Abstract

This study critically examines the threshold effects of exchange rate dynamics on the influence of public debt on international trade across Sub-Saharan Africa (SSA). Utilising the System Generalised Method of Moments (SGMM) alongside dynamic threshold estimation on panel data spanning 2000–2023, the analysis uncovers the relationships between external, domestic and total public debts and trade performance. The findings demonstrate that all categories of public debt exert a significant negative influence on trade, with total public debt imposing the most pronounced constraint. Importantly, exchange rate depreciation emerges as a critical catalyst, intensifying the adverse trade effects of public debt. The study identifies precise exchange rate thresholds at which external, domestic, and total debts begin to significantly hinder trade flows. These insights reveal the imperative for SSA policymakers to adopt integrated approaches encompassing sustainable debt management, exchange rate stabilisation through robust monetary frameworks, enhanced domestic revenue mobilisation and strengthened regional cooperation to mitigate debt vulnerabilities and catalyse resilient trade growth.

Introduction

International trade remains a critical driver of economic development in Sub-Saharan Africa (SSA), offering opportunities for growth through trade liberalisation and deeper global integration. Liberalised trade fosters efficiency by exposing firms to competition, stimulates innovation, and facilitates access to advanced technologies and resources (Baccini et al., 2022). Export earnings further generate foreign exchange that can finance investments in infrastructure, education, and health, laying a foundation for long-term welfare (Yang et al., 2024). Yet, these gains are increasingly conditioned by two important factors: the burden of public debt and the management of exchange rate regimes (Edo, 2024).

The relationship between public debt and trade in SSA is complex and often dual-edged. On one side, debt-financed government spending can provide a short-term stimulus, increase productive capacity and potentially raise export volumes. On the other hand, excessive indebtedness risks crowding out private investment and raising interest rates, thereby stifling export competitiveness (Ma & Abruzzian, 2022). High debt servicing obligations often divert funds from essential infrastructure and social programs that underpin trade performance. As of 2021, the SSA region’s debt-to-GDP ratio stood at 62.1%, or roughly $702 billion, underscoring persistent fiscal vulnerabilities (International Monetary Fund [IMF], 2024).

Equally important is the composition of debt. Domestic borrowing, typically held by local institutions, can restrict credit availability to firms, limiting export production (Ojeka et al., 2024). Conversely, external debt, usually foreign currency-denominated, exerts pressure on exchange rates and exposes economies to repayment risks that reduce import capacity (Islam & Nguyen, 2024). This reliance on external borrowing heightens exposure to global shocks, raising concerns about trade stability.

Exchange rate regimes further shape SSA’s trade performance. Fixed regimes offer predictability for international transactions but risk overvaluation, which erodes export competitiveness, while undervaluation makes imports cheaper, dampening domestic production (Samunderu, 2024). Flexible regimes, by contrast, permit automatic adjustments that can enhance export competitiveness when domestic currencies depreciate. However, excessive volatility undermines investor confidence, escalates repayment costs for foreign-denominated debt, and may trigger capital flight (Aladejare, 2023; Dvoskin & Landau, 2024). Thus, governments often deploy monetary tools and foreign reserves to stabilise currencies, though such measures are not always sustainable.

The interaction between debt and exchange rates produces further complexity. Depreciating currencies may partly offset high external debt burdens by boosting exports, though beyond certain thresholds, the benefits dissipate. Studies indicate that external debt levels above 50%–55% of GDP significantly impair trade performance, particularly in economies with fixed regimes lacking adjustment mechanisms (Rahman et al., 2019). Floating regimes, while offering some buffer, can exacerbate inflationary pressures and destabilise macroeconomic conditions when paired with large domestic debts (Dufrénot, 2023).

Failure to address these dynamics carries heavy costs. Persistent debt and currency instability may depress investment, slow growth, and deepen poverty. Indeed, SSA’s modest 3.4% growth in 2021 already lagged behind other regions, with projections warning of potential annual GDP declines if fiscal challenges persist (African Development Bank, 2024; World Bank, 2023).

Despite a rich literature on debt sustainability and exchange rate volatility, research rarely integrates their combined effects on trade flows. Recent analyses underline the importance of stable exchange regimes for growth (Klutse et al., 2022) and highlight how rising external debt constrains trade competitiveness (Edo et al., 2020). Yet, gaps remain in identifying precise threshold effects and context-specific implications for SSA.

This study, therefore, advances the debate by examining how exchange rates moderate the impact of public debt thus both domestic and external, on trade flows across the region. Also, employing dynamic panel techniques, it seeks to uncover nonlinearities and critical thresholds that either amplify or mitigate the effect, offering policymakers actionable insights for balancing macroeconomic stability with trade competitiveness.

Literature

Theoretical Review

This study situates itself within emerging debates on sustainable fiscal practices and macroeconomic stability in SSA, drawing primarily on two debt-related frameworks: the optimal debt theory and the debt overhang theory. The optimal debt theory posits a non-linear relationship between debt and growth, suggesting that moderate debt levels can stimulate development through productive investment, while excessive debt yields diminishing or negative returns (Corhay et al., 2023). Despite its elegance, the theory faces practical constraints in identifying precise debt thresholds and accounting for external shocks. Nevertheless, it remains valuable for assessing SSA’s diverse debt profiles, particularly in evaluating how surpassing optimal debt levels may weaken trade competitiveness depending on the composition of debt, either domestic or external.

Complementing this is the debt overhang theory, which emphasises the adverse implications of unsustainable debt. Thus, excessive debt burdens foster expectations of future austerity and higher taxation, discouraging private investment and stifling productivity-enhancing activities (Gan et al., 2022). This pessimism not only suppresses growth but also constrains trade as firms delay expansion and resources shift toward debt servicing. Although it highlights systemic consequences and the need for corrective measures, the theory struggles with defining unsustainable debt in heterogeneous economies (Joy & Panda, 2020).

To fully capture trade dynamics, this study integrates exchange rate considerations through the J-Curve hypothesis and the Marshall-Lerner condition. The J-Curve suggests that currency depreciation may initially worsen trade balances before eventual improvement due to delayed price elasticity effects (Parray et al., 2023; Trofimov, 2023). Meanwhile, the Marshall-Lerner condition posits that depreciation improves trade only when combined import and export elasticities exceed unity (Soliman, 2024). Although challenged by estimation difficulties, these models extend the analysis beyond debt, highlighting how fiscal and exchange rate policies jointly shape SSA’s trade performance.

This study expands upon the optimal debt theory by demonstrating that in SSA, the trade effects of public debt cannot be fully understood in isolation but are critically moderated by exchange rate dynamics, thereby integrating debt and trade theories into a unified analytical framework.

