Abstract

This article complements company-level approaches on the explicitization of Corporate Social Responsibility (CSR), zooming out to the national institutional level. We draw on qualitative data collected during several research stays in Japan, a case with a recent uptake of “explicit” CSR, where, historically, companies focused on “implicit” CSR. We present an empirically grounded framework for CSR explicitization at the national institutional level, involving three dimensions of changes: (a) ideas around CSR, (b) modes of evaluation of CSR, and (c) structures of control over CSR. In Japan, this process has been driven by the government, orchestrating these changes. Our framework contextualizes earlier understandings of CSR explicitization, allowing critical examination in relation to socio-political developments and providing the grounds for future comparative analysis of CSR explicitization. Furthermore, we add to the literature on the government-CSR nexus, introducing the notion of ideational steering as a new mode of government orchestration and shedding light on the role of financial market actors as co-regulators of CSR.

Keywords

Presently, we can observe an increase in explicit Corporate Social Responsibility (CSR) practices in countries previously described as having a tradition of implicit CSR. This change—or “explicitization” of CSR—has been conceptualized as a redefinition of traditionally “implicit CSR expectations into explicit CSR terms” (Matten & Moon, 2020, p. 18). It is most often observed in the multiplication of CSR reporting or the use of various social and environmental performance indicators as an explicit proof of heretofore implicit institutional expectations. However, what does such explicitization mean for the ability of CSR to address major societal challenges? Answering this question requires an understanding of the explicitization of CSR as it relates to other socio-political developments in a given national institutional context (de Bakker et al., 2020).

So far, however, CSR explicitization has been looked at mainly at the company level (e.g. Shabana et al., 2017), focusing on shifts in company-level practices, such as non-financial reporting. While some of these studies acknowledge that changes in CSR do not take place in a vacuum, they tend to look at the institutional context as solely an “input factor” (Hiss, 2009; Höllerer, 2013). In other words, they identify institutions as a driver for company-level changes but do not focus on changes in institutions as the main level of analysis. This leaves us with a somewhat de-contextualized view of CSR explicitization, whereby the institutions shaping CSR are treated as context rather than the objects of theorization in their own right (Jackson et al., 2019). This overemphasizes company discretion while the national institutional context remains undertheorized, disregarding the critical roles of both formal and informal institutions, such as government policies and agency (Knudsen & Moon, 2017, 2022), as well as norms and shared understandings of CSR (Campbell, 2007; Matten & Moon, 2008).

In this article, we zoom out from the company level to the national institutional level as our main unit of analysis, specifically focusing on what explicitization of CSR at the national institutional level involves and how this process unfolds. We draw on CSR literature from a comparative institutional perspective (e.g. Matten & Moon, 2008, 2020) and that on the CSR-government nexus (e.g. Knudsen & Moon, 2022; Kourula et al., 2019). These streams of research have significantly extended our understanding of the embeddedness of CSR in the national institutional setting. They have sensitized us to acknowledge the agentic nature of not only businesses but also other societal actors for shaping CSR, particularly governments. Such focus pinpoints changes at the national institutional level, specifically the “formal and informal rules, monitoring and enforcement mechanisms, and systems of meaning” (Campbell, 2004, p. 1), and how these are shaped by the government in interaction with other actors.

Empirically, we investigate the case of Japan over the past two decades, looking at how the historically implicit notion of CSR has become increasingly explicit (Mun & Jung, 2018; Suzuki et al., 2010). While Japan is certainly not the only country where this has happened (for Germany, see Hiss, 2009; for Austria, see Höllerer, 2013), it is well suited for CSR explicitization theorization at the national institutional level due to its government’s relatively strong involvement in economic matters (Brejnholt et al., 2022; Gond et al., 2011). We draw on data collected during several research stays in Japan, in particular qualitative interviews and a rich set of documents, collected with or drafted by government, companies, investors, employee and employer associations, and non-governmental organizations (NGOs); and notes taken at industry events.

Our findings contribute to the literature on CSR explicitization and that on the government-CSR nexus. We add an empirically grounded framework that depicts CSR explicitization as three complementary and interdependent changes at the national institutional level: changes in (a) the ideas around CSR, (b) the modes of evaluation of CSR, and (c) the structures of control over CSR. Complementing earlier studies on company-level explicitization (e.g. Hiss, 2009; Höllerer, 2013), we contextualize explicitization, enabling its more critical examination in relation to socio-political developments and comparative analysis of CSR explicitization. And we shed light on the so far unacknowledged role of the government in national-level CSR explicitization. Our contribution to the literature on the government-CSR nexus (e.g. Knudsen & Moon, 2022; Kourula et al., 2019) focuses specifically on government CSR orchestration (Eberlein, 2019; Schneider & Scherer, 2019) by introducing the notion of ideational steering as a new facilitative mode of governance. Finally, we shed light on the role of financial markets as regulatory intermediaries (Abbott et al., 2016, 2017).

Theory Section

From Implicit to Explicit CSR

Matten and Moon’s (2008) differentiation between implicit and explicit CSR is one of the most cited concepts in related research. 1 Defining CSR as the “policies and practices of corporations that reflect business responsibility for some wider societal good” (Matten & Moon, 2020, p. 12), the two scholars describe implicit CSR as values, norms, and rules that businesses adhere to because these are either codified and required by law or taken-for-granted social expectations concerning the roles and contributions of corporations (Matten & Moon, 2008, pp. 409–410). In contrast, they describe explicit CSR as clearly communicated, voluntary policies that businesses might be motivated to engage in deliberately because of incentives and opportunities provided by their institutional environment (Matten & Moon, 2008, pp. 409–410). CSR literature has widely used the distinction between implicit and explicit CSR to describe differences across national institutional contexts (e.g. Aguilera & Jackson, 2010; Brown & Knudsen, 2015; Höllerer, 2013; Koos, 2012; Morsing & Spence, 2019). Whereas explicit CSR tends to be linked to liberal market economies like the United States, implicit CSR is associated with continental European corporations, located inter alia in Scandinavian countries and Germany, as well as in Japan (Matten & Moon, 2008).

Against the background of CSR developments in the last decade, scholars have taken an increasing interest in the development of implicit and explicit CSR (Matten & Moon, 2020). Particular attention has been paid to the explicitization of CSR, which consists of adapting explicit CSR practices and reframing what has traditionally been part of the implicit expectations of the institutional environment (Matten & Moon, 2020). Examples include the increasing communication of CSR through non-financial reports, and the use of various social and environmental performance indicators as explicit proof of heretofore implicitly granted responsibilities.

So far, explicitization has mostly been perceived as company-level change in CSR policies and practices—both in its original conceptualization (see Matten & Moon, 2020, pp. 18–20) and in empirical work describing the dissemination of explicit CSR in traditionally implicit CSR countries. For instance, Shabana et al. (2017) examine the spread of CSR reporting among Fortune 500 companies. These studies tend to portray the uptake of explicit CSR as a strategic choice by companies, looking at CSR explicitization as somewhat decontextualized. Even those studies that take an institutional perspective on explicitization (Hiss, 2009; Höllerer, 2013) mainly focus on what companies do: how CSR is communicated in their annual reports (Höllerer, 2013); or the extent to which they engage in voluntary CSR such as introducing corporate codes of conducts to their supply chains (Hiss, 2009). The national institutional context, though regarded as important in these studies, has largely remained an “input factor” for company-level changes, leaving changes in the institutional context itself largely undertheorized. While not discounting prior studies and their relevant insights into how and why companies might move from one form of CSR to another, we lack an understanding of the changes in the national institutional context that accompany company-level explicitization. In other words, we lack detail of what CSR explicitization at the national institutional level involves and how this process unfolds—a limitation that is also acknowledged by Matten and Moon (2020, p. 23).

This shortcoming is striking, not least given the strong emphasis on the national institutional context in the original formulation of implicit and explicit CSR. Matten and Moon’s (2008) focus on the national institutional context reflects a rich tradition of research that investigates cross-national differences in CSR (e.g. Brown & Knudsen, 2015; Campbell, 2007; Gond et al., 2011; Jackson & Apostolakou, 2010; Jackson et al., 2020; Koos, 2012). Scholars investigating CSR from a comparative institutional perspective have deployed similar theories to capture the national institutional level, most notably the National Business System (Whitley, 1992, 1999) and the Varieties of Capitalism (Hall & Soskice, 2001) frameworks. What these frameworks share is the recognition that how corporations treat their stakeholders depends on the institutions within which they operate. Historically grown national institutional contexts both constrain and enable relations between businesses and other stakeholders and constitute a relevant setting in which CSR—including CSR explicitization—is embedded and by which it is shaped.

Consequently, research in that tradition demonstrates not only the relevance of the national institutional context for shaping company-level CSR but also points to the national institutional context as an important level of analysis in its own right. This is crucial because insights on explicitization at the national institutional level would provide critical ground for future work on the wider political significance of the increase of explicit CSR practices at the company level. Such a complementary perspective on explicitization also seems important for CSR research more generally. Against a situation where CSR became a pervasive phenomenon with a quasi-institutional character (Bondy et al., 2012), company-level changes are often taken as rather “neutral,” driven by economic rationales or legitimacy motives. Insights on explicitization at the national institutional level can contextualize such company-level research (Jackson et al., 2019) by inter alia pointing to the potential challenges that go hand in hand with explicitization. For example, the change from a strong tradition of implicit towards more explicit CSR is associated with a dis-embedding of firms from regulatory frameworks (Hiss, 2009), with the resulting voluntary CSR seen as unreliable and reifying rather than capable of limiting the negative consequences of capitalist markets (de Bakker et al., 2020; Schneider, 2020).

