Abstract

When do governments adopt ambitious climate policy? Charting the theoretical territory between climate change politics and long-term policymaking, this paper highlights the role of electoral competition in shaping how politicians respond to the intertemporal tradeoff of one important climate change mitigation policy: fossil fuel taxation. The more secure the government is in office, the more insulated it is from the vagaries of political competition, and the more likely it is to impose costs on constituents today to generate a future stable climate. By influencing governments’ time preferences, competition structures the myopia of elected officials. I test the arguments using an original dataset of gasoline taxation across high-income democracies between 1988 and 2013. I find evidence that higher levels of electoral competition are associated with lower gasoline tax rates, and that the relationship is moderated by the level of costs imposed on voters, but not government partisanship. More generally, the analysis highlights when governments can increase consumer prices to address long-term challenges.

Introduction

Climate change is one of the most significant long-term policy challenges facing governments. To address it, economists have, for decades, advocated carbon pricing (Nordhaus, 1977). Increasing the price of fossil fuels should reduce their consumption and attendant carbon dioxide (CO2) emissions. However, despite its theoretical elegance and wide diffusion in climate policy discourse (Meckling & Allan, 2020), politicians have been slow to take up such advice. By some estimates, 85% of global greenhouse gas emissions remain unpriced (High-Level Commission on Carbon Prices, 2017) and only around a quarter of emissions from OECD and G20 countries are priced at or above €30 per tonne—the lower-end estimate needed to meet the objectives of the Paris Agreement (OECD, 2021).

One explanation for this lack of enthusiasm is that vote-seeking politicians are reticent about drawing the ire of voters who prefer low energy prices (Rabe, 2010, 2018). Indeed, a large body of survey research consistently finds that individuals dislike costly climate policies (e.g., Drews & Bergh, 2015; Jagers and Hammar, 2009; Shwom et al., 2010). Beyond the ballot box, governments are fearful of mass protest in response to tax rate hikes, such as recent ones by the gilets jaunes in France.

The political calculus of imposing costs may be improved if the associated benefits arrive quickly to voters; since voters and politicians tend to be impatient, preferring policy benefits that arrive earlier in time (Jacobs and Matthews, 2012; Sheffer et al., 2017). However, the primary benefit of carbon pricing—a stable climate—is a diffuse, global public good generated over decades. Further complicating matters, avoided climate change is the absence of future harm, rather than an increase in an easily understood and tangible consumption good, such as healthcare, infrastructure, pensions, or education. Even ancillary benefits of climate mitigation, such as green jobs, innovation, or reduced air pollution, are likely to only be manifest in the medium term. In this way, fossil fuel taxation constitutes a type of intertemporal redistribution—short-term costs are borne today for benefits that arrive in the future (Finnegan, 2022a; Jacobs, 2011).

Considering these impediments, we can see why the politics of carbon pricing have proven tumultuous. Indeed, a perennial critique of democratic politics is that, being motivated primarily by re-election, politicians are systematically unable to see beyond the next contest. Instead of making tough choices today, they appeal to voters’ short-sightedness, put off any sacrifice for as long as possible, and ignore the future consequences. Yet, while the myopic pressures of democratic politics are daunting, the actual record of fossil fuel taxation presents a more complicated story.

As I show in this paper, fossil fuel tax rates vary widely across the high-income democracies and within them over time. In some countries, such as the Netherlands and Belgium, tax rates increase almost every year while rates have remained virtually unchanged for decades in the US and Canada. What explains this variation? Why are some governments willing to invest in long-term climate policies, like fossil fuel taxes, even at the risk of imposing short-term costs on their constituents? Surprisingly, we still do not know much about the answers to these questions. Despite its self-evident importance and the centrality of politics, climate change has remained curiously absent as a mainstream concern for political science (Keohane, 2015).

This article investigates the reasons for the puzzling variation in fossil fuel tax rates by charting the largely unexplored theoretical territory between comparative climate change politics and research from political science and economics on long-term policymaking. It focuses on the role of the electoral environment in structuring politicians’ time preferences. The basic argument is that the more secure the government is in office, the more insulated it is from the vagaries of political competition, and therefore, the more likely it is to increase taxes. By shaping the incentives of elected officials to impose direct and highly visible costs on voters today, electoral competition informs how governments come to value the future benefits of climate mitigation. In this way, electoral competition shapes politicians’ discount rates, and by extension their policy myopia. While I focus on fuel taxes, the argument is applicable more broadly to any long-term policy problem that requires short-term increases in consumer prices.

To test the theory, I analyze taxation of an important and widely consumed fossil fuel: gasoline. Gasoline is one of the largest sources of carbon pollution worldwide. In the US, for example, it accounted for 22% of energy-related CO2 emissions in 2018; on par with coal (U.S. Energy Information Administration, 2020). For this reason, gasoline taxes have been highlighted as one of the most important fossil fuel taxes adopted to date (Sterner, 2007); yet, pricing policies around the world have been mixed (Ross et al., 2017).

Utilizing an original dataset of gasoline excise tax rates and a measure of electoral competition developed using loss probability data from Kayser and Lindstädt (2015), I examine the relationship between competition and taxation within twenty high-income democracies between 1988 and 2013 using fixed effects models. I find robust evidence that higher levels of electoral competition are associated with lower gasoline tax rates, even after controlling for a wide range of potential confounders. Furthermore, the negative influence of competition is moderated by politicians’ perceptions of voter preferences. When a tax increase is expected to impose high costs on their constituents, because gasoline consumption is widespread, politicians are even less likely to increase rates. Perhaps surprisingly, I find that government partisanship plays little role in shaping tax rates. Taken together, the results provide strong evidence that electoral competition structures politicians’ strategic decision-making regarding long-term climate policies like fossil fuel taxation.

The paper contributes to the academic and policy literature in several ways. First, the paper contributes to the emerging subfield of comparative climate politics (Andersen, 2019; Harrison & Sundstrom, 2010; Hughes and Urpelainen, 2015; Lipscy, 2018; Mildenberger, 2020; Wood et al., 2019)—an under-researched area (Cao et al., 2014; Keohane, 2015). While important research has focused on the politics of fossil fuel taxation in particular jurisdictions (e.g., Andersen, 2019; Harrison, 2012; Rabe, 2010, 2018), this paper provides a general theoretical framework. The arguments import previously overlooked insights from the long-term policymaking literature (Garrett, 1993; Jacobs, 2011, 2016) and economics (Azzimonti, 2015; Nordhaus, 1975) to highlight the key role of politicians’ time preferences in shaping the politics of carbon taxation. Empirically, it is one of a very small handful of quantitative studies to examine environmentally-related taxation (Genovese et al., 2017; Ward & Cao, 2012).

Second, the paper contributes to broader debates in political science and economics about the extent to which electoral competition has a myopic effect on politicians’ behavior (Alesina & Tabellini, 1990; Cronert & Nyman, 2021; Hubscher and Sattler, 2017; Immergut and Abou-Chadi, 2014; Nordhaus, 1975; Schultz, 1995). To date, scholars have generally analyzed aggregate taxing and spending decisions, which can be blunt measures of political decision-making. By examining one tax policy decision with intertemporal redistributive consequences, this analysis provides a sharp empirical test of competition’s myopic effects. Lastly, it adds to research on the political economy of taxation by providing a general theory that specifies the electoral conditions under which increases in consumer prices are politically feasible (e.g., P. F. Andersson, 2022; Beramendi & Rueda, 2007; Levi, 1989; Martin, 2015; Rogowski & Kayser, 2002)

From a policy perspective the paper has practical implications for addressing climate change. Increased fossil fuel prices are often thought to be important to shift production and consumption onto a more sustainable path. However, in democracies, such policies are likely to face strong political headwinds if elections are highly competitive and fossil fuel consumption is diffuse. Policymakers should take these electoral incentives into account when choosing climate policy instruments, and when designing and implementing carbon taxes.

The Puzzle of Fossil Fuel Taxation

Since Nordhaus (1977), a tax on fossil fuels has been consistently advocated by economists as the most cost-effective policy to reduce CO2 emissions. By increasing the price of fossil fuels, taxes should reduce their consumption and associated emissions. 1 The idea gained traction and diffused widely, especially in the 1990s (Meckling & Allan, 2020).

Despite the theoretical elegance of taxes, the politics have proved tumultuous (e.g., Rabe, 2018). Politicians in Nordic countries were early adopters of carbon taxes and have been able to steadily increase rates over time, though not without conflict (Andersen, 2019; Kasa, 2000; Mildenberger, 2020). In British Columbia and Ireland, politicians had similar success in adopting carbon taxes in the late 2000s, but less success increasing rates (Convery et al., 2014; Harrison, 2012; Rabe, 2018). In the UK, rates for some fossil fuels were sharply increased in the 1990s, only to be halted amid protests in 2000 (Ekins et al., 2010). By 2013, Prime Minister David Cameron was demanding that his ministers get rid of green levies he believed were responsible for pushing up energy prices (Carter & Clements, 2015). An “eco-tax” was adopted in Germany in 1999 as part of a broader environmental tax reform package; though it has not been increased since 2003 (Beuermann & Santarius, 2006). In response to gilets jaunes protests in 2018, French politicians postponed planned increases in carbon tax rates. In Australia, a carbon pricing scheme was adopted in 2011 only to be repealed in 2014 (Mildenberger, 2020; Rabe, 2018). In the US, efforts to adopt an energy tax in 1993 fell flat, reflecting a marked aversion amongst politicians to directly impose costs on voters, which has kept fossil fuel taxes exceptionally low (Mildenberger, 2020; Rabe, 2010, 2018).

This rich literature offers important analyses of the political challenges of fossil fuel taxation in particular cases. However, we are still missing a general theoretical account that can explain why there has been such little implementation of what is widely considered to be the first-best policy to address climate change. Scholars have argued that vote-seeking politicians have few incentives to impose direct and highly visible costs on voters who, consistent with extensive survey research, dislike increased fuel taxes (Harrison, 2012; Kasa, 2000; Rabe, 2010, 2018). Yet this reasoning cannot explain the wide variation in fossil fuel tax rates that we observe across the high-income democracies. Lastly, the generalizability of existing country-specific studies is hampered by a lack of large-N investigations into fuel tax politics (with notable exceptions being Genovese et al. (2017) and Ward and Cao (2012)).

