Abstract

Previous studies have examined gender differences in environmental disclosure and corporate environmental responsibility, which are elements used to measure greenwashing. However, little attention has been given to the impact of firm leaders’ gender on greenwashing. This study applies a logit econometric model to estimate the probability of being greenwashers for female-led firms compared to male-led firms, using a sample of 7,870 private firms from 28 countries. Our main results suggest that female-managed firms are not less likely to conduct greenwashing. This study also evaluates the impact on greenwashing of other determinants, such as access to finance, firm size, pollution degree, and region, and whether the gender gap in greenwashing is attributed to the primary drivers of greenwashing. Finally, we draw implications from this study on how to enhance the credibility of environmental initiatives for both female-led and male-led firms.

Introduction

Stringent environmental regulations and the growing environmental concerns of stakeholders have been motivating firms to implement environmental initiatives. Corporate environmental responsibility (CER) further affects financial performance (P. Li et al., 2021; Zhang & Xie, 2021), access to financing (Wellalage & Kumar, 2021; Zhang, 2021; Zhang et al., 2022), and market values (Bolton & Kacperczyk, 2021; De Haan et al., 2012; Y. Li, 2017). However, in practice, empirical studies provide mixed findings regarding the benefits of CER. Firms convey their environmentally responsible activities through environmental information disclosure to meet stakeholder demands. Firms may selectively disclose positive environmental actions while concealing negative ones, indicating a form of greenwashing. Therefore, stakeholders may doubt the credibility of firms’ environmental performance, which negatively affects customer satisfaction (Ioannou et al., 2023) and investor confidence in firms’ greenness (Delmas & Burbano, 2011; Gatti et al., 2021). 1

Organizations tend to reveal benign performance indicators as a symbolic strategy to create a misleading and impressive overall performance (Bromley & Powell, 2012). In response to environmental regulations and stakeholders’ environmental concerns, firms may advertise environmentally friendly images (Clarkson et al., 2008; Du, 2015; Janssen et al., 2022), disclose environmental and other social responsibilities to pose as environmental performers (Mahoney et al., 2013), or selectively report their environmental impacts to mask the actual performance (Ioannou et al., 2023; Marquis et al., 2016). In some extreme cases, poor environmental performers may adopt environmental disclosures to boost their environmentally responsible activities (Doan & Sassen, 2020).

Firms’ symbolic strategies outlined above refer to greenwashing, meaning that firms selectively disclose positive environmental performance for green marketing while withholding deviations from environmental regulations (Bromley & Powell, 2012; Du, 2015). 2 In other words, greenwashers overcommit their promised environmentally responsible actions. As an organizational strategy, greenwashing behavior may vary across firms with different gender compositions. While much attention has focused on gender differences in CER and environmental disclosures (J. Li et al., 2017; Liao et al., 2015; Liu, 2018; Tingbani et al., 2020), little research has been dedicated to gender differences in greenwashing, which is measured through a comparison of environmental disclosures and CER.

In this study, we are to evaluate the determinants of firms’ greenwashing behaviors and whether there are gender differences. The potential determinants include access to finance, firm size, pollution degree, region, and other firm characteristics. For the gender gap in greenwashing behavior, we posit that female-managed firms are less likely than male-managed firms to adopt greenwashing behaviors, which is drawn from various overarching theories. Female leaders’ gender characteristics influence their prosocial behavior and public-oriented attitudes under gender socialization theory (Beutel & Marini, 1995; Eagly & Johannesen-Schmidt, 2001), which may bring a common value to the top management team and affect organizational outcomes according to the upper echelon theory (Hambrick, 2007). However, the obstacles to achieving effective leadership in organizations as demonstrated by the evolutionary leadership theory (van Vugt & Ronay, 2014) and implicit leadership theories (Offermann et al., 1994) may distort the link between firm leaders’ gender and greenwashing.

Using firm-level data covering 28 countries from the World Bank Enterprise Surveys conducted in 2019/2020, our empirical results indicate that exporters and firms with foreign ownership or environmentally concerned customers have a lower probability of greenwashing; the opposite is true for small and medium-sized firms or firm in a completive market. Firms with experienced top managers or with top managers who communicate with other managers more often conduct less greenwashing behavior. We do not find evidence that female-led firms are less likely to be greenwashers. For some regression results, female-led firms are even more likely than male-led firms to be greenwashers. We further investigate whether the greenwashing behavior of female-led firms depends on firms’ financing access, firm size, the industries to which they belong, and the regions in which they are located.

This study is probably the first to explore the impact of firm executives’ gender on greenwashing and then contributes to the literature in several ways. First, previous studies have examined the differences in environmental behavior between female-led and male-led firms regarding environmental activities (Bannò et al., 2023; Liu, 2018) and environmental information disclosure (Liao et al., 2015; Tingbani et al., 2020). This study is first motivated by the absence of research on gender differences in the consistency between environmental activities and disclosing, an indicator of greenwashing. Second, researchers have evaluated the impact of firm-level factors, industries, and country institutional settings on greenwashing (Marquis et al., 2016; Yu et al., 2020; Zhang, 2022a, 2022c). For each of the foregoing dimensions, we explore the differences between female-led and male-led firms. Thus, our study reveals the channels through which firm leaders’ gender affects greenwashing behavior. Third, our study explores greenwashing behavior of private firms and hence differs from previous studies, which usually use large, listed firms (Ioannou et al., 2023; Marquis et al., 2016; Yu et al., 2020; Zhang, 2022a, 2022c). Finally, this study modifies greenwashing measures used in past literature by taking industry heterogeneity into account.

Related Literature

This section briefly reviews past studies on the drivers of greenwashing and theories explaining gender differences in environmental behavior.

Although a symbol strategy taken by a firm to selectively disclose beneficial environmental information lies behind greenwashing (Bowen & Aragon-Correa, 2014; Marquis et al., 2016), the specific drivers of greenwashing behavior vary across firms, industries, and countries. In general, green practices target meeting the stakeholders’ requirements and then gaining benefits, such as saving costs and increasing revenue, easing credit constraints, and increasing market values. People may suspect that the primary purpose of firms’ green practices is to gain benefits like saving costs (Kim et al., 2022). Among firm-level determinants, firms’ credit-constraint condition is one of the factors influencing greenwashing (Zhang, 2022a) due to financial institutions’ consideration of environmental risk. Heavy polluting firms are less like to engage in selective disclosure because of stringent regulations (Marquis et al., 2016). However, Zhang (2022c) documents that heavily polluting firms are more likely to be greenwashers because of green finance regulations. Greenwashing may vary across countries depending on diverse institutional settings. Firms in a country that follows strictly global norms are less likely to selectively disclose environmental and other social responsibilities (Marquis et al., 2016). A less corrupted country system prevents greenwashing behavior (Yu et al., 2020). The above drivers of greenwashing are probably subject to firm gender composition, noting the documented gender gap in CER and environmental disclosures in the literature (Liao et al., 2015; Liu, 2018; Tingbani et al., 2020), which are elements used to measure greenwashing.

Researchers have investigated environmental practices in conjunction with gender issues under a variety of overarching theories. Generally, identity ascribed from personal demographic characteristics, such as gender, race, or ethnicity, renders individuals and environmental issues inseparable (Dawkins, 2015). Under social role theory, women and men differ in personal characteristics, such as role-taking capacities, empathic or sympathetic responding, moral responding, and internalized values and norms, which affect their prosocial or altruistic behaviors (Beutel & Marini, 1995). Since women express more of their concerns and responsibility for the well-being of others than men, they are the primary providers in jobs that require social skills to provide socioemotional support (Marini, 1990). Moreover, from the perspective of gender socialization theory, agentic, and communal characteristics are ascribed to men and women, respectively, due to their respective values and social expectations from society’s dominant culture (Eagly & Johannesen-Schmidt, 2001; Xiao & McCright, 2015). While agentic characteristics are associated with assertive, controlling, and confident features, communal characteristics primarily describe a concern for others and their well-being. In brief, females tend to be aware and caring regarding the needs of others and then carry out an ethic of care that values accountability and relationships. Those prosocial or pro-environmental attitudes are crucial antecedent to relevant intentions and behaviors (Miller et al., 2022).

On a firm’s basis, organizational outcomes are based on executives’ personalized interpretation of the situation they face, which are a function of executives’ experience, values, and personalities under upper echelon theory (Hambrick, 2007). Thus, organizational outcomes are associated with the personal characteristics of the top managers who bring a cognitive base and a particular set of values to the top management teams. Specifically, upper echelon characteristics of individual executives are highly important for firms in developing countries where the executives have a strong influence on strategic actions due to leadership style, culture, and the lack of corporate governance (Hewa Heenipellage et al., 2022). As such, female executives may contribute to values shared among top management teams, which motivates firms to engage in effective environmental practices (J. Li et al., 2017). This is also in accordance with the diverse theory (Siciliano, 1996). According to this framework, the diversity in a firm’s leadership benefits its decision-making process since top managers contribute to strategic actions by incorporating resources into the firm resulting from their divergent backgrounds.

Researchers have provided empirical evidence supporting theoretical expectations that female leadership exhibits stronger environmental values and attitudes. For example, firms with greater board gender diversity do not often violate environmental regulations (Liu, 2018). The empirical studies of Liao et al. (2015) for US-listed firms and Tingbani et al. (2020) for UK-listed firms confirm a positive relationship between the percentage of female directors on the board and the propensity to accurately disclose greenhouse gas emissions.

The critical role of female leadership in firms’ greenness may reflect female executives’ influences in the decision making process. On the other hand, the relationship between female executives and greenwashing is probably subject to firms’ organizational structure. Moreover, the obstacles to achieving effective leadership in organizations may distort the linkage between firm leaders’ gender composition and greenwashing behavior. According to evolutionary leadership theory, leadership and followership evolved to solve recurrent coordination problems that two or more individuals face, which depends on how leaders seize the initiative and then how others follow them, as stated in van Vugt and Ronay (2014). They further point out the difficulty of overcoming the “think leader, think male” biases. Masculinity is one of the primary dimensions of implicit leadership theory (Offermann et al., 1994), which may affect leadership effectiveness. For example, there is direct evidence suggesting that female relationships are characterized by greater emotional intimacy (Beutel & Marini, 1995 ). Followers may evaluate leader sensitivity negatively and link it to weak leadership (Offermann et al., 1994), influencing the achievement of social welfare.

Since greenwashing is measured through a comparison of CER and environmental disclosures, an issue is whether female managers disclose more environmental information than their environmental commitments. Besides organizational-level drivers, individual-level drivers such as optimistic bias also play a crucial role in greenwashing (Gregory, 2023). It is emphasized in social role theory that males are typically more overconfident than females (Eagly & Johannesen-Schmidt, 2001). Theoretically, females value accountability and perceive them as more reliable (Beutel & Marini, 1995), indicating that female leaders may seek a corporate constituency with integrity. In addition, females tend to be risk-averse and are often associated with less risky firms (Faccio et al., 2016). As such, the probability of selectively disclosing environmental performance is probably lower for female-led firms than their counterparts, noting the negative consequences of greenwashing (Delmas & Burbano, 2011; Gatti et al., 2021; Ioannou et al., 2023).

Data and Methodology

Data Sources

The World Bank Enterprise Surveys (WBES) provide data on the business environment for firms in most developing countries and some developed countries for comparison. The sample comprises firms in the non-agricultural private economy. For each sample country, quotas on region, industry, and firm size were applied to ensure representativeness.

The latest wave of WBES (2019/2020) covered firms in Central and Eastern Europe and Central Asia and included a Green Economy Module on firms’ green management practices. Researchers have used the WBES data to explore the gender gap in capital markets (Hansen & Rand, 2014; Wellalage et al., 2019) and the Green Economy Module to investigate the relationship between CER and financing (Wellalage & Kumar, 2021; Zhang, 2021; Zhang & Wellalage, 2022) and the moderating role of firm gender composition in this relationship (Zhang et al., 2022).

We select private firms from the latest WBES wave as our sample. Totally there are 7,870 firms covering 28 countries, which are member states of the European Union (EU), other Central and Eastern European countries (CEE), the Commonwealth of Independent States (CIS), or from other regions. See Table A1 in the Appendix for the sample distribution by country and industry.

Key Variables

Following previous literature (Yu et al., 2020; Zhang, 2022a, 2022c), we measure greenwashing scores based on the inconsistency between a firm’s environmental information disclosures and its environmental actions, which reflects a gap between symbolic and substantive actions (Siano et al., 2017). Specifically, greenwashing scores are measured by the gap between environmental disclosure (ED) scores and CER scores, both relative to their respective peers.

In the surveys, firms reported whether they had conducted environmental disclosures and environmentally friendly investments over the last 3 years. Although the reported environmental activities are probably executed in different years, the impact of gender stereotypes on environmental behaviors may not change drastically over a short time frame. Environmental disclosure information is based on the survey questions about whether firms completed an external audit of energy consumption, CO2 emissions, water usage, or other pollutants. 3 A firm’s ED score equals the ratio of the number of environmental disclosures to the total number of environmental disclosures.

In the surveys, firms reported whether they invested in 10 environmentally friendly measures, including heating and cooling improvements; more climate-friendly energy generation on site; machinery and equipment upgrades; energy management; upgrades of vehicles; improvements to lighting systems; air pollution control measures; water management; waste minimization, recycling, and waste management; other pollution control measures. Of them, six measures are related to energy consumption, reflecting the important role of energy-related carbon emissions in firms’ environmental impact (Dangelico & Pontrandolfo, 2010). A firm’s CER score is a ratio of the number of environmental protections the firm adopted to the total number of measures.

Both ED scores and CER scores depend on industrial sectors and then are less comparable across sectors. Accordingly, we normalize firm-level scores by using the industrial-sector-level means and standard deviations (

Finally, we set a dummy, Greenwashing, which equals 1 for firms with a positive greenwashing score (greenwashers) and 0 otherwise.

For the gender variable, FMF (female-managed firms) equals 1 for firms with female top managers and 0 otherwise.

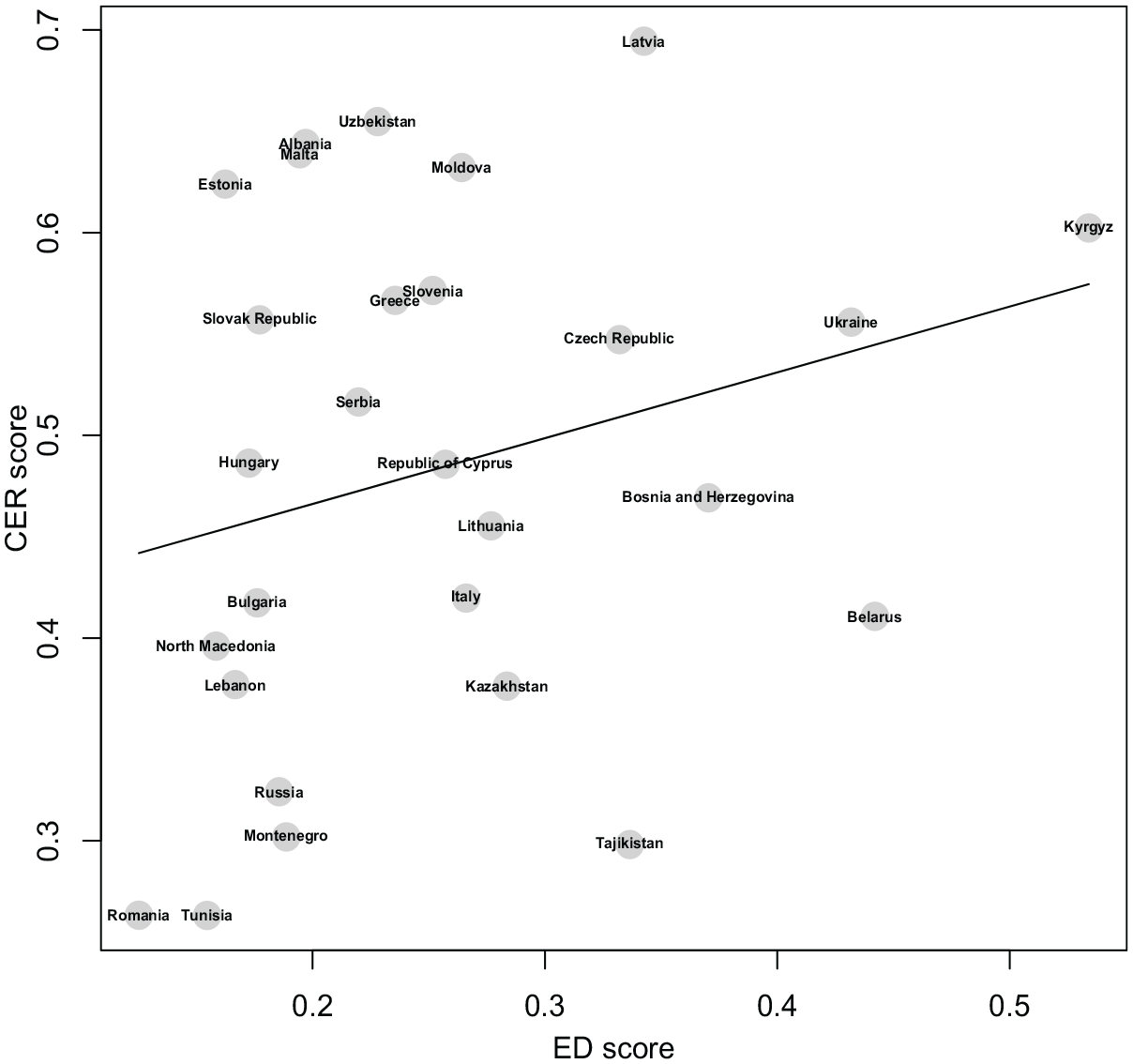

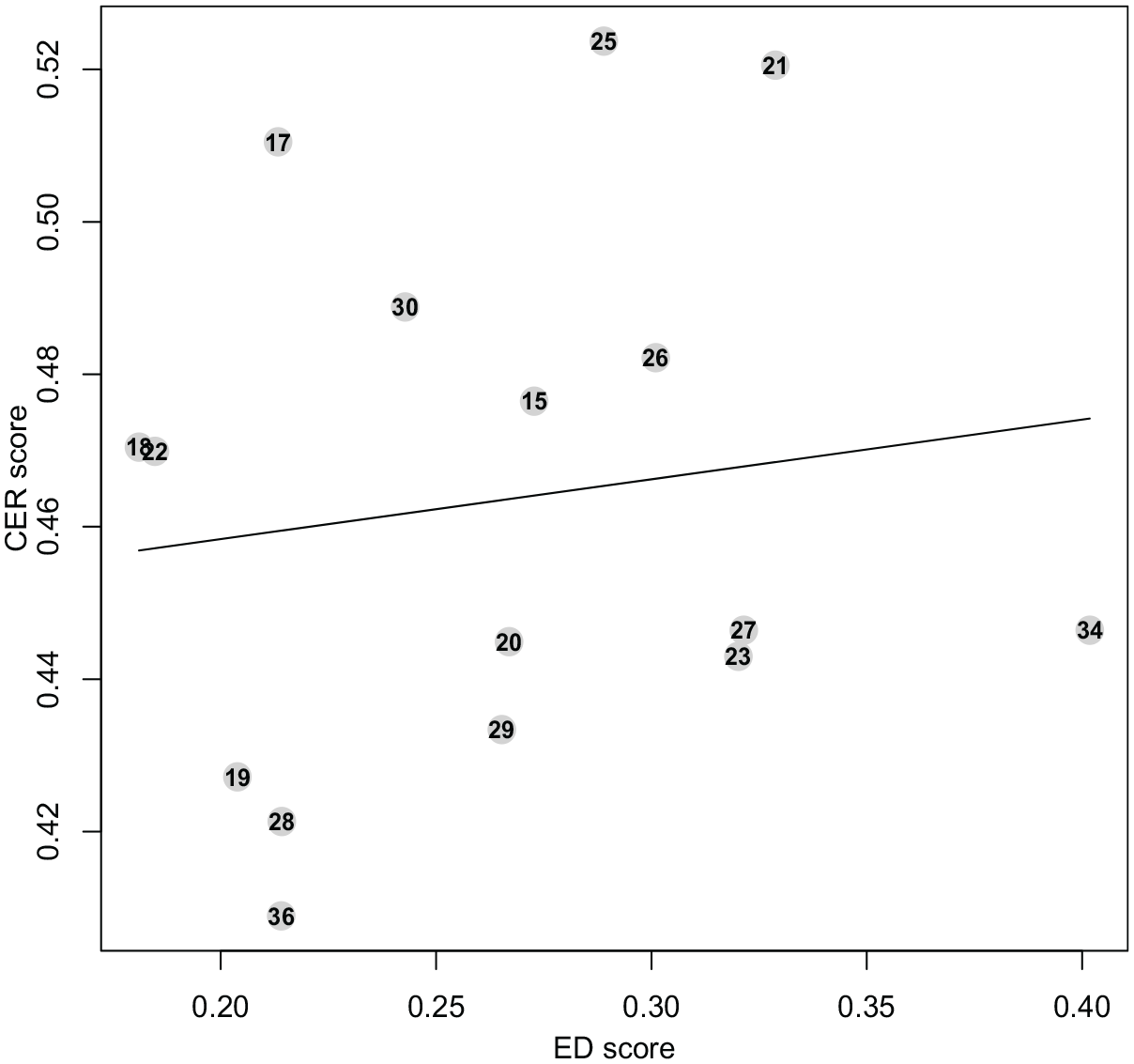

Figures 1 and 2 illustrate the relationship between relative ED scores and relative CER scores by country and industrial sector, respectively. As shown in the figures, the scattered points indicate a diverse relationship between ED and CER by country or industry, although the fitted lines show a positive relationship.

Relative environmental disclosing (ED) scores versus relative corporate environmental responsibility (CER) scores, by sample country.

Relative environmental disclosing (ED) scores versus relative corporate environmental responsibility (CER) scores, by industrial sector.

Determinants of Greenwashing

To model the impacts of female management on greenwashing, we need to identify the potential determinants of greenwashing. For individual top managers, their work experience may determine cognitive leadership prototypes, which affect followers through intensive communication. Accordingly, top managers’ work experience in years (Experience) and a dummy for them meeting with other managers more than once for a typical week (Communication) are incorporated in the models.

At the firm level, firm age and size in terms of the number of employees may affect firms’ capacity and incentives to adopt environmental disclosures and environmental activities. Firms with an entry into the global market (Exporter) and partly owned by foreign investors (Foreign-Ownership) may confront a high degree of environmental commitments (Yang et al., 2020). Firms with government ownership (Government-Ownership) may represent a type of social capital influencing the pressure they face due to environmental regulations.

Apart from firm characteristics, other factors representing market conditions may also influence firms’ greenwashing behaviors. For example, the degree of clustering represented by the number of firms within an industry in a country-region (Clustering) and the degree of competition in the final market (Competition) affect the incentives that firms invest in CER and other social responsibility activities (Hiller & Raffin, 2020). Customer environmental concerns (CEC) may negatively affect firms’ greenwashing behavior through their impact on firms’ capacity reputation (Ioannou et al., 2023). Locations are associated with market scales, economic development, and environmental regulations faced by firms, influencing their environmental behaviors.

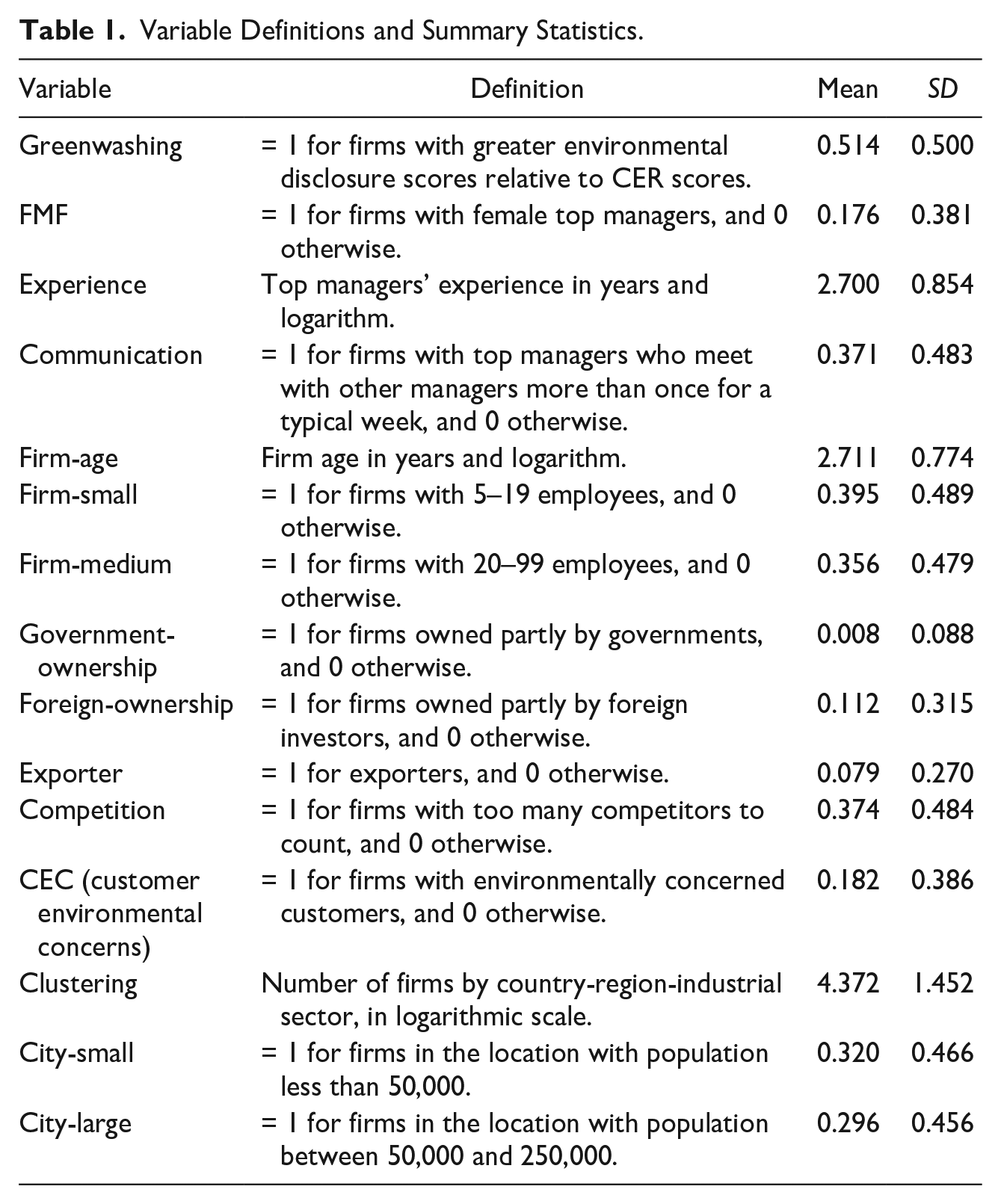

Table 1 presents the definitions of variables in correspondence to the above factors and their summary statistics. The mean of Greenwashing is about 0.514, indicating that more than half of the sample firms have higher relative ED scores than their relative CER scores. The share of firms managed by females is approximately 17.6%. As shown in Table A2 in the Appendix, the share of greenwashers is greater for the female-led firm group than for the male-led firm group (56.9%vs. 50.2%). However, female-led firms may differ from male-led firms regarding various firm characteristics, which are potential determinants of greenwashing. In order to obtain the “pure” gender gap in greenwashing or make female-led and male-led firms comparable, we need econometric methods to test differences in greenwashing behaviors for those types of firm groups by controlling for other greenwashing determinants.

Variable Definitions and Summary Statistics.

Econometric Models

Since the dependent variable Greenwashing is binary, we apply a logit model to evaluate the impact of female executives and other covariates on firms’ greenwashing behaviors. One advantage of the logit model is that we can calculate the probability of being greenwashers for female-led firms compared to their counterparts.

The baseline model specification is in the form of

where FMF is a dummy that equals one for female-managed firms; country dummies and sector dummies capture firm heterogeneity at the country and industrial sector levels;

Equations 3 and 4 imply that the natural exponent of a coefficient equals changes in the odds ratio in response to a one-unit change in the relevant variable, ceteris paribus. Following the common practice in the literature, we are to report the marginal effects of the covariates, which represent changes in probability when one of the covariates increases by one unit (from 0 to 1 for dummy variables).

Empirical Results

Main Findings

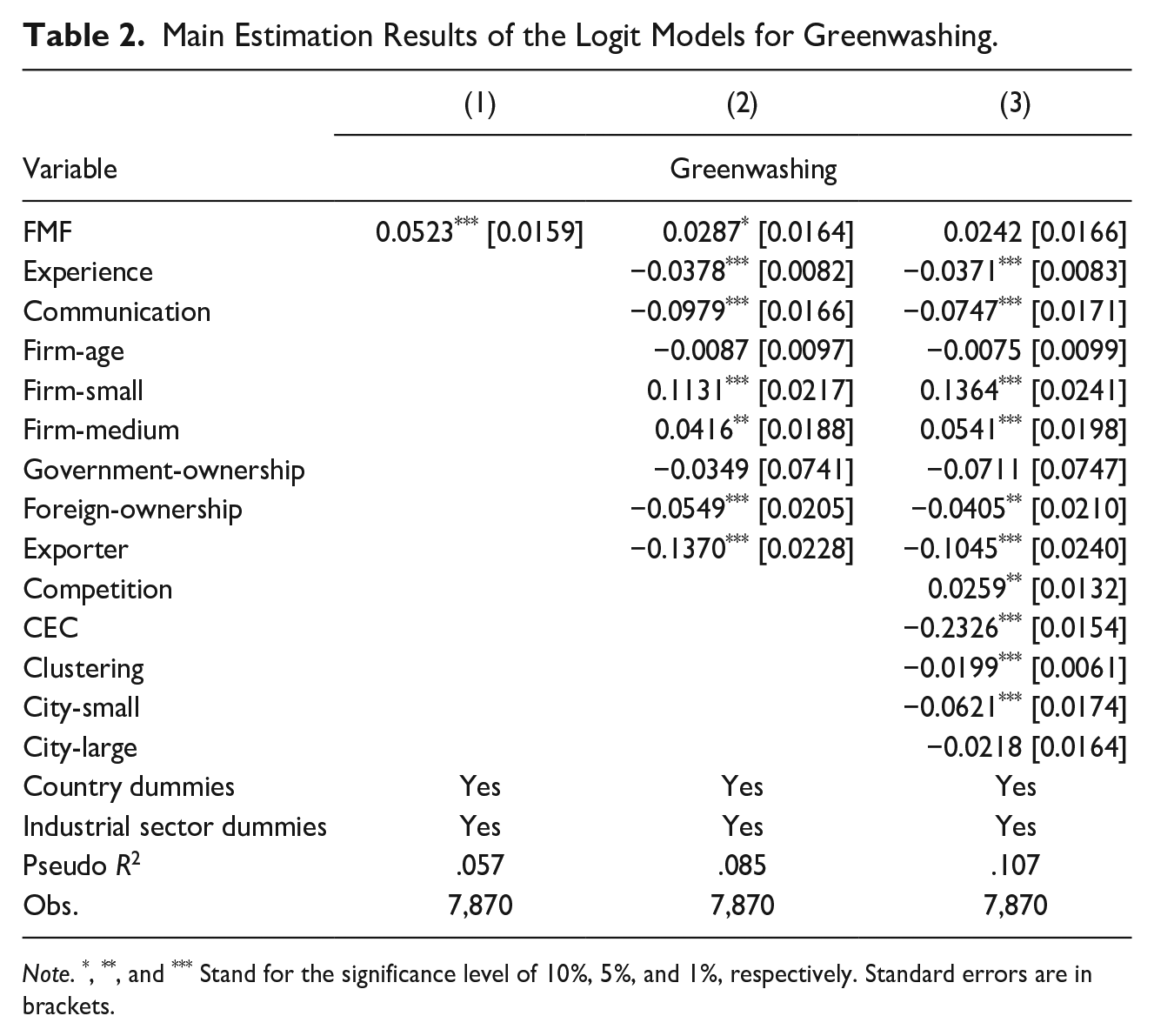

Table 2 reports the results of the fundamental estimation. We first estimate a simple model specification with only FMF and controlling for heterogeneity at the country and industry levels, then add variables representing top managers’ characteristics and firm characteristics, and finally include all explanatory variables in the model specification (i.e., the baseline model). The McFadden (1973) Pseudo R2 ranges between .057 and .107, indicating the impacts on greenwashing of other unobserved variables, such as firms’ decision process and cognitive-relevant variables for firm leaders. 4

Main Estimation Results of the Logit Models for Greenwashing.

Note. *, **, and *** Stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

Table 2 shows that the coefficient of FMF is significant and positive in two models, indicating that the odds of greenwashing are greater for female-led firms than for male-led firms. The results of the simplest model specification show that female-led firms have 5.23 percentage points greater probability of being greenwashers than their counterparts, which reduces to 2.87 percentage points in the model with variables for top managers and firm characteristics and 2.42 percentage points in the baseline model with all explanatory variables. In addition, FMF is insignificant in the baseline model. The changes in the estimated coefficient of FMF in the three models indicate that top manager-relevant variables, firms’ characteristics, market conditions, and locations are critical factors influencing greenwashing behaviors.

Our estimation results further indicate that experienced top managers and intensive communication between top management teams sustainably reduce the odds of greenwashing. Small and medium-sized firms, which are normally young, conduct more greenwashing behavior than do large firms. While government ownership does not affect greenwashing, foreign ownership effectively prevents firms from conducting greenwashing. Additionally, exporters are more consistent in environmental disclosures and actions. The level of competition on the demand side (Competition) promotes greenwashing, and the opposite is true regarding the supply side (Clustering). Interestingly, the variable CEC (customer environmental concerns) is the most important factor preventing greenwashing behaviors, indicating the important role of customers in firm green practices, as documented in Kim et al. (2022). The probability of greenwashing for firms with environmentally concerned customers is approximately 23.3 percentage points lower than the counterpart for other firms. Regarding location, firms in small cities engage less in greenwashing behaviors than firms in large cities.

Mechanism Explorations

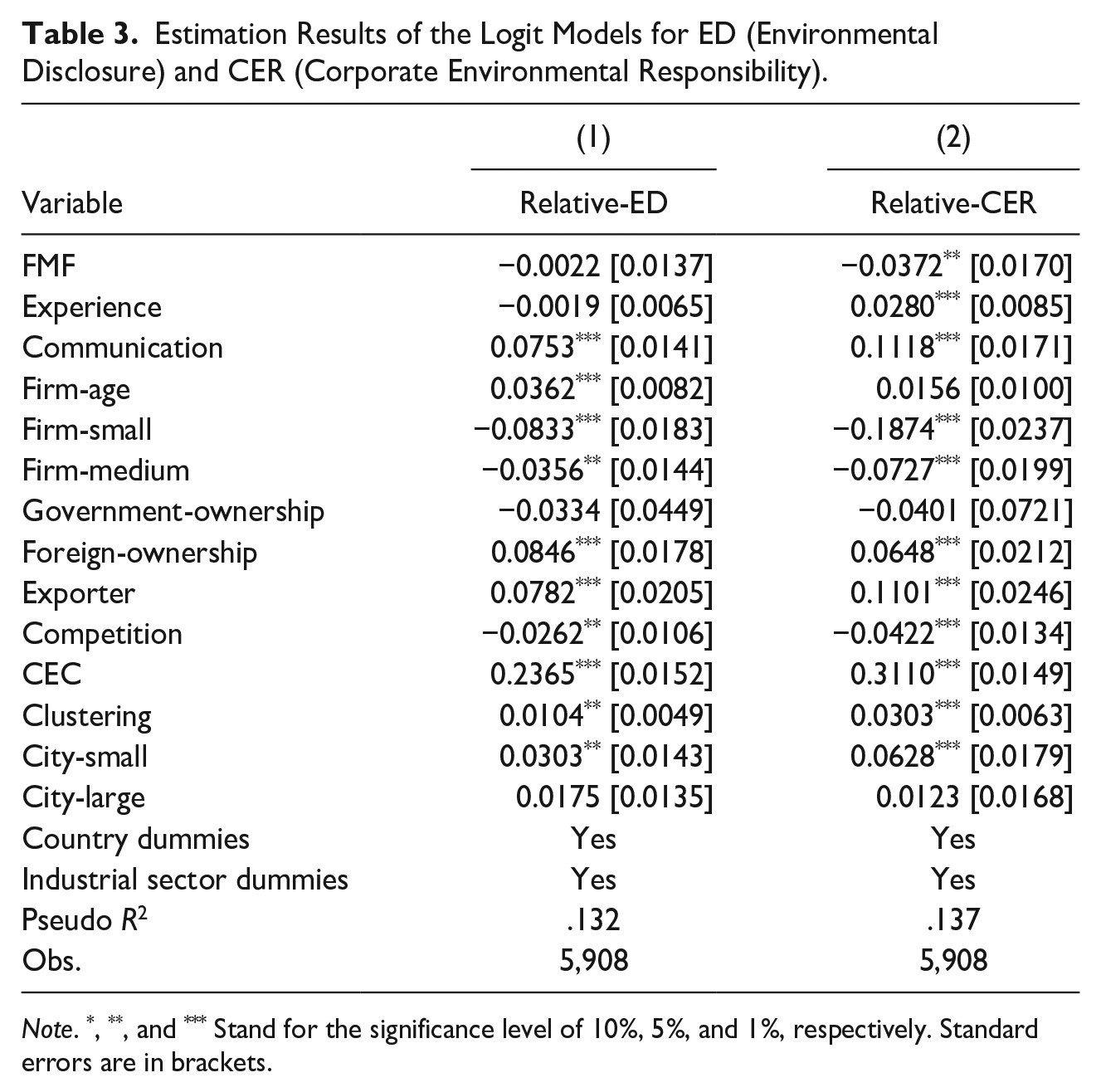

Since greenwashing scores equal the difference between environmental disclosure scores and CER scores, it is worth exploring whether female-managed firms reveal more environmental information and/or adopt less environmental actions. We set one dummy that equals 1 for firms with positive normalized environmental disclosure scores for one model, and another dummy that equals 1 for firms with positive normalized CER scores for another model. The estimation results are presented in Table 3. The coefficient of FMF is only significant in the model for relative CER and with a negative sign. Thus, there is no difference in environmental disclosures between female-led and male-led firms; however, female-led firms are less likely than male-led firms to conduct environmental actions.

Estimation Results of the Logit Models for ED (Environmental Disclosure) and CER (Corporate Environmental Responsibility).

Note. *, **, and *** Stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

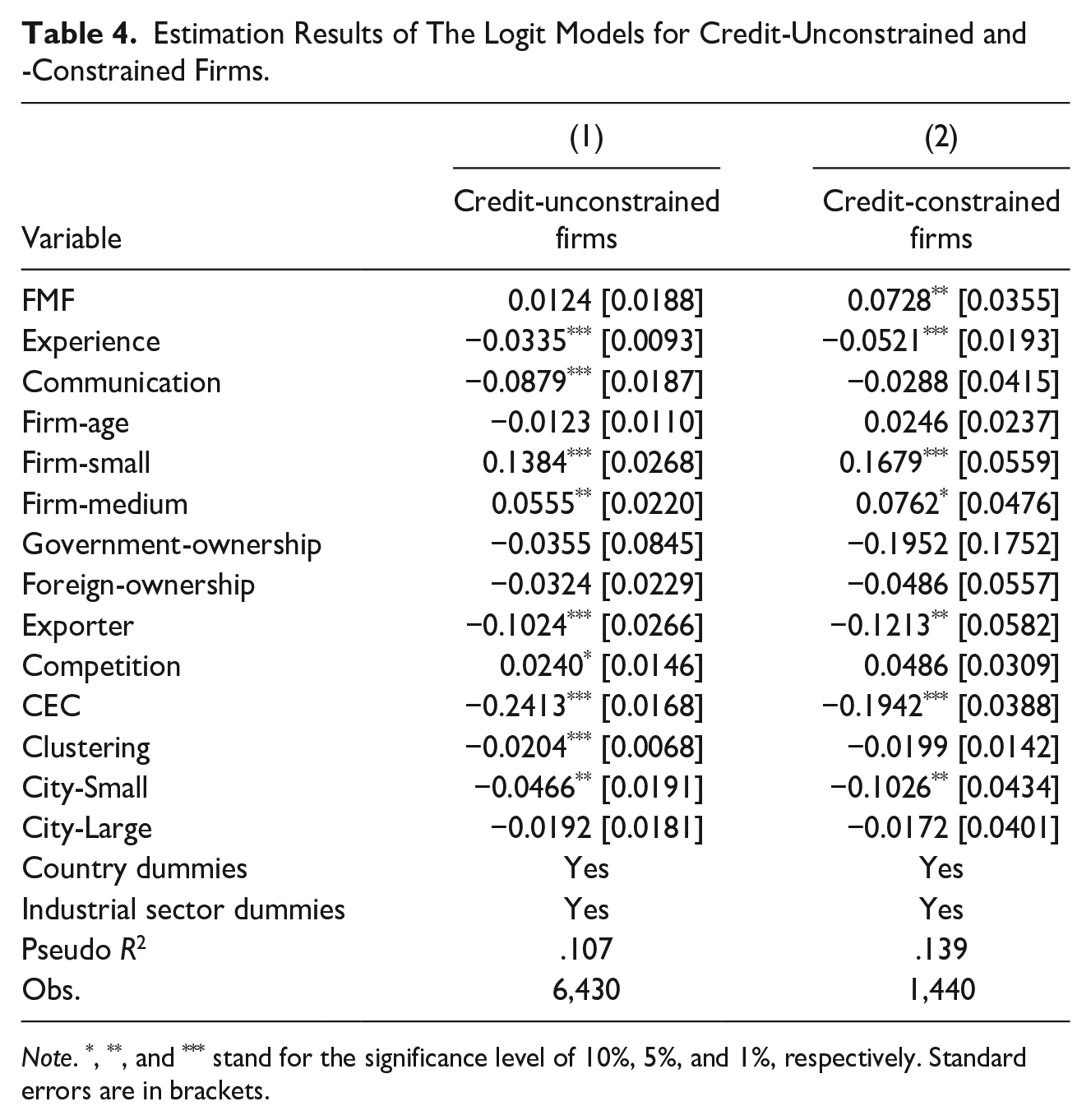

Gender discrimination in capital markets has been well-documented in the literature (Hansen & Rand, 2014; Wang et al., 2021; Wellalage et al., 2019). Additionally, firms’ environmental actions depend on their access to finance. Female-managed firms’ greenwashing behaviors are probably associated with firms’ credit constraint conditions. Following Hansen and Rand (2014) and Zhang (2022b), credit-constrained firms are those that applied for bank loans but got the applications rejected or did not apply for a line of credit for the reasons of high interest rate, insufficient loan size and maturity, or high collateral requirements. We estimate the baseline model for subsamples of credit-unconstrained firms and credit-constrained firms separately. Table 4 presents the estimation results for the two subsamples. FMF is only associated with greenwashing for credit-constrained firms. For firms with access to credit, the probability of conducting greenwashing is not different between female-managed and male-managed firms. The impacts of some determinants on greenwashing are substantially different between credit-constrained and credit-unconstrained firms. For example, Communication and Clustering are only adversely associated with the probability of greenwashing for credit-unconstrained firms. Customer environmental concerns (CEC) are more likely to reduce greenwashing for credit-unconstrained than credit-constrained firms (–0.24vs. –0.19).

Estimation Results of The Logit Models for Credit-Unconstrained and -Constrained Firms.

Note. *, **, and *** stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

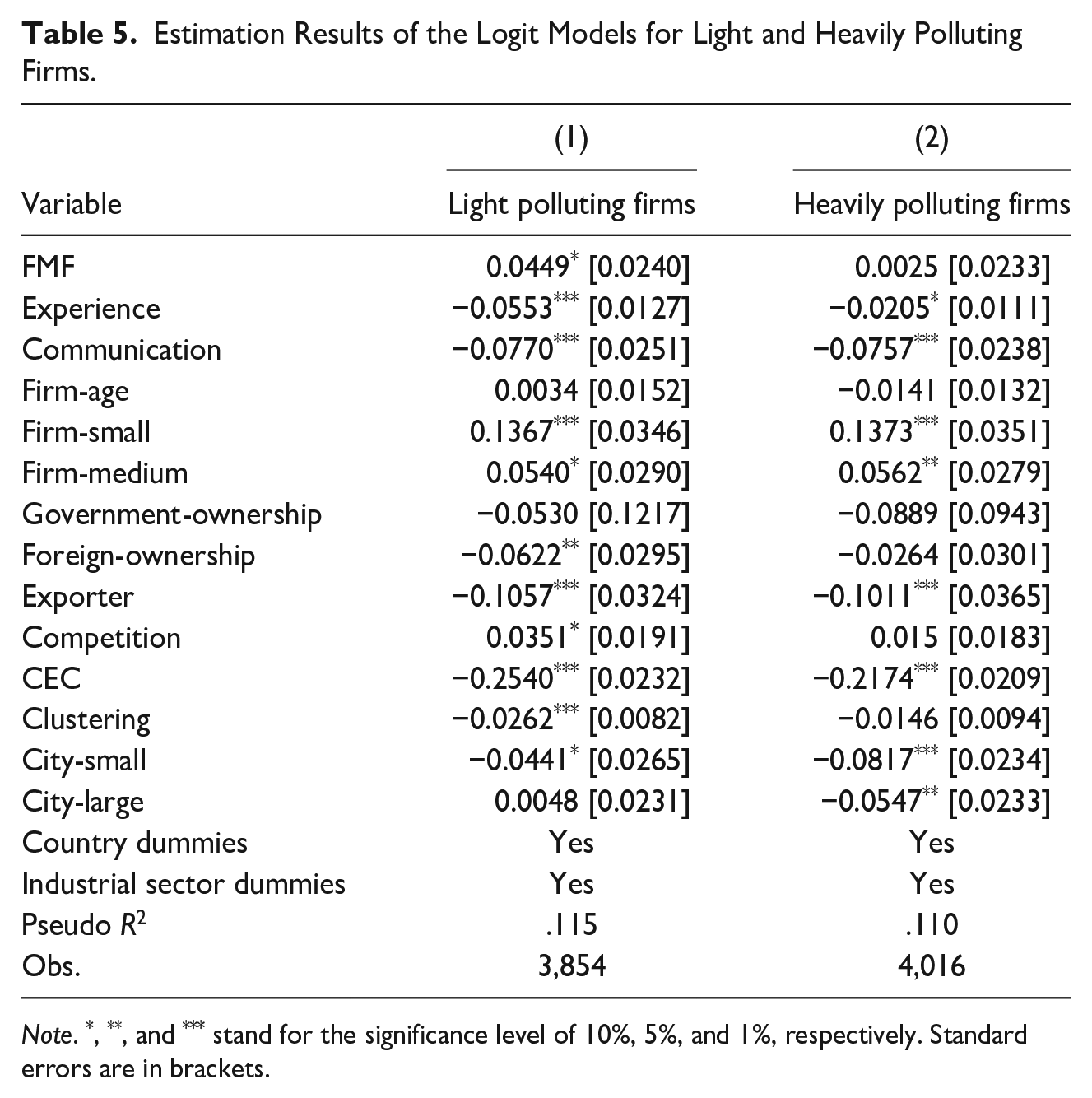

Greenwashing behavior may vary across firms with different polluting levels due to the strictness of environmental regulations. Greenwashing behaviors in light industry may be less severe than in the heavily polluting industry. We further estimate the baseline model specification for subsamples of light industries and heavily polluting industries separately. 5 Table 5 presents the estimation results. FMF is only significant in the model for light industry. For this industrial sector, the probability of greenwashing is 4.49 percentage points higher for female-managed firms than their counterparts.

Estimation Results of the Logit Models for Light and Heavily Polluting Firms.

Note. *, **, and *** stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

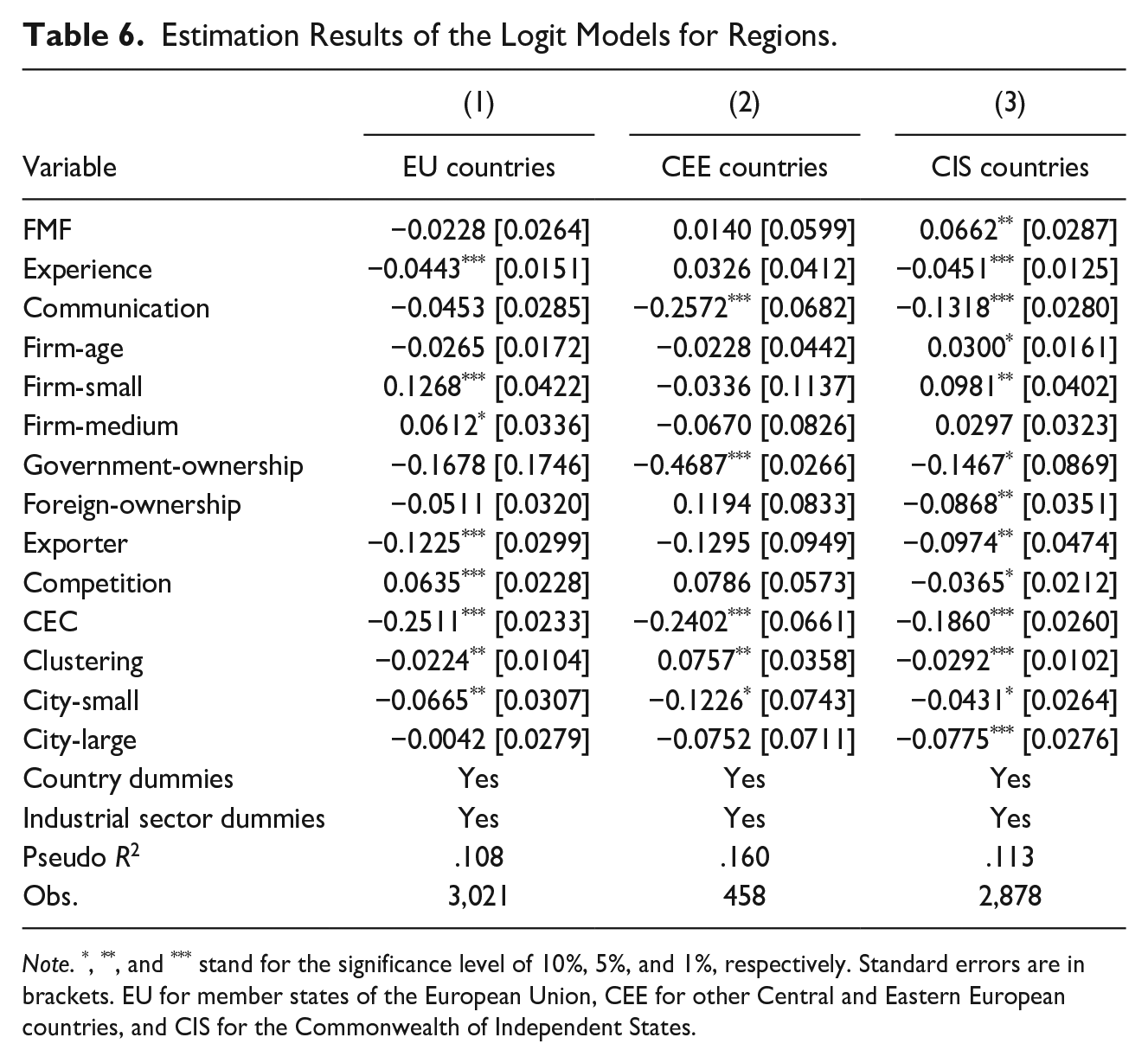

For the main results, more than half of the country dummies are significant, implying country heterogeneity regarding greenwashing behavior. The impact of the gender of firms’ top managers on greenwashing may vary across countries in different geographic regions. We, therefore, estimate three baseline models using subsamples confined respectively to three primary regions: the EU, CEE, and CIS. The estimation results in Table 6 show that the coefficient of FMF is only significant in the model for CIS, which may be attributed to regional differences in culture, economic development, and environmental regulations.

Estimation Results of the Logit Models for Regions.

Note. *, **, and *** stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets. EU for member states of the European Union, CEE for other Central and Eastern European countries, and CIS for the Commonwealth of Independent States.

Additional Analysis and Robustness Checks

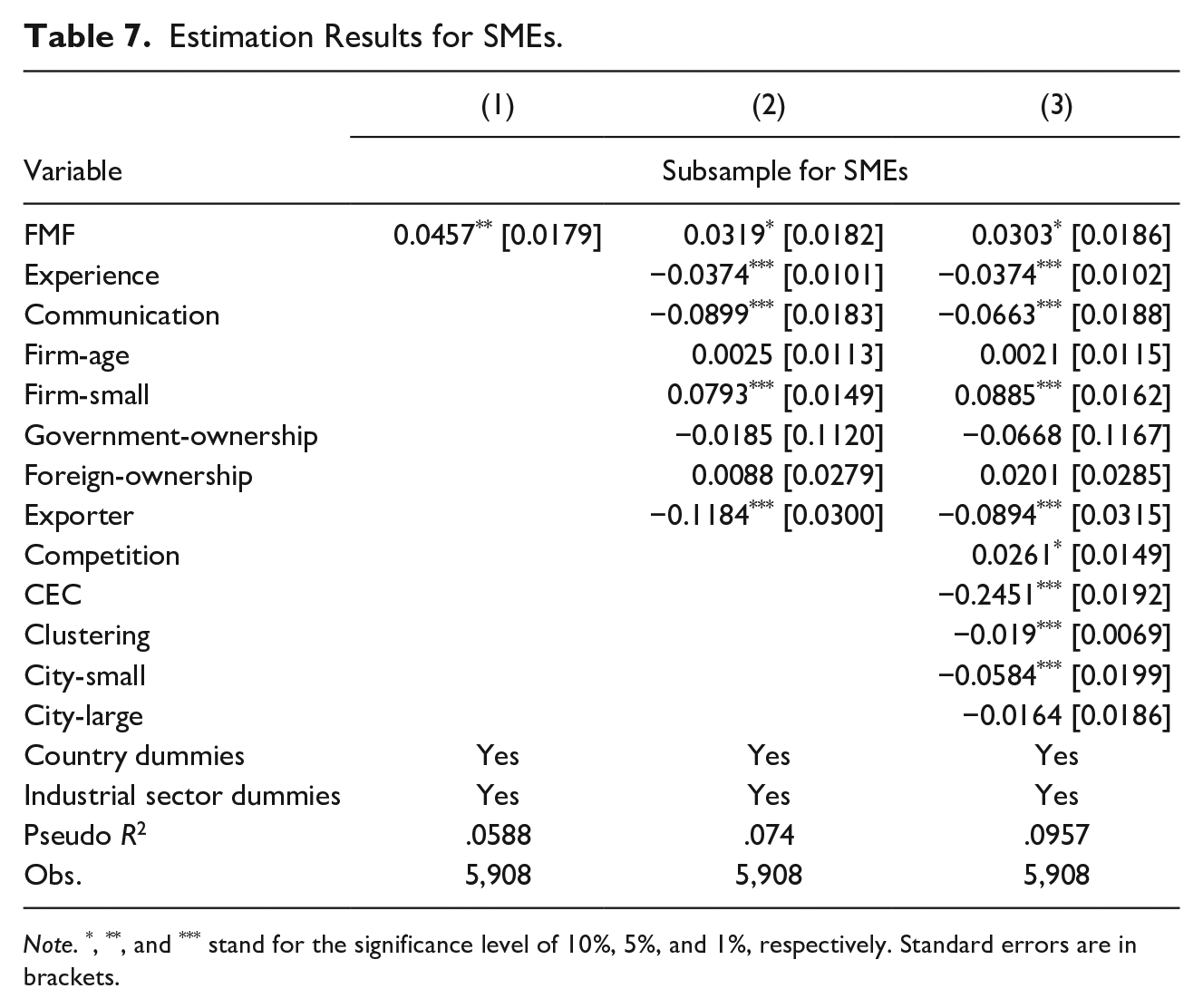

It is probably easier for female leaders to incorporate their individual values into small and medium-sized firms’ (SMEs) strategic actions including environmental commitments. As an additional analysis, we re-estimate the baseline models for SMEs. Comparing the results for SMEs in Table 7 with the main results in Table 2 indicates similar estimates for FMF in the model with FMF only and in the model with FMF, top manager-relevant variables, and firm-level variables. For the complete model specification in Column (3), FMF is significant at the 10% level for SMEs but not significant for the whole sample. Thus, our empirical findings indicate that female-led firms do not have a lower probability of being greenwashers, regardless of firm size.

Estimation Results for SMEs.

Note. *, **, and *** stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

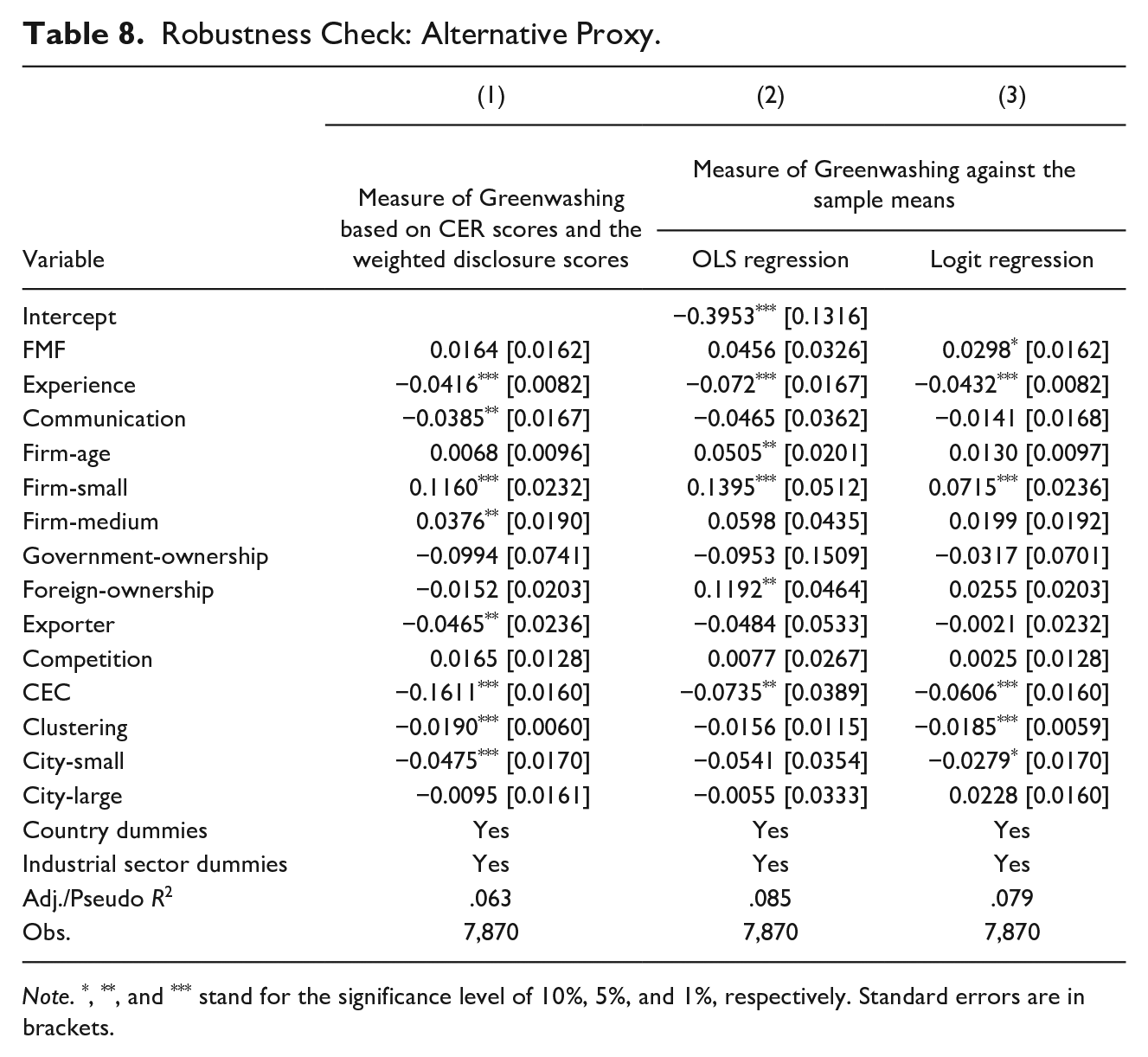

This study measures a firm’s greenwashing scores based on the number of ED and CER adopted by the firm out of the total numbers of environmental disclosures (4) and environmental activities (10) in the survey, respectively. There are six energy-relevant environmental activities, which correspond to energy efficiency assurance. Therefore, we update the relative ED scores by setting weights to individual environmental disclosures, namely, 0.6 for energy consumption, 0.2 for CO2 emissions, 0.1 for water usage, and 0.1 for other pollutants, from which we calculate new greenwashing scores. Table 8 presents the estimation results of the baseline model using the new greenwashing scores. Again, the coefficient of FMF is insignificant. Table 8 also reports the estimation results using the greenwashing scores based on the normalized ES and CER scores regardless of sector heterogeneity, following Yu et al. (2020) and Zhang (2022a, 2022c). Besides an Ordinary Least Squares (OLS) regression for the greenwashing scores, a logit model is applied to a binary measure of greenwashing. As shown in Table 8, FMF is only marginally significant in the logit model regression, in line with the main results.

Robustness Check: Alternative Proxy.

Note. *, **, and *** stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

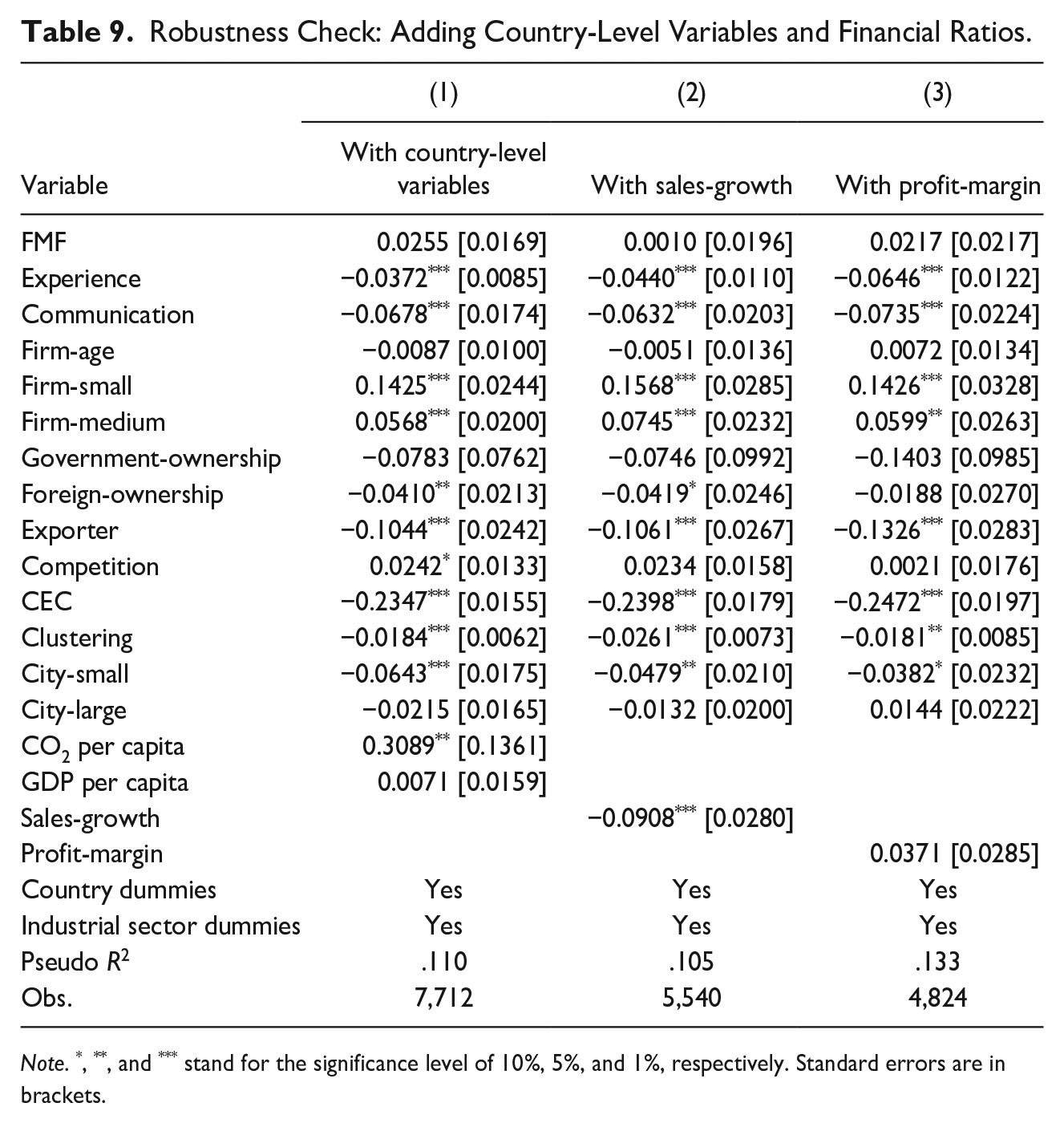

We further add country-level variables and financial ratios into the baseline model specification to test the robustness of the main findings. 6 Table 9 Column (1) reports the estimation results of the model including CO2 per capita and gross domestic production (GDP) growth, showing an insignificant coefficient of FMF. Including either sales growth or profit margin in the model specification does not yield a significant coefficient of FMF. Thus, these additional analyses suggest that female-managed firms are less likely than male-managed firms to engage in greenwashing. It is worth noting the significant and positive coefficient of CO2 per capita, an indicator of regulative pressure. Our estimation results confirm Mateo-Márquez et al.’s (2022) findings that regulative pressure may increase the likelihood of a firm’s engaging in greenwashing.

Robustness Check: Adding Country-Level Variables and Financial Ratios.

Note. *, **, and *** stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

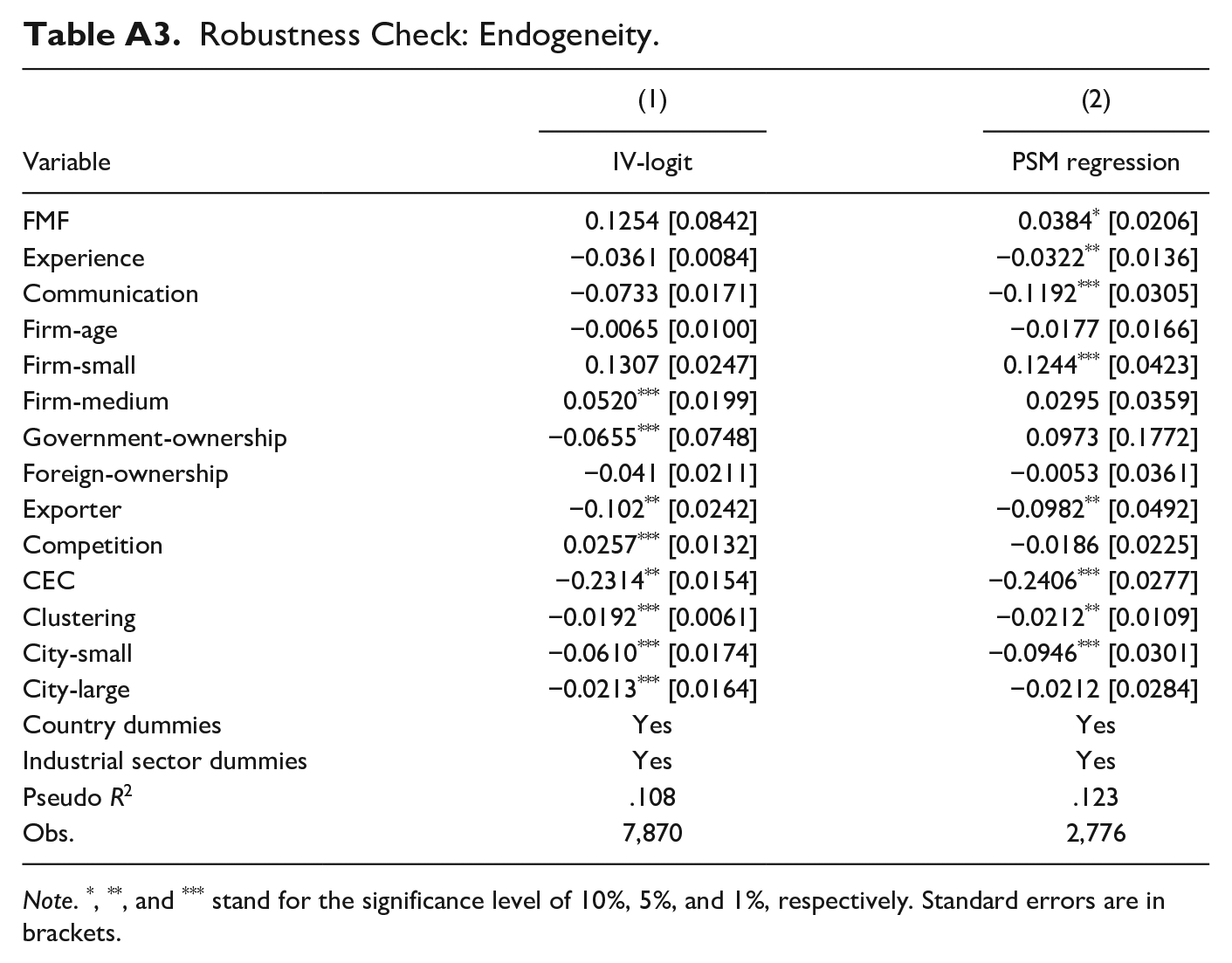

Finally, we test the endogeneity of the gender variable. A female manager may choose to join a firm depending on its CER or greenwashing behaviors, indicating an endogeneity issue. 7 We first re-estimate the baseline model by using the share of firms with female top managers by country and region as an instrumental variable (IV). The estimation results of the IV logit model in Table A3 in the Appendix show an insignificant FMF, although we cannot reject the endogeneity. Next, we use a propensity score matching (PSM) approach to control for endogeneity. We pair female-managed and male-managed firms to reduce systematic differences between the two types of firms, resulting in a subsample of 2,776 observations. We re-estimate the baseline model using the subsample; see Table A3 in the Appendix for the results. The coefficient of FMF is only marginally significant. Overall, these additional estimation results are not substantially different from the main results.

Discussions

The consistency between environmental activities and disclosures becomes a concern for customers, investors, regulators, and researchers. Top female managers may alleviate this concern since females tend to be more environmentally friendly due to gender stereotypes under gender socialization theory (Eagly & Johannesen-Schmidt, 2001) and upper echelon theory (Hambrick, 2007). However, this study’s results indicate that female-led firms are not less likely than male-led firms to conduct greenwashing behavior, indicating that female-led firms may disclose more environmental commitments. Our sample firms are primarily composed of small and medium-sized firms in developing or less developed countries, where female leaders may face barriers when incorporating their individual values into firms’ strategic actions. Researchers have observed that female managers’ commitment to their leadership roles may conflict with their gender roles depending on constraints they face or support they receive, and that female managers are not more effective at advancing environmental practices unless they get the support of women board members (Glass et al., 2016; Liu, 2018). 8

Since the measure of greenwashing is the difference between environmental disclosure scores and corporate environmental responsibility scores, we first explore the reason behind female-led firms’ greenwashing behavior by estimating models for the two individual scores separately. The estimation results indicate that female-led firms do not differ from their counterparts when disclosing environmental information but engage in fewer environmentally responsible activities than male-led firms, indicating that increasing environmental practices is an effective way to reduce greenwashing. There are several reasons probably explaining this finding. First, incorporating top managers’ individual values or prosocial attitudes into firms’ decisions may vary across environmental investments and strategic disclosures. Second, firms led by females may have more financial and non-financial barriers to conducting green practices than other firms. Third, our findings are probably confined to the sample used, which is primarily composed of small and private firms in developing or less developed countries. For example, for listed firms in the U.K., Tingbani et al. (2020) find a positive relationship between board gender diversity and environmental disclosure. For large, listed U.S. firms, Glass et al. (2016) document that the gender of CEOs is not associated with environmental concerns and strengths.

Firms’ financial status is one of the factors motivating them to greenwash (Gregory, 2023; Zhang, 2022c). Past literature has documented lending difficulties for female-led firms (Hansen & Rand, 2014; Wellalage et al., 2019; Zhang et al., 2022). Therefore, female-led firms’ greenwashing behavior is probably attributed to limited access to credit. Zhang (2022a) verifies a positive impact of credit constraints on greenwashing, irrespective of the gender of top managers. Our findings indicate a more severe impact of credit constraints on female-led firms’ greenwashing, suggesting that alleviating credit constraints may prevent female-led firms’ greenwashing behavior.

Female-led firms’ greenwashing may depend on contextual differences across industrial sectors. Firms’ environmental impacts vary across light and heavy industries (Zhu et al., 2008). Heavy industries rely more on energy use and have poor environmental performance, which may motivate firms in this industry to greenwash (Zhang, 2022a). Additionally, stakeholders’ high expected environmental performance for heavily polluting firms may force these firms to strategically disclose environmental information (Lyon & Maxwell, 2011). Light industries are more consumer-oriented, resulting in the great influence of consumer environmental concerns on firms’ environmental behavior and then greenwashing. Our empirical results suggest that female-led are more likely than male-led firms to be greenwashers only in light industries. Greenwashing behavior in heavy industries is not associated with leaders’ gender, which may attribute to stringent environmental regulations in this sector (Marquis et al., 2016).

Environmental regulations differ across countries and greenwashing relies on institutional features (Marquis et al., 2016; Yu et al., 2020). Our findings indicate that, for developed countries, female-led firms do not differ from male-led firms regarding greenwashing behavior. However, female-led firms in less developed countries tend to conduct greenwashing behavior. Those countries are probably less exposed to scrutiny and global norms, which are determinants of selective disclosure (Marquis et al., 2016).

Our estimation results for other determinants of greenwashing suggest a way to detect greenwashing behavior. For example, the probability of greenwashing is lower for firms with environmentally concerned customers. This is probably because customers perceive greenwashing as corporate hypocrisy, reducing customer satisfaction (Ioannou et al., 2023). Firms with foreign ownership or in the global market are more consistent in environmental disclosures and actions, in line with Zhang’s (2022a) findings.

Conclusion

Using a sample of 7,870 private firms from 28 countries, we investigate the determinants of greenwashing and whether female-led firms are less likely to be greenwashers. This study responds to past research on gender differences in environmental behavior since the measures of greenwashing rely on environmental disclosure and environmentally responsible activities. Our study supplements previous studies and is the first one that evaluates the difference in greenwashing behaviors for female-led and male-led firms.

Specifically, we measure greenwashing according to the gap in environmental disclosure scores and CRE scores, both relative to their respective averages by industry. Our main estimation results suggest that female-led firms are not less likely to conduct greenwashing behavior. This finding remains intact when we control for endogeneity and use alternative measures of greenwashing. Some regressions even provide evidence that female-led firms are more likely to be greenwashers. We conduct several additional regression analyses to explore the mechanisms of greenwashing behaviors for female-managed firms compared to male-led firms. Those analyses indicate that female-led firms engage in fewer environmentally responsible activities but are not different from their counterparts regarding environmental information disclosures. Moreover, female-led firms tend to greenwash when they are constrained by access to credit, belong to light industries, and are from less developed countries.

Greenwashing reduces the credibility of environmental performance, making consumers and investors reluctant to reward environmental performers, which may then affect firm performance and market value. Although female-led firms greenwash when they are constrained by access to finance, belong to light polluting industry, or are located in less developed countries, the consequences of greenwashing may affect those firms’ competitiveness and sustainable development, enlarging gender inequality. This further prevents from achieving one of the United Nations’ Sustainable Development Goals (SDG 5) targeting to foster “equal rights to economic resources, property ownership and financial services for women.” Therefore, our results reveal the mechanism of greenwashing behavior for female-led firms suggesting the direction for enhancing the credibility of environmental initiatives for these firms. First of all, alleviating credit constraints for female-led firms through governmental credit and loan guarantee programs may motivate female-led firms to conduct more green practices that match the content of environmental information disclosures. Mitigating greenwashing is challenging due to uncertain regulations. The industry-relevant greenwashing indicates the various levels of uncertainties of environmental regulations by industry. Designing industry-specified environmental regulations can minimize uncertainty, reducing greenwashing.

Despite its uniqueness, our research has certain limitations, which may suggest paths for future research. Different from previous studies on greenwashing, which focus on large, listed companies and measure greenwashing based on multidimensional environmental scores, this study focuses on private firms with limited available data on environmental performance. Most of our samples are small and medium-sized firms. It is a challenge to find comparable measures of greenwashing for those firms across industrial sectors and countries. Future research can use the sample of large, listed companies to test differences in greenwashing between female-managed and male-managed firms. Another limitation of this study is that the data do not provide more personal and cognitive variables for firms’ top managers. Although industry variables, firm-level variables, and market conditions could be proxies of top managers’ cognitive frames (Hambrick, 2007), incorporating individual demographic and cognitive characteristics in the models could help us evaluate the gender gap in greenwashing more precisely. This is another issue remaining for future study.

Footnotes

Appendix

Robustness Check: Endogeneity.

| Variable | (1) | (2) |

|---|---|---|

| IV-logit | PSM regression | |

| FMF | 0.1254 [0.0842] | 0.0384 * [0.0206] |

| Experience | −0.0361 [0.0084] | −0.0322 ** [0.0136] |

| Communication | −0.0733 [0.0171] | −0.1192 *** [0.0305] |

| Firm-age | −0.0065 [0.0100] | −0.0177 [0.0166] |

| Firm-small | 0.1307 [0.0247] | 0.1244 *** [0.0423] |

| Firm-medium | 0.0520 *** [0.0199] | 0.0295 [0.0359] |

| Government-ownership | −0.0655 *** [0.0748] | 0.0973 [0.1772] |

| Foreign-ownership | −0.041 [0.0211] | −0.0053 [0.0361] |

| Exporter | −0.102 ** [0.0242] | −0.0982 ** [0.0492] |

| Competition | 0.0257 *** [0.0132] | −0.0186 [0.0225] |

| CEC | −0.2314 ** [0.0154] | −0.2406 *** [0.0277] |

| Clustering | −0.0192 *** [0.0061] | −0.0212 ** [0.0109] |

| City-small | −0.0610 *** [0.0174] | −0.0946 *** [0.0301] |

| City-large | −0.0213 *** [0.0164] | −0.0212 [0.0284] |

| Country dummies | Yes | Yes |

| Industrial sector dummies | Yes | Yes |

| Pseudo R2 | .108 | .123 |

| Obs. | 7,870 | 2,776 |

Note. *, **, and *** stand for the significance level of 10%, 5%, and 1%, respectively. Standard errors are in brackets.

Acknowledgements

The author is grateful to the editors and reviewers for their valuable comments, especially with regards to the introduction of various overarching gender theories that have contributed to the conceptualization of this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.