Empirical Review

The interplay between exchange rate dynamics and public debt composition has been widely examined across both developed and developing economies, offering a nuanced empirical foundation for understanding their implications on international trade. In advanced economies, scholars such as Liu (2024) in China and Itskhoki and Mukhin (2021) in Japan demonstrate that exchange rate fluctuations exert substantial influence on import and export activities, ultimately shaping trade performance. In contrast, research in developing contexts often underscores vulnerabilities stemming from volatility and debt burdens. Ouattara (2023) and Warnes (2022), for instance, emphasise the detrimental effects of exchange rate instability on trade in Turkey and Argentina, while Abimbola et al. (2023) confirm similar outcomes across ECOWAS countries.

Methodological approaches in the literature reveal diverse strategies to disentangle these effects. Abimbola et al. (2023) employed a Panel ARDL framework, which captures both short- and long-term impacts while mitigating endogeneity. Similarly, Lal and Rai (2022) and Hidayah (2024) applied SVAR models to assess the dynamic effects of exchange rate changes in Russia, China, and Japan. Truong et al. (2022) advanced the discussion using threshold regression to expose non-linear and asymmetric relationships in Vietnam. Meanwhile, case studies by Ouattara (2023) and Warnes (2022) provide country-specific insights, illustrating the heterogeneous consequences of exchange rate volatility.

Parallel to exchange rate studies, significant scholarship has explored the implications of public debt composition for trade. Marie and Moslem (2023) argue that channelling public debt into productive investment bolsters the trade balance, while Ostrovskaya (2019) highlight that well-managed borrowing can enhance international creditworthiness. Yet, as Huang et al. (2018) note, high public debt often crowds out private investment, particularly in industries reliant on external finance. Zhang (2017) further situates debt dynamics within the broader framework of global growth, linking borrowing to structural changes and resource distribution, all of which shape trade flows.

Exchange rates, meanwhile, affect not only trade volumes but also competitiveness, profits, and costs. Volatility introduces uncertainty, raises hedging expenses, and disrupts pricing strategies, leading to shifts in trade patterns (Hidayah, 2024; Liu, 2024). Inflation compounds these effects: high inflation may diminish exports and increase imports, while low inflation tends to support export expansion (Liu, 2024). Sectoral evidence suggests that real exchange rate fluctuations particularly harm agricultural exports, though regional integration tools such as free trade agreements (FTAs) and the adoption of stable currencies like the Euro have been shown to mitigate volatility and enhance flows (Abimbola et al., 2023).

The debate surrounding exchange rate management thus centres on striking a balance between flexibility and stability. Proponents of flexibility underscore its role in allowing market-driven adjustments, while advocates of stability highlight its importance for reducing uncertainty and sustaining investor confidence. Empirical studies confirm that country-specific contexts significantly shape outcomes. Ouattara (2023) documents that sudden exchange rate jumps can sharply reduce exports, while Lal and Rai (2022) show, namely SVAR models, that real exchange rate fluctuations strongly influence export volumes. Itskhoki and Mukhin (2021) add complexity by demonstrating that devaluation can have both positive and negative effects depending on the composition of value-added trade.

A further dimension concerns the threshold effect. Truong et al. (2022) reveal that exchange rate volatility often harms trade balances in the short run but may prove beneficial over longer horizons as price adjustments take effect. Ormaechea (2020) underscores that large depreciations significantly increase public debt burdens, with stock-flow adjustments reaching up to 1.2% of GDP. Cross-regional analysis by Ouhibi and Hammami (2020) shows striking differences: while European countries record a positive association between exchange rate movements and debt, SSA experiences the reverse, with adverse consequences for trade.

The divergences in these findings stem partly from methodological choices and partly from structural heterogeneity. Models such as Panel ARDL, SVAR, and threshold regressions capture different temporal and dynamic aspects, shaping conclusions. For instance, ARDL models excel in separating short-run disequilibria from long-run equilibria, whereas SVAR frameworks trace lagged responses to shocks. Similarly, threshold regressions uncover non-linearities otherwise overlooked. Beyond methodological differences, structural conditions, including inflation histories, trade openness, institutional quality, and levels of dollarisation, moderate the transmission of exchange rate effects. In contexts lacking robust financial markets, limited hedging capacity amplifies short-run trade volatility (Itskhoki & Mukhin, 2021).

These findings imply that exchange rate dynamics and debt composition exert intertwined and context-dependent effects on trade. Particularly in SSA, where institutional fragilities and debt vulnerabilities are acute, the complexity of these interactions demands approaches sensitive to non-linearities and region-specific thresholds. Accordingly, this study advances the debate by employing a dynamic threshold modelling strategy, capturing both time-varying effects and critical inflexion points. Such an approach promises deeper insights into how exchange rate fluctuations shape trade outcomes, thereby offering more targeted and empirically grounded policy recommendations for promoting sustainable growth and trade integration.

