Abstract

Digital technologies challenge incumbent firms to rethink their established approaches to customer relationships. This article examines how a corporate bank reconfigured its relationship-oriented business model to benefit from digital transformation. The case analysis reveals a gradual transition toward a blended service model that first replaces, then complements, and finally augments physical with digital in increasingly complex customer interactions. While replacing and complementing human-enabled services with digital offerings are necessary steps of the digital transition, the associated competitive advantages are perceived as unlikely to endure. In contrast, augmenting human-enabled services with sophisticated digital technologies holds the potential for sustainable competitive advantage.

Keywords

Corporate banks have had a bumpy ride since the financial crisis. Despite the economic upturn that supported the recovery of many industries, most business banks’ profitability remained below pre-crisis levels owing to high operational expenses and intensifying competition. 1 Considering the rising risk costs brought about by the pandemic-driven stumbling of the global economy and geopolitical tensions, the banks’ short-term outlook is not bright either. For that reason, there is increased pressure on corporate banks to reinvigorate their customer-facing business processes.

This thrust is further amplified by changing customer needs. Increasingly, corporate customers expect integrated solutions and a fully digital, effortless experience with a self-service option to manage daily banking transactions. 2 Meeting such multifaceted requirements necessitates that corporate banks keep pace with evolving technology and enhance their digital capabilities. 3 Established players who fail to adapt face the risk of being replaced by more agile rivals or losing market share to digital-savvy new entrants. 4

Nevertheless, it seems that digital transformation is not yet pervasive but more of an emerging force in corporate banking. Only a minority of incumbents have fully embraced digitalization so far, and corporate customers are digitally underserved compared to the retail segment. 5 In fact, many wholesale banks rely on outdated, cumbersome processes and traditional service models. 6 On the other hand, the bulk of incumbent banks plan to significantly increase the amounts invested in digitalization 7 and consider technology-enabled offerings as crucial to improving their services. 8

Recognizing the digital imperative and allocating funding are essential but not sufficient steps toward a digital future. Corporate banks pursuing a digital strategy have to face complex competitive, technological, and demand dynamics, 9 making it difficult to decide where to invest and which initiatives to prioritize. In particular, finding the right combination of the “high-tech” digital elements and the “high-touch” physical and human elements is a key challenge for service firms like corporate banks. 10 Such ambiguity warrants a better understanding of the potential benefits of digital transformation over different time horizons, as well as the impact of digital transformation on corporate banks’ established business models, customer relationships, and competitive advantage.

To provide such understanding, this article analyzes digital transformation in the context of a European corporate bank, looking into how it can contribute to value creation and enhanced competitiveness. To help support business banks—as well as service firms more generally—along their digital path, this article investigates how digital transformation impacts the sources of competitive advantage, revealing the potential sources of value creation in digitally transformed corporate banking and a new, blended service model centered around the amalgam of human-enabled and digital service. The findings highlight the gradual rather than sudden nature of digital transformation, the importance of mutual transparency as a unique value source that digital technologies enable, and the possibility of achieving sustainable competitive advantage by moving from first replacing, to then complementing, and finally augmenting human with digital.

Background

Digital Transformation and Competitive Advantage

Digital transformation is a change process that emerges through the adoption of “combinations of information, computing, communication, and connectivity technologies.” 11 The adoption of digital technology changes the competitive landscape by disrupting the status quo, but it also creates novel opportunities for value creation. 12 Digital transformation can bring benefits to organizations in terms of both operational efficiency and organizational performance more broadly. 13 Operational efficiency includes reduced operating costs, 14 optimized administrative processes, 15 and faster decision-making. 16 Broader performance effects can include faster growth and better innovativeness, 17 as well as an upgraded customer experience. 18 Digital transformation frequently presents both pressures and opportunities for renewing the firm’s business model, 19 and navigating the digital transformation therefore requires the organization to take a strategic approach.

Digitally enabled value can be created not only by better addressing customers’ needs directly but also by making use of the business ecosystem more broadly. 20 First, to better understand clients’ behavior, customer touchpoints are converted into customer sensor points that are designed to collect and store data on customer behavior, and businesses develop their analytics capabilities to make use of this pool of customer data. The extracted insights are then employed to drive evidence-based decisions and create more personalized customer experiences. 21 However, companies with a narrow focus on a linear value chain are at a disadvantage 22 because value creation from digital transformation often occurs at the level of the ecosystem, which frequently includes complementors and even competitors. 23 Digital-savvy companies can outperform their competitors by engaging customers more continuously and collaboratively instead of having only episodic, detached transactions with them. 24

When facing a digital disruption, service firms can opt for a “high-tech” approach, fully digitizing their service processes, or a “high-touch” approach, aiming to gain competitive advantage by emphasizing the physical and human elements of the customer experience. 25 For established firms, a combination of the two is often thought to be the best approach, allowing them to gain the advantages of digital while keeping the advantages of their established physical competences. 26 However, how to go about implementing such a hybrid between digital and human is not trivial, as established firms usually cannot pivot without destroying some of the value created by their legacy business. 27 Therefore, an incremental approach of experimenting with a broader range of smaller digital initiatives, taking calculated risks, and building digital competences gradually may work best for digital non-natives. 28

Competitive Advantage and Digitalization in Corporate Banking

According to the commonly accepted view, it is hard to build competitive advantage in corporate banking. New product launches are quickly imitated, and the pressure on profit margins due to intense rivalry means that reducing prices is not rewarding either. 29 In such circumstances, customer relationships are believed to be a prime source of competitive advantage. 30 Banks tend to place increasing emphasis on customer relationships as competition increases 31 because it provides shelter from price wars 32 and helps protect their competitive position. 33 Previous studies have identified three crucial groups of resources in such a relationship-oriented strategy: skilled employees, who are the primary customer contacts and the best positioned to evaluate market developments 34 ; sector-specific expertise enabling meaningful conversations with customers 35 ; and proprietary information on clients gathered via multi-level communication. 36

