Abstract

A growing body of literature is concerned with the factors that determine the inflows of foreign direct investment (FDI) into a host country. However, hardly any literature has been carried out to provide a systematic literature review (SLR) of the FDI determinants. An SLR methodology underlies this conceptual paper to evaluate and categorise a literature survey of 112 empirical studies published from 2000 to 2018. The result indicates that the size of the host market is the most robust determinant, followed by trade openness, infrastructure quality, labour cost, macroeconomic stability, human capital, and the growth prospect of the host country. Market size is highly significant in virtually all studies. This partly reflects the fact that most of the world’s FDI are market-seeking. This study provides a clear understanding of the scope of the research in the field of FDI determinants as the practical implication for future research.

Keywords

Introduction

Foreign direct investment (FDI) is defined as an investment made to acquire a lasting interest in enterprises operating outside of the economy of the investor (IMF, 1993; WTO, 1996). In contemporary business environments, an increasing number of multinational corporations are engaging in FDIs. These companies are mainly motivated by the prospect of high profitability, along with the possibility of reducing the cost of production, gaining access to the local market, acquiring natural, physical, or human resources of higher quality at a lower cost, and raising efficiency to improve global market position (Dunning & Lundan, 2008).

The inflow of FDI is often considered an essential ingredient that spurs economic growth by bringing technology, knowledge, capital and jobs, which are likely to generate a positive impact on the host economy (Cambazoglu & Simay Karaalp, 2014). Therefore, governments of many developing and least-developed countries have unequivocally entrusted the private sector and foreign investors to transform their economies and accelerate economic growth. Consequently, many countries around the world are opening their economy to foreign investors, restructuring and liberalising their FDI regimes, and offering various fiscal and non-fiscal incentives to attract the optimal level of FDI. However, many countries are not able to attract their potential level of FDI, as the movement of FDI depends on several economic, political and institutional factors. Thus, the research in international business economics has gained substantial attention to empirically investigate the determinants of FDI inflow (e.g., Asiedu, 2002; Chakrabarti, 2001; Leonardo et al., 2018; Moosa, 2009; Tang, 2017; Wijeweera & Mounter, 2008). However, hardly any systematic literature review (SLR) methodology has been adapted. To complement that important methodological gap, this study provides a systematic review of the existing literature on the area of FDI determinants by adopting a structured and robust SLR methodology proposed by Denyer and Tranfield (2009).

A survey of 112 empirical studies published between 2000 and 2018 is reviewed. The article has identified several economic, political and institutional factors as the significant determinants of FDI. The result indicates that the size of the host market is the most robust determinant, followed by trade openness, infrastructure quality, labour cost, macroeconomic stability, human capital and the growth prospect of the host country. Market size is highly significant in virtually all studies. This partly reflects the fact that most of the world’s FDI are market-seeking.

The next section presents a rigorous SLR methodology, formulates the underlying research question and explains the principles for the selection and evaluation of the databases and journals. Next, the analysis and synthesis of the existing literature are presented, followed by the results of the systematic review. The study concludes with the key findings in the literature, along with implications for researchers and directions for further investigations.

Systematic Literature Review (SLR) Methodology

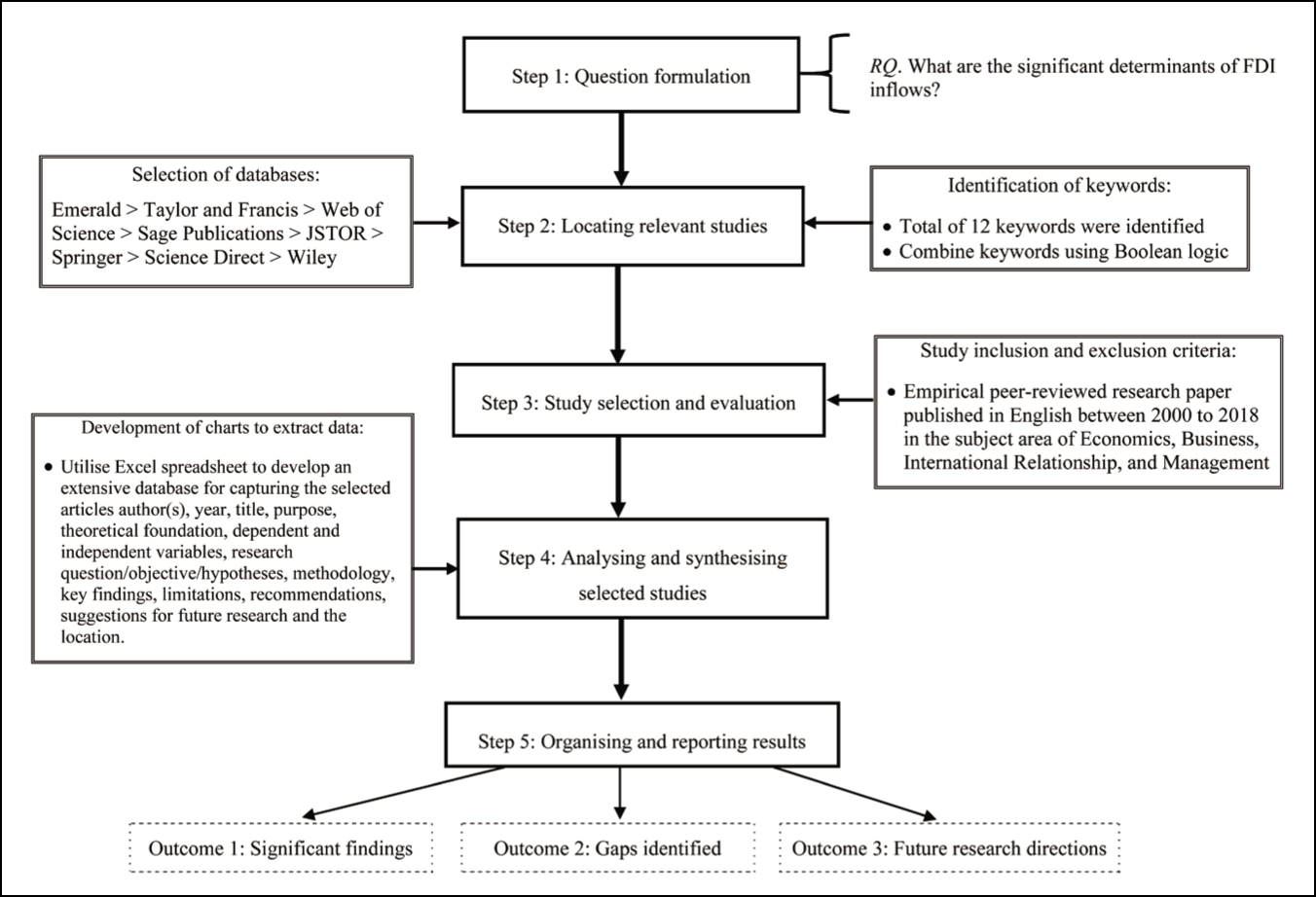

A traditional literature review is a summary and critical analysis of the prior relevant literature on the topic being studied (Hart, 2018), whereas a systematic review uses a more rigorous and well-defined approach to critically analyse the prior literature on a specific research area (Cronin et al., 2008). The SLR method is a major approach in evidence-based practice for identifying, selecting and analysing the existing body of literature (Colicchia & Strozzi, 2012; Tranfield et al., 2003). Denyer and Tranfield (2009) argue that a systematic review enables high-quality research by reducing bias and errors, due to its stronger focus on objective observation of search results. The SLR methodology for this study is based on a set of five steps proposed by Denyer and Tranfield (2009) that guide the overall systematic review process, as shown in Figure 1.

Steps of SLR Methodology Adopted in this Article.

Question Formulation

The first step of an in-depth SLR is to address a well-specified, informative and clearly defined research question. Rousseau et al. (2008) argue that clearly formulated research questions avoid ambiguity and develop a clear focus. The overall aim of this study is to systematically summarise the peer-reviewed journal literature to find out which factors have been identified as key determinants of FDI and provide insight into current research in this subject area to propose new avenues of future research. Hence, this article addresses the following research question:

RQ. What are the significant determinants of FDI inflows?

