Abstract

To delve deeper into the rise of trade in commercial services as the most important determinant of the recent increase in digital trade, this article offers a decomposition of international service trade using the latest release of the Inter-Country Input–Output (ICIO) tables. The analysis decomposes international service trade into a split between (a) direct services exports and services embodied in goods, (b) advanced economies and the major emerging markets, and (c) the major commercial services industries. We show that overall direct service exports have become more important relative to services embodied in goods, especially in advanced economies (the ‘cross-border’ effect). Further, we show that for emerging markets, the rise of the exports of services comes from the increase in volume of export of goods, which embed services and not because of an increased share of services embodied in the domestic value of exported goods (the ‘embodied volume’ effect). Finally, we show that the increase in services trade can be attributed to the increase in traded information technology (IT) services and not so much to that in financial and business services that are increasingly traded digitally across borders (the ‘plain vanilla digitalisation’ effect).

Introduction

Both the stagnation of trade in industrial products and the gradual increase in trade in services are among the most significant trends in world trade over the past 10 years. Another trend is the attention to trade through global value chains—see, for example, the World Development Report 2020 that focuses on this topic from a development perspective (World Bank, 2020)—which so far has paid limited analytical attention to the increased role of services in global value chains (GVCs). The rise of cross-border trade in services is especially observed in commercial services (Media, Telecom, information technology—IT, Finance and Other Business Services, which mainly relate to business consultancy) in which digitalisation plays an important role. As a case in point, the World Trade Organization (WTO) World Trade Report 2019 focuses exclusively on the increased importance of trade in services (WTO, 2019). In addition, digital operating platforms have enabled a further slicing up of the value chain over countries, increasing the number of traded goods and services between affiliates and affiliated outsourcing partners (Hummels et al., 2018). Although such digitalisation enables within the firm specialisation in headquarter services in developed economies, which are associated with knowledge capabilities, recently, there is a significant ‘Mathew effect’, where firms in emerging markets link, leverage and learn to become leaders in specialised services: India in business processes and China in artificial intelligence (AI) are eye-catching examples.

In this article, we analyse the drivers of the rise in trade in commercial services and thus comment on the underlying digitalisation of international trade. To do so, we draw on three trends in the analysis of trade flows. The first is to look at the domestic value-added components of trade instead of its gross value. Since gross trade flows do not consider the real value created in a country or industry, a focus on value-added trade would more clearly isolate the elements of comparative advantage and the income effects of international trade (Johnson & Noguera, 2017). The second trend is to make a distinction between services that are directly exported and services that are embodied in traded products and services. The latter is central to the extensive literature on global sourcing, which states that much of the trade we observe takes place within companies or is caused by the outsourcing of globally sliced production processes (Antras & Helpman, 2004; Antras et al., 2017; Grossman & Rossi-Hansberg, 2008). Not considering that services are used as inputs abroad and possibly exported again embodied in goods would exaggerate the ultimate effect of trade flows in supply and demand because of double counting. Therefore, when analysing trends in services trade flows, it is interesting to look at the difference between services that are consumed as an end product and services that are used as input. The third trend is the increased role of firms from emerging markets in global services trade, especially from Asia. Although much of the policy attention is on service liberalisation among developed economies, there are loud calls to action for emerging markets to open up for service industries. Such calls distract from the stylised fact documented in this article that emerging markets have become major exporters of services in their own right, so that they increasingly share the objective of a long overdue liberalisation of services trade and global coordination of regulatory harmonisation in service industries. 1

These trends have attracted the interest of researchers who, for example, try to explain the factors underlying overall trade in services, using the gravity model, with a focus on quantifying trade restriction in services (Nordas & Rouzet, 2017). Still, there is a research agenda to extend such quantitative analysis to include domestic value-added measures for trade in services and decompose the gravity effects across industries and country groupings. As noted, there is an emerging research agenda on embodied services (Los et al., 2015, 2016; Miroudot & Shepherd, 2016) but, so far, there is scope to improve on the Organisation for Economic Co-operation and Development (OECD) focus of this research by including a wider set of emerging markets to generalise the stylised facts. As we will see that services are an increasingly important element for emerging market economies by being embodied in trade in goods, this also calls to the fore the larger share of services value added in traded goods (servicification) as the so-called ‘Mode 5’ component of trade in services (Ariu et al., 2019; Cernat & Kutlina-Dimitrova, 2014). Moreover, there is an increased interest in documenting the policy restrictions on trade in services that are also important to analyse in the context of global digital integration. (Borchert et al., 2020; Ferencz, 2019; OECD, 2020). Increasingly, exporting and importing of services are not something that are exclusive for developed economies, but they are also increasingly important for emerging markets in Asia (ADB, 2017) and Latin America (Gonzalez et al., 2019). For Africa, the ‘Aid for Trade’ agenda puts an increasing emphasis on services to increase the value-added trade component of natural resources and agricultural products (Hoekman & Shingal, 2017; Roy, 2017; Shepherd, 2016). Much of this work is documented extensively in several surveys, and there are available overviews for theoretical backgrounds (Hoekman & Kostecki, 2009; Sauve & Roy, 2016). By combining value added data and bilateral trade flows at the country level over a substantial period of time, we provide stylised analytical facts on the trade in commercial services and thus on the dynamics of digital trade. We make use of the recent release of OECD’s Inter-Country Input–Output (IO) data set. ICIO provides high-quality data on an annual basis, based on official statistical sources, and, compared to alternative IO tables of similar quality, the most recent release of ICIO has covered a relatively large set of developing countries, which includes most major emerging economies in Central Europe, Southeast Asia and Latin America. ICIO documents not only the trade flows in goods and services that are used as final products but also the sourcing structure of domestic and traded intermediate inputs at the industry–country level. This makes it possible to link services to industrial production and thus identify the value-added services embodied in the exports of goods. This level of analysis is especially important because services are an important cornerstone of the debate in the renewal of the WTO, where questions arise on how to deal with complex value chain issues. Because the OECD database combines the observed trade flows in both industrial products and services with IO tables, it is possible to distinguish between value added that is generated by different domestic sectors and the gross exports of products of goods and services.

We present three main findings. The first is that especially for advanced economies, services are exported directly both to other developed economies and to emerging markets. Second, we find that direct export of services is increasing in emerging markets, but that it is complemented by a strong rise in exports of embodied services in goods. The first of two effects we call an ‘unbundling effect’, where more services are treated directly as separate (digital) service tasks and are less exported as embodied in goods. Second, there is an ‘embodied volume effect’ for emerging markets, where the strong rise in exports of manufacturing goods with embodied services increases the exports of commercial services. Third, we find that, although all services involving commercial services report rising exports, the IT sector has had the most spectacular increase, so that the ‘plain vanilla digitalisation’ effect of services through the IT sector has contributed most to the increase in trade in services globally. Although, recently, more data on services trade have been made available at the sectoral level, it is interesting to note that only a few comparative statistical analyses are available at the industry level.

With the increased digitisation of services and thus the supply across national borders as part of industrialisation 4.0, this article contributes by analysing the specific role of services in GVCs in more depth. The results of this article outlined earlier have important insights for both theory and policy practice. Many of the theoretical contributions in the field of GVCs in which IO tables are used show that added value is an important yardstick for measuring globalisation; however, little attention has yet been paid to the specific role that services play in this respect. We show that services deserve a bigger role in the analysis for GVC dynamics. We show that there are differences between developed and emerging regions in the extent to which services are traded as an end product or embodied in industrial products. Such divergent patterns are essential insights that highlight the non-linear relation between services trade and GVC participation with respect to economic development and thus informs about the rationale of differences in policy stances for services trade liberalisation across countries. In terms of policy practice, there is an emerging policy literature that revisits an old theme: participation in GVCs is of great importance for development (World Bank, 2020). However, internationalisation and participation in value chains cannot be achieved without a strong role for services that support this process. By analysing the contribution of services in the participation of GVCs, this article contributes to this policy discussion.

