Abstract

The study examines the interaction effect of trade and institutional quality on financial sector development in 20 leading economies in sub-Saharan Africa selected based on 2018 GDP per capita ranking (top 20 richest economies by GDP per capita released by the IMF) over the period 2005–2020. Using system-generalised method of moments estimation, the results indicate that the effect of the interaction term of trade and regulatory quality on financial development is positive and significant. Further findings show unidirectional causality running from the interaction term to financial development, implying that the likelihood of trade enhancing financial development depends on the soundness of the regulatory framework. It is confirmed that the magnitude and direction of the effect of trade on financial development are sensitive to the quality of institutions. Therefore, the poor quality of regulations on business activities and financial services could undermine the salutary impact of trade on financial development. It is suggested that creating a conducive regulatory environment to improve the level of financial development is crucial for mitigating the potential impact of the weak institutional quality risks. This remains a significant prerequisite for having a competitive business environment, thereby stimulating the role of trade in the process of financial development.

Keywords

Introduction

The political and socio-economic globalisation has been driven by the movement of human resources, goods and services (such as financial services) across national borders. Based on classical theories (such as absolute advantage), comparative advantage and Heckscher–Ohlin’s factor endowments, countries get involved in trade basically due to relative costs of production or factor endowments over others. Thus, opening up the economy to trade is central to improved economic performance. Although with significant knock-on benefits for the economy as a whole, openness to foreign financial services can lead to greater efficiency, dynamism and innovation by the providers, thereby stimulating the development of the domestic financial sector (Claessens, 2006; Mattoo et al., 2001).

In recognition of the significance of continental trade, African countries, on 30 May 2019, entered into force of the African Continental Free Trade Agreement (AfCFTA), which offers a significant avenue for the continued increase in their trade with respect to services. Accordingly, it is essential to give attention to the prominent role of services as the AfCFTA negotiations persist, because services seem to play a critical role in intra-African integration and the future of continental trade (Madden, 2019). It has become imperative for Africa to embrace this initiative, as Trade Facilitation Agreement may result in a decrease in trade costs of up to 15%, and has been linked to the attainment of the 2030 Agenda for Sustainable Development (UNCTAD, 2018). Hence, deep analysis of trade–finance nexus is crucial to economic development, especially in the African context. Given that economic prosperity is often measured by GDP per capita growth rates, the study focuses on 20 leading economies in sub-Saharan Africa (SSA). These countries are selected based on GDP per capita ranking (top 20 richest economies by GDP per capita (PPP) released by IMF (IMF, World Economic Outlook, 2018)). Pertaining to SSA in general, given the size of their GDP per capita, most of the selected countries contribute significantly to the region’s economic performance. For instance, Nigeria, which is among the countries selected, accounts for over 70% of sub-regional GDP in West Africa, and if Ghana, Côte d’Ivoire and Senegal are added, in total, it will amount to 90% (African Development Bank (AFDB), West African Economic Outlook, 2018). As a result, the study’s findings can be sufficient for offering effective policy measures considered appropriate for entire SSA countries.

Financial sector development has been the key stimulator of economic growth (Assefa & Mollick, 2017; Levine et al., 2000). While it has been discovered that SSA financial sectors are mainly bank-based, the region’s financial systems are largely underdeveloped (Andrianaivo & Yartey, 2009). A survey of the financial sector reforms between the 1980s and 1990s regarding Africa revealed that the move to improve the financial sector resulted in the enactment of some critical reforms, such as the liberalisation of interest rates, abrogation of credit ceilings, restructuring and privatisation of state-owned banks, institutionalisation of a variety of measures to enhance the development of financial markets (Senbet & Otchere, 2006). Nonetheless, Rajan and Zingales (2003) and Ibrahim and Alagidede (2017) opine that legal origin hugely elucidates the cross-country differences in the development of the financial sector. The argument, therefore, that financial sector development could be strongly influenced by the level of trade openness (Kim et al., 2010; Samba & Yan, 2009) might not hold in SSA considering the region’s economic peculiarities and pervasive weak institutions. The relationship between international openness and finance could be conditional on the quality of institutions or economic conditions (Bordo & Rousseau, 2012; Zhang et al., 2015). However, apart from a few authors like Awudu et al. (2018) who examine the nexus between finance and international trade based on the intermediate effect of economic growth mainly in Africa’s context, with respect to SSA, in general, studies on trade–finance nexus with the consideration of the intermediate role of institutions seem to have not been sufficiently explored. Beyond the seemingly direct effect of trade, the precise role of trade in the financial sector development process given governance quality is somewhat ambiguous. Due to this, there has been increasing concern as to the indirect effect of trade on financial sector development via the impact of institutions in SSA as a whole.

Arguably, SSA countries are still lagging behind in terms of attaining sound financial systems. Given this, the study is expected to offer a viable comprehensive model for stimulating the development of financial sectors across countries in the region. It also sets out to examine whether both trade and the quality of institutions are crucial determinants of financial sector development in the region. Furthermore, findings from the study may substantiate the claim that weak institutional arrangements and limited administrative capacities which are capable of undermining the potential role of international trade contribute to the underdeveloped state of the financial sector in the region.

Following the foregoing, the study examines the nexus between trade and financial sector development through the institutional channel in 20 leading SSA economies. The research findings would point out whether a trade is significant in determining the level of financial sector development in the region. Hence, for the adoption of a sustainable approach that can aid the development of the financial sector in the region, the novel contribution of the study will also stem from the application of the system-generalised method of moments (GMM). We follow this approach based on the notion that economic phenomena are persistent (Doyle, 2017). Given that the number of countries (20) is higher than the number of time period, the use of the technique is appropriate—in case of the dynamic panel, system-GMM seems to be the most efficient and reliable estimation technique, and even with the short sample period (Arellano & Bover, 1995; Fagbemi & Bello, 2019).

