Abstract

We study the trends and fluctuations in greenfield foreign direct investment (GFDI) during the first wave of the COVID-19 pandemic crisis on a global scale. We analyse the data of a data set of GFDI provided by fDi Markets (Financial Times) to understand the contraction of GFDI during the first three quarters of the year 2020, taking into account the sector of the investment and the host and home country. We analyse both the long-run trends and the quarter-over-quarter changes in GFDI to capture its fluctuations before and during the first wave of the COVID-19 crisis and the 2008 global financial crisis. Our findings cast light on which countries’ and industries’ GFDIs were most affected by the pandemic crisis and draw a comparison to the global financial crisis. To our surprise, many services industries have shown unexpected resilience of GFDI due to the flexibility for remote work. On the contrary, GFDI in the manufacturing industries, as well as the extractives and the utility industries, has shown a dramatic decline during the pandemic. These contractions raise questions of stability and resilience of the global supply chains these industries are a part of.

Keywords

Introduction

Economic historians distinguish two ‘waves of globalization’ in the past two centuries: the late nineteenth century to the First World War and a resurgence in global economic integration after the Second World War, which continues to the present. The waves of globalisation are characterised by surges in international trade, foreign investment, as well as a certain degree of business cycle synchronisation. The factors attributed to the rise of globalisation include international political stability, infrastructure development and falling costs of transport and communication. However, this greater interconnectedness of the world also means greater interdependence, which can lead to disruptions in times of crisis. A recent disruption in international trade and investment preceding the COVID-19 crisis was the 2008 global financial crisis. From the current perspective, the global financial crisis may turn out to be a short-lived disruption in comparison to the slowdown in international (and domestic) activity caused by the COVID-19 crisis. Today, the world is even more interconnected through global production value chains, international trade in parts and components, travel and tourism, as well as Internet and telecommunication technologies, which are the basis of new services industries.

The beginning of the COVID-19 pandemic crisis caused a dramatic economic shock that rippled across all economic sectors and geographical regions throughout the year 2020. At the very beginning of the crisis, the global foreign direct investment (FDI) flows were forecast to suffer a drastic decline, up to 40% in 2020 from their 2019 level of US$1.54 trillion (UNCTAD, 2020). Such a decline, the World Investment Report (WIR) (2020) argues, would bring FDI below the US$1 trillion mark for the first time since 2005 and will bring FDI further down in 2021 and 2022 (UNCTAD, 2020). Both GFDI and cross-border mergers and acquisitions (M&As) dropped by more than 50% year over year in the starting months of 2020 (UNCTAD, 2020). Further, based on FDI information sourced from United Nations Conference on Trade and Development (UNCTAD) Global Investment Trends Monitor, the first 6 months of the pandemic witnessed a 37% fall in global greenfield project announcements and a 15% fall in cross-border M&As. Further, the FDI index of the fDI markets database stood at 703 points in October 2020, 34.4% lower compared to October 2019 capturing the impact of the COVID-19 outbreak on the sentiments of foreign investors. In addition to the impact of COVID-19 on FDI, the pandemic also affected other aspects of trade and the global economy. The imposed lock-downs and social distancing measures affected the tourism and travel industry adversely. There was also a worldwide production shock. The policy response to the pandemic varied widely across countries. With massive supply chain disruptions, many economies closed their borders to exports as an unprecedented measure of national supplies preservation (UNCTAD, 2020).

The purpose of our analysis is to identify the trends in greenfield foreign direct investment (GFDI), taking into account the sector of the investment, the recipient country, as well as the level of the source country, using the dataset fDi Markets source from Financial Times. Our goal is to evaluate the behaviour of GFDI during the first wave of the pandemic (the first three quarters of 2020). Rather than being an empirical study, this study attempts to evaluate the trends and fluctuations of GFDI prior to and during the pandemic’s first wave and to make a comparison with the 2008 global financial crisis, which also affected the entire world adversely. We attempt to cast light on which countries’ and industries’ GFDIs were most affected by the pandemic crisis and draw a comparison to the global financial crisis. Our results show that many services industries have shown unexpected resilience of their GFDI. It is proposed that this might be due to their flexibility for remote work. On the contrary, GFDI in the manufacturing industries and the extractives and the utility industries has shown a dramatic decline during the pandemic. Since these industries are a part of global value chains (GVCs), the significant contraction of GFDI raises questions regarding the stability and resilience of these GVCs. The global vulnerabilities of GVCs and international trade, as well as the heavy dependence of countries on their GVC participation, have ultimately resonated in a contraction of GFDI as well.

The rest of the article is organised as follows: in the second section, we review the literature related to the COVID-19 economic crisis; in the third section, we examine the long-run trends of GFDI worldwide; in the fourth section, we identify the fluctuations in GFDI by main sectors and make a comparison between the behaviour of GFDI during the first wave of the pandemic and during the 2008 global financial crisis; the fifth section concludes the study.

The COVID-19 Pandemic as an Economic Shock

The literature on responsiveness of FDI to business cycles is fairly recent (Araujo et al., 2017; Broner et al., 2013; Doytch, 2015, 2021a; Lane, 2015). Araujo et al. (2017) demonstrate that capital inflows to low-income developing countries are procyclical but less than their developed countries’ counterparts. Broner et al. (2013) uncover a similar procyclicality finding regarding aggregate gross capital inflows and outflows. Doytch (2015, 2021a) uncovers counter-cyclicality of FDI flowing into services industries, and Lane (2015) emphasises the country’s characteristics in explaining cross-country variation in international net FDI flow cyclicality. The responsiveness of FDI to shocks or prolonged periods of recession, such as the current pandemic crisis, has not been well examined with the exception of a few studies that look at natural disaster shocks (Doytch, 2020) and economic accelerations and decelerations (Doytch, 2021b). Arguably, the COVID-19 pandemic crisis is shaping up as one of the most prolonged and severe global economic crises in recent history (Canh & Thanh, 2020).

The UNCTAD-Investment Trend Monitor Report (March 2020) highlights that the adverse effect of COVID-19 would channel through market-, resource- and efficiency-seeking FDIs. Moreover, the most affected economies and sectors are the ones with heavy involvement in GVCs. China and several other Asian economies were the first to witness the negative effects; for instance, in February of 2020, Toyota reported a 70% fall in sales in China (UNCTAD-Investment Trend Monitor Report, 2020). Besides these three channels, there was an indirect channel through which COVID-19 had further deterred FDIs. Given the demand shock, the earnings by foreign-affiliated firms were limited, and as a result, the level of capital generated through sales was reduced, which subsequently affected reinvestment. According to UNCTAD (2020), reinvested earning makes almost 40% of FDI inflows in developing countries and 61% in developed economies. The above-mentioned withdrawal statistics highlight the severity of the pandemic on global investment.

The experiences during the COVID-19 crisis echo the experiences during the global financial crisis. Prior to the financial crisis, the overall FDI, especially the GFDI announcements increased rapidly. These flows halted with the onset of the financial crisis which plummeted its average annual growth rate to 0.4% between 2008 and 2019 compared to 4.9% between 2000 and 2007 (WIR, 2020). After their steady phase of 2012–2017, the FDI flows experienced growth in 2018 and 2019 before the pandemic hit, leading to the withdrawal of FDI. Moreover, this fall in FDI projects and investments is skewed towards economies that are more integrated into GVCs. With the pandemic severely affecting the production chains, withdrawal of foreign investment will be more likely to affect such economies severely. This is supported by the fact that China, the world leader in fragmented production, witnessed a 13% fall in FDI inflows in the first quarter of 2020. Subsequently, FDI flows to developing Asia declined by US$474 billion (WIR, 2020).

Europe also experienced a net FDI outflow of US$7 billion in 2020 driven by repatriation of earnings by foreign firms in response to the pandemic (Dettoni, 2020). International investment agreements (IIAs) have been operating in a new economic environment. Some countries have made efforts to support them through online investment facilitation and others have tightened screening to protect strategic industries. The healthcare industry, in particular, has suffered measures such as mandatory production and export bans, which have affected the investment decisions of foreign companies too (Evenett et al., 2020; WIR, 2020) In addition, the COVID-19 crisis has been unravelling in the context of trade ‘war’ between the two largest economies, the USA and China. The WIR (2020) reports that ‘at least 11 large cross-border M&A deals were withdrawn or blocked for regulatory or political reasons’.

The withdrawal of M&As and GFDI deals highlights that the pandemic has an impact on the extensive margin of FDI investment. In this regard, using a Heckman selection model on a monthly panel data of 96 economies for the period of January 2019 to June 2020, Fu et al. (2021) highlight the adverse impact of COVID-19 on FDI flows. Specifically, they find that the spread of infection in the host country significantly affects the decision of FDI projects in the host economy. Further, higher mortality in the host economy also leads to a reduction in the value of FDI announcements. The study also finds that the severity of the virus in the home country leads to a delay in the completion of ongoing projects. Moreover, the results from the empirical analysis also showcase higher sensitivity of FDI flows to the service sector compared to others.

Given the frailty in GVCs highlighted by the pandemic, restructuring of GVCs and building more resilient GVCs would be the way forward to eventual recovery. While most economic sectors are affected by the crisis, there are some examples of growth, for example, ICT, financial services, life science and creative industries, as COVID-19 accelerates digitisation and brings healthcare in economic focus; for example, Xiaomi, the Chinese smartphone and electric scooters manufacturer has expanded its market footprint in overseas markets (FDI Intelligence, 2020). The Swiss pharma group Roche plans to open new branches in the Democratic Republic of the Congo, Tanzania and Angola (FDI Intelligence, 2020). The Spanish telecommunications company Telefonica and the German insurance company Allianz in a 50/50 joint venture are planning a 50,000-km broadband fibre-to-the-home (FTTH) network, worth €5 billion over the next 6 years (FDI Intelligence, 2020). The growth of more a service-oriented FDI is an outcome of a shift in global FDI patterns over the past two decades. According to fDI Markets estimates, in 2003, GFDI projects in manufacturing accounted for 37.8% of global GFDI projects compared to 12% for business services. Sixteen years later, GFDI projects in services were 2.3% more than that of manufacturing.

Another pattern of the shift in FDI prior to the pandemic was the investment in logistics and transportation projects driven by the rise of e-commerce industry (Doytch, 2021c). In this regard, the GFDI growth in 2018–2019 was driven by the services and IT industries. Further, lockdown restrictions imposed across the globe accelerated investment in these types of projects, which will be the basis of the growth of GFDI in the coming years; for instance, 2020 witnessed an expansion of Amazon, owing to larger demand through online stores. As a result, Amazon made investments in the USA, announcing a record 204 US interstate projects focused on logistics, transportation and distribution projects together valued at US$21.4 billion (Crawford, 2020). The single investment by Amazon led to jobs for over 36,000 US workers in the first 3 months of 2020 alone, resulting in a 34% increase in Amazon’s US workforce. Along similar lines, fDI Markets data indicate that GFDI worth US$73.5 billion was invested in logistics, distribution and transportation operations in 2019. These investments also highlight the global shift towards digitalisation in production and global trade.

In addition to the impact of COVID-19 on FDI, the pandemic has also affected other aspects of trade and the global economy. To briefly summarise, the first wave of pandemic led to the imposition of lockdown and social distancing norms which affected the tourism and travel industry adversely. The lockdown also resulted in a production shock which later resulted in an amplified demand shock. In this regard, Vidya and Prabheesh (2020) employ network analysis and show that the pandemic has resulted in a reduction in trade interconnectedness, connectivity and density among countries, and that there is an expected change in the structure of trade networks.

Moreover, the trade policy response to the pandemic shock also varied across countries. With massive supply chain disruptions, many economies closed their borders for the export of essential supplies and removed import restrictions for critical medical equipment and other essential items required to fight the pandemic. The decision to close borders for exports of essential items and equipment was in contrast to the notions resonated by experts and leading economic development organisations (EDOs), which propagated against the closing of borders for smooth functioning of the supply chains in order to boost production of essential items (Baldwin & Evenett, 2020; Bown, 2020a, 2020b; Mattoo & Ruta, 2020; OECD, 2020; WTO, 2020). Evenett et al. (2020) highlight that by May 2020, export restricting measures in the medical sector peaked against the import facilitation measures, which experienced a growth till September 2020, documenting the rapid increase in trade policy activism.

In addition to trade imbalances and policy effects, COVID-19 also adversely affected various aspects of the economy; for instance, using regression analysis on five Asian economies, Iyke (2020) documents an increase in economic uncertainty due to the COVID-19 outbreak. Within this frame of reference, using wavelet analysis, Choi (2020) highlights that the pandemic-induced policy uncertainty has affected the sectoral volatility with a magnitude greater than that witnessed during the global financial crisis. 1

It has also been documented that the pandemic resulted in a supply shock which soon led to a demand shock as well. In this regard, using China Household Finance survey, Liu et al. (2020) document a significant fall in Chinese household consumption. Yue et al. (2020) document a change in investment behaviour towards more risk-averse investments for Chinese households which have a connection with someone affected by COVID-19 virus. Further, Bauer and Weber (2020) and Yu et al. (2020) show the negative impact of the pandemic on labour force participation, and Shen et al. (2020) depict a negative impact on corporate performance. These studies highlight that COVID-19 pandemic has adversely impacted various facets of the global economy.

Long-Run Trends of Greenfield Foreign Direct Investment Worldwide

The fDi Markets data used in this study are transaction-based data. It records and reports all greenfield investment deals anywhere in the world with their value of the capital investment, number of employees, location of investment, home country of investment, industry activity, as well as the identity of the parent and investing company. The data span from January 2003 to August 2020. We have made several modifications to the data. First, we have aggregated the values by quarters and years, in order to analyse the respective trends. Second, we have applied a conversion algorithm from industry technology codes originally included in the data to the International Standard Industrial Classification (ISIC) Rev. 4 industrial classifications. We present below the analysis of trends of the top 10 host and home countries of GFDI, as well as the top 20 industry recipients of FDI.

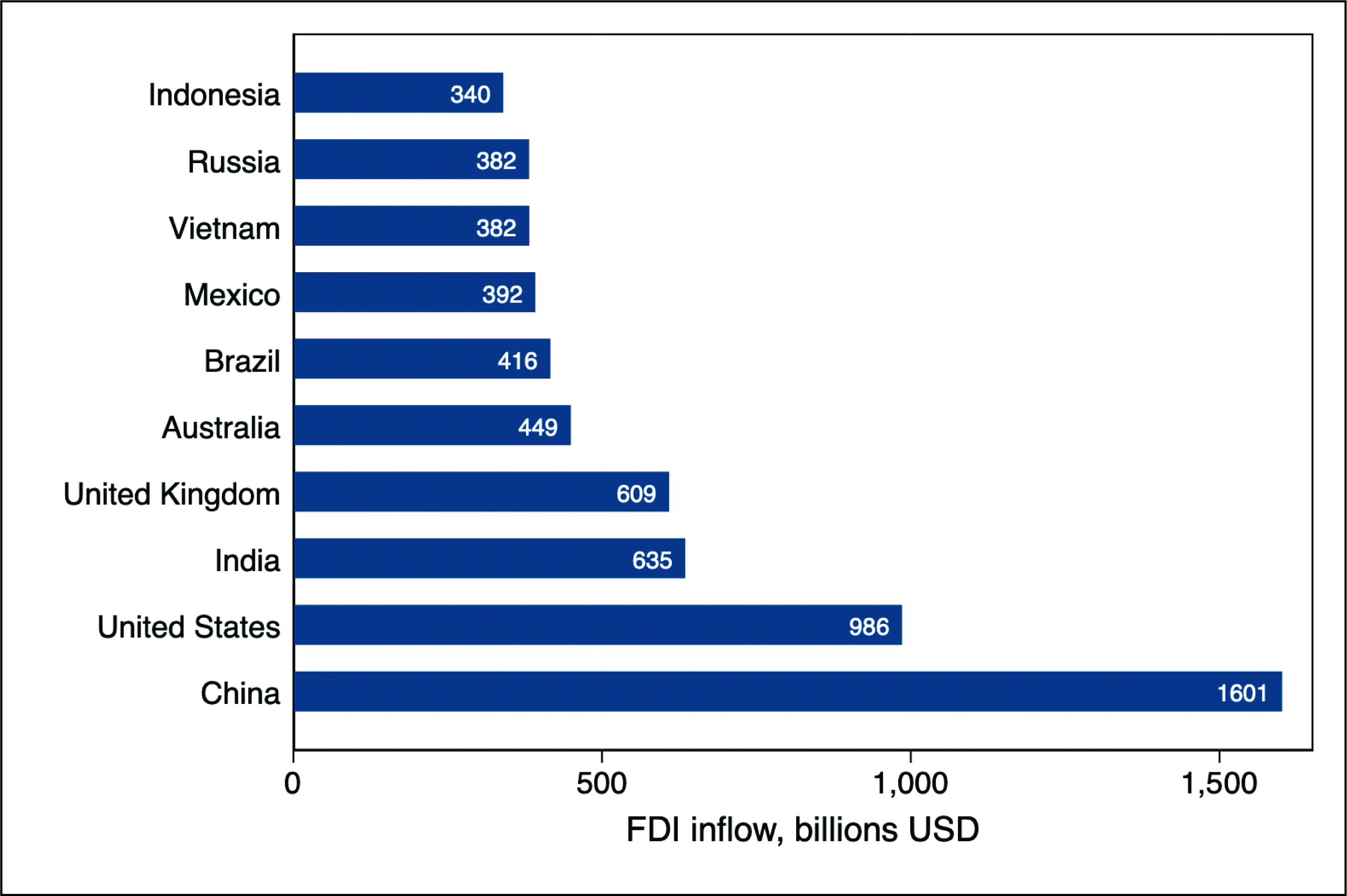

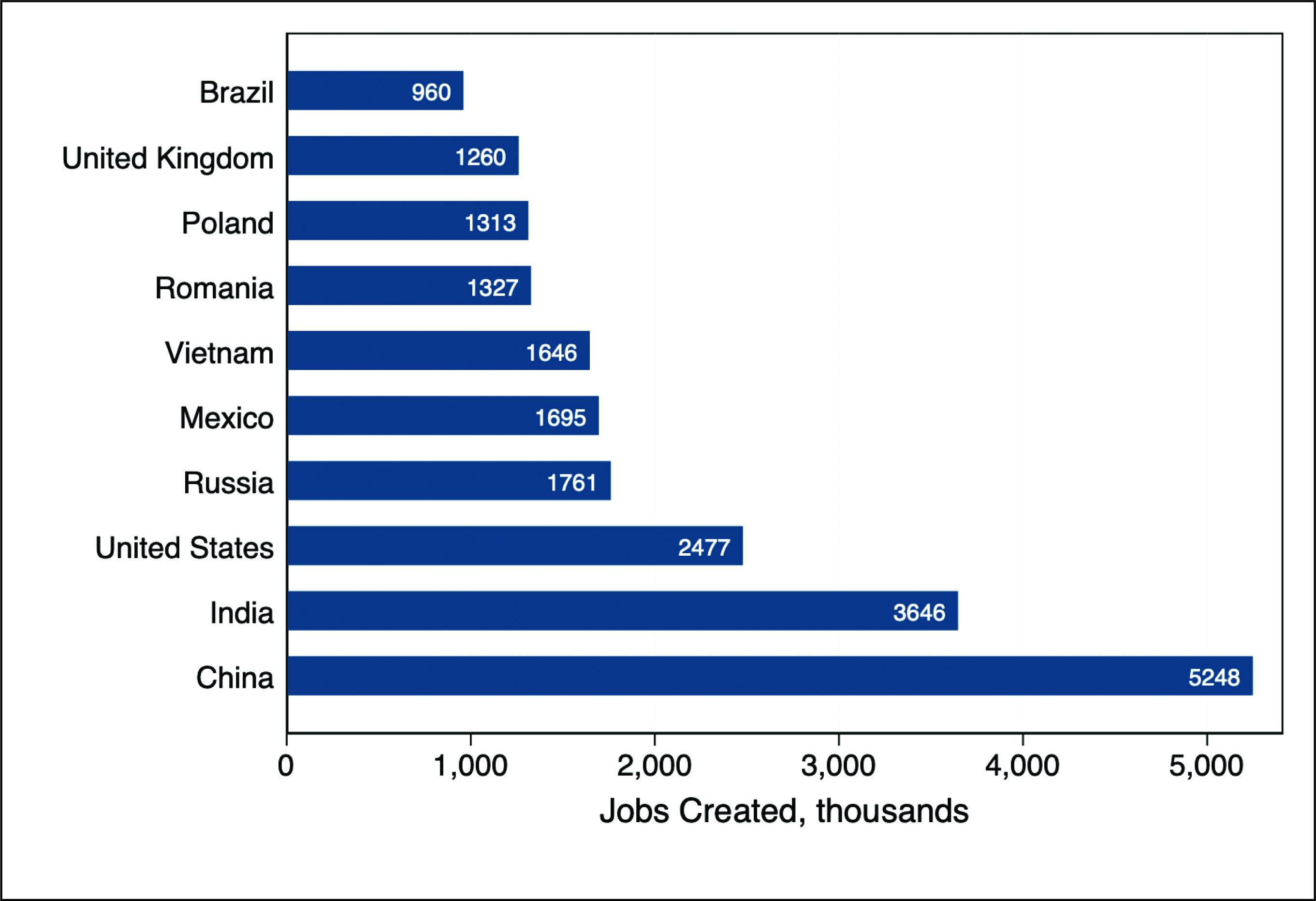

The top 10 recipients of FDI inflows during the period 2003–2020 have been China, USA, India, UK, Australia, Brazil, Mexico, Vietnam, Russia and Indonesia, a group that notably contains all the BRIC (Brazil, Russia, India and China) countries (Figure 1). China is a ‘distant first’ with over US$1.6 trillion in GFDI received (Figure 1). For comparison, the second country, the USA, has received less than a trillion in this period (Figure 1). A less discussed aspect of GFDI is the jobs created through the establishment of the new subsidiaries. In terms of the jobs created, the top 10 recipient countries of GFDI are China, India, USA, Russia, Mexico, Vietnam, Romania, Poland, UK and Brazil, whereas in China, there are over 5 million jobs created by GFDI, versus 3.6 million in India and 2.5 million in the USA (Figure 2).

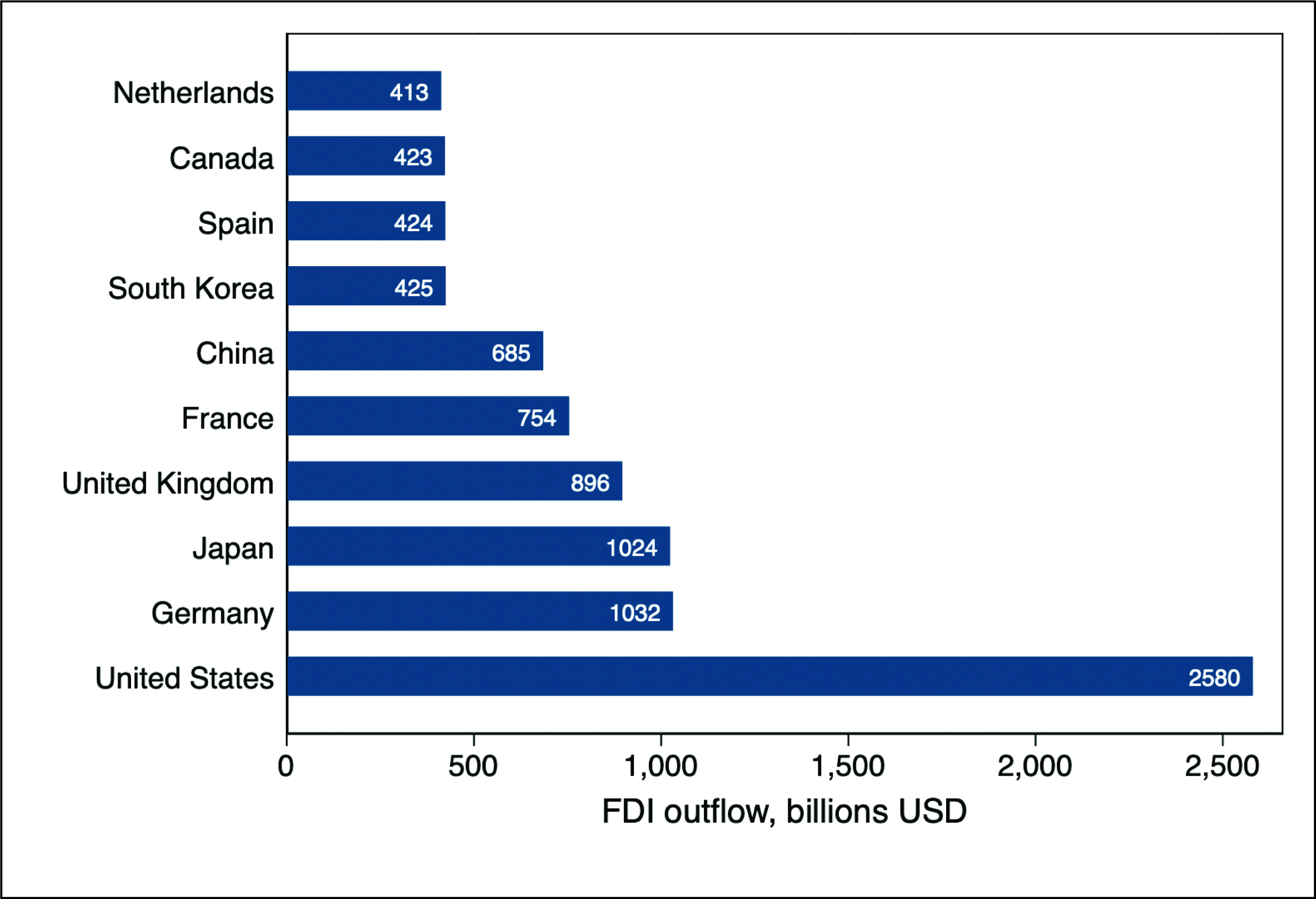

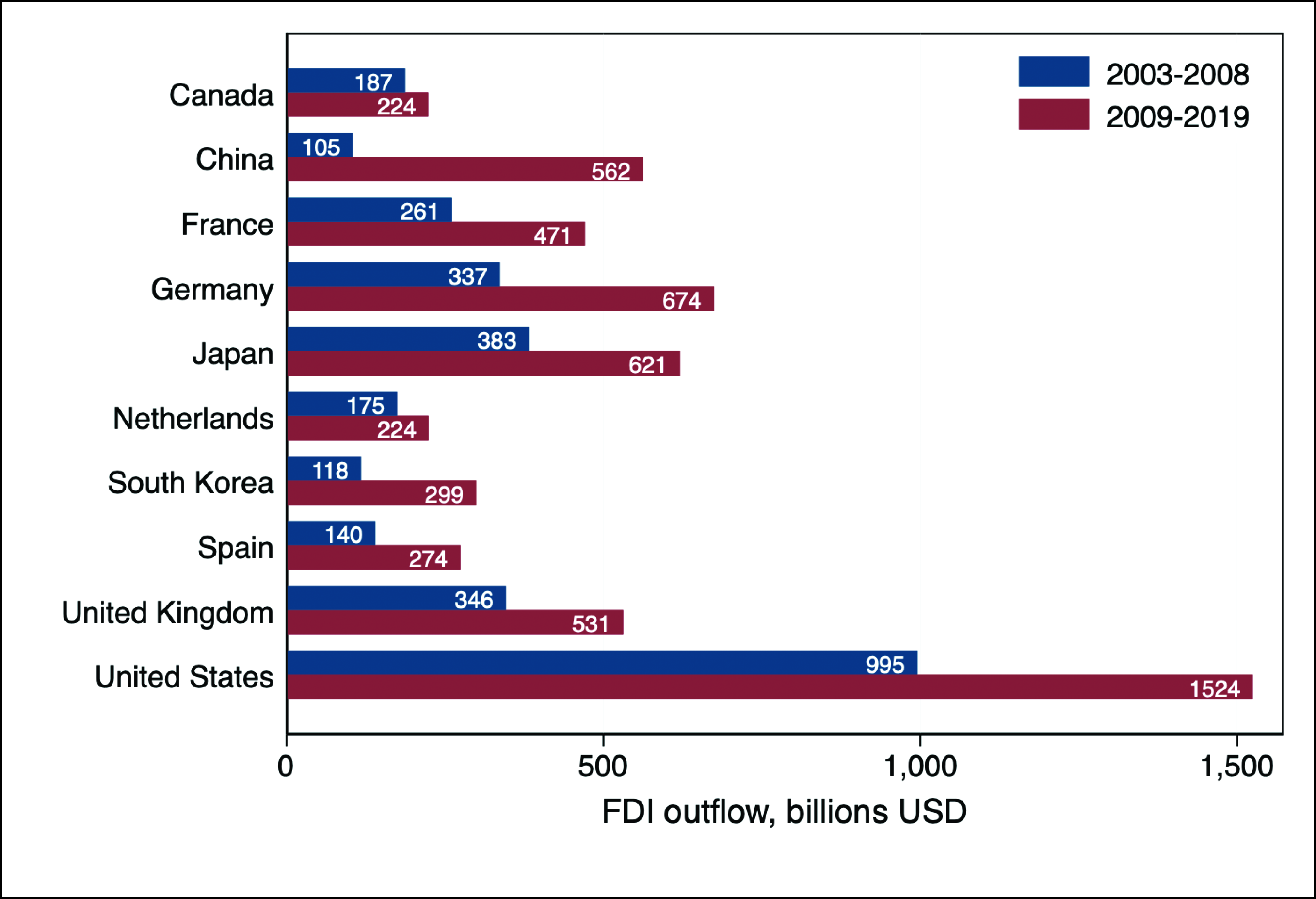

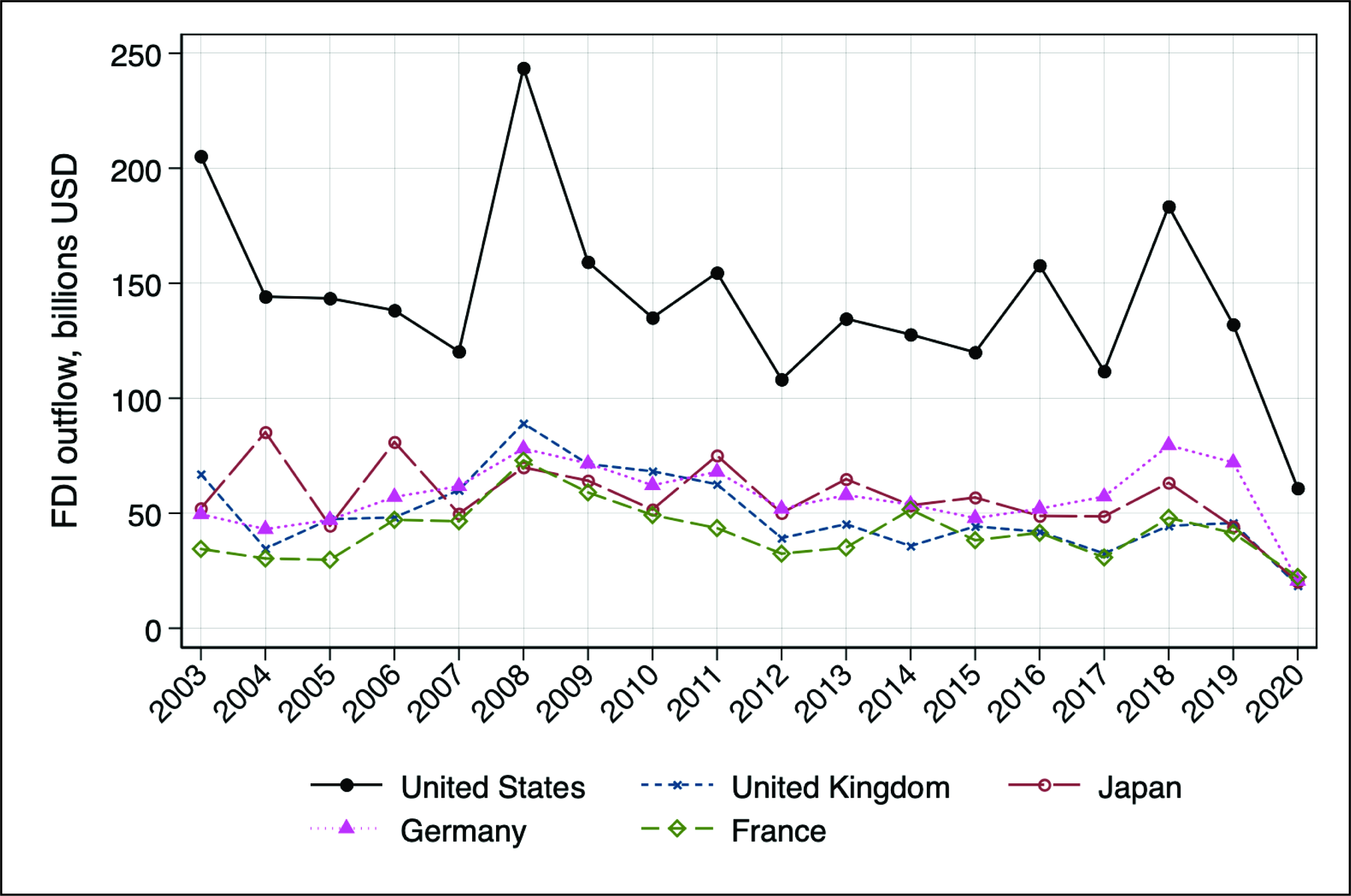

At the same time, the top 10 countries as sources of FDI outflows are USA, UK, Spain, South Korea, The Netherlands, Japan, Germany, France, China and Canada (Figure 3). Notably, all 10 but China are developed economies. The USA is a distant number one with over US$2.5 trillion GFDI abroad (Figure 3). Figure 2 also shows a significant increase in outward GFDI in the post-global financial crisis era (2009–2019), compared to pre-crisis (2003–2008) for all top 10 source countries. The most significant increase of outward GFDI in the post-crisis period was experienced by the only developing country in the group, China. The GFDI outflows from China between the two periods increased approximately five times (Figure 4).

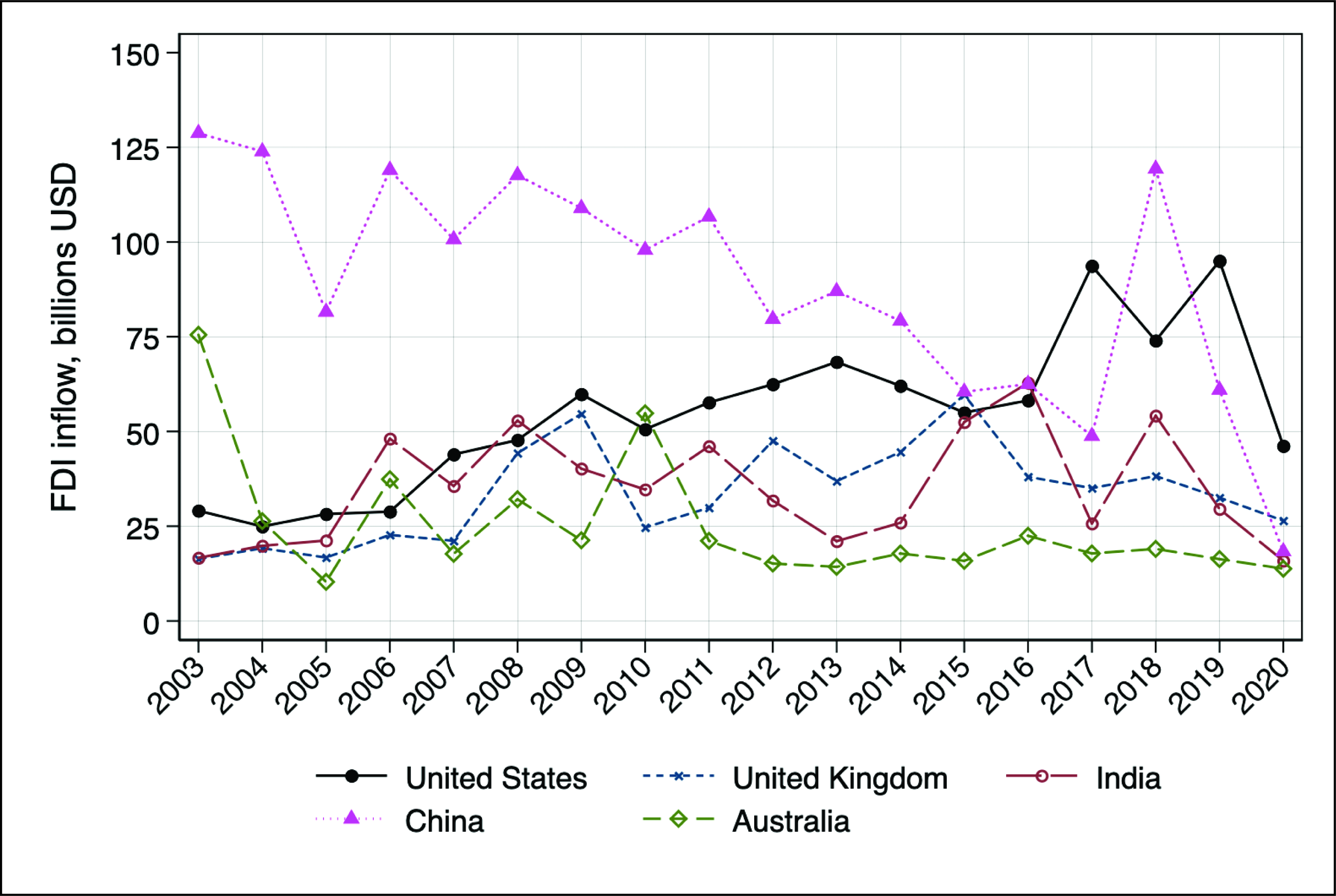

Analysis of the time series of GFDI inflows and outflows of the top five host and home countries reveals some interesting trends (Figures 5 and 6). China displays a downward trend in inflow GFDI and an upward trend in outflow GFDI, gradually turning from a net recipient of GFDI to a net source of GFDI in an ongoing process (Figures 5 and 6), illustrating its move along the investment development path (Dunning & Narula, 1996). At the same time, USA shows an upward trend in GFDI inflows and relatively stable levels of outflows, if we exclude 2020, the year of the pandemic (Figure 6). In both the cases, with the inflows and the outflows, we observe a sharp decline in FDI during the first three quarters of 2020. The decline in the inflows is the most substantial for China, a 73% y/y decline (Figure 5). The most significant decline in outflows is for the USA where the FDI outflows decreased by 54% y/y (Figure 6).