The remainder of the article is organised as follows: in the next section, we introduce the IO methods used for the service trade analytics, after which we introduce the data. In the third section, we will look specifically at added value trade and trade in intermediate products. Special attention is paid to the contrast with gross service trade, and the results are broken down for advanced economies and emerging markets. In the fourth section, we look in more detail at the differences between advanced economies and emerging markets, after which we split out exports for different sectors of commercial services. In the fifth and final section, we conclude the article by reflecting on the policy relevance of our findings.

Using Input–Output Tables to Focus on Domestic Value-Added Trade in Services

We derive domestic value added (DVA) by tracing the production process of a country’s export flow using IO analysis. Assume there are n industries in each country. The export flow of a country is denoted by a column vector E, with total n elements standing for the gross export from each industry.

2

This can be the total gross export to the world or bilateral gross export to a specific destination. The domestic IO structure is denoted by a so-called technical matrix A with the dimension of n x n. Each element Aij on row i and column j stands for the value of intermediate inputs from domestic industry i that are directly needed to produce $1 of gross output of industry j. To produce the gross export of Ej by an industry j, the intermediates demanded by each industry are given by A1jEj, A2jEj,…..AnjEj, respectively. In a matrix form, the intermediate inputs in producing the export flow are found by the matrix multiplication AE. The production process of these direct intermediate inputs will need other intermediates from upstream sources. Following the same logic, it can be seen that the required second tier upstream inputs is given by A(AE) = A2E , and third tier A3E, so on so forth. We are interested in the total of gross production by each industry that delivers the export flow of E, denoted by an n-element column vector yE. Summing up the last stage of production (i.e., E) and all production with regard to intermediates, we have:

Under weak conditions, it can be shown that the infinite sum of a matrix series converges to (I – A)–1, in which I is the identity matrix with the dimension of n x n. This is the famous Leontief Inverse (Leontief, 1953), and a sufficient condition for the summation to converge is roughly that the economic system does not need more intermediate inputs to produce outputs, which is safely satisfied for well-behaving IO databases. 3

We denote the value added to gross output ratio in each industry i by vi, which is the direct value added by the industry itself in producing $1 gross output. The DVA created by the sector in gross export is given by:

and the total DVA in gross export by the country is the sum of DV Ai over all i. When the summation is taken over by industries i that belong to the category of commercial business services, we obtain the service content in DVA. DVA from goods sectors and other services (like electricity and water supply, domestic transportation, etc.) can be derived in the same manner. Services DVA embodied in the export of goods can be derived by the same approach: instead of considering the gross export E by all industries, we consider only the gross export of goods sectors, EG, which has an element EG equal to Ei if an industry i is a goods producer, and zero otherwise. 4

Data: The Inter-Country Input–Output database

As mentioned in the introduction of this article, we use the latest ICIO from the OECD released in December 2018, covering 64 countries/regions as well as the estimates for the trade with the rest of the world (RoW) over the period from 2005 to 2015. The database contains most advanced economies and the important emerging markets, like the Brazil, Russia, India and China (BRIC) countries, all Central and Eastern European (CEE) of the EU and many of the South and Southeast Asian countries; a full list can be found in the data appendix. Such an extensive number of countries enables us to investigate the trends in trade in services from advanced to emerging economies and vice versa.

The databases that use the IO tables apply a classification of international trade by country and industry. Included are trade flows on the level of the country, whereas industries are classified according to the ISIC4 classification, rev. 4. The industries are classified at the two-digit level, but in some case, ISIC codes are pooled. For instance, the ‘Other Business Sector Services’ sector in ICIO includes the whole range of professional services from ISIC codes 69–82. The method does not identify the exact imports and exports as used in the IO table at an aggregate level. The main aim of using IO tables is to derive the DVA embodied in exports of each country, following the standard approach as in Koopman et al. (2014). DVA can be more informative than gross export flows since the latter contains the value of imported intermediates. Therefore, based on gross exports only, one cannot distinguish between two countries where one creates a substantial share of value added on its own when exporting, and another does only minimum processing on imported intermediates. Another advantage of using DVA is that we may identify the sector that created value added in gross exports. This is especially relevant for this article on services trade, since a share of services is not exported directly, but they are embodied in the exports of goods. An example is the value of software inside the exported electronics devices, which was created by domestic information and communications technology (ICT) services firms. Others are business consulting and financing services, which facilitate the business of a manufacturing exporter.

Global Trade in Services in Gross Value and in Domestic Value Added

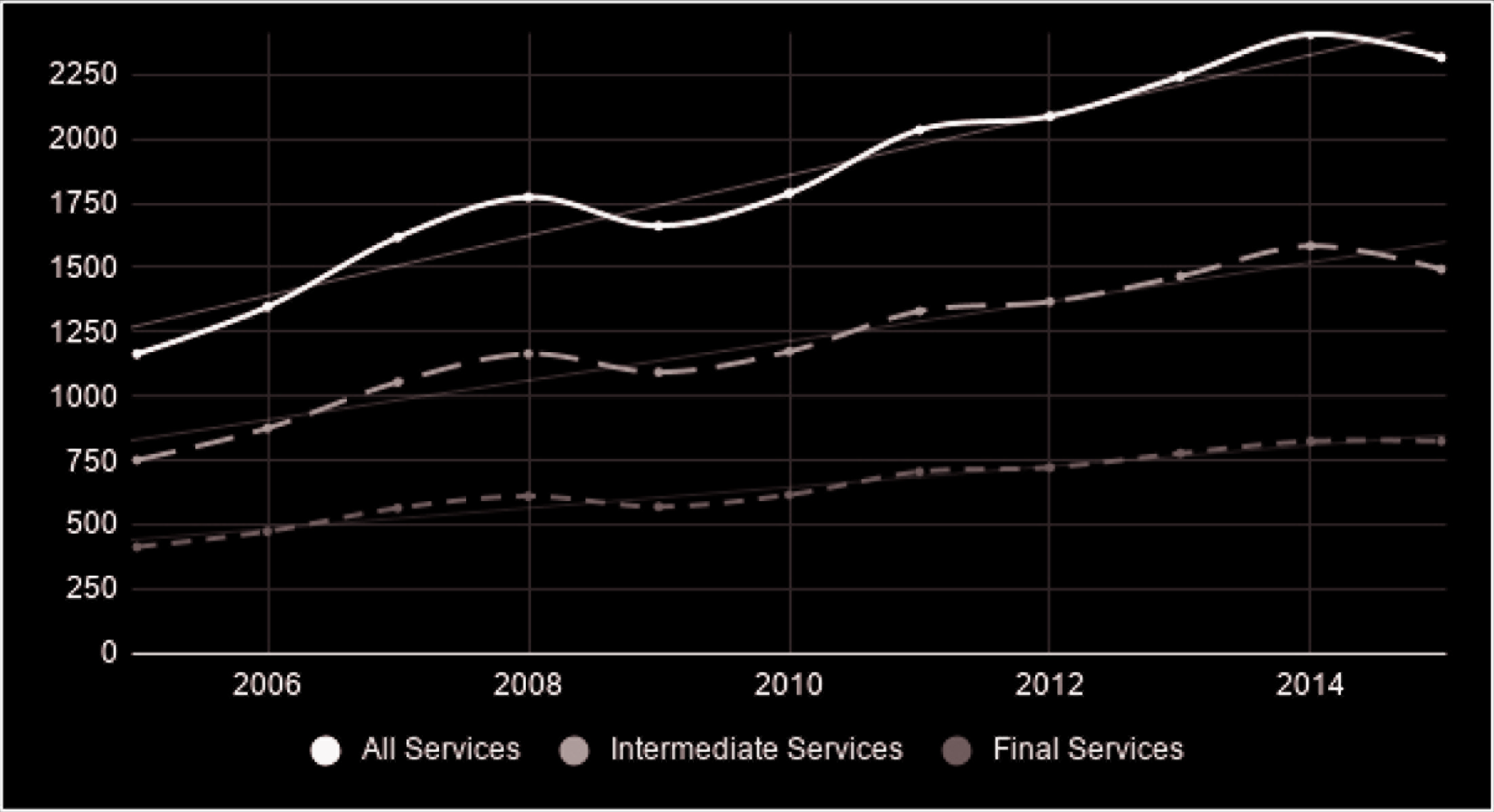

We start by examining the services trade of all countries in our sample in terms of export value, which is close to the world trends, given the country coverage. The left panel of Figure 1 analyses trends in trade in services in general, and the decomposition of trade in final services (consumed directly on foreign markets) and intermediate services as used in further production processes abroad. The top line shows that in overall services trade between 2005 and 2015, allowing for the hiccups of the financial crisis in 2008 and 2009, the trend is upwards. Decomposing all services trade, services exported directly are much lower than intermediate services used in other production processes, signalling the importance of services in GVCs.

b: Eatio services exports/goods exports

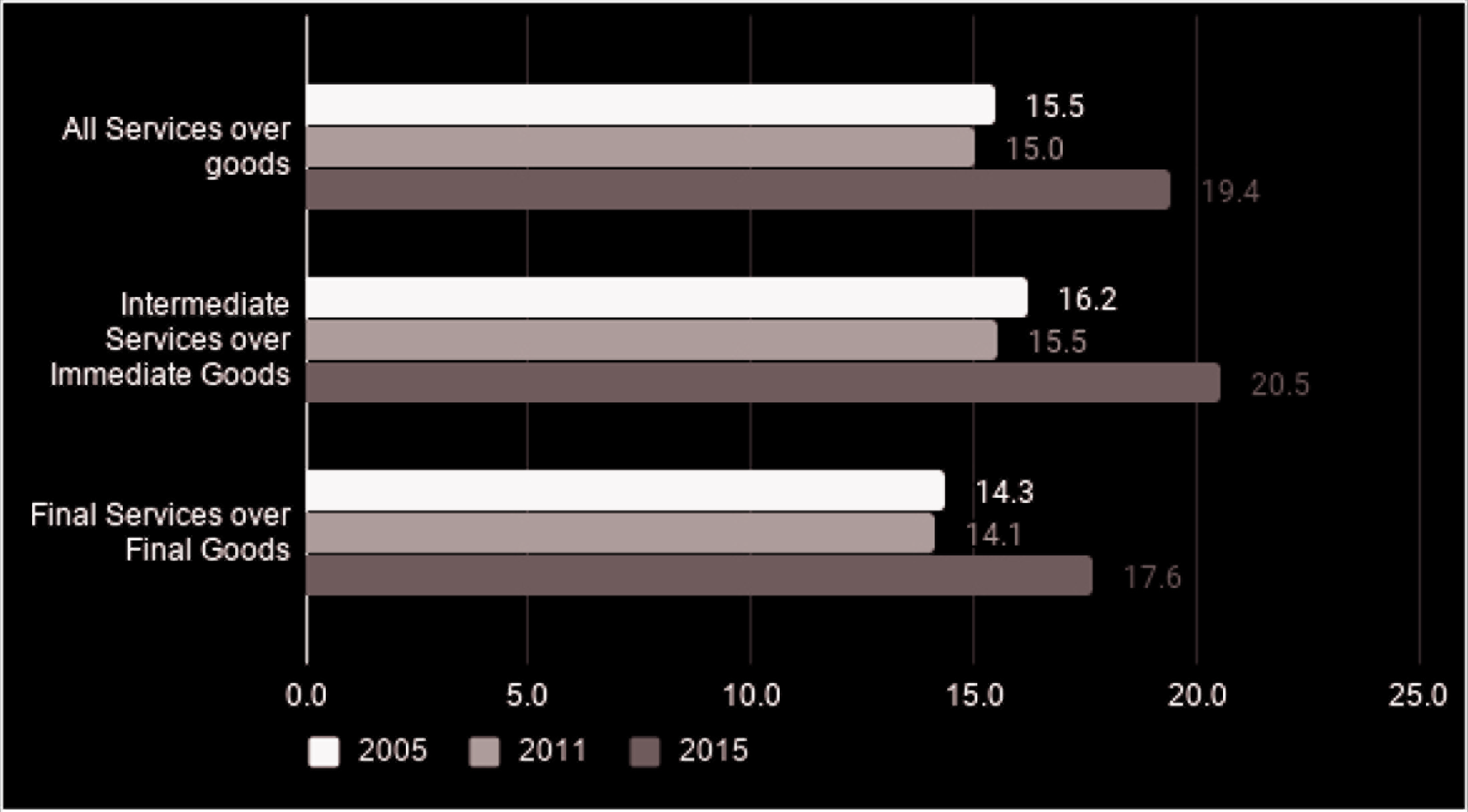

This finding of the importance of intermediate services is mirrored in the right- hand side of Figure 1. This bar chart is used to analyse whether services increase over time relative to trade in goods. The left-hand graph picks up a general time trend in expanding trade. On the right of the figure, the bar chart documents, in the top set of bars, trade in services as a ratio (%) to trade in goods in during the years 2005, 2011 and 2015, respectively. To begin with, we see that trade in services declines slightly in relative terms as compared to the period from 2005 to 2011, so we can conclude that overall trade in goods has grown faster than trade in services. The increased relative importance of trade in services worldwide is, therefore, a relatively recent phenomenon, shown in the substantial increase in the ratio between 2011 and 2015. 5 Interestingly, in the second and third sets of bars, we observe that the trends of intermediate services over intermediate goods and final services over final goods have a similar pattern. This reflects opposite movements of trade in goods as well. For intermediate services they go together with the rise in intermediate traded goods, both reflect the increased importance of global supply chains. Relative low growth in direct service exports used as final services goes together with low growth in world trade in goods. But for both sub-categories, the relative importance of services over goods traded increases in the more recent period.

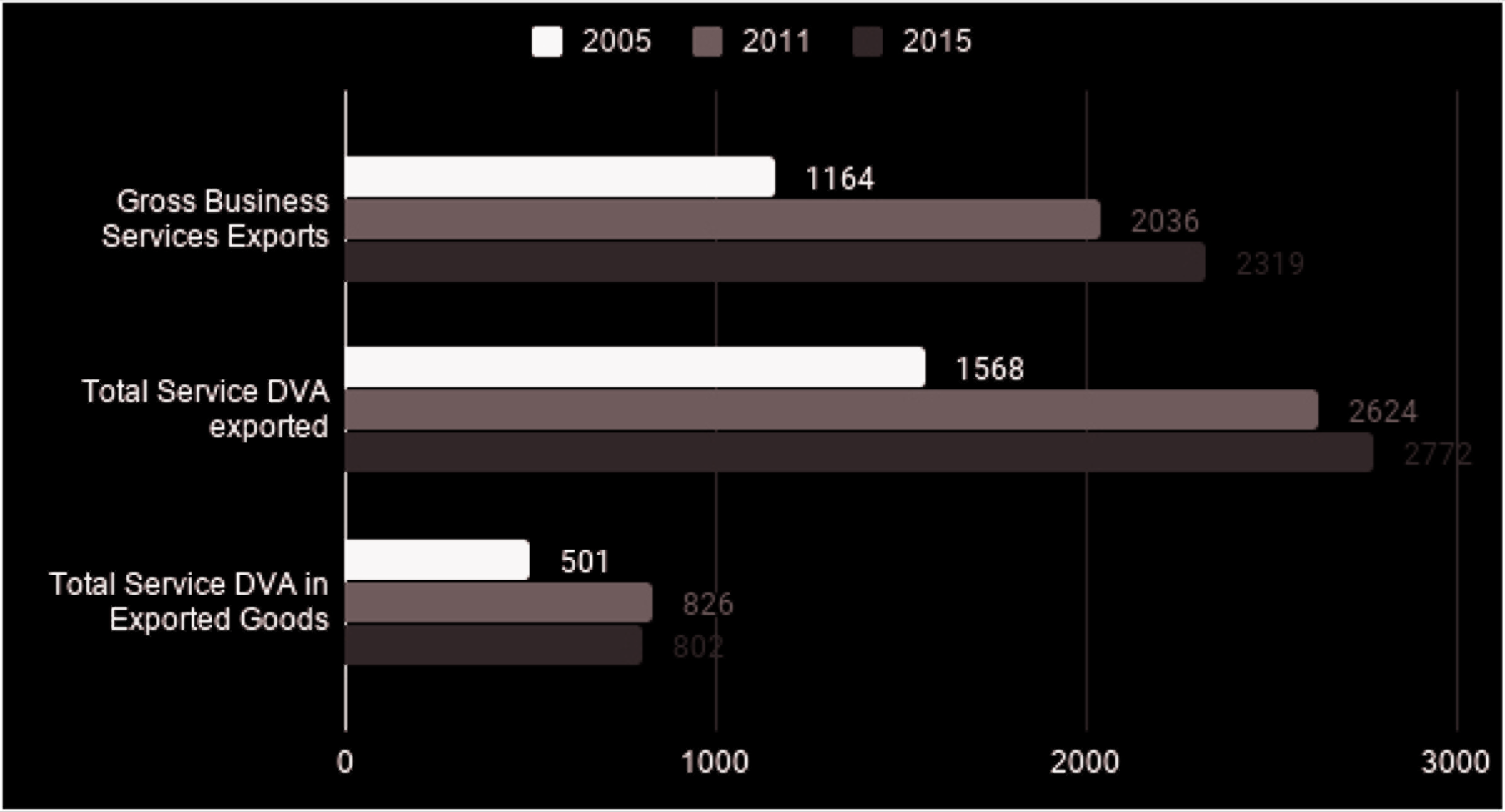

It is instructive to contrast the value of commercial services DVA exported in any form with the gross value of transaction accounts of services exports taken from the balance of payments. The former could not only be the services value added in the direct exports of final or intermediate services but also services embodied in other goods and services being exported.

Figure 2 presents three trends, of which two go against popular opinion. The first well-recognised trend is that, in reference to the top trio of bars, exports of services increase, as in Figure 1. Note that these service exports may be used as intermediate inputs in industries in foreign countries. The second bar trio shows the total services DVA, which is exported, of which some are exported directly as shown in the top bar trio. Because services are also embodied in the value chain in other exports, the value of DVA is higher than services exported directly. What is interesting to observe is that DVA of services between 2005 and 2015 has not risen as fast (from $1,568 to $2,772 billion) as commercial services exported (from $1,164 to $2,319 billion). This means that, globally, a lower share of exported services is embodied in other goods and services, and a higher share of services is exported directly. The bottom trio of bars shows the services that are embodied in goods exported. Between 2005 and 2011, the increase mirrors that of the increase in total DVA exported in the middle bars. However, for the years from 2011 to 2015, DVA in exported goods has declined. Hence, embodied DVA in services has shifted globally from embodiedness in goods to direct exports and services embodiedness in other services and other products like agriculture and natural resources. In the next section, we will see that these results are very different for advanced economies and emerging markets.

The general conclusion of this section is that, as in other studies, trade in services increases in both absolute and relative terms in total trade flows. We note that especially intermediate services used in production processes abroad have grown, but that this is especially the case before the financial crisis of 2008 and 2009. After the crisis, the importance of financial services trade increased, in particular, due to the export of advanced economies. Although services embodied in goods are an important phenomenon when analysing the export of services that amount to almost a third of all service DVA trade in the world, the importance of services embodied in goods for world exports has declining overall.

Splitting Advanced Economies and Emerging Markets

While the previous section analyses the dynamics of trade in services at a global level, there are substantial differences between advanced economies and emerging markets. It is, therefore, essential to break down the overall trends in trade in services as reported in the previous section into the statistics for advanced economies and emerging markets. 6 As the database is bilateral at the country level over industries, we can generate trade flows at the level of country groupings, while keeping track of bilateral flows at the level of industries to disentangle value added and intermediate services.

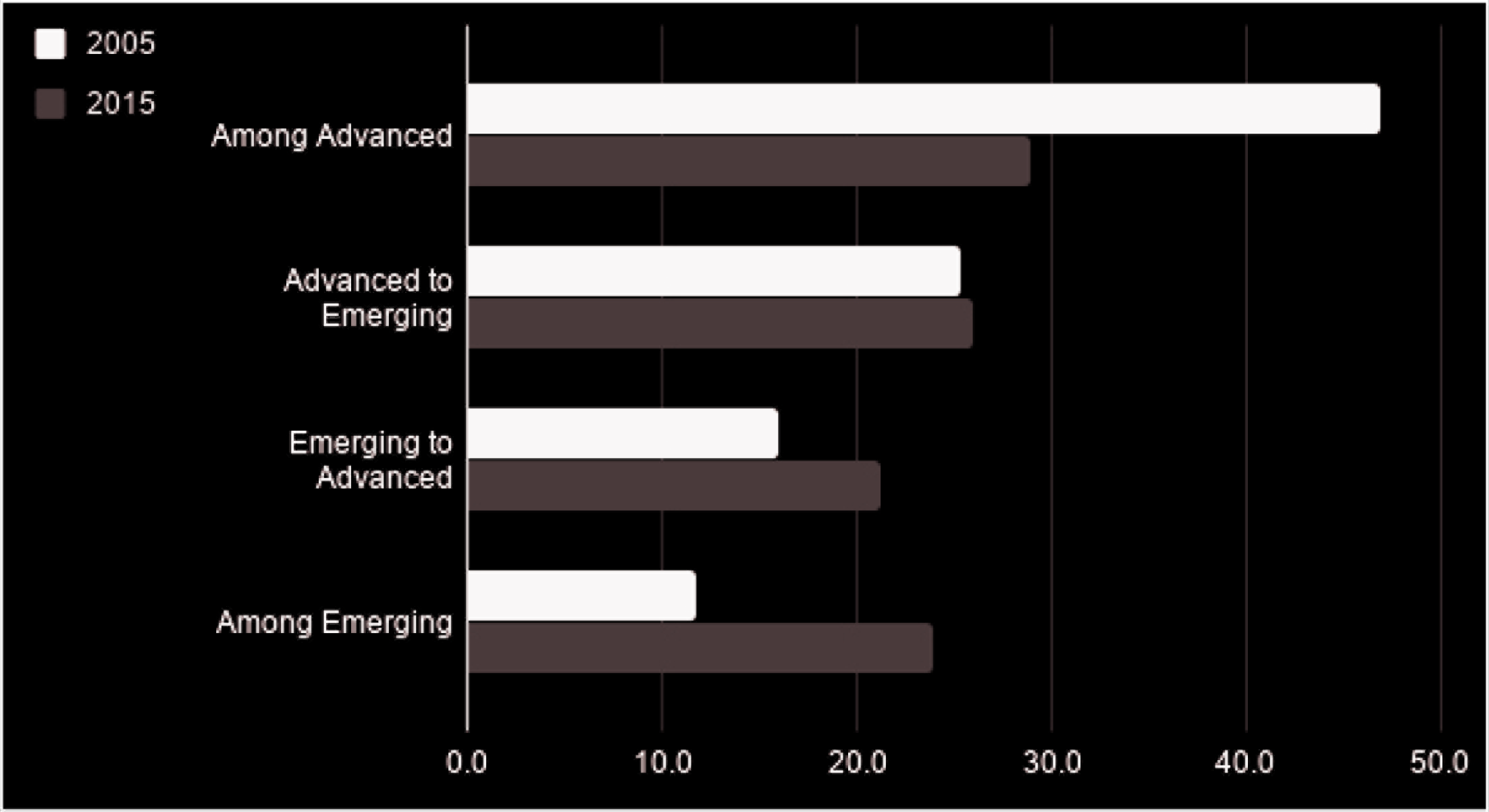

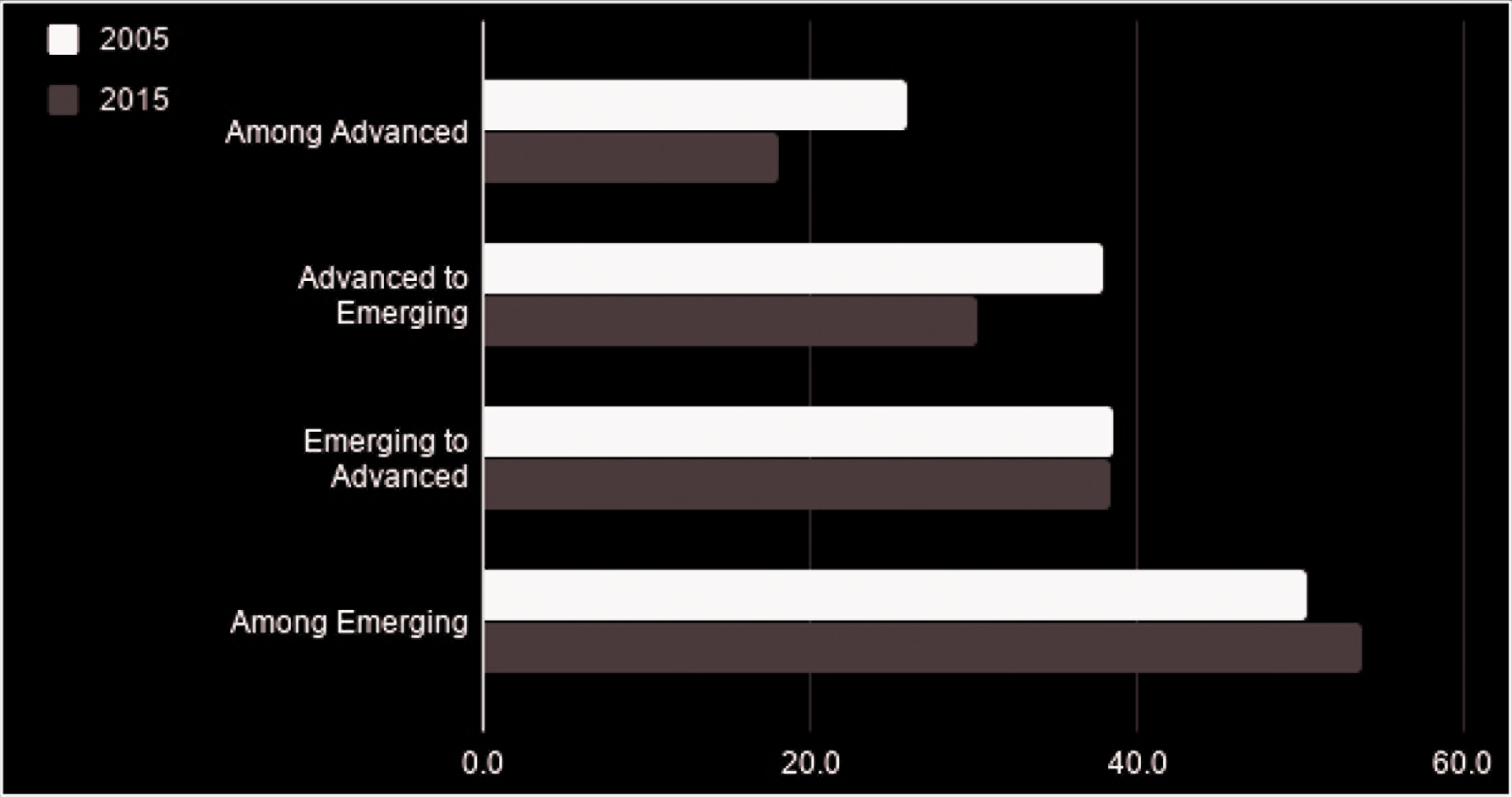

Figure 3 analyses the bilateral DVA service trade flows between the two country groups, advanced economies on the left-hand axis and emerging markets at the right-hand axis. As we can see, at first sight, trade flows between advanced economies are particularly large in current value terms, but they are also found to be increasing significantly over the period from 2005 to 2015. A second observation is that trade flows from emerging markets have increased rapidly, both in advanced economies and in emerging markets. Trade flows to advanced economies are the most important, both from other advanced economies as from emerging markets. A final observation is that, although still small in current value terms, trade in commercial services between emerging markets has rapidly grown in importance.

In the previous section, we documented that the difference between final and intermediate services is important when analysing trade in service flows. Moreover, when assessing Service DVAs, it is essential to distinguish between components of domestic trade in services that are directly exported and components of value added that are exported as domestic inputs embodied in exported goods. In fact, we find that the levels and the trends of the service DVA embodied in goods documented in the previous section differ significantly between advanced economies and emerging markets, analysed in Figure 4.