Because personal contact with customers is central to the value proposition of corporate banks, there is a conflict between banks’ economically rational intention to migrate smaller, less profitable relationships to digital channels and their clients’ limited willingness to adapt to such channels. 37 Even for larger, technologically savvy corporates, digital technologies have been considered a complement to rather than a replacement for personal interactions, as fully automated processes make customers perceive themselves as underserved. 38 Consequently, commercial banks’ inclination toward digitization of routine tasks and services can weaken the relationship-banking model and result in a transaction-oriented attitude in customers. 39 Transaction-oriented customers tend to unbundle their financial services needs and aggressively shop around after price and quality, placing less importance on relationships, 40 which undermines relationship-based competitive advantages. As the physical, digital, and social worlds are converging, corporate banks are confronted with the challenge of finding the optimal combination of these realms to create value. 41

Barras’s reverse product cycle model 42 offers insight into how digital transformation may impact the evolution of competitive advantages in the banking sector. The reverse product cycle theory suggests that the innovation process in service industries is the reverse of that observed in product-based sectors. First, initial investments in the new technology fuel incremental process innovations. Subsequently, as firms acquire knowledge of the new technology, they move toward more radical process innovations directed at improving the quality of services rather than decreasing costs. Finally, the accumulated experience of using digital technologies enables progress toward radical product innovation and developing a new generation of services. Parallelly, the competitive emphasis shifts from cost advantages to product differentiation. However, it is debatable whether competitive advantage can be sustained in a quickly evolving digital environment or if the maximum firms can aspire to is temporary advantages. 43

Method

The backbone of this research is an exploratory case study conducted in the business banking division (“Organization”) of a universal bank operating in an EU country (“Case Bank”). Case Bank belongs to a leading European banking group (“Parent Bank”) that considers Central Europe its strategic market. Case Bank is one of the seven large national banks, and it offers a wide range of financial solutions for retail and corporate clients. The latter segment is targeted by the Organization, which generated 42% of Case Bank’s profit in 2020. With an estimated 10% market share in lending and deposits, the Organization is a relevant player in its home country’s corporate banking market. Assurances of anonymity prevent more detailed information from being disclosed.

According to its strategy, the Parent Bank aspires to become a data-driven organization; it aims to shift its omnichannel approach to a digital-first distribution model and plans to invest heavily in Central European entities’ digital transformation. Although digitalization has already been an important pillar of Case Bank’s strategy since 2017, developments have focused predominantly on the retail segment. In 2020, digital gained even more ground in concurrence with the Parent Bank’s strategy, and a multi-year digital roadmap was outlined by the Organization, providing an illustrative empirical setting for the present research.

