Abstract

Many of the most successful firms—such as Alibaba, Google, and Uber—operate platforms. Electric vehicles (EVs) are platform goods as well because value comes from the vehicle plus complementary providers. Gasoline vehicles are also platform goods, but managers in the industry can ignore that because the refueling network is mature. However, temporal and structural differences in network effects for electric vehicles make it crucial for EV firms to incorporate platform strategies. This article explains these differences and outlines the key platform strategy decisions that EV firms need to make, including platform network coordination, launch, and openness.

Keywords

At first, the presence of chargers might not appear to matter so much. EVs have dramatically increased in range to 250 to 350 miles per charge, and most EVs can be charged overnight at home or at work during the day. Because commuters travel 40 miles or less per day, the need for fast-charging stations would seem to be low. However, research has shown that there are numerous obstacles to overcome, such as drivers who also wish to travel long distances in one day (5% of car trips are over 100 miles), apartment dwellers who may not be able to charge at home, and owners who worry about forgetting to charge overnight. 3 The result is that there are nowhere near enough fast-charging stations to accommodate the expected increase in the EV fleet. Thus, the biggest barrier according to the U.S. Department of Energy—and many other experts—is the low density of fast-charging stations. 4 This situation is finally changing with increased attention toward charging stations by automakers, private network investors, and government, although to date, plans and promises have vastly exceeded action. A recent article suggests that if EV sales reach one-third of vehicles sold by 2030, there will be $600 billion of charging investment needed by 2040. 5 The same article notes that reaching net zero carbon emissions by 2050 will require $1.6 trillion of EV charger investment.

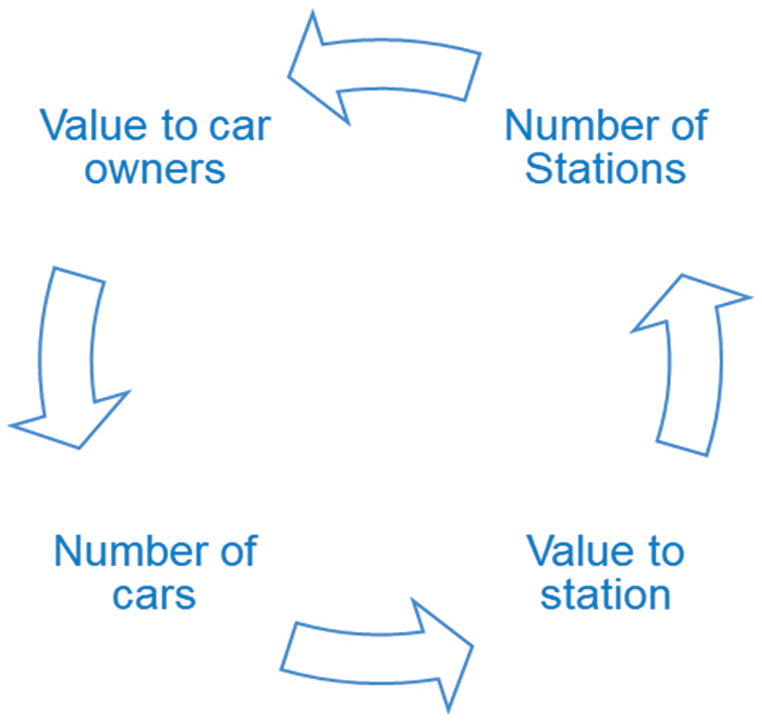

A chicken-and-egg relationship means that the number of charging stations is highly dependent on the number of compatible EVs on the road. Given that charging stations today have a mean utilization level of below 10%, their economic viability is highly responsive to demand. It might appear that the two sides are balanced: few cars and few stations. However, what matters is not the ratio but the absolute number of EV stations nearby. The result is that a firm entering the EV industry competes not only on the traditional dimensions of automotive quality such as acceleration, handling, cabin noise, aesthetics, and price, but also on its network of complementary providers, such as charging stations. This network dependency makes EVs a “platform” industry.

Network effects drive utility.

Platforms are widely seen in the economy, and most people interact with them every day. Common examples include using eBay, Etsy, or Amazon Marketplace, which provide consumers with goods from third-party sellers. Thomasnet and Alibaba provide similar services to industrial customers and suppliers. Facebook, Instagram, LinkedIn, and Twitter provide consumers the ability to interact with each other, but they also have a multisided platform aspect because third parties can sell their goods and services on these platforms. In business-to-business software systems, SAP and Salesforce sponsor platforms that provide standalone services. However, they also provide a conduit for external firms to sell services to business users through the platform. Platforms and their associated ecosystems are an active area of study in the economics and management literatures, and we provide some references to more comprehensive works as well as a quick summary to orient readers. 6

Other industries have demonstrated that the chicken-and-egg problem can be coordinated. These include video cassettes/video recorders, video games/video consoles, marketplaces such as eBay and Craig’s List, and payment systems, including Visa and Mastercard. Indeed, Google-sponsored contests in multiple categories in order to have a supply of Android applications for users to consume at launch. While these other industries differ from the automotive industry in many respects, they are nonetheless instructive.

