Abstract

A perennial challenge for executives in established firms is deciding how and when to respond to emerging technologies. This article demonstrates that the way emerging technologies play out in established industries differs according to how the business system is affected. Some have primarily a supply-side effect (on how a firm in the industry creates its product), while others have a primarily demand-side effect (on how users consume the product). Supply-side effects play out over relatively long periods of time in a predictable way, with incumbent firms executing similar strategies though at different speeds. Demand-side effects are faster-acting and more volatile, with incumbents often experimenting with a range of different business models as they seek a viable way forward in a changing market. By understanding these important differences between supply-side and demand-side effects and being able to anticipate the typical patterns of responses from incumbents, executives can make better choices in how and when to invest in emerging technologies.

Keywords

A perennial challenge for executives in established firms is deciding how and when to respond to emerging technologies. The stories of firms that were slow to embrace emerging technologies are well known (e.g., Kodak and Blockbuster), but there are also plentiful examples of firms that moved too quickly and incurred large losses (e.g., GM’s EV1 electric car and Time Warner’s merger with AOL). It is very easy for firms to get such decisions wrong because of the inherent uncertainty around any emerging technology, for example, in terms of how quickly it is developing, how it might be commercialized, and its impact on existing products.

Academic research has provided many useful insights into the dynamics of technological change by showing how technologies evolve in relatively predictable ways and by highlighting the different effects new technologies have on incumbent firms. Studies have identified many of the contextual factors that facilitate or impede the rise of new technologies and the importance of the wider business ecosystem on the speed of adoption. 1 Such research does not resolve the fundamental uncertainty with emerging technologies, but, by documenting what has happened in previous situations in a structured way, it helps executives to make better-informed judgments.

This article is written in the same vein, with the intention of providing new insight into the dynamics of technological change and helping improve executive decision making. Building on the distinction in the academic literature between supply-side and demand-side mechanisms, 2 this article argues that the way emerging technologies play out in established industries differs according to the part of the business system affected. Some have a primarily supply-side effect (on how a firm in the industry creates its product), while others have a primarily demand-side effect (on how users consume the product). Supply-side effects play out over relatively long periods of time in a predictable way, with incumbent firms executing similar strategies though at different speeds. Demand-side effects are faster-acting and more volatile, with incumbents often experimenting with a range of different business models as they seek a viable way forward in a changing market.

By understanding these important differences between supply-side and demand-side effects, and the typical patterns of responses from incumbents, executives can potentially make better choices themselves in how and when they invest in emerging technologies. Of course, many technologies are likely to affect both supply and demand sides. For example, in photography, digital technology had a supply-side effect (photosensor chips making silver-halide film obsolete), and then a few years later, it had a demand-side effect (with users sharing their pictures on Instagram rather than printing them and putting them in albums). In such cases, it is useful to analyze the effects separately to help diagnose the appropriate courses of action. It is also useful to consider how supply-side effects may subsequently lead to demand-side changes, and vice versa.

The article is based on a detailed historical analysis of 58 incumbent firms in 6 industries. The research question was how do incumbent firms respond to an emerging technology over time. To simplify and clarify the exposition, the “Findings” section focuses mostly on two industries (big pharma/biotech for the supply side and film studios/digital streaming for the demand side), with insights and evidence brought in from the other industries as appropriate.

Theoretical Background

There is a vast body of research seeking to understand the impact of new technologies on established industries. The classic view is that industries go through a series of “S-curve” transitions, with a new technology sparking a period of ferment that ends with the emergence of a dominant design, followed by a period of relative stability and an emphasis on process rather than product innovation. According to this view, new technologies are typically introduced by startups or firms moving in from adjacent industries, creating challenges for incumbent firms who suffer from various sources of rigidity that hamper their ability to adapt. 3 However, it is also recognized that the firm pioneering a new technology is often not the one that successfully commercializes it, as the process of bringing it to market involves deploying an array of complementary assets, many of which are typically held by incumbents. 4

This pattern of change is instantly recognizable to most observers, but the reality is that emerging technologies affect existing industries in a variety of different ways, depending on their characteristics. For example, book retailing went through a period of revolutionary change in the late 1990s with the advent of Internet technology, resulting in a shake-out of the traditional incumbents as theory would predict. However, retail banking did not suffer the same fate, and incumbent banks were able to sustain their dominant positions in most parts of the world by incorporating Internet-based services alongside branch and telephone-based services.

While these divergent outcomes for books and banking seem self-evident today, they were far from clear at the time (in 1996, a leading observer said the Internet would “tear apart banking as we now know it and create an entirely new financial system 5 ”). This is because emerging technologies are inherently uncertain—we do not know if they will become technically feasible or whether users will embrace them, and we do not know what complementary technologies will be needed to make them commercially viable. The characteristics of a given technology (e.g., disruptive vs. sustaining 6 ) are clear in retrospect but highly uncertain at the time decisions are made.

To help reduce the inherent uncertainty incumbent firms face when deciding how to respond to an emerging technology, this article draws a distinction between supply-side effects (technology changing the way a product or service is created) and demand-side effects (technology changing the way a product or service is consumed). Consider two current examples. Internet of Things technology appears to have primarily a supply-side effect on the mining and construction industry, as it enables equipment to operate in more efficient and effective ways. Virtual Reality technology appears to have a demand-side effect on firms in the entertainment and education sectors, as users start engaging with their products in new ways.

This argument builds on Joshua Gans’s research on disruption, 7 where he distinguished between a demand-side mechanism where “established firms can be blindside by certain types of innovations that change what products their customers want,” and a supply-side mechanism whereby “for certain innovations, successful incumbents may not be able to make the organizational changes necessary to compete with new entrants.” This is a useful distinction to make, but it also applies to all emerging technologies, whether or not they end up being disruptive. 8 As already noted, some emerging technologies end up having relatively benign effects on incumbents, while others have more serious consequences. It is important for executives to have this full range of possible outcomes in mind when they are deciding what to do.