Methodology

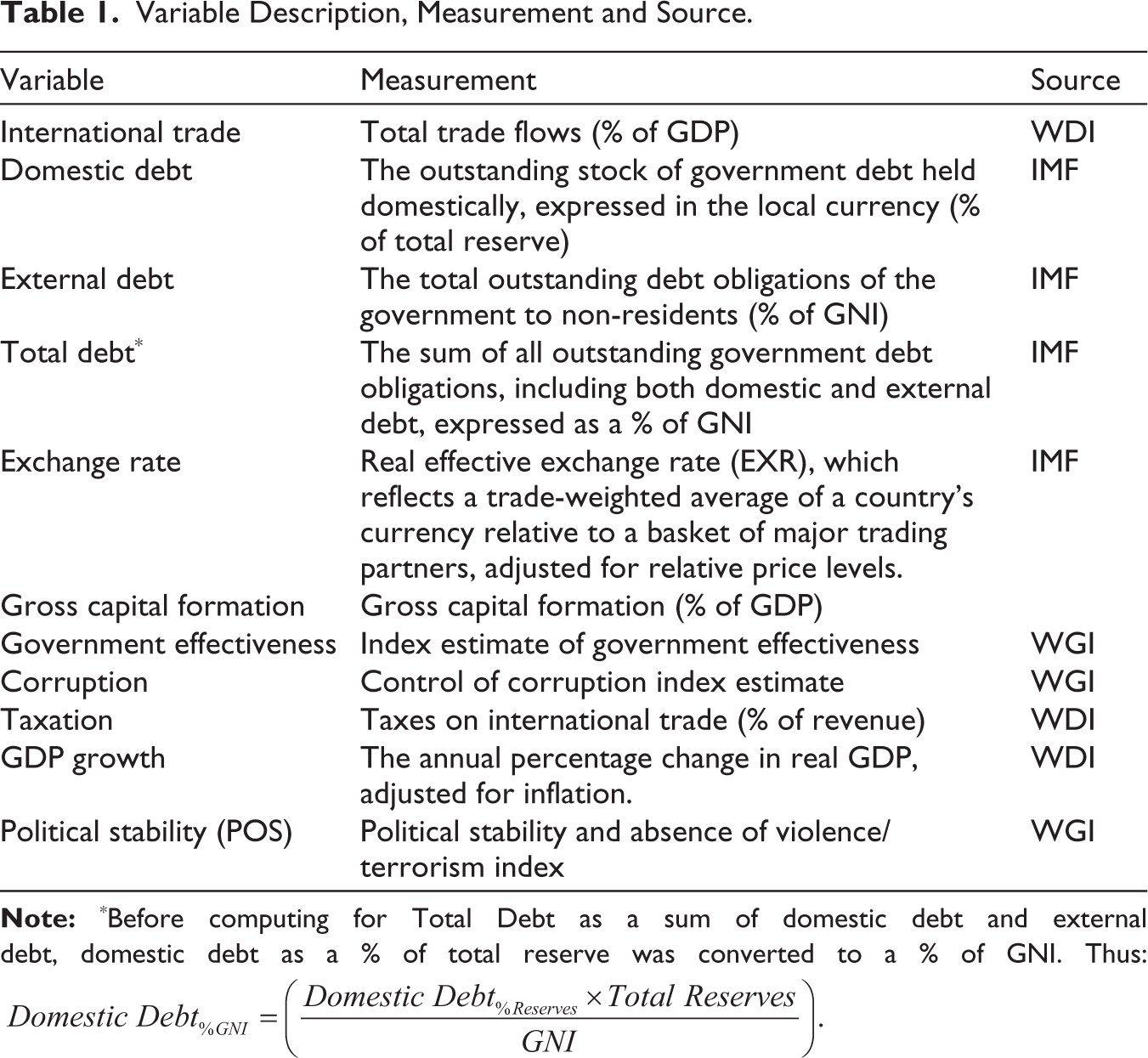

This study employs annual panel data from 2000 to 2023, covering the ten SSA economies with the highest IMF credit exposure, collectively representing 67% of Africa’s debt stock 1 (Afrexim Bank, 2024). Their varied economic structures provide a robust basis for analysing how public debt composition influences trade. Data were drawn from authoritative sources, including the World Bank’s World Development Indicators, the IMF, and the Worldwide Governance Indicators, to ensure accuracy and comprehensive variable coverage. This 24-year span, dictated by data availability, captures critical regional debt and trade dynamics while avoiding duplication across databases. Table 1 provides the variable description, measurement and expected signs.

Variable Description, Measurement and Source.

Justification of Controlled Variables

To ensure robustness, control variables were selected based on theoretical and empirical relevance to international trade. Gross capital formation reflects domestic investment capacity, shaping productive potential (Edo, 2024; Ormaechea, 2020). Government effectiveness captures policy quality and trade-supporting infrastructure (Abdulhamid et al., 2024), while corruption undermines competitiveness by raising transaction costs (Edo, 2024). Taxation affects firm incentives and global integration (Zhang, 2017), GDP growth indicates macroeconomic performance and trade volumes (Warnes, 2022), and political stability enhances predictability and investor confidence (Okara, 2023). Institutional quality is proxied by Government Effectiveness, Control of Corruption, and Political Stability dimensions most directly linked to trade, while excluding other Worldwide Governance Indicators to prevent multicollinearity (Marie & Moslem, 2023). This parsimonious yet rigorous selection ensures reliable isolation of debt and exchange rate effects.

Econometric Model

The analytical framework adopted for this study is the optimal debt theory expressed through an expanded equation that integrates exchange rates, public debt (domestic, external, and total), and international trade. By treating international trade (IT) as the dependent variable influenced by these factors. The framework below establishes the relationship while incorporating the potential impact of debt composition and exchange rate fluctuations.

Where, IT0 represents the trade level without the influence of debt or exchange rates. Ddom, Dext, Dtot represents domestic debt, external debt, and total debt, respectively. The coefficients (λ1, λ2, λ3) capture the sensitivity of trade to domestic, external, and total debt. Also, φ is the exchange rate sensitivity of trade, while EXR is the real effective exchange rate, where depreciation may increase exports but reduce imports, depending on elasticities.

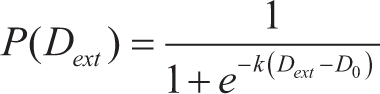

The δ1.P(Dext ).F(Dext ) expresses the negative impact of external debt distress on trade. Where the probability of distress from external debt, modelled as:

The distress cost function is expressed as:

Furthermore, δ1 is the weight capturing the impact of external debt distress on trade. Z is the other factors that affect external debt servicing and trade balance. δ2 is the sensitivity of trade to interest rates.

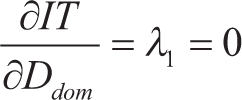

Considering the optimal debt composition (D*dom,D*ext) that maximise international trade, the first order condition is set as:

This study employed the two-step System GMM estimator, which integrates difference and level GMM to enhance efficiency in short panels with many cross-sections. The method addresses endogeneity, reverse causality, and omitted variable bias by using lagged levels and differences as internal instruments, ensuring consistent estimates even with endogenous regressors (Blundel & Bond, 2023; Cheng et al., 2024). It also corrects weak instruments and autocorrelation while capturing the dynamic nature of debt–trade interactions (Garfatta & Zorgati, 2021). Robustness was confirmed through the Hansen test for instrument validity and the Arellano-Bond AR(2) test for autocorrelation. Although traditionally used when N > T, recent studies extend its application where T > N, provided instrument proliferation is managed (Saygın & İskenderoğlu, 2022; Yayi, 2023). Following this practice, the study restricted instrument use and applied diagnostic tests, ensuring the reliability and validity of findings, consistent with prior research in SSA and other regions (Ledhem & Mekidiche, 2021; Rahman et al., 2019). The general equation for the main effect is established as:

For the moderating effect, the interaction of debt and exchange rate is introduced into the model and expressed as:

Where ITit is the dependent variable, thus international trade for cross-section i at time t. Debtit is the independent variable; thus, debt consists of domestic debt, external debt, and total public debt for cross-section i at time t. EXRit is the independent variable exchange rate for cross-section i at time t. Zi,t represents the controlled explanatory variables for cross-section i at time t. λ and β1 – β4 are the coefficients for the lagged dependent, explanatory variables, and controlled variables, respectively. The εit is the error term.

To establish the threshold level of exchange rate that triggers the significant impact of public debt on international trade in SSA, the study utilised the dynamic threshold technique due to its ability to capture non-linear relationships and structural breaks in panel data. It allows for different dynamics above and below a specified threshold, providing a deeper understanding of how variables interact under varying conditions (Barassi et al., 2023). This model also accommodates heterogeneity across entities and over time, making it flexible and robust for diverse datasets (Wang & Li, 2023). The general dynamic threshold models for the study are specified as follows.