Established automotive firms should recognize that, by pivoting toward a product line dominated by electric vehicles (EVs), they are entering a platform industry. However, the authors have heard numerous complaints from EV industry managers that this facet of competition is either underappreciated or ignored by traditional firms. As we will see below, these complaints ring true because few automotive firms are seriously addressing the network aspect of the EV industry. Part of the reason for this is that incumbent firms operate in an established industry that has had a robust network of refueling stations for over a century. 7 There are over 100,000 refueling stations in the United States, and all brands of cars are compatible with (nearly) all brands of stations. In contrast, the electric car industry is in an early stage, capturing less than 6% of new car sales in 2021, 8 with only around 5,500 fast-charging stations that can charge an EV in a half-hour or less. 9 Moreover, they are fragmented across brands of cars versus brands of charging stations.

Neglecting the platform nature of EVs creates an opportunity for firms whose managers recognize the platform context they exist in and can leverage platform strategies that have succeeded in other industries to create an additional source of competitive advantage. This opportunity can be illustrated by contrasting the performance of Nissan—which released the Nissan Leaf in 2010 (and which was the world’s #1 all-electric car from 2011 to 2014 and in 2016) but made no direct investments in charging stations—and industry newcomer Tesla—which (having released Model S in 2012) made heavy investments in their fast-charging stations, branded as “superchargers,” prior to selling a huge number of vehicles, and has been the top-selling EV automaker since 2017. 10

How Tesla Has Succeeded (So Far) with a Platform Strategy

Tesla has so far succeeded in the platform game by adopting a fully integrated approach, building and selling cars as well as deploying a (relatively) large network of fast-charging stations that are available only to Tesla vehicles. 11 Platform strategies include making strategic decisions about launch, openness, scaling, and network coordination. By owning the two sides of the market and building a technologically compatible infrastructure, Tesla has also performed the crucial platform role of coordination between the EVs and fast chargers. This includes both real-time coordination and longer-term planning and scaling coordination. A Tesla car owner has full, real-time visibility over the current status of charging stations, and stations can identify each car and apply personalized access and pricing rules. On the planning coordination side, Tesla can employ data from the automotive side to make decisions regarding the charging station network and vice versa. It also enables the coordination of pricing and openness on both sides of the market. Because the few incumbent automakers that have developed charging stations cannot gather such data, such coordination is difficult for them. These firms can coordinate one side of the market or the other, but not both.

Why Is This a Platform Strategy?

Platform businesses harness network effects such that the value proposition to users includes, in addition to its standalone value (what the system does for a user independent of any other users), some combination of same-side network value (the value that users derive from interacting with users like them) and cross-side network value (the value that users derive from gaining access to different types of users 12 ). Each type of user exchanging value on a platform—for example, video content providers, consumers, and advertisers on YouTube—is referred to as a “side” of the platform. Hence, platforms with cross-side values are viewed as being multisided. For example, Facebook provides both same-side value, because users interact with each other, and cross-side value, because of their third-party service providers and advertisers.

In addition to platforms, there is the rapidly growing stream of literature in the strategy field that focuses on ecosystems. “Ecosystems, we posit, are interacting organizations, enabled by modularity, not hierarchically managed, bound together by the nonredeployability of their collective investment elsewhere.”

13

Leading scholars in this field combine ecosystems and platforms to describe how platform systems can leverage external value creation through ecosystem partners. For example,

Platform technologies, and their ecosystems of complementors, are a manifestation of this shift in the way firms are organizing to create greater value for end-users. Platform technologies, and their ecosystems of complementors, are a manifestation of this shift in the way firms are organizing to create greater value for end-users.

14

For our purposes, we use the term platform to refer to not only the platform technology itself but the different types of users that bring value to the platform. For example, SAP’s ecosystem would include itself, its enterprise buyers, and providers of solutions that build on top of SAP technology to extend its functionality for users.

Because a multisided platform orchestrates value creation through interactions between multiple third-party participants, it is vital that the platform attract a critical mass on each side. However, since participants on each side receive value only when there is a large number of participants on the other side, this creates a chicken-and-egg problem. Platforms address this problem through many tactics, including complex business models that involve subsidies on one side in order to drive growth on that side, and thereby attract participants to the other side, until there is a robust flywheel of positive network effects on both sides.

Critical platform elements include a platform sponsor (or owner) with decision rights over who can participate in the ecosystem, what the technology trajectory will be, and how to connect to the system. The platform coordinator also sets up rules for participation and how they will be enforced. Additional elements include the types of users who participate in the system and what units of value those users exchange. A key issue for sponsors to manage is how the value that the platform creates through exchanges is captured and then shared among platform users. Tools employed by a platform to promote more efficient value exchange between sides include search, filtering, and matching mechanisms. Platform organizations must also attract external partners as members of their ecosystems to participate on the platform to contribute value. This drives the necessity for a platform to invest in the ability to coordinate the activities of users. 15

Despite this superficial similarity in the multisided platform nature of both gasoline and electric cars, there are vital differences between the two categories. The differences are as follows: temporal—pertaining to quantitative properties at the current time in the lifecycle of the two technologies, such as the size of the installed bases (or fleets in automotive parlance); and structural—with fundamental qualitative differences, such as the fact that electric vehicles can be recharged at home. These two differences combine to affect how the supply (or size of the network) influences utility or profitability.