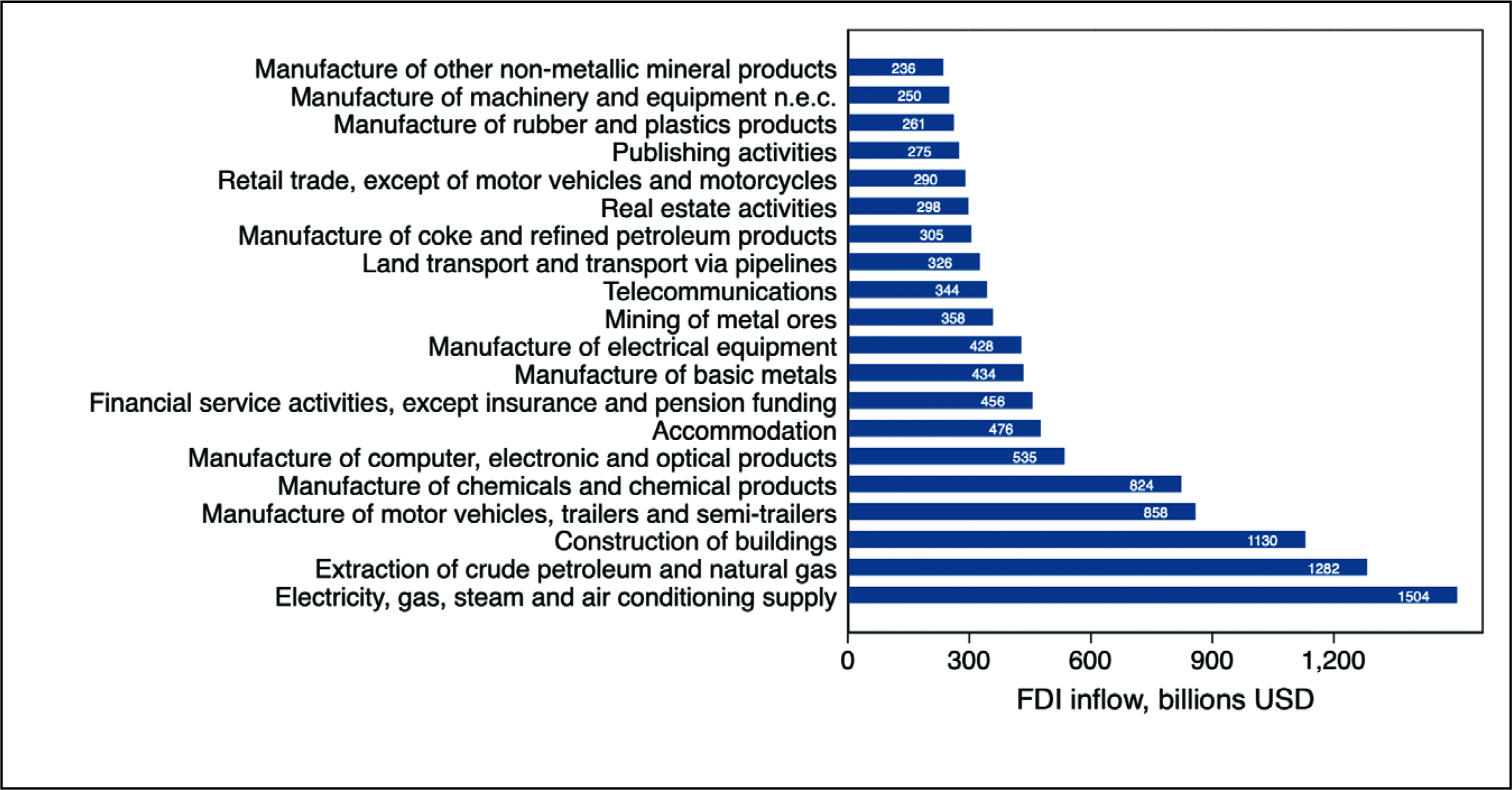

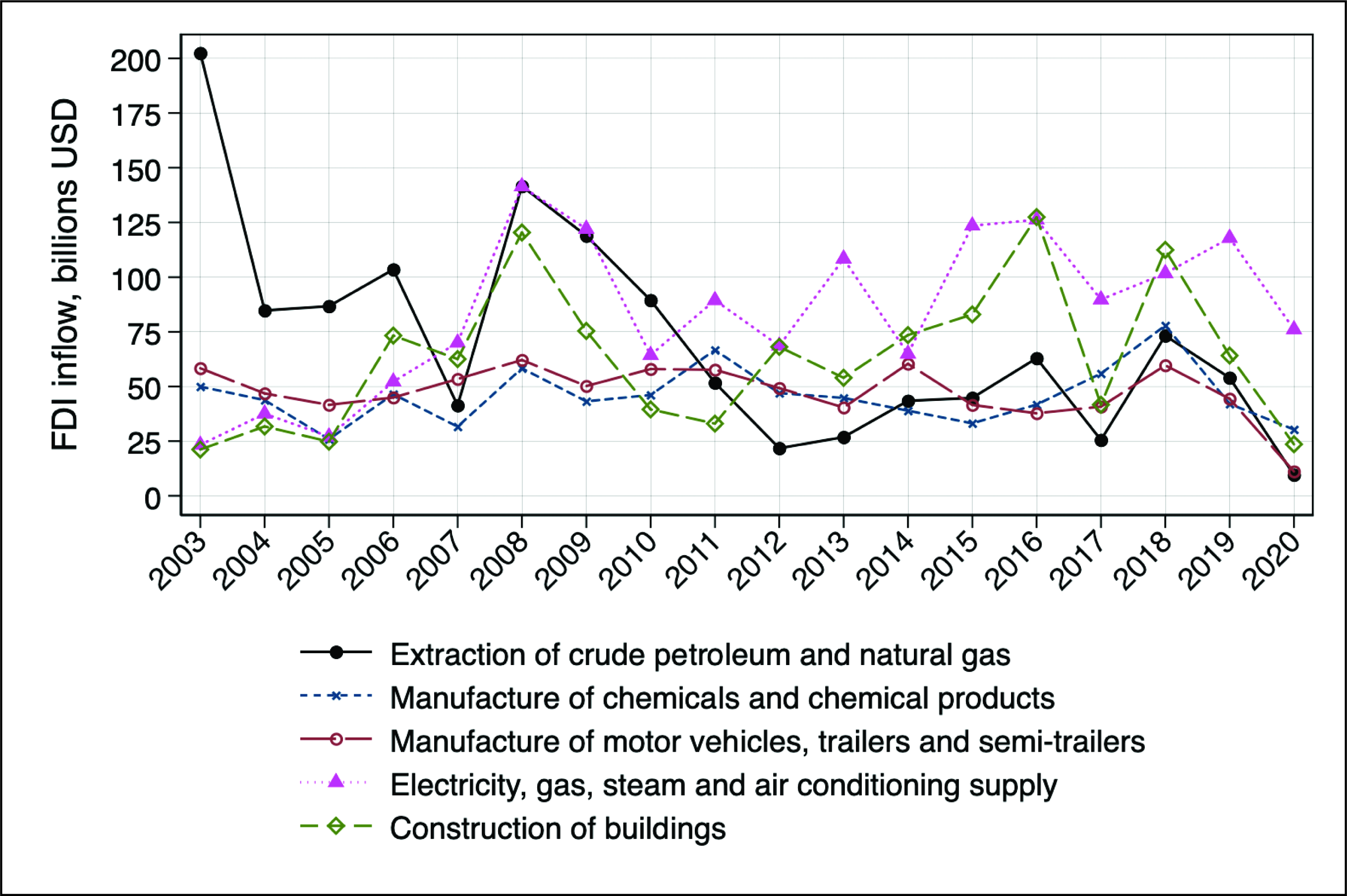

In terms of the industrial classification of the GFDI flows, the top six industries consist of primary and secondary sector activities: electricity, gas and air conditioning supply; extraction of crude petroleum and natural gas; construction; manufacture of motor vehicles; manufacture of chemicals; and manufacture of electronic and optical equipment (Figure 7). Most of these industries have stable levels; the extraction of crude oil and petroleum and natural gas displays a downtrend over the studied period (Figure 8). All top five industries show a sharp decline in 2020 (Figure 8).

GFDI During the Financial Crisis and the COVID-19 Pandemic

The most recent global economic crisis prior to the crisis caused by COVID-19 is the financial crisis of 2008. In this section, we attempt to compare the behaviour of GFDI during the global financial crisis and the COVID-19 crisis.

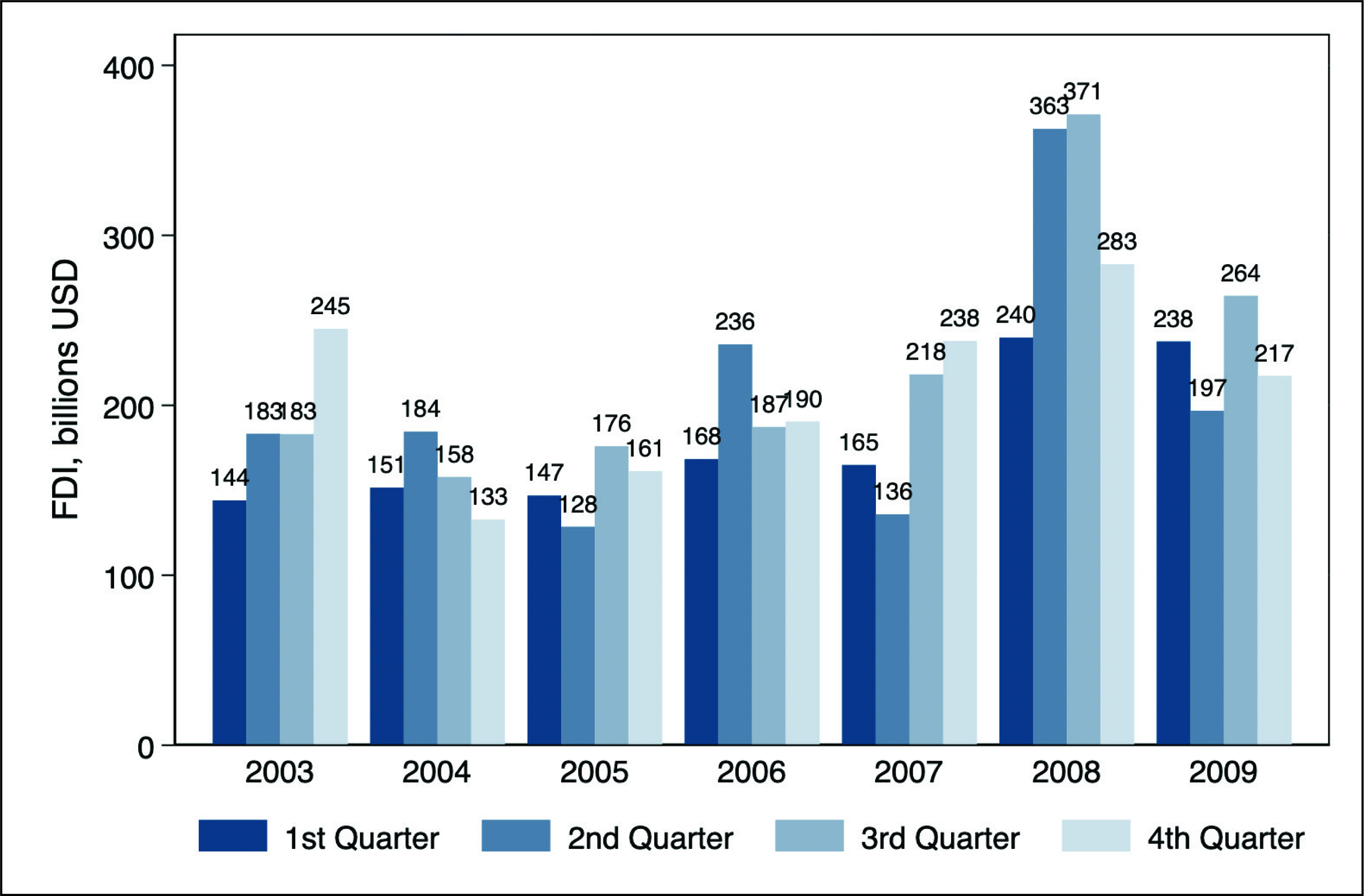

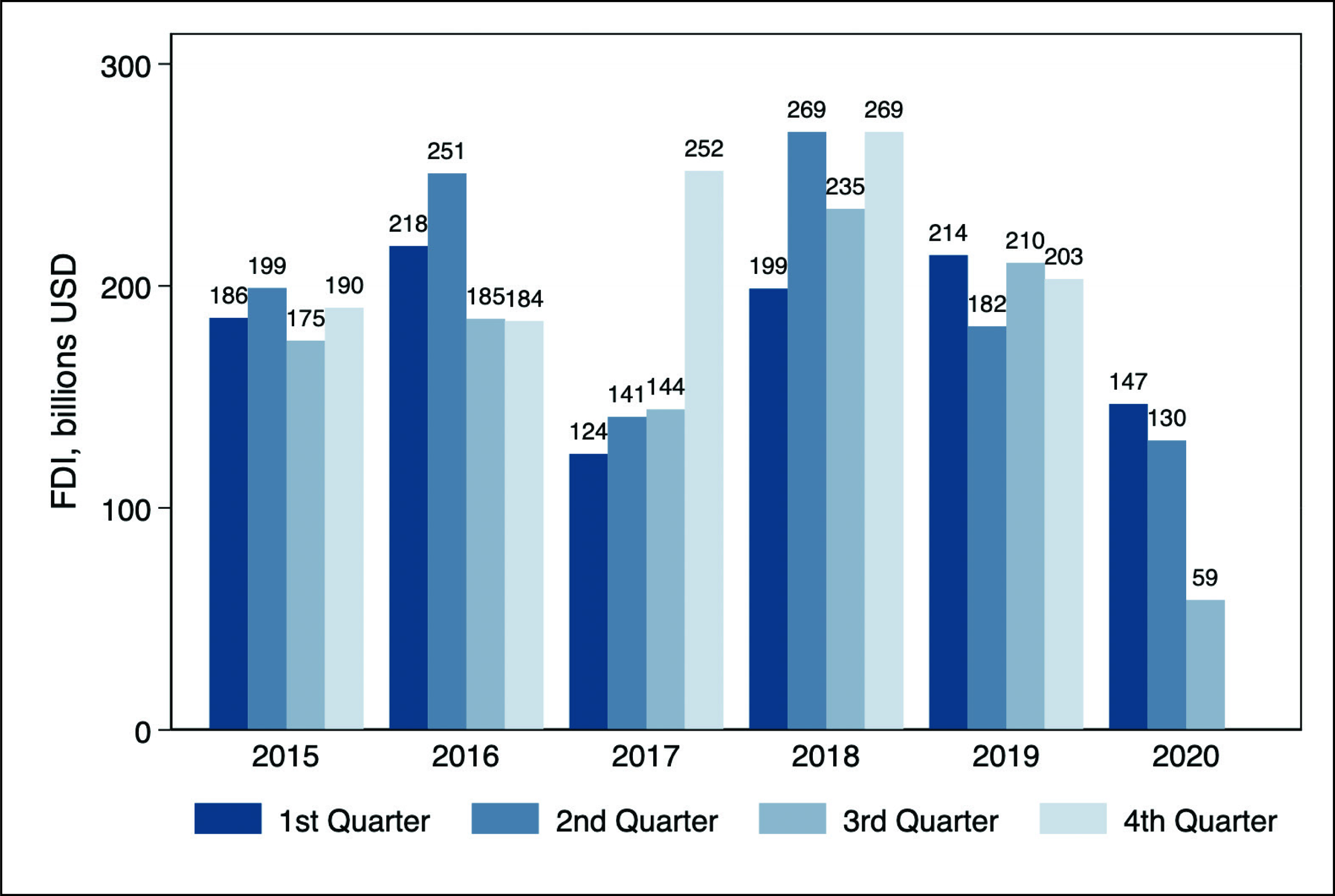

The quarterly data of the 5 years leading to the global financial crisis shows a spike of GFDI inflows in the second and third quarters of 2008 followed by a moderate decrease in 2009 (Figure 9). For comparison, the 5 years preceding the COVID-19 crisis display relatively stable levels of GFDI, followed by a progressive decrease in the first, second and third quarter of 2020, which is the last quarter we observe in this dataset (Figure 10).

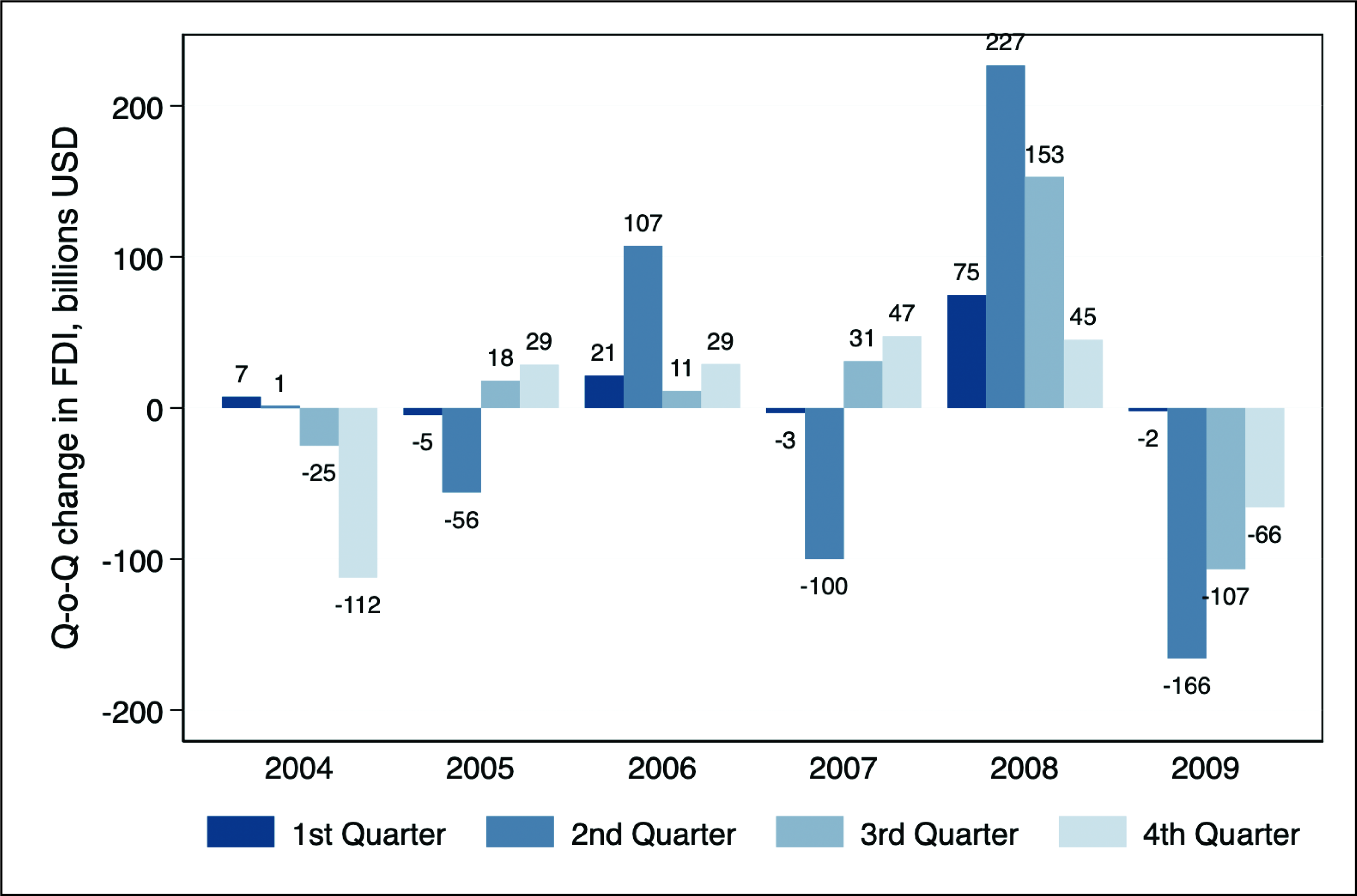

The quarter-to-quarter analysis shows a very different response of GFDI during the 2008 financial crisis and the ongoing COVID-19 crisis. The financial crisis, which intensified in the fourth quarter of 2008 had most of its impact on the world GDP, trade and financial flows in 2009. The GFDI flows collapsed by −166% in the second quarter of 2009 and then began to recover very slowly (Figure 11).

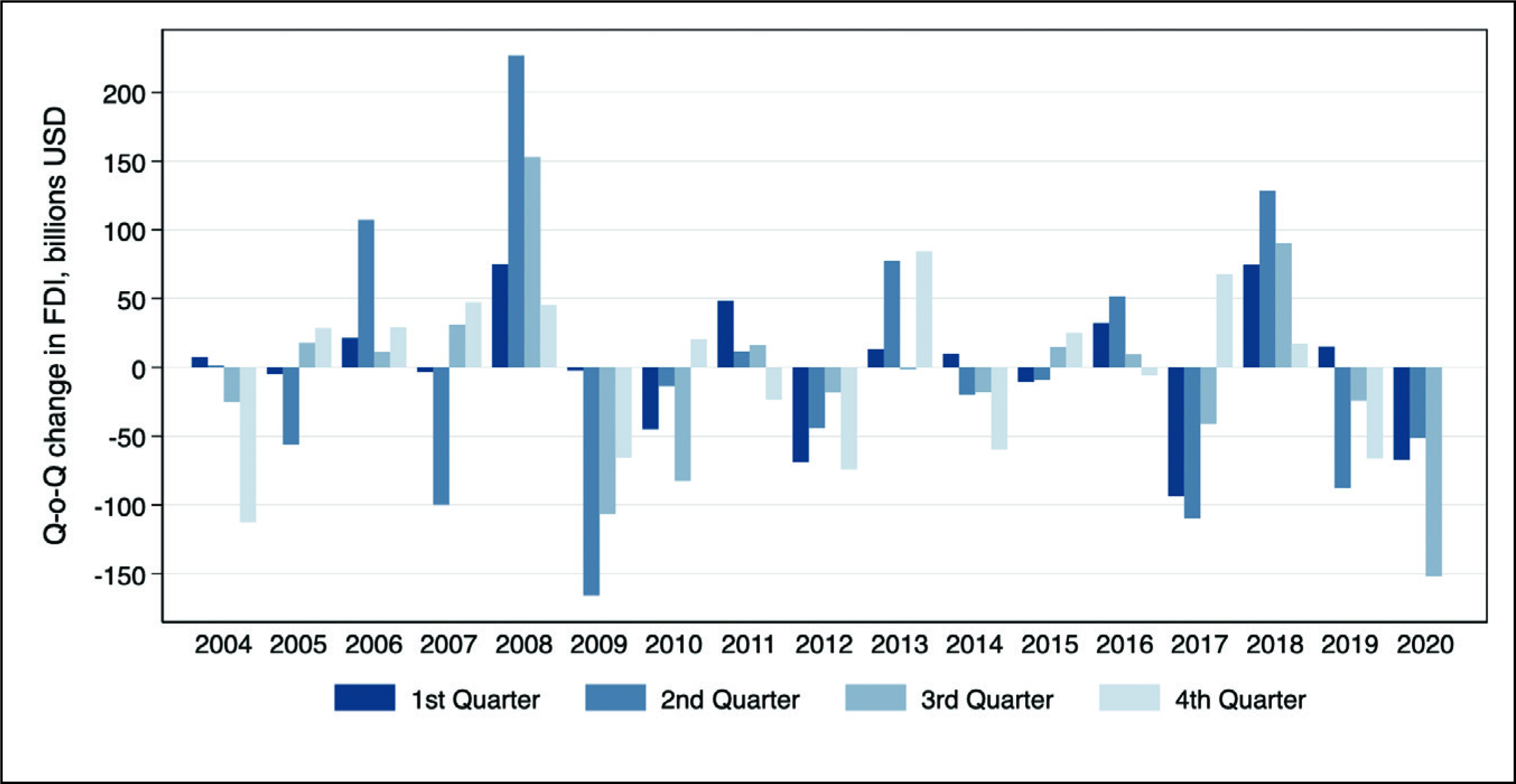

The overall behaviour of GFDI changed after the 2008 financial crisis. The crisis put an end to a stable growth trend of the flows in the 2000s. After the 2009 collapse, GFDI had a process of slow recovery, which continued until 2017 when the global governance situation changed with the election of a new US government administration that seeked to change the major trade agreements the country participated in. However, after the initial international economic uncertainty, provoked by policy changes in the USA, the global GFDI recovered and grew during 2018, only to slow down again in 2019. The hit of the pandemic started weighing heavily on the international investment flows in the third quarter of 2020 (Figure 12).

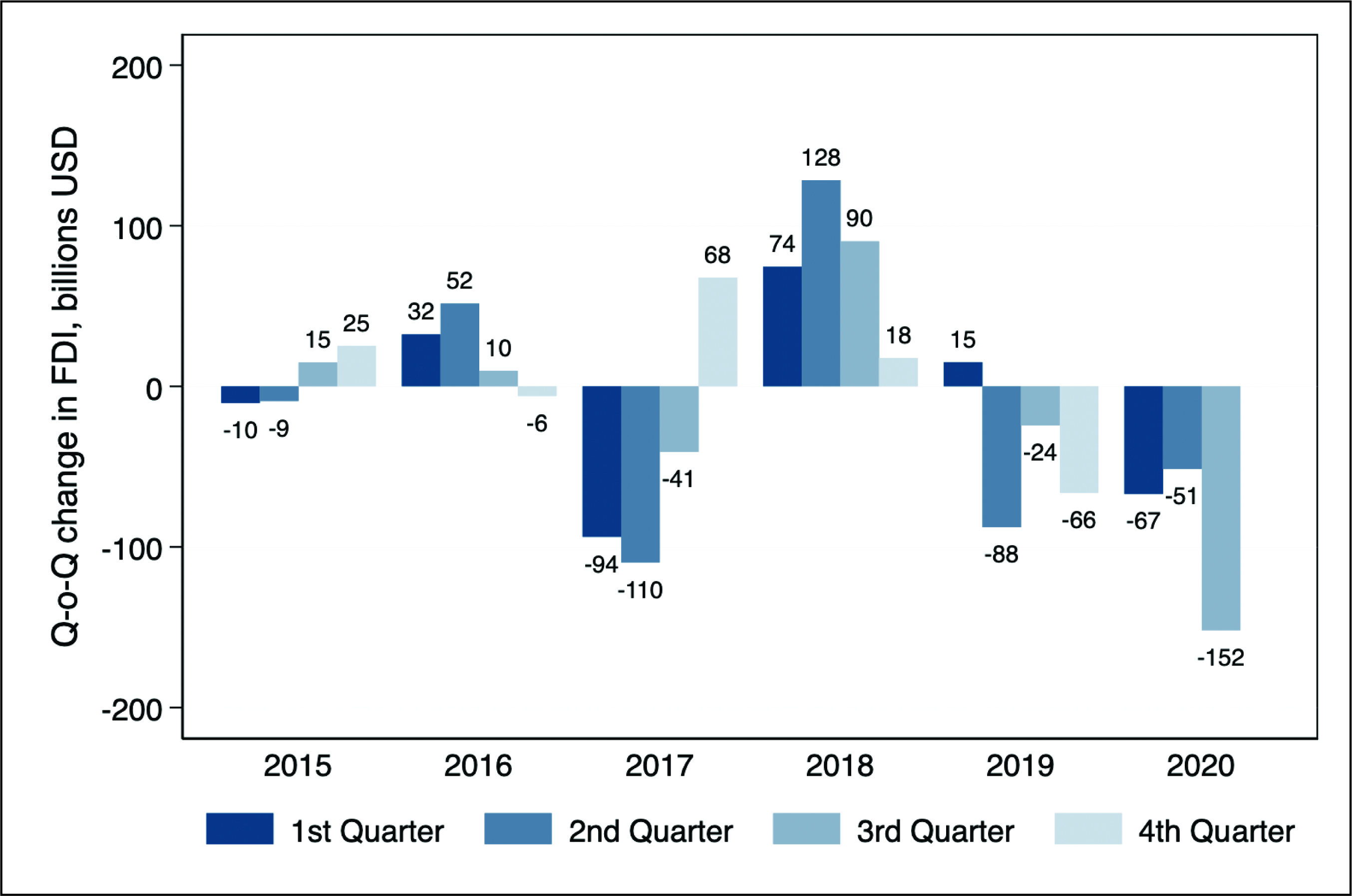

An analysis of the quarterly changes in GFDI in the 5 years preceding the pandemic shows the lack of long-term growth of global GFDI after 2008. During the 5 years preceding the pandemic, only 2 years witnessed a growth of GFDI, 2016 and 2018. For most of the post-2008 period, the flows have fluctuated around a stable worldwide level of US$200 billion without growing. The COVID-19 pandemic introduced an additional shock to the already stagnant flows. The first quarter of 2020 brought worldwide lockdowns of cities and states and increased uncertainty. The country that went first in and out of lockdown was China. As a result, the post-covid recovery in China also started before the recovery in Europe and the USA. The USA and parts of Europe have spent most of 2020 in partial lockdowns. The main hit of the pandemic on the global GFDI flows occurred in the third quarter of 2020, a decrease of 152% quarter to quarter. This decrease occurred in addition to a 51% drop in global GFDI flows in the second quarter and a 67% decline in the first quarter, which are to be added to a continuous decline throughout most of 2019 (Figure 13).