Where yit is the international trade (IT). xit represents domestic debt (Ddomit), external debt (Dextit) and total debt (Dtotit) and qit is the exchange rate. I (.) is an indicator function that equals 1 if the condition is true and 0 otherwise. γ is the threshold value to be estimated. β1 and β2 are the coefficients below and above the threshold, respectively. Z it is a vector of control variables (inflation, GDP growth, political stability). δ is the vector of coefficients for the control variables and εit is the error term. Empirically, the models are expressed as.

Findings and Discussions

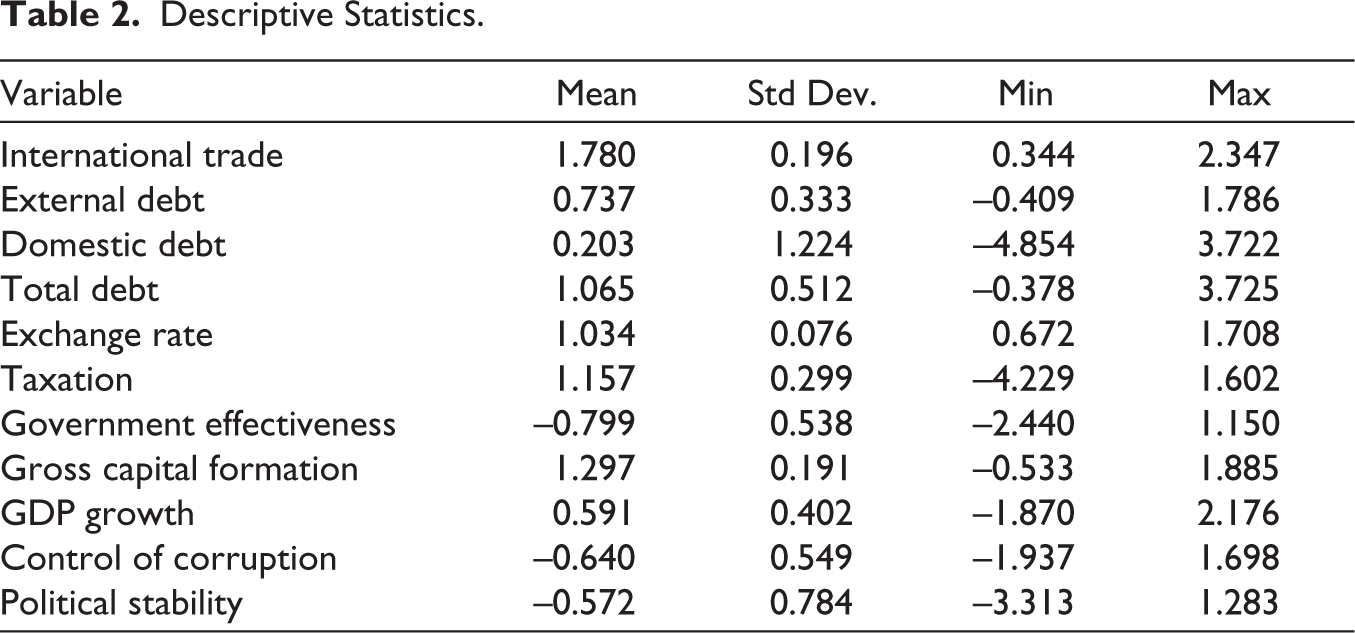

Table 2 presents descriptive statistics for SSA, offering key insights. International trade shows a strong mean of 1.78 with low variability, underscoring robust global engagement. External and total debt (0.737 and 1.065) indicate moderate borrowing with notable variation, while domestic debt (0.203) reveals diverse reliance on internal financing. A stable exchange rate (1.034) supports investor confidence. Taxation (1.157) varies widely, reflecting inconsistent policies. Governance indicators, government effectiveness (–0.799) and control of corruption (-0.640) remain low, highlighting institutional weaknesses. Despite this, gross capital formation (1.297) signals strong investment, though GDP growth (0.591) varies, influenced by political instability (-0.572). Appendix Figure A1 illustrates trade–debt trends.

Descriptive Statistics.