Literature Review: Theoretical Background and Empirical Evidence

McKinnon (1973) and Shaw (1973) argue that financial sector development could be affected by restrictions placed on the operation of financial systems by the government. Such restrictions could be in form of interest rate ceilings, directed credit programmes, reserve and liquidity requirements, which may hamper the quality and quantity of investment. Indeed, their framework suggests that interest rate controls can distort the economy in several ways. First, it may discourage entrepreneurs from investing in high-risk projects despite being potentially high-yielding investments. Second, financial intermediaries may become more risk averse and practice preferential lending to established borrowers. Third, borrowers who obtain their funds at relatively low costs may prefer to invest in only capital-intensive projects. Thus, high reserve requirements act as a tax on the banking system, resulting in further depression of interest rates. They, therefore, conclude that financial liberalisation and less government intervention in controlling and imposing ceilings on interest rates are vital for the financial sector development. This view is guided by the legal and finance theory/politics and finance theory. According to Olson (1993) and North (1990), the ruling class may create laws and institutions that would be supportive to the development of the financial sector, if they see that free financial markets would promote their interests. Therefore, the quality of institutions is a key determinant of the financial sector development.

Many researchers have demonstrated that finance is the core of economic performance (Khatun & Bist, 2019; Law & Singh, 2014; Robinson, 1952). However, the literature seems to have given less attention to the indirect effect of trade openness on financial development through the medium of institutional quality. Most of the studies pinpointed that financial sector development plays a prominent role in the economic growth process (Levine, 2005; Shahbaz & Rahman, 2012; Shaheen et al., 2011). Since the joint impact of trade openness and institutional quality on financial development could be associated with many controversies, investigating the role of these indicators, in the context of leading economies in SSA, may present different elucidations or another explanation for the reason for which the financial sector is at its current level in the region.

International Trade and Financial Sector Development

In the literature, one of the determinants of financial sector development is the level of international trade in the economy (Rajan & Zingales, 2003). It is argued that both the degree of openness and financial sector development are strongly correlated. Trade openness could affect the quest for external financing, and thus the state of financial deepening in an economy (Do & Levchenko, 2004). Empirically, based on samples from countries in the Asia Pacific region, Le et al. (2016) examine the link between trade openness and financial sector development, and it is affirmed that the development of the banking sector is positively determined by the openness of the countries’ trade. Similarly, Zhang et al. (2015) demonstrate that financial efficiency is enhanced by both trade openness and capital account liberalisation. Aggarwal et al. (2011) and Anzoategui et al. (2014) suggest that remittance and the state of financial sector development are strongly associated. Regarding the impact of foreign direct investment (FDI), the financial sector development in the host country is significantly and positively influenced by the level of FDI in the recipient country. In addition, following data from 50 countries joining the Belt and Road Initiative, Aibai et al. (2019) show that FDI is a significant determinant of the development of the financial sector.

Bilas et al. (2017) find a positive long-run and adverse short-run association between international trade and financial sector development in Croatia. Based on China, Zhang et al. (2015) investigate the effect of trade and financial openness on financial sector development. These authors argue that financial efficiency and competition are positively impacted by trade and financial openness. However, results indicate a negative effect on the size of financial sector development. Wajda-Lichy et al. (2019) using the Granger bootstrap panel approach based on seemingly unrelated regressions, the causality between trade openness and financial sector development in 11 new member states in the European Union. Findings show that unidirectional causality exists which runs from trade to finance in eight countries (Bulgaria, Estonia, Hungary, Latvia, Lithuania, Poland, Romania and Slovenia). On the other hand, finance significantly Granger causes trade in six countries (Croatia, Estonia, Latvia, Lithuania, Poland and Slovakia). In the study, the supply-leading hypothesis is majorly supported by the results. The empirical studies result in the argument that the findings on the trade–finance nexus are mixed. While some researchers confirmed that higher the level of trade and the higher the degree of financial sector development (Beck, 2002; Manova, 2013), Menyah et al. (2014) stress a weak relationship or conditional by the quality of institutions, showing causal direction from finance to trade. Economic or political institutions also determine the nexus from openness to finance (Bordo & Rousseau, 2012; Zhang et al., 2015). These studies majorly focused on high-income economies, whereas low- or middle-income economies (which include most SSA countries) have not been given sufficient coverage. Given this, it could be hypothesised that trade is significantly and positively associated with financial development in leading SSA economies.

Institutional Quality and Financial Sector Development

Empirical research on the role of institutional quality in financial sector development is one that has engaged the attention of some scholars. But the study on the indirect effect of institutions on financial sector development has received limited attention. Starting from North (1981), who initiated institutional economics, institutional quality has been viewed to be one of the significant determinants of economic development (Acemoglu & Verdier, 1998). Better quality of institutions stimulates international trade and FDI more effectively (Buchanan et al., 2012; Levchenko, 2007). Several arguments have been raised in support of the nexus between the quality of institutions and financial sector development (Huang, 2010; Law & Azman-Saini, 2012; Le et al., 2016; Nkoa & Song, 2020; Rajan & Zingales, 2003). Based on 469 firms listed on the Tehran Stock Exchange, Rostami et al. (2016) maintain that there is a significant and positive linkage between governance measures and financial market returns. In addition, Yasmina and Mohamed (2016) show that institutional quality is a key determinant of financial sector development in the MENA region between 1996 and 2011. The study’s measure of the quality of institutions is captured by an index representing the ability of governments to formulate and implement good policies as well as the degree of compliance with public institutions among citizens and government. Regulations related to law, institutions and political stability are found to have an influence on financial inclusion (Allen et al., 2016). This is equally held by Bongomin et al. (2018) in their study in Uganda. Similarly, in some African countries, Dwumfour and Ntow-Gyamfi (2018) support the assertion that the quality of institutions stimulates financial sector development. Regarding Nigeria, while Fagbemi et al. (2020) argue that regulatory quality is a significant determinant of stock market development, Fagbemi and Ajibike (2018) posit that institutional quality (institutional index representing political risk index such as investment profile, control of corruption, law and order, democratic accountability, government stability and bureaucratic quality) does not significantly explain financial sector development in the country. Strong institutional quality and a good legal system in a country would enhance the spillover effect of FDI on the recipient country’s economic development, resulting in increased activeness of FDI in the promotion of financial sector development (Alfaro et al., 2010). Thus, the hypothesis proposed in this study is that good institutional quality strongly influences the effect of international trade on financial development in SSA leading economies.