Electoral Competition and Fossil Fuel Taxation

The starting point for the argument is to reconceptualize fossil fuel taxation as a type of long-term policy. Taxes impose concentrated costs today on social actors for the globally diffuse benefit of a hospitable future climate; while doing nothing about climate change imposes diffuse costs in the future for concentrated benefits enjoyed today in the form of low energy prices. By entailing short-term pain for long-term gain, taxes are a type of “policy investment” that redistribute resources intertemporally (Finnegan, 2022a; Jacobs, 2011). As such, they present politicians with a sharp intertemporal tradeoff. A number of factors should influence how politicians confront this kind of tradeoff (e.g., Finnegan, 2022a; Jacobs, 2011, 2016). I focus on the way that the electoral environment shapes incentives to impose short-term costs on voters for benefits that arrive in the future. 2

I assume that politicians are concerned with re-election. They should not be expected to increase taxes if doing so will lose them the next contest. That said, I assume that elected officials are also concerned about implementing their preferred policies to shape society in their desired direction (Jacobs, 2011; Strom, 1990; Wittman, 1983). To be sure, there are a number of reasons why governments will not be interested in long-term policy investments like fuel taxes. Politicians do not always face strong incentives to maximize aggregate social welfare over the interests of their narrow constituencies that oppose policy change. Furthermore, parties may not expect to be in power when the full benefits of long-term policies are realized, and therefore not expect to reap the associated political benefits. Lastly, some will be ideologically opposed.

Nonetheless, there are at least four reasons why politicians might prefer to increase fossil fuel taxes (which can account for the attempts mentioned above by virtually all governments in high-income democracies to do so). Since the late 1980s, developed countries have faced common international pressure to address climate change. Being “Annex I” parties to the United Nations Framework Convention on Climate Change, they agreed to identical emissions reduction goals at the Rio Earth Summit in 1992 and signed the Kyoto Protocol in 1997 (though not all ratified it). Politicians have also at times faced pressure from civil society and social movements to act. Given that fossil fuel taxes have been widely advocated as the first-best climate policy, governments may implement them to respond to these international and domestic demands. Some parties may also be ideologically committed to addressing climate change, for example, green parties. Furthermore, governments can be motivated by an incentive to maximize revenues, in an effort to fund other policy programs or meet budget shortfalls (Beramendi & Rueda, 2007; Berry & Berry, 1992; Geschwind, 2017; Levi, 1989).

For governments that want to increase taxes, one important obstacle is electoral risk. Fossil fuels are widely consumed. Any direct tax will impose highly visible costs on voters—either at the pump or on energy bills.

A large body of survey research consistently finds that individuals’ support for climate policy, especially taxes, tends to decrease as the costs rise (for a review see Drews & Bergh, 2015). For example, Jagers and Hammar (2009) survey Swedish households on the country’s carbon tax. They find that 19% of respondents support an increase, while 48% oppose. In an open-ended US survey, 58% of respondents listed personal costs as a factor that determined their climate policy support—the most of any factor in the study (Shwom et al., 2010). Using survey experiments in France, Germany, the UK, and the US, Bechtel and Scheve (2013) find that public support for a global climate agreement decreases as the associated monthly household policy costs rise. More recently, the 2016 European Social Survey shows that across 22 countries, 30% of respondents were somewhat or strongly in favor of increasing fossil fuel taxes (European Social Survey, 2016). In only Sweden and Finland was the proportion greater than 50%. Moreover, 78% of respondents across Europe were extremely, very, or somewhat worried about energy affordability.

Beyond costs, cognitive biases can undermine public support for long-term policy investments. Negativity bias focuses individuals’ attention on negative information (short-term costs) rather than positive information (long-term benefits), while loss-aversion means they will tend to weigh short-term costs more than the prospective gains of avoided climate change (Jacobs, 2011, Ch.2; Kahneman et al., 1991). Lastly, there is evidence that voters are moderately impatient and distrust that politicians will keep their promise to deliver future benefits, preferring instead policy benefits that arrive more quickly, which biases them against taxes that involve intertemporal tradeoffs (Jacobs and Matthews, 2012).

The risk for politicians is that a tax increase elicits an electoral backlash. Indeed, consistent with a basic retrospective model of electoral accountability, there is evidence that voters punish politicians at the next election for tax increases (e.g., Kone & Winters, 1993) and costly climate policies more generally (Stokes, 2016). Additionally, fuel price increases are fertile ground for mass protest, with the most recent example being the gilets jaunes in France who, as mentioned above, took to the streets in opposition to a planned carbon tax increase.

While all elected officials should understand the electoral risks associated with tax increases, their risk tolerance will not be uniform. Instead, it should vary depending on political conditions. Crucially, how competitive they expect the upcoming election to be should structure their appetite for electoral risk. A more competitive election means higher uncertainty about a change in government control at the next contest from the perspective of the governing party(ies) (Blais & Lago, 2009; Boyne, 1998; Kayser and Lindstädt, 2015; Strom, 1990). Politicians certain to win or lose face low electoral competition, while those with a 50% probability of winning face high competition.

Competition should shape both the ability of governments to adopt long-term policies and their willingness to do so. When competition is low because the governing party is likely to win, a surplus of committed voters insulates it against marginal losses in vote shares that can result from electoral backlash. This increases its level of electoral safety, making it less risky to adopt policies that are costly in the near term, but promise future benefits. At the same time, high electoral safety lengthens governments’ time horizons by enabling them to focus their attention on long-term challenges rather than solely winning the next election. That is, as highlighted by spatial theories of electoral competition and probabilistic voting, they should be less vote-seeking and more policy-seeking (e.g., Hansson and Stuart, 1984; Roemer, 2001; Strom, 1990; Wittman, 1983). What is more, because politicians expect to stay in office, they can also expect to claim credit for any medium-term environmental and economic benefits that arise from fossil fuel taxation, as well as take advantage of the associated revenues. Lastly, putting up taxes means they may not need to increase them during the next term when their electoral fortunes might change.

Conversely, when competition is high, small changes in vote shares can remove the governing party from power. Knowing this, the party’s vote-seeking preferences should dominate its policy-seeking ones, and generate strong incentives to pursue a strategy of short-term vote-maximization in an effort to win the next contest. Under these conditions, long-term policy investments that could upset voters today, such as direct price increases, are unlikely to be adopted. The low probability of adoption is compounded by uncertainty about whether the party will remain in office long enough to reap any associated benefits.

When competition is low because the government is likely to lose, expectations are indeterminate. The party is insulated and can therefore afford to be far-sighted in its policymaking and pursue tax increases without fear of electoral backlash. Furthermore, by increasing rates, it can try to lock in its preferred policy and constrain an adversarial successor’s room to maneuver (Alesina & Tabellini, 1990). However, in the case of fossil fuel taxes, putting up rates might also expand a successor’s options. It can absolve them of the need to enact a painful policy choice, offer a new revenue stream, and give them the option to cut taxes to gain political capital. Anticipating this, the governing party may instead choose not to touch rates.

More broadly, by structuring the electoral risk associated with long-term policy investments, electoral competition should shape politicians’ discount rates, or the extent to which they value future policy benefits against short-term political expediency (Strom, 1990). Importantly, this effect should be causally prior to government preferences. While governments may have a variety of motivations to increase fossil fuel taxes, as described above, the first priority of all governments is re-election. Governments across the ideological spectrum should therefore respond to increasing competition by foregoing rate hikes.

The arguments import previously overlooked insights from long-term policymaking research to theorize the politics of fossil fuel taxation. Garrett (1993): 523 is perhaps the first to argue that “it is only governments that are relatively secure in office that can assume the longer-term time horizon necessary...to engage in the politics of structural change,” pointing to the creation of the Swedish welfare state and Thatcher’s neoliberal reforms in the UK as examples. Jacobs (2011) theorizes that low levels of electoral competition are a necessary condition for long-term policy investments, citing evidence from pension reforms. More recently, researchers have shown how electoral vulnerability shapes long-term policymaking in the case of social policy (Immergut and Abou-Chadi, 2014) and public finance (Hübscher and Sattler, 2017; Seiferling, 2020). Lastly, from the economics literature, Azzimonti (2015) demonstrates formally how lower competition decreases the discount rate of policymakers, resulting in higher levels of public investment. More broadly, the theory is consistent with work on political business cycles that connects high electoral competition with increased efforts by incumbents to manipulate macroeconomic policy (e.g., Nordhaus, 1975; Schultz, 1995) or constrain the behavior of the next government (e.g., Alesina & Tabellini, 1990).

Before moving on, two additional points are needed. First, the claim is not that myopia is the only reason why politicians are likely to cut fossil fuel taxes going into a close election. Consistent with the political business cycle literature, vote-seeking governments that are electorally vulnerable should be expected to reduce a range of taxes, including green ones, in an effort to stay in power. The insight here is that the relative magnitude of competition’s effect should be positively correlated with when the benefits of the tax arrive. Competition should have less of an effect when benefits arrive immediately and more when they arrive in the future. That is, when competition is high, politicians should be most likely to cut taxes associated with long-term policy investments over those that are used to fund immediate benefits for voters. For this reason, competition should be an especially important predictor of government short-sightedness, and by extension, their fossil fuel tax policy.

Second, the assumption that politicians will perceive voters as always opposed to fuel tax increases can be relaxed. Indeed, we should expect the negative effect of competition to be moderated by governments’ perceptions of voters’ tax preferences. I explore this possibility in further detail below.

Methods

Research Design

To test the arguments, I examine the relationship between electoral competition and one widespread type of fossil fuel taxation—gasoline taxes—in twenty high-income democracies between 1988 and 2013. 3 While the problem of climate change has been known to governments since at least the 1960s, it is starting around 1988 that governments began to take serious action (Finnegan, 2019, Ch 1). That year the World Conference on the Changing Atmosphere in Toronto marked the first major international, multilateral conference focused on policy solutions. In addition, governments began to convene expert commissions to develop domestic mitigation policies, including fossil fuel taxation, in countries like Germany and Sweden.

Gasoline is a major source of carbon pollution across the high-income democracies. Consequently, gasoline taxes are arguably the single most important fossil fuel tax they have adopted (Sterner, 2007). In practical terms, gasoline is widely consumed by voters across the sample of countries and over time, which is not the case for other fossil fuels, such as coal, natural gas, or heating oil. Moreover, motorists frequently visit gasoline stations to fill up, making changes in gasoline prices highly visible to voters. For these reasons, gasoline represents an ideal case for analyzing the politics of directly taxing a fuel that is consumed frequently and extensively by voters.

Governments have a number of policy design options when increasing taxes on gasoline. They may simply increase existing excise or value-added tax rates (VAT) or adopt an energy tax (a flat tax based on the energy content of the fuel), an environmental tax (typically an excise tax by a different name), or an explicit “carbon tax” (a flat tax based on the carbon content of the fuel). Indeed, all carbon taxes imply a tax on gasoline. Virtually, every carbon tax adopted by the sample of countries is applied to gasoline (see online appendix).

