Abstract

In the last four decades, sub-Saharan African countries have witnessed a substantial increase in trade openness and sovereign debt (foreign public debt and domestic public debt). The direct and interactive effects of these factors on economic growth are investigated in this study. The investigation covers the period 1980–2020 and employs the generalised method of moment methodology. The estimation results reveal that the direct effect of trade openness and domestic public debt is significantly favourable. The direct effect of foreign public debt is, however, found to be unfavourable. The results also reveal that the interactive effect of trade openness and domestic public debt is significantly favourable, whereas the interactive effect of trade openness and foreign public debt is fairly favourable. The estimation results thus imply that trade openness and sovereign debt are complementary drivers of economic growth in sub-Saharan African countries. In spite of the favourable role of trade openness and sovereign debt, economic growth has yet to achieve the desired level, which does not augur well for employment and welfare. The prospects of growth could be enhanced by strengthening the impact of trade openness and sovereign debt. However, policy makers should be aware of the direct negative impact of foreign public debt on economic growth, and the need to put measures in place to manage it.

Introduction

Trade openness generates resources for developing countries, through capital inflows and tariff revenue. Countries sometimes resort to sovereign debt (domestic and foreign) when resources generated from various sources are insufficient to facilitate economic growth (Eaton & Gersovitz, 1981). Thus, sovereign debt plays a complementary role to trade openness in facilitating growth and development (Combes & Sedik, 2002). Over the past four decades, trade openness has improved in developing countries, particularly sub-Saharan African (SSA) countries, due to economic liberalisation policies (International Monetary Fund (IMF), 2021). The important role of trade openness in facilitating economic growth is demonstrated in the classical theory of trade (Heckscher, 1950; Ohlin, 1933; Samuelson, 1949) and endogenous growth theory (Grossman & Helpman, 1990; Romer, 1986, 1990), which posit that trade openness creates welfare gains and stimulates economic growth. Indeed, several Asian and Latin American countries such as China, Brazil, India, Malaysia, Indonesia and Chile have achieved tremendous openness-growth over the years, and consequently lifted a large proportion of the population out of poverty (Lin, 2011). However, SSA countries have been unable to achieve similar feats; hence, the poverty level remains considerably high (UNCTAD, 2016). Bunje et al. (2022) confirmed this situation by observing that trade openness has adversely affected per capita gross domestic product (GDP) in most African countries.

In regard to sovereign debt, the Keynesian theory argued that public expenditures financed through debt have a multiplier effect on national output (Elmendorf & Mankiw, 1999). This theory is based on the principle that the stimulating effect of public debt on the economy exceeds its crowding out effect (Ncanywa & Masoga, 2018). This view suggests that public debt is important for boosting growth, provided it is not used for consumption. In this way, the impact of debt on growth is optimised, with moderate inflation (Driessen & Gravelle, 2019). On the contrary, the neoclassical theory argued that debt impairs economic growth by reducing budgetary discipline and private sector access to credit (Broner et al., 2014). Furthermore, debt repayment tends to crowd out economic growth by discouraging domestic investment (Saungweme & Odhiambo, 2019). However, the Keynesian view on sovereign debt seems to be more appealing to SSA countries, hence the obsession with massive borrowing to fill the resource gap. Again, these countries are encouraged to borrow, due to the incentives granted by external creditors, in the form of competitive interest rates and long moratorium periods (Reisen, 2007).

Over time, the levels of trade openness and sovereign debt have been on the increase in SSA countries, which is partly attributed to the consistent use of borrowed funds to cushion the deficits arising from trade openness (Edo et al., 2020; Zafar et al., 2015). It implies, therefore, that trade openness and sovereign debt interact to affect economic growth. Trade openness in SSA rose from the lowest level of 35.1% in 1982 to a peak of 62.2% in 2010, and has remained relatively stable around that level (IMF, 2021). Domestic debt that stood at 52% of GDP in 2004 declined to 24% in 2019, whereas foreign debt rose to 78% in 1994 and declined to 38% in 2019 (World Bank, 2020). The direct effect of both trade openness and sovereign debt on economic growth has been extensively investigated in several studies, such as Osei-Assibey and Dikgang (2020), Ssempala et al. (2020) and Asteriou et al. (2021). However, the interactive effect has not been given due attention, which creates a knowledge gap that needs to be filled. The significance of this issue lies in the fact that many developing countries, particularly in SSA, are faced with the challenge of managing increasing levels of trade openness and sovereign debt, which calls for the knowledge of how they interact to affect economic growth. It is, therefore, necessary to build on existing empirical works by carrying out a further study that investigates the direct effects of trade openness and sovereign debt on economic growth, as well as the interactive effect. This study attempts to undertake this investigation in order to fill the identified gap in literature, and add to the knowledge on economic growth in developing countries.

The study was carried out by employing the generalised method of moments (GMM) to estimate (i) the direct effects of trade openness and sovereign debt on economic growth and (ii) the interactive effect of trade openness and sovereign debt on economic growth. In terms of scope, the study covers 43 out of the 46 developing economies of SSA, and the period 1980–2020. There are seven sections in the study comprising introduction, literature review, descriptive analysis, model specification, estimation results and analysis, implications of study, and conclusion.

Literature Review

Theoretical Review

The classical theory of trade, which relates trade openness to the welfare of countries, was first propounded by David Ricardo in the early nineteenth century. The theory projected the case for free trade based on the principle of comparative advantage. The principle was centred around the argument that as trade becomes more open, countries specialise in producing goods in which they have a comparative advantage, due to differences in technology or natural resources. The specialisation then leads to welfare gains for trading countries and the global economy. The theory was subsequently popularised by Heckscher (1950), Ohlin (1933) and Samuelson (1949), who demonstrated the benefit of trade if each country produces and exports the good using its abundant factor (capital or labour). The theory, therefore, prescribes that countries are better-off under different comparative costs and terms of trade.

On the contrary, the theory of growth relates trade openness to economic growth, though it does not provide a clear relationship between them. In the early growth models, such as the Harrod–Domar model (Domar, 1946; Harrod, 1939), capital is the major factor of production, through which trade liberalisation exerts positive effect on growth. In the neoclassical model (Solow, 1956; Swan, 1956), growth is exogenously determined through trade openness that creates capital inflows. This postulation is underscored by the endogenous growth model (Grossman & Helpman, 1990; Romer, 1986, 1990), which posits that trade openness creates inflows of capital and intermediate goods needed for production in the economy. Furthermore, the postulation is supported by Chen and Gupta (2006), who argued that trade openness creates knowledge spillover and technological change that stimulate growth.