Methodology

Theoretical Framework

Given the basic objective of the study, the demand-following hypothesis is used as the theoretical framework. It is assumed that ‘trade creates demand for financial services’ (Wajda-Lichy et al., 2019, p. 2). Under this condition, exporters’ and importers’ need for external funds is somewhat related to international payments, likewise the reduction of commercial risks. This is based on the argument that in competitive international markets, with the creation of a permanent investment process, given the engagement of producers of tradable goods in such markets, exporters have to demand for external funds. Robinson is the proponent of the demand-following hypothesis, which is summarised as ‘where enterprise leads, finance follows’ (Robinson, 1952, p. 86). This theory was later supported by Rajan and Zingales (2003) who stressed that economic openness could cause financial sector development in light of the analysis of market structure. Furthermore, Baltagi et al. (2009) show support for the simultaneous openness hypothesis by giving evidence that both trade openness and economic institutions (or political institutions) could significantly influence financial development. It is emphasised that economic institutions are shaped by political institutions, thereby impacting financial sector development. Hence, given that the state of government regulations matter in the development of the financial sector based on the theoretical stance, in the study, regulatory quality is used as the indicator of institutional quality.

Econometric Techniques

The estimation approach adopted in this study is the system-GMM. We follow this approach based on the notion that economic phenomena are persistent (Doyle, 2017). Given that the number of countries (20) is higher than the number of time period, the use of the technique is appropriate—in the case of the dynamic panel, system-GMM seems to be the most efficient and reliable estimation technique, and even with the short sample period (Arellano & Bover, 1995; Fagbemi & Bello, 2019). By accounting for simultaneity in the explanatory variables through an instrumentation process, the estimation strategy takes endogeneity into account on the one hand, and, on the other hand, controls for the unobserved heterogeneity with time-invariant indicators. The system estimator corrects for inherent biases that are characteristic of the difference estimator. Based on the framework followed in this study, the Roodman (2009) empirical procedure is adopted. Under this condition, over-identification decreases, and cross-sectional dependence is accounted for (Baltagi, 2008; Boateng et al., 2018).

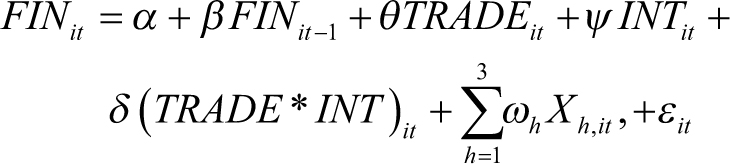

The standard system-GMM estimation procedure is summarised in level in Equation (1),

where FINi,t indicates financial sector development for country i in period t; FINi,t–1 is the financial sector indicator lagged by 1 to represent the initial level of financial development which accounts for the lagged dependent variable as well; INTi,t is the institutional quality indicator for country i in period t; TRADEi,t is the trade (% of GDP) for country i in period t; α is the constant; X is the vector of control variables: GDP growth (annual %) and FDI, net inflows (% of GDP); TRADE * INT is the interaction term of trade (% of GDP) and institutional quality (regulatory quality); and ε it represents the error term. θ, ψ, δ & ω are the coefficients (intercepts) of trade (% of GDP), regulatory quality, the interaction term and vector of control variables, respectively. Equation (1) has incorporated the individual effects of trade (% of GDP) and regulatory quality on the financial sector development.

where ϑit is the disturbance error term, while μit is the unobserved time-invariant country-specific effects.

Since a given variable may have something to do with explaining itself, there could be the possibility of dynamic information in the panel data framework, such that the incidence of endogeneity between financial sector development indicator and explanatory variables is possible (Wooldridge, 2002). Hence, to incorporate dynamics into the model, Equation (1) is then transformed to

To account for country-specific effects, Equation (3) is written in first differences which eliminate the country-specific effect component.

To account for the incidence of endogeneity bias, the two-step system-GMM estimation is specifically employed. Through the optimal weighting matrix, the efficiency gains of GMM estimation are obtained, Sargan test (the overidentifying restrictions of the model) and the relaxation of the assumption of i.i.d. In the model, it is expected that

Granger causality test is employed within the framework of the panel vector autoregressive model with the use of the following set of equations:

where Δ denotes the first difference operator, FINit, TRADE * INTit and μit stand for the financial sector development, the interaction term of trade and institutional quality and error term, respectively. Similarly, k = 1 denotes the minimum lag length selection which starts from 1, while p represents the maximum lag selected for the estimation. In the model, only both GDP growth (annual %) and regulatory quality are not in logarithm form as they are given in rates and also have negative values. Overall, the study deals with unbalanced panel data.