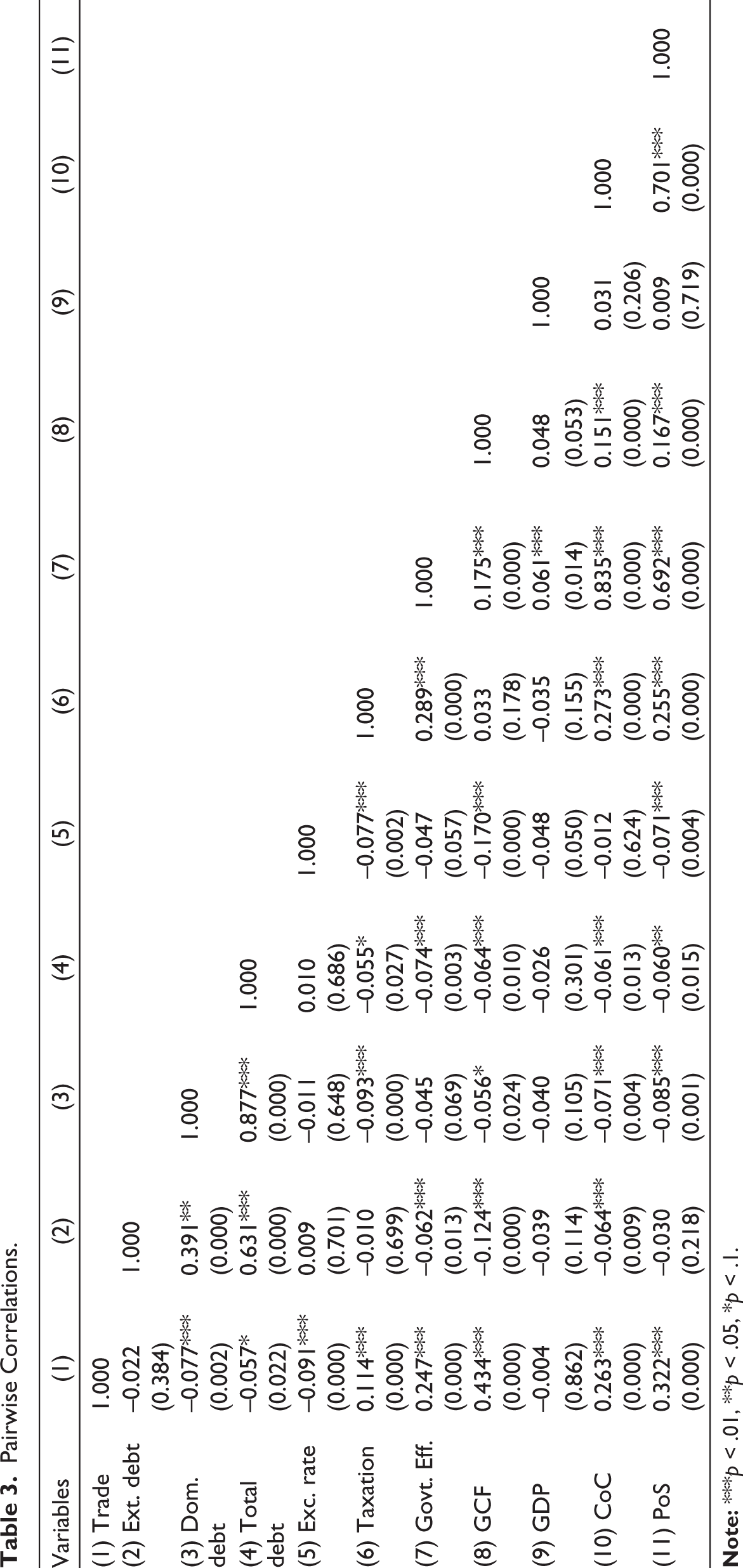

Table 3 highlights the trade dynamics in SSA. External debt exhibits a weak negative correlation (-0.022), while domestic (-0.077) and total debt (-0.057) reveal stronger adverse links, suggesting debt-driven crowding-out of trade-enhancing investment. The negative association with the real exchange rate (-0.091) indicates that appreciation undermines competitiveness. Conversely, positive correlations with taxation (0.114), government effectiveness (0.247), and gross capital formation (0.434) highlight the role of sound fiscal policy and capital investment. Notably, control of corruption (0.263) and political stability (0.322) strongly suppsort trade. Collectively, these findings provide a preliminary insight before the causal estimations.

Pairwise Correlations.

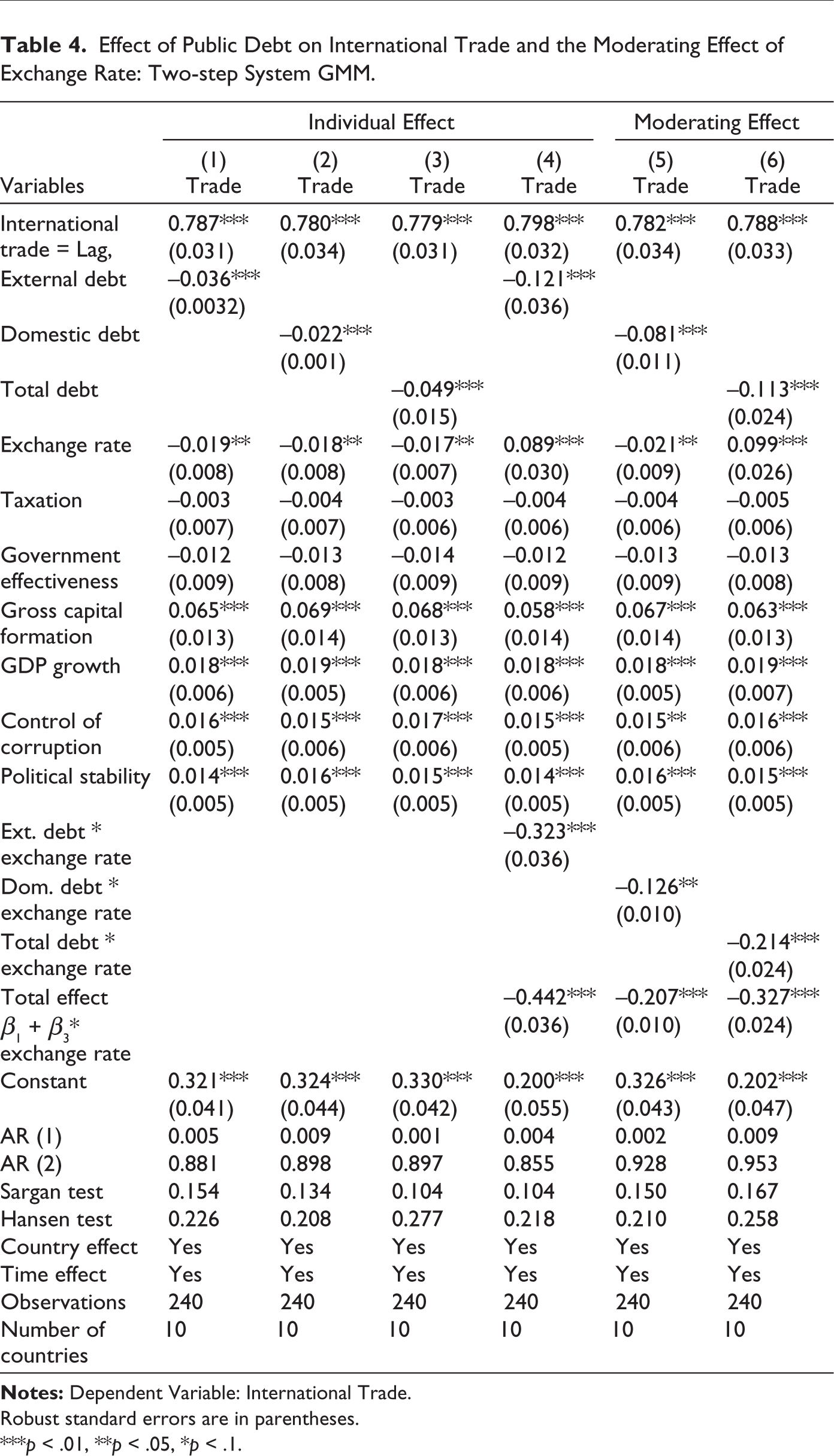

Effect of Public Debt on International Trade and the Moderating Effect of Exchange Rate

The two-step System GMM regression results presented in Table 4 provide compelling evidence of the adverse impact of public debt composition and exchange rate dynamics on international trade in SSA. Both external and domestic debt are found to significantly constrain trade, with coefficients of -0.036 and -0.022 at the 1% and 5% levels, respectively. Total public debt exerts an even larger negative effect (-0.049), reinforcing the notion that excessive borrowing diminishes the fiscal space available for investment in trade-enabling infrastructure and institutions. These findings support the debt overhang hypothesis, whereby debt burdens discourage productive investment and undermine trade potential. They align with Ojeka et al. (2024), who observed that external debt in SSA significantly hampers domestic investment.

Effect of Public Debt on International Trade and the Moderating Effect of Exchange Rate: Two-step System GMM.

Robust standard errors are in parentheses.

***p < .01, **p < .05, *p < .1.

Exchange rate dynamics further exacerbate these constraints. Across all models, the exchange rate variable records significant negative coefficients (-0.019, -0.018 and -0.017). In a region where most currencies chronically depreciate against the US dollar, such instability raises import costs, erodes export competitiveness, and intensifies inflationary pressures. This finding corroborates Abdulhamid et al. (2024), who linked exchange rate instability in SSA to persistent trade deficits and macroeconomic imbalances.