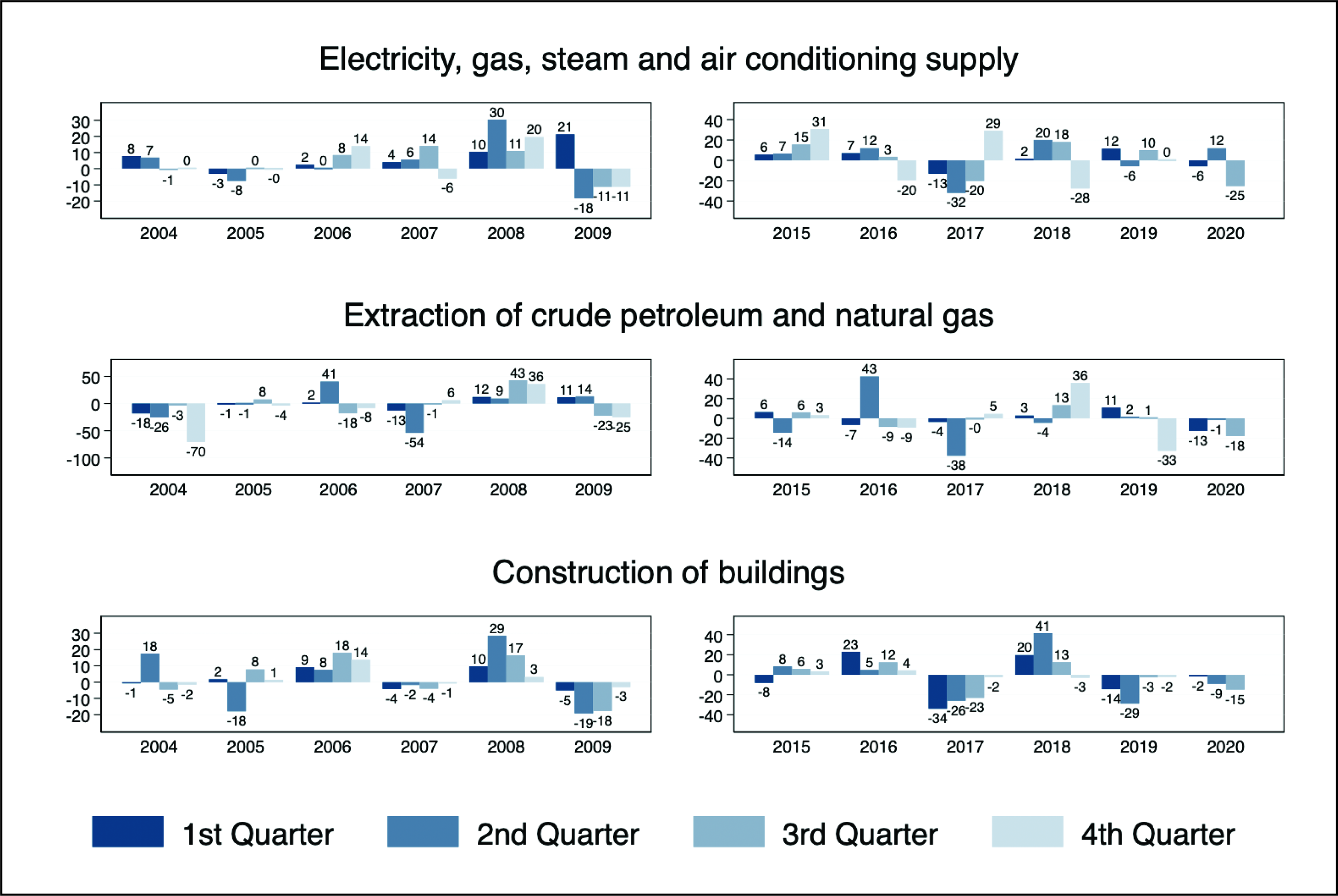

The pandemic-caused decline in the global GFDI, however, affected industries differently. In Figure 14, we explore quarter-over-quarter percentage changes of GFDI inflows to the top 10 industries of the world. In the left panel, we display 6-year quarter-over-quarter changes of GFDI covering the global financial crisis period, and in the right panel, we display 6-year time series of quarter-over-quarter changes of GFDI covering the pre- and post-pandemic period, ending with the third quarter of 2020.

The top 10 industries include activities from all 3 sectors, that is, primary, secondary and tertiary, in addition to utilities and construction. The parallel analysis of the left and the right panels shows that GFDI to the utility industry (Electricity, gas and air condition supply) was slow to respond to both cases However, once responded, the decline of the GFDI flows could be significant, up to 25%. GFDI in the Extraction of crude petroleum and natural gas has also responded with a relatively large contraction in both crises. The quarterly drops during the financial crisis were of the magnitude of 22% and 25% in the last two quarters of 2009, and the decline during the pandemic so far has reached 18% in the third quarter of 2020. This is not surprising considering the global pandemic lockdowns’ restrictions in travel and the full seizure of air travel. GFDI to the Construction sector has also responded with sharp declines in both crises.

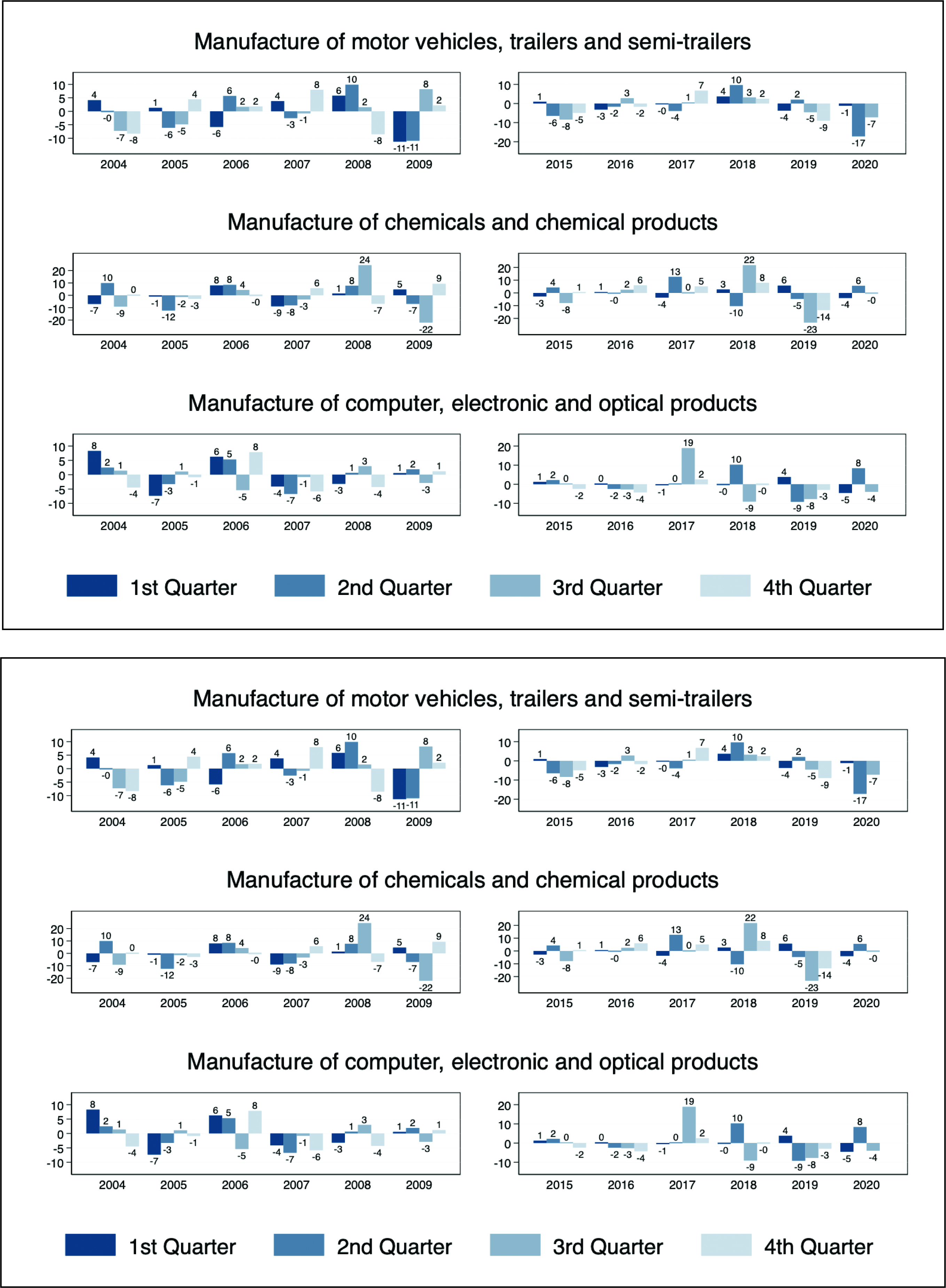

The following three industries are from the manufacturing sector. GFDI to manufacturing of motor vehicles, trailers and semi-trailers has been relatively sensitive to and relatively quick to respond to both crises with drops of the magnitude of 11% in the first two quarters of 2009 during the financial crisis and 17% in the second quarter of 2020. Again, this is a sector that is tightly linked to the ability to travel, and as such, it is expected to be highly affected by the pandemic-induced economic crisis. The other two manufacturing sectors have not responded in the same fashion. GFDI to manufacturing of chemicals and chemical products responded with a significant decline (22%) and a quick recovery during the financial crisis, but not in the pandemic crisis. GFDI to manufacturing of computer, electronic and optical equipment has barely decreased in both cases. The tenth top industry is the manufacturing of basic metals. GFDI into this industry was more responsive to the financial crisis rather than the current pandemic crisis.

In the top 10 industries, we have two services industries as well: accommodation and financial service activities. GFDI to the accommodation sector, which is a key part of tourism, declined by 11%–12% quarter-over-quarter in both crises. Although the tourism sector suffered an initial contraction at the beginning of the pandemic, many hotels re-positioned themselves as potential accommodation for lockdown periods and long-term stay for people working remotely. As a result, the sector started a partial recovery and the GFDI deals have not been completely interrupted. The GFDI in the financial industry has also had a minor contraction in both crises. Contrary to the expectation that a financial crisis would bring investment in banking and insurance to a standstill, this has not been the case for GFDI. After a decline by 5% in the second quarter of 2009, it went on a gradual recovery. The reason why the decline was not more severe was the fact GFDI is a brand new investment, not a purchase of existing banking assets whose value may have significantly declined during the crisis. Interestingly, GFDI in finance did not contract significantly in the current financial crisis either. This has been one of the industries, which continued to function in a remote mode.

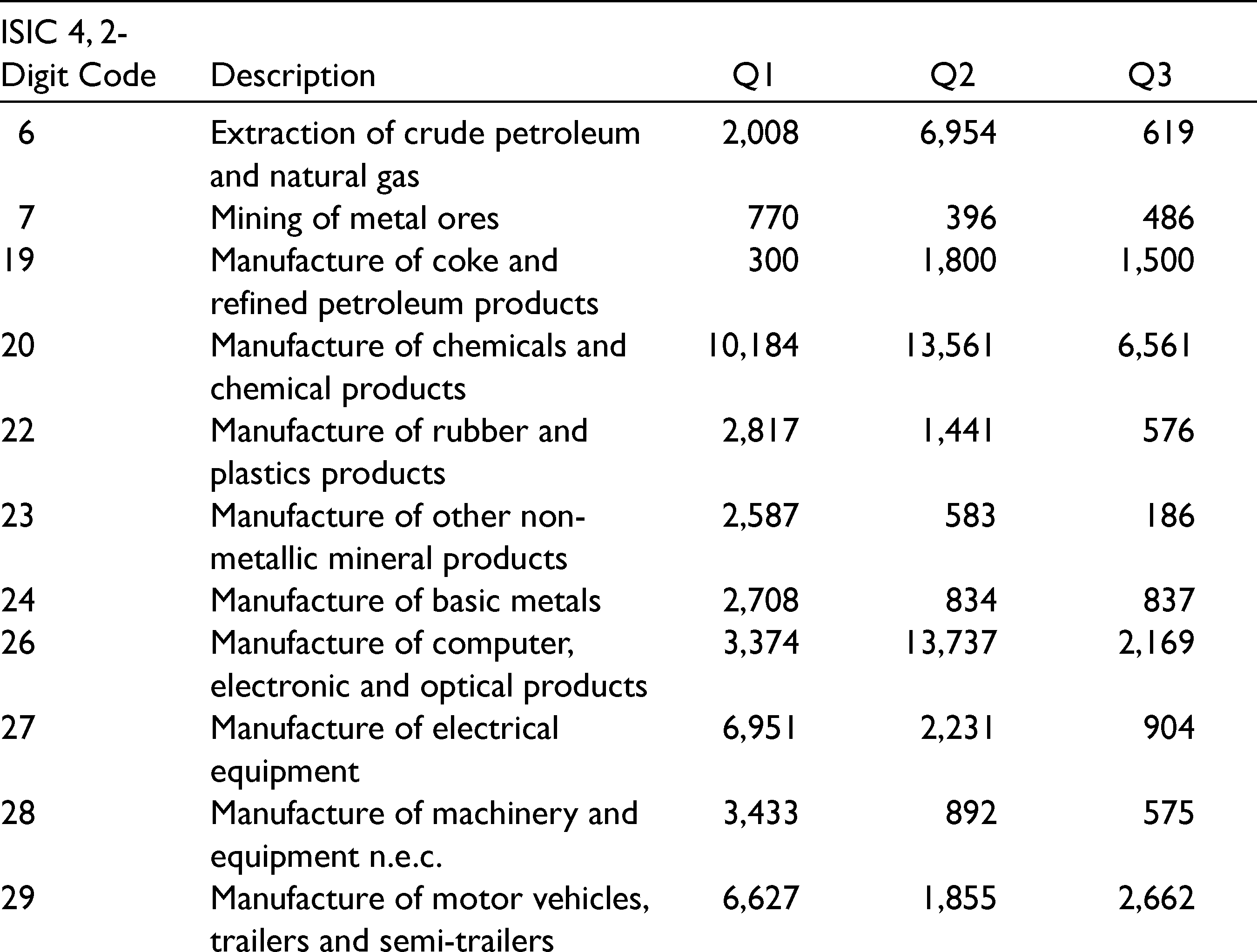

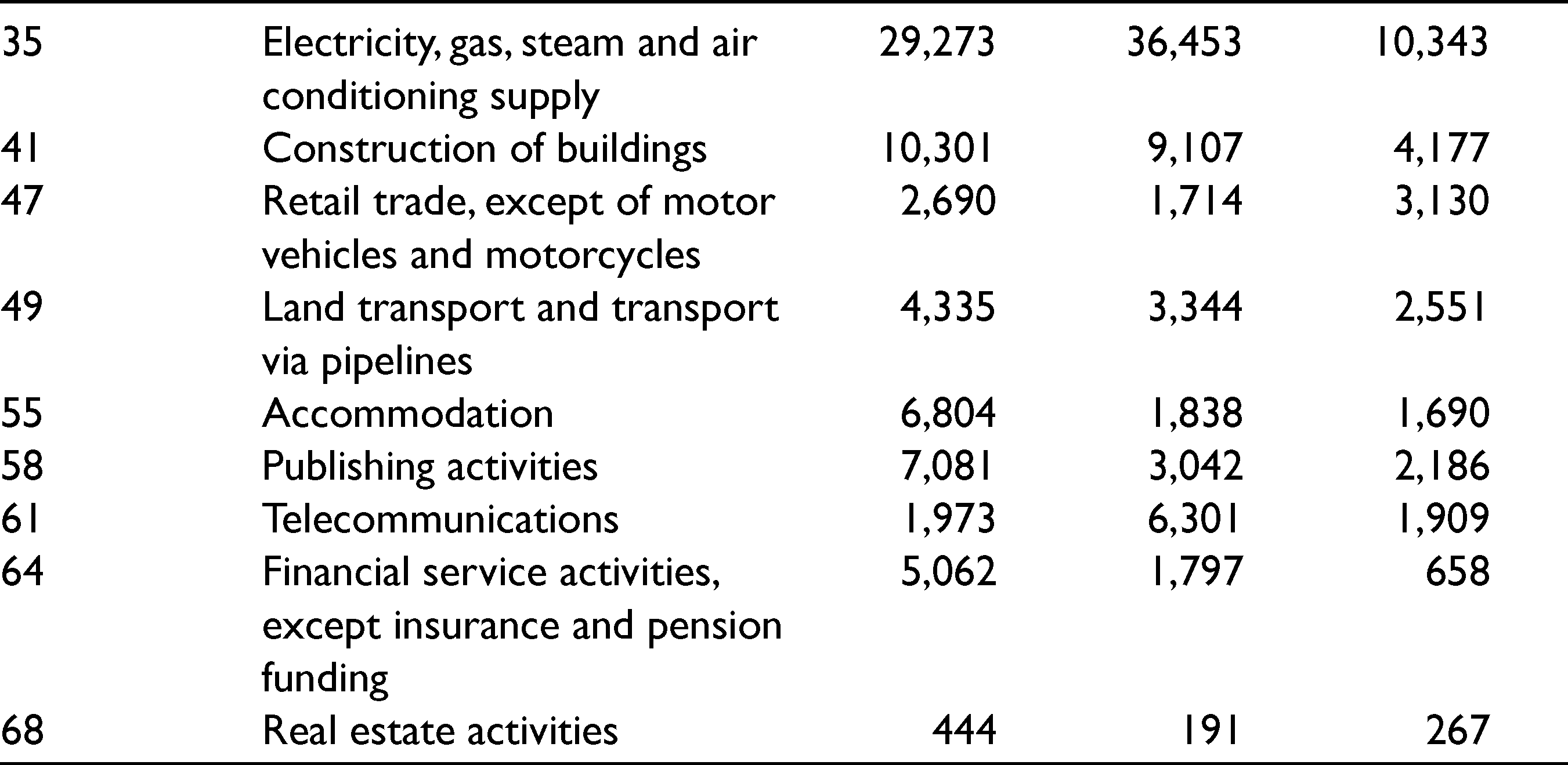

If we zoom into industry-level dynamics of GFDI during the COVID-19 lockdowns of 2020 (Table 1), we see that the most affected industries were manufacture of other non-metallic mineral products, with a decline of 77% between Q1 and Q2 of 2020; manufacture of machinery and equipment with a decline of 74%, accommodation, with a decline of 73%; manufacture of motor vehicles, trailers and semi-trailers, with a decline of 72%; financial service activities with a decline of 64% between Q1 and Q2 of 2020.

Industry-level GFDI During the First Three Quarters of 2020.

The industries affected the worst in the third quarter of 2020 were extraction of crude petroleum and natural gas, with a 91% q-o-q decline; manufacture of computer, electronic and optical products, with a decline of 84% q-o-q; retail trade, except of motor vehicles and motorcycles, with a decline of 83%; manufacture of other non-metallic mineral products, with a decline of 68%, and financial service activities, with a q-o-q decline of 63%. The above numbers show that by the second quarter of 2020, there was already a substantial slowdown of the international value chains, but by the third quarter, some industries’ GFDI was in collapse. Most notably, the extractives and some of the main manufacturing industries’ GFDI were very hard hit by the pandemic crisis.

Conclusion

In this article, we attempt to evaluate the behaviour of GFDI during the beginning of the pandemic, that is, the first three quarters of 2020. We do not attempt to estimate the magnitude of the effect with an empirical model, but rather evaluate the fluctuations in GFDI and make a comparison to the 2008 global financial crisis, which also affected the entire world adversely. We attempt to cast light on which countries’ and industries’ GFDI is most affected by the pandemic. To our surprise, many of the services industries GFDI flows have shown a certain resilience and flexibility to a switch to a remote work mode, while the manufacturing industries’ and the extractive and utility industries’ GFDI, which are parts of GVCs, have contracted more significantly.

The COVID-19 pandemic has brought to the forefront vulnerabilities of GVCs and globalised trade. The heavy dependence of the world on GVCs has resulted in these shocks resonating to other countries, adversely affecting global trade and future investments. In this regard, evidence from UNCTAD reports a substantial withdrawal of foreign investment overall, with rapid disinvestment from China and other supply chain-oriented economies (UNCTAD, 2020). However, despite the susceptibility of GVCs to global shocks, the way forward remains that of restructuring and building resilient GVCs. Fostering resilient GVCs brings to the foreground the importance of EDOs. With the rapid reduction in global foreign investment in developing countries, these organisations should direct their attention and resources to existing investors and make efforts at retaining their investments. Through such actions, they can provide avenues for host countries to strengthen their relationship with investors and local businesses. In this regard, the UNCTAD WIR 2020 report states that, with the reduction in GFDI, EDOs should use their services to support and foster joint ventures and other partnership modes, which would help countries recover from the pandemic shock faster along with aiding investment prospects at the time of global turmoil.

Every crisis presents an opportunity for improvement. The COVID-19 pandemic has brought about an urgency in building resilient supply chains. In a survey of 60 supply chain executives conducted by Mckinsy (McKinsey Global Institute, 2020), 93% reported their aim in making their supply chains more resilient. In this regard, one way forward would be to diversify supplier networks that safeguard a firm from national and regional shocks. This strategy, if adopted, would result in an inflow of FDI to diverse regions, thereby helping those economies which have been seeking to overtake China as the next hub of manufacturing. Another step towards building resilience in GVCs would be a greater sharing of knowledge between firms aimed at standardising the product, which could enable a swift shift of production during times of shocks. Another key aspect is improving logistics capability which, as documented earlier, was already on the rise, and the pandemic has accelerating investment in this segment. Hence, policies along these lines could help rejuvenate the falling foreign investment and direct them to more diverse regions and sectors.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The first author gratefully acknowledges PSC-CUNY (Grant # 68404-00 46).