CSR Explicitization Conceptualized at the National Institutional Level

Comparative institutional literature broadly understands the national institutional context to “consist of formal and informal rules, monitoring and enforcement mechanisms, and systems of meaning” (Campbell, 2004, p. 1), defining the environment wherein CSR takes place and by which it is shaped. Our theoretical conceptualization of the national institutional level takes this understanding as a starting point and builds on prior empirical studies investigating changes in CSR at the national institutional level. Here, a variety of studies have examined various factors likely to be relevant for national-level explicitization, without per se linking them to a process of explicitization.

For instance, the co-construction of the idea of CSR in the political arena (van den Broek, 2024) and the changes in systems of meaning of CSR in the national discourse have been highlighted (Lohmeyer & Jackson, 2024). This includes an increase in instrumental motives for promoting CSR, which are deemed to be relevant for the shift from implicit to explicit CSR. Others have underlined that the institutionalization of powerful tools such as CSR standards and metrics can play a performative role in the commensuration of sustainability reporting as a key component of explicit CSR (e.g. Gond & Brès, 2020; van Bommel et al., 2022). Moreover, scholars have zoomed in on the construction of “markets for virtue” as a powerful structure to incentivize CSR (e.g. van Bommel et al., 2022). Such developments go hand in hand with a change in who has influence over CSR, with, for instance, consultants playing a crucial role in shaping the CSR market, including its commodification (Brès & Gond, 2014). While these changes have mostly been looked at in isolation, a consolidated view of how these changes relate to and complement each other seems crucial for theorizing national institutional-level CSR explicitization.

The above studies pointed to several actors crucial for driving CSR-related changes: namely, companies (Kaplan, 2015) and industry associations (Kaplan, 2023; Kinderman, 2012) but also consultants (Gond & Brès, 2020) and civil society actors (e.g. Lohmeyer & Jackson, 2024). More recently, CSR literature has brought attention to the role of governments in steering CSR and changing established CSR practices (Brejnholt et al., 2022; Cashore et al., 2021; Gond et al., 2011; Knudsen & Moon, 2017, 2022; Kourula et al., 2019; Schneider & Scherer, 2019). Although CSR has never taken place in a regulatory vacuum and has always existed in relation to the law, over recent years governments seem to have been “taking more active roles in the governance of business conduct” (Kourula et al., 2019, p. 1,105), becoming a strategic actor for the governance of CSR (Giamporcaro et al., 2020; Shin & Gond, 2024).

Because government intervention in CSR is often relatively indirect (Schneider & Scherer, 2019), the concept of “government orchestration” has recently gained popularity in CSR research (Eberlein, 2019; Giamporcaro et al., 2020; Shin & Gond, 2024). Originating in political science (Abbott & Snidal, 2009; Abbott et al., 2016, 2017), government orchestration is defined as a “wide range of directive and facilitative measures designed to convene, empower, support, and steer public and private actors engaged in regulatory activities” (Abbott & Snidal, 2009, p. 510). Government orchestration includes not only governments steering CSR policies but also the constellation of other actors’ involvement (e.g. Abbott et al., 2017; Giamporcaro et al., 2020). A common government move is to steer various “regulatory intermediaries,” including NGOs, media, investors, and quasi-public organizations (Giamporcaro et al., 2020). Instead of the government directly being involved in steering CSR at the company level, such intermediaries are strategically mobilized by the government as well as promoted and empowered to become co-regulators.

Taken together, these studies suggest that the notion of CSR explicitization might gain from a perspective that embeds company-level investigations within a national institutional context. Previous research informs us about a variety of national institutional changes that are likely to be relevant for the development of a rather implicit CSR tradition toward more explicit CSR practices. It also makes us aware of the broad set of actors potentially involved in changes to CSR within a national institutional context, especially when the government takes a significant role. Here, government orchestration seems particularly beneficial in understanding the role of the government, also in relation to its more indirect forms of engagement and the involvement of other actors.

Empirical Study: Context, Method, and Data

We employed a theory-generating qualitative design to better understand national institutional-level CSR explicitization. Taking Japan as our case, we examined how, over the past two decades, the country’s historically implicit notion of CSR has become increasingly explicit (Mun & Jung, 2018; Suzuki et al., 2010). Japan is particularly suitable for understanding national institutional-level CSR explicitization for several reasons. First, Japan represents a revelatory case for a larger group of countries (for Germany, see Hiss, 2009; for Austria, see Höllerer, 2013) that were in a relatively similar situation (at a high level of abstraction), that is, showing a high degree of implicit CSR around the year 2000 (Matten & Moon, 2008), before explicit CSR practices became widespread around the world (Shabana et al., 2017). Second, it is fruitful for our study because its government has a relatively strong hold on the country’s economic matters (Brejnholt et al., 2022; Gond et al., 2011; more details follow below). This led us to expect at least some degree of government engagement in CSR explicitization at the national institutional level. Finally, in focusing on the Japanese case, we responded to recent calls suggesting a need to broaden our understanding of the dynamics of CSR beyond central-European and U.S. contexts (Matten & Moon, 2020, p. 23).

The Case of Japan—Changes in National Institutional Context and CSR

Long-lasting stakeholder relationship, often referred to as a stakeholder-oriented system (Dore, 2000; Jackson & Miyajima, 2008), were a key historical characteristic of the Japanese economic system. A term that encapsulates the relevance of stakeholders is that of the “community firm.” In recent decades, remarkable changes toward greater capital orientation have taken place. Next to changes in stakeholder relationships (Jackson & Miyajima, 2008) and ownership (Ahmadjian & Robbins, 2005; Jackson, 2005; Miyajima & Saito, 2021), Ahmadjian (2000) notes a “widespread acceptance, at least in rhetoric, that Japanese firms needed to adopt a ‘global standard’ of corporate governance” (p. 65). The here-indicated need for change refers to what has become known as the “lost decades,” which provided a strong impetus for societal changes (e.g. Whittaker, 2024). Importantly, however, it is worth noting that not all Japanese companies put such changes into practice but that a large proportion of Japanese corporations have remained “hybrid,” combining principles of market-based and relational forms of business exchange (Aoki et al., 2008; Miyajima, 2012, 2022).

Japan shows striking parallels to other coordinated market economies like Germany’s. Simultaneously, there are several stark differences between the Japanese way of doing business and a market-based system like that in the United States (Hall & Soskice, 2001; Jackson & Moerke, 2005; Kang & Moon, 2012). The particular focus on long-lasting relationships with various stakeholders (owners, employees, and suppliers, among others) has long been preserved by the “administrative guidance” of the government, which promotes a “cohesive and solidaristic model of national political economy” (Jackson & Miyajima, 2008, p. 5). A long tradition of research on the Japanese business system has emphasized the critical role of the government (Aoki, 2001; Culpepper, 2010; Vogel, 2006). Interestingly, despite changes in the Japanese business system, recent typologies of government involvement in economic activities still indicate a strong coordinating mechanism through “proactive intervention in the production processes and the functioning of the markets” (Wright et al., 2021, p. 7). Japan still shows high levels of statism (intervention and market guidance), as highlighted by one of our interviewees: “So, I think Japanese society is [a] government-cantered driven society.” (CSR expert/consultant 4). Yet we also notice, both in our findings and in the literature, a departure from this situation in Japan, with government interventions becoming more indirect and showing greater market orientation (Lechevalier et al., 2019).

The Japanese government has initiated recent economic reforms, known as “Abenomics” (named after Shinzō Abe, Prime Minister of Japan 2006–2007 and 2012–2020). A relatively strong administrative body (Johnson, 1982) and above all, more recently, the power of the Cabinet Office of the Prime Minister (Takenaka, 2021) has bundled policy formulation capacities. However, as Culpepper (2010) summarizes, these reforms were such that “business and government jointly pushed for regulatory changes that gave Japanese companies more options” (p. 118). Potentially antagonistic actors were relatively weak or fragmented (Maeda & Reed, 2021), also because neo-corporatist institutions lacked vigor (Gond et al., 2011). Labor unions had lost their “collective bargaining capability and been reduced to a consultative role in some major firms” (Dore, 2005, p. 442). Civil society and NGOs also had a very weak position, due to being only loosely embedded in the policy-making network (Foljanty-Jost, 2005). This was echoed in our data as well, where NGOs were quite consistently referred to as irrelevant by our interviewees, with, for instance, one CSR consultant stating that “Japanese companies do not feel the risk from NGOs. Because we think, [in] Japan, NGO or NPO has no power.” (CSR expert/consultant 1). Likewise, NGOs themselves described their role as difficult due to, inter alia, a historically challenging funding situation, a lack of public support and trust, and comparatively limited membership base, leading them to describe themselves as “immature” especially with regard to their ability to influence policy (CSO Network Japan, 2003, p. 7).