In regard to sovereign debt and economic growth, the two opposing theories are the classical and Keynesian theories. The classical school of thought argued that sovereign debt impairs economic growth by reducing budgetary discipline and private sector access to credit (Broner et al., 2014). Furthermore, debt repayment tends to crowd out economic growth by discouraging domestic investment (Saungweme & Odhiambo, 2019). On the contrary, the Keynesian school of thought argued that public expenditures financed through sovereign debt have a multiplier effect on national output (Elmendorf & Mankiw, 1999). The theory is based on the principle that debt stimulates the economy more than its crowding-out effect (Ncanywa & Masoga, 2018). This view suggests that sovereign debt is important for boosting growth, provided it is not used for consumption. In this way, its impact on growth is optimised, with moderate inflation (Driessen & Gravelle, 2019).

In theory, it is also contended that developing countries increase sovereign debt at the initial stage of development in order to cushion the deficits arising from trade openness (Zakaria, 2012). It follows that debt must necessarily accompany trade openness in developing countries experiencing balance of payment problems, for economic growth to be sustained. This theoretical argument on trade and debt was one of the major considerations for establishing IMF in the Bretton Woods conference of 1944, to provide loans for member countries suffering from trade deficits (Allen, 1961). According to Auboin (2004), the association between trade openness and debt can also be explained by the fact that openness improves economic prospects and the need to borrow more. Another theoretical perspective associating debt with trade openness states that trade creates external shocks and instability in the government budget, hence debt is needed to cushion the shocks and restore economic growth (Combes & Sedik, 2002).

In the foregoing theoretical considerations, it is established that trade openness and sovereign debt have a direct relationship with economic growth. More importantly, it is also established that trade and debt interact in the process of economic growth. This fact is buttressed by the inclusion of trade deficit financing in the IMF operational framework, aimed at sustaining growth in member countries (IMF, 2014).

Empirical Review

The relationship between trade openness and growth has been a controversial issue among researchers. A review of empirical studies on this issue is, therefore, presented in this section. In several studies, trade openness has been found to be an important factor affecting the economic growth of developing countries. Adeleye et al. (2015) investigated the effect of trade on growth in Nigeria, using error correction modelling techniques. The study found a long-run significant positive effect of trade, whereas other explanatory variables remained insignificant, which suggests that the economy derives substantial benefits from trade openness. The study, therefore, emphasised the imperative of sustaining trade openness, by encouraging more exports and imports. In the case study of South Africa, Osei-Assibey and Dikgang (2020) re-visited the trade–growth nexus by controlling for exchange rate shocks and global economic changes. The study found a robust trade-driven growth, suggesting that the increasing level of exports and imports contributed appreciably to economic growth.

Trade and economic growth in Zimbabwe was also revealed to have a significant long-run positive relationship by Caleb et al. (2014). The study covered the period 1975–2005, and employed the co-integration approach to establish the relationship. The same finding was replicated in a panel data study of selected SSA countries carried out by Chai (2016). The study covered the period 1985–2014 and found a significant positive effect of trade openness on economic growth. The results also showed that private investment complemented trade in facilitating growth. Furthermore, Bakari (2017) employed a vector error correction model (VECM) to investigate the effect of trade openness and investment on the economic growth of Algeria. The results showed that trade had a positive long-run relationship with economic growth, whereas investment had a negative impact. However, the study carried out by Adhikary (2011) presented a contrary scenario in Bangladesh, where liberalised trade regime caused large currency depreciation and an increase in the price of imported inputs used in production. Consequently, domestic markets became less competitive, leading to a considerable drop in economic growth. Similarly, Sheikh and Malik (2021) carried out a study on the BRICS countries, using the VECM methodology. The results revealed that trade openness did not play significant positive role in facilitating economic growth, in spite of the complementary support of institutional infrastructure.

Alessandro De Matteis (2004) carried out a study on a larger sample of countries to determine whether trade liberalisation generates favourable or unfavourable effects on economic growth. It was discovered that trade integration did not encourage growth during the various phases of economic development. Instead, it led to an increase in international exposure that negatively impacted economic growth. In another study, Zahonogo (2016) investigated how trade openness affects economic growth in 42 SSA countries, within the period 1980–2012. The study employed a dynamic growth model and pooled mean group estimation techniques to produce a trading threshold. The empirical results revealed that trade openness below the threshold had a positive effect on growth in some countries. Also, trade openness above the threshold impacted negatively on growth in other countries. The results, therefore, suggest that some SSA countries have challenges with trade openness.

The relationship between sovereign debt and economic growth is even more controversial than that of trade openness and economic growth. The sovereign debt and economic growth controversy was accentuated by the study carried out by Reinhart and Rogoff (2010) on 44 countries. The results revealed a threshold debt ratio of 90% for advanced countries and 60% for emerging countries. Furthermore, it was revealed that economic growth in advanced countries increased slightly when the debt ratio fell below the threshold, and declined significantly when the ratio rose above the threshold. On the contrary, economic growth in emerging countries fell by 2% when the debt ratio reached the threshold and drastically declined by 50% when the debt ratio rose above the threshold. It follows that too much debt burden tends to slow economic growth in both developed and emerging economies. Rahman et al. (2019) later carried out a survey of previous studies to ascertain the level of conformity with the Reinhart–Rogoff hypothesis that a high public debt burden tends to slow economic growth. The survey, covering 33 previous studies, revealed that the hypothesis did not hold in all the studies.

Law et al. (2021) used a dynamic panel technique to produce different threshold debt ratios in a study of 71 developing countries, during the period 1984–2015. The ratio was found to be 51.7%, which is much lower than the Reinhart–Rogoff threshold. However, the results of the study conformed to the Reinhart–Rogoff hypothesis. It was discovered that debt had an insignificant impact on growth at a debt ratio below the threshold but exerted a significant negative impact at a debt ratio higher than the threshold. The quality of institutions was found to have played an important role in minimising the adverse effect of debt on growth. In another study, Salameh (2020) examined the impact of sovereign debt on economic growth in several oil-rich countries, within the period 2002–2017, using a panel vector autoregressive approach. The results showed that public debt had no meaningful impact on growth, due to the inability of the government to manage debt resources.