A striking result concerns the interaction effects. Exchange rate depreciation markedly worsens the negative impact of debt on trade. For external debt, the moderating effect is substantial (-0.323), suggesting that currency depreciation amplifies debt overhang effects by escalating servicing costs. Similar dynamics are evident with domestic debt (-0.126) and total public debt (-0.214). This interplay reflects SSA’s vulnerability to macroeconomic instability, where volatile currencies magnify the trade-inhibiting effects of debt. Aladejare (2023) highlighted similar dynamics, noting that depreciation-driven increases in debt servicing often divert resources from trade-supportive investment. The total combined effects, with coefficients of -0.442 for external debt, -0.207 for domestic debt, and –0.327 for total debt, reinforce the gravity of these interlinkages. These results echo Aman et al. (2022), who found that indebted economies with unstable currencies face reduced export competitiveness and rising import costs.

The results also confirm the theoretical persistence of trade. The lagged trade variable is consistently positive and significant, underscoring path dependence in trade performance, consistent with Krugman’s (1988) argument on the cumulative causation of trade growth. Gross capital formation also significantly boosts trade, reflecting the role of investment in productive capacity and infrastructure. Carrasco and Tovar-García (2021) similarly noted that higher capital accumulation fosters export competitiveness. GDP growth positively influences trade outcomes, reflecting the interplay of rising production, increased demand, and global integration (Taha et al., 2023). Furthermore, institutional factors matter; both control of corruption and political stability significantly enhance trade performance. Okara (2023) emphasises that good governance and stable political environments facilitate trade by improving investor confidence and institutional efficiency.

The diagnostic tests confirm the robustness of these results. The absence of significant first-order or second-order autocorrelation, coupled with valid Sargan and Hansen test results, validates the reliability of the instruments. The inclusion of country and time effects addresses unobserved heterogeneity, further strengthening the estimations. The robustness checks using fixed effects with Driscoll–Kraay standard errors yielded consistent findings, mitigating concerns over heteroskedasticity, autocorrelation, and cross-sectional dependence (See Appendix Tables A1 and A2).

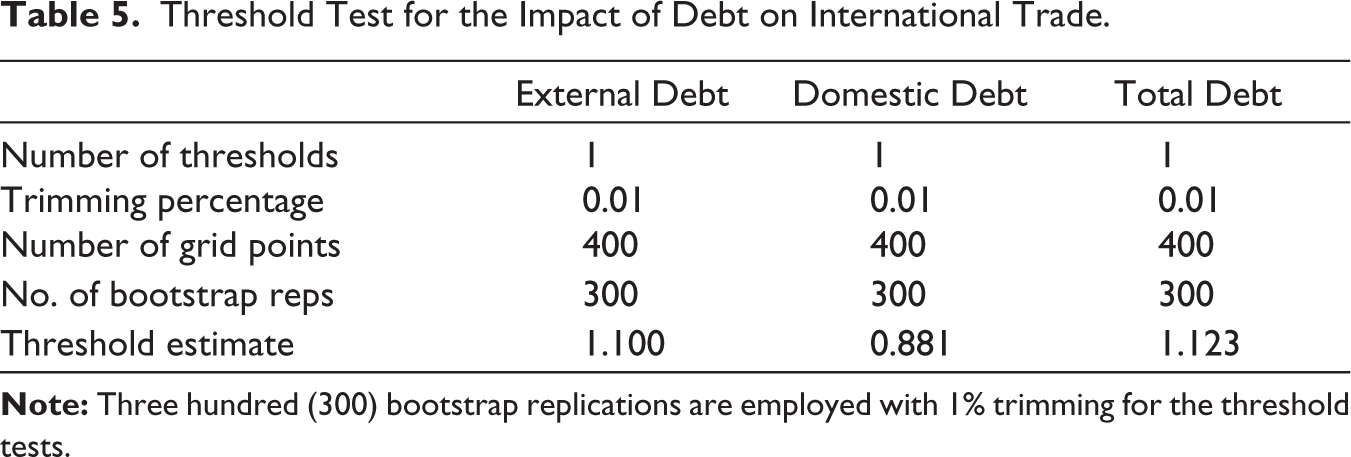

Panel Threshold Estimation Results

This study examined the threshold effects of public debt on trade, offering policymakers insights into optimal debt levels for sustainable growth. Results show thresholds of 1.100 for external debt, 0.881 for domestic debt, and 1.123 for public debt, derived from 300 bootstrap replications with 1% trimming. Below these levels, debt can support trade by financing investment; beyond them, adverse effects emerge. This highlights context-specific intervention points where prudent debt management is essential to enhance trade performance in SSA (Aladejare, 2023). Table 5 and Figure A2, provides the threshold estimates for each type of debt.

Threshold Test for the Impact of Debt on International Trade.

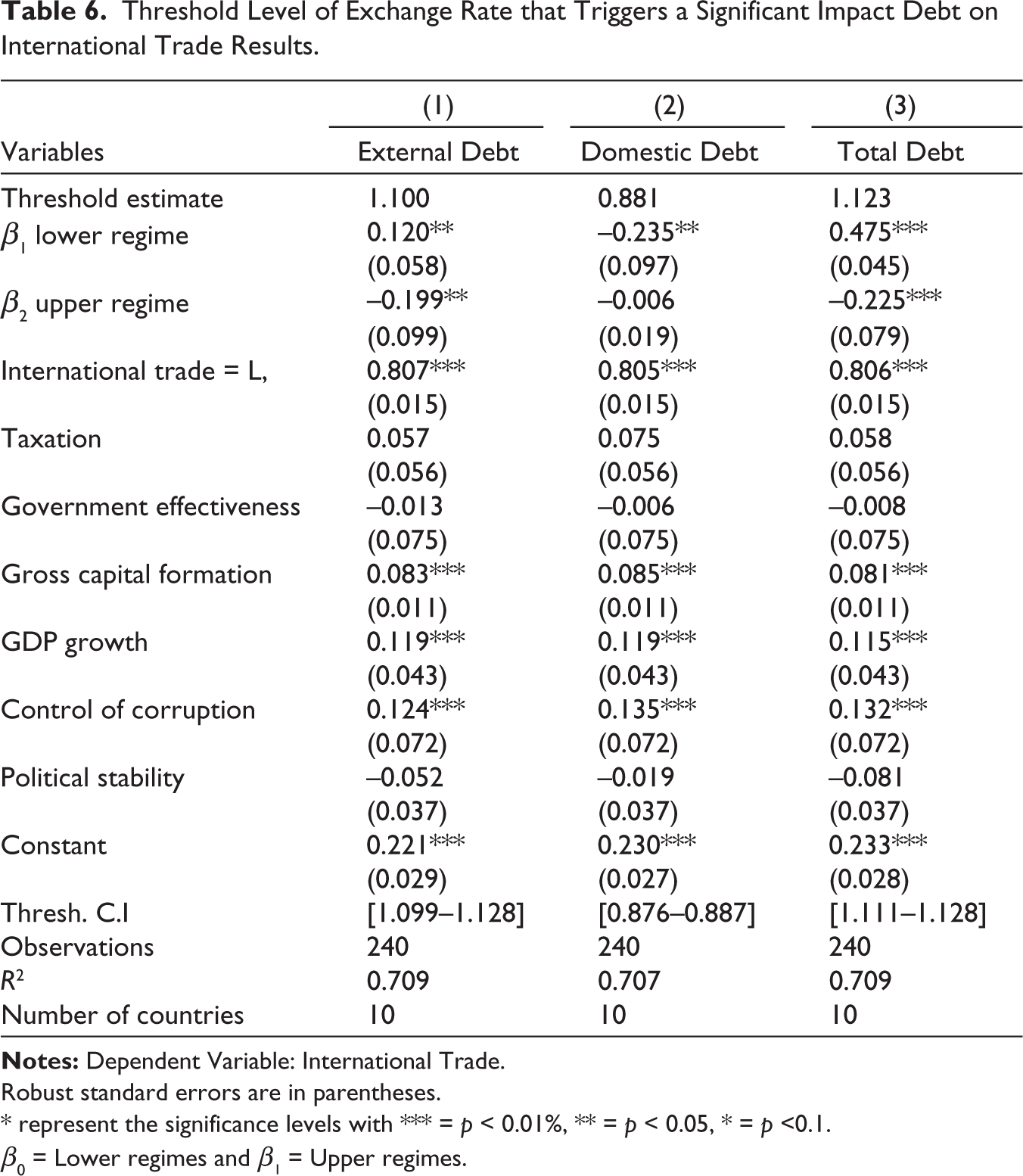

The threshold results in Table 6 reveal critical non-linear relationships between exchange rate dynamics and public debt composition in shaping international trade in SSA. For external debt, the exchange rate threshold of 1.100 proves significant. Below this threshold, external debt positively influences trade (0.120), indicating that manageable borrowing provides essential capital for infrastructure and productive investments, consistent with Ojeka et al. (2024). However, once the threshold is exceeded, the coefficient turns negative (-0.199), illustrating how depreciation amplifies debt burdens, crowds out trade-enhancing expenditure, and confirms the debt overhang theory (Krugman, 1988). Odionye et al. (2023) similarly emphasise that currency depreciation heightens debt servicing costs, diminishing trade performance when external debt becomes unsustainable.

Threshold Level of Exchange Rate that Triggers a Significant Impact Debt on International Trade Results.

Robust standard errors are in parentheses.

* represent the significance levels with *** = p < 0.01%, ** = p < 0.05, * = p <0.1.

β0 = Lower regimes and β1 = Upper regimes.

For domestic debt, the identified exchange rate threshold of 0.881 shows a contrasting pattern. In the lower regime, domestic debt exerts a significant negative effect (-0.235), suggesting that high borrowing levels crowd out private sector investment and raise borrowing costs. However, beyond the threshold, the effect becomes negligible (-0.006). This divergence implies that severe depreciation may erode the real value of domestic debt obligations, easing fiscal pressure despite macroeconomic instability. This contrasts with Messaging et al. (2022), who argued that sustainable domestic debt combined with stable exchange rates could foster trade growth. The difference underscores SSA’s contextual vulnerabilities, where fiscal inefficiencies and currency volatility interact in complex ways.

Similarly, for total public debt, the exchange rate threshold of 1.1232 delineates two distinct regimes. Below this level, total debt has a strong positive impact on trade (0.475), consistent with Romer’s (1986) investment-led growth theory, which posits that moderate borrowing can finance trade-supportive investments. Beyond the threshold, however, the relationship reverses (-0.225), reflecting the dual risks of debt overhang and currency depreciation. This finding aligns with Fagbemi and Adeosun (2021), who documented how rising debt servicing costs erode fiscal capacity and stifle trade in highly indebted economies.

Collectively, these results provide strong evidence that the effects of debt on trade in SSA are threshold-dependent and highly sensitive to exchange rate dynamics. Moderate borrowing, particularly external and total debt, can facilitate trade, but once exchange rate depreciation surpasses critical levels, the debt burden overwhelms potential benefits. Thus, the findings integrate Romer’s (1986) growth model with Krugman’s (1988) debt overhang framework, highlighting a non-linear debt–trade nexus mediated by exchange rates.

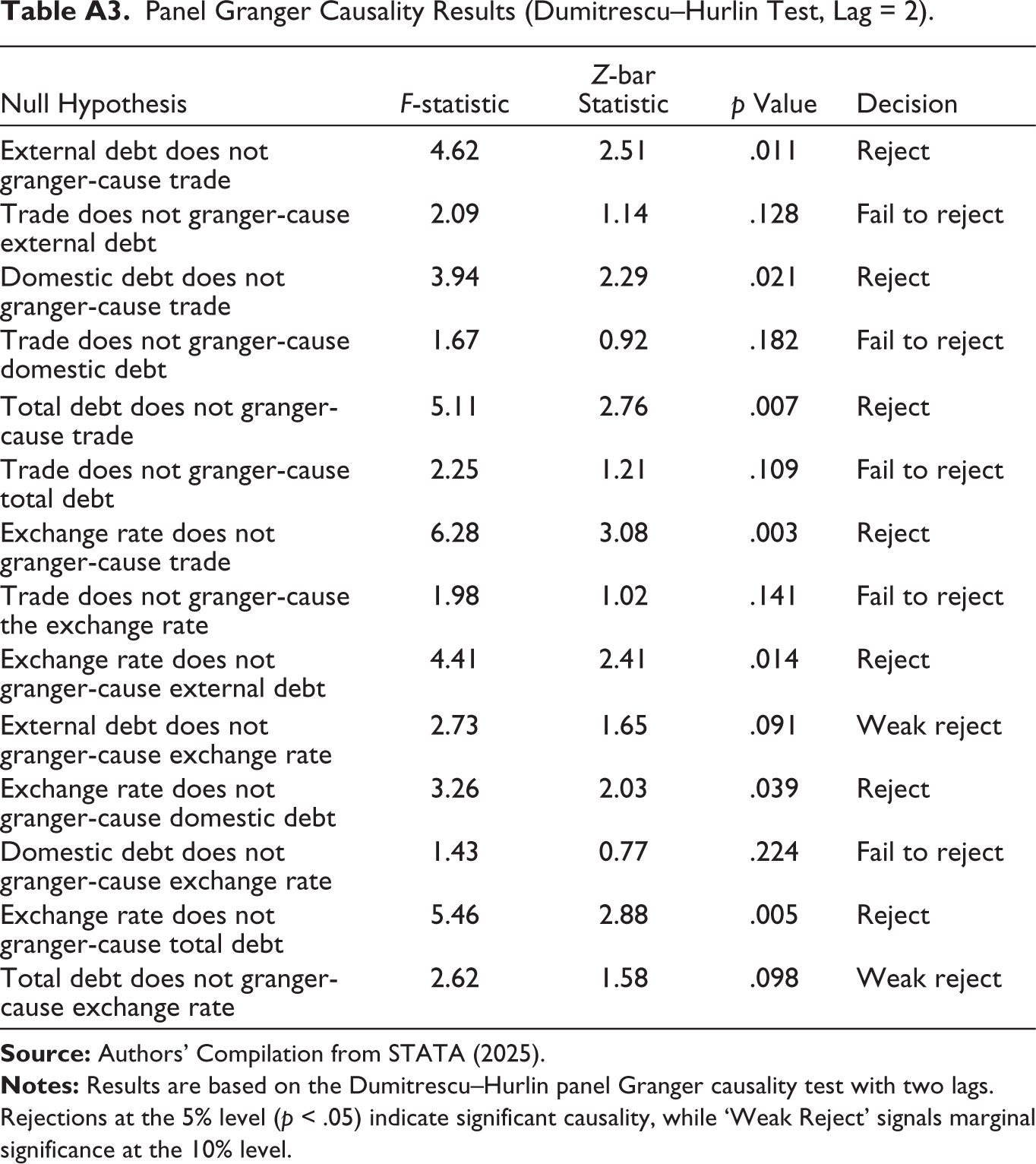

Control variables further reinforce the analysis. Gross capital formation significantly enhances trade, reflecting the role of investment in expanding productive capacity, consistent with Abdulhamid et al. (2024). GDP growth also shows a positive association with trade, confirming that expanding production and consumer demand drive import and export activities (Taha et al., 2023). Moreover, control of corruption consistently improves trade outcomes, supporting Okara’s (2023) conclusion that institutional quality fosters predictability and reduces transaction costs. These findings confirm the trend in Appendix Figure A1, where SSA’s trade-to-GDP ratio fell from 46.3% in 2010 to 42.5% in 2023, while public debt rose sharply from 25.4% to 60.4% of GDP. These shifts emphasise the structural imbalances caused by mounting debt and volatile exchange rates. To further strengthen the threshold, the endogeneity test (orthogonality), Perasan–Yamagata test (slope homogeneity), Chow test (structural breaks) and panel Granger causality test were conducted (See Appendix Table A3). The panel Granger causality results confirm unidirectional causality from debt dimensions (especially external and total debt) to trade, while reverse causality is weak. Also, exchange rate volatility strongly Granger-causes both trade and debt, confirming its central role as a transmission channel. Finally, there is evidence of feedback loops between external debt and exchange rates, suggesting a debt–currency spiral risk in SSA.

Nonetheless, this study acknowledges limitations. Focusing solely on ten high-debt countries may not capture SSA’s full heterogeneity, while reliance on IMF credit as the debt criterion omits other significant liabilities. Future research should expand the sample, incorporate bilateral and private debt, and explore sectoral trade dynamics. Employing methods such as the Pooled Mean Group estimator could further account for heterogeneity in exchange rate pass-through under varied policy frameworks.

Conclusion and Recommendations

This study demonstrates that in SSA, the composition of public debt, thus external, domestic, and total debt, exerts significant negative effects on international trade, with exchange rate depreciation amplifying these outcomes. Threshold analysis reveals that while moderate debt levels can support trade by financing infrastructure, surpassing critical exchange rate thresholds reverses these benefits, aligning with debt overhang theory.

Policy recommendations emerge directly from these findings. SSA governments should implement robust debt management frameworks that reduce both external and domestic debt to sustainable levels, preserving fiscal space for trade-enhancing investments. Also, exchange rate stabilisation must be prioritised: central banks should adopt credible inflation-targeting regimes, coordinate closely with fiscal authorities, and strengthen foreign reserves to mitigate volatility, thereby lowering import costs and enhancing export competitiveness.

Additionally, reducing reliance on debt requires strengthening domestic revenue mobilisation through broadening the tax base, digitising tax systems, and curbing illicit financial flows. These reforms would fund infrastructure domestically and support trade stability. Finally, regional cooperation should be institutionalised, namely joint debt monitoring under the African Union and ECOWAS frameworks, shared fiscal convergence criteria, and coordinated trade policies. Collectively, these measures will mitigate debt overhang risks, stabilise currencies, and promote sustainable trade growth in SSA.

Footnotes

Acknowledgements

We acknowledge the insightful comments from editors and reviewers of this journal towards enhancing the quality of our article.

Authors’ Contributions

All authors contributed to the study conception and design. Data collection, data curation and visualisation were performed by [DAD]. Also, software, material preparation and formal analysis were performed by [DAD]. Manuscript review and editing were performed by [CQ], whereas validation was performed by [CQ] and supervision by [CQ]. The first draft of the manuscript was written by [DAD], and [CQ] commented on the previous versions of the manuscript. All authors read and approved the final manuscript.

Data Availability Statement

The study relied on open-source secondary data obtained from publicly available databases namely: The World Development Indicators, the International Monetary Fund and the World Governance Indicators databases.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Statement

We declare that this study is ethically sound. This study utilised publicly available secondary data sources. All data were obtained from reputable sources and used in accordance with their respective terms of use. No human participants were involved, and thus ethical approval was not required.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Note

Appendix

Panel Granger Causality Results (Dumitrescu–Hurlin Test, Lag = 2).

| Null Hypothesis | F-statistic | Z-bar Statistic | p Value | Decision |

| External debt does not granger-cause trade | 4.62 | 2.51 | .011 | Reject |

| Trade does not granger-cause external debt | 2.09 | 1.14 | .128 | Fail to reject |

| Domestic debt does not granger-cause trade | 3.94 | 2.29 | .021 | Reject |

| Trade does not granger-cause domestic debt | 1.67 | 0.92 | .182 | Fail to reject |

| Total debt does not granger-cause trade | 5.11 | 2.76 | .007 | Reject |

| Trade does not granger-cause total debt | 2.25 | 1.21 | .109 | Fail to reject |

| Exchange rate does not granger-cause trade | 6.28 | 3.08 | .003 | Reject |

| Trade does not granger-cause the exchange rate | 1.98 | 1.02 | .141 | Fail to reject |

| Exchange rate does not granger-cause external debt | 4.41 | 2.41 | .014 | Reject |

| External debt does not granger-cause exchange rate | 2.73 | 1.65 | .091 | Weak reject |

| Exchange rate does not granger-cause domestic debt | 3.26 | 2.03 | .039 | Reject |

| Domestic debt does not granger-cause exchange rate | 1.43 | 0.77 | .224 | Fail to reject |

| Exchange rate does not granger-cause total debt | 5.46 | 2.88 | .005 | Reject |

| Total debt does not granger-cause exchange rate | 2.62 | 1.58 | .098 | Weak reject |

Rejections at the 5% level (p < .05) indicate significant causality, while ‘Weak Reject’ signals marginal significance at the 10% level.