Regarding the role of CSR in Japan, and in accordance with Matten and Moon (2008), the Japanese business system historically reflected an implicit form of how corporations take responsibility for their stakeholders. Within the implicit model, for instance, a company’s responsibility toward their employees is inscribed into the institutional environment through regulation as well as normative and cognitive institutions. This implicit notion of responsible business has existed since the Edo period (from 1603 to 1868). Historically, it has been defined as the philosophy of “Sanpo Yoshi,” which literally translates as “good on three sides”—for the buyer, the seller, and society: “Sanpō-Yoshi” refers to being good (yoshi) to urite (seller), kaite (buyer) and seken (society). Some may think that CSR in Japan seems slow but I think that some things are taken for granted and are in some cases not formulated as “CSR.” (union representative 2).

This notion differs remarkably from the modern Anglo-Saxon notion of CSR, with its emphasis on “voluntary” corporate activities. Historically, Japanese corporate responsibility was rather implicit both in its intent (as a response to norms and regulations) and the language used to describe it (the philosophy of being good to stakeholders).

Despite such a long-standing implicit CSR tradition, the Anglo-Saxon notion of corporate responsibility was introduced into the Japanese context as a response to its growing popularity in the United States and Europe during the 1990s. Despite some skepticism of Japanese managers vis-a-vis the Anglo-American notion of CSR (Fukukawa & Teramoto, 2008), interest in explicit CSR “increased rapidly and concrete action was taken” within Japanese companies (Tanimoto, 2004, p. 161). Corporate responsibility reporting took off, starting with environmental reporting. Companies also began setting up CSR departments and functions (Fukukawa & Teramoto, 2008): the first is said to have been at Ricoh in 2003 (Kawamura, 2004, p. 7). In the early introductory stages, there was little to no integration of CSR into overall management processes, however (Tanimoto, 2013). Socially Responsible Investment (SRI) developed slowly in the early 2000s (Solomon et al., 2004), gaining momentum over the years, with a clear and steep increase after 2014 (Arefeen & Shimada, 2020). Business associations became particularly active following several corporate scandals in the late 1990s and early 2000s and subsequent public demand for CSR (Fukukawa & Teramoto, 2008; Kawamura, 2004; Solomon et al., 2004, p. 559).

Data

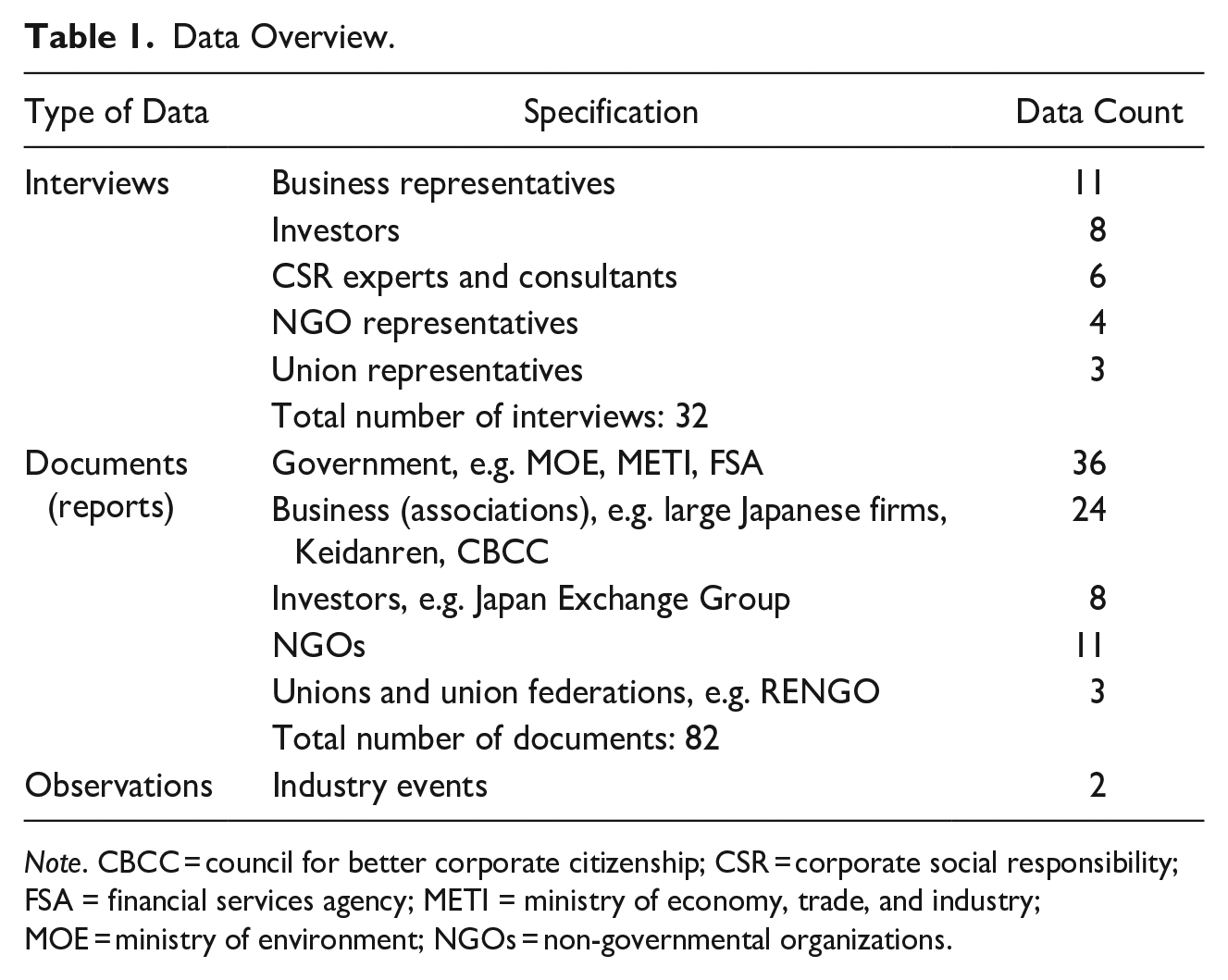

Data was collected by the authors during several research stays in Japan from 2016 to 2018. Our data comprise 32 qualitative face-to-face interviews with key actors engaged in CSR in Japan, namely business representatives, representatives of employee and employer associations, investors, CSR experts and consultants, and NGOs (see Table 1 for an overview of our data). For firms, we focused mainly on large, internationally oriented Japanese firms from various industries and talked to representatives either responsible for CSR or holding management functions that involved some responsibility for CSR. For employer and employee associations, we focused on peak associations such as RENGO, the Japanese Union Federation, or Keidanren, the Japan Business Federation, which brings together some 1,500 of Japan’s leading companies, major nationwide industrial associations and regional economic organizations, as well as its CSR body, the council for better corporate citizenship (CBCC), established in 1989. When it comes to investors, we focused on large Japanese investment companies, such as Nomura Asset Management or Daiwa Asset Management. Despite an increasing presence of international investment companies such as Blackrock, Japanese institutional investment companies continue to play a leading role in Japan. We also talked to representatives of socially responsible investment companies. Given their broad knowledge on the development of corporate responsibility in Japan, we also talked to several CSR experts and consultants, including consultants of large consultancy offices focused on CSR issues, but also policy advisors and representatives of research institutes focused on CSR or sustainable development more broadly. For NGOs, we talked to representatives of NGOs, including one NGO network, involved in CSR and sustainability.

Data Overview.

Note. CBCC = council for better corporate citizenship; CSR = corporate social responsibility; FSA = financial services agency; METI = ministry of economy, trade, and industry; MOE = ministry of environment; NGOs = non-governmental organizations.

Interview data is complemented by numerous secondary data: company reports (e.g. annual reports, non-financial reports, and codes of conduct); government reports 2 (e.g. central policy papers such as the Stewardship and Corporate Governance Code and related public consultations, including government responses to that, ministerial statements, and discussion papers); and guidelines and reports published by employee and employer associations as well as investors. We also carried out participative observation at two industry CSR events, during which extensive field notes were taken. Our data focus on developments in the decade 2008 to 2018, with a limited number of documents reaching further back (2004) or produced more recently (2023).

It is important to underline that both in the interviews and the documents we analyzed, actors not only described their own views on the matter but also extensively reflected on the roles of other actors. For example, business associations stressed the important role of the Abe administration in spreading socially responsible investment, or unions commented on the silence of NGOs on certain matters. Therefore, we learned about the roles of all actors not just through their own sayings and doings but also through the eyes of others.

The interviews were semi-structured; they explored the meaning and organization of CSR as well as the roles and interests of the various actors vis-à-vis CSR. While the interview guideline initially revolved around CSR and changes thereof, interestingly, the interviewees regularly brought up developments within the Japanese institutional landscape. This led us to adapt the interview guideline iteratively, focusing more and more on the link between CSR and broader institutional changes. Hence, we followed our interviewees’ interpretations, focusing on what they deemed important in terms of CSR changes and drivers thereof. Interviews were conducted in English (at times with the help of an interpreter), audio-recorded (except for one case, where extensive notes were taken), and transcribed.

A few comments are warranted regarding the collection of data in the Japanese business world (especially for interviews). During our research stays, our “otherness,” that is to say, the feeling or projection of being an outsider to the dominant group in a given environment (Özbilgin & Woodward, 2004, p. 677), became starkly apparent when we conducted interviews and visited companies and events. Given that information gained during interviews and events is co-constructed by the researcher and the researched, our “being different” might both have helped and, at times, hindered data collection, as well as interpretation (e.g. Essers, 2009). It may have helped us gain access to our primarily male, Asian, middle-aged interviewees. However, it may have influenced the information we received from our interviewees, who might have perceived us as “non-experts” or “inexperienced” in a business context that is still very much dominated by middle-aged men (see also Fukukawa & Teramoto, 2008, p. 137).