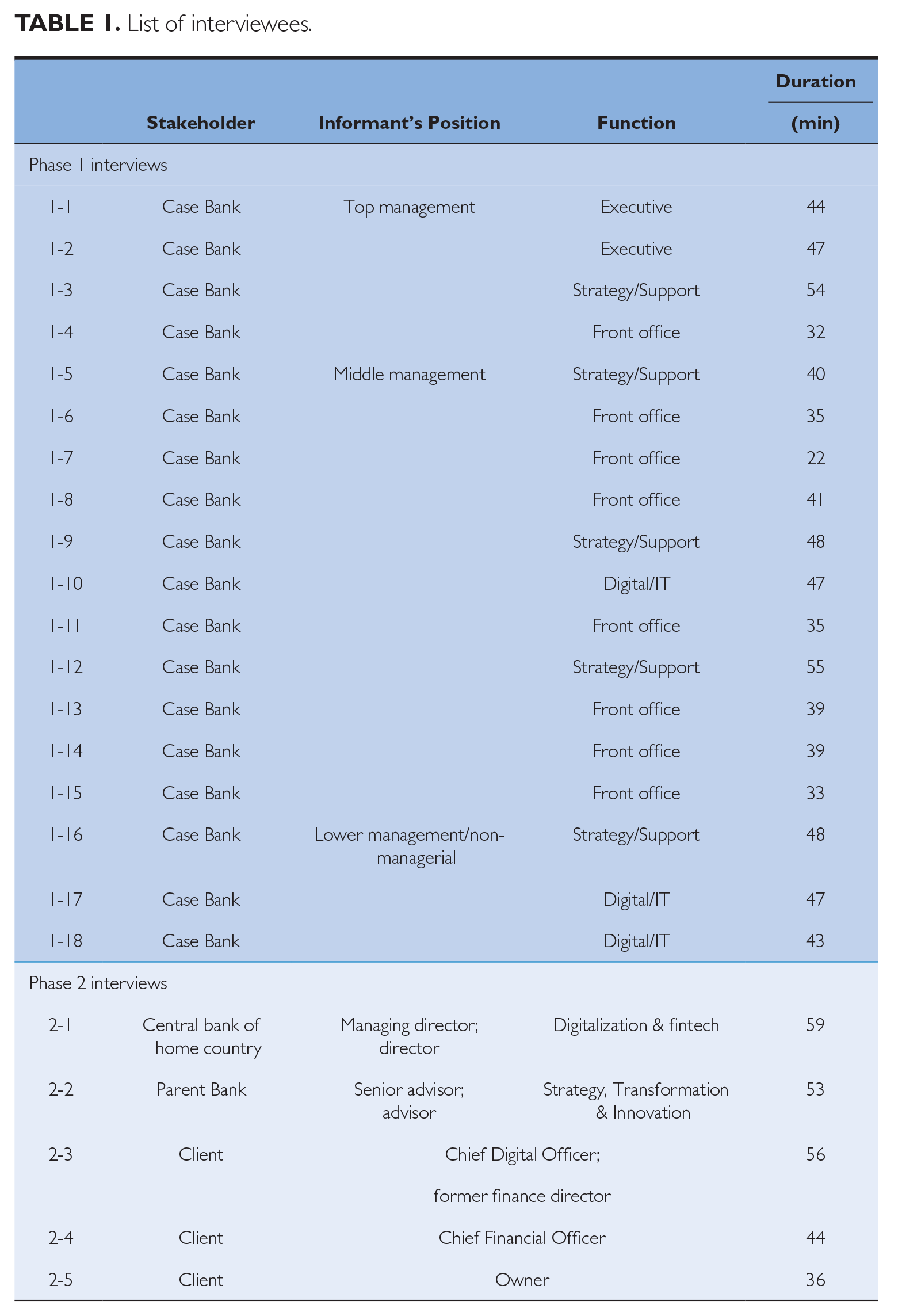

This study is primarily informed by semi-structured interviews conducted in two phases. The first 18 interviews were conducted within the Organization between November 2020 and January 2021. The interviewees included informants from all management layers and relevant functional domains. Involving executives enabled us to capture narratives from those who are directly involved in strategy formulation and allocate resources for digital initiatives. Interviewees from middle and lower management, responsible for strategy execution and delivery of digital projects, added a more operational perspective. As far as functional areas are concerned, informants were selected from three domains. Front office managers are the most knowledgeable about the relationship aspect of corporate banking and directly sense market trends as well as possible changes in customer behavior. People from the corporate strategy and product support departments were involved to capture insights about the links between strategy and ongoing digital developments. Finally, informants from IT provided a technological perspective on digital transformation. Sampling was continued until theoretical saturation was reached, that is, when further interviews did not yield significant new insights. 44 In the second phase, the emerging internal perspective was triangulated by data collected from external stakeholders between January and February 2021—including two informants in charge of digitalization and fintech at the central bank of the Case Bank’s home country; two advisors from the Parent Bank’s Strategy, Transformation, and Innovation Directorate; and three of the Organization’s corporate clients. The interviews were conducted either face-to-face (3) or online (20) and lasted between 22 and 59 minutes. The interviews were recorded and transcribed. The list of interviewees is presented in Table 1.

List of interviewees.

Secondary data obtained from two studies carried out by external research firms (commissioned by the Organization) was also used to supplement the customer perspective. The first survey was conducted in October 2019, involved 521 corporate clients, and assessed their satisfaction regarding their personal relationship with the Organization. The second study was carried out in mid-2020 to inform the re-design of Case Bank’s corporate e-bank. Besides collecting data on Europe-wide best practices in corporate e-banking solutions, it gathered user insights about these services through 16 semi-structured interviews with existing and target customers of the Organization and a survey involving 71 respondents. These secondary data were used to complement the primary interview data.

In addition, field observations were used as additional sources of information. Between August 2020 and January 2021, the first author was embedded in two of the Organization’s salient digitalization projects: the data-driven lead management initiative and the international workstream aiming to develop a digital business dashboard (DBD) for corporates. Participating in 22 online project meetings allowed the first author to collect observations recorded in the form of field notes made either during or after the meetings. All the collected data were analyzed using the Gioia methodology 45 to derive a conceptual model of digital transformation in the case firm.

Process of Digital Transformation

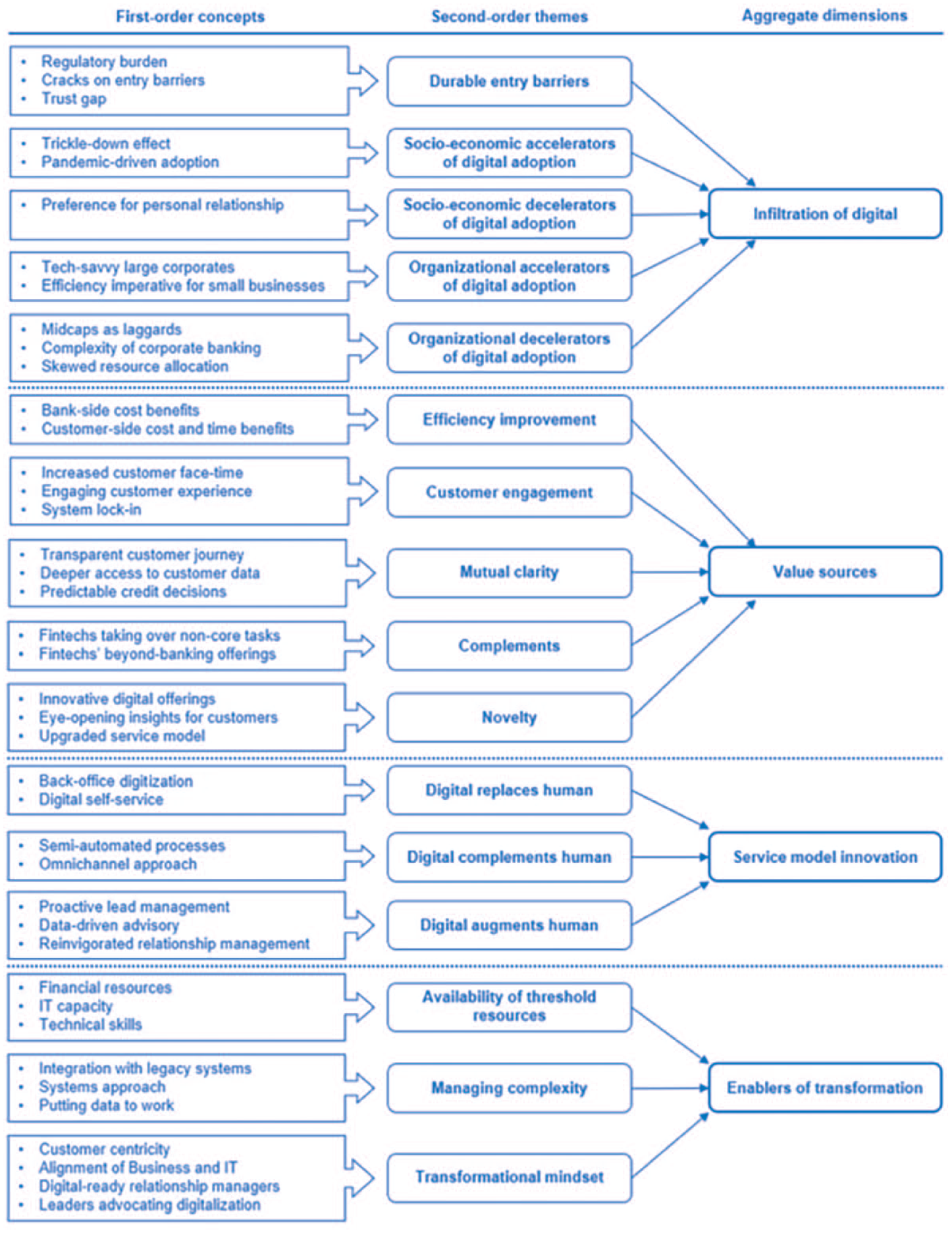

Our findings, depicted in Figure 1, reveal a process wherein, rather than a sudden transformation, digital infiltrates corporate banking step by step, triggering changes in the Organization’s relationship-oriented business model. The gist of the strategic response is spotting new value sources and engaging in service model innovation to unlock them by blurring the boundaries between physical and digital customer interfaces while relying on enablers of transformation. These findings are further elaborated in the following sections and illustrated using quotes from the interviews. The interview quotes are coded with phase and interview numbers as in Table 1, for example, phase 1, interview number 7 as 1-7.