Platform Strategy

To summarize, critical elements of a platform strategy include the following:

Finding a platform coordinator: Firms facing the EV transition must recognize they need to actively coordinate all sides of a platform: at a minimum, EVs on one side and the charging infrastructure on the other. Other sides are likely to emerge as well.

Launching a platform: How can companies solve the chicken-and-egg problem facing incumbents when establishing a platform.

Deciding on open vs. closed: Openness is a critical decision variable. Managers must decide whether to create their own closed systems, including both the vehicle and the charging infrastructure—as Tesla has done—or work with open systems that instead rely on ecosystems that embrace other firms.

Considering growth options: There are a number of approaches to growing a platform. Automotive firms must first consider these before deciding upon a strategy.

Organizing for platform strategies: As part of the EV industry’s evolution, its leaders will need to abandon decade-old practices and organizational structures and instead adopt new platform-based management strategies.

To further illustrate these platform strategies, we analyze the strategic choices made by Tesla—which has been actively following a platform strategy— and the other automakers and industry participants.

Tesla: Acting as Platform Coordinator

Coordination is one of the most difficult and critical platform challenges. The existence of cross-side network effects between two (or more) sides of the market means that there needs to be a coordinating entity that can ensure that strategic and operational decisions are made in a way that leverages those externalities. Decisions include product launch timing, pricing and monetization, efforts at network mobilization, and compatibility with other players. The coordinating entity may be the platform, and it may own proprietary technologies relevant to one or both sides. The coordinating entity could also be a firm that operates one side of the market, or possibly both sides, or it could be a consortium of firms operating on one side or across sides, or a separate party altogether. For instance, Google is the platform entity that coordinates the Android platform (with numerous firms that develop Android phones), VISA is the entity that coordinates the VisaNet credit card payments platform (with numerous banks that issue cards to consumers and cover merchants who accept these card payments), and Apple is the entity that coordinates the iOS platform (and is also the sole manufacturer of iOS phones).

Consider the Tesla system. First, in coordinating growth on the two sides of the market, Tesla ensures that the number of charging stations grows in a suitable proportion to the number of Tesla EVs sold. Tesla recognizes that the two costs of imbalanced growth—making car-owners unhappy or leaving stations underutilized—are asymmetric, which it factors into its platform growth and rollout strategy. Second, and more crucially, Tesla coordinates the locations of these charging stations as they are rolled out, ensuring that they match localized or regional sales of EVs as well as the driving patterns of Tesla owners. For instance, it would be wasteful to have a high density of charging stations in Southern California if Tesla buyers or their likely driving routes were concentrated in Northern California. Third, Tesla ensured that pricing schemes across the two sides of the market reflect strategic objectives or suitably address intertemporal considerations. For instance, Tesla provided unlimited free fast charging to Tesla buyers until 2017 in order to promote the purchase of Tesla EVs when the market and network were in relative infancy. Such a strategy would be challenging for an independent network that relied on charging revenues. Fourth, Tesla has coordinated the rollout of its EV product line over time, starting with the expensive proof-of-concept Roadster (2008), then the higher-end luxury models S and X (2012), and then the mass market targeted lower-priced Models 3 and Y. Fifth, Tesla built an information system through which it can inform EV owners about real-time availability of charging stations as well as dynamically manage access and pricing and priority between stations and EVs. Sixth, Tesla has decided for the time being to close its charging network to EVs made by other automakers for the most part, but retains the option to open up by contracting with automakers or directly with EV customers. In short, Tesla worked to optimize its overall objectives by making business decisions across the two sides of its network.

The “other” non-Tesla system provides a stark contrast. Crucially, there is no clear, well-defined entity that is performing the coordination role. Individual automakers make choices on the product line spectrum (e.g., high-priced luxury EVs or lower-priced mass-market models) in isolation. They base their decisions on many factors but without explicit and effective coordination of the network of charging stations, over which they have little say. Pricing decisions for each EV model reflect economic objectives for the model or the brand rather than system-wide objectives that combine the economics of the car and the economics of charging. Meanwhile, each charging station provider makes quantity and location decisions pursuing its own objectives based on its own information and its own predictions about future adoption of EVs. In the absence of a coordinating platform entity, there appears little evidence of cross-side incentives to promote balanced growth, an optimal mix of models, or the optimal location of charging stations. Moreover, although non-Tesla EV vehicle makers are fierce competitors of Tesla, non-Tesla charging station providers are all too happy to court Tesla EV owners as customers of their relatively thin non-Tesla EV fast-charging networks.