Our otherness also extended into the very mixed ability to communicate in English with our interviewees. At first, we felt that some of our interview requests were being rejected because our emails were written in English: those approached possibly felt unable to give an interview in English or were unsure about it. Our interview data may therefore be biased toward English-speaking (thus potentially better educated) interviewees. Once we gained access to interviewees, the information we received may have been influenced by either the interviewees’ proficiency in English (e.g. some interviewees expressed themselves in rather basic terms and, therefore, possibly provided us with a less complex story) or the disruption of communicating with each other through an interpreter (e.g. details potentially getting “lost in translation”). Here, extensive reliance on our document data, participating in events, and talking to colleagues who were familiar with the topic and the context, were helpful for filling in missing details. Some of these difficulties will stand out in what might be perceived as “simple” or sometimes “incorrect” English in the quotes. We have sensitively “ironed out” sentences where we felt it necessary while paying close attention to the intended meaning.

Analysis

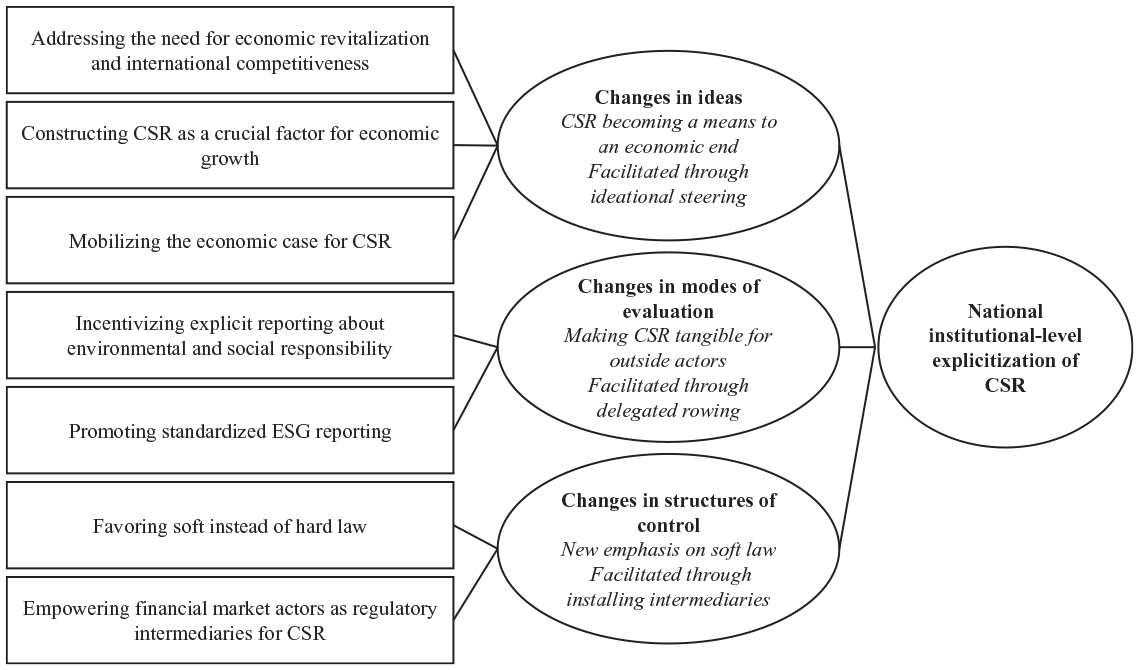

Data analysis was oriented toward unpacking shifts in CSR at the national institutional level. Using MAXQDA, a software tool for qualitative data analysis, we followed an iterative coding process to identify relevant trajectories within the broader CSR developments. After several rounds of coding and of discussing our codes in light of extant literature, we found the national institutional-level shift from implicit to explicit CSR best conveyed by three dimensions of institutional changes around CSR: changes in ideas around CSR (i.e. the way in which CSR is understood); changes in modes of evaluation of CSR (i.e. how CSR is evaluated); and changes in structures of control over CSR (i.e. how and by whom CSR is governed) (see Figure 1 for our data structure and Table A1 in Appendix for additional quotes illustrating our data structure).

Coding structure.

During a second round of coding, we have dived deeper into these three dimensions, focusing on the actors involved. This showed that changes were heavily influenced by the Abe administration as an orchestrator of national institutional-level CSR explicitization. Going back and forth between the literature on orchestration (e.g. Abbott et al., 2017; Giamporcaro et al., 2020) and our data, we identified the Abe administration engaging in three modes of orchestration: two of which were discussed in earlier studies on government orchestration, the other not previously mentioned. First, the Abe administration engaged in, what we call, ideational steering, that is, the mobilization of ideas to unite actors behind government reform, as a new mode of facilitative orchestration to change ideas around CSR. Second, the government engaged in delegated rowing: “the mobilization of state-controlled organizations to change market actor behavior” (Giamporcaro et al., 2020, p. 290) to change modes of evaluation. Third, the Abe administration installed financial market actors as intermediaries to co-regulate CSR, thereby changing control over CSR (Abbott et al., 2016, 2017).

Findings: CSR Explicitization at the National Institutional Level in Japan

Our findings suggest that CSR explicitization at the national institutional level in Japan can be best summarized as changes in three dimensions. First, the process involved the introduction of a new meaning of CSR (ideas) that has elevated CSR from taken-for-granted business activities to a means in national economic policy. Second, we observed a change in CSR evaluation (modes of evaluation), from it being assessed through interpersonal relations to it becoming suitable for insertion into the financial market and assessed by outside actors. Third, the process includes a change in how and by whom CSR is controlled (structures of control), installing the financial market as a new locus of control. These three analytically distinct but empirically overlapping dimensions can be understood as complementary and interdependent “ingredients” in the overall process of national institutional-level explicitization, complementing prior understandings of company-level explicitization. Our findings also show that these changes were orchestrated by the Abe administration, which referred to different modes of orchestration, including ideational steering, delegated rowing, and installing intermediaries.

In what follows, we present in detail our findings of the three dimensions of CSR explicitization at the national institutional level and the involvement of the government and other actors (see Table A1 in Appendix for additional quotes illustrating our data structure). Importantly, while we present the different dimensions and modes of orchestration in a sequential manner, they are, in fact, intertwined. Indeed, changes in ideas tend to take a somewhat precedential position against which the other dimensions are developed.

Changes in Ideas: CSR Turns into a Means for Economic Growth

The introduction of explicit CSR to the national institutional context of Japan has involved a significant shift in the meaning of CSR. While for many years CSR had been an interwoven part of the Japanese business culture reflecting societal norms and regulation, our interviewees pointed to the central role of a new idea of CSR, introduced by the Abe administration as part of the new national economic strategy. Although CSR changes were not its primary objective, the new national economic strategy played a key role in establishing a new idea of CSR in the Japanese economy.

The new national economic strategy, the Japan Revitalization Strategy, which the Cabinet approved in June 2013, may be seen as a response to the 2008 financial crisis and years of economic recession. The Abe administration engaged in a systematic effort

Neither are explicitly CSR codes but both codes refer to CSR. They mention environment, social, and governance (ESG) reporting as an important measure to realize the proposed Revitalization Strategy (Stewardship Code, 2014, p. 1). The codes thereby made CSR a topic of concern at the national level and established an idea of CSR as a means to an end. More specifically, both codes

The Abe administration

Changes in Modes of Evaluation: Tools and Instruments Making CSR Tangible for the Financial Market

For a long time, the Japanese national institutional context was known for a type of corporate responsibility that was evaluated through either interpersonal interaction, including board interdependencies and company reputation (e.g. Solomon et al., 2004), or mandated by legislation, particularly in the environmental sphere (business representative 2). As we will show below, part of the national institutional-level explicitization of CSR was the establishment of new modes of evaluation in the Japanese national institutional context, with the government incentivizing standardized CSR communication through which CSR became measurable and, ultimately, tangible for financial market actors.

To realize the idea of an “economic case for CSR,” the Abe administration began In the past, due to a lack of experience, due to a lack of communication between companies and investors, they didn’t care about ESG investment/ESG disclosure because they didn’t understand how important the ESG data is. Because they have not been asked such questions by investors. It’s simple, because their shareholders mostly were banks, Japanese banks. So, they didn’t care about ESG data. (CSR expert/consultant 2).

However, this changed when the Stewardship and Corporate Governance Code introduced standardized ESG reporting, described as “epoch-making events” (CSR expert/consultant 5). Both codes, thus, promoted a shift in how CSR was evaluated: “So far they [Japanese companies] are disclosing a narrative story, but from now on they need to show up with quantitative data linking to SDGs” (CSR expert/ consultant 2). A high-ranking union representative similarly described this shift, stating that Japanese companies had taken corporate responsibility for granted in the past: “in Japan [compared to the West] the organization is much more part of the social fabric [. . .]. Not now but in the past [. . .].” He went on to say that now this was changing, with companies needing to report in more standardized ways, because “they want to have an outfit . . . to show themselves to the global market” (union representative 1).

