Abstract

Political connections provide substantial benefits to firms. We emphasize the ownership of firms as an important channel through which political connections operate and identify a resulting link between political turnover and turnover in the ownership of firms: Political turnover prompts newly politically connected individuals to take, and newly disconnected individuals to cede, ownership of firms. This pattern should be more pronounced in countries with weaker property rights, among firms with publicly recorded owners, and among firms with more immobile assets. Moreover, firms that experience changes to ownership during periods of political turnover should have elevated political connections and therefore pay less taxes and earn higher profits. Analyses of the ownership structure of firms in 87 countries are consistent with the theory. Because politically connected owners allow firms to compensate for other vulnerabilities, the theory also explains mixed findings in prior work on the consequences of asset immobility.

Keywords

How do changes in political leadership affect the economy? A large literature highlights the connections between political and economic markets. Political turnover, through its competitive effects, encourages policy innovation and is a basic condition for political accountability (Dahl, 1967). It also ensures that policy failures are pointed out by the opposition and addressed by the incumbent or by a successor (Kono, 2006; Wittman, 1989). These effects should produce more efficient policies and faster growth. Yet, political turnover also results in uncertainty and policy change. By undermining investment and dampening growth, these effects point to the potentially adverse economic consequences of political turnover (Arezki & Fetzer, 2019; Earle & Scott, 2015).

Exploring another consequence of political turnover, we argue that political turnover is likely to lead to changes in firm ownership. We begin with two observations. First, owners with political connections plausibly expect to earn elevated profits relative to those without connections (Faccio, 2006; Fisman, 2001; Krueger, 1974; Szakonyi, 2018). 1 Second, political turnover leads to a shift in connections (Albertus & Menaldo, 2012; Mattes et al., 2016). Building on these premises, we identify a specific mechanism through which political turnover leads to ownership changes. Because political connections and thus some of the policy consequences of political turnover are specific to owners, a firm’s value is specific to owners as well: the value of a firm’s assets for a connected owner is higher than for an unconnected owner. Owners that lost connections are willing to sell at a lower price than before, and owners that gained connections are willing to purchase at a higher price than before. Political turnover thus creates a wedge in the value of ownership for current and potential owners, resulting in an environment in which the ownership of firms is likely to be transferred across individuals.

In extreme cases, governments may assist politically connected raiders with takeovers (Gray et al., 2019; Markus, 2015; Markus & Charnysh, 2017) or they may reassign ownership directly. After Viktor Yushchenko was elected President of Ukraine in 2005, the government nationalized and sold firms to new owners in a process called “reprivatization”. The targeted firms – including large steel producer Kryvorizhstal Steel – had few connections to President Yushchenko but their former owners were associated with former President Leonid Kuchma and his chosen successor Victor Yanukovych (Åslund, 2005; Earle & Scott, 2015). That these nationalizations are more common among politically connected firms suggests that ownership is sensitive to political conditions (Resimic, 2021).

We argue that these extreme cases are part of a broader pattern where the ownership of firms reacts to politics. We expect political turnover to result in elevated ownership turnover that is, at least partially, voluntary and widespread. These effects should be most pronounced in countries with weak property rights, among firms with more immobile assets, and among firms with more clarity in their ownership structure: Weak property rights create an opportunity for politically connected individuals to seize ownership, while the owners of firms with immobile assets are more sensitive to policy change (Bates & Lien, 1985; Boix, 2003). Firm owners may obfuscate their identities by locating the ownership of their assets in shell companies abroad; these may be harder for politically connected raiders to target (Earle et al., 2019; Markus, 2015).

Empirical results from firm-level data are consistent with our expectations. 2 Drawing on data from up to 87 countries, we identify direct shareholders of the largest firms in each market using the Orbis database. To measure turnover in firm ownership, we code changes to the identity of majority owners. We show that political turnover, as measured in the REIGN data set (Bell et al., 2021), leads to elevated ownership turnover. The effect is larger among firms with more immobile assets and in countries with weak property rights. The relationship is also confined to those firms where the names of individual owners are recorded in the Orbis database (which in turn draws on business registries): where ownership appears more obfuscated, the effects of political turnover are depressed.

Because the relationship could be endogenous due to omitted variables, we also report results from instrumental variable specifications, using exogenously timed elections as an instrument for political turnover. We further show that political turnover does not correlate with managerial turnover, indicating that these new owners are unlikely to have taken over due to superior expertise. Finally, we offer tentative evidence that firms whose ownership changed during political turnover earn higher profits and pay lower taxes.

By emphasizing political influence through the owners of a firm’s assets, we contribute to a growing literature that examines the use of ownership structures for political influence, for example through partnerships with foreign owners (Betz & Pond, 2019; Gray, 2020; Markus, 2008), through the design of complex offshore ownership structures (Betz et al., 2021; Earle et al., 2019), or through the issue of stock market securities (Pond & Zafeiridou, 2020). While we view the issue from the perspective of the owners, rather than from the perspective of firms, our framework builds on a similar logic: we identify how the ownership structure of firms responds to political conditions, because owners differ in their political clout. We consider owners whose clout comes from their ties to the government, rather than from owners whose clout comes from their independence from the government. We also note the distinction between firms and owners: Starting from the premise that political connections are fixed to individuals, we highlight how political connections become endogenous to firms, because connected individuals are more likely to become firm owners.

The paper has implications for several additional lines of inquiry. First, the paper has implications for the large literature aimed at measuring the effects of political connections on business performance. These studies primarily look to the participation of close family members or politicians themselves as owners or board-members to identify politically connected businesses (Faccio, 2006; Fisman, 2001; Gehlbach et al., 2010; Resimic, 2021; Szakonyi, 2018). In contrast, we focus on the association between leadership turnover and ownership turnover, which, we argue, extends to a broader set of firms than those with, for example, politicians as owners. By employing an alternative strategy to identify connections, our study complements existing work and is consistent with a positive, albeit small and imprecisely estimated, effect of connections on profits. Our results also suggest that existing work may have under-estimated the value of connections: if firm ownership adapts to political turnover, political change may have only muted observable effects on firm performance for any given firm.

Second, we offer a potential explanation for a pattern documented in recent research: contrary to theories that emphasize asset mobility as a source of firm influence (Bates & Lien, 1985; Boix, 2003; Vernon, 1971), immobile firms appear to receive better treatment from governments (Chen & Hollenbach, 2020; Danzman and Slaski, 2022; Jensen, 2013; Pond & Zafeiridou, 2020). Our argument suggests that immobile firms receive policy benefits because they are likely to have been purchased or taken over by someone with political connections. This interpretation is not inconsistent with the existing intuition: The owners of immobile firms are still subject to government intervention. This intervention shows up as ownership transfer rather than elevated tax rates.

Finally, political turnover can impose costs on firms through policy uncertainty (Bloom, 2009), inefficient fiscal and monetary cycles (Clark & Hallerberg, 2000), depressed growth (Aizenman & Marion, 1993), and shorter government time horizons (Fortunato & Turner, 2018). Political turnover creates additional inefficiencies if attempts to forge political connections trump business considerations. Political connections may for example provide policy benefits, as we argue, but they may also encourage risk-taking (Tihanyi et al., 2019), because politically-connected owners may have access to state-sponsored financing or they may expect to be bailed out. 3 Where firm ownership is political, there is no reason to expect competitive markets and qualified owners to prevail. The lack of business qualifications of some politically connected owners provides a new channel through which political influence suppresses economic growth. This is not to say that the downsides of political turnover overwhelm the benefits. But the downsides of political turnover for economic markets are worth understanding, as are the attempts by citizens and firms to adjust to such uncertainty.

From Political Connections to Political Ownership

In this section, we first outline the argument relating political turnover to turnover in the ownership of firms, and how this relationship is conditional on firm- and country-specific factors. We then derive empirical predictions from a formal model.

Governments can impose substantial benefits and costs on firms. Both a firm’s profits and the value of its assets are thus exposed to political decisions. The consequences, however, are not distributed evenly across firms. Politically connected firms are more likely to gain favorable treatment and to avoid adverse policies. Political connections may come from many sources, including family networks, shared ethnicity, party affiliation, previous employment, or education. One channel through which political connections operate is through the owners of the firm. Firm owners have strong incentives to leverage political connections, allowing them to earn higher profits or even to takeover firms from existing owners (Albertus & Menaldo, 2012; Earle & Scott, 2015; Faccio, 2006; Fisman, 2001; Krueger, 1974; Markus, 2015).

That owners benefit from political connections is, of course, not guaranteed. Recent work casts doubt on the extent to which connections confer such benefits (Resimic, 2021; Tihanyi et al., 2019), in part because politicians, rather than owners, might appropriate most of the excess rents stemming from connections. However, these studies also note that political connections allow firms to pursue riskier strategies, leading to a higher variance in outcomes that masks substantial benefits for some owners and in some contexts (Tihanyi et al., 2019). Moreover, some of the benefits of political connections may be informal and excluded from balance sheets. In what follows, we therefore simply assume that current and potential owners at least hold a belief that connections have some benefits. That such benefits can be expected to exist appears as a reasonable default assumption – even if political connections might ultimately have little reported payoff for the average owner ex post.

We focus on firms with connected owners, which are different from state-owned enterprises, where the state itself has control. That said, firms may have political influence if their owners are politicians themselves (Gehlbach et al., 2010; Markus & Charnysh, 2017; Szakonyi, 2018). Such owner-politicians should more easily secure their preferred policies. Politician-owners also face a simpler bargaining problem: they can appropriate all the rents from political connections. In the following, we do not distinguish between owner-politicians and connected owners; we instead assume that both confer benefits to firm owners. We further assume that political connections are fixed and exogenous to the individual. In particular, individuals cannot invest in strengthening their connections.

Connected owners may receive preferential treatment through a variety of channels. Most immediately, they might receive targeted benefits. Examples include biased selection procedures for government contracts, tax breaks and subsidies, selective enforcement of existing policies, or support in court cases. Governments can also reach for preferential regulatory policies, which mandate the use of specific technologies and products, driving up the profits of firms that produce those. Connected owners may also benefit from informational channels: they may use their access to policymakers to provide information that shapes policy in their favor (Hansen, 1991), or they may obtain private information about proposed policy changes. For firms without political connections, policies may impose direct costs from differential treatment or indirect costs if their competitors gain an advantage.

Several examples illustrate how political connections allow individual firms to gain privileged treatment from their government. Gürakar (2016) notes that the Turkish governing party, the AKP, has amended the country’s public procurement law over 150 times within a decade, increasing political discretion over government contracts and allowing the AKP leadership to award high-value contracts to individual firms. Firms whose owners had political connections and shareholders who publicly supported the AKP fared better in procurement contracts than other firms.

In Tunisia, the customs office appears to have selectively ignored underreporting by connected firms. Firms connected to then President Ben Ali reported lower unit values for each imported good, reducing the import duties they paid (Fisman & Wei, 2004). In 2009 alone, politically connected firms managed to evade import tax payments of over US$200 million relative to unconnected firms (Rijkers et al., 2015). With the ouster of Ben Ali in the Arab Spring and the privatization of these firms, previously connected firms lost these privileges relative to other firms, and the gap in reported unit values vanished.

Politicians’ ability to reward those with political connections is a specific type of corruption. In particular in non-OECD counties, corruption remains a substantial challenge, property rights enforcement is frequently incomplete, and politicians retain discretion in channeling benefits to their connections. This is not to say that political connections do not matter in OECD countries (Amore & Bennedsen, 2013; Markgraf & Rosas, 2019), rather that the benefits are plausibly smaller, more difficult to detect, and more likely to lead to scrutiny.

When political connections change, it opens up the possibility of ownership change through sale or takeover. Political change has two important consequences for firms and their owners. First, new politicians design and implement new policies, which may impose new costs and open up new opportunities for firms. Second, a change in the political leadership disrupts political connections. New politicians frequently have a new set of political connections. Newly connected owners can leverage their political connections to manage policy uncertainty and shape policy in their favor. Previously connected owners lose their privileged access to policy-makers and, uncertain about the future direction of policy, may want to exit the market.

An example from Ukraine illustrates this mechanism. When a new mayor came to power in the town of Kharkiv, he generated a new set of political connections. A friend of the mayor was interested in taking over a project from the firm Khar’kov-Moska. The friend’s interest was reflected in government actions, which included biased inspection reports, several legal cases against the firm, the annulment of the firm’s land lease, and the imposition of a large fine (Markus, 2015, p. 54). The allegations against the firm intensified, even as a county-level agency acknowledged that the case had no merit, and the local TV station reported that a local businessman – “who happened to be the mayor’s friend” – was interested in the project (Markus, 2015, p. 55). 4 The attack continued for 2 years, until Khar’kov-Moska abandoned the project.

We argue that this episode is part of a broader pattern: turnover in political connections changes the value of firm ownership for specific individuals and thus opens up opportunities for connected potential owners to buy or seize firms from unconnected owners. Although expropriation and other politically connected takeovers have received substantial attention in the literature, purchases of firms may be the most common method of ownership transfer. On the one hand, this implies that ownership transfers happen at least partially voluntarily. On the other hand, such a sale of firms may take place with the implicit understanding that the sale avoids complete loss for the current owner through expropriation. We formalize this interaction in the next section. For now, we note that political turnover should translate into ownership turnover. The underlying mechanism is that connected owners may perceive a higher value for the same underlying firm than unconnected owners, which opens up room for elevated rates of ownership turnover. Consequently, we expect such ownership transfers to be a systematic and relatively widespread pattern that is not limited to just a few firms.

A similar dynamic would apply if the owner is also a politician. In this case, if the owner or his allies lose office, it limits his ability to obtain his preferred policies. This loss of influence reduces rents, opening up an opportunity for buyers with stronger political connections who attach a higher value to the firm. Even those without political connections might seek ownership of the firm if they have more expertise than the former owner-politician. Alternatively, if the owner takes office, we expect his firm to perform better, perhaps providing him with the opportunity to expand his business and purchase other firms with more limited political influence.

While political connections provide benefits, the size of the benefits plausibly depends on the characteristics of firms and countries. We consider three such characteristics in the following: asset mobility, ownership clarity, and the rule of law.

First, firms vary in their reliance on mobile assets in the production process. Mobile assets can by definition be easily relocated or repurposed to a different use, which is not subject to government oversight. Firms with mobile assets, including liquid financial assets but also intangibles such as intellectual property or trademark rights, enjoy political influence regardless of the identity of their owner: They can threaten to move their assets abroad or to reallocate their assets to purposes that are more difficult to regulate or tax. This threat grants them influence, and politicians make policy concessions to these firms in order to retain their investment (Bates & Lien, 1985; Boix, 2003). Firms with mobile assets consequently are less affected by political connections, as they have political influence regardless of the identity of the individual firm owner.

In contrast, firms with immobile assets – which include physical assets like plants, property, and equipment – cannot credibly threaten to exit the market and thus lack political influence from their asset ownership. For these firms, the identity of the owner becomes more important. When politicians change policy, these firms must cope with the regulation. Immobile asset owners are not only likely to bear the costs of government taxation and regulation, they are also often the first targets for expropriation: Because their assets are difficult to hide, the future owner is assured of continued profits. The inability to withhold assets from government regulation and taxation therefore makes the owners of immobile assets especially vulnerable to government policies. The owners of Kryvorizhstal Steel, for example, had no recourse when the government seized their holdings.

Second, some firms and their owners should also be less exposed to politics because their ownership structure is obfuscated. For example, owners may nest their ownership claim in a shell company located in a tax haven, which often will not require them to report their identity. This allows owners to obscure their true holdings (Earle et al., 2019). This obscurity may make it harder for governments and raiders to target them (Markus, 2015), as they cannot rely on public reports to know who to target. Owners may also create subsidiaries in third markets that provide protection under bilateral investment treaties (Betz & Pond, 2019; Gray, 2020), which frequently grant access to investor-state dispute settlement bodies if they perceive that their property rights are violated by their home governments or by government supported individuals; or they may rely on complex corporate structures to benefit from the network of tax treaties (Arel-Bundock, 2017).

When an owner obscures an ownership claim through a shell or a firm located abroad, the physical assets remain in the country. Nevertheless, owners who have obscured their ownership structures – to deter government predation, to gain access to bilateral investment treaties or tax treaties, or to access financing – may be targeted for ownership transfer less frequently. At the same time, more obscure ownership structures frequently deter purchases by third parties. For example, the Financial Action Task Force notes that “corporate vehicles to obscure ownership” should serve as a red flag for financial institutions when deciding on customers. 5 Taking over such firms therefore should be less attractive to potential new owners who want to take advantage of their political connections. For these reasons, we expect political turnover to result in a smaller increase in ownership turnover among firms with obscured ownership.

Third, the effects of political turnover should also depend on country-level characteristics, and specifically the rule of law. In countries with strong rule of law, smaller gains are associated with political connections. Those who are harmed by the political connections of their competitors may have recourse in courts. They can initiate court cases and count on unbiased judges and impartial enforcement of their rulings. This makes it more difficult for politicians to provide benefits to associates, and reduces the wedge between firm valuations for politically connected and politically unconnected owners. The benefits may be even more pronounced in the extreme case of raiding: raiders cannot count on biased courts to uphold their frequently fraudulent claims. Moreover, awareness of these legal options can help deter preferential treatment in the first place. Politicians will be reluctant to provide benefits to their allies, knowing that their policies may be subject to challenge later.

We have less clear expectations for another country-level characteristic: the type of the economic system. On the one hand, in systems where state intervention in the economy is widespread, more firms have direct interactions with the state, such that political connections become potentially more important and relevant to a larger set of firms (Tihanyi et al., 2019). Especially where the financial system remains under state control, politicians can channel resources to firms with politically connected owners. Privatization episodes, when moving toward market economies, may also provide an opportunity for politically connected owners to takeover firms – and they might cede ownership later on in the wake of political turnover. On the other hand, in market economies, too, virtually all firms have indirect interactions with the state, for example through regulatory policies. These can be just as relevant. A finding from the literature on international investment illustrates this point: the majority of disputes between foreign investors and host governments are now over cases of ‘indirect expropriation’ (Pelc, 2017). Moreover, in market economies, deeper and broader financial markets might provide sufficient liquidity to make financing constraints less binding.

In the next section, we briefly present a formal model, which allows us to clarify some of our assumptions. It also elucidates the relationship between forced sales and voluntary purchases, and it identifies several conditional relationships which we exploit empirically.

Formal Model

There are n + 1 actors in the game, one current firm owner and n potential firm owners. These potential owners may become ‘buyers’ or ‘raiders’.

Sequence of Play (1) Nature determines whether there is political turnover. (2) Each potential owner decides whether to make an offer to buy the firm from the existing owner, to try to takeover the firm, or to do nothing. (3) If the potential owner made an offer, the current owner decides whether to accept or reject.

The owner attaches a value of v(α o ) to the firm, which depends on his connections to the politician in power, α o . For simplicity, we denote this v o in the following. Each potential buyer attaches a value of v (α i ) to the firm, where i ∈ 1, …, n (and n > 1) and similarly denoted v i . The value of the firm, for both the owner and potential buyers, is increasing in political connections ∂v i /∂α i > 0. We also denote the largest value of all the potential buyers’ valuations and the largest value for political connections as v m and α m respectively. We therefore assume that political connections are fixed to individuals.

The game starts with an owner who has the strongest political connections of any of the n + 1 individuals, α o = α m , and thus the highest valuation, v o = v m . With probability τ there is political turnover and with probability 1 − τ political leadership remains unchanged. When a new politician comes to power, we assume that existing political connections are disrupted. The new connections, α o for the owner and α i for each prospective owner, are independently drawn from distribution f(α i ). 6 Following turnover, 1/2 is the probability that any one owner has less valuable political connections than the existing owner, and 1/2 n is the probability that the n potential buyers all have connections that are less valuable than the existing owner. Thus 1 − 1/2 n is the probability that at least one of these buyers has stronger political connections than the existing owner (in which case a m ≠ a o ).

Changing firm ownership is associated with a cost, c, which is assumed to be exogenous. This cost is firm-specific and represents the challenge of operating a new firm, in which the new owner may have limited expertise (see Johns & Wellhausen, 2020). Consistent with prior work, this cost is distinct from the concept of mobility, which we turn to below. If the buyer offers to purchase the firm and the owner accepts, the owner’s payoff is l (the list price), while the buyer’s payoff is v i − l − c. If the owner refuses the offer, the owner’s payoff is v o while the buyer receives 0. If the buyer decides neither to offer to purchase the firm nor to force its sale, the owner’s payoff is v o and the buyer’s payoff is 0.

If the buyer attempts to takeover the company, both the owner’s and the buyer’s payoffs depend on the quality of property rights. There are two sources of property rights in the model: a political source and an institutional source. The political source is owner-specific and comes from the strength of political connections: If the owner has stronger political connections than the potential raider, α o ≥ α i , then the raider cannot takeover the firm. The owner would tap into his political connections to prevent any takeovers from less connected raiders.

When the owner does not have stronger political connections than potential buyers, α m ≠ α o , then he is subject to raiding, but he can tap into property rights from institutional sources, which we call ρ ∈ [0, 1]. Institutional sources of property rights include the availability of an unbiased legal process, where targets of takeovers can seek and obtain compensation through courts or arbitration. Where property rights are stronger, current owners receive a higher expected value, and potential acquirers a lower value, in case of an attempted takeover. This combines two interpretations of property rights: Where property rights are stronger, a forced sale is (1) less likely to be successful, and (2), if successful, requires ex-post compensation to the prior owner. We also allow for a reputational cost. We denote the reputation cost of takeovers as r, which is consistent with the idea that takeovers are likely to attract attention and discourage future investments (Markus & Charnysh, 2017). The owner’s payoff following takeovers is ρv o , while the raider receives (1 − ρ)v i − c − r.

We focus on the behavior of the buyer with the strongest political connections, α m , as we want to rule out cycles in ownership transfers and we expect that the most politically connected buyer would dominate when in competition with less connected buyers.

To solve for the subgame perfect Nash equilibrium of the game, we must consider two possible cases. The first case occurs when the owner retains the strongest political connections, α o = α m , and thus the highest valuation, v o = v m . 7 When the owner has stronger connections than all potential buyers, no buyer can force the sale. The prices that are acceptable to the buyer, v i − l − c ≥ 0⇒l ∈ [0, v i − c], are too small for the owner, who has the highest valuation, v o = v m > v i − c. In equilibrium, the buyer makes no offer anticipating that the owner will refuse.

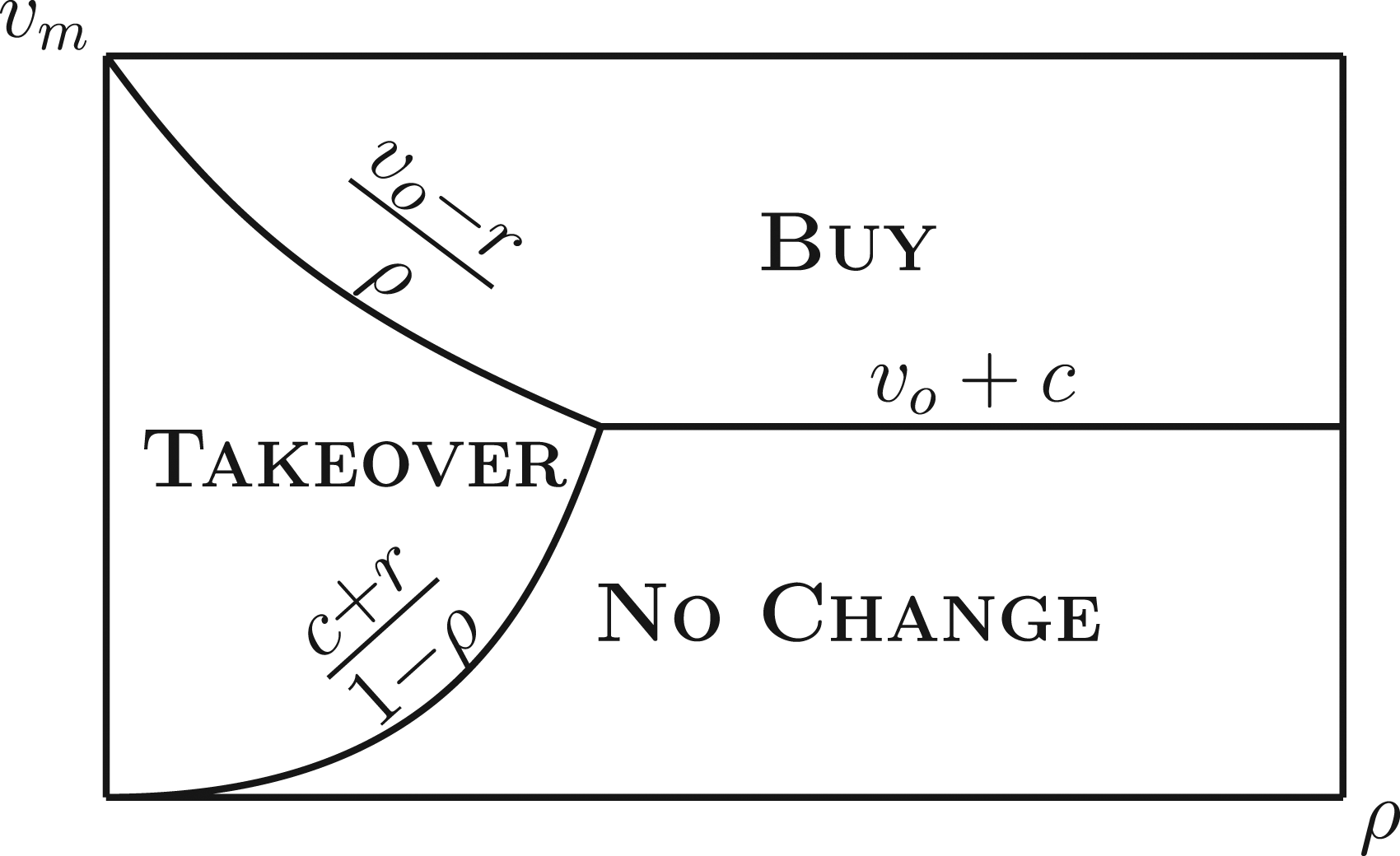

Now consider the second case, where the owner does not have the strongest connections and there is at least one valuation larger than the owner’s value, v

m

≠ v

o

. The owner will accept any price such that l ≥ v

o

. Which equilibrium obtains depends on the potential buyer’s behavior. He will offer and purchase the firm for l⋆ = v

o

if v

m

≥ v

o

+ c and v

m

≥ v

o

− r/ρ. He will instead takeover the firm if v

m

< v

o

− r/ρ and v

m

≥ c + r/1 − ρ. Finally, he will do nothing if v

m

< v

o

+ c and v

m

< c + r/1 − ρ. Figure 1 depicts the equilibria and the constraints. Sub-game perfect Nash equilibria (when v

o

≠ v

m

) as a function of the largest potential buyer valuation, v

m

on the horizontal axis, and the quality of property rights, ρ on the vertical axis.

From this discussion, we derive our first set of results. Proofs are in the Supplemental Appendix.

Political turnover increases the probability of ownership turnover.

Because political turnover has heterogeneous, individual-specific effects, granting some potential owners stronger political connections and thus higher valuations than others, it opens up the opportunity for ownership transfers. Newly connected owners purchase firms from newly disconnected owners. However, these effects are not the same across countries.

Although ownership turnover is elevated following political turnover, the magnitude of the ownership turnover is smaller in countries with stronger property rights.

In countries with stronger property rights, it is less likely that political turnover induces ownership turnover than in countries with weaker rights. Property rights reduce the benefits of forced takeovers, making it less likely that the value of the firm is sufficiently large to overwhelm the cost of the ownership transfer for the new owner. We now turn to two variations of the model which capture firm-specific attributes that condition the relationship between political turnover and ownership turnover.

Asset Mobility

The existing literature emphasizes the importance of asset mobility in providing firm owners with political influence, because mobile assets can be withdrawn from the government’s jurisdiction more easily. Following these arguments, we assume that the owner of a mobile firm can move the firm out of the government’s and potential raider’s reach if takeover is threatened. We thus remove the takeover action from the strategy space. 8

Although ownership turnover is elevated for all firms following political turnover, the magnitude of the ownership turnover is smaller for firms with mobile assets.

Obfuscated Ownership

The literature also highlights that some owners may choose to obfuscate their ownership, making it more difficult for governments and politically connected raiders to takeover their businesses. We add a move to the game where, following the move by nature, the owner can opt to obscure his identity. If he does so, we simply replace ρ, the level of the institutional property rights in the country, with ι, the quality of the obfuscation. 9 The owner’s payoff following an (attempted) takeover is ιv o , while the raider receives (1 − ι)v m − c − r.

Although ownership turnover is elevated following political turnover, the magnitude of the ownership turnover is smaller among companies whose owners have obfuscated their ownership.

Empirical Implications

In sum, we emphasize the ownership of firms as an important channel through which political connections matter. Political turnover results in a redistribution of political connections where newly connected owners can buy or seize firms and newly disconnected owners lose their ownership. The above discussion and formal model produce the following expectations.

Changes in political leadership should increase the probability of changes in firm ownership.

The effects of political turnover on ownership turnover should be less pronounced among (a) Firms with obfuscated ownership structures, (b) Firms with more mobile assets, and (c) Countries with stronger property rights.

Empirical Evidence

We first evaluate the unconditional relationship from Hypothesis 1. We also discuss several robustness checks and additional evidence for the mechanism we identify. We then turn to the conditional relationships from Hypothesis 2. Finally, we relate politically connected owners to metrics of firm performance.

We gather data on firm activities in 87 countries. Our main sample excludes OECD members, which share a commitment to the rule of law and transparent market economies; we therefore expect owners in OECD countries to rely less on political connections and potential raiders to face limits on their predation. 10 We also exclude countries that are not included in the REIGN data set (Bell et al., 2021), which we use to generate measures of political turnover, or in the ICRG data set (PRS Group, 2015), which we use to control for investor protections. We also exclude tax havens. Finally, we exclude most low-income countries by the 2015 World Bank classification, which have limited data on business ownership.

We assemble a data set in the firm-year format. While much of the literature on political connections measures connections between policy-makers and firms explicitly, we take a more agnostic approach. One of our contentions is that the logic of political connections applies to a broader set of firms than those with, for example, a policy-maker as owner. Consequently, we evaluate whether political turnover leads to changes in the ownership of firms, regardless of whether these firms can be classified as politically connected based on existing datasets.

We first require data that measure meaningful changes to firm ownership. We draw on Bureau van Dijk’s Orbis database to identify direct shareholders for up to the 5000 largest companies in each country (by operating revenue for the most recent available year). The companies in our data set represent all major industries and include both publicly-listed and privately held firms. We select the largest companies to mitigate the lack of information on firm characteristics. The data include owners from 2008 to 2018. In many countries, fewer than 5000 firms with available operating revenue are recorded in the Orbis database, and in some cases only a few firms are reported. Still, on average, Orbis lists 4749 firms with operating revenue per country. Even within this set of large firms, we frequently encounter missing data, and on average have ownership information for at least two consecutive years (which is necessary to identify ownership changes) for 3235 firms for each country (with a median of 3826). In a random sample of firms and in low-income countries, missing data become even more prevalent.

Selecting the largest companies may also reduce bias in our sample. Some countries are more transparent and have stronger reporting standards than others, which likely correlates with institutional variables related to political selection and economic systems (Hollyer et al., 2014). By looking at the largest firms, we increase the likelihood that we have a comparable sample across countries: a comparison with industry benchmarks and representative micro-data suggests that Orbis is most suitable for the largest firms within countries (Bajgar et al., 2020). The inclusion of country fixed effects, by conditioning for the source of missingness, also alleviates some of these concerns (Arel-Bundock & Pelc, 2018).

We identify controlling owners as those with an ownership share of at least 50%. Based on this variable, we code changes in the controlling owner of each firm.

Our focus on the 50% threshold is consistent with the prevalence of controlling owners around the world, even among the largest firms (La Porta et al., 1999). 11 The focus on majority owners also ensures that the results are comparable across publicly-traded and private firms and that the results are not driven by minor changes in shareholder composition or by inconsequential changes to executive boards. The results are robust when limiting the sample to firms with a majority owner (reported in the Supplemental Appendix). In any given year, 12.3% of the firms in our sample experience an ownership change. 41% of the firms in our sample experienced an ownership change at least once during the sample period.

Because we use data on recorded, direct shareholders, we cannot account for proxy ownership, where the true owner does not appear at all in the ownership chain, and indirect ownership, where the true owner uses intermediaries. The existence of proxy and indirect owners could bias the association between political turnover and ownership changes in several ways. First, we would observe elevated rates of ownership change if the proxy or indirect owner was better connected than the true owner and this is no longer the case with a change in government. Then the true owner might want to reorganize ownership, reinforcing the patterns we expect to observe. The underlying logic is still one of political connections, but it is no longer grounded in voluntary ownership transfers – rather, true owners are strategically re-assigning intermediary owners. Second, the existence of proxy or indirect owners might induce lower rates of ownership change if the goal of such structures is to insulate firms from politics. That is, rather than inserting connected owners, true owners might seek to put neutral owners in place, who become less susceptible to leadership change. Then, leadership change no longer necessitates ownership change. Third, proxy and indirect ownership might occur at differential rates across firms: plausibly, they are most common for politically exposed firms, as suggested by Earle et al. (2019), and more common in countries with weaker institutions and more government interference, reinforcing the first two mechanism for this set of firms. Unfortunately, accounting for proxy and indirect ownership is not feasible with our data, such that we leave it to future work to explore these issues. At the same time, we note that the first mechanism is broadly consistent with our argument of politically connected ownership, while the second mechanism would work against finding an association between political turnover and ownership change. We also strive to address at least some of these issues in the obfuscation models discussed below.

To measure political turnover, where a new leader takes power who is plausibly connected to a different set of constituents, we use the REIGN data (Bell et al., 2021). We code a dummy variable,

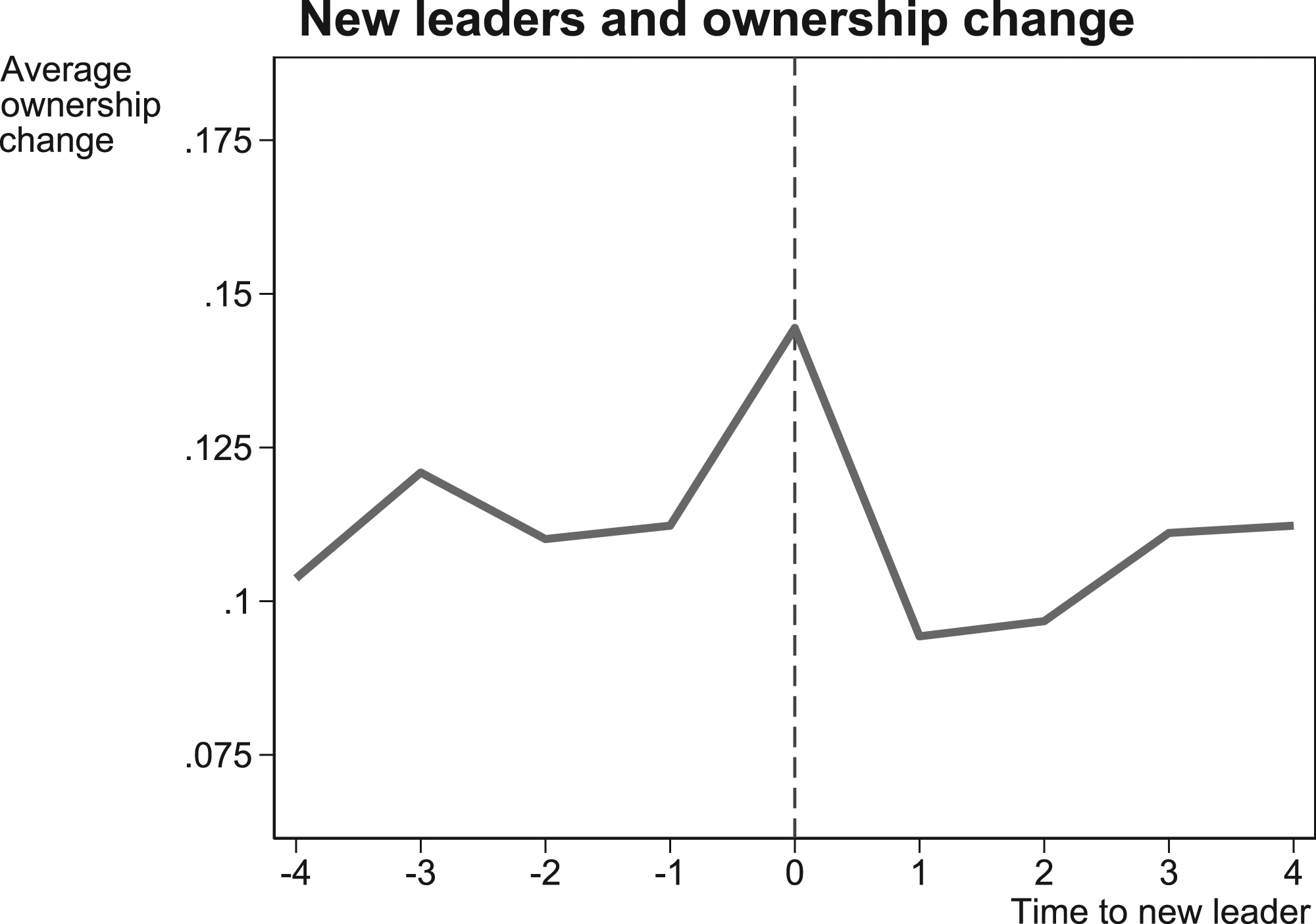

Figure 2 presents the average number of changes to controlling ownership as a function of the years since political turnover. The figure displays a large increase in controlling ownership change in the year of political turnover, but not in years before or after. To assess the robustness of this pattern, we next present a series of regression models. Leadership change and ownership turnover: Time to leadership change on the horizontal axis, share of firms with ownership change on the vertical axis.

We estimate linear regression models, with standard errors clustered by firms to account for arbitrary correlation within firms. We estimate linear regression models instead of logit models to facilitate interpretation across models and to accommodate some of the fixed effects specifications. We present results for alternative estimators and clustering choices in the Supplemental Appendix. As we report in the Supplemental Appendix, the results lose statistical significance when clustering at the country level, but regain statistical significance at the conventional 5% level in models that impose more structure, such as a random effects model. All models include year fixed effects to account for common time trends across observations. We include a series of control variables, which capture both country-specific and firm-specific variables (including country fixed effects). Once merged, the data set includes up to 457,729 firm-year observations, which represent 80,885 firms in 87 countries.

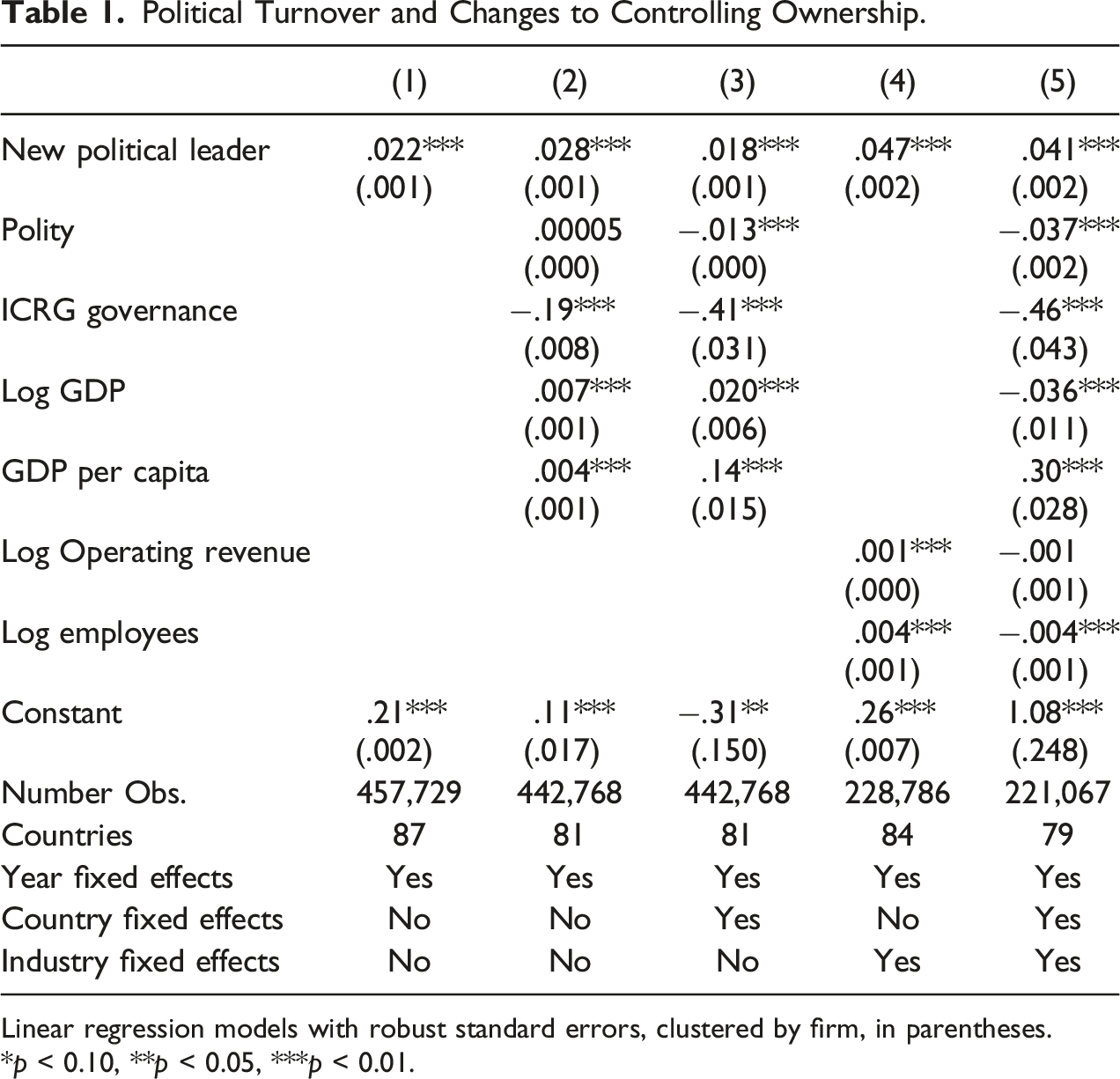

Political Turnover and Changes to Controlling Ownership.

Linear regression models with robust standard errors, clustered by firm, in parentheses.

*p < 0.10, **p < 0.05, ***p < 0.01.

On average, political turnover is associated with ownership turnover. The substantive effects are relatively large. In the simplest model, in column 1, leadership turnover results in an increase in ownership turnover of 2.2 percentage points, or 17.2% compared to the sample average. 13 This marginal effect increases to 21.5% with the introduction of country-level controls in column 2; it drops to 14.0% with the inclusion of country fixed effects in column 3. The marginal effects increase further with the introduction of firm-level control variables: based on the results in column 4, leadership turnover is associated with an increase in ownership turnover of 35.7%. Similar results obtain in the final model reported in column 5. The effects are statistically significant at the 5% level in all models.

In the Supplemental Appendix, we present results exploring different lead and lag structures. We find evidence of anticipation effects: while past leadership change depresses ownership turnover, future leadership change is associated with increased ownership turnover. We also find that the history of political turnover predicts ownership change: ownership change is less likely in countries with more frequent leadership changes. This is consistent with forward-looking buyers discounting the value of connections where turnover is frequent. 14

In the Supplemental Appendix, we also report that the results are robust when accounting for several alternative explanations.

Political Business Cycles

Because elections and therefore political turnover may be accompanied by monetary or fiscal expansions (Clark & Hallerberg, 2000), which could also increase ownership turnover, we add controls for monetary policy (broad money as a share of GDP) and fiscal policy (general government final consumption expenditure as a share of GDP). Both variables are from the World Development Indicators.

Political Violence

Political and economic turnover could result from episodes of violent conflict. We add controls for military expenditure as a share of GDP from the Stockholm International Peace Research Institute (SIPRI), the number of peacekeepers in the country from the UN Department of Peacekeeping Operations (logged) and the number of internally displaced persons from the Internal Displacement Monitoring Centre (logged).

Government Reporting

The capacity of governments to report data could be related to both political turnover and the quality of data provided about firm ownership. We add a control for the quality of reporting using the IMF Statistical Capacity Indicator. It is also possible that reporting standards, and the prevalence of different types of owners, vary across economic systems. We therefore control for the Fraser Index of Economic Freedom (Gwartney et al., 2021), for both the current level and the level in 1990 (to capture conditions before the economic transition in many post-Soviet states).

State Intervention

The results could be explained by privatization: If a new leader privatizes firms early in his tenure (Frye & Mansfield, 2004), leadership turnover would be associated with ownership turnover. As a (coarse) control for the extent of public ownership of firms, we add a control for the size of the public sector as a share of GDP. We also limit the sample to firms with at least two owners in any given year, which excludes all firms that are fully state-owned. And we control for the Fraser Index of Economic Freedom (Gwartney et al., 2021). Moreover, we report that the association between leadership change and ownership change is strongest in countries that underwent the largest movement toward a market economy on the Fraser Index of Economic Freedom; and that the effects are largest where financial markets are least repressed.

Identification and Placebo Test

In this subsection, we present results to further corroborate the causal mechanism: instrumental variable estimates to counter concerns over omitted variable bias, and a placebo test to provide evidence for the ownership mechanism we emphasize.

Instrumental Variable Estimates

New political leadership could be endogenous to turnover in firm ownership because of omitted variables. For example, if elections are scheduled when the economy is performing well and if ownership turnover is elevated during periods of rapid growth, political turnover might be associated with ownership turnover. This could explain some of the results reported here, even if political connections play no direct role in changes to firm ownership. To alleviate these concerns, in addition to using control variables, we use an instrumental variables approach.

We exploit political turnover induced by exogenously timed elections. Exogenously timed elections are an institutional characteristic. These elections cannot be scheduled during advantageous electoral times. Moreover, by focusing on exogenously timed elections, our results are not driven by leadership change that follows government failure, which might correlate with ownership turnover through other channels – such as societal turmoil.

To identify countries with exogenous election timing for executive elections, we use the distinction between presidential systems and parliamentary systems (data from Cruz et al., 2015). In presidential systems, the executive is not politically dependent on the legislature, and executive elections are the main mechanism for regular change in the executive. In parliamentary systems, in contrast, the legislature can replace the executive even outside regular election intervals. And, if the legislature is dissolved, the executive can call new elections in many parliamentary systems. We thus define a dummy variable for executive elections, which is equal to one in years of executive elections and zero otherwise, and limit our sample to countries with presidential systems, where election timing is exogenous. We observe leadership change in about 50% of all elections in our sample.

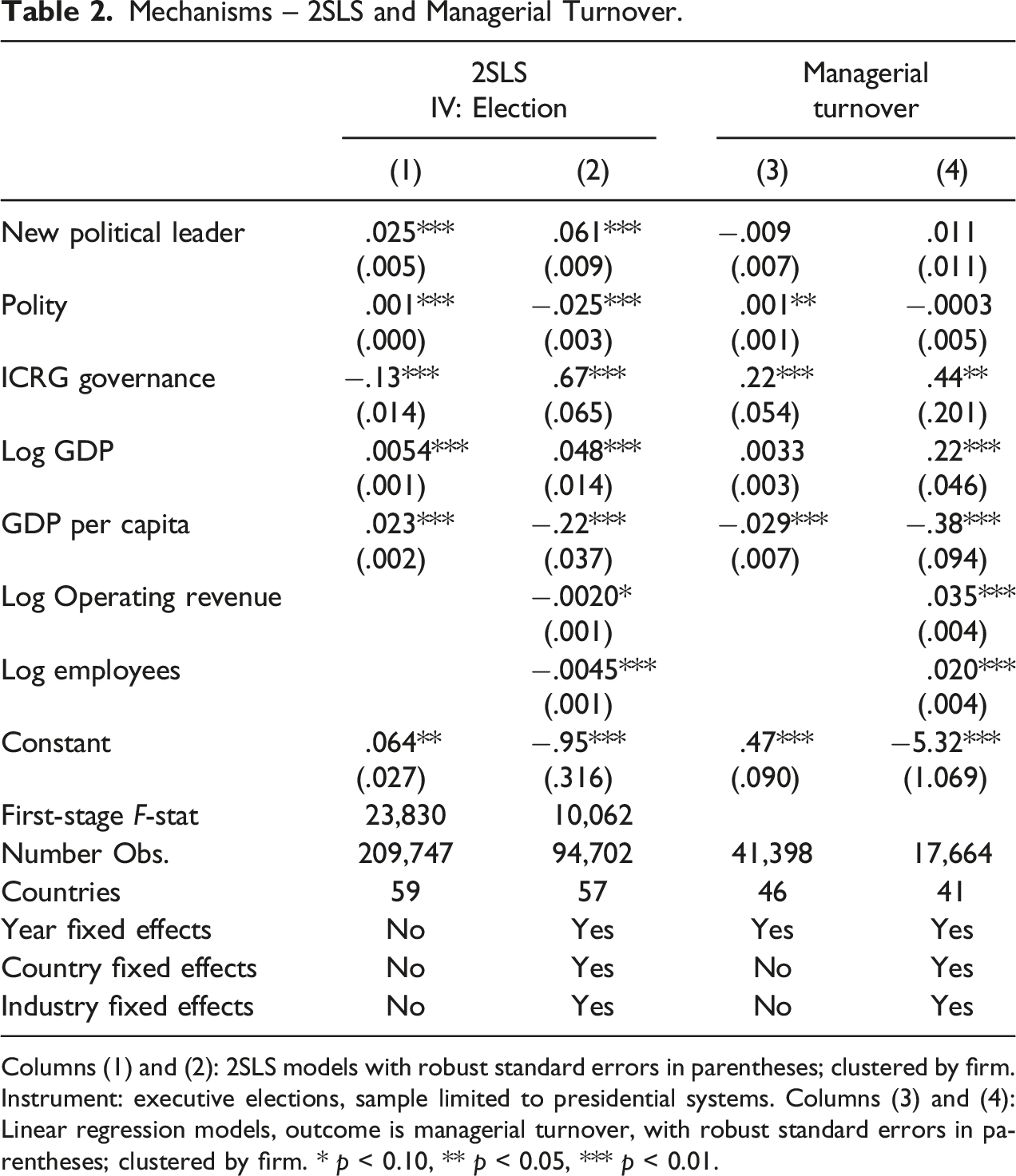

Mechanisms – 2SLS and Managerial Turnover.

Columns (1) and (2): 2SLS models with robust standard errors in parentheses; clustered by firm. Instrument: executive elections, sample limited to presidential systems. Columns (3) and (4): Linear regression models, outcome is managerial turnover, with robust standard errors in parentheses; clustered by firm. * p < 0.10, ** p < 0.05, *** p < 0.01.

Placebo Test

We emphasized the ownership of firms as a key channel through which political connections operate. In columns 3 and 4 of Table 2, we present results when focusing instead on managerial turnover as a placebo test. Both ownership and management turnover might follow, for example, poor economic performance or happen during economic crises, which in turn might be associated with political turnover; in contrast, the asset value mechanism we emphasize is limited to ownership turnover.

We obtain data on changes to management teams from Wharton Research Data Services’ (WRDSs) Capital IQ People Intelligence. We use the ISIN firm number, and are thus limited to firms that issued securities, to match the Orbis and WRDS data. We then code a dummy variable equal to one in any year that a new manager started his or her position or in which a previous manager gave up a position. The variable is zero when there is no change in management. We have data for less than 10% of the observations in our ownership data set. Management changes are much more frequent than ownership changes, and occur in over 60% of cases in our sample.

Using the dummy variable for managerial turnover, we again replicate the base model from column 2 and the full specification from column 5 of Table 1. The results offer no evidence for an impact of political turnover on managerial turnover. The effects are not statistically significant, substantively small, and of opposite sign in the two models.

Interactions: Obfuscation, Rule of Law, Asset Mobility, Firm Size

To further corroborate the mechanism we identified, we now turn to several conditional relationships, focusing on obfuscated ownership structures, rule of law, and asset mobility, as outlined in Hypothesis 2. We also explore an interaction with various measures of firm size to consider heterogeneous effects.

Obfuscation

Some individuals may have obfuscated their ownership through corporate structures and shell companies. Companies with such corporate structures should be less susceptible to political change. To proxy for such cases, we draw on information about each firm’s owner. For each shareholder, both corporations and inviduals, Orbis reports the shareholder name, which we used to code ownership changes. Additionally, for many of the owners in the sample, Orbis reports the last name of the owner. Because firms that attempt to obfuscate their ownership may be less likely to associate a specific individual with the firm, we code a dummy variable,

Political Turnover and Changes to Controlling Ownership – Interactions.

Linear regression models, robust standard errors in parentheses; clustered by firm.

*p < 0.10, **p < 0.05, ***p < 0.01.

Rule of Law

In rule of law-environments, where property rights are strong and courts indepedent, politically driven ownership changes should be less prevalent. To evaluate this proposition, we interact our main variable

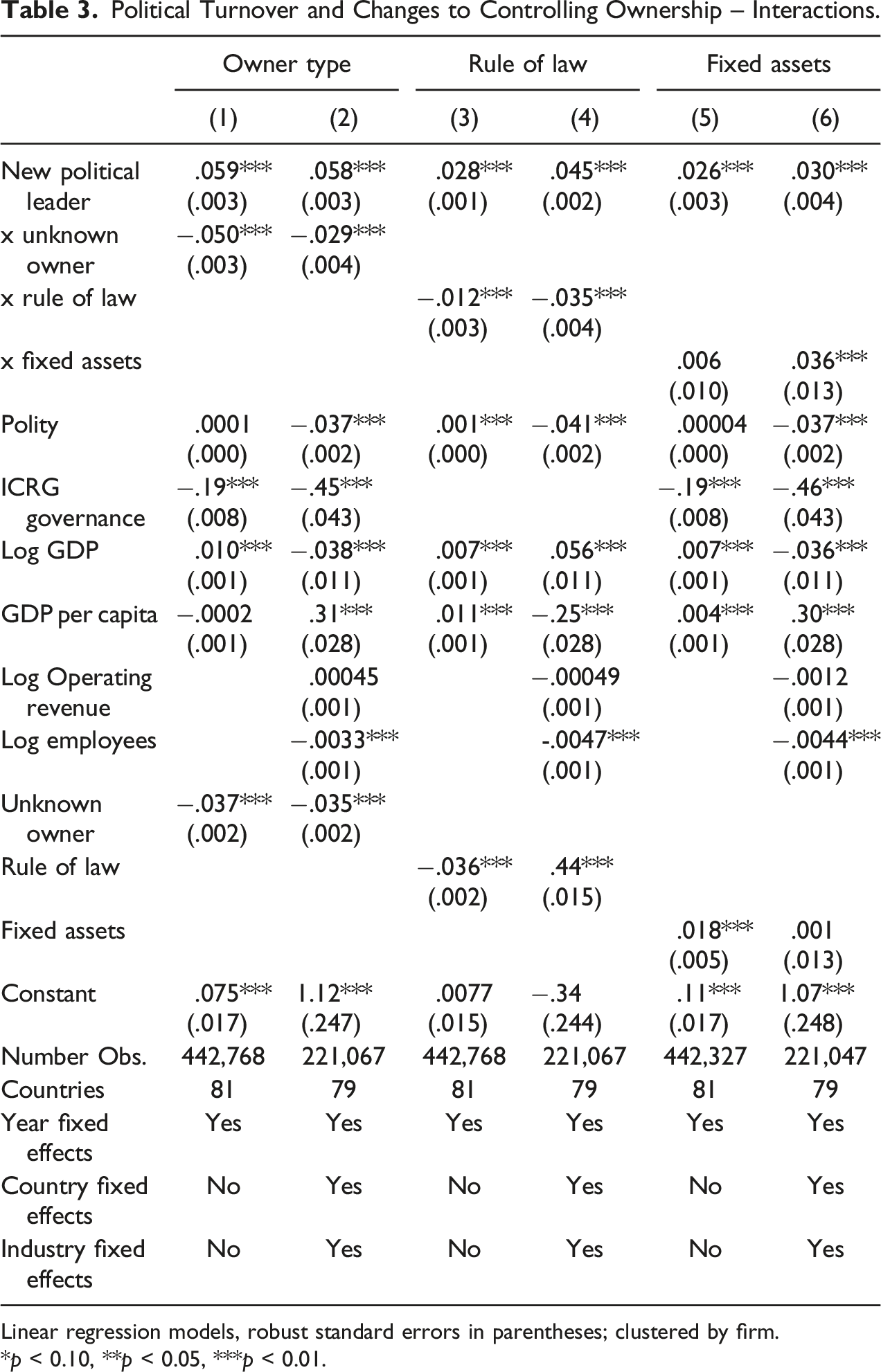

The results, reported in columns 3 and 4 of Table 3, support the proposition that political turnover has the largest effect on ownership turnoever where the rule of law is weak. The interaction between Marginal effect of a new political leader as a function of rule of law (left panel) and of fixed asset share (right panel). Marginal effect and 95% confidence interval, and distribution of rule of law and fixed asset shares in the sample (histogram in the background). Calculated from columns 4 and 6 of Table 3.

OECD Countries

As additional evidence, we present results for OECD members in the Supplemental Appendix. Our main sample excluded OECD members, consistent with most prior work on political connections: strong norms supporting the rule of law and free markets should suppress the role of political connections in OECD members. This suggests that leadership change should not be associated with elevated rates of ownership change. To evaluate this conjecture, we assembled a new data set, focusing on the largest 5000 firms in OECD members. In this sample, we find no evidence that leadership turnover is associated with higher rates of ownership turnover: the effect of leadership changes is negative and substantively negligible, and in many models statistically not significant. We also report results for the combined sample and show that the interaction between an OECD membership dummy and leadership change is negative and statistically significant. Similarly, the interaction between leadership change and the rule of law variable remains negative and statistically significant when estimating it in the combined sample.

Asset Mobility

To measure the sensitivity of firms to government policy, we use fixed assets as a share of total assets. Fixed assets (or plants, property, and equipment, PPE) are more difficult to move out of the government’s reach and more difficult to hide, and therefore more susceptible to political risk (Kerner & Lawrence, 2014). Due to substantial missing data for fixed and total assets at the firm level, we compute a measure at the four-digit NACE level, the most disaggregated level for which we have data on a large number of firms across countries. From the Orbis database, we create a random sample of 250,000 firms for which data on fixed and total assets are available. Using this random sample, we create a measure of fixed asset shares, computed as

Although our empirical analysis uses more disaggregated data, the values for fixed assets by industrial section (two-digit level) correspond well to conventional wisdom: Political risk is frequently considered pronounced in natural resource extraction, which includes ownership of many fixed assets. On average, 53% of the assets in the mining and quarrying section are fixed. The real estate section has 45% fixed assets. Financial and insurance services have one of the lowest values for fixed assets, only 31%.

Columns 5 and 6 in Table 3 report the same specifications as before, but include an interaction between

Firm Size

We also explore another source of heterogeneity across firms: firm size. On the one hand, large firms might be particularly attractive targets for politically connected owners, because they represent large prizes. On the other hand, the large firms tend to draw more public scrutiny. Policy-makers and potential owners alike might therefore be hesitant to target them. Small firms might also be less able to gain protection and influence through other means, such as lobbying, and thus be more reliant on politically connected owners. To explore whether one of these effects prevails on average, we interact the variable on leadership turnover with various measures of firm size: operating revenue, the number of employees, and a firm’s ranking (all relative to the largest firm for each country-year). For all of these measures, we find that the effects decrease with firm size.

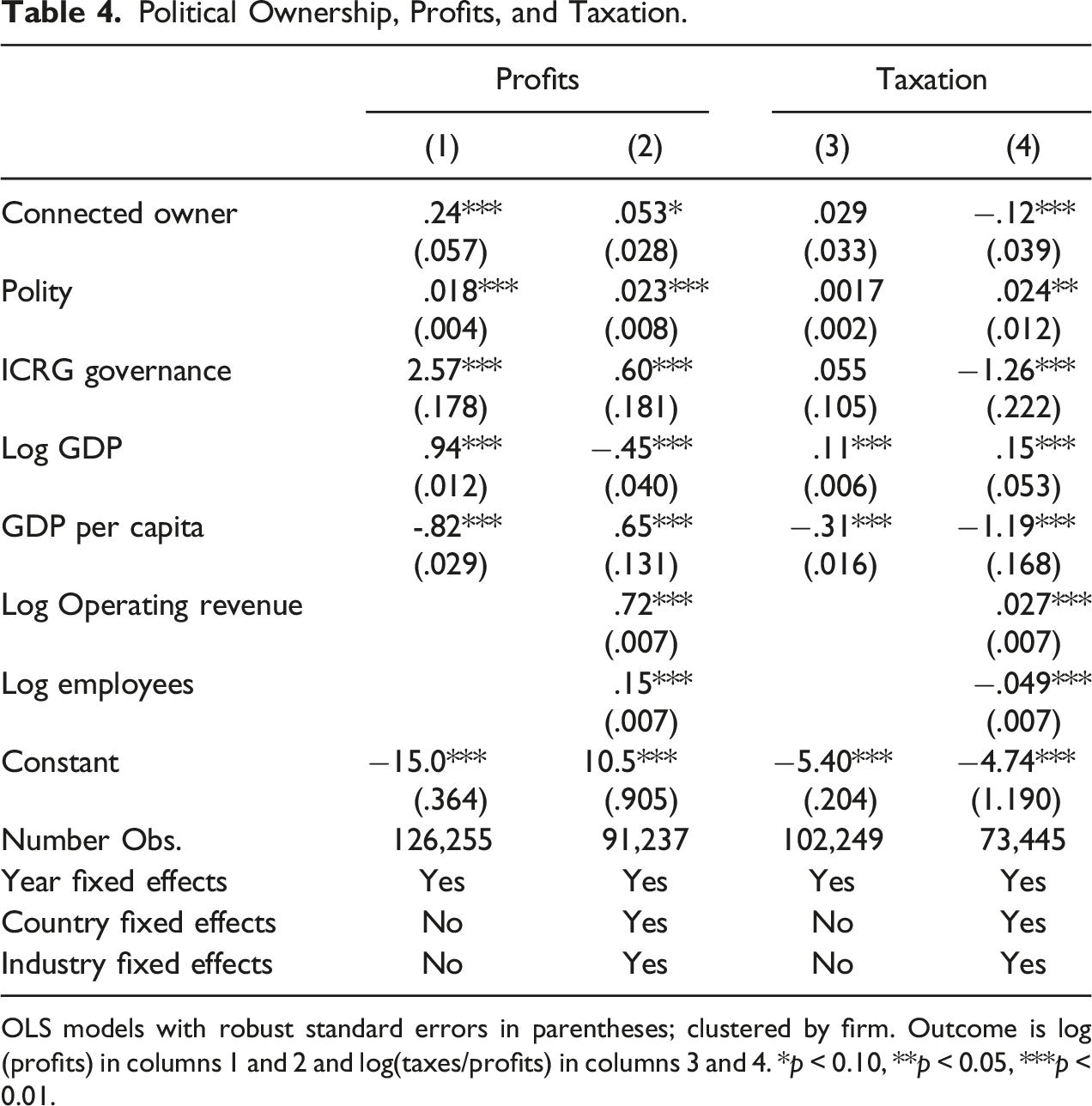

Political Ownership, Profits, and Taxation

Political Ownership, Profits, and Taxation.

OLS models with robust standard errors in parentheses; clustered by firm. Outcome is log(profits) in columns 1 and 2 and log(taxes/profits) in columns 3 and 4. *p < 0.10, **p < 0.05, ***p < 0.01.

We use two dependent variables: log profits earned by each firm and log taxes as a share of profits. The independent variable is a (likely)

The results in Table 4 show that connected owners tend to earn higher profits and to pay lower taxes as a share of profits, although the results are not very robust. Based on the results in column 1, a firm whose owner changed during the same year as the political leadership earns on average 24% higher profits than a firm without ownership change during a year of political leadership turnover. The effect decreases in size considerably, to 5%, in the model with all control variables and fixed effects, and the coefficient estimate fails to reach statistical significance at the 5% level. For taxation, we find a positive, but statistically insignificant effect in the base model in column 3. The results from the full model, in column 4, are again consistent with expectations: connected owners pay about 12% less taxes than other owners, and this effect is statistically significant at the 5% level.

Conclusion

This paper identifies changes in the ownership of firms as a response to political turnover. We emphasize that political connections operate through the ownership of firms, and that therefore the value of a firm’s assets is specific to the firm’s owner. This implies that periods of political turnover should be associated with turnover in the ownership of firms. Assembling a data set that documents the ownership of firms operating in 87 countries, we present evidence consistent with the theoretical propositions. Changes in political leadership are associated with changes in firm ownership, and the effect is larger among firms with less mobile assets and more transparent ownership structures, and in countries with weaker property rights. We also present preliminary evidence that firm owners that take over during political change pay less taxes and earn higher profits.

The study suggests several opportunities for future research. First, the state plays an active role in some economies through nationalizations and direct ownership of firms (Resimic, 2021). Where the state controls many firms, directly and indirectly, we might expect political turnover to have an especially large effect on firms. At the same time, the rationale for, and the consequences of, political connections might differ depending on the economic system. As Tihanyi et al. (2019) also suggested, it would be fruitful to examine more systematically the complementarities of state ownership and political connections, and how those operate differently across institutional contexts.

Second, our analysis was limited on several dimensions. The first issue is the presence of indirect ownership, where the true owners route ownership through corporate layers (which are potentially located abroad). Such an ownership structure might help reduce the political exposure of firms. The second, closely related, issue is the presence of foreign ownership. Foreign owners might have access to other means of securing protection, such as through investment treaties or backing by their home government. At the same time, foreign owners might be particularly susceptible to political conditions in the host country. The third issue is that we assumed political connections to be fixed to specific individuals. Future work could consider extensions where individuals can invest in connections, making connections endogenous to individuals and firms simultaneously. More broadly, future work should consider the interactions between these various strategies that firms take to mitigate political risk – including lobbying, ownership obfuscation, and foreign partnerships – and how they respond to political turnover.

Third, the study is relevant to a broad literature that looks to asset ownership as the source of political preferences and influence. For example, the interests of capital owners and labor are frequently pitted against one another; and among capital owners, the owners of mobile assets are thought to have more political influence. The literature tends to treat asset ownership as static, but ownership is at times quite flexible. Deriving political preferences from asset ownership, as is typically the case in the literature, becomes less straightforward when ownership itself becomes political: political connections allow individuals to become asset owners, reversing the causal chain in some of these theories.

Finally, the divide between economic and political elites is at the forefront in theories of democratization (Ansell & Samuels, 2014; North & Weingast, 1989). That the economic and the political elite often coincide, perhaps endogenously as in our framework, suggests dim prospects for democratization. At the same time, our paper identifies a new source of demands for property rights by the economic elite: current economic elites will demand property rights when facing uncertainty about the longevity of their political connections. Political uncertainty emerges as an important precondition for political and economic elites to demand property rights to protect their assets and perhaps to begin the process of democratic transition. The theory thus provides an explanation for the development of strong property rights institutions in places with frequent political turnover: property rights are necessary to encourage investment in politically competitive contexts where owners would otherwise lose control of their assets following political turnover. This rationale is separate from the constraints present in many democratic countries, and it also suggests a new perspective on why strong property rights coincide with democratic institutions (Olson, 1993). Future work could consider more thoroughly these interactions between expectations over political turnover, institutional reform, and political stability.

Supplemental Material

Supplemental Material - Politically Connected Owners

Supplemental Material for Politically Connected Owners by Timm Betz and Amy Pond in Comparative Political Studies

Footnotes

Acknowledgements

Many thanks to Michael Albertus, Sarah Bauerle Danzman, David Fortunato, Scott Gehlbach, Robert Gulotty, Timothy Hellwig, Seungjin Kim, Hannah Löffler, Erik Peinert, Thomas Sattler, Jerome Schaefer, Jessica Steinberg, Susan Stokes, and Paul Thurner for excellent comments. The paper benefited from many suggestions at the Ostrom Workshop Colloquium Series at Indiana University, the Annual Conference of the American Political Science Association, the GSI Empirical Research Seminar at the Ludwig Maximilian University of Munich, and the Comparative Politics Workshop at the University of Chicago. We thank Jonghoon Lee for excellent research assistance.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.