Because VAT rates vary little over time and not all countries have them, I analyze excise taxes. All countries in the sample have adopted excise taxes, offering variation across space and time. To measure rates, I compile an original dataset of excise tax levels per liter of gasoline in national currencies that draws on a variety of national and international sources, such as the International Energy Agency, government ministries, and national tax authorities. 4 In addition to standard excise taxes, the measure includes all carbon, energy, and other special environmental taxes applied to gasoline.

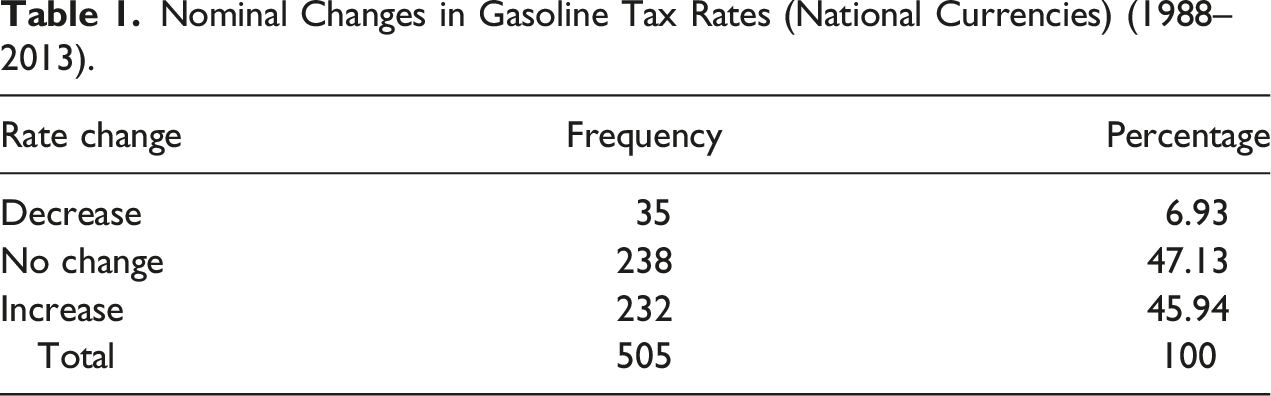

Nominal Changes in Gasoline Tax Rates (National Currencies) (1988–2013).

Operationalizing Key Variables

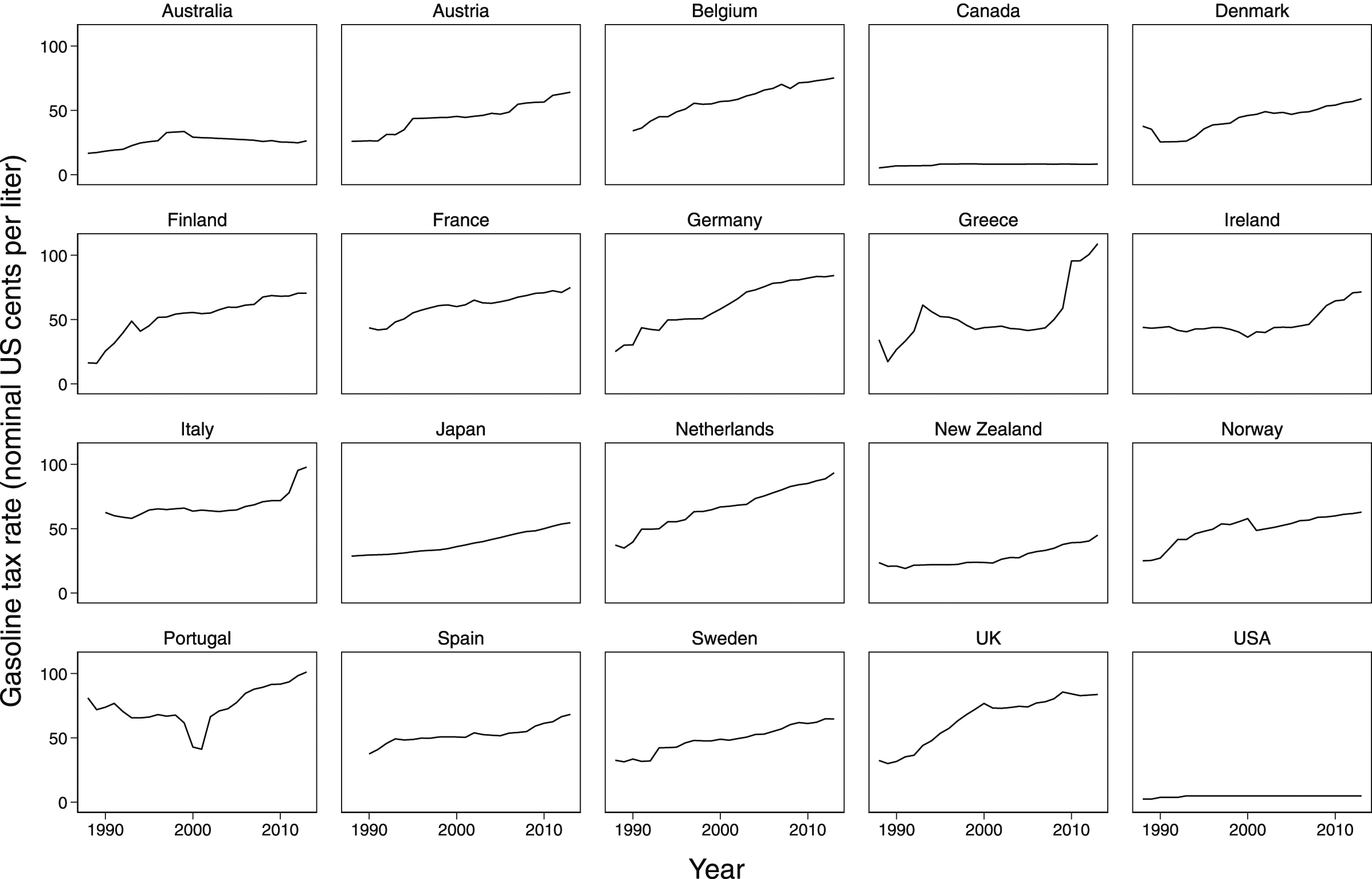

To measure gasoline taxes in a cross-nationally comparable way I convert national currency rates into a common unit—nominal US cents per liter—using USD purchasing power parity exchange rates (Figure 1). I use nominal rather than real rates to capture the behavior of politicians, since this is the phenomenon that my arguments seek to explain. Politicians only have direct control over the nominal rate. Moreover, it is nominal increases that are politicized during election campaigns (Li et al., 2014). Trends in gasoline taxation.

While the measure captures tax levels across countries in a comparable way over time, the drawback is that some artificial variation is introduced from exchange rate fluctuations, which are largely independent of tax decisions by politicians. To minimize measurement error, I include three macroeconomic controls that influence exchange rates: inflation, public debt, and economic growth. 5

The average tax rate for the sample is about 47 cents per liter and the median is around 49 cents, indicating a relatively normal distribution. Rates increase across all countries from 1988 to 2013, though the magnitude varies considerably. Increases are modest in Australia, Canada, Spain, and the US and most dramatic in Belgium, Germany, Greece, and the Netherlands. The US has the lowest rate in the sample (2.4 cents per liter in 1988–89), while Greece has the highest (109 cents in 2013).

An ideal measure of electoral competition would be based on incumbent perceptions of their re-election prospects at the time they are considering gasoline tax changes (Boyne, 1998; Cronert & Nyman, 2020). However, given the difficulty of gathering such data, I instead rely on a proxy measure of loss probability developed by Kayser and Lindstädt (2015). They estimate the “expected probability that the plurality party in parliament loses its seats plurality in the next election” from the perspective of that party (Kayser and Lindstädt, 2015, 243). I summarize their approach below. For a detailed discussion, see the original paper.

The probability of the plurality party being removed at the next election is the probability of a swing in the seat share between the two largest parties that exceeds the current seat share gap between them. This seat swing (St) can be written as

Because parties cannot know their vote shares at the next election (at time t+1), Kayser and Lindstädt rely on a proxy: vote swings in the past six elections. The assumption is that politicians predict vote swings in the upcoming contest based on the volatility of previous outcomes. They use a kernel density function to map historical swings to a probability density. By accounting for voter volatility, the measure better captures electoral risk than common alternative measures like vote or seat margins. Indeed, as the authors point out, what constitutes a safe margin in the Netherlands, where volatility is low, means little electoral security in Canada, where volatility is high.

The second key element in Kayser and Lindstädt’s measure is each country’s seats-votes elasticity (τ i ), or the extent to which changes in vote shares generate changes in seat shares. Elasticities depend on electoral rules and the geographic distribution of each party’s voters. For parties in proportional (PR) systems, seats-votes elasticities are equal to one. However, in majoritarian systems they are estimated using votes and seats data from the most recent election. Elasticities range from 1.88 in US in the 1988 election to 3.98 in Australia in 1990.

To summarize, a plurality party faces higher loss probability when it expects a vote swing large enough to remove its plurality status by reducing its seat share below the second largest party’s. Such a vote swing can be the result of changes in voter volatility and/or the geographic distribution of votes. It is therefore these factors that drive over-time changes in the data.

Loss probabilities are forward-looking and capture the view of the dominant policymaker regarding the electoral security of their position. Moreover, because they are estimated from previous elections they enjoy exogeneity from gasoline tax changes in a given term. While there is a spirited debate on the best measure of electoral competition (Abou-Chadi & Orlowski, 2016; Blais & Lago, 2009; Cox et al., 2020; Cronert & Nyman, 2020), this data offers the most complete and well-developed proxy of competition for the countries in my sample. It enables me to overcome data limitations that have previously prevented climate politics researchers from directly testing the effects of loss probability (e.g., Aklin & Urpelainen, 2013).

Kayser and Lindstädt estimate loss probabilities for the plurality party in the legislature. While this party is not always the governing party, it is for 92% of country-years in my sample. I therefore proceed using data for the plurality party. However, as a robustness check, I limit the sample to plurality parties that are also governing parties and find little substantive change in the results (see online appendix).