The standardization of ESG frameworks, which include popular responsibility issues such as working conditions but, also, governance-related matters such as board structure, meant that corporate responsibility had to be translated into standardized and quantifiable metrics (Schumacher et al., 2020). This, as our interviewees reported, allowed shareholders and stakeholders to evaluate and compare companies on the basis of their standardized CSR reporting: So in the past, for example for the consumer, they judged some products on the basis of the taste, or functions, or cost, or cool design or something. But regularly the consumer requires the producer to disclose where it is made, and what the product contains or something. So, as a result, the consumer can compare between product A and product B, even if it’s cheaper than this, still, if it was safer than this, the consumer chooses this one. So why the consumer can judge the decision? Because of disclosure. The same thing happened in investment [with ESG reporting]. So with ESG, transparent ESG factors, the investor can judge. Not only on the basis of the financial performance, past financial performance, but also non-financial data. So disclosure gives the element for stakeholders to judge. (CSR expert/consultant 2, emphasis by authors).

Our data show that it was the Abe administration that engaged in decisive efforts to make ESG reporting widespread and accepted, seeking to overcome the initial reluctance among companies and investors. Yet, it did so not by mandating reporting but rather by indirect measures. The one measure of indirect government steering that was described to us as the most crucial for the broad adoption of ESG reporting by almost all our interviewees was the integration of ESG demands into pension schemes (

As reporting is not only about the reception of tools and instruments by those disclosing but also about those using them in their investment, the GPIF’s endorsement was also highlighted as a significant step for domestic investors. For instance, a CSR expert argued that while “before, quite a minority of people in the financial industry were interested in ESG issues,” it was only when “GPIF finally signed PRI [that] quite a lot of asset management companies [have become] interested in ESG issues. So, it’s like top-down. It’s not bottom-up” (CSR expert/consultant 5). Others echoed the importance of GPIF’s endorsement: the head of the Japan branch of one of the largest international institutional investment companies recognized “quite a significant push” for investors to “take further consideration of ESG issues” (investor 2). This, as others reported lead to a “kind of a sudden big surge” in ESG investment (business 7). The relevance for investors also becomes visible as it encourages other investors to follow suit, further extending the spread of ESG. “The big move just came last yar, after the GPIF,” concurs an investor, “our big pension fund, has become the signatory [of UN-PRI]. So, that’s a significant, huge, giant leap” (investor 8). Also, the Labor Bank, in which the labor union deposits funds, endorsed the UN-PRI (union representative 2), giving ESG investment broader credence.

Others followed in promoting ESG reporting, with, inter alia, the Tokyo Stock Exchange (TSE) publishing the Practical Handbook for ESG Disclosure in 2020; and the Japan Exchange Group (JPX) launched a platform where listed companies and other interested parties can access ESG and sustainable finance-related information,

7

offering seminars for ESG disclosure, working groups around the uptake of ESG reporting, and events for financial institutions and investors. Such activities were perceived as necessary to catch up with global developments and to overcome the continuing reluctance of Japanese businesses to commit to ESG. Giving credence to both the intensity of diffusion efforts but also the strong belief in ESG reporting by its promoters, one interviewee referred to these as a form of “ministration”: So, I think of it as a “ministration.” So, CSR in the past was recognized as a concept. That’s why many Japanese companies believe they have CSR inherency. But nowadays [it is] becoming a business rule. [. . .] So if we didn’t realize that, maybe [we would be] missing business opportunities. So that’s why we need to educate about that here in Japan. (CSR expert/consultant 2).

Taken together, the government’s endorsement of ESG reporting has persuaded others to adopt or further promote this shift in how to evaluate CSR without resorting to coercion through hard law.

Changes in Structures of Control: New Emphasis on Soft Law, Empowering the Financial Market

CSR explicitization at the national institutional level has involved changes to the structures of control. Closely related to the aforementioned dimensions, the Abe administration, primarily by means of soft law with the Stewardship Code and the Corporate Governance Code, transferred power over corporate responsibility to the financial market and, in particular, institutional investors.

The Abe administration’s soft law approach to CSR was new to the Japanese context. Both the Stewardship Code and the Corporate Governance Code follow a “comply-or-explain approach,” and rely on a “principles-based” instead of a “rules-based approach,” underlining “self-motivated actions,” and meaning that the “aim and spirit” of these codes should be followed, rather than obeying them to the letter (Corporate Governance Code, 2015, pp. 4–5; Stewardship Code, 2014, pp. 3–4). (

Such emphasis on soft law could be interpreted as the government following a laissez-faire approach to CSR. Importantly, however, the Abe administration’s new soft law approach is embedded in an effort to

In particular, the Abe administration empowered the financial market by making Japanese companies an attractive investment. Toward this end, the Japanese Corporate Governance Code specified how to modernize company governance, establishing “fundamental principles for effective [. . .] ‘growth-oriented’ governance” (Corporate Governance Code, 2015 p. 3). These changes included, inter alia, a more relevant role for outside directors, strengthening disclosure and transparency as well as the dialogue between investors and investees, moving the Japanese corporate governance closer towards the Anglo-Saxon model: “We are pretty much on the UK model,” said one investor summarizing the changes introduced by the code (investor 8). A common motive for this change is based on companies needing to attract (more; international) investment, as opposed to the historically entrenched, bank-focused capital system: So, to do so the relationship between the company and the banks was almost gone. So, there was no space to welcome investments. So that’s why the governance code was released. To change the relationship between shareholders and companies as well as encourage the company to show off their long-term strategy to attract and offer investors. So this is the essence of the corporate governance code. (CSR expert/consultant 2).

This shifted the role of investors in the governance of Japanese companies: “The Japanese companies’ way of thinking [about] responsibility is something different from the Anglo-Saxon type of thinking. Not the shareholder may [be] in the first place. But he tends to [be] now” (investor 8). For CSR, the impact was notable. Our interviewees reported a closer orientation of companies’ CSR activities towards the financial market. As one CSR analyst mentioned, recently, “several Japanese corporations initiated ESG-IR [investor relations] meetings, like Ajinomoto or Omron. So, they noticed that these CSR or environmental management activities could be [of interest to] investors” (CSR expert/consultant 5). This is closely related to dimension 2 (change in modes of evaluation), since particularly standardized reporting has enabled CSR to become relevant for the financial market. Beforehand, this was only relevant to the very marginal Socially Responsible Investment (SRI) market in Japan (Solomon et al., 2004). 8

A Framework for CSR Explicitization at the National Institutional Level

Based on our empirical analysis of CSR in Japan, we have been able to zoom out from the otherwise dominant angle on company-level CSR explicitization to reveal CSR explicitization at the national institutional level. We ask what CSR explicitization on a national institutional level involves and how it comes about, with a particular focus on the role of the government in national institutional-level CSR explicitization.

Three Interdependent Dimensions of CSR Explicitization

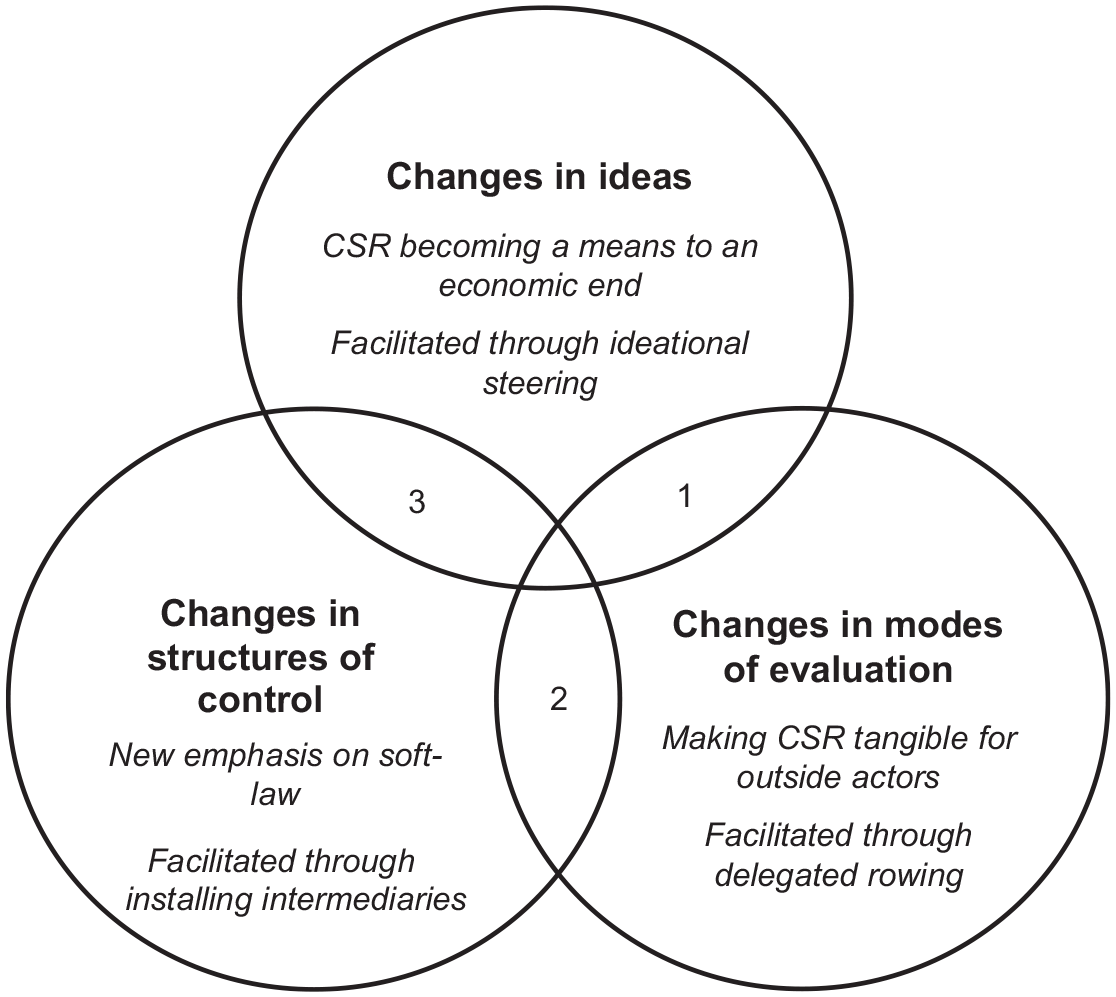

We identified three dimensions of CSR explicitization at the national institutional level (see Figure 2). First, changes in ideas refer to the changing meaning of CSR. In our case, CSR gained an instrumental meaning at the national institutional level due to its inclusion in Japan’s national policy for economic revitalization, presented as a lever for economic growth and international competitiveness. CSR, thus, was being portrayed as an economic case. Second, CSR explicitization at the national institutional level involves changes in modes of evaluation. The introduction of standardized reporting instruments to the national institutional context in Japan made CSR tangible and open to evaluation by outsiders. Here, ESG reporting in particular enabled outside stakeholders—notably investors—to measure and compare CSR. Third, changes in the structures of control refer to developments in who has authority over CSR. In the case of the Japanese national institutional context, this involved installing non-governmental regulatory intermediaries to govern CSR. With the government’s support, the financial market became a new locus of control for CSR. Financial market actors gained importance by integrating CSR into their investment decisions and in their dialogue with investees.

Explicitization of CSR at the National Institutional Level.

All three dimensions in themselves provide important angles for understanding CSR explicitization at the national institutional level, complementary to what has so far largely been described at the company level. What is more, we propose that cross-referencing changes in these dimensions highlights the potentially far-reaching impact of CSR explicitization. It is through such contextualization that we can begin to grasp the socio-political significance of CSR explicitization. We describe some of the most striking interdependencies, thereby referring to the overlap sections (numbered 1–3) in Figure 2. Importantly, Figure 2 describes the three dimensions—in the case of Japan—as overlapping, also pointing to their interdependency and the need to interpret each dimension in the context of the others.

Changes in Ideas and Modes of Evaluation (1)

Our findings point toward the complementarity of changes in ideas and modes of evaluation. For the realization of the “economic case,” the establishment of standardized modes of evaluation was necessary. Opening the traditional Japanese stakeholder system towards a stronger, explicitized corporate responsibility by disclosing CSR information in a standardized manner has allowed “outsiders” to evaluate and compare companies, thereby providing the ground for CSR to be included in consumption and investment decisions to realize the economic case. Such overlap should not be misinterpreted as natural given the possible alternatives. For instance, an instrumental approach to CSR for realizing economic growth could have also been possible through the promotion of the revival of the strong long-term, relationship-based way of doing business in Japan (i.e. the community firm, see Inagami & Whittaker, 2005). This approach would have led to a different, potentially more stakeholder inclusive pathway. Instead, embedding new modes of evaluation in an economic approach for growth and internationalization has resulted in targeting a specific set of outsiders, namely institutional investors.

Modes of Evaluation and Structures of Control (2)

Similarly, changes to the modes of evaluation and structures of control being developed hand in hand in the Japanese national institutional context have shaped CSR explicitization in particular ways. The government’s introduction of ESG reporting through the Corporate Governance Code and Stewardship Code, and promoting it through GIPF’s endorsement, put particular pressure on institutional investors to take up ESG measures while empowering them to oversee the ESG activities of Japanese companies. This is an important yet not inevitable overlap. Alternative changes to the modes of evaluation could have strengthened the role of other regulatory intermediaries. For instance, had the government stressed multi-stakeholder negotiation, civil society actors would have been able to reserve a seat at the table (Kaplan & Lohmeyer, 2021). Similarly, investors would have likely played a more minor role if the government would have chosen a hard rather than soft law approach, where the authority to evaluate company performance tends to remain with the state. Likewise, codifying company responsibilities in law can empower other stakeholders such as labor activists, who gain legitimacy and become stronger when human rights law is strengthened (Kahraman, 2018).

Changes in Ideas and Changes in Structures of Control (3)

In the Japanese national institutional context, the overlap between changes in ideas and changes ins structures of control was strongly supported by the orientation of the Abe administration’s economic policies. The changing nature and relevance of the financial market was one consistent factor in this respect, making the empowerment of investors seem inevitable. Nevertheless, this almost unique focus for investors is striking when compared to changes in, for instance, the European Union (Jackson et al., 2020), where civil society actors have also been included in the idea of evaluating business conduct.

CSR Explicitization at the National Institutional Level as Orchestrated by the Government

Secondly, our question concerned how CSR explicitization at the national institutional level comes about, and hence, how actors and their moves are involved in this development. Our results show that a variety of actors beyond only companies were involved. Hence, changes at the national institutional level reflect a collective process, albeit one in which the government plays a decisive role in orchestrating said changes. We highlighted these government moves in Figure 2.

The Abe administration engaged in three modes of orchestration. First, it undertook what we call ideational steering: the mobilization of ideas to unite actors behind government reforms or policies, as a new form of facilitative orchestration. The Abe administration shaped a discourse around the need for economic revitalization and, particularly, economic growth, promoting CSR as an important lever towards reaching these goals. Mobilizing the idea of the “economic case for CSR” served to unite actors behind its economic reforms. As we have shown, it was the idea of an “economic case for CSR” that other actors referred to. This does not necessarily mean that they agreed with it, but rather that it became so relevant that others took it up in their reference to CSR, while no criticism or alternatives were formulated either. Ideational steering was crucial for moving Japanese CSR explicitization in its particular direction.

Second, the government engaged in delegated rowing, mobilizing state-controlled organizations to change market actor behavior (Giamporcaro et al., 2020). In our case, for instance, the Abe administration promoted new modes of evaluation through the endorsement of ESG reporting by the Japanese public pension fund, thereby creating pressure on businesses to adopt these modes and isomorphic pressure for other investors.

And third, it engaged in installing intermediaries to co-regulate CSR. While the Abe administration has favored steering CSR by soft rather than by hard law, it simultaneously mobilized and empowered financial market actors as “regulatory intermediaries” (Abbott et al., 2017), enabling them to take control over CSR.

Discussion and Conclusion

In what follows we discuss how our empirically grounded framework of CSR explicitization at the national institutional level contributes, first and foremost, to literature on CSR explicitization. Beyond this, we discuss how our findings contribute to literature on the CSR-government nexus, especially that concerning government CSR orchestration.

Contributions to Explicitization Literature

Framework for CSR Explicitization at the National Institutional Level

Our first main contribution is to propose an empirically grounded framework for CSR explicitization at the national institutional level. We thereby respond to the recently renewed call by comparative institutional literature on CSR for a more dynamic understanding of implicit/explicit CSR (Matten & Moon, 2020). This complements literature on company-level explicitization (Hiss, 2009; Höllerer, 2013) in at least three ways.

First, zooming out from the company to the national institutional level delivers a “contextualized” view (Jackson et al., 2019) on the process of CSR explicitization (Matten & Moon, 2008, 2020). While focusing on this process from the company level might suggest such changes be the result of strategic choices by companies (thus overemphasizing company discretion) (e.g. Shabana et al., 2017), our framework highlights these changes to be part of developments at the national institutional level, pinpointed as changes in ideas, modes of evaluation, and structures of control. We show that the spread of explicit CSR communication at the company level can only be fully understood by placing these shifts in context, as this highlights the consequences of such a proliferation of CSR reporting. For instance, in the case of Japan, seeing an uptake of explicit reporting as part of the changes on the national institutional level allows to see them as part of a more general orientation toward the financial market, rather than cheerleading it as a civil-society serving increase in transparency.

Second, our framework establishes the connection between various national institutional developments. In particular, the complementarity and interdependence between processes of change at the national institutional level highlighted the wider socio-political implications of CSR explicitization. A rich literature exists that looks at macro-level changes around CSR more generally, that is, without focusing on explicitization in particular (e.g. Gond & Brès, 2020; Kaplan, 2015, 2023; Kinderman, 2012). This research has zoomed in on different dimensions of institutional change in isolation, highlighting for instance, changes in the meaning of CSR (e.g. van den Broek, 2024) or the uptake and related commensuration of CSR reporting (van Bommel et al., 2022). Our framework of CSR explicitization stresses the complementarities and interdependencies between these changes. For instance, earlier studies on standardized reporting have indicated how this is making CSR tangible for financial market actors (e.g. van Bommel et al., 2022). Linking such changes in the modes of evaluation to the shift toward a meaning of CSR as an “economic case” (changes in ideas) shows how this constituted an important factor for CSR to become an attractive area of engagement for institutional investors (changes in structures of control). This echoes insights from research on the “business case for CSR” (and similar concepts such as “shared value”) and its ideational power (Crane et al., 2014; de Bakker et al., 2020; Kaplan, 2020), which have been shown to “crowd out morality” in CSR (van Bommel et al., 2022), acting as ideas that different people can agree to (Wright & Nyberg, 2017) and make it challenging to voice alternatives (Lohmeyer & Jackson, 2024).