Elements of digital transformation in the case firm.

Pre-digital Competitive Setting

To better understand the initial context, it is essential to grasp a sense of the competitive environment before the emerging digital transformation. In Case Bank’s home market, corporate banks operate in “a not very consolidated competitive environment, in the sense that there are many banks fighting for their place in the market” (1-17). “The market is competitive, especially in terms of prices and credit conditions” (1-16). Banks offering identical products “have to fight for clients. Not only do large firms have a strong bargaining position, but smaller firms can also maneuver between banks” (1-2).

The Organization pursues a relationship-oriented approach. As one informant puts it, “We have very much focused on the client experience, and . . . differentiating ourselves based on the outstanding personal bond with the client” (1-17). The positioning also builds on being perceived as an independent, professional service provider: “Our number-savvy, advisory image is an objective judgment of the market, and it is definitely our advantage” (1-6).

Differentiation advantage derives from the skilled workforce, conservative credit culture, and professional ownership background. Respondents referred to these firm resources as follows:

Differences in the skills of relationship managers make the playing field somewhat uneven. If every bank had an average of adequate human resources, competition could be even more challenging (1-16). The fact that we have a professional and conservative approach to corporate lending is part of our culture; hence it is difficult to copy (1-10). We benefit from the expertise of the group, and what it brings us in terms of the technologies and the sophistication of our commercial approach (1-15).

When reflecting on the impact of digitalization on the competitive landscape, informants consistently reported that corporate banks had made little headway with digital transformation so far. They believe that instead of creating profound and sudden disruption, digitalization is gradually infiltrating business banking:

I would not call it disruption, in the sense that it’s not something that comes from one day to the other. . . . Actually when you look at the pace at which it goes, there is very little surprise (1-15).

Infiltration of Digital

The findings suggest that no digital “big bang” is experienced, but the infiltration of digital is more gradual. The interviews revealed several factors contributing to the tempered way technology is shaping the landscape. Durable entry barriers safeguarding incumbents’ competitive position offer some explanation for the slow pace of change. The stringent and complex regulatory burden discourages potential newcomers, or as one informant noted, “We complain about regulation, but in a world like today, I am convinced that Google and Apple and Facebook are not banks yet because they don’t want to deal with this complicated mess. So, regulation is, in a sense, our friend” (1-14).

While a few cracks have appeared in the barriers allowing fintechs some access to the market, the adoption of digital substitutes has remained limited due to the gap between the trust vested in banks and fintechs. This standstill was described by one of the informants as follows: “I do not see that [corporate banks] are very active in digitalization. No start-ups have entered who would take the market, and for the banks, this status quo is a good deal” (2-4).

If not mediated by new entrants, technology can bring changes directly to the operation of corporates and banks. The data suggest that the speed and scope of the transformation are determined by opposing forces that drive or restrain digital adoption. These forces are tied to macro-level trends in terms of socio-economic accelerators and decelerators and to firm-specific features in the form of organizational accelerators and decelerators.

Socio-economic accelerators and decelerators

Digital expectations were found to trickle down from managerial levels as the firm’s decision-makers themselves experience the benefits of simple, frictionless digital offerings in their daily lives as retail customers. Subsequently, they look for similar solutions for their company to manage daily banking tasks. As one informant put it, “young, dynamic, ‘techie’ leaders put the bar higher in terms of digital expectations” (1-1). This trend was magnified as society received a digital boost during the recent coronavirus lockdown periods: “The current pandemic has very much caused customers to think that it is vital for them that the bank can handle their needs through remote digital access” (1-5).

Informants noted, however, that as a headwind to digitalization, firms have a strong preference for personal contact with their corporate banker in case of complex needs: “Trust and personal nexus are essential in corporate banking. . . . Recently, when there has been no opportunity for personal contacts, we have been less successful in client acquisitions” (1-6).

Organizational accelerators and decelerators

The informants suggested that digital adoption is related to the size of the customer firm: Tech-savvy large corporates are leading the pack, while midcaps are lagging. “Larger corporates, especially international ones, have digital protocols dictated by their parents, and we as a bank have to comply with them” (1-3). “In the midcap segment, where the organizational structure is more developed, the [credit] limits are larger, and the cooperation is more complex, digitalization expectations are sidelined for the time being” (1-16).

On the other hand, it appears that smaller businesses with resource constraints and simple, if any, dedicated financial departments are inclined to manage their financials efficiently, thereby creating some need for digital banking: “There is usually no dedicated finance manager in smaller businesses; hence, they need digital solutions so that the managing director can focus on the core business” (1-5).

Overall, client pull has prompted limited digitalization efforts from corporate banks so far. “Digital service in the corporate segment is far from advanced, but there hasn’t really been a demand for it” (1-9). This was seen to stem from a more extensive, complex, and tailored product range, compared to retail banking. Furthermore, as some informants experienced, resource allocation is skewed toward meeting compulsory regulatory requirements and projects of the retail segment where pressures for digital adoption are more immediate. However, informants saw a gradual change in client pull in the corporate banking segment as well, as “these needs are popping up” (1-9).

Technology-Enabled Value Sources

Efficiency—Efficiency emerged from the data as the principal source of value, consistently mentioned by almost all respondents. “It’s clear that the first thing you think of is efficiency, it is the first stage of our strategy” (1-15). Informants also reported that gains in the form of decreased costs and accelerated processes could be reaped by the bank and customers: “The labor-intensive services that we still have are going to be processed in an automatic straight-through way, and as such will create a lot of efficiency both on the side of the bank and also on the side of the client” (1-17).

Customer Engagement—Interviews and observations pointed to three particular ways the Organization intends to strengthen the bond with customers to decrease the probability of switching to a competitor. First, with the introduction of the DBD, Case Bank aims to win the battle for customers’ digital face time. Second, there is a well-articulated intention to provide a superior customer experience aided by technology: “I think this is where the win-win of best client experience comes from. I mean, you provide a win to the clients by delighting them, . . . and consequently, the clients will be loyal, . . . the clients will want to do more things with you” (1-17). Third, building digital interfaces via machine-to-machine or multi-banking solutions is expected to result in system lock-in that can considerably increase switching costs.

Mutual clarity—Informants emphasized that streamlined digital processes combined with dashboard-like solutions can improve the transparency of the customer journey, thereby easing clients’ frustration from not being able to follow up on the progress of their requests: “Treasurers will be able to see everything on their own, and they will get the information very quickly. . . . For them, the greatest added value is to have an overall picture of the company’s financial state and an immediate overview of their most important banking matters” (1-11). Another aspect of clarity noted by the informants is that gaining automatic access to deeper layers of customer data contributes to a better understanding of corporates’ financial standing and business operations, which can make credit decisions more transparent and predictable. This is also something that the clients expect: “I think the decision points should be clear so that I can be sure, that if I have an open book with my bank, and my company fulfills certain conditions and the bank sees it transparently, I will get that extra credit almost automatically” (2-4).

Complements—Digital complements, such as e-invoicing, cash flow forecasting tools, and working capital management applications, enhance the value of traditional banking products. The design of the DBD was seen to facilitate adding such beyond-banking services. An external stakeholder further highlighted that third parties could also support corporate banks by taking over non-core, low-value-adding tasks, thus easing the administrative burden: “Fintechs can support banks in back-office digitalization, Know Your Customer tasks, and with chatbots” (2-1).

Novelty—The Organization intends to explore digital innovation along three main themes: creating novel customer-facing channels, improving the content of advice provided, and deploying a new service model. First, developing the unique, customizable dashboard that can serve as a landing platform for the planned digital assistant and the lead management engine is a salient example of new approaches to digital interaction with customers. “What could be a differentiator is offering the Parent Bank’s innovative, AI-powered, digital assistant for the corporates over time” (2-2).

Second, there is a clear intention to exploit proprietary data by supporting clients with customized insights that go beyond information related to core banking products. The client informants confirmed the potential value of such insights: “I would even pay for tailored analyses, cash flow forecasts, or comparative industrial benchmarks derived from the bank’s information to help me make decisions” (2-5).

Finally, an upgraded service model will embrace these innovative directions. “It will not be enough to have a human connection in the future. We will have to continue to upgrade our service model with convenience, with speed, with digital solutions that not only make the life of the client easy, but make them feel that we are on the top of the game” (1-17).

Service Model Innovation

Informants revealed that the renewed value path is envisioned as a blend of interactions via physical and digital channels. “Until artificial intelligence replaces owners and CEOs, personal contact has a place in corporate banking. However, digitalization will step by step carve out a growing slice of this relationship cake” (1-3). “In business banking, the human factor, the physical service, the personal bond with our clients will remain crucial . . . but it will be more and more supported by digital innovation” (1-17).

The service model innovation process encompasses three themes distinguished by the density of personal and digital interactions, leading to a blended service model. First, digital replaces human in simple, daily routine tasks, where manual intervention adds little value. “We will have to provide all the basic services digital, where the relationship manager has no added value other than collecting the papers” (1-18). “The back-office part, where the ugly things happen, is masked from the client. However, it is energy-consuming to operate this manually. Digitization needs to start there to make the biggest impact” (1-1).

Beyond automating back-office processes that are less visible to customers, this approach also covers digital self-service that allows customers to directly manage their basic transactions and administrative tasks without the involvement of the bank’s representative. It was observed that Case Bank systematically mapped its corporate customer support services and identified those that can be transformed into self-service functionalities of the DBD under development.

Second, digital complements human in more complex processes and as an additional channel of interaction. In semi-automated processes, humans would stay in the driver’s seat as they make credit decisions or negotiate with clients but could be assisted by descriptive analysis that collects, processes, and visualizes information in the preparatory phase. “80-90% of the work that is still today done manually can at some point be automated, . . . but the local knowledge still is a factor because sometimes these decisions hinge on other soft things you see when you visit the clients” (1-14). “Banks have started to realize that digital is not only a channel, but it can support the relationship manager in the form of a dashboard that provides a 360-degree overview of the customer” (2-1).

It was also noted that by introducing DBD, the Organization aims to supplement the relationship manager with an online touchpoint, reflecting a shift from a single point of contact toward an omnichannel approach. “DBD will be like the mobile app in retail: the digital interaction portal between the client and the bank” (1-17). “It will make digital applications easily accessible while creating a transparent, customizable workspace for customers” (1-9).

Third, at the most sophisticated stage, digital augments human. This augmentation builds on leveraging advanced technology, such as artificial intelligence, to improve the timing and content of sales efforts and the added value of personal advisory, thereby repositioning the relationship managers’ role. One informant illustrated it with a metaphor: “I can compare it to Formula 1, where cutting-edge technology works under well-skilled drivers to reach their goals in the elite league of motorsport” (2-1).

Observations concerning the Organization’s lead management project indicate that the backbone of this approach is the exploitation of proprietary customer data and contextual information with the help of predictive and prescriptive, rather than purely descriptive, analytical methods. In the case of proactive lead management, it boils down to detecting or even predicting the financial needs of corporate customers and satisfying them with relevant and timely product offers. “We should look around what is available outside of that individual experience of the corporate banker. What is available in the sector, in internal and external databases, and how we can use that to provide insights and assistance for the clients to do their business better” (1-17). Data-driven digital processes are also used to allocate tasks and commercial leads to the most appropriate employees based on skills, availability, and performance.

The Organization uses AI to generate customer insights and spot triggers that indicate particular types of customer needs. In simple cases, digital journeys where digital replaces human are created, and in the case of slightly more complex needs, digital is used to complement human by sending a commercial signal to the most appropriate employee to deal with the client. However, the most unique and sophisticated client processes are driven by digitally augmented humans, with customer insights empowering relationship managers to be better equipped when responding to client needs. “Digital client journeys are created for simple offers, while augmented humans conclude complex deals” (2-2).

Informants believed that digitalization could reinvigorate relationship management so that corporate bankers would be able to engage in more complex, meaningful deals and advisory-type conversations with customers. “If there will be a game-changing event, what we call a moment of truth, for instance an acquisition or a merger and the CEO or CFO wants to discuss it with a bank, then . . . we should be helped by technology to give much better advice than we have ever been able in the past” (2-2). “In a future bank-corporate relationship, a high value-adding personal relationship must be built on the digital foundation” (1-18). Digital augmenting human is seen as a central building block for competitive advantage in the future: “In the endgame, data-based algorithms steer and support the organization” (2-2).

Enablers of Transformation

Respondents also highlighted the importance of execution capability to successfully architect the envisaged blended service model. “Strategic visioning is there, maybe the directions we have come up with are good, but we need to be able to execute. . . . And for that, we need to build the necessary competencies, expertise, and routine” (1-16). The informants noted several enablers that were seen as crucial for successfully executing the digital transformation. First, threshold resources are the fundamental assets required to embark on digital projects, including financial resources, IT capacity, and relevant technical skills. The scarcity of IT capacity and shortcomings in essential technical skills (such as business acumen, project management, and IT development) can hinder execution even if funding is ensured. “Sometimes despite the availability of a budget, the project does not progress in the absence of IT capacity” (1-7).

The informants emphasized that the scale and speed of digitalization are also determined by the Organization’s ability to manage complexity. “We gave priority to four flagship projects because there is only so much complexity that we can manage” (1-15). The interviewees repeatedly expressed the importance of a systems approach that considers both the constraints of existing systems and the way ongoing and future digital developments can intertwine. “In the early phase of the digital dashboard project, the project team identified 17 legacy systems and 4 dependent projects that need to be taken into account when designing a minimum viable product” (First author’s field notes).

Respondents added that corporate banks are often envied for possessing a massive amount of unique customer data. However, putting the data to work is not a straightforward exercise, as the bulk of the information is unstructured and stored in fragmented data sources. Leveraging data requires that they are aggregated, analyzed, and subsequently translated into relevant insights. This is, at times, still a bottleneck: “We all see today it is a human-based decision, you need to know your client. . . . However, this is just because it is still today unstructured data, and we haven’t found a way of structuring that” (1-15).

The interviews also revealed that an overarching transformational mindset is fundamental to navigating digital transformation successfully. “Banks transforming systematically and adopting a digital mindset pervading the whole organization will excel, while those who look at digitalization as a bunch of imposed IT projects will lag” (2-2).

The case indicates that such a mindset is rooted in customer centricity, which has long been a pillar of Case Bank’s strategy. The attitude of “serving customers in the best possible way” (1-17) requires that customer needs and pain points are sensed in the front office and translated into digital initiatives that can be developed by IT. However, observations suggest that cross-functional cooperation can easily become cumbersome if different functions cannot understand each other’s drivers and logic but stick to the specific interests of their silos: “Even after many years spent with projects, communication between various functions is not clear enough to have the same understanding. . . . You say a sentence, and it is understood one way by IT and a completely different way by Business” (1-12).

Informants added that digital upskilling of salespeople is a vital ingredient, allowing them to deliver novel services to corporates and use data-enabled insights to strengthen the advisory-based bond. Finally, the cultural shift must be fostered by leaders ready to champion the transition to digital, raising consciousness about it and mobilizing the whole Organization toward the new service model. “I would call it modern leadership. You need that leadership talent of people who want to build a [digital] story, communicate it, and carry the entire organization into the belief and transformation of the behavior” (1-15).