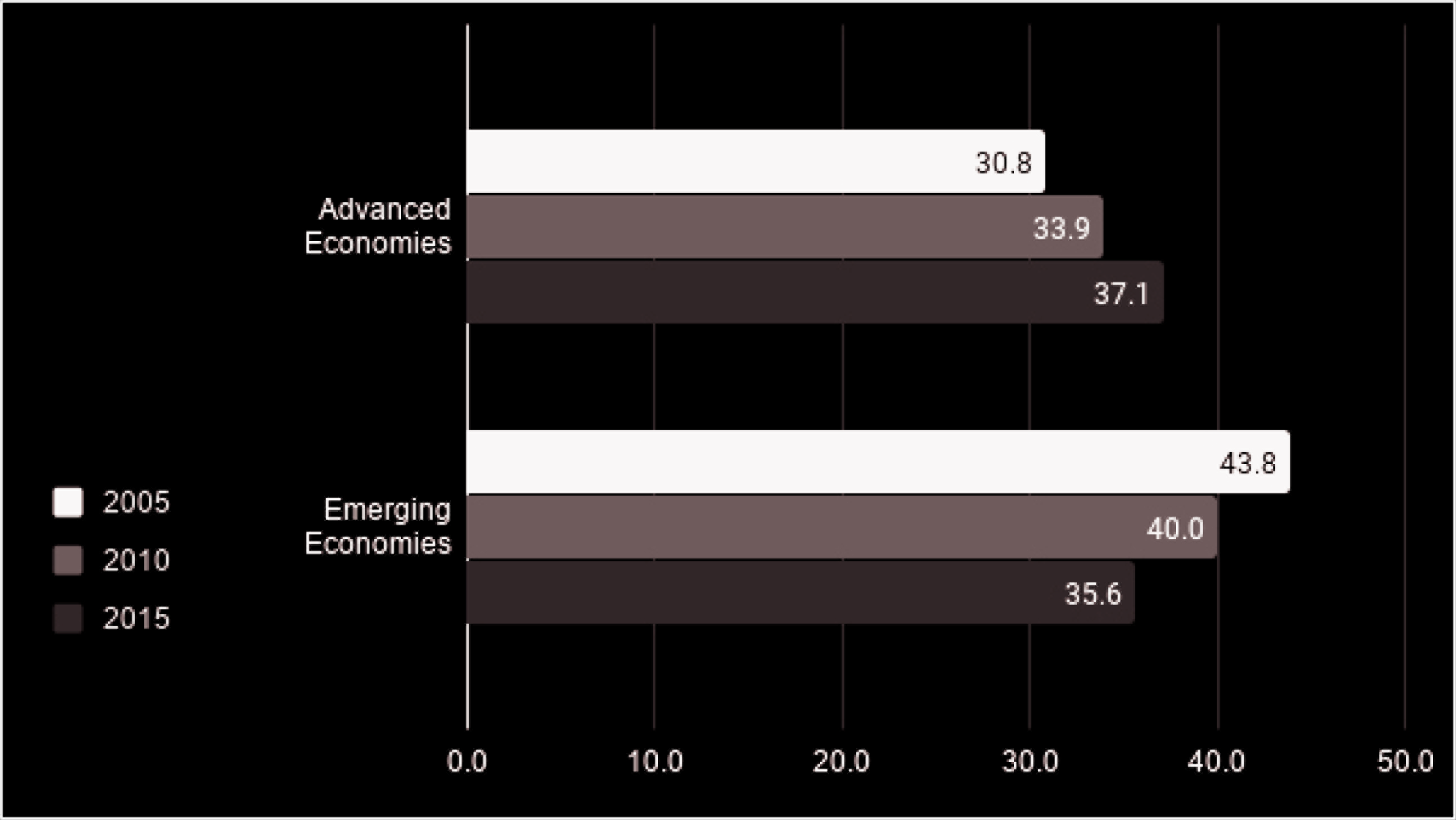

On the left side of Figure 4, we have mapped the dynamics in the world market shares of services embodied in the export of goods. In 2005, the trade between advanced economies dominated world trade of embodied service DVA. However, we see that this share has declined rapidly over time. In contrast, the importance of the indirect channel of services exports embodied in trade in goods has increased in the trade flows from emerging markets to advanced economies, and an even stronger growth is reported in the trade between emerging markets. We can say that services embodied in goods from emerging markets to advanced economies have replaced services embodied in goods in trade between advanced economies, and this is arguably the second most important driver of growth in world service DVA over the period under review. Through a decomposition analysis, we will show later that both the growth in the volume of goods exported and servicification, that is, an increasing share of services content in the value of exported goods, have contributed to the growth of embodied services exports from developing countries. To further illustrate these differences between country groups, Figure 4 on the right shows the shares of service DVA in total service export DVA that are embodied in the gross exports of goods. We note that service exports through the channel of goods is particularly important for the emerging markets, while the importance of these indirect service trade flows are less important for the advanced economies. Looking at the changes over time, we see that the embodied services component has become even less important for the export of services between advanced economies and from advanced economies to emerging markets. Embodied services have become less important for trade among emerging economies and have remained constant in the trade flows from emerging economies to advanced economies.

Share of services DVA embedded in goods as shareof total service DVA export

Interesting conclusions emerge when we combine the insights from Figures 3 and 4. Figure 3 shows that for advanced economies, commercial services exported DVA has increased over time. However, Figure 4 shows that the share of commercial services DVA embodied in goods for advanced economies has fallen, resulting in the conclusion that advanced economies in relative terms focus on exporting commercial services DVA directly. This rise in directly exported services DVA from advanced economies is the first most important driver of the overall increase in global exported services DVA. Figure 3 also shows a sharp increase in exported services DVA from emerging markets both towards advanced economies and among themselves. In Figure 4, we see that the share of services embodied in goods has increased in emerging markets, especially because of the sharp increase in the volume of goods exported. This is the second engine of the export of services, that service DVA from emerging markets have increased by being embodied in the rising volume of exported goods.

A potential caveat that would overstate the domestic services embodied in exported goods in emerging markets is whether these services are provided by domestic producers or whether they are from foreign affiliates. However, it is possible to estimate the imported service content in the exports of goods to assess the importance of GVCs in services. 7 To be more specific, we slice up the global production chain of exported goods by emerging market following Beverelli et al. (2017) and trace not only the domestic content but also the value-added contributions by foreign countries and industries where the value added is created. Figure 5 shows the dynamics of foreign commercial service content in the export of goods in both advanced and emerging economies.

A remarkable result of this decomposition is that the share of foreign service inputs in the total number of commercial services, which is embodied in the export of goods from emerging markets, decreases over time. While this may lead to the quick conclusion that over time, domestic providers become more important than imports in the domestic services value added in exported goods export of emerging market economies, it should be taken into account that the IO data set is constructed on a territory basis, such that foreign-owned subsidiaries are in fact counted as domestic service producers. The replacement of imports of services by the establishment of subsidiaries for the localised production of services can be substantial in countries like China. In contrast to the pattern of the emerging markets, the increase in services supplied from abroad in trade flows coming from advanced economies is noteworthy. It relates to a combined effect of a diversification of service as inputs among the advanced economies, and an increasing service offshoring to emerging markets or the foreign-owned subsidiaries there.