Third, the three dimensions of our framework—changes in ideas, modes of evaluation, and structures of control—could fertilize comparative studies, beyond our empirical case of Japan. Our three dimensions have their theoretical roots in the understanding of CSR institutions sensu Campbell (2004). While we would expect changes in the three dimensions highlighted in our model to happen in other cases of CSR explicitization as well (for Germany, see Hiss, 2009; for Austria, see Höllerer, 2013), the form of the identified dimensions, their relative importance and timing, and the constellations of actors involved is likely to differ across cases. While Japan has its very specific national institutional context, including the role of the government (Brejnholt et al., 2022; Gond et al., 2011), we see important similarities to other processes where, for instance, government had a role in pushing and enabling investors to increase their engagement in CSR (e.g. Giamporcaro et al., 2020).

We also note important boundary conditions. First, although explicitization is not unique to Japan, the country’s specific actor constellation and idiosyncrasies of the national institutional context are distinctive. For instance, in other contexts, we could imagine instances where other intermediaries such as consultants are key in transposing new ideas (Gond & Brès, 2020). Second, after years of extreme prosperity, the long Japanese recession created fertile soil for rather radical changes. Third, the governance system is politically and culturally rather consensus oriented. For instance, the Abe administration acted as a single actor (see Maeda & Reed, 2021; Takenaka, 2021) rather than a diverse set of parties. Hence, while being reflective of the idiosyncrasies of the Japanese context, we see our framework supporting future comparative investigations on CSR explicitization at the national institutional level, either in in-depth cases studies or comparative studies applying qualitative comparative analysis.

CSR Explicitization at the National Institutional Level as a Government Orchestrated Process

Our second contribution to explicitization literature emerges from our interest in how CSR explicitization comes about (i.e. the actors involved). We showed that rather than just involving companies, CSR explicitization at the national institutional level is a collective process, which—in the case of Japan—was decisively steered by the government. For capturing actors involved, the notion of government orchestration proved useful. It allowed us to understand the government as a strategic actor and to see how the other actors are steered (e.g. Abbott et al., 2017; Giamporcaro et al., 2020).

In Japan, the Abe administration empowered the financial market and enabled institutional investors to take over control of CSR (changes in structures of control), installing them as “regulatory intermediaries” (Abbott et al., 2017) in the governance of CSR, and in CSR explicitization more specifically. This connects with earlier studies on CSR in Japan, which have stressed institutional investors as the key drivers for an increasing uptake of CSR (e.g. Mun & Jung, 2018). Our findings do not contradict these studies but go beyond them by providing complementary insights into how the government provided the ground for institutional investors to play a key role in driving CSR (e.g. incentivizing ESG reporting and empowering the financial market). This was especially crucial in Japan’s bank-based financial system, which historically did not give such a prominent role to institutional investors (e.g. Solomon et al., 2004).

The financial market and its actors have only recently gained attention as co-regulators of CSR (for the French SRI market, see Giamporcaro et al., 2020). The empowerment of these actors, traditionally geared towards promoting private rather than public interests, might have powerful implications for CSR effectiveness. A rich literature on “financialization” links an increasing relevance of finance, financial markets, and financial institutions to consequences such as outsourcing (at the company level) or increasing inequality (at the societal level) (Davis & Kim, 2015; van der Zwan, 2014). For CSR specifically, the “imperative to satisfy investors” under financialization (p. 294) has been shown to steer CSR towards concerns prioritized by shareholders and away from stakeholder-related issues, including community welfare or labor protection (Jones & Nisbet, 2011), ultimately “crowding out” morality (van Bommel et al., 2022).

Contributions to Government-CSR Literature: Ideational Steering as New Form of Government Orchestration of CSR

Beyond contributing to CSR explicitization literature, we also advance literature on the government-CSR nexus (e.g. Brejnholt et al., 2022; Knudsen & Moon, 2017, 2022; Kourula et al., 2019; Shin & Gond, 2024) by further clarifying the decisive yet indirect roles of the government in CSR explicitization. We thereby respond to calls for a more nuanced understanding of the indirect modes of government involvement in CSR (Schneider & Scherer, 2019). Echoing prior research, our findings show that the Abe administration engaged in several forms of facilitative orchestration (see Abbott et al., 2016; Giamporcaro et al., 2020) to steer the national institutional-level process of explicitization. We observed modes of facilitative orchestration described in previous studies, including delegated rowing and the empowering of intermediaries (Giamporcaro et al., 2020; similarly, Shin & Gond, 2024). In this article, we introduce the notion of ideational steering as a new mode of facilitative orchestration, describing the mobilization of ideas to unite actors behind government reforms or policies. In the case of Japan, we saw the Abe administration introduce the idea of CSR as a path towards economic revitalization (an “economic case for CSR”), which particularly after years of economic recession presented an attractive idea for a variety of actors to follow government reforms. As discussed above, we see important parallels to what we know about the power of the idea of the “business case for CSR,” specifically its power to unite actors and to make it difficult to promote alternatives (as discussed in more detail above).

While previous orchestration literature has touched upon the relevance of ideas (e.g. Abbott et al., 2016; Eberlein, 2019), we feel highlighting ideational steering as a mode of orchestration in its own right is important. In the case of Japan, our analysis underlines that identifying ideas as a separate mode of orchestration, as compared to subsuming them into other modes (e.g. Eberlein, 2019; Giamporcaro et al., 2020), is crucial to showcasing the Abe administration’s specific objectives and priorities, and preferences for certain actors to become co-regulators. Thereby, ideational steering connects CSR orchestration to extant CSR literature highlighting the importance of ideas for grasping the directionality of CSR development more generally (Vallentin & Murillo, 2012; van den Broek, 2024) and linking ideas to the normativity of governance modes (Knudsen & Moon, 2022). For instance, the careful identification of ideational changes involved in explicitization allows to identify government decisions as part of broader neoliberal projects (e.g. Kaplan & Kinderman, 2020), including financialization and the privatization of regulation.

Furthermore, ideational steering refers to the diversity of indirect modes of government orchestration, and their different modi operandi as expressions of diverse forms of neoliberalism. For example, earlier conceptualizations of facilitative orchestration have mainly emphasized the use of rules, standards, or incentives (Abbott & Snidal, 2009; Abbott et al., 2016, 2017), which—although indirect—focus on government agency. Ideational steering, in contrast, relies on the mobilization of ideas, a relevant form of internalized neoliberal control (Amable, 2011). While powerful, ideas are much more elusive and, once taken up by other actors, become a moral imperative freed in part from government sovereignty. Hence, we see a the need for better understanding the agency of governments across different modes of (indirect) orchestration, including their control over corporate conduct.

Limitations

In addition to the discussed boundary conditions, our article comes with several limitations. Our main limitation relates to the question of what the observed CSR explicitization implies for the historically entrenched implicit CSR mode in Japan. Importantly, explicitization is not meant to describe the replacement of implicit with explicit CSR but rather the uptake of explicit CSR in a traditionally implicit CSR context (Kang & Moon, 2012). Yet, while we focus on instances where explicitization was most evident, it goes beyond our empirical scope to account for a potential erosion of the former implicit model. Questions about what Matten and Moon (2020, p. 8) refer to as hybridization, whereby CSR reflects “various and varying balances of explicit volition and implicit compliance,” are not tackled. However, we share the feeling that such CSR hybridization is relevant for comprehensively describing the Japanese context. Examples of other studies on CSR (e.g. Fukukawa & Teramoto, 2008) or the Japanese economy more broadly support such a dynamic of hybridization: Aoki et al.’s (2008) observation on how U.S.-based elements of corporate governance are layered over the established Japanese system, or Mun and Jung’s (2018) description of how diversity programs in Japanese multinationals have only been adopted in top management, with lower tiers remaining male-dominated.

Next, our data depicts CSR explicitization at the national institutional level in Japan as a rather consensual process, with little resistance from civil society or other actors. We are confident that the lack of active dissent as regards CSR explicitization is part of the empirical reality of the Japanese case. For instance, our interviewees explicitly mentioned the lack of dissent as well as the comparatively powerless role of actors such as unions and NGOs. Moreover, the described changes taking place against the background of the “two lost decades” and a general agreement around the necessity to change (Ahmadjian, 2000) are likely to have lowered resistance to change. However, we are also sensitive to the limitations of our understanding, as “outsiders,” of culturally engrained utterances of disagreement and conflict that are known to be less overt for Japan compared to other countries. This is not least the case, because in other, traditionally implicit contexts the introduction of explicit forms of CSR has raised resistance among civil-society actors (Kaplan & Lohmeyer, 2021) or conservative business elites (Höllerer, 2013).

Lastly, while we have included the ministries most relevant for CSR in our analysis, we did not deal with the dynamics between different ministries or political parties to this process. This might create the impression of an overly homogenous portrayal of the government. To some extent, this is justified given the strong administrative guidance the Abe administration has become known for (Wright et al., 2021). However, it also comes at the cost of understanding potential frictions related to the government’s moves.

Avenues for Future Research

Our findings suggest several avenues for future research. First, and since our study has not explored the interdependencies between the company and national institutional level changes, a promising avenue for future research would be to investigate the exact modes and mechanisms of this multi-level relationship. An empirically grounded understanding of these mechanisms is needed and could offer important insights into the aforementioned issue of hybridization.

A related avenue for further inquiry would thus be to study processes of hybridization of CSR (Matten & Moon, 2020). How do these patterns develop over longer periods of time? And what is the exact nature of CSR in terms of the mixture of implicit and explicit CSR? These are important endeavors for future research, which could take fruitful insights from the discussions on “localization” (Nilsson, 2023), “institutional layering” (Morris et al., 2018) or “CSR hybridization” (Matten & Moon, 2020). This could also involve a more systematic analysis of the temporality of the three dimensions of national-level CSR explicitization, which might differ across contexts.

Finally, an important avenue for future research would be studying explicitization in other contexts and time periods. As outlined in our boundary conditions earlier, research needs to investigate what stems from the idiosyncrasies of the Japanese setting, what is evident from Japan’s specific type of a national institutional context (Brejnholt et al., 2022; Gond et al., 2011; Kang & Moon, 2012), and what are further overarching patterns of national institutional-level CSR explicitization.

Footnotes

Appendix

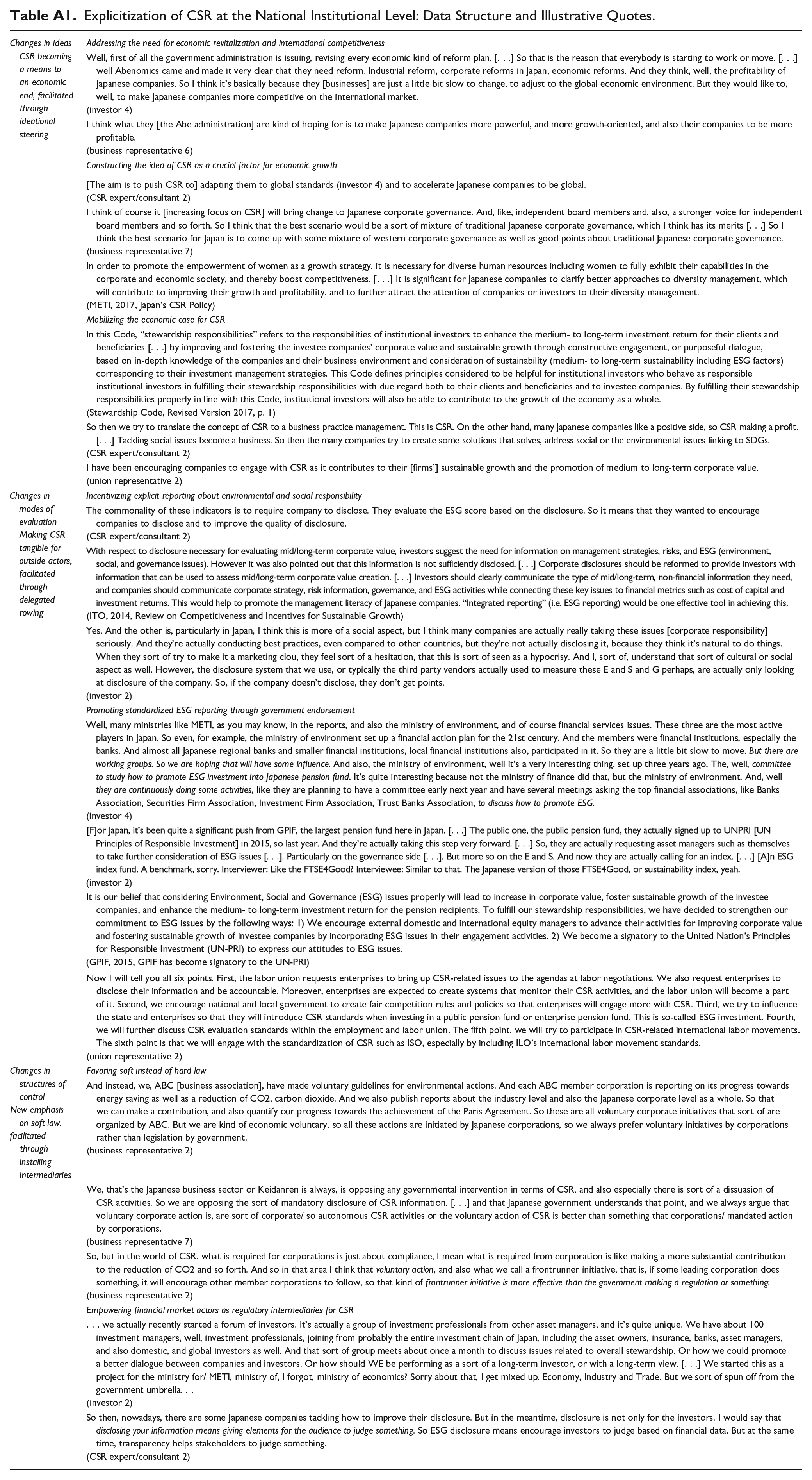

Explicitization of CSR at the National Institutional Level: Data Structure and Illustrative Quotes.

| Changes in ideas CSR becoming a means to an economic end, facilitated through ideational steering | Addressing the need for economic revitalization and international competitiveness |

| Well, first of all the government administration is issuing, revising every economic kind of reform plan. [. . .] So that is the reason that everybody is starting to work or move. [. . .] well Abenomics came and made it very clear that they need reform. Industrial reform, corporate reforms in Japan, economic reforms. And they think, well, the profitability of Japanese companies. So I think it’s basically because they [businesses] are just a little bit slow to change, to adjust to the global economic environment. But they would like to, well, to make Japanese companies more competitive on the international market. (investor 4) |

|

| I think what they [the Abe administration] are kind of hoping for is to make Japanese companies more powerful, and more growth-oriented, and also their companies to be more profitable. (business representative 6) |

|

| Constructing the idea of CSR as a crucial factor for economic growth | |

| [The aim is to push CSR to] adapting them to global standards (investor 4) and to accelerate Japanese companies to be global. (CSR expert/consultant 2) |

|

| I think of course it [increasing focus on CSR] will bring change to Japanese corporate governance. And, like, independent board members and, also, a stronger voice for independent board members and so forth. So I think that the best scenario would be a sort of mixture of traditional Japanese corporate governance, which I think has its merits [. . .] So I think the best scenario for Japan is to come up with some mixture of western corporate governance as well as good points about traditional Japanese corporate governance. |

|

| In order to promote the empowerment of women as a growth strategy, it is necessary for diverse human resources including women to fully exhibit their capabilities in the corporate and economic society, and thereby boost competitiveness. [. . .] It is significant for Japanese companies to clarify better approaches to diversity management, which will contribute to improving their growth and profitability, and to further attract the attention of companies or investors to their diversity management. |

|

| Mobilizing the economic case for CSR | |

| In this Code, “stewardship responsibilities” refers to the responsibilities of institutional investors to enhance the medium- to long-term investment return for their clients and beneficiaries [. . .] by improving and fostering the investee companies’ corporate value and sustainable growth through constructive engagement, or purposeful dialogue, based on in-depth knowledge of the companies and their business environment and consideration of sustainability (medium- to long-term sustainability including ESG factors) corresponding to their investment management strategies. This Code defines principles considered to be helpful for institutional investors who behave as responsible institutional investors in fulfilling their stewardship responsibilities with due regard both to their clients and beneficiaries and to investee companies. By fulfilling their stewardship responsibilities properly in line with this Code, institutional investors will also be able to contribute to the growth of the economy as a whole. |

|

| So then we try to translate the concept of CSR to a business practice management. This is CSR. On the other hand, many Japanese companies like a positive side, so CSR making a profit. [. . .] Tackling social issues become a business. So then the many companies try to create some solutions that solves, address social or the environmental issues linking to SDGs. |

|

| I have been encouraging companies to engage with CSR as it contributes to their [firms’] sustainable growth and the promotion of medium to long-term corporate value. |

|

| Changes in modes of evaluation Making CSR tangible for outside actors, facilitated through delegated rowing | Incentivizing explicit reporting about environmental and social responsibility |

| The commonality of these indicators is to require company to disclose. They evaluate the ESG score based on the disclosure. So it means that they wanted to encourage companies to disclose and to improve the quality of disclosure. |

|

| With respect to disclosure necessary for evaluating mid/long-term corporate value, investors suggest the need for information on management strategies, risks, and ESG (environment, social, and governance issues). However it was also pointed out that this information is not sufficiently disclosed. [. . .] Corporate disclosures should be reformed to provide investors with information that can be used to assess mid/long-term corporate value creation. [. . .] Investors should clearly communicate the type of mid/long-term, non-financial information they need, and companies should communicate corporate strategy, risk information, governance, and ESG activities while connecting these key issues to financial metrics such as cost of capital and investment returns. This would help to promote the management literacy of Japanese companies. “Integrated reporting” (i.e. ESG reporting) would be one effective tool in achieving this. |

|

| Yes. And the other is, particularly in Japan, I think this is more of a social aspect, but I think many companies are actually really taking these issues [corporate responsibility] seriously. And they’re actually conducting best practices, even compared to other countries, but they’re not actually disclosing it, because they think it’s natural to do things. When they sort of try to make it a marketing clou, they feel sort of a hesitation, that this is sort of seen as a hypocrisy. And I, sort of, understand that sort of cultural or social aspect as well. However, the disclosure system that we use, or typically the third party vendors actually used to measure these E and S and G perhaps, are actually only looking at disclosure of the company. So, if the company doesn’t disclose, they don’t get points. |

|

| Promoting standardized ESG reporting through government endorsement | |