Abstract

How do prime ministers manage investors’ expectations during financial crises? We take a novel approach to this question by investigating ministerial appointments. When prime ministers appoint technocrats, defined as non-partisan experts, they forgo political benefits and can credibly signal their willingness to pay down their debt obligations. This reduces bond yields, but only at times when the market is sensitive to expected repayments—that is, during crises. To examine the theory, we develop an event study analysis that employs new data on the background of finance ministers in 21 Western and Eastern European democracies. We find that investors reward technocratic appointments by reducing a country’s borrowing costs. Consistent with the theory, technocratic appointments under crises predict lower bond yields. Our findings contribute to the literature on the interplay of financial markets and domestic politics.

Introduction

On June 26, 2012, at the height of Greece’s debt crisis, newly elected Prime Minister Antonis Samaras appointed a technocrat as his finance minister after his predecessor resigned for health reasons. The appointment of Yiannis Stournaras, a 55 year old, non-elected and politically inexperienced professor of economics to the second highest post of the government was greeted with optimism by the international press and investors alike. The press stressed Stournaras’ credentials as an economics professor and the fact that he enjoyed the “respect and trust of lenders” (Alderman & Kitsantonis, 2012). Investors and the stock market in Athens responded with optimism, even if cautious, closing with an increase of 1.5% (Kathimerini, 2012).

Similar anecdotes abound across continents and periods, from the debt crises in Latin America in the 1980s and 1990s (Santiso, 2003; Schneider & Ross, 1998) to the recent financial turbulence in Mexico and the subsequent appointment of the technocrat finance minister Carlos Urzua, “a respected technocrat whose appointment did much to calm investors’ nerves after the election” (Wheatley, 2018b). Nonetheless, despite the widely held assumption that technocrat finance ministers improve governments’ credibility during financial crises (Hallerberg & Wehner, 2018; Kaplan, 2017), there is no large-n, comparative empirical evidence showing that markets notice and even reward governments for appointing non-elected policy experts to the government’s top economic post. Moreover, it is theoretically unclear why and how the appointments of these non-elected experts allay investors’ fears.

Scholars have stressed technocrats’ neoliberal credentials (Kaplan, 2017), which combined with their independence from electoral politics make them “willing to impose greater costs to achieve their ends…hence, they are associated with unpopular programs of orthodox stabilization” (Schneider & Ross, 1998). Once appointed, finance ministers are given significant power to set the policy agenda as they occupy the second most important post 1 and are the ones who decide on the government’s budget (Jochimsen & Thomasius, 2014; Hallerberg, 2004). Thus, it is argued, a non-elected expert with strong neoliberal economic preferences at the helm of a country’s economy sends a strong signal to investors that the government is serious about pro-market reform. Yet, this argument raises an important theoretical question: why would investors trust a minister to implement unpopular policies? For many, it seems naïve to believe that the identity of the finance minister has an impact on investor confidence since the prime minister (PM) or president can remove them from office overnight (Dewan & Hortala-Vallve, 2011). Technocrats, defined as non-elected policy experts (Camerlo & Pérez-Liñán, 2015a; McDonnell & Valbruzzi, 2014), should be particularly vulnerable to dismissals since they lack political clout and experience. Perhaps as a result of this tension, ministerial appointments are not considered critical events for markets in the way elections or policy announcements are (Bernhard & Leblang, 2006; Leblang & Mukherjee, 2005).

We offer a resolution to this tension by addressing the following empirical and theoretical questions: Do the appointments of technocrats credibly signal to investors, domestic and international, a government’s intention to stabilize its economy and meet its debt obligations during periods of financial crises? If so, how? Under what conditions do creditors take ministerial appointments seriously in the absence of formal policy delegation?

If indeed investors’ confidence in government increases as a result of a ministerial appointment, then appointing technocrats is an effective signal about the government’s priority to improve its public finances, thus lowering investors’ risk. If successful, a credible signal can help governments buy time by lowering the cost of borrowing, giving breathing space to implement longer-term structural reforms. International financial crises trigger monetary and fiscal crises domestically (Kahler & Lake, 2013; Reinhart & Rogoff, 2009b) and shake investors’ confidence that governments will honor their debt obligations (Ballard-Rosa, 2016; Gray, 2009; Haggard, 2000; Purfield & Rosenberg, 2010; Santiso, 2003). Regaining credibility is an arduous and long-term endeavor for governments (Bardhan, 2005; Grittersová, 2017) as the economy contracts, public debt rises and jobs are lost (Gray & Hicks, 2014). During such periods, voters’ and markets’ interests are likely to conflict, with the first demanding protection of jobs and benefits and the second demanding full repayment of sovereign debt obligations (Ballard-Rosa, 2016; Reinhart & Rogoff, 2009a).

Creditors fear that although governments announce their intention to “fix” their economies and reduce government expenditures, the short-term domestic political costs of economic adjustment will derail the announced reforms, increasing the risk of future default 2 on sovereign debt. Investors are called to assess the risk of lending to governments whose willingness to honor their debt obligations is not necessarily synonymous with their ability to do so (Gray, 2009; Hardie, 2011; Naqvi, 2019). The expected political costs of policy reform during economic crises increase investors’ uncertainty about future economic policies, and consequently the political risk premium (Pástor & Veronesi, 2013). In particular during financial crises when macroeconomic indicators deteriorate and the financial markets are volatile, investors rely disproportionately on heuristics and short-cuts (Gray, 2009; Naqvi, 2019). The 2008 financial and debt crisis stands as a reminder that this holds true even for developed, industrialized democracies with independent central banks (Bodea & Higashijima, 2017) and membership in the European Union (Barta & Makszin, 2020; Gray, 2013; Gray & Hicks, 2014).

Yet, unlike in other policy areas, for example, monetary policy (Bodea & Hicks, 2015), governments struggle to credibly commit to future fiscal policy (Beaulieu et al., 2012). Fiscal policy is subject to electoral competition and should, at the minimum, reflect the preferences of an electoral majority as it directly determines the distribution and re-distribution of a society’s resources (Alesina & Guido, 2007; Bickerton and Accetti, 2017). Consequently, elections (Sattler, 2013) and policy announcements (Pástor & Veronesi, 2013) are the critical events that update investors’ beliefs about governments’ future policies 3 . However, whether ministerial appointments are critical political events for markets has not been systematically studied.

We contribute to the literature and resolve this puzzle by developing a signaling model that provides the conditions under which appointing technocrats to the finance portfolio is an effective costly signal. During financial crises when the cost of borrowing and, in turn, the risk of sovereign debt default rises, only prime ministers who prioritize honoring their debt obligations are willing to forgo the political benefits of appointing a loyal partisan to the position. Creditors recognize this and reduce yield rates accordingly. Thus, our model examines the conditions under which creditors take ministerial appointments seriously, even in the absence formal policy delegation. In addition, unlike existing work (Kaplan, 2017; Schneider & Ross, 1998) our model need not make any assumptions about the policy preferences of the finance minister to be credible.

More specifically, we develop a model of appointments, budgeting, and bond markets. The market is unsure about the executive’s intention in stabilizing its economy and in turn paying back loans. The interaction begins with the executive choosing whether to appoint a partisan minister for a political benefit or pass on it and turn to a technocrat. We define technocrats as non-partisan, professional economists who never held elective office; partisans, on the other hand, are elected politicians, who might be economists, also known as technopols, 4 or not. The market then adjusts yield rates based on the information it has. Finally, the executive then chooses a budget allocation, with the country’s cost of borrowing (and subsequently debt) endogenously determined by investors.

Under normal circumstances, PMs should prefer to appoint partisans. Typically, finance ministers are experienced politicians with a long history of service to the party. Appointing ministers with political experience earns the PM political benefits, such as party discipline, government stability, effective policy communication with the electorate but also benefits from political patronage (Dumont & Patrick, 2008). These skills can prove particularly useful during major financial crises when the party’s backbench is called to vote on legislation that is not popular with voters and the party base. Indeed, PMs are more likely to appoint technopols over non-expert partisans to the finance portfolio during financial crises as they bring both policy expertise and political experience (Alexiadou & Gunaydin, 2019). Yet, some PMs forgo these political benefits to appoint technocrats during financial (and payments) crises. Following the appointment, the markets can make an inference about the executive’s policy intentions, and bond yields adjust accordingly.

We find that the executive can sometimes credibly communicate her preferences even though types who are less adverse to default have incentive to bluff their intention so as to obtain a lower yield. The logic boils down to a “burning money” mechanism. Less default-averse types place less disutility on higher bond yields than more default-averse types. Thus, by appointing technocrats, executives signal to investors that they must care a great deal about obtaining lower interest rates; otherwise, they would instead gain the benefit from making a political appointment. Meanwhile, types who are less averse to higher borrowing costs opt for the political appointment, as the benefit outweighs the consequences. In turn, bond yields are higher.

This observation generates a testable hypothesis: technocratic appointments ought to allay investor fears in times of crisis, resulting in lower interest rates. We empirically investigate whether markets react in this manner by studying the effects of technocratic appointments on sovereign bond yields. Utilizing novel data on the political and professional background of finance ministers in 21 Western and Eastern European countries from 1991 to 2012, we find strong empirical support of our model’s predictions. Markets are more trusting of governments who appoint technocrats to the finance portfolio during financial crises. Using event study analysis we find that although sovereign bond yields rise during financial crises, appointing a technocrat finance minister leads to a 1% drop in the abnormal returns of bond yields during a 7 day period and a 0.8% average drop over the course of a year. Importantly, we show that it is primarily distance from electoral politics rather than expertise in economics that investors seek in these ministerial appointments.

Motivating Appointments as Signals

Before working through our theory and gathering evidence for the mechanism, it is worth taking a step back to motivate the key elements of our model. Researchers agree that markets react to political events such as elections and policy announcements (Bernhard & Leblang, 2006; Sattler, 2013). With few notable exceptions (Alexiadou, 2015; Dargent, 2015; Kaplan, 2017), however, the dominant position in political science has been that ministerial appointments should not matter for policy outcomes.

What existing approaches fail to consider is the political benefits gained by partisan appointments—and, equivalently—lost by technocatic appointments. The appointment of Greek finance minister Stournaras provides an example. After the formation of the center-right coalition in June 2012, all the governing parties, together with the vast majority of Greek voters, wanted to renegotiate the conditions of the bailout agreement that had been signed by the previous government (AFP, 2012). One would expect that the PM’s challenge was to signal to investors his government’s intention to pay back the country’s debt, despite political pressure from the electorate and the party. By appointing Stournaras, a technocrat, as his finance minister, he effectively forwent the benefit of appointing a partisan who would be in tune with voters. Instead, he risked disagreements within the party and the cabinet (Times, Financial, 2012a). Stournaras’s appointment was not welcomed by many senior cabinet ministers and resulted in the resignation of the junior minister of employment (Hope, 2012). At the same time, and especially after Stournaras’s first meeting with the Eurogroup, it became clear that Samaras prioritized debt repayment over easing the social pain of fiscal austerity (Times, Financial, 2012a).

Resignations to the appointment of technocrats can also occur outside the cabinet, in politically sensitive positions. For example, when Turkish PM Bülent Ecevit appointed the technocrat finance minister Kemal Derviş during the 2001 financial crisis, he prioritized his government’s access to credit over his political friends. Within 24 hours of Derviş’ appointment, the chief Turkish banking regulator, a close lieutenant of the PM, resigned in protest at “being placed under Derviş’ authority” (Boulton, 2001d).

The potential loss of political benefits for the PM and her government extents to the loss of political patronage. Technocratic appointments can have direct costs to the PM and her government as they constitute a direct loss in patronage opportunities. For example, finance minister Derviş replaced all the political appointees who run Turk Telekom. This leads to an open conflict with communications minister Enis Oksuz and his party, the National Action Party (MHP), who up to then had controlled the “fixed-line monopoly” (Boulton, 2001a). The conflict earned publicity with the communications minister warning that “73,000 employees could lose their jobs” (Boulton, 2001a).

One might even argue that investors expect that appointing a technocrat finance minister is accompanied with more technocratic appointments in politically sensitive positions. Paulo Guedes, the technocrat finance minister appointed by the Brazilian president Jair Bolsonaro in 2019, “made market-friendly appointments, including fellow University of Chicago alumni Roberto Castello Branco as head of state-owned oil company Petrobras and Joaquim Levy, a former finance minister, as head of Brazil’s influential development bank BNDES” (Leahy and Schipani, 2018).

These anecdotes raise a theoretical and an empirical question. On the theoretical side, is our explanation coherent? A novel aspect of the argument here is that the appointment of finance ministers can alter market behavior separate from any anticipation of actual decisions by those ministers. Thus, if we wish to verify the signaling effects of the appointment decision, we ought to adopt an “experimental” approach (Paine & Tyson, 2019). This means removing extraneous features—the finance minister’s active decisions—from the model. We are not suggesting that day-to-day decisions of a finance minister are irrelevant. Rather, in contrast to Schneider and Ross (1998), we show that the appointment itself has an independent effect that is separate from the ministers’ market-conforming policy preference. The independent effect helps explain some features of market behavior that agenda setting theories cannot account for. That is, finance ministers have difficulty committing to higher payments than prime ministers would want—finance ministers face removal if they deviate from the prime minister’s policy preference (Dewan & Hortala-Vallve, 2011).

On the empirical side, are the examples of Stournaras or Derviş unique? Related research on the subject has yet to address this question in a large-n comparative study. We are the first to empirically generalize the hypothesis that executives appoint technocrats to gain the confidence of the markets (Haggard, 2000; Schneider & Ross, 1998). We provide systematic evidence that market pressures can induce democratically elected executives in Europe, not only in Latin America, to delegate economic policy to non-elected experts when the markets lose confidence in them. As such we show in a systematic way that not only emerging markets (Grittersová, 2017; Santiso, 2003) but even richer, developed economies are subject to the disciplining role of markets (Gray, 2013).

More broadly we provide crucial theoretical insights and empirical evidence in support of the effectiveness of ministerial appointments as signaling strategies to economic actors (Drazen, 2004), contributing to the important literature on policy delegation (Bodea & Hicks, 2015; Grittersová, 2017). Importantly, we provide theoretical and empirical evidence that it is not necessarily expertise, but independence from electoral politics that matters to investors, making an important contribution to literature on the appointments of experts (Hallerberg & Wehner, 2018) but also to the debate on the role of technocracy in democracies (Bertsou & Caramani, 2020). By rewarding the appointments of technocrats but not of technopols, markets indicate that technocratic appointments are not qualified for their technical superiority but for removing the policy process from the electoral arena.

Theoretical Model

Play proceeds as follows. Nature begins the game by drawing the Prime Minister as a “high” type with probability q. This type is more concerned with paying down sovereign debt. With probability 1 − q, Nature draws a “low” type that is less concerned. The draw is private information and maps to the plausible preferences given the observable features (e.g., party identification) of a Prime Minister. Afterward, she appoints a partisan or a technocrat. The market sees this and selects an interest rate r > 0. Finally, the Prime Minister allocates x ≥ 0 to reducing the amount of debt D and β − x to social spending, where β represents the Prime Minister’s budget constraint. Note that x cannot be greater than the minimum of β (because she cannot spend more than she has) and D (because she cannot pay down more debt than there is).

We model a strategic and competitive bond market. Thus, rather than focusing on specific investors’ utility functions, we instead formalize the interest rate. In particular, let r (E [x], t) map the expected debt payment x ∈ [0, d] and stability of the market t ≥ 0 to an interest rate, where d is the principal and higher values of t indicate greater financial instability. In turn, debt becomes D = d + r (E [x], t).

We make two key assumptions about the function r. First, for all t, it decreases in E(x). That is, regardless of the market turmoil, larger expected payments result in lower rates. Second, we assume that it has a strictly negative cross-partial derivative. This captures market sensitivity—when investors expect fuller repayments, turmoil matters less in determining interest rates. In addition, for notational simplicity, let r (d, t) = 0. 5

The Prime Minister’s payoff has three components: political appointment benefits, social spending, and debt obligations. Formally, her utility function is

Perfect Bayesian equilibrium is the appropriate solution concept. Before turning to the propositions, backward induction reveals a key insight. The Prime Minister faces a straightforward optimization problem regardless of her type. Because the market has already set the bond rate, she chooses the repayment amount that maximizes her tradeoff between social spending and debt obligations. The appendix shows that the optimal x for a generic type α equals

However, these anticipated debt payments have upstream consequences. Recall that the interest rate decreases in that debt payment. Because the high type pays more, the market wants to give that type a lower interest rate than the low type. But the market does not observe the Prime Minister’s type. Consequently, the low type has incentive to mimic the high type’s behavior to obtain the lower interest rate. This drives the tension of the signaling game.

Nevertheless, under certain conditions, the appointment choice can credibly separate the types. Because the high type finds higher interest rates relatively more painful than the low type, the high type is more willing to forgo the political benefit p in exchange for a lower interest rate. The tradeoff between the value of political benefit to the PM and a lower interest rate makes separation possible. However, the existence of a separating equilibrium still depends on p. If p is too large, then the high type prefers taking the big political benefit even if it means paying the higher interest rate. Yet if p is too small, then the low type becomes unwilling to suffer the higher interest rate in exchange for the now tiny political benefit.

Let

The condition in Proposition 1 generates the substantive intuition. The value

An interesting implication is that partisanship here is less important for signaling than the difference in potential types, holding fixed that partisanship. For example, imagine that a left-wing PM must make an appointment. If the market knows that the PM either plans to service none of the debt or a tiny amount, both types would make the political appointment, and the market would not update its information. In contrast, if the market knows that the PM either plans to service none of the debt or moderate amount, then the moderate type has incentive to forgo the political benefit to obtain a better rate. The market updates its information accordingly.

In sum appointed technocrats therefore serve as credible signals. The following comparative static reiterates this point:

The first half of Proposition 2 is a straightforward implication of the separating equilibrium’s logic. Only high types appoint technocrats. High types are committed to allocating a larger share of the budget to paying down debt. The markets respond with greater demand, thereby lowering interest rates. Meanwhile, only low types appoint partisans. Low types are not as committed to debt payments, leading to higher interest rates. The second half of the proposition is a consequence of the markets being more sensitive during times of turmoil. We show this in the appendix by demonstrating that the difference between

Combined, Propositions 1 and 2 validate the signaling logic of technocratic appointments. Forgoing a political benefit of appointing a partisan provides information to investors; only prime ministers averse to leaving debts unpaid are willing to sacrifice it. Demand correspondingly increases for sovereign bonds, which lowers the yield. 8

Empirical Analysis

With the core theoretical mechanism described, we now turn to its empirical implications and the associated evidence. We begin by deriving a testable hypothesis. Afterward, we describe our research design and show the results.

Hypothesis

Our substantive interest is how market turmoil and appointment decisions determine interest rates. Proposition 1 tells us that prime ministers who value repayment can credibly separate themselves who do not. Furthermore, Proposition 2 tells us that the difference in rates the market assigns to different signals may be negligible when a state’s economy is stable. However, a gap may surface when investors are more sensitive to the information available.

In turn, operationalizing market sensitivity gives us an opportunity to investigate whether the type of appointment matters. Financial crises are a promising candidate. Under regular economic conditions, governments have little incentive to default. Thus, bond prices between committed and uncommitted types would be relatively alike. In contrast, financial crises create economic sensitivity. What the market expects a prime minister to do has a greater impact on how it will adjust the rate. As such, bond prices between committed and uncommitted types would see a greater disparity.

Of course, our model does not capture the logic behind all ministerial appointments. Politicians may choose technocrats for reasons orthogonal to our mechanism. For example, technocrats are sometimes appointed during good economic times to push forward domestic policy reforms opposed by interest groups and trade unions (Alexiadou, 2018) but such appointments are of little importance or concern to international investors. Consequently, we do not claim that technocratic appointments universally reduce bond yields. Rather, our model indicates that the effect should be prominent during financial crises. This leads to our central hypothesis:

We test this hypothesis below.

Empirical Strategy

Our central empirical question is whether investors react to the appointments of technocrat ministers vis-a-vis partisans when there is economic uncertainty 9 , namely, during financial crises. Accordingly, the unit of analysis is the appointment of finance ministers. The structure of the data are appointments by government, by country/year. This data structure is preferable over yearly data which would not allow us to code multiple appointments within a calendar year or to identify the effects of the appointments on the day of the appointment. It is also preferable over daily data since appointments take place once every a few years or months, whereas market prices change daily.

To identify if and how investors respond to the appointments of technocrats, we use daily data on sovereign bond yields and event study analysis. Bond yields are the most direct measure of governments’ borrowing costs as they reflect the return at which investors are willing to hold government debt (Breen & McMenamin, 2013). We use event study models because we seek to investigate how an announcement moves these yields (Kothari & Warner, 2007). The challenge is to isolate the effect of the intervention (in our case appointment) from other events that affect the yield. Event study compares the realized behavior of yields to the expected behavior if the intervention had not happened (MacKinlay, 1997). In our case, we compare the actual bond yield after the appointment of finance ministers, to the expected bond yield if the appointment had not happened. Under the null hypothesis, there is no difference between the actual and the expected yield. The difference between the two is called the abnormal yield, and averaged over a specified window of days (7, 30, or longer), we obtain the average abnormal yield (AAY), which is our main dependent variable. 10 The abnormal yields after a ministerial appointment are averaged over the days of the event window. 11

Given our data and research hypothesis, event study models have many advantages over regression models as they do not suffer from the problem of serial correlation and can isolate the effect of a single event within the event window. By calculating the normal yields in the estimation window, we already incorporate all the information that investors have, and therefore we “control”’ for exogenous factors driving the level of rates. This is particularly useful in panel data with heterogeneous units. Moreover, by estimating the effect of the event in a short-horizon window, we can isolate the effect of the intervention from all other factors that are unlikely to change in the narrow event window (of 7 days, for example). It is easier to isolate the effect of the appointment on bond yields when using the event study analysis than by using simple regression analysis, assuming no new information is provided to investors other than the ministerial appointment.

One potential downside of event studies is that information about the intervention (appointment) is released before the event window, therefore under-estimating the effect of the intervention. This is quite likely in our case when appointments follow elections and prior to the formation of the new government. Since it is difficult to code the actual first rumor for each ministerial appointment, we rely on the formal start of a new cabinet; therefore, it is likely that our estimates are downward biased. For this reason, we also provide estimates for the appointments that follow cabinet reshuffles only. During cabinet reshuffles, it is typical for the PM to announce the new ministerial appointments on the day of the reshuffle, thus minimizing the problem of leakage into the estimation window.

We estimate the models with ordinary least squares regression that include country fixed effects. We include fixed effects for both theoretical and technical reasons. Firstly, we are primarily interested in explaining abnormal changes in the bond yield as a result of ministerial appointments within a country since we want to model transitions from partisan ministers to technocrats. Second, empirically, the fixed effects estimator is suitable for our data, where the regressors correlate with the units (i.e., technocrats with certain countries) when there is a large number of period units and auto-correlation is weak (Clark & Linzer, 2015; Plümper & Troeger, 2019). In addition, the within variation of most of the regressors is similar or larger than the cross-unit variation, thus making the fixed effects estimator appropriate. Finally, we chose to avoid robust standard errors as they are more biased compared to the classical standard errors when omitted variables cause unit heteroskedasticity (King & Roberts, 2015). Nonetheless, in the Online Appendix we provide estimates using country effects with robust standard errors but also estimates with random effects.

Data

Our main dependent variable is the average abnormal rates of sovereign bond yields. Bond yields are perhaps the most direct measure of investors’ confidence in a government 12 , as it reflects the rate investors are willing to pay to borrow government debt (Gray, 2013). We retrieved daily bond yields for one, two, five, and 10 years from the Bloomberg Terminal. 13

We utilize a unique, time-series and cross-country dataset on the professional and political background of finance ministers in 21 European democracies. 14 This is an original dataset that we compiled from multiple official and personal website sources. The dataset includes 283 appointments of finance ministers from 1991 to 2012. 15 We code the appointments of finance ministers at the start of a government’s life but also during ministerial reshuffles. For the Western European countries, sovereign bond yields are available since the early 1990s while for the Central European countries since the early 2000s with the exception of Hungary, starting in 1998 and the Czech Republic starting in 1997. 16

Our central explanatory variable is technocrat finance ministers. This is a binary variable that codes as 1 those ministers who (a) have never held elective office, either at the national, subnational, or local levels and (b) work as economists or have a PhD in economics. Technocrats should be seen as the “ultimate case” of those who exhibit both distance from electoral politics and the highest level of technical expertise. We seek to illustrate theoretically and empirically a crucial difference between un-elected economists (technocrats) and elected economists (technopols). Our definition differs from recent work that studies the appointments of economic experts (Hallerberg & Wehner, 2018; Kaplan, 2017). Our definition builds directly on work that differentiates experts between those who participate in electoral politics and are constrained by the electoral process and those who are political outsiders (Alexiadou, 2018; Bertsou & Caramani, 2020; Joignant, 2011).

We also created the indicator variable technopol finance ministers. These are ministers who currently hold or have held elective office and have a PhD in economics or have worked as economists prior to entering politics. The remaining category are partisan finance ministers, who are elected and are not economists; they are neither technocrats nor technopols. 17 On average, about 15% of finance ministers are technocrats, 27% are technopols, and 44% are partisans. Although our theoretical model treats all partisans—whether expert or not—as equal, it is important to empirically identify whether investors react to the level of expertise (to the appointments of technopols) or to independence from the electoral process (technocrats).

We expect markets to be more sensitive to the appointments of technocrats in the presence of a major financial crisis, i.e., when the distance between

If markets reward the appointments of technocrats then we should observe a drop in the average abnormal yield after such appointments. Moreover, if distance from electoral politics and not expertise is what moves the markets, then we should only see substantial and statistically significant lower yields after the appointments of technocrats and not after the appointments of technopols. All three indicators are binary, and we include all of the three constitutive terms of the interaction: financial crisis, technocrats and appointments*crisis. We expect the interactive term to be negative and the additive effect of the interaction terms, technocrats plus appointments*crisis to be negative and statistically significant (Brambor et al., 2005).

We include the following political controls that could be driving market reaction: left government, defined as the percentage of left seats in the cabinet (Armingeon et al., 2019), election if the appointment was the result of elections, and government change, defined as 1 when there is a new prime minister. The partisanship of the government is found to be an important driver of negative market reaction especially in emerging market economies (Campello, 2015). Partisan changes can have a large economic effect when economic and political uncertainty are high (Bernhard & Leblang, 2006; Sattler, 2013). The economic controls include: capital account openness, general government deficit as a percentage of GDP, change in inflation, and the log of international exchange reserves. 19 Our choice of economic controls echoes Manmohan and Baldacci (2010), Mosley (2003), and Breen and McMenamin (2013). In addition, we include whether the country is a member of the Eurozone or not (EMU) to control whether investors have a higher trust in the country due to its membership (Gray, 2013). Finally we include an indicator for whether the country is under an IMF program based on the IMF MONA database (IMF, 2020b). According to Nelson (2014), applicant countries are more likely to get more generous conditions by the IMF when their negotiating team includes like-minded economists. By extension, one might expect that appointing technocrats sends a strong signal to the IMF about the country’s credibility to receive a loan. 20

Descriptive Analysis of Abnormal Yields

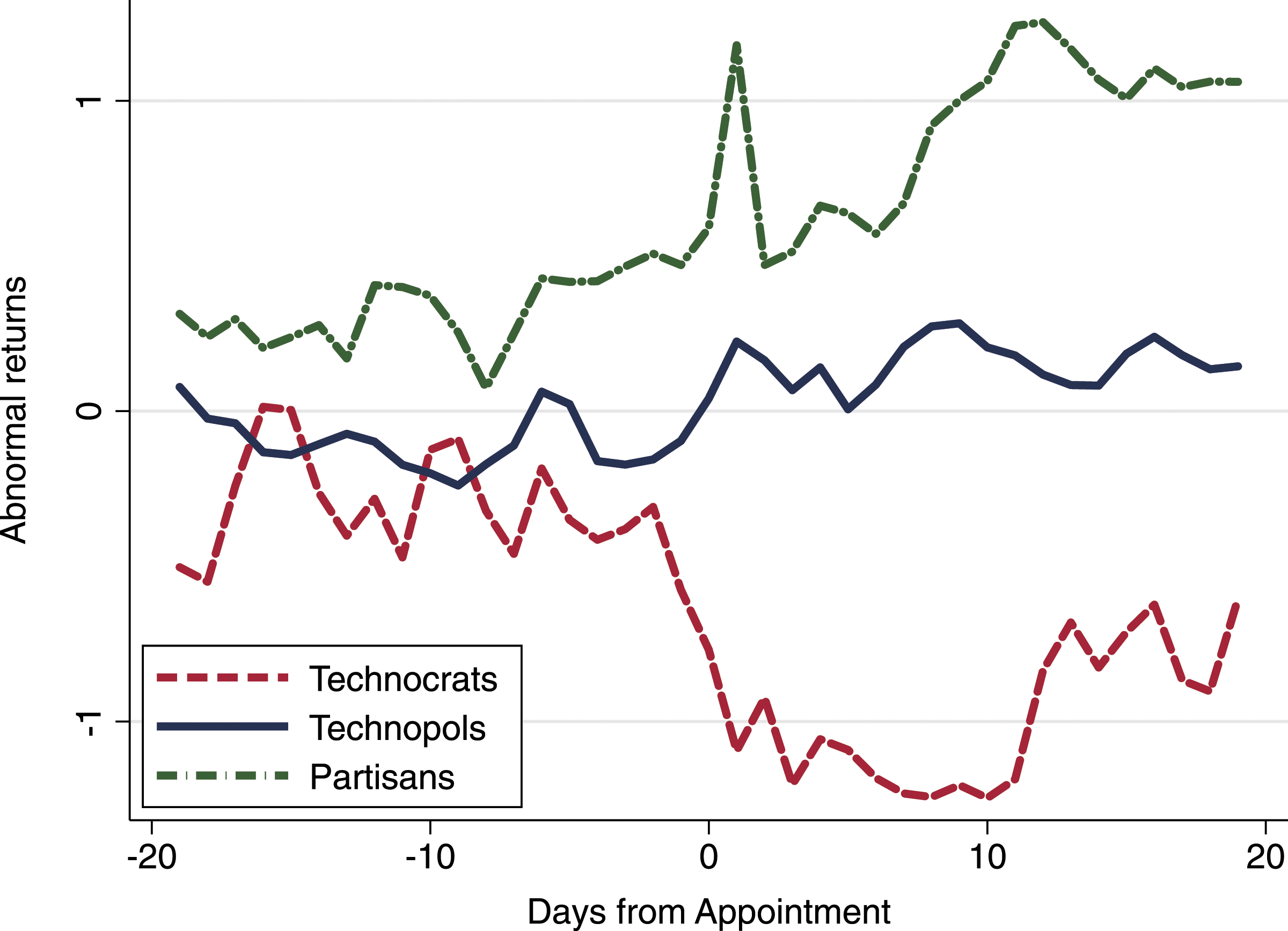

Before turning to the results of the event study analysis, we plot the abnormal bond yields over an event window of 20 days (−20, 20). This provides a descriptive visualization of market behavior before and after a ministerial appointment during financial crises. Figure 1 presents the average abnormal response to the appointments of technocrats, technopols, and partisan finance ministers. It reveals that the average abnormal response to the appointments of technocrats during financial crises is positive, meaning that the yields go down. Following the appointment of a technocrat (the appointment day or day-zero in Figure 1), the bond yield is on average 1 point lower for the next 20 days, and almost one and a half point lower compared to appointing a partisan. In fact, it appears that markets punish the appointments of partisans. Yields go up 1 point in the first day following the appointment of a partisan finance minister and have an upward trend for the 20 day period. In addition, according to Figure 1, financial actors do not anticipate the appointments of technocrats. However, as new information is revealed, investors adjust their response and reward governments that appoint technocrat finance ministers. Descriptive abnormal returns during financial crises.

Empirical Analysis of Average Abnormal Yields

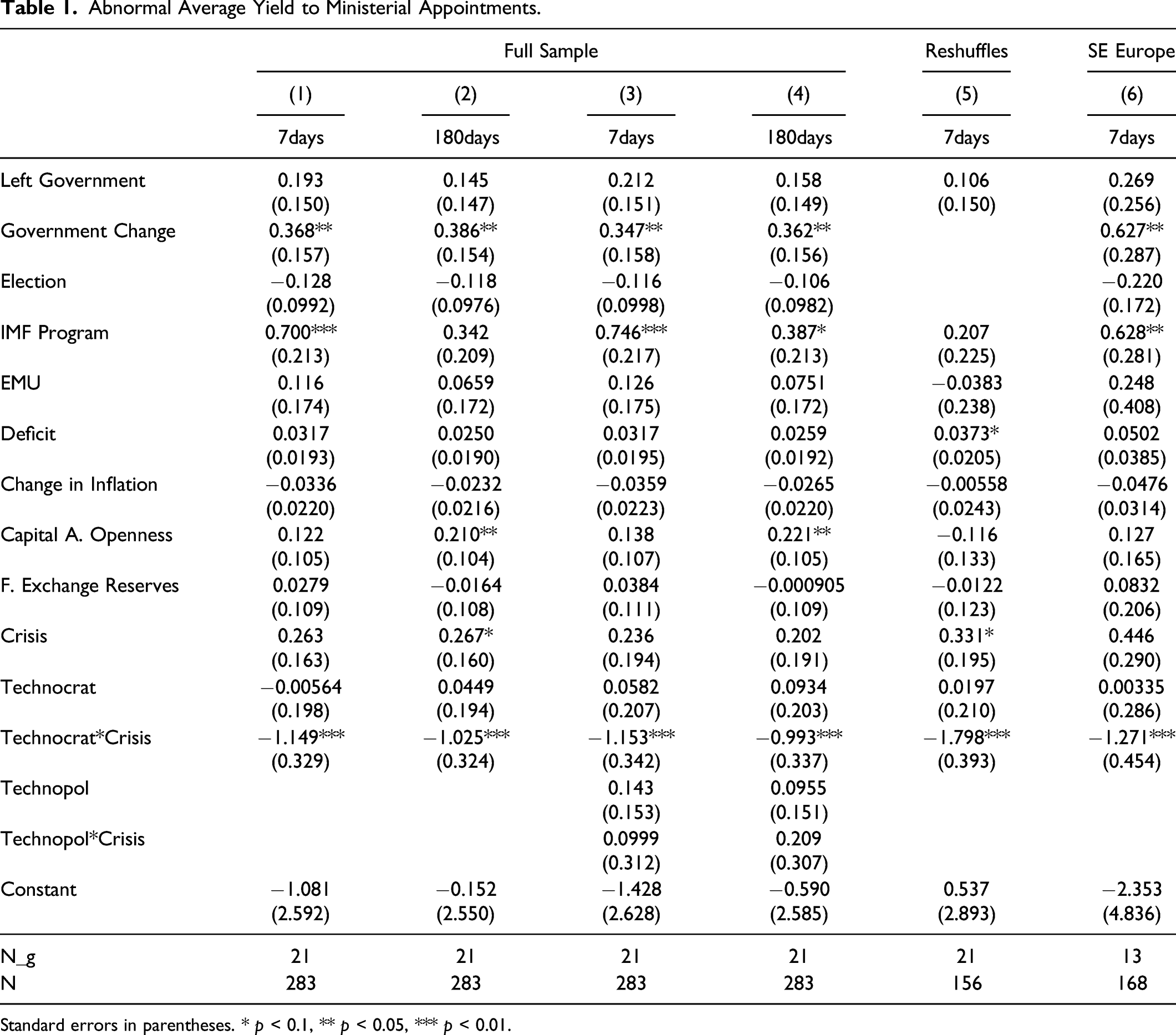

Abnormal Average Yield to Ministerial Appointments.

Standard errors in parentheses. * p < 0.1, ** p < 0.05, *** p < 0.01.

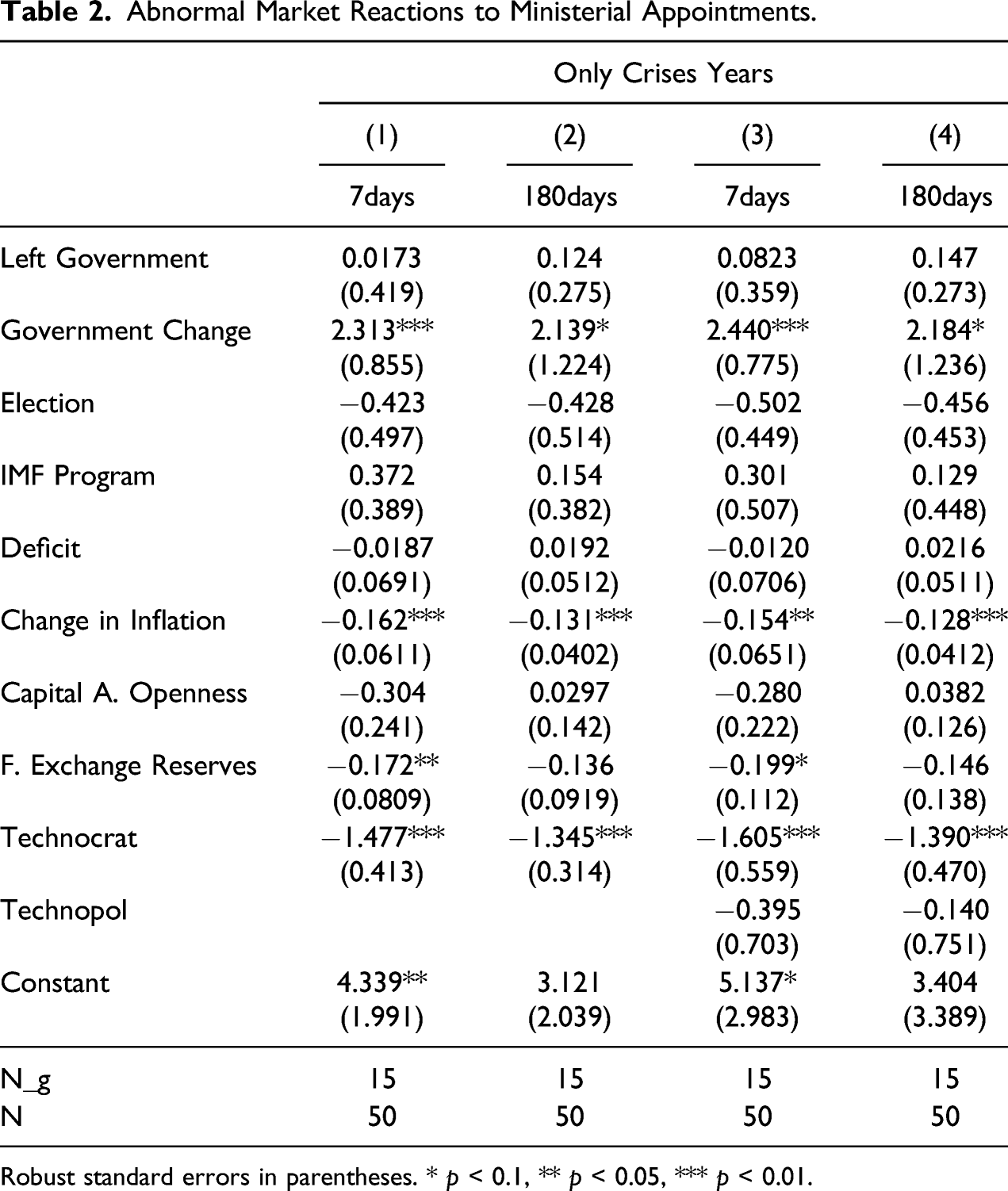

Abnormal Market Reactions to Ministerial Appointments.

Robust standard errors in parentheses. * p < 0.1, ** p < 0.05, *** p < 0.01.

The results bear out our expectations. The appointments of technocrat finance ministers significantly reduce the abnormal rates during periods of economic crisis. In Models 1 and 2, we test the market reaction to the appointments of technocrats in relation to partisans, both expert and not. Appointing a technocrat to the portfolio of finance decreases the average abnormal yield by 1% over a window of 7 days and by just under 1% over a window of 6 months. This means that investors react positively to the appointment of technocrats compared to the expected average, by offering to buy sovereign debt for a lower interest rate. 21 Importantly, the positive impact the technocratic appointment has on abnormal yields has lasting effects at least to 6 months. 22

These results are replicated in Models 3 and 4, where we include technopols in the regression. Yields drop by 1% within the 7 day period after the appointment and just over 0.9% over the period of 6 months. Importantly, markets do not react to the appointments of technopols in the same way they react to the appointments of technocrats. In fact, we fail to find any substantive or statistical effects on the average yield following the appointments of technopols. In Table 2, we can see more directly the impact of ministerial appointments on the yield during financial crises. This indicates that investors do not reward policy expertise per se but rather technocrats’ independence from electoral politics. 23

Technocratic appointments have an even larger effect on the abnormal yield when they take place outside elections. Model 5 reports the impact of technocratic appointments on the average abnormal yield during a 3 day window following a ministerial change outside elections. The substantive effect increases by 50%, to 1.8% from 1% in Model 1. This result supports our expectation that the abnormal yield is lower when investors are more “surprised” by the appointment. Finally, as a further robustness check, Model 6 replicates Model 1 in a sample that excludes the rich, Northern European countries. According to Model 6, the effects found in Models 1–4 are not artificially inflated by including these countries in the analysis.

Two of the control variables have the largest and most consistent impact across models in Table 1: Government Change and whether the country is under the IMF program. The yield is higher by 0.4% when there is a change in government and by 0.5% when the country is under an IMF program. Therefore, it is not changes in the executive or the presence of the IMF that allay investors’ worries; if anything the opposite is the case. Moreover, elections have a negative association but they are not statistically significant. These findings indicate that technocratic appointments have a significant effect on markets, independently of other important simultaneous events that affect investors’ expectations. Surprisingly neither membership in the Eurozone nor government partisanship are statistically significant. Given that other studies found significant effects for partisanship and EMU membership on sovereign bond yields, a likely explanation for the null finding is that these effects are already priced in the yield in the estimation window.

Table 1 is replicated using alternative estimation techniques (robust standard errors and random effects) in the Online Appendix. They are further replicated when using the Laeven and Valencia indicator for financial crises. We further investigate the sensitivity of our results to potential outlier countries. Supplementary Table 7 in the Online Appendix shows that no single country drives our empirical findings. In addition, we replicate the main models using a simple OLS model where the dependent variable is the change in the 9-day moving average of bond yields.

Table 2 provides further evidence that technocratic appointments matter for investors during major financial crises. Here, we regress the abnormal average yield on technocrats and technopols only during the years of financial crises. The drop in the yield is substantively and statistically significant for technocrats but not for technopols: appointing a technocrat in crises years leads to one and half percentage change in the yield in the 3 day window, and to 1.3% change in the 90 day window. The coefficients of the control variables are in line with findings in the literature. Changes in government lead to higher yields, while having more international reserves to lower yields.

To sum up, the empirical analysis corroborates our hypothesis. Technocrats lack political experience, and appointing them causes prime ministers to forgo the political benefits associated with selecting an internal candidate. The signal of commitment increases investor trust during financial crises. Moreover, it appears that investors are responding to something beyond a technocrat’s skill. Technopols, who share the same expertise, see less improvement to bond yields than technocrats. Finally, these improvements are unlikely to be due to the technocrats’ preference profiles compared to technopols. Technocrats and technopols, alike, share similar professional backgrounds, almost exclusively from academia with only a small number coming from the finance sector, as summarized in Supplementary Table 10 in the Online Appendix.

Technocrats in Office

The argument that appointing a technocrat to the finance portfolio sends a signal of policy commitment to investors is not uncontroversial. The dominant view is that policy delegation is credible when it is institutionalized—i.e., when the policy is delegated to politically independent agencies (Alesina & Guido, 2007). Finance ministers are in no way independent of the prime minister who appoints them and technically, they can be removed from office at any point they diverge from the prime minister’s policy preferences (Dewan & Hortala-Vallve, 2011). However, this debate is reminiscent of another debate in the literature on the policy effects of formal delegation vis-à-vis reputation. In a situation where policymakers and markets interact repeatedly, it is not in the interest of the policymaker to renege on her policy promises (see Drazen (2004)). Similarly, although prime ministers can replace technocrats when the latter diverge from her policy preferences, the cost of this removal could prove too high as it would damage her reputation as a debt-averse prime minister.

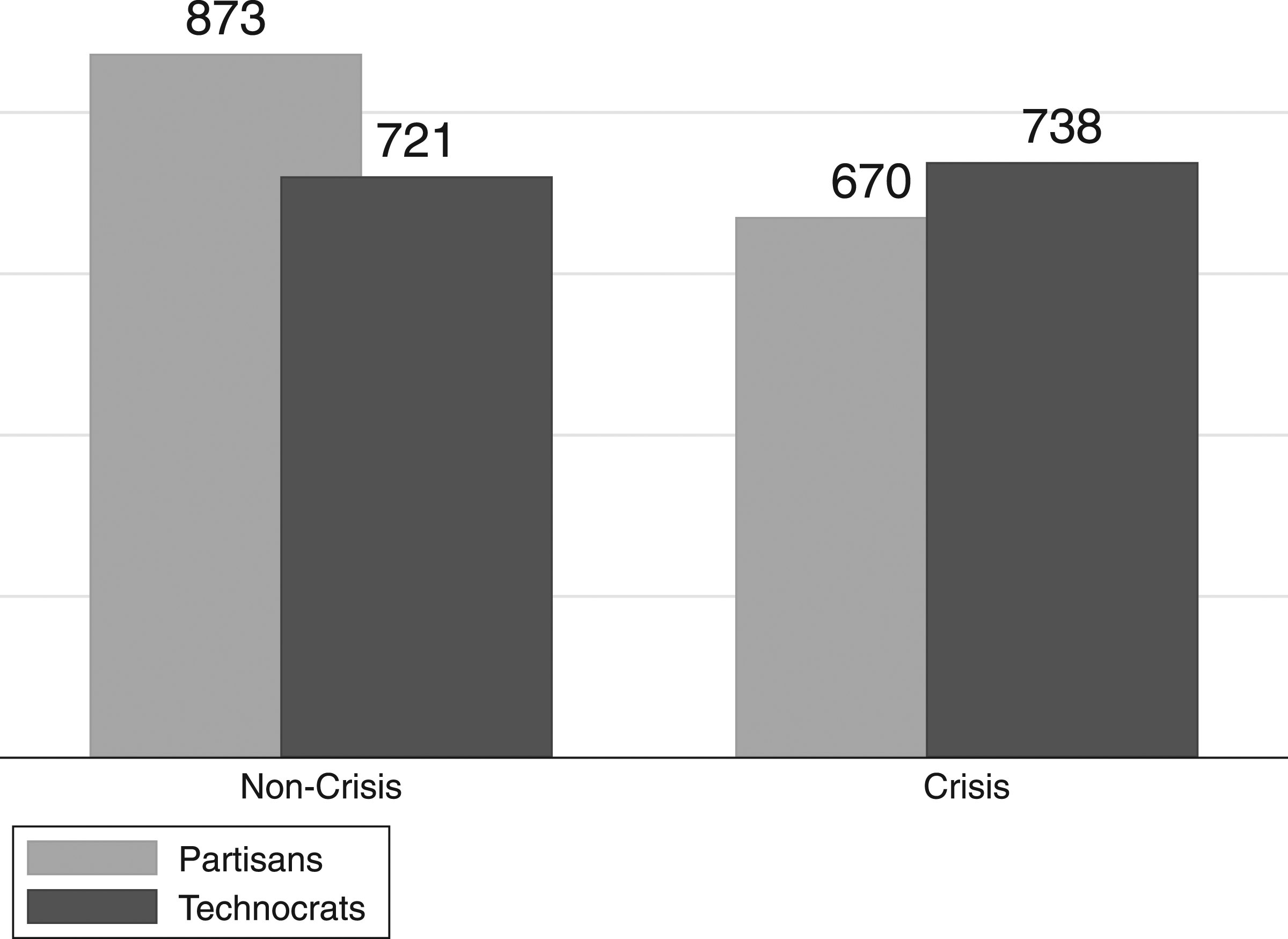

Figure 2 indicates that prime ministers are not likely to remove technocrats from office faster than partisans, even at times of crises. During regular times, technocrats have an average of 721 days in office as opposed to 873 days for partisans, an 8% difference. This is in line with literature on technocratic appointments (Camerlo & Pérez-Liñán, 2015b). During financial crises, the technocrats in our sample have a longer tenure than they did during non-crises years. Importantly, their tenures were almost 10% longer than the tenures of partisans. Technocrats stayed in office for 738 days, whereas partisans stayed in office for 670 days. These statistics indicate that prime ministers take the appointments of finance ministers seriously during economic crises and, importantly for us, once appointed, technocrats are as likely or even more likely to stay in office as partisans. Tenure of finance ministers in days.

To sum up, during financial crises prime ministers have the power to send a strong signal to investors that they will be honoring their debt obligations as long as they are willing to appoint a technocrat to the finance portfolio. Our empirical findings indicate that investors see these appointments as credible signals; technocratic appointments induce a large and statistically significant drop in the yield of sovereign bonds, reducing governments’ cost of borrowing. The long tenure of technocrats in office further indicates that prime ministers who do not prioritize debt repayment cannot easily “fake” their type by appointing and sacking technocrats for their short-term benefit.

Some Illustrations: Financial Crises and Technocratic Appointments in Greece and Hungary

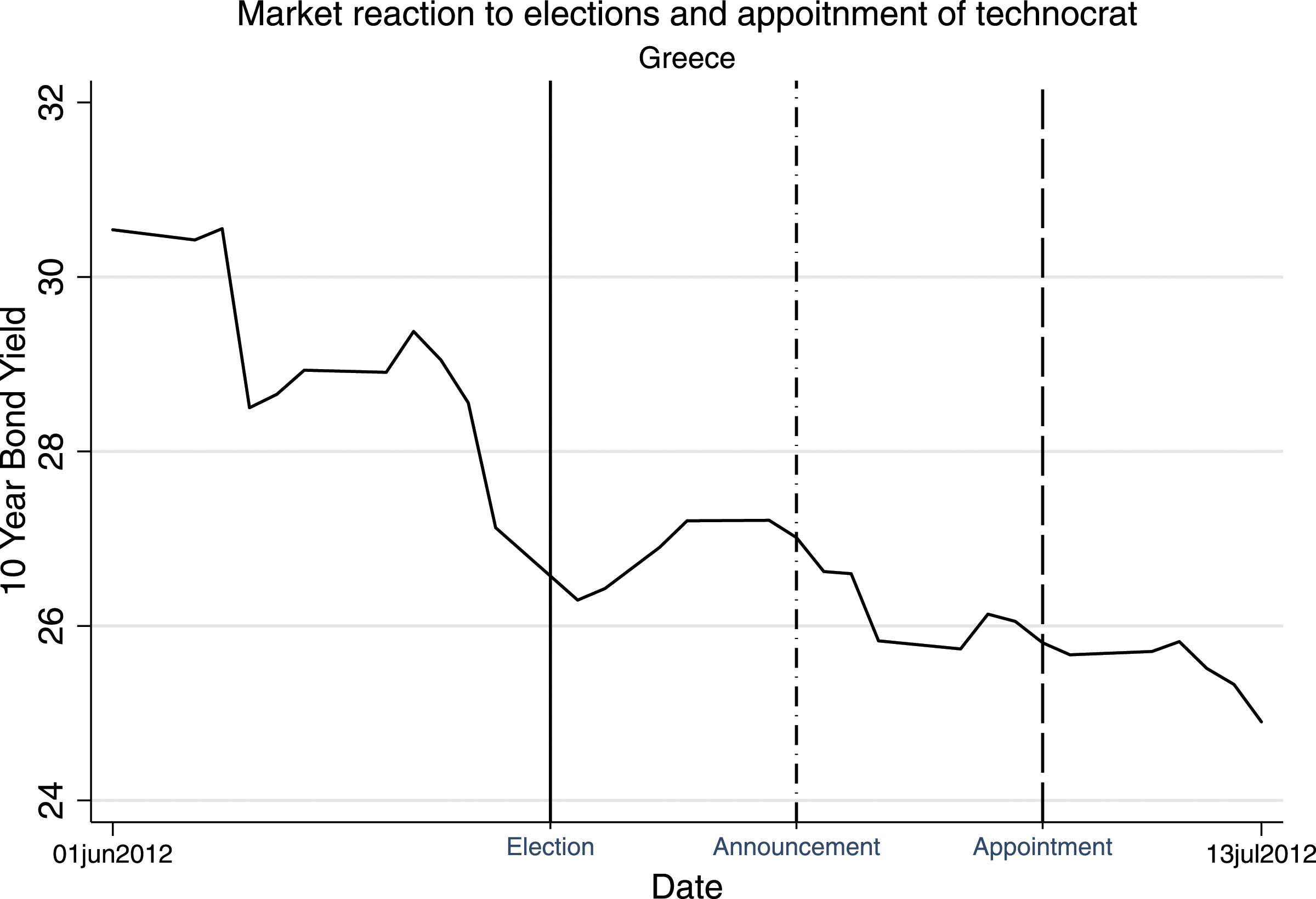

In our empirical analysis, we code ministerial appointments based on the date the minister’s appointment was confirmed. This is done for consistency reasons. In some cases, this is the first time the minister’s name is announced. Importantly, one cannot be certain of the appointment until it is formally confirmed. However, this creates a problem for us in that other factors during this announcement could be driving the market reaction. One way to check the robustness of our findings is to identify cases where the technocrat minister is announced with high certainty absent other appointments or political events. The appointment of the Greek technocrat Yannis Stournaras is one such case (Figure 3). Market reaction to Greek election and appointment of technocrat.

Stournaras was called to take the top economic job after his predecessor, Rapanos, resigned for health reasons. Since the elections had taken place 10 days prior to Stournaras’s appointment, and the government had already formed, we assume that any market reaction on the day Stournaras was appointed is a response to the appointment itself. The 10-year sovereign yield dropped nearly half a percentage point when Stournaras’s appointment was confirmed on July 5. Yet, as Supplementary Figure 5 clearly shows, the markets had already approved his appointment, reflected in the a significant drop in the yield the day after his appointed was reported in the press, on June 26.

Stournaras was indeed a successful reformer from the lender’s perspective and was voted as one of the most successful finance ministers in Europe in 2012 by the Financial Times (Times, Financial, 2012b). It is not a surprise then that when the prime minister reshuffled his cabinet 2 years later, he replaced Stournaras with another unelected, economics professor, banker, and no-nonsense reformer, Gikas Hardouvelis (Smith, 2014). According to former Greek finance minister Papaconstantinou (2016), “The move was meant to reassure creditors.”

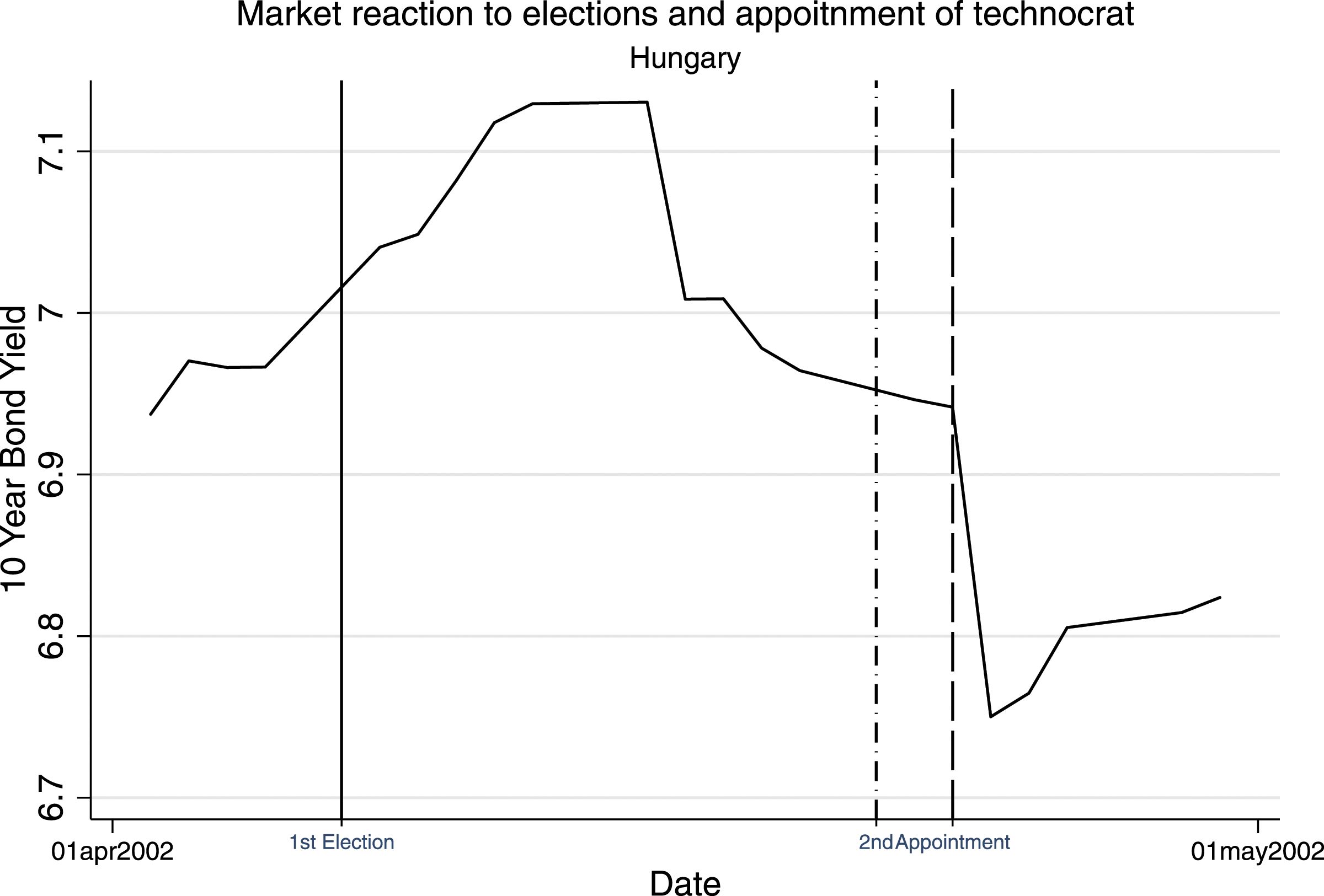

Markets have favored technocrats in Eastern European countries as well. The most prominent technocrat appointed in Hungary, Lajos Bokros, was appointed by the prime minister and leader of the Hungarian Socialist Party, MSZP in 1995 after his predecessor and party heavyweight resigned (Greskovits, 2001). Bokros is known for the “Borkos Package” which included significant market-conforming reforms and are thought to have put Hungary on the a path of fiscal sustainability. Consequently, when MSZP came back to power in 2002, investors expected a similar, market-friendly government. Indeed, already after the first round of the elections, Csaba Laszlo, an economist with experience in the ministry of Finance and the banking sector, was announced as the candidate finance minister of the incoming coalition. Figure 4 is indicative of the positive reaction by the markets, to the election of MSZP, but mostly to the appointment of Laszlo. Market reaction to Hungarian elections and appointment of technocrat.

In 2002, Hungary ran two-rounds of elections. Its mixed electoral system meant that those candidates that had not won an outright majority in the first round would go to a run-off. As Supplementary Figure 6 shows, the markets did not have a strong reaction immediately after the first round of elections on April 7. By April 9, Laszlo’s name was announced in the international press and it looked like the Socialists would be forming a coalition, ousting Orban’s party from government. After the second round of elections on April 21, and particularly after the formal announcement of Laszlo’s appointment to the finance portfolio, Hungary’s bond yield dropped even further.

Some Illustrations out of Sample: Financial Crises and Technocratic Appointments in Turkey and Brazil

The Hungarian and Greek cases illustrate that technocratic appointments are as beneficial for the less-economically developed Central European countries as for the richer West European members of the European Monetary Union. They further illustrate how even the announcement of a technocrat’s appointment is sufficient for allaying markets’ fears over the incoming governments’ policy intents. Yet, technocratic appointments should have even larger impact on investors’ trust in crisis-prone economies, particularly when these countries seek to receive financial aid (Nelson, 2014), as was the case during the 2001 banking crisis in Turkey (Arpac & Bird, 2009).

The appointment of technocrat finance minister Kemal Derviş during the 2000–2001 crisis exemplifies the point. Derviş, a Princeton trained economist and a senior World Bank staffer, was appointed as the Minister of Economic Affairs on March 2, 2001. According to the Financial Times, the appointment lifted the emerging markets bond prices (Ostrovsky & Chaffin, 2001). The appointment came at a time when the Turkish economy was facing near collapse and needed a loan from the IMF, following a dispute between the president and the prime minister. In a matter of days, the short-term interest rates skyrocketed (Pope, 2001). Unable to defend it, the Central Bank ended the exchange rate stabilization and let the currency float, which plunged nearly 50% (Washington Post, 2001). In response, the coalition government under the leadership of Bulent Ecevit, from the left nationalist Democratic Left Party (DSP), turned to Derviş (Arpac & Bird, 2009).

According to Mehmet Simsek, analyst at Merrill Lynch, the appointment “Shows the government is willing to move forward and try again (with a new reform programme)” adding that “Derviş is an excellent choice” (Boulton, 2001c). Investors’ optimism for appointing Derviş was justified. Within 10 days from his appointment Derviş drafted the government’s economic plan which included the privatization of Turk Telecom, the political independence of the Central Bank and the restructuring of three state-owned banks (Boulton, 2001b).

An illustrative example of an emerging market economy outside Europe is Brazil. In December 2015, Fitch became the second of the big credit rating agencies to downgrade Brazil’s debt to junk status (Economist, 2016). The economic crisis worsened further in 2016 when President Dilma Rousseff was impeached for hiding the size of the budget deficit. Three years later, voters and markets were called to choose between two presidential front-runners Jair Bolsonaro, a controversial far-right candidate, who as an elected legislator had “voted with the left to defend interventionist policies and special privileges” (Leahy & Schipani, 2018) and Fernando Haddad, a centrist lawyer and economist of the left-wing Workers’ Party (Schipani, 2018).

Bolsonaro’s electoral pledge was to maintain a market-oriented economic agenda. Nonetheless, to make his pledge credible he announced that, if elected, he would appoint Paulo Guedes, a University of Chicago-educated banker, as his finance minister (Schipani, 2018). According to the Financial Times: “Mr Guedes’ recruitment as economics adviser marked a tipping point in the campaign, as it brought in previously skeptical investors, business groups and entrepreneurs.” (Rathbone & Schipani, 2019). Investors did not initially trust Bolsonaro both because of his voting past but also because he would have to go against his constituencies if he were to cut public pensions and reduce the government’s deficit (Leahy & Schipani, 2018). A week later, two polls published that Bolsonaro was the front-runner. The markets reacted with jubilation: stocks rose almost 4% and yields on government 10-year bonds fell more than 4% (Wheatley, 2018a).

Conclusion

Ever since financial markets became global, governments sought their confidence. This game of confidence became harder to play as countries democratized and citizens’ preferences started to diverge from the preferences of investors (Eichengreen, 1996). International financial crises pit states against markets by forcing governments to choose between paying salaries and benefits over paying back their sovereign debt. In this confidence game, whom prime ministers appoint as their finance minister matters. Investors can influence democratically elected governments by rewarding them for choosing non-political experts to run their country’s finances. This is true not only for weaker, emerging economies but also for more “advanced” European economies.

In this article, we develop a credible mechanism through which prime ministers can earn that confidence. By appointing a technocrat to the top economic job in the country, prime ministers forgo important benefits from appointing loyal partisans. Thus, appointment of a technocrat, particularly during a time of financial crisis when the economy contracts, is a costly signal that the prime minister prioritizes debt repayment over other policy goals.

More specifically, we construct a signaling model that provides the conditions under which the appointments of technocrats are credible signals for a government’s commitment to repay its debt. We test our theoretical expectations on data from 21 Western and Eastern European countries over a period of 20 years (1990–2012). Our sample includes both countries that emerged from communist rule and suffered major economic crises in the nineties (such as Hungary) but also richer and more established Western European economies (such as Greece). We are the first to show in a systematic way that not only emerging markets but even richer, more developed democracies are subject to the disciplining role of international markets. Emerging markets, and in particular countries in Latin America, have been subject to the “confidence game” whereby democratically elected governments strive to gain the confidence of international investors (Santiso, 2003; Schneider & Ross, 1998). Our findings clearly show that the confidence game is not restricted to Latin America and can affect more established democracies. Ultimately we show that potentially all counties could be “forced” to delegate economic policy to non-elected experts when the markets lose confidence in them.

Our findings are in line with the large literature that on the interaction of markets and domestic politics (Bernhard & Leblang, 2006; Leblang & Mukherjee, 2005; Sattler, 2013). We show that elections, partisanship and even governments’ policy announcements are not the only or, in fact, the most important events markets watch for during periods of economic turmoil. Ministerial appointments are also consequential during periods of high economic uncertainty.

Ultimately we show that whom prime ministers appoint as their finance ministers matters to economic actors. Despite convincing evidence that the background of finance ministers has policy effects (Chwieroth, 2007; Christensen, 2017; Jochimsen & Thomasius, 2014; Kaplan, 2018), the dominant view within political science is that politicians’ personal background is not consequential. In this article, we contribute to this important debate by providing unique new evidence on the immediate effects of the appointments of finance ministers on financial markets.

Many questions remain unanswered. In our model, “high” types of PMs who prioritize debt repayment over domestic demands are more likely to appoint technocrats. Here we are not able to explore other ideological and political factors that might make these appointments more or less likely. Are left PMs, for example, more likely to appoint technocrats? These are questions that are not settled in the literature. In the Online Appendix, we provide some preliminary evidence that left governments might indeed have a positive likelihood of appointing technocrats during financial crises but more thorough research is required to address this question.

Do technocrats implement pro-market reforms? Are investors too optimistic by reacting positively to the appointments of technocrats? The ultimate risk of appointing a technocrat is that they will be out of tune with voters’ preferences. Romanian PM Emil Boc experienced his citizens’ wrath less than a year after he appointed Sebastian Vlădescu, a technocrat. Vlădescu, who was appointed to negotiate a loan with the IMF, oversaw the implementation of an austerity package that included a 25% cut in public pay, 15% cut in benefits and 5% increases in value-added tax. The cabinet became so unpopular that the PM sacked his finance minister together with four other key ministers (Bryant, 2010). Yet, we find that technocrats do not have shorter tenures than partisans and in fact have slightly longer tenures during periods of financial crises. Could this be due to the expectation that investors punish PMs for firing technocrats before the economy is stabilized? If they do, then technocrats could have a lot more policy power than recognized.

The number of technocrat ministers and technocratic governments across Europe rose dramatically since the Great recession raising questions about technocracy and economic governance. Moreover, financial crises are not the only events that trigger the appointments of technocrats. When the technocratic government of Mario Draghi came to office in February 2021 due to a crisis in government, investors rushed to buy Italian debt (Samson, 2021). Our article is one of the first to provide systematic evidence on the effects of technocratic appointments. Yet, more research is required before we know what the actual and longer-term policy effects of technocratic appointments are.

Supplemental Material

sj-pdf-1-cps-10.1177_00104140211024288 – Supplemental Material for When Technocratic Appointments Signal Credibility

Supplemental Material, sj-pdf-1-cps-10.1177_00104140211024288 for When Technocratic Appointments Signal Credibility by Despina Alexiadou, William Spaniel and Hakan Gunaydin in Comparative Political Studies

Footnotes

Acknowledgments

We would like to thank Jude Hays, Thomas Sattler, Alexandra Hennesy, Petra Schleiter, Mark Hallerberg, Jeff Frieden, Mark Manger, and Vincent Arel-Bundock, the participants at the 2018 APSA panel “The Politics of Economic Credibility,” the Politics Colloquium at the University of Oxford (2018), and the Speaker Series at the University of Essex (2018) for very useful comments. We thank the editors and the three anonymous reviewers for their careful reading and constructive feedback.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.