Data Description and Sources

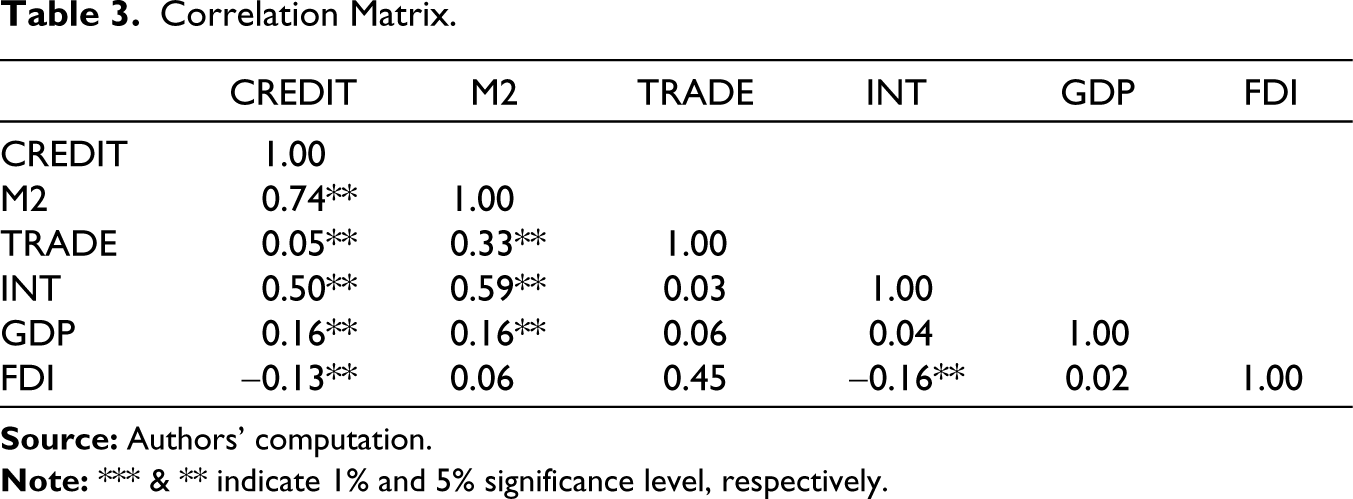

In the study, a panel data set covering the period 2005–2020 is used. The choice of the scope is mainly based on the availability of data for 20 countries covered. These countries are Equatorial Guinea, Seychelles, Mauritius, Gabon, Botswana, South Africa, Namibia, Eswatini, Cabo Verde, Republic of Congo, Angola, Nigeria, Ghana, Mauritania, Côte d’Ivoire, Zambia, Cameroon, Djibouti, Kenya and Senegal. We make use of two financial sector development indicators: domestic credit to the private sector (% of GDP) and broad money (% of GDP). The use of these financial sector development indicators is informed by the literature (Abdelaziztouny, 2014; De-Han, 2015; Fagbemi & Ajibike, 2018; Fagbemi et al., 2018). Trade (% of GDP) is the trade indicator, while regulatory quality is taken as the governance quality chosen to assess the intermediating role of institutional quality in trade–finance nexus. In addition, two control variables are employed: GDP growth (annual %) and FDI, net inflows (% of GDP). Since the concurrent use of private sector credit to GDP and M2 to GDP in the model may result in spurious outcomes due to their high similarity, the analysis involves two models with these financial sector development indicators taken as dependent variables respectively, while other variables are incorporated as independent variables. Data on financial sector development indicators, trade openness, GDP growth (annual %) and FDI were sourced from World Development Indicators, World Bank (2021), whereas that of the institutional measure were obtained from World Governance Indicators. The description and sources of the data are specifically stated in Table 1.

Data Description and Sources.

Empirical Results and Discussion

Descriptive Statistics

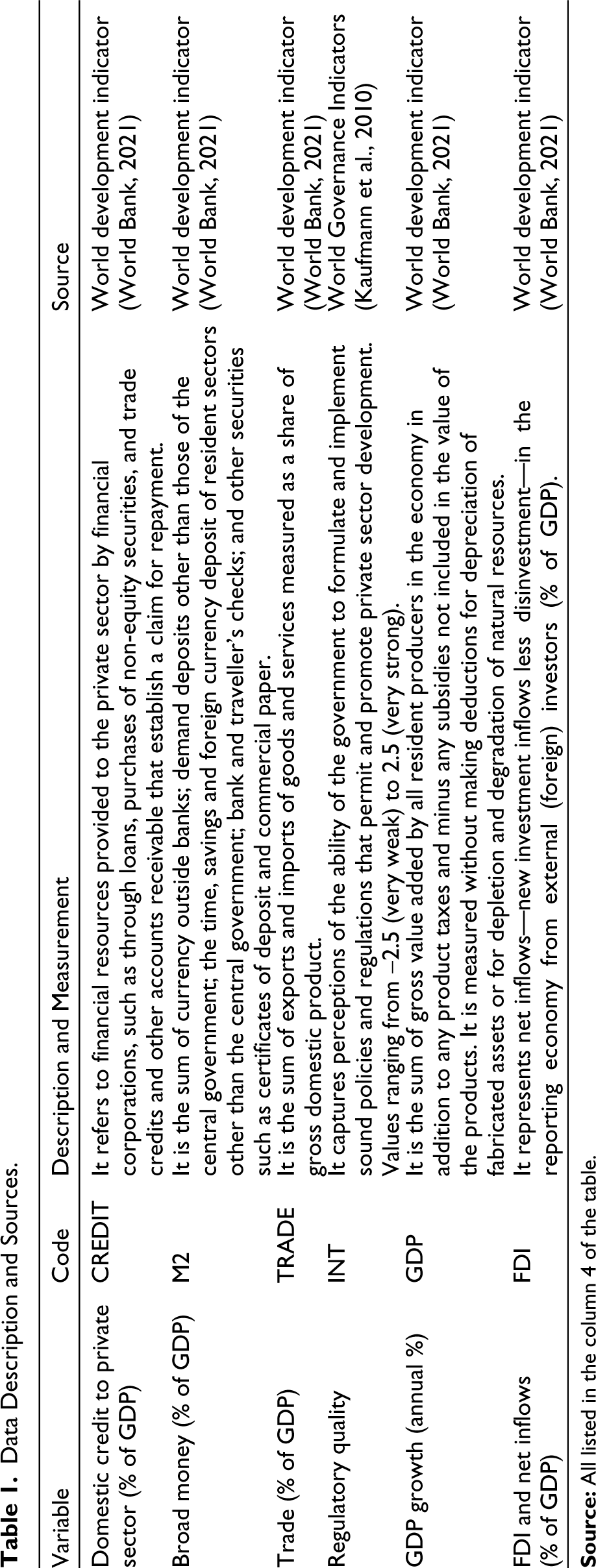

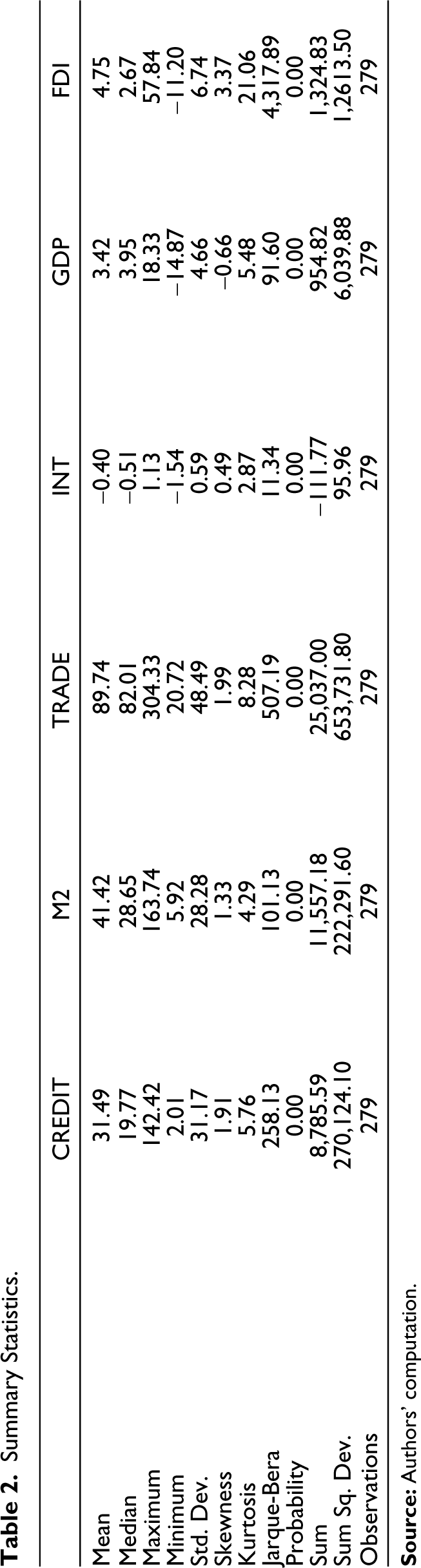

Table 2 shows summary statistics. Given the standard deviation, both financial sector development indicators used (CREDIT and M2) are widely varied across countries. The average level of financial sector development (CREDIT = 31.49%; M2 = 41.42%) is far below the world average of 104.35%. This implies that the selected countries have a lower level of financial sector development compared to the global average. The minimum and maximum values reflect a wide range for each variable in the model, prompting the use of dynamic system-GMM to enhance the robustness of the estimates. The trade in the countries seems to be more liberalised, as the average value of imports and exports amounts to 89.74% of GDP, which is somewhat above the world average, thus, the African leading economies are more open to trade. However, there is a wide variation in the level of trade across countries. On the regulatory quality, the selected countries have relatively weak regulatory systems necessary for the development of the financial sector. In addition, Table 3, which presents the correlation matrix, indicates that both TRADE and INT are significantly and directly correlated with financial sector development. This suggests that the level of trade and institutional quality could determine the dimension of financial sector development.

Summary Statistics.

Correlation Matrix.

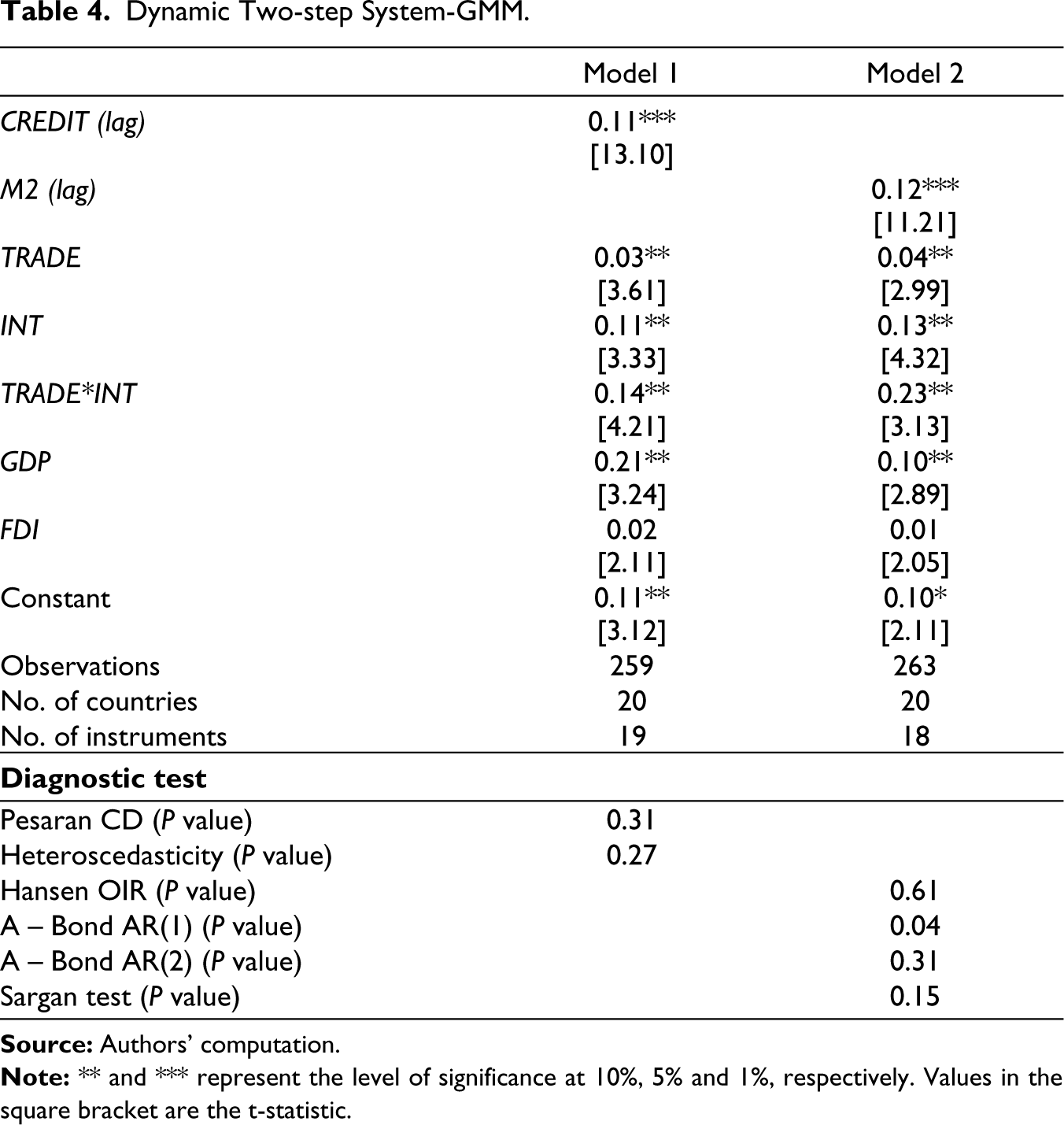

Dynamic Two-step System-GMM Estimation

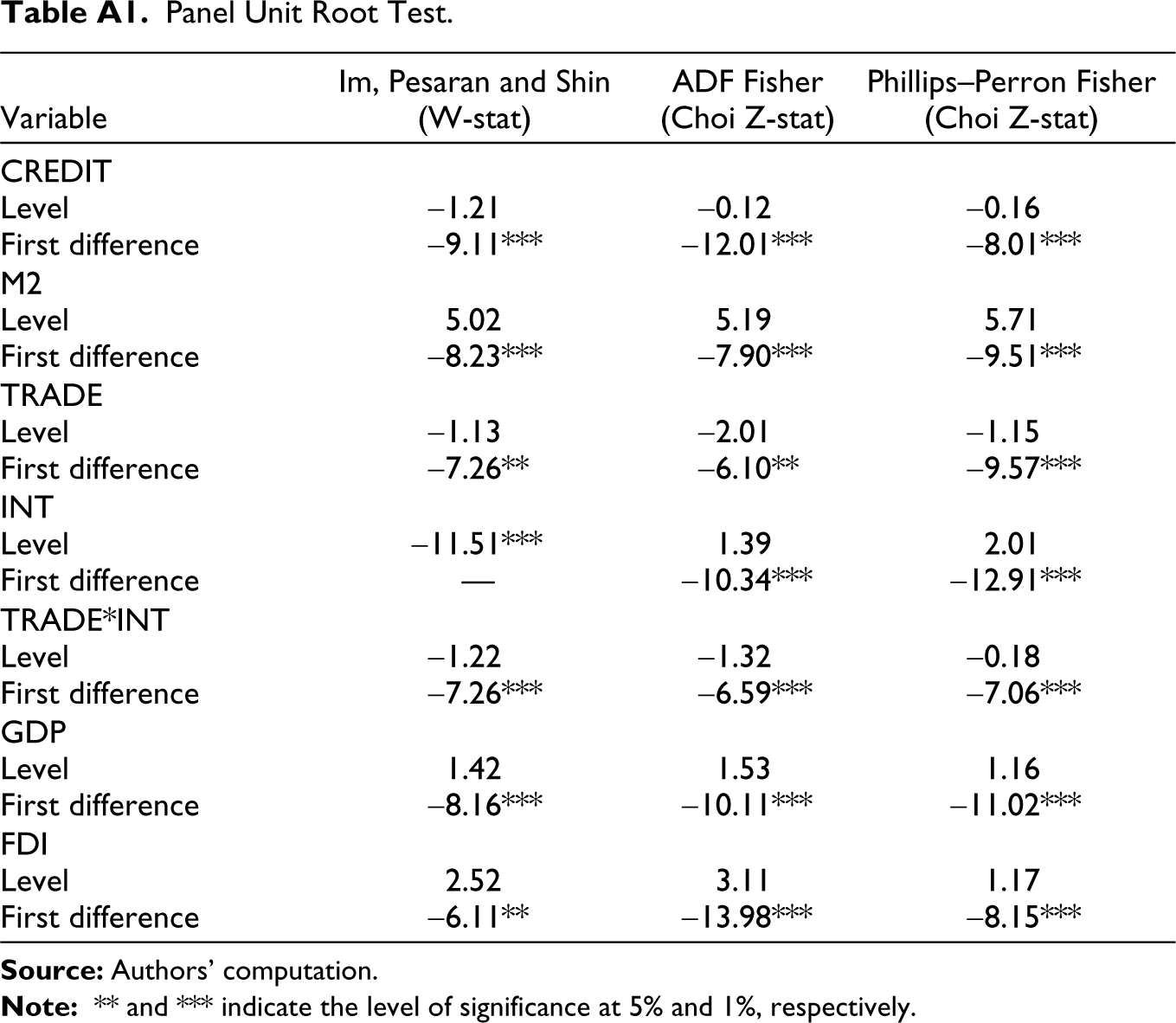

The estimated results in Table 4 allow us to explain the effect of the interaction term of trade and institutional quality on financial sector development in selected SSA countries. The analysis contains two models. 1 While model 1 indicates the use of CREDIT as the dependent variable, model 2 is for M2. The diagnostic test shows that the specification follows a statistically robust process. Although in dynamic Two-step System-GMM estimation, the test of unit root is not necessary, it is reported in the Appendix (Table A1) to enable us to know the specific features of the variables. As we first accounted for the estimates without the interaction term, results show that regulatory quality has a larger positive effect on the financial sector development compared to trade. This shows that no matter the level of trade in SSA, the quality of the regulatory framework matters in this case. Regarding the interaction term, as anticipated, the estimates of TRADE*INT in models 1 and 2 are significant and positive as well. This means that, jointly, trade and institutional quality significantly stimulate the level of financial sector development in the countries. It is, indeed, confirmed that financial sector underdevelopment is more pervasive in countries where the institutional quality is poor, and trade is less liberalised (Law & Azman-Saini, 2012;; Le et al., 2016; Nkoa & Song, 2020; Zhang et al., 2015). This further gives credence to the hypothesis that sound institutional quality consolidates the effect of trade on financial sector development. Hence, strong institutions