There are two linked choices required by incumbent firms when considering an emerging technology (regardless of whether it affects the supply side or demand side). The first is when to act. A sizable academic literature has grown up around the concept of first-mover advantage, examining the benefits and risks in being the first player to bring a new technology to market. There are also studies arguing for a slower approach whereby the incumbent firm holds off, perhaps making small-scale bets to build its understanding, and then positioning itself for a rapid scale-up when the timing is right. 9

The second choice for the incumbent is what to do. Many options have been explored in the literature, for example, investing in the technology head-on and cannibalizing existing lines of business, often through the creation of a separate unit; doubling down on existing areas of strength; lobbying regulators to restrict the adoption of the new technology; taking out the new competitors through “killer acquisitions”; and so forth. There are also choices to be made about how to execute the chosen strategy, for example, internal investment, acquisition, or alliance. On both these dimensions, there are many factors influencing the decision. 10

These choices vary depending on whether the emerging technology’s effect is on the supply side or demand side. In terms of when to act, it involves the timing of response for all incumbents and the mix of early movers and late movers in each industry. In terms of what to do, there are three generic options: fight back directly (in the new market space opened up by the technology), double down and retrench (within an existing market space), or move away (into new or unthreatened market space). 11 There are also practical steps incumbents use, such as engaging in acquisitions or alliances to get access to the new technology.

Consistent with existing literature, the term “emerging technology” refers to any technology that is developing quickly, has the potential to have a significant impact on existing industries, and presents considerable ambiguity over how it will play out over time. 12 As noted already, such technologies are potentially disruptive even though they often end up having a relatively small or non-disruptive impact on existing industries.

Research Methodology

To gain a broad understanding of the responses of incumbent firms to emerging technologies over time, data were collected on six industries from 1990 to 2020. For each industry, a specific emerging technology was identified, and the decisions made by a cohort of leading firms vis-à-vis that technology over the 30-year period were mapped. This cohort-based analysis, starting with the firms that were industry leaders before the new technology emerged, helped avoid the risk of sampling on the dependent variable.

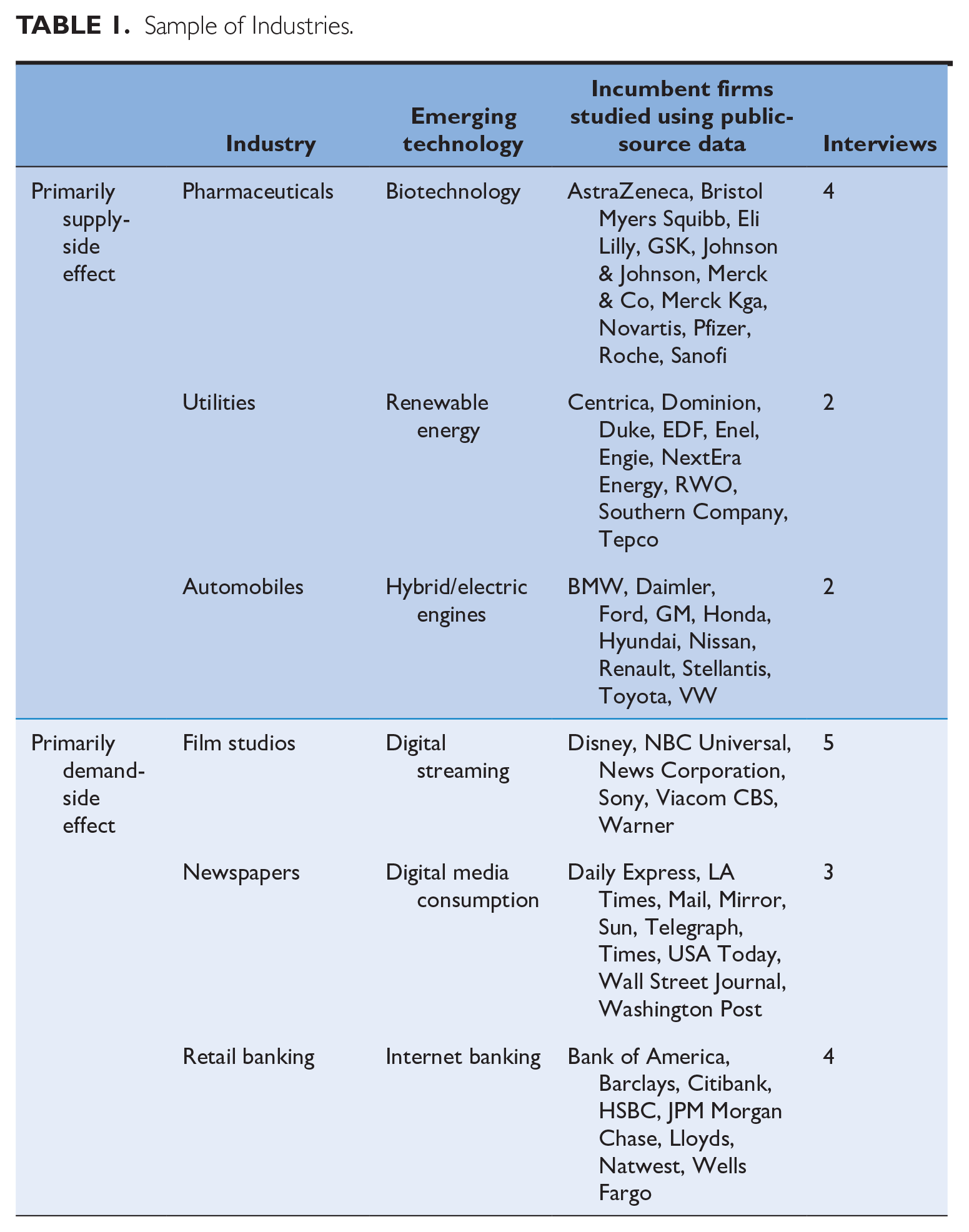

The choice of industries was to some degree based on having access to public-source data, which meant a bias toward well-known industries and a strong presence in North America and Europe. The industry-technology pairing also had to fit within the 1990-2020 timeframe to make comparison easier. Consistent with the research focus, industries were chosen with a mix of demand-side and supply-side effects. These criteria led to the six industries, as summarized in Table 1.