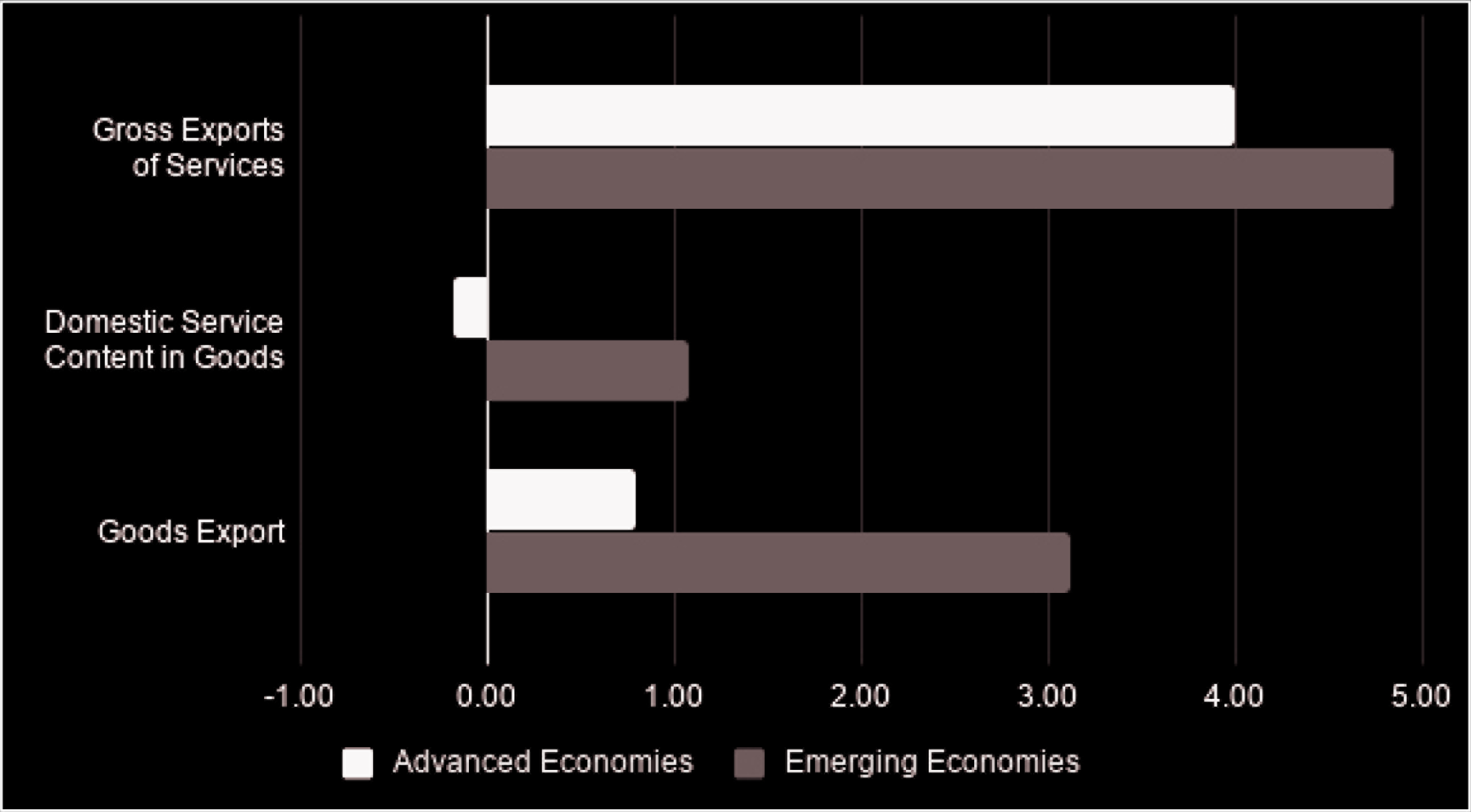

The advantage of using IO tables and thus value-added components of international trade in services is that the sources of growth in commercial services can be broken down for the two groups of countries. So far, there is evidence that services consumed and used as intermediate inputs directly abroad, in particular, are the main driver of the growth of services trade for advanced economies. For emerging markets, trade in services grow mainly through its embodied components in the export of goods. The latter embodied element has two subcomponents. The first is that exports of these services will increase as exports of manufactured goods increase, especially in intermediate products. The second component is that domestic services are a more substantial component of the inputs of exported goods than other inputs.

Figure 6 presents the growth of the exports of commercial services DVA by advanced economies and emerging markets into separated components to provide a picture of the importance of the aforementioned drivers. We decompose the total growth of service DVA into three components: growth due to an increase in the gross exports of services and the services content embodied in the exports of goods. The later embodied service DVA growth is further broken down into two parts: the growth in service intensity, that is, a deepening of domestic service content in the value of exported goods and the growth in the volume of goods exported.

For emerging markets, on the other hand, all three components contribute positively to the overall average annual growth rate of 9%. The direct exports of services are the largest part contributing to this growth, of which we know that the exports of intermediate services play an important role. In contrast to advanced economies, close to half of the increase in the exports of commercial services DVA stems from the embodied services content in exported goods. This is not only because of a rapid increase in the volume of goods exported by the developing countries we also find that the domestic service intensity is increasing. The goods exported by developing countries contain a higher share of domestic service content, which may originate from an increasing degree of servitification in the domestic supply chain of the emerging markets. But it is also likely that foreign services inputs are being replaced by foreign-owned affiliates in the domestic country.

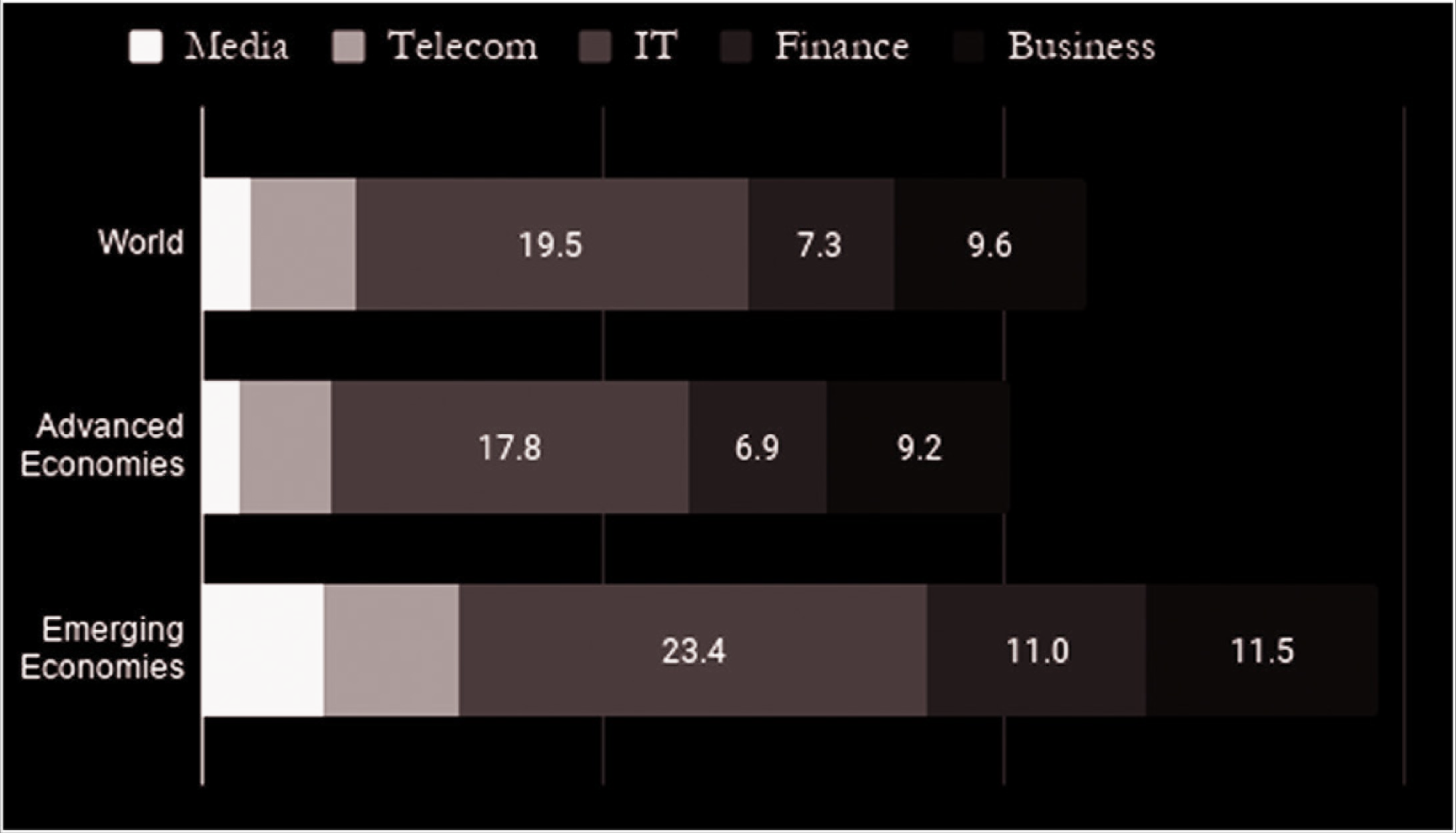

Commercial Services Industries

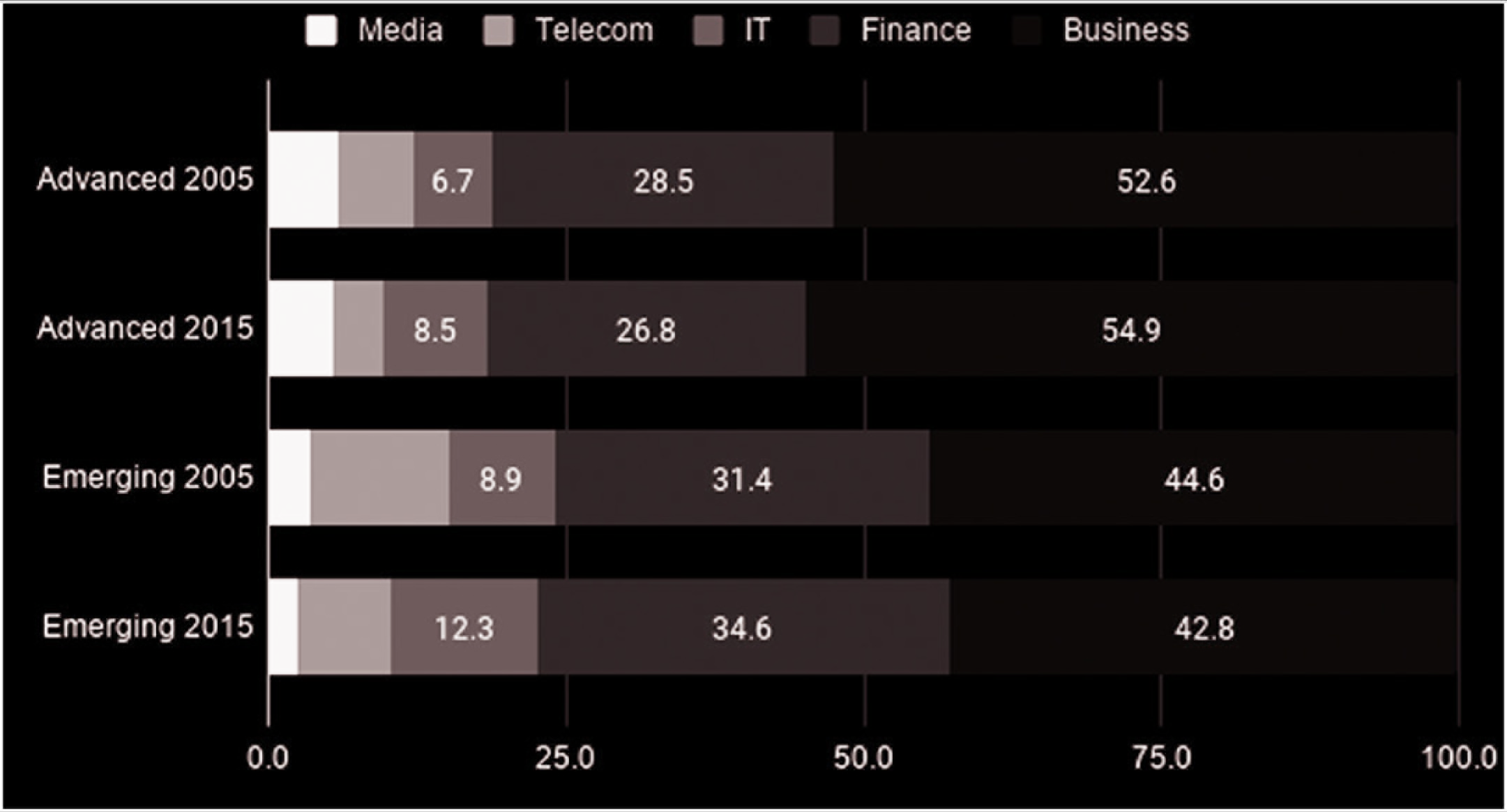

The subtheme in this section is to break down total trade in commercial services into five sectors representing the two-digit ISIC codes for trade in ICT services, finance and insurance, business services (including management consulting, accounting and legal services), telecommunications and media. Figure 7 on the left-hand side zooms in on the breakdown of services DVA in the world trade by industry and country of origin, and the right-hand side shows the average yearly growth rates. We have chosen to present the data by giving an index for the year 2005 and 2015, showing that trade in financial and business services is much higher in absolute terms than the other three sectors.

Average yearly export growth by commercial services sector

The results show a very substantial rise in international trade in IT services. Overall, the exports of IT services increase by 19% on an yearly basis, and the growth is more substantial in emerging markets, with an annual growth of 23% as compared to 17% increase in advanced economies. This comes from the effects of digitalisation over the time because IT services have substituted telecommunication services as Internet services are have replaced the more traditional coordination mechanisms between organisations. Another explanation is the rapid increase in the offshoring in this period of the software industry, particularly to China and India. Furthermore, it is interesting to note that for advanced economies, the share of financial services export has fallen relative to other business services, whereas, for emerging markets, the effect is the opposite. There is little growth in cross-border trade in telecommunication and media. 8 However, the time periods that we are analysing is pre-streaming so that the recent platform internationalisation of companies like Netflix and Disney in media are not taken into account. If we look at the next 10 years, we can expect to see a spectacular increase in media services traded coming from advanced economies.

We see a substantial increase in the importance of the subcategory ‘IT services’ in the total traded commercial services we call the ‘plain vanilla effect’ because IT services are the basic element of digital trade that is subsequently sourced into other forms of services. However, we can observe that ‘software is eating all industries’, and that it is difficult in the age of AI to distinguish between IT services and management consultancy—see the likes of IBM and the increasing dominance of Accenture in management consulting—and probably also between IT services and financial services—the rise of Ant Financial and Alipay coming from Alibaba and Apple and Google Pay. And because media platforms like Netflix are run by deeply intelligent algorithms, it may be increasingly difficult to put walls around the IT sector when contrasting them with media services. So, it may be that many commercial service industries will become ‘plain vanilla plus’ IT services, and if so, the time frame up to 2016 that we are considering simply shows the first signs of the trend of things to come. In other words, the rise in IT services, together with the moderate rise in other services, simply shows that the digitalisation of services trade will substantially increase the cross-border offerings of all commercial services.

Concluding Comments

In this article, we have documented trade in commercial services DVA for the period from 2005 to 2015. We have focused on DVA components of services to include the most recent discussions on the importance of services trade. It is not simply direct exports of services but also services embodied in goods that shape the dynamics of service trade globally, and we have seen different patterns of services trade across advanced economies and emerging markets. For both groups, direct exports of services have increased dramatically, but they are more pronounced in the share of total service trade for advanced economies. For emerging market economies embodied in the exports of goods are an important component, especially because goods exports are rising fast. Not only towards advanced economies are these exports increasing, emerging markets are part of the trade web among themselves and towards developing economies. In addition, we have documented the primacy of trade in IT services that increases sharply over time, which we attribute to a ‘software eating the world’ phenomena in which others like financial services and business services are being consumed by IT services.

Although this article does not deal directly with digital trade in services, it does provide several starting points on which to build. It is to be expected that digitisation will mainly affect commercial services across national borders, so that digitisation will be an enabler that will further integrate commercial services into GVCs. The finding that it is especially the IT services that have increased dramatically in terms of exports share over time period considered is evidence that, increasingly, software is eating the world, and, more broadly, that data are being used to run the world. We point to substantial difficulties in measuring and especially splitting IT services from other digitally traded services in finance and management accounting. And we may anticipate that, in current times and even more so in the near future, the distinction between IT services and media will disappear. The result will be that data will drive almost everything and that the policy agenda on digital trade will be the most important element of future WTO negotiations accordingly. We already see that the digital trade component in the current free trade agreements creates headaches and that especially issues such as how to deal with universal privacy considerations provide for substantial differences in opinion among the major trading blocs. These discussions on digitalisation of financial services, consultancy and media, and especially the merging of those industries based on AI, also create a lively debate about the international taxation of data flows. Although countries have different trajectories of development of digital trade in services, this article suggests that the issue has gained increasing importance for all countries considered.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.