A comparative study of domestic and foreign public debt in Nigeria was undertaken by Ajayi and Edewusi (2020) for the period 1982–2018, with the aid of VECM. It was discovered that domestic public debt exerted a positive effect on economic growth in the short run and long run, whereas foreign public debt had a significant negative effect. Ssempala et al. (2020) found a significant negative impact of public debt on economic growth in Uganda in the short run, whereas the impact was significantly positive in the long run. It suggests that public debt in Uganda constrained the private sector and investment activities in the short run.

In a large sample study of 43 African countries, over the period 2001–2018, Ehikioya et al. (2020) used the GMM model to examine the relationship between sovereign debt and economic growth. The results revealed the existence of a significant long-run relationship and also discovered that beyond a certain level, the sovereign debt had a deteriorating impact on growth. The findings, therefore, support the threshold hypothesis of sovereign debt and economic growth. The study provided some insight into how the benefits of sovereign debt have been short-lived in most African countries, due to the misappropriation of resources. Bidzo (2018) further demonstrated that public over-borrowing impacted negatively on economic growth in the Gabonese economy. The GMM model was employed to produce the result, which showed that an increase in public debt led to considerable deterioration in economic activities. On the contrary, Wibowo (2017) used the VAR model in the study of eight South-East Asian countries, over the period 2006–2015. The study revealed that it took public debt some time to impact positively on economic growth. A similar study was conducted, by Asteriou et al. (2021), on a panel of selected Asian countries, for the period 1980–2012. The study employed ARDL model to produce results that showed an increase in public debt impacted negatively economic growth in both the short run and long run.

Generally, there are other studies where sovereign debt was found to have a negative impact on growth, as a result of inefficient allocation of debt resources to consumption, rather than investment. They include Yasar (2021), Saad (2012), Choong et al. (2010) and Hameed et al. (2008). Also, there are other studies that found sovereign debt to be a significant driver of economic growth. These are Sulaiman and Azeez (2012), Chinaemerem and Anayochukwu (2013) and Jayaraman and Lau (2009).

Gap in Literature

Previous empirical studies have produced conflicting evidence on the direct effect of trade openness on the economic growth of developing countries. The effect has been observed to be either positive or negative. Some of these studies include Adeleye et al. (2015), Osei-Assibey and Dikgang (2020) and Adhikary (2011). Similarly, there has been a sharp divide on the direct impact of sovereign debt on economic growth, in several studies such as Ajayi and Edewusi (2020), Ssempala et al. (2020) and Asteriou et al. (2021). Several studies, therefore, exist on the direct effects of trade openness and sovereign debt on economic growth in developing countries. However, due attention has yet to be given to the interactive effect of trade openness and sovereign debt on economic growth. That is, the effect of trade openness is contingent on interaction with sovereign debt. It is important to fill this gap and add value to knowledge. The significance of this issue to policy lies in the fact that many developing countries, particularly in SSA, have been increasing the levels of trade openness and sovereign debt, without knowing how they interact to affect economic growth. It is, therefore, pertinent to carry out a further study that would produce both direct and interactive effects of the two factors on growth. Such study is considered more relevant to policy making.

Descriptive Analysis

Trade Openness and Sovereign Debt in sub-Saharan Africa

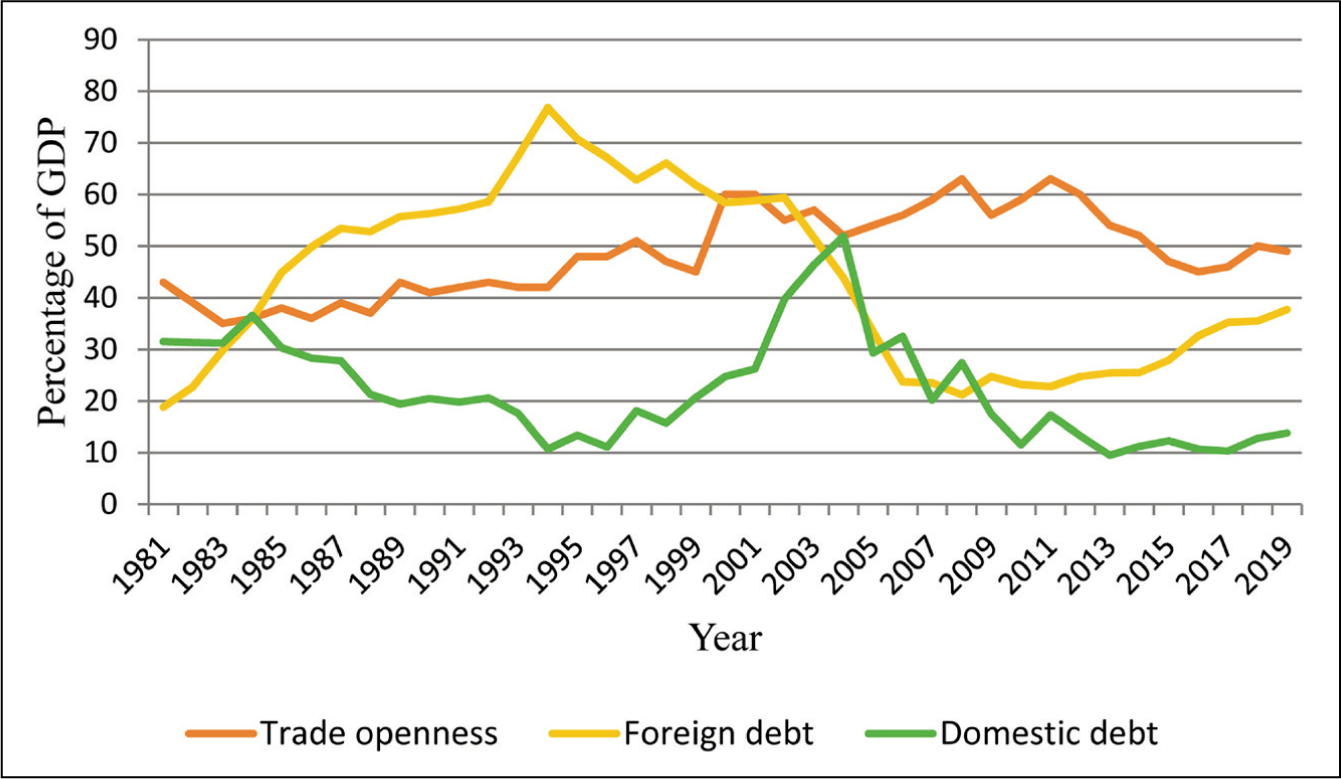

Trade openness in SSA, measured by the ratio of external trade to GDP, has been increasing slowly over the last four decades (Figure 1). It stood at 43.2% in 1981 but declined to 37.1% in 1988. Thereafter, it fluctuated significantly and rose to a peak of 63.3% in 2011, and subsequently dropped to 49.1% in 2019. Some economic analysts attribute this trend to domestic and external factors, such as government policies and global market conditions. The entire period was, therefore, characterised by an unstable trajectory of trade openness in SSA.

On the contrary, sovereign debt is composed of foreign debt and domestic debt. Foreign debt escalated in the 1980s, when its ratio to GDP rose sharply from 18.8% in 1981 to a peak of 76.8% in 1994, and declined to 22.8% in 2008. Although it rose again to 37.7% in 2019, the rise is less dramatic than what happened in the 1980s. The debt escalation has been attributed to the ambition of African countries to facilitate economic growth through external borrowing, the willingness of foreign creditors to lend long-term funds, and floating interest rates in the global financial market. The subsequent sharp decline is attributed to the debt relief program for developing countries, sponsored by IMF and the World Bank in 1990s. The current rising trend may be attributed to incentives, such as concessionary lending rates and long moratorium from external creditors, particularly China and the multilateral development institutions.

The domestic debt component of sovereign debt declined from 31.5% in 1981 to an all-time low of 10.7% in 1994. It then increased sharply to a peak of 51.9% in 2004, when the access of African countries to external loans was frozen by foreign creditors, due to their inability to meet existing debt obligations. However, the domestic debt declined from its peak in 2004 to 11.5% in 2010 and has remained low around that level. Generally, the two components of sovereign debt (foreign and domestic) recorded wide fluctuations, as against trade openness that recorded a relatively stable increase, over time.

Economic Growth

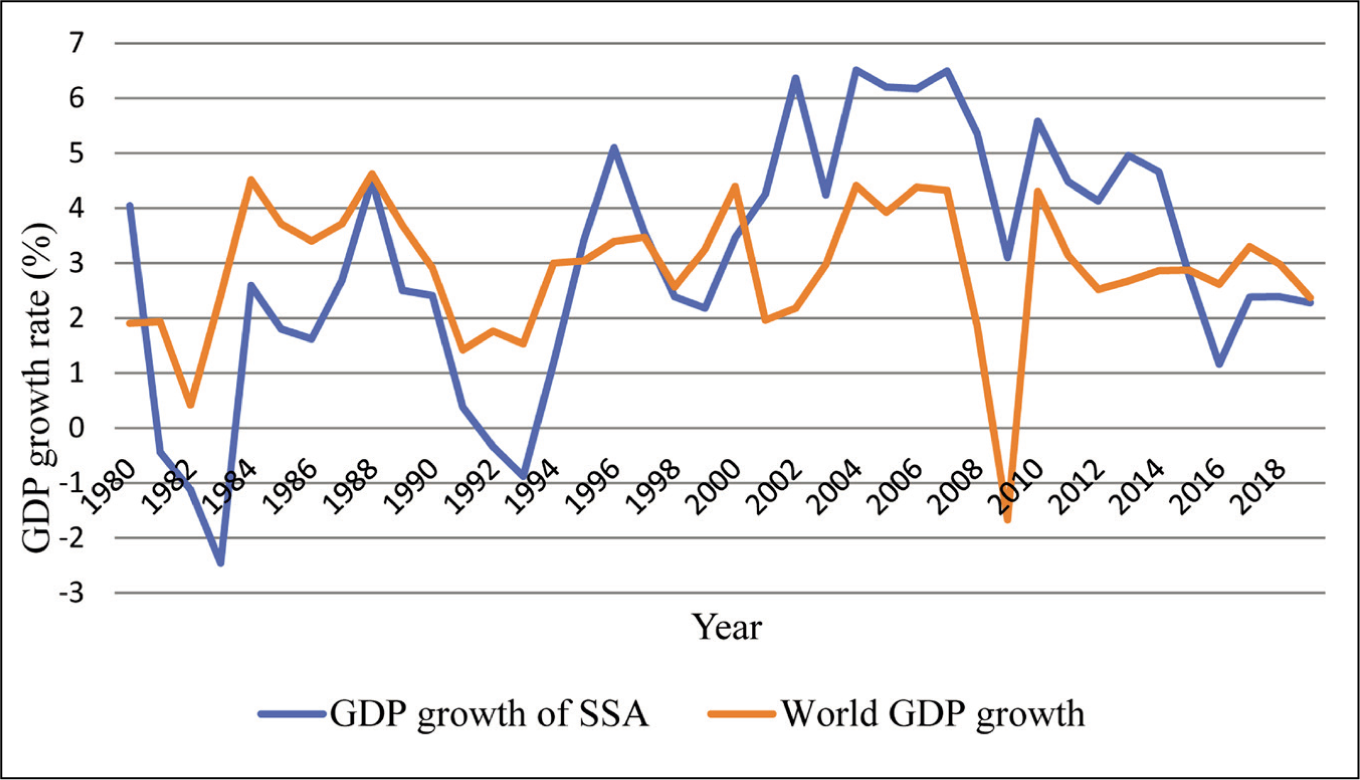

SSA witnessed a robust GDP growth of 4.1% in 1980, which dropped sharply to a negative growth of –2.2% in 1984, as shown in Figure 2. This downturn was caused by the decline in revenue from the export of primary commodities, following the slump in prices in the global market. As SSA countries depend largely on earnings from primary commodity exports, the negative impact on growth was quite severe. Another negative growth of –0.4% was recorded in 1994. Thereafter, it oscillated to a peak of 6.2% in 2004, and subsequently dropped to 2.3% in 2019, due to domestic and external shocks. Within the period 1980–2000, the growth of SSA remained well below world GDP growth. There was a significant break in 2001, when the growth soared and remained above world GDP growth up to 2015. The period 2001–2015, therefore, witnessed a growth trend that was mostly above 4.0% in SSA. In 2019, the growth of SSA and the world economy converged at 2.3%.

Model Specification (GMM)

The classical trade theory together with neoclassical and endogenous growth theories (Domar, 1946; Grossman & Helpman, 1990; Harrod, 1939; Romer, 1986, 1990; Solow, 1956; Swan, 1956) underscore the importance of trade openness in the economic growth of developing countries. Similarly, the classical and Keynesian theories underscore the role of sovereign debt in the economic growth of less-developed countries (Broner et al., 2014; Driessen & Gravelle, 2019; Elmendorf & Mankiw, 1999; Ncanywa & Masoga, 2018; Saungweme & Odhiambo, 2019). It follows that both factors are important in explaining economic growth. However, there are other control variables that also affect economic growth. The GMM model showing the direct effect of these variables on economic growth is constructed as follows:

The functional relationships are represented in Equation (1a), whereas stochastic relationships are depicted in Equation (1b). The dependent variable in the model is ERit (economic growth), whereas the explanatory variables are TPNit (trade openness), FPDit (foreign public debt), DPDit (domestic public debt), FDIit (foreign direct investment), CPSit (capital stock) and PPGit (population growth). The vector Xit contains all the explanatory variables, and μit is the stochastic error term. The parameters α

j

(j = 1, 2, …, 6) are coefficients of the corresponding explanatory variables. Theoretically, economic growth is expected to bear a positive relationship with all the explanatory variables (α

j

˃ 0). The stochastic model (Equation (1b)) is transformed into the GMM model as proposed by Arellano and Bond (1991), and extended by Blundell and Bond (1998), as follows:

Equation (2a) represents the GMM model relating the dependent variable to its own lag and the lags of explanatory variables, including the unobserved country effect represented by the parameter τit. The vector Xit–1 contains the lagged explanatory variables. The model is normalised in Equation (2b) by transforming the variables into logarithmic first differences, as indicated by the operator (Δ), which eliminates the country effect. Instrumental variables are included by increasing the period of lagged dependent variable from one to three, which helps to minimise auto-correlation. In theory, instrumental variables are expected to be strong correlates of the lagged dependent variable (ΔlnEGit–1); hence, ΔlnEGit–2 and ΔlnEGit–3 are included in this model as the instrumental variables.

The interaction between trade openness and sovereign debt in facilitating growth has also been given theoretical exposure in the works of Allen (1961), Combes and Sedik (2002) and Zakaria (2012), supported by IMF (2014). In view of this exposure, the direct effect model is modified to include the interactive effect, by introducing the interaction term as follows:

In Equation (3a), the interactive effect of trade openness and sovereign debt is introduced into the model. The vector Zit–1 contains the interactive terms (TPN–1^FPD–1 and TPN–1^DPD–1). The model is normalised in Equation (3b), and required to meet the moment conditions stated below in order to produce reliable estimates.

E(εit) = E[εit(η)] = E[f(EGit, Xit–1, Zit–1, η)] = 0

E(Q′εit) = 0, where Q represents the instrumental variables

V(η) = εit(η)′ Q[Q′Σ(η)ZV]–1 Q′εit (η), where V is value function of unknown parameter η.

There is η* that minimises the value function V(η), making it normally distributed.

Generally, the GMM model has been employed in several studies to determine the dynamic relationships among variables. Such studies include Andrei et al. (2017), Gries and Redlin (2012), Taghizadeh-Hesary et al. (2019) and others. In this study, the model is estimated for the period 1980–2020, with data obtained from World Bank Open Database, World Development Indicators, OECD Statistics and IMF World Debt Table. The measures of the variables are indicated in parentheses as follows: economic growth (GDP growth rate), trade openness (import plus export of goods as a percentage of GDP), foreign public debt (as a percentage of GDP), domestic public debt (as a percentage of GDP), foreign direct investment (as a percentage of GDP), capital stock (gross fixed capital formation as a percentage of GDP), population growth (growth rate of the population).

Empirical Results and Analysis

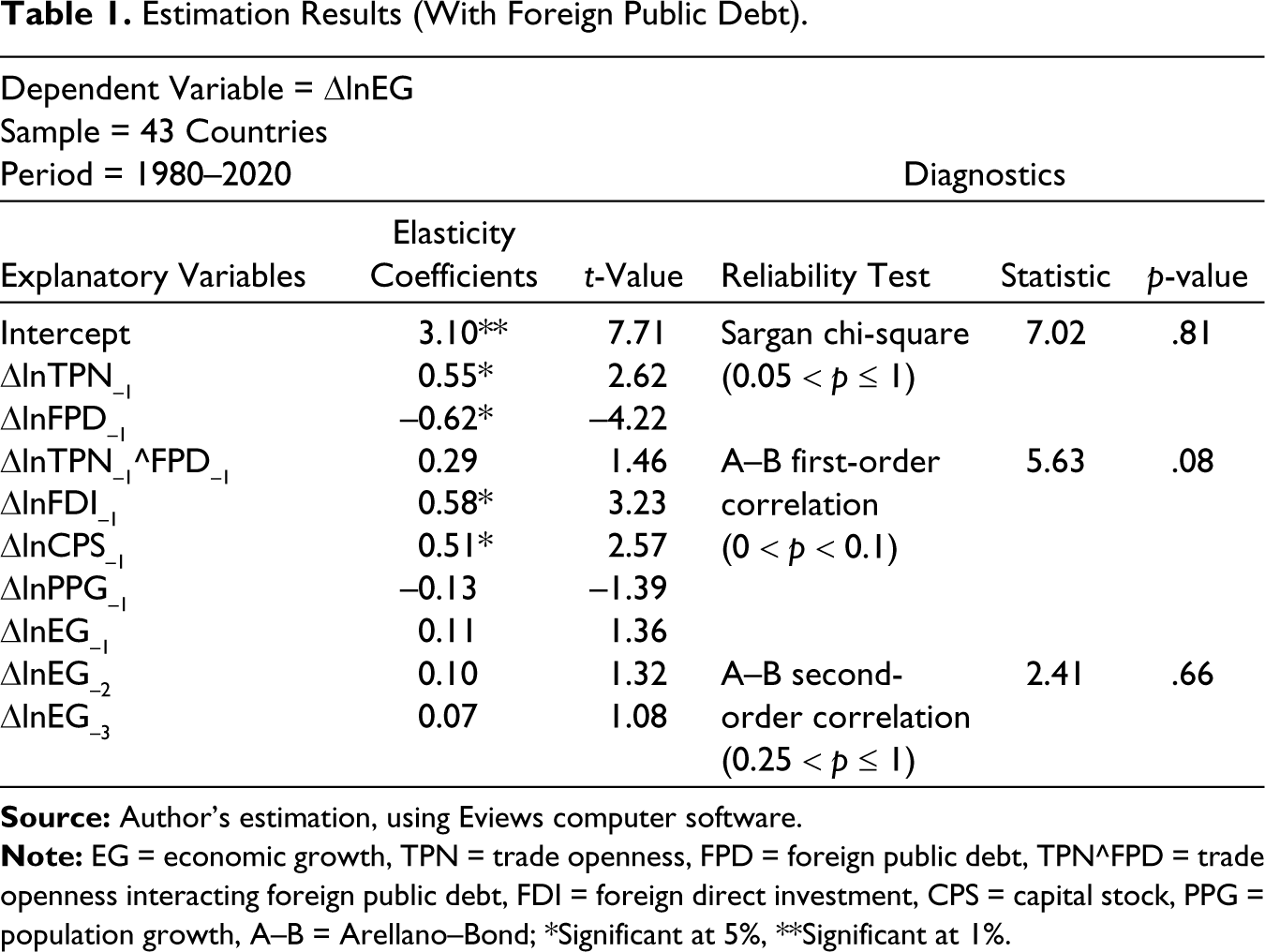

Estimation Results (with Foreign Public Debt)

The first estimation was carried out by including the foreign public debt component, as shown in the results reported in Table 1. In the results, one unit increase in trade openness (ΔlnTPN–1) directly led to a rise of 0.55 in economic growth (ΔlnEG), which is significant at 5% level. The results also show that foreign public debt (ΔlnFPD–1) had a significant negative effect of –0.62, which means that the direct effect of foreign public debt on economic growth is unfavourable, contrary to expectations. However, the interactive effect of trade openness and foreign public debt (ΔlnTPN–1^FPD–1) on economic growth is 0.29, which is positive but insignificant. Foreign direct investment (ΔlnFDI–1) and capital stock (ΔlnCPS–1), as control variables, had significant positive effects of 0.58 and 0.51, respectively, and therefore encouraged growth. The effect of population growth (ΔlnPPG–1) is –0.13, which indicates an adverse contribution to economic growth. The one-lag economic growth (ΔlnEG–1) has an estimate of 0.11, which is insignificant, indicating that growth did not sufficiently reinforce itself. The insignificant response of economic growth to itself is also replicated in the two-lag economic growth (ΔlnEG–2) and three-lag economic growth (ΔlnEG–3), with corresponding estimates of 0.10 and 0.07. It is particularly importance to note that the interactive effect, though weak, turned out to be positive. Therefore, foreign public debt fairly complemented trade openness in driving economic growth. The theory of trade openness interacting with sovereign debt to facilitate economic growth is thus validated.

The diagnostics show that the p-values of Sargan statistics fall within the critical range, hence the null hypothesis of no correlation between instrumental variables and residuals can be accepted. Similarly, the p-values of Arellano–Bond (A–B) statistics fall within the critical range, indicating acceptance of the null hypothesis of no correlation among the residuals. The direct and interactive effect estimates of the model are, therefore, unbiased and reliable.

Estimation Results (With Foreign Public Debt).

Estimation Results (with Domestic Public Debt)

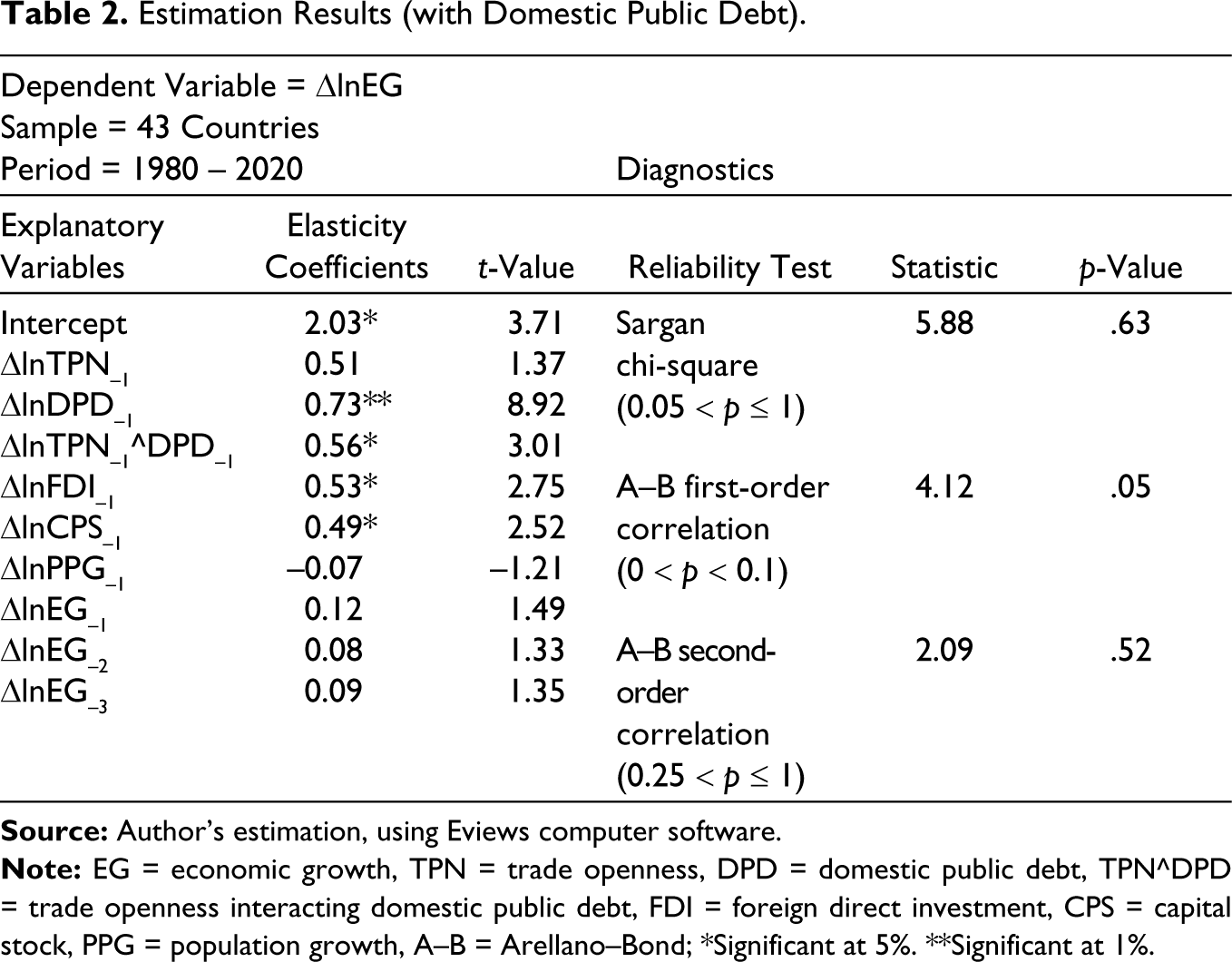

The second estimation was carried out by including domestic public debt component, as shown in the results reported in Table 2. The results reveal that the direct effect of trade openness (ΔlnTPN–1) on economic growth (ΔlnEG) is 0.51, which is positive and significant at 5%. The direct effect of domestic public debt (ΔlnDPD–1) is 0.73, which is even more significant at 1%. The interactive effect of trade openness and domestic public debt (ΔlnTPN–1^DPD–1) is 0.56, which is significant at 5%. It follows that domestic public debt strongly complemented trade openness, in driving economic growth. It is also observed that foreign direct investment (ΔlnFDI–1) and capital stock (ΔlnCPS–1) have estimates of 0.53 and 0.49, which are again significant at 5%. The effect of population growth (ΔlnPPG–1) remains negative with an estimate of –0.17, whereas the three lags of economic growth (ΔlnEG–1, ΔlnEG–2 and ΔlnEG–3) remain insignificant. The results of this estimation strongly validate the theory of trade openness interacting with sovereign debt to facilitate economic growth.

Estimation Results (with Domestic Public Debt).

Sargan statistic of 5.88 falls within the critical range; hence, the null hypothesis of no correlation between instrumental variables and residuals can be accepted. Similarly, A–B statistics of 4.12 and 2.09 fall within the critical range, indicating acceptance of the null hypothesis of no correlation among the residuals. The estimated interactive effects of trade openness and sovereign debt are, therefore, consistent and reliable.

Structural Stability

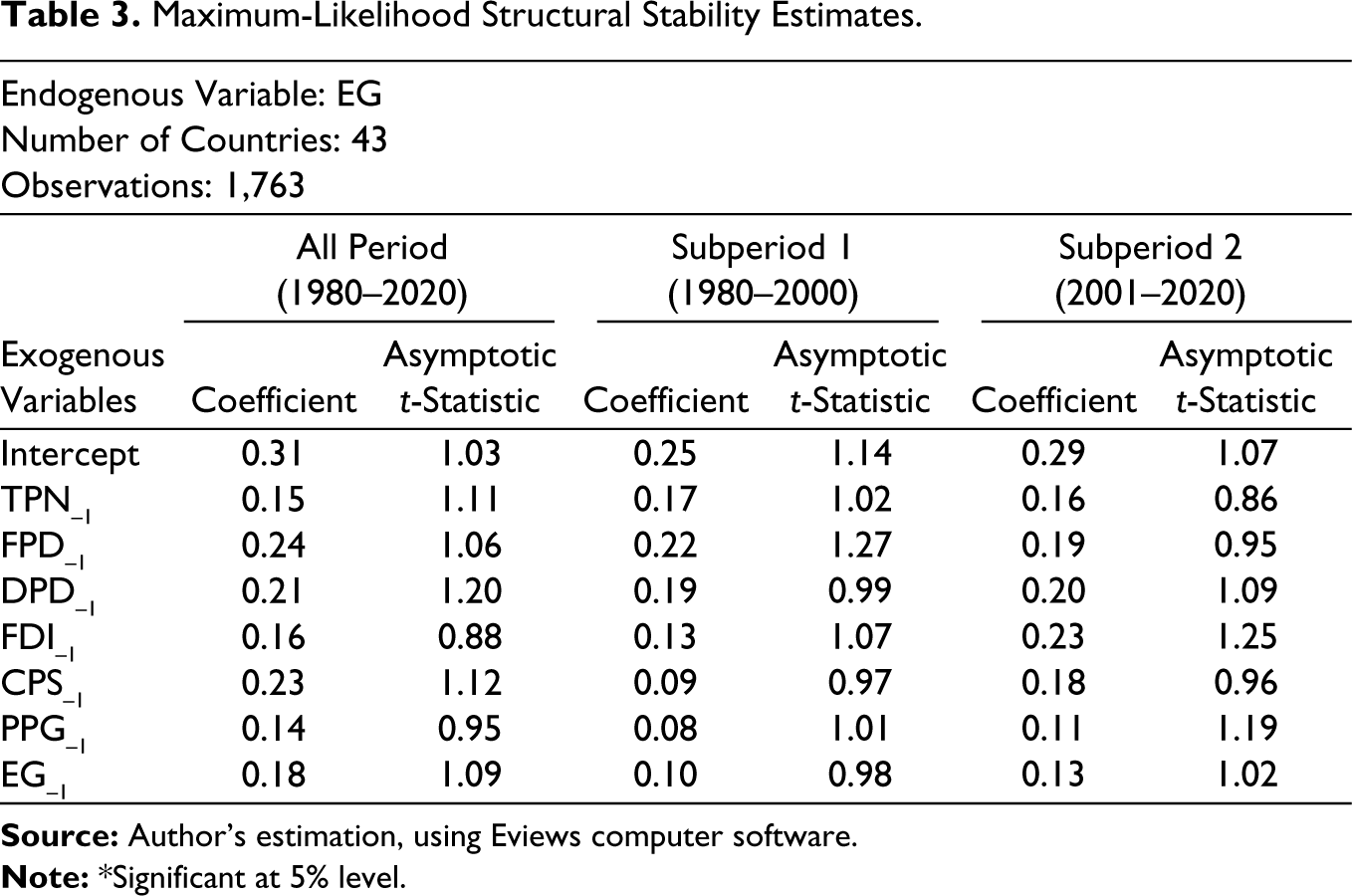

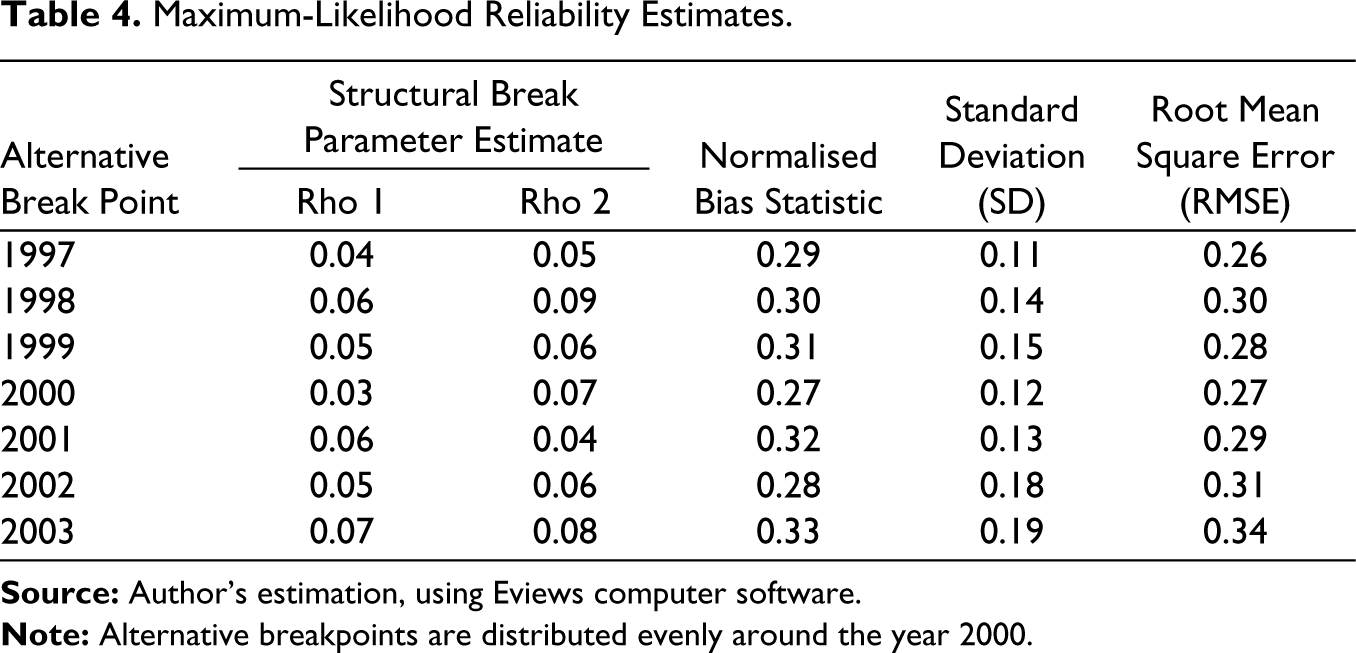

Results of the model can only be considered useful for purpose of policy making when long-run structural stability exists in the economy. It is, therefore, important to conduct a test of stability. In this study, the maximum-likelihood technique is employed to test for structural stability. It involves splitting the panel data of the entire study period into two sub-periods, by choosing a suitable breakpoint (Yu et al., 2008). The breakpoint in this study is the year 2000, which was characterised by structural reforms in all the countries under investigation. The test results are reported in Tables 3 and 4.

In Table 3, the maximum-likelihood estimates of the entire period (1980–2020) and sub-periods (1980–2000 and 2001–2020) are generally not significant at 5% level. Again, the sub-period estimates of each variable are not significantly different. Therefore, the null hypothesis of no structural stability is rejected, hence the long-run estimation results may be considered suitable for policy making. In Table 4, the variations in values of structural break parameters (Rho 1 and Rho 2), normalised bias statistic, standard deviation, and root mean square error, are not significant. These values confirm that the structural stability estimates are unbiased and reliable.

Maximum-Likelihood Structural Stability Estimates.

Maximum-Likelihood Reliability Estimates.

The Implications of Study

In the descriptive analysis section of this study, trade openness and sovereign debt in SSA were observed to have increased over the past four decades. Empirical results revealed that the trend of trade openness had a direct favourable effect on economic growth. In the case of sovereign debt, the domestic component had direct favourable effect, whereas the foreign component had a direct adverse effect. On the contrary, the interactive effect of trade openness and sovereign debt (foreign and domestic components) was found to be favourable. Two control variables (foreign direct investment and capital stock) also played a positive role in driving economic growth, whereas one control variable (population growth) played a negative role. In spite of the positive effects (direct and interactive) of a larger number of variables, economic growth in SSA countries has not been able to reinforce itself, over time. The implications of these findings are not far-fetched.

The direct favourable effect of trade openness on economic growth in this study does not support the findings of Alessandro De Matteis (2004) and Zahonogo (2016), where trade openness contributed negatively to growth. It is, therefore, pertinent for SSA countries to strengthen trade openness, in order to sustain its positive role in economic growth. This could be done by expanding the export base.

The direct favourable effect of domestic public debt, and the direct adverse effect of foreign public debt, align partially with the findings of some studies that reported only the positive or negative impact of sovereign debt. These studies include Ssempala et al. (2020), Bidzo (2018) and Asteriou et al. (2021). However, SSA countries may need to reverse the negative impact of foreign public debt on economic growth, by ensuring that the external debt burden does not exceed the IMF/World Bank prescribed optimum level of 30% (IMF, 2018).

The favourable interactive effect of trade openness and sovereign debt on economic growth conforms to the theoretical arguments of Allen (1961), Combes and Sedik (2002) and Zakaria (2012), that trade openness and sovereign debt are complementary. It is, therefore, important for these countries to maintain the favourable effect by strengthening trade openness and regulating the level of sovereign debt.

The findings on the interactive effect of trade openness and sovereign debt in this study are expected to create a benchmark for further studies on the interface between trade openness and sovereign debt in the economic growth of developing countries.

Conclusion

The role of trade openness in economic growth cannot be over emphasised. However, its direct impact has been a subject of controversy among researchers in developing countries. The direct impact of sovereign debt on economic growth is even more controversial, due to the burden of repayment. The existing studies seem to have focused largely on the direct effect of trade openness and sovereign debt on economic growth. The interactive effect that has been given theoretical exposure by some economists remains under-investigated. In order to bridge this gap, an attempt is made in this study to determine both direct and interactive effects of trade openness and sovereign debt on economic growth in SSA countries. The study employed the methodology of GMM to investigate the issue, within the period 1980–2020.

The results revealed that trade openness exerted a direct positive impact on growth. The direct impact of domestic public debt is also positive. However, foreign public debt had a direct negative impact on growth. The results also showed that the interactive effect of trade openness and sovereign debt (foreign and domestic) was favourable to economic growth, which indicates that the two variables are complementary. Two control variables (foreign direct investment and capital stock) also contributed positively to growth, whereas one control variable (population growth) tended to impair the economic growth process. In spite of the salutary role of several variables, economic growth in SSA countries has yet to achieve the desired level.

These estimation results do not support the claims in some existing studies that trade openness has a negative impact on economic growth in developing countries. On the contrary, trade openness tends to encourage growth in SSA. Again, the results partially support the outcomes of some existing studies that found only the positive or negative effect of sovereign debt on economic growth in developing countries. More importantly, the estimation results validate the theoretical argument that trade openness and sovereign debt are complementary, in facilitating the growth of developing countries. Therefore, appropriate policies are required to ensure that trade openness and sovereign debt maintain favourable effects (direct and interactive) on economic growth in SSA.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

In the absence of research grant, this study was funded from personal savings of the author.