Toward a Blended Service Model

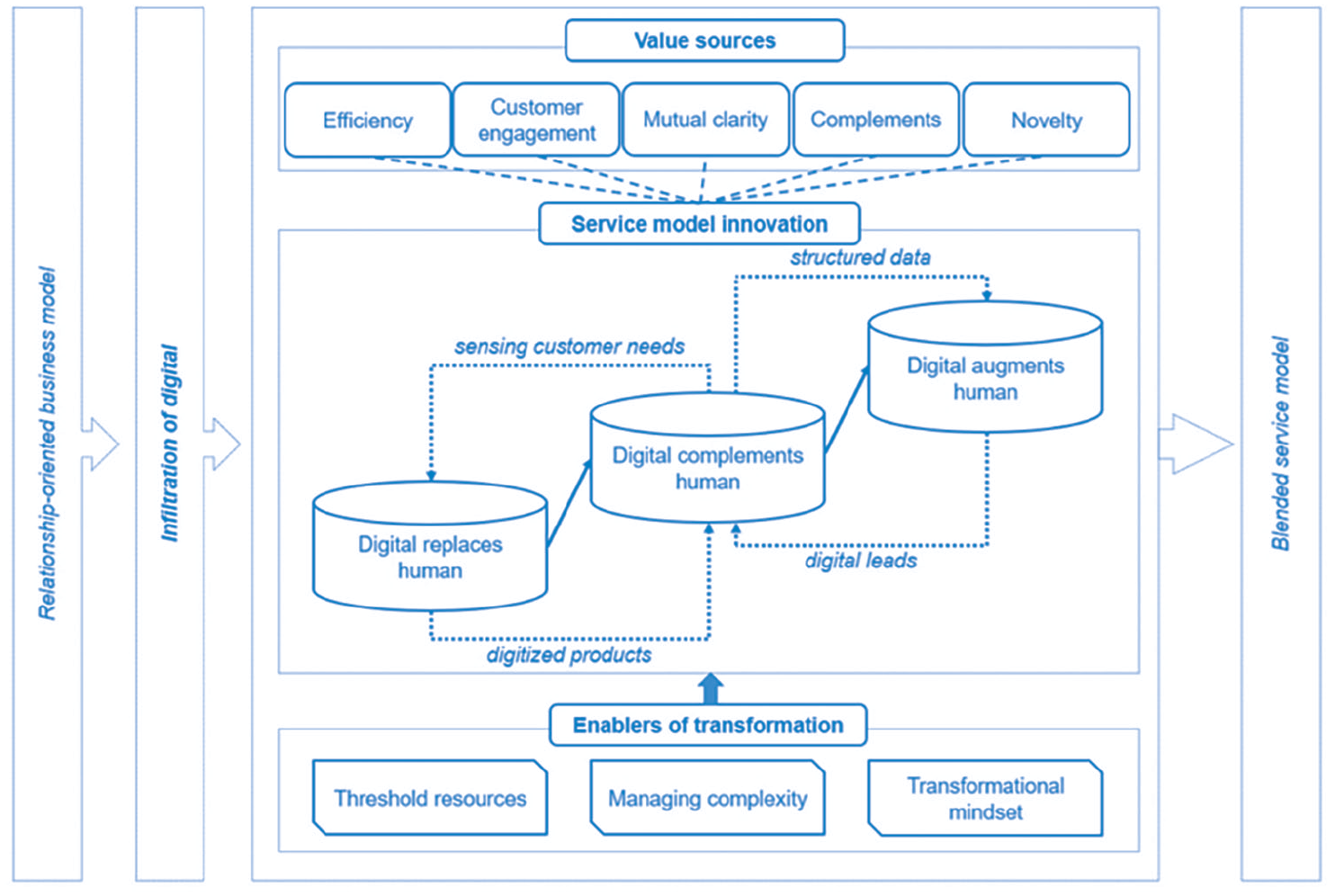

The thematic dimensions discussed earlier describe the influencing factors and main components of the Organization’s planned digital journey. However, it is equally important to understand the interactions and connections between them. Figure 2 depicts the process of responding to the sensed digital trends by altering the relationship-oriented approach and moving toward a blended service model, as suggested by the interview data.

Building blocks of a blended service model.

As Figure 2 shows, the relationship-oriented business model can be transformed incrementally through the infiltration of digital, following the order depicted in the center of the figure. Our findings suggest that an incumbent may move from simple digital developments to more comprehensive ones step by step, following a path from “digital replacing human” through “digital complementing human” to “digital augmenting human.” “We digitize basic transactions, payments, and the administrative stuff first. . . . Then we are moving into the more sophisticated customer experience. . . . There is this gradual stepping up the ladder regarding where we go in terms of complexity” (1-15).

There are three important features of this roadmap. First, the stages are closely interrelated, and the linkages between them define the trajectory. Digitized products where digital replaces human are a prerequisite for the platform where digital complements human: “To have a DBD, we need to have self-service functions first that we can add to it; hence, we need to get to a certain level in the first pillar. The relationship between the two cannot be reversed” (1-18). On the other hand, the omnichannel approach where digital complements human will have an essential role in sensing client needs and behavior that can trigger further digitized products. “It can help us know more about our customers’ needs, and thus we could sharpen the direction of future developments” (1-9).

Moving further in the roadmap, informants noted the importance of DBD and the processes where digital complements human in structuring customer data, which is essential for data-driven solutions where digital augments human. “We have numerous applications and e-channels, which boils down to unstructured, scattered information about our clients. We aim to address this with our integrated dashboard” (1-12). On the other hand, the processes where digital augments human feed digital leads back to the DBD platform, which was again seen as a necessary condition for the more advanced stage to be viable in the first place. “By the time [lead management] will go live, we will need a platform that digital leads can land on. Therefore, it is a prerequisite to have a well-functioning dashboard” (1-18).

Second, threshold resources provide the foundation, and the higher-level enablers of complexity management and transformational mindset gradually kick in as the digital journey progresses. As the transformation moves toward more sophisticated stages, there is more complexity to manage, and the transformational mindset becomes increasingly crucial as the significance of the human factor increases. While we found that digital solutions that replace manual, repetitive, administrative tasks are easy to adopt, omnichannel journeys where clients may switch back and forth between digital and human interactions require bankers who understand how to use digital tools effectively. The most challenging part was found to be the effective utilization of data to digitally augment human, as this requires that bankers trust the model that defines digital insights, that the delivery of the digital insights is well orchestrated, and that the digital insight provided to the physical channel is effectively applied. The most crucial enablers thus change from resources to management to mindset as the firm advances on the roadmap.

Third, certain value sources seem to gravitate to specific phases of the cycle. Efficiency gains were most often mentioned in connection with replacing manual processes with digital ones. Digitized products and novel digital channels were considered to engage customers via convenience and system lock-in. As digital will gradually complement the human interface, clarity is expected to improve thanks to semi-automated decisions and processes managed on digital platforms. The DBD was seen as essential for capturing the value of complements through its planned connectivity to third-party applications. Finally, the augmented human approach is expected to involve the most radical and novel innovations.

Implications for Digital Transformation and Competitive Advantage

While the right way of combining digital with human has long been seen as a key characteristic of successful service models in the digital future, for example, in the “digital first” school of thought, 46 what has generally received less attention is the process of how incumbent service firms can get there. Our findings suggest that the digital transformation process should not only be gradual and conducted in small, manageable steps but also give important insight into the roadmap that this process should follow. Specifically, the process model depicted in Figure 2 can point incumbent service firms to the necessary building blocks of different stages of the digital transformation process in terms of the types of service innovation to pursue, the most important enablers of transformation, and potential value sources that can be expected to be the most salient in different stages of the transformation process.

Our findings further help to establish important links between digital transformation and competitive advantage. As an informant suggested, “the essence of competition will not change. The question is how corporate banks can amplify their strength via digital” (2-1). In this regard, the three elements of the blended service model—digital replaces human, digital complements human, and digital augments human—were found to have different implications for the sustainability of the associated competitive advantages. 47

Replacing daily, routine human tasks with their digital counterparts emerges from the analysis as a threshold capability. “Basic self-service, basic products via digital . . . will be a minimum expectation to be able to start the game” (1-18). Digital technologies by themselves exhibit low barriers to entry 48 and require only moderate organizational efforts to implement, and thus are likely to become commodities. As one informant concluded, “This is not so much about gaining a competitive advantage but avoiding the disadvantage” (1-3). Routine tasks where digital replaces human can therefore, at most, be a source of competitive parity.

In applications where digital complements human, the Organization strives for a sequence of first-mover advantages by deploying the DBD as an innovation platform. According to the business concept, “DBD is expected to bolster new product launches by decreasing development costs and accelerating time-to-market of innovative products and services” (Case Firm documents). However, even if successful, the associated advantages are anticipated to be temporary because of the imitability of the products. “Whoever can digitize faster is sure to gain some competitive edge . . . for a while until others catch up, and it will be a must afterward” (1-5). “These digital products can now be copied quickly, especially if you develop them in an agile organization” (1-7). These findings echo the arguments that the rewards of pioneering digital changes are not necessarily enduring 49 and suggest that approaches where digital complements human can provide, at best, a temporary competitive advantage.

In contrast, approaches where digital augments human arose in the findings as potential sources of sustainable competitive advantage. Two resource-based arguments support this implication. First, unstructured information was found to be a roadblock on the way toward making sense of data. Therefore, leveraging data could be the privilege of business banks that can cross this barrier by connecting the dots within their complex systems. Second, adopting a transformational mindset arose from the interviews as a prerequisite and a key challenge of reaching the most advanced phases of digital transformation where digital augments human. However, once a culture that integrates human and digital becomes a part of the “unspoken, unperceived common sense of the firm,” 50 it is also difficult to imitate. Thus, if corporate banks are able to combine their traditional resources of skilled employees and proprietary data with digital capabilities to support their clientele with data-driven, personalized services, this can provide a sustainable advantage. The consequent improvement of the business relationship results in even more customer data, further strengthening the resource position barriers 51 and increasing the durability of competitive advantage.

Managerial Recommendations

Four specific suggestions stem from the findings, which can be instrumental for managers in incumbent service firms to successfully guide their organizations through a digital transformation.

Define a digital roadmap—Although sporadic digital initiatives may have a viable stand-alone business case, launching them in an uncoordinated manner carries the risk of disregarding the logical dependencies between the different kinds of initiatives and thus limiting the benefits gained. Moreover, adding new elements to the already opaque banking systems generates more complexity, decreasing the understandability of the system and potentially leading to unmanageability. 52 Such pitfalls could be avoided with a comprehensive digital business strategy, including a roadmap that guides and connects digital initiatives. Such a digital roadmap should consider the firm’s target market, existing resources and capabilities, and how much the intended service model is skewed toward high tech versus high touch. Based on this, the roadmap should mark out which stage of service model innovation will be crucial (are the benefits to be gained from replacing, complementing, or augmenting human with digital), articulate the most important resources needed, and outline the main intended value sources. For example, a professional service provider targeting the largest companies with bespoke services would likely create and capture the most value by focusing on augmenting human, whereas a firm offering standard services to a wider clientele might want to focus on efficiency gains by replacing human with digital.

Be lean—Even though you should have an overall digital roadmap, it is important to not try to do everything at once. While, in the long term, digitalization is inherently disruptive, 53 our findings indicate that its organizational impact can be more gradual. This is in line with arguments that established firms pursuing a future-proof business model should opt for a piecemeal digital transformation. 54 Although digital trends can fundamentally transform entire industries, our findings suggest that responding to such trends is best done gradually, rather than attempting to implement a sudden and disruptive transformation. Adopting tools from the “lean startup” methodology, 55 such as taking small, calculated risks by launching several “minimum viable product” (MVP)-type digital initiatives of limited scope and adjusting based on the associated customer feedback, is generally better than attempting to transform the entire service model in one go.

Be receptive to a broad range of value sources—Not all sources of value from digital transformation can be directly translated into monetary terms, and decision-making should incorporate the strategic, less quantifiable aspects as well when evaluating digital initiatives. To complement the more well-known value sources from digital transformation, including efficiency improvements, 56 customer engagement, 57 complements, 58 and novelty, 59 we identify mutual clarity and transparency as an additional value source that has thus far received little scholarly attention. Transparency alleviates uncertainty, for example, by increasing the feeling of progress when queuing 60 and making customers less sensitive to their wait time. 61 It further helps customers to better understand and appreciate the work done on their behalf, 62 which can increase the perceived value of the service, customer satisfaction, willingness to pay, and loyalty. 63 Transparency also helps in building trust, 64 which is a vital value creation ingredient in relationship-based service industries such as corporate banking. 65 The finding that digitalization helps unlock the value of mutual clarity also appears to be transferable to other industries. Providing online delivery updates based on carrier information and allowing customers to track and trace the full path of the order has become a standard operating model in B2C services. Similar requirements are trickling into B2B markets where the stakes and the value of predictability are even higher, and businesses are becoming less tolerant of non-transparent processes. Our findings suggest that firms looking to benefit from digitalization should consider the transparency that digital technologies allow as a potentially important source of value creation.

Know where your competitive advantage lies—Once there is a better view of the potential sources of competitive advantage, decisions on how to develop digital capabilities can be better underpinned. Involving external developers or considering partnerships with fintechs might be valid choices for an incumbent in the case of fully automated solutions that are expected to be copied and are therefore unlikely sources of long-term competitive advantage. On the other hand, data-driven solutions considered central to the augmented human approach are best developed in-house to protect the capabilities contributing to sustainable competitive advantage. Understanding when to build, when to buy, and when to partner helps optimize scarce internal development capacity. In particular, the finding that digitization of daily banking services offers little if any potential for achieving competitive advantage might foster cooperation between fintechs and incumbents. While fintechs struggle to cross the trust gap and reach scale, established banks fight against complexity and face the imperative of allocating scarce resources to projects that most probably will not lead to competitive advantage. This setting should motivate fintechs to reposition themselves from substitutes to complementors and encourage incumbent banks to consider fintechs as potential partners in daily banking services, with incumbents aiming to gain their competitive advantage from more advanced digital applications that augment their human processes.

A final practical observation of note is that we found surprisingly little opposition to digital transformation in any management layer within the Organization. In fact, all interviewed stakeholders considered digital transformation as an imperative, being essential to improve or even maintain competitiveness. Thus, while implementing the blended service model entails a lot of practical complexity and, as a change process, requires special management attention, 66 the importance of digital transformation appears to be sufficiently well established in the industry to not require any active management of cognitive inertia and resistance within the firm.

In conclusion, the model of blended service innovation presented in this study can help us understand digital transformation and its repercussions on competitive advantage in the context of professional B2B service providers. Being based on a single-case study, our findings only highlight one potential model of digital transformation, and the process may need to be adjusted based on contextual factors such as the size of the firm, its current level of digital competence, or the industry environment it is facing. However, the findings suggest that the dynamics between relationship-oriented firms and the increasingly digital environment warrant further managerial and scholarly attention to maximize the positive impact of digital advancements and to realize their potential for generating competitive advantage.

Footnotes

Notes

Author Biographies

Gergely Lóska is General Manager at KBC Group and has a 20-year career in corporate banking (email:

Juha Uotila is Associate Professor of Strategic Management at Warwick Business School, University of Warwick (email: