Abstract

Brand collaborations are widely used to generate attention, yet many fail to create lasting value. This is because brands focus too much on who to partner with rather than on how to design the collaboration. Using the Omega/Swatch collaboration and drawing on interviews and search data, this article develops a playbook for designing effective collaborations. Successful collaborations require each brand to contribute something unique, brand identities to remain distinct, and added value for both consumer bases. They also need to balance similarity and differentiation to avoid substitution and shift focus from short-term hype to sustained cross-brand spillovers.

Key Recommendations

Engineer “irreducible” co-branded products that go beyond logo swaps: Design collaborations where removing either brand would materially weaken the product, making sure each partner contributes a distinct functional or symbolic element that customers can explicitly recognize.

Deliberately keep separation in brand image to prevent substitution and brand dilution: While staying true to the core of both brands, build visible differentiation into materials, mechanics, distribution channels, and usage context so the collaboration acts as a new entry point, not a cheaper substitute.

Use collaborations to drive cross-portfolio traffic, not just one-off hype: Track and maximize spillovers by making sure the product appeals to customers of both brands, converting collaboration buyers into repeat customers across both brands.

Run collaborations as a sequenced platform, not a limited stunt: Plan a cadence of releases anchored in iconic assets (e.g., hero products, heritage symbols) to sustain attention and learning, rather than relying on scarcity-driven, one-off drops.

Despite the popularity of brand collaborations as a growth strategy, many collaborations fail to generate real excitement or to create strategic value for both partners. In this article, we derive three critical factors brands can use as a blueprint to make their brand collaborations successful:

First, from a product perspective, the joint offering must be unique, reflecting the distinctive contributions of both brands. Second, from a brand perspective, while the partnering brands should complement one another, it is essential that each has a clear and distinct brand identity. Third, from a customer perspective, the collaboration must deliver added value to the customer base of both brands. By adhering to these three principles, brand collaborations can amplify the unique strengths and heritage of both partners.

The collaboration between Omega and Swatch offers a particularly revealing example of how these three principles can turn an unlikely partnership into a strategic success. When the Omega x Swatch collaboration called MoonSwatch dropped in 2022, headlines declared it had broken the internet. Interest, sales, and hype were at an all-time high, with even presidents unsuccessfully trying to get their hands on the new watch. 1 The Swatch Group, which owns both brands, has maintained hype through new drops and has continued the collaboration beyond the initial launch. On the surface, this is not a natural brand fit: Swatch is a plastic, entry-level brand known for its quirky designs with watches priced between $30 and $600. From featuring the artwork of renowned painter Basquiat to turning the Simpsons donut into a watch face, Swatch’s portfolio reflects a deliberately broad and unconstrained aesthetic. On the other hand, Omega, tracing its history to 1848, is one of the most iconic high-end watch brands in existence, with a more tightly controlled design language, deep heritage cues, and a consistent emphasis on craftsmanship and precision. The cheapest Omega at $2,400 is four times more expensive than the top-of-the-line Swatch, and Omega prices go all the way up to $725,000. Omega was the first watch on the moon, has been the official timekeeper of the Olympics for over 90 years, 2 and is worn by James Bond, 3 Prince William, and George Clooney.

The Omega x Swatch collaboration provides a compelling test case for these three principles and what marketers can learn from them as they explore co-branding to reach new audiences and maintain excitement around heritage brands.

The Collaboration

Omega’s Speedmaster is the first watch worn on the moon and a legendary part of the Apollo 13 story, 4 in which astronauts used the watch to time a critical engine burn after an onboard explosion. The basic model retails for over $6,000, with more precious-metal versions going all the way up to $50,000. The astonishment could not have been larger when Omega and Swatch released a shared version of the Moonwatch, the MoonSwatch, selling for barely $260. It mimics the original design, swaps stainless steel for Swatch’s sustainable plastic called “bioceramic,” and uses an electronic quartz movement instead of a mechanical one (see Figure 1). Eleven versions were released, each named after our solar system’s planets (and for the nostalgic, Pluto is still included).