Sample of Industries.

For each industry, a timeline around the emergence of the technology was put together, which typically meant going back to the mid-1980s even though the “action” in terms of firm responses mostly began in the mid-1990s. The top firms in each industry in 1990 were identified, and their strategic moves were followed for a 30-year period until 2020. The selection of firms was based on the Fortune 500 and Global 500 ranking lists, though, in some cases, U.S. and U.K. firms were favored to make data collection more straightforward. A research assistant was employed to write a detailed case history of each firm, focusing especially on their responses to the emerging technologies in question. These accounts were then analyzed, looking first for patterns within industries, and then for common themes across industries. In addition, we (several researchers and I) interviewed 20 senior executives who worked in these industries to shed light on their internal deliberations and to help us make sense of our emerging insights.

While our analysis centers on the distinction between supply-side and demand-side effects, some industries experience both effects to some degree—notably automotive (mostly supply side, a bit of demand side) and retail banking (mostly demand side, a bit of supply side). As explained in the Appendix, there are several limitations in terms of firms and industries studied and data availability. Our intention was to illustrate and elaborate on a conceptual argument (about the distinction between supply-side and demand-side effects) and to develop propositions that might be tested in future studies.

Findings

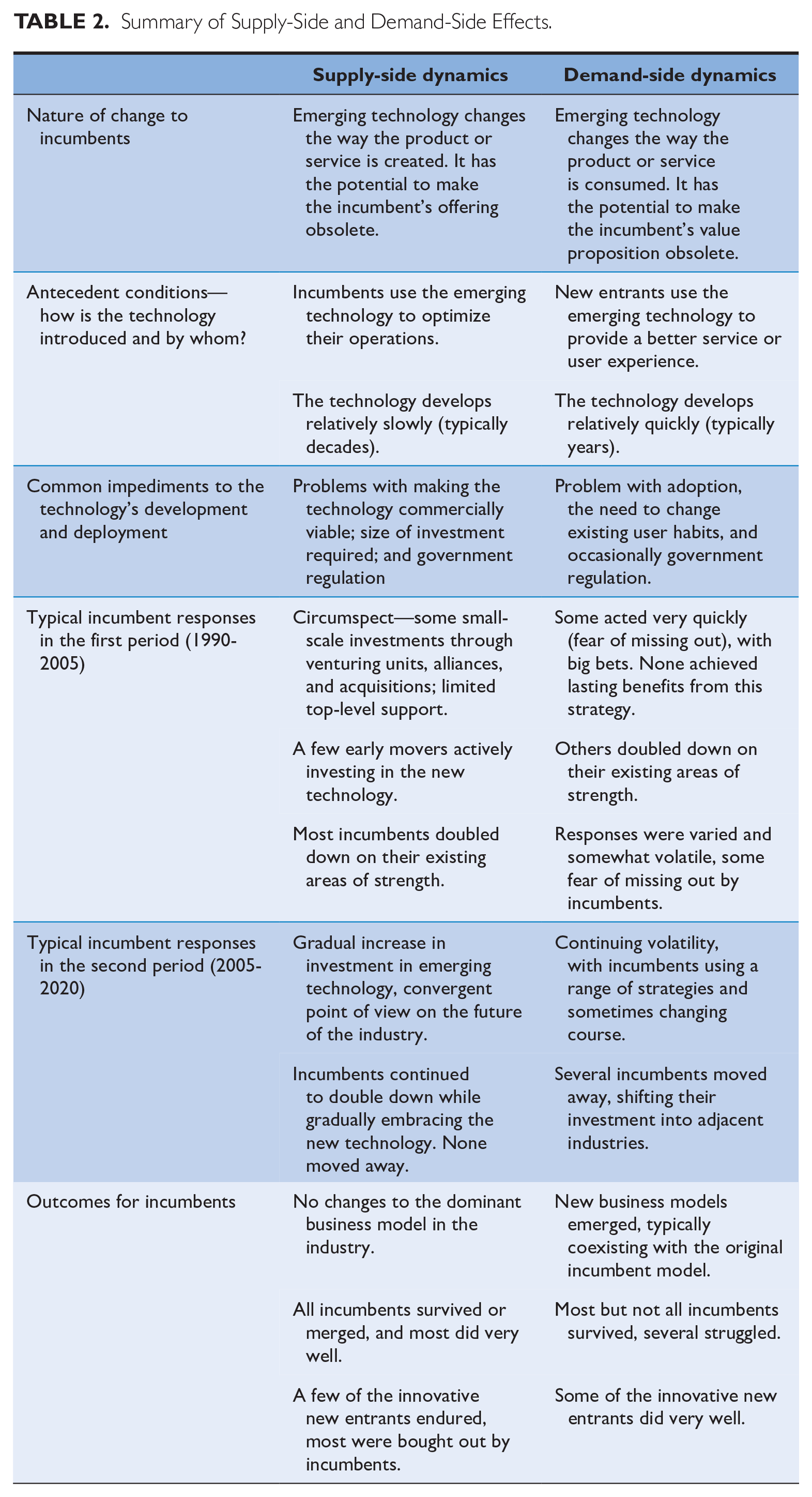

The findings are structured as follows. We look first at supply-side effects—the antecedent conditions that led to the introduction of the emerging technology, the responses of incumbents, and the outcomes. We do a deep dive into one industry (the response of big pharma to the biotechnology revolution), and we then look at common themes across the three industries (pharmaceuticals, automotive, and utilities). Then we consider demand-side effects in a similar way, looking in detail at how film studios responded to digital streaming before considering the common themes across the three industries (film studios, newspapers, and retail banks). The findings are summarized in Table 2. Finally, we summarize the key points of difference between the supply-side and demand-side effects, and we look at the ways in which the two effects interact with one another.

Summary of Supply-Side and Demand-Side Effects.

Supply-Side Effect: How Big Pharma Responded to the Biotechnology Revolution

Modern biotechnology is usually traced back to breakthroughs in gene splicing in the 1970s, which made it possible to scale up natural products made in the body, such as Insulin. The first biotech firms, including Genentech and Amgen, gained venture capital funding in the 1980s. Big pharma firms (including Eli Lilly, Merck, and Roche) began making small-scale investments in biotechnology during the 1980s and early 1990s. 13

Progress was slow, and by the late 1990s, the biotechnology revolution was characterized as “long on promise and short on profitable drugs. 14 ” In 2000, the biotech bubble burst and investment in the industry was reduced. But research continued and eventually—starting around 2010—a stream of so-called “biologic” drugs was being approved for use, notably those based on monoclonal antibody (MAB) technology. Some of these became big successes: by 2020, eight of the top ten drugs in the world are biologics. 15

The field of biotechnology has several important characteristics, evident even in the early days of its development. The technology is complex and uncertain, with many subfields (MABs, gene therapy, peptides, and mRNA) developing at different speeds. Regulatory oversight is strong, with new drugs taking at least a decade to work their way through development and clinical trials. The capital investment requirements are high. It is therefore not surprising that biotechnology took a long time to realize its potential.

How did the incumbent big pharma firms respond? Most of the 12 firms were cautious in their embrace of biotechnology through the first wave, which ended with the 2000 market crash. They all undertook R&D alliances with biotech firms, and several made corporate venturing investments, but compared with the size of their overall R&D budgets, these were small sums of money. 16

The two exceptions were Eli Lilly, who bought Hybritech for $350 million in 1986, and Roche, who bought a controlling stake in Genentech for $2.1 billion in 1990. Eli Lilly’s move was a failure (Hybritech was unloaded for $10 million in 1996), while Roche’s was a success (its three best-selling drugs in the 2010s all came from Genentech), the point being that big early moves such as these tend to be very risky.

Alongside their small-scale R&D investments, most big pharma firms doubled down on their core activities, with continued investment in their chemistry-based R&D but also with a greater emphasis on their downstream activities in global distribution, marketing, and sales. Pfizer rose to prominence in this period through marketing prowess more than through science (with blockbuster drugs Lipitor and Viagra). 17 Several of the biggest players, including Pfizer, AstraZeneca, Novartis, and BMS, showed very little interest in biotechnology for many years, with less than 5% of their sales from biologic drugs in 2005 (Figure 1).

Summary of incumbent response strategies.

The situation shifted perceptibly in the mid-2000s, with the approval and success of monoclonal antibody drugs such as Humira (Abbott Labs). Earlier movers, including Roche and J&J, were vindicated in their decision to invest in biotechnology, with more than 20% of their drug revenues coming from biologics by 2005 (Figure 1). The laggards sought to catch up: AstraZeneca bought CAT for $1 billion in 2006 and MedImmune in 2008 for $15.6 billion; BMS launched its “string of pearls” strategy with 11 small acquisitions of biotechs from 2007 to 2012; Sanofi bought Genzyme in 2010 for $20 billion. 18

By 2015, every big pharma firm in our dataset had made an explicit commitment to biotechnology as a part of its future growth plan. By 2020, all 12 firms had at least 10% of their drug sales coming from biological drugs.

Who were the winners and losers in the biotechnology revolution? Some of the venture-backed pioneers, such as Amgen and Gilead, remained independent and became highly successful. But for the most part, it was the incumbent firms who won out. Some moved earlier than others, but all of them successfully adapted through a mix of strategies, including R&D alliances, acquisitions, hiring of biotech-trained scientists, and corporate venturing. They were also effective at leveraging their existing assets in the transition, including relationships with regulators, their global distribution capability, and their sales and marketing prowess.

Comparing Supply-Side Effects in Other Industries

In addition to big pharma/biotechnology, we studied two other industries. In automobiles, GM and Ford created electric vehicle projects in the late 1990s but abandoned them quickly because battery technology was not sufficiently advanced. Toyota took the lead in hybrid vehicles in the 2000s, but it was Tesla’s founding in 2007 that gave established firms the impetus, from 2010 on, to develop their own battery-powered vehicles. By 2020, sales of hybrid/battery vehicles as a percentage of the total ranged from Toyota at 21% to Ford at 2%, but the espoused strategy of all 11 firms was similar, namely, to accelerate their rollout of electric vehicles while continuing to sell their petrol/diesel lines as long as possible.

In utilities, incumbents were making small investments in wind and solar during the 1990s (e.g., Enel built a small photovoltaic plant in 1993 and a wind farm in 1994), but the cost of production meant they were not profitable activities. The transition to renewables gained impetus around 2000, with Enel, Iberdrola, and NextEra Energy putting significant investment into wind and solar. Over the second period of the study, technology improvements coupled with government and social pressure enabled further investment. By 2020, 8 of the incumbents were at 20%-60% renewable capacity and 2 (Dominion and Duke) were at lower levels, but all of them had pledged to move toward 100% renewables, though at varying speeds.

Looking across the three sectors, the pattern of responses was similar and can be summarized as follows.

First, while the impetus for technology change came from outside the industry (as one would expect), the incumbents invested large sums of money in R&D to build capabilities and maintain their competitiveness. Both new entrants and incumbents contributed to the technical and commercial feasibility of these new technologies, though the relative balance varied significantly between sectors.

Second, progress was slow. Battery-powered cars had been mooted for many years (and indeed had existed in a very different form before the internal combustion engine was invented). Pioneering products such as GM’s EV1 in 1996 had failed. Toyota’s hybrid car was a success in the early 2000s, though it still relied on an internal combustion engine for longer journeys. It was Tesla’s innovation in battery technology in 2007 that finally made EVs commercially viable. 19 In electricity generation, alternative sources of energy such as solar, wind, and hydro had always been part of the conversation, but the transition to renewables only gained impetus around 2000, thanks to a combination of social pressure, government intervention, and technological innovation. 20

Third, the actions of incumbents were predictable and convergent. In each case, there were pioneers from outside the industry, there were early movers (e.g., Roche, Toyota, and Enel), and there were late movers (e.g., AstraZeneca, GM, and Dominion Energy). But once the emerging technology took off, the late movers were quick to fall in line. At the time of writing, all the major auto firms had committed to EVs, and all the major utilities had committed to investing in renewables. In all three industries, the incumbents were moving in the right direction, though at different speeds.

Fourth, the incumbents gained leverage from their downstream assets during the transition. As already noted, the big pharma firms’ strengths in clinical trials, global distribution, marketing and sales, and regulatory approvals enabled them to withstand the shift in technology for developing new drugs. For utilities, energy distribution and retail (B2C) service were central to their raison d’être and not adversely affected by the shift to renewables. In automobiles, it remains to be seen how effective Tesla might be at scaling up its activities, but the evidence to date suggests the incumbents’ capabilities in assembly, distribution, marketing, and sales will continue to be valuable. In all three cases, these assets helped incumbents to weather the changes brought about by the emerging technology.

Finally, in terms of “how” the incumbents responded, we saw the full range of tactics, including acquisitions, strategic alliances, hiring of key people from startups, and internal investments, so it is hard to generalize. However, in comparison with the industries facing demand-side effects, there was a greater emphasis here on internal investment and capability building. This was in part because good acquisition options were few in number and in part because incumbents could see the pathway to commercial viability would be long (so they had time to build rather than buy).

Was there a risk for incumbents if they did not invest in these emerging technologies? In the short and medium term, the risks were relatively small, for example, a loss of internal efficiency in how they were working or a dent in how they were perceived (by not embracing renewable technologies). In the longer term, not investing in supply-side technologies as they become important could be very risky, but this is a hypothetical argument as none of the firms we studied had fallen into this trap.

Demand-Side Effect: How Film Studios Responded to Digital Streaming

Shifting now to the demand side, we focus here on the six major film studios in 1990 (Disney, NBC Universal, News Corporation, Sony, Viacom CBS, and Warner) and their response to the emerging technology of digital movie streaming.

As is widely known, the Internet became available for commercial activities in the early 1990s, and there was a clear expectation from the outset that it would transform many industries as processing power and connectivity speeds increased. While downloading pictures and streaming music was already possible in the 1990s, the bundle of technologies necessary for live-streaming movies to the home came together around 2005, leading to the emergence of YouTube, Netflix, and Amazon Video. Live streaming to mobile phones became possible with the rollout of 4G networks in the early 2010s.

We view the emergence of digital streaming technology as a demand-side effect because it changed how users consumed the product of the film studios (movies and TV shows). In comparison with biotechnology, it had much lower levels of regulation and involved somewhat lower levels of capital investment. It was a highly visible arena, attracting enormous amounts of investment and media attention. Technological progress was remarkably predictable, with the doubling of processing power every 18 months. All of which contributed to the relatively rapid emergence of digital streaming, from initial concept in the early 1990s to reality in the mid-2000s.

How did the film studios respond to the emergence of the Internet? From the outset, they recognized its potential for changing the way people would consume entertainment (“We are hell-bent on not being in a railroad car as jets fly over us,” said Disney CEO Michael Eisner in 1999 21 ). Three of the six made major investments. In 1993, Rupert Murdoch’s News Corporation acquired Delphi Internet Services, a smaller rival to early online leaders CompuServe and Prodigy. Delphi struggled, and News Corp sold it three years later. Disney made a big move in 1998, acquiring Starwave (which owned ESPN.com) and 43% of Infoseek (an Internet service provider) and launching the GO Network, which provided access to other Disney content websites. These assets were shut down and sold off in 2001, with Disney taking a $800 million loss. Time Warner also moved online early, through its 1995 buyout of Turner Broadcasting and CNN.com, and then its ill-fated $165 billion acquisition of AOL in 2000, which was eventually unwound nine years later. 22

Chastened by these early failures, the film studios pulled back from online activities in the years following the 2000 dotcom crash. For the most part, they opted to double down on their core moviemaking activities. Disney bought out Pixar and acquired Marvel and Lucasfilm. Sumner Redstone merged Viacom (which owned Paramount Pictures) with CBS and Blockbuster to create an integrated entertainment company. NBC merged with Universal. Sony emphasized content digitization and links to its gaming business through a dedicated unit, “Sony Pictures Digital Entertainment.” News Corporation was the only incumbent to make a major online investment in this period, with the launch of Fox Interactive Media in 2005 and the purchase of Myspace, “looking at new ways to leverage our vast content through new distribution outlets.” 23 However, this venture was not a success, and MySpace was eventually sold off in 2011.

The film studios’ interest in digital streaming was reignited with the launch of Netflix’s streaming service in 2007. They responded in a variety of ways. Initially, there were several defensive moves, such as News Corporation and NBC launching Hulu in 2009 and Warner following with TV Everywhere a year later. Disney continued to double down on content through the Marvel and Star Wars franchises it had acquired, but, in 2015, it put in place the strategic moves that would allow it to launch Disney+ in 2019. Warner was bought by AT&T in 2016 to give the telecom giant a stronger direct relationship with consumers, and it launched HBO Max in 2020. In a similar vein, NBCUniversal was sold to Comcast in 2013 and launched its Peacock streaming service in 2020. CBS had an unsuccessful attempt at streaming in 2014 (CBS All Access) and relaunched it as Paramount+ in 2020. Columbia Pictures was alone in staying away from streaming, preferring to work in partnership with existing providers like Netflix and Amazon rather than to compete with them directly. It was also, of course, a relatively small part of the Sony group.

Looking across these six incumbent firms, there was no consistent or clear pattern of response. Four of them embraced digital streaming, but with different levels of success and on different timelines. Some opted for vertical integration with cable providers (Warner to AT&T, NBCUniversal to Comcast), while others prioritized their own content (Disney and Columbia). All were part of multi-business firms, some of which prioritized moviemaking (Disney, Warner) while others did not (News Corporation, Sony). This is in marked contrast to what we observed in the pharmaceutical industry: the big pharma firms converged in their actions vis-à-vis biotechnology during the period of study, whereas the film studios continued to have differentiated strategies vis-à-vis digital streaming throughout.

Why was there such a variety of responses? An important factor is that digital streaming disrupted the dominant business model in the industry, with Netflix and Amazon providing “over the top” subscriber services that disintermediated the cable companies and changed the balance of power between content producers and distributors. With their traditional source of profit under threat, the incumbents were proactive in seeking out alternative monetization strategies in pursuit of a new equilibrium. Indeed, even at the time of writing, the outcome of this battle of business models was far from resolved, with most film studios offering their own streaming services. Netflix, Amazon, and Apple invested heavily in content, and all players struggled to turn a profit from their streaming activities. It would therefore be premature to identify winners and losers. The original six film studios in 1990 all survived in some form or other, but without the dominance they had before.

Comparing Demand-Side Effects in Other Industries

In addition to the film studios and digital streaming, we also studied how newspapers and retail banks responded to the arrival of the Internet. Unlike the supply-side story above, the picture here is more complex because two different patterns emerged. The newspaper industry went through a painful and messy period of transition, not unlike the film studios. We tracked ten newspapers. They all developed an online presence quickly (in the mid-1990s) with varying degrees of success. And they all survived in some shape or form, but with low and varying levels of profitability. The heart of the challenge was that the Internet made it possible to access news information for free and for the offerings of traditional newspapers to be unbundled. The incumbents were therefore forced to rethink their traditional business model. Some shifted to subscription services (New York Times, Telegraph, Times), while others continued to offer news for free (LA Times, Daily Mail, Sun) with varying levels of advertising.

Retail banking, in contrast, went through a huge transition in the consumer experience, and yet the incumbent firms all continued to prosper while the online-only banks mostly failed. 24 All ten firms developed an online presence quickly and migrated their customers (at varying speeds) toward this new channel. The difference in outcome between newspapers and retail banks, we suggest, is largely a function of regulation, with the business model of incumbent banks (deposit-taking and lending) more-or-less guaranteed through their banking licenses. Notwithstanding the efforts of new entrants to shake up the retail banking industry, the Fintechs succeeded only on the margins and in very specialized niches (e.g., Wise and Plaid in payments).

We summarize the patterns of responses as follows.

First, in terms of antecedent circumstances, the early running and indeed most of the actual innovation (in terms of technical feasibility) was done by new entrants. This was clearly seen in the cases of digital streaming and online news, less so in online retail banking where startups and incumbents both played their part. This created the impetus for change to which incumbents adapted. In this respect, it was quite different from those industries facing a supply-side effect, where incumbents played a bigger part in making the emerging technology viable.

Second, progress was relatively rapid. While the technologies underlying the Internet undoubtedly took a long time to be laid down, the launch of the World Wide Web in the early 1990s sparked dramatic shifts in consumer behavior and also rapid responses from firms in many sectors as they sought to harness the new technology. As noted, three of the film studios acted quickly with major investments in online services during the 1990s. The newspapers and retail banks we tracked all created online offerings before the year 2000 (the Telegraph newspaper and Wells Fargo bank were first movers, both in 1994). However, it is worth noting that none of the early movers gained any significant advantage from moving quickly. There was probably some useful learning—for example, Disney’s early investment in Infoseek and Go.Com gave it insights that were useful later—but no clear penalty was paid by those who took a bit longer to respond.

Third, the actions of incumbents were unpredictable and somewhat volatile, as they sought out new business models to cope with changes in consumer behavior. 25 This statement is based on what we observed with film studios and newspapers, and indeed what we have seen in many other industries including book publishing, music, retailing, and education (we view retail banking as an important exception due to regulation). Typically, the incumbents sought to cling to their established business model while exploring new ones, but it often took many years for the industry to stabilize again. In newspapers, for example, the New York Times had several failed attempts at a subscription-based business with a paywall, starting in 1995, before succeeding in 2011. 26

In terms of how incumbents responded, we observed a full range of tactics, from acquisitions to alliances to internal investments. But one useful generalization is that there was more acquisition activity (in comparison with what we saw on the supply side). This was partly because there were many external startups experimenting with new Internet-based technologies (hence more acquisition candidates), but in the cases of newspapers and retail banking, there was also a “fear of missing out,” given the speed with which the Internet was changing user behavior.

Fourth, the incumbents gained leverage from their upstream assets during the transition. This point is a mirror image of what we observed in the supply-side affected industries. The top film studios and newspapers reaffirmed Sumner Redstone’s adage that “content is king” 27 and showed that people will still pay for high-quality storytelling and journalism in an era of free content. For retail banks, the disintermediation of their branch network was less disruptive than it might have been because of their complementary assets—the security and trustworthiness of their banking services, underpinned by their state-backed banking licenses.

Finally, what about the risk of not investing in emerging technologies? For retail banks and newspapers, the consequences of ignoring the Internet altogether would have been severe, whereas the film studios had the option (which many took) of doubling down on content. As a general observation then, demand-side effects created greater risks for incumbents than supply-side effects, though largely because they were faster-acting.

Summarizing the Differences between Supply-Side and Demand-Side Effects

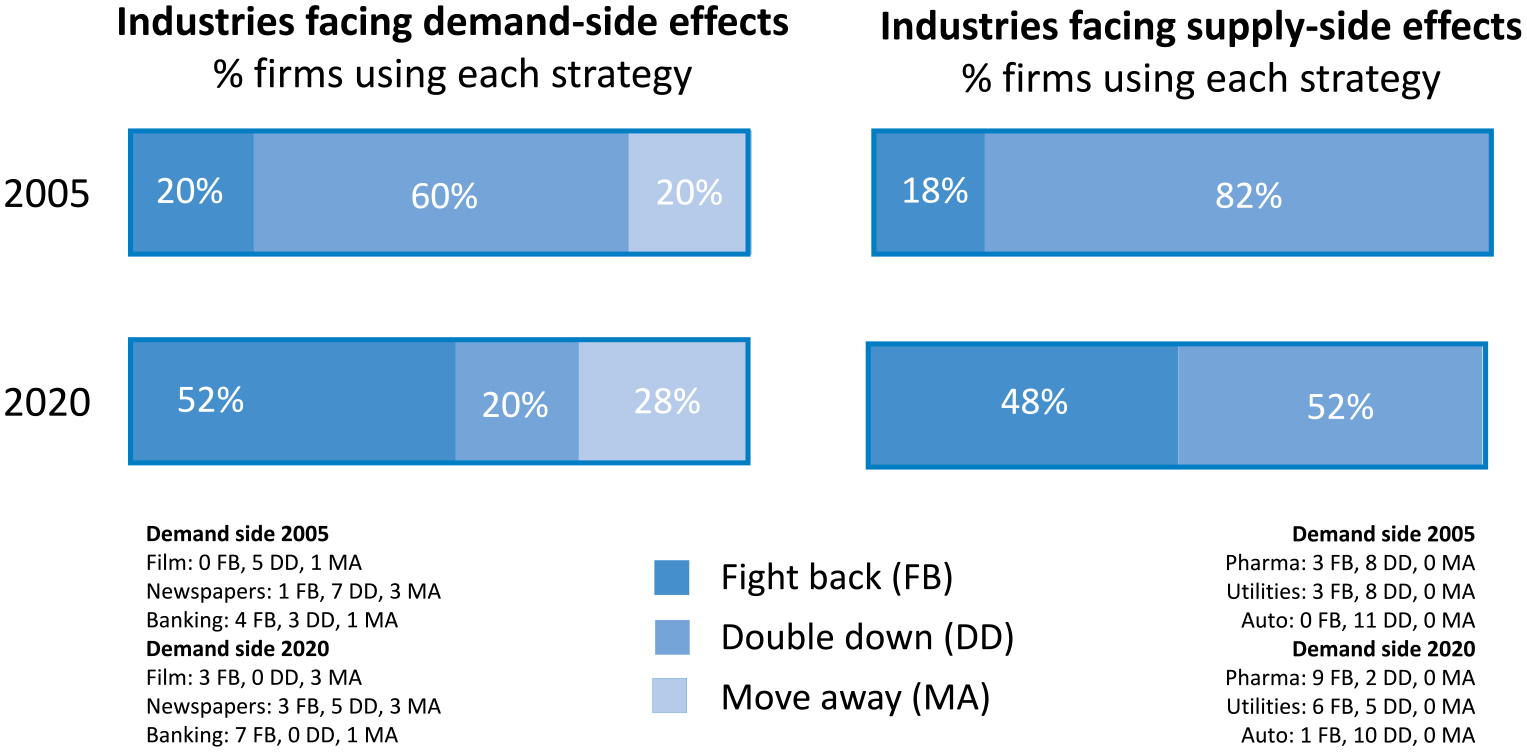

To summarize the differences between these supply-side and demand-side effects, we undertook a quantitative analysis of the specific choices made by the firms. Specifically, we sought to categorize the choices each firm made using the terminology put forward by Birkinshaw. 28 We measured the level of investment they made in the emerging technology (e.g., revenues from biotechnology-based products or revenues from movie streaming) and also the extent to which they invested in other areas (e.g., Roche investing in diagnostics or Sony investing in consumer electronics). This allowed us to categorize each firm’s strategy as fighting back, doubling down, or moving away. The results are summarized in Figure 1, at the mid-point (2005) and the end-point (2020) of the research period.

This analysis provides confirmation of many of the qualitative observations above. Firms facing demand-side effects pursued a greater variety of strategies, especially in the earlier time period, driven largely by uncertainty about the viability of various business models for film studios and newspapers. In contrast, the incumbents in industries facing supply-side effects were more cautious, especially in the first period but even toward the end of the period of study.

Supply-Side and Demand-Side Dynamics

We now consider how supply-side and demand-side effects might interact with one another. The findings above are framed around a clear split between the three industries with a supply-side effect and the three with a demand-side effect. However, this split is not always that clear cut. As noted, the introduction of electric vehicles led to some immediate shifts in user attitude and behavior (e.g., “range anxiety”) alongside the more fundamental changes in how automobiles were manufactured. Looking across these cases—and also other industries that we did not study in detail in this research—it is interesting to make a few observations about the interaction between the two sides so that future studies might explore them further.