The discussion above highlights the vast gap between the coordination within the Tesla system and the disorganization seen in the non-Tesla multi-player system. At the end of 2021, about two million EVs were registered in the United States, 16 Tesla had 70% of the EV market 17 and had set up over 1,300 fast charging 18 stations in the United States (most with over ten stalls each, many with over 40 stalls 19 ) roughly 4000 stations worldwide. The non-Tesla firms combined have only 30% of the market and 550 non-Tesla fast-charging stations. 20 In short, the evidence suggests that EV firms will face difficulty making the EV transition without some entity taking on the task of platform coordination. The lack of such coordination partially explains why the broader EV industry has been marked by lofty promises and unmet goals.

Tesla has been able to make quicker and better decisions on both sides of the market, which has been critical during the company’s early growth phase. Although it required substantial investment, Tesla’s DIY strategy has provided three additional advantages.

Reduced Friction: Tesla can mix and match revenue models for its vehicles and charging stations as needed. By comparison, independent charging providers need to develop business models based purely on offering the charging infrastructure.

Higher Levels of Freedom to Incentivize One Side: Having no strategic partners, Tesla can change tactics with relative ease. Tesla offered free fast charging until 2017, but having achieved critical mass, it then switched to fee-based charging. Indeed, in the future, Tesla might copy current gas station practice and profit from selling convenience store items and would thus prefer to serve a larger vehicle base that includes non-Telsa EVs.

Greater Choice of Openness: Tesla is free to decide how open or closed it wants its network to be. It has closed the network to all but Tesla vehicle owners. But the company could change that strategy any time it wished. And without any strategic partners, Tesla can make that decision easily.

However, Tesla’s DIY strategy comes with substantial risks. These include the large investment, the possibility of being outperformed by consortia, and the risk of settling on an inferior standard. Another danger is that a government might nationalize Tesla’s private network or mandate open access to other brands. Still another danger is that a government might impose a standard different from Tesla’s for antitrust or other reasons, stranding much of Tesla’s investment. Indeed, there are signs that the standards war for non-Tesla chargers might be coming to an end, with CCS1 emerging as a potential victor. 21 Teslas sold in Europe, where CCS2 has become dominant, are compatible with those sold in the United States and can still benefit from CCS1 investment through the use of adapters. 22 Coping with these risks might explain why Tesla appears to be gradually opening up its charger network at the time of this writing.

Tesla: Deciding on Open vs. Closed

A core feature of platforms or platform architecture products is that they often build on an ecosystem of partners. Openness describes the extent to which other organizations are allowed to (or not) act as complementors and interact with the platform. Tesla followed a closed approach by developing incompatible charging infrastructure (especially on the software side) and decided to build out the complementing almost completely on its own (with the exception of the Destination Charging program for Level 1 charging). In this way, it prevents competitors from benefiting from its extensive charger investment.

Tesla: Considering Growth Options

One key strategy for growth is signaling. To attract complementors, a company can try to signal to one particular side that joining its system is better than joining the others. 23 However, signaling in a multisided market can be a challenge. For example, if a company signals only at the product level, as many EV makers are now doing, it may miss opportunities on the network side. 24 Another risk of signaling is that it can cannibalize products. This happened when Tesla introduced its Model 3 car as an affordable EV with an anticipated price in the range of $35,000. This announcement helped attract charging infrastructure complementors, but it also cannibalized Tesla’s more expensive and higher-margin EVs while creating a false anchor in consumers’ minds. When the Model 3 finally shipped years later, the car’s actual price tag was in the much higher range of $55,000 to $60,000, rendering the level of cannibalization needlessly high.

A different option for growth is attracting complementors; only with complementors do EV products make sense. Yet to date, most EV makers have failed to attract charging complementors. In part, that’s because many important choices have been left undecided. For example, where should charging stations be located and what levels of charging speed should be offered? The industry’s failure to coordinate on these and other decisions has discouraged complementors from investing. In addition to charging networks decisions, consumer benefit can be added by complementors who can fine-tune automobile performance, add to the multimedia entertainment experience, or provide enhanced value in other ways such as customized bodies. In this area as in others, Tesla has taken an entirely different approach. Rather than trying to attract complementors, Tesla has built its own complementary products, even moving to full-service charging stations that offer (and monetize) food, drinks, wifi, and other services, which is traditionally where gasoline stations have made their profits. 25 However, as the discussion above noted, the DIY approach is difficult to scale. Now Tesla faces a new strategic question: When and to what extent should the company open its platform to others?

History of Fossil Fuel

As we have observed, traditional gasoline automobiles are also a platform because they also need a network of refueling stations, as do cars that run on other types of fuel such as compressed natural gas or hydrogen. Hence, we draw some insights from the history of the gasoline automotive industry. In the early 2020s, the developmental stage for EV charging stations appears at first to resemble the early stages of gasoline vehicles in its platform aspects, but this does not bear closer inspection. Examining these differences is instructive. First, the immensely large Standard Oil entered the market for gasoline when the automotive industry was just beginning to take off. It had a large mature distribution network for kerosene on which it could piggyback gasoline distribution. Other oil firms soon contested the gasoline market as it grew larger, but they did so by investing in expanding distribution via filling stations. No automotive firm attempted to enter the fueling market because the auto firms were comparatively small. Establishing a closed system was difficult, and fuel compatibility in early automobiles was greater than today; a Ford Model T could even run on benzene or ethanol in a pinch. Nozzle size could be worked around with a funnel. Standards were only set in the gasoline industry once automotive producers became powerful stakeholders, and each side negotiated as a consortium.

Tesla has faced a very different strategic climate. Unlike oil, electricity is provided by distribution firms as a commodity that is available to home chargers, thus undercutting the charging station’s potential pricing power. Because there is little motive or capability for energy utilities to subsidize an expensive charger network to promote sales of their product, the result is that there is no equivalent to Standard Oil. Lacking competition on either side of the market, Tesla could subsidize a network of charging stations and make it part of its value proposition because it could deny the benefits of its network to competitors’ vehicles. The result is that Tesla could establish itself as the leading player on both sides of the market and resolve technical issues, set standards, and geographically distribute charging stations in its own favor to enhance its market position in a way that traditional automotive firms never could at the dawn of the petrol automobile age.

What Is Tesla’s Strategy Going Forward?

Although Tesla showed impressive progress in deploying fast-charging infrastructure in many countries and, through their closed approach, can ensure comparably extremely high levels of quality for their complement, Tesla lacks the generativity of a bigger ecosystem. As a result, scaling is difficult, and it faces the decision of what to do next.

A possible way forward could be counterintuitive from a classical strategy point of view: Become more open on the car side by opening patents (and thus become a partially open platform architecture). This could help to scale and decrease costs in the entire supply chain and consequently build the installed base of cars. As Tesla owns the proprietary complement (the charging infrastructure), it could retain sufficient control. Tesla could continue to control critical aspects of the system, such as route planning, and become a complement in adjacent platform markets such as energy, stationary trade, or introduce reservation systems.

Other paths forward include leveraging the data Tesla gathers from their cars as they are driven, such as service history, vehicle usage, safety event camera recording, and of course, fast charger usage. The data can be used to improve the current driving experience with revised vehicle control algorithms, continually updated maintenance schedules and diagnoses, and even as an input to improve future vehicle designs. Strictly speaking, because the data is not sold to a third party, the strategy does not leverage a multisided market. However, it remains a platform strategy because the competitive advantage accruing from data collection increases with the amount of data and hence the number of EVs a firm has as its installed base.

Because Tesla’s customer base is so large relative to its competitors, it has much more data, which creates a competitive advantage for Tesla that its competitors cannot yet match because of their smaller installed EV bases. The result is a same-side externality, in which the increased database creates a better vehicle experience, resulting in more vehicle sales, a larger installed base, and ultimately an even bigger database creating a virtuous cycle of advantage for Tesla. Infotainment data and mobile app usage are also recorded by Tesla.

The most powerful implementation of this strategy might be “Autopilot,” which is Tesla’s autonomous driving application. Autopilot collects data from vehicle cameras that are inputs to controlling Autopilot’s autonomous driving routines. Because Tesla’s fleet is bigger, particularly the Autopilot equipped fleet, Tesla has a significant data advantage that can be used to improve the autonomous control algorithms. This is especially important because the artificial intelligence for autonomous driving needs much more data to “train” their control systems than do traditional control-theoretic algorithms. On the other hand, once they are trained, AI-based algorithms are more effective for controlling autonomous driving. This implies that Tesla has a platform-based advantage because it can improve future revisions of Autopilot more quickly than its competitors.

Big Changes Are Coming: What Should Other Automakers Do?

Despite Tesla’s headstart and the many advantages that creates, we do not see the industry ending up with a winner-take-all situation like Google’s domination of the U.S. internet search market. The automotive platform is more complex involving physical as well as digital aspects. For example, adding new charging stations involves a marginal cost, unlike digital platforms, and charging at home continues to be an option for many consumers. Challengers to Tesla have a number of options. One is to attempt to create their own charging network either themselves or through a consortium. Another is to compete on a third side of the market. Finally, they can bring engineering strengths on the vehicle market side to bear that Tesla is weak in.

Traditional automotive firms can benefit from their ability to manufacture highly reliable, low-defect products at scale, which requires significant institutional knowledge that newer firms, including Tesla, lack. Tesla’s vehicles have a notoriously poor reputation for quality, as evidenced by Consumer Report’s rating Tesla 27th out of 28 manufacturers evaluated in 2021. Elon Musk has even admitted that reliability is especially poor when scaling up new models, which is noteworthy because EVs are typically easier to assemble than gasoline-powered vehicles. Incumbents can challenge Tesla by rapidly introducing new products while focusing on product quality, 26 product range (whether broad or narrow), 27 and timing. In a networked market such as EVs, decisions on these factors can differ dramatically from those made for a standalone market. 28 That’s because a company’s network’s size determines the network benefit for users.

One architectural innovation strategy for a few firms might be to move into the business of producing modular “skateboards” (chassis that also contain motor, transmission, and batteries in a flat form factor resembling skateboards) probably in conjunction with extant skateboard startups. Skateboards have all the hallmarks of a scale business, demanding near zero-defect conformance, reliability, and robustness, and they do not provide much differentiation to the customer. Hence, one would expect that skateboard scale volumes might exceed those of today’s vehicles, leading to a shakeout of smaller startups and even incumbents. Where would these displaced firms go? Some will likely go out of business. Others could make body design and manufacturing more similar to that of ambulance and moving van makers. These firms do not make their own chassis and engines but instead buy large pickup trucks whose flatbeds have been removed and “drop” specialized low-volume bodies and interiors onto the exposed flat area behind the cab. A skateboard is not so simple as that, but it is much simpler than assembling today’s vehicles that lack a modular skateboard architecture, including Tesla’s integrated designs. In particular, skateboards would potentially make establishing some set of standards for a given class of vehicle’s physical, electrical, and electronics interface easier. This suggests that the EV transition might drive the losers of a skateboard shakeout into the body and interior space, to some extent decoupling the traditional vertically integrated body and engine auto firm.

Firms have recognized that Tesla’s DIY strategy might increase the risk of stranded investment and a destructive investment “arms race” if more and more EV firms attempt it. Even Rivian, which appears to emulate Tesla by making direct charging investments, is using the CCSI open standard for its chargers. This reduces risk because it can easily open up to other makers’ EVs later on to avoid stranded investment. It is also differentiating its network from Tesla’s by being powered by all renewable energy sources. It is locating many of its chargers in national parks and other recreational areas, which it is branding as its “Adventure Network.” Volkswagen (VW) presents another twist on the do-it-yourself strategy. It is investing heavily in the Electrify America network at which almost all brands of EVs can charge. Part of the reason for this apparent altruism is that the investment is required by a settlement with the US Environmental Protection Agency in 2016 to resolve VW’s diesel emissions scandal. However, VW is the world’s largest car manufacturer by unit sales and is the number one EV seller in Europe as well as the number two seller in America. It has also committed to selling 20% to 25% EVs by 2025 and has even discontinued developing new gasoline engines. Hence, while being open levels the playing field for all brands, VW may ultimately benefit most of all from its network because of its anticipated EV sales, particularly if it can force other firms, such as Tesla, to open up their own closed networks.

VW is making similar investments in charging networks in Europe and China. VW’s strategy in Europe reveals another potential method of competing with Tesla because it is doing so there in a partnership with BP. Consortia are a common strategy for those seeking to challenge platform dominance. Players on one side can form multi- or bi-lateral cooperation agreements with suppliers from the other side. These agreements typically aim to reduce investment risks for all sides by letting each side build on the other side’s installed base. Benefits from this approach include the ability to leverage multiple firms’ installed bases to attract charging infrastructure suppliers. Consortium members can also benefit from the group’s combined financial resources. Possible downsides include slow or ineffective decision making, hindering coordination. Another downside is the difficulty of figuring out cost mechanisms and revenue sharing. The failure of the JICRS (joint industry computerized reservation system) in the airline reservation industry offers a cautionary tale of delay, inability to reach a cost-sharing consensus, free-riding, and even sabotage. However, there are also many benefits, particularly for cross-industry collaboration between incumbents on opposite sides of the market. For example, in the VW and BP partnership, VW is installing chargers at existing BP gasoline stations.

Tesla competitors might also wait for or actively lobby governments to unilaterally make decisions for the industry. For example, firms could wait for the government to invest in the other side of the platform (in this case, a network of charging stations as China has done) or impose standards that ensure that each participant on both sides of the platform is completely compatible. Indeed, the Biden administration announced a proposed $5B of investment in high-speed chargers along highways. 29 Although this approach has the potential to spur innovation and investment, there is the possibility that a government might make poor decisions by ignoring industry input, such as choosing an inferior standard that will hamper some or perhaps all EV makers. For the time being, industry input on standards may be less necessary because the CCS1 seems to be crowding out its main competitor, CHAdeMo in the United States. Even Tesla has promised to come out with adapters that will allow its newer vehicles to charge at CCS1 chargers, although that has not happened at the time of the writing of this article. Importantly, older Mitsubishi and Nissan EVs, which used the CHAdeMo system, will not be able to use CCS1 and are stranded.

Standards fragmentation between regions around the world appears likely as Europe, China, and Japan are all settling on standards different from the United States and from each other, complicating the engineering tasks for global firms such as VW and Toyota. Finally, because a thirty-minute charge cycle is still slow relative to gasoline refueling stations, the door is open for new, faster technical standards such as the 800-volt architectures used by the Porsche Taycan, which can again drive fragmentation even within regions.

Others: Considering Additional Platform Options

Another possibility for EV manufacturers to compete with Tesla is to explore platform sides beyond charging that can be attacked. There already exist independent third-party apps to improve Tesla’s functionality (SentryView, Tezlab, TeslaFi, Stats). Tesla discourages this, but other EV firms could deliberately cultivate a third-party complementor ecosystem, following the IBM PC’s Windows strategy. 30 That would mean creating an open standard with respect to software, likely expanding upon the engineering and technology firm Bosch’s Controller Area Network (CAN) standard used by many automotive firms for embedded electronics. This would be particularly useful if the EV makers could level the playing field by convincing regulators to enforce openness in charging stations. In effect, this strategy could emulate how the Android standard competed with the iPhone. It offered the customizability of an open system to successfully contest a closed, less flexible system. Despite the risk of commoditization with this strategy, it could help non-Tesla EV firms achieve significant scale.

What Should Fossil Fuel Incumbents Do?

Energy companies such as BP, Shell, and Chevron face a challenge as well in the EV charging platform wars. According to MarketWatch, the number of gas stations has dropped sharply since 2020. How do they avoid being excluded as the market shifts? For example, general stores suffered when dedicated gasoline filling stations emerged in the 1920s. While BP is beginning to add EV chargers to its gas stations in Europe, this strategy may not scale. One major problem is that changing to electric vehicles involves significant infrastructure costs. Longer EV charging times require the number of charger ports required at a station to be roughly six times greater than the number of petroleum fuel pumps to serve the same number of cars per hour. This implies additional real-estate costs, particularly in urban areas. Another issue is the infrastructure needed to bring sufficient electric power to those stations, particularly in rural areas. One possibility is to increase offerings like some Tesla stations are beginning to do. They could concentrate on increasing the convenience store business of the longer charging times at EV chargers by bringing in groceries and impulse electronics business or adding (perhaps multiple) restaurants or a coffee lounge to take advantage.

Trucking companies and other firms that have large private long-haul fleets are considering building their own infrastructure. Fossil fuel companies could team up with them with respect to investment and broker multi-firm alliances to achieve the sufficient scale of investment necessary. This would be helpful because long-haul trucks require a scale of electrical infrastructure much greater than that for passenger EVs with perhaps 100-150 MW required to power a station for Class-8 “18-wheeler” trucks equivalent to today’s truck stops. However, because these charging systems would be closed to fleets outside the alliance, the specter of government forcibly opening up these systems to create scale and prevent fragmentation might discourage investment. Complicating the issue is competition from other technologies, such as hydrogen fuel cells and compressed natural gas, with potentially better economics for truck applications than battery EVs. None of the infrastructure for these technologies is compatible, and current regulations require that refueling/recharging for trucks powered by these technologies be physically separated, encouraging deeper fragmentation that cannot be obviated through standards.

What Should Private Network Providers Do?

There are numerous private companies that are investing in EV charging networks. These include firms such as ChargePoint and EVgo, which are among the largest non-Tesla networks. The challenge these firms face is the same chicken-and-egg dilemma noted above. With low utilization percentages, it is difficult for a standalone firm to generate enough revenue to recover the necessary investment or even ongoing operations. 31 At least two options present themselves. The first is to continue to rely on government subsidies. The second is to negotiate with the non-Tesla firms for financial assistance in building out networks. Although there has been skepticism that automobile firms will invest substantially, firms such as VW are making substantial commitments and make attractive partners for private network providers.

What Should Government Do?

At the moment, the standards contests in the United States and elsewhere appear to be resolved, but they may reemerge in the future because EV technology is rapidly evolving. If society wants a faster transition to carbon-free transportation, then policymakers should work to prevent long and costly competition between various platforms. Instead of looking at traditional antitrust regulation, interventions should focus on value creation before focusing on competition. On the charging network side, it is important to ensure that multi-homing is possible between platforms. The emerging CCS1 standards are encouraging and may reduce the need for direct government intervention in standards.

Government bodies should also keep a close eye on potential anti-competitive behavior. In the event that Tesla continues to dominate the high-speed charging market and is able to use that dominance to prevent competition on one or more sides of the market, then some intervention may be warranted. In such an event, a case might be made for direct government investment, as seen in the recent plans to invest $5B in chargers along highways. The issue we noted above is the need to avoid technological dead ends. Another challenge is the tradeoff between seeding a market versus preventing competition within the market. Once scale is achieved, then charging network providers either need to prove economic viability or find a way to work with EV manufacturers to capture enough funding to maintain operations.

Related to this is the question of standards for automotive service data. While the market can likely be left to expand EV service by itself, standards for service data will be necessary for rapid scaling. There is already an extant standard, OBD II, for onboard automotive diagnostics, but it will need to be expanded to include appropriate EV diagnostics information.

Another important area for government policy is the data layer. Here we would hope to see data sharing along the lines of that proposed in the European Union’s Digital Markets Act. To achieve data sharing, we strongly believe that traditional (ex-post) antitrust intervention takes far too long and will be less effective in markets driven by network effects. Instead, policymakers should pursue prescriptive (ex-ante) regulatory frameworks. 32

Discussion

Rise of the Data Layer

We believe that the industry is undergoing a massive transition in which new product architectures, new forms of value, and new business models are combining to pose a threat to incumbent manufacturers in the automotive industry. The platform game is not over with charging, however. EVs are part of the shift in the automobile industry to a more digitally based value proposition. This will create additional sides of the market that did not exist in the gasoline car era, such as automated driving, powertrain optimization “apps,” EV-capable service stations fueled by client’s driving and maintenance data, and infotainment, all of which can involve third-party providers. This shift to external value creation creates the opportunity to engage a broad ecosystem of partner organizations that can supply capabilities that enhance vehicles’ value and avenues of product competition. Those firms that excel at orchestrating platform ecosystems partners and incumbent manufacturers will reap competitive advantage. However, if incumbents fail to adopt platform-based strategies, they leave it open for other firms or consortia to step into the void and drive them out of the market.

Implications for Other Industries

The questions raised by this story are not unique to the automotive industry and bring up some more general insights. As digital platforms move into industries that have physical assets representing a large part of the (current) value proposition, these issues will rise again and again. Many, if not most, strategic insights into platforms involve highly digitalized business-to-consumer platforms, including smartphones, ride-sharing, and online marketplaces. Most of these lessons still apply, but as the EV industry shows, they often have a twist. As one example, complementors such as smartphone app developers face essentially zero marginal costs when adding customers. This is clearly not the case for charging stations in the EV space. As with Tesla, platform owners will more likely need to subsidize the complementor participation, which makes them less likely to tolerate free-riding and thus close the system, which increases fragmentation relative to digital platforms. In some cases, fragmentation may be fine, but in others it may prove problematic for society.

The Internet of Things (IoT) is a good example of a setting that will face challenges similar to electric vehicles. The IoT embeds sensors and digital communications into everyday items (“things”) to enable coordination and optimization. The challenges echo the electric vehicle industry because adding software and electronic interfaces is expensive relative to items such as thermostats, leading to highly fragmented ecosystems like Tesla’s. Social welfare improvement from IoT might best be captured at a municipal, regional, or even national and international scale, driving a likely policy intervention to open up systems through the creation of standards. But that can create a prisoner’s dilemma in the short run, disincentivizing platforms from subsidizing complementors and investing in ecosystem growth until standards are settled.

Another example is business-to-business (B2B) platforms. By their nature, business customers have more complex needs than consumers. For example, business customers create much more complex orders for their complementor suppliers to fulfill. They are also more actively engaged with a third side of the market, logistics providers. Based on an analysis by two of our authors of B2B platform startups in a recent article, it appears that this may lead to fragmentation of the market by industry segment because domain-specific knowledge can reduce transaction costs sufficiently to reduce economies of scale. 33 To provide a specific industry example, consider the rapid growth of agricultural platforms to track seed and fertilizer usage, to help farms optimize their operations, and to provide easier access to markets. 34 There is a contest underway between platforms provided by capital equipment manufacturers such as John Deere, consumable input manufacturers such as BASF and Monsanto, and third-party operators such as Farmers Business Network, major technology firms, and commodity trading systems. 35 Decisions of standards, coalitions, openness, and more will all be influenced by standard economic forces that have shaped the industry for decades. However, these decisions are increasingly affected by platforms, and industry participants will have to add that lens to their toolkit as they develop their plans.

Conclusions

The electric vehicle story provides an example of how platform strategies can disrupt incumbent firms, even in large and established industries. The example also shows that platform strategies go far beyond digital. Businesses must apply the principles of platform strategies in a deliberate manner to create diverse ecosystems while avoiding the trap of assuming that all platforms are the same. Given the network nature of the emerging EV market, the high need for platform market coordination, and the potential for lock-in or lock-out effects, governments need to pay close attention to make sure the industry evolves in a way that is aligned with society’s goals, especially with respect to reducing carbon emissions.

If the traditional automakers do not leverage their quality and potential scale advantages in producing electric vehicles immediately, preferably in tandem with investing in open charging solutions, they will leave Tesla with two major competitive advantages. First, Tesla will have produced the most EVs to date, meaning it will continue to improve scale economies. Second, Tesla has a well-developed charging network that will provide substantial competitive advantage as it works to extend its reach into additional areas such as autonomous driving.

Footnotes

Notes

Author Biographies

Edward G. Anderson studies engineering economics in platform industries and their contribution to supply chain innovation at the University of Texas, where he is the Mr. and Mrs. William F. Wright, Jr. Professor for the Management of Innovative Technology and Director of Supply Chain Academic Programs at the McCombs School of Business (email:

Hemant Bhargava studies and teaches platform and technology strategy at the University of California Davis, where he is the Suran Chair in Technology Management and Director of the Center for Analytics and Technology in Society (email:

Jonas Boehm manages TWAICE Technologies’ strategic ecosystem globally and is a Fellow at the World Economic Forum. He holds a Ph.D. from the University of St. Gallen (email:

Geoffrey Parker studies the economics of network effects and the strategy of platform markets at Dartmouth College, where he is a Professor of Engineering and Executive Director of the Master of Engineering Management program (email: