Abstract

Given the unforeseen and uncertain circumstances during the pandemic, the role of government expenditure becomes extremely relevant in sustaining lives and livelihoods of the masses. This brings forth public sector deficit as a key issue of macroeconomic policy debate. This article aims at investigating the effects of an unanticipated adverse shock like COVID-19, on the real value of public debt, in a small open economy, consisting of traded and non-traded sectors, along with proposed management of such crisis with fiscal and monetary expansion. The results of policy-induced and exogenous shocks depend on the difference in the speeds of adjustments in real exchange rate, interest rate and real value of debt, and the associated multitudes of cross effects. While an unanticipated adverse shock like COVID-19 causes contraction of both traded and non-traded sectors and reduces consumption expenditure, investment expenditure and level of employment and real value of aggregate income in the short run, fiscal expansion causes higher real value of debt and lower real exchange rate.

Introduction

In the current pandemic situation, where economies, developed and developing as well, are at crossroads, the role of the government becomes extremely relevant. Associated with the enhanced importance of designing appropriate macroeconomic policy and its coordinated implementation are the key issues pertaining to fiscal policies, which the governments are undertaking to sustain the livelihoods of the poor by doling out subsidies and grants along with the lump sum expenditure in the development of infrastructure, including the health sector. Given the unforeseen and uncertain circumstances, the burden on the treasuries cannot be ignored. This once again brings forth public sector deficits and mounting public debt as key issues at the heart of macroeconomic policy debate in an open economy framework. This article addresses the legitimacy of strict adherence to fiscal discipline, in a situation of crisis, in which symptoms of recovery are not in sight. Given the importance of fiscal prudence and management in policymaking, this article is an attempt to provide a theoretical understanding of interaction between debt dynamics 1 and real exchange rate dynamics in the presence of endogenous risk premium and partial wage indexation in an open economy structure.

There have been numerous questions with regard to fiscal solvency, adequate monetary policy mechanisms, inflationary tendencies or global and local macroeconomic shocks, which account for a rise in debt-to-GDP ratio. While researchers like Masson and Mussa (1995) have pointed out population, inflation and productivity growth as the main reasons behind worsening fiscal balance sheets (see Blanchard & Perotti, 2002; Christiano et al., 1999; Fatas & Mihov 2002; Friedman, 2006; Hasko, 2007; Marcellino, 2006; Melitz, 1995; Mountford & Uhlig, 2002), others like Burnside (2005) showed that the change in the debt-to-GDP ratio is the sum of five components: (a) interest payments, (b) the primary balance, (c) seigniorage, (d) the inflation effect and (e) the growth effect.

The pertinent question is how to sustain such fiscal deficit—by debt financing or to put additional taxes, 2 which in turn may depress demand. This should not be out of recording that debt in itself might not be a major macroeconomic problem. However, the issue at stake is utilisation and management of debt. 3 The situation of Argentina and Mexico are excellent case studies in this regard. 4 This once again proved that a prudent mix of policies along with the specific characteristics of the country and its leadership is essential in the efficient management of debt.

In the Indian context, the Fiscal Responsibility and Budget Management Act (FRBM Act), 2003, was introduced in line with an extant of literature, which dwells on aspects of fiscal sustainability that refer to the government’s ability to maintain its current policies and satisfy its lifetime budget constraint 5 without defaulting on its debt obligations. This has led to repeated analysis and scrutiny of the long-term profile of fiscal deficit and debt, relative to GDP in India (See Rangarajan & Srivastava, 2005; Singh & Srinivasan, 2004).

Debt dynamics cannot be isolated from dimensions of openness in general, and exchange rate in particular. Asonuma (2016) shows that there might be a bidirectional causality between exchange rate dynamics and probability of default, which depends on the sequence of events. Escude (2002) used multiple theoretical models to demonstrate the co-movement of exchange rate and public debt under convertibility along with wage or price rigidity in presence of adverse macroeconomic shocks.

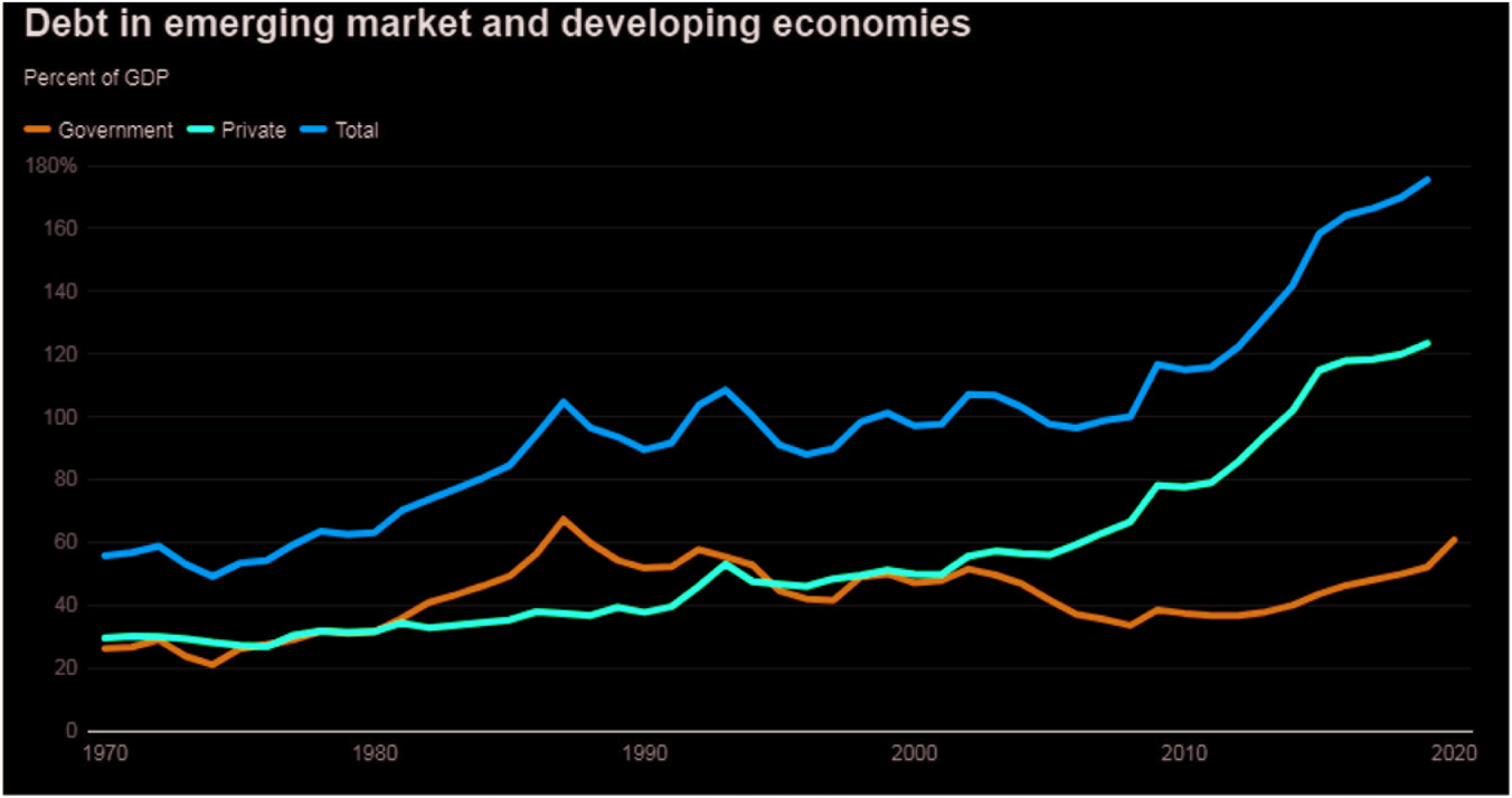

Considering some stylised facts pertaining to public debt across the globe, we observe that the COVID-19 pandemic has heightened the overall debt, particularly for the emerging market and developing economies, as evident from the following figure.

Under such circumstances, the unprecedented fiscal stimulus to boost overall economy has caused a surge in debt build-up, which may eventually become a liability to the government. Given that majority of the economies were already under substantial burden of public debt, it remains to be seen how such an unprecedented situation can be managed. Moreover, along with trade barriers being imposed to contain the disease, there have been substantial capital withdrawals since the outbreak.

The existing literature discusses the implications of public debt in an aggregative macroeconomic framework. 6 More generally, Blanchard (1984) developed a simple theoretical model to examine the steady-state interest rate, or the dynamic effects of government deficit finance, which crucially depend on the horizon of economic agents. This article makes an attempt to clarify the literature by introducing the non-traded sector. In doing so, we are choosing a dependent economy 7 framework. In particular, it clarifies the respective roles of debt dynamics and real exchange rate dynamics in determining the level of employment, sectoral composition of output, wage rate, and real exchange rate and real value of debt, and risk premium in response to policy-induced shocks and exogenous unanticipated shock. The model in this article is based on the works of Dornbusch (1982), Buiter (1985), Escude (2002) and Sikdar (2014). What is missing in the literature is an analytical implication for lives and livelihoods post the pandemic. In its orientation, our model is closer to the works of Escude (2002), who developed a simple deterministic dynamic model, stressing the importance of downward inflexibility of prices and nominal wages. The theoretical model is an extension of Buiter’s (1985) study, which explores the factors determining the change in real value of public debt over time. While the concept of endogenous risk premium was introduced by Dornbusch (1982), 8 Sikdar (2014) considered its macroeconomic implications in an effective demand model. Borrowing from Sikdar (2014), we address the role of risk premium in determining the interface between debt dynamics and real exchange rate dynamics. In our model, risk premium depends on the net exports and real value of public debt.

The remainder of the article is organised as follows: the second section presents the model. The effects of fiscal policy and an unanticipated adverse shock on the premises of the model are examined in the third section. The fourth section summarises the main results and offers some concluding remarks.

Model

We consider a small open economy, consisting of the traded and non-traded sectors. Labour (L) and capital 9 (K) are used in the production of both traded and non-traded goods. Capital is a composite good produced by combining domestic and imported components in fixed proportions. 10 We assume that only the non-traded sector produces domestic capital goods. 11 Price of non-traded goods is flexible. Money wage rate is partially indexed to the consumer price index, which depends on both the price of non-traded goods and imported goods. This wage indexation causes involuntary unemployment. The real exchange rate dynamics is driven by interest rate differential. The asset structure of the model consists of money, domestic bonds and foreign bonds. The risk premium is endogenous, which drives the dynamics of the system. The dynamics of the model is driven by real exchange rate and public debt.

Supply Function of Traded and Non-traded Sectors

Production function of the traded good is represented by the following equation:

Here, A1 represents technological parameter. A technological progress raises marginal product of labour. Hence, production of traded goods increases. On the other hand, a technological regress reduces marginal product of labour. Consequently, production of traded goods falls. Now, the technological parameter is negatively related to unanticipated adverse shock like COVID-19, that is,

Let us consider that the firms’ revenue per unit of exportable is e.

13

Therefore, the profit of the traded sector is as follows:

The profit maximisation behaviour of the firms gives us demand for labour and supply function of the traded sector:

The production function of the non-traded sector takes the following form:

Here, A2 represents technological parameter. A technological progress raises marginal product of labour. Hence, production of non-traded goods increases. On the other hand, a technological regress reduces marginal product of labour. Consequently, production of non-traded goods falls. Now, the technological parameter is negatively related to unanticipated adverse shock like COVID-19, that is,

Firms are selling non-traded goods at price PN. Hence, profit of the non-traded sector is:

The profit maximising exercise of the firms in the non-traded sector determines demand for labour and supply of non-traded goods, represented by the following equations:

Labour Market

Total demand for labour consists of level of employment in both the traded and non-traded sectors and is given by the following:

Using Equations (3), (8) and (10), we get aggregate employment, given by the following:

The effects of θ, w and PN and technological progress are self-explanatory.

Total labour force is fixed at

The wage rate is given by the following equation:

where

An increase in consumer price index raises the wage rate less than proportionately, and hence, real wage in terms of consumer price index falls.

Now, the consumer price index can be expressed as follows:

where θ is the real exchange rate.

Now, the wage rate can be written as follows:

Consumption

Consumption function is given by

τ is the tax rate and 0 < τ < 1.

Here, consumption expenditure is positively related to real value of dispos-able income [YT (1 – τ)]. However, consumption expenditure is negatively related to uncertainty (σ1). Unanticipated adverse shock (∈) like COVID-19 increases uncertainty from expected job loss, illness, etc., that is,

Consumers spend β proportion of their total consumption expenditure on traded goods and (1 – β) proportion on non-traded goods. 15

Hence, consumption for traded goods is as follows:

And consumption for non-traded goods is as follows:

Now, the real aggregate income is as follows:

Hence, Y = θ1–βY TR + θ–βY NT .

Investment

The investment expenditure is negatively related to interest rate as well as uncertainty (σ2) in the business prospect. An unanticipated adverse shock like COVID-19 raises this uncertainty, that is,

The economy spends γ fraction of the total investment expenditure on non-traded goods and (1 – γ) fraction on traded goods.

Market for Non-traded Goods

The demand for non-traded goods consists of consumption expenditure, investment expenditure and the real value of government expenditure:

Supply of non-traded goods is represented by the following equation:

Now the equilibrium condition in the market for non-traded goods is given by the following:

From Equation (19), we can determine the equilibrium price of non-traded good (PN), and it can be expressed as follows:

Let us consider partial effect of each variable on PN. An increase in θ raises consumer price index, leading to generate a negative effect on the consumption expenditure. On the other hand, the increase in θ leads to expansion of the traded sector (YTR), which generates a positive effect on the consumption. Moreover, the higher consumer price index leads to higher interest rate, which entails decrease in investment expenditure as well. Therefore, the demand for non-traded goods may increase or decrease. Moreover, the increase in θ causes higher wage rate as consumer price index rises. This may lead to decrease in the real wage in terms of the non-traded goods, and hence, production of the non-traded good falls. Therefore, the increase in θ generates an ambiguous effect on the PN. Consequently, we get

A technological progress (regress) leads to expansion (contraction) of the non-traded sector, and hence, we get

The equilibrium value of non-traded good is as follows:

Real Aggregate Income

The real aggregate income can be expressed as follows:

Let us consider the partial effect of each variable on Y. An increase in θ may lead to contraction of the non-traded sector. On the other hand, the increase in θ leads to expansion of the traded sector (YTR). Hence, the effect on the real value of aggregate income is ambiguous, and we get

Money Market

Equation (33) represents the money market equilibrium. The left-hand side of the equation shows the supply of real money balances

From the money market equilibrium we get equilibrium interest rate as follows:

Let us consider the partial effect of each variable on r. An increase in real value of aggregate income (Y) raises demand for money, and hence, interest rate rises, that is,

Net Exports

The traded sector sells its entire output in the world market at a given price. Since there is no domestic consumption of traded good, the entire production is the volume of exports. Value of exports can be represented as the value of traded goods expressed in terms of foreign currency

Hence, net exports can be expressed as follows:

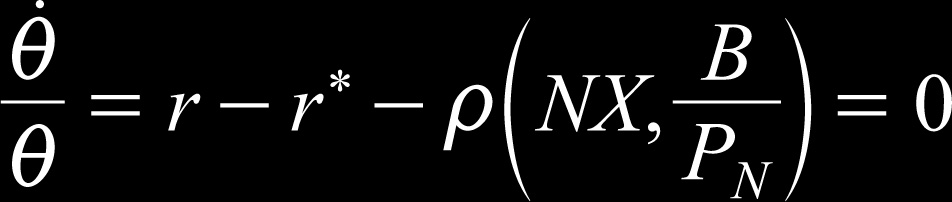

Interest Rate Parity Condition with Endogenous Risk Premium

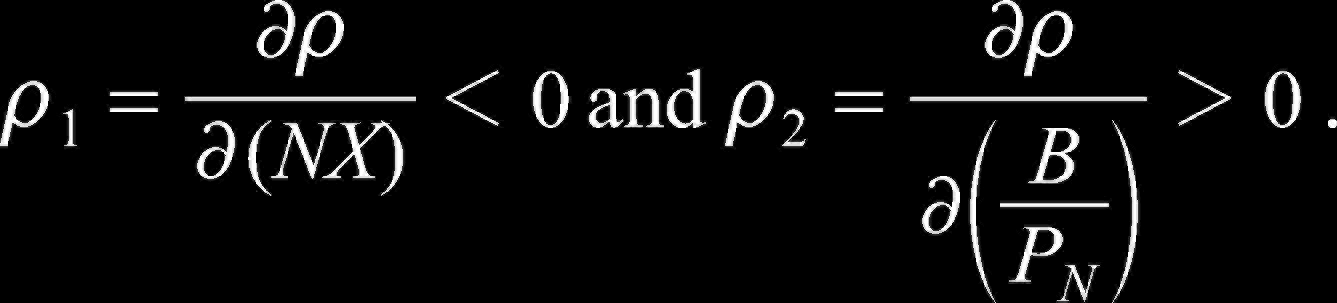

In this article, domestic and foreign currency bonds are considered to be imperfect substitutes. Hence, equilibrium in the foreign market requires that the domestic interest rate is equal to the sum of foreign interest rate, expected change in exchange rate and a risk premium, ρ, that reflects the difference between the riskiness of domestic and foreign bonds.

Here, we note that weak macroeconomic fundamentals, particularly trade surplus or deficit, and public debt have major bearing on credit worthiness of a country, and accordingly risk premium depends on these macroeconomic fundamentals (Dornbusch, 1982):

Dynamics

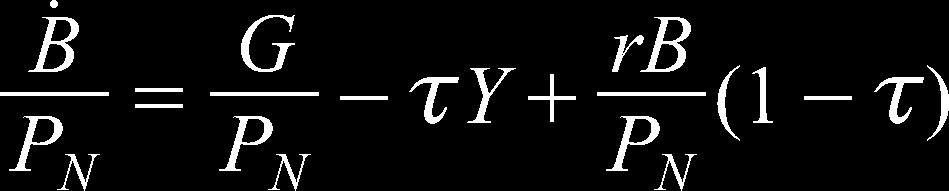

The debt dynamics is given by the following equation:

where

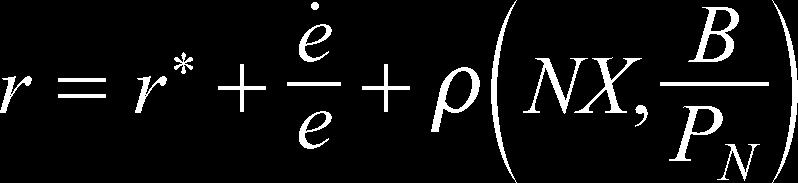

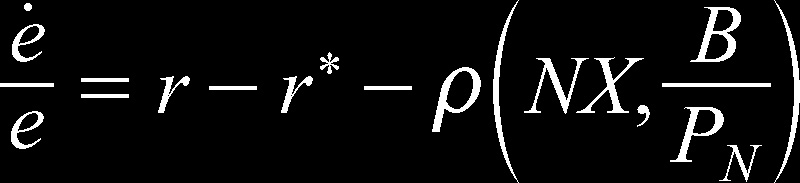

From the interest rate parity condition, we get the exchange rate dynamics as follows:

Equation (45) shows that an over-time adjustment of exchange rate depends on domestic interest rate, foreign rate of interest and endogenous risk premium.

Now, the real exchange rate dynamics is as follows:

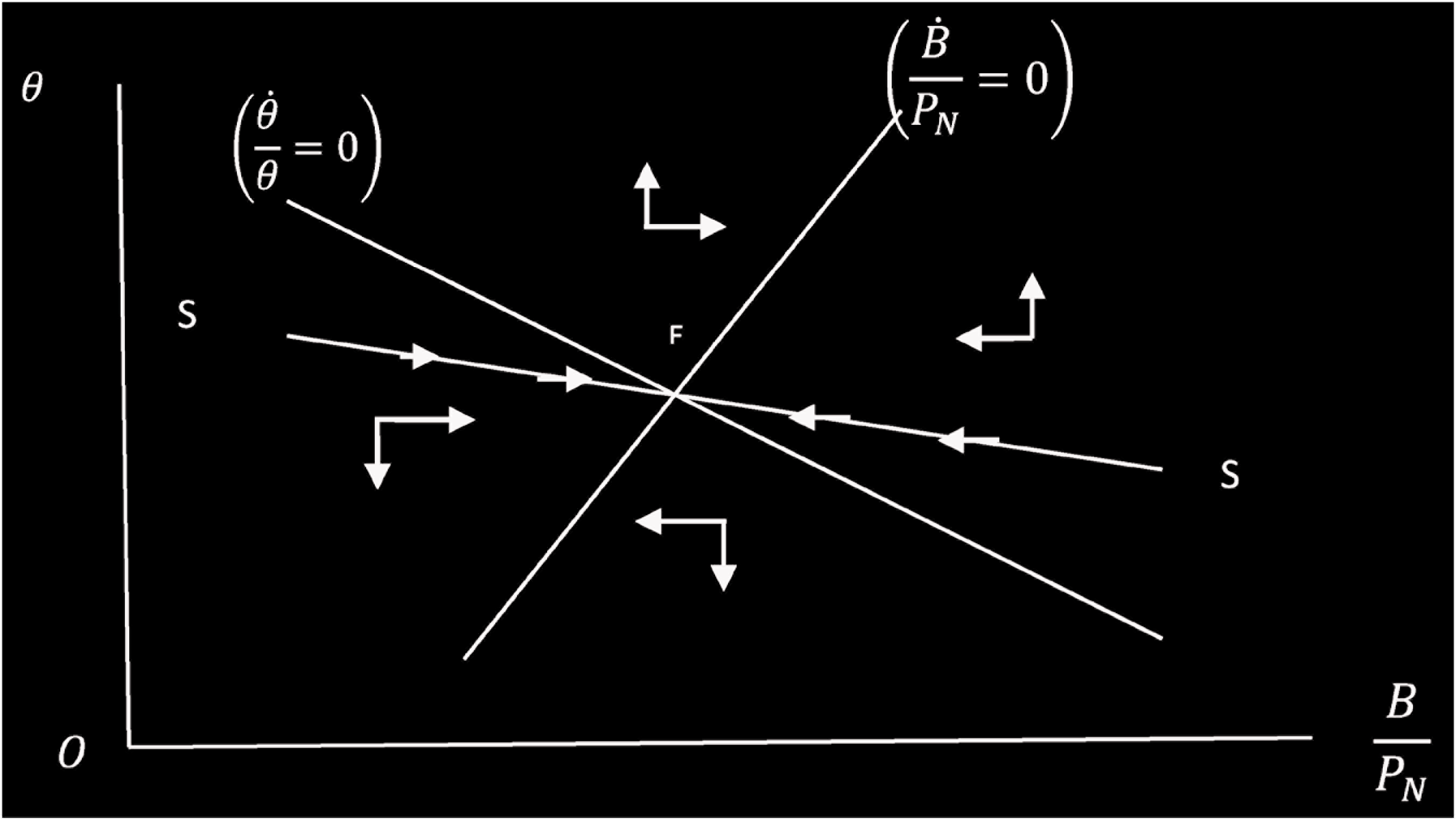

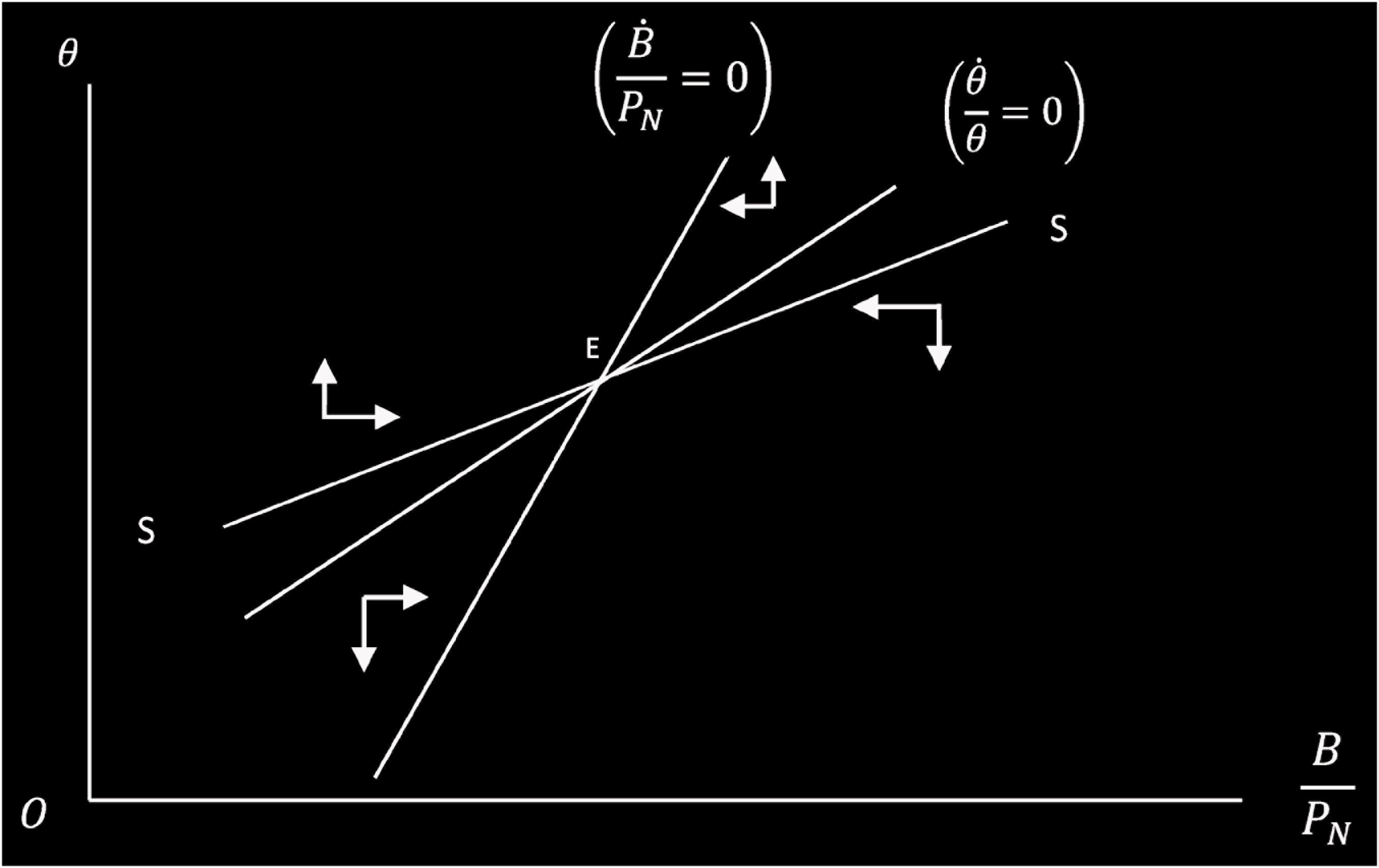

Steady State

The steady-state real value of the debt is obtained from the following condition:

From Equation (47), we get a relationship between real values of debt

Hence, we get a positive relation between real value of public debt

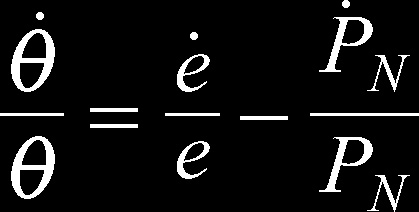

The real exchange rate (θ) is at a steady state if the following condition holds:

An increase in θ raises net exports and generates an ambiguous effect on the price of non-traded goods and real value of debt. Therefore, ρ changes ambiguously in response to increase in θ. Moreover, the increase in θ raises consumer price index, which, in turn, causes higher domestic interest rate. Here, we consider that increase in interest rate dominates the ambiguous change in ρ such that we get

An increase in

If the increase in

In Figures 2 or 3, the stationary equilibrium E represents the saddle point stability, so that the only convergent path is SS. Saddle path is negatively sloped in Figure 2. In contrast, Figure 3 shows positively sloped saddle path. Now stability of the equilibrium requires that the

Some Applications

We will carry out few comparative static exercises, pertaining to the pandemic crisis and fiscal policy.

An Unanticipated Adverse Shock (COVID-19)

An unanticipated adverse shock like COVID-19 generates a devastating effect on the economy. In recent time, the world economy faces this shock, which leads to almost the shutdown of the system through lockdown. In our model, we are incorporating this shock, which leads to