Locating Relevant Studies

The second step is concerned with locating journal articles relevant to the subject areas. The purpose of searching relevant studies is to create a comprehensive list of core contributions concerning the review questions (Denyer & Tranfield, 2009). Thus, to cover a wide range of sources, the study utilised diverse online databases, including Science Direct, Taylor and Francis, Web of Science, Emerald, Sage Publications, JSTOR, Wiley Online Library and Springer, which are widely accepted in the academia and have been used in studies addressing the systematic review of the literature (e.g., Colicchia & Strozzi, 2012; Rafi-Ul-Shan et al., 2018; Winter & Knemeyer, 2013).

Consistence with prior systematic reviews, this study uses defined keywords as the search criteria in online databases. Whereas some of the keywords were derived from the existing literature, the authors also conducted a few brainstorming sessions to identify and validate the keywords to enhance quality. To create a more focused and accurate literature review, selected keywords were refined by combining them into a series of search strings using Boolean logic, for instance, ‘FDI and determinants’ and ‘FDI and location’. After that, these search strings were used to search for the relevant studies in the online databases mentioned above.

Study Selection and Evaluation

This study only focuses on published peer-reviewed journals, as a quality indicator of methodological and conceptual accuracy (Newbert, 2007). The following criteria were followed for the inclusion and exclusion of the papers:

Articles published in peer-reviewed journals in English. Journals in the subject areas of Economics, Business, International Relationships and Management. Empirical research papers. Papers published from 2000 to 2018. The year 2000 is selected as the starting point for the inclusion in the study because almost 70% of the academic journal articles on this topic area were published after 2000. The end of 2018 is chosen as the endpoint to include the most recent articles. Articles which contain at least one keyword in their title.

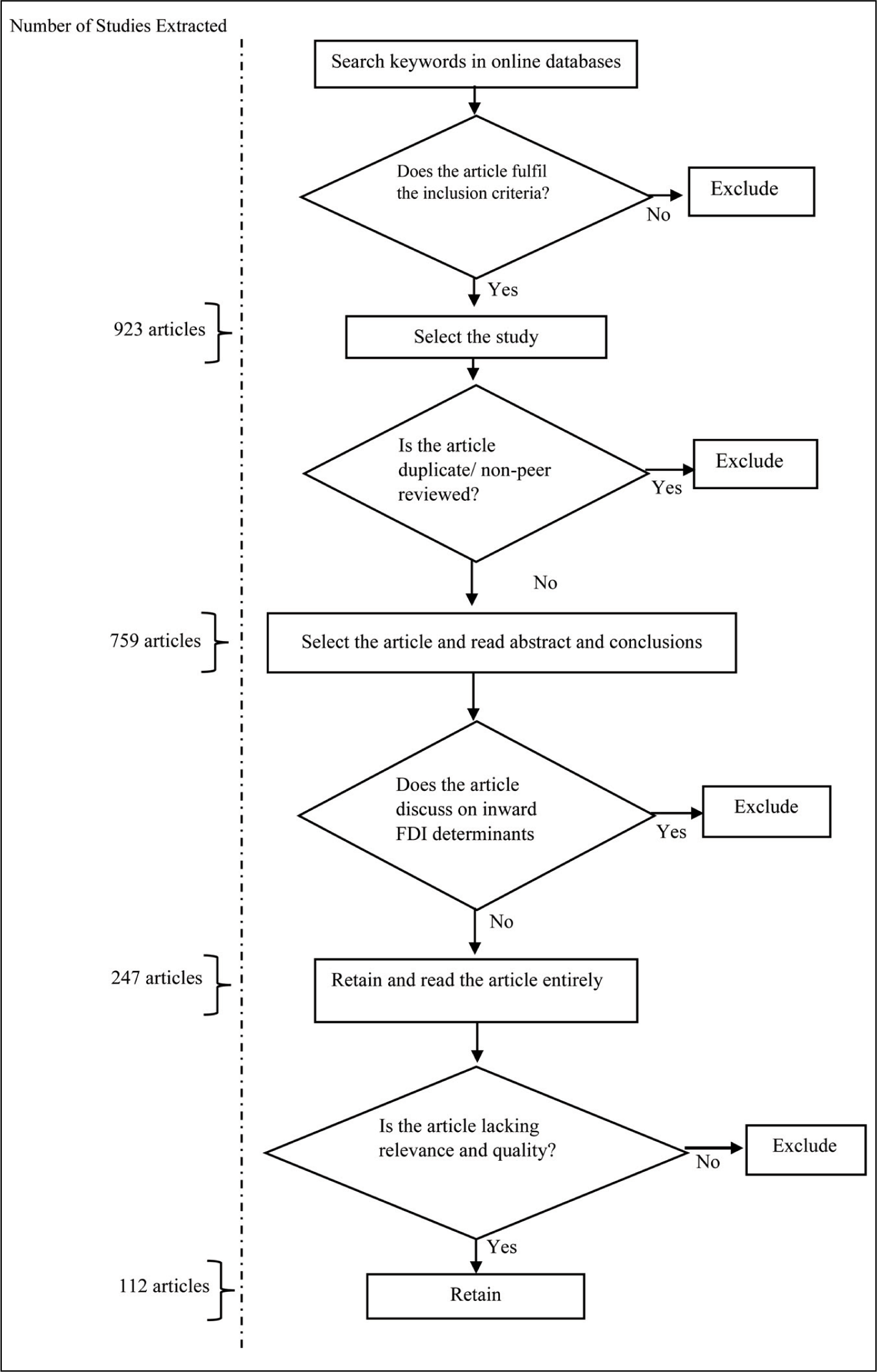

To create a systematic and reliable analysis, this study followed a systematic article selection process, as summarised in Figure 2.

Inclusion and Exclusion of Studies.

First, the selected online databases were scanned for the defined keywords. The articles found were sorted by relevance. Figure 2 shows that a preliminary sample of 923 articles was found that fulfilled the inclusion criteria mentioned above. Overall, 759 articles were identified after excluding articles which were duplicates and non-peer reviewed.

After that, the researcher read the abstracts and conclusions of each article to determine the article’s relevancy to the underlying research question. Studies which seemed non-relevant to the purpose of this study were eliminated to ensure a consistent focus. In total, 247 articles were identified that were relevant to the criteria of this study. Finally, 247 articles were read entirely. The articles demonstrating a clear relation to this article’s content were selected for the final analysis. The extraction process resulted in a total of 112 academic peer-reviewed articles. These articles were then analysed and synthesised to address the formulated research question.