To be sure, the consequences of losing plurality status differ across electoral systems. In majoritarian systems, it almost always means leaving government, while in proportional systems with coalition governments this might not be the case. Coalition bargaining can mean that parties stay in power even after losing their seats plurality. It can also enable smaller parties to wield disproportionate power over government formation. A limitation of the loss probability estimates is that they do not capture these bargaining dynamics. Instead, they rely on the straightforward assumption that retaining plurality status is important for the largest party regardless of post-election coalition bargaining dynamics, because it means getting the first chance to form a government and having agenda-setting powers (Kayser and Lindstadt, 2015, 243–4). Still, I control for electoral systems and government types in the empirical analysis below.

An additional drawback is that values change only in election years, and therefore do not capture changes in politicians’ perceptions of electoral risk in years between elections. As a consequence, measurement error may be introduced if plurality parties’ loss probabilities change dramatically between elections. However, if present, such error would lead to attenuation bias. That is, my estimates would be closer to zero, and therefore more conservative, than the true effect. Lastly, there is limited coverage for Italy, Japan, and New Zealand due to their electoral system changes in the 1990s.

Electoral competition is highest at middle values of loss probability. It is around these values that plurality parties should be most responsive to the electorate in an effort to maximize votes and secure electoral success. To measure electoral competition, I therefore use equation (2) to calculate the absolute distance of each plurality party’s loss probability from .5, or theoretically perfect competition, and then rescale the variable to a range of 0–1, where 1 is equal to perfect competition:

This new measure assumes that parties with a low probability of losing the next election (i.e., “likely winners” with a loss probability below .5) and those with a high probability of doing so (i.e., “likely losers” with a loss probability above .5) behave similarly. In an effort to maximize their chances of winning, both act myopically and refrain from putting up taxes as their loss probability moves toward .5. Empirical tests provide evidence that there is no statistical difference between the behavior of likely winners and likely losers (see online appendix). I therefore proceed with the measure. However, given mixed theoretical expectations, I separately analyze the behavior of likely winners and likely losers in the Likely Winners, Likely Losers, and Government Preferences section below.

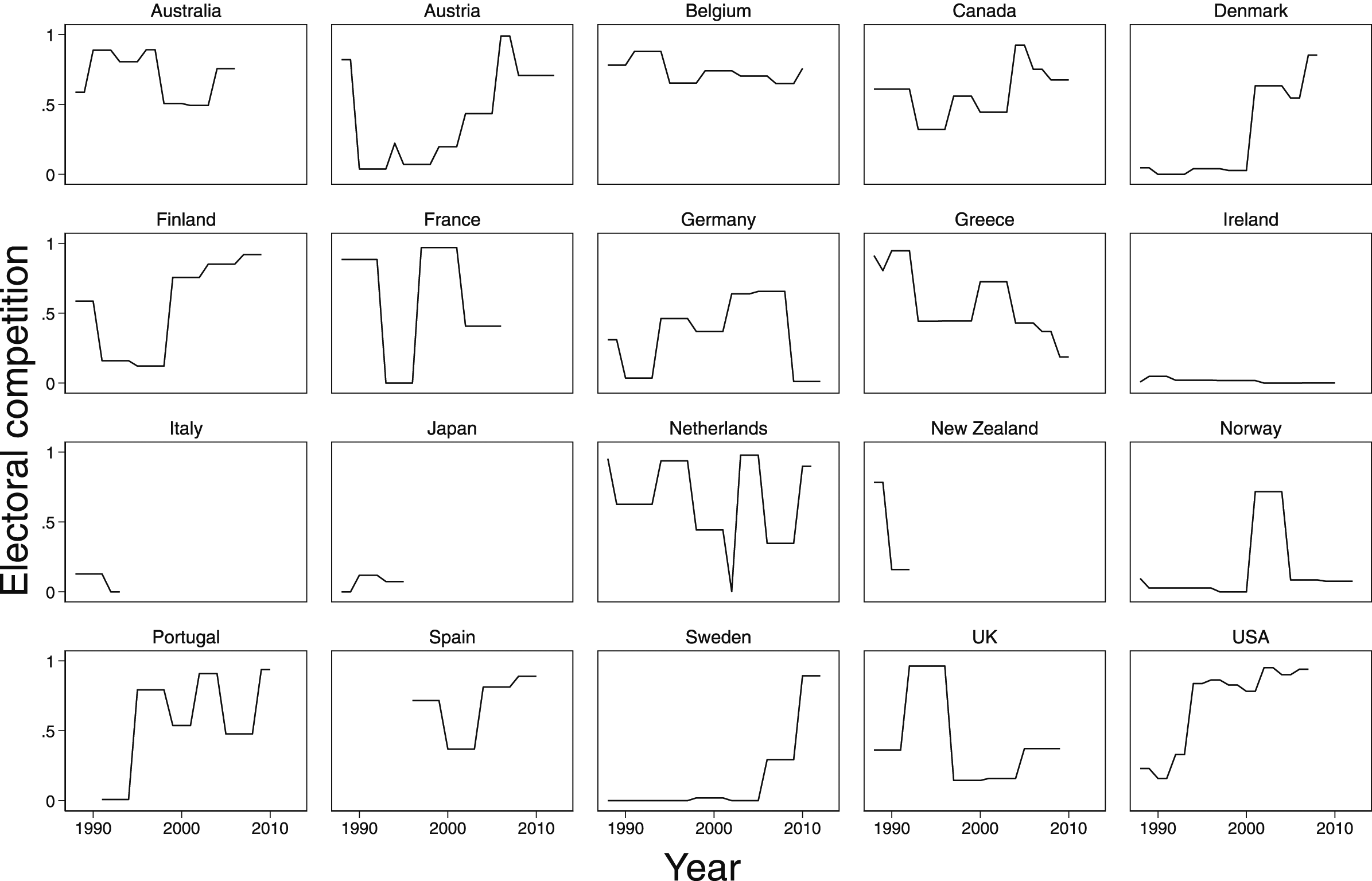

Figure 2 shows the new measure of electoral competition. Mean competition for the sample is .44 with a standard deviation of .34. On average, electoral competition is highest in Belgium and Australia and lowest in Ireland, Norway, and Sweden. Trends in electoral competition.

Model Specification and Controls

There is generally a lag between when politicians adopt tax increases and when they implement them. Rates tend to be set in the current year and implemented in subsequent years. For example, the Swedish government adopted its carbon tax in 1990 and implemented it in 1991 (Andersen, 2019). I therefore assume that the tax rate in time t is a result of political decisions made, and information available, in time t-1. To model this delay, I lag all variables 1 year apart from the electoral cycle. 6 As mentioned, loss probabilities are calculated using data from previous elections. There should therefore be little endogeneity between the measure of electoral competition and gasoline tax rates, especially once lagged.

I estimate OLS models of the form

I include two additional sets of controls. The first control for differences in tax policy preferences across governments. Depending on their partisanship, governments may be more or less inclined to adopt tax increases. To control for political party, I include the percentage of cabinet seats held by green parties and the percentage held by non-green left parties. Even if politicians experience electoral safety, they may still face opposition to gasoline tax increases from powerful business groups, especially oil companies (Mildenberger, 2020; Ward & Cao, 2012). To control for the influence of oil sector companies and unions, I include domestic oil production per capita. Last, I control for differences in fiscal health, which may push governments to maximize tax revenues in an effort shore up their finances, by including the budget deficit and public debt as a percentage of GDP (Berry & Berry, 1992; Geschwind, 2017).

The second set of controls includes factors that may influence political opportunities for tax rate increases. The large literature on political business cycles predicts that governments should be less likely to increase taxes as elections draw near (e.g., Nordhaus, 1975; Schulze, 2021). To control for this possibility, I include a dummy for election years. I control for inflation since times of inflation may provide cover to increase taxes or tax increases may be indexed to inflation (Berry & Berry, 1992; Goel & Nelson, 1999). Nominal GDP growth is included to control for national economic shocks that may affect voters’ sensitivity to fuel price increases (Berry & Berry, 1992). I include gasoline VAT rates to control for fuel taxation apart from excise taxes. Lastly, I control for the saliency of environmental issues across the political system by calculating the average pro-environmental stance across all parties in each country-year using data from the Comparative Manifestos Project (per501). The measure should also provide a proxy for environmental issue salience amongst voters, since issue attention amongst parties should, to some extent, reflect that of voters. The online appendix provides sources and summary statistics for all variables.

I restrict the analysis in the first instance to these variables. However, the results are robust to the inclusion of a wide variety of additional controls, including government type (single-party versus multiparty), ideology, veto points, spending on social policy, GDP per capita, urbanization, income tax structure, Kyoto Protocol ratification, and EU membership (see online appendix).

There are two types of problems that can arise when analyzing time-series cross-sectional data. First, the error terms may suffer from autocorrelation and/or heteroskedasticity. To correct for both I use robust standard errors clustered at the country level. The second potential problem is nonstationarity. If both the dependent and key independent variable are heavily trending upward or downward, they may be nonstationary. If so, an association between them may be spurious. An Im-Pesaran-Shin unit root test of electoral competition rejects the null hypothesis that all panels contain a unit root at the 1% level. In the case of tax rates, the evidence against the null is weaker and can only be rejected the 10% level. Since both the dependent and independent variables are not nonstationary, I proceed with the analysis. Robustness tests using percent changes as the dependent variable, which does not have a unit root, further decrease concerns about nonstationarity.

As final checks, I use jackknife resampling to investigate whether one country in the sample is driving the results. I find no evidence of this. I also estimate an alternative specification using logit models. The dependent variable equals 1 if the tax rate is increased and 0 otherwise. This setup assumes that all tax increases are equal in magnitude, which in practice is not valid. However, it enables a very strict test of whether competition decreases the probability of any tax increase. This alternative specification does not substantively alter the findings. 7

Results

Electoral Competition and Gasoline Taxation

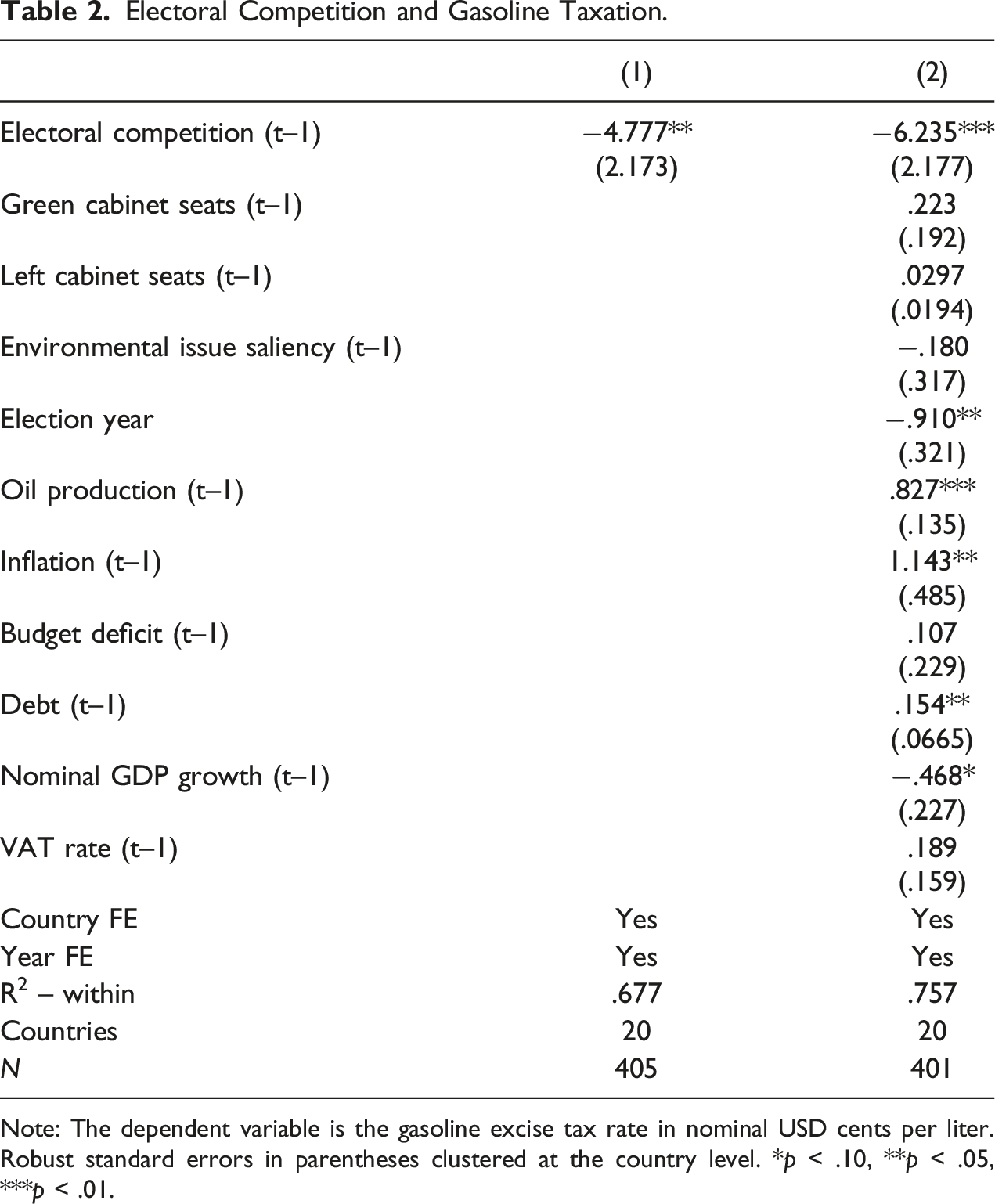

Electoral Competition and Gasoline Taxation.

Note: The dependent variable is the gasoline excise tax rate in nominal USD cents per liter. Robust standard errors in parentheses clustered at the country level. *p < .10, **p < .05, ***p < .01.

Apart from being statistically significant, the results are substantively meaningful. Consider the case of Ireland. It has the lowest average level of electoral competition in the sample. Since the adoption of its carbon tax in 2008, the gasoline tax rate has increased annually by around 4.2 cents per liter. If competition was to suddenly increase one standard deviation, we would expect this rate of increase to be cut in half. Such a change would likely increase the country’s carbon emissions.

The results offer strong evidence that electoral competition structures the politics of fossil fuel taxation. By incentivizing governments to focus myopically on the next contest, high levels of competition discourage increased rates. It is parties that feel secure in office that can look past the next election to contemplate and address society’s long-run challenges, even if it means increased short-term political risk.

More broadly, the findings help us make sense of countries’ fossil fuel tax experiences. In Sweden, the Social Democrats dominated politics for most of the 20th century, rarely receiving less than 40% of the vote. It was from this electorally secure position that the party adopted one of the world’s first carbon taxes in 1990, applying it to gasoline and other household fuel use. However, more recently, sharp increases in competition going into the 2022 election have coincided with fuel tax cuts. In Germany, the government adopted an eco-tax in 1998, which was applied to a range of fossil fuels, including gasoline, and was set to increase annually. However, after electoral competition increased dramatically following the 2002 election, the Social Democratic-Green coalition decided against any further increases. Lastly, elevated competition in the UK since 2010 has corresponded with the Treasury’s decision to first freeze the gasoline tax rate and then reduce it in 2022.

Two control variables deserve brief mention. First, I find no significant independent association between partisanship and tax rates, which adds to mixed findings in the literature on the effect of partisanship on climate policy (e.g., Mildenberger, 2020; Schulze, 2021; Ward & Cao, 2012). Second, I find strong evidence of a political business cycle effect. Tax rates are almost 1 cent lower in election years compared to non-election years. This result provides further evidence of such cycles in the context of climate policymaking (e.g., Aklin & Urpelainen, 2013; Fankhauser et al., 2015; Schulze, 2021).

Voters and Personal Costs

The main results assume that politicians will tend to view voters as uniformly opposed to fossil fuel tax increases. Here, I relax that assumption to investigate how politicians’ response to rising competition is shaped by variation in their perception of voter preferences.

One heuristic used by governments to anticipate voter preferences should be costs. Similar to other taxes, voter preferences toward fossil fuel taxes should, in general, be shaped by the costs and benefits to them of such taxes (Hettich and Winer, 1988). As mentioned, the crucial problem for the governing party is that, like other long-term policy investments, the costs and benefits of increased taxation are not temporally aligned for voters.

The governing party should expect that voter preferences for fossil fuel taxes depend primarily on the average short-term individual cost, or personal cost, that such taxes generate. For example, they should expect that SUV drivers are unlikely to prefer an increase in the gasoline tax rate, while cyclists are likely to be indifferent or even supportive. This reasoning is also consistent with survey research mentioned above. Furthermore, it is consistent with the logic of cost-benefit analysis, which usually describes policy costs in terms of average short-term costs to households and is often used by governments to evaluate the distributional effects, and political feasibility, of fossil fuel taxes.

The negative effect of electoral competition on tax rates should be different at different levels of personal cost. When the governing party perceives the personal costs of an increase to be low, there should be less political risk in adopting it, even at high levels of competition, as the party expects voters to be relatively indifferent about rate changes. Put differently, it should be politically safe to increase taxes if such increases do not cost voters anything. However, as personal costs rise, voter preferences become tilted against tax rises. High personal costs coupled with high electoral competition should generate the strongest incentives to not increase rates, or reduce them.

A measure of politicians’ perceptions of voters’ personal costs presents a number of possibilities. The most straightforward is gasoline consumption per capita. The more the average voter consumes gasoline, the more a tax increase will cost them, all else equal. To be sure, consumption is endogenous to the tax rate. To reduce endogeneity, I lag consumption two years. To measure fuel consumption, I calculate average gasoline consumption (liters per capita) using data on household gasoline consumption and population. 9

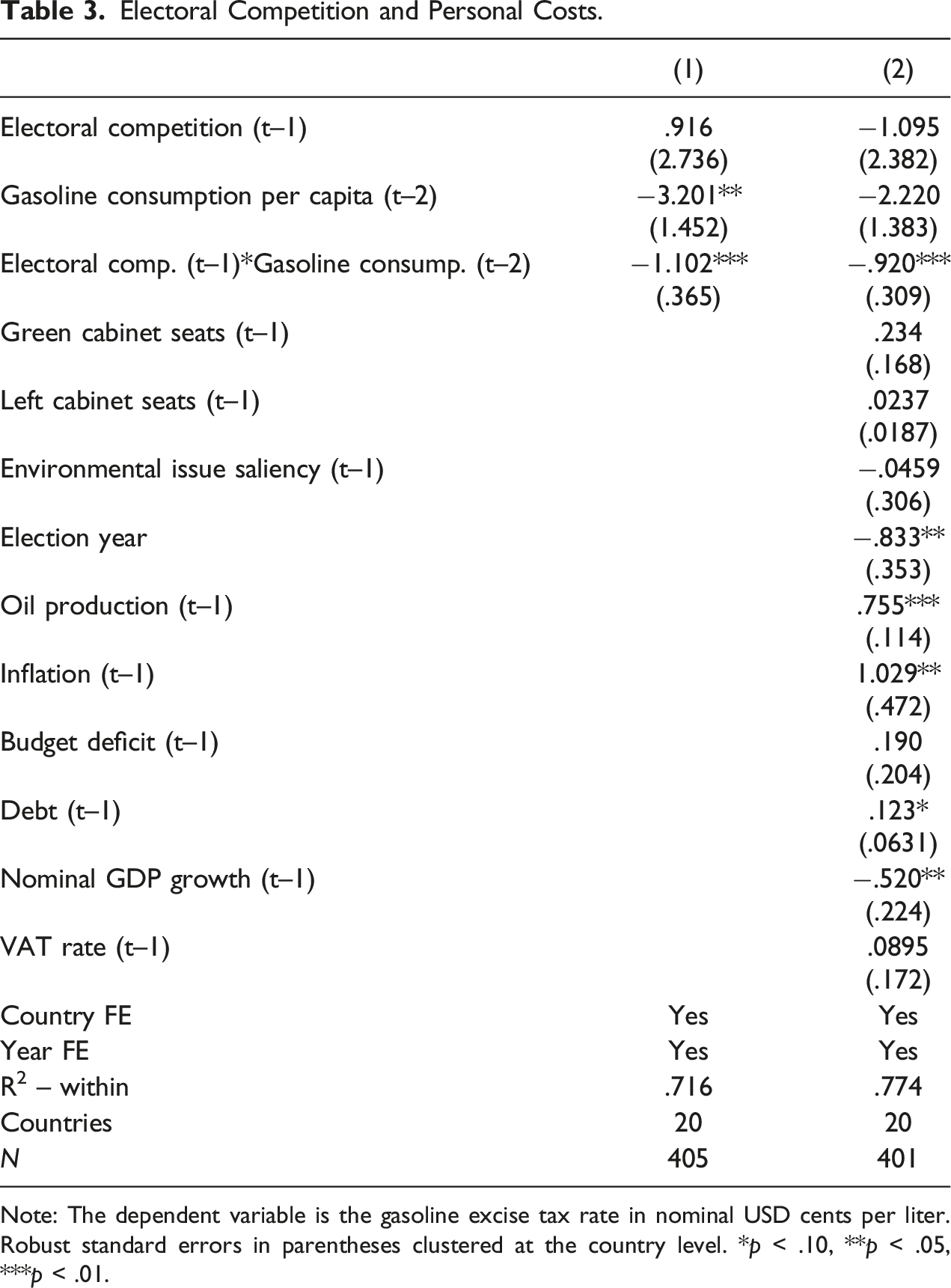

Electoral Competition and Personal Costs.

Note: The dependent variable is the gasoline excise tax rate in nominal USD cents per liter. Robust standard errors in parentheses clustered at the country level. *p < .10, **p < .05, ***p < .01.

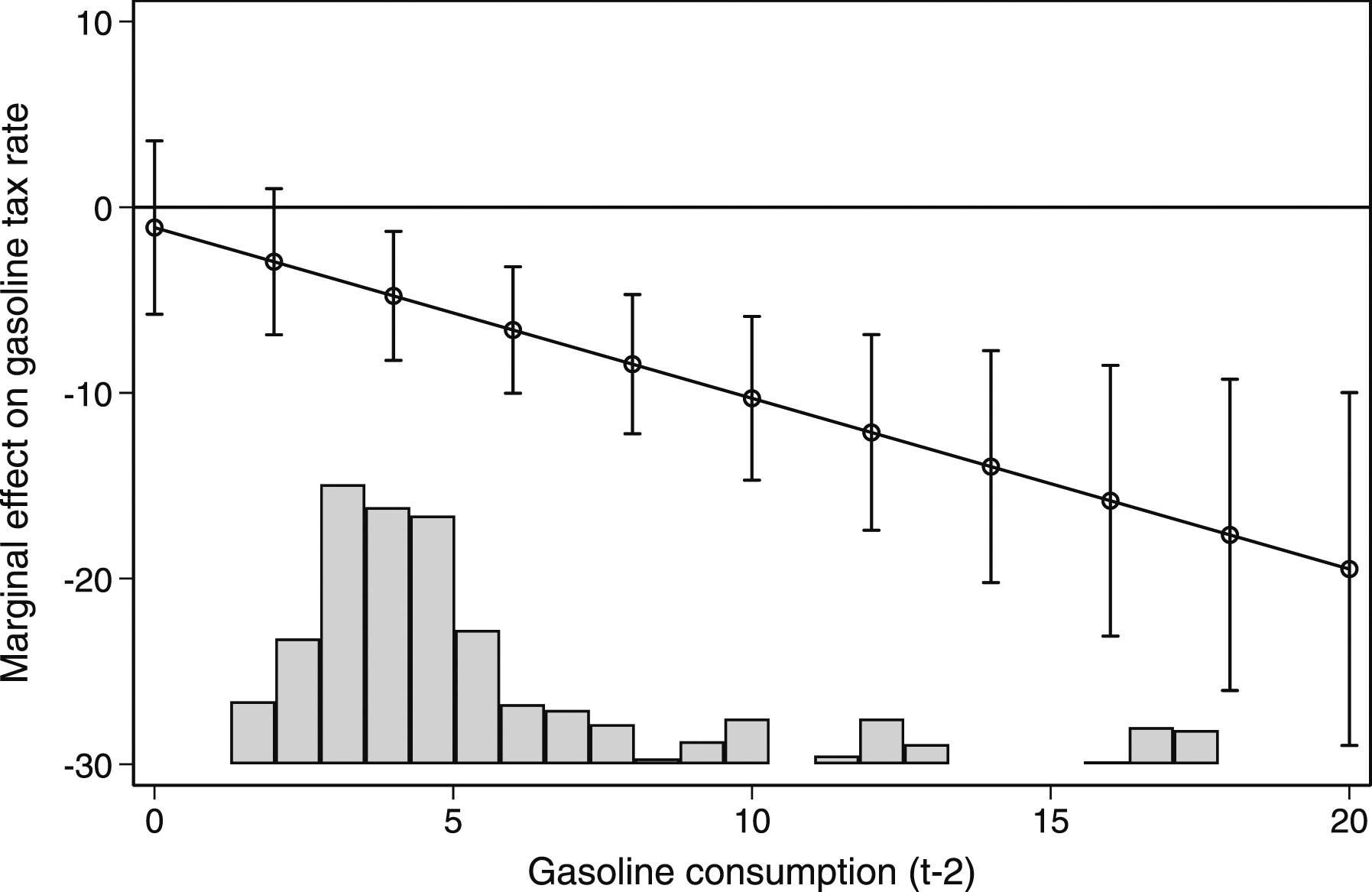

Marginal effects of electoral competition at different levels of gasoline consumption.

We also see that electoral competition has no influence on the tax rate at very low levels of fuel consumption. This should be expected. When the personal costs of a tax increase are low, electoral competition is unlikely to affect politicians’ decision-making, since rate increases on goods that are not widely consumed are less likely to lose votes. Indeed, in a world where no voter consumes fossil fuels putting up tax rates would involve little political risk. It explains the high tax rates we observe in Belgium, which has one of the highest levels of electoral competition, but one of the lowest levels of gasoline consumption.

I check the robustness of the results in a number of ways (see online appendix). I first investigate their sensitivity to the sample of included countries using jackknife resampling. I find that they are sensitive to the inclusion of the US. There is reason to expect this given the distribution of the consumption data. Consumption changes slowly over time within countries, which means country observations tend to be grouped together. Because the US has the highest consumption in the sample, its observations are grouped at the high end of the range. Removing them makes the estimates noisier. However, there is little substantive reason to consider dropping the country. Its high consumption does not make it an outlier, but a key case for the theory to explain.

I next perform diagnostic tests recommended by Hainmueller et al. (2019). Binning estimates confirm the sensitivity of the results to observations of high gasoline consumption. Moreover, kernel estimates suggest some non-linearity of the effect, whereby the impact of competition increases more quickly as consumption climbs above the sample average of 500 L per capita.

To further test the robustness of the findings and be reassured that the US alone is not driving the results, I use an alternative measure of personal cost: expenditure on gasoline as a percentage of household income (see online appendix). Using this measure does not substantively change the findings. Moreover, the results are not sensitive to the inclusion of the US or any other country. Binning and kernel estimates confirm their robustness.

Taken together, the findings provide evidence that government perceptions of voters’ personal costs moderate the relationship between electoral competition and tax rates. They also offer two broader implications. The first is a two-way relationship between consumption of a taxed good and its tax rate. Standard economic theory predicts that tax rates affect consumption. However, the results here indicate that consumption also affects the tax rate by shaping politicians’ perceptions of voter preferences. The general implication is that tax policy is structured by the size of the group subject to the tax, especially in the case of consumption taxes.

Secondly, the results suggest a long-run positive feedback effect between electoral competition, fossil fuel consumption, and tax rates. Lower taxes mean lower prices, which in turn encourage higher consumption. Higher consumption should make it more difficult for politicians to increase tax rates, even at low levels of competition. As a result, there may be a “high consumption-low tax trap.” Conversely, higher taxes mean higher prices, which helps to reduce consumption, and by doing so, make it easier for politicians to raise taxes in the future. This effect should generate strong path dependencies over time that push countries onto different fossil fuel taxation and consumption trajectories. Those on high tax-low consumption trajectories, such as Belgium, Italy, and Portugal, should find it more politically feasible to purge fossil fuels from the economy over time using taxation. However, for those caught in a high consumption-low tax trap, changing trajectories using pricing instruments alone will likely prove difficult, especially in times of heightened electoral competition. This dynamic helps to explain why high consumption-low tax countries such as Australia, Canada, and the US have found it so politically difficult to increase fossil fuel prices (Rabe, 2010, 2018).

Likely Winners, Likely Losers, and Government Preferences

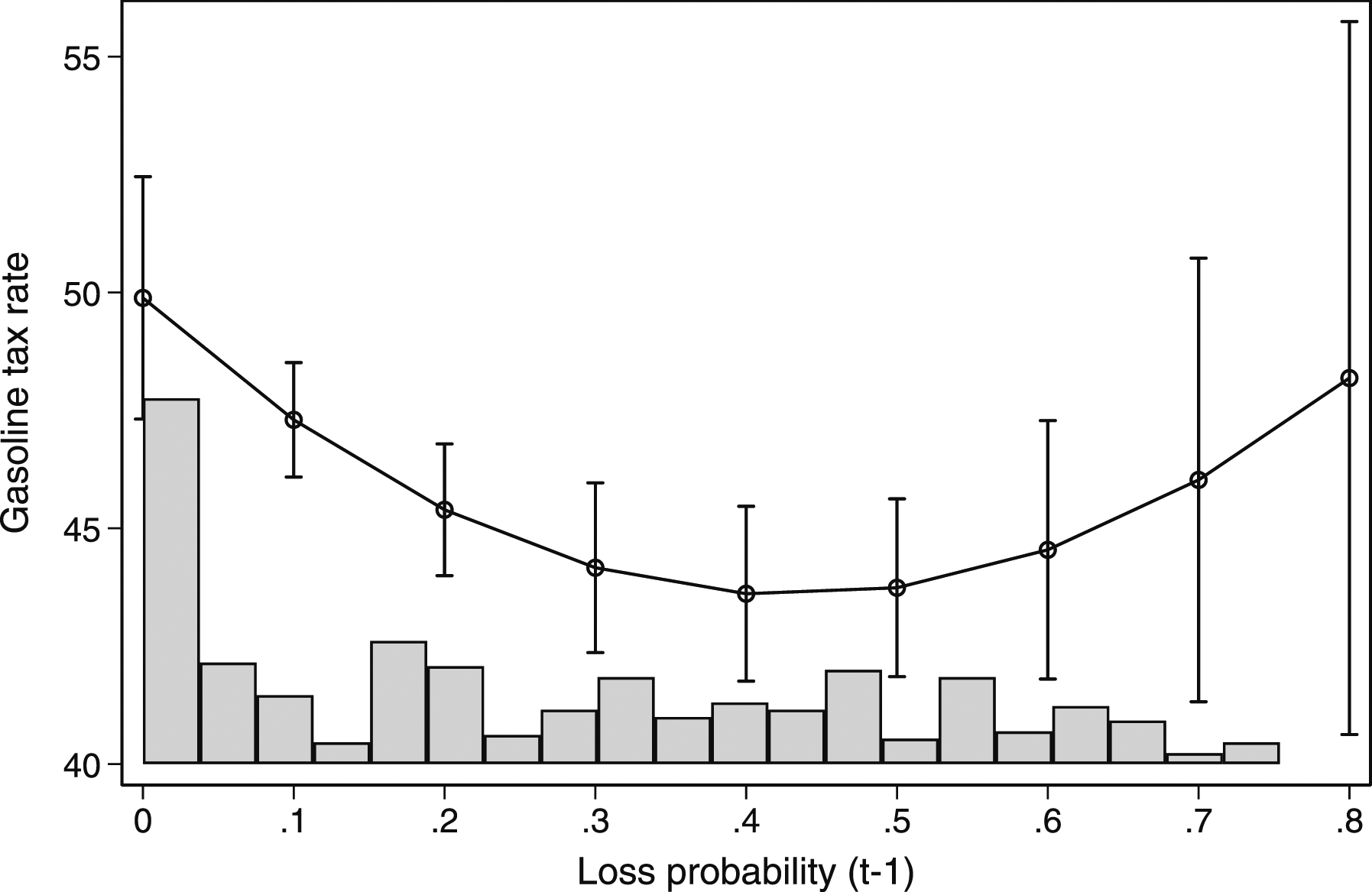

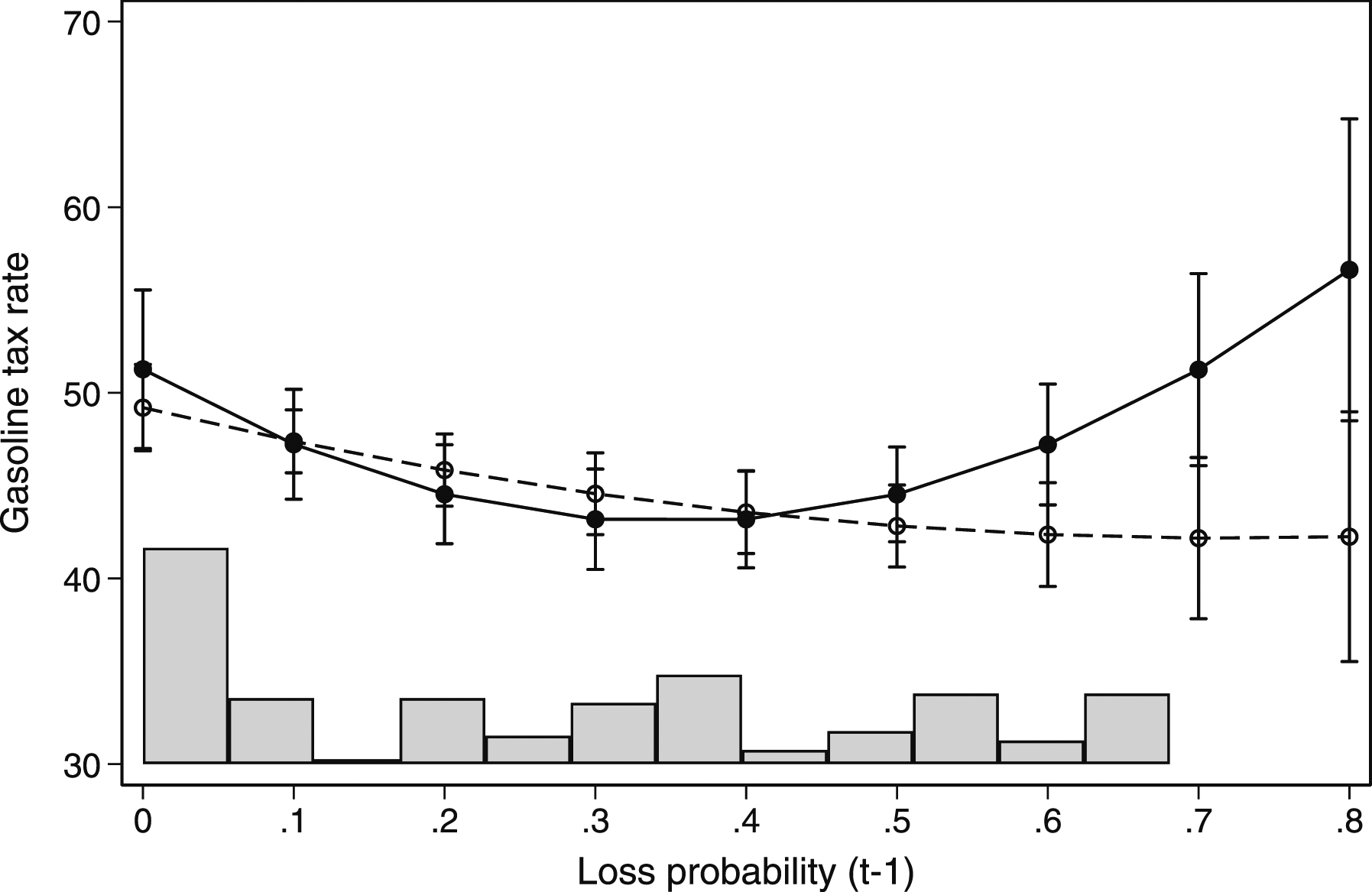

Lastly, I explore whether behavior varies between governments that are likely to win the next election (likely winners) versus those that are likely to lose (likely losers), as well as governments of different parties. To do so, I utilize the raw loss probability data from Kayser and Lindstädt (2015). Electoral competition is highest around middle values of loss probability and lowest at very high and very low values. Likely winners should reduce rates as their loss probability approaches .5. For likely losers, expectations are mixed, as described above. To model the relationship, I estimate quadratic fixed effects regressions that include loss probability and its square.

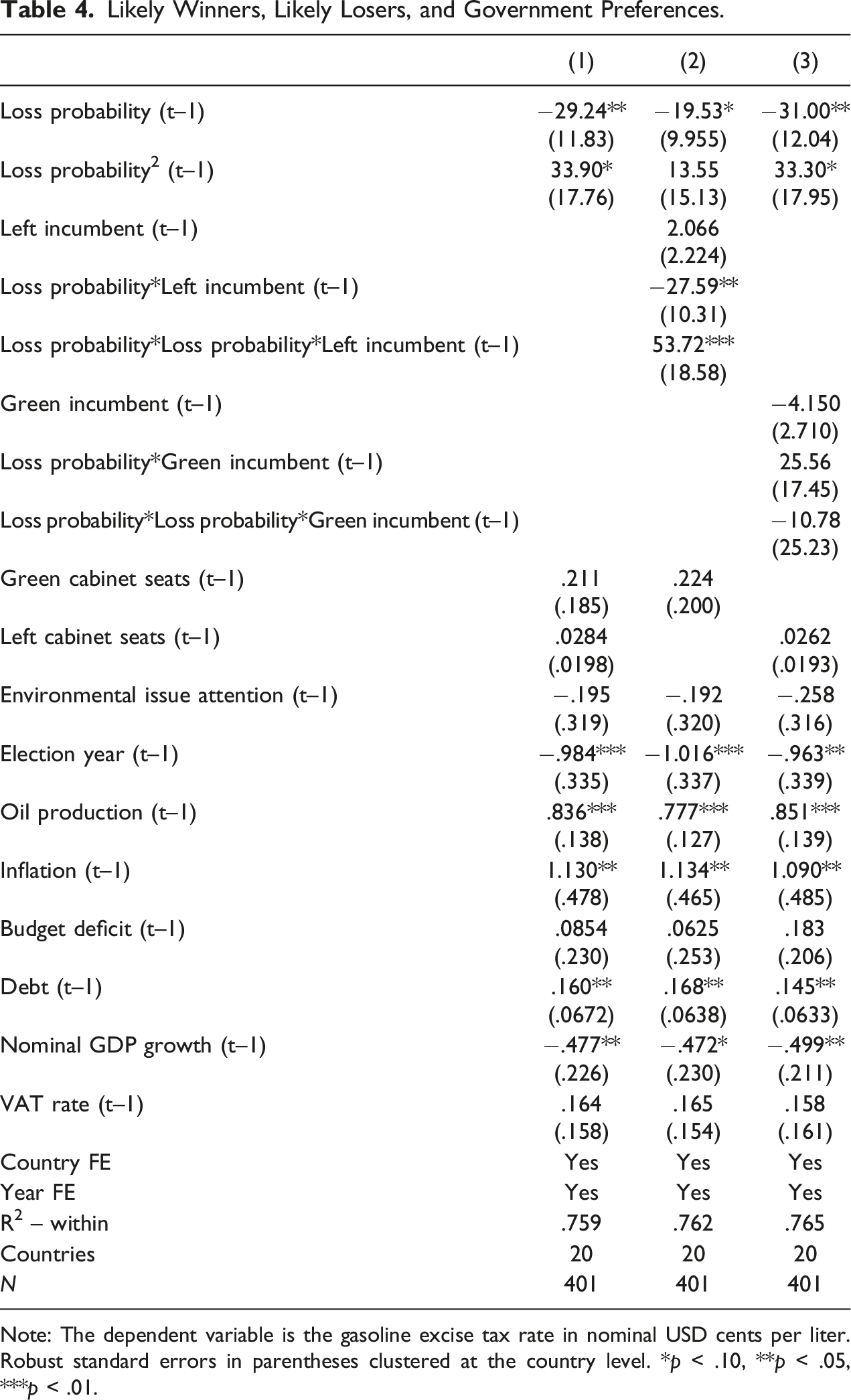

Likely Winners, Likely Losers, and Government Preferences.

Note: The dependent variable is the gasoline excise tax rate in nominal USD cents per liter. Robust standard errors in parentheses clustered at the country level. *p < .10, **p < .05, ***p < .01.

Likely winners versus likely losers.

To further analyze likely losers and to investigate the role of government preferences, I examine whether the behavior of likely winners and losers varies by partisanship using three-way interactions. It is not obvious which parties will consistently take a pro-climate position. Climate policy, and environmental policy more generally, is often a cross-cutting cleavage that does not fit neatly along a conventional left–right dimension (Mildenberger, 2020). Indeed, some studies suggest a link between green parties and environmental performance (Jahn, 2016; Jensen and Spoon, 2011), left parties and the environment (Jahn, 2016; Schulze, 2021; Ward & Cao, 2012), and left parties and consumption taxes (Beramendi & Rueda, 2007). However, others do not find clear partisan effects (Aklin & Urpelainen, 2013; Fankhauser et al., 2015; Mildenberger, 2020; Rafaty, 2018). As mentioned, the main analysis in this study finds no independent relationship between partisanship and tax rates.

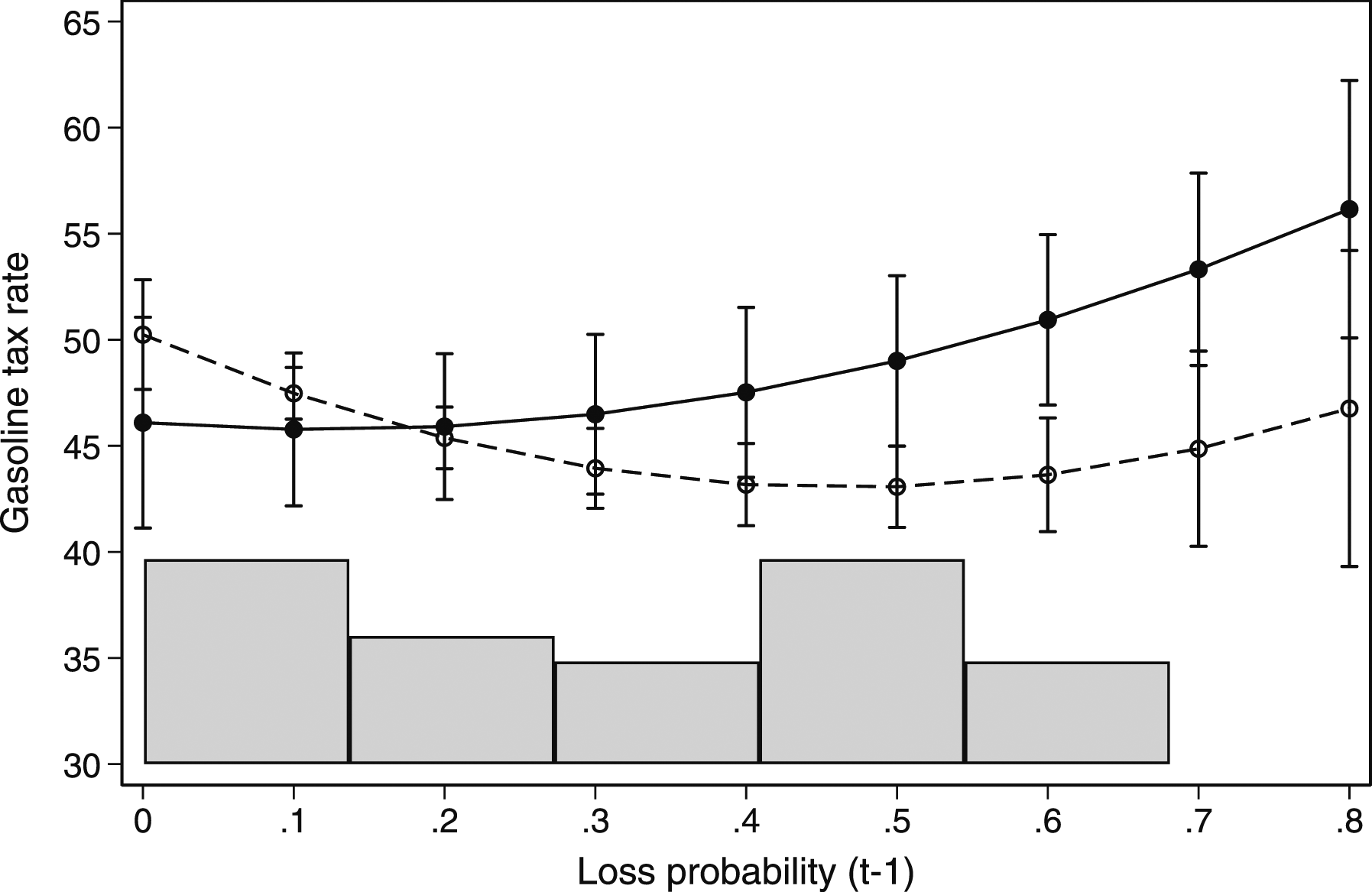

For simplicity, I focus on parties along two dimensions: left–right and green–non-green. Given their historical reliance on consumption taxes to fund social policy (Beramendi & Rueda, 2007), I assume that left parties are more likely to prefer increased fossil fuel taxation as an instrument to mitigate climate change. Likewise, given their ideological commitment to the environment, I assume green parties will hold the strongest pro-climate preferences of any party. I use dummy variables to measure left incumbent governments and incumbent governments where greens control at least one cabinet seat. Models 2 and 3 in Table 4 present the results. For ease of interpretation, I plot the three-way interaction results graphically.

Turning first to the left–right dimension, we see that both left and right likely winner governments act in a similar way, increasing taxes as their loss probability decreases (Figure 5). Once they become likely losers, the results are again less precise. Point estimates suggest that their behavior diverges, with left governments appearing to increase rates and right ones appearing to reduce them. To be sure, the difference is not statistically significant. Nevertheless, it may indicate that left governments are hoping to lock in their preferred policy before leaving office. This partisan divergence may further help to explain the large confidence intervals in Figure 4 above. Likely winners versus likely losers along left–right dimension.

The results are similar on the green—non-green dimension (Figure 6). Again, there is suggestive evidence that green governments increase rates more than non-green ones, especially when going into elections where they are likely to lose. Similar to left parties, green governments may be increasing rates when they are likely to lose in an effort to lock-in their preferred policies. However, again, there is no statistical difference in the behavior of green and non-green governments. Likely winners versus likely losers along green–non-green dimension.

Overall, I find that likely winner governments of all parties behave in a manner consistent with my theory, increasing rates as their likelihood of winning grows. Similarly, governments of all parties facing close contests decrease them. The results provide some evidence that the effect of competition is causally prior to governments’ policy preferences. Amongst likely loser governments on the other hand, there is weak evidence of divergence, with left and green governments increasing rates as their likelihood of losing increases and non-left and non-green governments leaving them unchanged. More broadly, the results are consistent with the climate politics research mentioned above, which has found mixed evidence for a partisan effect.

Conclusion

Fossil fuel taxation presents governments with a sharp intertemporal tradeoff: increase voters’ energy costs today to mitigate future climate change and promote long-run aggregate welfare; or keep costs low now, but generate greater future harm. This paper argues that how elected officials respond to this tradeoff depends in part on the electoral environment.

In times of low electoral competition, when governing parties are secure in office, they are better insulated from electoral backlash. Higher insulation enables them to look beyond the next election to society’s long-run welfare and tolerate the electoral risks of imposing costs on voters today for future benefits. However, when competition is high, governments must focus myopically on winning the next contest. Any long-term policy investment that could upset voters, such as fossil fuel taxes, is unlikely to be considered. While politically expedient, such a strategy contributes to greater future costs. In this way, electoral competition shapes governments’ discount rates. When it is low, politicians place a higher value on the future benefits of policy relative to its short-term costs. But when it is high, politicians are likely to heavily discount future policy benefits.

Analyzing an original dataset of gasoline taxation, I find robust empirical support for these arguments. Across a range of model specifications, increases in electoral competition are associated with significant decreases in tax rates. Moreover, I find that the negative impact of competition is moderated by politicians’ perception of voter preferences. When tax increases are expected to impose large personal costs on voters, because fuel consumption is high, heightened competition generates even stronger incentives to not increase rates. The analysis suggests a long-run positive feedback effect between electoral competition, fossil fuel consumption, and fossil fuel taxation, which should generate path dependencies that push countries onto different fossil fuel consumption and taxation trajectories. For those caught in a “high consumption-low tax trap,” such as the US, changing trajectories using taxation alone will likely prove difficult. Lastly, I find little evidence that government partisanship is a significant predictor of tax policy, suggesting that the impact of competition on intertemporal policymaking is relatively independent of party and ideology.

By focusing on the role of the electoral environment, this paper provides a general theoretical framework that can account for the substantial diversity of fuel tax levels within countries over time and across them. Doing so contributes to the emerging subfield of comparative climate politics (Andersen, 2019; Harrison and Sundstrom, 2010; Hughes and Urpelainen, 2015; Lipscy, 2018; Mildenberger, 2020; Wood et al., 2019). While I examine fossil fuel taxes, the argument is applicable to consumption taxes more generally. We should expect electoral competition to play a crucial role is shaping the ability of governments to increase prices for any widely consumed good. Lastly, the paper provides a sharp test of intertemporal policy choice, contributing to debates in political science regarding the politics of long-term policymaking and the myopic effects of electoral competition (Alesina & Tabellini, 1990; Azzimonti, 2015; Boston, 2016; Cronert and Nyman (2021); Garrett, 1993; Hubscher and Sattler, 2017; Immergut and Abou-Chadi, 2014; Jacobs, 2011, 2016; Nordhaus, 1975; Seiferling, 2020).

More broadly, the findings point to a causal mechanism—electoral competition—that should link macro institutions to climate policy. Politicians elected under proportional electoral rules tend to enjoy systematically lower levels of electoral competition relative to those elected under majoritarian rules (Kayser and Lindstädt, 2015). As a consequence, we should expect long-run fossil fuel tax rates to be consistently higher in PR countries. This reasoning is aligned with work that highlights the key role of electoral rules in shaping climate policy outcomes, particularly regarding costs for consumers (Finnegan, 2022a; Lipscy, 2018).

Finally, the findings shed light on the politics of climate policy instrument choice. In instances of low competition, governments should be more likely to increase consumer energy prices using taxes. However, when competition is high, such policies are unlikely to be politically feasible. Instead, politicians are likely to use policies that hide costs from voters. For example, in the transport sector, they are likely to choose fuel efficiency standards (which impose direct costs on manufacturers) or subsidies for electric vehicles (funded through general revenues) over fuel tax increases. Indeed, amidst high levels of competition, recent US climate policy under the Inflation Reduction Act eschews carbon taxation in favor of subsidies, funded in part by increased corporate tax rates. In this way, electoral competition also shapes how politicians distribute the short-term costs of climate change mitigation between producers and consumers. When it is high, costs should be distributed toward producers, and when it is low, toward consumers.

Supplemental Material

Supplemental Material - Changing Prices in a Changing Climate: Electoral Competition and Fossil Fuel Taxation

Supplemental Material for Changing Prices in a Changing Climate: Electoral Competition and Fossil Fuel Taxation by Jared J. Finnegan in Comparative Political Studies

Footnotes

Acknowledgments

For their helpful feedback, I thank Julius Andersson, Dan Berliner, Bjorn Bremer, Marion Dumas, Lior Herman, Robert Keohane, Tobias Kruse, Cathie Jo Martin, Jonas Meckling, David Soskice, Kai Spiekermann, David Vogel and Joachim Wehner, colleagues at the Niehaus Center for Globalization and Governance at Princeton University and the Grantham Research Institute on Climate Change and the Environment at LSE, as well as audiences at the UCLA Comparative Politics Workshop, Stockholm Institute of Transition Economics, 2020 APSA Annual Meeting, 2017 MPSA Annual Conference, and 12th Annual Graduate Conference at the Hebrew University of Jerusalem.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.