technological regress in both traded and non-traded sectors. This causes a fall in the production of both traded and non-traded goods and, hence, level of employment as well. Moreover, the unanticipated adverse shock raises uncertainty due to expected job loss and illness. Hence, consumption expenditure for both traded and non-traded goods falls. In addition, investment expenditure on both traded and non-traded goods decreases due to an uncertain business prospect. The real aggregate income decreases as production of both traded and non-traded goods falls. Moreover, there is a decrease in the money wage rate in response to this adverse shock. However, the effect on the price of non-traded goods is ambiguous. It depends on whether a fall in supply dominates a fall in demand for the non-traded goods. Hence, the supply of real money balances changes ambiguously. However, the decrease in real aggregate income reduces demand for money. Therefore, interest rate may fall. Hence, interest payment on real value of debt changes ambiguously. The real government expenditure in terms of non-traded goods also changes ambiguously. However, the real tax revenue decreases as real aggregate income falls. As a result, the effect on

This unanticipated adverse shock generates an ambiguous effect on the net exports as traded sector contracts, as well as both consumption expenditure and investment expenditure on the traded goods fall. Moreover, real value of debt changes ambiguously. Hence, the effect on risk premium is ambiguous. In addition, interest rate may decrease in response to lower demand for money. So this unanticipated shock has an ambiguous effect on

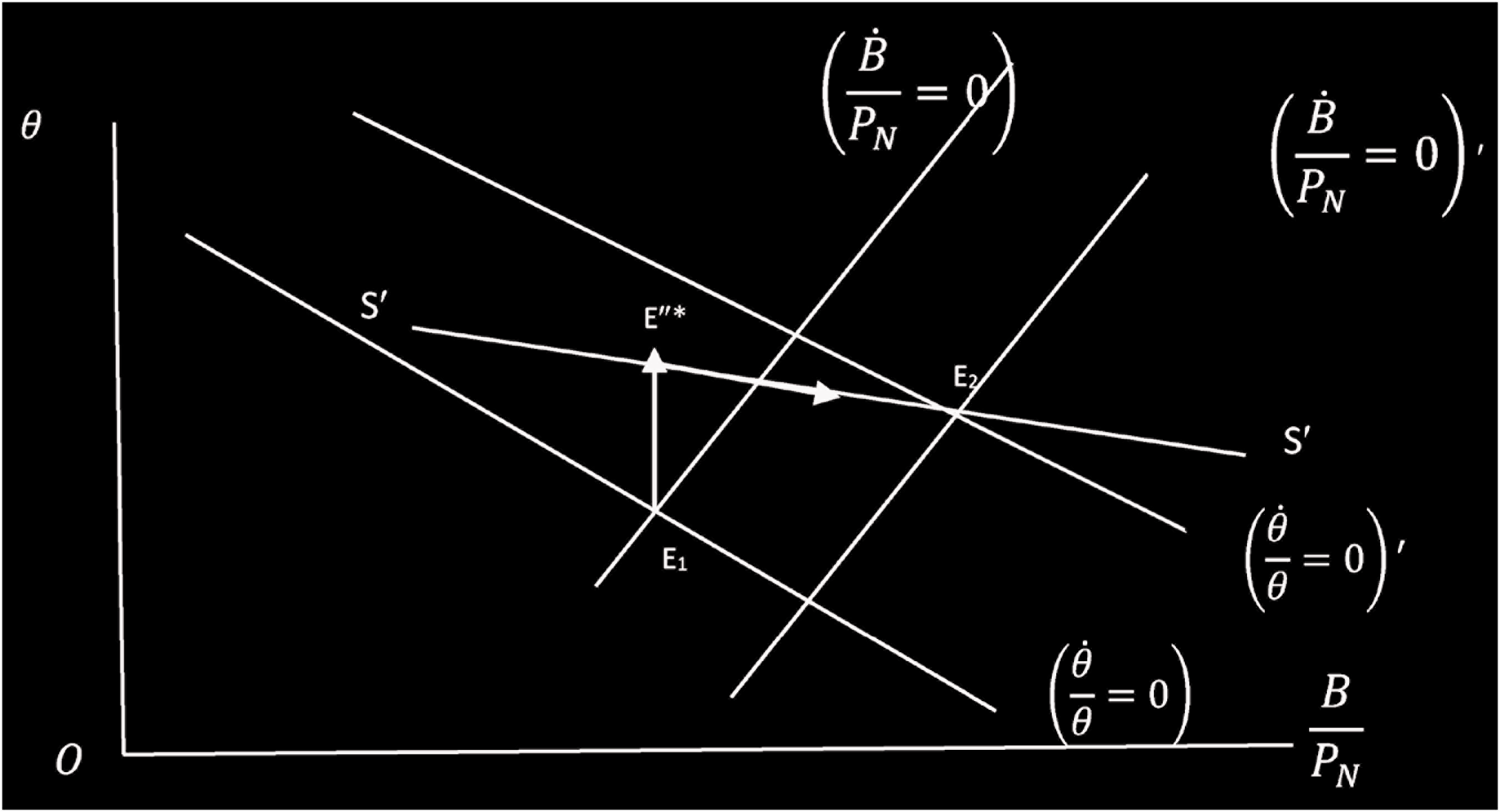

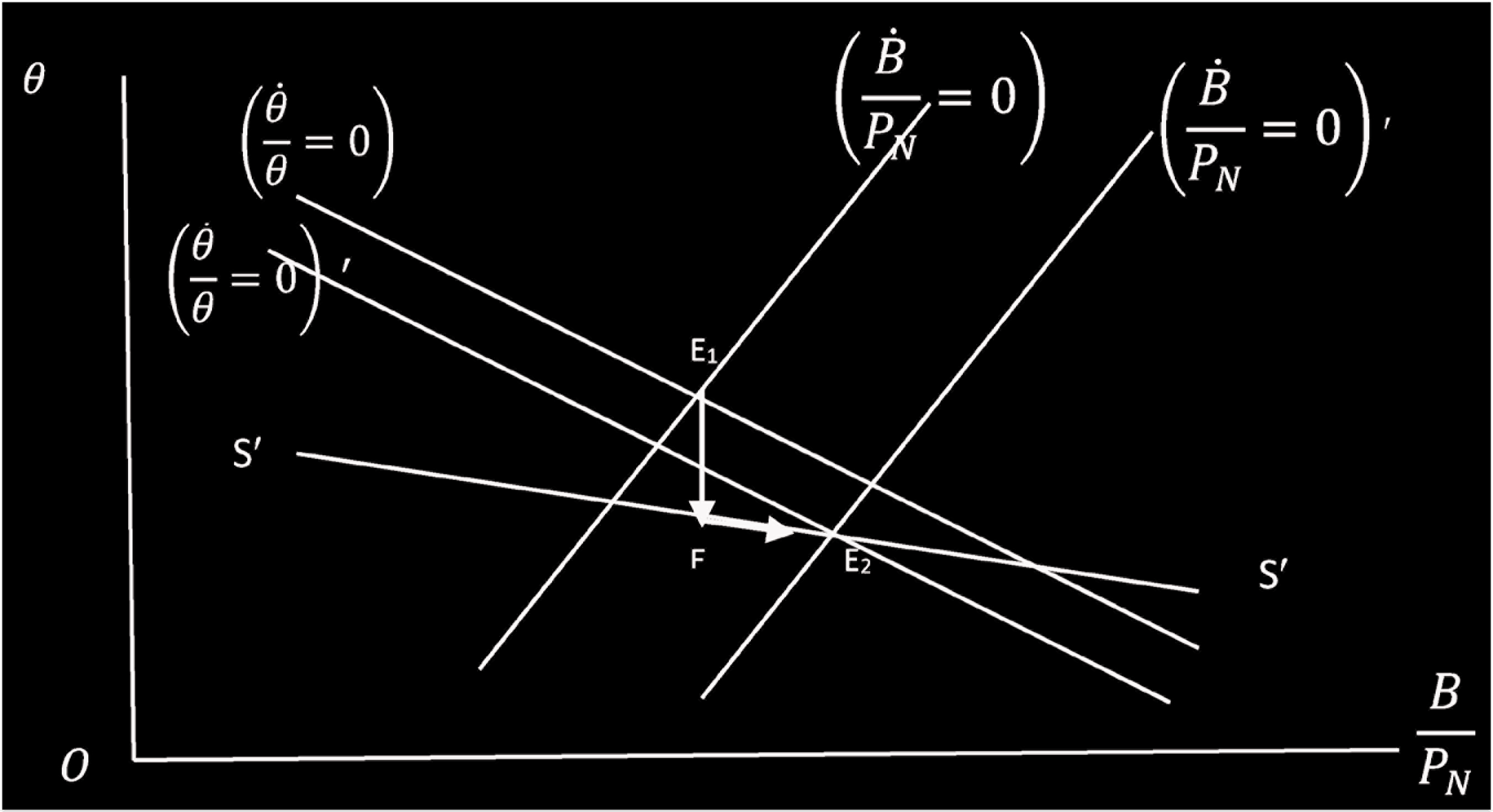

In Figure 4, both real exchange rate and real value of debt increase, corresponding to the new steady state as represented by the point E2. On the other hand, Figure 5 shows that both real value of debt and real exchange rate decrease at the new steady state point E2. Therefore, the effect of the unanticipated adverse shock, for instance, COVID-19, on the steady-state real value of debt and real exchange rate is ambiguous. Hence, production of both traded and non-traded goods changes ambiguously, corresponding to the new steady state. Consequently, level of employment also changes ambiguously. The price of non-traded goods may increase or decrease. Hence, the effect on the money wage rate as well as on the domestic interest rate is also ambiguous at the new steady state. Risk premium may increase or decrease at the new equilibrium as both net exports and real value of debt change ambiguously. There is ambiguous change in real value of aggregate income, consumption expenditure and investment expenditure at the new steady state.

Let us consider the dynamic adjustment process. According to Figure 4, the unanticipated adverse shock leads to immediate increase in the real exchange rate such that the economy immediately moves from the initial equilibrium point E1 to the point E' on the new saddle path S'S' at the given real value of debt. Over time the economy gradually moves along the saddle path S'S' to the new equilibrium point E2, which corresponds to the higher values of both real exchange rate and real value of debt. In this case, an over-time increase in the real value of debt offsets the initial increase in the real exchange rate to some extent, and hence, the real exchange rate initially overshoots its steady-state value, as represented by the point E', and decreases thereafter. In Figure 5, the unanticipated adverse shock leads to an immediate decrease in the real exchange rate such that the economy immediately moves from the initial equilibrium point E1 to the point E' on the new saddle path S'S' at the given real value of debt. In this case, an over-time decrease in the real value of debt reinforces the initial decrease in real exchange rate, and hence, the real exchange rate initially undershoots its steady-state value, as represented by the point E' in Figure 5.

Expansionary Fiscal Policy

In response to the unanticipated adverse shock like COVID-19, the government emphasises fiscal expansion to stimulate the economy. Let us now discuss the effects of increase in government expenditure in our model. An increase in government expenditure (G) raises demand for non-traded goods, which generates excess demand in the market for non-traded goods. Therefore, price of non-traded goods rises to restore the equilibrium in the market for non-traded goods. As PN rises, real wage in terms of the non-traded goods falls, which, in turn, causes expansion of the non-traded sector. However, the traded sector contracts as real wage rate in terms of traded goods rises in response to higher PN. Hence, the effect on real value of aggregate income is ambiguous. The increase in PN causes higher interest rate as well. The increase in government expenditure initially generates a positive effect on

On the other hand, the fiscal expansion causes higher interest rate, which generates a positive effect on

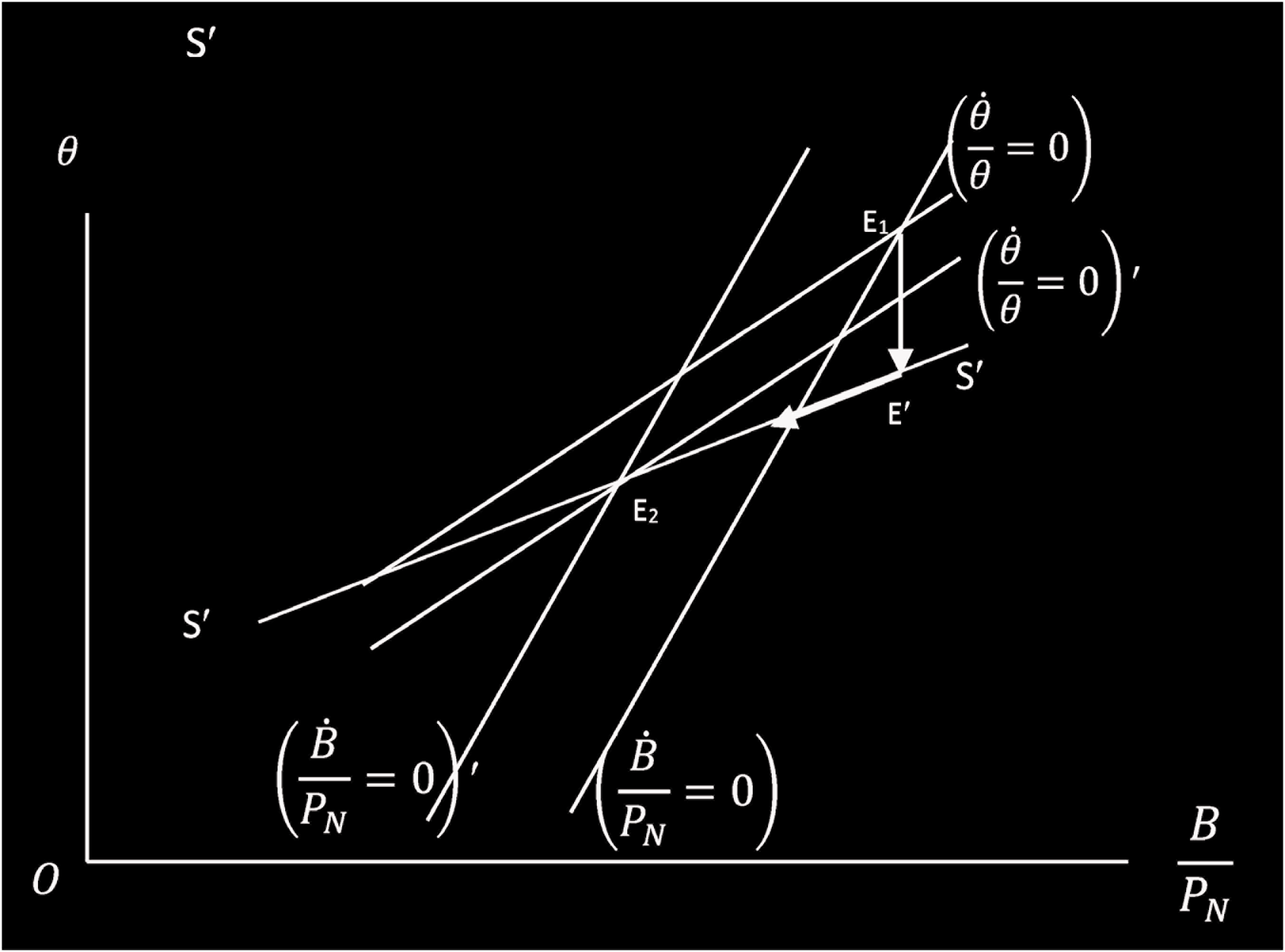

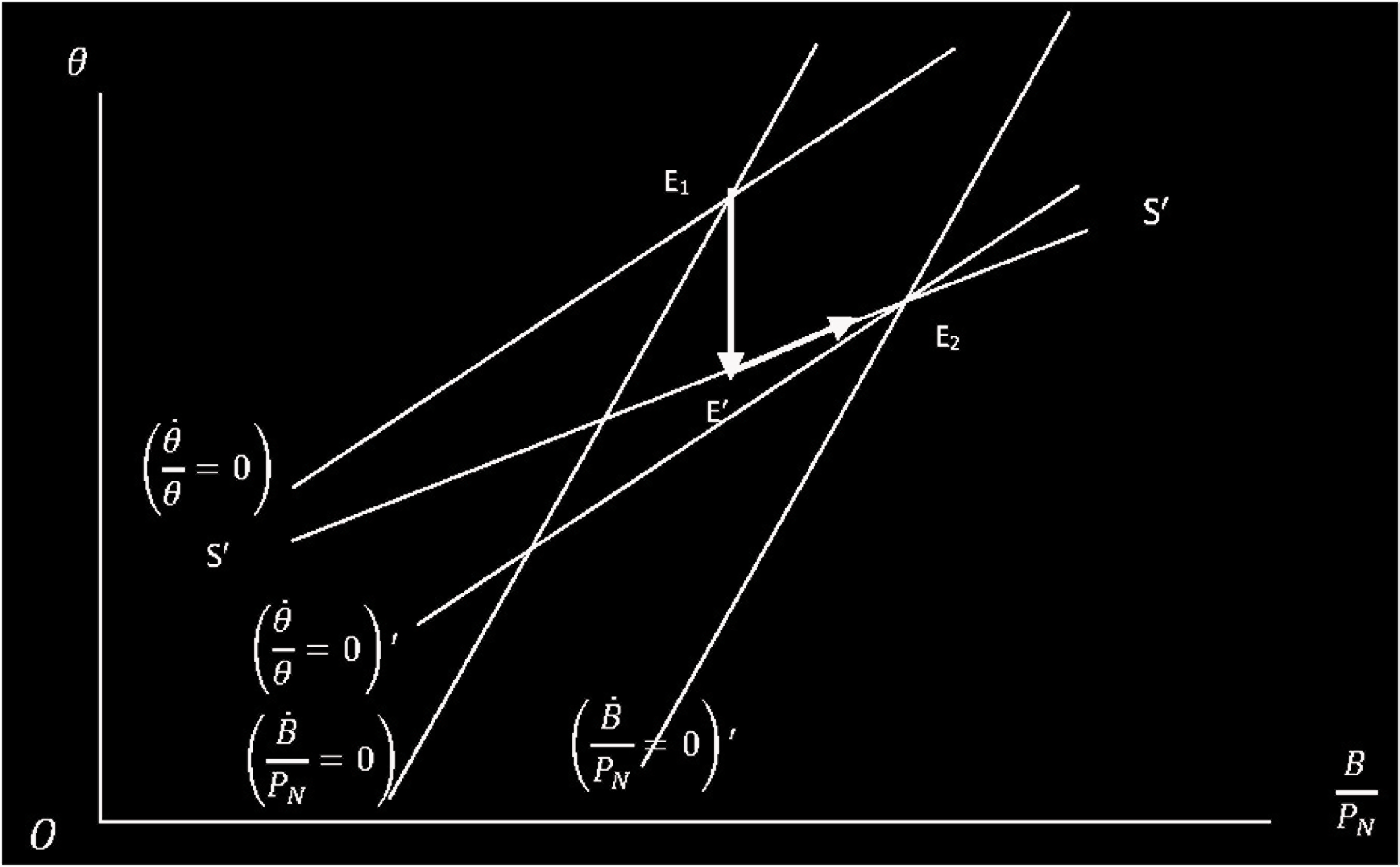

The fiscal expansion causes higher real value of debt and lower real exchange rate at the new steady state as represented by the point E2 in Figures 6 and 7. The increase in real value of debt leads to a further increase in demand for the non-traded goods, which causes further expansion of the non-traded sector at the new steady state. Hence, the level of employment in the non-traded sector rises. However, the decrease in real exchange rate causes further contraction of the traded sector, leading to a decrease in the level of employment in the traded sector. Consequently, the fiscal expansion generates an ambiguous effect on the level of employment at the aggregate level.

Let us explain the dynamic adjustment process. The fiscal expansion leads to an immediate decrease in the real exchange rate such that the economy immediately moves from the initial equilibrium point E1 to the point E' on the new saddle path S'S' at the given real value of debt, as represented by the Figures 6 and 7. Over time, the economy gradually moves along the saddle path S'S' to the new equilibrium point E2, which corresponds to the lower values of real exchange rate and higher real value of debt. In Figure 6, an over-time increase in real value of debt reinforces the initial decrease in real exchange rate, and hence, the real exchange rate initially undershoots its steady-state value, as represented by the point E', and decreases thereafter. According to Figure 7, an over-time increase in the real value of debt offsets the initial decrease in real exchange rate to some extent, and hence, the real exchange rate initially overshoots its steady-state value, as represented by the point E' in Figure 7.

Conclusion

The current pandemic crisis has been an eye-opener for all of us, including researchers and scientists in the domain of medical science and policymakers. The absence of appropriate vaccine in the initial phase and subsequent non-availability of vaccines due to supply shortage in developing countries led to the lockdown as an immediate policy response to this crisis. This, in turn, initiated the natural conflict between lives and livelihood. Hence, any facile conclusion is unwarranted. There is simply no gain saying the fact that COVID-19 and associated policy measures have myriad dimensions in the socio-economic sphere. We have tried to make a simple analytical construction to reflect on certain aspects of the crisis. In doing so, we have constructed a dependent economy model, which may apply to a large class of developing countries.

Our first attempt is to examine effects of COVID-19, which has led to phenomenal increase in government expenditure and, in the Indian context, has raised doubts about the strict adherence to the Fiscal Responsibility and Budget Management Act, 2003. What the article shows is that an unanticipated adverse shock like COVID-19 causes contraction of both traded and non-traded sectors and reduces consumption expenditure, investment expenditure and the level of employment and real value of aggregate income in the short run. Naturally, the need arises to explain fiscal expansion associated with the pandemic as a policy response. The model shows that fiscal expansion causes higher real value of debt and lower real exchange rate at the new steady state. The increase in real value of debt causes an expansion of the non-traded sector. The decrease in real exchange rate causes a contraction of the traded sector.

There exists future scope of research, which is a standard practice in the professional domain. Naturally, one may raise the question of adequate supply of funds to manage such crisis. As far as the Indian economy is concerned, one may explore consequences of certain recent initiatives in the post-COVID-19 scenario. Some of the measures, which are worth mentioning inter alia, are special economic and comprehensive packages under Atmanirbhar Bharat, which include cash transfer relief measure, employment provision measures, deregulation of agriculture, credit guarantee and equity infusion–based relief measures for micro, small and medium enterprises (MSMEs) among others.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

The slope of

Provided,

and

Provided,

Here,

Now, slope of the

Next, we consider

Provided,

Now slope of the

Now, the Jacobian or matrix of first partial derivatives for (66), (![]() ) is

) is

If a21 > 0, then det J is negative. Since, det J is negative, one of the characteristic roots must be negative. Hence, the system has saddle point stability.

If a21 < 0, then det J is ambiguous. However, saddle point stability requires negative det J which leads to ![]() .

.

where

Let A1 = 0, therefore we get the following:

Now, the equation of the Saddle Path is

Slope of the Saddle Path

Slope of the

Hence, Saddle Path is flatter than the

A4.1. An Unanticipated Adverse Shock like COVID-19.

The steady-state effect on the real value of debt is

The steady-state effect on the real exchange rate is

where

The steady-state effect on the real value of debt is

The steady-state effect on the real exchange rate is

where

![]() .

.