Abstract

Introduction

Financial capability and financial well-being are vital social determinants of health (Brandow et al., 2020; Brzozowski & Spotton Visano, 2020) and growing areas of practice addressed by many health practitioners and researchers, including occupational therapists (e.g., Bell et al., 2020; Bottari et al., 2011; College of Occupational Therapists of British Columbia (COTBC), 2015; Goverover et al., 2019; Sherraden et al., 2017; Swarbrick & Stahl, 2009). Yet, for a large proportion of the population financial capability and financial well-being are often not addressed—namely for persons who live with a disability (PWD), a diverse group of people which comprises approximately 15% of the world's population and 22% of Canadians (Morris et al., 2018; World Health Organization (WHO) & The World Bank, 2011). PWD, including many individuals who live with a chronic health condition or access occupational therapy services, on average experience worse financial well-being compared to individuals who do not live with a disability (Brandow et al., 2020; Wall, 2017). They can experience financial capability limitations, information and support access restrictions, financial exclusion, and personal financial management challenges that influence their financial well-being (Bangma et al., 2021; Brandow et al., 2020; Gewurtz et al., 2019). Financial education programs, including informational products (i.e., programs that provide information but do not require human interaction to be consumed or used) or human-interaction services (i.e., programs that involve interaction or contact between humans), that are tailored to the needs of PWD can help address challenges and can be a resource for health practitioners to address financial issues with their clients. Yet, the state of current financial education programs in Canada aimed at PWD is not known, and information related to financial programs has been largely ignored in health and disability literature (Brandow et al., 2020). The purpose of this study was to examine the state of financial education programs in Canada that are aimed at improving the financial capability or financial well-being of PWD.

Literature Review

Financial well-being is a social determinant of health, where decreased financial well-being is associated with lower general health and well-being outcomes (Hamilton et al., 2019; Meyer, 2017; Weida et al., 2020). Financial and economic literature describes financial well-being as a person's ability to comfortably meet current and future needs and financial commitments within a certain socio-economic environmental context (Kempson & Poppe, 2018). Experiences of decreased financial well-being, including experiences of poverty, low income, and financial stress/strain, have been associated with negative social experiences, barriers to participation in health-care, and worsening or new onset of many chronic health conditions (Hamilton et al., 2019; Weida et al., 2020). The reciprocal association is also evident—on average, the experience of chronic health issues or disability is related to worse or declines in financial well-being. Individuals living with a disability experience higher rates of low income, poverty, financial stress/strain, and financial abuse that are a threat to their health and well-being (Morris et al., 2018; Wall, 2017).

Decreased financial well-being for PWD is multifactorial. While income for PWD can vary in amounts and sources, including employment wages and related benefits, governmental benefits and funding, private funds, and insurance payments, often the available financial income from these sources are inadequate for the financial demands faced by PWD (Morris et al., 2018; WHO & The World Bank, 2011). Reduced rates of paid employment, especially employment with higher wages, and decreased governmental income support amounts, where governmental disability benefits often fall below the poverty line, leaves PWD at an increased rate of low-income and poverty; this is a global phenomenon for PWD (Brandow et al., 2020; WHO & The World Bank, 2011). Further, PWD often experience higher costs associated with having a disability or health condition, such as costs associated with prescription drugs, assistive devices, health/rehabilitation care, or support services not covered by public or insurance funding (Mitra et al., 2017). These realities negatively influence the financial well-being of PWD.

When compared to individuals who do not live with a disability, PWD may face increased difficulty or impairments in financial capability (Bangma et al., 2021). Financial capability, which is the knowledge, skills, attitudes, and applied behaviors related to managing money and finances, accessing resources, planning ahead, making financial choices, and getting help when needed (Kempson et al., 2005), is an integral part of financial well-being (Kempson & Poppe, 2018). Challenges or reductions in financial capability can leave some PWD at increased risk for financial errors and exploitation. Capability challenges have been documented in many different disability and health diagnostic populations including (but not limited to) those living with intellectual/developmental disabilities (Albuquerque & Carvalho, 2020), brain injury/stroke (Bottari et al., 2011; Engel et al., 2019), mental health conditions (Elbogen et al., 2011), dementia (Lichtenberg et al., 2016), attention or hyperactivity related conditions (Bangma et al., 2020), and neurodegenerative health conditions (Bangma et al., 2021; Goverover et al., 2019).

Regardless of disability status or financial capability level, financial education programs, including knowledge or skill building, decision-making, or behavior change programs, have the potential to improve an individual's financial capability and financial well-being (Fernandes et al., 2014; Kaiser & Menkhoff, 2017; Miller et al., 2015). Financial education programs, which include consumable informational products and human-interaction services, can address some of the multi-factorial and biopsychosocial challenges related to finance.

It should be highlighted that financial education programs are not a panacea to resolve the larger complex issues of financial well-being, poverty, financial exclusion, and financial inequities. While education programs can be part of a comprehensive approach to address the financial capability and well-being challenges experienced by PWD, they do not address the larger socio-economic, institutional, and political systemic issues that underlie increased poverty and financial strain experienced by PWD. These issues include lack of access to governmental and private benefits for many PWD, governmental benefit amounts for PWD that are vastly below the poverty line, policies that create claw-back of benefits and prevent PWD from escaping poverty, lack of affordable and accessible housing options, and decreased opportunity for employment that can provide adequate income for the individual and their dependents (Gewurtz et al., 2019; Morris et al., 2018; Prince & Peters, 2014; Senate Canada, 2018). These systemic barriers create a situation where financial well-being is likely impossible to achieve regardless of the level of personal financial capability. However, financial education programs can be part of the solution for addressing aspects of financial capability and financial well-being (Financial Consumer Agency of Canada (FCAC), 2021).

There is no current index of programs aimed at improving financial capability and well-being for Canadians living with disabilities. This is surprising as around the world the call for improving peoples’ financial capability and well-being has been in effect for years, including the Canadian national strategy for financial literacy that began in 2015 (see FCAC, 2015, 2019a, 2019c, 2021; Financial Literacy and Education Commission, 2016; The Organisation for Economic Co-operation and Development (OECD), 2017). However, only recently has guidance highlighted the need to tailor financial education programs to improve accessibility and content uptake specifically for PWD (see: Brandow et al., 2020; FCAC, 2019b, 2021).

Social and enterprise development innovations (SEDI), now known as Prosper Canada, published an online report of Canadian programs aimed at PWD in 2008 (SEDI, 2008). This report, now published over a decade ago, identified 119 programs (products and/or services). However, since 2008 the Canadian financial system has changed in many ways. An updated review of programs would be a valuable resource for PWD, their close-others/caregivers, and related health and finance practitioners who address financial capability and financial well-being with their clients. By identifying these programs from online sources, where this program information can be found, multi-disciplinary health and financial practitioners could use this information to direct clients to valuable resources. Further, a critical appraisal of these programs could highlight potential areas for future research, improvement, and advocacy.

Therefore, the primary questions guiding our study are: (a) what Canadian programs, and in particular human interaction services, are available that are aimed at improving the financial capability and financial well-being of PWD, and (b) what are the programs’ content and delivery structure specific to PWD? Our focus on Canadian programs was necessary as financial policies can be geo-political specific. Focusing on human-interaction services arose as human contact and social support have been identified as foundational to occupations related to financial capability and well-being (Engel et al., 2019; Gewurtz et al., 2019).

The sub-questions for this study included:

What types of programs are available? What populations or groups of people are the programs aimed? What are the readability and accessibility of the programs’ online content? How do service providers who deliver financial human-interaction services specific to PWD perceive services’ focus on disability, strengths, needs, challenges, and areas for growth?

This topic and these objectives are of importance to occupational therapy practice and research. While limited, published and grey literatures have noted the involvement of occupational therapists in financial capability and well-being related clinical practice and research (e.g., COTBC, 2015; Goverover et al., 2019; Swarbrick & Stahl, 2009). Occupational therapy services addressing financial capability and financial well-being crosses diagnostic practice areas and includes both assessment and intervention practice and research. Despite decades old documentation of occupational therapists addressing occupations related to finance (e.g., Kaseman, 1981), it is currently an emerging area of occupational therapy research. Understanding financial education programs can provide a practice resource and help indicate areas for future research to continue to build evidence-based occupational therapy practice.

Method

We completed an environmental scan framed by scoping review methods and reporting (i.e., Arksey & O'Malley, 2005; Levac et al., 2010; Tricco et al., 2018). We chose to frame this study within scoping review methods and guidance to provide structure and transparency to our search, selection, charting, and mapping of programs. Using scoping review methods to guide this study provided structure and transparency to our methods as currently there lacks consensus or clear guidance on environmental scanning methods (Charlton et al., 2021). Further, our study included completing the sixth stage of scoping reviews (i.e., consultations) via a descriptive qualitative study where we completed consultation interviews with service providers. In alignment with the varied ways the consultation phase can be completed, we used these consultation interviews to gain “valuable insights about issues relating to the…services that the scoping review alone would not have alerted us to” (Arksey & O'Malley, 2005, p. 29).

A priori protocols guided this study, and a study log/journal documented the research process. The protocols are available from the first author. The qualitative consultation interviews were approved by a university health research ethics board, and participants completed written informed consent.

Search and Identification of Programs with Online Content

We used an in-depth search structure and four methods of searching. A focus on online sources was necessary as the information related to current programs does not reside in the peer-reviewed published literature. First, we conducted a Google Advanced search using broad search terms (n = 11 finance and n = 30 disability/health terms) developed in collaboration with a university librarian/information specialist (Supplement A). We used the Google Incognito mode and Google Advanced region and language filters to limit results to be less influenced by past search history algorithms and restrict to Canadian-published and English-language online content. The search was completed on March 17, 2020. Second, we conducted a snowball search to investigate any additional websites or resources listed on included websites/programs identified in the Google Advanced search. Third, we hand searched five already known resources, albeit ones not specific to disability (Supplement B). Last, we consulted eight experts in our networks regarding programs they were aware; these experts work in the fields of disability, health, or finance across Canada.

Online Program Selection

We completed the screening and selection process to identify programs from the online search, where at least two research team members independently reviewed each website/link and met to reach agreement (Supplement C). A third researcher was available for disagreement. All links identified in the Google search were screened for inclusion. To identify and categorize all related web-content, programs were identified using unique website addresses (i.e., unique address = a program) and then further classified into organizations using root URL addresses (i.e., root URL = an organization that could have multiple programs).

Data Charting, Mapping, and Online Content Critical Appraisal

We developed and piloted a Microsoft Excel-based electronic data charting form and charting guide; piloting was done with a random 15% of included programs. Two researchers then independently extracted data and reached agreement about charted data. A third researcher was available for disagreement. Data mapping (i.e., analysis and synthesis) included first making narrative summaries related to the program descriptions. These narrative summaries were then used to analyze and synthesize information about the programs using descriptive statistics, namely counts and proportions, related to the program format (i.e., products and/or services); program focus (i.e., accessing governmental benefits vs. other foci); who the program is aimed (e.g., PWD, families/caregivers, health practitioners, financial professionals, or not specified/general); and disability or health condition diagnoses.

We critically appraised the accessibility and readability of online information using standardized tools. Readability was determined using an online Flesch–Kincaid readability calculator (Richard et al., 2018). The Flesch–Kincaid Reading Ease Score range, where higher scores are interpreted as improving the readability for a wider breadth of people, are categorized as: 7th grade level = 70 to 80; 8th/9th grade level = 60 to 70; high-school level = 50 to 60; College level = 30 to 50; and college graduate and above level = 0 to 30 (Richard et al., 2018). Accessibility features of the online content were dichotomously coded (i.e., observed/discussed in the online content versus not observed/discussed) using the guidance of the Web Content Accessibility Guidelines (WCAG 2.0; World Wide Web Consortium (W3C), 2008).

Service Provider Consultation Interviews

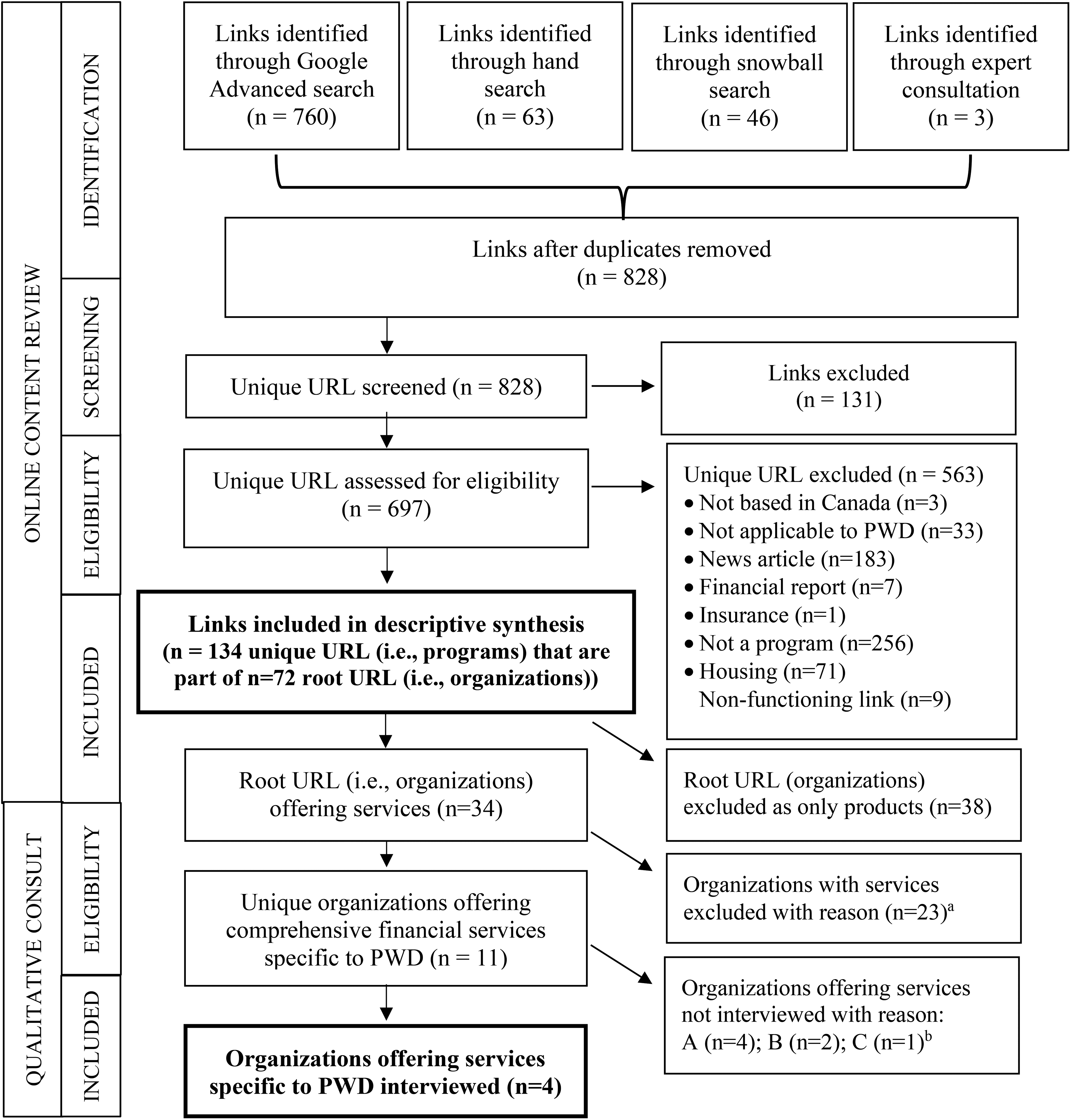

To gain a more in-depth understanding of the financial services available, we contacted service providers from the 11 financial services who provide comprehensive services to PWD that were identified in the online search. We completed a one-hour qualitative semi-structured consultation interview with each service provider. Inclusion criteria were they (a) provided financial human-interaction services related to PWD, and (b) provided services that extended beyond only completing forms or applying for governmental benefits, as we were wanting to gain an in-depth understanding of programs that offer diverse or comprehensive services (Figure 1). All people contacted were employed in paid staff positions in the service. All participants completed informed consent.

Online content review and qualitative consultation flowchart.

We used descriptive thematic analysis (Braun & Clarke, 2006) guided by the framework approach (Gale et al., 2013) to provide detailed accounts of the data and examine similarities and differences in perspectives between participants. Analysis and generated themes were primarily from a perspective that was based in the data, including direct quotes incorporated in naming some of the themes, and not explicitly influenced by previous theory and frameworks (i.e., inductive reasoning). However, as previous knowledge can always influence our thoughts as researchers, theme generation most likely was influenced by the guiding theories and frameworks foundational to this project (i.e., abductive reasoning; Lipscomb, 2012; Wiltshire & Ronkainen, 2021), namely Kempson and Poppe's (2018) model of financial well-being that was described in the introduction and models of occupational therapy that acknowledge the environment influence on occupational participation familiar to our research team that all had training in occupational therapy. Three of us independently analyzed the data to create codes, then group codes into categories and categories into meaningful themes. Credibility was addressed through researcher triangulation and expert review by the senior researcher for this project and an external financial empowerment community professional who was not a study participant but was knowledgeable about finance, financial services, and disability. Transferability was addressed through detailed descriptions of the participants, the financial services offered, and through direct quotes. We kept an audit trail and reflective journals to document progress and maximize confirmability.

Findings

Search and Analysis of Programs with Online Content

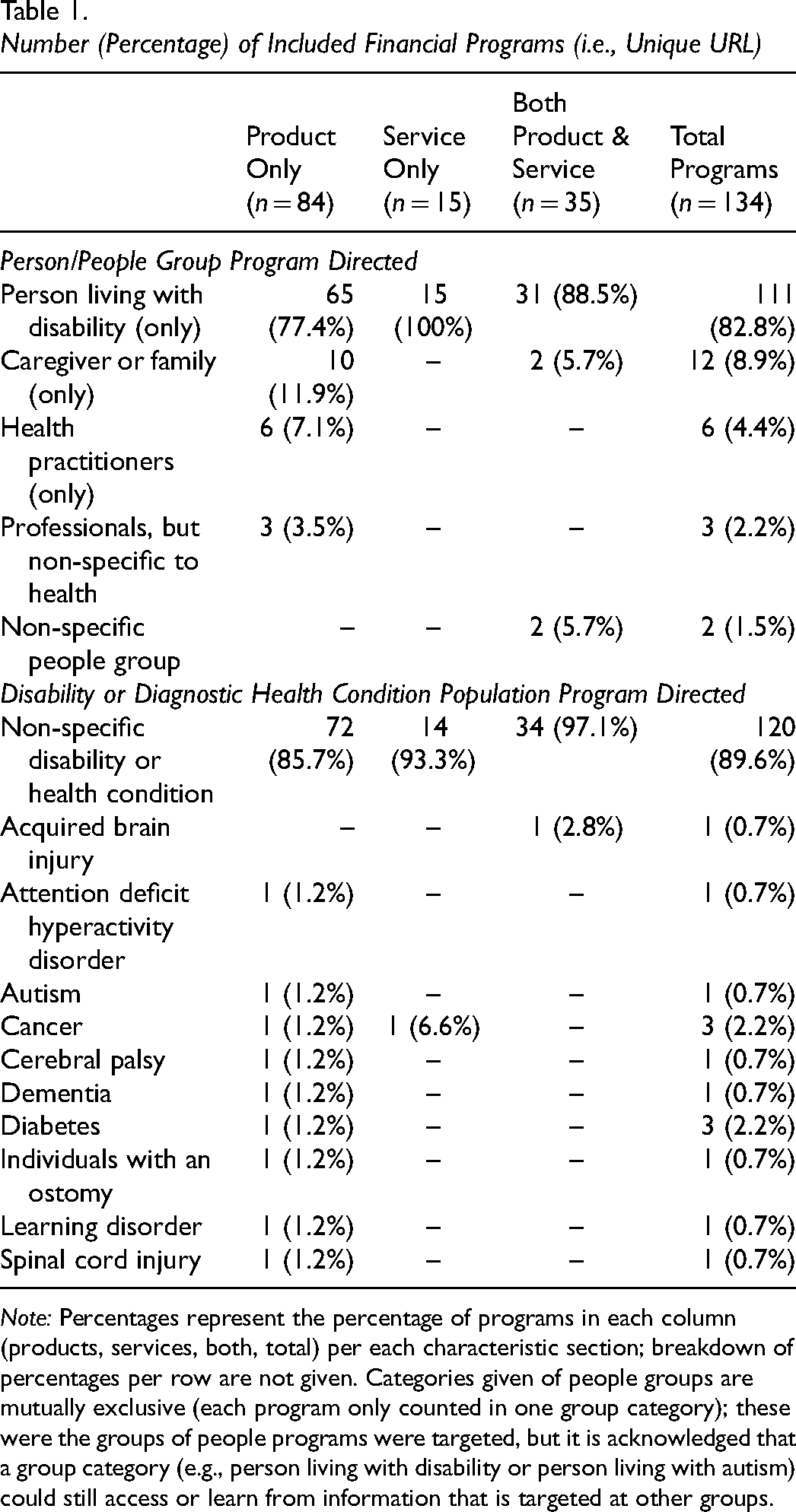

Of the 828 links identified, 134 unique programs (i.e., unique URL) met the inclusion criteria; these represented 72 organizations (i.e., same root URL; Figure 1 and Supplement E). Of the included programs, 84 (62.7%) were only informational products, 15 (11.2%) were only services that include a human interaction component, and 35 (26.1%) included both product(s) and service(s). Only 15 (11.2%) of these programs were identified in both this review and in the previous SEDI (2008) report. Person/people group and diagnostic health conditions that programs were directed are outlined in Table 1.

Number (Percentage) of Included Financial Programs (i.e., Unique URL)

Note: Percentages represent the percentage of programs in each column (products, services, both, total) per each characteristic section; breakdown of percentages per row are not given. Categories given of people groups are mutually exclusive (each program only counted in one group category); these were the groups of people programs were targeted, but it is acknowledged that a group category (e.g., person living with disability or person living with autism) could still access or learn from information that is targeted at other groups.

Most of the included programs had information about completing forms and applications for two governmental benefits for PWD: the Canadian Disability Tax Credit (DTC) and the Registered Disability Savings Plan (RDSP). One hundred and six (79.1%) programs included information about DTC and/or RDSP and 73 programs (54.5%) were exclusively about the DTC or RDSP.

Using the Flesch–Kincaid reading ease and grade level indicators (Richard et al., 2018), the range of readability for online content of the included programs was between a 7th grade and college graduate level. The range of readability scores (higher indicating more readable) was 6.5 to 76.4. The readability score mean was 38.6, the standard deviation was 13.64, and median was 39.65. Thus, the average and middle readability scores were at a college level. Most programs contained online content at a college or college graduate reading level (56.7% and 22.4%, respectively). Only 16.4% of programs contained content at a high school level and only 4.4% had online content at a 9th grade level or lower.

Accessibility was addressed in 26 (19.4%) programs. Of these 26 programs, 15 indicated they followed specific accessibility standards or guidelines, 6 explicitly mentioned using the Web Content Accessibility Guidelines (WCAG 2.0; W3C, 2008), and 11 had online content accessibility features including adjustable font sizes, videos with closed captioning, and/or high contrast options.

Service Provider Consultation Interviews

Participant's organizations are described in Supplement D. The qualitative results are summarized in three themes.

Theme 1: An Individualized Approach is Required

Financial service providers were committed to providing an individualized approach to best suit their clients’ varied needs. Accessibility and accommodations that cater to various people's needs was noted as important by all financial service providers interviewed. Service accessibility approaches included adaptations for visual, auditory, and/or physical disabilities, such as providing American sign language (ASL) interpreters or word captioning, larger font, and making accommodations for clients using a mobility device. Participants also described a multi-method approach to deliver financial services for PWD, including a one-on-one approach and/or group-based or workshop-oriented services as well as varied and flexible content. Common content offered included saving and budgeting, navigating government funding, and longevity-focused financial planning. Clients were encouraged to identify their financial priorities, and adaptation was viewed as necessary. Participants expressed that mainstream financial services often disregard the needs of many PWD, and noted the importance of considering the support needs of PWD: All this sort of off-the-shelf planning tools … they don’t really work for people with disabilities because their life-line is different. (P1)

…some clients are happy to do paperwork and follow up with the government regulators on their own. But we're more than happy to accommodate that and help them tailored to whatever level of accommodation the patient or caregiver needs. (P2)

Further, participants noted there is a need to shift the service approach for PWD, specifically noted for individuals who live with cognitive changes or impairments. This population typically experiences increased difficulty in comprehending and/or remembering information presented. Service providers used repetition, frequent explanation, and provided strategies to assist with clients’ cognitive challenges: I’ve seen it with some of our junior advisors that they get frustrated because they told this person the same thing six times. Like, yep, but that's why you want to write it down and email it to them and give them those reminders, because then it does embed. (P1)

An individualized approach included working with PWD and their close-others or support systems. Including these supports was an integral aspect to providing individualized and client-centered services. Multiple participants noted the need to offer direction to PWD support networks to help them integrate and implement the financial advice for the PWD: … with the client's permission, we’ll disclose next steps to the care services team, so case manager, occupational therapist, support worker, social worker … to get through those steps and then we will check in regularly to see that things are done and to see if there are more questions. (P1)

Theme 2: “Getting the Word Out” is Essential for Services

The second theme was the importance of “getting the word out” (P3) about financial services and financial information for PWD to clients, other financial service providers and stakeholders, and policy-makers. Participants discussed an overall lack of awareness regarding what financial resources and services are available for PWD, and how maintaining knowledge of current resources is a continual task. Financial service providers talked about informing clients about what is available to them through learning about their specific situation and being able to match them with the resources for which they are eligible: …a lot of people also don't know about these benefits… so, when they come in to get their taxes, this is where I can notice right away, ‘you should be getting the primary’ or ‘you should be applying for the disability tax credit.’ (P3)

Financial service providers needed to remain up to date as resources change and update, which adds a challenge to this profession: … legislation always changes. The federal government announced their budget and they’re thinking about changing some bits related to the disability tax credit for example, our advice will change and have to adapt… we're pretty good at adapting and making sure we're on the pulse with changes. (P4)

Moreover, “getting the word out” also included the importance of working with other organizations who potentially serve the same population. This includes ensuring other organizations or professionals working alongside PWD are aware of each other and understand what each offer. Participants highlighted collaborating with other organizations to better serve this population. These networks are an essential part of promoting financial capability and well-being for PWD: I have found that when I first started, I reached out a lot more to people. I haven't had to do that as much … people are really getting the word out and knowing about our program, which is great. If I ever find that it's getting slow again, I'll do my rounds. (P3)

Creating these networks provided the opportunity for reciprocal client referrals between financial services and other organizations serving PWD. Additionally, it promoted inter-organizational learning and use of a holistic approach while working alongside PWD. One participant improved accessibility of their financial services based on inter-organizational learning: That comes from establishing partnerships with other organizations, hearing more about specific requirements from the people they work with, or getting feedback from people about, ‘it would be great if you provided this.’ (P4)

Financial service providers also “got the word out” by advocating for change and increased financial inclusion for PWD to other organizations and policy-makers. Noted barriers to financial inclusion for PWD included accessibility and usability of government forms, websites, or telephone lines. Participants referred to experiences of long wait times, lack of returned calls, or frequent phone disconnections: Once I had [on the federal government TTY line] ‘no one is available at this time, please leave a message.’ I’m deaf; like it’s really bad! And then they’ll call you two days later and expecting the person who’s deaf to be there to answer those questions, so that’s been a huge barrier. (P3)

Overall, participants argued that more should be done by the government to support PWD in achieving financial capability and well-being. They felt their role included advocating for a better financial context for PWD: … there isn't enough coming from government, and I feel that disabled persons in Canada are slipping through the crack … they’re falling further behind. So, I think the biggest chance for improvement is going to be legislative. (P1)

Further, they described themselves being in a unique position, with the “credibility and expertise” to advocate to members of government and policy-makers to make changes to what they are experiencing as shortcomings in the current system: I don’t think a patient has to constantly advocate for themselves and that I find… it’s a huge problem in our country. A lot of people are doing it 'cause they don’t have a choice, they have to, but they shouldn’t have to—they’re dealing with enough stuff as it is. It should be a lot of our jobs. (P3)

Theme 3: Service Growth and Sustainability are Needed but Tenuous

An identified challenge and area for improvement or growth discussed by all participants was related to sustainability and feasibility for personnel, such as staff and volunteers, and funding. The participants each represented a small financial service. Whether increasing the number of paid staff or volunteer roles, overall growth of the financial service was identified by all participants as an important need for service success and sustainability. Although, specific challenges of using volunteers in this area were discussed related to required client confidentiality and increased volunteer training requirements. Three of the four participants represented a non-profit organization and identified continuous funding as a major threat to the sustainability of their financial service, as much of the organizational funding comes from government grants and programs that are not consistent over time.

Discussion

This is the first study to map and examine the education programs aiming to improve the financial capability and financial wellbeing of PWD. While the results are specific to Canada, the results most likely extend to multiple other countries around the world that also currently have national strategies to improve citizens’ financial capability and well-being (see: OECD, 2017). Our study makes three influential contributions to this area of practice and research. First, this review provides a brief overview of current evidence-based financial and micro-economic theory and policy external to health and disability, thereby strengthening the links to theory foundational to this area (e.g., Kempson et al., 2005; Kempson & Poppe, 2018)—connections to date that have not been explicitly made in health or occupational therapy literature. Second, acknowledging and addressing financial capability and financial well-being in health and disability populations is increasing in the health fields (Birkenmaier et al., 2021). However, there are practice challenges to address client financial capability and well-being including lack of education, professional development, time, and funding (Birkenmaier et al., 2021). Health and financial practitioners, including occupational therapists, can use the program mapping results (i.e., Supplement E) to improve client referrals and develop new program partnerships to support the qualitative theme of “getting the word out.” Use of referrals and partnerships with already established financial programs could be an avenue to improving practice in this area. Third, the quantitative and qualitative results from this study provide avenues for advocacy to policy-makers and improvement to further practice and research related to financial capability and well-being for PWD.

Interestingly, only 15 programs were identified in both this scoping review and the 2008 Social and Enterprise Development Innovations (SEDI) report. The differences in findings between the 2008 report and this present review may be information and resource driven. The programs we identified were primarily focused on two governmental programs that were introduced in 2008: (a) the DTC, that requires an individual to apply and meet specific criteria and if approved can claim for a non-refundable tax credit when filing their annual taxes, and (b) the RDSP, where individuals who are already approved for the DTC can further apply to have a tax-sheltered savings account and apply for related governmental grants and bonds (Prince & Peters, 2014; Senate Canada, 2018). Thus, the change in the financial landscape most likely influenced a change in the offered programs. This vast change in identified programs across time demonstrates the changing nature of financial education programs and the need to regularly update reviews in this area.

In addition, the large focus on the DTC/RDSP benefits raises important issues about the available programs, particularly the available informational or educational products. These results also highlight the lack of comprehensive programs, as the financial capability and well-being needs of PWD extend beyond knowledge of and accessing the DTC/RDSP. Further, while knowledge, skills, and applied behaviors related to applying for eligible resources is integral to financial capability (Kempson et al., 2005), the DTC/RDSP benefits are highly problematic, not inclusive of all persons living with a disability, and as non-refundable tax credits the DTC is often not useful to PWD who live on low income (Prince & Peters, 2014; Senate Canada, 2018).

There are multiple areas to improve practice in this area. Both the mapping of online content and the qualitative consultation results demonstrated financial programs need to be more tailored, individualized, accessible, and comprehensive to address the breadth of financial issues of different individuals, including PWD. These findings align with other health and disability literature (see Brandow et al., 2020; Gewurtz et al., 2019; Kaiser & Menkhoff, 2017) and current financial/economic sector recommendations (see: FCAC, 2021). While the qualitative consultation results highlight that professional staff providing human interaction services in this area are striving for a flexible, tailored, and individualized approach, the online content findings indicate that this can still be improved in the areas of what information is being provided and the readability and accessibility of online program information. Individualizing and optimizing accessibility for financial education programs can be a key area where involvement of occupational therapists can help improve this area of practice. Through development of new programs and improving current programs through strategic partnerships, an occupational therapy perspective could assist in improving how financial education programs meet the financial capability and financial well-being needs of Canadians who live with disabilities.

There is a need to have programs that extend beyond only providing information for building financial knowledge or literacy, as is the goal of financial informational products, to programs that can improve financial knowledge, attitudes, skills, and applied behaviors across broad areas of financial capability. These comprehensive programs usually require some type of human interaction (Sherraden et al., 2010). However, the programs identified in this review were predominantly informational consumable products that passively provided information; only 50 (37.3%) of the programs included human interaction services. Increased access is needed to individualized services that address financial capability and well-being (Gewurtz et al., 2019; Prosper Canada, 2021).

Last, our results highlight the lack of programs aimed at improving the skills of multi-disciplinary health practitioners who address financial needs with PWD, including occupational therapists. Only 9 programs had information directed to health or financial practitioners and all of these were informational products. Further, the qualitative findings indicated the need for continued learning and professional development for anyone providing finance related services for PWD. Many health and financial practitioners are involved in addressing clients’ financial capability and financial well-being (Bell et al., 2020; Swarbrick & Stahl, 2009). However, there is evidence that questions if health practitioners have adequate financial capability themselves, and health practitioners may not be adequately prepared to address client financial capability and financial well-being issues (Ahmad et al., 2017; Sherraden et al., 2017). The findings of this study highlight the need for comprehensive education and professional development programs to aptly prepare health and finance practitioners to meet the finance needs of their clients.

Limitations and Future Research

Our study is limited to Canadian programs for geo-political and economic policy specificity. Thus, the results may not be generalizable to other countries. Further, it is possible that some Canadian-based financial programs that would be identified more through provincial or territorial location terms were not captured. The search was conducted in English and included only programs with an English online content option. This likely limited the number of programs identified from Francophone Canada. The combination of search terms was determined based on Google Advanced searching limitations. While the search structure was broad to capture all related programs, additions or changes in terms could identify different online content. We did not include programs which only related to accessing and improving paid employment, disability insurance, or accessible housing; while these topic areas are related, the topics are large and outside the feasible scope of this study. Further, although the studies examined accessibility features using a standardized approach, we did not specifically evaluate online content compatibility with accessibility technology for visually impaired users. The small sample size of the qualitative consultation interviews limits generalizability. Despite a small sample size, the included participants represent 36% (i.e., 4/11) of the total Canadian financial service organizations eligible for inclusion in these consultations. Thus, the participants represent a significant proportion of the related financial services in Canada who can be key informants and provide vital “information power” about financial education programs for PWD (Malterud et al., 2016, p. 1754). Last, we must reiterate that this review is focused on financial education programs, and these programs do not address the larger systemic, institutional, and political policy issues that underly the increased poverty and financial strain levels experienced by PWD in Canada (Morris et al., 2018; Senate Canada, 2018). A critical appraisal of the literature, policies, and resources related to these issues is beyond the scope of this project.

Due to the quickly changing financial landscape in Canada and changes to financial education programs over time, this review should be updated periodically. Other reviews may benefit from including separate searches for other countries to examine generalizability of these findings or from including specific searches per region of each country (e.g., province and territory). While examining the online content and provider consultations provide initial information, further investigation about the financial education programs is needed from the perspective of the individuals who access these products and services. Future studies should qualitatively and quantitatively explore and evaluate financial program content, structure and format, specificity to the needs of PWD, and outcome evaluation or effectiveness.

Conclusion

The findings of this study demonstrate a need for more comprehensive and accessible financial programs for PWD, as well as improved professional development options in this area for health and financial practitioners. There is a need for advocacy to policy-makers in this area, pushing for more tailored programs and funding that meet the needs of PWD in Canada. This is pertinent as Canada continues its national financial capability strategy (FCAC, 2021) and the country currently undergoes updates to its disability benefits plan (Government of Canada & Governor General, 2020). To adequately address the health and well-being of PWD, issues related to finance need to be acknowledged and addressed, and partnerships between health practitioners, including occupational therapists, and the already available financial programs can be a way to further improve practice in this area. Continued improvements in financial capability and financial well-being education can be a part of improving general health and well-being outcomes. Finance is an area of practice that should come to the forefront for addressing the health and well-being of PWD.

Key Messages

Occupational therapists who address financial occupations can refer to and partner with the available Canadian financial education programs to improve client care.

To further develop financial education programs in Canada, occupational therapists could partner with currently available programs and assist in improving access and content.

Occupational therapists are well positioned to lead the much-needed developments in financial capability or financial well-being human interaction services aimed at individuals living with disabilities.

Supplemental Material

sj-docx-1-cjo-10.1177_00084174221129947 - Supplemental material for Review and Consultations of Canadian Financial Education Programs for Individuals with Disabilities

Supplemental material, sj-docx-1-cjo-10.1177_00084174221129947 for Review and Consultations of Canadian Financial Education Programs for Individuals with Disabilities by Lisa Engel, Taryn Rampling, Emma J. Brautigan, Tamika Bazin, Kelsey Dilts, Taylor Williams, Thalin M. Dyck, Ellie M. Jack and Heather Colquhoun in Canadian Journal of Occupational Therapy

Supplemental Material

sj-docx-2-cjo-10.1177_00084174221129947 - Supplemental material for Review and Consultations of Canadian Financial Education Programs for Individuals with Disabilities

Supplemental material, sj-docx-2-cjo-10.1177_00084174221129947 for Review and Consultations of Canadian Financial Education Programs for Individuals with Disabilities by Lisa Engel, Taryn Rampling, Emma J. Brautigan, Tamika Bazin, Kelsey Dilts, Taylor Williams, Thalin M. Dyck, Ellie M. Jack and Heather Colquhoun in Canadian Journal of Occupational Therapy

Footnotes

Acknowledgements

The authors would like to acknowledge Hal Loewen (librarian/information specialist, University of Manitoba) for their assistance in developing the online search plan, and Lani Zastre (expert staff, SEED Winnipeg, Inc.) for their perspective on the consultation qualitative findings.

Funding

This review, including qualitative consultations, was not conducted with funding from a specific grant from any funding agencies in the public, commercial, or not-for-profit sectors. Dr. Engel's current research program is funded in part by the University of Manitoba, Government of Canada’ Social Development Partnerships Program (Disability component), and the Canadian Institutes of Health Research. However, these funders had no role in this scoping review project.

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.