to matter.

The present article seeks to counter that absence through the analysis of an empirical case, a small-scale stock market for high-growth companies, founded in London in 1995 and active until the financial crisis of 2008. Developing the insights of scholars such as Ben Khaled and Gond (2019) and Mercier-Roy and Mailhot (2019), the article draws on the science and technology studies (STS) inflected social studies of markets (Çalışkan and Callon, 2010; MacKenzie, 2009) to explore how multiple and often contradictory organizational moralities are performed through agency-filled ‘socio-technical assemblages’ (Orlikowski, 2007), or ‘agencements’ (Callon, 2008). It theorizes material devices as ethical generators (Preda, 2006) to present an ‘ecological reading’ (Mercier-Roy and Mailhot, 2019) of the performance of morality in its empirical site. The article shows that the market’s normative moral orders – being the notions of acceptable practice, worth and value held in common within a given community – arise in dialectic between the social and the material, embedded in the sociomaterial infrastructures of the exchange. Unlike the high-level ‘orders of worth’ envisaged by Boltanski and Thevenot (2006), the moral orders identified are locally specific and fragmented; they remain subject to challenge from rival orders embedded in rival mechanisms of trading. By this account, moral orders require considerable work, and are specific, contested and temporary; they are social facts deserving of empirical study, as Weber understood (Hitlin and Vaisey, 2013).

Understanding morality as organizational and material, rather than personal, dovetails with other concerns in the literature. Sociologists have in recent years become aware of the micro-political contestations ‘congealed’ into the design of markets (MacKenzie, 2018); I emphasize the ethical dimensions of such struggles, a topic of pressing relevance for those interested in the organization, or reorganization, of markets (Brunsson and Jutterström, 2018). My argument suggests that such contestations have moral aspects, and that they shape the moral agency of market participants. Notions of good are local, specific and historically dependent, a claim that problematizes accounts of morality as individual and embodied prevalent in the literature, and augments the defence of formal organization and the ethics of office (Du Gay, 2000, 2008). The article continues to advance our understanding of the role of the material in organizations, extending the powerful concept of ‘sociomateriality’ to the domain of organizational ethics, and highlighting the ethically generative capacity of the sociomaterial architectures of the markets. To paraphrase Orlikowski (2007), materiality and morality are ‘constitutively entangled’: for those interested in organizations and ethics, whether as scholars, managers or both, matter matters a great deal.

Ethics and organizations: The classical and critical traditions

The fathers of classical sociology, Durkheim and Weber especially, understood the ethical problems facing organizations and commerce. Durkheim saw ethics as a resource – as potential solutions to social problems – specifically the anomie of barbarous industrialization that threatened, in his view, to overcome society. Durkheim had tackled Spencer’s assertion of competitive egoism as the basis for moral organization, claiming instead that deeper social structures held mankind above the state of continuous, self-interested warfare (Steeman, 1963). He recognized that professional ethics were specific to categories of employment and dependent upon the structural organization of those professions, ‘as many forms as morals as there are different callings’ (Durkheim, 1957: 5). It is likely, he argued, that professional ethics will be more developed and more advanced, the greater the stability and the better the organization of the professional group in question. In the case of industry and trade, the lack of organization means that scarcely any professional ethics exist in the whole sector. This line of argument led him to call for the organization of business into corporations which, like the mediaeval guilds, would be able to reintegrate the moral and professional aspects of life (Hendry, 2001). Weber was equally fascinated with the constitution of organizational ethics, the inescapable ‘iron cage’ of formal-rational calculation. He famously noted that ‘the objective discharge of business primarily means the discharge of business according to calculable rules and without regard for persons’ (Weber, 1978: 975, emphasis in original). This phrase, inverted by Bauman (1989), has led a critique that sees Weber as privileging formal over substantive rationality. As Du Gay (2000) makes clear, this is unjustified, for Weber recognized the ethical contradictions inherent in bureaucratic logics; like Durkheim, he saw the ethical ‘character’ as dependent upon a given situation.

This sense has fallen out of more recent scholarship on organizational ethics. Although Weber’s dehumanized bureaucrat is an ideal type far removed from the complicated person holding the office, Bauman (1989) used it as a polemical device to accuse bureaucracy of creating moral distance and a purely technical responsibility. Scholars have followed Bauman’s lead, seeing morality as individual and subjective, and set against the rule-bound frameworks of rational organization (Jackall, 2010; Rhodes and Wray-Bliss, 2013). Critically inclined researchers, setting out from the entirely reasonable empirical observation that many organizations do go bad, have offered increasingly subtle and sophisticated accounts of how organizational norms can be corrupted. Brannan (2017) presents an ethnographic study of financial services mis-selling, showing the ritualized nature of toxic organizational culture. Others have focused on narratives of self-justification and their consequences (Collins and Wray-Bliss, 2005; Whittle and Mueller, 2012). McMurray et al. (2011) offer an account of ethics as a means of moral agency and freedom in organizations, while Munro (2014) argues that ethics should be understood as a spiritual discipline through which novel subjectivities can arise, a means of resisting the discursive disciplining demanded by employers (Halsall and Brown, 2013). For Weiskopf and Willmott (2013), ‘ethics’ is most properly understood as a mode of individual agency displayed in the face of organizational power structures, norms and moral orders. As Eggebø (2013: 314) writes, ‘emotions have no place in bureaucratic practice; the professional bureaucrat is required to control emotional reactions and resist emotional involvement in order to realize the principle of equal treatment’. But only up to a point. Eggebø’s study of immigration officials shows them operating a kind of ethical doublethink, where ethics spring from their emotional responses, offering a means of negotiating the often blurred lines of formal organization. In the same way, Pullen and Rhodes (2015: 160) suggest that ‘affectual relations, care, compassion or any other forms of feeling that are experienced pre-reflexively through the body’ form the basis for ethical agency.

Much of the contemporary critical literature of ethics and organization is, therefore, distinguished by its determination to move away from rational-philosophical accounts of ethics, critiqued as thinly disguised regimes of domination, embedded in relations of gender as well as race (Contu, 2018; Knights, 2015; Tyler, 2019). The ethical subject is one who manages to articulate a moral position within the confines of organizational action; ethical responsibility becomes a feat of rebellion (McMurray et al., 2011). Moreover, where classical sociology recognized the functional specialization of professional ethics, ethics that emphasize their claim on the individual as a whole must be universal and consistent: ‘The possibility of categories and practices of personhood’, writes Du Gay (2008: 132), ‘expressing distinctive ethical comportments, irreducible to common principles, appears quite foreign to those for whom a common or universal form of moral judgement is held to reside in the figure and capacities of the self-reflective person’.

Ethics and the (socio)material

Treating morality as an individual property ignores the ‘obvious fact’ (Bykov, 2019: 198) that moral frameworks differ between groups, a phenomenon that characterizes morality as a sociological problem and one that becomes acute in the study of organizations. A sociological analysis of a more Weberian kind – treating ethics as social facts worthy of study – may seek to investigate the social processes behind given sets of morals understood as belonging ‘more to cross-cutting groups . . . religions, occupations, generations, educational categories, organizations, and social movements’ (Hitlin and Vaisey, 2013: 53). In this vein, economic sociologists have shown markets to be sites of moral work, legitimizing certain activities and erecting boundaries between others (see, for example, Healy, 2004; Zelizer, 2005). Such scholars have largely focused on the discursive and cultural framings of markets and market boundaries (De Goede, 2005). Empirical studies have also emphasized the cultural construction of particular kinds of agency (e.g. Ailon, 2019). Scholars have insisted on the agency of individuals over and above the tools that they use. Svetlova (2012) argues that institutional practices may greatly inhibit the performative power of financial models, while Beunza’s (2019) study of Wall Street morals suggests that models lead to a moral disengagement that must be countered by interpersonal relations. Cultural framings will necessarily differ between sites, and actors may inhabit multiple moral persona. This is well theorized by Boltanski and Thevenot (2006), who propose the existence of rival orders of worth. In their theory, actors infer social norms – what is valued, what is (un)worthy – from ‘principles of coherence present both in the mental schemas of individuals and in the arrangement of objects, persons’ (2006: 145). Actors may shift from one order of worth to another, depending on social situation: for example, the industrial order, which dominates the workplace and factory, has different values from the civic or domestic orders. Boltanski and Thevenot’s (2006: 14) intention is to produce a high-level schema of modes of justification in political-social discourse, ‘moving back and forth between classical constructions of political philosophy and justifications produced by actors in disputes . . . to construct a solid link between political philosophy and sociology’.

The present article proposes another approach – a ‘flank movement’ (Muniesa, 2011) – to the understanding of ethics in organizations. It follows Mercier-Roy and Mailhot’s (2019) endeavour to move beyond the discursive strategies of morality to examine the ‘concrete recomposition of laws, conventions, devices, persons’ – the ‘agencement’ of human and non-human actors that give meaning to action and settle ‘the common good’. The term ‘agencement’, borrowed from the STS-inflected study of markets (Çalışkan and Callon, 2009; Callon, 2008) signifies an arrangement of human actors, material devices and organizational practices, inscribed with certain knowledges and capable of action as a single entity. The agencement enhances the cognition of individuals, distributing (Hutchins, 1995) it across this heterogeneous array of devices. Thus a hedge fund comprising people, telephones, machines and an outsourced back office can be productively theorized as an agencement (Hardie and MacKenzie, 2007). The present article invokes the notion of agencement as not just cognitive prosthesis (Callon, 2008) but also a moral one; in doing so, it extends organization theory’s concerns with the interrelations of materiality and sociality to the domain of the moral.

An array of work within organization studies and elsewhere has contested the philosophical and empirical privileging of the social over the material. It is no longer novel to propose that the material shapes organizational life, nor indeed to argue that the material is itself socially constructed. Early contributions from the sociology of scientific knowledge demonstrated that the material is highly social, that it takes its particular form as a result of social processes worked into material artefacts (Pickering, 1992). Actor Network Theory sought to distribute agency across ontologically flat, heterogeneous ‘agencements’ (Callon, 2008), often termed ‘assemblages’ in organization theory (e.g. Orlikoski, 2007). 2 Latour (1993) highlighted the ethical consequences of such a move, seeking to decompose the bifurcated ontologies of fact/value and end/means, artificial categories imposed by the intellectual disciplines of modernity. For Latour the endeavour of separation has never been wholly successful: we have never been modern.

A parallel approach is taken by those scholars in organization theory who follow Barad to suggest that organizations are neither social nor material but ‘sociomaterial’, emerging through a ‘constitutive entanglement’ of the two domains (Orlikowski, 2007). Such ‘agential realism’ (Barad, 2003: 810) is first and foremost a theory of epistemology, suggesting that reality is produced intersubjectively in our attempts to understand it, with the material an ontological category separated from the social through our own ‘agential cuts’. Orlikowski has argued that there is no social that is not also material, and no material that is not also social. For Leonardi (2012, 2013a) and Mutch (2013) this is so much scholasticism. Leonardi argues that the conceptual entanglement of social and material occurs only after the empirical entanglement, and that the appropriate unit of analysis is the artefact and the people interacting with it and around it.

Nonetheless, the term sociomaterial may be wielded with a lighter philosophical touch to denote the fundamental interconnectedness of material artefact and social practice and the present article adopts such a usage. For there remains an area of consensus around the notion that the material is not a neutral substrate for human action. This insight is familiar to students of technology and science; technological outcomes are freighted with the power relations that surround their design, a point made especially strongly by feminist theorists, following Haraway (1985) and others. Recent scholarship has explored, for example, how moral work buried in algorithms creates moral consequences, reinforcing or undercutting ethical principles. It reshapes the provision of care in acute medical settings (Roscoe, 2015) or the life chances of individuals (Fourcade and Healy, 2013). Moral technologies have been theorized as disciplinary devices productive of everyday life. The Rich Dad Poor Dad board game, for example, is revealed as a technology of neo-liberal economic citizenship by Fridman (2016). In an important precursor to the present study, Mercier-Roy and Mailhot (2019) take up the concept of agencement to explore how the Uber app has reconfigured notions of appropriate behaviour around the taxi industry. They invoke the notion of agencement to provide an ‘ecological’ account of the orders of worth (Boltanski and Thevenot, 2006) that evolve and settle around the app. Mercier-Roy and Mailhot (2019) emphasize controversies as moments of ethical change and discontinuity that offer points of entry for analysis. Such controversies often become apparent as the process of automation forces participants to make explicit the norms underpinning market action (Muniesa, 2008; Pardo-Guerra, 2019). So, for example, Grossman et al. (2006) examine the implementation of an electronic system in the Paris bourse in terms of ‘transparency’, a polyvalent concept embedded in rival discourses of justification. On the one hand brokers demanded transparency of identity in order to know with whom they were transacting; on the other, the bankers argued that transparency of the order book (i.e. anonymity of counterparties) would facilitate efficient pricing. The authors distinguish between concepts of transparency: a literal transparency, being transparency of network relationships, and an abstract transparency, an informational transparency that aids processing.

From these studies emerges a recognition of the dialectic between the material and the moral. There can be no separation between technology and morality, between ends and means (Latour and Venn, 2002). The material, as Preda (2006: 775) argues, has ‘agential features, which, while allowing for standardizing routines, open up supplementary paths of institutional intervention’. Preda’s study of the invention of the tickertape and the resulting transformation of financial markets theorizes it as a ‘generator’, a device able to reinforce temporal structures, visualization modes, representational and interpretive languages, cognitive tools and categories, and group boundaries. The ticker becomes a time generator, a generator of cognitive tools and a device for the organization of knowledge; from the ticker flow new ways of seeing and doing in the markets and new conceptions of what appropriate action might be. Moral standards and orders emerge from new material apparatus or from controversies around notions such as transparency or safety; they may be held in place by material apparatus; they may prove sticky and persist even after new sociomaterial arrangements give rise to new articulations of the moral. In organizational settings, the stabilization of morality ‘can only ever be partial and temporary . . . frames of valuation persistently overflow and must be reframed’ (Roscoe, 2015: 117). Through a case study this article will explore such a dialectic in action.

Methodology

Data were collected as part of a larger project to write a ‘historical sociology’ (MacKenzie and Millo, 2003) of two stock markets founded in London in the 1990s. 3 A historical sociology focuses on the social and technical/material interactions that gave rise to the formation of these markets, a deliberate counterpoint to accounts focusing on individual, institutional entrepreneurs and regulatory change (e.g. Posner, 2009). The perspective of material sociology presupposes an actor network ontology (Latour, 2007) and a methodological injunction to follow the actors, be they screens, notebooks, individuals or European directives, through the data (Latour, 1988). Such analysis leads to a richly descriptive, narrative account, the basis for this case study.

I did not initially set out to chart the moral orders of these markets. Normative accounts of market operation emerged – unexpectedly – throughout the interviews. They appeared both as justifications, operating as relatively high-level ‘orders of worth’ (Boltanski and Thevenot, 2006) and as much more specific articulations of proper conduct and moral value within the markets, the ‘moral orders’ of this article. Interviewees spoke not only of what they did or should have done, but also of how appropriate courses of action emerged within the affordances of the sociomaterial arrangements of the marketplace. Press releases and newspaper commentary speak of aspirations and expectations, while company disclosures offer a terse, timestamped, commentary on progress. Through a historical perspective, it is possible to follow moral orders through a process of social and technological development (a new trading platform, perhaps) to a retrospective analysis of their success, or otherwise.

Over a period of 18 months, I conducted 54 interviews with 39 participants, totalling 73 hours; I interviewed almost all of the major participants in the new markets. 4 Many interviews were conducted on a named basis appropriate to the historical nature of the project (see Appendix 1). Where interviewees requested anonymity, usually because they were more junior colleagues still working in the sector, it has been necessary to anonymize an entire group (e.g. ‘market executive 1/2/3’). I recorded and transcribed interviews or recorded them with field notes; reasons for using notes rather than transcriptions included awkward or noisy interviewing locations, sensitive interviews and in one instance disability. Field notes were extensively augmented immediately after the interview. Personal communications and informal conversations also contributed.

Access to elite interviews often requires existing contacts in the field. 5 I had worked as a financial journalist after graduating and had encountered OFEX at the apogee of the market’s fortunes during the dot-com era. I also encountered PLUS while working as a jobbing copywriter to fund a PhD and a young family. My academic interest in the sociology of markets owes much to these experiences and, in due course, I came to recognize an intuition that the birth of the small-company markets in 1990s London was an episode worth documenting. I had maintained contact with one corporate advisor, a personal friend, who was able to facilitate introductions. I was also remembered by some market participants, notably Jonathan Jenkins who persuaded the family to cooperate, opening up the tight personal networks around the market. My position as former group member led to interviews that flowed easily, assuming shared languages and cognitive resources (Miller and Glassner, 1997) and yet I found myself distanced by over a decade of academic training and work, enjoying what Goodall (2010: 257) terms ‘perspective by incongruity’. I have reflected elsewhere on the process of data collection and writing in such a setting, as well as the responsibilities it incurs (Roscoe and Loza, 2019).

Interviews followed a strategy of oral history (Yow, 2005), seeking to elaborate individual careers and spark recollections of key events. Oral narratives make reference to cultural and moral norms and provide a rich source for a researcher seeking to unpack these issues. This article’s underlying historical-sociological method sought to access the – now lost – material dimension of these markets through the memories of participants, supplemented by other kinds of material. Interviews, suggests Perks (2010: 40), ‘have proved particularly effective at documenting the minutiae of repetitive daily routine and everyday practices, those which have often disappeared and might not otherwise be recorded’. Similarly, Yow (2005) argues that oral histories, built up through ‘active interviewing’ (Holstein and Gubrium, 1997), will go beyond the scope of public records and help the researcher to discern the power structures embedded within existing narratives. There are pragmatic motivations as well, for in the absence of letters, diaries and other such archival material – rarely maintained by organizations – interviews become an increasingly important source. For the present article, justifications and partialities may even be an advantage; oral history is particularly useful in unpacking organizational norms and culture (Perks, 2010) which surface incidentally in the telling of other, more political stories.

I made use of textual sources as a complement to interview accounts and a means of triangulation. Textual sources amounted to over 1000 pages and included newspaper articles, company documents, prospectuses and annual reports, newsletters and lobbying materials, regulatory disclosures, press releases, photographs and marketing materials. These resources offered an accurate chronology of events, additional insight into strategy, justification and motivation of firms and individuals, and information on the technical arrangements and ambitions of markets. Documents are in the most part backgrounded in the case study and are more systematically referenced in the narrative account of the markets’ formation available on an institutional repository (Roscoe, 2017). A draft of the narrative account was circulated to interviewees and provoked a further round of discussions.

Data collection and analysis ran concurrently, following a process of systematic combining, iterating between the existing literature and the evolving empirical understanding and analytical insights (Charmaz, 2006; Dubois and Gadde, 2002). Data were coded in nVivo, with codes motivated by the existing concerns of the STS-inflected study of markets and emergent themes in the data. As a strategy of following actors suggests, coding focused on specific individuals, episodes and technologies as well as practice, expertise and normative judgements. Crucially, normative statements were entangled with discussions of everyday practice and the infrastructure within which that took place. A corporate advisor might describe the obligations attached to preparing a company for market in terms of the practicalities of preparing the documentation, and the material shape and demands of that document. In order to follow the actors through the data it was necessary to take a phenomenological, rather than discursive, approach to the interview material; to treat accounts of artefacts and processes as representative of the lived experience of market participants (Cope, 2005). Normative claims were, therefore, treated as such and the two moral orders (and justifications) discussed below were abstracted by a reading across the codes. Competition is valorized across multiple interview transcripts and documents; the term intervention appears only once (in an interview with Jonathan Jenkins) but encapsulates a particular set of trading practices described by those participating in matched bargain trading or market-making. A coding summary is provided in Appendix 2.

Moral economies and trading technologies

The article considers the evolution of trading practices – and associated moralities – as technological and social change reshaped OFEX, from the early 1990s through to the late 2000s. The exchange went by three names during that period: it was established in 1991 as JP Jenkins Ltd, took the name OFEX in 1995 and was renamed PLUS in 2004. Each stage of the exchange’s development embodies a specific set of trading practices, embedded in particular material technologies and associated with a specific moral order, these latter usefully analysed in terms of Grossman et al.’s (2006) taxonomy of literal and abstract transparency. As JP Jenkins Ltd it undertook matched bargain trading, an archaic practice that stands as a counterfactual to the electronic training by that point common across the London markets (Pardo-Guerra, 2010). As OFEX, the market attempted, with limited success, to open itself up to competing market-makers. As PLUS, it employed sophisticated computer systems built by the American exchange NASDAQ to resist the encroachment of electronic ‘order book’ trading from the London Stock Exchange’s junior market AIM. The article explores the material architectures of markets as ‘generators’, offering temporalities, cognitive tools (ways of seeing and understanding in the market) and ways of organizing knowledge. In each case the exchange’s sociomaterial arrangements co-produced specific conceptions of ‘the right thing’. These moral orders remain sticky, persisting even after new sociomaterial arrangements begin to generate new market norms. The resulting story is one of temporary stability, overflow, contestation and reframing (Geiger and Gross, 2018).

The virtues of intervention: Matched bargains, notebooks and ‘my word is my bond’

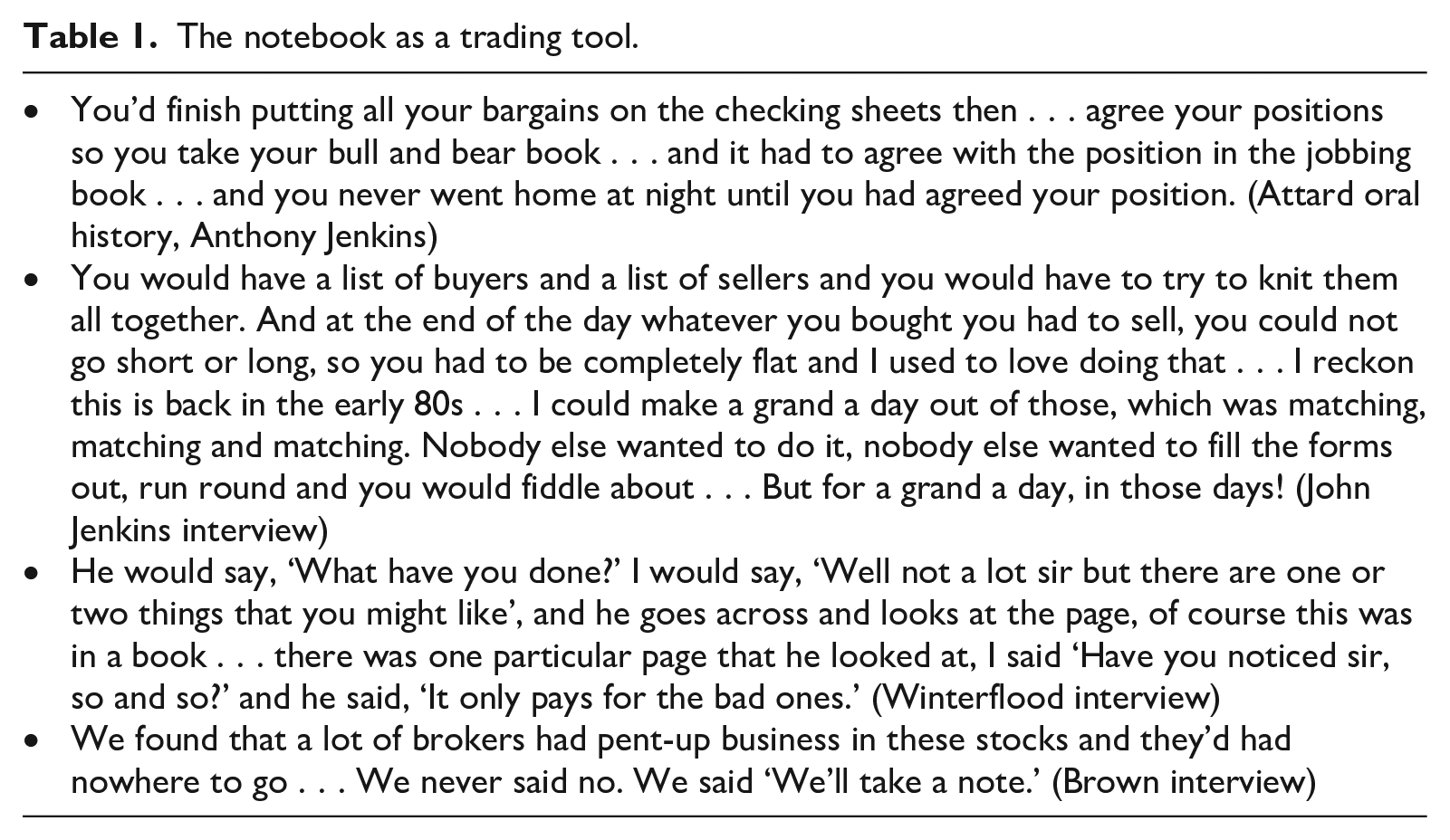

From the 1970s onwards the London Stock Exchange (LSE) allowed member firms to trade in unlisted securities (i.e. the shares of private companies) under its Rule 163.2 (later renamed Rule 535.2 and 4.2). This exemption allowed the LSE to be seen to be supporting the entrepreneurial aspirations of the UK by supporting smaller, growing firms, and at the same time discharging its regulatory responsibilities to more established listed companies. This trading took place within the LSE’s established sociomaterial architectures, conducted in the exchange’s great domed hall. Brokers circulated among ‘jobbers’ (the anachronistic title for market-makers) who stood at rickety ‘pitches’, wooden boards on which were chalked the prices of stocks. Trading was conducted through a complicated verbal ritual (Pardo-Guerra, 2010) anchored by the solid materiality of paper sheets, notebooks and account books. As Buckland and Davis (1989: 130) note, when dealing in smaller company stocks, ‘such modest volumes of stock are available as to render the concept of liquidity, if not meaningless, a very unlikely attribute of most OTC [over the counter] securities’; one can draw a stark contrast here between the illiquid market in junior stocks and the vast, hyper-liquid global bond markets, over-the-counter but anchored by phone and screen (Knorr Cetina and Bruegger, 2002). Low volumes necessitated ‘matched bargain’ trading, storing up orders and negotiating between buyers and sellers in return for a commission on the bargain. In these sets of trading practices the many notebooks function as generators: as a time generator, a generator of cognitive tools and a device for the organization of knowledge. Just as open outcry pits concentrated liquidity in time and place (Zaloom, 2006), so orders accumulated in the notebook, a space that coordinated chains of buyers and sellers, who might often wait some time before their order could be filled. The notebook (see Table 1) offered tools for making the market visible, both managing past transactions and organizing future sales and purchases, recorded and made visible so that they might be conducted and tallied up. As the quotations from John Jenkins and Paul Brown suggest, it was fiddly, unfashionable work, building up an order book through the slow accumulation of notes. ‘Noting’ and ‘fiddling’ are morally freighted practices here: assisting brokers with pent-up business, helping those with nowhere to go, even when the transaction would be unlikely and inconvenient. It also offered a means of surveillance and discipline, whether in the mundane daily process of checking and sorting, or the malevolent eye of Winterflood’s senior partner, returned from an unsuccessful lunchtime visit to the betting shop.

The notebook as a trading tool.

As the Rule 163 exemption survived the upheavals of 1986’s Big Bang and the move to electronic trading, so did the paper-based practices that surrounded it. When, on 11 February 1991, John Jenkins and his business partner Paul Brown launched JP Jenkins Ltd with a plan to trade unquoted stocks ‘over the counter’, these habits rolled into the new venture, ‘two guys and a sofa’ trading with pen, paper and phone (John Jenkins interview). Business depended on the ability to collect sufficient orders to match desired purchases and sales. ‘Taking a note’ was the central sociomaterial practice of this trading regime; Jonathan Jenkins, John’s son, remembers ‘I’ll take a note’ as the firm’s catchphrase. Muniesa (2008) suggests that automation forces the disclosure of taken-for-granted organizational norms, and the importance of the notebook became clear when the firm finally automated its trading practices, commissioning a bespoke system that simply mimicked the existing arrangements of notebook and pencil.

These sociomaterial arrangements are illuminating precisely because of their anachronism. They generate market practices and associated norms that valorize practices of intervention, and the associated belief that some form of intervention is required in order that less liquid markets function at all. Electronic trading, implemented across the LSE’s other markets, could supply cheap (understood in terms of small commissions and narrow spreads) and cost-effective exchange and settlement for the majority of stocks where reasonable supply and demand existed. The existence of a liquid market in standardized securities is itself a considerable sociological achievement depending upon a crowd of buyers and sellers and a degree of standardization of the traded commodity (Carruthers and Stinchcombe, 1999). In this case the paucity of orders for unquoted stocks together with the heterogeneity of financial instruments associated with them made it unlikely that transactions would take place without some kind of manual intervention. The labour of matching and physical intervention makes (performs) the market.

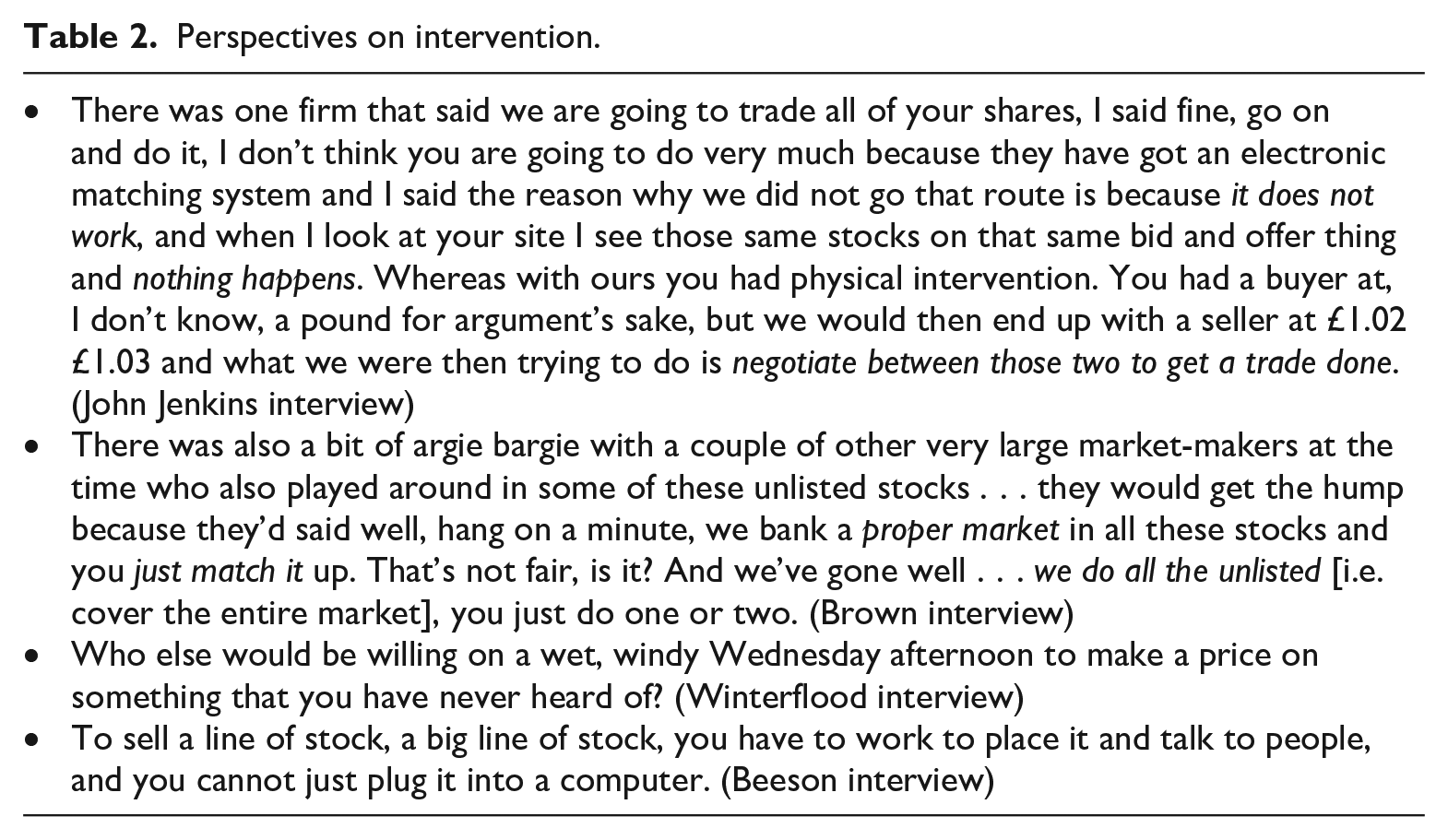

The notebook (and trading sheets and ledgers) – replicated in electronic trading systems built for the business as it became more successful – is a crucial part of a moral agencement valorizing interventionist practices in the market. The notebook, and the practice of taking a note, coordinated long trains of social relationships and negotiated the competing obligations of the work: honesty of trading, the need to make a profit, the physical complexity of paper-based share settlement and the obligations to support growing companies through the issuance of stock. The notebook, as generator, offered a sociomaterial space in which the social could be inscribed; it is through the mundane act of writing that the social was, in Muniesa’s (2008) terms, ‘folded’ into the notebook. One can contrast the anachronistic style of trading with electronic financial markets, theorized by Knorr Cetina and Bruegger (2002) as globally distributed microstructures held together by screens, telephones and voice boxes. The distinguishing characteristic of a microstructure is its synchronicity, and that appears to be missing here; the temporality enacted by the notebook is one of distance, rather than closeness. Like Preda’s (2006) tickertape, the notebook telescopes time as well as geography, allowing orders to sit until a counterparty can be found. It organizes knowledge, presenting the market in a particular way and demonstrating what is worth knowing (Dussauge et al., 2015), in this case the whereabouts of supply and demand, the people to whom orders are attached and the conditions under which they are issued, and the moral order within which trading should be conducted. Table 2 articulates perspectives on intervention, the sociomaterial order that underpins matched bargain trading. In order to get trades done negotiation is needed, argues Jenkins, while other actors draw attention to the moral force of making the market, and doing so on a wet, windy Wednesday afternoon; of working hard rather than letting the computer execute trades; and of covering the entire market. All of these quotes draw attention to the labour involved in these operations, and the implicit worthiness of ‘making’ the market, as a source of moral value and, of course, economic profit.

Perspectives on intervention.

Edging towards ‘competition’ and the stickiness of organizational morality

Matched bargain trading was most suitable for the smallest and most illiquid stocks. Slightly larger firms benefited from the attention of ‘market-makers’. Rather than matching stock and taking a commission, these traders seek to buy stock cheaply and sell it at a profit; they are obliged to make two-way ‘bid/offer’ (buy and sell) prices and show a ‘spread’ between the two. Market-makers are exposed to risk through price fluctuations in stock that they hold and through their legal and moral commitment to execute trades at prices offered. The standard sociomaterial practices for this kind of trading were established by the London Stock Exchange during the 1970s and 1980s (Pardo-Guerra, 2010); buy and sell prices are displayed on market screens, with trades conducted by telephone or electronic media. As JP Jenkins’ business grew and began to service larger firms, including recognized household names such as Weetabix, it matured naturally into a market-making operation with a profitable monopoly on smaller company stocks. Strategic moves by the London Stock Exchange, notably the launch of its own smaller-company exchange (AIM) in 1995, forced JP Jenkins to badge up its operations as OFEX. During the late 1990s OFEX metamorphosed into a small-scale, independent stock exchange dependent on new listings and external brokers. It became the venue of choice for many small-scale dot-com start-ups and was increasingly popular with retail investors.

There now occurred a moment of contestation between the existing paternalist-interventionist order and the competition-based logic of contemporary stock markets. Crucially, it was the changes in OFEX’s technical infrastructure of trading that rendered it subject to other forms of accountability and made interventionist trading practices hard to defend. OFEX had begun making prices widely available through a partnership with the Reuters news wire service, and yet was not living up to the mores of competitive organization embedded in electronic screens (Knorr Cetina and Bruegger, 2000; Zaloom, 2006). Regulators worried that, in the absence of competition among market-makers, retail investors were not enjoying ‘best execution’, that trades were not being transparently allocated to the cheapest bidder. In a single market-maker system this could not, by definition, be the case, and brokers taking work to the market were likely to ‘get a shot across our bows from the regulator by asking us have we given best execution’ (Hoodless interview). ‘Best execution’ emerges here as a regulatory mandate for a moral order based on competition (cf. Castelle et al., 2016) incompatible with the single market-maker, even though (as Hoodless subsequently makes clear) there was not enough profit in the market for two competing traders. Moreover, market folk-wisdom held that the perceived lack of liquidity stemming from a single market-maker discouraged institutional fund managers from investing in OFEX-quoted stocks. John Jenkins resisted the pressure for a while, aware of the limited profits available, but eventually gave in. The norm of competition – of abstract transparency – triumphed, and the material infrastructure of trading would be forced to catch up.

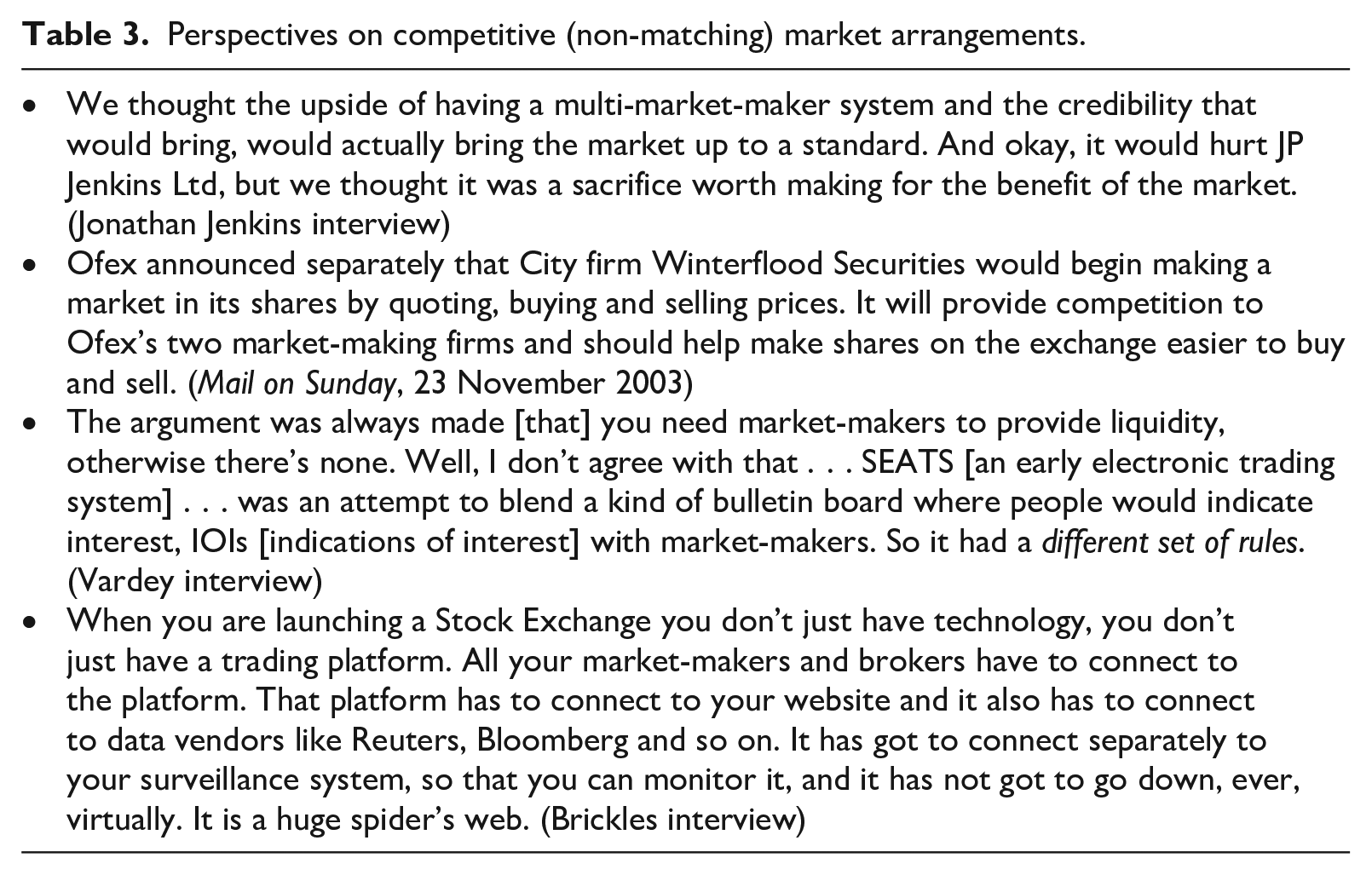

OFEX therefore raised funds of its own – £1.45m – and moved to open up the market by introducing competing market-makers; that is, to allow those wishing to transact a choice of execution. The exchange used the capital to develop the new systems necessary to facilitate the display of competing prices from multiple participants. Some in the community expected new business to follow, while others pointed to the need for a deeper technological reorganization. Table 3 illustrates how market actors expected, though in different ways, new systems to fundamentally change the operation of the market. There are normative statements and justifications at work, such as Jonathan Jenkins’ use of ‘sacrifice’ and ‘worth’ but also mundane expectations about credibility, ease and responsibility that accompany the affordances of the new technology. Vardey’s comment in particular highlights the entanglement of normative expectations about how a market should operate and the market’s sociomaterial arrangements. In sum, while the external forces of regulation and commercial pressure forced a change in the structure of the exchange, everyday market practices are embedded in the sociomaterial agencements of trading (Hardie and MacKenzie, 2007), and a heavy investment in technology is required to reproduce and stabilize these new practices. A stock market that wishes to constantly re-perform itself as a venue for competitive trading can only do so through the technical and material structures that mandate competitive market action (Castelle et al., 2016). OFEX’s new systems had limited success in terms of delivering competition. Practices of market making had, like matched-bargain trading, been well established in the pre-digital LSE, where ‘jobbers’ displayed buy and sell prices on wooden boards or ‘pitches’ on the exchange floor (Pardo-Guerra, 2019). OFEX’s market-maker system, ‘a very rudimentary connectivity mechanism which connected those few market-makers involved in trading OFEX stocks’ (Market executive 2), reproduced the norms of this kind of trading. It seems that despite the impetus towards competition the system did not do enough to upset the established agencements of trading; prices remained wide enough ‘to drive an 18 wheel truck through’ (anonymous comment) and the new market-makers justified their returns by pointing to the obligations they incurred by offering prices for all the stocks listed on the exchange.

Perspectives on competitive (non-matching) market arrangements.

Again, the notion of ‘generator’ is useful for theorizing this outcome. The new system performed and framed the market as a site encompassing the trading books of market-makers and their broker clients. It offers a temporality that is more immediate than that of matching, but far from instantaneous. It offers a more transparent, though not perfectly competitive, presentation of market knowledge in the form of multiple bid/offer prices displayed on the connected screens and reported through OFEX’s proprietary news service, Newstrack. This midway position comprised a moral order that hybridized notions of intervention and competition, of literal and abstract transparency (Grossman et al., 2006). It evoked both the best-execution defences of competitive order-processing via market-makers, and the reputational reassurances of the brokers network, tied to named individuals. In doing so, the material system reproduced the norms of intervention embedded in the notebooks, repeatedly justified by interviewees. It did not, as the Jenkins family hoped, usher in a new level of credibility. Instead, in valorizing the moral order based on intervention, entrenched in the powerful sociomaterial networks of trading (Latour, 1988) it made possible a market coup, a realignment of the primary business flow away from Jenkins to rivals such as Winterflood Securities, a prominent small-company market-maker. For the Jenkins family the move to competing market-makers jeopardized the only part of the business that had been reliably profitable, and in 2004 the family lost control of the business after a failed fundraising.

Competition arrives? New systems and dark pools

Large-scale electronic stock exchanges rely upon order book systems where traders lodge buy and sell orders and these are matched algorithmically. Electronic order books perform a moral order that valorizes efficiency; electronic matching of orders ensures low costs and narrow spreads (between bid and offer prices). These trading systems are used without exception for the stocks of larger companies where a much greater turnover of stock means that there is likely to be a congruence of buy and sell orders (Lee, 1998). For less liquid stocks, however, the decision to implement order books is politically fraught. During the early 2000s, the LSE sought to expand the operation of its order books into its junior markets and this provoked conflict with the existing market-maker community, who advocated intervention-based trading and, crucially, resented the fees charged by the LSE: ‘people hated the LSE. It was . . . vicious’ (Market executive 2).

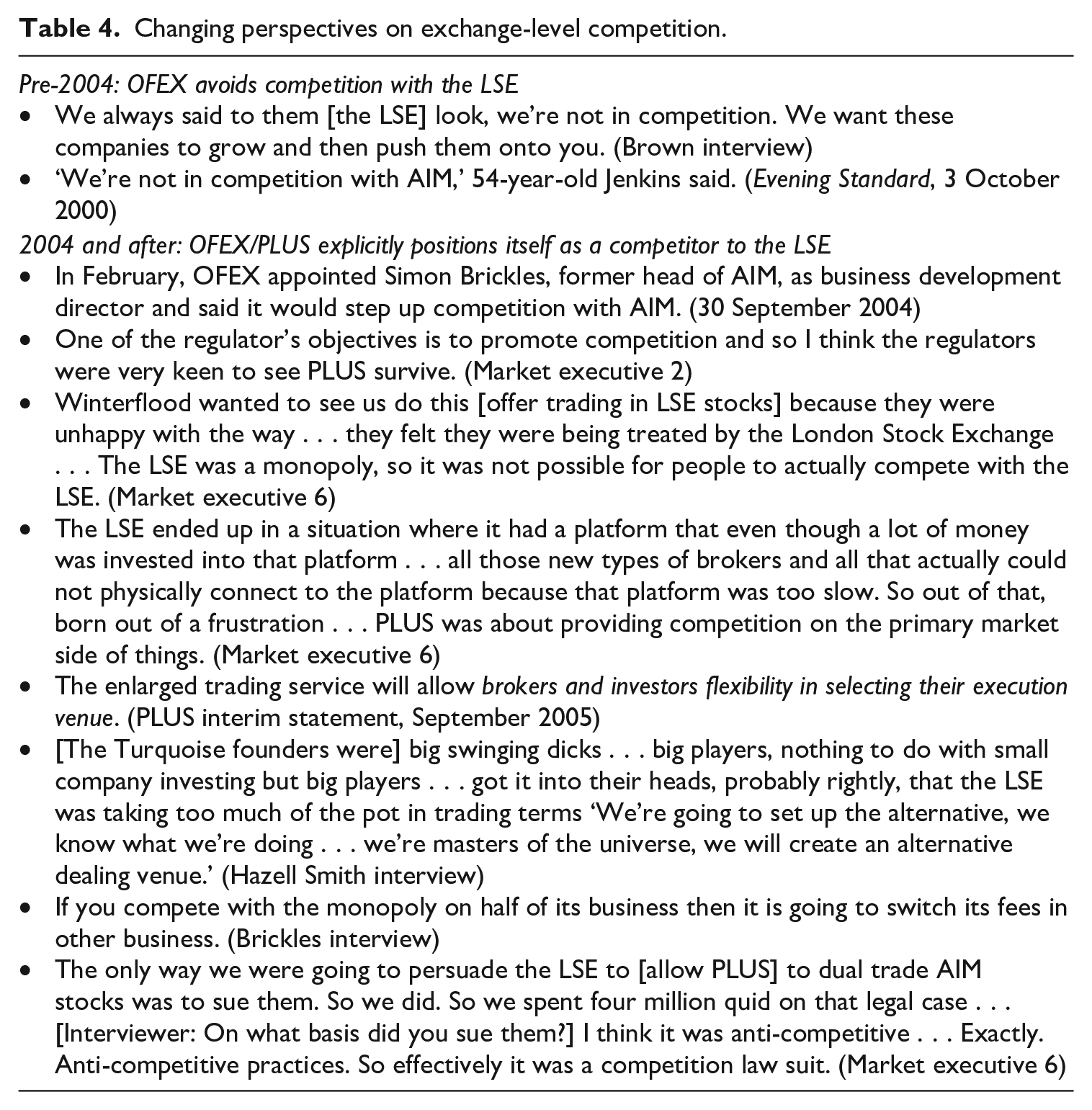

In 2004, Simon Brickles took over as chief executive of OFEX. He had previously been head of the LSE’s smaller company market AIM, where he had been committed to a disclosure-based, caveat emptor market. He now saw an opportunity to rebuild OFEX – now renamed PLUS – as a direct competitor to AIM. Table 4 shows the firm’s changing attitudes to competition with the LSE, a possibility that itself depended on European regulation that sought to create a market in stock exchange services. Before 2004, the management had been certain that competition with the LSE would be foolhardy, a ‘fight with the biggest gorilla in the room’ as one executive put it; under new management the market adopts a morally charged discourse of unseating a ‘monopoly’ and using legal action to overthrow ‘anti-competitive practices’ where the LSE was ‘taking too much of the pot’.

Changing perspectives on exchange-level competition.

A system able to challenge the LSE directly would require yet more investment in technical systems, and Brickles commissioned a £6.5m platform from American exchange NASDAQ. The sociological study of markets has long recognized that liquidity and competition are organizational, sociomaterial achievements (Carruthers and Stinchcombe, 1999; MacKenzie, 2009) and the new market infrastructure acted as generator for competition. It offered a synchronistic temporality, with simultaneous connection of market participants, data vendors and surveillance; it offered traders ways of making sense of the market through screens and workstations (cf. Knorr Cetina, 2005). It performs not just competition between market-makers but between market operators, subjecting market operators to the norms ascendant in the stock markets themselves, and increasingly ascendant in regulatory frameworks with the EU’s ambition to offer a market in markets. Alongside the market-maker driven service for smaller firms, PLUS now had the technological capabilities to compete with the LSE for market share of business conducted through order books and PLUS sought to make customer choice possible in a competitive market for exchange services.

This competition came to the fore in the autumn of 2007 through the short-lived and distracting proposal to establish a ‘dark pool’ (Lagna and Lenglet, 2020), a proprietary trading venue in direct competition to the LSE. In this episode, codenamed ‘Project Turquoise’, a number of senior UK executives of global investment banks came together with the idea of setting up their own lightly regulated trading system to take their business away from the exchange. By October, details were leaking out. On 6 October 2007 the Daily Telegraph ‘revealed’ that PLUS was negotiating the terms of a ‘takeover’ with Turquoise, and the Independent announced a ‘merger’. PLUS’s shares were suspended pending an announcement. But talks came to nothing, and the project had earned the nickname ‘Tortoise’ in the financial press. PLUS did eventually manage to make inroads into the LSE’s market share but was ultimately unsuccessful, derailed by strategic resistance from the LSE and the credit crisis of 2008.

This episode, together with PLUS’s longer-term ambition of competing with the LSE, is based upon the presence of a market infrastructure that has been constructed to produce competition. It is a performation of certain ideas about market function, and reproduces within itself a particular kind of normative worldview. Having secured its own materially embedded moral orders, where the intervention needed to make markets function – understood in terms of ‘making a market’ by buying, holding and selling stock – remained the primary obligation of market actors, PLUS could now reproduce and directly challenge the LSE’s automated order books, with everything that entailed. Traders choosing to use PLUS not only are entangled in a sociomaterial system that is predicated upon and reproduces competitive market relations, but also engages in higher-level competitive process taking place between exchanges. Competition overspills from the infrastructures of exchanges to the relationships between them.

Discussion: Sociomateriality and organizational morality

This article has presented a historical sociology of the founding and development of a small-scale, British stock exchange named OFEX. The case offers a rich empirical source for those wishing to explore the formation of markets. Concerns over the structure and organization of markets surface, as do the many factors that led to short- and medium-term success but eventual failure. The present article takes up a theme that emerged unexpected from the empirical material: the interrelation of market architecture, trading mechanism and the moral orders of the markets. It argues that sociomaterial assemblages, or ‘agencements’ (Callon, 2008), are a crucial part of the evolution of distinct moral orders – as the concept of sociomateriality recognizes the ontological intertwining of the social and the material, so it allows us to see how moral orders emerge in a dialectic between the social (practice, regulation, etc.) and the material (organizational structures, technological systems and everyday artefacts).

Reviewing the short and complex history of OFEX the article offers an ‘ecological reading’ (Mercier-Roy and Mailhot, 2019: 998) of the interplay between rival moral orders centring on intervention and competition, or literal and abstract transparency (Grossman et al., 2006). The first claims a lineage of practice from the face-to-face trading of the pre-electronic London Stock Exchange and depends upon a regulatory dispensation from the institution. It is embedded in notebooks (later computer-based) that coordinate buyers and sellers and help to perform a particular kind of moral work. Market norms are, as indicated by previous literature, reproduced by ritual and discourse (Abolafia, 1998; Brannan, 2017); this study shows that they are also made possible by the generative capacity (Preda, 2006) of the sociomaterial arrangements of the exchanges. In the second stage of the exchange’s evolution, discourse and regulation have come to endorse a mode of market interaction based on competition. Market-makers’ business practices and justifications point to earlier norms as their intervention-based strategies are reproduced by the material architectures of the market. OFEX’s management is impotent in the face of the durable agencements of trading and the justifications they generate. Only after a substantial further investment are the norms of competition fully instantiated in the exchange’s infrastructure, and then they begin to overflow, leading to competition between exchanges themselves.

The article’s central endeavour is to draw together several important insights from sociology and organizational theory. First, that markets are sites of political contestation where powerful actors impose their dominance on others in pursuit of ongoing profit (Fligstein, 1996); the STS-inflected study of markets upon which this article draws has begun to recognize the importance of material structures in reproducing such contestations (MacKenzie, 2018). Second, that markets are designed entities, rather than natural occurrences (MacKenzie, 2009), a theme now prominent in organization theory (Brunsson and Jutterström, 2018; Palo et al., 2020). Third, that social and political relations are compounded into the material: there is no material that is not social, and no social that is not material, writes Orlikowski (2007). The article recognizes that institutions are the result of the summing up of micro-level sociomaterial interactions (Latour, 2007) that comprise not only political struggles but also moral ones. Throughout the story of OFEX, the market’s material structures are constantly under negotiation, designed and redesigned by actors according to competing understandings of good practice. Market design (MacKenzie, 2009, 2018) is therefore a consequence of moral orders in the marketplace. But it is also a source of moral order: the study shows how material structures, densely patterned with social codes, organize conduct within the markets. The article theorizes these as ethical ‘generators’ (Preda, 2006), providing actors with the cognitive schemas and calculative tools for moral action. Conceptions of worth (efficiency or intervention) are not transcendent or a priori, nor are they purely embodied; it is not clear that they are even meaningful out of context; they are local and specific and entangled with the sociomaterial arrangement of the market. The study here makes a significant contribution to the economies of worth literature (Boltanski and Thevenot, 2006; Mercier-Roy and Mailhot, 2019) by establishing that moral orders within institutions are specific, local and limited to their context, be that a workplace, markets or organizations.

It follows, therefore, that organizations cannot be understood as morally toxic yet peopled by the occasional virtuous free spirit. Much current scholarship on morality in organizational settings would suggest just this, arguing that moral rectitude is dependent upon developing an individual, subjective ethical agency that is free from the corrosive restrictions of organizational accountabilities and bureaucratic structures (Ailon, 2019; Eggebø, 2013; Rhodes and Wray-Bliss, 2013). My account of the sociomaterial dimension of morality supplements Du Gay’s (2000, 2008) spirited rehabilitation of Weber, a contrary voice in this debate. Du Gay sees organizational settings as containing their own distinctive moral character, or ethics of office. To do the right thing is to do what the office demands, irrespective of one’s personal ethos. I have argued that such ethos of office – a local, specific moral order – is inscribed into the sociomaterial arrangements of the market, and that there is always a political and historical dimension to the design and organization of such arrangements. On this basis one must doubt whether it is possible for the critically minded, virtuous soul to exist at all: the constitutive entanglement of morals and materials would seem to preclude the kind of embodied and effectual ethics envisaged by critical scholars.

My argument suggests that notions of professionalization as a moral panacea are problematic. Durkheim (1957) exempts trade and industry from his systems of professional ethics, protesting that its loose organization means that an entire sector of society is left without a moral code. He, and others since, have advocated professional codes of conduct as a cure for moral turpitude (Hendry, 2001; Rubin and Dierdhorff, 2013). This approach neglects the ethically generative capacity of sociomaterial structures, positing morals as the property of atomized intellects, and its supposition that the manager can transcend the sociomaterial structures of moral decision making in organizations is problematic (Roscoe, 2020). On the other hand, it might be that Durkheim is unduly pessimistic on the moral codes of trade and industry: material arrangements are mechanisms by which individual sectors might achieve coordinated, if specific, moral capacity. Such a recognition has the potential to inform ongoing debates in organizational studies, notably the discussions of critical performativity that have featured prominently in this journal (Cabantous et al., 2016; Wickert and Schaefer, 2015). It shows that scholars wishing to make a difference in organizational culture should seek to influence the sociomaterial structures of the organization as well as its discourses and rhetoric; there are similar implications for managers wishing to organize in accordance with particular moral goals.

Organizational morals are necessarily variegated, as both Durkheim and Weber observed, ‘expressing distinctive ethical comportments’ (Du Gay, 2008: 132). A sociological approach that treats morals as social facts to be investigated is predicated on empirical work at the level of the institution rather than the individual. Hitlin and Vaisey (2013: 55) distinguish between ‘thin’ and ‘thick’ morality, the latter a ‘richer array of virtues and vices, like dignity, hospitality, exploitation, fanaticism, and piety . . . what kind of person (or society) it is good to be’. My account has focused on the second category: underlying understandings of how markets should function, reproduced in the sociomaterial apparatus of the exchange. OFEX’s history is shaped by a contest between two of these understandings. On the one hand, a paternalist vision of the market as requiring considerable, expensive human intervention for trades in growing companies to take place, justified by the contribution made to the national economy and structured by a literal transparency of visible network relations. On the other, a vision of free competition that embraces ‘best execution’, an abstract transparency, openness and efficiency, justified by the protection of eventual consumers. Thin morality, conceptions of what is appropriate in particular situations, flows from these deeper understandings: by the paternalist view it is unacceptable to exploit gullible investors, while these same must tread carefully in a competitive, caveat emptor market; the LSE is ‘hated’ on account of its restrictive practices and rent-seeking while Brickles’s attempt to establish ‘a high temple of capitalism’ is widely praised. These are moral facts (Durkheim, 1957). It is against this backdrop that one of OFEX’s chief executives – Jonathan Jenkins – could make his emotive claim, ‘we did what we thought was right for the market’.

The article therefore offers an organizational contribution to the growing ‘new sociology of morality’ (Hitlin and Vaisey, 2013: 54), a Weberian approach to the analysis of morals that explores not only historical context of specific moralities, but also the ‘social processes that create and sustain particular conceptions of morality’. More importantly, it argues that particular conceptions of morality inform not only social processes, but the material arrangement of organizations, and that this in turn reproduces and sustains moral orders. The article urges researchers to become sensitized to the dialectic between the material and the moral: to recognize that matter matters in our understanding of ethics and organizations.

Footnotes

Appendix

First-level data coding summary.

| Advisory work and responsibilities Amara Dhari Broking Episodes and anecdotes Episodes and anecdotes/Characters (multiple codes) Episodes and anecdotes/Competitors GXG and 535 Episodes and anecdotes/OFEX episodes Episodes and anecdotes/Petra Diamonds Episodes and anecdotes/Turquoise Family business and tensions Fees and costs History History/AIM founding and development History/Commodities boom History/Dot com mania History/JP Jenkins tail History/Newstrack History/OFEX 2004 placing History/OFEX as ISDX at ICAP History/OFEX founding and development History/OTC and Third Market History/PLUS decline and fall History/PLUS Markets Brickles and beyond History/USM and its closure Innovative practices Material architectures Material architectures/(Non)mechanization and digitization |

Material architectures/(Non)mechanization and digitization/News and market information Material architectures/(Non)mechanization and digitization/Settlement Material architectures/(Non)mechanization and digitization/Trading Material architectures/Documents Over-promoted Performativity Performativity/Performative practices and conventions Performativity/Politics of performativity Regulation Regulation/1980s sell-offs, Big Bang, bull market, etc. Regulation/AIM rules Regulation/European regulation Regulation/FCA (and FCA killing off markets) Regulation/LSE monopoly, restrictive practices, challenges Regulation/LSE Rulebook Regulation/OFEX regulatory position Reputation and legitimacy Role UK plc Running a capital market Running a capital market/Compliance and supervision Running a capital market/Improving competition Running a capital market/Institutional investors Running a capital market/Internationalization Running a capital market/Liquidity |

Running a capital market/Private investors (Mrs Miggins) Running a capital market/Raising money (advisory work) Running a capital market/Revenue streams and costs Running a capital market/RIE Running a capital market/Tax advantages Smaller companies Social context Social context/Apprenticeships Social context/Hard times back in the day Social context/LSE as a club Social context/Negative sentiment and general criticism Social context/Networks and information Social context/Political lobbying Social context/Promoting the market Trading and market making Trading and market making/Corporate broking Trading and market making/Public relations Trading and market making/Sharp practices Values and valuation Values and valuation/A good business (advisory) Values and valuation/Affective content Values and valuation/Expertise Values and valuation/Making a fortune Values and valuation/Market data as valuable Values and valuation/Market valuations and fees Values and valuation/Mores and responsibilities |

Acknowledgements

I have greatly benefited from the comments of three anonymous reviewers and from the support and guidance of Dr Timothy Kuhn, acting editor for this article. I am indebted to my colleagues in the AGOG group at the University of St Andrews, particularly Dr Shona Russell and Dr Francois-Regis Pouyou, for comments on an early draft. Early ideas were explored at the Critical Finance Conference, Leicester, 2017, and the Chains of Value workshop, Edinburgh, 2017. I am grateful for comments and thoughts on these occasions. Most of all, I would like to thank all those who gave me time and shared their memories and scrapbooks, especially the Jenkins family, who were extremely generous with time during a difficult period. Errors and omissions remain mine alone.

Funding

The author disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by a Leverhulme Trust Research Fellowship