First, emerging technologies often affect both supply-side and demand-side to some degree. For example, as noted earlier, electric vehicles change the user experience for longer journeys, and the operations of retail banks have had to adapt to the Internet world. However, we contend that it is still usefully analytically and practically to ascertain whether the emerging technology is likely to have a bigger effect in the near future on how a firm’s product is created (supply-side effect) or how it is consumed (demand-side effect), so the patterns of response across the industry can be anticipated and planned for.

Second, there is also an interaction effect between the two sides, with shifts on one side stimulating shifts on the other. For example, in the pharmaceutical industry, some gene therapy treatments are one-off cures rather than ongoing drug treatments, which potentially leads to significant changes in consumer behavior. 29 Electric vehicles can be used like traditional ones in the short term, but, over time, they will change how we think about auto ownership and journey planning. In utilities, the shift away from fossil fuels is leading to innovations in distributed generation with consumers potentially generating their own power. 30

Demand-side changes might also stimulate supply-side changes, though probably to a lesser degree. For example, newspapers have made changes to the length and style of their writing as they adapt to the needs of an online audience. Film studios have adapted their content to accommodate binge-watching. Banks have developed new services for their online customers. It seems likely, in other words, that whenever an emerging technology has a significant impact on an existing industry, its consequences will eventually reverberate through the whole business system. Executives need to be thoughtful both about the immediate effects of the technology and its longer-term implications.

Third, there may be some industries hit by both supply-side and demand-side effects together. We touched on the photography industry earlier, noting that changes in how images were created (digitally rather than film) were followed quickly by changes in how images were consumed (online, not through print). This meant incumbent firms such as Kodak and Fujifilm had few lines of defense, as they could not gain much leverage from their upstream or downstream assets during the transition. It is not surprising, in retrospect, that this “double whammy” led to the demise of several firms (Kodak and Polaroid) and others (such as Fujifilm, Canon, and Olympus) moving away into other business areas. It would be interesting to see if other industries affected by both supply-side and demand-side effects suffered similar outcomes.

Discussion

The purpose of this article is to help executives understand how to assess and respond to emerging technologies. By highlighting the distinction between supply-side and demand-side effects, we sought to identify patterns in the responses of incumbent firms that are informative and potentially help them make better decisions.

At a conceptual level, it is useful to relate these ideas back to prior research. A variety of studies over the years have suggested useful ways of categorizing new technologies in terms of their impact on incumbent firms—they can be disruptive or sustaining, competence-enhancing or competence-destroying, and they can result in architectural or modular innovations. 31 We would argue that our characterization, in terms of technologies having a (primarily) supply-side or demand-side effect, cuts across these existing typologies. For example, the (demand-side) Internet was a disruptive innovation for newspapers but a sustaining innovation for retail banks. In contrast, digital imaging (on the supply side) was a disruptive technology to camera firms but a sustaining technology for medical device firms. Our analysis suggests that demand-side effects are more likely to have disruptive consequences because of their effect on the traditional business model, whereas supply-side effects are more likely to have sustaining consequences. But we know there are exceptions, such as retail banking. It is therefore useful to consider this supply-side/demand-side distinction as a complementary perspective alongside existing theory to help executives develop a more complete picture of how things are likely to play out.

At a practical level, we offer here some specific advice to executives, with the important disclaimer that our evidence is based on a limited sample of firms over a limited period of time. The starting point is for executives to assess where the technology might affect their business. Does it operate primarily on the creation of the product/service (supply side) or on the way the user consumes the product/service (demand side)? Or if it affects both, which side is likely to be affected first?

If a supply-side effect is anticipated, our evidence suggests executives should respond cautiously, for example, by investing small amounts in a range of different technologies, working in consortia with other firms, and occasionally making acquisitions to fill gaps in expertise (e.g., the early forays into biotech by Roche, J&J, and GSK; Enel’s early investments in renewables; and Toyota’s incremental commitment to electric vehicle technology). Doubling down on an existing area of downstream expertise (e.g., customer relationships and global reach in the cases of Pfizer) is likely to be helpful. Monitoring and copying the actions of competitors is often a useful defensive ploy (e.g., Sanofi and AstraZeneca in biotech and Duke and Dominion Energy in renewables).

If a demand-side effect is anticipated, there is typically more urgency to act. Building direct relationships with users to understand how their attitudes and behaviors are changing is important (e.g., the initial efforts by newspapers and retail banks to create an online presence). Partnering with and/or acquiring startups through venture units or accelerators is a useful source of insight (retail banks such as Citi and Barclays did this well). Experimenting with new business models to explore alternative sources of revenue may be helpful (e.g., the New York Times and the Times of London). At the same, there is also value in doubling down on existing areas of upstream expertise (e.g., Disney’s acquisitions of Pixar, Marvel, and Lucasfilm) as a defensive ploy.

The final practical advice for executives is to keep an eye on the dynamics between the supply side and demand side. Most emerging technologies have the potential to affect firms in multiple ways, and sometimes changes in one area stimulate further changes in another area. In the unfortunate situation where an industry is affected simultaneously on both supply and demand sides, it is sometimes necessary to take more drastic action, for example, by shifting investment into adjacent markets that are not in such a perilous position.

Conclusion

To conclude, our research on 58 incumbent firms in six industries showed that supply-side effects play out over relatively long periods of time in a predictable way, with incumbent firms executing similar strategies, though at different speeds. Demand-side effects are faster-acting and more volatile, with incumbents often experimenting with a range of different business models as they seek a viable way forward in a changing market. By understanding these important differences, executives can potentially make better choices in how and when they invest in emerging technologies.

One closing thought: It is worth noting that the overall pattern across these 58 firms was one of cautious and incremental adaptation, which is not what typically gets discussed in the popular business press (“companies that adopt bold strategies improve their odds of coming out winners” was one article sub-heading in 2017). 32 While the pursuit of bold and courageous strategies sometimes works out well, our broad advice is to draw insights from as wide a body of evidence as possible and to work with the odds, not against them.