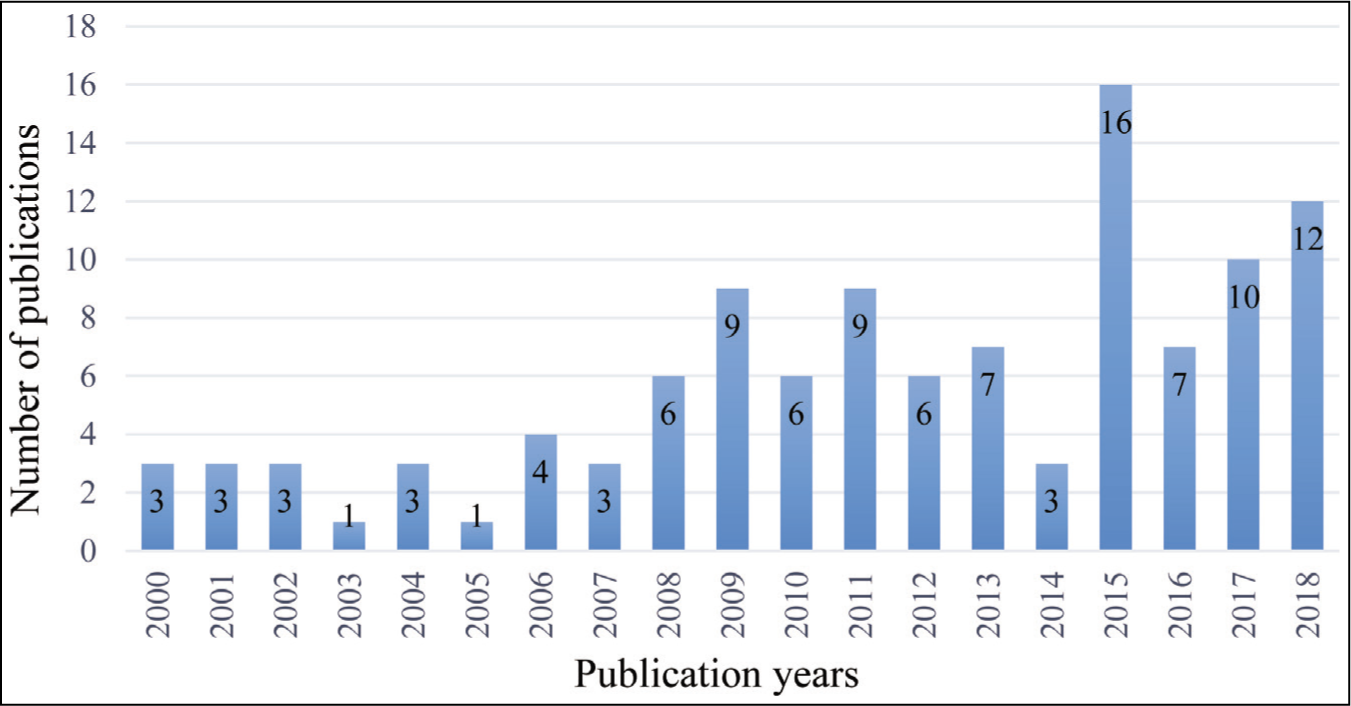

From the yearly distribution of the selected articles shown in Figure 3, this study found that research in this domain has gained momentum in recent years. For instance, almost 68% of the selected studies (76 out of 112) were published from 2010 to 2018. This growing interest proves that research in this topic area will continue to grow as both the significance and volume of the World FDI are increasing exponentially over the years.

Number of Selected Articles by Publication Year.

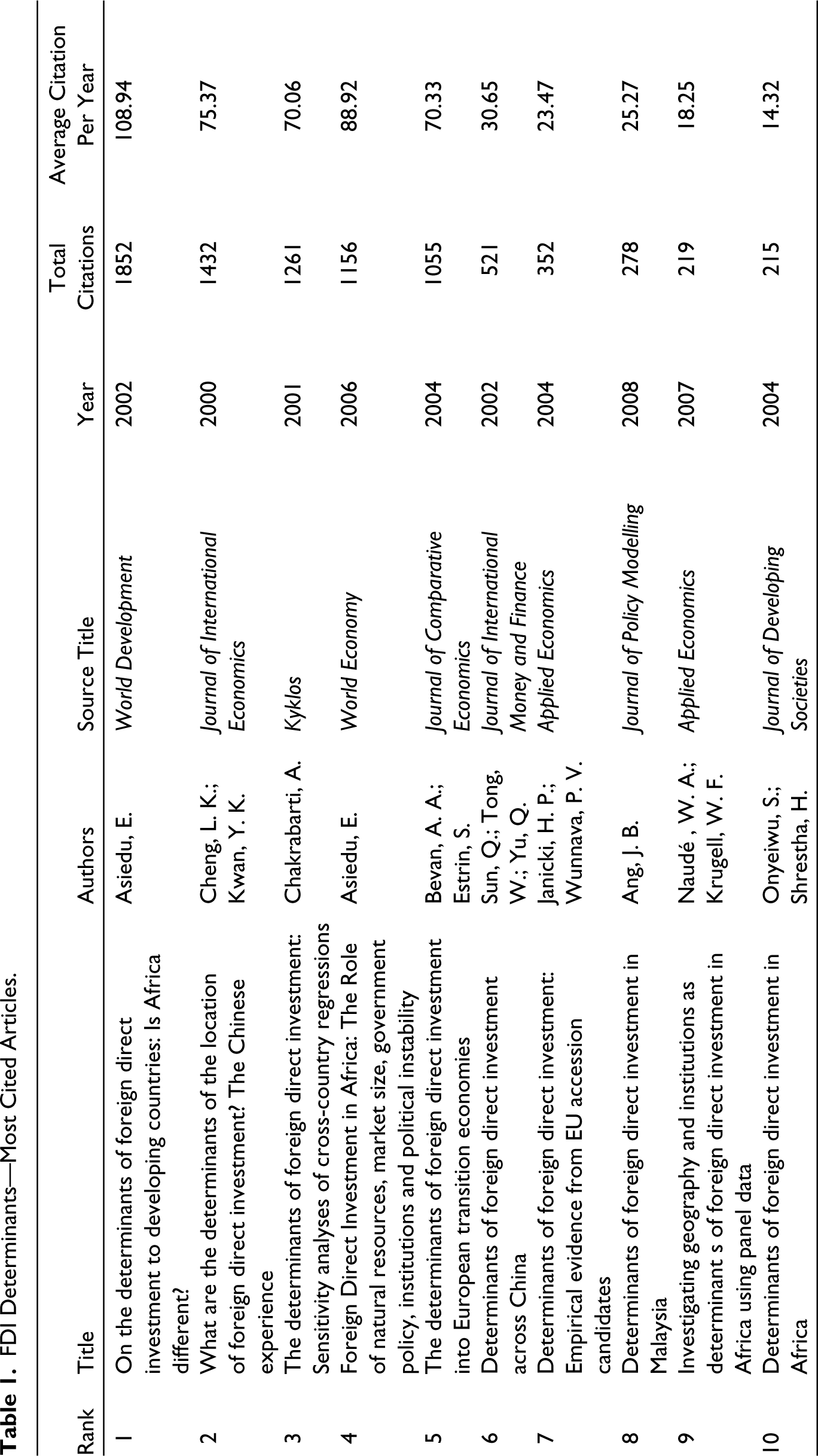

From the selected articles, this study found that Asiedu (2002) is the most frequently cited article, which has been cited 1852 times, with an average of almost 109 citations per year, followed by Cheng and Kwan (2000) and Chakrabarti (2001). A list of key articles in this research domain is shown in Table 1.

FDI Determinants—Most Cited Articles.

The 112 selected studies were published in 79 interdisciplinary journals, shown in Table 2. Most of them were contributed by leading journals, such as Applied Economics (6), Prague Economic Papers (4), Economic Modelling (4), International Business Review (3) and World Economy (3). '

Number of Articles Published by Each Academic Journal.

Analysis and Synthesis of Selected Studies

This step of the systematic review process is concerned with the development of charts to extract data to find the answer to the formulated research question. To do so, Microsoft Excel software was used in this study to develop an extensive database for capturing the selected articles. Data concerning the author(s), year, title, purpose, theoretical foundation, dependent and independent variables, research question/objective/hypotheses, methodology, key findings, recommendations, limitations, suggestions for future research and the location of the study were collected and inserted into an Excel spreadsheet to organise these datasets for the each of 112 selected articles.

Study Findings

The empirical investigation of the determinants of FDI has gained substantial attention in recent years. Prior literature in this topic area has investigated the significance of potential determinants of FDI to a host country within different settings: individual countries and the combination of multiple countries. In the following section, studies concerning the determinants of FDI inflows will be reviewed based on two categories: country-specific studies and cross-country studies. Supplemental Table summarises the empirical evidence regarding the determinants of inward FDI of the empirical studies reviewed in this study.

Empirical Studies: Country-specific Study

Over the years, several country-specific studies explored the determinants of FDI in various South, East and South-east Asian countries.

There were six studies conducted between 2008 and 2018 concerning the determinants of FDI in Malaysia. Among those studies, Ang (2008) applied the two-stage least squares regression approach to the data for the period 1960–2005 to explore the significant determinants of FDI in Malaysia. He found that the size of the domestic market, infrastructure development, trade openness and corporate tax rates were significant to inward FDI in Malaysia. The cointegration results of the study conducted by Choong and Lam (2010) show that human capital, trade openness and market size were significant to Malaysia’s inbound FDI. Tang et al. (2014) found that GDP, real exchange rate, financial development, corporate income tax, macroeconomic uncertainty and social uncertainty factors significantly affect inward FDI in Malaysia. Kinuthia and Murshed (2015) compared the determinants of FDI in Kenya and Malaysia for the period 1960–2009. Their study showed that infrastructure, macroeconomic stability, proxied by inflation, exchange rates and trade policies were substantial to Malaysia’s success in attracting a significant amount of FDI in that period. Hussin et al. (2016) assessed the determinants of FDI inflow to Malaysia between 1980 and 2010. They explored factors like exchange rate, labour cost and interest rate that were significant in attracting FDI to Malaysia. A recent study by Siew Yean et al. (2018) also concluded that the market size, human capital, communication infrastructure and wages significantly influenced FDI inflows into Malaysia.

In neighbouring Vietnam, Vi Dũng et al. (2018) examined the economic and non-economic determinants of FDI inflows based on a longitudinal dataset for the period 2008–2013 of 63 provinces in Vietnam. They found that market size, infrastructure, labour quality, institutions and policies were determinants of FDI inflows at the subnational level in Vietnam. They concluded that the quantity and the cost of labour did not matter to foreign investors in Vietnam.

Khamphengvong et al. (2018) examined the determinants of FDI inflow to the Lao People’s Democratic Republic (Lao PDR). Econometric analysis of panel data covering the period ranging from 1995 to 2015 revealed that the market size, trade openness, inflation rate, labour cost and exchange rate were significant to FDI inflows in Lao PDR.

Cuyvers et al. (2011) explored the determinants of FDI in Cambodia by referring to its political, geographic and economic characteristics. Pooled OLS, random-effect and fixed-effect models were applied to analyse factors that might have influenced FDI inflows in Cambodia from 1995 to 2005. Their study found that GDP, exchange rates, geographical distance and bilateral trade with the host country were the factors that influenced the volume of FDI in Cambodia over the study period.

Mah and Yoon (2010) examined the determinants of FDI flows into Indonesia and Singapore. Their empirical evidence based on a small sample cointegration test showed that, in the case of Singapore where per capita income is quite high, market size appeared to influence FDI inflows positively and significantly, while variables reflecting production factor costs were revealed not to influence those. For Indonesia, the market size was also revealed to be significant. The small sample cointegration test indicated that wage levels were not statistically significant, while the interest rate had a positive and statistically significant effect on FDI flows into Indonesia.

Several studies have also been carried out to explore the determinants of FDI in various South Asian countries. Regarding FDI determinants in India, Wei (2005) concluded that cheap labour costs and geographic distance factors were significant in attracting FDI. Sury (2008) examined the determinants of FDI in India over the period 1991–2003, using the ordinary least squares (OLS) model. FDI inflows were found to be significantly determined by market size, trade openness, labour cost and tax rates for the period under study.

Zheng (2009) investigated and compared the determinants of FDI inflows in India and China by considering both host and home countries’ characteristics. His study revealed that labour costs, market growth, country political risk, imports and policy liberalisation were the major determinants for both countries. However, cultural and geographical distance factors were significant to India’s FDI, while market size, exports and borrowing costs were important to China’s FDI. The size of the market, development level of the state, financial strength of the state and level of infrastructure were some other determinants of FDI inflow into India, as revealed by Dhingra and Sidhu (2011). Singhania and Gupta (2011) found that inflation rates, GDP, scientific research and FDI policy reform had played an important role in the inflow of FDI in India over the period from 1991 to 2008.

Panigrahi and Panda (2012) examined the significant determinants of FDI inflows in the context of India, China and Malaysia during the period ranging from 1991 to 2010 by employing annual time series data obtained from world development indicators and world investment reports. Correlation analysis was used for their study to specify those determinants that wield significant influence on inward FDI in the countries under study. Their study found that GDP, external debt, capital infrastructure, the volume of import and export, and domestic investment had significantly influenced FDI inflow into India and China, whereas in the case of Malaysia, only domestic investment had significantly correlated to inward FDI.

Regarding the determinants of FDI inflows in Pakistan, Khan and Nawaz (2010) applied the OLS regression model to time series data for the period 1970–2005. They concluded that the GDP growth rate, population, price index, tariff on imports and volume of exports had been the most powerful determinants of FDI in Pakistan. In another study, Hakro and Ghumro (2011) investigated the determinants of FDI flows in Pakistan by analysing time series data from 1970 to 2007. The vector autoregressive (VAR) model revealed that cost-related macroeconomic factors were the significant determinants that emerged in the short-run dynamics. However, output growth, openness, employment rate, capital formation and human capital exhibited a long-run relationship with FDI.

Awan et al. (2011) analysed the economic determinants of FDI in the commodity-producing sector of Pakistan covering the period 1996–2008. Their results revealed that gross domestic product (GDP), the growth rate of GDP, gross fixed capital formation, foreign exchange reserves, degree of trade openness and per capita income were the significant determinants of FDI inflows in the commodity-producing sector of Pakistan. Rehman (2016) examined both economic and social determinants of FDI in Pakistan for the period 1984 to 2015. The results indicated that the coefficient of market size, openness and inflation were statistically significant to FDI inflows in Pakistan. However, natural resources were insignificant, which implies that the availability of natural resources is not sufficient to attract the adequate flow of FDI into Pakistan.

Wijeweera and Mounter (2008) have identified the wage rate as the most significant factor to attract inbound FDI in Sri Lanka by using the VAR model on the data for the period 1950–2004. They suggested that wage rate coupled with economic indicators such as GDP, level of external trade, interest rate and the exchange rate should be given due consideration in policies designed to enhance the volume of FDI in Sri Lanka. Ravinthirakumaran et al. (2015) also sought to investigate the determinants of FDI in Sri Lanka using annual data spanning the period 1978–2013. Their study revealed the market size, labour cost, infrastructure, trade openness and political stability as the most important determinants of FDI inflows into Sri Lanka.

Regarding Bangladesh, Qamruzzaman (2015) found that trade and foreign exchange liberalisation, infrastructure availability and sound economic and political conditions increased FDI inflows.

Adhikary (2017) examined and compared the macroeconomic factors influencing FDI in five SAARC economies—India, Pakistan, Bangladesh, Sri Lanka and Nepal—but estimated each country separately. The results of the two-stage least squares and fully modified OLS methods show that the determinants of inward FDI for South Asian countries were not homogenous across economies in terms of either significance level or sign, although they had several determinants in common. For instance, human capital and market size were the most common factors attracting FDI in each country, except for Nepal, which had a negative relationship between FDI inflows and market size. Factors such as market size, infrastructure, exchange rates and financial stability were found to be significant and positive for FDI inflows in Bangladesh, whereas for India, factors such as market potential, market size, inflation, domestic investment and human capital were positive and significant to attract FDI. Importantly, the results of Adhikary (2017) did not achieve harmony on the issue of the determinants of inward FDI for South Asian economies, thereby indicating that the determinants of FDI are certainly country specific.

As China becomes a potential destination of world FDI, a wide range of literature is concentrated to explore the factors that determined the movement of FDI across China. Cheng and Kwan (2000) found that the large regional market, good infrastructure and preferential policy had a significant impact on FDI inflow in China. However, the effect of education was found to be statistically insignificant. In a later study, Sun et al. (2002) concluded that the importance of the FDI determinants across China had changed over time. In their study, they found that the determinants of FDI before and after 1991 were quite different. However, they concluded that labour quality and infrastructure, political stability and openness to the foreign world added an important dimension to drawing in foreign capital. Ali and Guo (2005), while investigating the determinants of FDI that yield a significant impact on China’s inward FDI, concluded that market size was the primary factor influencing US firms to invest in China, while cheap labour costs were the important consideration for Asian firms when deciding to invest in China.

Na and Lightfoot (2006) analysed the determinants of FDI at both country and regional levels in China using a regression model. Their study revealed that GDP proxies for the market size, market expansion potential, degree of openness and labour quality were the most instrumental factors for the distribution of FDI across China.

Jiang et al. (2013) also investigated the determinants of FDI in China. Their study employed provincial panel data over the period from 1985 to 2006. The pooled OLS model used by their study revealed that the large domestic market, infrastructure quality, trade openness and lower wage rate had been significantly linked to China’s success in attracting FDI from all over the world. Chan et al. (2014) also confirmed the direct influence of market size on the inward FDI of China. In a recent study, Saleem et al. (2018) examined the significant determinants of FDI inflows in China using the bounds test approach for the period 1980–2015. Their study found that the main determinants of FDI included labour cost, the size of market, trade openness, economic policy uncertainty and real exchange rate. Similarly, in another recent study, market potential, labour cost, infrastructure and human capital have been found to be significant to inward FDI in China by Song and Cieslik (2018).

Kim and Yang (2014) analysed the determinants of FDI inflows to Korea over the period from 1995 to 2012 using the panel quantile regression model. They found that GDP, employment and human resource education levels of the host country were significant determinants of FDI inflows only when the level of the inflow was low. However, corruption and anti-environment investment levels were statistically significant determinants for middle- and high-level FDI inflows.

Studies have been carried out to explore the determinants of FDI in various South American countries. In the context of Brazil, De Angelo et al. (2010) sought to investigate the determinants of FDI inflows during the period from 2000 to 2007. The findings of their study indicated that internal market growth was a significant determinant of FDI in Brazil. Martins Correa da Silveira et al. (2017) also analysed the determinants of FDI into Brazil between 2001 and 2013 by using a vector error correction (VEC) model. The results show that FDI inflows in Brazil in this period were mainly driven by the size of the domestic market, levels of economic activity, wages and productivity, which were positively related to FDI inflows, indicating that investors pursued market-seeking and efficiency-seeking strategies when targeting the Brazilian market. Although less important, the stability of the national economy and the exchange rate also proved statistically significant in explaining FDI inflows into Brazil. Santos et al. (2017) also found a significant impact of the domestic market on the inflows of FDI in Brazil for the period post-1990.

Ramirez (2006) analysed the significant economic and institutional determinants of FDI flows to Chile. The econometric results suggest that market size, the real exchange rate, the debt service ratio and institutional variables—captured via the inclusion of dummy variables— were statistically significant in explaining the variation of FDI flows to Chile over the 1960–2001 period.

Concerning determinants of FDI in North America, List (2001) examined the county-level determinants of FDI in the US regions. Results of the two-step modified county data model suggest that previous counts of FDI, market size and accessibility, and land area were positively related to FDI occurrences, while higher wage rates and more stringent environmental regulations weakly deterred new firms’ entry.

There were several studies conducted to explore the determinants of FDI in various Middle Eastern countries. Among those studies, Coskun (2001) explored factors influencing foreign investment decisions in Turkey based on the findings of three different surveys. Results found that market size and the economic potential of the country were the most important considerations when deciding to invest in Turkey. In addition, membership in powerful economic blocks, low-cost labour and cheaper inputs were other significant determinants of FDI in Turkey. Dumludag (2009) empirically verified that the market size, growth rate, GDP per capita, low levels of corruption, government stability, enforcement of contract law, functioning of judicial systems, transparent, legal and regulatory frameworks, political and economic stability, intellectual property rights, the efficiency of justice and prudential standards had a significant impact on FDI into the Turkish economy by focusing on the results of a questionnaire applied to the executives of 52 multinational corporations operating in Turkey in 2006.

Bilgili et al. (2012) investigated the dynamics of FDI in Turkey by employing Markov regime-switching models, within the time interval from the 1988 first quarter to the 2010 second quarter. This analysis found that the basic determinants of FDI in Turkey were Turkish GDP growth, labour cost, electricity price growth, the growth in average prices of high sulphur fuel oil, coal, steam coal and natural gas, export growth, import growth, the discount rate and country risk indexes for Turkey, the US, and the EU. Kalyoncu et al. (2015) investigated the determinants of FDI for Turkey over the annual period 1975–2012. Significant positive effects of market size, openness, energy production and labour productivity on FDI inflows were found in this study.

Regarding Iran, Mohammadvandnahidi et al. (2012) found that infrastructure and exchange rates had a significant impact on FDI inflows. However, openness had no impact. In their study, the autoregressive distributed lag (ARDL) model and Dickey–Fuller generalisation least squares test were applied to analyse the annual time series data covering the period ranging from 1975 to 2007.

Bekhet and Al-Smadi (2015) evaluated the short-run and long-run relationship between FDI and its potential determinants in Jordan from 1978 until 2012. The bound testing approach of their study found that FDI had a robust and significant relationship with GDP, money supply and trade openness.

In an analysis of the determinants of FDI in Oman during the period from 1980 to 2013, Ibrahim and Abdel-Gadir (2015) found that market size, inflation rate, natural resources and trade openness are the key determinants of FDI flows to Oman. In another study, Al Shubiri (2016) aimed to identify the economic, financial, management and marketing factors that influenced FDI in the Sultanate of Oman over the 10 years ranging from 2005 to 2014. The results showed a statistically significant relationship with and impact of annual growth of GDP, fiscal balance, investment expenditure, income velocity of broad money and trade balance on inward FDI in Oman.

Studies have also been carried out in European countries, Dimitropoulou et al. (2013) examined the factors determining the location of FDI in the United Kingdom (UK) based on a database of 2,267 observations of FDI projects in UK regions during the period from 1997 to 2003. They concluded that existing regional specialisation was the single most important determining feature of where inward FDI is located.

Regarding Poland, Chidlow et al. (2009) found market-seeking factors as the main drivers of FDI in the Mazowieckie region (including Warsaw), while efficiency and geographical factors encouraged FDI in the other areas of Poland. In another study, Nazarczuk and Krajewska (2018) found that transport infrastructure enhanced the inflow of FDI in Poland.

An empirical study by Masuku and Dlamini (2009) revealed that openness to foreign trade, internal and external economic stability, and infrastructure, as well as the size and attractiveness of the domestic market, were the significant factors influencing FDI inflows in Switzerland.

Rodríguez and Pallas (2008) found that the differential between labour productivity and the cost of labour was an important determinant of FDI in Spain. They also concluded that factors related to the demand, the evolution of human capital, the export potential of the sectors and certain macroeconomic determinants that measured the differential average between Spain and the European Union also played a crucial role in attracting flows of FDI into Spain. In another study, the regional distribution of FDI across the Spanish regions over the period 1995–2005 was analysed by Villaverde and Maza (2012). The econometric analysis carried out revealed that factors such as economic potential, infrastructure, labour conditions and competitiveness were important for attracting FDI both at aggregate and sectoral levels; on the other hand, the market size was not relevant at all as a booster of FDI.

An analysis of the determinants of inward FDI in Norway under location-specific advantages, within the OLI framework was carried out by Boateng et al. (2015). The econometric estimation of quarterly time series data from 1986 to 2009, by utilising the fully modified OLS and the vector autoregressive and error correction models, suggested that real GDP, sector GDP, exchange rates and trade openness had a positive and significant impact on FDI inflows. However, money supply, inflation, unemployment and interest rates produced significantly negative results.

Ledyaeva (2009) applied a spatial autoregressive model of cross-sectional and panel data to the empirical analysis of the factors that either enhanced or impeded FDI inflows into Russia from 1995 to 2005. The important determinants of FDI inflows into Russia in that period appeared to be market size, the presence of large cities and seaports, oil and gas availability, its proximity to the European market and political and legislative risks.

Regarding the FDI determinants of Australia, Yang et al. (2000) found that interest rates, wages and openness of the economy were the main determinants of FDI inflow into Australia over the period of September 1985 to March 1994. Koojaroenprasit (2013) also sought to identify the determinants of FDI in Australia during the period from 1986 to 2011. He found that the large market size, trade openness, corporate tax rate and exchange rate were the significant factors that determined the flow of FDI into Australia.

Several studies have been carried out in various African locations regarding the determinants of FDI. Malefane (2007) used time series data for the period 1973–2004 to identify the determinants of FDI in Lesotho. Evidence from cointegration and error correction modelling indicated that the South African market size and export orientation promoted Lesotho’s FDI during that period. Furthermore, the real exchange rate seemed to be in favour of the country’s FDI since the results exhibited a positive coefficient. A significant political instability dummy is a clear indication that civil unrest hurts the FDI potential of the host country.

Ibrahim and Hassan (2013) investigated the determinants of FDI in Sudan by employing several econometric models, including the VEC model, the Granger causality test and the Johansen causality test. Their analysis of annual time series data from 1970 to 2010 revealed that the size of the local market, exchange rate, inflation rate and investment policies had been significant in determining the inflows of FDI in Sudan.

Yohanna (2013) conducted an empirical investigation of the macroeconomic determinants of FDI in Nigeria from 1981 to 2010 using the stationarity and a cointegration approach. Econometric analysis of time series data found that the market size was the most significant variable in the determination of FDI in Nigeria, followed by human capital, infrastructural development, inflation and the index of energy consumption.

Seetanah and Rojid (2011) found the quality of labour, wages and trade openness as the most influential factors for attracting FDI in Mauritius. Moreover, they found that market size has a lesser impact on FDI inflow for this small but successful FDI recipient country in Africa.

Empirical Studies: Cross-country Study

Several papers have conducted cross-country studies on the determinants of EU economies (e.g., Bellak et al., 2009; Casi & Resmini, 2010; Igošina, 2015; Janicki & Wunnava, 2004; Leonardo et al., 2018; Özkan-Günay, 2011; Stack et al., 2017; Su et al., 2018; Villaverde & Maza, 2015; Tang, 2017).

Bevan and Estrin (2004) found labour costs, gravity factors and market size as the significant determinants of FDI in Central and Eastern European countries (CEECs). Interestingly, contrary to the findings of Janicki and Wunnava (2004), host country risk proved not to be a significant determinant of the CEECs in the study of Bevan and Estrin (2004). Janicki and Wunnava (2004) revealed that the key determinants of FDI inflows in CEECs were the size of the host economy, host country risk, labour costs in the host country and openness to trade. Carstensen and Toubal (2004) also found that market potential, labour cost, skilled labour force and corporate tax rates exert a significant influence on the inflow of FDI in CEECs.

Bellak et al. (2009) analysed the importance of taxes on corporate income and production-related tangible infrastructure as determinants of FDI in CEECs. Panel econometric analysis showed that both taxes and infrastructure were significant to FDI in the CEECs region. However, they found no significance of the host market size and labour productivity in influencing FDI in CEECs.

In another study, Casi and Resmini (2010) analysed factors that were driving FDI into the EU region during the 2005–2007 period, based on information on over 100,000 FDI located in 260 regions in the EU countries. They found that traditional determinants, such as GDP growth rate, labour cost and market potential, were the important drivers of FDI inflows into the EU region.

Özkan-Günay (2011) aimed to identify underlying fundamental factors in attracting FDI among the EU countries where there exists a large discrepancy in terms of their economic and technological development levels. Empirical results for the period 1998–2008 revealed that market size, gas and telecommunications prices, level of internet access and high-technology exports were the significant determinants of FDI.

Villaverde and Maza (2015) examined the determinants of FDI in the EU region over the period from 2000 to 2006. Their study found that labour market characteristics, economic potential, competitiveness and technological progress exert a significant impact on FDI inflows in the EU region, whereas labour regulations and market size did not play any significant role. In contrast, Igošina (2015) found that market size, in conjunction with GDP growth rate, trade openness, labour cost and inflation rates, was significant to attract FDI in EU countries. Regression of panel data using the econometric methodology of fixed and random effects also revealed that existing FDI stock was a significant determinant of the investment flows, which implies that the more FDI an investor has created in previous years, the more is expected to be received in future.

Stack et al. (2017) assessed the determinants, changing nature and the performance of FDI in eastern European countries within the knowledge capital model framework. They conducted an econometric analysis of panel data sets consisting of bilateral FDI stocks from 10 eastern European countries over the period 1996–2007, which revealed that the foreign investment in the eastern European countries was potentially influenced by low labour costs, economic and political stability, tax rate, infrastructure, a skilled workforce, larger market size and the economies of large-scale production.

Tang (2017) examined the determinants of FDI in the CEECs during 1994–2012, based on the gravity model. Econometric estimation of the two-stage least squares and generalised method of moments (GMM) confirmed that the higher bank credit flows, the stock market size and a higher country income, in interaction with a higher bank credit flow, promoted FDI in CEECs countries.

Leonardo et al. (2018) identified the determinants of FDI for 10 developing European economies, using a stepwise panel regression approach. The analysis of quarterly data covered the period from the first quarter of 2010 until the first quarter of 2017, while the yearly data covered 15 intervals from 2002 until 2016. Their results found the effect of GDP and labour costs on FDI inflows. At the same time, their results showed a statistically significant influence on FDI from voice and accountability, government effectiveness, regulatory quality and control of corruption.

Su et al. (2018) examined the factors with a significant impact on FDI in four EU countries. They employed both time series and panel data approaches to empirically test FDI determinants for Poland, Hungary, Czech Republic and Slovakia in the period 2005–2016. The panel approach based on the ARDL model identified a significant relationship between FDI, the corruption index and the labour force with advanced education but only in the long run.

There are six cross-country studies on the determinants of FDI in the ASEAN region. The determinants of FDI in the ASEAN region were estimated by Bhatt (2008) taking market size, exchange rates, trade openness and domestic investment as determining variables. He applied the OLS and fixed effect model on the panel data for the period 1976–2003. The estimation of the models showed that market size, exchange rates, infrastructure and trade openness were significant to FDI in the ASEAN region. Ismail (2009) applied a semi-gravity-type approach to the data for the period 1995–2003, to identify the determinants of FDI in ASEAN economies. He found that market size coupled with the high exchange rate, lower inflation rate, good governance, trade policy, transparency, excellent telecommunication and infrastructures were essential to encourage inward FDI into the ASEAN region.

Hoang and Bui (2015) investigated the determinants of FDI in the ASEAN region over the period between 1991 and 2009. The results of their study from the feasible generalised least squares regression and the random effects model indicated that market size, infrastructure quality, trade openness, labour productivity and human capital were the significant factors that had a substantial impact on FDI inflow of ASEAN region during that period. Surprisingly, this study also found that cheap labour which is widely accepted as a significant factor for inward FDI does not help to attract FDI to the ASEAN region. Xaypanya et al. (2015) also investigated the determinants of FDI in ASEAN countries over the period from 2000 to 2011. Their study revealed that market size, infrastructure quality and level of openness were significant to attract FDI in ASEAN economies.

Tan et al. (2018) used the panel data econometric framework for the 10 ASEAN economies from 1986 to 2012. The empirical study revealed that the significant determinants of FDI inflows into the ASEAN region were the host market size of member states, political stability and the degree of trade openness of the regional economy. Hadi et al. (2018) used the static panel data model to study the sector-wise FDI determinants in six ASEAN countries from 2001 to 2016. The finding of their econometric analysis suggests that different sectors may have different factors that attract inward FDI. In addition, they noted a lack of research into FDI determinants on the sectoral level, which is surprising, since FDI is related to industry rather than to countries.

Concerning both South and South-east Asia, Azam and Lukman (2010) examined the determinants of FDI in India, Pakistan and Indonesia covering the period between 1971 and 2005. By using the linear regression model and the method of least squares, their empirical study revealed that market size, trade openness, domestic investment, external debt and physical infrastructure were the most significant economic determinants of FDI in these three countries. Further, their study found variations in the economic determinants of FDI between these countries.

In the context of BRICS, a random effect model was employed by Ranjan and Agrawal (2011) to explore the determinants of FDI in the BRIC countries. The empirical findings of their study showed that labour cost, trade openness, market size, infrastructure facilities, growth prospects and macroeconomic stability were the important determinants of FDI inflow in these countries, whereas labour force and gross capital formation were insignificant. Gupta and Singh (2016) found trade openness, inflation rates, unemployment rates, the industrial production index, real effective exchange rates and labour cost as the most important determinants in attracting FDI inflows in BRICS economies.

Several studies had explored the determinants of FDI in African countries. An empirical study based on a panel of 29 African countries over the period 1975–1999, by Onyeiwu and Shrestha (2004), identified openness of the economy, inflation, international reserves, economic growth and natural resource availability as significant determinants of FDI. Contrary to conventional wisdom, their study found that infrastructure and political rights were insignificant for FDI flows to the African region. Subsequently, Asiedu (2006) examined the determinants of FDI inflow to 22 African countries covering the period between 1984 and 2000. Her study indicated that large local markets, good infrastructure, natural resource endowments, excellent investment frameworks, an effective legal system and low inflation could promote FDI inflows. Naudé and Krugell (2007) empirically examined the determinants of FDI in Africa by analysing panel data covering a long period of two decades. Using the GMM approach, they identified several robust determinants of FDI, namely, political stability, inflation rate, government consumption, initial literacy, the rule of law, accountability and regulatory burden.

Moosa (2009) empirically examined the determinants of FDI inflows to 18 Middle Eastern and North African (MENA) countries. He found that GDP growth rates, domestic investment, human capital proxied by enrolment in tertiary education, R&D expenditure and country risk were the determinants of FDI in MENA countries. He concluded that countries that are more successful compared to others in obtaining FDI are those that pay attention to education and research, have growing economies, has a high return on capital and have a lower country risk.

Jiménez (2011) analysed FDI flows from Spain, France and Italy to North African countries and CEECs for which reliable data could be found. The dynamic panel data analysis revealed that good economic prospects, human capital, development of infrastructures and higher levels of political risk measured through scales of political discretion, corruption and economic freedom attracted higher FDI inflows.

Rjoub et al. (2017) investigated the determinants of FDI for the 13 ‘landlocked countries’ in Sub-Saharan Africa (SSA) over the period 1995–2013. The panel data analysis revealed that market size, trade openness, natural resource endowment, domestic investment, human capital and political constraints have a positive and significant impact on FDI flow, with only the countries’ tax policies seen otherwise.

Nkoa (2018) investigated the impact of financial development on FDI in 52 African countries under the OLI paradigm from 1995 to 2015. The empirical results show that money and quasi-money, banking credit to the private sector and interest rate liberalisation play a positive role in FDI in countries without a financial market. Money and quasi-money, market capitalisation and financial market value positively influence FDI in countries with a financial market.

In a study regarding the Caribbean and Latin America, Lall et al. (2003) evaluated economic and structural/locational variables associated with US FDI in 8 Caribbean countries and 14 Latin American countries over the period from 1983 to 1994. The analysis confirmed that the exchange rate, infrastructure and market size were statistically significant for both the Caribbean and Latin American countries to attract FDI in this period.

There were two studies concerning OECD countries in the selected papers. Alam and Shah (2013) investigated the potential determinants of FDI for a panel of ten OECD countries over the period 1985–2009. The fixed effects estimation suggested that labour cost, market size and quality of infrastructure were the major determinants of FDI to the countries under study, while political stability and tax rates had no significant impact on FDI inflows. In a more recent study, Economou et al. (2017) examined FDI inflow determinants in 24 OECD and 22 developing (non-OECD) countries over 1980–2012 using the standard fixed effects as well as a dynamic panel approach. The most robust finding of their study was that lagged FDI, market size, gross capital formation and corporate taxation significantly affected FDI inflows in OECD countries.

Among papers on South Asia, Thangamani et al. (2011) investigated the determinants and growth effect of FDI in India, Bangladesh, Pakistan and Sri Lanka by employing the gravity model approach over the period 1995–2008. They found that human development, trade openness and infrastructure were the significant factors that were motivating inward FDI in South Asian economies.

Concerning Arab economies, Aziz and Mishra (2016) examined the determinants of FDI inflows to 16 Arab economies spanning the period from 1984 to 2012. Their study found that trade openness, market size, financial development and preferential trade agreements were the most instrumental determinants for attracting FDI in Arab economies.

Numerous papers have conducted cross-country studies on the determinants of developing, developed, emerging and transition economies (e.g., Biswas, 2002; Cevis & Camurdan, 2007; Chakrabarti, 2001; Chanegriha et al., 2017; Dauti, 2015; Demirhan & Masca, 2008; Farazmand & Moradi, 2015; Gorbunova et al., 2012; Kok & Ersoy, 2009; Kumari & Sharma, 2017; Lucke & Eichler, 2016; Mottaleb & Kalirajan, 2010; Rachdi et al., 2016; Saini & Singhania, 2018; Tampakoudis et al., 2017; Urata & Kawai, 2000).

Among these papers, Chakrabarti (2001) examined the determinants of FDI involving 135 countries. Analyses of cross-country regressions revealed that a country’s openness to trade is more ‘likely’ to be correlated with its FDI, followed by its wage, net exports, growth rate, tax, tariffs and exchange rate. He also found strong support for the explanatory power of the market size of a host country in its FDI.

Asiedu (2002) examined the determinants of FDI in 71 developing countries covering the period from 1988 to 1997. She revealed that liberalized trade regimes, excellent infrastructure and better government policies had no significant impact on FDI in SSA countries but had a positive impact on non-SSA countries.

Moosa and Cardak (2006), after examining the determinants of FDI in 138 countries over the period 1998–2000, concluded that countries with a larger market, low country risk and a high degree of openness tended to be more successful in attracting FDI.

Cevis and Camurdan (2007) applied the generalised least squares and fixed effect models on the data for the period 1989–2006, to examine the determinants of FDI in 17 developing and transition economies. They concluded that the growth rate of the economies, interest rate, inflation rate and trade openness were the most powerful determinants of FDI for the developing and transition economies in that period.

Demirhan and Masca (2008) identified the determining factors of inward FDI in 38 developing countries by estimating a cross-sectional econometric model over the 2000–2004 period. They concluded that the growth rate of per capita GDP, the degree of openness, infrastructure, tax rate and inflation rate were significant in determining the inflow of FDI in the countries under study.

Among these studies, Mottaleb and Kalirajan (2010) studied the determinants of FDI in 31 low-income and 37 lower-middle income countries in Asia, Africa and Latin America, using panel data covering the period from 2005 to 2007. Their study demonstrated that countries with larger GDPs, a higher proportion of international trade, higher GDP growth rates and a more business-friendly environment were more successful in attracting FDI.

Tampakoudis et al. (2017) empirically investigated the determinants of FDI for a panel of 15 middle-income countries covering the period between 1980 and 2013. The results of the random effect model of their study confirmed that GDP, trade openness and population growth had a significant impact on inward FDI, whereas infrastructure, inflation rate, financial development and natural resources were found to be insignificant.

From the literature discussed above, it can be seen that prior empirical studies have identified a number of economic, political and institutional factors as the significant determinants of FDI across the world. These key factors are as follows:

• Market size

• Investment /business climate

• Domestic investment

• Trade openness

• Natural resource endowment

• Political stability

• Unemployment rate

• Growth prospect

• Level of crime/ corruption

• Exchange rate

• Labour cost

• Labour productivity

• Inflation rate

• Infrastructure Quality

• Governance indicators

• Interest Rate

• Human Capital

• Corporate Tax

Conclusion and Recommendations

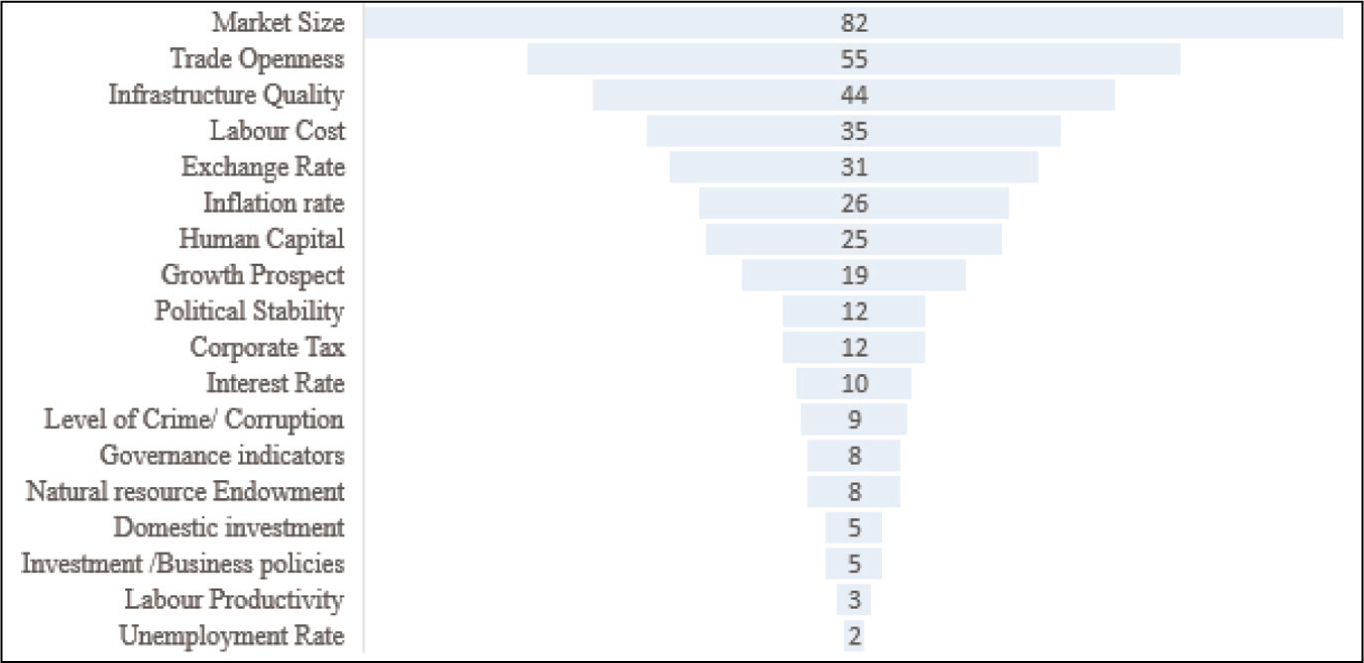

A growing body of literature is interested in the factors that determine the inflows of FDI into an economy. However, they lacked the application of the SLR methodology. Therefore, this article’s contribution comes to fill this methodological gap and provides a better understanding of the significant determinants of FDI. In addition, our SLR shows that the size of the host market is the most robust determinant, followed by trade openness, infrastructure quality, labour cost, macroeconomic stability, human capital and the growth prospect of the host country. Market size is highly significant in virtually all studies (81 out of 112), followed by trade openness, the infrastructure of the host country, labour cost and macroeconomic stability. This partly reflects the fact that most of the world’s FDI are market-seeking. Figure 4 shows the ranking of the determinants of FDI according to their frequency in the studies surveyed here.

Key Determinants of FDI According to their Frequency.

After evaluating the empirical literature on the determinants of FDI, it emerges that there is no consensus among the empirical studies regarding the significant determinants of FDI. This is happening because different types of FDI are affected by different factors. Thus, there is a lack of consensus on determinants of FDI amongst scholars and researchers. Our study agrees with Chakrabarti’s (2001) claim that this is due to a wide difference in the perspectives, methodologies and analytical tools used in studies.

The systematic review conducted in this study contributes to a better understanding of the significant determinants of FDI inflows. However, as with previous studies in this area, our study has its limitation. The SLR methodology chosen for our study relied on some online databases using predefined search strings and a limited time horizon. The requirement for SLR methodology restricted our search area from using specific databases that may limit the breadth of our search.

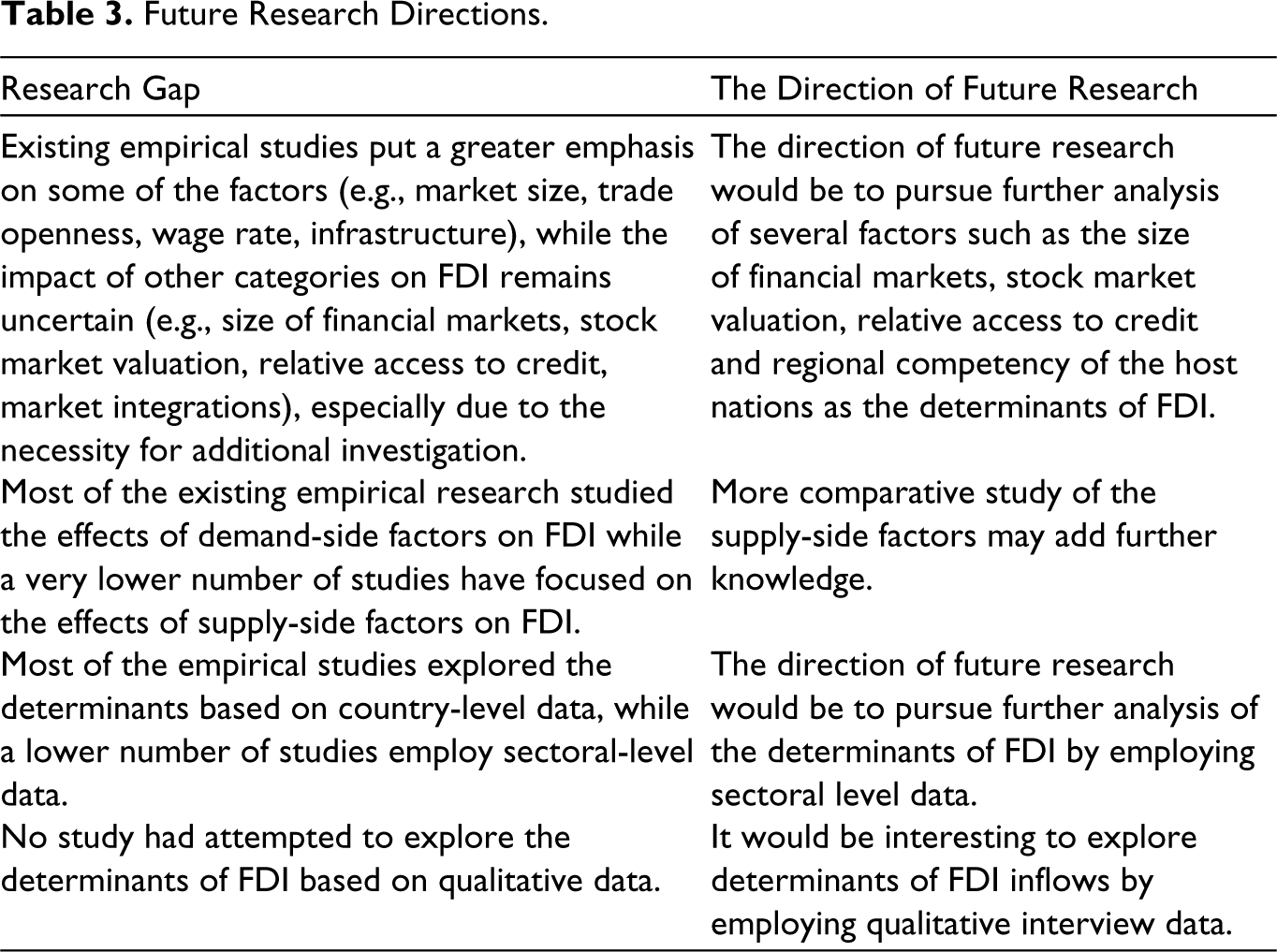

Based on 112 academic peer-reviewed journal articles published from 2000 to 2018, our study identified several possible directions of future research around FDI determinants as shown in Table 3.

Future Research Directions.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.