Comparison between both designs, MoonSwatch on the left, Moonwatch on the right © The Swatch Group

How did this unlikely collaboration come about?

Swatch Group owns both brands but historically kept them separate. Shared ownership within the Swatch Group naturally reduced coordination challenges, ensuring strategic alignment, cultural fit, and streamlined distribution, making the collaboration easier to execute operationally. Independent firms can still apply the same customer-facing principles, but they are likely to face higher coordination costs and a greater risk of misalignment in execution.

Despite Swatch’s more recent history, and its lower price point, it is not looked down upon within the enthusiast community. The brand has saved the Swiss watch industry before, 5 when Japanese electric watches entered the market, which led to over 60% of Swiss brands closing down and 70% of those in the industry losing their jobs.

Swatch also has a history of creative collaborations on its designs, 6 with artists like Keith Haring and even Pigcasso, a talented pig who likes to draw (see Figure 2). Omega has a very curated approach; special editions were released when the first plane powered purely by solar panels went around the world, and to commemorate the 50 years since winning NASA’s “Snoopy” safety award 7 for their work with the Apollo missions—a watch currently on a multi-year waitlist, with a retail price of $10,000 and many paying twice as much on the secondary market for the privilege to buy one.

Pigcasso providing the design behind the Swatch © The Swatch Group

During subsequent releases, specifically when Swatch released its version of the “Snoopy” MoonSwatch in 2024 for 3% of the original’s price ($310), lines again formed at the stores, where we interviewed customers about their motivation to acquire it. We found that consumers of the collaboration are fans of both brands. How does a collaboration that combines irreverence and accessibility to the general public appeal to Omega consumers, who, on the surface, want a more traditional, expensive luxury product?

We found that the fun element of it was key. While Omega has to be much more strategic and conservative in its offering, fans appreciated the variance and colorfulness that Swatch could add. As one consumer told us, “I quite like the planetary concept of it. . .and now the colors.” The sales staff in Swatch Boutiques told us the collaboration has led to a new type of customer becoming regulars: high-end watch consumers, often Omega owners, who would buy the MoonSwatch but also broaden out to other Swatch models, usually buying them as presents for their family and friends. While anecdotal, these employee insights pointed to an important pattern: the collaboration did not simply raise overall interest in watches, but appeared to encourage cross-brand engagement, highlighting a potential spillover effect between the two brand portfolios. This stands in contrast to many previous brand collaborations that aimed to broaden a luxury brand's market share, which were typically supported only by consumers of the more affordable brand.

What happened?

From a sales perspective, the collaboration is a success, having sold over a million MoonSwatches in the first twelve months alone, with a profit margin rumored to be close to 90 percent. As the New York Times wrote, “MoonSwatch now is recognized by many as the watch industry’s defining moment of 2022, and perhaps of the decade—even though the year is only half over and the decade has seven years to go.” 8 The general interest in Swatch has been revived, as a couple we interviewed at the London store who used to buy Swatch watches decades ago, put it, “Swatch is not as popular as it was then during our teenage years, but them coming out with collaborations like this makes us want to have it again.” Omega is also an aspirational brand for them. “[I] wanted a real Omega, so this will make do for now.” Yet, the bigger question was about Omega, as this was the brand that risked brand dilution by doing this collaboration. Critics feared that a $260 plastic watch that looked nearly identical to a $6,000 Speedmaster would cannibalize Omega’s sales and damage its luxury reputation. That risk becomes particularly stark when consumers perceive the lower-priced offer as a substitute for the hero product, rather than as a distinct expression of the same brand story.

Instead, the opposite happened: MoonSwatch made Omega even more desirable. While the Swatch Group is highly secretive about individual brands' performance, the classic Omega model used to be easy to source but is now sold out in most stores around the world. As Omega CEO Raynald Aeschlimann reported, “In terms of Speedmaster sales since the launch of the MoonSwatch, there was a 50 percent increase globally, on new, current, and vintage models. In fact, even the value of vintage model Speedmasters increased because of the demand.” 9 The lesson is not that any price gap can work, but that even a substantial price gap can be viable when the lower-priced product is clearly differentiated in materials, mechanics, and purpose, so that it complements rather than substitutes for the higher-end original.

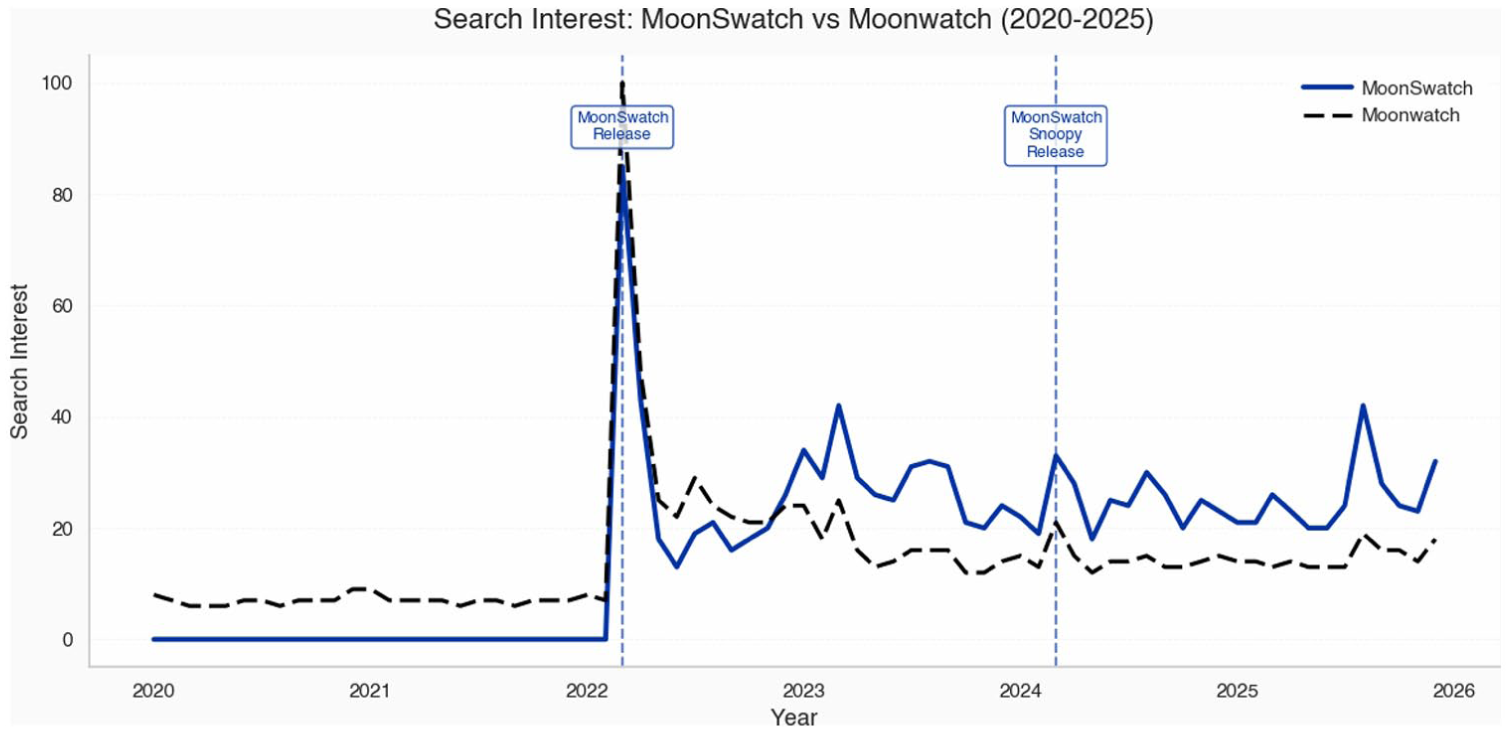

We also used Google Trends to investigate shifts in consumer attention and brand interest through search pattern data. As shown in Figure 3, search interest in the original Moonwatch rose sharply following the MoonSwatch release, indicating a substantial increase in brand attention. What is noticeable is that well into 2025, and three years since the original release, even the weakest months for the original Omega Moonwatch outperform previously seen interest in the brand, meaning that interest has sustainably increased for the more aspirational brand, too.

Normalized global search interest in MoonSwatch and Moonwatch on Google’s search engine, highlighting how interest in the original Moonwatch increased, too, and continues to be at significantly stronger levels ever since. Indeed, search volume for the original Moonwatch is 95% stronger in the last 6 months, compared with the 6 months before the collaboration.

What’s next?

Swatch Group’s brand portfolio covers almost every brand point via its wide-ranging brand portfolio, including brands such as Tissot, Hamilton, and Glashütte. In order to capitalize on its brand portfolio, Swatch Group is now applying the blueprint to other brands, hoping to unlock attention, demand, and new entry points across its brand architecture. In 2023, Swatch collaborated with Blancpain to revive its Fifty Fathoms dive watch in a plastic, $400 version. While Blancpain is a niche brand, it claims to be the world’s oldest surviving watch brand.

Unlike the quartz MoonSwatch, the Blancpain x Swatch features a mechanical movement, and as a result, is almost twice as expensive. We observed that the appeal of the brand collaboration extends to people who had never heard of Blancpain before, which likely aligns with the Swatch Group’s aim. One customer, who had already bought four different Swatch x Blancpain, told us he had never heard of Blancpain before but became fascinated once he heard about it. Swatch has been successful in turning Blancpain again into an aspirational brand. It remains to be seen if there will be excitement among brand enthusiasts of both brands, something that made the MoonSwatch so special. There are reasons to be less optimistic about the mutual interest, as the watch enthusiast community is one that chooses to buy watches that can cost as much as a house and values the appeal of having a mechanical piece that can be repaired and handed down across generations. Indeed, Patek Philippe, one of the most established ultra-high luxury watch brands, advertises that you never truly own their watch but merely take care of it for the next generation. 10 Swatch has been at the forefront of the industry with its new mechanical movement, the first in the world to be assembled entirely automatically without any human involvement. 11 The drawback is that, because it is permanently sealed, it cannot be serviced or repaired, which classical Blancpain customers likely would have valued.

What can already be said based on the search patterns around Blancpain is that brand interest in Blancpain has significantly and sustainably increased. This is likely indicative of an increase in brand awareness in the first place. Of note, the search interest in Blancpain is still twice what it used to be before the collaboration release, even more than two years later (see Figure 4).

Normalized global search interest in Blancpain on Google’s search engine. Even though peak interest came down, search volume is still twice as strong in the last 6 months, compared with the 6 months before the launch.

Overall, these successive releases by the Swatch Group, spanning 2022 through 2025, highlight that the collaboration framework is not a one-off event, but part of an ongoing, deliberately sequenced strategy to get and sustain attention and demand.

Can it be replicated?

The positive spillover to both brands is quite unique about the MoonSwatch collaboration and stands in contrast to many previous failed brand collaborations, with Target's Neiman Marcus collaboration being a prominent example. 12 Target started selling a collection in collaboration with high-end retailer Neiman Marcus, which had prominent designers such as Marc Jacobs and Diane Von Furstenberg on board. Likely worried about brand dilution, the designers, however, did not engage with the staple pieces they were known for, but rather offered dog bowls, thermoses, and yoga mats at Target. Target’s customers not only lacked an appetite for these products, but also for the price point: What might be cheap for a Neiman Marcus customer was prohibitive for Target’s audience. 13 Neiman Marcus' usual customers were also less likely to shop at Target.

Other brands are trying to replicate the new Omega x Swatch collaboration model given its success, but few so far have gotten it right. For example, TAG Heuer, the LVMH-owned premium watch brand with close ties to motorsports (Formula 1 in particular), released a limited-edition collaboration with the fashion and lifestyle brand Kith, charging $1500 for it. While the MoonSwatch brought together iconic elements from both brands in the collaboration, the TAG Heuer/Kith watch is a heritage reissue of TAG Heuer’s 1986 Formula 1 watch. 14 Considering it is a heritage reissue, TAG Heuer could have released an almost identical watch without a collaboration. This highlights an important boundary condition: the strategy works best when the collaboration is anchored in a product, design, or symbol with enough iconic value to make the joint offer feel necessary rather than interchangeable.

How is it different?

Most brand collaborations follow a predictable structure. They typically involve a “host” brand already active in the category and a “guest” brand that joins by lending something recognizable, either a tangible or a symbolic element. 15 A classic example is the successful Supreme x Rimowa collaboration, 16 in which Rimowa, the well-established luxury luggage brand, acted as the host brand and added Supreme’s highly recognizable streetwear logo to help capture more of the millennial market and position itself as more lifestyle-focused. Previous work highlights that the host brand might not always be credited for the collaboration, 17 and, in a luxury mass-market context in particular, the more selective brand has to be careful about brand dilution, which is often mitigated by keeping the collaboration temporally limited and thus scarce. 18 The MoonSwatch collaboration challenges all of these expectations. Both partners are watch brands, so the usual host/guest logic does not apply. It’s also less of a binary insertion of elements; rather, it mixes tangible and symbolic elements from both brands. The collaboration is also not a scarce, short-term, low-risk experiment; rather, it has become a multi-year platform, with the Swatch Group being transparent from the beginning that the MoonSwatch would not be a limited edition. Taken together, these divergences from the typical brand collaboration playbook make MoonSwatch a useful case for rethinking how collaborations create value and for refining the principles that guide them.

Unlike conventional collaboration models that focus on brand similarity and market access, our framework shifts attention to how value is created and perceived in the joint offering. Rather than treating collaborations as symbolic add-ons or short-term exposure strategies, we conceptualize them as product-level design problems that must generate irreducible contributions from both brands while preserving their distinct identities. This perspective also reframes success from immediate buzz to sustained cross-brand spillovers, emphasizing how collaborations can strengthen entire brand portfolios rather than dilute them.

The Three Keys to a Successful Brand Collaboration

The success of the MoonSwatch collaboration, which deviates from traditional co-branding, provides a compelling blueprint for other brands considering such partnerships. Co-branding outcomes are fundamentally shaped by brand associations, and we therefore frame the playbook through the lens of brand theory, where brands benefit from associations that are strong (memorable), favorable (positively perceived), and unique (clearly differentiated)— all grounded in baseline brand awareness. These associations shape how customers interpret and respond to any collaborative offer.

In Table 1, we translate the three customer-centric key points into a practical decision tool, including diagnostic questions managers can ask, common mistakes to avoid, and metrics to monitor when assessing a potential collaboration.

Success Criterion for Brand Collaborations.

The success factors we derive are intentionally focused on external, customer-visible drivers that shape how the collaboration is perceived and valued in the market. Because the principles operate at the level of consumer perception, they are broadly transferable across partnership contexts, even though differences in ownership structures, resource configurations, and distribution systems can make some collaborations easier to execute than others.

Traditionally, successful co-branding has been understood as a partnership between like-minded brands, often of similar stature, that complement each other to tap into new markets or audiences, such as Rimowa x Supreme, both luxury brands, which allowed Rimowa to reach Supreme’s younger customers. The MoonSwatch playbook, however, challenges this notion by demonstrating that successful collaborations don't necessarily have to be between brands with parity, whether in terms of stature or similar market positioning. Instead, the critical factor lies in creating a partnership where both brands bring something unique and valuable to the table—beyond market access. As such, the first key to success is that both brands must bring something unique. Omega brought heritage, Swatch brought irreverence. Omega loyalists found the Swatch collaboration a breath of fresh air, and Swatch enthusiasts had an aspirational and historically grounded piece that they could now own. Before engaging in a collaboration, each brand must be clear on what it is bringing, whether consumers of both brands will value it, and whether the product would be meaningfully weaker without either partner. Managers should also test whether customers can clearly articulate what each brand contributed, as this is often where weak collaborations begin to unravel. In this sense, Criterion 1 requires that each brand contribute something unique and that both partners possess strong, favorable, and distinctive associations that complement rather than duplicate one another, enabling the collaboration to create meaning that neither brand could deliver alone.

A collaboration that did this well was BMW’s with Kith, which involved creating a custom car and color shade, along with matching accessories and clothing. 19 BMW provided its automotive design and motorsport heritage, while Kith brought its streetwear experience and credibility to the table, resulting in a sold-out collection that neither brand could have done without the other.

The second key to success is that the brand identities are distinct from each other. The Swatch and Omega collaboration succeeded because it wasn’t just about offering a more affordable version of a luxury product; it was about merging two distinct brand identities to create something that resonated with consumers from both brands. Swatch brought its playful, accessible design ethos, while Omega contributed its heritage and prestige, resulting in a product that felt authentic and innovative to both brand loyalists and new customers alike. Criterion 2 emphasizes that each brand’s existing associations must remain intact and favorable throughout the collaboration, ensuring that the partnership does not blur positioning or dilute what makes each brand credible. Managers should therefore closely monitor whether price, design, communications, or channel choices threaten their brand’s identity. Omega likely considered this question and therefore decided to sell the collaboration only through Swatch stores.

We can see this with LEGO as well in its collaboration with Adidas on a LEGO model of Adidas trainers, which appealed to fans of both brands. But Lego hasn’t always gotten it right. It once collaborated with Shell, resulting in co-branded products and sales channels for over four decades, which ultimately ended when Lego was heavily attacked by Greenpeace in the 2010s, 20 harming its brand image.

The final Criterion for success is that the brand collaboration brings added value to customers. At its core, the success of brand collaborations depends on a sharp, customer-centric orientation that prioritizes delivering added value to consumers over market access and expansion. Before embarking on a collaboration, brands should always be asking: “What added value does this bring to our customers, and how can we use that added value to reinforce our brand relationships?” Collaborations need to be ones that consumers value, and that allow them to engage with the brands in a new manner that goes beyond the sum of its parts. Managers need to distinguish between short-term hype and genuine spillover into the broader brand portfolio.

The collaboration between MAC Cosmetics and Disney 21 for their "Aladdin" and "Cinderella" collections provided fans with makeup inspired by beloved characters. MAC brought its reputation as a top-tier makeup brand, while Disney added the emotional connection to its stories. The collaboration added value by allowing consumers to engage with Disney's magic through self-expression.

These principles are not a guarantee of success, and managers should also be clear about the boundary conditions. Shared ownership, as in the case of Swatch Group, can make execution easier by reducing coordination frictions and aligning incentives, but it is not a prerequisite if independent firms can achieve similar alignment around product, positioning, and distribution. Likewise, not every collaboration needs an iconic hero product, but it does need a product or design cue with enough symbolic weight to make the joint offering feel meaningful rather than arbitrary. Finally, large price gaps are not inherently disqualifying, as MoonSwatch shows, but they become risky when the lower-priced offer feels like a discounted substitute rather than a distinctive entry point that reinforces the more aspirational brand. In practice, applying these principles often involves navigating difficult trade-offs rather than optimizing each independently. The very features that make a collaboration compelling, such as strong visual or symbolic links to an iconic product, can also increase the risk that the lower-priced offer is perceived as a substitute rather than a complement. Managers therefore face a delicate balancing act: the collaboration must be close enough to the original to benefit from its associations, yet sufficiently differentiated to preserve brand distinctiveness. The MoonSwatch illustrates this tension clearly, as its success depended on simultaneously leveraging the Speedmaster’s design while preventing direct substitution through deliberate differences in product architecture, materials, mechanics, and channel strategy.

Ultimately, the MoonSwatch collaboration teaches us that the most impactful brand partnerships are those that are thoughtfully constructed with an eye toward enhancing the consumer experience. It's not about diluting a luxury brand to make it more accessible, but about finding a way to celebrate what makes each brand special, creating a new product that feels fresh and exciting to both sets of customers. This is the true lesson for marketers seeking to innovate through collaboration and co-branding: success lies in creating something that feels authentic and valuable to the consumer, regardless of the price point or market position of the brands involved.