Abstract

Little is known about voters’ demands in response to rising house prices. We argue that voters’ house-price perceptions and housing policy preferences depend on countries’ differing economic institutions. In the UK’s liberal welfare and credit regimes, we expect voters to view house-price growth as a comparatively positive sign for the economy and show little demand for policies restraining prices. In Germany’s generous welfare and restrictive credit regimes, we expect voters to view house-price appreciation with more skepticism and demand policies restraining prices. First, through a custom survey, we experimentally demonstrate that British homeowners regard house-price growth as a sign of economic health, while German homeowners and renters from both countries do not. Second, we find that German voters, both homeowners and renters, support policies restraining house prices more so than their British equivalents. Our findings suggest that similar types of voters have different housing attitudes in differing institutional contexts.

Keywords

Introduction

Surges in house prices over the last decade have become a major political challenge in advanced economies. The stark rise in house prices has not only led to macroeconomic fears about financial instability, but also directly affected the distribution of wealth in rich democracies. While many homeowners have seen massive gains in household wealth, renters—often marginalized social groups—are instead facing increasingly unaffordable rental markets (Anderson & Kurzer, 2020; Ansell & Cansunar, 2021; Bohle & Seabrooke, 2020; Dewilde & Flynn, 2021; Fuller et al., 2020). Scholarship in political science has caught on to the political consequences of housing, studying how changes in house prices shape voters’ welfare preferences (Ansell, 2014) or party choices (André et al., 2018) as well as the growing role of housing as a form of asset-based welfare (Mertens, 2017).

However, we still know surprisingly little about voters’ house-price perceptions in advanced economies—that is, how voters actually perceive changes in house prices. An increasingly common assumption in the comparative politics literature is that voters generally welcome rising house prices as a sign of economic health, while falling house prices would signal an economy or community in decline. Voters’ positive views of rising house prices would then result in less support for populist parties or greater support for incumbents (Adler & Ansell, 2020; Ansell et al., 2022; Larsen et al., 2019). However, there is little direct evidence that voters, in fact, do consider rising house prices as a positive development for the economy.

Even less is known about voters’ housing policy preferences. Existing studies have necessarily relied on large-scale institutional surveys that tend to ask rather broad questions on housing, such as whether governments have a responsibility for providing decent housing for their populations (Ansell & Cansunar, 2021). A series of new studies have relied on custom surveys (Dancygier & Wiedemann, 2023; Hager et al., 2023; Hankinson, 2018; Löffler & Pond, 2023; Marble & Nall, 2021; O’Grady, 2020), which generated important insights on voter attitudes toward more specific housing policies, such as rent control, residential construction, or landlord expropriation. However, existing survey research has rarely investigated voters’ views on a range of owner-oriented and renter-oriented policies.

This article presents a two-step argument with original survey evidence on voters’ house-price perceptions and preferences. First, we argue that voters do not uniformly view rising house prices as a positive sign for the economy across rich democracies. Rather, our expectation is that perceptions of house prices are context-specific and thus likely differ between countries. For a comparison, we chose Germany and the UK as diverse cases that differ in their credit, welfare, and housing regimes. As we detail below, house-price appreciation is essential for households to finance consumption, pensions, or welfare services in the context of the UK’s liberal welfare and credit regimes—much like in the United States, Canada, or Australia—but it is less essential in the context of Germany’s more generous welfare and restrictive credit regimes, as is the case in Austria. German voters thus likely view rising house prices as a relatively negative economic development, while British voters view them more favorably.

Second, and relatedly, we expect housing policy preferences to differ across advanced economies, owing to differences in credit, welfare, and housing regimes. As German voters do not routinely rely on asset-price appreciation for social welfare or private consumption, we expect them to hold relatively favorable views of policies that both restrain house prices and make renting and homeownership more affordable. As British voters—and particularly the high number of existing homeowners—do rely on real estate for generating private consumption and asset-based welfare, we expect them to hold less favorable views of policies that restrain house-price growth and lower the cost of renting and homeownership. In short, voters’ reactions to rising house prices—including their house-price perceptions and housing policy preferences—depend on voters’ positioning in a country’s institutional context.

Through a custom survey with a pre-registered experiment, we first find that British voters view rising house prices as a more favorable economic development than German voters. While British homeowners regard rising house prices as a sign of national economic health, German homeowners do not (even though both groups welcomed rising house prices for their own pocketbooks). German homeowners’ reactions are thus more aligned with those of both countries’ renters, who also do not consider rising house prices as a favorable economic development. Second, we find that German voters—both homeowners and renters—have more favorable attitudes towards policies that restrain house prices and make both rental and owner-occupied housing more affordable compared to their British equivalents. Finally, we explore the individual-level correlates of housing policy preferences and find rather weak empirical support that such preferences are associated with voters’ perceptions of house prices.

Our findings contribute to a burgeoning literature on the politics of housing in advanced economies. First, we provide more direct and fine-grained measures of voters’ house-price perceptions and housing policy preferences than previous scholarship. Doing so advances our understanding of how voters evaluate rising house prices and which measures they want their governments to adopt in response. Second, we suggest that countries’ differing credit and welfare regimes shape previously under-appreciated cross-national variation in voter attitudes towards housing prices and policy. Our experimental evidence challenges the widespread socio-tropic assumption that voters generally regard rising house prices as signs of economic health. We find that British homeowners do regard rising property prices as a sign of a vibrant economy, while German homeowners do not. In addition, both countries’ renters regard rising house prices as a negative economic development. Similarly, we find that German homeowners and renters show higher support for policies to restrain house prices than their British equivalents. Our findings thus reveal that similar social groups have different attitudes toward housing prices and policies across countries, likely owing to differing institutional contexts.

State of the Art: Perceptions of House Price Changes and Housing Policy Preferences

Housing has become a key pillar of comparative political economy scholarship (Johnston & Kurzer, 2020). Recent studies have analyzed the political consequences of housing, such as the effect of housing on social policy preferences, voting behavior, support for populist parties, as well as the role of housing in economic growth models or welfare states (Adler & Ansell, 2020; Anderson & Kurzer, 2020; Ansell, 2014; Bohle & Seabrooke, 2020; Dewilde & Flynn, 2021; Fuller et al., 2020; Kohl, 2017; Mertens, 2017; Reisenbichler, 2022; Reisenbichler, forthcoming). However, less is known about what voters think about house-price developments and which policies they want their governments to adopt in response.

An important body of work suggests that rising house prices—and particularly voters’ house-price perceptions—shape political outcomes, such as populist voting or voters’ redistributive demands. The main posited mechanisms linking house prices and political outcomes are voters’ ego-tropic and socio-tropic evaluations of house-price changes. The ego-tropic (or pocketbook) mechanism is based on an individual’s material self-interest. It implies that homeowners view rising home values positively as they derive financial benefits from asset-price appreciation. It also implies that renters should oppose rising property prices that can translate into higher rents for them. Such ego-tropic motives would then shape homeowners’ preferences for less redistribution—as they can generate private income from house-price appreciation in lieu of welfare programs (Ansell, 2014)—and their opposition to new housing developments to protect property values, even if these homeowners are otherwise liberal (Marble & Nall, 2021).

Scholars also emphasize voters’ socio-tropic (or geo-tropic) evaluations of house prices, which are based on individuals’ assessments of a community’s economic wellbeing (as opposed to one’s personal economic wellbeing). In other words, voters’ perceptions of house prices inform their assessments of national economic wellbeing. In an important study on Denmark, Larsen et al. (2019) suggest that relative changes in local house prices affect electoral outcomes at the national level. Their argument is that voters—both renters and owners—would view “increasing housing prices […] as a cue of a booming national or local economy” (Larsen et al., 2019, p. 513). As a result, voters would reward politicians in areas with rising house prices and punish politicians in areas with stagnant or falling house prices. Their socio-tropic reasoning is that rising house prices would have broader growth-generating effects in a community: rising local house prices would allow homeowners to borrow and spend more, which would then also benefit renters through higher employment and business activity (Ibid., p. 501). It is, however, uncommon to leverage one’s home for consumer credit and spending in restrictive credit regimes found in Germany and Austria (Reisenbichler, 2022; Wiedemann, 2021), meaning that house-price gains do not dissipate much beyond homeowners in those countries.

In another study on the Nordic countries, Ansell et al. (2022) suggest that voters’ local house-price perceptions are linked to national populist voting. Their argument is that populist voting is stronger in local communities with relatively low house-price growth, while it is weaker in communities with high growth in property values. Their geo-tropic assumption is that “[w]here prices are rising, citizens feel…communally satisfied with the political and economic status quo and continue to vote for mainstream parties,” whereas voters in areas with declining prices would feel a sense of economic decline relative to thriving economic areas, which would then push them to the populist right (Ibid., p. 1424). The authors even note that renters potentially dislike falling house prices in their local communities, as “nonhomeowners may be concerned about declining house prices, since they signal that the market does not value places like the one in which they live” (Ibid., p. 1424; also see Adler & Ansell, 2020, pp. 349–350).

In short, this important body of work suggests that both renters and homeowners would view rising house prices as a favorable and falling housing prices as a negative development for their local and/or national economies. However, an empirical limitation of these studies is that they do not include direct measures on how voters perceive changes in house prices. One general problem is data limitation, as institutional surveys rarely contain fine-grained questions about how voters evaluate rising house prices. Rather, these studies have shown robust relationships between changes in local house prices (with data taken from national registries) and precinct-level or individual-level voting behavior. Yet, linking local housing data with voting behavior leaves open the question of whether voters actually perceive rising house prices as growth-generating developments for their communities.

What voters perceive to be beneficial housing developments, we contend, differs from context to context. We have strong reasons to suspect that voters do not uniformly view rising house prices as a sign of economic health across advanced economies. For example, a majority of residents in Berlin—a city with strong relative house-price gains compared to other local communities of the country—voted to expropriate commercial landlords in a 2021 city-wide (non-binding) referendum. Rising house prices might thus be a cause for celebration in countries like the United States and UK, but they are likely a cause for concern in countries like Germany or Austria.

Another body of work relates to voters’ housing policy preferences—that is, voters’ views on which housing policies governments should adopt in response to rising house prices. The small number of comparative studies on housing policy preferences is partly due to the fact that institutional surveys rarely ask respondents detailed questions about housing. Scholars thus necessarily relied on rather broad items from such surveys. In an important study, Ansell and Cansunar (2021) find that homeowners tend to oppose government interventions that make housing more affordable, particularly in expensive areas. While their findings are convincing in the context of the available data, using institutional survey data on housing has limitations. One of their housing policy preference variables comes from the International Social Survey Program (ISSP), which asked respondents whether the “government has a responsibility to provide decent housing” (Ibid, p. 601). However, responses to this question do not tell us whether or how citizens want the government to make housing more affordable. Another of their housing variables comes from the British Social Attitudes Survey (BSAS), asking respondents whether they would “support or oppose more homes being built in your local area” (Ibid, p. 606). While the question is more specific, it is similarly impossible to know whether citizens associate this question with housing affordability or other typical NIMBY concerns, ranging from environmental protection to neighborhood preservation. More generally, the question of supporting housing construction is one of many important dimensions in the universe of available housing policies that are related to affordability concerns.

A growing number of studies has relied on original surveys to identify more fine-grained housing policy preferences. Studies on the United States examined voters’ housing policy preferences on new housing construction in local communities. Hankinson (2018) finds that even renters oppose new housing developments in high-rent cities, fearing higher rents resulting from luxury developments—a NIMBY-like policy stance often associated with homeowners. Relatedly, Marble and Nall (2021) find that, while liberal homeowners support local and state aid to renters in line with their left-leaning welfare ideology, they are—much like their conservative counterparts—opposed to new housing developments in their local communities to protect the value of their homes and/or their quality of life.

In the case of Germany, recent work based on custom surveys has similarly explored attitudes toward individual housing policies. Hager et al. (2023) show that tenants in rent-controlled apartments are more open to new construction in their local communities, as they would be somewhat shielded from gentrification. In another study, Löffler and Pond (2023) find that, when prompting German respondents with experimental vignettes of how foreign buyers drive up house prices, voters support restrictions to foreign housing transactions. Similarly, Dancygier and Wiedemann (2023) examine German voters’ preferences for landlord expropriation. They find that, when presenting respondents with a scenario of rising house prices brought about by commercial landlords, these respondents strongly favor government measures of landlord expropriation.

All these studies share a single shortcoming: they have not generated data on individuals’ views about a much broader range of rental and homeownership policies, particularly not from a comparative perspective.

Theoretical Assumptions and Hypotheses

Our core assumption is that countries’ political economies consist of differing economic institutions and deep-seated shared understandings about what makes for a successful economy. While for some political economies asset-price appreciation might be an essential element of economic growth or privatized welfare (i.e., the UK, United States, and Canada), it is not in others (i.e., Germany and Austria), and we expect this to matter for individuals’ attitudes toward both house-price changes and housing policies. We compare Germany and the UK as two diverse cases that differ in their credit, welfare, and housing regimes that likely affect voters’ reactions to rising house prices and their housing policy preferences in the following ways.

Voter Perceptions of House Price Changes

In the UK, the liberal welfare regime with ungenerous public pensions encourages households to treat housing as an investment that is supposed to grow in value and provide a form of private insurance in old age (Ansell, 2014). In addition, the country’s “permissive” credit regime (Johnston et al., 2021; Wiedemann, 2021), which facilitates easy access to mortgages paired with low property transaction costs, allows households to treat their homes as ATMs from which to extract home equity. As Ronald (2008, p. 54) states, “[t]he possibility for financial gain has been bound tightly to home ownership within the specific context of building equity in conditions of house-price inflation.” Home equity loans, mortgage refinancing, or selling homes with a profit allows households to extract home equity to finance consumption, maintain living standards, smooth income losses, or finance welfare services (Hay, 2013; Reisenbichler & Wiedemann, 2022). Finally, the UK is considered “a nation of homeowners” in which two-thirds of the population own a home (40% of all households own their home outright, while another 28% are owners with a mortgage), while public policy privileges homeownership over renting (Hay, 2013; Oren & Blyth, 2019; Reisenbichler & Wiedemann, 2022; Ronald, 2008; Toussaint & Elsinga, 2009). As Hilber (2023) notes, “the ‘median voter’ in the UK is an existing homeowner who likely believes themselves to be a beneficiary of the status quo with rising house prices.” In short, rising house prices are part and parcel of the UK’s economic growth and welfare models (Baccaro et al., 2022; Hassel & Palier, 2021).

In socio-tropic terms, we would therefore expect the large number of British homeowners to view rising house prices as a favorable economic development for their country. First, British homeowners might associate rising home values with financial opportunities—such as leveraging their homes for more consumer credit and spending made possible by the country’s permissive credit regime—which would then spur activity in the wider economy (Larsen et al., 2019, p. 501). Second, in a majority-homeowner nation in which homeownership is the dominant form of housing tenure, a typical British homeowner is likely aware that most other British households own their homes, and they might therefore view rising house prices to be economically beneficial not only for themselves but also for other homeowners like them. Third, as most British households rely on housing wealth as a form of privatized welfare, homeowners likely view housing-wealth gains to be a country-wide socio-economic benefit. However, we expect British renters to view rising house prices as a negative economic development for their country; in fact, it is likely that British renters associate rising—not falling—prices with an economy that excludes them from the prosperity-generating spoils of homeownership and drives up the cost of living.

In contrast, Germany’s welfare state offers more generous public pensions, which reduces incentives for German households to view housing assets as substitutes for pensions. 1 Moreover, Germany’s credit regime restricts access to mortgages, and homebuyers face high property transaction costs (Johnston et al., 2021; Wiedemann, 2021; Reisenbichler, forthcoming). Instead of considering housing as an asset from which to realize financial gains by climbing up or down the property ladder, Kofner (2014, p. 266) notes correctly that for many Germans “the motto is ‘Once in a Lifetime’: Those who become homeowners do so late, but with full commitment—and speculative motives only play a minor role in tenure choice.” Even if German homeowners wanted to capitalize on rising house prices, they would be limited by the country’s conservative mortgage system in which home equity loans are uncommon. Germans thus rarely trade up or down the property ladder, and few use housing wealth as leverage to finance consumption (Reisenbichler, 2022). Germany is considered a “nation of renters” in which roughly half the population rents (only 26% of all households own their home outright, while another 18% are owners with a mortgage) and public policy has for decades promoted stable housing costs (Führer, 2016; Kohl, 2017; Kohl & Sørvoll, 2022; Muellbauer, 2018).

Rising house prices are thus not an integral part of the country’s economic growth and welfare models, as German voters tend to treat housing as a place to live rather than an investment (Dancygier & Wiedemann, 2023). In socio-tropic terms, we therefore expect German voters, including renters but also homeowners, to evaluate rising house prices as a comparatively negative economic development for their country. First, German homeowners cannot leverage rising home values for consumer credit and spending, making it difficult for them to see how house-price gains would directly translate into broader economic activity. On the contrary, in Germany’s highly restrictive credit regime, homeowners likely perceive that booming home prices will make it more difficult for households to build or buy a home, which they likely associate with stifling economic activity. Second, in a majority-renter country in which homeownership is not the dominant form of housing tenure, German homeowners are likely aware that they constitute only about half the population, which makes it difficult for them to view rising home prices as a positive economic development that benefits the country as a whole (and not just homeowners like themselves). Third, German homeowners are also presumably aware that most Germans do not rely on asset-based or privatized welfare, which again means that German homeowners likely do not view house-price gains as a country-wide socio-economic benefit. Finally, much like British renters, we expect German renters to associate rising property values with rising housing costs and rents as well as with increases in the cost of living in the wider economy. 2 To summarize our socio-tropic predictions, we expect German voters to view rising house prices as a more negative economic development than British voters, driven mainly by the different house-price perceptions of both countries’ homeowners.

Finally, we have little reason to expect much cross-national variation in voters’ ego-tropic house-price evaluations, as those are based on an individual’s pocketbook concerns. In line with the existing literature (Ansell, 2014; Marble & Nall, 2021), we expect ego-tropic evaluations of rising house prices to be positive among homeowners in both countries, as they benefit from increased household wealth, the ability to sell a home at a higher value (and the ability to use the proceeds of the sale as a supplement for retirement or old-age care), and the ability to pass on a valuable asset to their children. 3 By contrast, we expect negative ego-tropic evaluations of rising property values among both countries’ renters, as they likely associate rising house prices with higher rental costs or higher entry costs in the property market. We will test the following hypotheses:

Evaluations of Housing Policies

For similar reasons, we also expect cross-national differences in housing policy preferences. As the German economy relies less on rising house prices as a growth and welfare strategy, German voters likely favor government interventions that tend to restrain house prices when compared to British voters. This should especially be the case for German renters, many of whom rent for a lifetime, but also for German homeowners who do not rely on growing housing wealth for consumer spending or old-age provision to the same degree as British homeowners. Relatedly, we also expect German renters and homeowners to show higher levels of support for affordable rental and homeownership policies than their British counterparts—that is, policies that expand access to affordable housing by lowering the cost of renting or homeownership.

In contrast, asset-price appreciation is key for growing the British economy and for most British households’ welfare. British homeowners especially have an incentive to protect their home values by restricting access to affordable housing (Ansell & Cansunar, 2021, p. 598). The literature on NIMBYism in the United States and UK has produced a wealth of evidence that homeowners often block new housing developments to preserve not only their neighborhoods but also the value of their most important asset by artificially restricting supply (Fischel, 2002; Hall & Yoder, 2022; Marble & Nall, 2021; O’Grady, 2020).

As a result, British voters are less likely to favor policies that restrain house prices compared to German voters. More specifically, we expect British homeowners to show lower levels of support for government actions to restrain house prices than German homeowners, as the former can capitalize on rising house prices more so than the latter. Relatedly, British homeowners should show lower levels of support for making renting and homeownership affordable when compared with German homeowners, since British homeowners might view restricting access to affordable housing as a means to protect home values and an unaffordable housing status quo from which they benefit. As reducing the cost of homeownership and renting broadens access to housing, British homeowners might associate such programs with additional housing in their local communities that could negatively affect their property values.

In contrast, British renters likely favor actions to restrain house prices and favor affordable rental and homeownership policies to lower their rental costs or help them onto the property ladder. However, we also expect British renters to favor restraining house prices to a lesser degree than German renters. While rising house prices increase the cost of buying property in both countries, the majority of British renters are aspirational (UK Government, 2023), unlike their German counterparts. As a result, British renters might tolerate rising house prices more than German renters, as rising property values make housing an attractive investment class with anticipated future investment returns from asset-price appreciation after becoming homeowners (Ansell et al., 2022, p. 1423). We will test the following hypothesis:

The perceived and actual effects of affordable homeownership and rental policies are complex (Nall et al., 2022). Our assumption is that voters view such policies as making housing cheaper and more accessible by reducing an individual’s housing costs. However, the reality is that such policies often have the opposite effect of driving up housing costs and prices. For example, renter-oriented policies designed to bring down rental costs, such as rent controls, can paradoxically increase housing costs by deterring investment and thus stifling new home building. Similarly, owner-oriented programs often have the goal of “making homeownership more affordable and thus accessible” by subsidizing the demand-side of purchasing a home, with hoped-for supply-side effects of building more homes (Carozzi et al., 2020, p. 1). However, such policies often drive up house prices and thus make homeownership even less affordable. For example, first-time buyer subsidies or credit programs like the German Baukindergeld or the British Help to Buy Program were designed to lower the cost of homeownership and stimulate owner-occupied housing construction (Johnson, 2022; Scholz, 2018). 4 Yet, both programs did not stimulate much new construction and instead drove up house prices in supply-constrained areas (Carozzi et al., 2020; Sachverständigenrat für Wirtschaft, 2018, pp. 373–376).

For the purpose of our analysis, we assume that voters view renter- and owner-oriented programs as lowering the cost of housing, thus making housing more affordable and accessible, not least because policymakers advertise these programs in such ways. Consequently, we expect existing British homeowners to show little support for affordable housing programs, hoping to protect an unaffordable housing status quo from which they benefit.

To explore what might lie behind the expected cross-national variation in housing policy preferences, in a final step, we investigate the individual-level relationship between housing policy preferences and house-price perceptions. This part of the empirical analysis below allows us to probe whether individuals who are satisfied (or dissatisfied) with rising house prices also favor certain housing policies over others, or whether other individual-level variables are more important correlates of housing policy preferences. It thus also allows us to discern whether differences in house-price perceptions between German and British voter groups can help account for the predicted cross-national differences in policy preferences. Our goal here is to reveal which types of voters (and attitudes) are associated with different kinds of policy preferences.

Case Selection and Research Design

We selected the UK and Germany as two diverse cases (Seawright & Gerring, 2008). Both countries differ along several crucial dimensions in comparative political economy: welfare regimes (liberal vs. conservative), electoral systems (SMD vs. mixed/PR), multi-level governance (unitary vs. federalist), and forms of capitalism (liberal or demand-led vs. coordinated or export-led). At the same time, the economic performance of both countries was comparable when the survey was fielded in 2022 (see Appendix A1 for more information on the comparative economic context). Most importantly, both countries experienced a prolonged boom in real house prices, which increased by 21% in the UK and even 46% in Germany between 2015 and early 2022, making it a comparable setting for the survey (OECD, 2024).

Choosing these two diverse cases allows us to discern how similar types of social groups, such as homeowners, might have different attitudes and policy preferences toward rising house prices, owing to both countries’ different institutional contexts (Wiedemann, 2021, pp. 19-20). As mentioned above, German homeowners rely much less on house-price appreciation for consumer spending or old-age provision than British homeowners. As a result, their housing attitudes and policy preferences might differ from their British counterparts. Such cross-national variation has thus far been under-theorized, and our comparative design sheds light on potential differences in housing attitudes and policy preferences among similar voter groups in the two countries.

Our cases also represent a larger population of countries (Slater & Ziblatt, 2013). The UK mirrors a host of countries with liberal credit and welfare regimes as well as high rates of homeownership, such as the United States, Canada, or Australia. Germany is part of a small set of countries with restrictive credit regimes, generous public welfare and pensions, and low homeownership rates, including Austria. While we chose only two cases for our study, we expect our findings to be relevant for this broader population of cases.

Our data comes from an original survey that we fielded in summer 2022. The 675 participants from Germany and 677 participants from the UK were recruited from an online panel of the certified panel provider Bilendi, using quotas for homeownership, age, and gender (see Appendix A1). As the next sections show, the goal of our survey was three-fold: to examine how voters feel about house-price changes in different socio-economic contexts; to shed light on voters’ housing preferences in a comparative setting; and to probe the individual-level determinants behind housing policy preferences, including the role of house-price perceptions.

Voter Perceptions of Rising House Prices

We designed our survey to account for previously under-appreciated cross-national differences in how voters evaluate rising and falling house prices. Thus far, much of the literature operates under the assumption that voters would have relatively similar ego-tropic or socio-tropic views on rising or falling house prices. With questions designed to probe voters’ attitudes towards rising house prices, including an experimental component, we test those assumptions. 5

Measures

For the comparison of British and German voters’ attitudes towards house-price changes, we employ two different approaches and measures. First, we directly asked voters to evaluate house-price changes, such as whether they considered rising house prices to be (i) a good thing for themselves personally and (ii) a good thing for their country. Using a 5-point scale, with response options ranging from “do not agree at all” to “completely agree,” respondents were asked to evaluate the following statements: “Generally speaking, rising house prices are good for me personally” and “Generally speaking, rising house prices are good for the British [German] economy.” These two variables allow us to investigate directly who deems increasing house prices as a positive development.

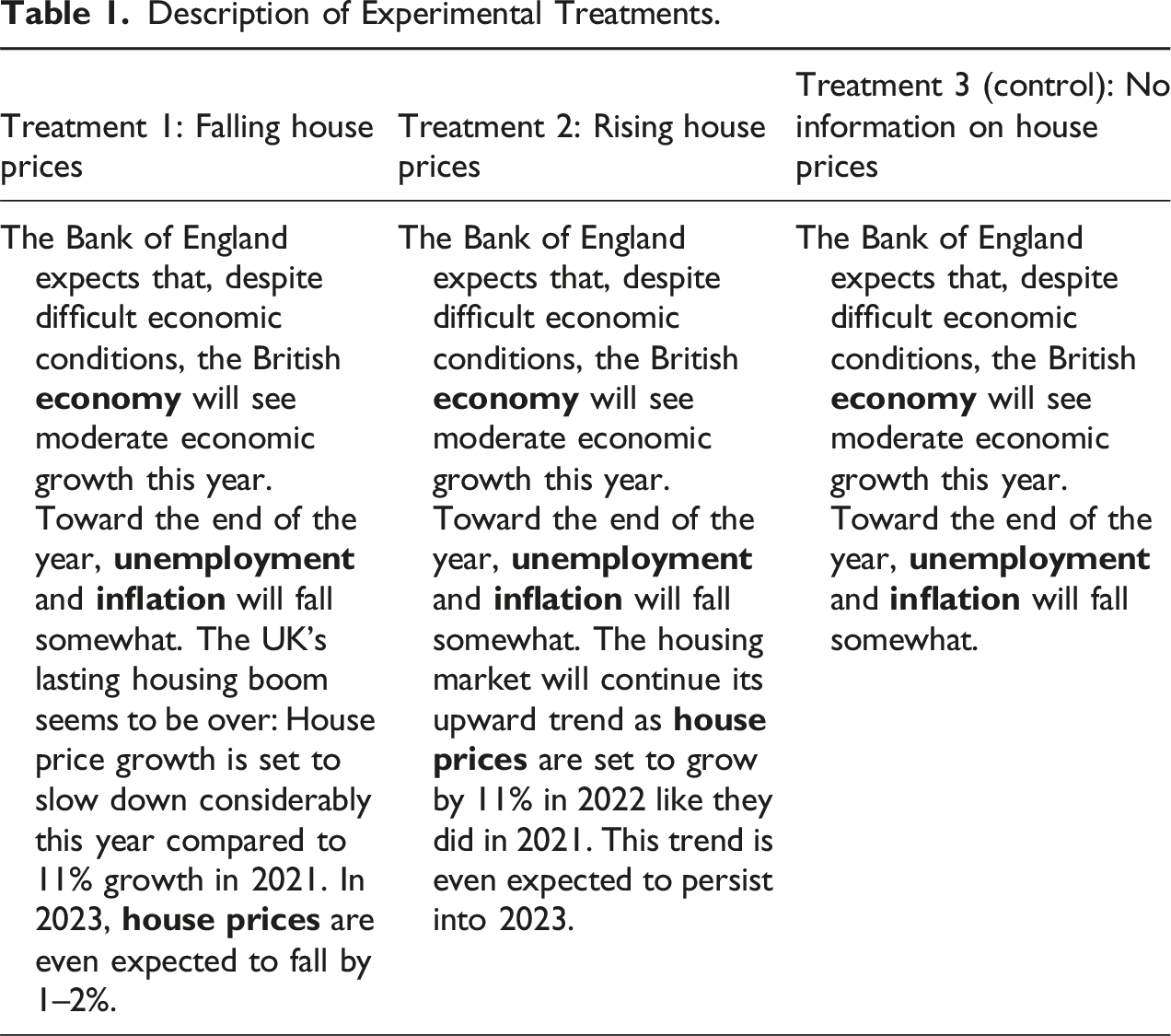

Description of Experimental Treatments.

Directly after these treatments, we asked participants to state whether they viewed the presented economic outlook as positive or negative (a) for themselves and (b) for their country (scaled from 1 to 7). Consequently, we can infer that any differences with respect to respondents’ ego- and socio-tropic evaluations between the experimental groups were the result of respondents’ differing reactions to changes in house prices that they read.

We chose an unambiguously positive economic outlook on economic growth, unemployment, and inflation, and therefore expect the control group, which received no house-price information, to react with overall positive ego-tropic and socio-tropic views on the presented outlook. For the treatment groups, adding different house price projections allows us to tease out which kind of housing information either (i) reinforces respondents’ positive view of the economy or (ii) contradicts an overall positive outlook by leading respondents to evaluate an otherwise positive economic outlook in more negative terms.

Findings

For ease of interpretation, we rescaled all variables to the range of 0–1 before estimating the models. We start by presenting evidence from our survey item that asked whether respondents view rising house prices as a good thing for themselves (ego-tropic) and for the country (socio-tropic). The correlation between respondents’ direct ego-tropic and socio-tropic evaluations of rising house prices is r = 0.56. Although there is a moderate correlation, what voters perceive to be a good development for themselves is not automatically viewed as a good development for the country. They are related but distinct evaluations.

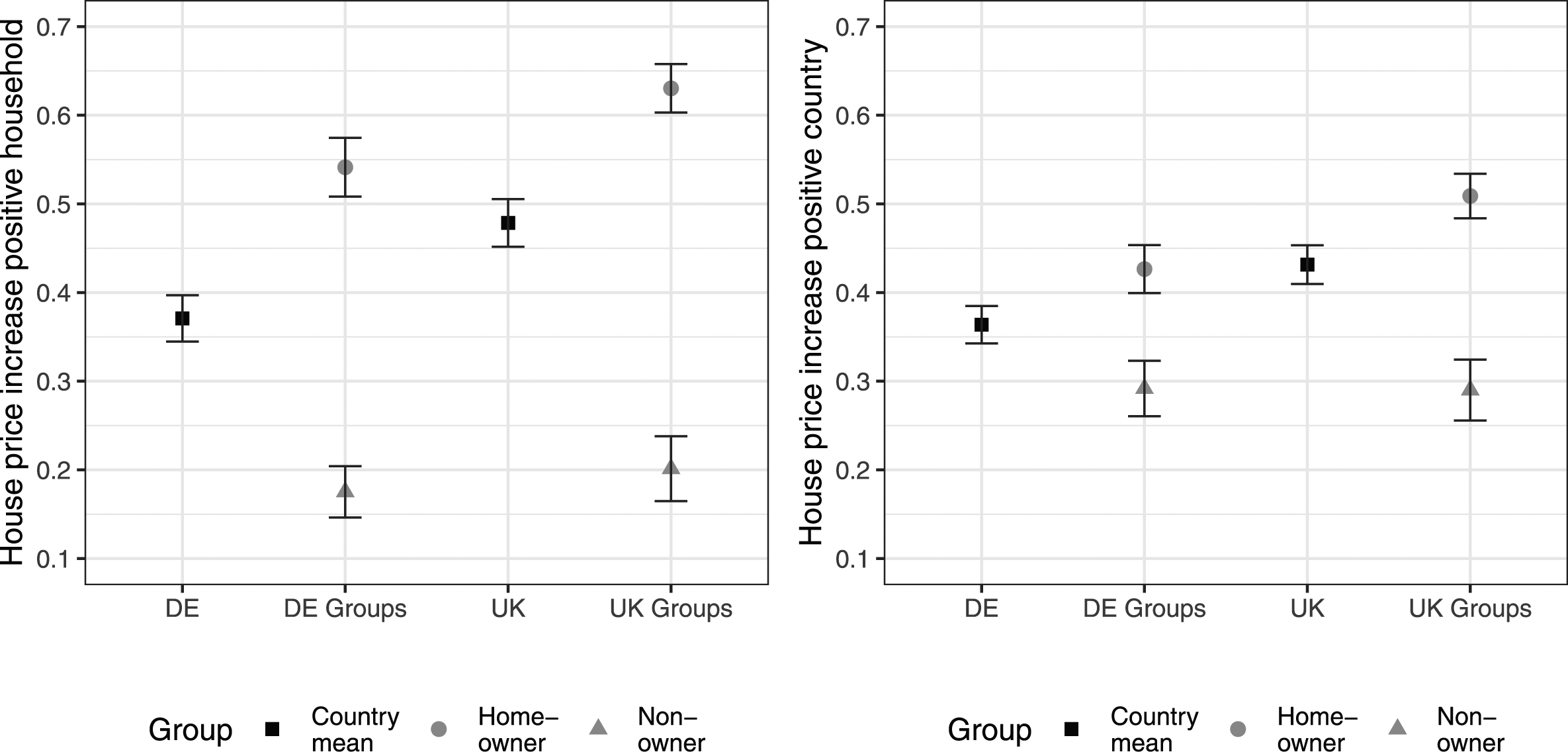

As Figure 1 indicates, there are clear differences in German and British house-price perceptions. On average, British voters view rising house prices more positively than German voters in both ego-tropic (left panel) and socio-tropic terms (right panel). As both countries’ renters show similar levels of disapproval of rising house prices in both ego-tropic and socio-tropic terms, the different national averages are primarily driven by the perceptions of homeowners. Homeowners, who make up a larger share in the UK than in Germany, tend to view rising house prices more positively than renters in both countries. Direct evaluations of changing house prices as a good development for oneself (left) and for the economy (right), by homeowners and non-owners (scale from 0 to 1).

However, there are important differences in house-price perceptions between German and British homeowners. In ego-tropic terms, both German and British homeowners view rising house prices as positive developments for themselves, with average scores above the scale’s mid-point of 0.5. Nonetheless, German homeowners show lower levels of approval than British homeowners, likely because German owners cannot leverage rising home values for consumer spending, while British owners can. 8 In socio-tropic terms, German homeowners evaluate rising house prices more negatively than British homeowners. Strikingly, German homeowners’ average responses are even below the mid-point of 0.5, while those of British homeowners are above the mid-point. 9 These findings provide initial support for H1a and H1b.

These country differences are further corroborated by our experimental evidence on how voters react to differing information about house-price changes embedded in an economic outlook, which includes three informational treatments: (i) rising house prices, (ii) falling house prices, and (iii) and no house-price information.

10

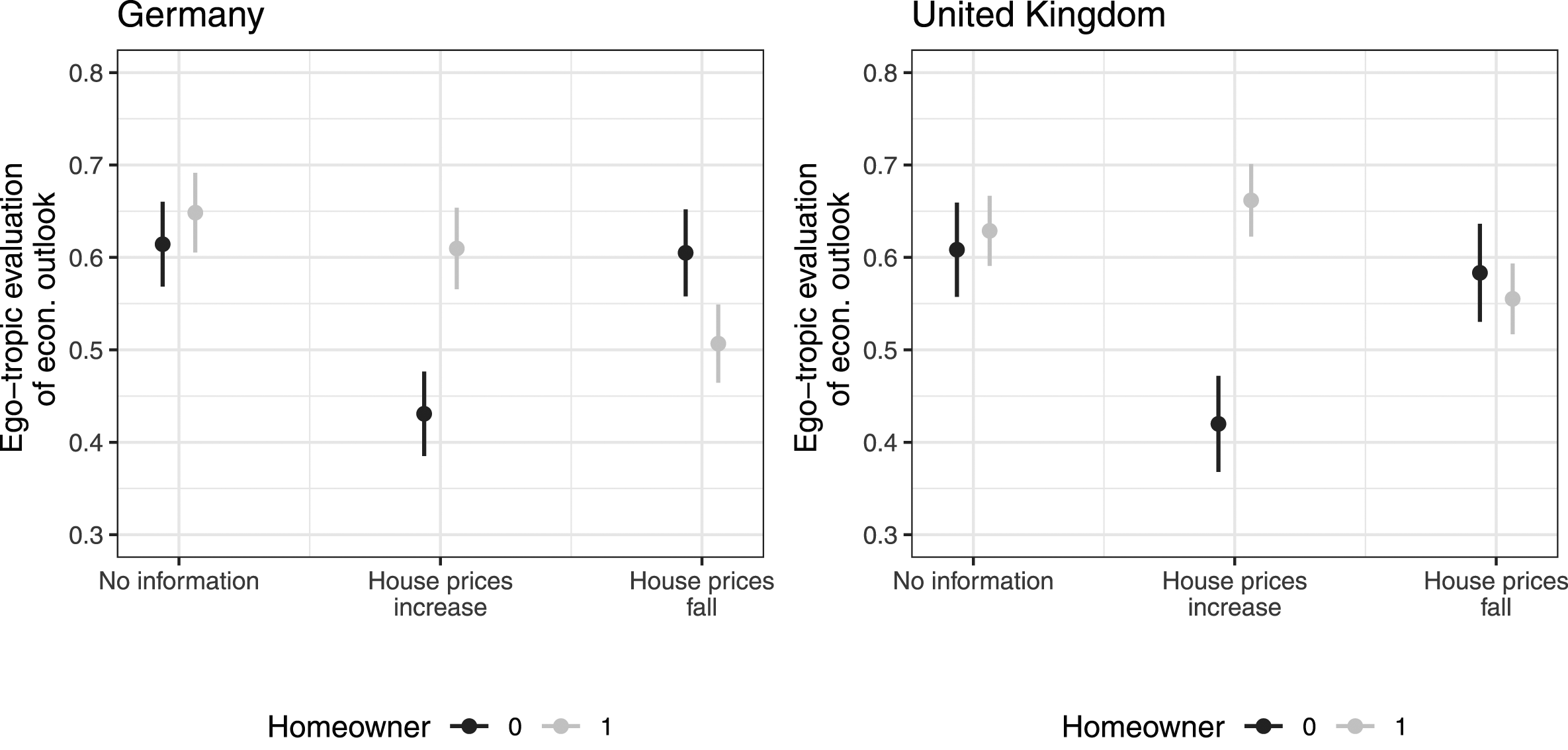

The results for ego-tropic house-price evaluations are in line with studies on pocketbook effects (Ansell, 2014; Cohen, 2023; Marble & Nall, 2021). As Figure 2 shows (see Appendix A3-A5 for regression tables), German and British homeowners evaluate an economy—with moderate economic growth, falling unemployment, and falling inflation—much more positively for themselves when house prices rise compared to when house prices fall.

11

For both countries’ homeowners, rising house prices mean gains in household wealth, while falling property values mean the opposite. Even though German homeowners do not rely on rising home values as leverage for personal spending, they still derive various material benefits from rising prices, such as being able to sell their homes at a higher value; leaving their children a home that appreciated in value; and producing a sense of financial security in otherwise uncertain economic times. By contrast, the inverse is true for German and British non-owners. They prefer an economy with falling property values for their pocketbooks—likely due to the expectation of lower rental costs—over an economy with rising house prices that they might associate with higher rents. Ego-tropic evaluations of the presented economic outlook in Germany (left) and the UK (right) for homeowners and non-owners (scale from 0 to 1). X-axis labels refer to experimental treatments.

In short, we conclude that both countries’ homeowners regard an economy with rising house prices to be in their material self-interest, while renters view an economy with falling house prices to be beneficial to theirs. We therefore find strong support for H1b.

While Figure 2 shows that the treatments of falling and rising house prices elicit different ego-tropic reactions among respondents, the reactions of the treatment groups are not always different from those of the control groups. In both countries, homeowners in the control group (no housing information) and treatment group (rising prices) had somewhat similarly positive ego-tropic reactions. The same is true for renters in the control group and treatment group (falling prices). Our interpretation is that the control group evaluated good news on unemployment, economic growth, and inflation as positive for themselves. Adding a treatment that homeowners perceive to be another piece of good economic news—rising house prices—likely reinforced their view of an economy that benefits them. The same logic likely applies to renters: adding a treatment that they consider good economic news—falling house prices—reinforced their view of an economy that serves their material interests. 12 Compared to the control group, however, homeowners do respond much more negatively to a scenario of falling house prices, and so do renters when faced with a scenario of rising house prices.

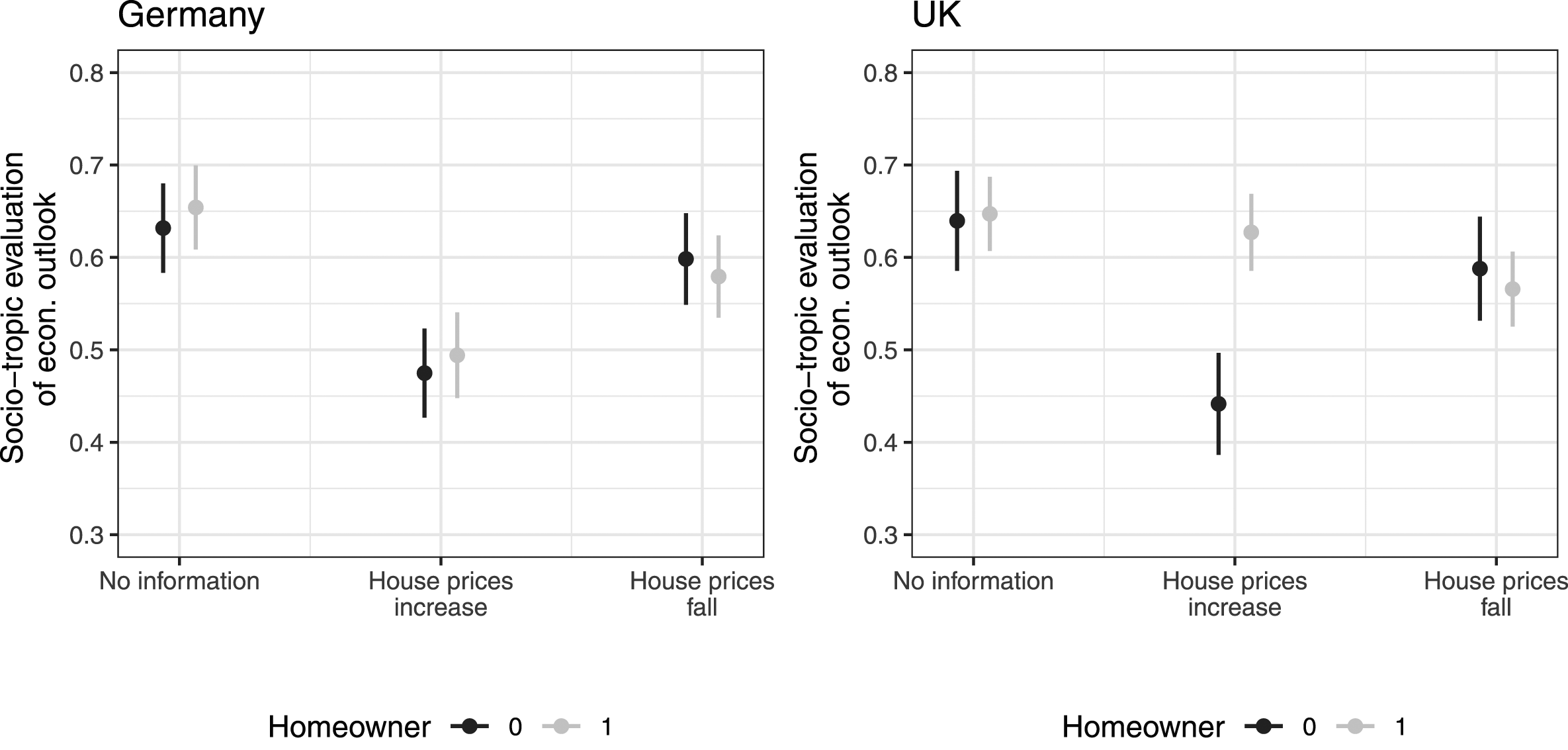

A strikingly different pattern emerges in our socio-tropic experimental findings. Turning to Figure 3, homeowners in the UK view an economy experiencing rising house prices to be much better for the country than an economy with falling house prices. The inverse is true for British renters.

13

In contrast, both German homeowners and non-owners view an economy with rising house prices as relatively negative for their country when compared to an economy with falling house prices. German voters, on average, consider the economy to be in better shape when house prices fall compared to when house prices rise.

14

Socio-tropic evaluations of the presented economic outlook in Germany (left) and the UK (right) for homeowners and non-owners (scale from 0 to 1). X-axis labels refer to experimental treatments.

After a decade of rising home values, German homeowners seem to view further increases in home prices as detrimental for the economy. We interpret this finding to mean that German homeowners see little economy-wide benefit in continued rises in house prices. First, they cannot convert rising home equity into consumer spending that would stimulate the wider economy. Second, they might be concerned that rapidly rising house prices could produce speculative financial bubbles that could destabilize the wider economy. Third, they might not see how rising home prices have wider socio-economic benefits beyond homeowners themselves. One important implication from our experimental findings is that, by viewing rising house prices as a relatively negative development for the economy, German homeowners act more like German or British renters than British homeowners in this respect.

We thus find strong support for H1a that German voters view rising house prices as a negative development for their country, while British voters view rising home prices more favorably, a finding mainly driven by the different house-price perceptions of both countries’ homeowners. 15 Our findings thus point to important and previously under-appreciated cross-pressures: German homeowners view rising house prices as a positive economic development for themselves, but as a relatively negative one for their country. 16

To some extent, these findings challenge a common socio-tropic (or geo-tropic) assumption in political science research on housing. We find that voters do not generally perceive rising house prices as a positive development for their country (Adler & Ansell, 2020; Ansell et al., 2022; Larsen et al., 2019). This assumption neither holds for German homeowners nor German or British renters in the analysis above. However, one limitation of our survey findings is that we analyze voter perceptions of national—but not local—house-price developments. We therefore cannot rule out that voters would have provided different responses if asked to evaluate changes in local house prices.

Voters’ Housing Policy Preferences

In a first step, this section shows descriptive variation in German and British voter groups’ housing policy preferences. Going beyond previous studies, we asked respondents about their views on (i) whether government interventions should restrain house-price growth and (ii) on a range of owner- and renter-oriented policy instruments. In a second step, we use these different measures of housing policy preferences as dependent variables in a series of regression models. Doing so allows us to investigate the individual-level relationship between voters’ house-price perceptions and housing policy preferences, including whether our experimental treatments are associated with differences in housing policy preferences. Differences in house-price perceptions may also account for cross-national variation in housing policy preferences among German and British voter groups. The analysis furthermore sheds light on the degree to which several other theoretically-informed determinants correlate with housing policy preferences—that is, which voter groups and attitudes correlate with certain kinds of housing policy preferences.

Measuring Housing Policy Preferences

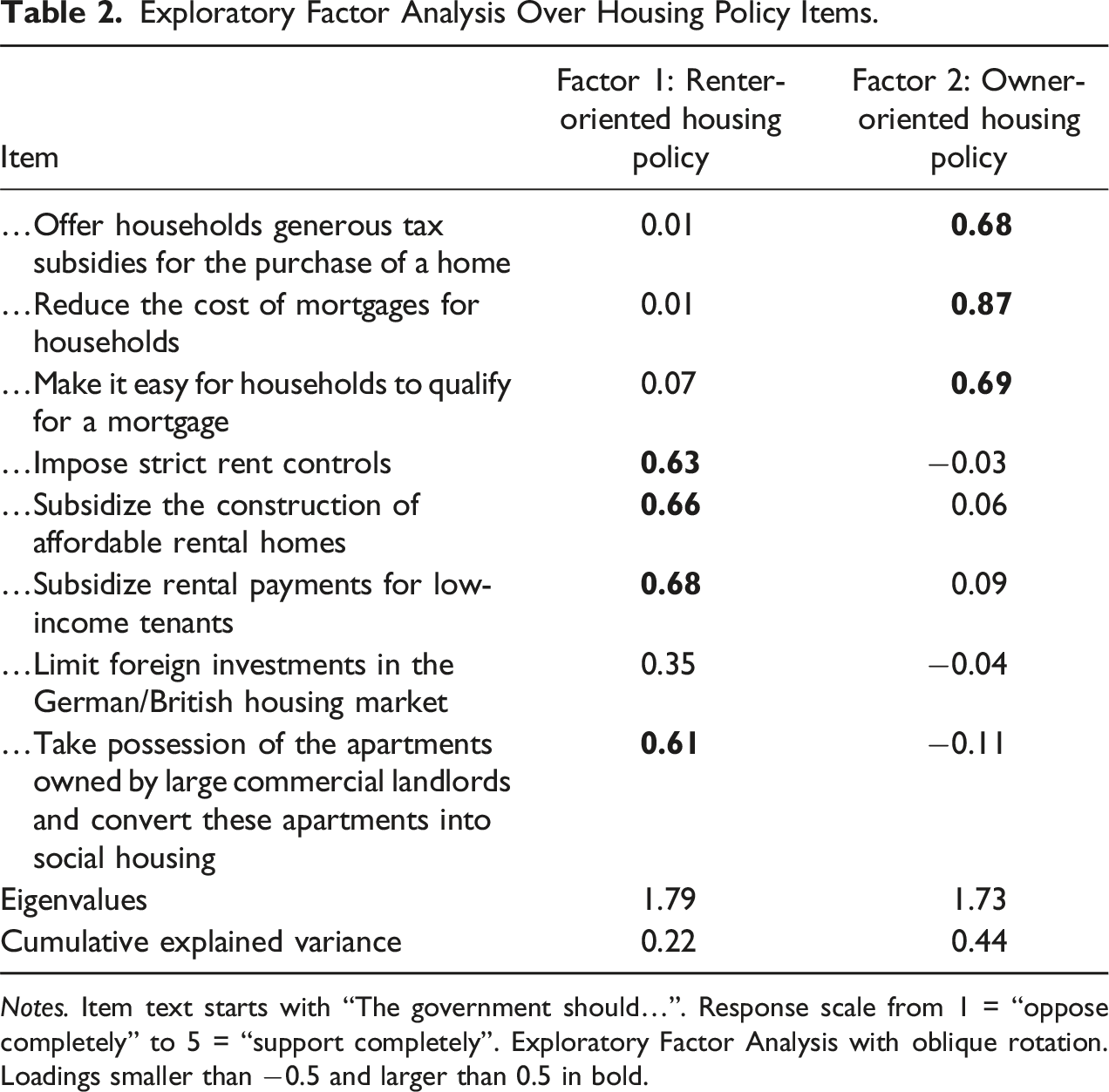

Exploratory Factor Analysis Over Housing Policy Items.

Notes. Item text starts with “The government should…”. Response scale from 1 = “oppose completely” to 5 = “support completely”. Exploratory Factor Analysis with oblique rotation. Loadings smaller than −0.5 and larger than 0.5 in bold.

The resulting index variables of housing policy preferences are thus conceptually similar to Ansell and Cansunar’s (2021, p. 599), who define it as “attitudes to government intervention in the housing market in order to make housing more affordable (by subsidizing either housing construction or providing resources to citizens to help them afford housing)”. But our measures also improve upon existing work by distinguishing between renter and homeowner support and by including more fine-grained items that cover a range of specific policy measures that other studies have not yet captured. 21

Descriptive Findings: Cross-National Variation in Housing Policy Preferences

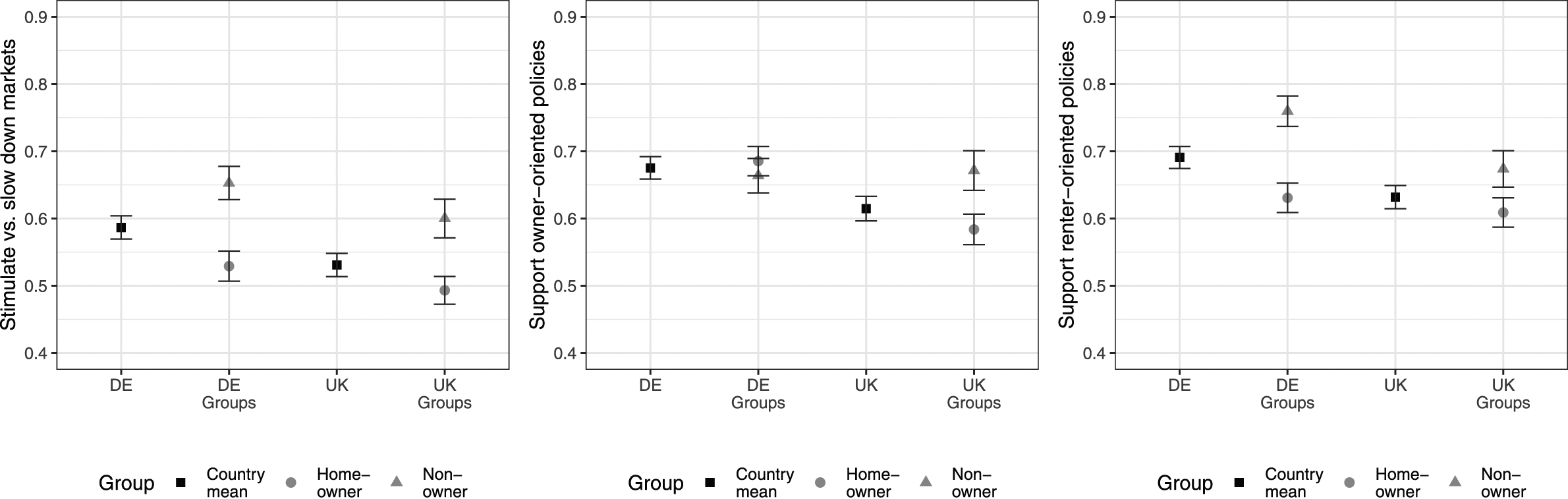

Figure 4 visualizes the mean values for our three housing policy preference variables: support for policies restraining housing markets and prices as well as the two scales of homeowner-oriented and renter-oriented policies. In general, the results show that German voters have more favorable attitudes towards government interventions that make housing more affordable than British voters, which is line with H2.

22

Housing policy preferences by country and housing tenure. Variables rescaled ranging from 0 to 1. Lower scores in the left panel represent support for stimulating housing markets and prices, while higher scores mean support for cooling housing markets and prices.

Figure 4 (left panel) indicates, first, that German voters are more supportive of government interventions that restrain housing markets and prices (higher scores) than British voters. Even German homeowners have a slight preference for deflating measures that would restrain house prices, while British homeowners have a slight preference for stimulative measures that would boost house prices. Both countries’ renters have a strong preference for deflating measures that would dampen prices, although German renters show higher values compared to British ones.

Second, German voters show higher average scores regarding both owner- and renter-oriented policies. In terms of owner-oriented policies, British homeowners show the lowest levels of support for policies aiming at affordable homeownership among all groups, likely because they view restricting access to homeownership as protecting their property values on which they depend in the context of ungenerous public pensions and liberal welfare (see Figure 4, middle panel). In contrast, German homeowners are significantly more supportive of making homeownership affordable, likely because they have fewer incentives to boost property values through restricting access to homeownership. Renters in both countries show similarly high levels of support for owner-oriented policies, likely because many of them are aspiring homeowners or know people who are.

Third, in terms of renter-oriented policies, both German homeowners and non-owners show higher levels of support toward making renting affordable compared to their British counterparts (see Figure 4, right panel). It is striking that German renters show much higher support for rental housing policies than British renters. The difference could be explained by the fact that for many Germans renting is the norm in the context of relatively generous public pensions, while many British renters aspire to become homeowners partly treating homeownership as a form of privatized welfare in old age.

Regression Analysis: Measures

We now turn to the individual-level determinants of housing policy preferences by using the above variants of housing policy support as dependent variables. We regress these dependent variables on a range of theoretically informed independent variables from our survey, focusing especially on the role of voters’ house price perceptions. These regression analyses allow us to identify which voter groups (and attitudes) are correlated with certain kinds of housing policy preferences, and whether these predictors can potentially account for the cross-national variation in housing policy preferences we found for German and British voter groups.

Our main set of independent variables includes two variants of house-price perceptions. First, we include respondents’ direct evaluations of house prices—that is, rating rising house prices as (i) a good thing for themselves and (ii) a good thing for their country. These two (pre-treatment) variables allow us to investigate how individual-level house-price perceptions are related to housing policy preferences. Second, we also include the experimental treatments—prompting respondents with different house-price projections—which allows us to see whether the informational treatments are associated with voters’ housing policy preferences.

Moreover, we include an important set of control variables. An important control variable potentially related to housing policy preferences is voters’ financialization attitudes—that is, their attitudes toward borrowing, credit-financed spending, and leveraging one’s own home. Including financialization attitudes allows us to capture the growing yet varying importance of assets in households’ everyday lives (Bohle & Seabrooke, 2020; Fligstein & Goldstein, 2015; Montgomerie, 2020; Pagliari et al., 2020). For example, while some voters might view housing primarily as an asset that is supposed to grow in value over time and from which to extract financial gains, others might primarily view it as a place to live (Dancygier & Wiedemann, 2023). As recent scholarship has shown, attitudes toward financialization generally (Wiedemann, 2021, p. 206) and housing financialization specifically (Dancygier & Wiedemann, 2023) might also structure social or housing policy preferences.

We measure financialization attitudes in two distinct ways. First, we include a variable based on a bipolar rating question about whether voters view housing mainly as a place to live or mainly as an investment opportunity (scaled from 1 to 11). Second, we construct an index on respondents’ attitudes toward financialization based on a set of twelve indicators that we asked respondents prior to the experimental treatments. Four items asking about respondents’ money attitudes were taken from the monetary security scale by Furnham et al. (2012), five further items asked about their attitudes toward consumption, credit, and debt. We newly devised two of these items for this study, while the other three items are from Wiedemann (2021, p. 285) (Items 6 & 8) and the Federal Reserve Board (2019) (Item 9). Based on studies describing differences regarding attitudes toward housing as a financial asset (Fligstein & Goldstein, 2015), we formulated three additional items (Items 10, 11, 12) that refer specifically to housing as an asset that people can leverage to finance consumption. To create the measure, we added the items loading on the first dimension of an exploratory factor analysis (see Appendix A15 for results, Cronbach’s Alpha of the additive measure is 0.78). 23

We also include homeownership status as an important socio-demographic control variable potentially associated with housing policy preferences. Social policy attitudes are another important control, as respondents’ housing policy preferences are likely related to their general redistributive preferences (Ansell & Cansunar, 2021, p. 604). To capture participants’ views on social policy, we use a standard item from the German Longitudinal Election Study (Roßteutscher et al., 2017), asking whether people prefer lower taxes even if this means fewer social benefits or prefer more social benefits even if this means higher taxes. This bipolar measure is scaled from 1 to 11. Our survey also includes common socio-demographic variables: gender (female, non-binary, male, transgender), age, and formal education. As a proxy for income, we include a measure on subjective socio-economic status, using the MacArthur Scale running from 1 (very low social status) to 11 (very high social status). 24 Importantly, all survey items that we use as independent variables and controls were asked prior to the treatments.

Regression Analysis: Findings

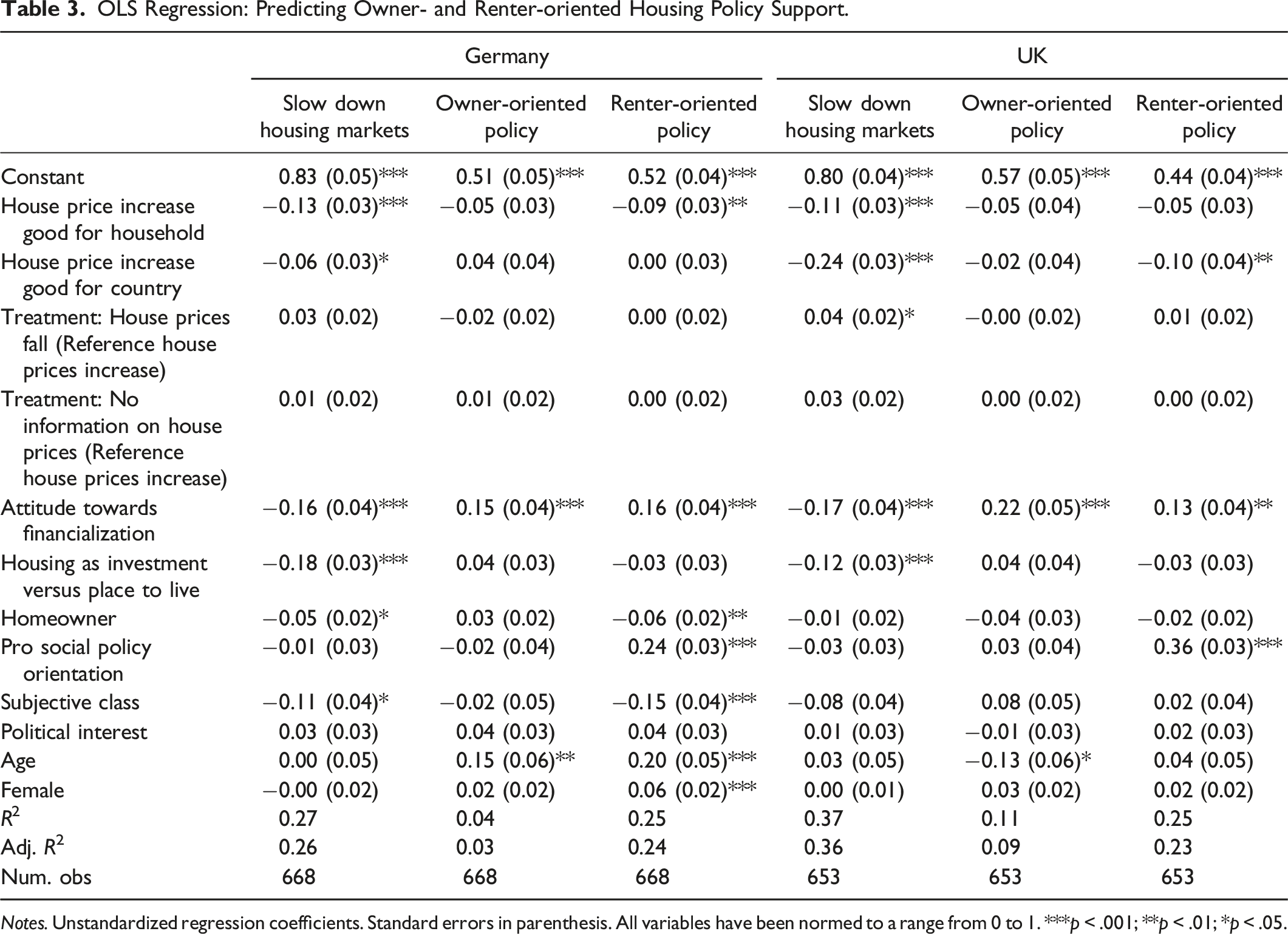

OLS Regression: Predicting Owner- and Renter-oriented Housing Policy Support.

Notes. Unstandardized regression coefficients. Standard errors in parenthesis. All variables have been normed to a range from 0 to 1. ***p < .001; **p < .01; *p < .05.

For the models predicting support for policies restraining housing markets and prices, we find relatively strong associations with respondents’ house-price perceptions (our main independent variables). Indeed, we find that voters’ positive ego-tropic and socio-tropic house-price evaluations are correlated with a policy preference for stimulating rather than deflating housing markets and prices in both countries. In other words, unsurprisingly, respondents who view rising house prices positively (for themselves and/or the country) tend to show higher support for stimulative housing measures that grow house prices rather than deflating measures that dampen prices. While the associations of ego-tropic house-price evaluations are relatively similar in both countries, the magnitude of socio-tropic ones differs. In the UK, viewing rising house prices as positive for the economy is the strongest predictor of a preference for stimulating rather than cooling housing markets and prices, while the association is much weaker in Germany. In line with our argument, British voters seem to view rising house prices as a sign of a healthy economy, while this is less the case in Germany. Our informational treatments on different house-price scenarios, however, are not statistically significant, and we also do not obtain significant conditional relationships when interacting the treatments with homeownership (see Appendix A21).

We also find that support for policies restraining housing markets and prices strongly correlates with some control variables, particularly voters’ attitudes toward financialization. Indeed, stronger financialization attitudes are associated with higher demands for government actions that stimulate rather than deflate housing markets and prices in both countries. Another proxy for household financialization—considering a house as an investment rather than a place to live—is similarly associated with a preference for measures that fuel house-price growth. Voters with favorable views toward borrowing and leveraging home equity thus prefer policies that inflate housing markets and prices over those that would deflate them. Homeownership and higher subjective class (i.e., a proxy for income) are also weakly associated with a preference for stimulating measures that grow house prices, but only in Germany. 26

When it comes to the models predicting support for owner- and renter-oriented policies, we find only weak associations with voters’ house-price perceptions. There is some evidence that respondents’ positive house-price evaluations negatively affect rental policy preferences in both countries, but the coefficients are small. More precisely, German voters who view rising house prices positively for themselves—and British voters who view rising property values positively for the economy—tend to show lower levels of support for renter-oriented policies. Moreover, there is no significant relationship between voters’ evaluations of house prices and owner-oriented policies. The informational treatments again are not statistically significant. 27

Rather, some of our control variables are stronger and more consistent predictors of renter- and owner-oriented policy preferences. Attitudes toward financialization are positively associated with a preference for making both owner-occupied and rental housing more affordable. 28 A possible reason is that financialization attitudes are likely related to greater demand for government intervention to mitigate personal financial risk (Wiedemann, 2021). For example, renters who rely on credit to finance their expenses should care about renter affordability, while indebted homeowners—or aspiring homeowners planning to take on debt in the future—should support homeownership affordability to lower the cost associated with owning a home. 29 Our data, however, does not distinguish between aspiring or mortgaged homeowners, which makes our interpretations necessarily tentative. 30

The other control variables show relatively inconsistent relationships with renter- or owner-oriented policy preferences. First, homeownership status is negatively associated with support for renter-oriented policies in Germany only (although the coefficient is small), which suggests that homeownership itself is a rather weak predictor of housing policy preferences. Second, a pro-welfare attitude shows a strong positive association with support for rental policies in both countries, meaning that voters likely perceive rental housing policies—but not homeownership programs—to be redistributive welfare policies. Third, German respondents, who perceive themselves to have lower socio-economic status, show higher support for renter-oriented policies than those with a higher status. Fourth, women in Germany appear to want stronger renter-oriented housing policy, although the association is substantively small. Finally, age is an important predictor for rental and homeownership policy preferences, but it differs between the two countries. While higher age in Germany is positively associated with support for renter- and owner-oriented housing policies, the relationship is negative in the UK. This could reflect British homeowners’ fear that government interventions might reduce their property values essential to old-age security. In Germany, in contrast, people become homeowners later in life, if at all, and this could be why they support owner-oriented policies with increasing age.

Overall, we conclude that voters’ perceptions of house prices are relevant but relatively weak predictors of housing policy preferences (also see Kohl & Hadziabdic, 2022, p. 946). Strikingly, while our house-price treatments clearly show an effect on how voters evaluate their personal and/or national economic wellbeing, the treatments are not associated with voters’ housing policy preferences. In other words, voters’ housing policy preferences seem unaffected by house price projections. Rather, other individual-level dispositions, such as social welfare or financialization attitudes, show overall stronger associations with housing policy preferences.

Conclusion

In the context of a growing housing affordability crisis in rich democracies, our article sheds new light on voters’ house-price perceptions and housing policy preferences. We contribute to the comparative politics literature on housing in several ways.

First, we identify previously under-appreciated cross-national variation in voters’ house-price perceptions. Our experimental evidence shows that British voters view rising house prices as a more favorable economic development than German voters, which we trace back to both countries’ different institutional contexts of welfare, credit, and housing regimes. The difference is most striking among both countries’ homeowners: British homeowners regard rising house prices as a sign of national economic health, while German homeowners do not. In other words, homeowners’ reactions to rising house prices likely depend on their positioning in a country’s institutional context. In more generalizable terms, homeowners might view rising house prices as a cause for celebration in contexts of liberal credit and welfare (i.e., UK, United States, Canada, and Australia), but as a cause for concern in contexts of generous welfare and restrictive credit (i.e., Germany and Austria). Irrespective of institutional context, renters seem to view rising house prices as a negative economic development not only for themselves but also for their countries. Our findings thus help us rethink a major assumption in existing research on the politics of housing, positing that voters would tend to regard rising house prices as signs of national economic health across advanced economies (Adler & Ansell, 2020; Ansell et al., 2022; Larsen et al., 2019). Our evidence, however, is restricted to voters’ perceptions of national—but not local—house-price developments, which could be an important avenue for future research.

Through a custom survey, second, we provide more comprehensive and fine-grained measures of housing policy preferences than previous studies. By asking respondents about a battery of housing policy instruments, we were able to identify two systematically related dimensions of housing policy preferences: (i) policies that make homeownership more affordable and (ii) policies that make renting more affordable. Conventional measures of voter demand for housing programs either relied on relatively broad housing policy items from institutional surveys, such as whether the government has a responsibility to provide decent housing (Ansell & Cansunar, 2021), or asked about voters’ views on an individual housing policy from custom surveys, such as rent control (Cohen, 2023; Dolls et al., 2023; Hager et al., 2023; Müller & Gsottbauer, 2022), restricting foreign housing investments (Löffler & Pond, 2023), new homebuilding (Hankinson, 2018; Marble & Nall, 2021; O’Grady, 2020), or landlord expropriation (Dancygier & Wiedemann, 2023). Our study covers a broader range of housing policy preferences regarding both homeownership and renting than is covered by previous studies.

Third, our findings suggest that there are important cross-national differences in housing policy preferences, even when comparing similar types of voters across countries. We find that German voters have more favorable attitudes towards restraining house-price growth and making housing affordable than British voters. German voters are not only more supportive of government interventions that restrain house-price growth compared to British voters, but German voters also show higher levels of support for affordable rental and homeownership policies than British voters. We find especially striking differences between German and British homeowners. German homeowners show higher levels of policy support for restraining house prices as well as for rental and homeownership programs than their British counterparts. British homeowners likely view restricting access to homeownership and rental housing as a means to protect their property values and an unaffordable status quo from which they benefit in the context of ungenerous public pensions and a permissive credit regime that allows them to leverage housing wealth. In contrast, German homeowners are less concerned with boosting property values in the context of relatively generous pensions and restrictive credit.

Our findings suggest that institutional features play an important role for housing policy preference formation (Wiedemann, 2021), although more research on the precise institutional mechanisms is needed to substantiate our conclusions. In general, we expect our findings to be representative of a broader population of countries with liberal credit and welfare regimes, such as the United States, Canada, and Australia, and countries with restrictive credit and generous welfare models, such as Austria.

The policy implication resulting from our findings is that German policymakers have an electoral interest in restraining house-price growth, while British policymakers have more incentives to stimulate house prices. In turn, these different political interests can then translate into differing but consequential economic outcomes. In the UK—as well as in the United States, Canada, and Australia—policymakers have incentives to fuel asset-price booms as a growth and welfare strategy, while simultaneously running the risk of producing financial instability. In Germany—and Austria—policymakers have more incentives to limit house-price growth, an approach that tends to limit the likelihood of housing-based financial crises.

Moreover, our study consistently finds polarizations between homeowners and renters in terms of house-price perceptions and policy preferences in the context of rising property prices. Renters in both countries show much higher levels of disapproval of rising house prices when compared to homeowners, and renters also show higher levels of support for government actions to make housing more affordable compared to homeowners. As the spoils of growing housing wealth are unevenly distributed, housing likely is an important contributor not only to wealth inequality (Fuller et al., 2020) but also to political and intergenerational polarizations in rich democracies (Ansell & Cansunar, 2021; Dewilde & Flynn, 2021).

Finally, we also provide novel evidence on the individual-level determinants of housing policy preferences. Surprisingly, we find that voters’ house-price perceptions—that is, the degree to which they view rising house prices as a positive thing for themselves or the economy—is a relatively weak predictor of housing policy preferences. Rather, our observational evidence points to a previously underexplored factor that emerged as a key determinant of housing policy preferences: financialization attitudes. We find that attitudes toward borrowing, credit, and consumption are strongly associated with a preference for boosting house prices, likely because these voters view rising property values as an investment and/or borrowing opportunity. Financialization attitudes are also associated with a preference for making homeownership and renting more affordable, which can be interpreted as a form of financial risk protection for individuals that are indebted or planning to take on debt (Wiedemann, 2021). Future research might further explore financialization attitudes as an explanatory variable for social or housing policy preferences.

As our study is limited to two countries, future research might explore whether the findings travel to other advanced economies with generous welfare states and restrictive mortgage regimes as well as other high-homeownership countries with liberal welfare states and credit regimes. Scholars might also design innovative custom surveys to distinguish house-price perceptions, housing and social policy preferences, and voting behavior between outright, mortgaged, and aspiring owners in different institutional contexts.

Supplemental Material

Supplemental Material - Cause for Celebration or Concern? Voter Reactions to Rising House Prices

Supplemental Material for Cause for Celebration or Concern? Voter Reactions to Rising House Prices by Alexander Reisenbichler and Pascal D. König in Comparative Political Studies.

Footnotes

Acknowledgments

We would like to thank Charlotte Bartels, Asli Cansunar, Nicholas Fraser, Hanno Hilbig, Alison Johnston, Dustin Voss, Andreas Wiedemann, and the three anonymous reviewers for their valuable comments on earlier versions of this article. We are also grateful for financial support provided by the Minda de Gunzburg Center for European Studies (CES) at Harvard University.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Minda de Gunzburg Center for European Studies, Harvard University.

Data Availability Statement

The online appendix contains additional information and analyses. Replication data can be found at Reisenbichler & Koenig (2024).

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.