and high level of trade are essential ingredients for raising the performance of the financial sector, whereas weak institutional quality, as is the case in most SSA countries, is not conducive to the financial sector development. This result is, however, contrary to Aibai et al. (2019), who does not support that strong government regulation strengthens the efficiency of the allocation of capital resources in market in the ‘The Belt and Road’ countries. He nonetheless posits that trade openness is good to the development of the financial sector. Overall, the findings are consistent with Yasmina and Mohamed (2016) who demonstrate that the quality of institutions is a significant component of financial sector development in the MENA region. Hence, the role of trade in financial sector development may be hampered by poor quality of institutions (poor governance regulatory framework).

Dynamic Two-step System-GMM.

Focusing on the control variables, the estimates of GDP and FDI are positive, while only GDP is statistically significant. The results suggest that higher economic growth could enhance financial sector development, which is consistent with Le et al. (2015), Cherif and Gazdar (2015) and Bayar (2016). However, the insignificance of FDI could be attributed to the low level of foreign investors’ presence in SSA or unattractiveness of the region to foreign investment, reflecting the poor state of the SSA business environment. This may hinder the potential role of FDI in countries. On the other hand, in regions where there is no moderate inflow of FDI, the catalytic effect on domestic investment may be undermined, and thus negligible contribution to financial sector development.

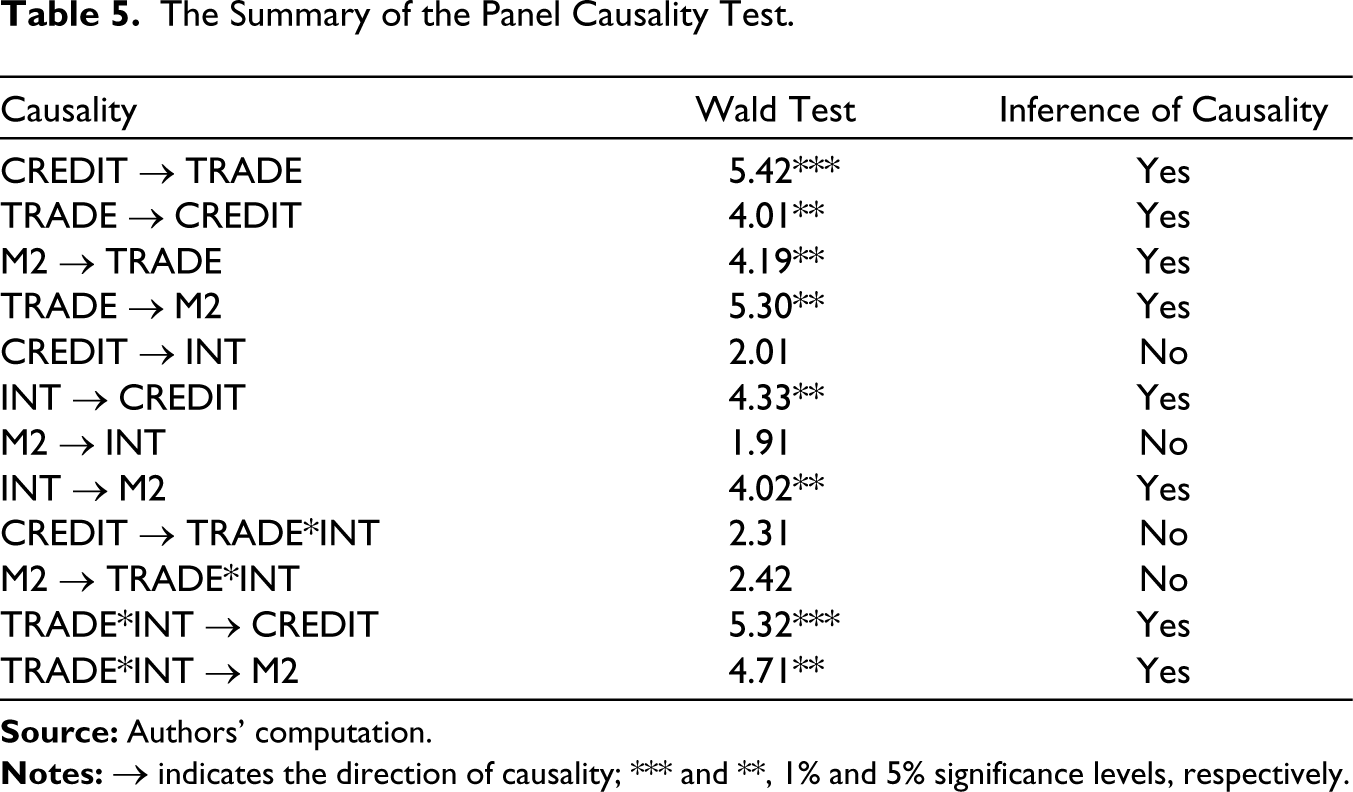

Panel Causality Test

Table 5 presents the summary of the causality test conducted based on Toda and Yamamoto (1995), and Dolado and Lütkepohl (1996). In this section, the interrelationships between trade and financial sector development through the mediating effect of regulatory quality are examined. The findings indicate that the interaction term of trade and institutional quality are significant, implying that TRADE and INT jointly cause financial sector development. However, financial sector development does not cause the interaction term of TRADE and INT. This suggests unidirectional causality running from the interaction term to financial sector development, meaning that the likelihood of trade enhancing financial sector development is conditional on having a sound regulatory framework across countries. In addition, unidirectional causality exists between regulatory quality and financial sector development indicators, which runs from the regulatory quality to financial sector development. On the other hand, bidirectional causality is found to exist between trade and the financial sector development. In economies where the governance regulatory framework is sound, people are more likely to adhere to the rules guiding financial contracts, thereby lending and borrowing become smoother. As a result, domestic financial services could be stimulated by international trade, which would further enhance the development of the financial sector. These results corroborate the findings of Bordo and Rousseau (2012), Menyah et al. (2014) and Zhang et al. (2015), who posit that the nexus between trade openness and finance is conditional on the quality of institutions.

The Summary of the Panel Causality Test.

Concluding Remarks

Given that empirical investigations suggest that financial sector development is crucial for growth enhancement and a reduction in its volatility rate in SSA, the level of financial sector development in the region is somewhat below the global benchmark. Following these concerns, coupled with the limited attention given to trade–finance nexus via the mediating effect of institutional quality, it is imperative to carry out the study. Hence, the study examines the interaction effect of trade and institutional quality on financial sector development in 20 leading economies in SSA selected based on 2018 GDP per capita ranking (top 20 richest economies by GDP per capita (PPP) released by IMF) over the period 2005–2020. As the frontier of knowledge in this direction is shifting towards providing answers as to why in most SSA countries, the financial sector is underdeveloped, the analyses majorly cover how financial development could be promoted by the openness of trade in the presence of improved regulatory frameworks.

It is found that improved financial sector development is associated with a strong regulatory framework. Thus, the quality of institutions may create a stable environment for domestic financial services to flourish with implications on the rapid expansion of business activities. As the performance of businesses improved, this development will be more conducive to the openness of trade, and hence financial sector development in the region. Indeed, the magnitude and direction of the effect of trade on financial development are sensitive to the quality of institutions in the selected SSA countries. By enhancing regulations, therefore, may potentially make it less costly for the desired level of financial sector development to be realised in SSA. However, poor quality of regulations on business activities and financial services could undermine the salutary impact of trade on financial development.

Taking into account these findings, the study offers critical insights for policy reforms, particularly in SSA. In order to create a conducive climate for the development of the financial sector, efforts should be aimed at strengthening the regulatory frameworks which are central to the improvement of the financial systems. Establishing an appropriate mechanism for the enforcement of prudential standards is crucial. In addition, building an enabling regulatory environment to improve the level of financial sector development is vital for mitigating the potential impact of the weak institutional quality risks. This remains a significant prerequisite for creating a competitive business environment, thereby enhancing the role of trade in the process of financial development.

It is necessary to note that financial sector development indicators used in the study are those that specifically related to only financial institutions. Since financial sector development comprises both financial institutions and markets, a further empirical study incorporating broader measures that possibly capture financial institutions as well as financial markets is critical. In addition, the study solely centres on the effect of quality of regulatory framework in the selected countries, given that there are other dimensions of quality of institutions such as political stability, control of corruption and government effectiveness, it implies that results illustrate only impacts of regulatory quality. Thus, further research study could consider the effect of other institutional measures. By implication, the introduction of a set of policies that could help enhance financial sector development in SSA would be greatly encouraged.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

Panel Unit Root Test.

| Variable | Im, Pesaran and Shin (W-stat) |

ADF Fisher (Choi Z-stat) |

Phillips–Perron Fisher (Choi Z-stat) |

| CREDIT Level First difference |

-1.21 -9.11*** |

-0.12 -12.01*** |

-0.16 -8.01*** |

| M2 Level First difference |

5.02 -8.23*** |

5.19 -7.90*** |

5.71 -9.51*** |

| TRADE Level First difference |

-1.13 -7.26** |

-2.01 -6.10** |

-1.15 -9.57*** |

| INT Level First difference |

-11.51*** — |

1.39 -10.34*** |

2.01 -12.91*** |

| TRADE*INT Level First difference |

-1.22 -7.26*** |

-1.32 -6.59*** |

-0.18 -7.06*** |

| GDP Level First difference |

1.42 -8.16*** |

1.53 -10.11*** |

1.16 -11.02*** |

| FDI Level First difference |

2.52 -6.11** |

3.11 -13.98*** |

1.17 -8.15*** |